FY 2010 results EN - Safran · FY 2010 Earnings - February 24, 2011 2 Safran FY 2010 Highlights...

54

February 24, 2011 Full-Year 2010 Earnings Jean-Paul HERTEMAN CEO Ross McINNES CFO Safran

Transcript of FY 2010 results EN - Safran · FY 2010 Earnings - February 24, 2011 2 Safran FY 2010 Highlights...

February 24, 2011

Full-Year 2010 Earnings

Jean-Paul HERTEMANCEO

Ross McINNESCFO

Safran

FY 2010 Earnings - February 24, 2011

2

Safran

FY 2010 Highlights

Jean-Paul HERTEMANCEO

FY 2010 Earnings - February 24, 2011

3

FY 2010 financial highlightsSolid operating leverage

Growing revenue with strongperformance in Defence and Security

FY 09 FY 10

10,448 10,760+3.0%

Recurring operating income at 8.2% of revenue highlighting good control

of cost base

FY 10

729878+20%

Higher net profit (group share) at €1.27 per share

FY 09restated

FY 10

395508+29%

Net cash positive. Driven by better-than-expected WC

and very strong operating CFFY 09 FY 10

(498)

24

+€522 M

Proposed 2010 dividend up 32% vs. 2009

FY 09 FY 10

0.38

0.50+32%

(€M) (€M) (€M)

(€)

(€M)

FY 09restated

FY 2010 Earnings - February 24, 2011

4

Key strategic business achievementsSuccessful launch of LEAP-X

Selected by COMAC C919 for an integrated powerplant (LEAP-X engine, nacelle, thrust

reverser and pylon)

CFM LEAP-X selected on A320neo and Safran selected for the nacelle of CFM-

powered A320neo

First 100 C919 orders (Hainan Airlines, China Eastern, China

Southern, GECAS, CDB Leasing)

Already 180 A320neo orders (Virgin, Indigo); engines yet to be awarded

LEAP-X

FY 2010 Earnings - February 24, 2011

5

Introducing a new advanced engine: LEAP-X

Provides superior performance vs. latest upgrade of CFM56Burn 15% less fuelProduce 15% less CO2 emissionProduce 50% less NOxReduce noise by up to 15 EPNdB (Effective Perceived Noise)

Market potential for re-engined variant: 18,000 engines4,000 A320neo aircraft2,000 C919 aircraft3,000 B737 aircraft

R&D investment for LEAP-X (incl. the nacelle)Total cash R&D of c.€1bn (Safran’s share for 2011-2016)

LEAP-XA new baseline turbofan engine to power future replacements

for current narrow-body aircraft

EIS in 2016

The successor of CFM56

FY 2010 Earnings - February 24, 2011

6

Key strategic business achievementsEmerging stronger from 2010

Acquiring new businesses in core businesses

Winning key contracts

Pending government approvals

1,175 long-range IR goggles order for French Army

Supply of full fuselage wiring system on A380 for the whole life

of the program

Team-up with COMAC to provide C919 wiring

systems

7-year contract for ID documents (electronic passports and national identity cards) for the Netherlands

Issued the 12-digit unique ID numbers for 1.5 million residents

in India

SuperJet100 now certified in Russia. Significant orders

from Interjet

FY 2010 Earnings - February 24, 2011

7

(1)%

(20)%

(12)%

22%

(2)%

1,251

830

74

127

313

1,263

1,032

84

104

321

Number of deliveries

1. CFM56 engines

2. Helicopter engines

3. A380 nacelles

4. A330 nacelles

5. Small nacelles (biz & regional jets)

Aerospace OE

20,858

58%

FY 2010

5.2%

+5pts

19,823

53%

Total installed base

Share of 2nd gen. engines

ChangeFY 2009CFM56 engines

(0.6)%4,7424,771 OE revenue* Prop. & Equipment (in €M)

Increased share of 2nd generation CFM engines in fleet

future flow of high value services

1,583 new orders (2x vs. 2009)

1. Stable CFM56 deliveries

2. Decline in small helicopters

3. Inventory build-up at end 2009 due to A380 deliveries delay

4. Continued growth on A330

5. Stabilization in business & regional jets

* Including revenue from R&D contracts and miscellaneous

CFM workhorse continued at top rates; 1,583 new orders

FY 2010 Earnings - February 24, 2011

8

Propulsion

CFM spares’ trends improving sequentially: Q4 > Q3 > Q2.FY2010: -17% in $Q4 2010: flat in $ yoy

Good performance of services to military customers although growth slowing down in H2

2-digit growth in high thrust widebodyengine spares (e.g. GE90 on B777)

Equipment

Increased civil MRO activity but lower spares business

* Including spares and maintenance & repair activities

Aerospace services

0.7%3,6963,669Total services revenue

0.7%(0.5)pt

88731.3%

88131.8%

Aircraft EquipmentServices share of total revenue

2,80950.1%

FY 2010

0.8%0.9pt

2,78849.2%

Aerospace PropulsionServices share of total revenue

ChangeFY 2009

Services* revenue(in €M)

Resilient total services revenue

FY 2010 Earnings - February 24, 2011

9

Over 5-year backlog to date in CFM OEM (6,263 engines)9,500 engines yet to have their first shop visit

The aftermarket recovery has begun Outstanding fleet of CFM56 engines

CFM engines

0

5 000

10 000

15 000

20 000

82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11E

(Nom

bre

de m

oteu

rs C

FM)

20,000

15,000

10,000

5,000

0

Global CFM56 spare parts revenueBasis 100 - 9/11/2001Basis 100 - Sept. 2008

2009 2010 2011

60708090100110120130140

2002 2003 2004

After Lehman

After 9/11

FY 2010 Earnings - February 24, 2011

10

Organic and acquisition-driven growth Fast-paced development of Security

0

200

400

600

800

1000

1200

2007 2008 2009 2010

Revenue from acquisitions (Printrak, GE HLP)Restated revenue at 2008 perimeter (excluding Monetel activity) and excluding contract in Ivory Coast

Average reported growthCAGR2007-10 = ~21%

Average organic growth CAGR2007-10 = ~15%

Revenue (€M) - Security

1,041

904

695

481

FY 2010 Earnings - February 24, 2011

11

Optronics: continued growth driven by soldier protection & supported by order backlog (€1.2bn+)

Strong dynamics on export marketsSignificant contracts notified by DGA for the supply of 16,454 Felin systems and 1,175 new-generation long-range infrared binoculars (JIM LR2)

AvionicsContract notified by DGA at end-2009 for the supply of 3,400 AASM modularair-to-ground weapons Continued Research and Technology DGA funds for strategic navigation activitiesSuccess on export markets not limited to Rafale export sales

Safran focused on resilient defence niches

FY 2010 Earnings - February 24, 2011

12

Investing for the futureA gradual approach for a long term vision

€2Bn+ - Targeted acquisitions in core markets

€300M+ - Investing in world class industrial facilities

HLP

Massy - June 2010

Bordes - June 2010

Queretaro - March 2010

(pending govtapproval)

Aerospace Propulsion Aircraft Equipment

(pending govtapproval)

Security

World class excellence centre in Europe

Growing low cost & $ basis

Bidos - Sept. 2010

« Grand Emprunt » projects – Epice*, Ariane 6, TM800…

* Advanced civil aero-engine demonstrator, called Epice

FY 2010 Earnings - February 24, 2011

13

Our M&A strategy pays off - successful, selective Proven track record

HLP

Recent acquisitions

Renewed a 7-year contract for ID documents for the Netherlands

Provider of fingerprinting technology for FBI’s Next generation ID program

Rationalisation

Reinforce our position in US aircraft and helicopters wiring systems (military & commercial)

Solid order intake in Explosive Detection Systems (TSA, Israel…)

XRD3500 system compliant with European ECAC Standard 3

Unmatched positions in North America with long-term contracts

Now fully integrated into ID business

Delivered 16% EBIT margin in 2010

Stable, strategic asset for France. Excellent long term visibility

Expected to deliver 15% EBIT margin in 2011

Delivered 22% EBIT margin in 2010

Expected run-rate cost synergies of appx. $30M (within 18 months after the closing)

Commercial success Delivering results

Value potential

+ to ++

+++

Transactions pending regulatory approvals

FY 2010 Earnings - February 24, 2011

14

Enhancing productivityContinued & lasting savings

Split of Safran+ gains by action in 2010

Optimize the supply chainSupporting suppliers switch to dollar and emerging zonesManaging the price rise in commodities (e.g. Nickel)World class new or revamped facilities

Lean manufacturing and improved productivityAcceleration of lean actions to reduce production costsEnhancing worker autonomy & involvement

Reduction of overhead expensesPooling of Purchasing teamsPooling of HR processes (e.g. payroll, hiring)

Improve marketing and accelerate services growthDynamic action plan to sell higher added-value & spares sales despite of the crisis

Reduction of structural cost

Sell better and accelerateservices growth

Lean manufacturing and product development

Optimize the Supply-Chain

Cost reduction

25%

16%

15%

44%

FY 2010 Earnings - February 24, 2011

15

Safran

Full-Year 2010 Results

Ross McINNESCFO

FY 2010 Earnings - February 24, 2011

16

All figures in this presentation represent Adjusted data (see “Additional Information” for bridge with consolidated accounts)

Safran’s consolidated income statement has been adjusted for the impact of:

purchase price allocations with respect to material business combinations. Since 2005, this restatement concerns the amortization charged against intangible assets relating to aeronautical programs that were revalued at the time of the Sagem-Snecma merger. With effect from the first-half 2010 interim financial statements, the Group has decided to restate the impact of purchase price allocations for all material business combinations (and not only those relating to the Sagem-Snecma merger). In particular, this concerns the amortization of intangible assets recognized at the time of the acquisition, and amortized over extended periods, justified by the length of the Group's business cycles;

the mark-to-market of foreign currency derivatives, in order to better reflect the economic substance of the Group's overall foreign currency risk hedging strategy:

revenue net of purchases denominated in foreign currencies is measured using the effective hedging rate, i.e., including the costs of the hedging strategy,the recognition of all mark-to-market changes on non-settled hedging instruments at the closing date is neutralized, including the “ineffective” portion with effect from the publication of the 2009 financial statements, given that the Group's hedging strategy includes optional hedging instruments and optimization measures combined with highly volatile market inputs used to mark to market.

Recurring operating incomeIt excludes income and expenses which are largely unpredictable because of their unusual, infrequent and/or material nature such as: impairment losses/reversals, capital gains/losses on disposals of operations and other unusual and/or material non operational items).

ForewordDefinitions

FY 2010 Earnings - February 24, 2011

17

FY 2009 restated income statement

3-3Share in profit from associates

69431663Profit from operations

0.990.94EPS (in €)39519376Net income – group share

(16)(2)(14)Minority interests(4)-(4)Profit (loss) from discontinued op.

(108)(10)(98)Income tax expense(174)-(174)Net financial income (expense)

6.6%6.3%% of revenues

(35)(35)Other non-current charges/income

7.0%6.7%% of revenues72931698Recurring operating income

10,44810,448Revenue

(i)(in Euro million)

FY 2009 restated

PPAFY 2009 reported

Income Statement

Full-year 2009 adjusted results which shall serve as a basis of comparison have been restated for:(i) Purchase price allocation entries impacts for major acquisitions (especially in the Security business).

FY 2010 Earnings - February 24, 2011

18

Fx volatility

Continued Fx volatility during FY 2010

Translation effect: foreign currencies translated into €⇒ Strong positive impact from $, AUD, BRL and CAD⇒ Impact on Revenue and Return on Sales

Transaction effect: mismatch between $ sales and € costs is hedged⇒ Mild negative impact from $ ⇒ Positive impact from other currencies ($/CAD, $/GBP)⇒ Impact on Profits

Mark-to-market effect⇒ €(275)M on fair value of financial instruments⇒ Impact on consolidated “statutory” accounts

Diverse impacts on P&L

Hedge rate

$ 1.44$ 1.42FY 2010FY2009

Average spot rate

$ 1.33$ 1.39FY 2010FY 2009

Spot rate

$ 1.34$ 1.44Dec. 31, 2010Dec 31, 2009

FY 2010 Earnings - February 24, 2011

19

Consolidated and adjusted income statements

PPA impacts -other business combinations

Amortization of intangible assets -

Sagem/Snecma

102

(3)

105

(54)

159

159

159

87843(15)(260)951Recurring operating income

(13)(13)Other non current operating income / expense

508251704207Parent

(20)(3)4(18)Minority interests

(5)(5)Profit (loss) from discontinuing operations

53328170230Profit (loss) from continuing operations

(173)(15)(90)(14)Income tax expense

99Income from associates

(168)275260(703)Net finance costs / income(136)(136)Other finance costs /income

4275260(531)Foreign exchange financial income (loss)

(36)(36)Cost of debt

86543(15)(260)938Profit (loss) from operations

(9,882)43(15)8(10,077)Other operating income / expense

10,760(268)11,028Revenue

Deferred hedging

gain (loss)

Re-measurement

of revenue

Adjusted consolidated

income statement

Business combinationsHedge accountingConsolidated

income statement

(In €M)

2010 reconciliation

FY 2010 Earnings - February 24, 2011

20

FY 2010 profit from operations

8658.0%

6946.6%

Profit from operations% of revenue

--

(13)

7(70)

28

Capital gain (loss) on disposalsImpairment reversal (charge)Other infrequent & material non operational items

(13)(35)Total one-off items

8788.2%

7297.0%

Recurring operating income% of revenue

10,76010,448Revenue

FY 2010FY 2009restated (In €M)

Recurring operating income: €878M in FY 2010 (8.2% of revenue)

M&A transaction costs (L-1 Identity Solutions, HCM,

SME, …)

FY 2010 Earnings - February 24, 2011

21

FY 2010 income statement

Of which cost of net debt of €(36)M

3760.94

(174)(98)

(4)(14)

3

6636.3%

6986.7%

10,448

FY 2009reported

5081.27

3950.99

Profit - group shareBasic EPS* (in €)

(168)(173)

(5)(20)

9

(174)(108)

(4)(16)

3

Net finance (cost) incomeIncome tax expenseProfit (loss) from discontinued op.Minority interestsShare in profit from associates

8658.0%

6946.6%

Profit from operations% of revenue

8788.2%

7297.0%

Recurring operating income% of revenue

10,76010,448Revenue

FY 2010FY 2009restated(In €M)

EPS growth of 28%

* Based on 399,552,920 shares

Effective tax rate of 25%

FY 2010 Earnings - February 24, 2011

22

FY 2010 revenue

Defence (optronics) and Security (detection) up

Mild decline in OE aerospace with resilient services

Favourable currency impact

Translation: positive impact $, AUD, BRL, CAD

Transaction: negative impact of $ ($1.44 in 2010 vs. $1.42 in 2009)

Changes in the scope of consolidation include:

8 months of MorphoDetection (GE HLP): €133M

3 months of MorphoTrak(Printrak): €8M

FY 2010Currency impact

FY 2010at constant FY 2009 perimeter

Acquisitions & activities newly consolidated

FY 2009

(In €M)

10,44810,344

10,563

(1.0)%organic

Organic variation

FY 2010 at constant

FY 2009 perimeter and exchange rate

(104)219

197

3.0% increase

+3.0%

10,760

FY 2010 Earnings - February 24, 2011

23

FY 2010 recurring operating income

Improved profitability driven by:

OE CFM unit revenue

Aftermarket (military, helicopters, high-thrust engines)

Lower production costs on nacelles

External growth in Security

Safran+ productivity improvements and costs efficiency

Lower R&D impact

Recurring operating margin improved by 1.2 point

FY 2010Currency impact

FY 2010at constant FY 2009 perimeter

Acquisitions & activities newly consolidated

FY 2009restated

(In €M)

729

879 854

+21%organic

Organic variation

FY 2010 at constant

FY 2009 perimeter and exchange rate

878150 (25) 24

7.0%RoS

8.2%RoS

+20%

FY 2010 Earnings - February 24, 2011

24

(3)179182Capitalized expenses

(50)458508Recorded as operating expenses

(0.7)pt5.9%6.6%% of revenue

(7.7)%637690Total self-funded R&D(before tax credit*)

ChangeFY 2010FY 2009(In €M)

(159)406565Ebit impact after R&D tax credit *

(133)530663Ebit impact before R&D tax credit *

(83)72155Amortisation / depreciation

(50)458508Recorded as operating expenses

ChangeFY 2010FY 2009(In €M)

Research & Development

R&D effort maintained with normative trend at 6 to 7% of revenue

Tailing off of R&D developmentson SJ100, A400M and B787

Increasing R&D developments on LEAP-X engine as well as A350 program

Tax credit* impact of €124M in 2010vs. €98M in 2009

* “Crédit Impôt Recherche” in France & Canada

R&D effort maintained, lower impact on EBIT

Of which €71M impairment charge on B787 in 2009

FY 2010 Earnings - February 24, 2011

25

Aerospace Propulsion

Mild decline in revenue

Growth in services for military, helicopters & high trust engines

Lower OE deliveries (military, helicopters, high trust engines)

Soft but improving CFM aftermarket

Growing profits despite CFM aftermarket softness

Aftermarket (military, high trust engines)

Impact of better OE CFM unit revenue

Productivity improvements

Slight adverse currency effect

R&D: tailing off of SaM146 and TP400; increasing efforts on LEAP-X

102145Capex (tangible assets)

9884Capitalized expenses

233252Recorded as opex

5.9%5.9%% of revenue

331336Total self-funded R&Dbefore tax credit

FY 2010FY 2009(In €M)

-29One-off items

+0.7pt11.8%11.1%% of revenue

5.6%663628Recurring operating income

11.8%

663

5,604

FY 2010

(1.2)%

Change

(3.1)%5,673Revenue

11.6%% of revenue

657Profit (loss) from op.

Organic Change

FY 2009restated(In €M)

Key figures

FY 2010 Earnings - February 24, 2011

26

Aircraft Equipment

Revenue back to growth

Driven by new programs (B787) and stabilization in business and regional jets segment

Offset by lower nacelle activity

1-month consolidation of HCM

Recovery plan delivering results

Drastic reduction of losses in nacelles (reached operating breakeven in Q4 2010)

A 380 : lower volumes, improved production costs, commercial agreement with Airbus

B 787 : higher volumes, commercial agreement with Boeing

Repair & Overhaul on landing systems

6186Capex (tangible assets)

4565Capitalized expenses

6780Recorded as opex

4.0%5.2%% of revenue

112145Total self-funded R&Dbefore tax credit

FY 2010FY 2009(In €M)

(2) (71)One-off items

+1.9pt4.5%2.6%% of revenue

74%12773Recurring operating income

4.4%

125

2,834

FY 2010

2.4%

Change

Flat2,767Revenue

ns% of revenue

2Profit (loss) from op.

Organic Change

FY 2009restated(In €M)

Key figures

FY 2010 Earnings - February 24, 2011

27

Defence

Over 30% growth in Optronics with a favourable volume/price impact on profits

Felin, long-range IR goggles, thermal cameras, …

Avionics: mild decline in revenue, impacting profits in flight control systems

Further incremental costs to put in place Safran Electronics

6735Capex (tangible assets)

1833Capitalized expenses

91113Recorded as opex

8.8%13.8%% of revenue

109146Total self-funded R&Dbefore tax credit

FY 2010FY 2009(In €M)

--One-off items

+3.6pts4.4%0.8%% of revenue

511%559Recurring operating income

4.4%

55

1,240

FY 2010

16.9%

Change

12.4%1,061Revenue

0.8%% of revenue

9Profit (loss) from op.

Organic Change

FY 2009restated(In €M)

Key figures

Of which €(35)M loss at completion on A400M

navigation systems in 2009

FY 2010 Earnings - February 24, 2011

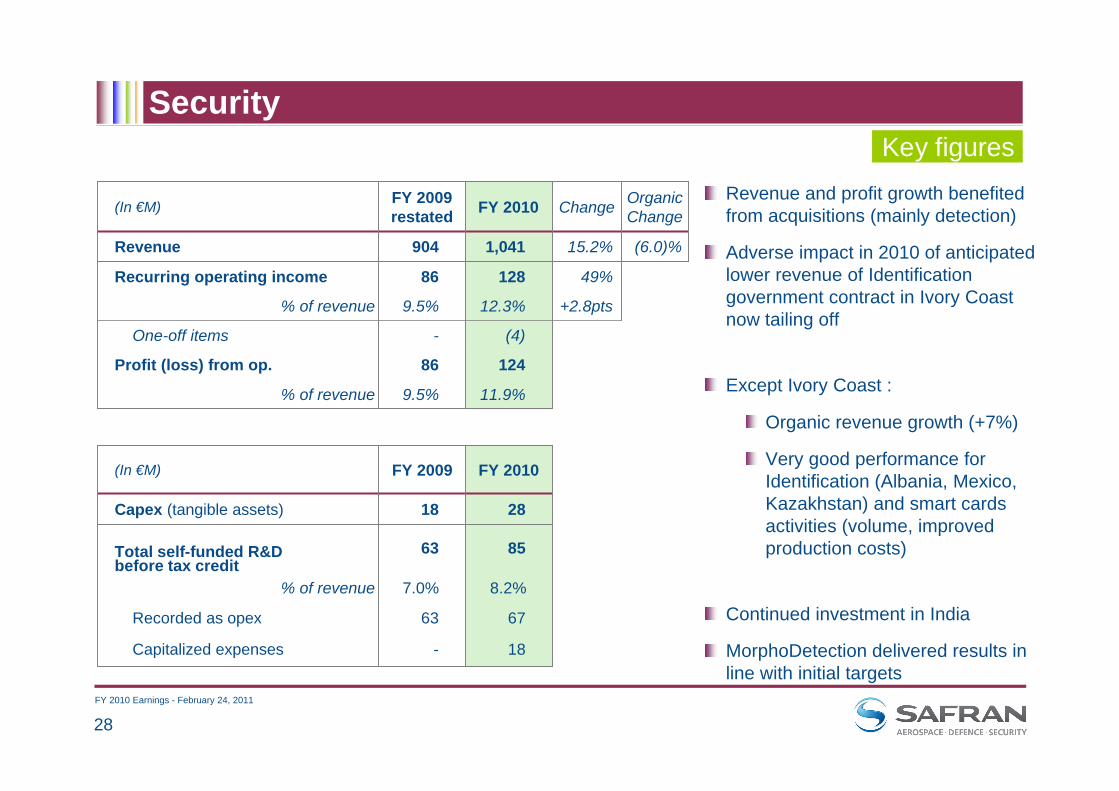

28

(4) -One-off items

+2.8pts12.3%9.5%% of revenue

49%12886Recurring operating income

11.9%

124

1,041

FY 2010

15.2%

Change

(6.0)%904Revenue

9.5%% of revenue

86Profit (loss) from op.

Organic Change

FY 2009restated(In €M)

Security

Revenue and profit growth benefited from acquisitions (mainly detection)

Adverse impact in 2010 of anticipated lower revenue of Identification government contract in Ivory Coast now tailing off

Except Ivory Coast :

Organic revenue growth (+7%)

Very good performance for Identification (Albania, Mexico, Kazakhstan) and smart cards activities (volume, improved production costs)

Continued investment in India

MorphoDetection delivered results in line with initial targets

2818Capex (tangible assets)

18-Capitalized expenses

6763Recorded as opex

8.2%7.0%% of revenue

8563Total self-funded R&Dbefore tax credit

FY 2010FY 2009(In €M)

Key figures

FY 2010 Earnings - February 24, 2011

29

3-year hedging policy

Hedge portfolio, Feb 18, 2011

1.34

1.34

1.29

1.28

1.30

1.30

1.39

1.38

1.441.42Achieved

Target

Estimated exposure needsIn US$ bn

Hedge rates locked-in for 2011 to 2013

2012: $3.6bn achieved at $1.34 to rise to $4.6bn at $1.34as long as €/$<1.65 for most of 2011

2013: $3.6bn achieved at $1.30 to rise to $4.6bn at $1.30 as long as €/$<1.52 for most of 2011

2014 hedging well advanced

$1.3bn achieved at $1.29 to rise to $2.9bn at $1.25 as long as €/$<1.52 for most of 2011 and 2012

€/$ hedge rate

Portfolio optimized by another 4 cents over 2011-2014

Total: $12.8bn

1.3

3.7 3.7

~ 4.7 ~ 4.7

2.9

4.54.0

4.3

0

1

2

3

4

5

2009 2010 2011 2012 2013 2014

~4.7

FY 2010 Earnings - February 24, 2011

30

-100

-50

0

50

100

150

200

250

300

350

400

3-year hedging policy

An estimated cumulative €400M tailwind in EBIT over the next 4 years

Currency impact on profitability is around 2/3rd in Propulsion and 1/3rd in Equipment; non material for Defence and Security businesses

Estimated impact on recurring operating incomeof targeted €/$ hedge rates

Material tailwind in profitability expected over 2011-2014

102134

(44)

75

1.42

1.44

1.38

1.30

2009 2011E 2012E

1.34

2013E 2014E

108

1.28

2010

200

100

0

-100

EBIT impactvs. previousyear (in €M)

1.2

1.3

1.4

1.1

1.35

1.25

1.15

1.05

1

€/$hedge

rate

300

56

FY 2010 Earnings - February 24, 2011

31

Free Cash Flow

Excellent FCF generation

Strong cash receivables collection (including from the French MoD)

Tight control of capex

One-off cash impact

Commercial settlements with airframers

French Government stimulus package accelerated some tax credits

934818Free cash flow

(254)(292)Capex (intangible assets)

(271)(293)Capex (tangibles assets)

317361Change in Working capital

1,1421,042Cash from operating activities

5(1)Elimination of discontinued operations

16772Others

462576Depreciation, amortization and provisions

508395Adjusted net profit (loss)

FY 2010FY 2009 restated(in €M, at Dec. 31)

Cash from operations greater than recurring operating income

FY 2010 Earnings - February 24, 2011

32

(in €M)

(498)

317

Dividend

1,142(251)

Net cash position

Cash flow from operations is 1.30x EBIT

Dividend to parent holders was €152M (€0.38 per share)

€100M cash-out for the HCM acquisition

Net debt at Dec 31, 2009

Cash flowfrom ops

Others

Net cash at Dec 31, 2010

Change in WC

Tangible & Intangible

Capex

€934M Free Cash Flow

(161)

24

Preserving our financial flexibility

(525)

o/w €(100)M HCM acquisition

FY 2010 Earnings - February 24, 2011

33

Gross cash & debt

Credit line - €800M, undrawn, maturity Jan. 2012; no covenants

Credit line - €1,600M, undrawn, maturity Dec. 2015; subject to 1 covenant (net debt/EBITDA <2.5)

EIB loan (€300M) has been fully drawnMaturity 2020; subject to 2 covenants (net debt/EBITDA <2.5 and Gearing <1)

Available financing resources:Committed & undrawn = €2.4bn

Gross debt repayment schedule(Dec 31 , 2010)

301

568

1,182

<1 year 1 to 5 years >5 years

€1,250m

€1,000m

€750m

€500m

€250m

€0m

<1 year

The Group is adequately funded

FY 2010 Earnings - February 24, 2011

34

Balance sheet highlights

2,2985,383

657843

24

2,1265,418

722965

(498)

GoodwillTangible & Intangible assetsOther non current assetsOperating Working CapitalNet cash (debt)

4,530175

1,5722,424

504

4,353148

1,7392,354

139

Shareholders’ equity - Group shareMinority interestsNon current liabilities (excl. Net cash/debt)ProvisionsOther current liabilities / (assets) net

Dec. 31, 2010

Dec. 31, 2009(In €M) Shareholders’ equity up

by €177M

Net cash position further to a €0.5bn improvement

OWC decreased by €122M at €843M (7.8% of revenue)

Provisions remained stable

Solid balance sheet

FY 2010 Earnings - February 24, 2011

35

Customer financial guarantees

62110Provisions

66117Net exposure on these guarantees

61120Estimated value of pledges

127237Total guarantees

Dec. 31,2010

Dec. 31,2009(In $M)

Further decrease of total guarantees

Marginal Safran outstanding risk on Aircraft financing, representing less than 1% of Safran revenue on an annual basis

Further decrease of total guarantees reflecting a low level of request for manufacturers financing support

Outstanding risk of the portfolio covered by the conservative estimated value of the assets securing the financing and the provisions booked in Safran account

FY 2010 Earnings - February 24, 2011

36

2010 dividend

A proposal for a dividend payment of €0.50 at next Annual General Meeting on April 21, 2011

Approximately €200M cash disbursement in 2011

Ex-dividend date: April 26, 2011

Payment date: from April 29, 2011

Dividend per share(€)

Dividend distribution

(€M)167

104152

0.40

0.25

0.38

2007 2008 2009

0.50

c.200

2010

Highest dividend ever

FY 2010 Earnings - February 24, 2011

37

Safran

Outlook

Jean-Paul HERTEMANCEO

FY 2010 Earnings - February 24, 2011

38

As of Dec. 31, 2009

French State30.2%

Areva7.4%

Public38.1%

Treasury shares

4.2% Employees20.1%

Equity shareholdingFree float increased by 9.5 points in 2010

As of Dec. 31, 2010

French State30.2%

Areva2.0%

Public47.6%

Treasuryshares4.2%

Employees*16.0%

(*) of which 80% are available for sale

FY 2010 Earnings - February 24, 2011

39

Sustained traffic growth from 2010 and pickup in OE build rates for 2010/13

Aerospace fundamentals strengtheningThe civil aerospace recovery has breadth, strength and duration

Aircraft deliveries 2009-2013E

Short-medium range aircraft (A320, B737)CAGR 2010-13E = 3%

Long range aircraft (A330/340/350/380, B777/747…)CAGR 2010-13E = 12%

Commercial aviation passenger traffic (2000-2013E)

0

100

200

300

400

500

600

700

800

900

1000

2009 2010 2011E 2012E 2013E

RPK

(bill

ions

)#

airc

raft

Revenue Passenger per KilometreCAGR 2010-13E = 4.9%

2008 crisis severe enough to impact long term traffic (2 years of growth lost) but finally less severe than the 2001-03 period (almost 3 years of growth lost)

3000

3500

4000

4500

5000

5500

6000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011E 2012E 2013E

Opportunities for SafranExisting product base

and new programs

FY 2010 Earnings - February 24, 2011

40

2011 key assumptions

Civil aerospace aftermarket up 10-15%

Healthy rise in aerospace OE deliveries

Short term cautiousness specific to A380 and B787 programs

Increased R&D effort

• Includes spares and MRO• Driven by CFM and high-thrust engines

• Driven by A320, B737, B777, business andregional jets

• Aircraft equipment business linked to production & delivery rates

• Net impact of €50M+ on P&L and €200M+ in cash, notably for LEAP-X development

Growth in civil aerospace aftermarket and OE

FY 2010 Earnings - February 24, 2011

41

2011 outlook

Note: 2011 outlook does not include any contribution from L-1 Identity Solutions and SNPE Matériaux Energétiques

Revenue expected to increase by at least 5%at an estimated average spot rate of USD 1.33 to the Euro

Recurring operating income expected to increase by at least 20%at a targeted hedge rate of USD 1.38 to the Euro

Free cash flow expected to represent about a third* of the recurring operating income taking into account an expected increase in OWC and R&D investments

(*) An average of more than 50% across 2010-2011. 2010 FCF benefited from strong cash receivables ahead of 2011.

FY 2010 Earnings - February 24, 2011

42

Healthy prospects beyond 2011

Pick-up in build rates on the OE side and aftermarket growthOE to resume growth (A320/B737, B777, A380, B787, SJ100, bizjet…)Civil aftermarket revenue should grow at 2-digits for several years

Profitable growth in SecurityStrong demand for our technologyLong term target: 20% of revenue & mid-teen operating margins

Favourable hedge ratesGradual improvement through 2014

On-going Safran+ plan to enhance competitiveness and reduce overheads

2012 recurring operating margin well on the way to the 10% threshold

FY 2010 Earnings - February 24, 2011

43

Safran

Questions & Answers

FY 2010 Earnings - February 24, 2011

44

Safe harbor

Except for historical information, all other information in this presentation consists of forward-looking statements within the meaning of the US Private Securities Litigation Reform Act of 1995, as amended. These forward looking statements include statements regarding the future financial and operating results of Safran such as (i) expected revenue for full year 2011, (ii) expected profit from operations for the full year 2011 and iii) free cash flow for the full year 2011. Words such as "expects," "anticipates," "targets," "projects," "intends," plans," "believes," "estimates," variations of such words and similar expressions are intended to identify such forward-looking statements which are not statements of historical facts.These forward-looking statements are not guarantees of future performance and involve certain risks, uncertainties and assumptions that are difficult to assess. Therefore, actual outcomes and results may differ materially from what is expressed or forecasted in such forward-looking statements. These risks and uncertainties are based upon a number of important factors including, among others: our ability to operate effectively in a highly competitive industry with many participants; our ability to keep pace with technological advances and correctly identify and invest in the technologies that become commercially accepted; difficulties and delays in achieving synergies and cost savings; fluctuations in the aerospace market; exposure to the pricing pressures in the regions in which we sell; the pricing, cost and other risks inherent in long-term sales agreements; exposure to the credit risk of customers;reliance on a limited number of contract manufacturers to supply products we sell; the social, political and economic risks of our global operations; the costs and risks associated with pension and postretirement benefit obligations; the complexity of products sold; changes to existing regulations or technical standards; existing and future litigation; difficulties and costs in protecting intellectual property rights and exposure to infringement claims by others; compliance with environmental, health and safety laws; the economic situation in general (including exchange rate fluctuations) and uncertainties in Safran’s customers businesses in particular; customer demand for Safran’s products and services; control of costs and expenses; international growth; conditions and growth rates in the aerospace industry; and the impact of each of these factors on sales and income. For a more complete list and description of such risks and uncertainties, refer to Safran’s Document de Référence for the year ended December 31, 2009. Safran disclaims any intention or obligation to update any forward-looking statements after the distribution of this news release, whether as a result of new information, future events, developments, changes in assumptions or otherwise.

* Adjusted data

For forward looking statements

FY 2010 Earnings - February 24, 2011

45

Safran

Additional Information

FY 2010 Earnings - February 24, 2011

46

SME

Safran to acquire SNPE Matériaux EnergétiquesStrengthens the solid propulsion industry, a key to the long-term viability of European launch vehicles and missilesClosing expected in Q1 2011

Safran received specific guarantees concerning environmental liabilities due to past operationsUp to 40 years; up to €240M with a Safran contribution between 10 and 50%Covers third parties claims and closing of sitesWith a counter guarantee from the French government of up to €216M

Financial impact~ €270M cash-out~ €10M one-off restructuring & transaction costs in operating income (accounted for in one-off items)

Estimated 2011 annualized data2011E Sales: ~ €300M2011E EBITDA: ~ €45M

Creating a world leader in solid propulsion

FY 2010 Earnings - February 24, 2011

47

L-1 Identity Solutions

Transaction still pending final government approvals HSR terminated; L-1 shareholders approved the transactionCFIUS process still on-goingClosing expected in H1 2011

Subject to successful closing in 2011~ €780M cash-out~ €30M one-off restructuring & transaction costs in operating income (accounted for in one-off items)

Estimated 2011 annualized data2011E Sales: ~ $530M2011E EBITDA: ~ $100M (incl. cost synergies)

Creating a world leader in biometric solutions

FY 2010 Earnings - February 24, 2011

48

L-1: Creating a global leader in biometricsSafran to acquire the biometrics & enterprise access solutions, secure credentialing solutions and enrollment services businesses of L-1, a US-based leading global identity management provider

Transaction conditioned upon sale of L-1’s government consulting services (GCS) businesses to a third party and regulatory approvals

Significant step in the implementation of Safran’s strategy to develop as world leader in the field of mission critical high tech tier one players in the group’s three businesses: Aerospace, Defence and Security

Combination will provide an ideal platform to accelerate growth, notably in the U.S., and expand into new territories

Highly complementary businesses with a strong fit and compelling product, geography and client-mix

All-cash offer, fully financed with Safran’s existing cash on-hand

Accretive from year one with operating synergies

FY 2010 Earnings - February 24, 2011

49

L-1: A complementary technology approach

L-1 adds a suite of best of breed technologies that would enhance Safran’s (Morpho) own technology and product offering across a broad range of IDmanagement and Homeland Security applications

Main owned technologies

Ø AFIS software •Ø Secured printing •Ø Smart cards •Ø Explosive detection •

Ø Multimodal biometric platform •Ø Iris recognition •Ø Facial recognition •Ø Livescan and multi-biometric acquisition devices •

This will create a pool of technologies to enhance further security for state and local governments, aviation and other critical infrastructure

FY 2010 Earnings - February 24, 2011

50

L-1: Yielding significant operating synergies

Value creation drivers

Operating synergies

Cost synergies at different levels:Rationalisation of sitesInternational salesR&DOther support and operations

Safran will obtain hardware / software internally (rather than from 3rd parties) for Biometric equipment and blank documents for Secure Credentialing

Run-rate synergies expected to be fully

realized within 18 months from the

effective closing of the transaction

Approximately $30 M run-rate and not including likely top-line commercial synergies

Estimatedimpact ($M)

Sourcing synergies

FY 2010 Earnings - February 24, 2011

51

* Source : Ascend

Aerospace

79%

21%

1st CFM56 generation (-2, -3, -5A, -5C)

Dec. 31, 2009468 aircraft

2nd CFM56 generation (-5B, -7)

91%

9%

Dec. 31, 2010428 aircraft

Number of grounded planes powered by CFM56 engines Grounded CFM-equipped aircraft

represent 4% of the total CFM fleet

vs. 11% for the total active aircraft market*

A majority of B737NG returned to traffic

Some 2nd generation CFM A320 were back to lessors

40 CFM56 powered aircraft returned to service in FY 2010

FY 2010 Earnings - February 24, 2011

52

Global CFM spares revenue in $: -17% in 2010 vs. 2009Q4 flat vs. Q4 2009, but up 15% vs. Q3 2010

Airlines consume their inventory, delay shop visits & decrease scope of overhauls - optimizing their engine fleet

40 CFM56 powered aircraft returned to service

46% of CFM active fleet still to have their first shop visit (>67% of the 2nd generation engines)= 9,500 engines

Aerospace - CFM aftermarket

FY 2009

2,305

FY 2010CFM56 shop visits

(total worldwide)2,120

47%53% 52% 48%

Total -8.0%1st gen. CFM56 -8.4%2nd gen. CFM56 -7.6%

Shop visit numbers are estimates; these can be revised marginally as airlines finalise reports

1st gen. 1st gen.2nd gen. 2nd gen.

Improving CFM aftermarket

FY 2010 Earnings - February 24, 2011

53

Aircraft Equipment shipset

$4.5MPPPA350XWB

$5MPPPPB787

€7MPPPPA400M

$18-19MPPPA380

Equipmentshipset value

WiringWheelsbrakesMain LGNose LGNacelles

FY 2010 Earnings - February 24, 2011

54

Income taxAdjusted accounts

(in € millions)Profit (loss) before tax 523 706

Standard tax rate applicable to the parent company 34,43% 34,43%

Tax (expense) benefit at standard rate (180) (243)

Impact of permanent differences 6 (7)

Impact of research tax credit 34 46

Impact of reduced tax rates 15 30

Impact of unrecognized taxes (3) 16

Impact of tax adjustments 9 (16)

Impact of tax credits and other items 11 1

Current income tax benefit (expense) recognized in profit or loss (108) (173)

Effective taxe rate 20,66% 24,50%

31.12.2009 31.12.2010