GarantiBank International N.V.garantibank.eu/downloads/Moody's_Credit Opinion-GBI... · GarantiBank...

9

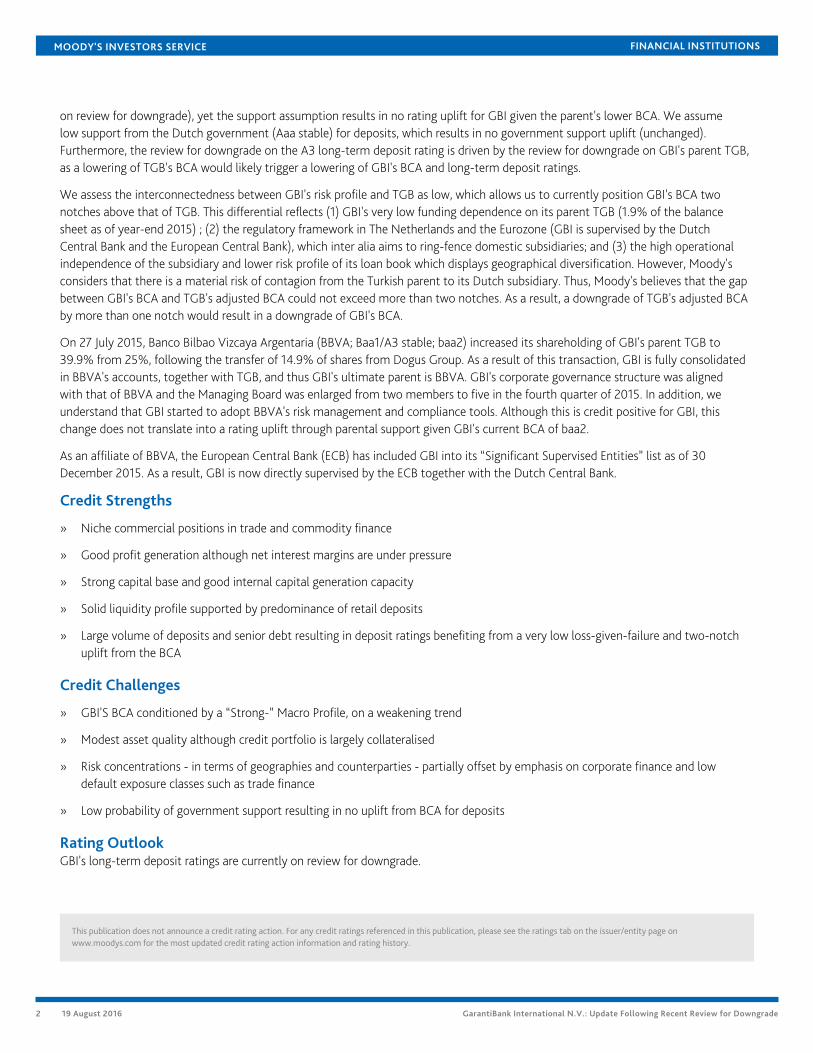

FINANCIAL INSTITUTIONS CREDIT OPINION 19 August 2016 Update RATINGS GarantiBank International N.V. Domicile Amsterdam, Netherlands Long Term Debt Not Available Type Not Available Outlook Not Available Long Term Deposit A3 , Possible Downgrade Type LT Bank Deposits - Fgn Curr Outlook Rating(s) Under Review Please see the ratings section at the end of this report for more information. The ratings and outlook shown reflect information as of the publication date. Analyst Contacts Guillaume Lucien- Baugas 33-1-5330-3350 VP-Senior Analyst [email protected] Yasuko Nakamura 33-1-5330-1030 VP-Senior Credit Officer [email protected] Andreea Prodea 33-1-5330-1055 Associate Analyst [email protected] Alain Laurin 33-1-5330-1059 Associate Managing Director [email protected] Nick Hill 33-1-5330-1029 Managing Director - Banking [email protected] GarantiBank International N.V. Update Following Recent Review for Downgrade Summary Rating Rationale GarantiBank International NV's (GBI) BCA and adjusted BCA are baa2, on review for downgrade, and its long-term deposit ratings are A3, on review for downgrade. We assign a Counterparty Risk Assessment (CR Assessment) of A2(cr)/Prime-1(cr) to GBI. GBI's BCA of baa2, on review for downgrade, reflects the bank's (1) solid capitalization; (2) diversified trade-finance activities, which affords good profitability; (3) sound liquidity and solid deposit funding base; and (4) moderate asset quality. Additionally, GBI's ratings reflect (1) high credit risk concentrations and cross-border risk caused by the geographical imbalance between foreign assets and domestic liabilities; and (2) the bank's focus on trade finance, corporate finance and treasury revenues, which Moody's regards as a more volatile income source. The review for downgrade of GBI’s BCA and adjusted BCA of baa2 reflects increased asset risks in relation to Turkey, after the country was subject to a military coup attempt. The evolving political and economic situation could entail further deterioration in the domestic operating environment in Turkey, which might, in turn, affect the Netherlands-based GBI’s financial strength through a weakening asset quality and deteriorating profitability. Exhibit 1 Rating Scorecard - Key Financial Ratios Source: Moody's Financial Metrics GBI's deposit ratings benefit from a very low loss-given-failure, which results in a two-notch uplift from the BCA. We assess a very high probability of parental support from its 100% shareholder Turkiye Garanti Bankasi AS (TGB; Baa3/Baa3 on review for downgrade, ba1

Transcript of GarantiBank International N.V.garantibank.eu/downloads/Moody's_Credit Opinion-GBI... · GarantiBank...

FINANCIAL INSTITUTIONS

CREDIT OPINION19 August 2016

Update

RATINGS

GarantiBank International N.V.Domicile Amsterdam,

Netherlands

Long Term Debt Not Available

Type Not Available

Outlook Not Available

Long Term Deposit A3 , PossibleDowngrade

Type LT Bank Deposits - FgnCurr

Outlook Rating(s) Under Review

Please see the ratings section at the end of this reportfor more information. The ratings and outlook shownreflect information as of the publication date.

Analyst Contacts

Guillaume Lucien-Baugas

33-1-5330-3350

VP-Senior [email protected]

Yasuko Nakamura 33-1-5330-1030VP-Senior [email protected]

Andreea Prodea 33-1-5330-1055Associate [email protected]

Alain Laurin 33-1-5330-1059Associate [email protected]

Nick Hill 33-1-5330-1029Managing Director [email protected]

CLIENT SERVICES

Americas 1-212-553-1653

Asia Pacific 852-3551-3077

Japan 81-3-5408-4100

EMEA 44-20-7772-5454

GarantiBank International N.V.Update Following Recent Review for Downgrade

Summary Rating RationaleGarantiBank International NV's (GBI) BCA and adjusted BCA are baa2, on review fordowngrade, and its long-term deposit ratings are A3, on review for downgrade. We assign aCounterparty Risk Assessment (CR Assessment) of A2(cr)/Prime-1(cr) to GBI.

GBI's BCA of baa2, on review for downgrade, reflects the bank's (1) solid capitalization; (2)diversified trade-finance activities, which affords good profitability; (3) sound liquidity andsolid deposit funding base; and (4) moderate asset quality. Additionally, GBI's ratings reflect(1) high credit risk concentrations and cross-border risk caused by the geographical imbalancebetween foreign assets and domestic liabilities; and (2) the bank's focus on trade finance,corporate finance and treasury revenues, which Moody's regards as a more volatile incomesource.

The review for downgrade of GBI’s BCA and adjusted BCA of baa2 reflects increased assetrisks in relation to Turkey, after the country was subject to a military coup attempt. Theevolving political and economic situation could entail further deterioration in the domesticoperating environment in Turkey, which might, in turn, affect the Netherlands-based GBI’sfinancial strength through a weakening asset quality and deteriorating profitability.

Exhibit 1

Rating Scorecard - Key Financial Ratios

Source: Moody's Financial Metrics

GBI's deposit ratings benefit from a very low loss-given-failure, which results in a two-notchuplift from the BCA. We assess a very high probability of parental support from its 100%shareholder Turkiye Garanti Bankasi AS (TGB; Baa3/Baa3 on review for downgrade, ba1

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

This publication does not announce a credit rating action. For any credit ratings referenced in this publication, please see the ratings tab on the issuer/entity page onwww.moodys.com for the most updated credit rating action information and rating history.

2 19 August 2016 GarantiBank International N.V.: Update Following Recent Review for Downgrade

on review for downgrade), yet the support assumption results in no rating uplift for GBI given the parent's lower BCA. We assumelow support from the Dutch government (Aaa stable) for deposits, which results in no government support uplift (unchanged).Furthermore, the review for downgrade on the A3 long-term deposit rating is driven by the review for downgrade on GBI's parent TGB,as a lowering of TGB's BCA would likely trigger a lowering of GBI's BCA and long-term deposit ratings.

We assess the interconnectedness between GBI's risk profile and TGB as low, which allows us to currently position GBI's BCA twonotches above that of TGB. This differential reflects (1) GBI's very low funding dependence on its parent TGB (1.9% of the balancesheet as of year-end 2015) ; (2) the regulatory framework in The Netherlands and the Eurozone (GBI is supervised by the DutchCentral Bank and the European Central Bank), which inter alia aims to ring-fence domestic subsidiaries; and (3) the high operationalindependence of the subsidiary and lower risk profile of its loan book which displays geographical diversification. However, Moody'sconsiders that there is a material risk of contagion from the Turkish parent to its Dutch subsidiary. Thus, Moody's believes that the gapbetween GBI's BCA and TGB's adjusted BCA could not exceed more than two notches. As a result, a downgrade of TGB's adjusted BCAby more than one notch would result in a downgrade of GBI's BCA.

On 27 July 2015, Banco Bilbao Vizcaya Argentaria (BBVA; Baa1/A3 stable; baa2) increased its shareholding of GBI's parent TGB to39.9% from 25%, following the transfer of 14.9% of shares from Dogus Group. As a result of this transaction, GBI is fully consolidatedin BBVA's accounts, together with TGB, and thus GBI's ultimate parent is BBVA. GBI's corporate governance structure was alignedwith that of BBVA and the Managing Board was enlarged from two members to five in the fourth quarter of 2015. In addition, weunderstand that GBI started to adopt BBVA's risk management and compliance tools. Although this is credit positive for GBI, thischange does not translate into a rating uplift through parental support given GBI's current BCA of baa2.

As an affiliate of BBVA, the European Central Bank (ECB) has included GBI into its “Significant Supervised Entities” list as of 30December 2015. As a result, GBI is now directly supervised by the ECB together with the Dutch Central Bank.

Credit Strengths

» Niche commercial positions in trade and commodity finance

» Good profit generation although net interest margins are under pressure

» Strong capital base and good internal capital generation capacity

» Solid liquidity profile supported by predominance of retail deposits

» Large volume of deposits and senior debt resulting in deposit ratings benefiting from a very low loss-given-failure and two-notchuplift from the BCA

Credit Challenges

» GBI'S BCA conditioned by a “Strong-” Macro Profile, on a weakening trend

» Modest asset quality although credit portfolio is largely collateralised

» Risk concentrations - in terms of geographies and counterparties - partially offset by emphasis on corporate finance and lowdefault exposure classes such as trade finance

» Low probability of government support resulting in no uplift from BCA for deposits

Rating OutlookGBI's long-term deposit ratings are currently on review for downgrade.

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

3 19 August 2016 GarantiBank International N.V.: Update Following Recent Review for Downgrade

Factors that Could Lead to an UpgradeAn upgrade of GBI’s BCA and deposit ratings is unlikely in view of increased country risk and asset risks, as reflected in the currentreview for downgrade on these ratings.

Factors that Could Lead to a DowngradeA downgrade of GBI’s BCA and long-term deposit ratings could result from (1) a high level of balance-sheet exposure to weakeningexposures and geographic regions, (2) a lowering of TGB’s adjusted BCA by more than two notches below GBI’s current BCA or (3) adeterioration in GBI's loss absorption capacity and liquidity profile.

Key Indicators

Exhibit 2

GarantiBank International N.V. (Unconsolidated Financials) [1]12-152 12-142 12-133 12-123 12-113 Avg.

Total Assets (EUR million) 5021.5 4978.4 4665.9 4575.3 4178.6 4.74

Total Assets (USD million) 5454.8 6024.2 6429.4 6032.0 5424.4 0.14

Tangible Common Equity (EUR million) 546.0 534.7 488.9 430.4 375.9 9.84

Tangible Common Equity (USD million) 593.1 647.0 673.7 567.5 487.9 5.04

Problem Loans / Gross Loans (%) 4.7 5.0 3.6 2.7 2.9 3.85

Tangible Common Equity / Risk Weighted Assets (%) 16.8 17.6 18.7 18.4 17.6 17.26

Problem Loans / (Tangible Common Equity + Loan Loss Reserve) (%) 21.1 21.8 16.1 14.0 13.4 17.35

Net Interest Margin (%) 1.3 1.7 1.7 1.5 1.7 1.65

PPI / Average RWA (%) 1.9 2.7 3.7 3.7 3.2 2.36

Net Income / Tangible Assets (%) 0.2 0.9 1.3 1.2 1.3 1.05

Cost / Income Ratio (%) 40.7 33.7 29.2 31.5 33.3 33.75

Market Funds / Tangible Banking Assets (%) 21.8 19.1 16.9 14.7 22.9 19.15

Liquid Banking Assets / Tangible Banking Assets (%) 23.4 28.7 30.0 31.9 36.7 30.15

Gross loans / Due to customers (%) 86.2 78.4 71.4 70.2 68.1 74.85

[1] All figures and ratios are adjusted using Moody's standard adjustments [2] Basel III - fully-loaded or transitional phase-in; LOCAL GAAP [3] Basel II; LOCAL GAAP [4] Compound AnnualGrowth Rate based on LOCAL GAAP reporting periods [5] LOCAL GAAP reporting periods have been used for average calculation [6] Basel III - fully-loaded or transitional phase-in &LOCAL GAAP reporting periods have been used for average calculationSource: Moody's Financial Metrics

Detailed Rating ConsiderationsGBI's BCA is conditioned by a Strong - Macro Profile, on a weakening trendGBI's exposure to the Dutch economy is around 18%. Due to its large exposures to lower Macro-Profiles, including 37% to Turkey(Moderate), the overall Macro Profile for GBI is Strong -, below the Strong + Macro Profile of The Netherlands. Turkey is an importantbuilding block for GBI’s Macro Profile. Turkish economic growth is expected to remain subdued in 2016, reflecting the country’ssignificant external financing needs, political uncertainty following the failed coup attempt and volatile capital flows towards emergingmarkets, which is reflected in the review for downgrade of the sovereign bond rating (18 July 2016).

Niche commercial positions in trade and commodity financeThe bank's commercial activities are essentially split into four divisions:

1. Trade & Commodity Finance, focusing on international trade and commodity finance. The contribution of this division hasdecreased since 2011 because of the bank's improving revenue diversification into other transaction banking activities.

2. Treasury, focusing on commercial trading activities in addition to the bank's balance-sheet risk management, i.e., liquidity andinterest risk management. The revenue generation activities comprise investments in bonds and mainly commercial, flow-drivenand intra-day trading.

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

4 19 August 2016 GarantiBank International N.V.: Update Following Recent Review for Downgrade

3. Structured Finance, which was created in 2008 and combines activities in corporate lending, Islamic finance and shipping finance,as well as payments and cash management services for corporate clients. The revenue contribution is on a positive trend, as GBIhas increased leverage in this business segment.

4. Institutional Sales & Private Banking, which offers tailor-made financial services to institutional and high-net-worth clients. WhileInstitutional Sales focuses on balance sheet and market risk hedging offerings to firms, Private Banking promotes execution-onlyand advisory services to international high-net-worth individuals.

As of year-end 2015, 65% of the bank's liabilities were composed of deposits, most of which (68%) were retail deposits while theremainder is corporate and private banking deposits. The direct retail deposit-taking activities are carried out in The Netherlands and inGermany, through call centers and the Internet.

The Netherlands and Germany account for 27% and 73% respectively of total retail deposits. Around 95% of these are covered by theDutch Deposit Guarantee Scheme. GBI's deposit base demonstrated robust stability since the onset of the 2008 global financial crisis.GBI has managed to maintain its market shares during the crisis and ever since (approximately 0.10% in The Netherlands and 0.05% inGermany) while its saving deposit interest rate offerings as of 2015 year-end are not ranked among the top 20 in the Netherlands or inGermany. We consider that internet-based deposits are inherently more sensitive to reputational risk, but we acknowledge that thesedeposits have shown a great degree of stability until now and throughout the financial crisis.

At year-end 2015, the breakdown of GBI's gross credit exposures by geographic area including cash on the balance sheet was asfollows: Turkey (37%; 34% in 2014); Europe excluding the Netherlands (33%; 30% in 2014), the Netherlands (18%; 19% in 2014),the Commonwealth of Independent States (CIS) (4%; 4% in 2014); and rest of the world (8%; 13% in 2014). We observe that someof GBI's gross exposure to the rest of the world were replaced by higher exposures to Turkey and European countries others than theNetherlands.

Given the business mix, we consider GBI's earnings to be more volatile than pure retail banking income.

Largely collateralised credit portfolio, with asset quality deemed modestAt year-end 2015, GBI's NPLs-to-gross loans ratio improved to 4.7% from 5.0% at year-end 2014 (2013: 3.6%). The NPL ratio remainsweaker compared to the 1.6% recorded in 2009 prior to the global recession. The bank's NPLs are predominantly corporate exposuresand we observe a lack of granularity in the corporate loan book compared to total receivables (a constraint derived from the relativelysmall size of the bank). Loan- loss provision coverage was reported at 59%, which is average yet reflects the bank's high recoveriesgiven the collateralised nature of the credit portfolio.

Our assigned asset risk score of ba2 reflects the bank's modest asset quality and the low granularity of its loan book. We believe thatasset quality is a relative weakness for the bank.

Risk concentrations - in terms of geographies and counterparties - are partially offset by emphasis on corporate finance andby low default exposure classes such as trade financeGBI has well-established credit-monitoring processes and practices and selective credit selection. In general, the control cultureappears to be strict. Nonetheless, we note that GBI has relatively high gross related-party exposures at 25% of Tier 1 capital as of year-end 2015. This number falls to 6% of Tier 1 on a net basis, when off-setting the exposures with funding provided by group entities.Furthermore, credit-risk concentrations remain high, as demonstrated by the top 20 bank and corporate credit exposures, whichamounts to a high multiple of the bank's capital.

Strong capital base and good internal capital generation capabilityAt year-end 2015, GBI reported a Common Equity Tier 1 (CET1) ratio of 16.3% excluding 2015 H2 profit (2014: 16.7%, as reported tothe Dutch Central Bank, excluding H2 2014 profit). The slight decrease in the CET1 ratio is driven by a growth in the loan book. GBIapplies the Internal Ratings Based Approach for credit risk calculation; and it has adopted the Standardised Approach to market risk andthe Basic Indicator Approach to operational risk. GBI has not issued any hybrids.

The CET1 ratio appears to be high; however, we note that the following factors should also be taken into consideration:

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

5 19 August 2016 GarantiBank International N.V.: Update Following Recent Review for Downgrade

1. GBI's “headroom” over the regulatory requirement is lower than it might appear because of the Pillar 2 requirements of the Dutchsupervisor.

2. GBI's exposures to the potentially more volatile macroeconomic environment of developing and emerging markets.

The impact of CRD IV (Basel III) regulations has a limited impact on GBI because of its strong core Tier 1 capital, the absence of hybridcapital instruments, the bank's modest trading portfolio, and its good liquidity and funding profile.

Our assigned Capital score of a1 is a reflection of the strong capitalisation of the bank.

Good profit generation although net interest margins are under pressureAs of year-end 2015, GBI reported operating revenues (Dutch GAAP) of EUR 103 million (-17% year-on-year), that resulted in pre-provisioning income of EUR 63 million (-19%), leading, in turn, to a net income of EUR 11 million (-75%). The drop in profitability atGBI reflects both weaker net banking income generation and an increase in cost of risk.

GBI's operating revenues are 61% composed of net-interest income and 39% of non-interest revenues. The fall in revenues in 2015was driven by a reduction of both income sources compared to the previous year. Net interest income dropped despite a growing loanbook, reflecting margin pressure due to the low interest environment that prevails in Europe.

GBI's cost-to-income ratio increased to 41% during 2015 (2014: 34%; 2013: 29%), reflecting lower net banking revenues while the sizeof operating costs was stable. GBI's efficiency remains strong, thanks to the lack of physical branch network.

Cost of risk has been quite limited over the past two years, ranging from 16% to 22% of the bank's pre-provision income. However, thecost of risk increased significantly to EUR 49 million in 2015, compared to EUR 19 million provisioned for the full year 2014, absorbing77% of the bank's pre-provision income. This increase in cost of risk is notably related to loans to companies active in commoditiestrading.

Despite the bank's strong efficiency, profitability deteriorated due to pressure on interest margins and on fees and commissions. Inaddition, the recent rise in loan loss provisions has affected profitability. We remain cautious on the sensitivity of the bank's bottom-line profit to sudden hike in cost of risk due to several credit concentrations in their loan book.

Solid liquidity profile supported by predominance of retail depositsGBI has a solid liquidity profile, supported by (1) a low average loan-to-deposit ratio of 84% as of year-end 2015 (2014: 77%; 2013:70%); (2) a predominance of retail deposits (that are covered by the Deposit Guarantee Scheme), which were stable during the globalfinancial crisis; and (3) a satisfactory share of liquid assets on its balance sheet. Additionally, the short duration of a large proportionof its assets (loans representing 26% of the balance sheet mature within three months), confers greater flexibility to GBI to adapt itsbalance-sheet structure.

At year-end 2015, GBI had the following funding sources:

» 65% of balance sheet is deposit funded (primarily composed of retail deposits), offered primarily through the Internet or callcenters

» Interbank (20%) consisting of a syndicated loan borrowing, money market borrowings, bilateral wholesale fundings, repos andborrowings under the ECB's TLTRO

» 10-year subordinated debt (2%) from its shareholder (TGB) issued in 2011 and in 2015

Historically, GBI has not issued preferred bonds and other debt capital market instruments, owing to its short asset durations (69% ofassets have remaining maturity of 1 year or less). Yet it relies on the interbank market as stated above.

As of year-end 2015, GBI liquid assets (presented as the sum of cash and assets due from central banks, interbank money-marketexposures to banks and securities) as a proportion of total assets was at 43%, compared to 47% of year-end 2014. Half of such liquidassets have counterparties in the developed countries and the other half have counterparties in emerging markets, which may provedifficult to liquidate in an adverse scenario.

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

6 19 August 2016 GarantiBank International N.V.: Update Following Recent Review for Downgrade

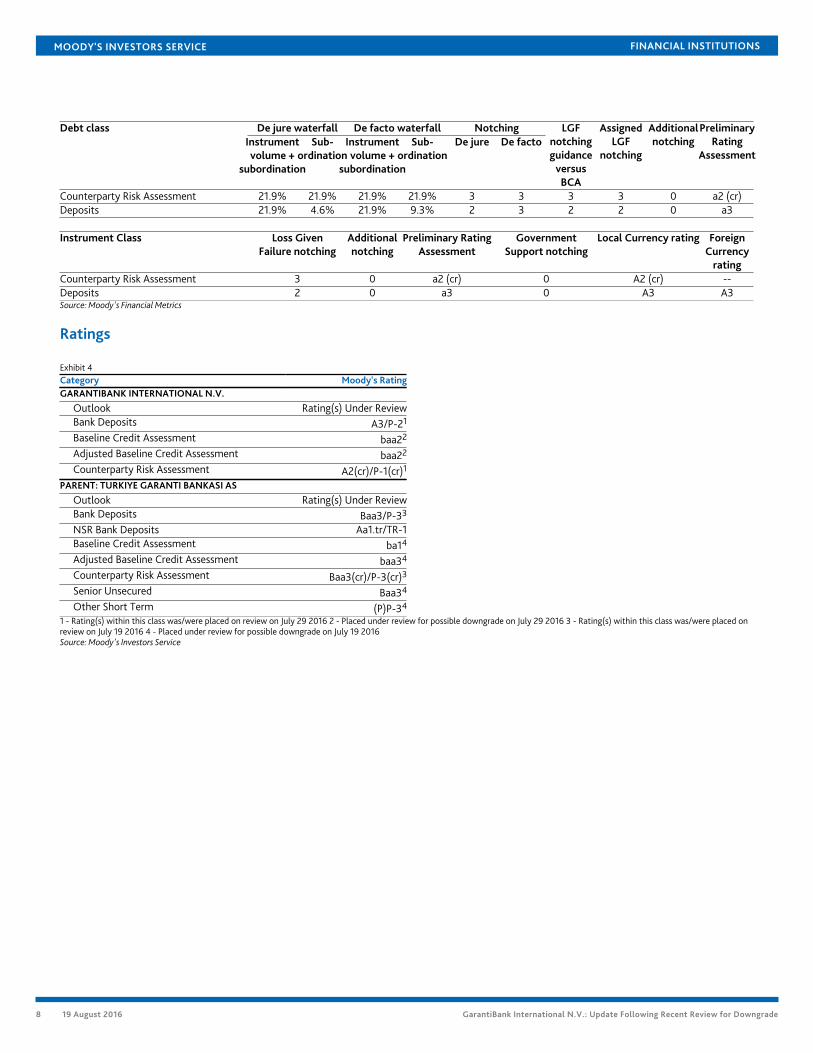

Notching ConsiderationsLoss Given Failure and Additional NotchingGBI is subject to the EU Bank Resolution and Recovery Directive (BRRD), which we consider to be an Operational Resolution Regime.We assume residual tangible common equity of 3% and losses post-failure of 8% of tangible banking assets, a 25% run-off in “junior”wholesale deposits, a 5% run-off in preferred deposits, and assign a 25% probability to deposits being preferred to senior unsecureddebt. These are in keeping with our standard assumptions.

We believe that GBI's deposits are likely to face very low loss-given-failure, due to the loss absorption provided by the combination ofa substantial deposit volume (we estimate junior deposits to make up about 13% of the group's tangible banking assets in failure), andsubordination of about 5% of tangible banking assets (and 9% in the event of deposits being preferred to senior debt). This results intwo notches of uplift from the adjusted BCA.

Government SupportThe implementation of the BRRD has led us to reconsider the potential for government support to benefit the bank's creditors. Weexpect a low probability of government support for GBI's deposits, resulting in no uplift for the long-term deposit ratings (unchanged).

Counterparty Risk AssessmentCR Assessments are opinions of how counterparty obligations are likely to be treated if a bank fails and are distinct from debt anddeposit ratings in that they (1) consider only the risk of default rather than both the likelihood of default and the expected financial losssuffered in the event of default and (2) apply to counterparty obligations and contractual commitments rather than debt or depositinstruments. The CR Assessment is an opinion of the counterparty risk related to a bank's covered bonds, contractual performanceobligations (servicing), derivatives (e.g., swaps), letters of credit, guarantees and liquidity facilities.

The CR Assessment is positioned at A2(cr)/Prime-1(cr). The CR Assessment is positioned three notches above the Adjusted BCA ofbaa2, based on the cushion against default provided to the senior obligations represented by the CR Assessment by subordinatedinstruments amounting to 21.9 % of Tangible Banking Assets. The main difference with our Advanced LGF approach used to determineinstrument ratings is that the CR Assessment captures the probability of default on certain senior obligations, rather than expectedloss, therefore we focus purely on subordination and take no account of the volume of the instrument class.

About Moody's Bank ScorecardOur Scorecard is designed to capture, express and explain in summary form our Rating Committee's judgment. When read inconjunction with our research, a fulsome presentation of our judgment is expressed. As a result, the output of our Scorecardmay materially differ from that suggested by raw data alone (though it has been calibrated to avoid the frequent need for strongdivergence). The Scorecard output and the individual scores are discussed in rating committees and may be adjusted up or down toreflect conditions specific to each rated entity.

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

7 19 August 2016 GarantiBank International N.V.: Update Following Recent Review for Downgrade

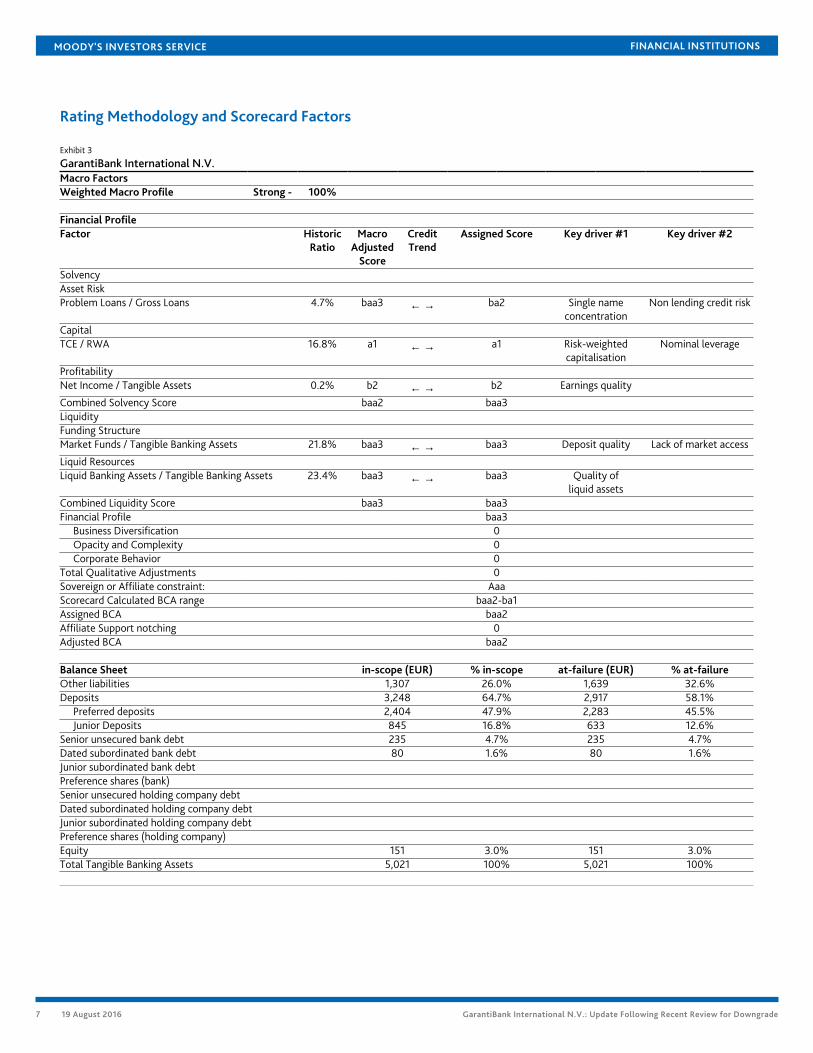

Rating Methodology and Scorecard Factors

Exhibit 3

GarantiBank International N.V.Macro FactorsWeighted Macro Profile Strong - 100%

Financial ProfileFactor Historic

RatioMacro

AdjustedScore

CreditTrend

Assigned Score Key driver #1 Key driver #2

SolvencyAsset RiskProblem Loans / Gross Loans 4.7% baa3 ← → ba2 Single name

concentrationNon lending credit risk

CapitalTCE / RWA 16.8% a1 ← → a1 Risk-weighted

capitalisationNominal leverage

ProfitabilityNet Income / Tangible Assets 0.2% b2 ← → b2 Earnings quality

Combined Solvency Score baa2 baa3LiquidityFunding StructureMarket Funds / Tangible Banking Assets 21.8% baa3 ← → baa3 Deposit quality Lack of market access

Liquid ResourcesLiquid Banking Assets / Tangible Banking Assets 23.4% baa3 ← → baa3 Quality of

liquid assetsCombined Liquidity Score baa3 baa3Financial Profile baa3

Business Diversification 0Opacity and Complexity 0Corporate Behavior 0

Total Qualitative Adjustments 0Sovereign or Affiliate constraint: AaaScorecard Calculated BCA range baa2-ba1Assigned BCA baa2Affiliate Support notching 0Adjusted BCA baa2

Balance Sheet in-scope (EUR) % in-scope at-failure (EUR) % at-failureOther liabilities 1,307 26.0% 1,639 32.6%Deposits 3,248 64.7% 2,917 58.1%

Preferred deposits 2,404 47.9% 2,283 45.5%Junior Deposits 845 16.8% 633 12.6%

Senior unsecured bank debt 235 4.7% 235 4.7%Dated subordinated bank debt 80 1.6% 80 1.6%Junior subordinated bank debtPreference shares (bank)Senior unsecured holding company debtDated subordinated holding company debtJunior subordinated holding company debtPreference shares (holding company)Equity 151 3.0% 151 3.0%Total Tangible Banking Assets 5,021 100% 5,021 100%

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

8 19 August 2016 GarantiBank International N.V.: Update Following Recent Review for Downgrade

De jure waterfall De facto waterfall NotchingDebt classInstrumentvolume +

subordination

Sub-ordination

Instrumentvolume +

subordination

Sub-ordination

De jure De factoLGF

notchingguidance

versusBCA

AssignedLGF

notching

Additionalnotching

PreliminaryRating

Assessment

Counterparty Risk Assessment 21.9% 21.9% 21.9% 21.9% 3 3 3 3 0 a2 (cr)Deposits 21.9% 4.6% 21.9% 9.3% 2 3 2 2 0 a3

Instrument Class Loss GivenFailure notching

Additionalnotching

Preliminary RatingAssessment

GovernmentSupport notching

Local Currency rating ForeignCurrency

ratingCounterparty Risk Assessment 3 0 a2 (cr) 0 A2 (cr) --Deposits 2 0 a3 0 A3 A3Source: Moody's Financial Metrics

Ratings

Exhibit 4Category Moody's RatingGARANTIBANK INTERNATIONAL N.V.

Outlook Rating(s) Under ReviewBank Deposits A3/P-21

Baseline Credit Assessment baa22

Adjusted Baseline Credit Assessment baa22

Counterparty Risk Assessment A2(cr)/P-1(cr)1

PARENT: TURKIYE GARANTI BANKASI AS

Outlook Rating(s) Under ReviewBank Deposits Baa3/P-33

NSR Bank Deposits Aa1.tr/TR-1Baseline Credit Assessment ba14

Adjusted Baseline Credit Assessment baa34

Counterparty Risk Assessment Baa3(cr)/P-3(cr)3

Senior Unsecured Baa34

Other Short Term (P)P-34

1 - Rating(s) within this class was/were placed on review on July 29 2016 2 - Placed under review for possible downgrade on July 29 2016 3 - Rating(s) within this class was/were placed onreview on July 19 2016 4 - Placed under review for possible downgrade on July 19 2016Source: Moody's Investors Service

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

9 19 August 2016 GarantiBank International N.V.: Update Following Recent Review for Downgrade

© 2016 Moody's Corporation, Moody's Investors Service, Inc., Moody's Analytics, Inc. and/or their licensors and affiliates (collectively, "MOODY'S"). All rights reserved.

CREDIT RATINGS ISSUED BY MOODY'S INVESTORS SERVICE, INC. AND ITS RATINGS AFFILIATES ("MIS") ARE MOODY'S CURRENT OPINIONS OF THE RELATIVE FUTURE CREDITRISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES, AND CREDIT RATINGS AND RESEARCH PUBLICATIONS PUBLISHED BY MOODY'S ("MOODY'SPUBLICATIONS") MAY INCLUDE MOODY'S CURRENT OPINIONS OF THE RELATIVE FUTURE CREDIT RISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKESECURITIES. MOODY'S DEFINES CREDIT RISK AS THE RISK THAT AN ENTITY MAY NOT MEET ITS CONTRACTUAL, FINANCIAL OBLIGATIONS AS THEY COME DUE AND ANYESTIMATED FINANCIAL LOSS IN THE EVENT OF DEFAULT. CREDIT RATINGS DO NOT ADDRESS ANY OTHER RISK, INCLUDING BUT NOT LIMITED TO: LIQUIDITY RISK, MARKETVALUE RISK, OR PRICE VOLATILITY. CREDIT RATINGS AND MOODY'S OPINIONS INCLUDED IN MOODY'S PUBLICATIONS ARE NOT STATEMENTS OF CURRENT OR HISTORICALFACT. MOODY'S PUBLICATIONS MAY ALSO INCLUDE QUANTITATIVE MODEL-BASED ESTIMATES OF CREDIT RISK AND RELATED OPINIONS OR COMMENTARY PUBLISHEDBY MOODY'S ANALYTICS, INC. CREDIT RATINGS AND MOODY'S PUBLICATIONS DO NOT CONSTITUTE OR PROVIDE INVESTMENT OR FINANCIAL ADVICE, AND CREDITRATINGS AND MOODY'S PUBLICATIONS ARE NOT AND DO NOT PROVIDE RECOMMENDATIONS TO PURCHASE, SELL, OR HOLD PARTICULAR SECURITIES. NEITHER CREDITRATINGS NOR MOODY'S PUBLICATIONS COMMENT ON THE SUITABILITY OF AN INVESTMENT FOR ANY PARTICULAR INVESTOR. MOODY'S ISSUES ITS CREDIT RATINGSAND PUBLISHES MOODY'S PUBLICATIONS WITH THE EXPECTATION AND UNDERSTANDING THAT EACH INVESTOR WILL, WITH DUE CARE, MAKE ITS OWN STUDY ANDEVALUATION OF EACH SECURITY THAT IS UNDER CONSIDERATION FOR PURCHASE, HOLDING, OR SALE.

MOODY'S CREDIT RATINGS AND MOODY'S PUBLICATIONS ARE NOT INTENDED FOR USE BY RETAIL INVESTORS AND IT WOULD BE RECKLESS AND INAPPROPRIATE FORRETAIL INVESTORS TO USE MOODY'S CREDIT RATINGS OR MOODY'S PUBLICATIONS WHEN MAKING AN INVESTMENT DECISION. IF IN DOUBT YOU SHOULD CONTACTYOUR FINANCIAL OR OTHER PROFESSIONAL ADVISER. ALL INFORMATION CONTAINED HEREIN IS PROTECTED BY LAW, INCLUDING BUT NOT LIMITED TO, COPYRIGHT LAW,AND NONE OF SUCH INFORMATION MAY BE COPIED OR OTHERWISE REPRODUCED, REPACKAGED, FURTHER TRANSMITTED, TRANSFERRED, DISSEMINATED, REDISTRIBUTEDOR RESOLD, OR STORED FOR SUBSEQUENT USE FOR ANY SUCH PURPOSE, IN WHOLE OR IN PART, IN ANY FORM OR MANNER OR BY ANY MEANS WHATSOEVER, BY ANYPERSON WITHOUT MOODY'S PRIOR WRITTEN CONSENT.

All information contained herein is obtained by MOODY'S from sources believed by it to be accurate and reliable. Because of the possibility of human or mechanical error as wellas other factors, however, all information contained herein is provided "AS IS" without warranty of any kind. MOODY'S adopts all necessary measures so that the information ituses in assigning a credit rating is of sufficient quality and from sources MOODY'S considers to be reliable including, when appropriate, independent third-party sources. However,MOODY'S is not an auditor and cannot in every instance independently verify or validate information received in the rating process or in preparing the Moody's Publications.

To the extent permitted by law, MOODY'S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability to any person or entity for anyindirect, special, consequential, or incidental losses or damages whatsoever arising from or in connection with the information contained herein or the use of or inability to use anysuch information, even if MOODY'S or any of its directors, officers, employees, agents, representatives, licensors or suppliers is advised in advance of the possibility of such losses ordamages, including but not limited to: (a) any loss of present or prospective profits or (b) any loss or damage arising where the relevant financial instrument is not the subject of aparticular credit rating assigned by MOODY'S.

To the extent permitted by law, MOODY'S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability for any direct or compensatorylosses or damages caused to any person or entity, including but not limited to by any negligence (but excluding fraud, willful misconduct or any other type of liability that, for theavoidance of doubt, by law cannot be excluded) on the part of, or any contingency within or beyond the control of, MOODY'S or any of its directors, officers, employees, agents,representatives, licensors or suppliers, arising from or in connection with the information contained herein or the use of or inability to use any such information.

NO WARRANTY, EXPRESS OR IMPLIED, AS TO THE ACCURACY, TIMELINESS, COMPLETENESS, MERCHANTABILITY OR FITNESS FOR ANY PARTICULAR PURPOSE OF ANY SUCHRATING OR OTHER OPINION OR INFORMATION IS GIVEN OR MADE BY MOODY'S IN ANY FORM OR MANNER WHATSOEVER.

Moody's Investors Service, Inc., a wholly-owned credit rating agency subsidiary of Moody's Corporation ("MCO"), hereby discloses that most issuers of debt securities (includingcorporate and municipal bonds, debentures, notes and commercial paper) and preferred stock rated by Moody's Investors Service, Inc. have, prior to assignment of any rating,agreed to pay to Moody's Investors Service, Inc. for appraisal and rating services rendered by it fees ranging from $1,500 to approximately $2,500,000. MCO and MIS also maintainpolicies and procedures to address the independence of MIS's ratings and rating processes. Information regarding certain affiliations that may exist between directors of MCO andrated entities, and between entities who hold ratings from MIS and have also publicly reported to the SEC an ownership interest in MCO of more than 5%, is posted annually atwww.moodys.com under the heading "Investor Relations — Corporate Governance — Director and Shareholder Affiliation Policy."

Additional terms for Australia only: Any publication into Australia of this document is pursuant to the Australian Financial Services License of MOODY'S affiliate, Moody's InvestorsService Pty Limited ABN 61 003 399 657AFSL 336969 and/or Moody's Analytics Australia Pty Ltd ABN 94 105 136 972 AFSL 383569 (as applicable). This document is intendedto be provided only to "wholesale clients" within the meaning of section 761G of the Corporations Act 2001. By continuing to access this document from within Australia, yourepresent to MOODY'S that you are, or are accessing the document as a representative of, a "wholesale client" and that neither you nor the entity you represent will directly orindirectly disseminate this document or its contents to "retail clients" within the meaning of section 761G of the Corporations Act 2001. MOODY'S credit rating is an opinion asto the creditworthiness of a debt obligation of the issuer, not on the equity securities of the issuer or any form of security that is available to retail investors. It would be recklessand inappropriate for retail investors to use MOODY'S credit ratings or publications when making an investment decision. If in doubt you should contact your financial or otherprofessional adviser.

Additional terms for Japan only: Moody's Japan K.K. ("MJKK") is a wholly-owned credit rating agency subsidiary of Moody's Group Japan G.K., which is wholly-owned by Moody'sOverseas Holdings Inc., a wholly-owned subsidiary of MCO. Moody's SF Japan K.K. ("MSFJ") is a wholly-owned credit rating agency subsidiary of MJKK. MSFJ is not a NationallyRecognized Statistical Rating Organization ("NRSRO"). Therefore, credit ratings assigned by MSFJ are Non-NRSRO Credit Ratings. Non-NRSRO Credit Ratings are assigned by anentity that is not a NRSRO and, consequently, the rated obligation will not qualify for certain types of treatment under U.S. laws. MJKK and MSFJ are credit rating agencies registeredwith the Japan Financial Services Agency and their registration numbers are FSA Commissioner (Ratings) No. 2 and 3 respectively.

MJKK or MSFJ (as applicable) hereby disclose that most issuers of debt securities (including corporate and municipal bonds, debentures, notes and commercial paper) and preferredstock rated by MJKK or MSFJ (as applicable) have, prior to assignment of any rating, agreed to pay to MJKK or MSFJ (as applicable) for appraisal and rating services rendered by it feesranging from JPY200,000 to approximately JPY350,000,000.

MJKK and MSFJ also maintain policies and procedures to address Japanese regulatory requirements.

REPORT NUMBER 1036543