Garment Sector Wage Digitization

22

AUGUST 2021 Garment Sector Wage Digitization A Practical Guide for Financial Service Providers

Transcript of Garment Sector Wage Digitization

AU G U S T 2 0 2 1

Garment Sector Wage DigitizationA Practical Guide for Financial Service Providers

Digitizing wages in the global garment industry represents a significant opportunity worth billions of dollars for Financial Service Providers. However, the segment remains untapped.

I N T R O D U C T I O N

As the world begins to move beyond COVID-19, and as digitization continues to accelerate at unprecedented rates, 230 million adults globally, mostly women, still receive their wages in cash.1

By helping to bring these workers into the digital economy, Financial Service Providers can play a catalytic role in driving financial inclusion while unlocking a new consumer segment that can represent significant incremental growth in terms of user base and revenue.

HERproject has been partnering with Financial Service Providers in Bangladesh, Cambodia, and Egypt to digitize wages in the garment industry, with support from Mastercard Center for Inclusive Growth and the Bill & Melinda Gates Foundation. Based on insights gathered through our work, this guide sets out recommendations that Financial Service Providers can leverage to unlock the potential of this segment and help bring millions of garment workers into the formal financial system.

The guide includes:

• The Financial Behaviors of Garment Workers

• The Case for Promoting Garment Sector Wage Digitization

• Three Stages to Developing the Digital Wages Market Segment

• Developing Partnerships for Scale

2

Introduction

O P P O R T U N I T Y S I Z E

3

Opportunity SizeSignificant garment exporting countries, specifically Bangladesh, Cambodia, Egypt, and Pakistan, have low levels of people with financial accounts, from 18 to 41 percent of the population, and high levels of private sector cash wages from 78 percent to 96 percent.3

Rates of saving, borrowing, and sending remittances through any method is significantly higher in these countries than the use of financial products and services for these needs. For example, in Egypt, 31 percent of adults reporting saving money, however only 6 percent saved at a financial institute. In Cambodia 42 percent of adults sent or received a domestic remittance, however only 5 percent did so through a mobile phone.4

Therefore, wage digitization in the garment industry, which has a high concentration and aggregation of unbanked workers, can provide entry-level financial accounts for many people, with the potential to use a range of products as they gain knowledge and confidence with financial services.

The chart data is taken from the World Bank Group Global Findex Database2

O P P O R T U N I T Y S I Z E

4

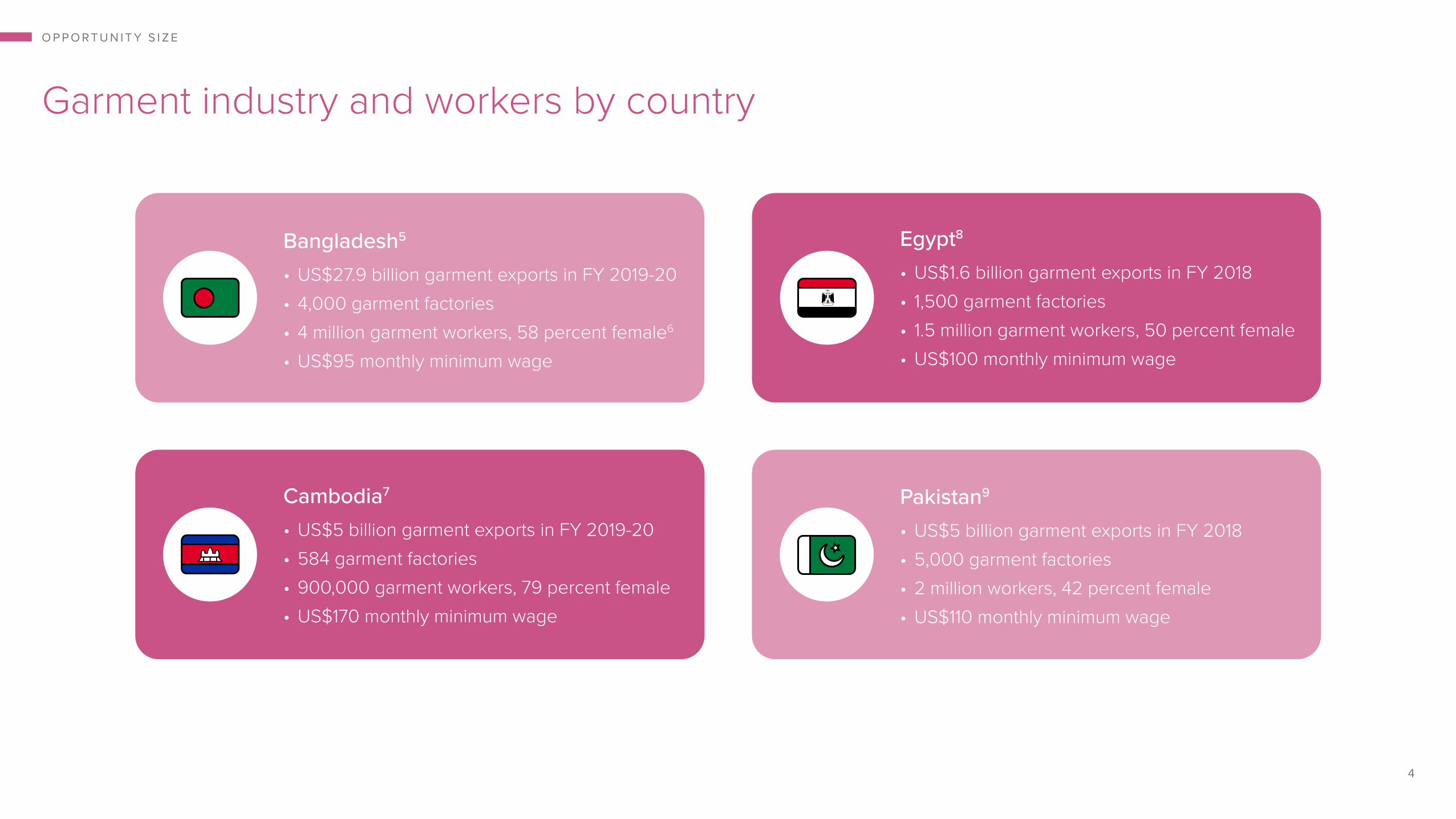

Cambodia7

• US$5 billion garment exports in FY 2019-20 • 584 garment factories• 900,000 garment workers, 79 percent female• US$170 monthly minimum wage

Egypt8

• US$1.6 billion garment exports in FY 2018 • 1,500 garment factories• 1.5 million garment workers, 50 percent female• US$100 monthly minimum wage

Pakistan9

• US$5 billion garment exports in FY 2018 • 5,000 garment factories• 2 million workers, 42 percent female• US$110 monthly minimum wage

Bangladesh5

• US$27.9 billion garment exports in FY 2019-20 • 4,000 garment factories• 4 million garment workers, 58 percent female6

• US$95 monthly minimum wage

Garment industry and workers by country

“I send some money home, to my aunt, who is looking after my daughter, each month”

F E M A L E W O R K E R , C A M B O D I A

“If I have to send money home to my mother, I give it to a neighbour in cash and they take it to her.”

M A L E W O R K E R , E G Y P T

F I N A N C I A L B E H AV I O R S

5

The Financial Behaviors of Garment WorkersGarment workers conduct a variety of cash-based financial transactions on a day-to-day basis (see table).

As Financial Service Providers begin to explore ways in which to displace this cash and enable a new set of digitally active customers, it is imperative to design appropriate and affordable financial solutions that meet these consumers where they are.

“I have a bank account for my wages but I cash everything out, because most of the merchants I use (e.g. vegetable sellers) only accept cash.”

F E M A L E W O R K E R , E G Y P T

“I have to keep the money on me all the time, because it is not safe to leave my money at home”

M A L E W O R K E R , C A M B O D I A

“I want to open a bank account but I don’t know how.”

F E M A L E W O R K E R , C A M B O D I A

“I have to visit the market to top up my phone airtime.”

F E M A L E W O R K E R , B A N G L A D E S H

Wages in cash from employers Payroll direct to bank account, pre-paid payroll card or mobile wallet

Government social protection payments directly into bank account,

pre-paid card or mobile wallet

Digital payments at merchant location (debit card or QR code)

Transfer money via mobile wallet

Bill payment via mobile wallet

Send money (person-to-person) via mobile wallet (domestic and cross-border)

Mobile recharge

Time-bound cash expenses, including rent and school fees

Cash payments for household expenses, such as groceries, and health

Bill payment in cash at utility office

Send cash to family

Buy airtime in cash at the market

Save cash in informal group or at home

Government social protection payments (such as pensions social benefits or

COVID-19 emergency wage subsidies) via cash transfers

Savings account

Regular cash in-flows or out-flows

Recommended digital financial products and services to replace cash

C O N T E X T

The Case for Promoting Garment Sector Wage Digitization

Benefits for Financial Service Providers

• Expanding relationship with factory client base

• Incremental user base and revenue growth from previously untapped segment

• New, active customers with potential to use a range of products

• Multiplier effect in communities adopting financial services

• Improved government relations resulting from supporting government digitization policies

Benefits for garment factory owners and senior management

• Improved business efficiency

• Reduced payroll cost

• Reduced risk of theft of cash payroll while on premises

• Demonstration of transparency and compliance for global buyers

Benefits for workers

• Increased safety of and control over wages

• Increased ability to access savings accounts, which helps to reduce financial risk and increase resilience

• Cost and time savings associated with using digital financial solutions to make remittance and bill payments

• Digital trail of financial situation, which can be leveraged to apply for and gain additional financial services and products

6

C O N T E X T

After garment factories in Bangladesh digitized wages,

women living in nearby communities were 2.5 times more likely to

actively use an account11

In Bangladesh, on average, women experienced a 50-percentage point increase in mobile money account ownership following wage digitization12

Female garment workers in Bangladesh conduct an average of eight transactions a month, and male garment workers thirteen, following wage digitization and participation in HERfinance Training10

In Egypt, there was a 26-percentage point increase in female workers reporting that they opened a savings account following participation in HERfinance13

Wage digitization in Bangladesh reduced administration time on payroll by more than half14

Worker production-time lost on payday cut by more than three-quarters following Wage Digitization in Bangladesh10

7

Three Stages to Developing the Digital Wages Market Segment

1 Acquiring new customers – understanding the financial behaviors and needs of garment sector employers and workers and developing financial solutions which would be in high demand

2 Driving account usage of financial services – supporting clients and customers to digitize and become active account users

3 Retaining customers and reaching scale – building relevant use cases and collaborations to build the ecosystem

T H R E E S TAG E S

8

The Inside Track

Keep “cash-out” costs low to maximize initial adoption: Garment workers will want to retain the option to pay basic expenses such as food and rent in cash. Any cost attached to withdrawing cash will impact the trust in—and acceptance of—payroll accounts. Incorporating options such as one or two free cash withdrawals a month can help workers adjust.

Assess Know Your Customer (KYC) requirements and understand their implications: Workers, especially women, may not have National IDs which are often required to open accounts. Considering the use of alternative KYC documentation can help ensure that males and females can equally benefit from payroll programs. In Cambodia, for example, a birth certificate or a Work ID can be used when a National ID is unavailable.

Design solutions that can be used on different types of phones: Despite a gradual increase in smartphone penetration, many workers, especially women, still use feature phones. It is therefore important to develop mobile solutions that can be used through an app or through Unstructured Supplementary Service Data (USSD) to maximize access.

How to Increase Understanding of the Garment Sector:

• Dedicate sales resources to specifically focus on the garment sector and include at least one member who has garment industry experience. Map the garment ecosystem and power dynamics within it to understand how to secure support for digital payroll from critical stakeholders.

• Identify the unique financial behaviors of male and female garment workers by working with NGOs who have detailed market knowledge. Conduct focus group discussions with a range of male and female workers in different age groups and roles/teams within the factory to understand their financial behaviors.

• Identify a range of products and services which are affordable and relevant, and when combined with financial capability training (see Driving Usage of Financial Services section), can be adopted by garment workers, including savings products, mobile wallets, and payroll accounts.15

• Review transaction data to identify which products male and female workers value and adjust marketing campaigns to drive further usage.16

T H R E E S TAG E S / S TAG E 1

Acquiring New Customers

Top Tips:Promote financial resilience from the start by developing use case for savings products, and investing in financial capability building.

9

How to attract garment sector employers as clients:

• Make the business case to employers by demonstrating the benefits of financial services, including increased efficiency, cost savings, safety, and convenience. Clearly explain all the costs and fees, and help managers understand the savings that come from transitioning from cash to digital wages.

• Work closely with factory management to understand their payroll process and challenges. Wage digitization is new for the garment sector, and management may need additional support to change their payroll system. Forging a close partnership between Financial Service Provider and client will help to build trust and confidence and secure their buy-in, which is critical for success.

• Ensure sufficient options to withdraw cash exist by mapping available ATM and/or agent cash out points and factoring in the demand at these points. Ensuring there is enough cash in ATMs around payday, for example, is critical in building trust of digital payroll programs and supporting adoption. A poor first-customer experience will reduce acceptance and adoption of digital payroll.

T H R E E S TAG E S / S TAG E 1

10

The Inside Track

Help employers understand the cost savings of digital payroll: Cash payroll has hidden costs, including time needed by managers to count and distribute cash wages, and the production time lost as workers queue to collect their wages. If these are not considered, a digital payroll may be perceived to cost more than cash. HERproject’s Business Benefit Analysis Tool can be used to calculate the cost of cash and digital payroll. Cost savings by employers can be used to offset additional charges associated with a digital payroll, including subsiding cash-out fees that may be incurred by workers.

Optimize account opening processes for scale: Production pressure means that managers are reluctant to allow workers time to open accounts, which can lead to delays in digitization. Therefore, the account opening process needs to allow for quick and efficient account openings. This could include enabling a group of workers to open accounts at one time, rather than individually, or attending at different times of the day to ensure workers on different shifts can be supported.

Be transparent about all fees and charges associated with the digital solution: Workers are used to cash, so they need to be convinced of the benefits of digital accounts. All fees and charges need to be clearly set out and shared with workers as part of the consultation.

Top Tips:Encourage the factory’s senior management team to make wage digitization an organization-wide initiative, with manager and worker representative buy in through consultation.

11

“One of the barriers to digitizing payroll was the lack of opportunity for workers to cash out wages on payday. There was only one ATM near the factory. We addressed this by arranging a mobile ATM on site for payday and the following few days. Managers staggered workers’ breaks to reduce demand on the ATM, and factory transport buses stopped at ATMs on the way home. The next step is to encourage workers to use more financial services, which will reduce their need to cash out on payday.”

- TA M E R E L- D E S S O U K I , S U S TA I N A B I L I T Y M A N AG E R LOT U S G A R M E N T S , A L E V I S T R AU S S & C O S U P P L I E R I N E G Y P T

11

T H R E E S TAG E S / S TAG E 1

@Lotus Garments Group/Egypt

12

T H R E E S TAG E S / S TAG E 2

How to Onboard Garment Workers:

• Build the capacity of sales teams and agents to serve male and female garment workers by working with local NGOs, including developing capacity to engage female workers.

• Provide relevant product information to garment workers that explains how to access and use the payroll accounts. The materials should also provide clear information on fees and charges to avoid misunderstandings and grievances, and they should include information on fraud awareness and protection information.

• Provide support on payday, such as arranging for sales agents to visit factories to answer any questions and help workers, especially women, to use ATMs or cash out points.

• Create an awareness campaign around fraud prevention that can be promoted within the factory, especially around payday. This will help reduce sharing of PINs with others, including fraud callers.

The Inside Track

Increase active usage of accounts through product training to build workers’ knowledge and confidence in using a range of financial solutions. This could be through a short group session as part of opening an account, through larger townhall meetings in the factory, or through a booth on the factory premises. Open-source tools, such as HERfinance Digital Wages Tech tools, videos and posters, can be used to help workers make the transition [See page 21 for details].

Agents, branch staff and ATM security staff can be important sources of information to help workers use their accounts and deal with common challenges, such as resetting PINs. Therefore, it’s important to ensure they have the support and materials they need to be able to respond to questions and to follow the customer data protection guidelines.18

Ensure workers can withdraw cash quickly and easily: Experience has shown that workers want to withdraw 100 percent of wages during early phases of payroll digitization. The inability of them to do so results in a significant drop in trust and impacts long-term adoption of digital financial services. Therefore, local agents and ATMs need to have enough liquidity, especially on payday, to facilitate large withdrawals.

Driving Usage of Financial Services

Top Tips:A positive first experience with digital payments can create a customer for life. Invest in financial capacity building to enable workers to make digital payments with confidence.

1313

“After [HERfinance] training, I understood the benefits of using a debit card and how to use it for purchasing, and the bonus system when paying by the card. [I also learned about] smart wallet and its uses for paying bills, transferring money, and [airtime] top-up. I also leave some money in my account to save.”

- A L I I B R A H I M , G A R M E N T W O R K E R , P O R T S A I D , E G Y P T

1313@BSR/CDS-M.Moawad/Egypt

T H R E E S TAG E S / S TAG E 2

The majority of garment workers are female; therefore, it’s critical to understand their financial behaviors and challenges in order to maximize success. Lower levels of education, experience, and confidence with financial services and technology mean that it is often more challenging for women to adopt digital wages compared to their male counterparts. This, coupled with gender norms and the perceived roles of women in society, may result in women having less access to resources needed to open and use accounts. To combat this, it is important to design products, marketing campaigns, and training materials that cater to the unique needs and constraints of women.19 This will make the financial product more meaningful to female customers, increasing usage20 and providing greater return on investment for Financial Service Providers.

Engaging Female Customers

How to Engage Female Customers:

• Provide additional support and training to address problems that women commonly encounter, such as accessing the resources needed to open accounts and using ATMs. Developing peer champions within the factory, who female workers trust and look up to, can be an effective way for women to get support with using their accounts.

• Recruit female sales agents to support account opening to help women feel more comfortable with the process. Ensure that there is enough time during account opening for women to ask questions, as they are likely to have less confidence and experience with financial services and technology than men.

• Collect and analyze gender-disaggregated data to better understand the financial behaviors and needs of female workers. Work with NGOs who can facilitate discussions with female workers to collect further insights on their financial lives.

F E M A L E C U S TO M E R S

14

Top Tips:Use examples, pictures, and quotes from women in promotional materials. Seeing other women using financial solutions will make the solutions more relatable and help them recognize that they, too, can access, use, and benefit from financial services.

F E M A L E C U S TO M E R S

Understanding the Unique Constraints Faced by Women:

• Women are less likely to have the resources needed to open and use accounts compared to men. In low- and middle-income countries, smartphone ownership is 20 percent lower for women than for men,21 and their SIM card may be registered in someone else’s name. Promoting mobile money products that work on feature phones and helping women access their own SIM cards can start to address this.

• Women are more likely to hand over their account details to someone else.In Egypt, 14 percent of women surveyed shared their bank card with a coworker.22 In India, 48 percent of women surveyed shared their PIN codes with ATM helpers when making a transaction.23 Training and support to help build women’s knowledge and confidence to use their accounts themselves will reduce this and promote increased control over finances.

• Women are more likely to be victims of fraud calls. In Bangladesh, 3 percent of garment workers reported receiving SMS messages or phone calls from an unknown person asking them to send money or share personal information — only 57 percent of women ignored this, compared to 87 percent of men.24 Therefore, it is important that regular awareness campaigns are run to understand and avoid the dangers of fraud.

• Women may be expected to hand over their wages to male family members. This can lead to women hiding part of their wages for their own use or to send to relatives. An SMS with the salary amount could cause a problem with male family members, with 40 percent of managers in Bangladesh reporting this as an issue for female workers. Work with local NGOs to understand any unintended consequences of wage digitization and identify solutions.

15

1616

“Once I encountered a fraud call. The caller said he had sent a PIN code to my cell phone and was requesting me to share the PIN code with him, otherwise my [mobile money] account would get deleted. From the moment I picked it up, I knew it was a fraud call and I knew how to tackle this. I learned it from my HERfinance training, and I was able to avoid a disaster.”

- S H A N TO N A , G A R M E N T W O R K E R , D H A K A , B A N G L A D E S H

16

F E M A L E C U S TO M E R S

16@BSR/Kamrul Hassan/Bangladesh

T H R E E S TAG E S / S TAG E 3

How to Develop the Digital Financial Ecosystem:

• Identify important cash transactions and work with agents and merchants in the community to incentivize digital acceptance. This could include providing merchants with low-cost acceptance solutions.

• Promote opportunities for digital payments to workers such as bills and utilities, remittances, and airtime top-up. This could be during onboarding and also through ongoing awareness campaigns in the factory and community.

• Work with fast-moving consumer good (FMCG) company clients to support and incentivize digitization of retail payments in their supply chains, especially by small merchants in garment sector communities.

17

Retaining Customersand Reaching Scale

Top Tips:Promote and incentivize digital payments and acceptance through appropriate discounts and earning bonus points, which could be promoted through SMS messages.

The Inside Track

Understand the challenges faced by merchants to accept digital payments. Growth in mobile money usage among neighborhood residents has not been sufficient to motivate merchants to accept mobile money payments.25 Grocers need to pay their suppliers in cash and therefore want to receive cash payments from workers. However, if suppliers and wholesalers accepted digital payment, then grocers would consider switching to digital payment.

Identify opportunities for interoperability. While recognizing the need to balance competition and innovation, ensuring the interoperability of platforms and agents will increase usage of financial products and services by workers. Identify ways that garment workers can make digital financial transactions regardless of where they live or who their provider is and promote these.26

Take the time to develop garment segments in a sustainable way. People need to build their confidence by knowing that they can cash out first and trusting that their money will always be available before they start using additional products or payments.

18

T H R E E S TAG E S / S TAG E 3

“When I went out with my daughter, we saw a shop which had a 50-percent discount, but we didn’t have enough cash on us. Then I remembered that I have my debit card and the shop accepted it for paying. We got a benefit from the discounts and bought what we wanted.”

- A M A L , G A R M E N T W O R K E R , P O R T S A I D , E G Y P T

18@Lotus Garments Group/Egypt

19

PA R T N E R S H I P S F O R S C A L E

Partnerships for ScaleDigitizing private sector wages presents a significant opportunity for Financial Service Providers to reach a new market segment. Wage digitization pilots have developed best practice and insight for the smooth transition from cash to digital payroll.

The next step is scaling payroll digitization, which requires innovation and cross-sector collaboration. Many different organizations, including governments, companies, and development agencies, have committed to supporting inclusive digital payment ecosystems, including through the UN-based Better Than Cash Alliance.28

This represents an opportunity for Financial Service Providers to partner with others with complementary assets and competencies. For example, multinational organizations with a local presence, like Mastercard, bring knowledge, technology and economies of scale for one primary goal: to help people improve their lives an build sustainable futures by connecting them with digitally base financial tools and services. In Egypt, Mastercard, have been working with Commercial International Bank (CIB), Levi Strauss & Co, and HERproject to pilot wage digitization at a Levi’s supplier, Lotus Garments Group, resulting in over 8,000 workers being paid into accounts.

1919@ILO/Better Factories Cambodia 1919

20

PA R T N E R S H I P S F O R S C A L E

20

Develop Partnerships for Scale by Working with:

• Global apparel buyers to identify opportunities to digitize and incentivize supply chain payments and to understand and address the barriers to scale. This could include garment brands, who can facilitate wage digitization in the garment sector, or FMCG companies, who can promote acceptance of digital payments in their supply chains.

• Telcos to increase and promote workers access to smart phones to drive access and usage of mobile wallet solutions. This could include agreeing on offers on handsets and data as well as addressing the issues around SIM card ownership and registration.

• Worker associations to understand and promote the benefits of digital payroll to their members as well as to increase understanding of the needs of garment workers and build their trust.

• Governments to support and scale their commitments to digitize payments across private sector digital wages and government social protection payments. This should include addressing barriers to intra-operability, including around ATMs and agents, to drive usage.

• NGOs and worker associations to increase understanding of the financial needs of garment workers to ensure that financial products and services are relevant. NGOs can also support and deliver financial capability training that engages male and female workers, driving their usage of financial products and services.

2020202020

• Multinational organizations to leverage global expertise to provide locally relevant solutions which can improve efficiency, promote cash conversion, drive financial inclusion, achieve sustainable economic growth, and enhance people’s lives.

• Funders to develop and share risk of wage digitization initiatives. This can include development of a sustainable cost-sharing financial model that does not pass on the costs of cashing out to garment workers.

• Manufacturer associations to promote the benefits of digital payroll to their members and to identify and address the challenges to scale.

HERfinance Videos and AnimationsDeveloped with QuizRR, these can be used during training or shown on their own, such as in factory canteens. Playlists available in Arabic, Bangla & Khmer.

HERfinance PostersA set of six posters with information about financial services and financial management. They are available in English, Bangla, Khmer, Arabic, Hindi, Kannada and Tamil.

HERfinance Digital Wages Toolkit for ManagersSets out best practice and guidance for garment managers to transition towards digital payroll in a responsible and efficient manner. Available online in Arabic, Bangla, English, Khmer and Mandarin. For offline access download from Google Playstore.

HERfinance Tech Learning Tool for WorkersDeveloped with QuizRR, uses engaging videos and quizzes to support workers to increase their knowledge of financial services, improve financial health and build their digital literacy. Available in Bangla, Khmer and Arabic.

HERfinance Audio MessageA song that can be played on the public address (PA) system and provides information about using financial services. It is available in Bangla, Hindi, Kannada and Tamil.

Better Than Cash Alliance ‘Responsible Digital Payments’ GuidelinesThese identify eight good practices for engaging with clients who are sending or receiving digital payments and who have previously been financially excluded or underserved.

Digital Wages Resources

R E S O U R C E S

The following Digital Wages training resources are open source and readily available online.

21

BSR’s HERproject™ is a collaborative initiative that strives to empower low-income women working in global supply chains. Bringing together global brands, their suppliers, and local NGOs, HERproject drives impact for women and business via workplace-based interventions on health, financial inclusion, and gender equality. Since its inception in 2007, HERproject™ has worked in more than 900 workplaces across 14 countries and has increased the well-being, confidence, and economic potential of more than 1 million women and 620,000 men.

www.herproject.org

References

22

Acknowledgements Learn MoreThis guide was written by Ella Moffat at BSR, with input from Natasha Jamal at Mastercard Center for Inclusive Growth, Brendan Murphy at Mastercard, Christine Svarer and Smita Nimilita at BSR, and Marjolaine Chaintreau at Better than Cash Alliance.

HERproject would like to thank the following organizations for contributing their time and expertise: Acleda Bank, bKash, Commercial International Bank CIB Egypt, Dutch-Bangla Bank Rocket, Wing (Cambodia).

HERproject would also like to thank our HERfinance Digital Wages partners: Mastercard Center for Inclusive Growth, The Bill & Melinda Gates Foundation, Levi Strauss Foundation, and The Walt Disney Company.

For more information about the HERfinance Digital Wages Program, please visit the HERfinance Resource Hub - a centralized site dedicated to hosting and sharing tools, publications, and media resources to help companies and organizations integrate wage digitization in a way that considers the needs of female workers.

Thank you to ILO/Better Work and Lotus Garments Group for giving permission to use their photos.

Photo credit front page: BSR/CDS-M.Moawad/Egypt

The Center for Inclusive Growth advances equitable and sustainable economic growth and financial inclusion around the world. The Center leverages the company’s core assets and competencies, including data insights, expertise and technology, while administering the philanthropic Mastercard Impact Fund, to produce independent research, scale global programs and empower a community of thinkers, leaders and doers on the front lines of inclusive growth. For more information and to receive its latest insights, follow the Center on Twitter @CNTR4growth, or subscribe to the Center’s newsletter.

www.mastercardcenter.org

1, 2, 3, 4 Demirguc-Kunt, Asli, Leora Klapper, Dorothe Singer, Saniya Ansar, and Jake Hess. “The Global Findex Database 2017: Measuring Financial Inclusion and the Fintech Revolution.” World Bank, Washington, DC, 20185 https://www.bgmea.com.bd6 HERproject Impact Portal7 Cambodia Garment and Footwear Sector Bulletin, ILO, 2018 8 A Look at Sourcing Apparel From Egypt and Investing in its Textile Industry’ Sourcing Journal, April 20199 Digital Financial Services in Pakistan landscape research, HERproject and Microsave Consulting, September 202010, 12, 14 Digital Wages Positive Impact for Women and Business Report. HERproject, March 202011, 25 The Impact of Wage Digitization: Neighbourhood Spillover Effects from Paying Garment Factory Workers with Mobile Money Report, Intermedia Financial Inclusion Insights, May 201913, 22 HERfinance Digital Wages survey data collected at Lotus Garments Group, Egypt, through 50 baseline surveys and 47 end-line surveys15, 18, 26 Responsible Digital Payments Guidelines Better than Cash Alliance, November 2016

16 How Fintechs Can Profit From the Multi-Trillion Dollar Female Economy Report, Financial Alliance for Women, 202019 Yasmin Bin-Humam, Personas show how social norms impact womens financial inclusion blog, CGAP, December 202020 Julia Arnold, ‘The Case for a Gender Intelligent Approach an Opportunity for Inclusive Fintechs’ Brief, Center for Financial Inclusion, January 2021 21 The Mobile Gender Gap Report 2020, Connected Women, GSMA, 202023 Financial Behavior of Garment Workers in India HERproject and Microsave, October 2019 24 Daniela Ortega, Mixing it up: The co-existence of cash and digital financial services Garment Worker Diaries, Microfinance Opportunities, July 202027 Digitizing for Inclusion – insights from wage digitization in the garment sector, BSR and Mastercard, 202028 https://www.betterthancash.org/about/members

https://www.ilo.org/wcmsp5/groups/public/---asia/---ro-bangkok/documents/publication/wcms_663043.pdf

https://herproject.org/files/reports/HERproject-digital-wages-positive-impact-for-women-business.pdf