FY 2016 Financial Results Presentation

21

Dom Development S.A. 2016 Results Presentation 28 February 2017

-

Upload

dom-development-sa-investor-relations -

Category

Investor Relations

-

view

58 -

download

0

Transcript of FY 2016 Financial Results Presentation

Dom Development S.A.

2016 Results Presentation 28 February 2017

2016

• Net profit of PLN 125.7m (+56% YoY)

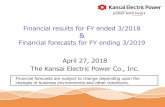

• Record-high sales of 2 735 units (+15% YoY)

and handovers of 2 482 units (+20% YoY)

• Average transaction value of PLN 512k in 2016 - a result of a shift up-market

• Net operating Cash Flow of PLN 265m

• High cash levels (PLN 437m) and no net debt as of 31.12.2016

2

Residential Market

• Strong sales with prices slightly increasing

• Supply and demand still balanced

• Record low interest rates support demand

• Increasing share of cash buyers – approx. 40% of overall

transactions at Dom Development

• High competition on land market

3

820

1 4681 801

1 4781 699

1 944

2 3832 735

0

500

1 000

1 500

2 000

2 500

2009 2010 2011 2012 2013 2014 2015 2016

Annual Net Sales

4

No. of units

Quarterly Net Sales

5

407

483509

545

467

598640

678

615

701 705 714

0

100

200

300

400

500

600

700

I kw. 2014 II kw. 2014 III kw. 2014 IV kw. 2014 I kw. 2015 II kw. 2015 III kw. 2015 IV kw. 2015 I kw. 2016 II kw. 2016 III kw. 2016 IV kw. 2016

No. of units

6

37% 30% 28% 25% 21%

32% 38%

37% 32%

23%

17% 16% 18%

22%

24%

14% 16% 18% 21% 32%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2012 2013 2014 2015 2016

up to PLN 350k 350-450k 450-550k over PLN 550k

Sales segmentation based on transaction value

* Transaction value includes price of a flat with fit-out (if purchased), storage room (if purchased) and parking place (if purchased).

1 621 1 555 1 545 1 679 2 022

1 696 2 104

219 242 496 261

312 557

402

-

500

1 000

1 500

2 000

2 500

31/12/2010 1 840

31/12/2011 1 797

31/12/2012 2 041

31/12/2013 1 940

31/12/2014 2 334

31/12/2015 2 253

31/12/2016 2 506

Units under construction Finished units

Dom’s Offer

7

As of 31/12/2016 Dom’s offer includes units in 15 Warsaw and 2 Wroclaw sites

No. of units

New construction starts

8

Liczba lokali

2 projekty 3 projekty 2 projekty 4 projekty 4 projekty 7 projektów 1 projekt 3 projekty

2 199

1 716 1 7211 892 1 960

2 403

Q1: 426

Q2:1 349

Q3: 557

Q4:555

0

500

1 000

1 500

2 000

2 500

3 000

2010 2011 2012 2013 2014 2015 2016

2016: 2 887 units in 19 projects

10 projects

10 projects

12 projects

11 projects

13 projects

12 projects

No. of units

Units under construction and in preparation

2 989 2 153

3 029 2 927 2 958 3 543

8 190

7 152 6 360

4 672

6 504 6 450

0

1 000

2 000

3 000

4 000

5 000

6 000

7 000

8 000

31/12/2011 31/12/2012 31/12/2013 31/12/2014 31/12/2015 31/12/2016

Under construction In preparation

9

No. of units

Handovers

10

Units sold but not delivered (presales)

31.12.2015 31.12.2016

1 427 units

1 680 units, including

• 241 finished units • 1 439 units under construction

707

1 313

2 0111 594

1 996 2 0622 482

0

500

1 000

1 500

2 000

2 500

2010 2011 2012 2013 2014 2015 2016

No. of units

11

Cumulative net sales to be recognized in P&L

PLN m

200

300

400

500

600

700

800

900

1 000

1 100

I II III IV V VI VII VIII IX X XI XII I II III IV V VI VII VIII IX X XI XII I II III IV V VI VII VIII IX X XI XII I II III IV V VI VII VIII IX X XI XII

2013 2014 2015 2016

Financial Results Summary

2016 2015 Change Q4 2016 Q4 2015 Change

Sales Revenues 1 153.0 904.2 28% 567.1 480.0 18%

Gross Profit on Sales 271.1 203.9 33% 141.8 110.1 29%

Gross Profit Margin 23.5% 22.6% 0.9 pp 25.0% 22.9% 2.1 pp

Operating Profit 156.6 102.5 53% 105.0 81.8 28%

Operating Profit Margin 13.6% 11.3% 2.3 pp 18.5% 17.0% 1.5 pp

Profit Before Tax 155.9 100.6 55% 105.5 81.8 29%

Net Profit 125.7 80.8 56% 85.3 66.1 29%

EPS (PLN) 5.07 3.26 56% 3.44 2.67 29%

12 IAS 18, PLN m

Balance Sheet and Profitability

13

Consolidated Balance Sheet IAS 18, PLN m 31.12.2016 31.12.2015 Change

Shareholders’ funds (equity) 929.5 883.4 5%

Net debt* (57.1) 144.6 (139)%

Gearing (net debt/equity) (6.1)% 16.4% (22.5) pp

Net asset value per share (PLN) 37.50 35.66 5%

Shares in issue (m) 24.8 24.8 -

ROE 14.2% 9.4% 4.8 pp

ROCE 13.2% 8.2% 5.0 pp

*Bank debt plus bonds in issue less cash at banks (including escrow accounts)

Dividends

14

0,15

2,04

0,80 0,80 0,90 1,50

3,68

2,20 2,25

3,25

5,05*

0,1%

3,3%

2,1% 1,5%

1,9%

4,9%

8,5%

4,4% 4,5%

6,3%

0,0%

1,0%

2,0%

3,0%

4,0%

5,0%

6,0%

7,0%

8,0%

9,0%

0,00

1,00

2,00

3,00

4,00

5,00

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

3% 25% 14% 23% 56% 45% 100% 100% 100% 100% 100%

Dividend Yield

*Managment Board’s Recommendation % of net profit

According to the Dividend Policy in place from 3 April 2013, the Company pays as dividends 100% of its consolidated net profit, starting

with the net profit for the year 2012. The Management Board plans to maintain this dividend policy even if the acquisition of the Euro

Styl Capital Group housing business takes place.

Dividend per share (PLN)

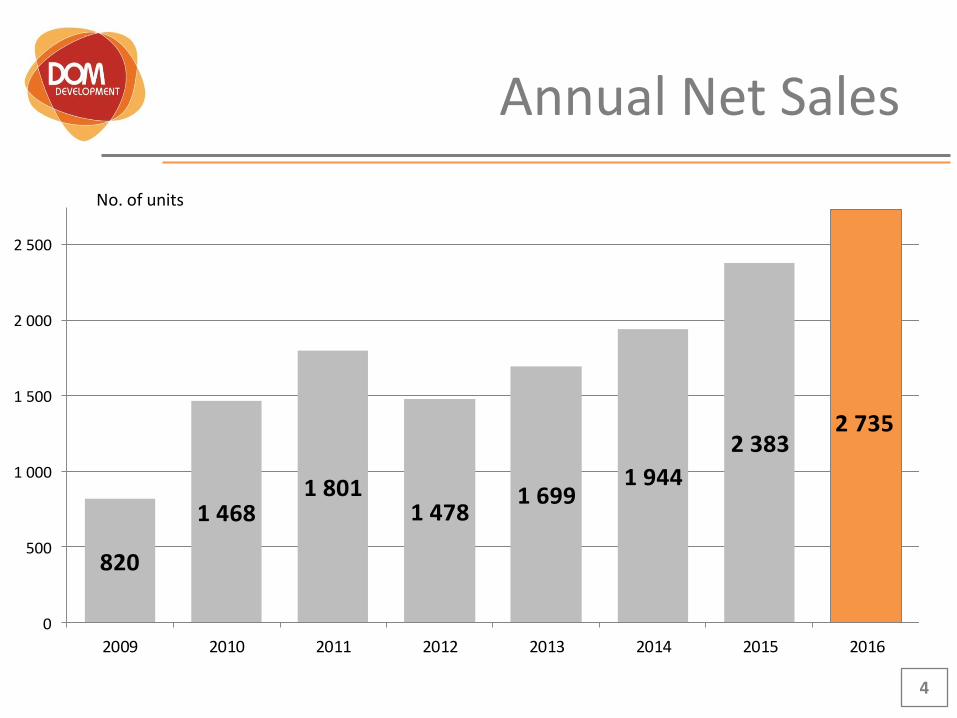

Debt Maturity Structure

15

120

50

100 110

0

20

40

60

80

100

120

140

by 31.12.2017 by 31.12.2018 by 31.12.2019 by 31.12.2020 by 31.12.2021

Unsecured Bonds Bank Loans

PLN m

Cash as of 31/12/2016 – PLN 437m

2016

16

Summary:

Net profit of PLN 125.7m (+56% YoY)

Record-high sales of 2 735 units (+15% YoY) and handovers of 2 482 units (+20% YoY)

Commencement of 19 new projects with 2 887 units

Record-high number of locations in the offer (Warsaw - 15, Wroclaw - 2)

Land bank diversification by project location, scale and segment

Cooperation with the best general contractors – all 12 project completions planned for

2016 were on time or ahead of schedule

Strong balance sheet - PLN 437m of cash and no net debt

Consistent dividend policy – recommendation of 100% of the net profit payment for the

fifth consecutive time

Appendices

18

NO PROJECT UNDER

CONTRUCTION

IN PREPARATIO

N

1 ŻOLIBORZ ARTYSTYCZNY 403 ---

2 PREMIUM 576 361

3 OS. PRZYJACIÓŁ 95 ---

4 WŁODARZEWSKA 30 (NOWOSOLIPSOWSKA)

123 ---

5 OS. POD RÓŻAMI III 50 ---

6 PRZY PARKU --- 46

7 MARINA MOKOTÓW --- 731

8 APARTAMENTY MOKOTÓW NAD SKARPĄ (BUKOWIŃSKA II)

184 ---

9 BUKOWIŃSKA III --- 190

10 CYBERNETYKI --- 633

11 TANECZNA 119 ---

12 URSYNOVIA (ANODY) 190 ---

13 SOBIESKIEGO --- 153

TOTAL LEFT BANK 1 740 2 114

NO PROJECT UNDER

CONTRUCTION IN

PREPARATION

14 REGATY --- 217

15 PALLADIUM (AKACJE) 214 566

16 KLASYKÓW 204 ---

17 KOWALCZYKA --- 792

18 MODERNA 554 184

19 AMSTERDAM (SAMARYTANKA)

60 514

20 WILNO 240 1 556

21 FORMA (MOTOROWA)

--- 507

22 SASKA III 359 ---

TOTAL RIGHT BANK 1 631 4 336

Warsaw

TOTAL UNDER

CONSTRUCTION IN PREPARATION FINISHED

WARSAW 3 371 6 450 26 176

WROCŁAW (AURA PROJCET)

172 --- 721

DOM 3 543 6 450 26 897

1 2

4 5

12

9

15 16

22

14

17 18

20

21

7 6

13

11

3

10 8

19

Appendix 1:

Projects Under Construction and in Preparation no. of units, as of 31/12/2016

PROJECT IN PREPARATION

PROJECT UNDER CONSTRUCTION

19

Project No. of units in project Commencement of handovers

Q2

Moderna etap 1 171 May 2017

Premium etap 1 206 May2017

Apartamenty Mokotów nad Skarpą 184 June 2017

Q3 Osiedle Przyjaciół etap 3 95 August 2017

Palladium etap 1 214 September 2017

Q4

Premium etap 2 236 October 2017

Ursynovia etap 1 79 October 2017

Ursynovia etap 2 111 October 2017

Moderna etap 2 194 November 2017

Osiedle Pod Różami etap 3 50 November 2017

Saska III 359 November 2017

Żoliborz Artystyczny etap 5 126 November 2017

Żoliborz Artystyczny etap 6 137 November 2017

Żoliborz Artystyczny etap 7 140 November 2017

Wille Taneczna 119 December 2017

Wilno III etap 2 129 December 2017

Wilno III etap 3 111 December 2017

Appendix 2:

Commencement of handovers in 2017

5 January 2017 – Dom Development S.A. obtained an exclusivity until 30 June 2017 to conduct negotiations concerning the purchase of the housing development segment of the Euro Styl Capital Group

Euro Styl is one of the Tri-City market leaders

20

661 units sold in 2016 (+24% YoY)

527 unit offer as of 31.12.2016

1 800 unit land bank as of 31.12.2016

10 years in housing development

3 803 units sold to date

Appendix 3:

Tri-City expansion plans

21

For further information, please contact: Magdalena Cumanis Investor Relations

tel. +48 22 351 68 49 e-mail: [email protected] www.inwestor.domd.pl

Dom Development S.A. endeavours to ensure that the information in the presentation is complete. up-to-date and accurate. However. we do not make any guarantees in this respect. Dom Development S.A. connot accept responsibilty for the consequences of using such information. and in particular any loss caused by reliance thereon for the purpose of investment decisions. The material contained in the presentation originates from reliable public sources and to the best knowledge of Dom Development S.A. may be considered reliable.