Future Strategies for VoLTE Deployment

18

Future Strategies for VoLTE Deployment VoLTE reduces cost but will be difficult to monetize Reference Code: TE011-001193 Publication Date: 19 Feb 2013 Author: Jeremy Green, Nicole McCormick, Sara Kaufman SUMMARY In a nutshell Mobile operators preparing to roll out LTE don’t need to hurry to deploy voice over LTE (VoLTE). There are still service and supply issues to be worked out, and time (and the effort of others) will solve most of this. In the meantime, VoLTE won’t deliver any compelling services, revenue opportunities, or business prospects. While VoLTE will enable network efficiency and cost savings in the long term, operators should continue to focus on data services for the time being. Ovum view For most operators, the eventual deployment of LTE is a foregone conclusion. While issues remain around determining exactly when to launch LTE, deciding not to roll out the technology at all is a niche position that few operators in competitive markets will take. A similar logic applies to providing voice services on LTE. Being a data-only operator or providing customers with telephony via an over-the-top (OTT) service (either in-house or on a BYO basis) is again a niche position that few operators will take. Operators are neither willing nor able to avoid providing telephony services as doing so carries too many commercial risks and will not be permitted by regulators. While there are some questions about how to provide voice services during an interim period when the LTE network sits alongside legacy 3G and 2G networks, there is a general consensus that the ultimate destination is a solution based on IP multimedia subsystem (IMS) that has been designated as VoLTE – “voice over LTE”. However, the key question for operators is one of timing. As with LTE, some operators will find reasons to launch VoLTE services early. The drivers of an early VoLTE deployment include: • network efficiency Future Strategies for VoLTE Deployment (TE011-001193) 19 Feb 2013 © Ovum. Unauthorized reproduction prohibited Page 1

-

Upload

sandeep755 -

Category

Documents

-

view

178 -

download

2

description

Strategies for VoLTE deployment

Transcript of Future Strategies for VoLTE Deployment

Future Strategies for VoLTE DeploymentVoLTE reduces cost but will be difficult to monetize

Reference Code: TE011001193Publication Date: 19 Feb 2013

Author: Jeremy Green, Nicole McCormick, Sara Kaufman

SUMMARY

In a nutshell

Mobile operators preparing to roll out LTE don’t need to hurry to deploy voice over LTE (VoLTE). There are still service and supply issues to be worked out, and time (and the effort of others) will solve most of this. In the meantime, VoLTE won’t deliver any compelling services, revenue opportunities, or business prospects. While VoLTE will enable network efficiency and cost savings in the long term, operators should continue to focus on data services for the time being.

Ovum view

For most operators, the eventual deployment of LTE is a foregone conclusion. While issues remain around determining exactly when to launch LTE, deciding not to roll out the technology at all is a niche position that few operators in competitive markets will take. A similar logic applies to providing voice services on LTE. Being a dataonly operator or providing customers with telephony via an overthetop (OTT) service (either inhouse or on a BYO basis) is again a niche position that few operators will take. Operators are neither willing nor able to avoid providing telephony services as doing so carries too many commercial risks and will not be permitted by regulators.

While there are some questions about how to provide voice services during an interim period when the LTE network sits alongside legacy 3G and 2G networks, there is a general consensus that the ultimate destination is a solution based on IP multimedia subsystem (IMS) that has been designated as VoLTE – “voice over LTE”.

However, the key question for operators is one of timing. As with LTE, some operators will find reasons to launch VoLTE services early. The drivers of an early VoLTE deployment include:

• network efficiency

Future Strategies for VoLTE Deployment (TE011001193) 19 Feb 2013

© Ovum. Unauthorized reproduction prohibited Page 1

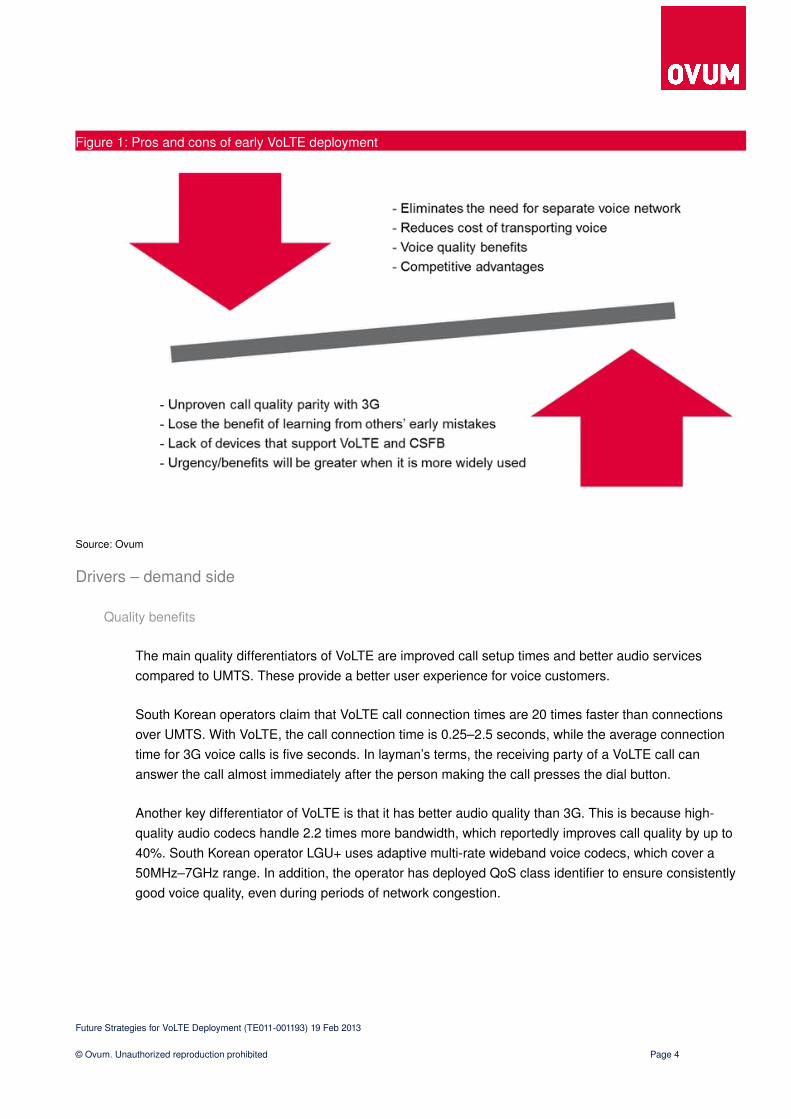

• VoLTE eliminating the need for a separate voice network, and the promise of spectral efficiency further reducing the cost of transporting voice

• quality benefits, especially in terms of call setup time compared to UMTS

• the possibility of new services such as HD voice, simultaneous voice and data usage, and Rich Communication Suite (RCS) offerings.

However, other operators will find reasons to hang back and not get ahead of the pack. They cite a host of service parity issues, including support for emergency calls and incall handover between LTE and other networks. They also point to problems with devices, including the insufficient availability of devices that support VoLTE and unresolved issues about device performance (most notably battery drain).

Ovum prefers the second strategy, believing that it will be the second mouse that gets the cheese rather than the early bird that gets the worm. We believe that the opportunity to gain firstmover advantage in the VoLTE space is outweighed by the potential teething problems that the technology could face. As with every other launch of a new network technology, there will be issues associated with the availability of suitable devices. The service parity issues, and in particular the questions around handover, also seem to be substantial.

The service benefits of VoLTE also appear to be tenuous. Even if RCS services were a surefire winner (and this is by no means an established certainty), their deployment is largely unrelated to LTE, as the few commercial deployments to date largely demonstrate. It is a similar situation with HD voice, which can be deployed on both LTE and nonLTE networks.

Nor is there a straightforward relationship between VoLTE and new charging models for voice. Although some mobile operators are beginning to either feel or anticipate pressure from OTT VoIP services, VoLTE in itself neither facilitates nor requires a new kind of charging model. It is designed to support all of the recording, charging, and billing mechanisms that apply in traditional telephony. Operators can choose to implement a different set of billing principles (including “unlimited voice”), but they can do this independently of LTE.

For all of these reasons, our advice to operators is to stay engaged with VoLTE but to not rush to deploy the technology. Ovum believes that if operators can afford to wait, they should. Operators that can’t afford to wait should do what they can to avoid any problems by making detailed plans for device acquisition and workarounds for any service parity shortcomings. Operators should also continue to sell LTE on its real benefits in terms of data services rather than on the shaky potential benefits provided by voice services. The real benefit of offering voice on a LTE network is that it allows for more efficient operation and thus reduced opex, but that is not something that customers want or need to hear about.

Future Strategies for VoLTE Deployment (TE011001193) 19 Feb 2013

© Ovum. Unauthorized reproduction prohibited Page 2

DRIVERS AND BARRIERS TO EARLY VOLTE DEPLOYMENT

Overview

In the short term, operators need to decide whether to implement VoLTE now or wait until the usual teething problems associated with being a first mover, such as a lack of device availability, are resolved.

We find it difficult to make a compelling argument for the vast majority of operators to become first movers on VoLTE other than for the fact that the IPbased voice platform is designed to be more efficient and will therefore be more cost effective for operators. For example, voice over a spectrally efficient LTE network with an allIP core will reduce the cost of transporting voice. VoLTE, which eliminates the need for a separate voice network, is a prerequisite for this.

It is argued by suppliers and some operators that VoLTE will pave the way for new voice services, such as simultaneous voice and video, and enhance existing services, such as video chat. However, these services will have to compete with similar offerings from OTT players, many of which will be free. In this context, it will be difficult for operators to monetize VoLTE valueadded services (VASs).

Although standards and the roadmap for supporting voice telephony over LTE are now well defined, many operators are still hesitant about implementing VoLTE in the short term. These operators want voice telephony that is fully interoperable with legacy services and that will have no deficit in quality compared to those services. Currently, operators are continuing to conduct VoLTE trials for quality assurance testing rather than rushing in with a commercial VoLTE offering.

So far, four operators have launched commercial VoLTE services. These include all three South Korean mobile network operators (MNOs) – SK Telecom (SKT), KT, and LGU+ – and regional US operator MetroPCS. In South Korea, the three operators believed that offering VoLTE services would provide them with differentiation in the market. However, this was short lived, with both SKT and LGU+ launching VoLTE services in August 2012 and KT following in October 2012. MetroPCS’s early move to VoLTE has had more substance and will allow the operator to free up CDMA spectrum for the expansion of its LTE network. Ovum does not expect that many more operators will launch commercial VoLTE services until 2014 or 2015.

Future Strategies for VoLTE Deployment (TE011001193) 19 Feb 2013

© Ovum. Unauthorized reproduction prohibited Page 3

Figure 1: Pros and cons of early VoLTE deployment

Source: Ovum

Drivers – demand side

Quality benefits

The main quality differentiators of VoLTE are improved call setup times and better audio services compared to UMTS. These provide a better user experience for voice customers.

South Korean operators claim that VoLTE call connection times are 20 times faster than connections over UMTS. With VoLTE, the call connection time is 0.25–2.5 seconds, while the average connection time for 3G voice calls is five seconds. In layman’s terms, the receiving party of a VoLTE call can answer the call almost immediately after the person making the call presses the dial button.

Another key differentiator of VoLTE is that it has better audio quality than 3G. This is because highquality audio codecs handle 2.2 times more bandwidth, which reportedly improves call quality by up to 40%. South Korean operator LGU+ uses adaptive multirate wideband voice codecs, which cover a 50MHz–7GHz range. In addition, the operator has deployed QoS class identifier to ensure consistently good voice quality, even during periods of network congestion.

Future Strategies for VoLTE Deployment (TE011001193) 19 Feb 2013

© Ovum. Unauthorized reproduction prohibited Page 4

Possibility of new services

VoLTE opens up the prospect of operators offering new voice services, such as simultaneous voice and video, which will help to keep voice relevant to consumers. However, it is not entirely clear why operators expect VoLTE to succeed in this area when they have thus far been unable to develop compelling versions of these services.

We do not believe that the prospect of offering new services will be an important demandside driver (i.e. a new revenue source) for launching VoLTE. In fact, we think that it will be difficult for operators to make any money from services offered over VoLTE.

Firsttomarket and OTT advantage

Some operators have justified the early commercialization of VoLTE for competitive reasons. However, the competitive advantage provided by being a VoLTE first mover could be short lived. For example, leading South Korean operator SKT identified that being the firsttomarket with VoLTE would be strategically important in the highly competitive South Korean market. It also believed that being the first to launch VoLTE services was necessary to maintain its image as a technology leader. While SKT was the first operator in South Korea to launch VoLTE services, the smallest operator in the market, LGU+, launched its own VoLTE service shortly afterwards, negating any firstmover advantage aside from the spurious marketing claim of being “first”.

In markets where OTT messaging platforms have had a significant impact, VoLTE could prove to be a valuable competitive weapon. However, we would be surprised if operators offered more compelling services through VoLTE than those provided by OTT messaging players.

Drivers – supply side

Lower cost and better spectral efficiency

VoLTE is a more cost effective means of providing voice services compared to legacy circuitswitched networks. In addition, VoLTE will reduce future costs for operators as it eliminates the need for a separate voice network alongside a datacentric LTE network.

Ovum believes that the lower cost of operation per customer should be the main driver of the early adoption of VoLTE services. Many operators don’t currently place enough emphasis on reducing opex, and deploying VoLTE will help with this. However, the immaturity of the VoLTE ecosystem means that the majority of operators will defer deploying VoLTE in the short term, despite its cost advantages.

Refarming existing spectrum for LTE

Operators view VoLTE as a first step towards freeing up spectrum that can be refarmed for LTE once it is no longer required for voice.

Future Strategies for VoLTE Deployment (TE011001193) 19 Feb 2013

© Ovum. Unauthorized reproduction prohibited Page 5

The launch of VoLTE services will allow US operator MetroPCS, which is the only operator to have deployed the technology in the US, to free up CDMA spectrum for LTE. In the US, intense LTE competition among all the major operators and pressure to refarm existing spectrum for LTE is driving a commitment by many operators, including Verizon Wireless and AT&T, to roll out VoLTE in the next 12–18 months.

For GSM operators elsewhere, especially those that have been allocated new spectrum for LTE in the 2.5GHz or 700MHz bands, there is less need to adopt VoLTE for capacity reasons.

Barriers – demand side

Monetization is difficult

Currently, VoLTE VASs are limited. For example, besides offering highquality calls, SKT’s only other VoLTE VAS allows users to switch between voice and video during a call. Other VASs will be added shortly, including the ability to share video files during a call. While additional VASs will emerge in the future, the main difficulty facing operators will be monetizing them, especially when OTT players offer similar services for free.

RCS does not need VoLTE

In October 2012, MetroPCS launched Rich Communication Suite (RCS) 5.0 services alongside VoLTE under the GSM’s Joyn brand, which is a standard for combining and integrating the functionality of voice, messaging, and other data services (such as video) under one umbrella. MetroPCS’s introduction of RCS may appear to signal the dawn of a new services market, but in fact, the company’s RCS launch is limited and lackluster in terms of the customers it touches, the new services it promises, and the revenues it can generate.

MetroPCS chose to launch RCS on only one smartphone – the Samsung Galaxy Acclaim 4G – although the operator claimed that it would introduce 10 RCScapable devices by the end of 2012. In addition, MetroPCS’s LTE network coverage of just 14 US cities is a significant impediment to it gaining any real traction in the market. When combined with the fact that it has less than 10 million of the 367 million US mobile subscribers, these factors mean that the potential customer base for RCS is only a tiny fraction of the total market.

However, the biggest shortcoming of MetroPCS’s RCS launch is the underwhelming selection of capabilities and features that it enables for customers. One of the most desirable and promoted features of the new RCS services – video calling – is only available over WiFi. In addition, VoLTE, which the operator has touted as a key enabler of RCS, seems to have no material role since it is being offered on a different handset.

South Korea’s three MNOs were all scheduled to launch interoperable RCS services in November 2012. However, if this took place, it was done with little fanfare compared to the attention that surrounded the

Future Strategies for VoLTE Deployment (TE011001193) 19 Feb 2013

© Ovum. Unauthorized reproduction prohibited Page 6

declaration of intent. While it is still early days for RCS, we believe that the service will more of an opportunity for operators in markets where OTT messaging/VoIP platforms have had limited success.

As demonstrated by MetroPCS’s launch, the deployment of RCS is largely unrelated to LTE. As RCS does not require IMS, the services can be offered by operators with existing 3G/3.5G networks.

IMS lacking

VoLTE has become a mediumterm ambition for many operators as they are still rolling out the required IMS capability in their networks. IMS involves a substantial financial commitment that has been an issue for some operators, especially those in emerging markets. IMS deployments are also typically slow and this has hindered the rapid rollout of VoLTE services. Once IMS investments have been made, a further challenge for operators will be the realignment of their operational and business support systems for the new IP environment. These factors highlight just how complex and timeconsuming the rollout of IMS is for operators.

CSFB works well enough for now

Some LTE operators believe that circuitswitched fallback (CSFB) is a good interim solution that will provide reliable coverage and voice performance while they monitor the development of the VoLTE ecosystem and launches in other markets. Several operators have stated that they have been pleasantly surprised by the performance of CSFB, which has enabled them to delay the commercial rollout of VoLTE while they wait for a sufficient device ecosystem to emerge. However, some operators that have deployed CSFB have a much less favorable opinion of the solution.

Roaming is a shortterm challenge

According to many operators, providing VoLTE services to roaming customers will only become a reality once VoLTE becomes widely available in both the network and terminals. Ultimately, the roaming opportunity depends on operators’ mutual IMS deployments.

First movers have not rushed to sign roaming agreements, preferring to wait for the rest of the international community to catch up with VoLTE before adding roaming to the already complex implementation. Most operators expect to continue to use the same mechanisms that they use for circuitswitched telephony to support voice roaming on LTE.

Barriers – supply side

Lack of devices and platforms

The lack of suitable devices is one of the biggest barriers to the early adoption of VoLTE, and Ovum expects that it will take until at least 2014 for VoLTE to become a mainstream option in new LTE smartphones. As shown in Figure 2, there are currently only three handsets that support VoLTE.

Future Strategies for VoLTE Deployment (TE011001193) 19 Feb 2013

© Ovum. Unauthorized reproduction prohibited Page 7

MetroPCS announced plans to introduce three VoLTEcapable handsets in 2012, but to date has launched just one, the LG Connect 4G. The only VoLTEcompatible handset available from SKT is Samsung's Galaxy S III smartphone. Existing Galaxy S III devices became VoLTEcapable via a software upgrade at the end of August 2012. LGU+ launched its VoLTE service with two VoLTEenabled smartphones: LG's Optimus II and the Galaxy S III. Upgrades for existing models of these devices were also made available in August 2012.

Figure 2: VoLTE handsets (as of September 2012)

Source: Ovum

As well as a lack of devices, operators have stated that until network infrastructure for VoLTE was available, voice services would have to reside on existing networks. This is a particular concern for European operators.

Lack of operational solutions

When discussing active call handoff, CSFB is not relevant as an orthogonal technique for VoLTE because it forces a device to take or make calls on a 2G/3G network instead of LTE. As such, if CSFB is deployed, there is no LTE to 3G handoff for an active call.

With single radio devices, the handoff technique is referred to as single radio voice call continuity (SRVCC), which is initiated from the LTE network when the LTE signal deteriorates. The SRVCC enhancement standard – which allows comparable legacy circuitswitched handover performance between 2G/3G networks and LTE networks – was completed in 3GPP’s Release 10. An alternative for

Future Strategies for VoLTE Deployment (TE011001193) 19 Feb 2013

© Ovum. Unauthorized reproduction prohibited Page 8

dualradio devices is to use voice call continuity (VCC). According to some operators, the lack of SRVCC solutions has been an impediment to the early adoption of VoLTE.

No incall handover in the US

In the US, current VoLTEequipped devices are not SRVCC or VCCenabled and thus do not support incall handover between VoLTE and CSFB. Therefore, a call is dropped if a user moves outside of the coverage of a LTE base station. As LTE network coverage expands, incall handover will become less of an issue for operators.

In fact, SRVCC and VCC are only required where there is not universal LTE coverage. In South Korea, SRVCC’s immaturity has not been an issue as operators do not require handoff from LTE to 3G since LTE networks are deployed nationwide. Verizon’s plan to launch VoLTE services once it has completed the rollout of its nationwide LTE network in early 2014 supports the notion that operators can bypass the need to develop SRVCC.

Service parity for VoLTE is required

As shown in Figure 3, maintaining full service parity with circuitswitched telephony is highly complex. In addition to persontoperson calling, circuitswitched telephony is used for a wide range of commercial and noncommercial VASs. Neither session initiation protocol (SIP) nor IMS support all of these “out of the box”, meaning that a more complex architecture of dedicated servers and interfaces is required.

The IMScompliant telephony application server supports:

• voice and video calls • the IP multimedia service control (ISC) and Ma interfaces per 3GPP 24.229 • the multimedia telephony service (MMTel) standard per 3GPP 24.6xx series specifications

• IMS profile for voice as specified in GSMA IR.92 and for video as specified in IR.94

The control of media resource function (CMRF) for media resource function controller/media resource function processer (MRFC/MRFP) functionality supports tones, announcements, conferencing, transcoding, and “prompt and collect” (SIP, MSML RFC 5707, and VoiceXML).

Future Strategies for VoLTE Deployment (TE011001193) 19 Feb 2013

© Ovum. Unauthorized reproduction prohibited Page 9

Figure 3: VoLTE architecture

Source: Mavenir

Future Strategies for VoLTE Deployment (TE011001193) 19 Feb 2013

© Ovum. Unauthorized reproduction prohibited Page 10

Alongside QoS, battery life is a concern

Maintaining a good customer experience is an important consideration for operators when making the transition to VoLTE. Operators have expressed concerns about call quality continuity with VoLTE and the battery life of devices given that the early CSFB experience from the US showed that battery life was a problem. Operators would prefer to test VoLTE with scale – on both the network and handset – before undergoing an early commercial launch and potentially jeopardizing customer experience. We expect that many operators will take this approach, especially those that are positioned at the premium end of the market.

Devices lack support for emergency calling

VoLTE devices offered by UMTS 3G operators in the US, such as AT&T and TMobile, will not support emergency calling as it currently requires a circuitswitched connection. CDMA operators have a solution to this problem, which is partly why Verizon has a more aggressive VoLTE launch timetable than AT&T. The lack of emergency calling support is an especially big issue in the US, where a telco’s operator license is dependent on meeting strict national E911 emergency service location requirements.

In a 2011 response to the Federal Communications Commission’s (FCC) proposed rulemaking for VoIP services, MetroPCS argued that commercial mobile radio service (CMRS) operators should be allowed to use their existing circuitswitched networks as an E911 solution for VoLTE. However, one of the concerns with this method is that VoLTE and CMRS services often use different network architecture that could result in coverage holes where VoLTE is available but the circuitswitched network is not. In this scenario, the CSFB solution would not meet minimum FCC E911 requirements and would therefore not be a viable solution.

MetroPCS and other operators have argued that a lack of clarity in the regulation of new technologies such as VoLTE should not inhibit their development. The operators further argue that the objective and purpose of regulation should be to provide a clear target for operators to meet, not to define how to achieve it. Although the FCC has yet to make an official ruling on this issue, US operators seem to have persuaded the regulator to take an agnostic position on the methods used to provide E911 as long as an operator can provide equivalent coverage.

Lack of interconnection

Currently, operators do not view IP interconnection as a major priority. Ultimately, the longterm plan will be for operators to use SIP for interconnection rather than traditional signaling system 7 (SS7) interconnection interfaces.

Most operators expect that SS7 signaling will support initial interconnect for VoLTE. One operator has stated that it plans to work with other operators on IP interconnect solutions as the need reaches critical mass.

Future Strategies for VoLTE Deployment (TE011001193) 19 Feb 2013

© Ovum. Unauthorized reproduction prohibited Page 11

Operators are delaying their SIP investments as they do not provide significant additional benefits until scale is an issue. This reinforces our overall interpretation that operators are focusing on using VoLTE to support a basic telephony service rather than looking to develop new services or business models.

Focus is on coverage

Another reason why operators are delaying VoLTE launches is because they are preoccupied with expanding network coverage. As network reach continues to be a leading differentiator among operators, it is not surprising that VoLTE is viewed as a more distant commercial reality.

For some operators, the focus remains on expanding 3G network reach, while for others the goal is to ensure that LTE coverage is national before launching VoLTE to avoid incall handover and service quality issues.

THE CURRENT STATE OF VOLTE DEPLOYMENTS

AsiaPacific

A number of developed market operators in AsiaPacific, most notably in South Korea, see VoLTE as a way to position themselves as technology leaders and gain “first to market” marketing prestige. South Korea also has a proactive vendor community, which may have helped to drive operator interest in the technology. However, Japanese operators have not rushed to deploy VoLTE. Currently, leading Japanese operator NTT DoCoMo is focusing on increasing its LTE coverage and has struggled to justify a VoLTE deployment. Ovum expects that NTT DoCoMo will roll out VoLTE services in 2013.

Other operators have opted to take a cautious approach to VoLTE deployment. Their views are summed up in Table 1. These operators are testing VoLTE or plan to start trials soon, but do not see its commercialization as urgent. CSL’s CTO, Christian Daigneault, told a recent conference that he does not see VoLTE as a differentiator. CSL currently offers HD voice for 3G and CSFB for LTE. Daigneault stated that VoLTE is purely a “capacity issue” for CSL, noting that consumers have not expressed any concern over the quality of CSFB. CSL believes that an operator’s readiness to refarm 3G spectrum for LTE will provide the incentive for the deployment of VoLTE services.

Another operator in this category stated that having a foundation IMS capability developed across its fixed and mobile networks took priority over VoLTE. The operator said that it was important to see whether VoLTE offered similar call performance and drop levels to circuitswitched voice services before deploying the technology. It also stated that the optimization of the packet radio and device ecosystem needed to mature and stabilize. In the meantime, its network performance using CSFB is providing “good and reliable coverage and performance”.

Some AsiaPacific operators in emerging markets view VoLTE as a distant proposition. In lowARPU markets, the focus will be on deploying IMS capability.

Future Strategies for VoLTE Deployment (TE011001193) 19 Feb 2013

© Ovum. Unauthorized reproduction prohibited Page 12

Table 1: VoLTE status of selected operators in AsiaPacific

Operator Launch Reason for launch/delay

Services Interconnection

Roaming RCS Price

SK Telecom August 2012 Maintain technology lead.

Switching between voice and video calls.

Plans to cooperate with other operators soon.

Will start when other international telcos commercialize VoLTE.

November 2012

Same.

Operator 1 2014 Device shortage.

n/a n/a n/a Seen as a new service for LTE

Difficult to justify timebased charging.

CSL Lab testing CSFB is a good interim solution. The need to refarm 3G spectrum is an incentive for VoLTE.

No new services.

n/a n/a n/a n/a

Operator 2 Test in 18 months

Implementing IMS, device shortage, and monitoring VoLTE’s call performance and drop levels.

No significant change in user behavior expected.

Will work with other operators as interconnection reaches critical mass.

A roamer can use the 3.5G network if the handset is not VoLTEenabled.

n/a Will likely charge for VoLTE in a similar way to traditional telephony.

Operator 3 2013 or 2014 Waiting for VoLTE to mature.

Looking at HD voice services to maintain ARPU.

Depends on multiple operators’ IMS capability.

n/a n/a Integrating address book with voice/video calling is a potential revenue opportunity.

Operator 4 Depends on timing of IMS rollout

IMS is a substantial financial commitment. Need to realign BSS/OSS systems.

n/a n/a n/a n/a It will be a challenge to charge for VoLTE.

Source: Ovum

North America

Because of MetroPCS’s small size, its VoLTE launch is not likely to change any of the larger US operators’ plans or give MetroPCS substantially more influence over the handset manufacturers that it relies on to make its VoLTEcapable devices. However, from a customer perspective, MetroPCS’s early

Future Strategies for VoLTE Deployment (TE011001193) 19 Feb 2013

© Ovum. Unauthorized reproduction prohibited Page 13

VoLTE launch reinforces the operator’s brand positioning as a technology and services leader in a market in which it is otherwise overshadowed by its competitors.

As MetroPCS is a fraction of the size of Verizon and AT&T, it doesn’t have a lot of influence with handset manufacturers, significant marketing resources to promote its VoLTE launch, or the brand power to make a major impact outside of its home LTE markets. These limitations have forced MetroPCS to move slowly when introducing VoLTEcapable handsets, with the operator only releasing one to date: the LG Connect 4G.

When Verizon introduced its new IMS core in 2009, the operator appeared to be positioning itself as the VoLTE services leader in the US. However, Verizon’s eagerness with VoLTE has waned considerably. Initially, the operator announced plans to commercially launch VoLTE in 2012, but it subsequently changed its launch date to late 2013 to coincide with the completion of its LTE network rollout. More recently, Verizon again pushed back its launch plans, saying that it would introduce VoLTE sometime in early 2014. As with operators in other regions, building its national coverage footprint has taken priority over developing new services for the LTE network.

AT&T, Sprint, Clearwire, and NetAmerica Alliance have all announced plans to launch VoLTE in 2013 or 2014.

Europe

European mobile operators do not see VoLTE as a shortterm necessity, with none of the operators that we have spoken to having a detailed plan or a firm timetable for implementing the technology.

• Telefonica has no firm launch date, vision, or plan for LTE voice services. The operator also has no detailed plan as to how to support roaming or implement interconnect.

• Deutsche Telekom/TMobile Germany also has no detailed plans or a specific date for a trial. Informal comments from the operator suggest that a launch is at least two years away.

• Orange/France Telecom began VoLTE trials in 2012 and will continue to conduct them in 2013. However, data is Orange/France Telecom’s priority when it comes to its LTE network, with the operator stating that “until the devices and network infrastructure for VoLTE are available, voice services for LTE subscribers will be provided by the 3G or 2G networks”.

• One large operator, which did not want to be identified, differed from the consensus in believing that VoLTE, together with RCS, would be a platform for innovative services that would combine communications with the “social sharing” of content.

That so few European operators are willing to participate in interviews about their VoLTE strategy highlights just how far off practical commercial deployments are.

Future Strategies for VoLTE Deployment (TE011001193) 19 Feb 2013

© Ovum. Unauthorized reproduction prohibited Page 14

VOLTE SERVICES AND PRICING MODELS

VoLTE services

Ovum believes that operator expectations for new VoLTE services are unrealistic. As shown in Figure 4, operators have identified a number of new VoLTE services and capabilities that they expect to be able to monetize.

Figure 4: Services operators expect VoLTE to enable

Source: Ovum

Although all of these services can be supported by VoLTE, the difficulty will be in monetizing them, especially when OTT players offer similar services for free. In fact, we believe that there is little incremental revenue to be gained from HD voice services, inapp video chat, or ingame voice services via VoLTE. One of the most compelling competitive advantages to having VoLTE while the competition does not is VoLTE’s ability to lower the cost of transporting voice traffic. The lower cost of the transportation of voice traffic will allow operators to pass on the savings to their customers in an effort to compete and entice new subscribers.

Future Strategies for VoLTE Deployment (TE011001193) 19 Feb 2013

© Ovum. Unauthorized reproduction prohibited Page 15

A common misconception in the industry is that RCS is an LTEonly service. Although VoLTE requires IMS, RCS does not and can be implemented over 3G or 3.5G networks.

A more realistic expectation for operators is that as increasing numbers of multimedia data services are enabled by LTE and IMS, VoLTE will provide the underlying technology to increase capacity, offer better bandwidth and efficiency for voice services, and reduce costs. Ultimately, operators cannot get carried away with the notion that VoLTE is anything more than a voice service on the LTE network.

VoLTE pricing models

There is some confusion in the industry as to the impact of VoLTE on voice pricing models. At least one of the operators that we spoke to believed that it would be difficult to implement timebased charging for VoLTE calls, while others believed that it would be commercially impractical to continue to charge in this way in the long term. However, these two viewpoints confuse two different issues.

There is no technical reason why operators cannot continue to use timebased charging for VoLTE calls. The IMS architecture on which VoLTE is based was specifically designed to create call detail records (CDRs) in exactly the same way as traditional switches, even though the calls themselves are carried over a packetbased network. These CDRs can be passed to a billing system and operators can then implement whatever billing scheme they want. Indeed, operators that have defined how they will charge for VoLTE services say that this is exactly what they are going to do. SKT and LGU+ in South Korea and MetroPCS in the US all say that they will not tariff VoLTE differently to circuitswitched calls. The South Korean operators plan to use the same persecond pricing for VoLTE calls, but also plan to offer some bundles of voice minutes to new VoLTE customers as part of a promotional offer. Similarly, MetroPCS plans to offer VoLTE on the same terms as its existing voice plans.

There may be commercial reasons for using a different charging model for VoLTE. For example, operators may opt for alternative pricing models in an effort to encourage subscribers to migrate to VoLTE services. As the cost savings generated by LTE increase dramatically when an operator retires its legacy network, persuading customers to migrate to LTE quickly is a good strategy.

LTE also provides operators with an opportunity and incentive to rebalance customer tariffs to more closely reflect costs. In terms of demand on network capacity, voice telephony is relatively trivial, with customers already paying more for voice on a bitforbit basis than they do for other kinds of usage. If operators continue to charge for telephony at anything like historic rates, then LTE will exacerbate this discrepancy. This doesn’t mean that telephony pricing will necessarily become unsustainable as operators have not traditionally passed on the benefits of every cost reduction to customers. However, competitive pressure, both from peers and OTT providers, may force them to lower their voice prices. While LTE and VoLTE do not in themselves make it imperative for operators to move to new charging models for voice calls, they do make it easier for them to respond to other challenges.

Ovum believes that operators should be prepared to create new kinds of voice tariffs, but they should move with caution. Most plans with large bundles of voice minutes exclude specific types of calls (such

Future Strategies for VoLTE Deployment (TE011001193) 19 Feb 2013

© Ovum. Unauthorized reproduction prohibited Page 16

as international and roaming calls) and thus far this has been acceptable to customers. Although the bundling of international calls has taken place in a few markets, this is still a minority practice. Operators must be aware that it is difficult to remonetize something that has begun to be offered for free, and voice calls on LTE will be no exception.

APPENDIX

Methodology

Ovum conducted several interviews with operators in AsiaPacific, Europe, and the US for this report. Due to commercial sensitivities, the majority of operators preferred to remain anonymous. The report also utilized Ovum’s ongoing research into the global telecoms industry.

Further reading

Global Mobile Market Outlook: 2012–17 (TE011001200, February 2013)

Mobile Operator Responses to VoIP: The Six Steps (TE011000931, April 2010)

The Future of Voice (TE011001145, July 2012)

“There’s no harm in taking a slow road to VoLTE deployment” (TE011001196, January 2013)

US Wireless Carriers’ Attitudes Toward Consumer VoIP Services (TE011000811, May 2009)

Author

Jeremy Green, Principal Analyst, Telco Strategy

Sara Kaufman, Analyst, Telco Strategy

Nicole McCormick, Senior Analyst, Telco Strategy

Future Strategies for VoLTE Deployment (TE011001193) 19 Feb 2013

© Ovum. Unauthorized reproduction prohibited Page 17

Ovum Consulting

We hope that this analysis will help you make informed and imaginative business decisions. If you have further requirements, Ovum’s consulting team may be able to help you. For more information about Ovum’s consulting capabilities, please contact us directly at [email protected].

Disclaimer

All Rights Reserved.

No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form by any means, electronic, mechanical, photocopying, recording, or otherwise, without the prior permission of the publisher, Ovum (an Informa business).

The facts of this report are believed to be correct at the time of publication but cannot be guaranteed. Please note that the findings, conclusions, and recommendations that Ovum delivers will be based on information gathered in good faith from both primary and secondary sources, whose accuracy we are not always in a position to guarantee. As such Ovum can accept no liability whatever for actions taken based on any information that may subsequently prove to be incorrect.

Future Strategies for VoLTE Deployment (TE011001193) 19 Feb 2013

© Ovum. Unauthorized reproduction prohibited Page 18