Full year results presentation - Bupa/media/files/site-specific-files/our... · Full year results...

31

Full year results presentation 12 months ended 31 December 2016

Transcript of Full year results presentation - Bupa/media/files/site-specific-files/our... · Full year results...

Full year results presentation 12 months ended 31 December 2016

Overview Financial review Outlook & operating priorities

Agenda

2016 full year results presentation

Section 1

Overview

Evelyn Bourke Group CEO

Financial review

Joy Linton CFO

Gareth Evans Group Treasurer

Outlook and operating priorities

Evelyn Bourke Group CEO

Section 2 Section 3

2

Overview Financial review Outlook & operating priorities

Section 1

Overview

Evelyn Bourke Group CEO

3

Overview Financial review Outlook & operating priorities

Funding and providing services to help people live longer, healthier, happier lives

Our business model

We fund Helping customers fund health and

care through domestic and international

health insurance, as well as other

funding models

We provide Providing health and care services

through primary care clinics, hospitals,

dental centres, and aged

care services

Our services

Underpinned by

Delivering for

Customers

Employees

Partners

Society

4

Overview Financial review Outlook & operating priorities

5

Investing in strength and depth

Winning locally, enabled globally

Ever-focused on quality, efficiency, safety and compliance. Disciplined in risk and capital management

Our strategy to drive the next phase

of Bupa’s growth in today’s digital age

Our refreshed Strategic Framework

Overview Financial review Outlook & operating priorities

Revenue and profit growth in challenging market conditions

6

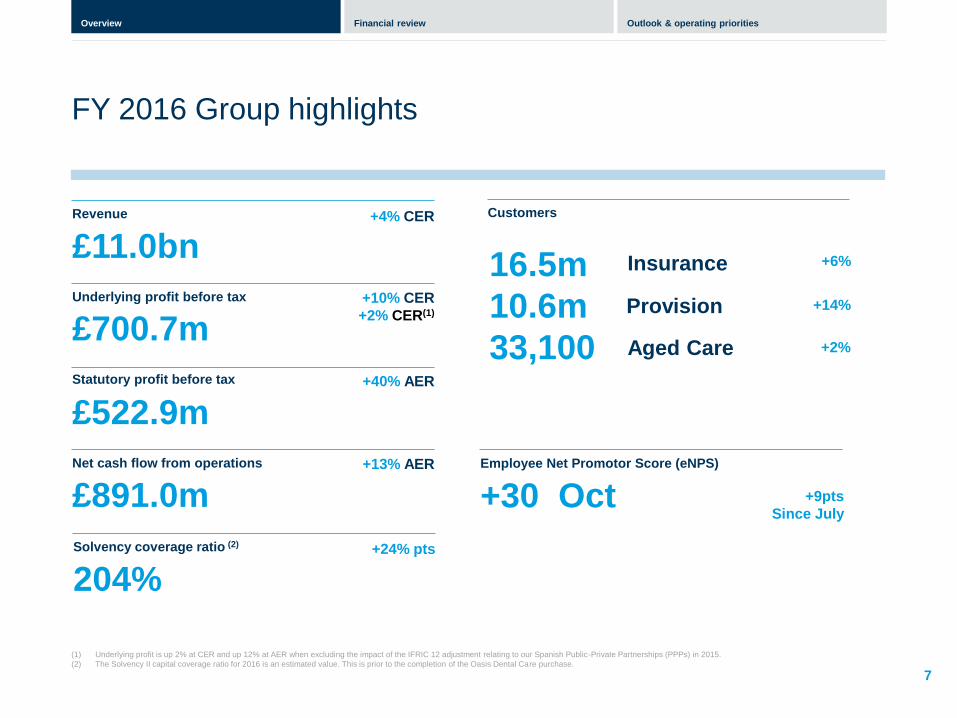

FY 2016 Group highlights

Reshaped UK portfolio, exiting home healthcare and purchasing Oasis Dental Care (1)

Operating highlights:

Good profit growth in three largest Market Units

Reduced from five to four Market Units Appointments to executive team

Weaker macro backdrop and political change

Changing customer and regulatory expectations

Consumer and government affordability pressures

Operating environment characterised by:

(1) Sale of Bupa Home \Healthcare in July 2016. Purchase of Oasis Dental Care on 09 February 2017 subject to CMA approval

Australia's leading health insurer

Overview Financial review Outlook & operating priorities

FY 2016 Group highlights

7

(1) Underlying profit is up 2% at CER and up 12% at AER when excluding the impact of the IFRIC 12 adjustment relating to our Spanish Public-Private Partnerships (PPPs) in 2015.

(2) The Solvency II capital coverage ratio for 2016 is an estimated value. This is prior to the completion of the Oasis Dental Care purchase.

Revenue

£11.0bn +4% CER

Underlying profit before tax

£700.7m +10% CER

+2% CER(1)

Statutory profit before tax

£522.9m +40% AER

Net cash flow from operations

£891.0m +13% AER Employee Net Promotor Score (eNPS)

+30 Oct +9pts

Since July

Solvency coverage ratio (2)

204% +24% pts

Customers

Insurance +6% 16.5m

10.6m

33,100

+14%

+2%

Provision

Aged Care

Overview Financial review Outlook & operating priorities

Revenue up 7%; profit up 9%

8

Australia and New Zealand

Revenues

Underlying profit

Revenues by business

Customers

(FY 2015: £4,078.3m CER)

£4,360.6m +7% CER

+20% AER

(FY 2015: £314.7m CER)

£344.4m +9% CER

+23% AER

Insurance

Operating Environment

• Customer affordability remains an industry-wide challenge;

Bupa maintaining focus on service and value

• Continue to engage with Government regarding expected

adverse impact of reduced Aged Care Funding Instrument

Performance

• Resilient growth in Health Insurance business, becoming

Australia’s largest health insurer

• Health Services Australia business maintained strong market

position; Bupa is the country’s largest dental provider

• Bupa Aged Care Australia remains the country’s leading private

aged care provider, caring for nearly 7,000 residents

• Aged care business in New Zealand grew, with four new care

homes and three retirement villages

• Building new tools and capabilities for meaningful and

personalised customer interactions

Provision

Aged care

4.0m

1.9m

10,800

Overview Financial review Outlook & operating priorities

Revenue down 3% (up 5% like-for-like(1)); profit up 7%

9

United Kingdom

Revenues

Underlying profit

Revenues by business

Customers

(FY 2015: £2,857.8m)

£2,785.9m -3%

(FY 2015: £182.6m)

£194.9m +7%

Operating Environment

• Further increases to the Insurance Premium Tax (IPT).

Committed to making quality, value-for-money healthcare

more affordable and accessible

• Continue to negotiate with local authorities to cover the true

cost of care including impact of National Living Wage

• Limited impact from Brexit at this stage

Performance

• Decline in revenue of 3% due to sale of Bupa Home

Healthcare in July, up 5% when comparing like-for-like (1)

• Health insurance business performed well, with profit

driven by improved corporate and consumer loss ratios

• Digital transformation and innovation remains a priority

• Active management of our Care Services portfolio

• Significant re-shaping of UK portfolio with sale of Home

Healthcare and Oasis Dental Care purchase(2)

Insurance

Provision

Aged care

2.4m

1.2m

17,400

(1) When excluding Bupa Home Healthcare from 2015 and 2016.

(2) Bupa Home Healthcare sole July 2017. Purchase of Oasis Dental Care completed February 2017 subject to CMA approval.

Overview Financial review Outlook & operating priorities

Purchase of Oasis Dental Care

Rationale

• Dentistry is a strategic growth area for Bupa, as it enables us to build

relationships with a broader base of customers

• Unique opportunity to establish a national retail presence and cross-sell

Oasis overview

• Customer-centric model: accessible, transparent pricing, high quality care

• Strong customer satisfaction: Net Promoter Score 2x market average

• First dental chain to advertise nationally

Transaction summary

• Purchase announced on 18 November 2016

• Transaction completed 9 February 2017 with an enterprise value of £835m(2)

Solvency Impact

• Reduced our coverage ratio to an estimated 165%, comfortably within our

capital risk appetite

UK Dental market size

£7.1bn Total Bupa UK dental clinics post purchase

c.420 Dentists

1,800 Customers

2m

(1) Estimated figure

(2) Subject to CMA approval.

Pro forma Group Solvency ll coverage ratio(1)

165%

10

United Kingdom

Overview Financial review Outlook & operating priorities

Revenue up 10%; profit up 63% (up 10% like-for-like(1))

11

Europe and Latin America

Revenues

Underlying profit

Revenues by business

Customers

(FY 2015: £2,251.8m CER)

£2,474.7m +10% CER

+22% AER

(FY 2015: £101.8m CER)

£165.6m +63% CER

+84% AER

Operating Environment

• Challenging Spanish political environment; we remain

confident in our PPPs

• Mitigating the adverse impact of uncertainties relating to the

Chilean premium increase process on Isapre through tighter

cost management

Performance

• Revenue growth across a number of business units in Spain,

including continued growth in our Sanitas insurance business

• Achieved strong year-on-year revenue growth in Bupa Chile

driven in part by Isapre performance improvement

• Ongoing investment in full digital transformation delivering

improved customer journey

• Aged care business, Sanitas Mayores, delivering consistently

high occupancy rates

• Increased ownership of Bupa Chile from 73.7% to 100%

• LUX MED in Poland achieved significant revenue growth

Insurance

Provision

Aged care

2.9m

6.7m

4,900

(1) Under IFRIC 12, which applies to service concession contracts such as Public-Private Partnerships, we use the average operating

margin for the life of the contract (based on historic performance plus projections) as a means for recognising results. Once there is a

change in performance compared to expectations, the operating margin is reassessed and an adjustment made to the current year

results to bring the contract performance to date in line with the revised margin. In 2015, this negative non-cash adjustment of £52.0m

included an amount relating to the current year of £8.8m together with a retrospective adjustment for the years preceding 2015 of

£43.2m. To compare the result on a ‘like for like’ basis with 2016, we have excluded £48.6m (being £43.2m retranslated at 2016 rates)

from underlying profit in 2015.

Overview Financial review Outlook & operating priorities

Revenue up 1%; profit down 52% driven by Bupa Global

12

International Markets

Revenues(1)

Underlying profit

Revenues by business(2)

Customers

(FY 2015: £1,418.9m CER)

£1,427.8m +1% CER

+10% AER

(FY 2015: £138.1m CER)

£65.9m -52% CER

-48% AER

Operating Environment

• Operate in diverse markets with healthcare regulation and

economic environment constantly evolving

• Challenging market conditions in Saudi Arabia, including a

slowing economy

• Indian health insurance sector attracting new entrants and

highly competitive

Performance

• Decline in Bupa Global profit driven by the ongoing impact of

our 2013 decision to exit non-strategic markets, investment in

capability and infrastructure, and lower than anticipated rate

of growth in Individual and Small Medium Enterprise books

• Strengthened position in Hong Kong

• Strong customer and revenue growth in Bupa Arabia despite

challenging backdrop

• Increased shareholder in Max Bupa from 26% to 49% in June

• Acquired Care Plus in Brazil in December

(1) Revenue of £1,427.8m does not include the revenues of our equity accounted associates (Max

Bupa, India, Bupa Arabia and Highway to Health, part of Bupa Global North America)

(2) Chart includes 100% of Bupa revenues from all businesses to give a sense of scale

Insurance

Provision

7.2m

0.7m

Overview Financial review Outlook & operating priorities

Section 2

Financial review

Joy Linton, CFO

Gareth Evans, Group Treasurer

13

Overview Financial review Outlook & operating priorities

Strong financial management discipline with focus on sustainable growth

FY 2016 Financial overview

Debt restructured

Financial highlights:

Strong cash generation

Robust capital base

Credit rating improved

14

Overview Financial review Outlook & operating priorities

Continued growth in revenue and underlying profit

15

FY 2016 Financial overview

Revenue

Underlying profit before tax(2)

FY 2016

FY 2015 (CER)

£11.0bn

£10.6bn

• Revenue increased by 4%, with good growth in

Australia and New Zealand, UK(1) and Europe and

Latin America

• Excluding the impact of the IFRIC 12 non-cash

adjustment relating to our Spanish PPPs in 2015(4),

underlying profit before taxation is up 2% at CER

and up 12% at AER

FY 2016

FY 2015 (CER)

£700.7m

£638.1m

(1) Like for like growth when adjusted for the disposal of Bupa Home Healthcare in July 2016.

(2) In order to reflect trading performance in a consistent manner year on year, a number of non-trading items that limit comparability are removed from our statutory profit before tax to arrive at underlying profit. This

distinguishes underlying profit from other constituents of the statutory profit before tax, excluding items relating to business combinations and disposals, fluctuations in foreign exchange, property revaluations and

investment returns on return-seeking assets, along with other one-off items.

(3) Underlying profit is up 2% at CER and up 12% at AER when excluding the impact of the IFRIC 12 adjustment relating to our Spanish Public-Private Partnerships (PPPs) in 2015

(4) Under IFRIC 12, which applies to service concession contracts such as PPPs, we use the average operating margin for the life of the contract (based on historic performance plus projections) as a means for recognising

results. Once there is a change in performance compared to expectations, the operating margin is reassessed and an adjustment made to the current year results to bring the contract performance to date in line with the

revised margin. In 2015, this non-cash adjustment of £52m included an amount relating to the current year of £8.8m together with a retrospective adjustment for the years preceding 2015 of £43.2m. To compare the

result on a “like for like’ basis with 2016, we have excluded £48.6m (being £43.2m retranslated at 2016 rates) from underlying profit in 2015.

+4% at CER

+12% at AER

+10% at CER

+2%(3) at CER

+20% at AER

Overview Financial review Outlook & operating priorities

Statutory profit up 40%

16

FY 2016 Financial overview

Revenue

Statutory profit before tax

+4% at CER

+12% at AER FY 2016

FY 2015 (CER)

£11.0bn

£10.6bn

• No significant write downs in 2016 compared to

£181.9m in the UK Care Services business in 2015

• Net loss of £112.3m on the redemption of the

secured loan notes in April 2016

• Favourable FX movements

+40% at AER FY 2016

FY 2015 (AER) £374.3m

Underlying profit before tax

+10% at CER

+2% at CER FY 2016

FY 2015 (CER)

£700.7m

£638.1m

£522.9m

+20% at AER

Overview Financial review Outlook & operating priorities

Continued strong cash generation

17

FY 2016 Financial overview

Revenue

Net cash generated from operating activities

+4% at CER

+12% at AER FY 2016

FY 2015 (CER)

£11.0bn

£10.6bn

• Strong net cash generated from operating

activities with £102.9m increase

• Increase driven by growth in earnings, positive

working capital movements in ANZ and

favourable impact of FX

FY 2016

FY 2015 (AER)

£891.0m

£788.1m

Underlying profit before tax

FY 2016

FY 2015 (CER)

£700.7m

£638.1m

Statutory profit before tax

+40% at AER FY 2016

FY 2015 (AER)

£522.9m

£374.3m

+13% at AER

+10% at CER

+2% at CER

+20% at AER

Overview Financial review Outlook & operating priorities

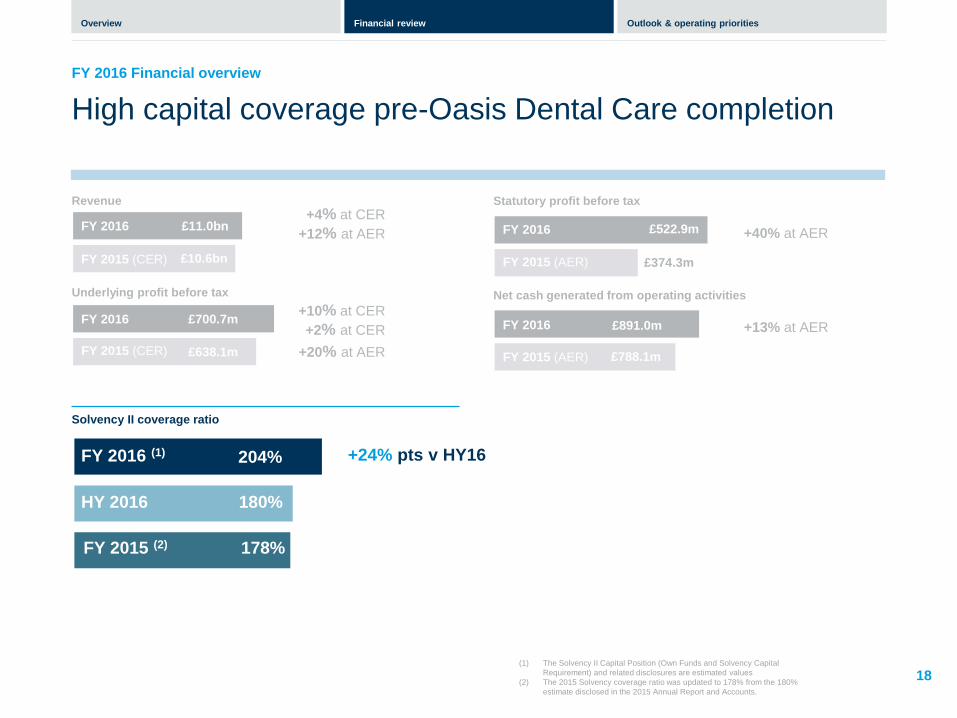

High capital coverage pre-Oasis Dental Care completion

18

FY 2016 Financial overview

Revenue

Solvency II coverage ratio

+4% at CER

+12% at AER FY 2016

FY 2015 (CER)

£11.0bn

£10.6bn

+24% pts v HY16 FY 2016 (1)

HY 2016

204%

180%

(1) The Solvency II Capital Position (Own Funds and Solvency Capital

Requirement) and related disclosures are estimated values

(2) The 2015 Solvency coverage ratio was updated to 178% from the 180%

estimate disclosed in the 2015 Annual Report and Accounts.

Underlying profit before tax

FY 2016

FY 2015 (CER)

£700.7m

£638.1m

Statutory profit before tax

+40% at AER FY 2016

FY 2015 (AER)

£522.9m

£374.3m

Net cash generated from operating activities

+13% at AER FY 2016

FY 2015 (AER)

£891.0m

£788.1m

FY 2015 (2) 178%

+10% at CER

+2% at CER

+20% at AER

Overview Financial review Outlook & operating priorities

Estimated Solvency capital coverage ratio: 204%, pre-Oasis

19

Solvency

Solvency II coverage ratio

Risk sensitivities

204%(1) HY 2016

HY 2015 (AER)

180% FY 2016

HY 2016

Own funds £4.2bn

£2.1bn SCR

HY 2016 HY 2015 (AER)

180%

Own funds £3.4bn

SCR

coverage

(1) The Solvency II Capital Position (Own Funds and Solvency Capital

Requirement) and related disclosures are estimated values

Solvency coverage ratio

Interest rate +/- 100bps

Credit spreads + 100bps assuming no credit transaction

SCR

SCR

SCR

SCR

SCR 196%

201%

203%

201%

193%

204%

204%

204%

204%

0 50 100 150 200

Solvency Coverage Ratio

Interest rate +/- 100bps

Credit spreads + 100bps assuming no credit transaction

Equity markets - 20%

Property values – 10%

GBP appreciates by 10%

Pension risk +10%

USP + 0.2%

• As Bupa generates substantial profits

and cash surpluses, solvency

capital builds relatively quickly

• A £400m tier 2 subordinated bond

issued in December 2016 is a key

contributor to the 24% increase in

coverage

• Bupa’s Solvency II capital position is

relatively insensitive to market related

risks Loss ratio worsening by 2%

FY 2015

£1.9bn

Own funds £3.1bn

SCR £1.8bn

Overview Financial review Outlook & operating priorities

Leverage down following cash repatriations and favourable FX movements

20

FY 2016 Financial overview

Revenue

Leverage(1)

+4% at CER

+12% at AER FY 2016

FY 2015 (CER)

£11.0bn

£10.6bn

FY 2016

HY 2016

22.6%

24.3%

Underlying profit before tax

FY 2016

FY 2015 (CER)

£700.7m

£638.1m

Statutory profit before tax

+40% at AER FY 2016

FY 2015 (AER)

£522.9m

£374.3m

Net cash generated from operating activities

+13% at AER FY 2016

FY 2015 (AER)

£891.0m

£788.1m

Solvency II coverage ratio

+24% pts v HY16 FY 2016

HY 2016

204%

180%

(1) Gross debt (including hybrid debt) / gross debt plus equity

-1.7% pts v HY16

FY 2015 27.7%

FY 2015 178%

+10% at CER

+2% at CER

+20% at AER

Overview Financial review Outlook & operating priorities

A strong year for funding as leverage reduced and our senior debt rating improved

21

FY 2016 Financial overview

Leverage

27.6%

28.0%

27.7%

24.3%

22.6% Dec-16

Dec-15

Jun-15

Dec-14

Jun-18 Debt maturity profile at 31 December 2016

Jun-16

0

200

400

600

800

1000

1200

£m

Bupa Finance plc Tier 2 Subordinated

Bupa Finance plc Senior

Bupa Finance plc Tier 1 Subordinated perpetual guaranteed

Other Senior unsecured

Bank Loans

• Leverage fell to 22.6% (HY16: 24.3%)

• Good cash repatriations and favourable FX

• Senior debt ratings A- (Fitch) and Baa1

(Moody’s) following one notch Moody’s

upgrade in September

• Simpler debt structure following bond

maturity and securitisation redemption

• £650m acquisition facility signed January

2017 to part fund Oasis Dental Care

purchase

Other

Overview Financial review Outlook & operating priorities

Good bond returns; we continue to manage cash prudently

22

FY 2016 Financial overview

CASH AND INVESTMENT PORTFOLIO • £3.6bn cash and financial investments

• Approximately 86% of portfolio held in

investments rated at least A-/A3

• £367m return-seeking assets (externally-

managed bond and loan funds) held in UK

and Australian regulated entities

• Good returns in 2016 from bond and loan

portfolio £22.9m (2015 £7.0m)

• Low yield environment continues to provide

a challenging investment backdrop

FY16

Jun-18 FY16 CASH AND INVESTMENTS BY CREDIT RATING (%)

HY 16

£3.6bn

£3.6bn

Cash (e.g. deposits, liquidity funds)

Return seeking assets

FY 15 £3.4bn

Overview Financial review Outlook & operating priorities

Section 3

Outlook and operating priorities Evelyn Bourke, Group CEO

23

Overview Financial review Outlook & operating priorities

Market conditions remain challenging; focused on enhancing our services for customers in this digital age

Outlook and operating priorities

Outlook:

Operating priorities:

• Demand for high quality, value-for-money healthcare

expected to remain strong

• Consumer and government affordability pressures with

medical costs outpacing inflation

• Changing political environments, including UK preparing

to exit the EU

• Rapidly-changing customer standards of personalisation,

ease and choice; high expectations of quality, safety,

privacy and transparency

• High quality, value-for-money services in the digital age

• Empowering our people to deliver for our customers

• Focus on management of risk and compliance, upholding

the high standards our customers and regulators expect

• Disciplined capital management

• Investing in growth in our key existing markets; selective

expansion into new growth markets

Overview Financial review Outlook & operating priorities

Questions and answers

25

Overview Financial review Outlook & operating priorities

Appendices

26

Overview Financial review Outlook & operating priorities

Organisation structure

27

Market Units

Australia and New Zealand

• Bupa Health Insurance

• Bupa Health Services

• Bupa Aged Care Australia

• New Zealand Care Services

(1) The sale of Bupa Home Healthcare to Celesio completed on 1 July 2016

(2) Bupa completed the purchase of Oasis Dental Care on 09 February 2017

Appendix

UK (1) Europe & Latin America

International Markets

• Bupa UK Insurance

• Bupa Care Services

• Bupa Health Clinics

• Bupa Cromwell Hospital

• Oasis Dental Care (2)

• Sanitas Seguros

• Sanitas Hospitales and

New Services

• Sanitas Dental

• Sanitas Mayores

• LUX MED

• Bupa Chile

• Bupa Global

• Bupa Arabia

• Bupa Hong Kong

• Quality HealthCare

(Hong Kong)

• Max Bupa (India)

• Bupa Thailand

• Bupa China

Overview Financial review Outlook & operating priorities

Bupa’s footprint and participation

28

Appendix

Hong

Kong Thailand India (1)

Saudi

Arabia (1) Poland

International Markets

Funding

Healthcare

provision

UK

UK

Spain

Europe and Latin

America

Chile Australia New

Zealand

Australia and

New Zealand

Private medical insurance

Pay-as-you-go

Dental insurance

Clinics

Hospitals

Dental clinics

Bupa

Global

Optical

Travel insurance

Aged care

provision

Care homes

Retirement villages

4.0m 2.4m 2.9m 7.2m

(1) Bupa Arabia in Saudi Arabia and Max Bupa in India are associate businesses

(2) Global international insurance available in most countries. Includes 49% stake in Highway to Health (GeoBlue) in

the US

(3) Excludes Oasis Dental Care 2017

(4) Domestic insurance and clinics in Brazil

(5) In addition to Quality HealthCare Hong Kong, two clinics in development in Guangzhou, China

(6) Home healthcare rather than care homes

(7) In addition to care homes, New Zealand also has brain rehabilitation and home alarm businesses

(7)

1.9m 1.2m (3) 0.7m 6.7m

10,800 17,400 4,900

Funding customers

Provision customers

Aged care residents

(2)

(4) (5)

(6)

Overview Financial review Outlook & operating priorities

Breakdown of borrowings

29

FY 2016 £m

HY 2016 £m

FY 2015 £m

Borrowings under £800m bank facility 0 90 -

£500m subordinated bond due 2023 501 500 500

£330m perpetual hybrid bond (g’teed by Bupa Insurance Ltd) 387 407 387

£350m senior bond due 2016 - 363 363

£350m senior bond due 2021 348 348 348

£400m subordinated bond due 2026 395 - -

£235m care homes securitisation due 2029 / 2031 - - 238

Bupa Chile borrowings 207 197 153

Other 83 83 85

Total borrowings 1,921 1,988 2,074

Appendix

Overview Financial review Outlook & operating priorities

Analysis of Bupa’s Solvency Capital Requirement

30

FY 2016 HY 2016 FY 2015

Insurance risk 19% 23% 19%

Market risk 60% 56% 61%

Spread risk 2% 2% 3%

Equity risk 2% 2% 1%

Property risk 34% 32% 31%

Currency risk 16% 12% 13%

Pension scheme 6% 8% 13%

Counterparty risk 4% 3% 3%

Operational risk 11% 11% 11%

Participations (Associates and JVs) 6% 7% 6%

Total 100% 100% 100%

Appendix

Overview Financial review Outlook & operating priorities

Cautionary statement concerning forward-looking statements

31

This document may contain certain forward-looking statements with respect to certain of the British United Provident Association Limited Group’s (“Bupa’s”) plans and its current goals and expectations relating to future financial condition,

performance and results.

By their nature forward-looking statements involve risk and uncertainty because they relate to future events and circumstances which are beyond Bupa’s control, including, among others, global economic and business conditions, market related risks such as fluctuations in interest rates and exchange rates, the policies and actions of governmental and regulatory authorities, the impact of competition, the

timing, impact and other uncertainties of future mergers or combinations within relevant industries. As a result, Bupa’s actual future condition, performance and results may differ materially from the plans, goals and expectations set out in

Bupa’s forward-looking statements. Bupa does not undertake to update forward-looking statements contained in this document or any other forward-looking statement it may make.

Disclaimer