G B (S S R L - RNS · PDF fileAppendix to the Explanatory Notes to "Golden Bar Stand Alone...

121

GOLDEN BAR (SECURITISATION) S.R.L. 12th FINANCIAL YEAR FINANCIAL STATEMENTS AS AT 31 DECEMBER 2 0 1 1 Director Mr. Tito Musso Auditors Deloitte & Touche S.p.A.

Transcript of G B (S S R L - RNS · PDF fileAppendix to the Explanatory Notes to "Golden Bar Stand Alone...

GOLDEN BAR (SECURITISATION) S.R.L.

12th FINANCIAL YEAR

FINANCIAL STATEMENTS AS AT 31 DECEMBER 2 0 1 1

Director Mr. Tito Musso Auditors Deloitte & Touche S.p.A.

TABLE OF CONTENTS

REPORT ON OPERATIONS ..................................................................................................... 1

ANALYSIS OF FINANCIAL POSITION AND INCOME RESULTS .................................................. 4

OTHER INFORMATION WORTH MENTIONING ........................................................................ 4

OTHER DISCLOSURES .......................................................................................................... 4

PROPOSED ALLOCATION OF THE RESULT FOR THE YEAR ...................................................... 6

BALANCE SHEET ................................................................................................................... 8

INCOME STATEMENT ............................................................................................................ 9

STATEMENT OF COMPREHENSIVE INCOME ......................................................................... 10

STATEMENT OF CHANGES IN SHAREHOLDERS' EQUITY ....................................................... 11

CASH FLOW STATEMENT .................................................................................................... 13

NOTES TO THE ACCOUNTS ................................................................................................. 14

1 Part A - Accounting Policies ................................................................................. 14

2 Part B - Information on the Balance Sheet ........................................................... 18

3 Part C - Information on Income Statement ........................................................... 22

Appendix to the Explanatory Notes to "Golden Bar Securitisation Programme" ................. 36

Appendix to the Explanatory Notes to "Golden Bar Securitisation Programme II" ............. 52

Appendix to the Explanatory Notes to "Golden Bar Securitisation Programme III" ............ 62

Appendix to the Explanatory Notes to "Golden Bar Securitisation Programme IV"............. 72

Appendix to the Explanatory Notes to "Golden Bar Stand Alone 2011 -1" ........................ 84

Appendix to the Explanatory Notes to "Golden Bar Stand Alone 2011 -2" ........................ 96

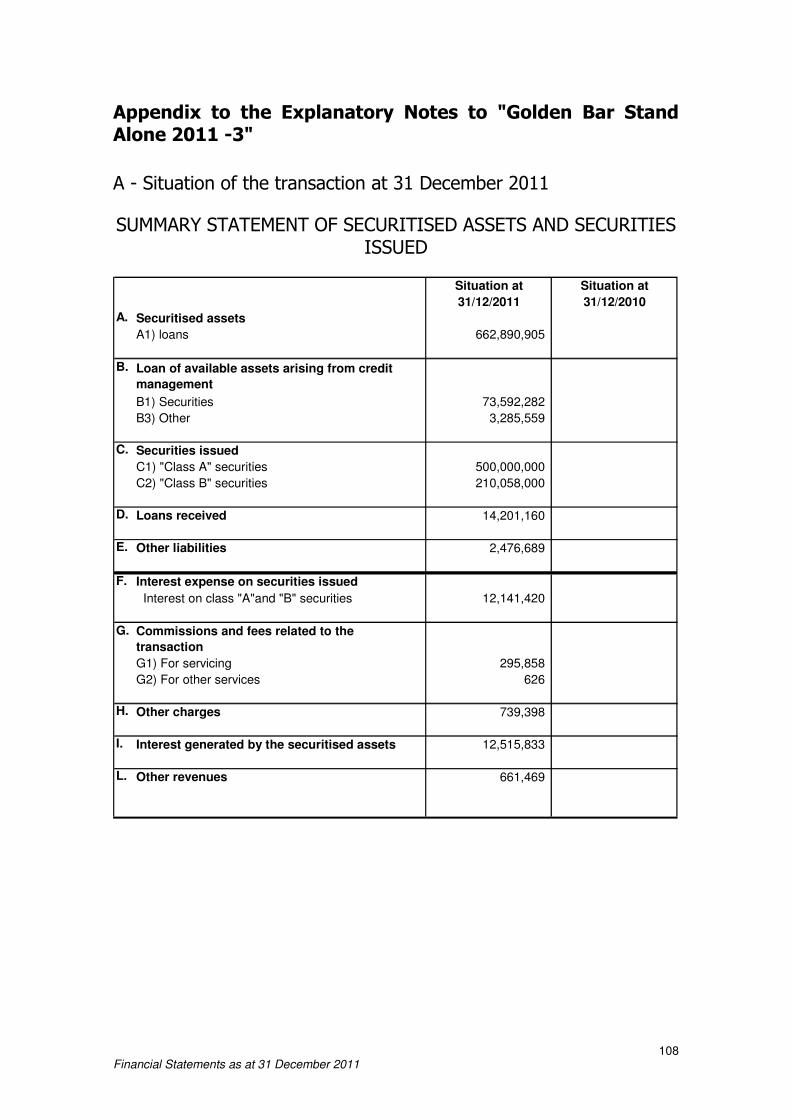

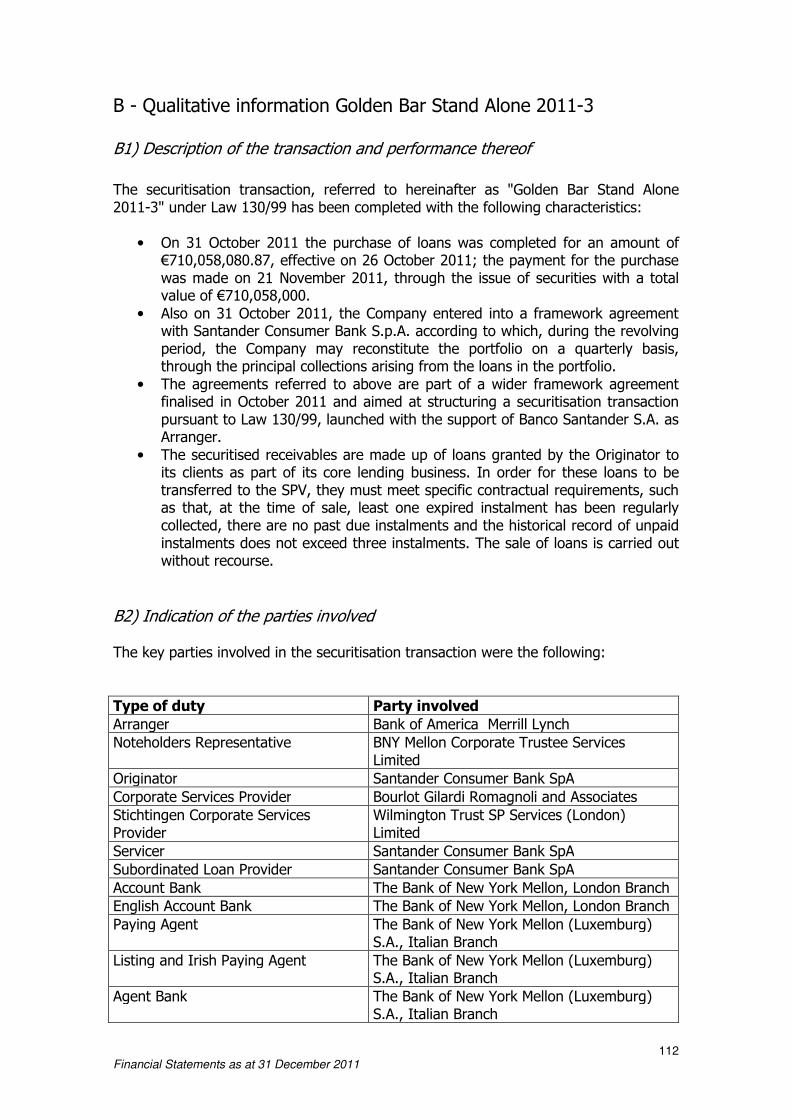

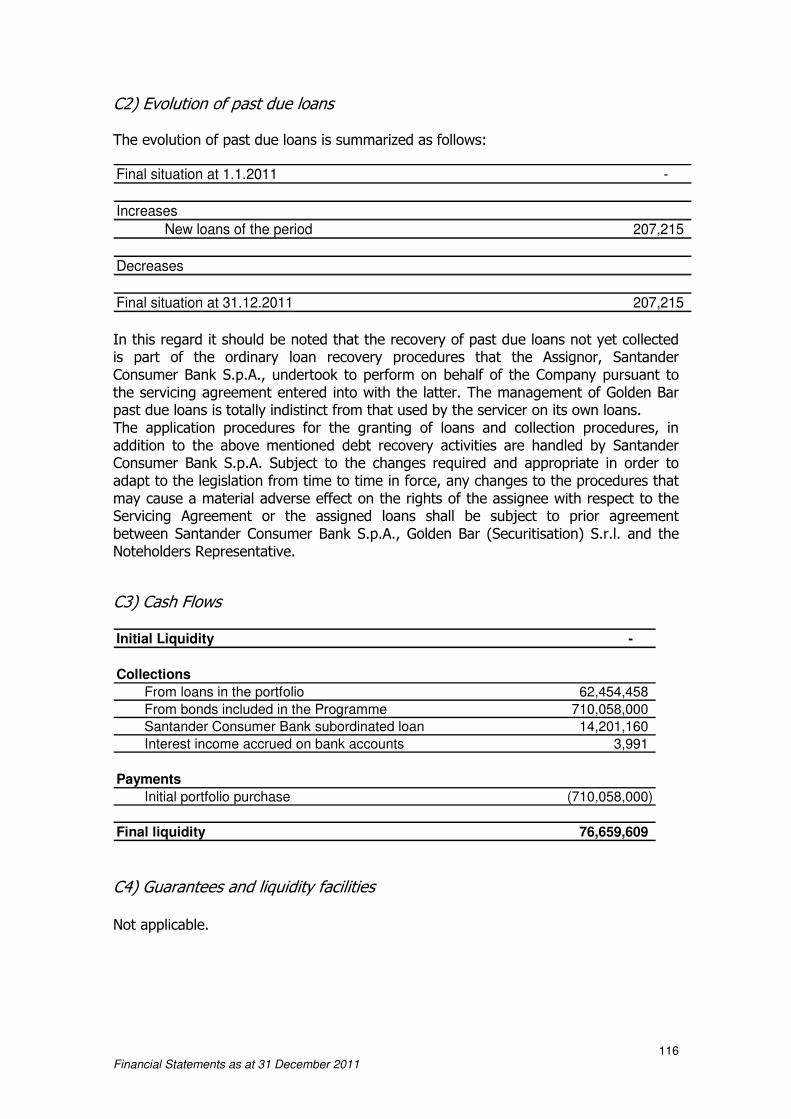

Appendix to the Explanatory Notes to "Golden Bar Stand Alone 2011 -3" ...................... 108

1 Financial Statements as at 31 December 2011

REPORT ON OPERATIONS

Dear Shareholders, Your Company's 12th financial year ended 31 December 2011; during the year, a securitisation transaction originated in November 2010 was finalised and 2 new securitisation transactions of consumer loans generated by Santander Consumer Bank S.p.A. and financed through the issue of securities were carried out. In March 2011, we completed the stand-alone transaction named "Golden Bar Stand Alone 2011-1" 1(originated in 2010) with the issue of the first and only series of securities amounting to €600,000,000, divided into three classes with decreasing reimbursement priority, the first of which has a rating issued by Moody's Investors Services (Aaa) and Fitch Ratings Ltd. (AAA) and the second has a rating issued by Moody's Investors Services (Baa1). The class A security was subscribed for an amount of €150,000,000 by an institutional investor and an amount of €261,000,000 by Santander Consumer Bank SpA, while the remaining classes of securities were fully subscribed by the Originator. During the year the Company purchased additional loan portfolios (revolving purchases), within the limits of its proceeds (principal) arising from loans already transferred to it and not immediately used to exercise the securities embedded rights, amounting to €199,703,967. The portfolio that was initially purchased will be reconstituted quarterly with portfolios having the same characteristics throughout the revolving period. As part of the second stand-alone Securitisation transaction, named "Golden Bar Stand Alone 2011-2", in August 2011 we made the initial purchase of a performing loan portfolio amounting to €950,000,104 from Santander Consumer Bank. In October 2011, the transaction was finalised by issuing the first and only series of securities amounting to €950,000,000, divided into three classes with decreasing reimbursement priority, the first of which has a rating issued by Moody’s Investors Services (Aaa) and DBRS Inc (AAA) and the second has a rating issued by Moody's Investors Services (Baa1) and DBRS Inc. (A(high)). The securities issued were fully subscribed by Santander Consumer Bank. The portfolio that was initially purchased will be reconstituted quarterly with portfolios having the same characteristics throughout the revolving period. During the year the Company purchased additional loan portfolios (revolving purchases), within the limits of its proceeds (principal) arising from loans already transferred to it and not immediately used to exercise the securities embedded rights, amounting to €89,076,201. As part of the third Securitisation transaction, named "Golden Bar Stand Alone 2011-3", in October 2011 we made the initial purchase of a performing loan portfolio amounting to €710,058,081 from Santander Consumer Bank. In November 2011 the Transaction was finalised with the issuance of the first and only series of securities amounting to €710,058,000, divided into two classes with decreasing reimbursement priority, both without rating. The A class was fully privately subscribed by Bank of America and the Junior security by Santander Consumer Bank.

1 In the Balance Sheet for the year ended 31 December 2010, that securitisation transaction

was named "Golden Bar Securitisation 7" as it had not yet been finalised.

2 Financial Statements as at 31 December 2011

The portfolio that was initially purchased will be reconstituted quarterly with portfolios having the same characteristics throughout the revolving period. The Programmes previously issued have a structure that provides for a series of sales of loans by Santander Consumer Bank to the Company, each of which is funded by a new securities issue; the loans purchased from time to time by Golden Bar represent a single asset, with no segregation between the various loans purchased from time to time, so that the securities of each issue are backed by the entire loan portfolio purchased over the life of the Programme. Unlike the Programme, the new stand-alone Transactions are characterized by a single sale of receivables and related issue of securities. With reference to the Programme launched in December 2003 through the initial purchase from Santander Consumer Bank SpA of performing loans amounting to €200,002,344 (Golden Bar Securitisation Programme - Series 1/2004), within which three successive initial purchases of loan portfolios and respective securities issues were carried out, more specifically in November 2004 for an amount of €500,007,552 (Golden Bar Securitisation Programme - Series 2/2004), in November 2005 for an amount of €700,008,227 (Golden Bar Securitisation Programme - Series 3/2006) and in December 2006 for an amount of €700,005,785 (Golden Bar Securitisation Programme - Series 4/2007), during the year there no new issues. As per Pricing Supplement signed in March 2004, the Company completed the redemption of the 1/2004 securities Series, for an amount of €8,390,000; it has also continued with the redemption of the securities of the 2/2004 Series, for an amount €60,296,949, the 3/2006 Series, for an amount of €138,980,209 and the 4/2007 Series for an amount of €349,392,096, for a total amount at the balance sheet date of €557,059,254. During the year the Company did not purchase additional loan portfolios (revolving purchases). With reference to the Programme launched in March 2008 through the initial purchase from Santander Consumer Bank SpA of performing loans amounting to €700,001,956 (Golden Bar Securitisation Programme II - Series 1/2008), during the year no new issues were carried out; the Company purchased instead additional loan portfolios (revolving purchases), within the limits of the proceeds (principal) arising from the loans already transferred to it and not immediately used to exercise the securities embedded rights amounting to €60,079,302. This Programme was terminated in advance on 15 July 2011 and the related securities were fully redeemed, for a total of €700,000,000. With reference to the Programme launched in December 2008 through the initial purchase from Santander Consumer Bank SpA of performing loans amounting to €700,002,164 (Golden Bar Securitisation Programme III- Series 1/2008), during the year no new issues were carried out; the Company purchased instead additional loan portfolios (revolving purchases), within the limits of the proceeds (principal) arising from the loans already transferred to it and not immediately used to exercise the securities embedded rights amounting to €135,204,669. As for the previous Programme, also this Programme was terminated in advance on 15 July 2011 and the related securities were fully redeemed, for a total of €750,000,000. With reference to the Programme launched in November 2009 through the initial purchase from Santander Consumer Bank SpA of performing loans amounting to

3 Financial Statements as at 31 December 2011

€800,001,181 (Golden Bar Securitisation Programme IV- Series 1/2009), during the year no new issues were carried out; the Company purchased instead additional loan portfolios (revolving purchases), within the limits of the proceeds (principal) arising from the receivables already transferred to it and not immediately used to exercise the securities embedded rights amounting to €283,947,440. With reference to the transaction “Golden Bar Stand Alone 2011-1”launched in November 2010 through the initial purchase from Santander Consumer Bank SpA of performing loans amounting to €600,001,249 the Company purchased additional loan portfolios (revolving purchases), within the limits of the proceeds (principal) arising from the loans already transferred to it and not immediately used to exercise the securities embedded rights amounting to €199,703,967. All securitised receivables arise from loans granted by Santander Consumer Bank SpA to its clients as part of its core lending business. As regards these transactions, Santander Consumer Bank also assumed the "servicer" role, having been provided with technical tools and an organizational structure suitable to monitor the various securitisation stages and to effectively perform collection and cash and payment services. Pursuant to Law no.130/1999 the receivables for each transaction, are totally segregated assets both with respect to each other and the assets of the Company and therefore, consistent with the independence of assets that characterizes the transactions, their accounting treatment and reporting is done individually, in accordance with the instructions given by the Bank of Italy by Regulation dated 29 March 2000 and subsequent ones. Consequently, the accounting information relating to these transactions is shown separately in special attachments to the Notes containing the qualitative and quantitative data necessary for a complete and clear presentation. The year 2011 ended with a loss of €218 after recovering, pursuant to contractual conditions and against the segregated assets, the costs incurred to operate the business.

4 Financial Statements as at 31 December 2011

ANALYSIS OF FINANCIAL POSITION AND INCOME RESULTS The assets on the balance sheet consist of "receivables" relating to current account balances (€11,434), current "Tax assets" arising mainly from a residual corporate income tax receivable for 2010 (IRES) carried forward (€126,012), "Other assets" relating to a receivable from the "separated assets" mainly due to the charge back of the costs pursuant to contractual conditions (€279,281). The liabilities in the balance sheet are almost exclusively made up of paid in "Capital" (€10,000) and "Other liabilities" (€509,257), the latter consisting of amounts due to service suppliers and payables to the segregated assets. The income statement, which reflects the costs incurred for the normal operation of the Company, charged back to the segregate assets, shows a positive result before taxes, while presenting a net loss of €218 as a result of the income tax for the period. The financial statements are audited by Deloitte & Touche S.p.A. in compliance with the appointment made by the competent corporate bodies for the period 2009 to 2011. This appointment was made voluntarily and not pursuant to Legislative Decree 39/2010.

OTHER INFORMATION WORTH MENTIONING In the first three months of 2012, the Company, in accordance with the contractual provisions of each securitisation transaction, completed "revolving" purchases of loans for a nominal value of €81,110,702 in relation to the "Golden Bar Securitisation Programme IV", € 61,254,261 in relation to the "Golden Bar Stand Alone 2011-1", €78,410,215 in relation to the "Golden Bar Stand Alone 2011-2" and €95,567,182 in relation to the "Golden Bar Stand Alone 2011-3". In the same period securities relating to the second, third and fourth series issued under the first Programme were redeemed for a value equal respectively, to €7,910,000, €19,194,009, €49,829,250.

OTHER DISCLOSURES In relation to the provisions of Legislative Decree no.196 of 30 June 2003 ("Personal Data protection Code"), it should be noted that pursuant to Article 29, paragraphs 1 and 3 of the above Code, the Company appointed Santander Consumer Bank as data processor with regard to the processing of data performed during the administration, management, collection and recovery of receivables.

RESEARCH AND DEVELOPMENT ACTIVITIES No research and development costs were incurred by the Company.

5 Financial Statements as at 31 December 2011

TREASURY SHARES OR SHARES OF THE PARENT COMPANY Pursuant to the provisions of Art. 2428 of the Italian Civil Code please note that during the year the Company did not purchase, sold or hold in portfolio - either directly or through trust companies or nominees -treasury shares or shares of the parent.

MANAGEMENT AND CO-ORDINATION ACTIVITIES Pursuant to the provisions of Art. 2497bis of the Italian Civil Code please note that no person exercises management and coordination over the Company.

TRANSACTIONS WITH RELATED PARTIES AND INTRA-GROUP TRANSACTIONS The information regarding related party transactions, as required by art. 2428 of the Italian Civil Code, is provided in the Notes. In any case, the company did not carry out transactions with related parties and intra-group transactions except those made under the securitisation transaction with the company Santander Consumer Bank S.p.A.. For additional information and details please refer to Part D of the notes.

DISCLOSURES ON RISKS AND HEDGING POLICIES With reference to the company's assets, credit risk and market risk, in light of the business in which the Company is engaged, can be considered negligible and, therefore, it was not deemed necessary to implement any hedging policy. With reference to securitised assets and considered the provisions of Law 130/1999, the above risks are transferred to the securities holders. Regarding operational risk, it should be noted that the Company has no employees and it has delegated the performance of its functions and the associated operational risk to the entities in charge as per contract.

DISCLOSURE PURSUANT TO ARTICLE. 123-BIS OF LEGISLATIVE DECREE 58/98 Pursuant to Article.123-bis of Legislative Decree no. 58 of 24 February 1998, the reports of issuers of securities admitted to trading on regulated markets must contain a specific section, named "Report on corporate governance and ownership structure", which, pursuant to paragraph 2, letter b), of the said article, contains information about "the main characteristics of existing risk management and internal audit systems used in relation to the financial reporting process, including consolidated reports, where applicable". The Company has no employees. In pursuit of its corporate purpose, and consequently also for activities related to risk management and internal audit systems in place in relation to the financial reporting process, the Company appointed agents for this purpose. In particular, risk management and internal audit systems used in relation to

6 Financial Statements as at 31 December 2011

the financial reporting process can be traced back to the originator of the securitisation transaction and the corporate servicer. The contractual documentation of the securitisation transaction governs the appointment and specific tasks that each Company's agent is required to perform. This information is also contained in Part D, Section F.3, of the Notes. The transaction's agents are appointed from among parties that carry out the tasks assigned by the company as part of their business activity. This task must be performed by the agents in accordance with the applicable law and in such a manner that the Company can timely fulfil its obligations under the transaction documents and the law. The main roles of these agents are the following:

(i) Servicer, who, among other things, manages the purchased loans; (ii) Corporate Servicer, who is in charge of the Company's administrative and

accounting management, and (iii) Cash Manager, Computation Agent and Paying Agent, who perform treasury

management, calculation and payment services. In particular, the Servicer is the "entity responsible for the collection of purchased receivables and treasury and payment services" as provided for in Article 2, paragraph 3, letter (c) of Law 130/1999. Pursuant to Article 2, paragraph 6, of Law 130/1999 the Servicer role may be covered by banks or by intermediaries registered in the special list referred to in art. 107 of Legislative Decree no. 385 of 1 September 1993, which check that transactions comply with the law and the prospectus. Also pursuant to Bank of Italy Regulation of 23 August 2000 the Servicer is responsible both for tasks of an operating nature and for "guaranteeing" that securitisation transactions are properly carried out in the interests of securities holders and, in general, of the market. Finally, with reference to financial information, this is prepared by the Corporate Servicer primarily using data provided by the person responsible for the management of purchased receivables. The Sole Director of the Company monitors and verifies agents' compliance with the tasks assigned to them, in their respective roles, including with regard to the financial reporting process.

PROPOSED ALLOCATION OF THE RESULT FOR THE YEAR

The company ended the year with a loss of €218 which we propose to carry forward. Turin, 05 April 2012 The Sole Director

Tito Musso

7 Financial Statements as at 31 December 2011

FINANCIAL STATEMENTS AS AT 31 DECEMBER 2011

8 Financial Statements as at 31 December 2011

BALANCE SHEET

Assets 31/12/2011 31/12/2010

60 Accounts receivables 11,434 11,427

120 Tax assets 214,071 172,380

a) current 214,071 165,319

b) advanced - 7,061

140 Other assets 298,360 169,203

TOTAL ASSETS 523,865 353,010

Liabilities and shareholders' equity 31/12/2011 31/12/2010

10 Payables 0 0

70 Tax liabilities 3,187 3,728

a) current 3,187 3,728

90 Other liabilities 509,257 337,643

120 Capital 10,000 10,000

160 Reserves 1,639 1,744180 Profit (loss) for the year (218) (105)

TOTAL LIABILITIES AND SHAREHOLDERS' EQUITY 523,865 353,010

9 Financial Statements as at 31 December 2011

INCOME STATEMENT

Items 31/12/2011 31/12/2010

10 Interest income and similar income 125 59

20 Interest expenses and similar charges (206) (60)

GROSS OPERATING INCOME (81) (1)

110 Administrative expenses: (558,439) (215,807)

a) staff costs (42,610) (40,019)

b) other administrative expenses (515,829) (175,788)

160 Other operating income and expenses 581,965 217,086

INCOME FROM OPERATIONS 23,445 1,277

OPERATING PROFIT (LOSS) FROM ORDINARY

ACTIVITIES BEFORE TAXES 23,445 1,277

190 Tax on current operations for the period (23,663) (1,382)

OPERATING PROFIT (LOSS) FROM ORDINARY

ACTIVITIES AFTER TAXES (218) (105)

200

Profit (Loss) of groups of operations being discontinued after

taxes 0 0

PROFIT (LOSS) FOR THE YEAR (218) (105)

OPERATING PROFIT (LOSS) FROM ORDINARY

ACTIVITIES AFTER TAXES(218) (105)

200Profit (Loss) of groups of operations being discontinued after

taxes- -

PROFIT (LOSS) FOR THE YEAR (218) (105)

10 Financial Statements as at 31 December 2011

STATEMENT OF COMPREHENSIVE INCOME

10 Profit (loss) for the year (218) (105)Other income components after taxes

20 Available for sale financial assets

30 Tangible assets

40 Intangible assets

50 Foreign investment hedge

60 Cash flow hedge

70 Currency differences

80 Non-current assets held for sale

90 Actuarial profits (losses) on defined benefit plans

100 Share of the valuation reserves of equity investments

designated at equity

110 Total other income components after taxes - -

Items 2011 2010

120 Total profitability (Item 10. + 110.) (218) (105)

11 Financial Statements as at 31 December 2011

STATEMENT OF CHANGES IN SHAREHOLDERS' EQUITY Financial year 2011

Reserves

Dividends

and other

allocations

New

shares

issued

Own

shares

purchased

Extra

dividends

Changes in

equity

instrument

s

Other

changes

Capital 10,000 - 10,000 10,000 Issue premium

Reserves:

a) profit 1,744 - 1,744 (105) 1,639 b) other

Valuation reserves

Capital instruments

Own shares

Profit (loss) for the period (105) (105) (218) (218)Shareholders' equity 11,639 11,639 (218) 11,421

Comprehensive income for 2011

Allocation of

profits/losses for the

previous year Shareholders’ equity transactions

Changes in the year

Change in opening balance

Shareholders' equity as at 31

December 2011

Balance as at 1 January 2011

Balance as at 31 December 2010

Changes in

reserves

12 Financial Statements as at 31 December 2011

Financial year 2010

Reserves

Dividends

and other

allocations

New

shares

issued

Own

shares

purchased

Extra

dividends

Changes in

equity

instrument

s

Other

changes

Capital 10,000 - 10,000 10,000 Issue premium

Reserves:

a) profit 1,703 - 1,703 41 1,744 b) other

Valuation reserves

Capital instruments

Own shares

Profit (loss) for the period 41 - 41 (41) (105) (105)Shareholders' equity 11,744 11,744 (105) 11,639

Balance as at 31 December 2009

Change in opening balance

Balance as at 1 January 2010

Allocation of

profits/losses for the

previous year

Changes in

reserves

Changes in the year

Shareholders’ equity transactions

Shareholders' equity as at 31

December 2010

Comprehensive income for 2010

13 Financial Statements as at 31 December 2011

CASH FLOW STATEMENT

2011 2010

1 Management 23,445 (105)

- Interest income received (+) 125 59

- Interest expenses paid (-) (206) (60)

- Dividends and similar revenues (+) - -

- Net commissions (-/+) - -

- Staff costs (-) (42,610) (40,019)

- Other costs (-) (515,829) (175,788)

9 - Other revenues (+) 581,965 217,086

- Taxes and duties (-) 0 (1,382)

- Cost / revenue from discontinued groups of assets and net of - -

tax effect (+/-)

2 Liquidity generated/absorbed by financial assets (194,510) 5,716

- financial assets held for trading - -

- financial assets designated at fair value - -

- available-for-sale financial assets - -

- loans to banks - -

- due from financial institutions - -

- loans to customers - -

- other assets (194,510) 5,716

3 Cash generated/absorbed by financial liabilities 171,072 (5,653)

- amounts owed to banks - -

- due to financial institutions - -

- amounts owed to customers - -

- securities in issue - -

- financial liabilities from trading - -

- financial liabilities designated at fair value - -

- other liabilities 171,072 (5,653)

Net liquidity generated/absorbed by operating activities 7 (42)

B. INVESTING ACTIVITIES

1 Liquidity generated by - -

- equity investment disposals - -

- dividends received on equity investments - -

- disposal/reimbursement of financial assets held to maturity - -

- tangible asset disposals - -

- intangible asset disposals - -

- business unit disposals - -

2 Liquidity absorbed by - -

- equity investment acquisitions - -

- acquisition of financial assets held to maturity - -

- tangible asset acquisitions - -

- intangible asset acquisitions - -

- business unit acquisitions - -

Net liquidity generated/absorbed by investing activities - -

C. FUNDING ACTIVITIES

- own shares issues/acquisitions - -

- capital instrument issues/acquisitions - -

- dividend distribution and others - -

Net liquidity generated/absorbed by funding activities - -

NET LIQUIDITY GENERATED/ABSORBED DURING THE YEAR 7 (42)

2011 2010

Cash and cash equivalents at the beginning of the year 11,427 11,469

Total net liquidity generated/absorbed during the year 7 (42)

Cash and cash equivalents at year end 11,434 11,427

RECONCILIATION

Amount

A. OPERATING ACTIVITIESAmount

14 Financial Statements as at 31 December 2011

NOTES TO THE ACCOUNTS

1 Part A - Accounting Policies

A.1 GENERAL PART Section 1 - Statement of compliance with international accounting standards These financial statements are prepared in accordance with the international accounting standards issued by the International Accounting Standards Board (IASB) and the related interpretations of the International Financial Reporting Interpretations Committee (IFRIC), endorsed by the European Commission, as established by EU Regulation no. 1606 of 19 July 2002. In preparing the financial statements, the IAS/IFRS in force at 31 December 2011 as approved by the European Commission were applied. Section 2 General Drafting Principles The financial statements are in accordance with the IAS/IFRS and the provisions contained in the Bank of Italy Regulation of 13 March 2012 concerning " Instructions for the preparation of the annual financial statements by financial Intermediaries pursuant to art. 107 of the CBA, electronic money institutions (EMI), asset management companies (AMC) and Brokerage Firms (Italian SIM)". In particular, the financial statements are prepared in accordance with the general principles laid down in IAS 1, on a going concern basis (IAS 1 par. 25 and par. 26), in accordance with the accrual basis of accounting (IAS 1 par. 27 and par. 28) and in compliance with the consistency of presentation and classification of financial statement items (IAS 1 par. 29.) Assets and liabilities, income and expenses were not offset unless required or permitted by a standard or an interpretation (IAS 1 par. 32). There were no exceptions to the application of IAS/IFRS. The corporate financial statements comprise the balance sheet, income statement, statement of comprehensive income, statement of changes in equity, cash flow statement and the notes. The financial statements are accompanied by the Sole Director's report on operations and the Company's situation. The financial statements are clear and provide a true and correct representation of the equity, financial position and results of operations for the period. If the information required by the international accounting standards and the provisions contained in "Instructions for the preparation of financial statements of financial intermediaries (...)" issued by the Bank of Italy on 13 March 2012 were not sufficient to provide a true and correct, relevant, reliable, comparable and understandable presentation, the additional information necessary for such purpose is included in the notes The balance sheet and income statement schedules are made up of items, identified by numbers, sub-items, identified by letters, and additional information details, the "of which" of items and sub-items. The items, sub-items and information details make up the accounts of the financial statements. Data for 2011 are presented in comparison with the previous year 2010. In accordance with art. 5 of Legislative Decree no. No. 38/2005, the financial statements are prepared using the euro as reporting currency.

15 Financial Statements as at 31 December 2011

The amounts in the financial statements, the data reported in the notes, as well as those indicated in the Report are expressed in euros, unless otherwise indicated. Securitisation transactions The accounting recognition of purchased receivables, securities issued and other transactions carried out as part of securitisation transaction(s) is described in a special section of the Notes and does not form part of the financial statements, pursuant to administrative regulations issued by the Bank of Italy in accordance with art. 9 of Legislative Decree 38/2005, or the Bank of Italy's instructions of 14 February 2006, and most recently the Bank of Italy's instructions of 13 March 2012. This approach is also consistent with the provisions of Law no.130 of 30 April 1999, according to which "receivables relating to each transaction constitute separate assets in all respects from those of the Company and those associated with other transactions." Consequently, the amounts relating to the securitisation transaction, were not affected by the application of IAS/IFRS. For completeness it should be noted that, according to international accounting standards, the subject of accounting treatment of financial assets and/or groups of financial assets and financial liabilities arising from securitisation transactions is still under analysis by the bodies responsible for the interpretation of accounting standards. The accounting information and the qualitative and quantitative data relating to the securitisation transaction are highlighted in Part D, "Additional Information" of these Notes. Section 3 Events after the reporting period There were no events occurring after the reporting period that should be mentioned pursuant to IAS 10. Pursuant to IAS 10 it is hereby specified that these financial statements were authorized for issue on 26 April 2012. Section 4 Other issues None

16 Financial Statements as at 31 December 2011

A.2 SECTION ON MAIN ITEMS OF THE FINANCIAL STATEMENTS The accounting standards adopted for preparing these financial statements are described below, with reference to the main items of assets and liabilities. 1) Receivables a) recognition criteria Receivables are recorded in the Balance Sheet when the Company becomes party to the contractual provisions of the instrument, thus becoming the owner of rights, obligations and risks. This item includes amounts due from banks. b) classification and measurement criteria Receivables are initially recognised at their nominal value, as representing their fair value. Receivables are subsequently measured at amortised cost. The amortised cost method is not used for short-term receivables, as the effect of discounting to present value is deemed to be immaterial. Therefore, these receivables continue to be measured at their initial carrying value. c) derecognition criteria Receivables are derecognised when they are sold, substantially transferring all the risks and benefits attached to them. In case this is not ascertainable, the receivables are derecognised when no control whatsoever is maintained over them. Furthermore, the receivables sold are derecognised if the Bank retains the contractual right to the related cash flows but at the same time it assumes a contractual obligation to pay precisely those cash flows to third parties. 2) Current and deferred taxes a) recognition criteria The effects of current and deferred taxes calculated in accordance with national legislation are recognised on the basis of accrual accounting, consistent with the recognition in the financial statements of the costs and revenues from which they arose, by applying the tax rates in force. Current taxes, payable or receivable, include the net balance, for each individual tax, between current liabilities and the related tax receivables. Deferred tax assets and liabilities are determined based on temporary differences - without time limits - between the value attributed to an asset or a liability in accordance with the Italian Civil Code and the corresponding values for tax purposes. These deferred tax assets and liabilities, and deferred tax assets resulting from tax losses, are recognised to the extent that it is reasonably likely they will be absorbed in subsequent years. b) classification and measurement criteria Deferred tax assets and liabilities are systematically assessed to take into account any changes in applicable laws or rates. Any provisions set against tax risks is also subject to adjustments to meet the costs arising from already notified tax assessment or ongoing litigation with tax authorities.

17 Financial Statements as at 31 December 2011

c) recognition criteria of Income Statement items If the deferred tax assets and liabilities relate to items affecting the income statement, the contra item is income taxes. When deferred tax assets and liabilities regard transactions recognised directly in equity, with no impact on the income statement (such as the measurement of available-for-sale financial assets), they are recognised in equity, in separate reserves where applicable. 3) Other liabilities a) recognition criteria Liabilities are recognized for accounting purposes at the time the contractual obligation is incurred by the Company. This item includes trade payables. b) classification and measurement criteria They are initially recognised at nominal value, and continue to be reported at the initial cost as this is an approximation of fair value. c) derecognition criteria Payables are derecognised when they are extinguished or expired. 4) Interest income and expense and similar Interest income and expense are recognized on a time basis that takes into account the effective return. Interest on short-term receivables/payables for which the amortised cost is not applied is recognized according to the pro-rata temporis accrual of the nominal interest rate contractually established.

18 Financial Statements as at 31 December 2011

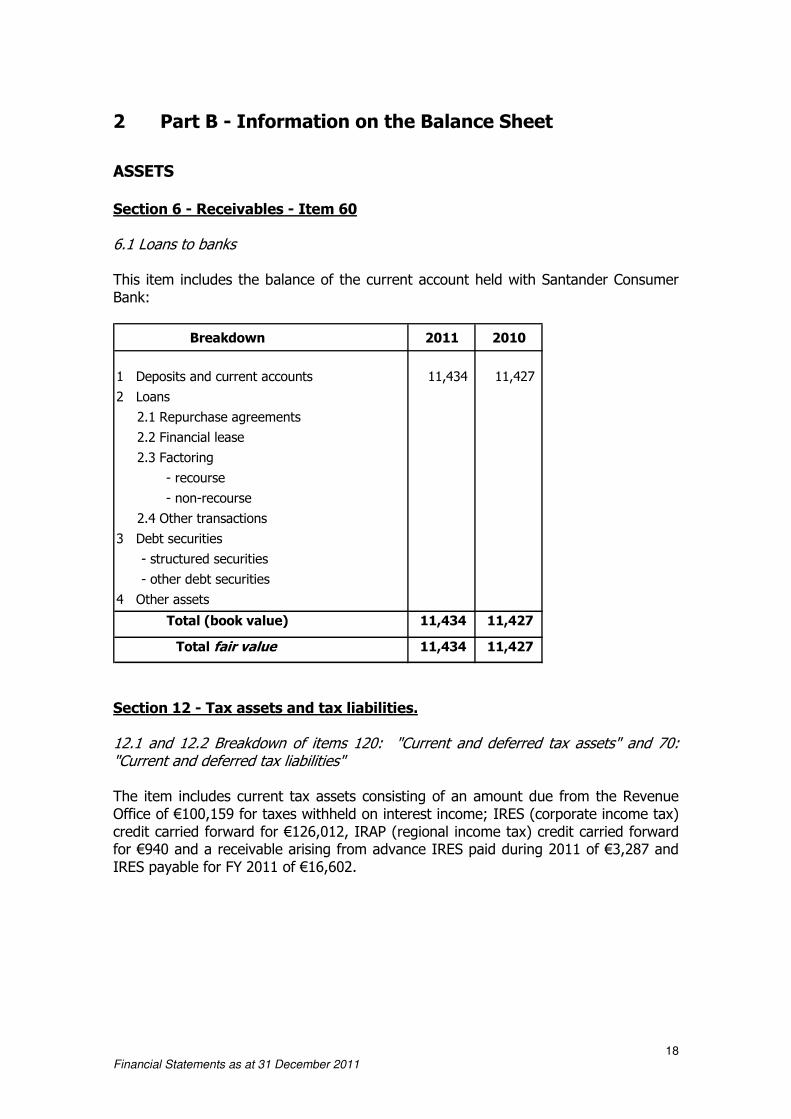

2 Part B - Information on the Balance Sheet

ASSETS Section 6 - Receivables - Item 60 6.1 Loans to banks

This item includes the balance of the current account held with Santander Consumer Bank:

Breakdown 2011 2010

1 Deposits and current accounts 11,434 11,427

2 Loans

2.1 Repurchase agreements

2.2 Financial lease

2.3 Factoring

- recourse

- non-recourse

2.4 Other transactions

3 Debt securities

- structured securities

- other debt securities

4 Other assets

Total (book value) 11,434 11,427

Total fair value 11,434 11,427

Section 12 - Tax assets and tax liabilities. 12.1 and 12.2 Breakdown of items 120: "Current and deferred tax assets" and 70: "Current and deferred tax liabilities" The item includes current tax assets consisting of an amount due from the Revenue Office of €100,159 for taxes withheld on interest income; IRES (corporate income tax) credit carried forward for €126,012, IRAP (regional income tax) credit carried forward for €940 and a receivable arising from advance IRES paid during 2011 of €3,287 and IRES payable for FY 2011 of €16,602.

19 Financial Statements as at 31 December 2011

The tax liabilities, amounting to €3,187, consist of taxes withheld by the Company on third parties and payable by it, for €2,481 and the Value Added Tax for the last quarter which was paid during 2011 and amounting to €706. Deferred taxes are zero, as in the previous year. Therefore there were no changes in the item. 12.3 Changes in deferred tax assets (offsetting entry in income statement)

1 Opening balance 7,061 7,087

2 Increases

2.1 Advanced taxes recorded during the year

a) relating to previous years

b) due to changes in accounting standards

c) write-backs

d) other 7,061

2.2 New taxes or increases in tax rates

2.3 Other increases

3 Decreases

3.1 Advanced taxes cancelled during the year

a) re-endorsements (7,061) (7,087)

b) write-downs due to non-recoverability

b) due to changes in accounting standards

d) other

3.2 Reductions in tax rates

3.3 Other decreases

4 Closing balance - 7,061

2011 2010

Section 14 - Other assets - Item 140

Breakdown of item 140 "Other assets"

The item Other assets includes the receivable from the Segregated assets relating to the charge back of the relevant costs, amounting to €279,281 and €19,079 for prepaid expenses.

20 Financial Statements as at 31 December 2011

LIABILITIES Section 7 – Tax liabilities – Item 70

Please refer to the comments in section 12 of the Assets.

Section 9 - Other liabilities - Item 90

Breakdown of item 90 "Other liabilities" The item Other liabilities includes the following amounts:

Description 2011 2010

Remuneration payable to Directors - 26,702

Amounts owed to suppliers 24,925 19,645

Payables to separate assets 334,092 246,775

Due to Santander Consumer Bank SpA 150,240 44,521

Total 509,257 337,643

Payables to Santander Consumer Bank for €150,240 euro refer to amounts advanced on behalf of the Company.

Section 12 - Shareholders' equity - Item 120, Item 160 . 12.1 Breakdown of Item 120 "Capital"

Classes Amount

1 Capital

1.1 Ordinary shares 10,000

1.2 Other shares

Total 10,000

The capital, subscribed and fully paid up, consists of 2 "quotas", amounting respectively to €7,000 and €3,000. These amounts are unchanged from the previous year.

21 Financial Statements as at 31 December 2011

12.5 Other information

The breakdown and changes of the item "reserves" are as follows:

Legal

Retained

earnings

(accumulated

losses)

Others Total

A. Opening balance1,744 (105) 1,639

B. Increases

B.1 Profit allocation

B.2 Other changes

C. Decreases

C.1 Use

- coverage of losses

- allocation

- transfer to capital

C.2 Other changes

D. Final Balance1,744 (105) - 1,639

In accordance with Article 2427, paragraph 1, no. 7-bis of the Italian Civil Code, the reserves are detailed in the schedule below, separately depending on their availability and possibility of distribution.

Summary of the use made

in the two previous years

Amount Possibility of use

Distributable share

To cover losses

Other reasons

Capital 10,000

Retained earnings

-Legal reserve

1,744 B -Losses carried

forward (105)

TOTAL RESERVES 1,639

Non-distributable

share

1,639

22 Financial Statements as at 31 December 2011

3 Part C - Information on Income Statement Section 1 - Interest - Item 10, Item 20 .

1.1 Breakdown of item 10 "Interest and similar income"

Debt

securitiesLoans

Other

transactio

ns

2011 2010

1 Financial assets held for trading

2Financial assets designated at fair

value

3 Available for sale financial assets

4 Financial assets held to maturity

5 Accounts receivables

5.1 Loans to banks 125 125 59

5.2 Due from financial institutions

5.3 Loans to customers

6 Other assets

7 Hedging derivatives

Total - - 125 125 59

Items/Categories

1.2 Interest income and similar revenues: other information This item refers to interest earned on bank current account.

1.3 Breakdown of item 20 "Interest expense and similar charges"

Loans SecuritiesOther

transactions2011 2010

1 Amounts owed to banks

2 Due to financial institutions

3 Amounts owed to customers

4 Securities in issue

5 Financial liabilities from trading

6Financial liabilities designated at

fair value7 Other liabilities 206 206 60

8 Hedging derivatives

Total - - 206 206 60 This item refers to interest expense on taxes paid and bank charges on current accounts.

23 Financial Statements as at 31 December 2011

Section 9 - Administrative expenses - Item 110 9.1 Breakdown of item 110.a "Personnel expenses"

Total 2011 Total 2010

1

a) wages and salaries

b) social security charges

c) staff termination indemnity

d) social security costs

e) provision for staff termination indemnity

f) provisions for pensions and similar obligations

- defined contribution

- defined benefits

g) payments to external complementary pension plan

- defined contribution

- defined benefits

h) other expenses

2

3 42,610 40,019

4 Retired staff

5

6

Total 42,610 40,019

Recovery of expenses for employees seconded to other

companies

Recovery of expenses for employees seconded to the

company

Items/Categories

Employees

Other working staff

Directors and Auditors

The Company has no employees or other staff. The item Directors includes the fixed remuneration of €40,971 and social security contributions of €1,639. 9.2 Average number of employees by category The Company had no employees during 2011. Section 9.3 - Breakdown of item 110.b "Other administrative expenses"

Description 2011 2010

1 Tax consulting and administration 114,807 32,044

2 Costs for vehicle management 362,328 102,094

3 Cost of audit firms 38,000 37,513

4 Other expenses and taxes 694 4,138

Total 515,829 175,788 The item fees for vehicle management includes the fees for the placement of securities at the Luxembourg Stock Exchange, the supervision costs requested by Consob and the cost of corporate services.

24 Financial Statements as at 31 December 2011

Section 14 - Other operating income and charges - Item 160 14.1 Breakdown of item 160 "Other operating income and charges" The item includes revenues obtained from charging the costs incurred by the vehicle company back to the segregated assets for €615,721 and other operating charges of €33,756. Section 17 - Income taxes on continuing operations - Item 190 17.1 – Breakdown of Item 190 – Income taxes for the year on continuing operations" The tax charge recognised in the income statement is presented in the table below according to expected cash disbursement, determined on the basis of the provisions governing the calculation of the tax base in relation to direct taxes.

Total 2011 Total 2010

1 Current taxes (16,602) (3,303)

2 Change in current taxes for previous years - 1,947

3 Reduction of current taxes

4 Change in advanced taxes (7,061) (26)

5 Change in deferred taxes

Total (23,663) (1,382)

25 Financial Statements as at 31 December 2011

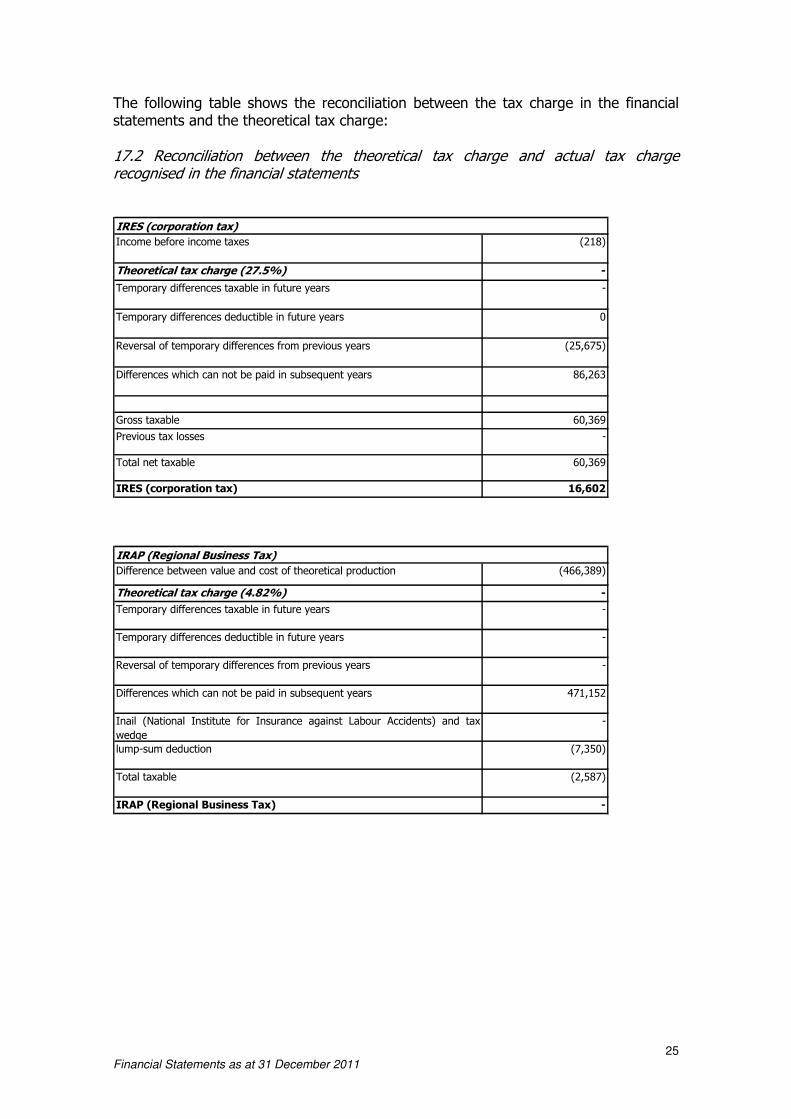

The following table shows the reconciliation between the tax charge in the financial statements and the theoretical tax charge: 17.2 Reconciliation between the theoretical tax charge and actual tax charge recognised in the financial statements

Income before income taxes (218)

Theoretical tax charge (27.5%) -

Temporary differences taxable in future years -

Temporary differences deductible in future years 0

Reversal of temporary differences from previous years (25,675)

Differences which can not be paid in subsequent years 86,263

Gross taxable 60,369

Previous tax losses -

Total net taxable 60,369

IRES (corporation tax) 16,602

Difference between value and cost of theoretical production (466,389)

Theoretical tax charge (4.82%) -

Temporary differences taxable in future years -

Temporary differences deductible in future years -

Reversal of temporary differences from previous years -

Differences which can not be paid in subsequent years 471,152

Inail (National Institute for Insurance against Labour Accidents) and tax

wedge

-

lump-sum deduction (7,350)

Total taxable (2,587)

IRAP (Regional Business Tax) -

IRES (corporation tax)

IRAP (Regional Business Tax)

26 Financial Statements as at 31 December 2011

4 Part D - Other Information Section 1 - Specific references to activities

F. SECURITISATION OF RECEIVABLES At 31 December 2011, the Company had two Programmes and three stand-alone Transactions outstanding for the securitisation of performing consumer loans: • The first started in 2003 and is called "2,500,000,000 Euro Medium Term Asset-

Backed Notes Programme";

• The second is named "2,500,000,000 Euro Medium Term Asset-Backed Notes Programme IV," whose notes were issued in December 2009;

• The first stand-alone Transaction is named "411,000,000 Class A - 2011 and 129,000,000 Class B - 2011 Asset-Backed Floating Rate Notes", whose notes were issued in March 2011.

• The second stand-alone Transaction is called "532,000,000 Class A - 2011 – 2 and 95,000,000 Class B - 2011 – 2 Asset-Backed Floating Rate Notes", whose notes were issued in October 2011.

• The third stand-alone Transaction is named "Up to €750,000,000 Class A Asset-Backed Floating Rate Variable Funding Notes and Up to €306,338,100 Class B Asset-Backed Variable Funding Notes” whose notes were issued in November 2011.

As stated above, on 15 July 2011 the portfolio of programmes launched in March and December 2008, were repurchased by the Originator and the entire amount of the notes was redeemed in advance. Within each outstanding Transaction, the Company acquired an initial portfolio of performing consumer loans and at the same time it entered into a framework agreement that gives it the right to acquire additional portfolios with the same characteristics. The first two programmes are carried out pursuant to Law 130/99 with the company Santander Consumer Bank S.p.A., as originator, in the form of issue programmes, according to a scheme that is similar to the so called "Master Trust" transactions, as they are performed in Italy. The loans acquired by the vehicle, within each Transaction, make up a single asset, with no segregation between the loans purchased from time to time. As a result, the securities of each series, consisting of different classes, which have different degrees of subordination with respect to one another, are backed by the entire loan portfolio purchased over the life of the programme.

Under the Programme launched in 2003 the Company carried out four sets of issues for a total of €2,100,000,000, substantially using up the capacity originally agreed:

• Golden Bar Programme Series 1 – 2004, 17 March 2004; • Golden Bar Programme Series 2 – 2004, 09 December 2004;

• Golden Bar Programme Series 3 – 2006, 08 February 2006; • Golden Bar Programme Series 4 – 2007, 31 January 2007;

27 Financial Statements as at 31 December 2011

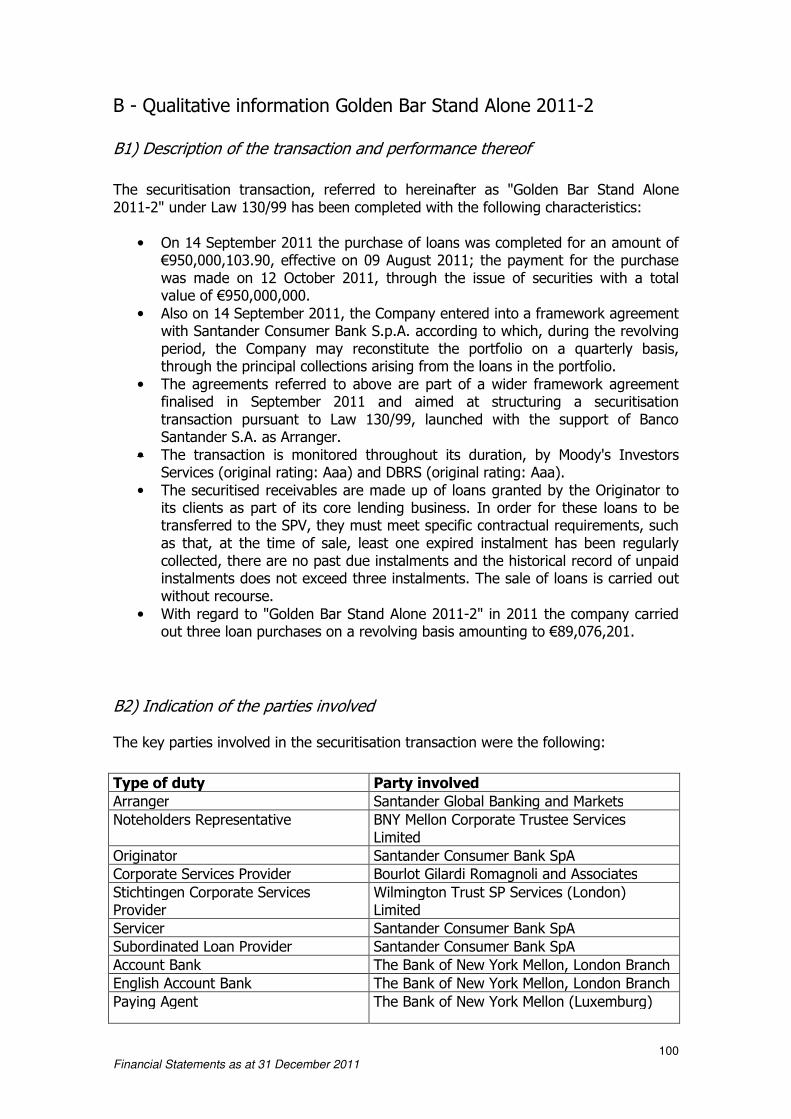

During the year no revolving without recourse purchases were made aimed at reconstituting the portfolio through the revolving purchase of additional loans funded by the principal collections available. In 2011, the Company continued the redemption of Class A Series 2, Series 3 and Series 4, already initiated, respectively, in 2007, 2008, 2009 and 2010. In 2011, repayments were made amounting to €8,390,000 for the Series 1, €60,296,949 for the Series 2, €138,980,209 for the Series 3 and €349,392,096 for the Series 4. Under the second Programme, started in 2007, the Company issued the first series of notes on 11 March 2008 for a total of €700,000,000, divided into four classes with decreasing degree of subordination. During the year the Company has reconstituted the portfolio through revolving purchases for an amount of €60,079,302. On 15 July 2011 this Programme was terminated in advance and the related securities were fully redeemed, for a total amount of €700,000,000. Under the third Programme, which commenced by purchasing an initial portfolio of performing loans for €750,002,164, on 23 December 2008 the Company issued the first series of notes totalling €750,000,000, divided into four classes with decreasing degree of subordination. During the year the Company has reconstituted the initial portfolio through revolving purchases for an amount of €135,204,669. On 15 July 2011 this Programme was terminated in advance and the related securities were fully redeemed, for a total amount of €750,000,000. Under the fourth Programme, which commenced by purchasing an initial portfolio of performing loans for €800,001,181, on 23 December 2009 the Company issued the first series of notes totalling €800,000,000, divided into three classes with decreasing degree of subordination and entirely subscribed by the Originator. During the year the Company has reconstituted the initial portfolio through revolving purchases for an amount of €283,947,440. The three stand-alone Transactions, are made pursuant to Law 130/99 through an initial purchase financed by means of a single securities issue. The first stand-alone Transaction, started in the previous year with the purchase of a portfolio of performing loans for a total of €600,001,249, was finalised in March 2011 through the issue of one series of notes totalling €600,000,000, divided into three classes with decreasing degree of subordination. The class A security was subscribed for an amount of €150,000,000 by an institutional investor and an amount of €261,000,000 by Santander Consumer Bank SpA, while the remaining classes of securities were fully subscribed by the Originator. During the year the Company has reconstituted the initial portfolio through revolving purchases for an amount of €199,703,967. Under the second stand-alone Transaction, which started in August 2011 through the purchase of an initial portfolio of performing loans for €950,000,104, on 12 October 2011 the Company issued the first and only series of notes totalling €950,000,000, divided into three classes with decreasing degree of subordination and entirely subscribed by the Originator.

28 Financial Statements as at 31 December 2011

During the year the Company has reconstituted the initial portfolio through revolving purchases for an amount of €89,076,201. Under the last stand-alone Transaction, which was started in October 2011 through the purchase of an initial portfolio of performing loans for €710,058,081, on 21 November 2011 the Company issued the first and only series of notes totalling €710,058,081, divided into two classes with decreasing degree of subordination, both without rating. The A Class was fully privately subscribed by Bank of America National Association - London Branch, and the Junior security by Santander Consumer Bank S.p.A. The portfolio that was initially purchased will be reconstituted quarterly with portfolios having the same characteristics throughout the revolving period. During the year, the transactions were monitored by Moody's Investors Services and Standard & Poor's, with reference to the first Programme, by Standard & Poor's with reference to the fourth Programme, by Moody's Investors Services and Fitch Ratings Ltd with reference to the first stand-alone Transaction, by Moody's Investors Services and DBRS INc. with reference to the second stand-alone Transaction. As part of the Programmes, the rating companies are responsible for verifying that subsequent issues do not lead to a deterioration of the rating assigned to the previous ones. Santander Consumer Bank, as servicer, sends a "servicing report", on a quarterly basis, to the Calculation Agent, represented by Deutsche Bank S.p.A., for the two securitisation Programmes and for the first Stand Alone Transaction, and by Bank of New York Mellon for the second and third Stand Alone Transactions. By supplementing the information on the portfolio with financial data, the Calculation Agent produces an "Investor Report" for each transaction, which is distributed to the rating agencies, investors and the international financial community; the reports provide analytical information on collection performance and the major events that may concern the securitised loans (early redemptions, late payments, defaults, etc..). As servicer, Santander Consumer Bank S.p.A. is responsible, among other things, for managing collections from customers, immediately crediting the funds collected to the SPV and, finally, activation of debt recovery procedures, where necessary. The qualitative and quantitative information on individual securitisation transactions are listed in the Annex to these notes.

29 Financial Statements as at 31 December 2011

Section 3 – Information on Risks and Hedging Policies 3.1 CREDIT RISK QUALITATIVE INFORMATION 1 GENERAL INFORMATION a) ORDINARY OPERATIONS -

The Company is not subject to credit risk as it has only current account deposits.

b) SEGREGATED ASSET - The securitisation transaction is subject to the risks arising from: - mismatch in cash flows - failure to collect amounts owed by the assigned debtors; - failure of Servicer to perform the tasks and commitments taken, consisting in collecting sufficient funds to meet the payment obligations arising from time to time from the securitisation. These risks are mitigated by the following techniques: (i) asset-backed securities issued totalling less than the gross book value of the

loans under the securitisation programme as a result of being granted a subordinated loan;

(ii) issue of a subordinated class of securities, subscribed by the originator, with repayment priority lower than the classes of senior securities.

3.2 MARKET RISKS 3.2.1 INTEREST RATE RISK QUALITATIVE INFORMATION 1 GENERAL ASPECTS a) ORDINARY OPERATIONS -

The Company is not subject to interest rate risk as it has only current account deposits.

b) SEGREGATED ASSET - Market risk is primarily represented by the potential loss arising from changes in interest rates. The securities issued in fact follow the trend of the Euribor variable market rate, while securitised assets have a fixed rate. As a result of this mismatch between interest rates on assets and liabilities, should the Euribor exceed a certain level, the Company may not have sufficient funds to pay all its obligations arising from the securitisation. Therefore, in order to protect the Company against fluctuations in interest rates payable on securities issued, at the same time as the issue of the notes, and for each series of securities, the Company entered into an Interest Rate Swap agreement to hedge this risk. More specifically, in the first Programme four agreements were signed, on 11 March 2004, 6 December 2004, 3 February 2006 and 26 January 2007, of which the first two with Deutsche Bank, the third and fourth with Banco Santander.

30 Financial Statements as at 31 December 2011

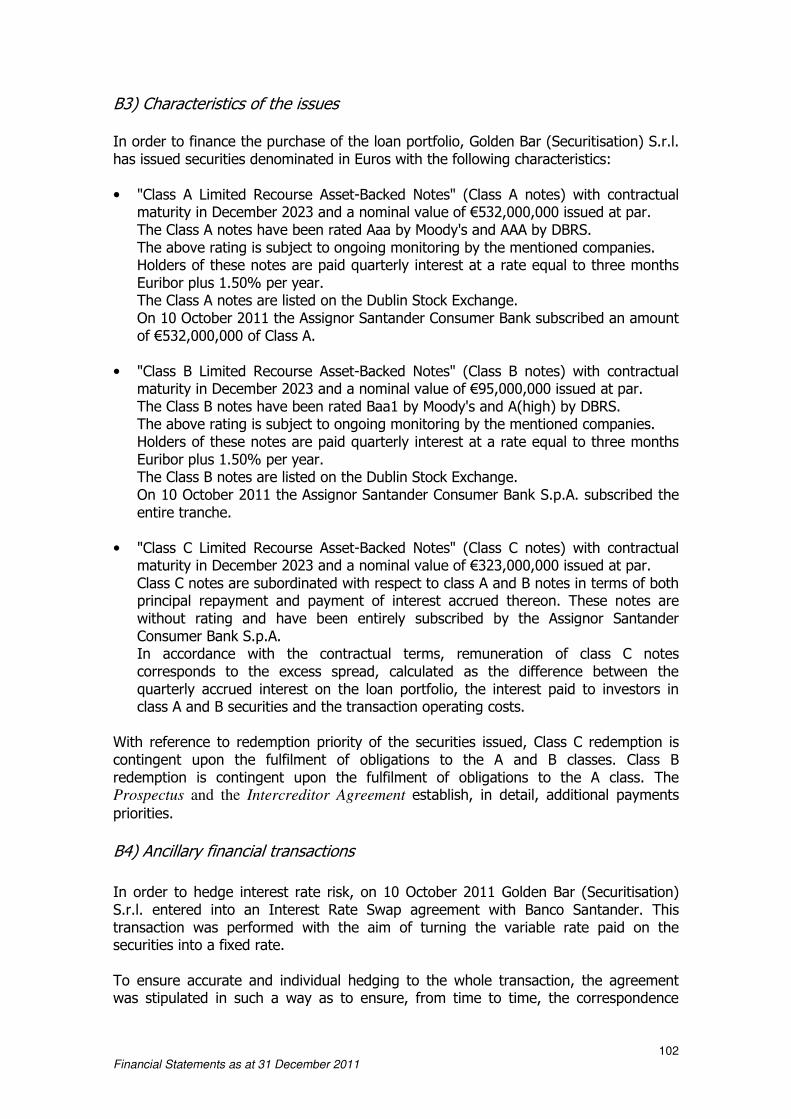

Within the fourth Programme the Company entered into a Hedging Agreement with the counterparty Banco Santander on 23 December 2009. For the stand alone Transaction "Golden Bar Stand Alone 2011-1" on 31 March 2011 the Company entered into a hedge agreement with the counterparty Banco Santander. For the stand alone Transaction "Golden Bar Stand Alone 2011-2" on 10 October 2011 the Company entered into a hedge agreement with the counterparty Banco Santander. For the stand alone Transaction "Golden Bar Securitisation 10" on 17 November 2011 the Company entered into a hedge agreement with the counterparty Banco Santander. To ensure accurate and individual hedging, the agreements were stipulated in such a way as to ensure, from time to time, the correspondence between the amount of receivables included in the portfolio and the notional amount to which

the hedge relates. 3.2.2 PRICE RISK QUALITATIVE INFORMATION 1 GENERAL ASPECTS a) ORDINARY OPERATIONS - The Company is not subject to price risk as it does not trade goods and services on the market.

b) SEGREGATED ASSET -

The segregated assets are not subject to price risk since the receivables owned by the Company are not traded but held until they are fully collected.

3.2.3 EXCHANGE RATE RISK QUALITATIVE INFORMATION 1 GENERAL ASPECTS a) ORDINARY OPERATIONS -

The Company is not subject to exchange rate risk as it only operates in the domestic market and is therefore not exposed to exchange rate risk.

b) SEGREGATED ASSET - The segregated assets are not subject to exchange rate risk as the related receivables are only at a domestic level.

31 Financial Statements as at 31 December 2011

3.3 OPERATIONAL RISK

QUALITATIVE INFORMATION 1. GENERAL ASPECTS, MANAGEMENT AND MEASUREMENT OF OPERATIONAL RISK It is the risk to incur losses caused by inefficiencies in business processes, technological systems failures, external events that cause or may cause tangible and measurable losses for the Company. According to the Basel Committee unexpected losses can be attributed to the occurrence of four factors: human error, system failures, inadequate procedures and controls, external events. Operational risk is a pure risk as it is associated to events having only adverse effects. The ability of the Company to meet its obligations arising from the securitisation totally depend on third parties that have been delegated all the characteristic functions of an organizational structure as well as the internal control systems; indeed, the Company, by its nature, has no employees. More specifically, the success of the securitisation transaction depends on the ability of the Servicer to manage the loan portfolio according to the Servicing Agreement's provisions. Therefore, in order to mitigate the risk arising from Servicing activities and to ensure that the receivables are managed in a consistent and uniform manner, the Servicer: - acknowledged that its obligations under the Servicing agreement are the same

obligations it has to meet in the normal course of its business; - has undertaken to manage the servicing activities with the best professional

diligence, it being understood that, if in carrying out its tasks, it identifies a conflict between its interests as a provider of services in relation to the assigned debtors and the interests of the Company, the Servicer shall report this circumstance to the Company and the Representative of the Noteholders and, in any case, it shall act only in accordance with the directives issued by them;

- undertook to perform the Servicing activities through its operating structure, ensuring that it is equipped with all the infrastructure, the technical, organizational and IT resources necessary for efficiently performing the aforementioned activities.

3.4 LIQUIDITY RISK

QUALITATIVE INFORMATION 1 GENERAL ASPECTS, MANAGEMENT AND MEASUREMENT OF LIQUIDITY RISK a) Ordinary operations - The Company is not subject to liquidity risk as it has "Loans to Banks" of €11,000 consisting of sight current account deposits. b) Segregated asset - For the Company, liquidity risk is mainly represented by the mismatch in cash flows from the securitised loan portfolio and its payment obligations emerging from the securitisation Transaction. This risk is mitigated both by the techniques discussed in the context of credit risk and by Interest Rate Swaps, which are entered into when there appears to be an interest rate risk that needs to hedged.

32 Financial Statements as at 31 December 2011

With regard to quantitative information, please refer to paragraph "F Securitisation of receivables" in section 1 above as well as the Annex.

33 Financial Statements as at 31 December 2011

Part E - Information on shareholders' equity 4.1.2.1 Shareholders' equity: breakdown

Amount 2011 Amount 2010

1 Capital 10,000 10,000

2 Additional paid-in capital - -

3 Reserves

- profits:

a) legal 1,639 1,744

b) statutory - -

c) own shares - -

d) other - -

- other - -

4 (others) - -

5 Valuation reserves

- Available-for-sale financial assets - -

- Intangible assets - -

- Tangible assets - -

- foreign investment hedge - -

- Cash flow hedge - -

- Currency differences - -

- Non-current assets and groups of assets held

for sale

- -

- Special revaluation laws - -

- Actuarial gains (losses) on defined benefit

plans

- -

- Share of the valuation reserves of equity

investments valued at equity

- -

6 Capital instruments - -

7 Profit (loss) for the year (218) (105)

Total 11,421 11,639

Items/Categories

34 Financial Statements as at 31 December 2011

Section 5 - Detailed statement of comprehensive income

Gross

amountIncome tax

Net

amount10 (218)

20 Available for sale financial assets

a) changes in fair value

b) reversal to income statement

- adjustments for impairment

- gains/losses on sales

c) other changes

30 Tangible assets

40 Intangible assets

50 Foreign investment hedge:

a) changes in fair value

b) reversal to income statement

c) other changes

60 Cash flow hedge:

a) changes in fair value

b) reversal to income statement

c) other changes

70 Currency differences:

a) changes in fair value

b) reversal to income statement

c) other changes

80 Non-current assets held for sale:

a) changes in fair value

b) reversal to income statement

c) other changes

90 Actuarial profits (losses) on defined benefit

plans100 Share of the valuation reserves of equity

investments valued at equity: a) changes in fair value

b) reversal to income statement

- adjustments for impairment

- gains/losses on sales

c) other changes110 - - -

120 (218)

Profit (loss) for the year

Other income items

Total other income components after taxes

Comprehensive income (Item 10.+110)

Section 6 – Transactions with Related Parties 6.1 Disclosure on the remuneration of directors and executives As established by resolution passed on 22 April 2008, the Company paid €40,971 as remuneration to the Sole Director and € 1,639 as social security contributions.

35 Financial Statements as at 31 December 2011

6.2 Loans and guarantees issued in favour of directors and statutory auditors No loans were granted nor guarantees provided in favour of the Sole director. In accordance with the Memorandum of Association and the provisions of art. 2477 of the Italian Civil Code, the Company has not appointed a Board of Statutory Auditors. 6.3 Disclosure on transactions with related parties There were no transactions with related parties, except those with Santander Consumer Bank, Originator of the transactions, which have already been widely described in the Notes.

36 Financial Statements as at 31 December 2011

Appendix to the Explanatory Notes to "Golden Bar Securitisation Programme"

A - Situation of the transaction at 31 December 2011 SUMMARY STATEMENT OF SECURITISED ASSETS AND SECURITIES

ISSUED

Situation at Situation at

31/12/2011 31/12/2010

A. Securitised assets

A1) loans 142,827,541 629,095,327

B. Loan of available assets arising from credit

management

B1) Securities 72,723,832 184,560,928

B3) Other 4,120,167 10,885,510

C. Securities issued

C1) "Class A" securities 97,115,955 626,955,209

C2) "Class B" securities 57,170,000 80,390,000

C3) "Class C" securities 28,500,000 31,500,000

C4) "Class D" securities 9,500,000 10,500,000

E. Other liabilities 22,089,543 65,203,472

F. Interest expense on securities issued

Interest on class "A", "B", "C" and "D" securities 16,056,682 34,313,529

G. Commissions and fees related to the

transaction

G1) For servicing 2,241,062 5,544,580

G2) For other services 120,191 245,775

H. Other charges 10,998,495 34,130,789

I. Interest generated by the securitised assets 23,860,890 66,636,640

L. Other revenues 5,555,540 7,598,033

37 Financial Statements as at 31 December 2011

Drafting criteria of the summary statement of securitised assets and securities issued

Securitised assets The securitised assets, consisting of receivables from consumer credit transactions, are recognised at nominal value corresponding to the estimated realizable value. Receivables are stated in the summary statements net of deferred income relating to the portion of interest income and collection commissions not yet accrued. Default interest receivables are recorded in the summary statement net of write-downs relating to default interest.

Securities issued, loans received and other liabilities They are stated at nominal value.

Interest, charges and other revenues These items are included on an accrual basis.

Derivative contracts The spreads on Interest Rate Swap agreements entered into in order to hedge the risk of interest rates fluctuations, are shown as costs or revenues on an accrual basis.

38 Financial Statements as at 31 December 2011

Further information on the summary statement (Golden Bar Securitisation Programme) SECURITISED ASSETS

Represented by:

Value of loans at maturity 148,066,017

Deferred liability for interest to accrue (3,316,701)

Deferred liability for collection commissions to accrue (1,225,778)

Risk reserve for interest on delayed payment (695,997)

142,827,541

LOAN OF AVAILABLE ASSETS ARISING FROM CREDIT

MANAGEMENT

Represented by:

Securities 72,723,832

Commercial paper 72,723,832

Liquidity 4,120,167

Bank accounts 4,120,167

76,843,999

OTHER LIABILITIES

Represented by:

Due to Santander Consumer Bank SpA -Junior note 22,328,574

Due to Santander Consumer Bank SpA -refund of collections (246,403)

Payables for portfolio management 7,372

22,089,543

INTEREST EXPENSE ON SECURITIES ISSUED

Refer to:

Interests on class "A" securities 4,568,395

Interests on class "B" securities 1,184,274

Interests on class "C" securities 587,203

Interests on class "D" securities 9,716,810

16,056,682

OTHER CHARGES

Consist of:

Loan loss 4,908,627

Reversal of loss on disposal (141,717)

Portfolio management charges 116,616

Allowances payables 2,470

Late payment penalties 11,833

IRS negative differentials 6,100,666

10,998,495

39 Financial Statements as at 31 December 2011

INTEREST GENERATED BY SECURITISED ASSETS

Consist of:

Interest income from securitised assets 25,020,329

Reversal of interest income on early redemptions (1,713,454)

Early redemption fees 209,508

Interest on delayed payments received 182,576

Contingent assets on delayed payment 161,931

23,860,890

OTHER REVENUES

Consist of:

Profits from commercial paper 1,547,312

Collection fees 4,338,712

Reversal of collection fees (275,572)

Interest income on bank accounts 123,651

Adjustment to provision for default interest (178,719)

Allowances receivable 156

5,555,540

The item "penalties for late payment" refers to the write-off of penalties accrued in prior years and not collected.

40 Financial Statements as at 31 December 2011

B - Qualitative information Golden Bar Securitisation Programme B1) Description of the transaction and performance thereof

The securitisation transaction completed pursuant to Law 130/99 had the following essential characteristics:

• On 22 December 2003 the initial purchase of loans was completed for an amount of €200,002,344, effective on 18 December 2003; subsequently, in March 2004, the Company financed this purchase by issuing securities with a total value of €200,000,000 (Golden Bar Securitisation Programme - Series 1/2004).

• Also on 22 December 2003, the Company entered into a framework agreement with Santander Consumer Bank S.p.A., with registered office in Turin, Via Nizza 262, ABI code 03191, according to which, except in the event of early amortisation, the latter may sell additional loan portfolios of the same type, pursuant to and in accordance with Articles 1 and 4 of Law 130/99. The Company may buy these loans, within the limits of its principal collections arising from its existing loan portfolio.

• The agreements referred to above are part of a wider framework agreement finalised in March 2004 and aimed at structuring a "Program of subsequent issues of securitised assets over time," launched with the support of Deutsche Bank as Arranger.

• This Programme provided for a series of sales of loans over time, from Santander Consumer Bank to Golden Bar, each financed by a new securities issue; the loans gradually acquired by Golden Bar represent a single asset, with no segregation between the loans purchased from time to time, according to a scheme similar to the so-called "Master Trust" transactions, as implemented in Italy.

• The portfolio consisting of each loan assignment, funded by issuing a series of securities, was reconstituted quarterly during the revolving period, allowing Golden Bar to purchase additional loans using the principal collections arising from its existing loan portfolio.

• The program is monitored throughout its duration by Moody's Investors Services and Standard & Poor's, whose responsibilities include, inter alia, verification that subsequent securities issues do not lead to a worsening of the rating assigned to the previous ones.

• The securitised receivables are made up of loans granted by the Assignor to its clients as part of its core lending business. In order for these loans to be transferred to the SPV, they must meet specific contractual requirements, such as that, at the time of sale, least one expired instalment has been regularly collected, there are no past due instalments and the historical record of unpaid instalments does not exceed three instalments. The sale of loans is carried out without recourse.

• In December 2004, as part of the Programme and according to Law 130/99, the second securities issue was completed, totalling €500,000,000 (named Golden Bar Programme Series 2 - 2004) aimed at purchasing the loans sold on 19 November 2004 (effective date 12 November) for an amount of €500,007,552.

• In November 2005, under the Programme and pursuant to Law 130/99, the third purchase of loans from the transferor Santander Consumer Bank S.p.A.

41 Financial Statements as at 31 December 2011

was completed for an amount of €700,008,227 funded through a subsequent securities issue totalling €700,000,000 (named Golden Bar Programme Series 3-2006), which took place on 8 February 2006.

• On 13 December 2006 the fourth sale of loans by the originator was finally completed for an amount of €700,005,785, which was finalised on 31 January 2007 by issuing the fourth securities series for an amount of €700,000. 000.

• With regard to the "Golden Bar Securitisation Programme" portfolio, in 2011 no additional performing loans were purchased on a revolving basis.

• On 22 August 2011, the Series 1 securities issued in 2004 were fully redeemed; at the same time, redemption of the Series 2 Class A securities was completed. During 2011, redemption of the series 2 class B securities began and redemptions of the Series 3 and 4 class A securities continued. In 2011, securities redemptions amounted respectively to €8,390,000 for the Series 1, €60,296,949 for the Series 2, €138,980,209 for the Series 3 and €349,392,096 for the Series 4.

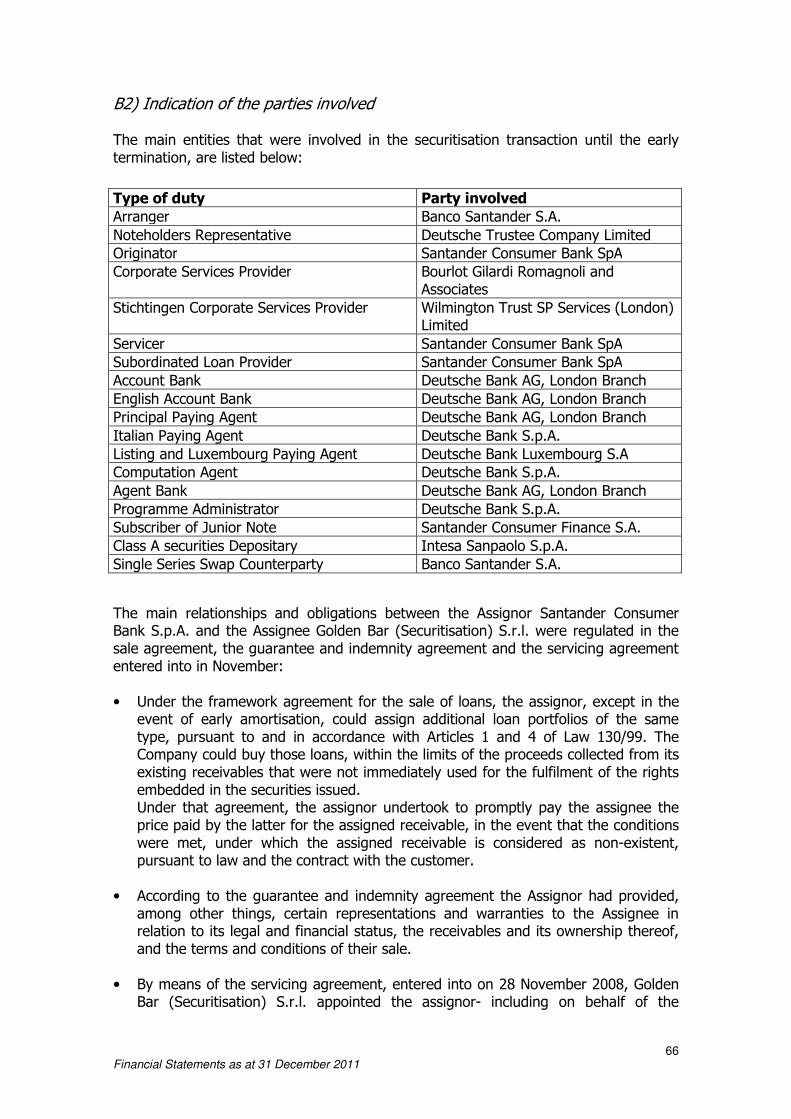

B2) Indication of the parties involved The key parties involved in the securitisation transaction were the following:

Type of duty Party involved

Arranger Deutsche Bank AG- London Branch

Co-Arranger (Series 3) Banco Santander S.A.

Co-Arranger (Series 4) Merrill Lynch & Co Inc.

Lead Manager Deutsche Bank

Lead Manager (Series 3) Merrill Lynch & Co Inc.

Lead Manager (Series 4) Merrill Lynch & Co Inc.

Servicer Santander Consumer Bank SpA

Representative of the Noteholders Deutsche Trustee Co. Ltd

Cash Manager Deutsche Bank S.p.A.

Originator Santander Consumer Bank SpA

Calculation Agent Deutsche Bank S.p.A.

"Class D" securities Depositary Montetitoli S.p.A.

Swap agreement (series 1 and 2) counterparty

Deutsche Bank AG

Swap agreement (series 3 and 4) counterparty

Banco Santander S.A.

The main relationships and obligations between the assignor Santander Consumer Bank S.p.A., the Assignee Golden Bar (Securitisation) S.r.l. and the other parties involved in the securitisation transaction - governed by contract - are the following: • Under the framework agreement for the sale of loans, the assignor, except in the

event of early amortisation, may assign additional loan portfolios of the same type, pursuant to and in accordance with Articles 1 and 4 of Law 130/99. The Company may buy those portfolios, within the limits of the proceeds collected from its existing receivables which are not immediately used for the fulfilment of the rights embedded in the securities issued.

42 Financial Statements as at 31 December 2011

Under that agreement, the assignor undertook to promptly pay the assignee the price paid by the latter for the assigned receivable, in the event that the conditions were met, under which the assigned receivable is considered as non-existent, pursuant to law and the contract with the customer.

• By means of the servicing agreement, Golden Bar (Securitisation) S.r.l. has appointed the assignor- including on behalf of the notes holders and the Cash Manager pursuant to art. 1411 of the Italian Civil Code - to carry out the collection of the assigned receivables and manage collection procedures.

• The Assignor subscribed the class D subordinated security at par, for a nominal value of €1,000,000, €2,500,000, €3,500,000 and €3,500,000 respectively for the Series 1 (contractual maturity in November 2020 and already fully repaid on 22 August 2011), Series 2 (contractual maturity in November 2021), Series 3 (contractual maturity in November 2022) and Series 4 (contractual maturity in November 2023).

• As part of the Intercreditor agreement, the Assignor has accepted the payment cascade by the assignee which provides, inter alia, that consideration for servicing activities is paid after payments to the banks and other service providers, but before interest payment and repayment of principal to securities holders.

B3) Characteristics of the issues In order to finance the purchase of the loan portfolio, Golden Bar (Securitisation) S.r.l. has issued securities denominated in Euros with the following characteristics: Series 1 (17 March 2004)

• "Class A Limited Recourse Asset-Backed Notes" (Class A notes) with contractual maturity in November 2020 and a nominal value of €188,000,000 issued at par. The Class A notes had been rated Aaa by Moody's Investors Service Inc. and AAA by Standard & Poor's. The above ratings were subject to ongoing monitoring by the mentioned companies and did not change during the year. Holders of these notes were paid quarterly interest at a rate equal to three months Euribor plus 0.26% per year. The Class A notes were listed on the Luxembourg Stock Exchange.

• "Class B Limited Recourse Asset-Backed Notes" (Class B notes) with contractual maturity in November 2020 and a nominal value of €8,000,000 issued at par. The Class B notes had been rated A2 by Moody's Investors Service Inc. and A by Standard & Poor's. The above ratings were subject to ongoing monitoring by the mentioned companies and did not change during the year. Holders of these notes were paid quarterly interest at a rate equal to three months Euribor plus 0.60% per year. The Class B notes were listed on the Luxembourg Stock Exchange.

• "Class C Limited Recourse Asset-Backed Notes" (Class C notes) with contractual maturity in November 2020 and a nominal value of €3,000,000 issued at par.

43 Financial Statements as at 31 December 2011

The Class C notes had been rated Baa2 by Moody's Investors Service Inc. and BBB by Standard & Poor's. The above ratings were subject to ongoing monitoring by the mentioned companies and did not change during the year. Holders of these notes were paid quarterly interest at a rate equal to three months Euribor plus 1.20% per year. The Class C notes were listed on the Luxembourg Stock Exchange.

• "Class D Limited Recourse Asset-Backed Notes" (Class D notes) with contractual maturity in November 2020 and a nominal value of €1,000,000 issued at par. Class D notes were subordinated with respect to class A, B and C notes in terms of both principal repayment and payment of interest accrued thereon. These notes were without rating and had been subscribed by the Assignor. In accordance with the contractual terms, remuneration of class D notes corresponded to the excess spread, calculated as the difference between the quarterly accrued interest on the loan portfolio, the interest paid to investors in class A, B and C securities and the transaction operating costs.

• The company, in accordance with the Pricing Supplement, on 22 August 2011 completed the redemption of all Series 1 securities.

Series 2 (09 December 2004)