FY17

55

-

Upload

pranav-rao -

Category

Investor Relations

-

view

243 -

download

1

Transcript of FY17

IMPORTANT NOTICE AND DISCLAIMER

Important notice and disclaimer

This document is a presentation of general background information about the activities of Mantra Group Limited (Mantra Group) current at the date of the presentation, 29 August

2017. The information contained in this presentation is of general background and does not purport to be complete. It is not intended to be relied upon as advice to investors or

potential investors and does not take into account the investment objectives, financial situation or needs of any particular investor. These should be considered, with or without

professional advice, when deciding if an investment is appropriate.

Mantra Group, its related bodies corporate and any of their respective officers, directors and employees (Mantra Group Parties), do not warrant the accuracy or reliability of this

information, and disclaim any responsibility and liability flowing from the use of this information by any party. To the maximum extent permitted by law, the Mantra Group Parties

do not accept any liability to any person, organisation or entity for any loss or damage suffered as a result of reliance on this document.

Forward looking statements

This document contains certain forward looking statements and comments about future events, including Mantra Group’s expectations about the performance of its businesses.

Forward looking statements can generally be identified by the use of forward looking words such as, ‘expect’, ‘anticipate’, ‘likely’, ‘intend’, ‘should’, ‘could’, ‘may’, ‘predict’, ‘plan’,

‘propose’, ‘will’, ‘believe’, ‘forecast’, ‘estimate’, ‘target’ and other similar expressions within the meaning of securities laws of applicable jurisdictions. Indications of, and guidance

on, future earnings or financial position or performance are also forward looking statements.

Forward looking statements involve inherent risks and uncertainties, both general and specific, and there is a risk that such predictions, forecasts, projections and other forward

looking statements will not be achieved. Forward looking statements are provided as a general guide only, and should not be relied on as an indication or guarantee of future

performance. Forward looking statements involve known and unknown risks, uncertainty and other factors which can cause Mantra Group’s actual results to differ materially from

the plans, objectives, expectations, estimates and intentions expressed in such forward looking statements and many of these factors are outside the control of Mantra Group. As

such, undue reliance should not be placed on any forward looking statement. Past performance is not necessarily a guide to future performance and no representation or

warranty is made by any person as to the likelihood of achievement or reasonableness of any forward looking statements, forecast financial information or other forecast. Nothing

contained in this presentation nor any information made available to you is, or shall be, relied upon as a promise, representation, warranty or guarantee as to the past, present or

the future performance of Mantra Group.

Non-IFRS financial information

Mantra Group uses certain measures to manage and report on its business that are not recognised under Australian Accounting Standards. These measures are referred to as

non-IFRS financial information. Mantra Group considers that this non-IFRS financial information is important to assist in evaluating Mantra Group’s performance. The information

is presented to assist in making appropriate comparisons with current periods and to assess the operating performance of the business. All non-IFRS financial information is

reconciled to IFRS financial information.

All dollar values are in Australian dollars (A$) unless otherwise stated. 2

CONTENTS HIGHLIGHTS 4

MANTRA GROUP’S BUSINESS 9

FINANCIAL PERFORMANCE 18

STRATEGY AND OUTLOOK 27

PROPERTIES SCHEDULED TO ENTER PORTFOLIO 31

APPENDIX 34

3

HIGHLIGHTS

4

HIGHLIGHTS

5

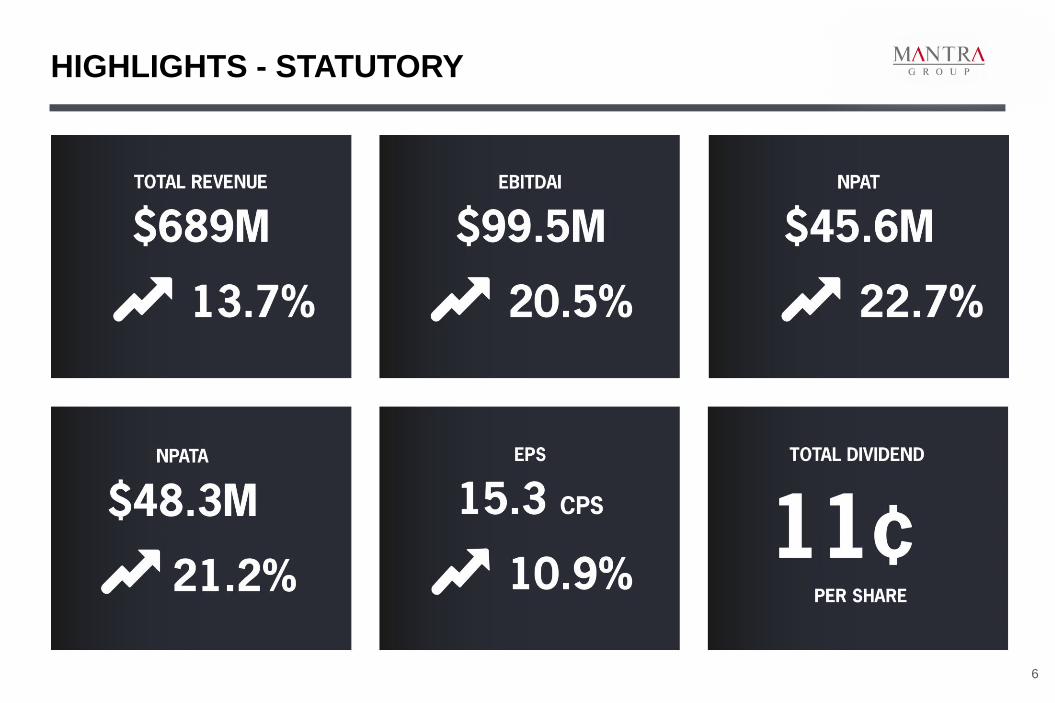

HIGHLIGHTS - STATUTORY

6

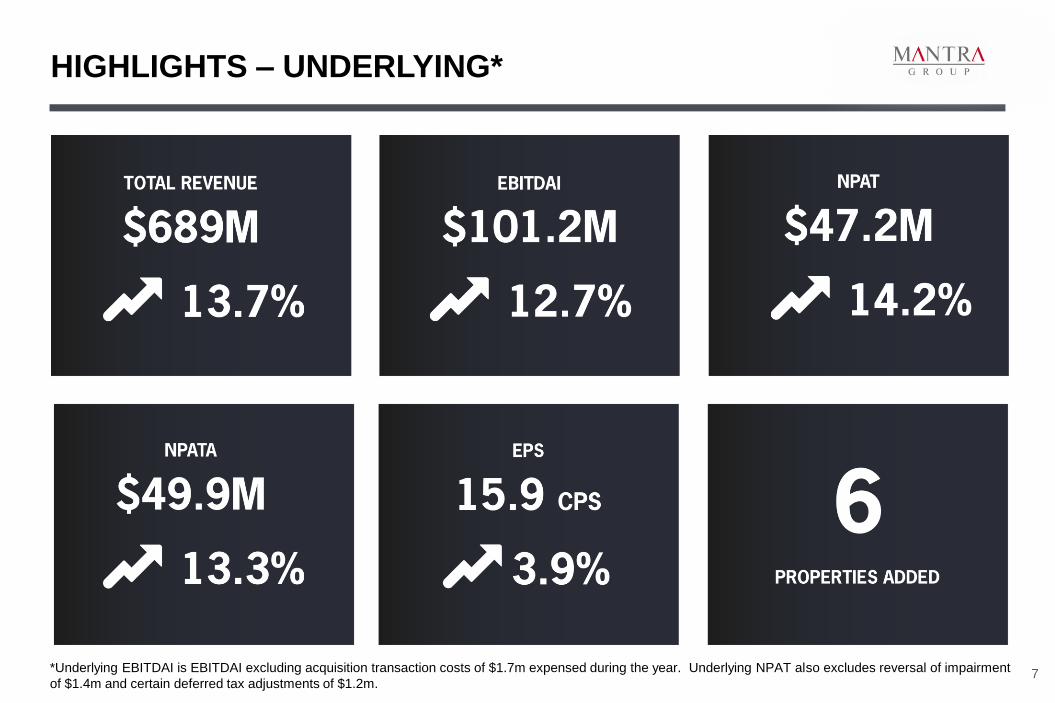

HIGHLIGHTS – UNDERLYING*

7 *Underlying EBITDAI is EBITDAI excluding acquisition transaction costs of $1.7m expensed during the year. Underlying NPAT also excludes reversal of impairment

of $1.4m and certain deferred tax adjustments of $1.2m.

HIGHLIGHTS – STRONG TRACK RECORD

8

*N/C – not calculated

** Underlying NPAT excludes transaction costs of $1.7m (FY2016: $7.3m) incurred in respect of business combinations, the reversal of impairment of $1.4m

(FY2016: $2.1m) and an impairment related deferred tax expense of $1.2m (FY2016: benefit of $1.0m).

Strong growth on all key metrics since listing in June 2014

Year ended Keys under

management Room nights

Underlying

EBITDAI $m

Underlying NPAT

$m

Underlying EPS

Cents per share

June 2014 11,500+ 2,400,000+ 61.3 (0.3) (0.3)

June 2015 13,000+ 2,700,000+ 73.1 36.2 14.2

June 2016 15,000+ 3,300,000+ 89.8 41.3 15.3

June 2017 16,500+ 3,675,000+ 101.2 47.2 15.9

Three year CAGR 13.1% 14.1% 18.2% N/C* N/C*

MANTRA GROUP’S BUSINESS

9

MANTRA GROUP LOCATIONS

Mantra Group benefits from diversified geographic presence in the Australian accommodation market and has a

growing presence in selected overseas markets

10

128 properties

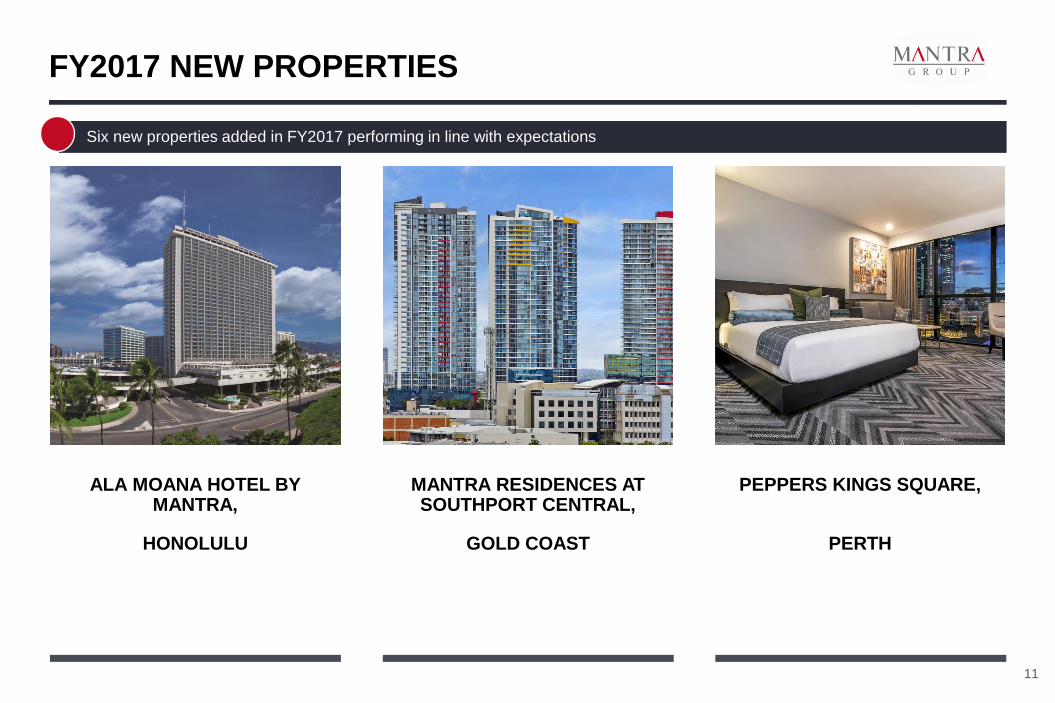

ALA MOANA HOTEL BY MANTRA,

HONOLULU

MANTRA RESIDENCES AT SOUTHPORT CENTRAL,

GOLD COAST

PEPPERS KINGS SQUARE,

PERTH

FY2017 NEW PROPERTIES

Six new properties added in FY2017 performing in line with expectations

11

MANTRA THE OBSERVATORY,

PORT MACQUARIE

MANTRA CLUB CROC,

AIRLIE BEACH

TRIBE PERTH,

WEST PERTH

FY2017 NEW PROPERTIES

12

Six new properties added in FY2017 performing in line with expectations

Internationally scalable & best in class

Sihot & Revenue Management

Mantrahotels.com – global booking channel

brand launch

Mantra+ loyalty launched - 100k+ members

SYSTEMS & PROGRAMS

13

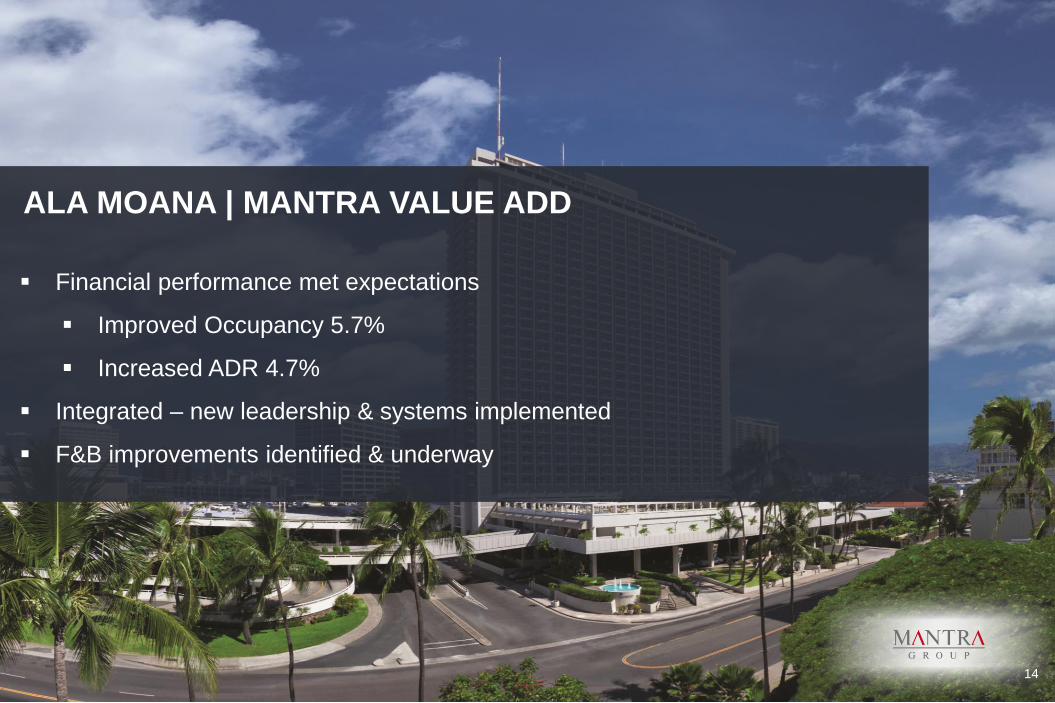

ALA MOANA | MANTRA VALUE ADD

Financial performance met expectations

Improved Occupancy 5.7%

Increased ADR 4.7%

Integrated – new leadership & systems implemented

F&B improvements identified & underway

14

• 5,500+ Team Members

• 21 Rising Stars

• 122 Emerging Leaders

• 86.3% Team Member satisfaction

• Women in Mantra & diversity initiatives

• 700+ Team Members next 12 months

• Employer of Choice 2017

• Mantra Awards for Excellence

TEAM & TRAINING & DEVELOPMENT

15

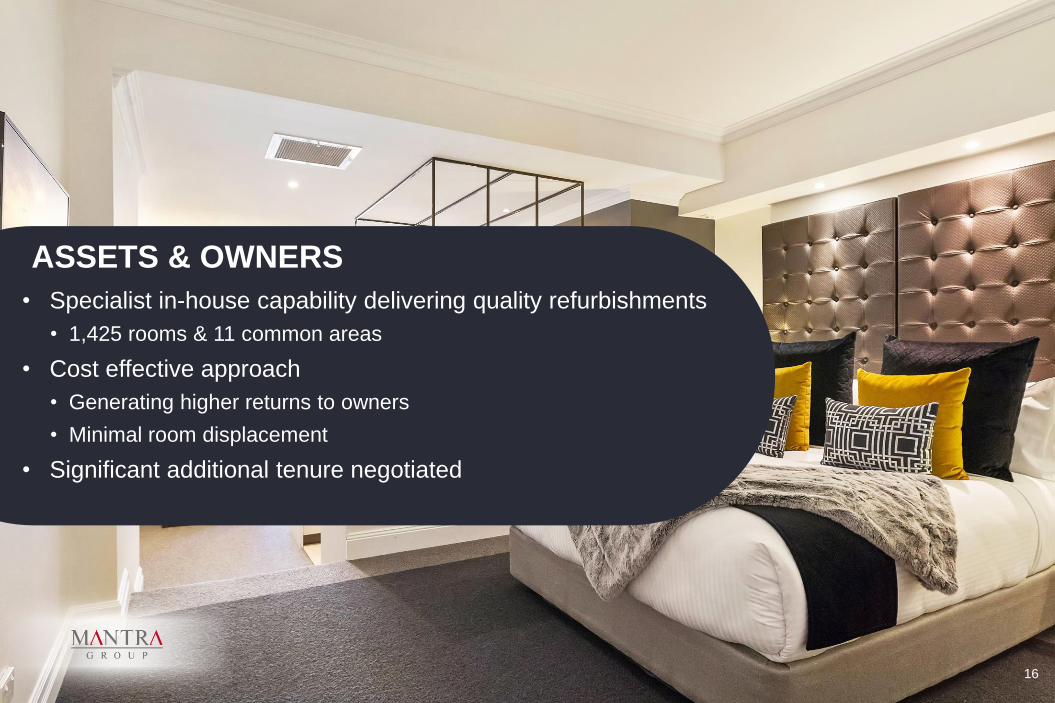

• Specialist in-house capability delivering quality refurbishments

• 1,425 rooms & 11 common areas

• Cost effective approach

• Generating higher returns to owners

• Minimal room displacement

• Significant additional tenure negotiated

16

ASSETS & OWNERS

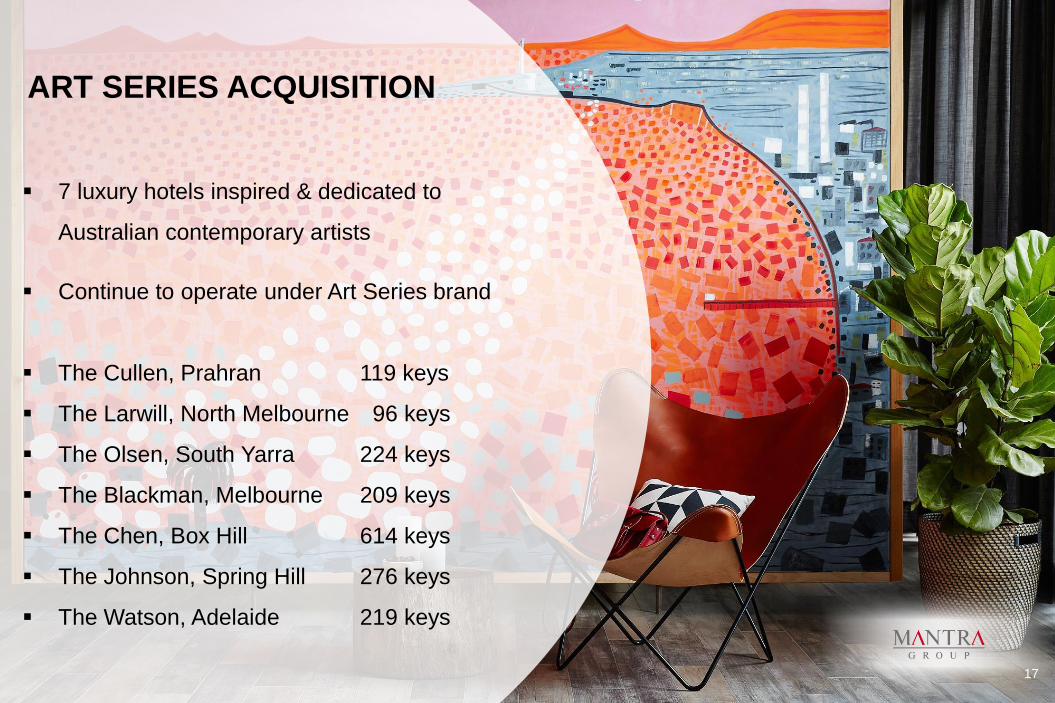

7 luxury hotels inspired & dedicated to

Australian contemporary artists

Continue to operate under Art Series brand

The Cullen, Prahran 119 keys

The Larwill, North Melbourne 96 keys

The Olsen, South Yarra 224 keys

The Blackman, Melbourne 209 keys

The Chen, Box Hill 614 keys

The Johnson, Spring Hill 276 keys

The Watson, Adelaide 219 keys

ART SERIES ACQUISITION

17

FINANCIAL PERFORMANCE

18

YEAR ON YEAR RESULTS OVERVIEW

• Strong FY2017 performance with occupancy,

ARR and RevPAR increasing 1.8%, 3.6% and

5.5% respectively

• Total revenue increased by 13.7% to $689m from

$606.1m

• Statutory EBITDAI increased by $16.9m (20.5%)

to $99.5m

• Strong revenue growth driven by:

• Six property acquisitions completed in the

period contributed $59.5m

• Organic growth of $23.4m

FY2017

($m)

FY2016

($m)

Change

($m)

Change

(%)

Total revenue 689.0 606.1 82.9 13.7

Statutory results

EBITDAI1 99.5 82.6 16.9 20.5

NPAT 45.6 37.2 8.4 22.7

NPATA 48.3 39.9 8.4 21.2

Underlying Results

EBITDAI1,2 101.2 89.8 11.4 12.7

NPAT2 47.2 41.3 5.9 14.2

NPATA2 49.9 44.0 5.9 13.3

Other key statistics

Rooms available (‘000) 4,650 4,234 416 9.8

Occupancy (%) 79.5 78.1 1.4 1.8

Average room rate ($) 175.24 169.14 6.1 3.6

RevPAR ($) 139.38 132.14 7.24 5.5

COMMENTS

1 EBITDAI – Earnings Before Interest, Taxation, Depreciation, Amortisation and Impairment

2 Underlying EBITDA is EBITDAI excluding transaction costs of $1.7m (FY2016: $7.3m) incurred in respect of business combinations. Underlying NPAT & NPATA also excludes the reversal of

impairment of $1.4m (FY2016: $2.1m) and an impairment related deferred tax expense of $1.2m (FY2016: benefit of $1.0m). 3 Organic excludes properties added in FY2017

19

1 EBITDAI – Earnings Before Interest, Taxation, Depreciation, Amortisation and Impairment 2 Underlying EBITDAI is EBITDAI excluding transaction costs of $1.7m (FY2016: $7.3m) incurred in respect of business combinations. Underlying NPAT also excludes the reversal of impairment of

$1.4m (FY2016: $2.1m) and an impairment related deferred tax expense of $1.2m (FY2016: benefit of $1.0m).

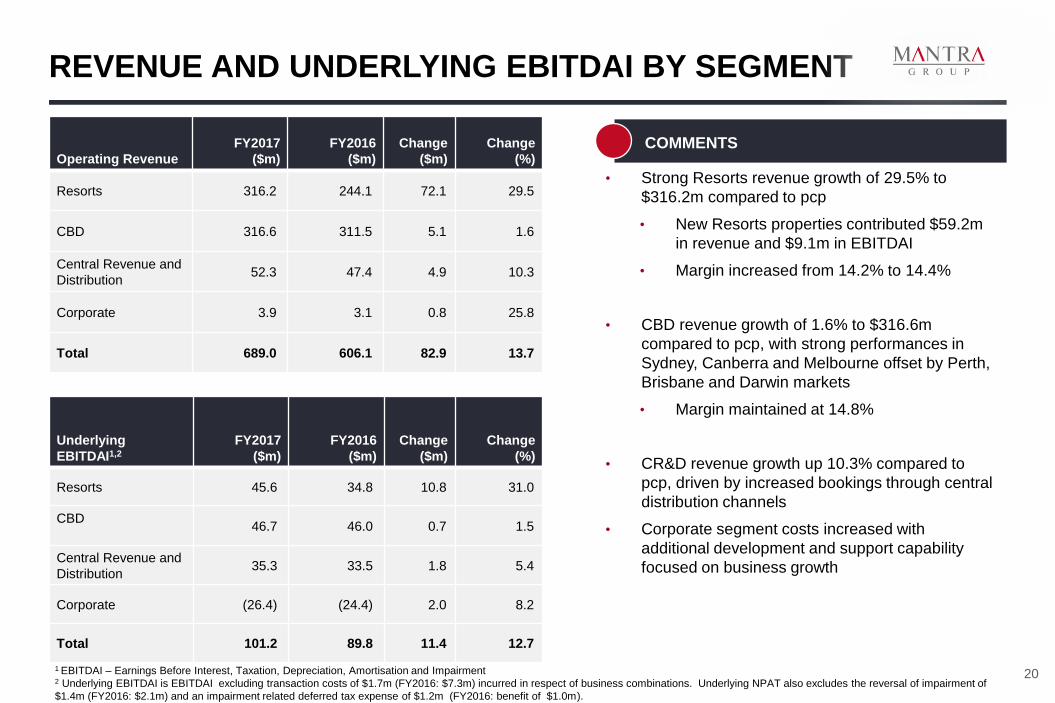

REVENUE AND UNDERLYING EBITDAI BY SEGMENT

• Strong Resorts revenue growth of 29.5% to

$316.2m compared to pcp

• New Resorts properties contributed $59.2m

in revenue and $9.1m in EBITDAI

• Margin increased from 14.2% to 14.4%

• CBD revenue growth of 1.6% to $316.6m

compared to pcp, with strong performances in

Sydney, Canberra and Melbourne offset by Perth,

Brisbane and Darwin markets

• Margin maintained at 14.8%

• CR&D revenue growth up 10.3% compared to

pcp, driven by increased bookings through central

distribution channels

• Corporate segment costs increased with

additional development and support capability

focused on business growth

Operating Revenue

FY2017

($m)

FY2016

($m)

Change

($m)

Change

(%)

Resorts 316.2 244.1 72.1 29.5

CBD 316.6 311.5 5.1 1.6

Central Revenue and

Distribution 52.3 47.4 4.9 10.3

Corporate 3.9 3.1 0.8 25.8

Total 689.0 606.1 82.9 13.7

Underlying

EBITDAI1,2

FY2017

($m)

FY2016

($m)

Change

($m)

Change

(%)

Resorts 45.6 34.8 10.8 31.0

CBD

46.7 46.0 0.7 1.5

Central Revenue and

Distribution 35.3 33.5 1.8 5.4

Corporate (26.4) (24.4) 2.0 8.2

Total 101.2 89.8 11.4 12.7

COMMENTS

20

FY2017

Actual

FY2016

Actual Change

Change

(%)

Total rooms available (‘000) 2,748 2,364 384 16.2

Paid rooms sold (‘000) 2,084 1,732 351 20.3

Occupancy (%) 75.8 73.3 2.5 3.4

Average room rate ($) 177.91 165.30 12.62 7.6

RevPAR ($) 134.88 121.12 13.76 11.4

RESORTS SEGMENT - HIGHLIGHTS

Outstanding growth in Resorts segment across all key metrics

RevPAR movements in key regions

Gold Coast 2.1% Dreamworld impacted record bookings

Sunshine Coast 11.7% Noosa key driver due to strong leisure demand

TNQ 5.2% Strong domestic and Asian inbound

New Zealand 15.2% Strong leisure and Asian inbound

Hawaii N/A Delivered improvements in first year

Pipeline FY2018-FY2020 Keys

Scheduled* 0

Targeted** 2,612

21

* Scheduled – agreements are signed and properties will join the portfolio, subject to customary completion terms

** Targeted – contracts are under negotiation

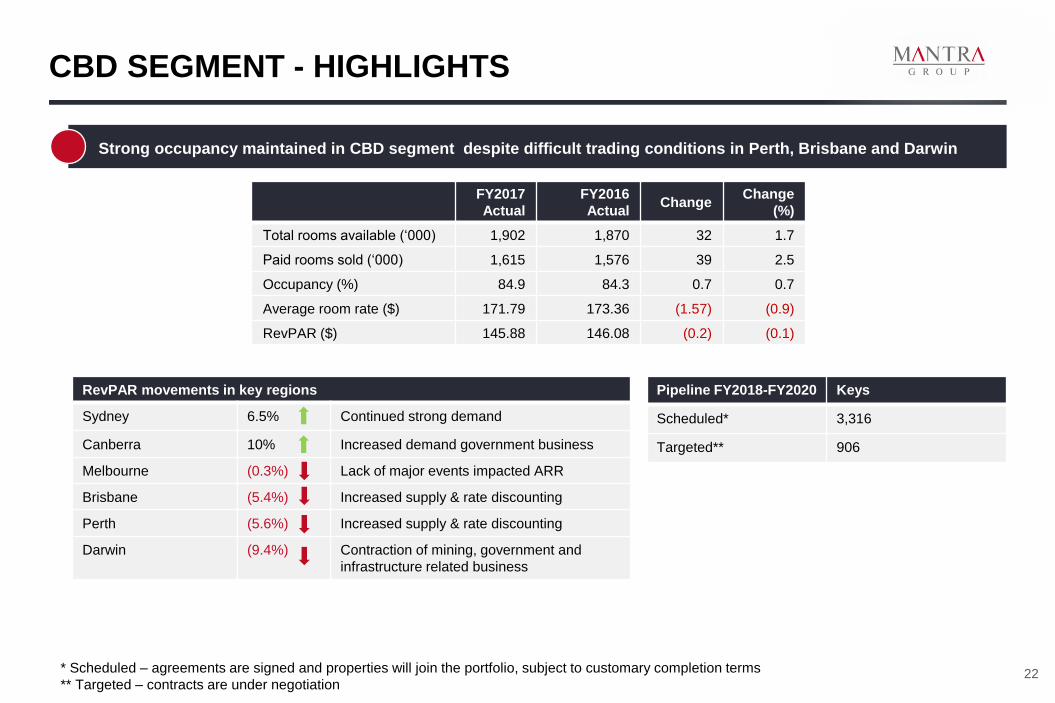

CBD SEGMENT - HIGHLIGHTS

Strong occupancy maintained in CBD segment despite difficult trading conditions in Perth, Brisbane and Darwin

FY2017

Actual

FY2016

Actual Change

Change

(%)

Total rooms available (‘000) 1,902 1,870 32 1.7

Paid rooms sold (‘000) 1,615 1,576 39 2.5

Occupancy (%) 84.9 84.3 0.7 0.7

Average room rate ($) 171.79 173.36 (1.57) (0.9)

RevPAR ($) 145.88 146.08 (0.2) (0.1)

RevPAR movements in key regions

Sydney 6.5% Continued strong demand

Canberra 10% Increased demand government business

Melbourne (0.3%) Lack of major events impacted ARR

Brisbane (5.4%) Increased supply & rate discounting

Perth (5.6%) Increased supply & rate discounting

Darwin (9.4%) Contraction of mining, government and

infrastructure related business

Pipeline FY2018-FY2020 Keys

Scheduled* 3,316

Targeted** 906

22 * Scheduled – agreements are signed and properties will join the portfolio, subject to customary completion terms

** Targeted – contracts are under negotiation

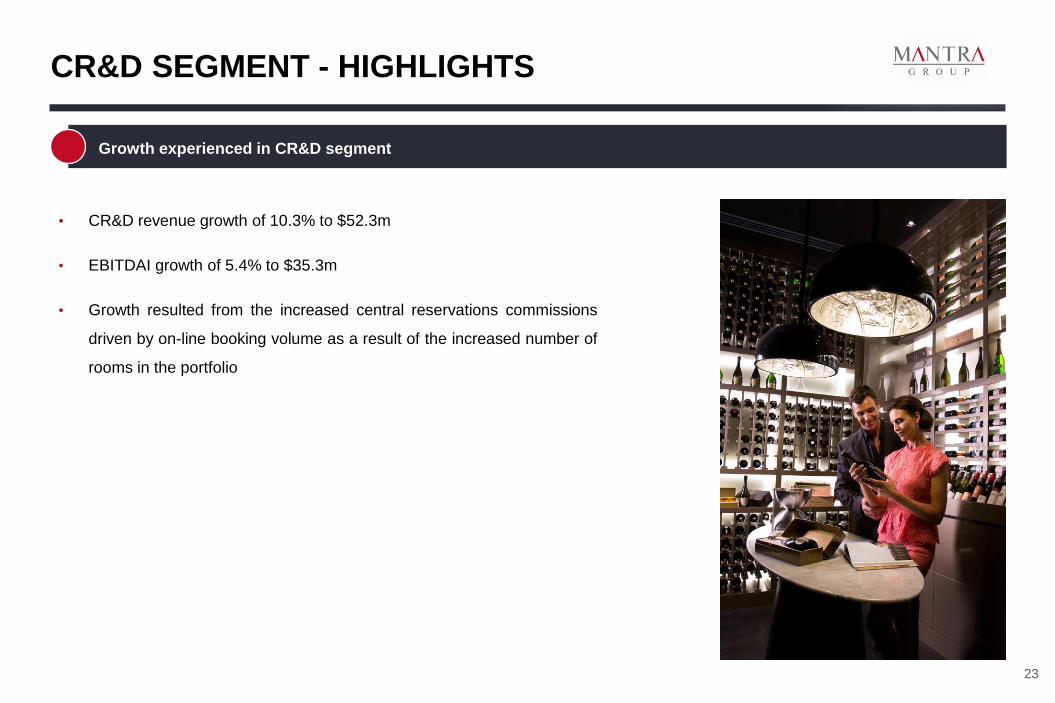

CR&D SEGMENT - HIGHLIGHTS

Growth experienced in CR&D segment

• CR&D revenue growth of 10.3% to $52.3m

• EBITDAI growth of 5.4% to $35.3m

• Growth resulted from the increased central reservations commissions

driven by on-line booking volume as a result of the increased number of

rooms in the portfolio

23

STATUTORY PROFIT AND LOSS FOR THE PERIOD

FY2017

($m)

FY2016

($m)

Change

($m)

Change

%

Operating revenue 689.0 606.1 82.9 13.7

Other income 0 0.1 (0.1) (100)

Total operating expenses (589.5) (523.6) 65.9 12.6

EBITDAI1 99.5 82.6 16.9 20.5

Net reversal of impairment 1.4 2.1 (0.7) (32.1)

Depreciation and amortisation (excluding

amortisation of lease rights) (23.9) (19.5) (4.4) 22.4

Amortisation of lease rights (3.8) (3.8) 0 0

Net finance costs (4.7) (5.2) (0.5) (10.0)

Profit before tax 68.6 56.2 12.4 22.0

Tax expense (23.0) (19.1) 3.9 20.5

NPAT 45.6 37.1 8.4 22.7

NPATA 48.3 39.8 8.4 21.2

EPS 15.3 13.8 1.5 10.9

COMMENTS

1 EBITDAI – Earnings Before Interest, Taxation, Depreciation, Amortisation and Impairment 2 Organic excludes properties added in FY2017

• Business has performed strongly in FY2017

• Revenue, EBITDAI, NPAT and NPATA all

performed ahead of the pcp

• Operating revenue increased by $82.9m

(13.7%)

• EBITDAI increased by $16.9m (20.5%)

• Growth in NPAT impacted by transaction

costs arising from business combinations

(FY2017: $1.7m, FY2016:$7.3m)

• Strong revenue growth driven by

• Six property acquisitions completed in the

period (increase of $59.5m)

• Remaining increase driven by organic2

growth (increase of $23.4m)

• Net reversal of impairment of $1.4m in FY2017.

All intangible assets are tested for impairment at

least annually.

24

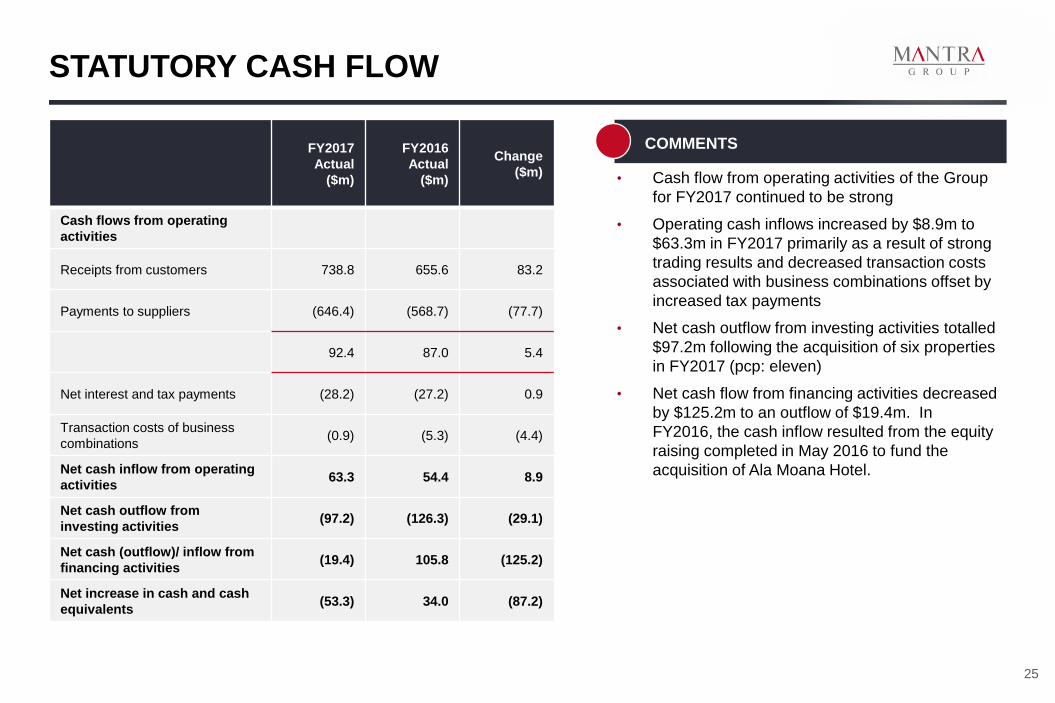

STATUTORY CASH FLOW

• Cash flow from operating activities of the Group

for FY2017 continued to be strong

• Operating cash inflows increased by $8.9m to

$63.3m in FY2017 primarily as a result of strong

trading results and decreased transaction costs

associated with business combinations offset by

increased tax payments

• Net cash outflow from investing activities totalled

$97.2m following the acquisition of six properties

in FY2017 (pcp: eleven)

• Net cash flow from financing activities decreased

by $125.2m to an outflow of $19.4m. In

FY2016, the cash inflow resulted from the equity

raising completed in May 2016 to fund the

acquisition of Ala Moana Hotel.

FY2017

Actual

($m)

FY2016

Actual

($m)

Change

($m)

Cash flows from operating

activities

Receipts from customers 738.8 655.6 83.2

Payments to suppliers (646.4) (568.7) (77.7)

92.4 87.0 5.4

Net interest and tax payments (28.2) (27.2) 0.9

Transaction costs of business

combinations (0.9) (5.3) (4.4)

Net cash inflow from operating

activities 63.3 54.4 8.9

Net cash outflow from

investing activities (97.2) (126.3) (29.1)

Net cash (outflow)/ inflow from

financing activities (19.4) 105.8 (125.2)

Net increase in cash and cash

equivalents (53.3) 34.0 (87.2)

COMMENTS

25

BALANCE SHEET AND CREDIT METRICS

Statutory balance sheet

30 Jun 17

Actual

$m

30 Jun 16

Actual

$m

Cash and cash equivalents 62.9 117.1

Other current assets 67.2 60.0

Current assets 130.2 177.1

PPE 157.7 121.9

Intangible assets 513.4 469.4

Other non-current assets 5.1 0.7

Total non-current assets 676.1 591.9

Total assets 806.3 769.0

Trade and other payables 52.6 44.8

Other liabilities 45.0 44.6

Total current liabilities 97.6 89.3

Borrowings 135.3 125.1

Other non-current liabilities 95.4 91.5

Total non-current liabilities 230.7 216.6

Total liabilities 328.3 306.0

Net assets 477.9 463.1

Credit metrics 30 Jun 17

Actual

$m

30 Jun 16

adjusted*

$m

Borrowings ($m) 135.3 125.1

Cash and cash equivalents ($m) 62.9 62.3

Net total indebtedness ($m) 72.4 62.8

Net debt /LTM Underlying

EBITDAI 0.7x 0.7x

FY2017 LTM Underlying

EBITDAI/LTM Net finance cost 21.7x 17.4x

• Strong balance sheet and cash position leaves

the Group sufficient facilities to fund the Art

Series Hotel Group acquisition out of current

available funds

• Intangible assets have increased by $44.0m

(9.4%) since 30 June 2016 following the

acquisition of six properties. Useful life of

intangible assets is reassessed each year.

• The Group is well within debt covenants under

banking facilities

COMMENTS

*Cash balance adjusted to remove cash used to purchase Ala Moana in July 2016 26

STRATEGY AND OUTLOOK

27

Mantra Group expects FY2018 Underlying

EBITDAI to be between $107m - $115m in

constant currency terms

• In our commitment to drive ongoing growth and

deliver shareholder value in FY2018, Mantra Group

will continue to deliver on its key strategies

supporting these objectives

• Art Series start date subject to conditions precedent

• Peppers FV subject to conditions precedent

• FY2018 growth expected across the Resorts, CBD

and CR&D segments

28

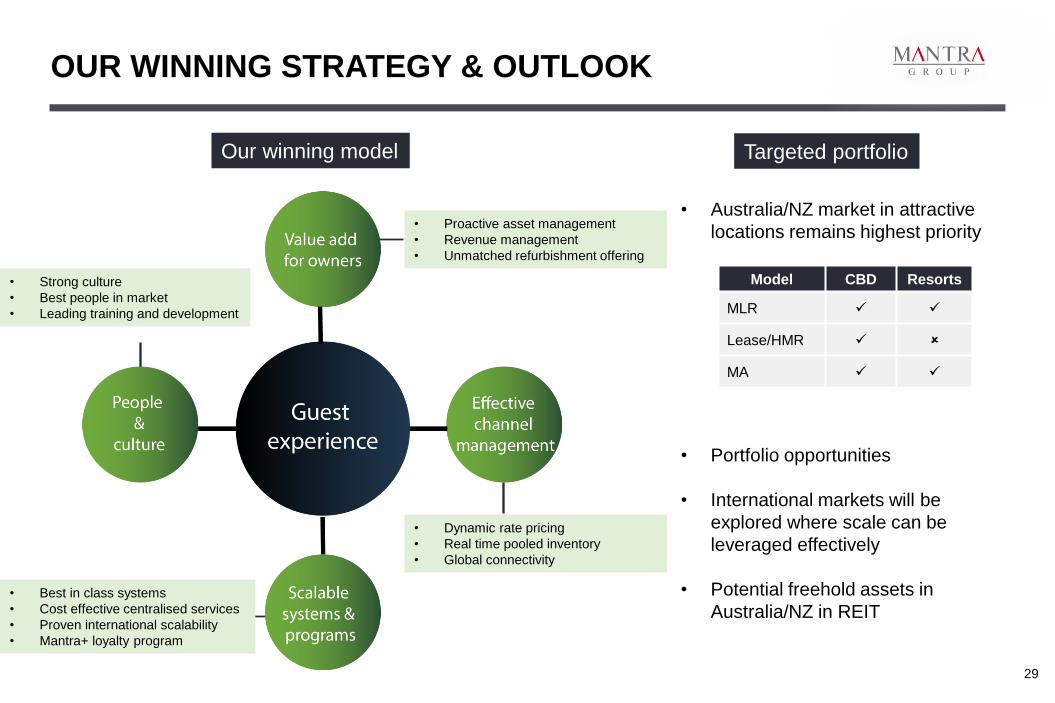

OUR WINNING STRATEGY & OUTLOOK

29

Our winning model Targeted portfolio

• Australia/NZ market in attractive

locations remains highest priority

• Portfolio opportunities

• International markets will be

explored where scale can be

leveraged effectively

• Potential freehold assets in

Australia/NZ in REIT

Model CBD Resorts

MLR

Lease/HMR

MA

• Proactive asset management

• Revenue management

• Unmatched refurbishment offering

• Dynamic rate pricing

• Real time pooled inventory

• Global connectivity

• Best in class systems

• Cost effective centralised services

• Proven international scalability

• Mantra+ loyalty program

• Strong culture

• Best people in market

• Leading training and development

PROPERTIES SCHEDULED TO ENTER PORTFOLIO

30

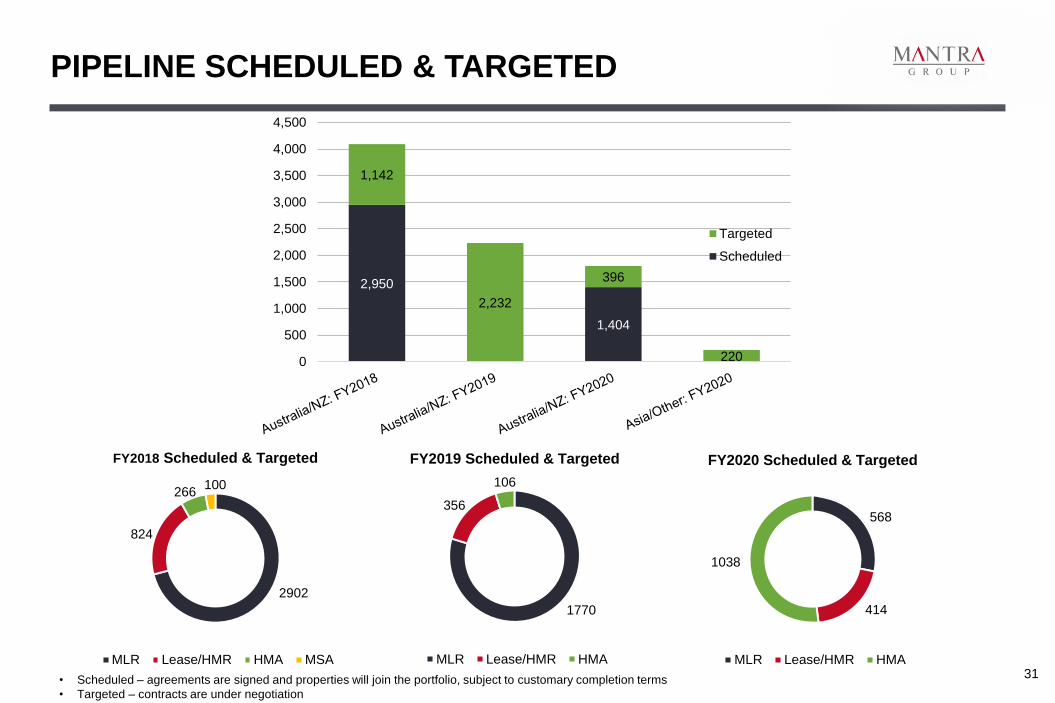

568

414

1038

FY2020 Scheduled & Targeted

MLR Lease/HMR HMA

2902

824

266 100

FY2018 Scheduled & Targeted

MLR Lease/HMR HMA MSA

2,950

1,404

1,142

2,232

396

220 0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

Targeted

Scheduled

1770

356

106

FY2019 Scheduled & Targeted

MLR Lease/HMR HMA

PIPELINE SCHEDULED & TARGETED

31 • Scheduled – agreements are signed and properties will join the portfolio, subject to customary completion terms

• Targeted – contracts are under negotiation

Strong performance for FY2017 maintaining market leading position

Highly cash generative business

Australian tourism sector continues to strengthen with strong gains in domestic and international tourism

Continue to leverage our proven core capabilities to deliver our growth strategy

The business is in prime position to capitalise on opportunities

CONCLUSION

32

APPENDIX

33

PROPERTIES SCHEDULED TO ENTER PORTFOLIO

34

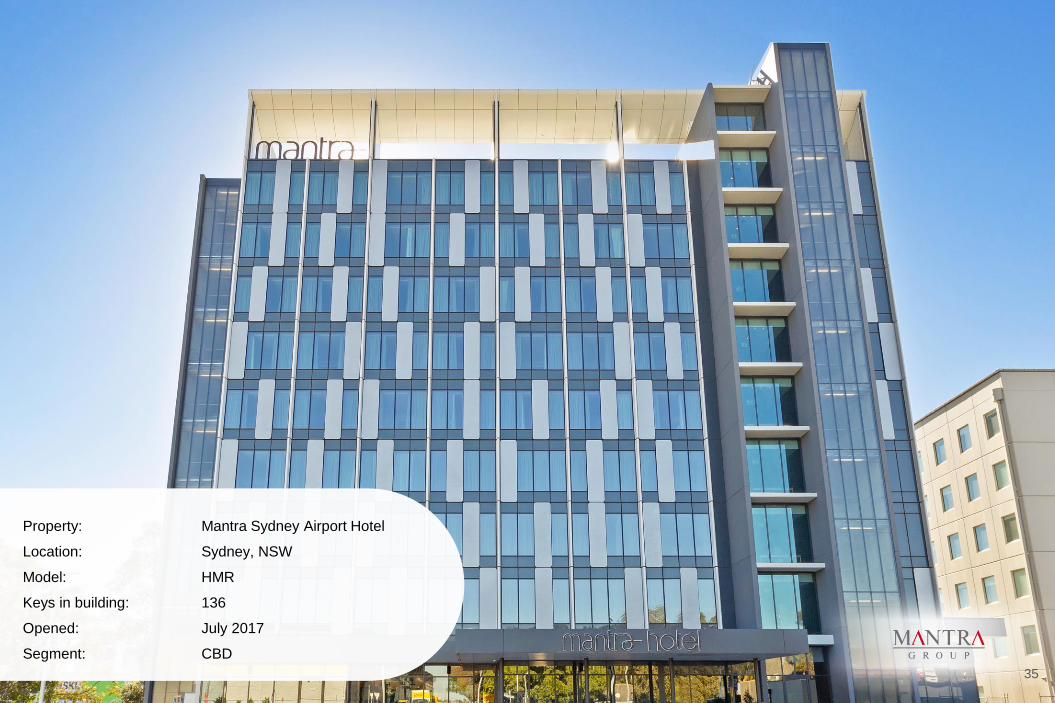

Property: Mantra Sydney Airport Hotel

Location: Sydney, NSW

Model: HMR

Keys in building: 136

Opened: July 2017

Segment: CBD

35

Property: FV

Location: Brisbane, QLD

Model: MLR

Keys in building: 969 (across 3 towers with the

3rd tower to open H1FY2020)

Opening: H1FY2018

Segment: CBD

36

Property: Mantra Macarthur Hotel

Location: Canberra, ACT

Model: LEASE

Keys in building: 176

Opening: H1FY2018

Segment: CBD

37

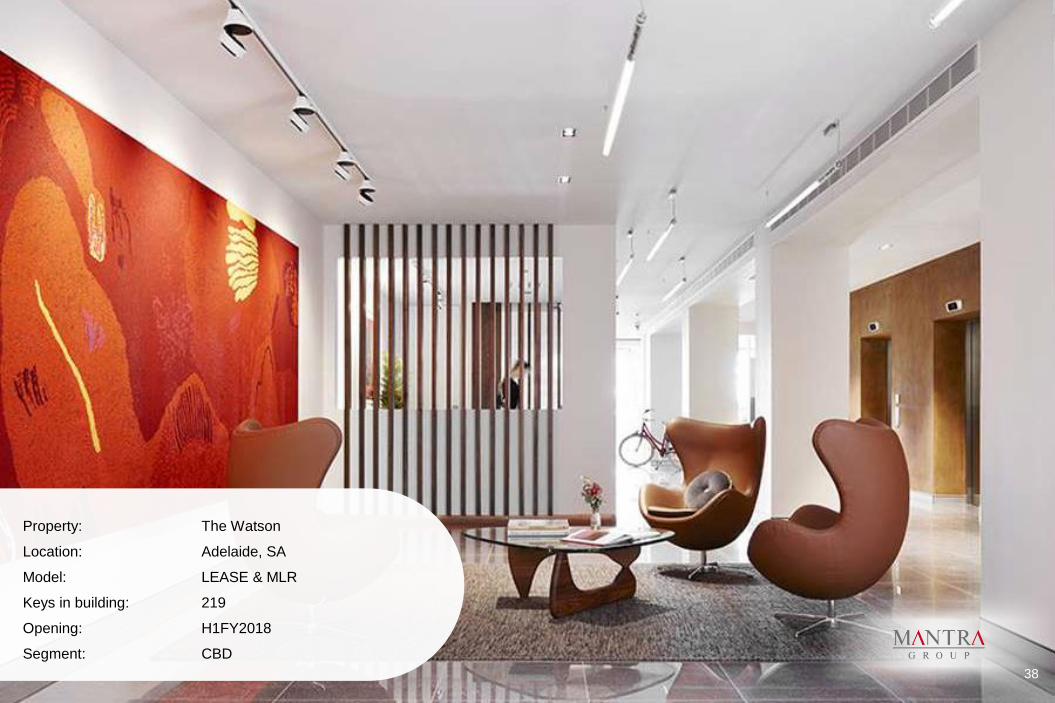

Property: The Watson

Location: Adelaide, SA

Model: LEASE & MLR

Keys in building: 219

Opening: H1FY2018

Segment: CBD

38

Property: The Olsen

Location: South Yarra, VIC

Model: LEASE

Keys in building: 224

Opening: H1FY2018

Segment: CBD

39

Property: The Blackman

Location: Melbourne, VIC

Model: LEASE

Keys in building: 209

Opening: H1FY2018

Segment: CBD

40

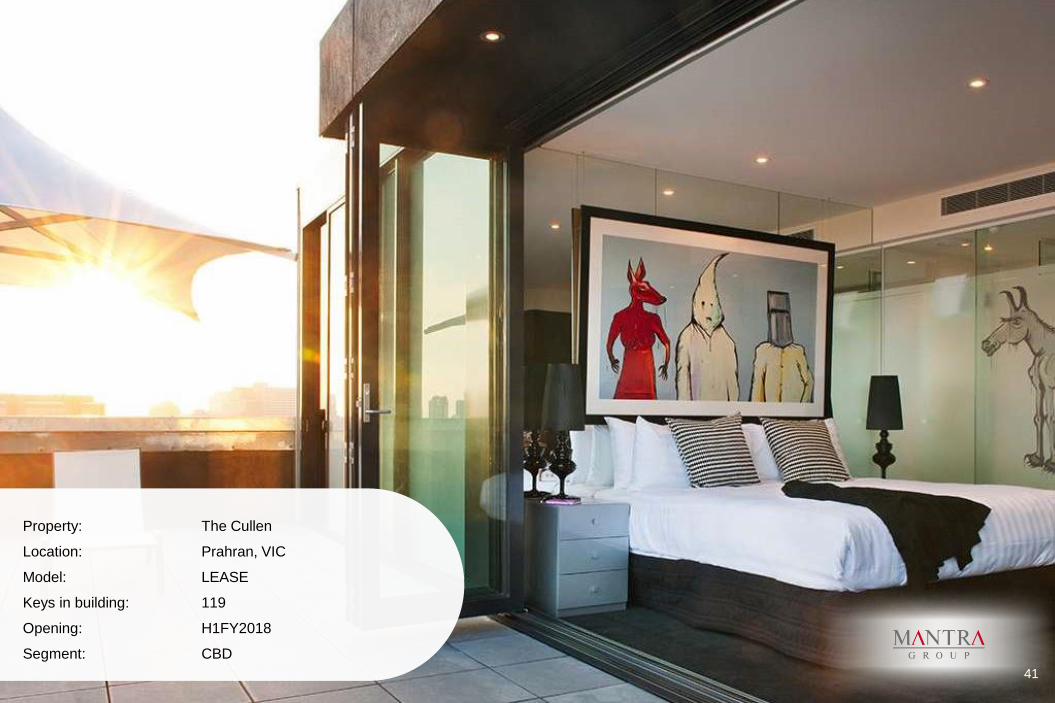

Property: The Cullen

Location: Prahran, VIC

Model: LEASE

Keys in building: 119

Opening: H1FY2018

Segment: CBD

41

Property: The Larwill

Location: Melbourne, VIC

Model: LEASE

Keys in building: 96

Opening: H1FY2018

Segment: CBD

42

Property: The Chen

Location: Box Hill, VIC

Model: LEASE & MLR

Keys in building: 614

Opening: H1FY2018

Segment: CBD

43

Property: The Johnson

Location: Spring Hill, QLD

Model: LEASE & MLR

Keys in building: 276

Opening: H1FY2018

Segment: CBD

44

Property: Peppers Silo Hotel

Location: Launceston, TAS

Model: HMR

Keys in building: 108

Opening: H2FY2018

Segment: CBD

45 45

Property: Mantra Albury

Location: Albury, NSW

Model: HMR

Keys in building: 158

Opening: H2FY2018

Segment: CR&D

46

Property: Mantra Southport Sharks

Location: Gold Coast, QLD

Model: MSA

Keys in building: 100

Opening: H2FY2018

Segment: CORPORATE

47

Property: Mantra 900 Hay Street

Location: Perth, WA

Model: LEASE

Keys in building: 250

Opening: H1FY2020

Segment: CBD

48

Property: Peppers Southbank Melbourne

Location: Melbourne, VIC

Model: LEASE

Keys in building: 164

Opening: H1FY2020

Segment: CBD

49

Property: Mantra Epping

Location: Epping, VIC

Model: HMR

Keys in building: 212

Opening: H1FY2020

Segment: CR&D

50 50

Property: Peppers Queenstown

Location: Queenstown, New Zealand

Model: HMR

Keys in building: 260

Opening: H2FY2020

Segment: CR&D

51

Property: Mantra Sky Hotel Tekapo

Location: Lake Tekapo, New Zealand

Model: MA

Keys in building: 100

Opening: H2FY2020

Segment: CR&D

52

Property: Mantra Wallaroo Shores

Location: Wallaroo, SA

Model: MA

Keys in building: 100

Opening: H2FY2020

Segment: CR&D

53

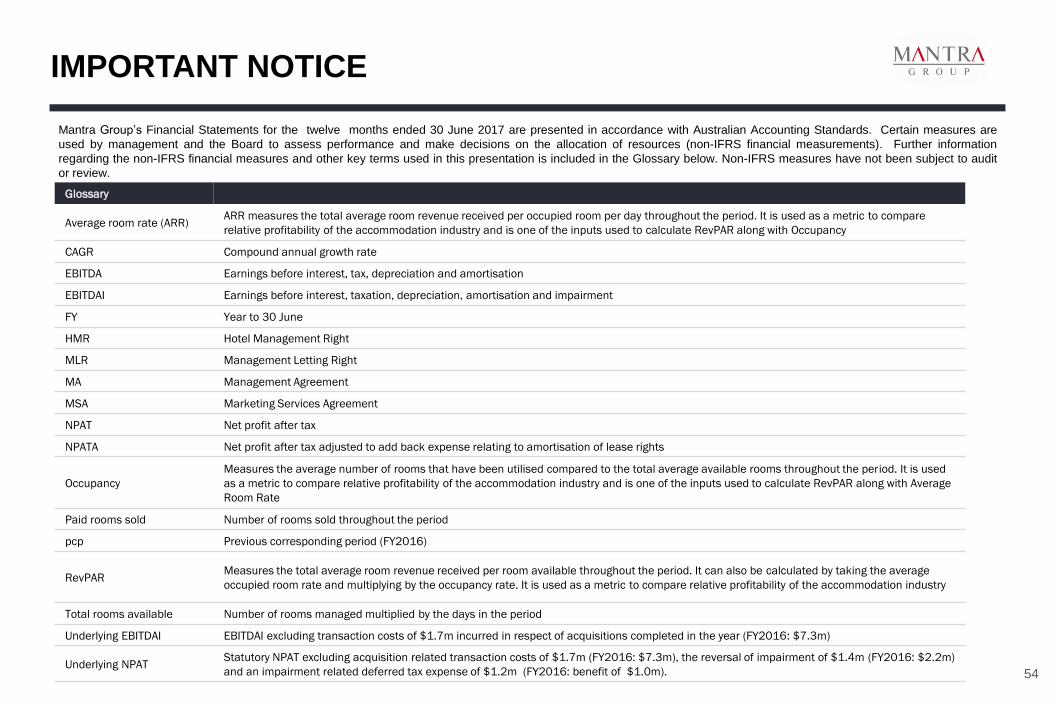

IMPORTANT NOTICE

Mantra Group’s Financial Statements for the twelve months ended 30 June 2017 are presented in accordance with Australian Accounting Standards. Certain measures are

used by management and the Board to assess performance and make decisions on the allocation of resources (non-IFRS financial measurements). Further information

regarding the non-IFRS financial measures and other key terms used in this presentation is included in the Glossary below. Non-IFRS measures have not been subject to audit

or review.

Glossary

Average room rate (ARR) ARR measures the total average room revenue received per occupied room per day throughout the period. It is used as a metric to compare

relative profitability of the accommodation industry and is one of the inputs used to calculate RevPAR along with Occupancy

CAGR Compound annual growth rate

EBITDA Earnings before interest, tax, depreciation and amortisation

EBITDAI Earnings before interest, taxation, depreciation, amortisation and impairment

FY Year to 30 June

HMR Hotel Management Right

MLR Management Letting Right

MA Management Agreement

MSA Marketing Services Agreement

NPAT Net profit after tax

NPATA Net profit after tax adjusted to add back expense relating to amortisation of lease rights

Occupancy

Measures the average number of rooms that have been utilised compared to the total average available rooms throughout the period. It is used

as a metric to compare relative profitability of the accommodation industry and is one of the inputs used to calculate RevPAR along with Average

Room Rate

Paid rooms sold Number of rooms sold throughout the period

pcp Previous corresponding period (FY2016)

RevPAR Measures the total average room revenue received per room available throughout the period. It can also be calculated by taking the average

occupied room rate and multiplying by the occupancy rate. It is used as a metric to compare relative profitability of the accommodation industry

Total rooms available Number of rooms managed multiplied by the days in the period

Underlying EBITDAI EBITDAI excluding transaction costs of $1.7m incurred in respect of acquisitions completed in the year (FY2016: $7.3m)

Underlying NPAT Statutory NPAT excluding acquisition related transaction costs of $1.7m (FY2016: $7.3m), the reversal of impairment of $1.4m (FY2016: $2.2m)

and an impairment related deferred tax expense of $1.2m (FY2016: benefit of $1.0m). 54