Future developments in Private Banking · PDF fileHSBC Private Bank. Contents 1. Changing...

25

Future developments in Private Banking PUBLIC Charlie Hoffman Managing Director HSBC Private Bank

-

Upload

truongcong -

Category

Documents

-

view

218 -

download

1

Transcript of Future developments in Private Banking · PDF fileHSBC Private Bank. Contents 1. Changing...

Future developments in Private Banking

PUBLIC

Charlie HoffmanManaging DirectorHSBC Private Bank

Contents

1. Changing demographics

2. Where is Private Banking today?

3. Where does Private Banking need to betomorrow?

2 PUBLIC

3. Where does Private Banking need to betomorrow?

4. How can you shape the journey?

Demographics – many major economies are seeing their population shrink

Annual population growth (%)

1.0

1.5

2.0

2.5

1,200

1,600

2,000

2,400

300

400

500

600

Total population (m) Total population (m)

3Source: US Census Bureau, HSBC Private BankForecasts are subject to change. PUBLIC

(1.0)

(0.5)

0.0

0.5

US

UK

Japa

n

Euro

pean

Uni

on Indi

a

Braz

il

Chi

na

Afric

a

2015 2025 2050

0

400

800

0

100

200

1995 2005 2015 2025 2050

US UK Japan

European Union Brazil India (RHS)

China (RHS) Africa (RHS)

Demographics – the US has both natural growth and immigration tomaintain population growth and a young and active labour force

Net international migration and naturalincrease (births – deaths): 2012 to 2060Middle series projections

1,400

1,600

1,800

Numbers (in thousands)

250

300

350

400

450

Population (m)

4 PUBLICSource: US Census Bureau, 2012 National ProjectionsForecasts are subject to change.

0

200

400

600

800

1,000

1,200

2012

2016

2020

2024

2028

2032

2036

2040

2044

2048

2052

2056

2060

Natural increase Net international migration

Net international migration isprojected to overtake naturalincrease as the driver ofpopulation growth in 2032 in theMiddle series. This occurs in 2027in the High series and 2038 in theLow series.

0

50

100

150

200

1995 2005 2015 2025 2050

US

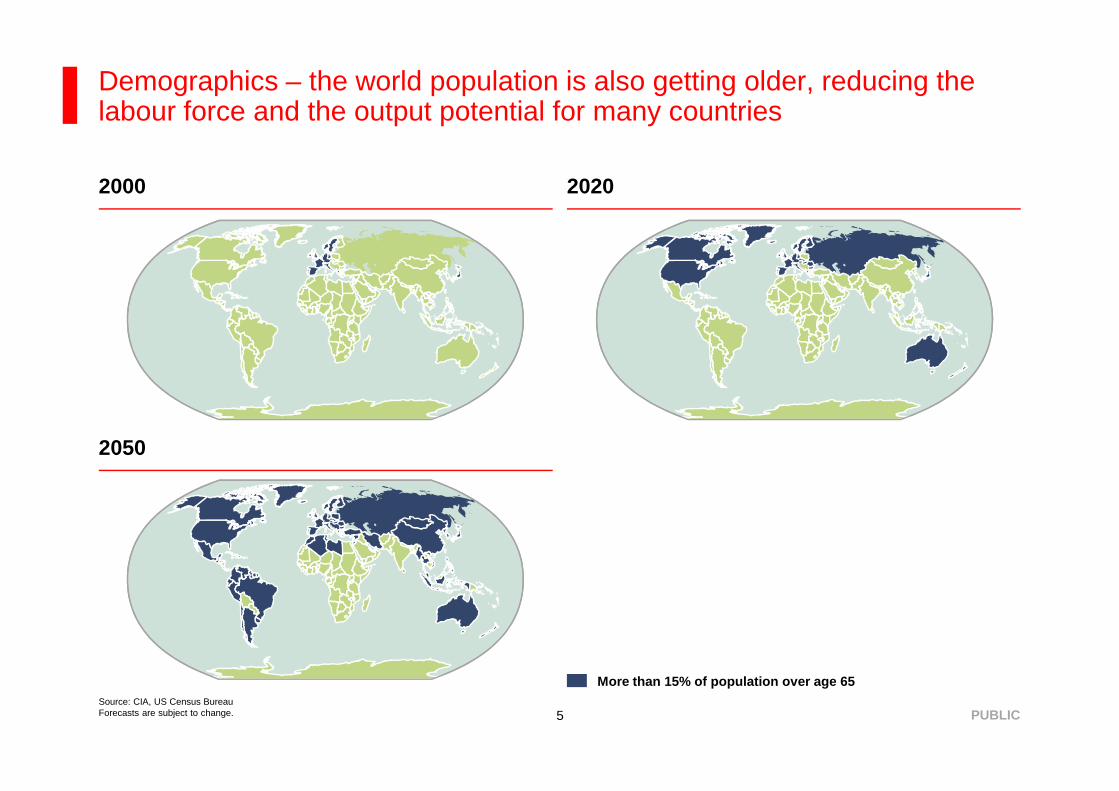

Demographics – the world population is also getting older, reducing thelabour force and the output potential for many countries

2000 2020

5 PUBLICSource: CIA, US Census BureauForecasts are subject to change.

More than 15% of population over age 65

2050

Demographics – implications

US economic growth is supported in the long-term by demographic growth – deficits canbe ‘traded out’

Risk to growth for Japan, Europe and China lower tax intake and higher social cost = growingdeficits and deflationary pressures

6

EM (ex China) faring better for the next 10 to 20 years, especially Africa, the Middle Eastand India

Market impact: Better demographics better growth prospects better market performance

PUBLIC

A global growth picturePredicted % increase of UHNW, centa-millionaires and billionaires by 2023

+21%

+20%

+20%

+66%

+52%

+43%

+25%

+22%

+21%

North America Europe

Middle East

Asia

7 PUBLIC

UHNW (+USD30m AuM)

Centa-millionaires

Billionaires

Key:

+45%

+44%

+42%

+19%

+20%

+18%

+52%

+51%

+53%

+35%

+36%

+35%Latin America

Africa

Australasia

Source: The Wealth Report 2014

Source of wealth by region

Savings through earnings 67%Profit from property 16%Business sale and/or profit 21%Inheritance 20%

US

Savings through earnings 51%Profit from property 29%Business sale and/or profit 41%Inheritance 21%

Europe

Savings through earnings 57%Profit from property 61%Business sale and/or profit 57%Inheritance 33%

Asia-Pacific (excluding Japan)

8 PUBLICSource: Barclays – A Changing Wealth Landscape - 2013

The values displayed sum to more than 100% because respondents could choose multiple choices.

Savings through earnings 34%Profit from property 56%Business sale and/or profit 58%Inheritance 36%

Latin America

Savings through earnings 40%Profit from property 56%Business sale and/or profit 68%Inheritance 36%

South Africa

Savings through earnings 41%Profit from property 32%Business sale and/or profit 48%Inheritance 49%

Middle East

Today vs tomorrow

Data Usage New Advisors

Innovation New Models

9

Winners (and Losers) Performance

Client Requirements Digital Era

PUBLIC

An era of transformation for global private banksA convergence of pressure from three directions

Clients

An evolving client-advisorrelationship

10

Private Bank

PUBLIC

Management

Scalability and investmentpriorities

Competitors

Accelerating the need fortransformation but leading toopportunity for global players

12182

140 159 172 178

2008 2009 2010 2011 2012 2013Operating Profits

Profits are hard-won

Profits are hard-wonin an environment offlat operatingincomes (marginsqueeze) andoperating expensesthat are tough tocontrol

742 739 716 804

Operating profits (USDm)

Operating income (USDm)

11 PUBLIC

443 449742 739 716 804

2008 2009 2010 2011 2012 2013

Operating income

(282) (309) (437)(673)

(518) (609)

2008 2009 2010 2011 2012 2013Operating expenses

Operating expenses (USDm)

Source: Scorpio Partnership Private Banking KPI Benchmark 2014

What does it take to grow market share?

USD20.3trn1

Today, the global wealth industry manages

What does the industry have to do to increase this?

12 PUBLIC

USD35trn2

Source:Notes:1. Scorpio Partnership, Benchmark market sizing 20142. Estimate of the proportion of HNW investable wealth that HNWs will book

with wealth managers globally

Building an entrepreneur acquisition strategyHow can private banks and wealth managers capitalise on theopportunity available?

The industry cando more to make

its messageloud and clear

Impressions of privatebanking brandsremain positive

Opportunity for differentiationthrough client segmentation

Referral strategiesappear weak

Brand challengeInstitution vs RM

Wealth managementmarketing mix

is changing

13

Referral strategiesappear weak

Brand challengeInstitution vs RM

Educationis key

Entrepreneurs’ needs aregrowing

more complex

Wealth managementmarketing mix

is changing

The personal rapport withRM remains vital

PUBLICSource: Gulland Padfield / Wealth Briefing – 2013

Customer engagement =

Ongoing

Customer Engagementmeans an on-going,value-drivenrelationship between acustomer and abusiness…

Customer choice

Which is consciouslymotivated accordingto the customer’sreasons and choices

Value driven

Engagement is builtthrough the abilityof the customer and thebusiness to both derivevalue from therelationship over time

Trust and knowledge

The ability of thebusiness to enablevalue creation overtime builds trust, andthe accumulationof trust, and mutualshared knowledge,builds engagement

14

The ability of thebusiness to enablevalue creation overtime builds trust, andthe accumulationof trust, and mutualshared knowledge,builds engagement

= which drives the customer experience

PUBLIC

The full journey is assessed in four parts by clients

Wealth mappingFinancial targets

Allocation and planning

Outputs linked to wealthprofiling and wealth connection

Strategies supportingwealth creation andwealth preservation

Experience Content

Based on client and advisor feedback, the four areas of the journey comprising overallcustomer experience that matter are: the experience, the content, the process, thegovernance

15

Wealth mappingFinancial targets

Allocation and planning

Strategies supportingwealth creation andwealth preservation

Asset managementAsset monitoring

Administration

Leadership (views ofmanagement) Service

excellence (awards etc)

Governance

Analysis and planningReporting

Administration

Process

C-Sat Multi-channel access(RM, team, digital, branch)

Asset supervisionFinancial targets

Allocation and planning

PUBLICSource: Scorpio Partnership

Take a truly client centric approachSix elements to address to become institutionally client centric

StrategyBrand and

Communications

Are you, should you, have you been auditing these?

16 PUBLIC

Services andProducts

Structure andOperations

People andRewards

ClientRelationships

TheClient CentricPrivate Bank

Sources: Gulland Padfield Report “The era of the Client Centric Advisor 2014” ; PwC Global PrivateBanking and Wealth Management Survey, 2011; European Private Banking Survey, McKinsey, 2011;BCG; The Asset Management Battle, BCG; The Value of Trust, Bruce Weatherall, August 2011

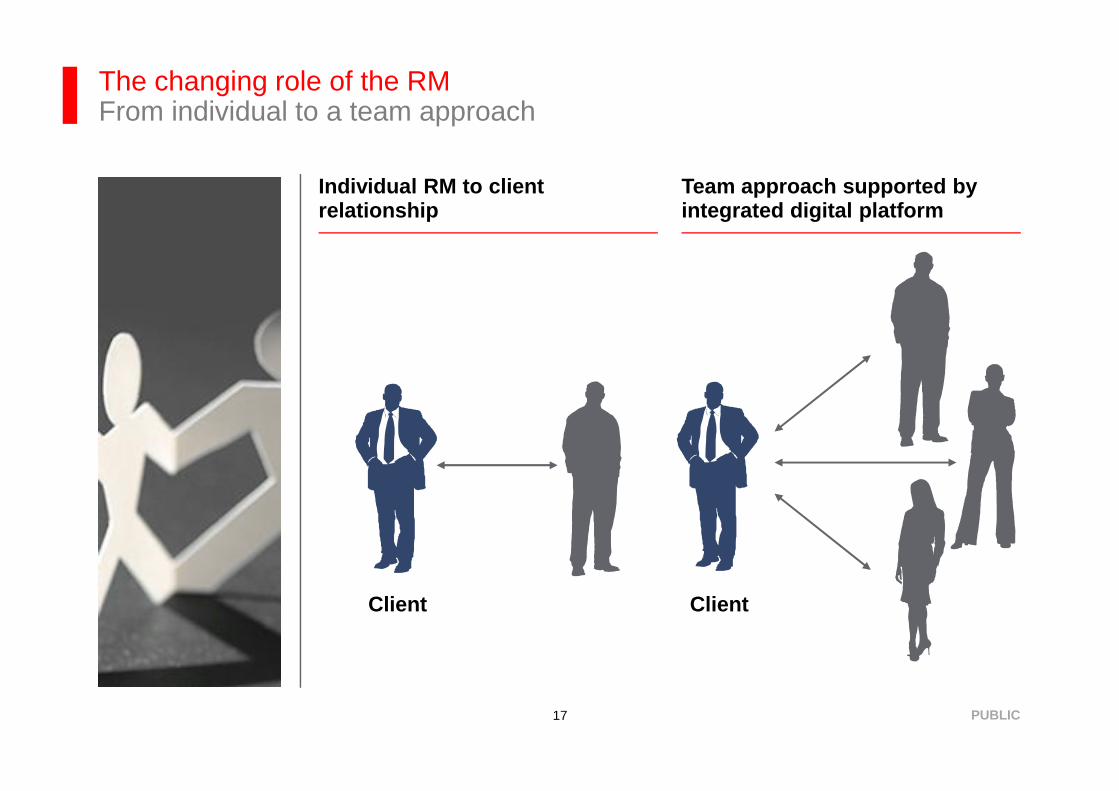

The changing role of the RMFrom individual to a team approach

Individual RM to clientrelationship

Team approach supported byintegrated digital platform

17 PUBLIC

Client Client

UHNWs view their advisors as a “management team”

14%

28%

34%

23%I want to find the best options

What is the main reason that you would consider taking financial advice?(NB. Sums to 100%)

18

UHNWs seek input and expertise for complexfinancial decisions.

PUBLIC

38%

14%19%

32%

11%

23%There are things I would rather be doing than managing my money

I want my money managed professionally

My time and energy are better focused on my career

<USD10m

USD10m+

N = 1,718

Source: Scorpio Partnership, Withers “The meaning of wealth in the 21st century”, 2014

Case study – top 5 global private bankImportance vs performance of client service attributes

4.4

4.5

4.6

4.7

Impo

rtan

ce(M

ean)

High

Delivers what they promise

Level of knowledge about current developments in the financial markets

Ability to explain complex matters in a structured and intelligible way

Availability (including replacement by a deputy)

19

4.0

4.1

4.2

4.3

3.6 3.7 3.8 3.9 4.0 4.1 4.2 4.3 4.4

Impo

rtan

ce(M

ean)

Performance(Mean)

Low High

Low

Friendliness

Preparation for meetings

PUBLICSource: Gulland Padfield client research for a top 5 global private bank. Base: 119 clients globally

Awareness of importance of digital is growing

30%

50%

30% 35%

50%

5%

North America

Europe

But regional variations: ‘High importance’ and ‘Top of agenda’dominates Europe (40%), North America (50%), and Asia 55%

How prominentlyis the topic“digitisation”positioned on thetop managementagenda?

20 PUBLIC

10%

60%

10%

50%

20%

25%

50%

20%

20% 35%Asia

Middle East

Latin America

Not relevant Low importance Medium importance High importance Top of agenda

Source: Interviews with wealth management executives, Strategy and analysis. Strategy & (PWC) Globalwealth management outlook 2014-2015

The changing relationship

Know me Compliance andprivacy demands

Join up channels tocommunicate as one

From general to personalised

Business challengesCustomer expectations

21 PUBLIC

Make it matter

One conversation Operational andbusiness silos

Reliance on IT

From general to personalised

From one-way communicationto conversation to pull

through the journey

Interactions focusedon value

Source: Thunderhead.com

The digital opportunity

Digital technology= opportunity to build clear differentiation and competitive advantage Based on strong and valuable customer relationships Built through true customer engagement based on knowledge

Focus on customer care and service development Agile customer centric business model Reduce friction Added value services through exploiting dynamic value ecosystem Remember: In the digital economy everything is a service

22 PUBLIC

Digital technology= opportunity to build clear differentiation and competitive advantage Based on strong and valuable customer relationships Built through true customer engagement based on knowledge

Focus on customer care and service development Agile customer centric business model Reduce friction Added value services through exploiting dynamic value ecosystem Remember: In the digital economy everything is a service

The digital opportunity – how

Actionablecustomerjourneys

Value-driveninteractions

Customerengagement

Gain a deeper understanding of the customer, customerbehaviour, and intent

Connect – anytime, anywhere

Provide a seamless omni-channel customer experience

Use customer insight and context to drive value-driveninteractions

Use customer insight and context to dynamically drive thecustomer journey

Exploit digital technology to build a system of engagement to empower therelationship manager

23 PUBLIC

Understandingcustomer behaviour,

intent and context

Customerengagement

Gain a deeper understanding of the customer, customerbehaviour, and intent

Connect – anytime, anywhere

Provide a seamless omni-channel customer experience

Use customer insight and context to drive value-driveninteractions

Use customer insight and context to dynamically drive thecustomer journey

Source: Thunderhead.com

So… plotting the journey from the client’s perspective is key

4 3 2 1

24 PUBLIC

Volume WealthManagement

Self selection oninvestments

Commoditisedproducts

“Facilitation”experience

Knowledge

Deliverable

Difference

WealthManagement

Volume-basedadvisory

Packagedproducts

“Convenience”experience

PrivateBanking

Model-basedadvisory

Selectedproducts

“Life sensitive”experience

MFO, SFO orIndependentBoutique

High leveladvisory

P2P investingand access

“Limited edition”experience

Source: Scorpio Partnership

Important notice

In the United Kingdom, this document has been approved for issue and distribution by HSBC Private Bank (UK) Limited whoseoffice is located at 78 St James’s Street, London SW1A 1JB.

No part of this publication may be reproduced, stored in a retrieval system, or transmitted, on any form or by any means,electronic, mechanical, photocopying, recording or otherwise, without the prior written permission of HSBC Private Bank (UK)Limited.

Copyright© HSBC Private Bank (UK) Limited 2015

ALL RIGHTS RESERVED

25 PUBLIC