FULL YEAR RESULTS PRESENTATION 2013 - SThreeFULL YEAR RESULTS PRESENTATION 2013 RESULTS FOR THE YEAR...

67

FULL YEAR RESULTS PRESENTATION 2013 RESULTS FOR YEAR ENDED 1 DECEMBER 2013

Transcript of FULL YEAR RESULTS PRESENTATION 2013 - SThreeFULL YEAR RESULTS PRESENTATION 2013 RESULTS FOR THE YEAR...

FULL YEAR RESULTS PRESENTATION 2013RESULTS FOR YEAR ENDED 1 DECEMBER 2013

www.sthree.com | SThree plc 2

FULL YEAR RESULTSPRESENTATION 2013RESULTS FOR THE YEAR ENDED 1 DECEMBER 2013

INTRODUCTION & OVERVIEW

FULL YEAR RESULTSPRESENTATION 2013RESULTS FOR THE YEAR ENDED 1 DECEMBER 2013

www.sthree.com | SThree plc 3

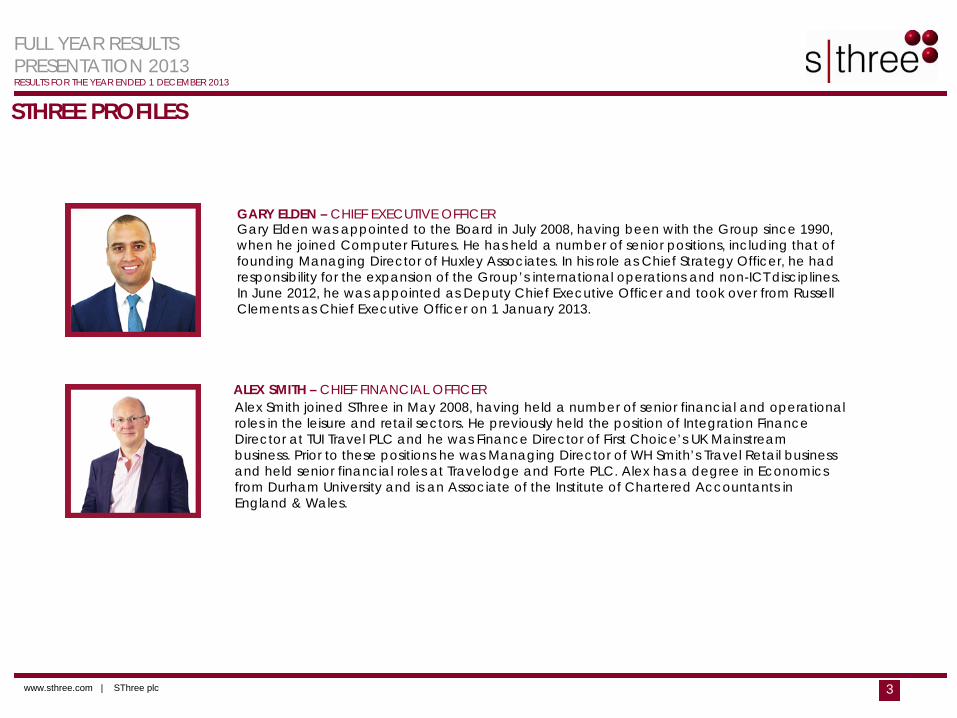

STHREE PROFILES

GARY ELDEN – CHIEF EXECUTIVE OFFICER

ALEX SMITH – CHIEF FINANCIAL OFFICER

Gary Elden was appointed to the Board in July 2008, having been with the Group since 1990, when he joined Computer Futures. He has held a number of senior positions, including that of founding Managing Director of Huxley Associates. In his role as Chief Strategy Officer, he had responsibility for the expansion of the Group’s international operations and non-ICT disciplines. In June 2012, he was appointed as Deputy Chief Executive Officer and took over from Russell Clements as Chief Executive Officer on 1 January 2013.

Alex Smith joined SThree in May 2008, having held a number of senior financial and operational roles in the leisure and retail sectors. He previously held the position of Integration Finance Director at TUI Travel PLC and he was Finance Director of First Choice’s UK Mainstream business. Prior to these positions he was Managing Director of WH Smith’s Travel Retail business and held senior financial roles at Travelodge and Forte PLC. Alex has a degree in Economics from Durham University and is an Associate of the Institute of Chartered Accountants in England & Wales.

FULL YEAR RESULTSPRESENTATION 2013RESULTS FOR THE YEAR ENDED 1 DECEMBER 2013

www.sthree.com | SThree plc 4

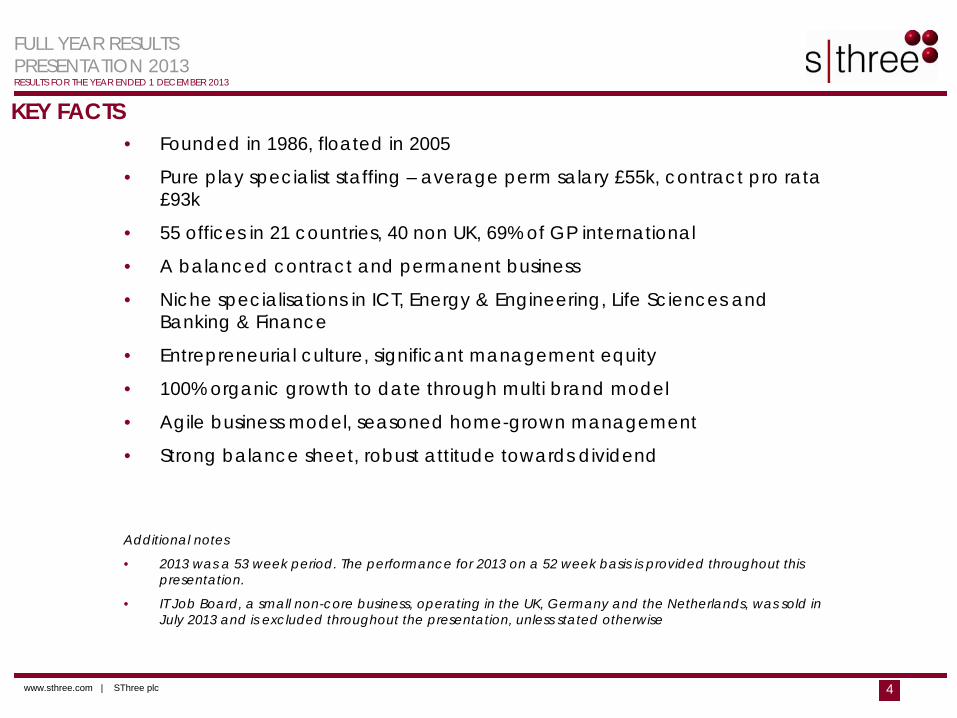

• Founded in 1986, floated in 2005

• Pure play specialist staffing – average perm salary £55k, contract pro rata £93k

• 55 offices in 21 countries, 40 non UK, 69% of GP international

• A balanced contract and permanent business

• Niche specialisations in ICT, Energy & Engineering, Life Sciences and Banking & Finance

• Entrepreneurial culture, significant management equity

• 100% organic growth to date through multi brand model

• Agile business model, seasoned home-grown management

• Strong balance sheet, robust attitude towards dividend

KEY FACTS

Additional notes

• 2013 was a 53 week period. The performance for 2013 on a 52 week basis is provided throughout this presentation.

• IT Job Board, a small non-core business, operating in the UK, Germany and the Netherlands, was sold in July 2013 and is excluded throughout the presentation, unless stated otherwise

FULL YEAR RESULTSPRESENTATION 2013RESULTS FOR THE YEAR ENDED 1 DECEMBER 2013

www.sthree.com | SThree plc 5

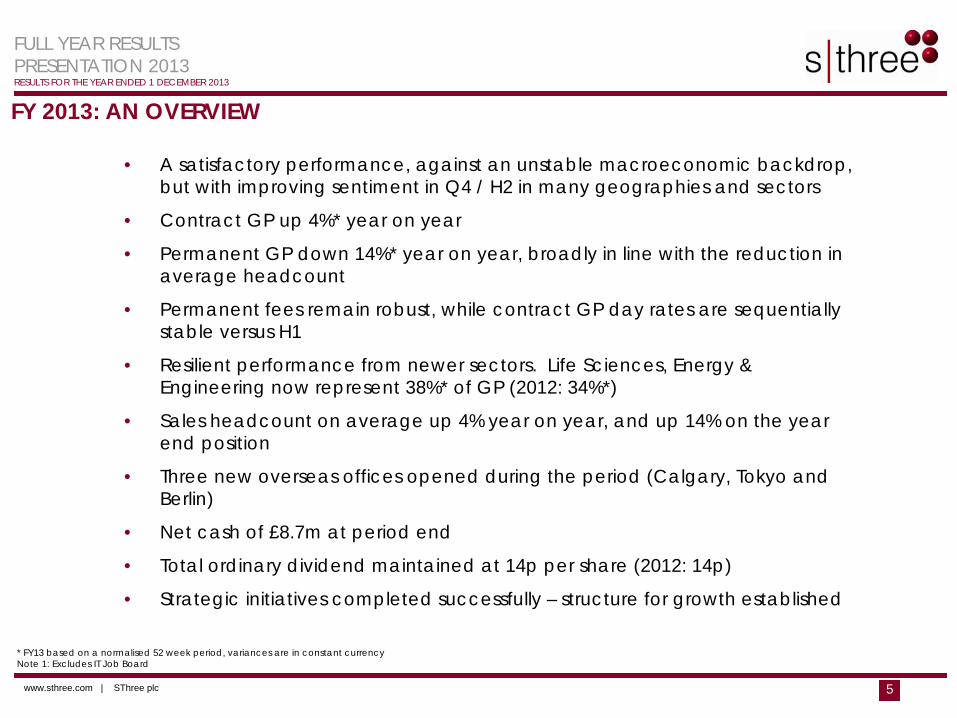

FY 2013: AN OVERVIEW

* FY13 based on a normalised 52 week period, variances are in constant currencyNote 1: Excludes IT Job Board

• A satisfactory performance, against an unstable macroeconomic backdrop, but with improving sentiment in Q4 / H2 in many geographies and sectors

• Contract GP up 4%* year on year

• Permanent GP down 14%* year on year, broadly in line with the reduction in average headcount

• Permanent fees remain robust, while contract GP day rates are sequentially stable versus H1

• Resilient performance from newer sectors. Life Sciences, Energy & Engineering now represent 38%* of GP (2012: 34%*)

• Sales headcount on average up 4% year on year, and up 14% on the year end position

• Three new overseas offices opened during the period (Calgary, Tokyo and Berlin)

• Net cash of £8.7m at period end

• Total ordinary dividend maintained at 14p per share (2012: 14p)

• Strategic initiatives completed successfully – structure for growth established

www.sthree.com | SThree plc 6

FULL YEAR RESULTSPRESENTATION 2013RESULTS FOR THE YEAR ENDED 1 DECEMBER 2013

FINANCIAL RESULTS

FULL YEAR RESULTSPRESENTATION 2013RESULTS FOR THE YEAR ENDED 1 DECEMBER 2013

www.sthree.com | SThree plc 7

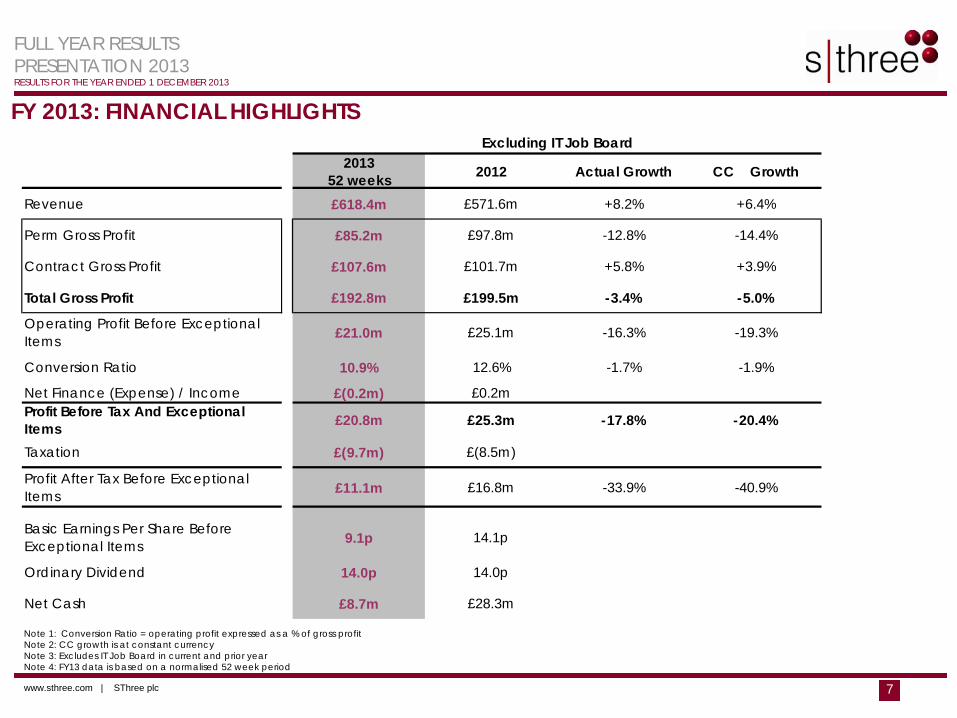

FY 2013: FINANCIAL HIGHLIGHTS

Note 1: Conversion Ratio = operating profit expressed as a % of gross profitNote 2: CC growth is at constant currencyNote 3: Excludes IT Job Board in current and prior yearNote 4: FY13 data is based on a normalised 52 week period

2013 52 weeks 2012 Actual Growth CC Growth

Revenue £618.4m £571.6m +8.2% +6.4%

Perm Gross Profit £85.2m £97.8m -12.8% -14.4%

Contract Gross Profit £107.6m £101.7m +5.8% +3.9%

Total Gross Profit £192.8m £199.5m -3.4% -5.0%

Operating Profit Before Exceptional Items £21.0m £25.1m -16.3% -19.3%

Conversion Ratio 10.9% 12.6% -1.7% -1.9%

Net Finance (Expense) / Income £(0.2m) £0.2mProfit Before Tax And Exceptional Items £20.8m £25.3m -17.8% -20.4%

Taxation £(9.7m) £(8.5m)

Profit After Tax Before Exceptional Items £11.1m £16.8m -33.9% -40.9%

Basic Earnings Per Share Before Exceptional Items 9.1p 14.1p

Ordinary Dividend 14.0p 14.0p

Net Cash £8.7m £28.3m

Excluding IT Job Board

FULL YEAR RESULTSPRESENTATION 2013RESULTS FOR THE YEAR ENDED 1 DECEMBER 2013

www.sthree.com | SThree plc 8

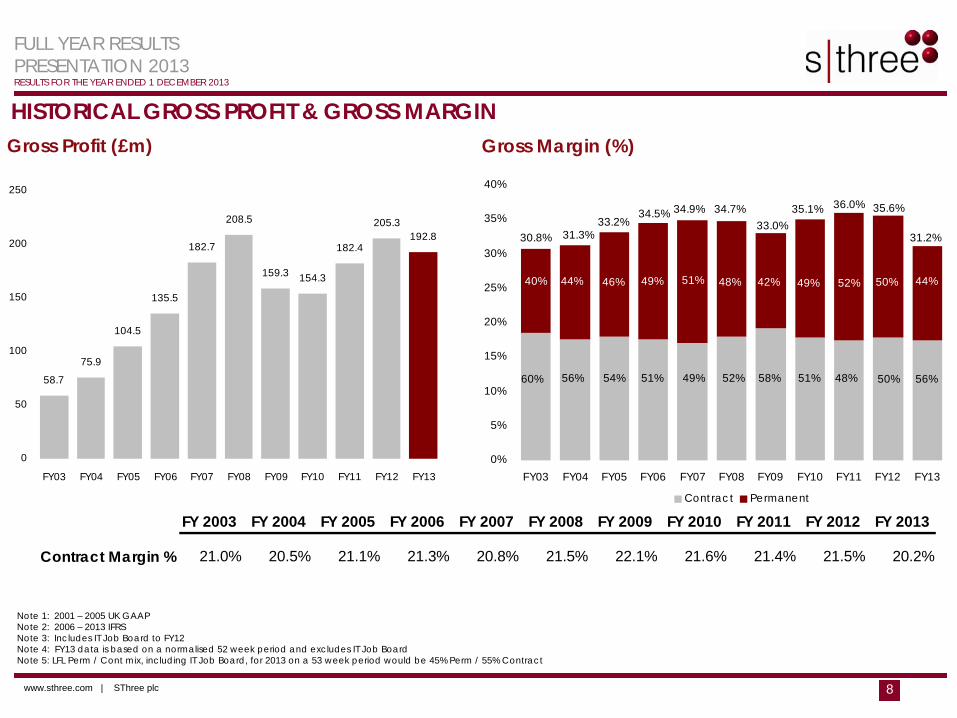

HISTORICAL GROSS PROFIT & GROSS MARGINGross Profit (£m) Gross Margin (%)

Note 1: 2001 – 2005 UK GAAPNote 2: 2006 – 2013 IFRSNote 3: Includes IT Job Board to FY12Note 4: FY13 data is based on a normalised 52 week period and excludes IT Job BoardNote 5: LFL Perm / Cont mix, including IT Job Board, for 2013 on a 53 week period would be 45% Perm / 55% Contract

FY 2003 FY 2004 FY 2005 FY 2006 FY 2007 FY 2008 FY 2009 FY 2010 FY 2011 FY 2012 FY 2013

Contract Margin % 21.0% 20.5% 21.1% 21.3% 20.8% 21.5% 22.1% 21.6% 21.4% 21.5% 20.2%

58.7

75.9

104.5

135.5

182.7

208.5

159.3 154.3

182.4

205.3192.8

0

50

100

150

200

250

FY03 FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY130%

5%

10%

15%

20%

25%

30%

35%

40%

FY03 FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13

Contract Permanent

30.8% 31.3%33.2%

34.5% 34.7%33.0%

35.1% 36.0%

40% 44% 46% 49% 51% 48% 42% 49% 52%

48%51%58%51% 52%49%54%56%60%

50%

35.6%

50%

44%

56%

31.2%

34.9%

FULL YEAR RESULTSPRESENTATION 2013RESULTS FOR THE YEAR ENDED 1 DECEMBER 2013

www.sthree.com | SThree plc 9

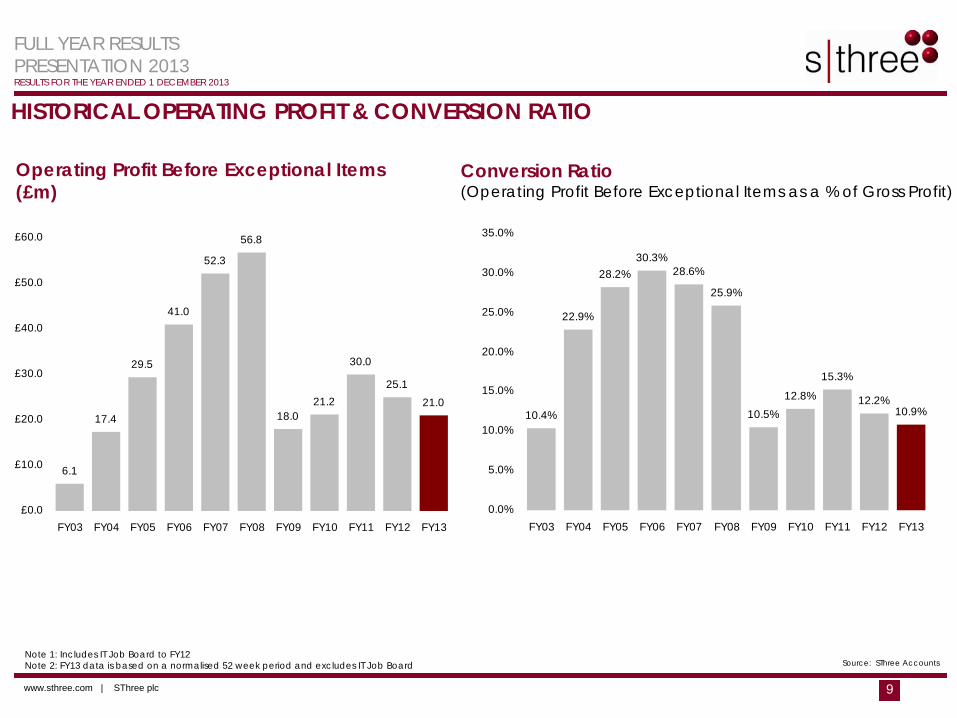

HISTORICAL OPERATING PROFIT & CONVERSION RATIO

Conversion Ratio (Operating Profit Before Exceptional Items as a % of Gross Profit)

Operating Profit Before Exceptional Items (£m)

Note 1: Includes IT Job Board to FY12Note 2: FY13 data is based on a normalised 52 week period and excludes IT Job Board Source: SThree Accounts

6.1

17.4

29.5

41.0

52.3

56.8

18.021.2

30.0

25.1

21.0

£0.0

£10.0

£20.0

£30.0

£40.0

£50.0

£60.0

FY03 FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13

10.4%

22.9%

28.2%30.3%

28.6%

25.9%

10.5%

12.8%

15.3%

12.2%10.9%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

FY03 FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13

FULL YEAR RESULTSPRESENTATION 2013RESULTS FOR THE YEAR ENDED 1 DECEMBER 2013

www.sthree.com | SThree plc 10

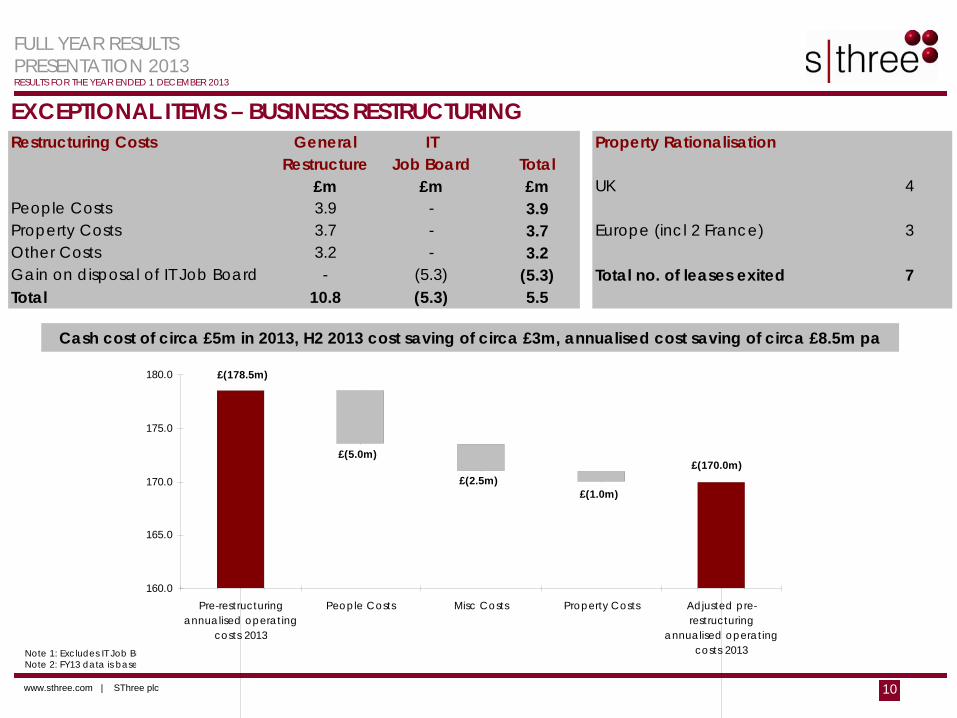

EXCEPTIONAL ITEMS – BUSINESS RESTRUCTURING

Cash cost of circa £5m in 2013, H2 2013 cost saving of circa £3m, annualised cost saving of circa £8.5m pa

£178.3m

£169.8m

Note 1: Excludes IT Job BoardNote 2: FY13 data is based on a 52 week period

Restructuring Costs General IT Property RationalisationRestructure Job Board Total

£m £m £m UK 4People Costs 3.9 - 3.9Property Costs 3.7 - 3.7 Europe (incl 2 France) 3Other Costs 3.2 - 3.2Gain on disposal of IT Job Board - (5.3) (5.3) Total no. of leases exited 7Total 10.8 (5.3) 5.5

160.0

165.0

170.0

175.0

180.0

Pre-restructuringannualised operating

costs 2013

People Costs Misc Costs Property Costs Adjusted pre-restructuring

annualised operatingcosts 2013

£(178.5m)

£(5.0m)

£(2.5m)£(1.0m)

£(170.0m)

FULL YEAR RESULTSPRESENTATION 2013RESULTS FOR THE YEAR ENDED 1 DECEMBER 2013

www.sthree.com | SThree plc 11

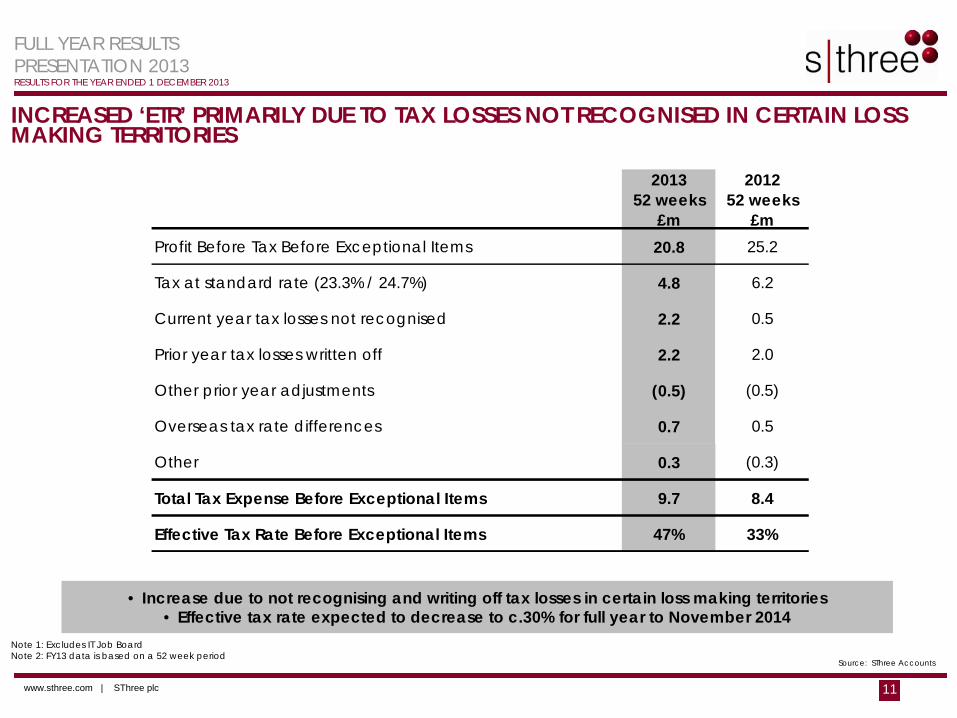

INCREASED ‘ETR’ PRIMARILY DUE TO TAX LOSSES NOT RECOGNISED IN CERTAIN LOSS MAKING TERRITORIES

Source: SThree Accounts

• Increase due to not recognising and writing off tax losses in certain loss making territories• Effective tax rate expected to decrease to c.30% for full year to November 2014

Note 1: Excludes IT Job BoardNote 2: FY13 data is based on a 52 week period

2013 52 weeks

£m

2012 52 weeks

£mProfit Before Tax Before Exceptional Items 20.8 25.2

Tax at standard rate (23.3% / 24.7%) 4.8 6.2

Current year tax losses not recognised 2.2 0.5

Prior year tax losses written off 2.2 2.0

Other prior year adjustments (0.5) (0.5)

Overseas tax rate differences 0.7 0.5

Other 0.3 (0.3)

Total Tax Expense Before Exceptional Items 9.7 8.4

Effective Tax Rate Before Exceptional Items 47% 33%

FULL YEAR RESULTSPRESENTATION 2013RESULTS FOR THE YEAR ENDED 1 DECEMBER 2013

www.sthree.com | SThree plc 12

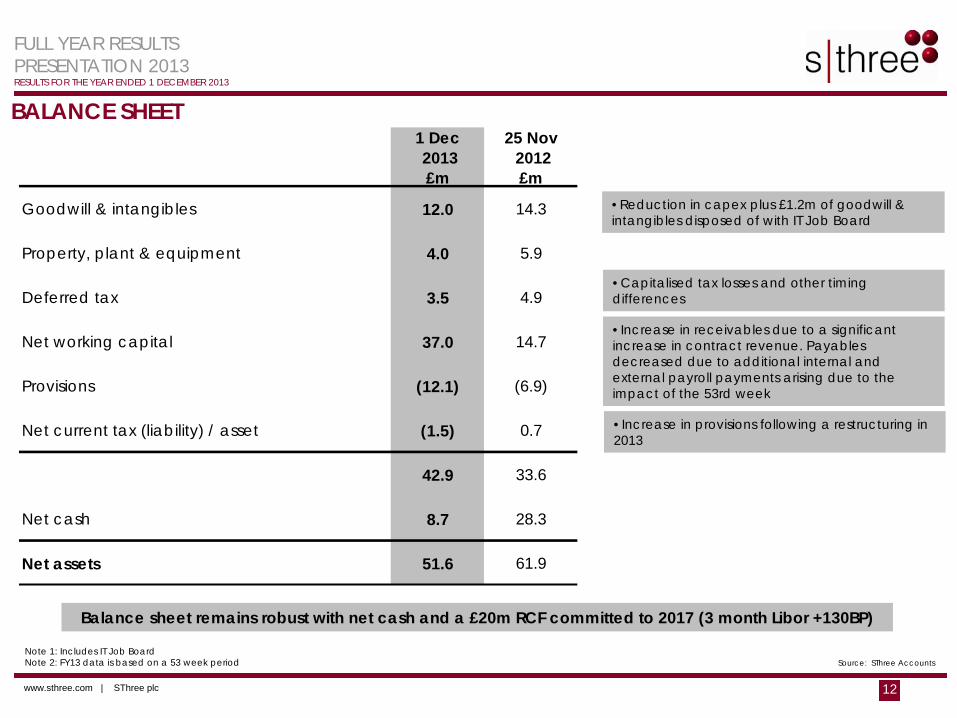

BALANCE SHEET

Source: SThree Accounts

Balance sheet remains robust with net cash and a £20m RCF committed to 2017 (3 month Libor +130BP)

Note 1: Includes IT Job BoardNote 2: FY13 data is based on a 53 week period

•Reduction in capex plus £1.2m of goodwill & intangibles disposed of with IT Job Board

•Capitalised tax losses and other timing differences

•Increase in receivables due to a significant increase in contract revenue. Payables decreased due to additional internal and external payroll payments arising due to the impact of the 53rd week

•Increase in provisions following a restructuring in 2013

1 Dec 2013 £m

25 Nov 2012 £m

Goodwill & intangibles 12.0 14.3

Property, plant & equipment 4.0 5.9

Deferred tax 3.5 4.9

Net working capital 37.0 14.7

Provisions (12.1) (6.9)

Net current tax (liability) / asset (1.5) 0.7

42.9 33.6

Net cash 8.7 28.3

Net assets 51.6 61.9

FULL YEAR RESULTSPRESENTATION 2013RESULTS FOR THE YEAR ENDED 1 DECEMBER 2013

www.sthree.com | SThree plc 13

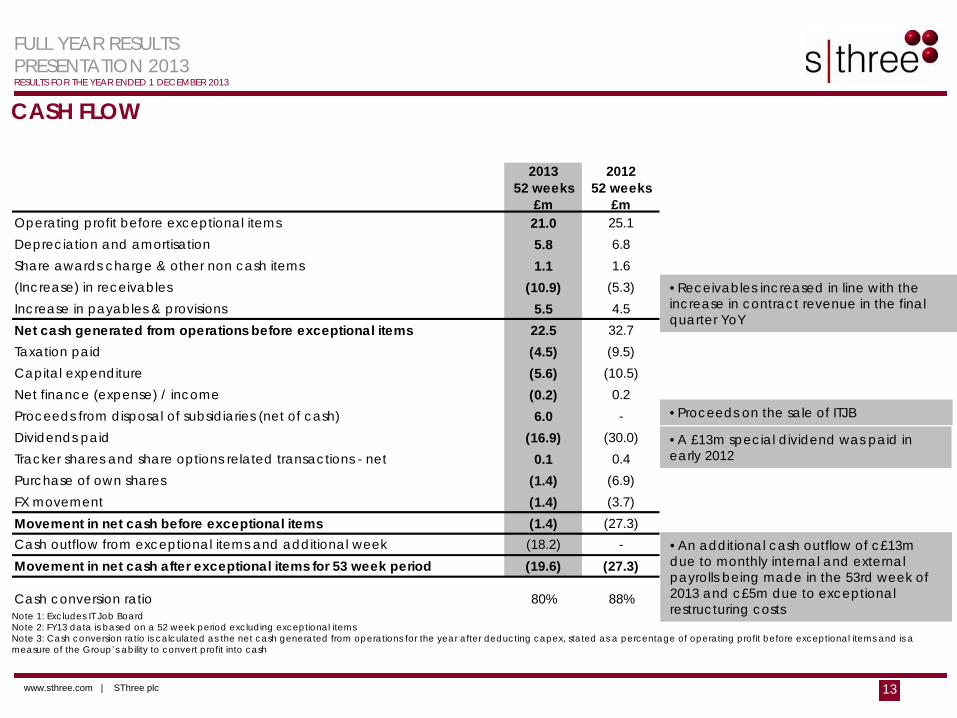

CASH FLOW

Note 1: Excludes IT Job BoardNote 2: FY13 data is based on a 52 week period excluding exceptional itemsNote 3: Cash conversion ratio is calculated as the net cash generated from operations for the year after deducting capex, stated as a percentage of operating profit before exceptional items and is a measure of the Group’s ability to convert profit into cash

•Proceeds on the sale of ITJB

•Receivables increased in line with the increase in contract revenue in the final quarter YoY

•An additional cash outflow of c£13m due to monthly internal and external payrolls being made in the 53rd week of 2013 and c£5m due to exceptional restructuring costs

•A £13m special dividend was paid in early 2012

2013 52 weeks

£m

2012 52 weeks

£mOperating profit before exceptional items 21.0 25.1Depreciation and amortisation 5.8 6.8Share awards charge & other non cash items 1.1 1.6(Increase) in receivables (10.9) (5.3)Increase in payables & provisions 5.5 4.5Net cash generated from operations before exceptional items 22.5 32.7Taxation paid (4.5) (9.5)Capital expenditure (5.6) (10.5)Net finance (expense) / income (0.2) 0.2Proceeds from disposal of subsidiaries (net of cash) 6.0 -Dividends paid (16.9) (30.0)Tracker shares and share options related transactions - net 0.1 0.4Purchase of own shares (1.4) (6.9)FX movement (1.4) (3.7)Movement in net cash before exceptional items (1.4) (27.3)Cash outflow from exceptional items and additional week (18.2) -Movement in net cash after exceptional items for 53 week period (19.6) (27.3)

Cash conversion ratio 80% 88%

FULL YEAR RESULTSPRESENTATION 2013RESULTS FOR THE YEAR ENDED 1 DECEMBER 2013

www.sthree.com | SThree plc 14

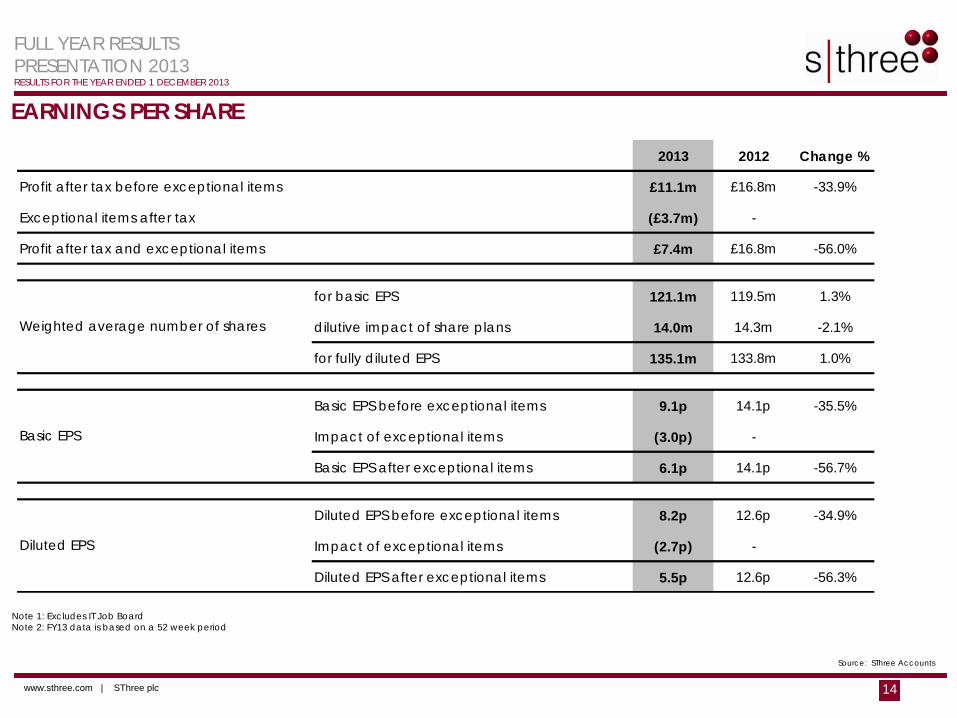

EARNINGS PER SHARE

Source: SThree Accounts

Note 1: Excludes IT Job BoardNote 2: FY13 data is based on a 52 week period

2013 2012 Change %

Profit after tax before exceptional items £11.1m £16.8m -33.9%

Exceptional items after tax (£3.7m) -

Profit after tax and exceptional items £7.4m £16.8m -56.0%

for basic EPS 121.1m 119.5m 1.3%

dilutive impact of share plans 14.0m 14.3m -2.1%

for fully diluted EPS 135.1m 133.8m 1.0%

Basic EPS before exceptional items 9.1p 14.1p -35.5%

Impact of exceptional items (3.0p) -

Basic EPS after exceptional items 6.1p 14.1p -56.7%

Diluted EPS before exceptional items 8.2p 12.6p -34.9%

Impact of exceptional items (2.7p) -

Diluted EPS after exceptional items 5.5p 12.6p -56.3%

Weighted average number of shares

Basic EPS

Diluted EPS

FULL YEAR RESULTSPRESENTATION 2013RESULTS FOR THE YEAR ENDED 1 DECEMBER 2013

www.sthree.com | SThree plc 15

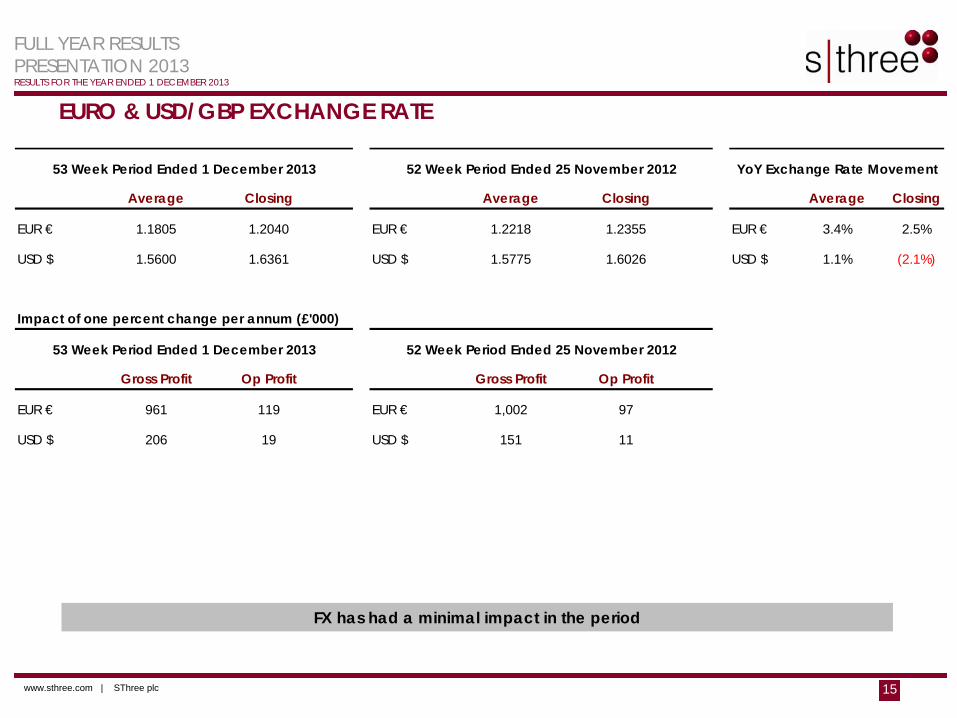

EURO & USD/GBP EXCHANGE RATE

FX has had a minimal impact in the period

Average Closing Average Closing Average Closing

EUR € 1.1805 1.2040 EUR € 1.2218 1.2355 EUR € 3.4% 2.5%

USD $ 1.5600 1.6361 USD $ 1.5775 1.6026 USD $ 1.1% (2.1%)

Impact of one percent change per annum (£'000)

Gross Profit Op Profit Gross Profit Op Profit

EUR € 961 119 EUR € 1,002 97

USD $ 206 19 USD $ 151 11

YoY Exchange Rate Movement53 Week Period Ended 1 December 2013 52 Week Period Ended 25 November 2012

52 Week Period Ended 25 November 201253 Week Period Ended 1 December 2013

www.sthree.com | SThree plc 16

FULL YEAR RESULTSPRESENTATION 2013RESULTS FOR THE YEAR ENDED 1 DECEMBER 2013

OPERATIONAL ANALYSIS

FULL YEAR RESULTSPRESENTATION 2013RESULTS FOR THE YEAR ENDED 1 DECEMBER 2013

www.sthree.com | SThree plc 17

STRATEGY - UPDATE• 2013 - Strong foundations laid for next phase of growth

• Management structure strengthened• Sector Heads appointed

• Regional CEOs appointed to high growth strategic geographies of Americas & APAC / MENA

• Investment in Contract headcount and new client-facing business structure

• After reduction in first half, permanent headcount increased 8% in second half of 2013

• Focus on longer term client relationships becoming culturally embedded in the business

• Contract margin controls in place & monitored daily

• Cost base rationalised

• 2014 – Focus on delivering against plan in the year ahead• Raising productivity as 2013 hires mature and further measured headcount investment

• Focus on driving up returns from our office portfolio following cost reduction initiative

• Significant further potential in continued roll-out of Life Sciences and Energy disciplines

• Building on recovery in Banking & Finance, ICT and Engineering, in line with growing economic confidence

• Remain fully committed to a balanced business model between Permanent and Contract

FULL YEAR RESULTSPRESENTATION 2013RESULTS FOR THE YEAR ENDED 1 DECEMBER 2013

www.sthree.com | SThree plc 18

STRATEGY – BUSINESS MIX• Clear focus on margin discipline & Life Time Contract Values

• Margins monitored on daily basis with real time reporting of margins on new deals and extensions

• Contract LTVs monitored on quarterly basis

• Prepared to trade some margin for higher volumes, but strong focus on margins remains and still focused on niche specialist roles

• Expect to see a recovery in margins in more mature UK & European markets as the global economic recovery takes hold

• Client mix evolving as growth profile changes business mix • SThree is seeing faster growth from sectors/geographies dominated by blue chip customers:

• e.g. client base in newer high growth sectors such as Energy and Life Sciences

• Rest of World tends to have a more blue chip client base than traditional UK/European markets

• Expect to see greater exposure to larger blue chip companies but remain committed to SME markets

FULL YEAR RESULTSPRESENTATION 2013RESULTS FOR THE YEAR ENDED 1 DECEMBER 2013

www.sthree.com | SThree plc 19

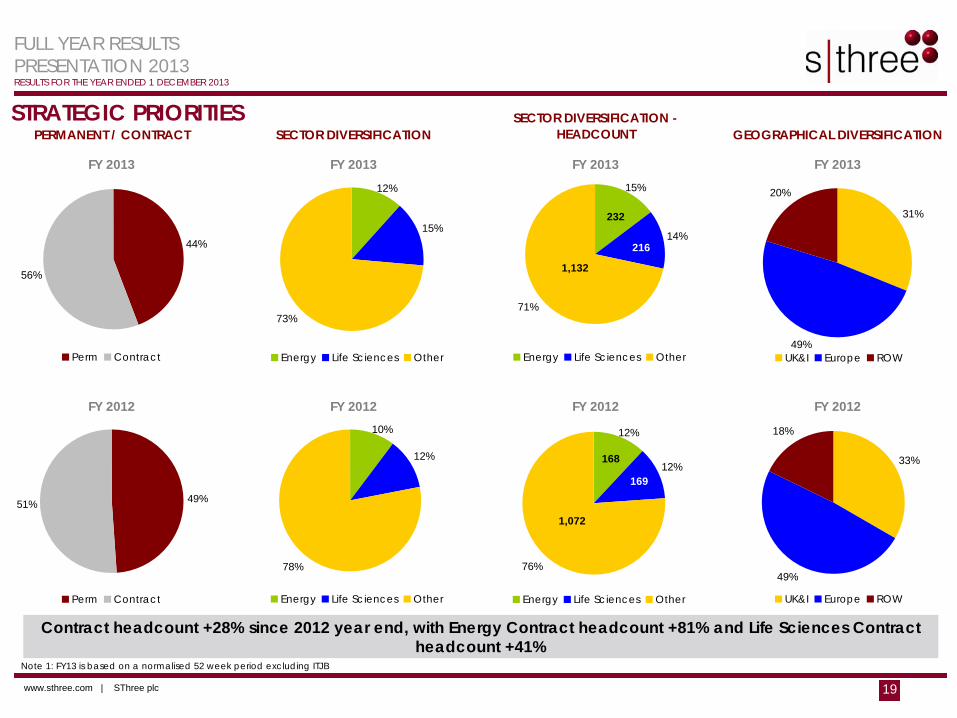

FY 2013

FY 2012FY 2012 FY 2012 FY 2012

GEOGRAPHICAL DIVERSIFICATIONSECTOR DIVERSIFICATIONPERMANENT / CONTRACT

FY 2013 FY 2013 FY 2013

SECTOR DIVERSIFICATION - HEADCOUNT

44%

56%

Perm Contract

15%

73%

12%

Energy Life Sciences Other

31%

49%

20%

UK&I Europe ROW

49%51%

Perm Contract

12%

78%

10%

Energy Life Sciences Other

33%

49%

18%

UK&I Europe ROW

14%

71%

15%

Energy Life Sciences Other

12%

76%

12%

Energy Life Sciences Other

STRATEGIC PRIORITIES

Note 1: FY13 is based on a normalised 52 week period excluding ITJB

Contract headcount +28% since 2012 year end, with Energy Contract headcount +81% and Life Sciences Contract headcount +41%

232

216

1,132

168

169

1,072

FULL YEAR RESULTSPRESENTATION 2013RESULTS FOR THE YEAR ENDED 1 DECEMBER 2013

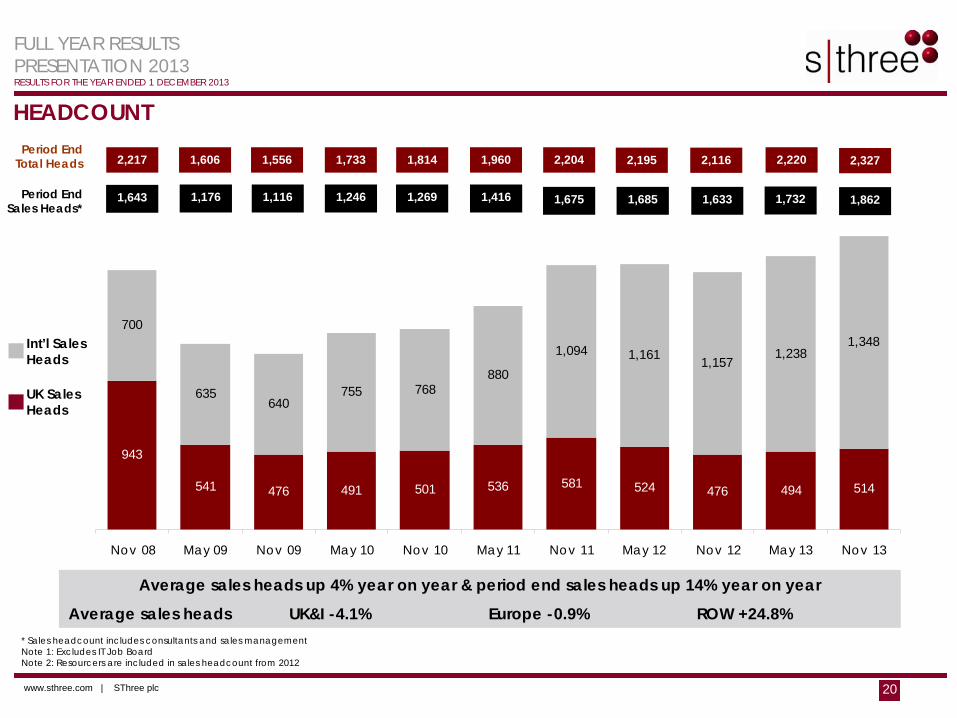

www.sthree.com | SThree plc 20

943

541 476 491 501 536 581 524 476 494 514

700

635640

755 768880

1,094 1,161 1,1571,238

1,348

Nov 08 May 09 Nov 09 May 10 Nov 10 May 11 Nov 11 May 12 Nov 12 May 13 Nov 13

HEADCOUNT

Average sales heads up 4% year on year & period end sales heads up 14% year on year

Average sales heads UK&I -4.1% Europe -0.9% ROW +24.8%

Int’l Sales Heads

UK Sales Heads

1,606 1,556 1,733 1,814 1,960 2,204 2,220

Period End Sales Heads*

1,176 1,116 1,246 1,269 1,416 1,675 1,732

2,195

1,685

2,116

1,633

Period End Total Heads

* Sales headcount includes consultants and sales managementNote 1: Excludes IT Job BoardNote 2: Resourcers are included in sales headcount from 2012

2,217

1,643

2,327

1,862

FULL YEAR RESULTSPRESENTATION 2013RESULTS FOR THE YEAR ENDED 1 DECEMBER 2013

www.sthree.com | SThree plc 21

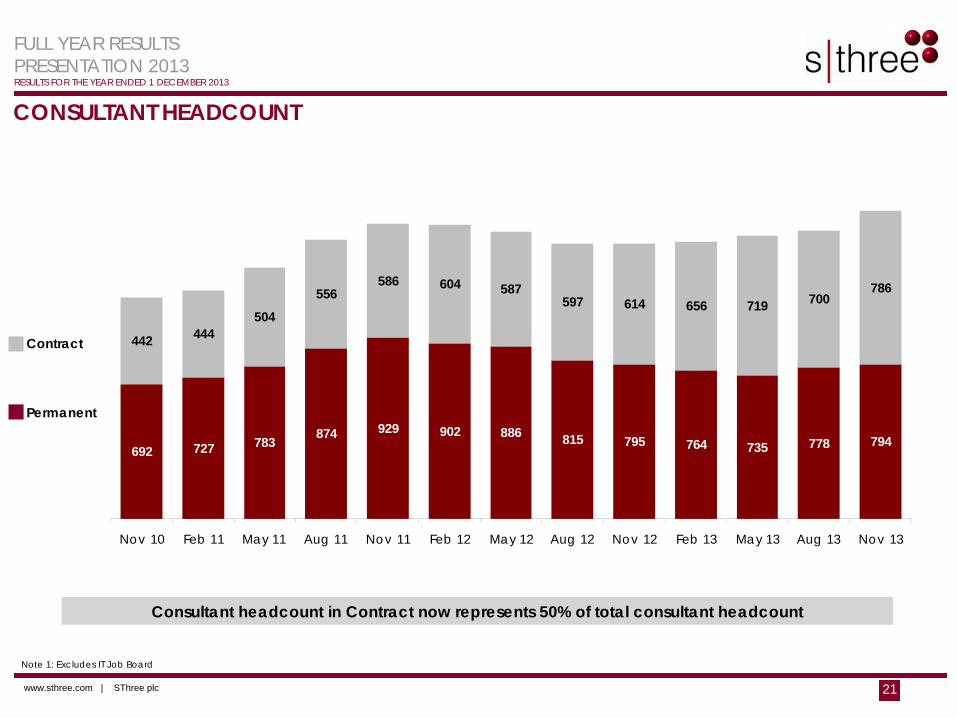

CONSULTANT HEADCOUNT

Contract

Permanent

Note 1: Excludes IT Job Board

692 727 783 874 929 902 886 815 795 764 735 778 794

442 444504

556586 604 587

597 614 656 719 700786

Nov 10 Feb 11 May 11 Aug 11 Nov 11 Feb 12 May 12 Aug 12 Nov 12 Feb 13 May 13 Aug 13 Nov 13

Consultant headcount in Contract now represents 50% of total consultant headcount

FULL YEAR RESULTSPRESENTATION 2013RESULTS FOR THE YEAR ENDED 1 DECEMBER 2013

www.sthree.com | SThree plc 22

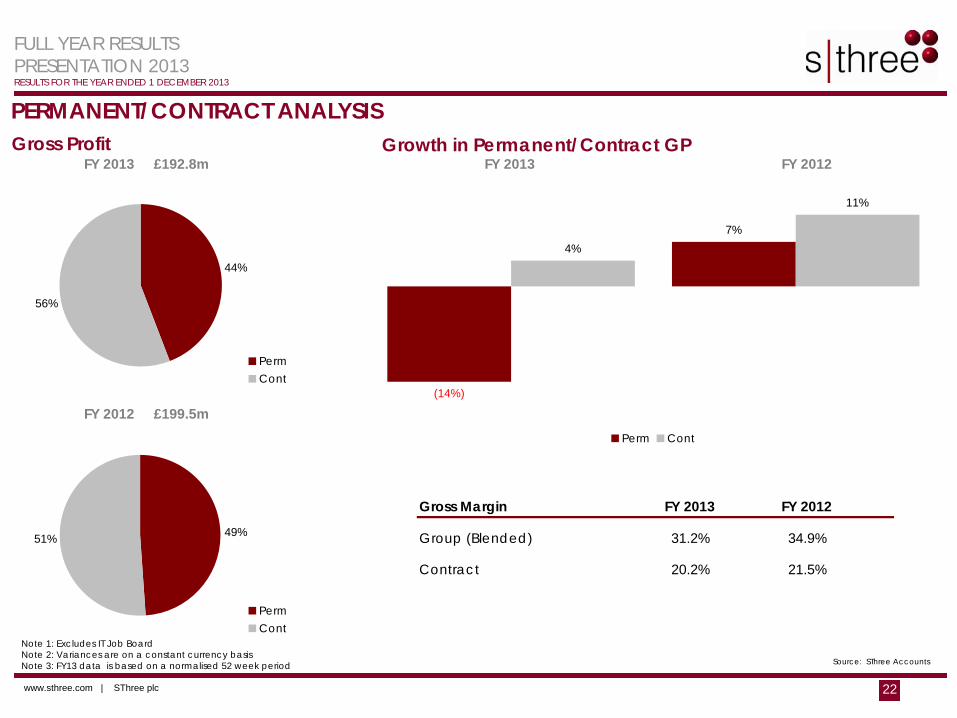

PERMANENT/CONTRACT ANALYSISGross Profit

Note 1: Excludes IT Job BoardNote 2: Variances are on a constant currency basisNote 3: FY13 data is based on a normalised 52 week period Source: SThree Accounts

Growth in Permanent/Contract GP

Gross Margin FY 2013 FY 2012

Group (Blended) 31.2% 34.9%

Contract 20.2% 21.5%

FY 2012 £199.5m

FY 2013 £192.8m FY 2012FY 2013

44%

56%

PermCont

49%51%

PermCont

(14%)

7%4%

11%

Perm Cont

FULL YEAR RESULTSPRESENTATION 2013RESULTS FOR THE YEAR ENDED 1 DECEMBER 2013

www.sthree.com | SThree plc 23

£8,084£9,252

£9,834

£11,383 £11,510£12,255 £12,715 £12,695

£0

£2,000

£4,000

£6,000

£8,000

£10,000

£12,000

£14,000

FY 2006 FY 2007 FY 2008 FY 2009 FY 2010 FY 2011 FY 2012 FY 2013

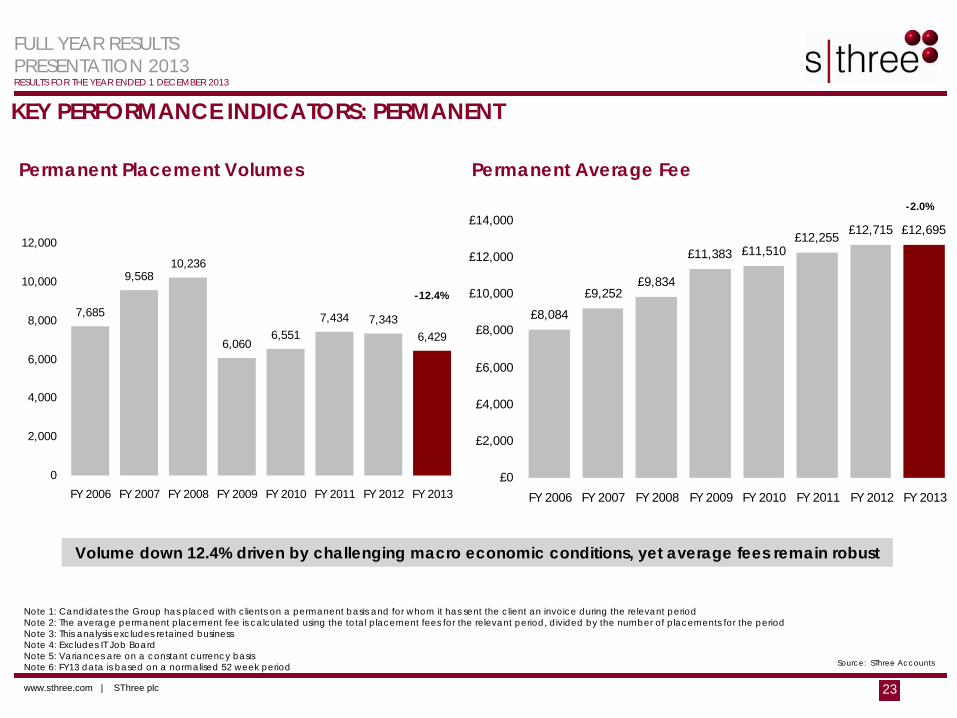

KEY PERFORMANCE INDICATORS: PERMANENT

Permanent Average Fee

Note 1: Candidates the Group has placed with clients on a permanent basis and for whom it has sent the client an invoice during the relevant periodNote 2: The average permanent placement fee is calculated using the total placement fees for the relevant period, divided by the number of placements for the period Note 3: This analysis excludes retained businessNote 4: Excludes IT Job BoardNote 5: Variances are on a constant currency basisNote 6: FY13 data is based on a normalised 52 week period Source: SThree Accounts

Permanent Placement Volumes

Volume down 12.4% driven by challenging macro economic conditions, yet average fees remain robust

7,685

9,56810,236

6,0606,551

7,434 7,3436,429

0

2,000

4,000

6,000

8,000

10,000

12,000

FY 2006 FY 2007 FY 2008 FY 2009 FY 2010 FY 2011 FY 2012 FY 2013

-12.4%

-2.0%

FULL YEAR RESULTSPRESENTATION 2013RESULTS FOR THE YEAR ENDED 1 DECEMBER 2013

www.sthree.com | SThree plc 24

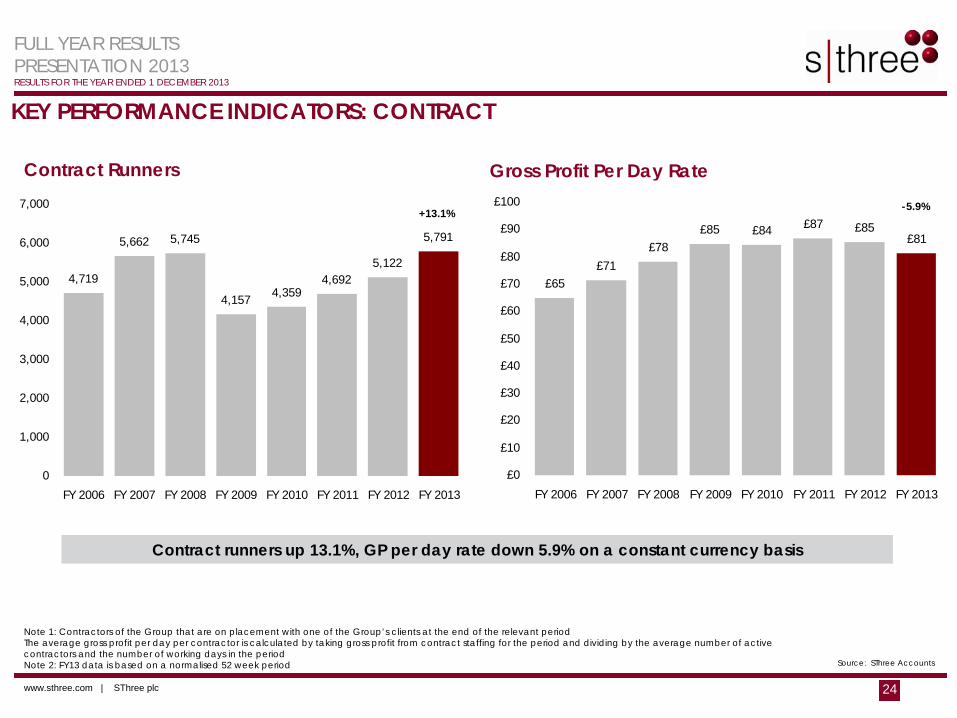

4,719

5,662 5,745

4,157 4,3594,692

5,122

5,791

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

FY 2006 FY 2007 FY 2008 FY 2009 FY 2010 FY 2011 FY 2012 FY 2013

KEY PERFORMANCE INDICATORS: CONTRACT

Gross Profit Per Day Rate

Note 1: Contractors of the Group that are on placement with one of the Group’s clients at the end of the relevant periodThe average gross profit per day per contractor is calculated by taking gross profit from contract staffing for the period and dividing by the average number of active contractors and the number of working days in the periodNote 2: FY13 data is based on a normalised 52 week period

Contract Runners

Contract runners up 13.1%, GP per day rate down 5.9% on a constant currency basis

+13.1%

Source: SThree Accounts

-5.9%

£65£71

£78£85 £84 £87 £85

£81

£0

£10

£20

£30

£40

£50

£60

£70

£80

£90

£100

FY 2006 FY 2007 FY 2008 FY 2009 FY 2010 FY 2011 FY 2012 FY 2013

-5.9%

FULL YEAR RESULTSPRESENTATION 2013RESULTS FOR THE YEAR ENDED 1 DECEMBER 2013

www.sthree.com | SThree plc 25

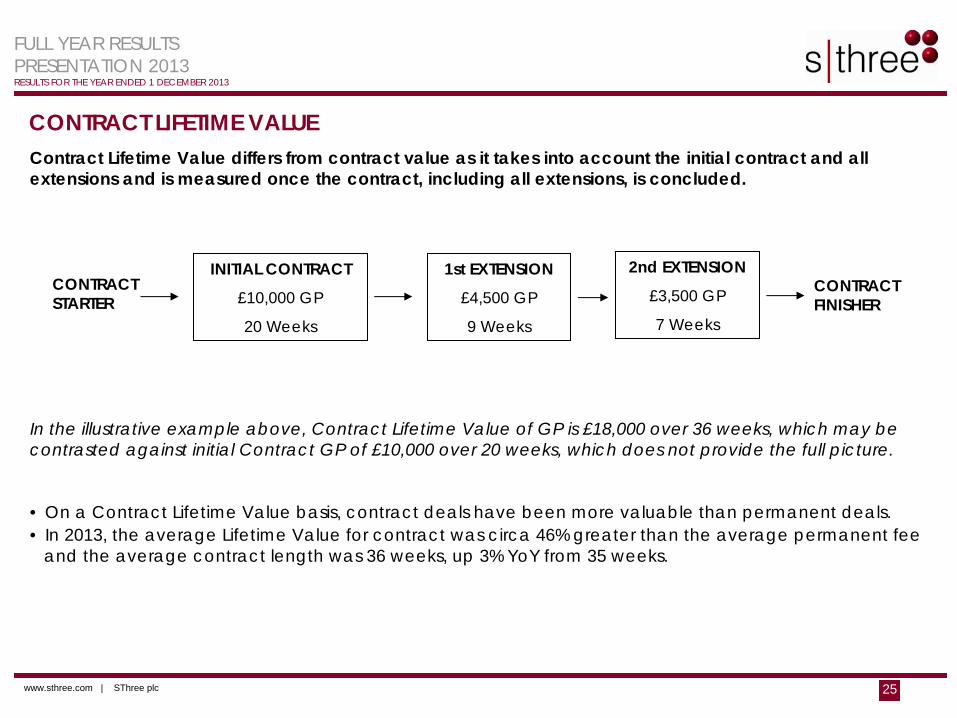

CONTRACT LIFETIME VALUEContract Lifetime Value differs from contract value as it takes into account the initial contract and all extensions and is measured once the contract, including all extensions, is concluded.

In the illustrative example above, Contract Lifetime Value of GP is £18,000 over 36 weeks, which may be contrasted against initial Contract GP of £10,000 over 20 weeks, which does not provide the full picture.

• On a Contract Lifetime Value basis, contract deals have been more valuable than permanent deals. • In 2013, the average Lifetime Value for contract was circa 46% greater than the average permanent fee

and the average contract length was 36 weeks, up 3% YoY from 35 weeks.

INITIAL CONTRACT

£10,000 GP

20 Weeks

1st EXTENSION

£4,500 GP

9 Weeks

2nd EXTENSION

£3,500 GP

7 Weeks

CONTRACT STARTER

CONTRACT FINISHER

FULL YEAR RESULTSPRESENTATION 2013RESULTS FOR THE YEAR ENDED 1 DECEMBER 2013

www.sthree.com | SThree plc 26

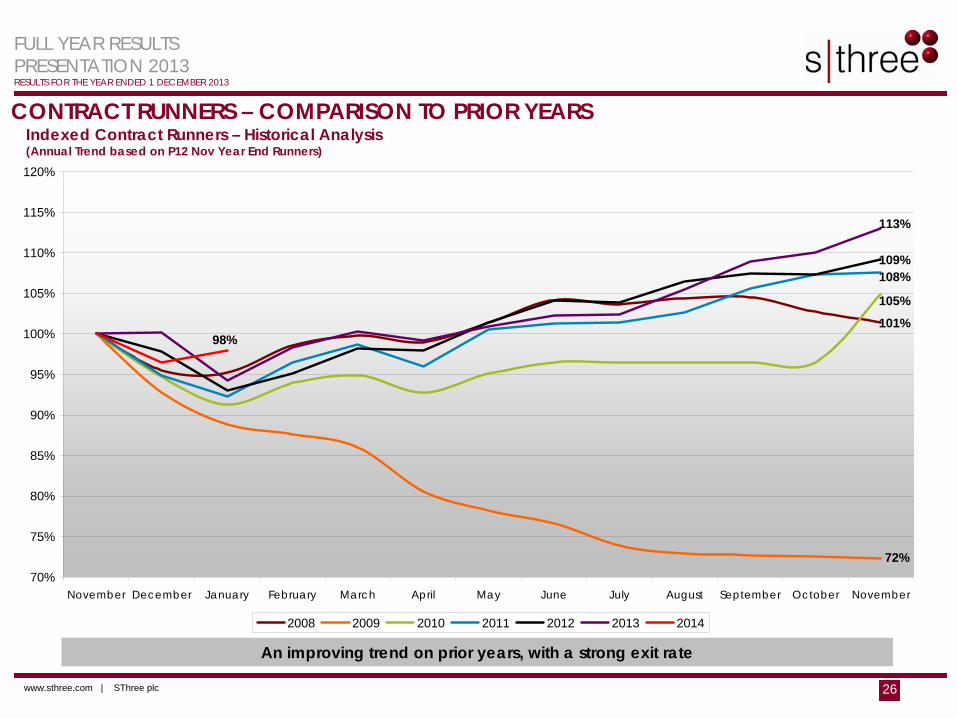

CONTRACT RUNNERS – COMPARISON TO PRIOR YEARS

An improving trend on prior years, with a strong exit rate

Indexed Contract Runners – Historical Analysis(Annual Trend based on P12 Nov Year End Runners)

101%

72%

105%

108%109%

113%

98%

70%

75%

80%

85%

90%

95%

100%

105%

110%

115%

120%

November December January February March April May June July August September October November

2008 2009 2010 2011 2012 2013 2014

FULL YEAR RESULTSPRESENTATION 2013RESULTS FOR THE YEAR ENDED 1 DECEMBER 2013

www.sthree.com | SThree plc 27

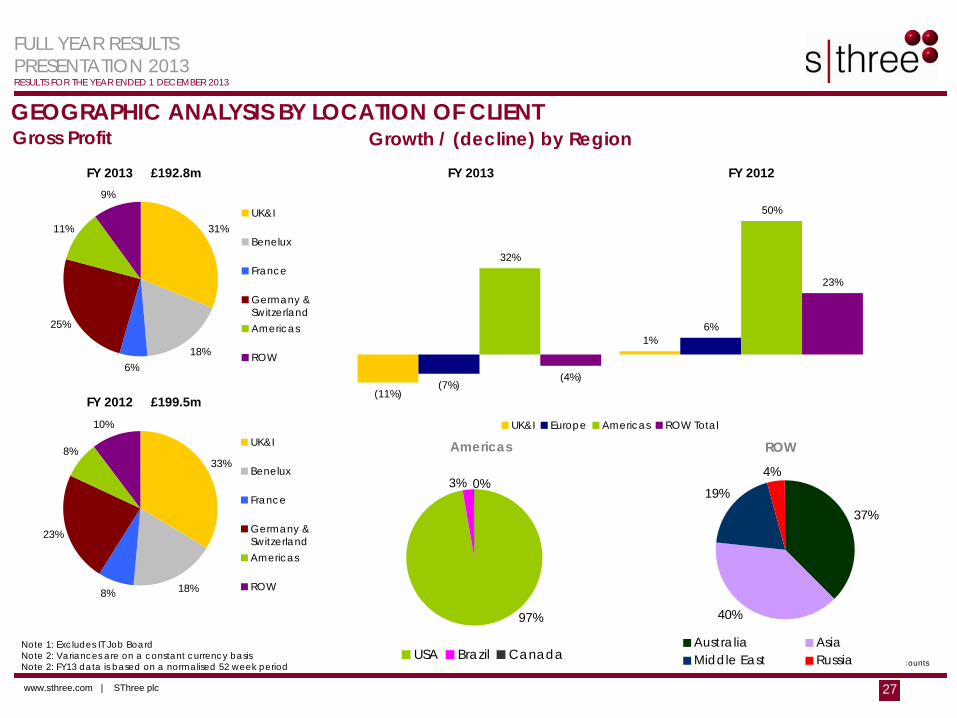

GEOGRAPHIC ANALYSIS BY LOCATION OF CLIENTGross Profit

Source: SThree Accounts

Growth / (decline) by Region

Note 1: Excludes IT Job BoardNote 2: Variances are on a constant currency basisNote 2: FY13 data is based on a normalised 52 week period

Americas

97%

0%3%

USA Brazil Canada

ROW

19%37%

4%

40%

Australia AsiaMiddle East Russia

FY 2013 £192.8m

FY 2012 £199.5m

FY 2012FY 2013

18%6%

25%

11%

9%

31%UK&I

Benelux

France

Germany &SwitzerlandAmericas

ROW

33%

18%8%

23%

8%

10%UK&I

Benelux

France

Germany &SwitzerlandAmericas

ROW

(11%)

1%

(7%)

6%

32%

50%

(4%)

23%

UK&I Europe Americas ROW Total

FULL YEAR RESULTSPRESENTATION 2013RESULTS FOR THE YEAR ENDED 1 DECEMBER 2013

www.sthree.com | SThree plc 28

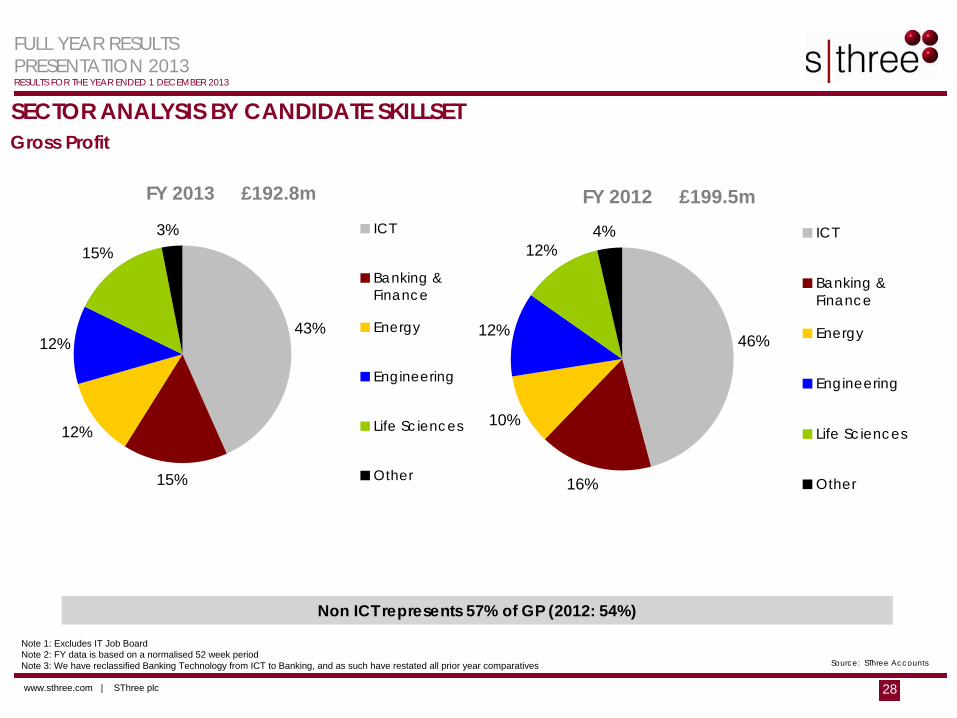

SECTOR ANALYSIS BY CANDIDATE SKILLSETGross Profit

Source: SThree Accounts

Note 1: Excludes IT Job BoardNote 2: FY data is based on a normalised 52 week periodNote 3: We have reclassified Banking Technology from ICT to Banking, and as such have restated all prior year comparatives

Non ICT represents 57% of GP (2012: 54%)

FY 2013 £192.8m

43%

15%

12%

12%

15%3% ICT

Banking &Finance

Energy

Engineering

Life Sciences

Other

FY 2012 £199.5m

46%

16%

10%

12%

12%4% ICT

Banking &Finance

Energy

Engineering

Life Sciences

Other

FULL YEAR RESULTSPRESENTATION 2013RESULTS FOR THE YEAR ENDED 1 DECEMBER 2013

www.sthree.com | SThree plc 29

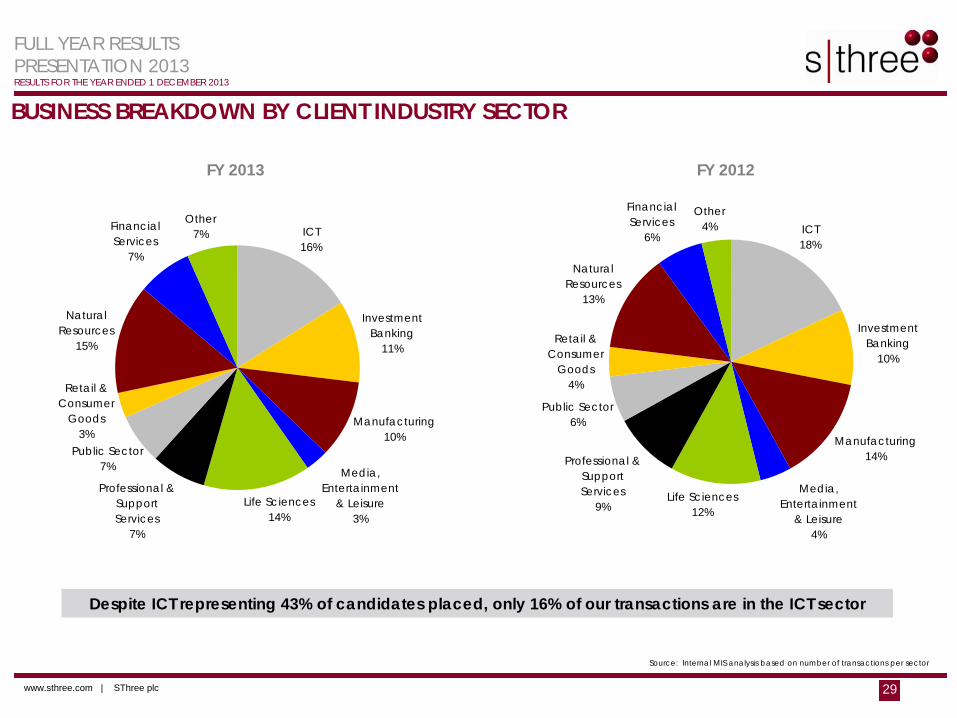

BUSINESS BREAKDOWN BY CLIENT INDUSTRY SECTOR

Despite ICT representing 43% of candidates placed, only 16% of our transactions are in the ICT sector

Source: Internal MIS analysis based on number of transactions per sector

FY 2013 FY 2012

ICT16%

Investment Banking

11%

Manufacturing10%

Media, Entertainment

& Leisure3%

Life Sciences14%

Professional & Support Services

7%

Other7%

Natural Resources

15%

Public Sector7%

Retail & Consumer

Goods3%

Financial Services

7%

ICT18%

Investment Banking

10%

Manufacturing14%

Media, Entertainment

& Leisure4%

Life Sciences12%

Professional & Support Services

9%

Other4%

Financial Services

6%

Retail & Consumer

Goods4%

Public Sector6%

Natural Resources

13%

FULL YEAR RESULTSPRESENTATION 2013RESULTS FOR THE YEAR ENDED 1 DECEMBER 2013

www.sthree.com | SThree plc 30

43%

12%

12%

15%3%

15%ICT Banking & Finance

Energy Engineering

Life Sciences Other

72%

12%

0%7%

2%7%

ICT Banking & Finance

Energy Engineering

Life Sciences Other

BUSINESS MIX – GEOGRAPHICAL & SECTORAL

A balanced portfolio

Source: SThree Internal Analysis

Note 1: Excludes IT Job BoardNote 2: FY13 data is based on a normalised 52 week periodNote 3: We have reclassified Banking Technology from ICT to Banking, and as such have restated all prior year comparatives

56%

40%

4%

UK&I Europe ROW

31%

49%

20%

UK&I Europe ROW

2013

2013 2008

2008

FULL YEAR RESULTSPRESENTATION 2013RESULTS FOR THE YEAR ENDED 1 DECEMBER 2013

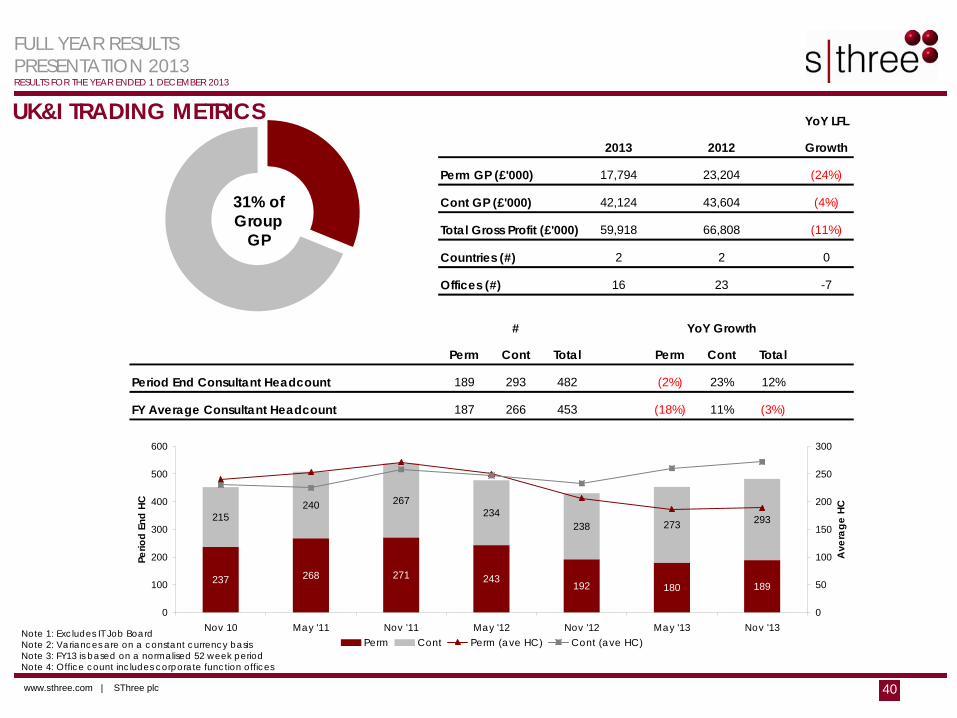

www.sthree.com | SThree plc 31

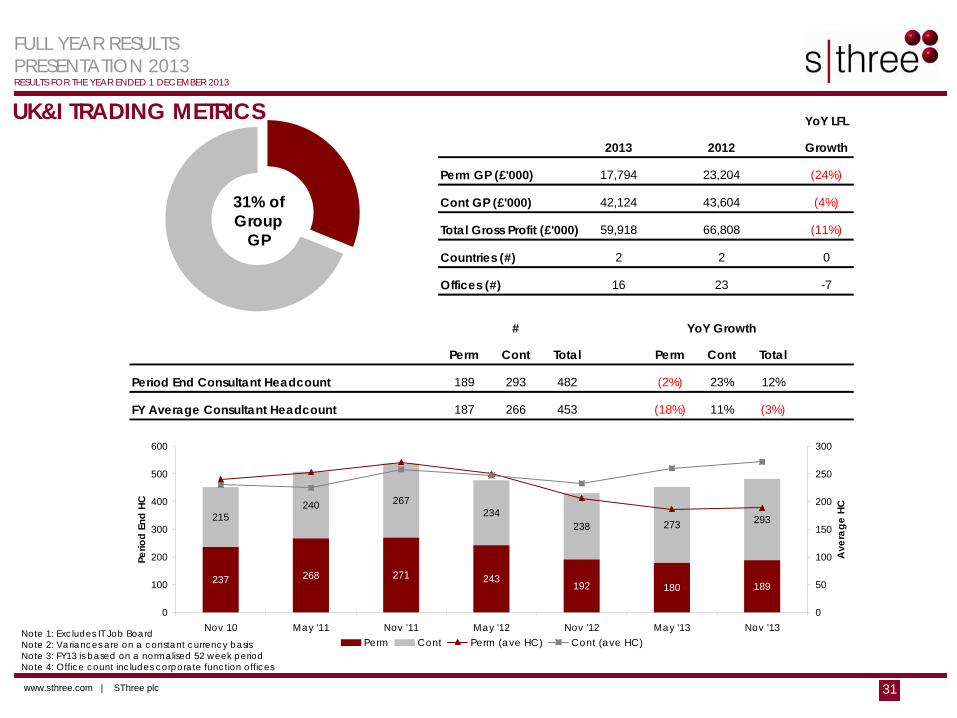

YoY LFL

2013 2012 Growth

Perm GP (£'000) 17,794 23,204 (24%)

Cont GP (£'000) 42,124 43,604 (4%)

Total Gross Profit (£'000) 59,918 66,808 (11%)

Countries (#) 2 2 0

Offices (#) 16 23 -7

Perm Cont Total Perm Cont Total

Period End Consultant Headcount 189 293 482 (2%) 23% 12%

FY Average Consultant Headcount 187 266 453 (18%) 11% (3%)

# YoY Growth

237 268 271 243192 180 189

215240 267

234238 273 293

0

100

200

300

400

500

600

Nov 10 May '11 Nov '11 May '12 Nov '12 May '13 Nov '13

Perio

d En

d HC

0

50

100

150

200

250

300

Ave

rage

HC

Perm Cont Perm (ave HC) Cont (ave HC)

UK&I TRADING METRICS

31% of Group

GP

Note 1: Excludes IT Job BoardNote 2: Variances are on a constant currency basisNote 3: FY13 is based on a normalised 52 week periodNote 4: Office count includes corporate function offices

FULL YEAR RESULTSPRESENTATION 2013RESULTS FOR THE YEAR ENDED 1 DECEMBER 2013

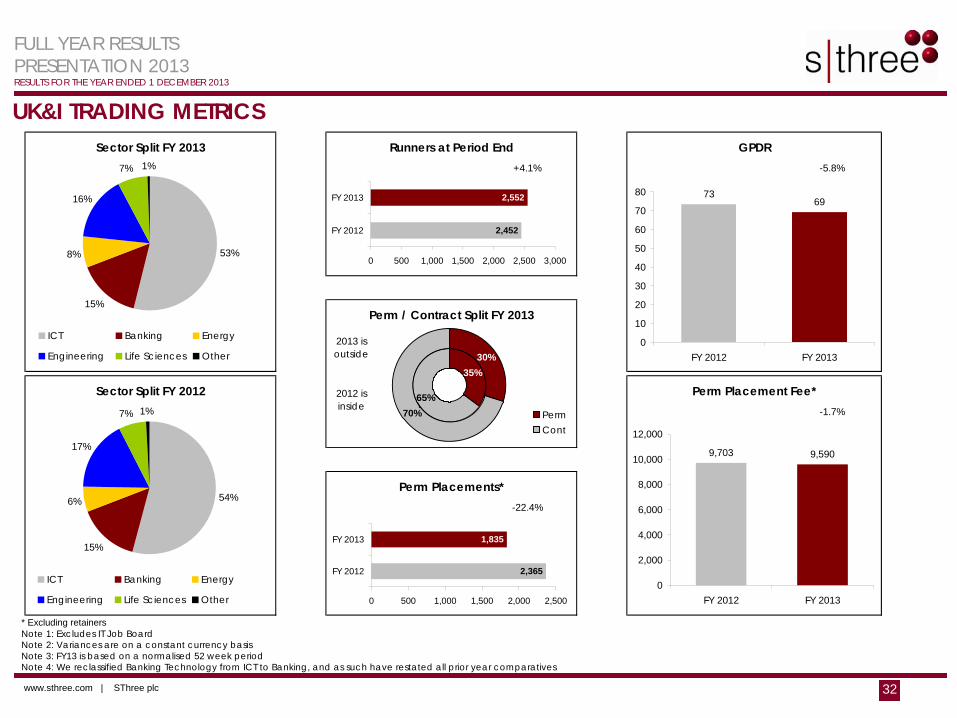

www.sthree.com | SThree plc 32

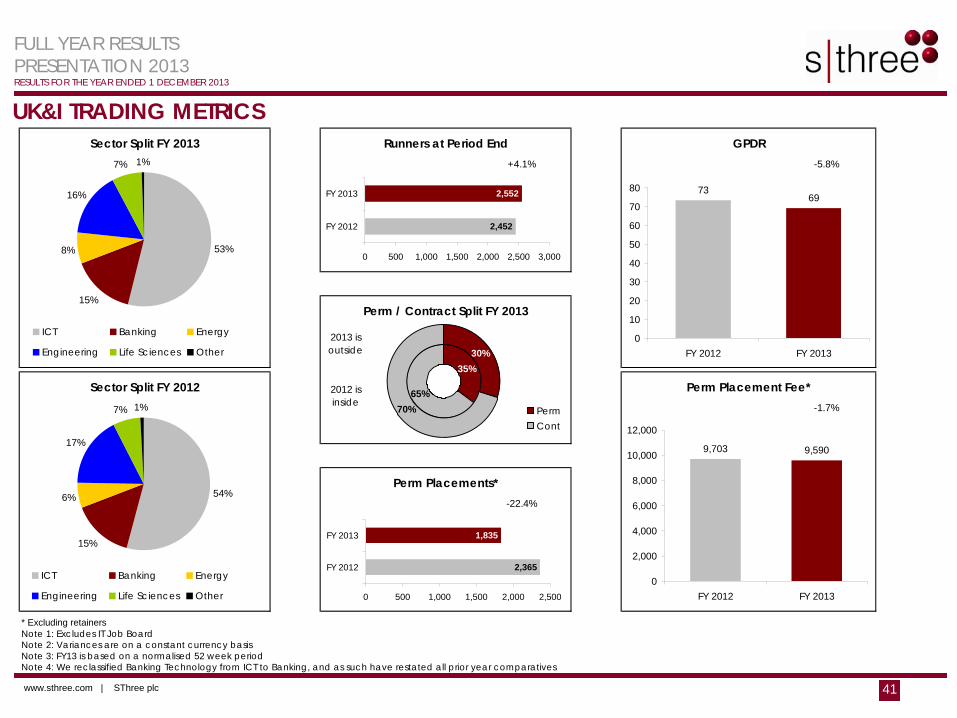

UK&I TRADING METRICS

* Excluding retainersNote 1: Excludes IT Job BoardNote 2: Variances are on a constant currency basisNote 3: FY13 is based on a normalised 52 week periodNote 4: We reclassified Banking Technology from ICT to Banking, and as such have restated all prior year comparatives

Runners at Period End+4.1%

GPDR-5.8%

Perm Placement Fee*-1.7%

Sector Split FY 2012

Sector Split FY 2013

Perm Placements*-22.4%

Perm / Contract Split FY 2013

2012 is inside

2013 is outside

2,452

2,552

0 500 1,000 1,500 2,000 2,500 3,000

FY 2012

FY 2013

2,365

1,835

0 500 1,000 1,500 2,000 2,500

FY 2012

FY 2013

7369

0

10

20

30

40

50

60

70

80

FY 2012 FY 2013

9,703 9,590

0

2,000

4,000

6,000

8,000

10,000

12,000

FY 2012 FY 2013

53%

15%

8%

16%

7% 1%

ICT Banking Energy

Engineering Life Sciences Other

54%

15%

6%

17%

7% 1%

ICT Banking Energy

Engineering Life Sciences Other

65%70%

35%30%

PermCont

FULL YEAR RESULTSPRESENTATION 2013RESULTS FOR THE YEAR ENDED 1 DECEMBER 2013

www.sthree.com | SThree plc 33

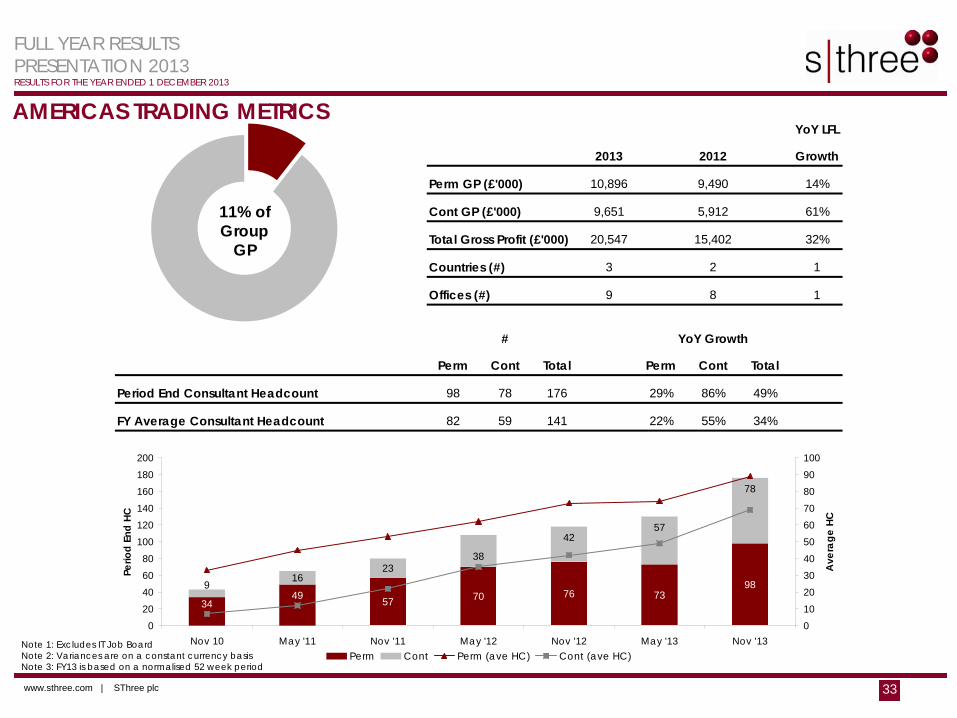

YoY LFL

2013 2012 Growth

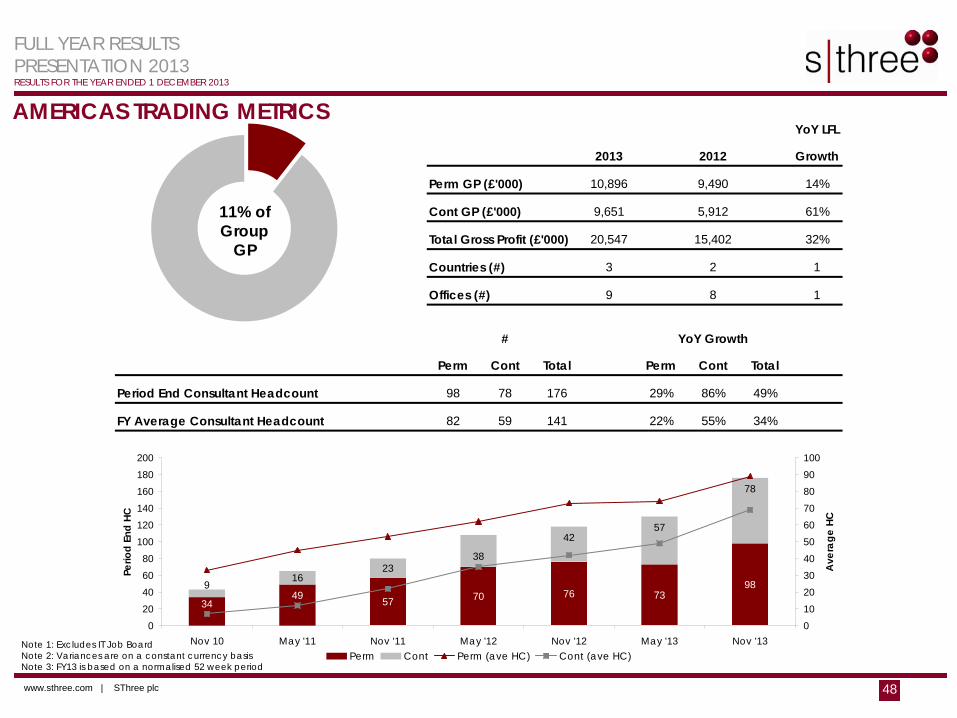

Perm GP (£'000) 10,896 9,490 14%

Cont GP (£'000) 9,651 5,912 61%

Total Gross Profit (£'000) 20,547 15,402 32%

Countries (#) 3 2 1

Offices (#) 9 8 1

Perm Cont Total Perm Cont Total

Period End Consultant Headcount 98 78 176 29% 86% 49%

FY Average Consultant Headcount 82 59 141 22% 55% 34%

# YoY Growth

57 70 76 739816

3449

9

42

3823

57

78

020406080

100120140160180200

Nov 10 May '11 Nov '11 May '12 Nov '12 May '13 Nov '13

Perio

d En

d HC

0102030405060708090100

Ave

rage

HC

Perm Cont Perm (ave HC) Cont (ave HC)

AMERICAS TRADING METRICS

11% of Group

GP

Note 1: Excludes IT Job BoardNote 2: Variances are on a constant currency basisNote 3: FY13 is based on a normalised 52 week period

FULL YEAR RESULTSPRESENTATION 2013RESULTS FOR THE YEAR ENDED 1 DECEMBER 2013

www.sthree.com | SThree plc 34

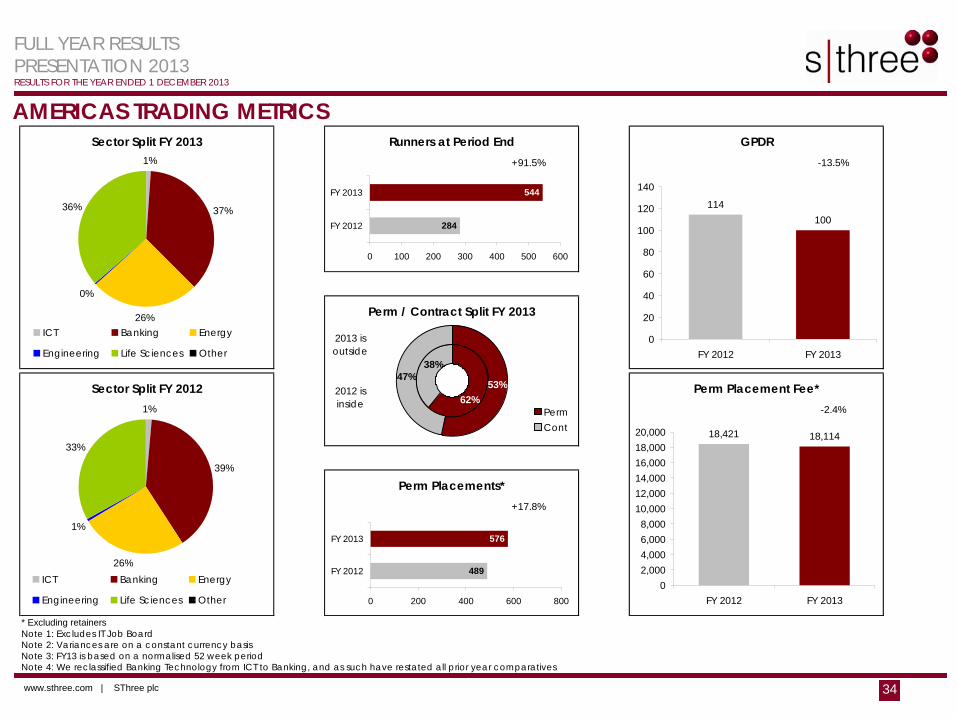

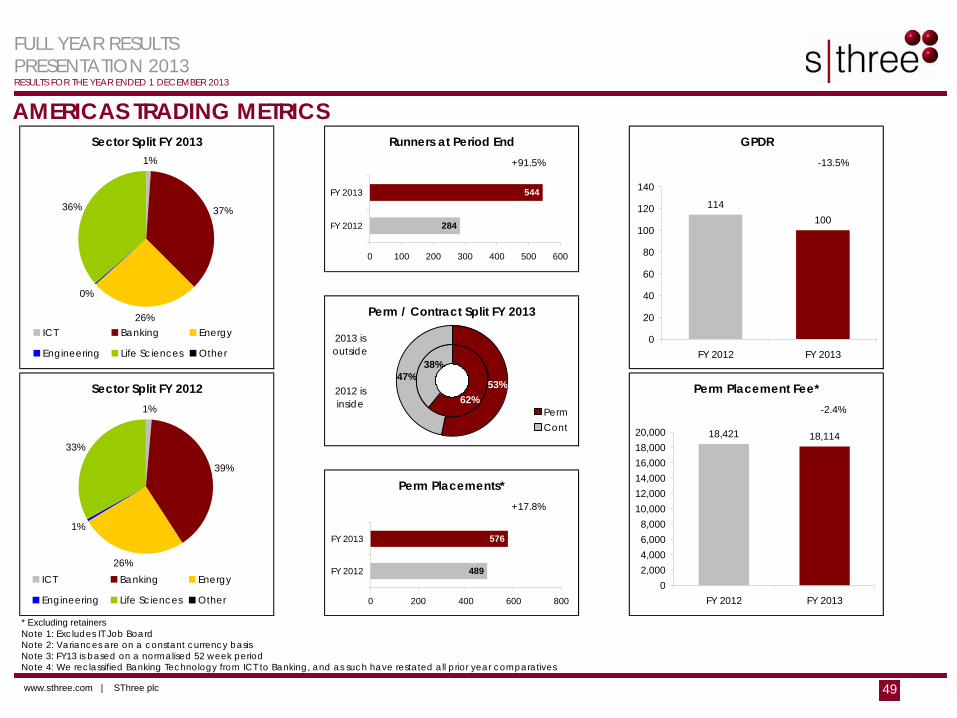

AMERICAS TRADING METRICS

* Excluding retainersNote 1: Excludes IT Job BoardNote 2: Variances are on a constant currency basisNote 3: FY13 is based on a normalised 52 week periodNote 4: We reclassified Banking Technology from ICT to Banking, and as such have restated all prior year comparatives

Runners at Period End+91.5%

GPDR-13.5%

Perm Placement Fee*-2.4%

Sector Split FY 2012

Sector Split FY 2013

Perm Placements*+17.8%

Perm / Contract Split FY 2013

2013 is outside

2012 is inside

284

544

0 100 200 300 400 500 600

FY 2012

FY 2013

489

576

0 200 400 600 800

FY 2012

FY 2013

114100

0

20

40

60

80

100

120

140

FY 2012 FY 2013

18,421 18,114

02,0004,0006,0008,000

10,00012,00014,00016,00018,00020,000

FY 2012 FY 2013

1%

37%

26%

0%

36%

ICT Banking Energy

Engineering Life Sciences Other

1%

39%

26%

1%

33%

ICT Banking Energy

Engineering Life Sciences Other

47%38%

62%53%

PermCont

FULL YEAR RESULTSPRESENTATION 2013RESULTS FOR THE YEAR ENDED 1 DECEMBER 2013

www.sthree.com | SThree plc 35

SUMMARY & 2014 OUTLOOK

• Improving sentiment evident in some markets but overall picture remains mixed

• Demand in newer sectors such as Energy and Life Sciences remains resilient

• Contract headcount up by 28% since the start of last year, and expect to see the full benefit of this investment in 2014

• Permanent headcount issues addressed and consultant productivity beginning to build

• Organisational structure strengthened and focused

• Cost rationalisation initiative reduces our underlying annualised cost base by circa £8m

• Remain financially strong & agile and continue to invest for the long term

• Foundations for future growth established – focus on execution in 2014

www.sthree.com | SThree plc 36

FULL YEAR RESULTSPRESENTATION 2013RESULTS FOR THE YEAR ENDED 1 DECEMBER 2013

QUESTIONSThank you for listening, please feel free to ask any questions

www.sthree.com | SThree plc 37

FULL YEAR RESULTSPRESENTATION 2013RESULTS FOR THE YEAR ENDED 1 DECEMBER 2013

SUPPLEMENTARY MATERIAL

FULL YEAR RESULTSPRESENTATION 2013RESULTS FOR THE YEAR ENDED 1 DECEMBER 2013

www.sthree.com | SThree plc 38

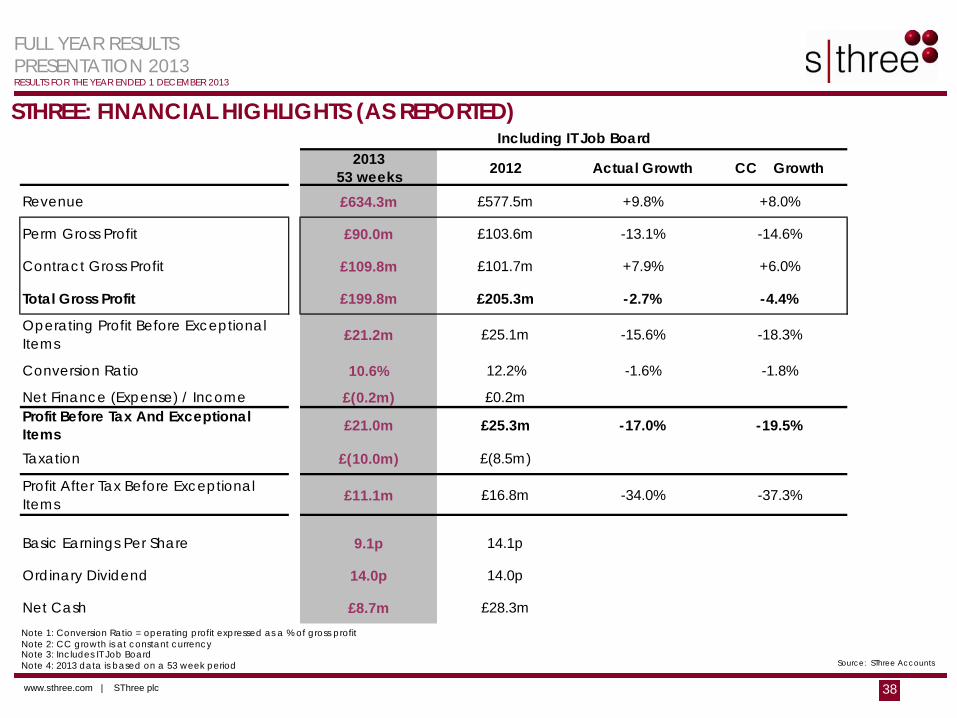

STHREE: FINANCIAL HIGHLIGHTS (AS REPORTED)

Note 1: Conversion Ratio = operating profit expressed as a % of gross profitNote 2: CC growth is at constant currencyNote 3: Includes IT Job BoardNote 4: 2013 data is based on a 53 week period Source: SThree Accounts

2013 53 weeks 2012 Actual Growth CC Growth

Revenue £634.3m £577.5m +9.8% +8.0%

Perm Gross Profit £90.0m £103.6m -13.1% -14.6%

Contract Gross Profit £109.8m £101.7m +7.9% +6.0%

Total Gross Profit £199.8m £205.3m -2.7% -4.4%

Operating Profit Before Exceptional Items £21.2m £25.1m -15.6% -18.3%

Conversion Ratio 10.6% 12.2% -1.6% -1.8%

Net Finance (Expense) / Income £(0.2m) £0.2mProfit Before Tax And Exceptional Items £21.0m £25.3m -17.0% -19.5%

Taxation £(10.0m) £(8.5m)

Profit After Tax Before Exceptional Items £11.1m £16.8m -34.0% -37.3%

Basic Earnings Per Share 9.1p 14.1p

Ordinary Dividend 14.0p 14.0p

Net Cash £8.7m £28.3m

Including IT Job Board

FULL YEAR RESULTSPRESENTATION 2013RESULTS FOR THE YEAR ENDED 1 DECEMBER 2013

www.sthree.com | SThree plc 39

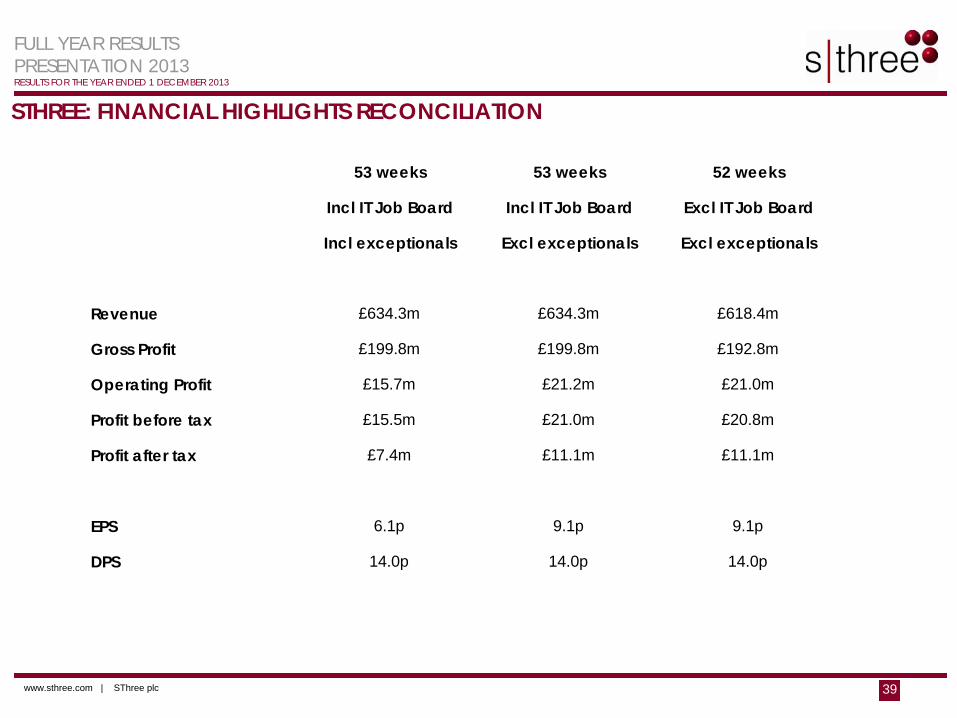

STHREE: FINANCIAL HIGHLIGHTS RECONCILIATION

53 weeks 53 weeks 52 weeks

Incl IT Job Board Incl IT Job Board Excl IT Job Board

Incl exceptionals Excl exceptionals Excl exceptionals

Revenue £634.3m £634.3m £618.4m

Gross Profit £199.8m £199.8m £192.8m

Operating Profit £15.7m £21.2m £21.0m

Profit before tax £15.5m £21.0m £20.8m

Profit after tax £7.4m £11.1m £11.1m

EPS 6.1p 9.1p 9.1p

DPS 14.0p 14.0p 14.0p

FULL YEAR RESULTSPRESENTATION 2013RESULTS FOR THE YEAR ENDED 1 DECEMBER 2013

www.sthree.com | SThree plc 40

YoY LFL

2013 2012 Growth

Perm GP (£'000) 17,794 23,204 (24%)

Cont GP (£'000) 42,124 43,604 (4%)

Total Gross Profit (£'000) 59,918 66,808 (11%)

Countries (#) 2 2 0

Offices (#) 16 23 -7

Perm Cont Total Perm Cont Total

Period End Consultant Headcount 189 293 482 (2%) 23% 12%

FY Average Consultant Headcount 187 266 453 (18%) 11% (3%)

# YoY Growth

237 268 271 243192 180 189

215240 267

234238 273 293

0

100

200

300

400

500

600

Nov 10 May '11 Nov '11 May '12 Nov '12 May '13 Nov '13

Perio

d En

d HC

0

50

100

150

200

250

300

Ave

rage

HC

Perm Cont Perm (ave HC) Cont (ave HC)

UK&I TRADING METRICS

31% of Group

GP

Note 1: Excludes IT Job BoardNote 2: Variances are on a constant currency basisNote 3: FY13 is based on a normalised 52 week periodNote 4: Office count includes corporate function offices

FULL YEAR RESULTSPRESENTATION 2013RESULTS FOR THE YEAR ENDED 1 DECEMBER 2013

www.sthree.com | SThree plc 41

UK&I TRADING METRICS

* Excluding retainersNote 1: Excludes IT Job BoardNote 2: Variances are on a constant currency basisNote 3: FY13 is based on a normalised 52 week periodNote 4: We reclassified Banking Technology from ICT to Banking, and as such have restated all prior year comparatives

Runners at Period End+4.1%

GPDR-5.8%

Perm Placement Fee*-1.7%

Sector Split FY 2012

Sector Split FY 2013

Perm Placements*-22.4%

Perm / Contract Split FY 2013

2012 is inside

2013 is outside

2,452

2,552

0 500 1,000 1,500 2,000 2,500 3,000

FY 2012

FY 2013

2,365

1,835

0 500 1,000 1,500 2,000 2,500

FY 2012

FY 2013

7369

0

10

20

30

40

50

60

70

80

FY 2012 FY 2013

9,703 9,590

0

2,000

4,000

6,000

8,000

10,000

12,000

FY 2012 FY 2013

53%

15%

8%

16%

7% 1%

ICT Banking Energy

Engineering Life Sciences Other

54%

15%

6%

17%

7% 1%

ICT Banking Energy

Engineering Life Sciences Other

65%70%

35%30%

PermCont

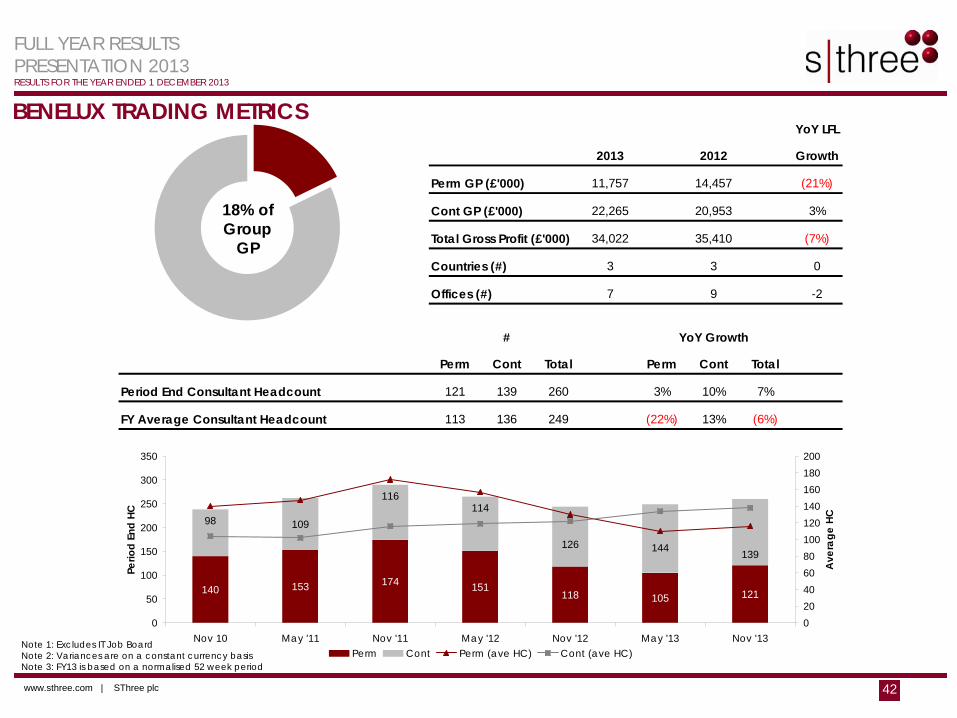

FULL YEAR RESULTSPRESENTATION 2013RESULTS FOR THE YEAR ENDED 1 DECEMBER 2013

www.sthree.com | SThree plc 42

YoY LFL

2013 2012 Growth

Perm GP (£'000) 11,757 14,457 (21%)

Cont GP (£'000) 22,265 20,953 3%

Total Gross Profit (£'000) 34,022 35,410 (7%)

Countries (#) 3 3 0

Offices (#) 7 9 -2

Perm Cont Total Perm Cont Total

Period End Consultant Headcount 121 139 260 3% 10% 7%

FY Average Consultant Headcount 113 136 249 (22%) 13% (6%)

# YoY Growth

140 153 174 151118 105 121

109

139

11498

126 144

116

0

50

100

150

200

250

300

350

Nov 10 May '11 Nov '11 May '12 Nov '12 May '13 Nov '13

Perio

d En

d HC

020406080100120140160180200

Ave

rage

HC

Perm Cont Perm (ave HC) Cont (ave HC)

BENELUX TRADING METRICS

18% of Group

GP

Note 1: Excludes IT Job BoardNote 2: Variances are on a constant currency basisNote 3: FY13 is based on a normalised 52 week period

FULL YEAR RESULTSPRESENTATION 2013RESULTS FOR THE YEAR ENDED 1 DECEMBER 2013

www.sthree.com | SThree plc 43

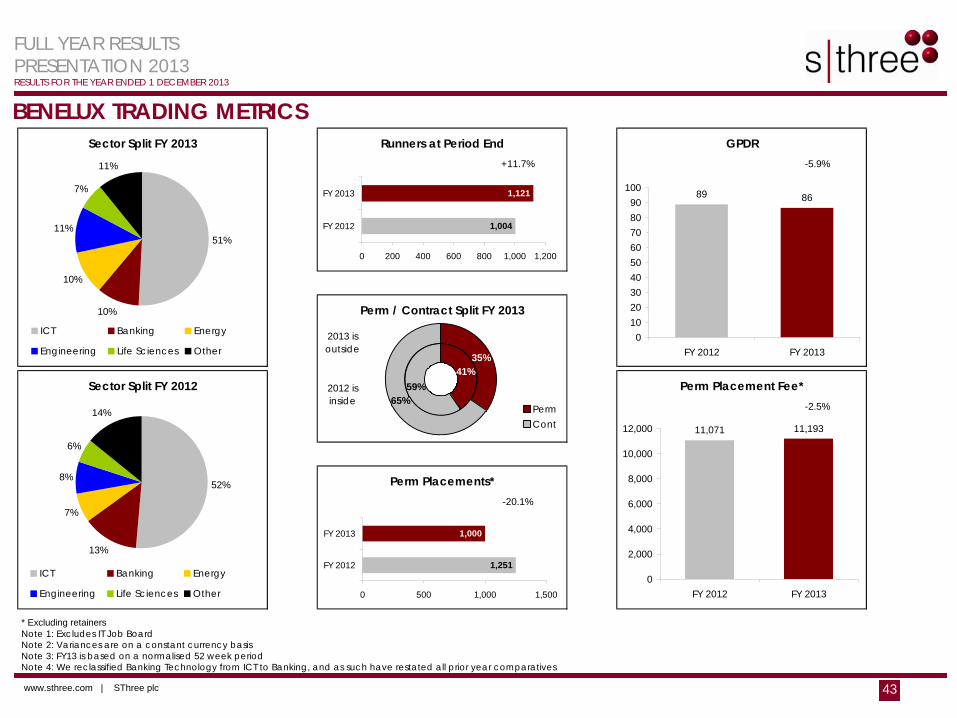

BENELUX TRADING METRICS

* Excluding retainersNote 1: Excludes IT Job BoardNote 2: Variances are on a constant currency basisNote 3: FY13 is based on a normalised 52 week periodNote 4: We reclassified Banking Technology from ICT to Banking, and as such have restated all prior year comparatives

Perm Placements*-20.1%

Perm / Contract Split FY 2013

2013 is outside

2012 is inside

Perm Placement Fee*-2.5%

Sector Split FY 2012

Sector Split FY 2013 Runners at Period End+11.7%

GPDR-5.9%

1,004

1,121

0 200 400 600 800 1,000 1,200

FY 2012

FY 2013

1,251

1,000

0 500 1,000 1,500

FY 2012

FY 2013

89 86

0102030405060708090

100

FY 2012 FY 2013

11,071 11,193

0

2,000

4,000

6,000

8,000

10,000

12,000

FY 2012 FY 2013

51%

10%

10%

11%

7%

11%

ICT Banking Energy

Engineering Life Sciences Other

52%

13%

7%

8%

6%

14%

ICT Banking Energy

Engineering Life Sciences Other

59%65%

41%35%

PermCont

FULL YEAR RESULTSPRESENTATION 2013RESULTS FOR THE YEAR ENDED 1 DECEMBER 2013

www.sthree.com | SThree plc 44

YoY LFL

2013 2012 Growth

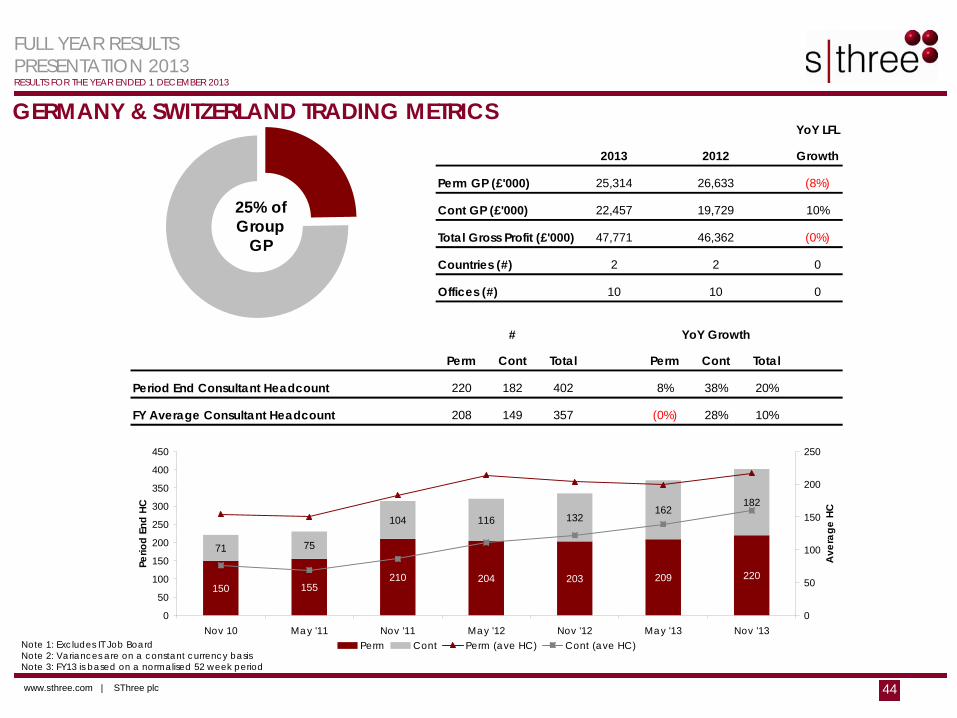

Perm GP (£'000) 25,314 26,633 (8%)

Cont GP (£'000) 22,457 19,729 10%

Total Gross Profit (£'000) 47,771 46,362 (0%)

Countries (#) 2 2 0

Offices (#) 10 10 0

Perm Cont Total Perm Cont Total

Period End Consultant Headcount 220 182 402 8% 38% 20%

FY Average Consultant Headcount 208 149 357 (0%) 28% 10%

# YoY Growth

150 155210 204 203 209 220

71 75

116

182132

162104

0

50

100

150

200

250

300

350

400

450

Nov 10 May '11 Nov '11 May '12 Nov '12 May '13 Nov '13

Perio

d En

d HC

0

50

100

150

200

250

Ave

rage

HC

Perm Cont Perm (ave HC) Cont (ave HC)

GERMANY & SWITZERLAND TRADING METRICS

25% of Group

GP

Note 1: Excludes IT Job BoardNote 2: Variances are on a constant currency basisNote 3: FY13 is based on a normalised 52 week period

FULL YEAR RESULTSPRESENTATION 2013RESULTS FOR THE YEAR ENDED 1 DECEMBER 2013

www.sthree.com | SThree plc 45

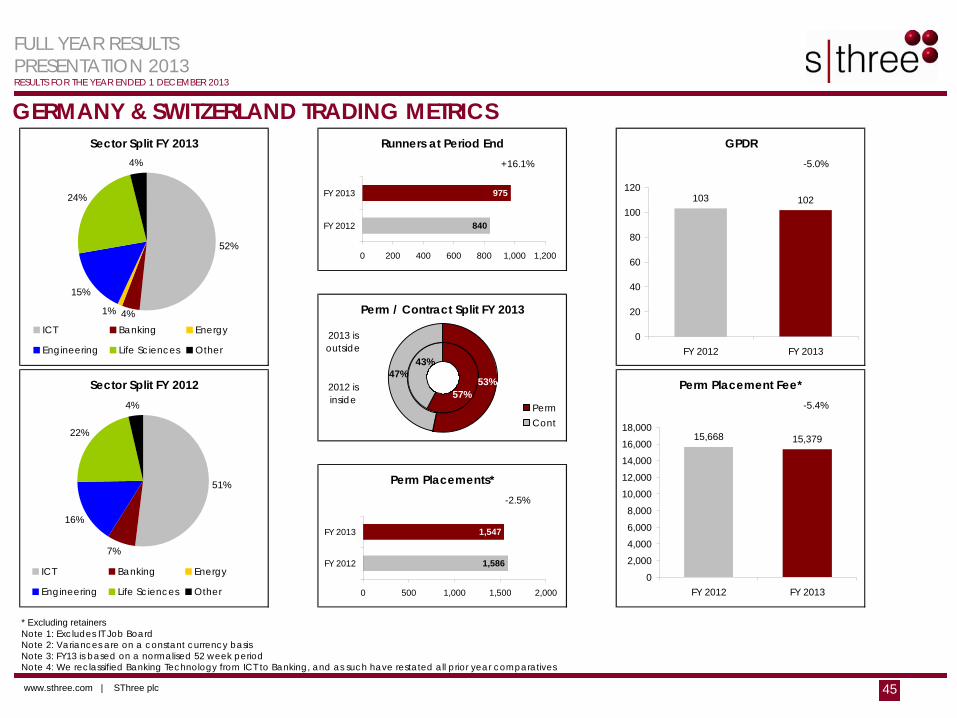

GERMANY & SWITZERLAND TRADING METRICS

* Excluding retainersNote 1: Excludes IT Job BoardNote 2: Variances are on a constant currency basisNote 3: FY13 is based on a normalised 52 week periodNote 4: We reclassified Banking Technology from ICT to Banking, and as such have restated all prior year comparatives

Sector Split FY 2012

Sector Split FY 2013 Runners at Period End+16.1%

GPDR-5.0%

2013 is outside

2012 is inside

Perm Placements*-2.5%

Perm / Contract Split FY 2013

Perm Placement Fee*-5.4%

840

975

0 200 400 600 800 1,000 1,200

FY 2012

FY 2013

1,586

1,547

0 500 1,000 1,500 2,000

FY 2012

FY 2013

103 102

0

20

40

60

80

100

120

FY 2012 FY 2013

15,668 15,379

02,0004,0006,0008,000

10,00012,00014,00016,00018,000

FY 2012 FY 2013

52%

15%

24%

4%

1% 4%ICT Banking Energy

Engineering Life Sciences Other

51%

16%

22%

4%

7%

ICT Banking Energy

Engineering Life Sciences Other

47%43%

57%53%

PermCont

FULL YEAR RESULTSPRESENTATION 2013RESULTS FOR THE YEAR ENDED 1 DECEMBER 2013

www.sthree.com | SThree plc 46

YoY LFL

2013 2012 Growth

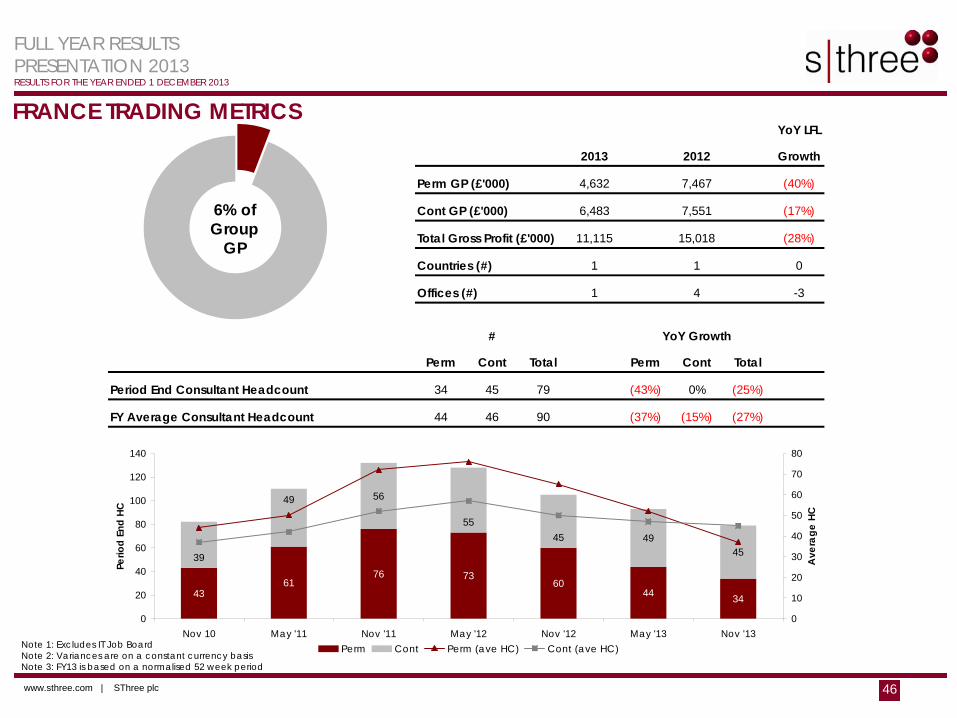

Perm GP (£'000) 4,632 7,467 (40%)

Cont GP (£'000) 6,483 7,551 (17%)

Total Gross Profit (£'000) 11,115 15,018 (28%)

Countries (#) 1 1 0

Offices (#) 1 4 -3

Perm Cont Total Perm Cont Total

Period End Consultant Headcount 34 45 79 (43%) 0% (25%)

FY Average Consultant Headcount 44 46 90 (37%) (15%) (27%)

# YoY Growth

4361

76 7360

44 34

45

56

4945

39

55

49

0

20

40

60

80

100

120

140

Nov 10 May '11 Nov '11 May '12 Nov '12 May '13 Nov '13

Perio

d En

d HC

0

10

20

30

40

50

60

70

80

Ave

rage

HC

Perm Cont Perm (ave HC) Cont (ave HC)

FRANCE TRADING METRICS

6% of Group

GP

Note 1: Excludes IT Job BoardNote 2: Variances are on a constant currency basisNote 3: FY13 is based on a normalised 52 week period

FULL YEAR RESULTSPRESENTATION 2013RESULTS FOR THE YEAR ENDED 1 DECEMBER 2013

www.sthree.com | SThree plc 47

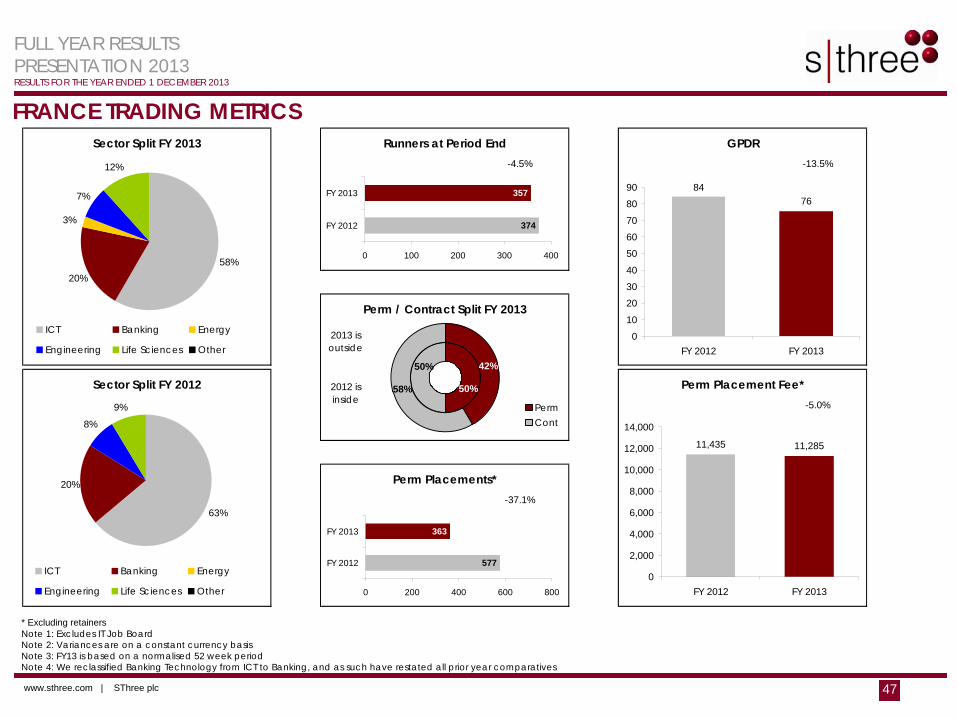

FRANCE TRADING METRICS

* Excluding retainersNote 1: Excludes IT Job BoardNote 2: Variances are on a constant currency basisNote 3: FY13 is based on a normalised 52 week periodNote 4: We reclassified Banking Technology from ICT to Banking, and as such have restated all prior year comparatives

Perm Placements*-37.1%

Perm / Contract Split FY 2013

Perm Placement Fee*-5.0%

Sector Split FY 2012

Sector Split FY 2013 Runners at Period End-4.5%

GPDR-13.5%

2013 is outside

2012 is inside

374

357

0 100 200 300 400

FY 2012

FY 2013

577

363

0 200 400 600 800

FY 2012

FY 2013

8476

0102030405060708090

FY 2012 FY 2013

11,435 11,285

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

FY 2012 FY 2013

58%

7%

12%

3%

20%

ICT Banking Energy

Engineering Life Sciences Other

63%

8%

9%

20%

ICT Banking Energy

Engineering Life Sciences Other

58%

50%

50%

42%

PermCont

FULL YEAR RESULTSPRESENTATION 2013RESULTS FOR THE YEAR ENDED 1 DECEMBER 2013

www.sthree.com | SThree plc 48

YoY LFL

2013 2012 Growth

Perm GP (£'000) 10,896 9,490 14%

Cont GP (£'000) 9,651 5,912 61%

Total Gross Profit (£'000) 20,547 15,402 32%

Countries (#) 3 2 1

Offices (#) 9 8 1

Perm Cont Total Perm Cont Total

Period End Consultant Headcount 98 78 176 29% 86% 49%

FY Average Consultant Headcount 82 59 141 22% 55% 34%

# YoY Growth

57 70 76 739816

3449

9

42

3823

57

78

020406080

100120140160180200

Nov 10 May '11 Nov '11 May '12 Nov '12 May '13 Nov '13

Perio

d En

d HC

0102030405060708090100

Ave

rage

HC

Perm Cont Perm (ave HC) Cont (ave HC)

AMERICAS TRADING METRICS

11% of Group

GP

Note 1: Excludes IT Job BoardNote 2: Variances are on a constant currency basisNote 3: FY13 is based on a normalised 52 week period

FULL YEAR RESULTSPRESENTATION 2013RESULTS FOR THE YEAR ENDED 1 DECEMBER 2013

www.sthree.com | SThree plc 49

AMERICAS TRADING METRICS

* Excluding retainersNote 1: Excludes IT Job BoardNote 2: Variances are on a constant currency basisNote 3: FY13 is based on a normalised 52 week periodNote 4: We reclassified Banking Technology from ICT to Banking, and as such have restated all prior year comparatives

Runners at Period End+91.5%

GPDR-13.5%

Perm Placement Fee*-2.4%

Sector Split FY 2012

Sector Split FY 2013

Perm Placements*+17.8%

Perm / Contract Split FY 2013

2013 is outside

2012 is inside

284

544

0 100 200 300 400 500 600

FY 2012

FY 2013

489

576

0 200 400 600 800

FY 2012

FY 2013

114100

0

20

40

60

80

100

120

140

FY 2012 FY 2013

18,421 18,114

02,0004,0006,0008,000

10,00012,00014,00016,00018,00020,000

FY 2012 FY 2013

1%

37%

26%

0%

36%

ICT Banking Energy

Engineering Life Sciences Other

1%

39%

26%

1%

33%

ICT Banking Energy

Engineering Life Sciences Other

47%38%

62%53%

PermCont

FULL YEAR RESULTSPRESENTATION 2013RESULTS FOR THE YEAR ENDED 1 DECEMBER 2013

www.sthree.com | SThree plc 50

YoY LFL

2013 2012 Growth

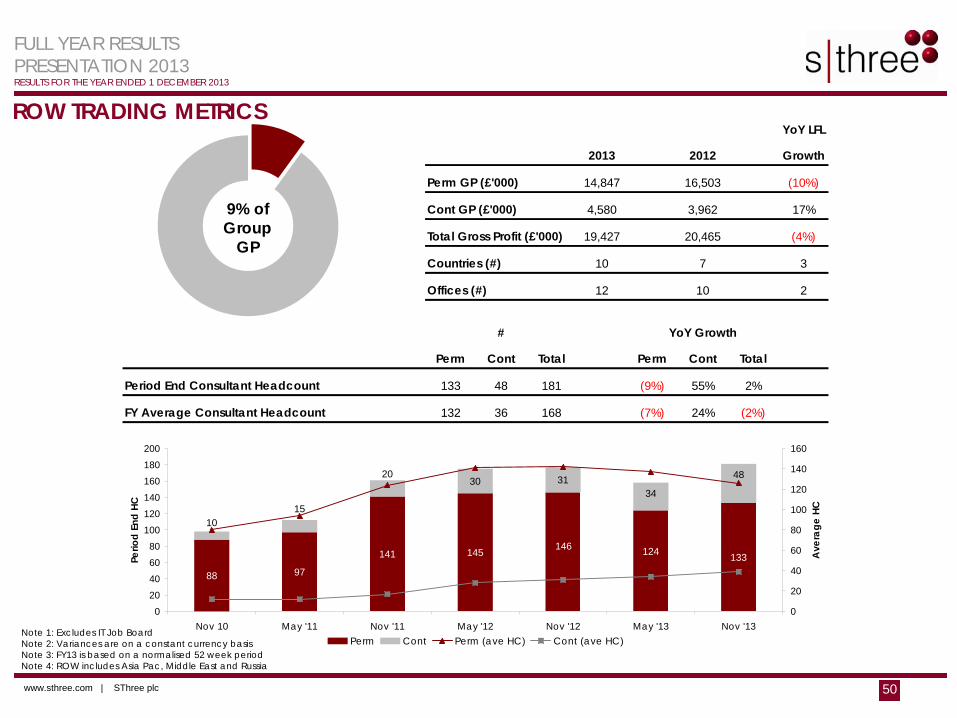

Perm GP (£'000) 14,847 16,503 (10%)

Cont GP (£'000) 4,580 3,962 17%

Total Gross Profit (£'000) 19,427 20,465 (4%)

Countries (#) 10 7 3

Offices (#) 12 10 2

Perm Cont Total Perm Cont Total

Period End Consultant Headcount 133 48 181 (9%) 55% 2%

FY Average Consultant Headcount 132 36 168 (7%) 24% (2%)

# YoY Growth

88 97

141 145 133

30 31

146 124

4820

3415

10

020406080

100120140160180200

Nov 10 May '11 Nov '11 May '12 Nov '12 May '13 Nov '13

Perio

d En

d HC

0

20

40

60

80

100

120

140

160

Ave

rage

HC

Perm Cont Perm (ave HC) Cont (ave HC)

ROW TRADING METRICS

9% of Group

GP

Note 1: Excludes IT Job BoardNote 2: Variances are on a constant currency basisNote 3: FY13 is based on a normalised 52 week periodNote 4: ROW includes Asia Pac, Middle East and Russia

FULL YEAR RESULTSPRESENTATION 2013RESULTS FOR THE YEAR ENDED 1 DECEMBER 2013

www.sthree.com | SThree plc 51

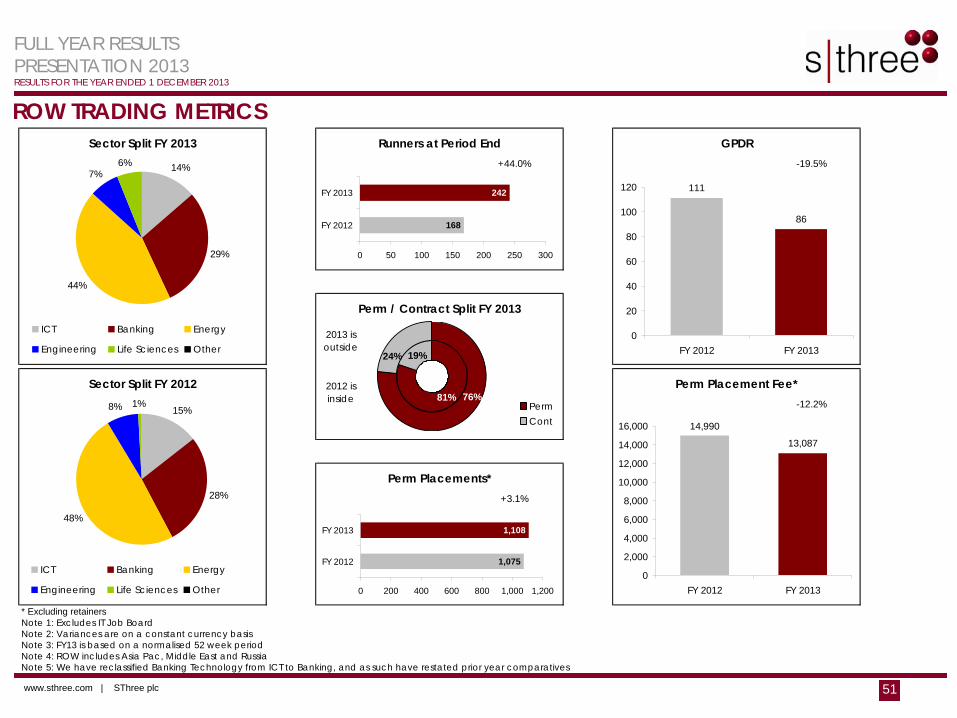

ROW TRADING METRICS

* Excluding retainersNote 1: Excludes IT Job BoardNote 2: Variances are on a constant currency basisNote 3: FY13 is based on a normalised 52 week periodNote 4: ROW includes Asia Pac, Middle East and RussiaNote 5: We have reclassified Banking Technology from ICT to Banking, and as such have restated prior year comparatives

Sector Split FY 2012

Sector Split FY 2013 Runners at Period End+44.0%

2012 is inside

Perm Placements*+3.1%

Perm / Contract Split FY 2013

Perm Placement Fee*-12.2%

GPDR-19.5%

2013 is outside

168

242

0 50 100 150 200 250 300

FY 2012

FY 2013

1,075

1,108

0 200 400 600 800 1,000 1,200

FY 2012

FY 2013

111

86

0

20

40

60

80

100

120

FY 2012 FY 2013

14,990

13,087

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

FY 2012 FY 2013

14%

29%

44%

7%6%

ICT Banking Energy

Engineering Life Sciences Other

15%

28%

48%

8% 1%

ICT Banking Energy

Engineering Life Sciences Other

19%

81%

24%

76%PermCont

FULL YEAR RESULTSPRESENTATION 2013RESULTS FOR THE YEAR ENDED 1 DECEMBER 2013

www.sthree.com | SThree plc 52

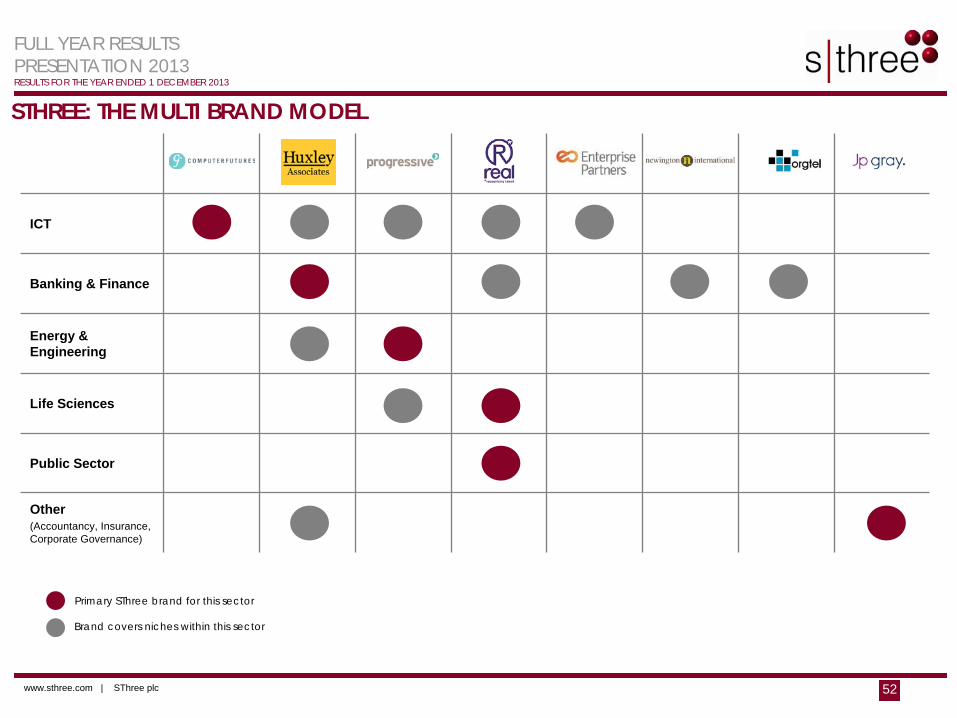

STHREE: THE MULTI BRAND MODEL

ICT

Banking & Finance

Energy & Engineering

Life Sciences

Public Sector

Other(Accountancy, Insurance, Corporate Governance)

Primary SThree brand for this sector

Brand covers niches within this sector

FULL YEAR RESULTSPRESENTATION 2013RESULTS FOR THE YEAR ENDED 1 DECEMBER 2013

www.sthree.com | SThree plc 53

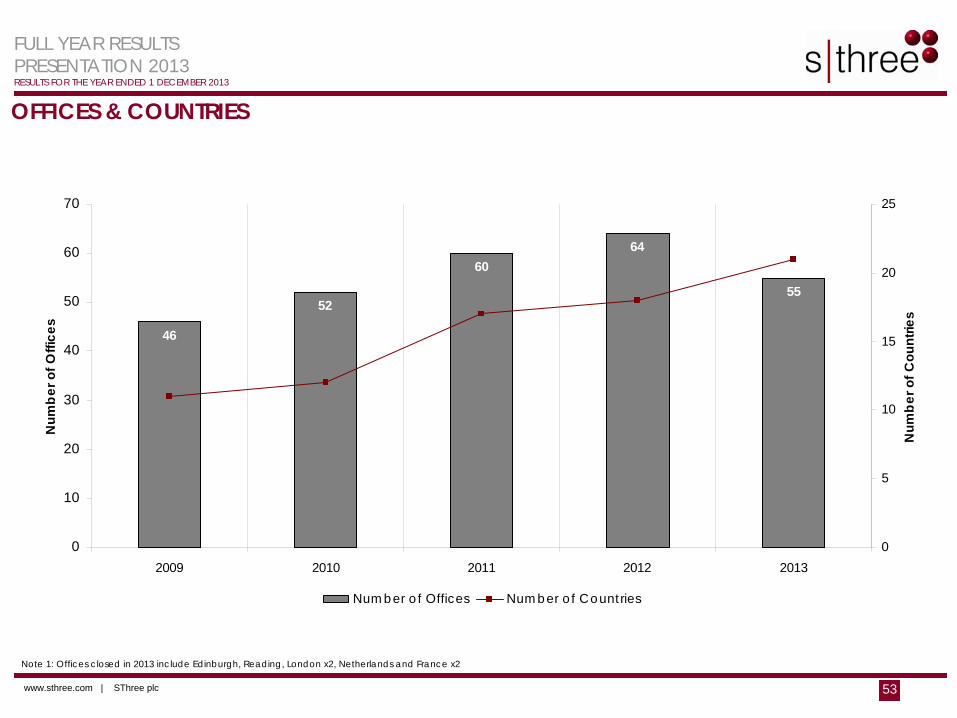

OFFICES & COUNTRIES

55

6460

52

46

0

10

20

30

40

50

60

70

2009 2010 2011 2012 2013

Year

Num

ber o

f Offi

ces

0

5

10

15

20

25

Num

ber o

f Cou

ntrie

s

Number of Offices Number of Countries

Note 1: Offices closed in 2013 include Edinburgh, Reading, London x2, Netherlands and France x2

FULL YEAR RESULTSPRESENTATION 2013RESULTS FOR THE YEAR ENDED 1 DECEMBER 2013

www.sthree.com | SThree plc 54

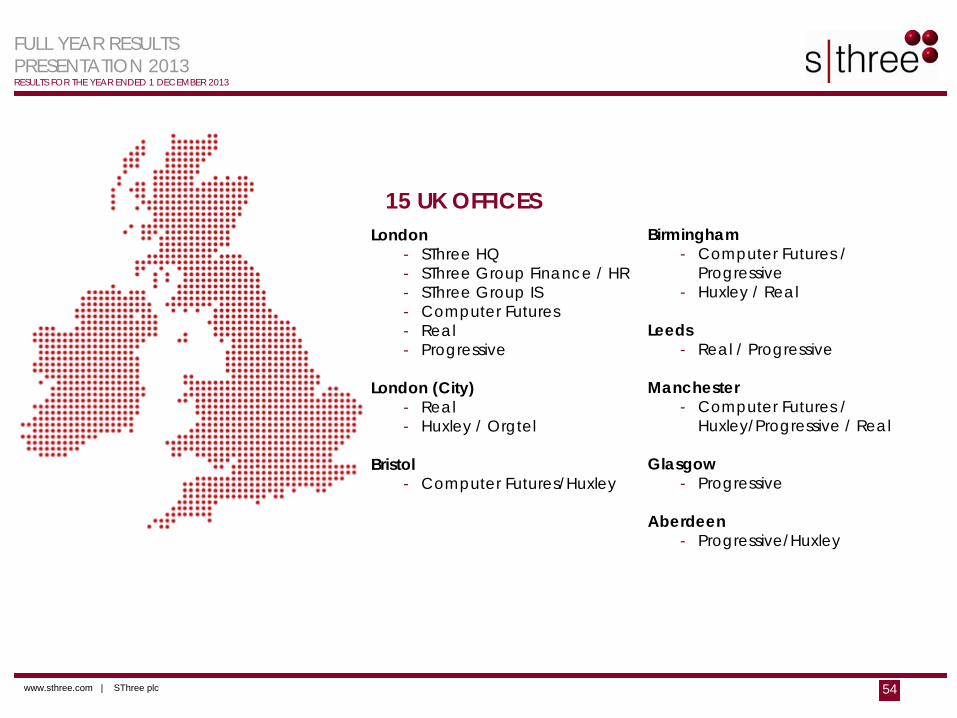

15 UK OFFICESLondon

- SThree HQ- SThree Group Finance / HR- SThree Group IS- Computer Futures- Real- Progressive

London (City)- Real- Huxley / Orgtel

Bristol- Computer Futures/Huxley

Birmingham- Computer Futures /

Progressive- Huxley / Real

Leeds- Real / Progressive

Manchester- Computer Futures /

Huxley/Progressive / Real

Glasgow- Progressive

Aberdeen- Progressive/Huxley

FULL YEAR RESULTSPRESENTATION 2013RESULTS FOR THE YEAR ENDED 1 DECEMBER 2013

www.sthree.com | SThree plc 55

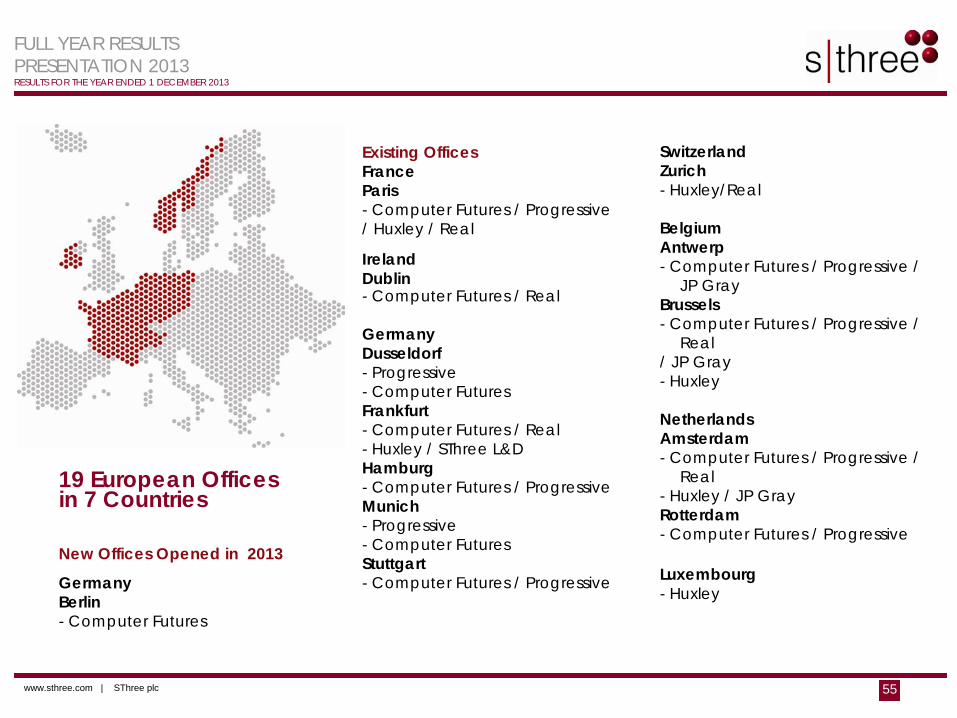

19 European Officesin 7 Countries

New Offices Opened in 2013

GermanyBerlin- Computer Futures

Existing OfficesFrance Paris- Computer Futures / Progressive/ Huxley / Real

IrelandDublin- Computer Futures / Real

Germany Dusseldorf- Progressive- Computer FuturesFrankfurt- Computer Futures / Real- Huxley / SThree L&D Hamburg- Computer Futures / ProgressiveMunich- Progressive- Computer FuturesStuttgart- Computer Futures / Progressive

SwitzerlandZurich- Huxley/Real

BelgiumAntwerp- Computer Futures / Progressive /

JP GrayBrussels- Computer Futures / Progressive /

Real / JP Gray- Huxley

NetherlandsAmsterdam- Computer Futures / Progressive /

Real- Huxley / JP GrayRotterdam- Computer Futures / Progressive

Luxembourg- Huxley

FULL YEAR RESULTSPRESENTATION 2013RESULTS FOR THE YEAR ENDED 1 DECEMBER 2013

www.sthree.com | SThree plc 56

MalaysiaMiri- ProgressiveKuala Lumpur- Progressive

Existing OfficesSingapore- Progressive / Huxley

/ Real

21 ROW Officesin 13 CountriesNew Offices Opened in 2013CanadaCalgary- Progressive

JapanTokyo- Computer Futures / Real

ThailandBangkok- Progressive

AustraliaPerth- ProgressiveSydney- Progressive / Huxley /

Real

Hong Kong- Huxley

IndiaMumbai- Huxley

GCCDubai- Progressive / HuxleyDoha- Progressive / Huxley

Russia Moscow- Progressive

USABoston - HuxleyChicago- Huxley / RealHouston - ProgressiveNew York- Huxley / Real / Computer

FuturesSan Diego- RealSan Francisco- Real / Computer Futures

BrazilSao Paulo- HuxleyRio De Janeiro- Progressive

FULL YEAR RESULTSPRESENTATION 2013RESULTS FOR THE YEAR ENDED 1 DECEMBER 2013

www.sthree.com | SThree plc 57

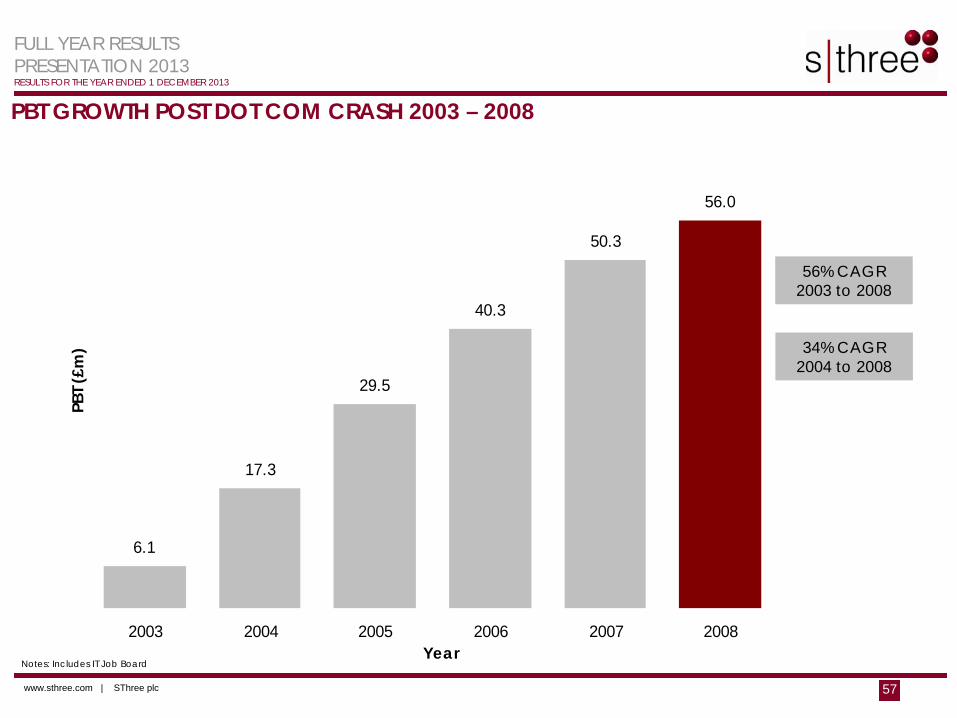

6.1

17.3

29.5

40.3

50.3

56.0

0

10

20

30

40

50

60

2003 2004 2005 2006 2007 2008

PBT GROWTH POST DOT COM CRASH 2003 – 2008

56% CAGR 2003 to 2008

Year

PBT (

£m) 34% CAGR

2004 to 2008

Notes: Includes IT Job Board

FULL YEAR RESULTSPRESENTATION 2013RESULTS FOR THE YEAR ENDED 1 DECEMBER 2013

www.sthree.com | SThree plc 58

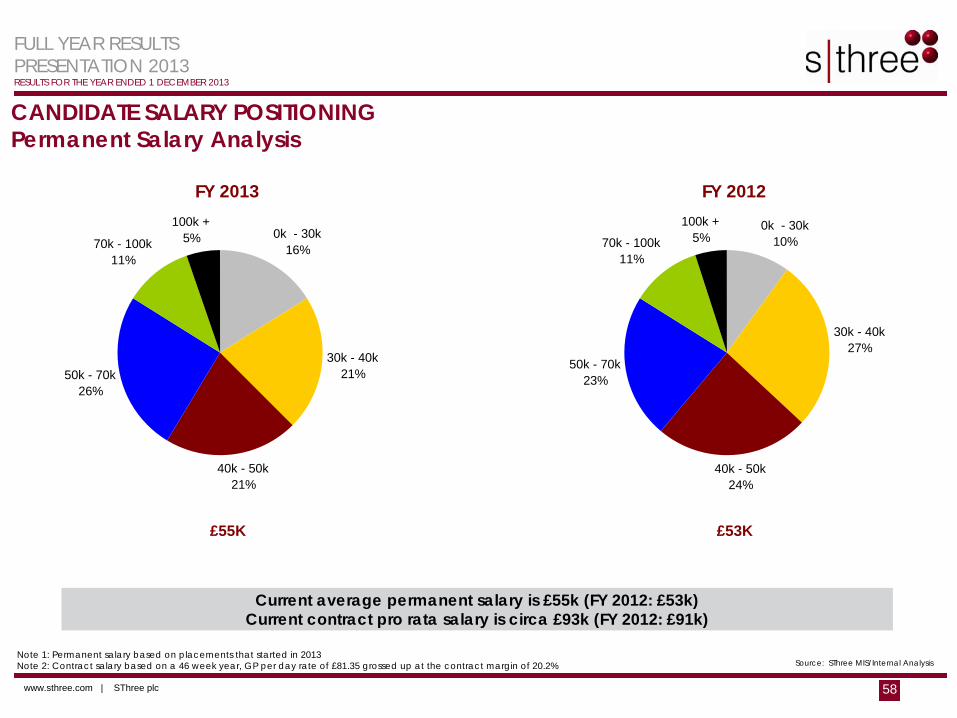

CANDIDATE SALARY POSITIONINGPermanent Salary Analysis

Current average permanent salary is £55k (FY 2012: £53k) Current contract pro rata salary is circa £93k (FY 2012: £91k)

Note 1: Permanent salary based on placements that started in 2013Note 2: Contract salary based on a 46 week year, GP per day rate of £81.35 grossed up at the contract margin of 20.2% Source: SThree MIS/Internal Analysis

£55K £53K

FY 2013 FY 2012

30k - 40k21%

40k - 50k21%

50k - 70k26%

70k - 100k11%

100k +5% 0k - 30k

16%

30k - 40k27%

40k - 50k24%

50k - 70k23%

70k - 100k11%

100k +5%

0k - 30k10%

FULL YEAR RESULTSPRESENTATION 2013RESULTS FOR THE YEAR ENDED 1 DECEMBER 2013

www.sthree.com | SThree plc 59

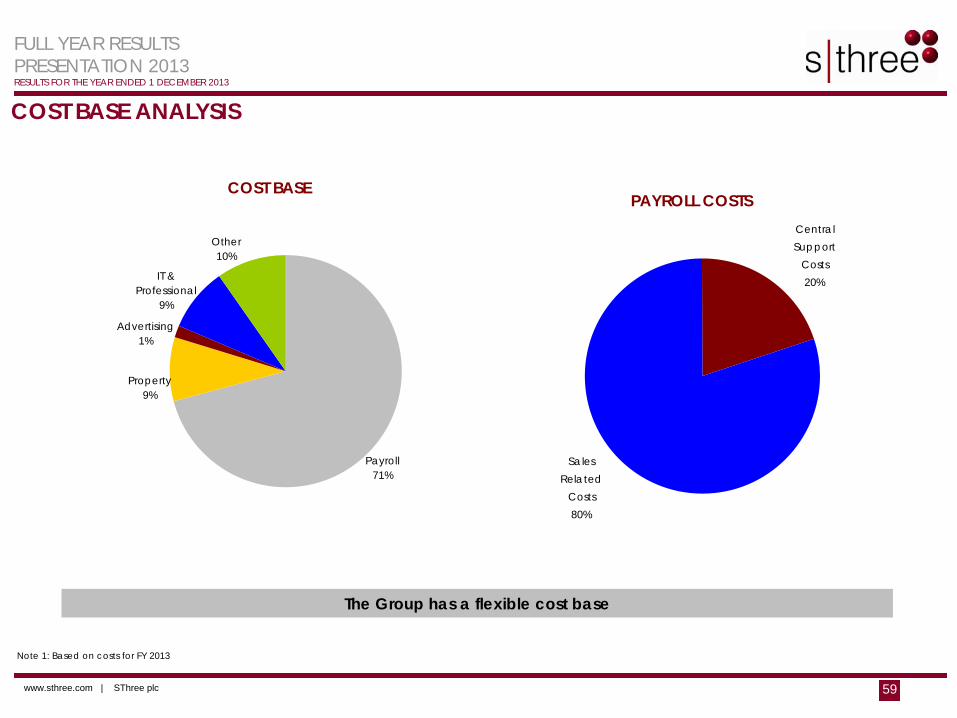

COST BASE ANALYSIS

The Group has a flexible cost base

Note 1: Based on costs for FY 2013

COST BASE

Other10%

Advertising1%

IT & Professional

9%

Payroll71%

Property9%

Sales Related

Costs80%

Central Support

Costs20%

PAYROLL COSTS

FULL YEAR RESULTSPRESENTATION 2013RESULTS FOR THE YEAR ENDED 1 DECEMBER 2013

www.sthree.com | SThree plc 60

Background• Circa 100 participants, across all geographies and sectors

• An opportunity to buy into a new business at an early stage, to become a part owner

• A key retention and attraction tool, a point of difference, given low barriers to entry

Features• A senior individual may be invited to invest in the scheme at fair value

• After a set number of years of MI holding and employment (typically 5 years), the individual can offer the vested stake for sale to SThree, against SThree shares

• The sale price is set with reference to a formula, typically between 1/2 and 2/3 x tracked business PAT x SThree plc historic PE ratio

• SThree is not obliged to purchase a minority stake offered. All stakes offered back will be considered by the MI Steering Committee, comprising of the CEO & CFO and approved by the main Board

• Buy backs for 2013 were c£7m

• Expected future buy backs to be £5m - £15m pa in shares, with marginal dilution if new shares are issued

• Buy backs in any year are dependent upon whether or not a stake is offered up for sale and accepted by SThree, the PAT of tracked businesses, the Group PE Ratio and the Board’s desire to buy out the shares offered

TRACKER SHARES (MINORITY INTEREST) ARRANGEMENTS

FULL YEAR RESULTSPRESENTATION 2013RESULTS FOR THE YEAR ENDED 1 DECEMBER 2013

www.sthree.com | SThree plc 61

Accounting• Accounting governed by IFRS 2 “Share-Based Payments”, with no income statement charge as the

payment made by participants equals the fair value of the award at that time

• A provision of £3.7m (2012: £4.4m), relating to the obligation to repay subscriptions if an employee leaves the Group before vesting, is held on the Balance Sheet

• Diluted EPS shows the dilutive impact of tracker share arrangements if all profitable tracked businesses had vested and are based on the previous year’s profits and by applying the last month’s (November 2013) average Group PE Ratio

TRACKER SHARES (MINORITY INTEREST) ARRANGEMENTS (continued)

FULL YEAR RESULTSPRESENTATION 2013RESULTS FOR THE YEAR ENDED 1 DECEMBER 2013

www.sthree.com | SThree plc 62

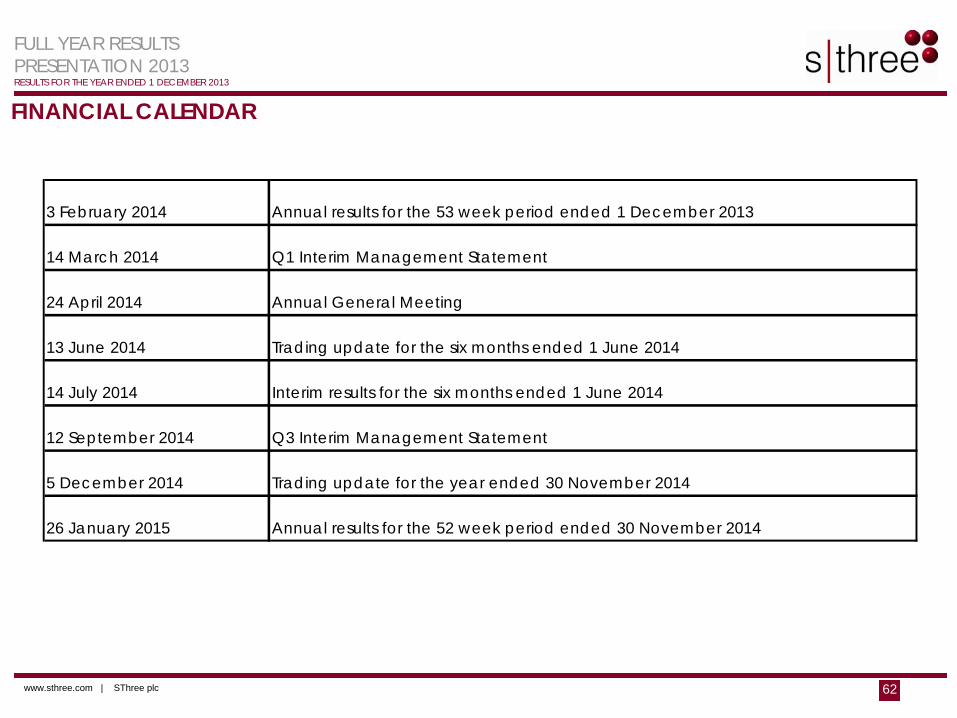

FINANCIAL CALENDAR

3 February 2014 Annual results for the 53 week period ended 1 December 2013

14 March 2014 Q1 Interim Management Statement

24 April 2014 Annual General Meeting

13 June 2014 Trading update for the six months ended 1 June 2014

14 July 2014 Interim results for the six months ended 1 June 2014

12 September 2014 Q3 Interim Management Statement

5 December 2014 Trading update for the year ended 30 November 2014

26 January 2015 Annual results for the 52 week period ended 30 November 2014

FULL YEAR RESULTSPRESENTATION 2013RESULTS FOR THE YEAR ENDED 1 DECEMBER 2013

www.sthree.com | SThree plc 63

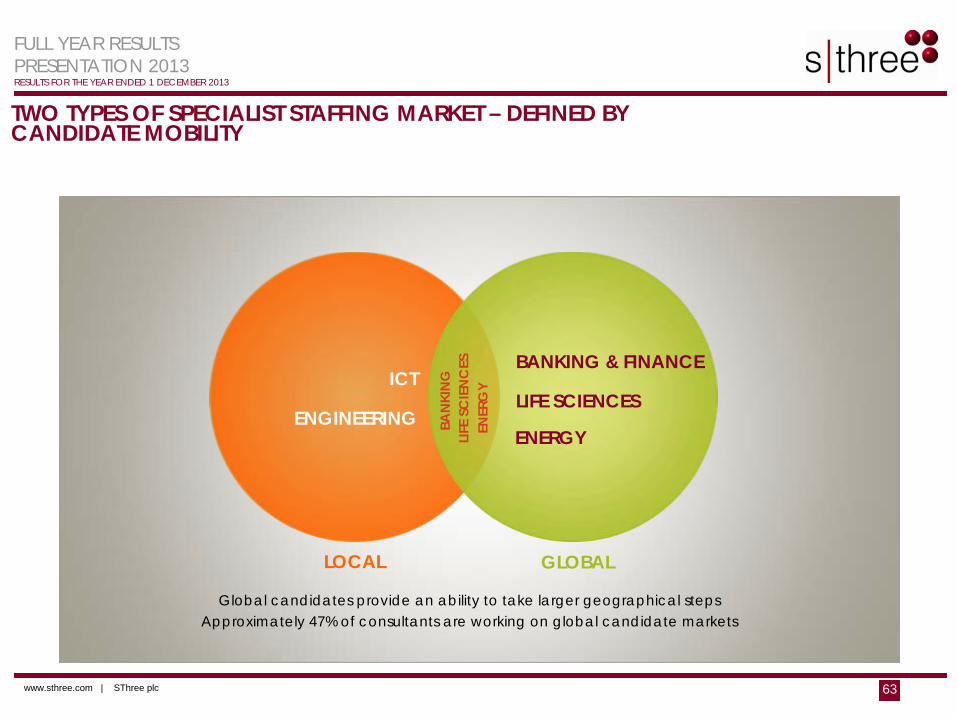

TWO TYPES OF SPECIALIST STAFFING MARKET – DEFINED BY CANDIDATE MOBILITY

LIFE SCIENCES

BANKING & FINANCE

ENERGYENGINEERING

ICT

LIFE

SC

IEN

CES

BAN

KIN

G

ENER

GY

GLOBALLOCAL

Global candidates provide an ability to take larger geographical steps Approximately 47% of consultants are working on global candidate markets

FULL YEAR RESULTSPRESENTATION 2013RESULTS FOR THE YEAR ENDED 1 DECEMBER 2013

www.sthree.com | SThree plc 64

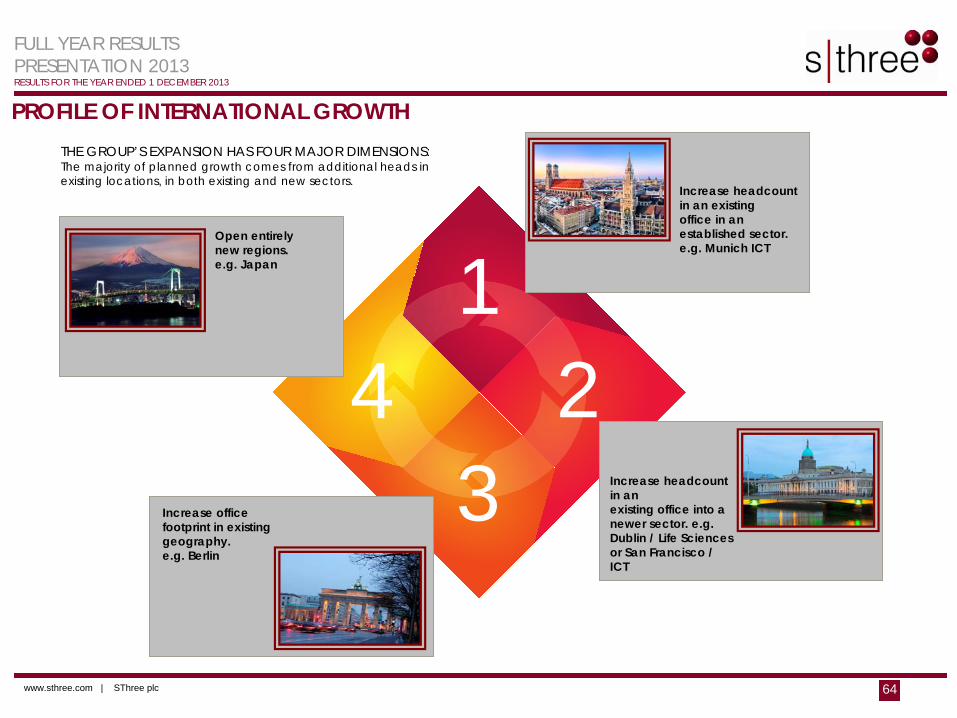

THE GROUP’S EXPANSION HAS FOUR MAJOR DIMENSIONS: The majority of planned growth comes from additional heads in existing locations, in both existing and new sectors.

12

34

Increase headcount in an existing office in an established sector.e.g. Munich ICT

PROFILE OF INTERNATIONAL GROWTH

Increase headcount in anexisting office into a newer sector. e.g. Dublin / Life Sciences or San Francisco / ICT

Open entirely new regions.e.g. Japan

Increase office footprint in existing geography. e.g. Berlin

FULL YEAR RESULTSPRESENTATION 2013RESULTS FOR THE YEAR ENDED 1 DECEMBER 2013

www.sthree.com | SThree plc 65

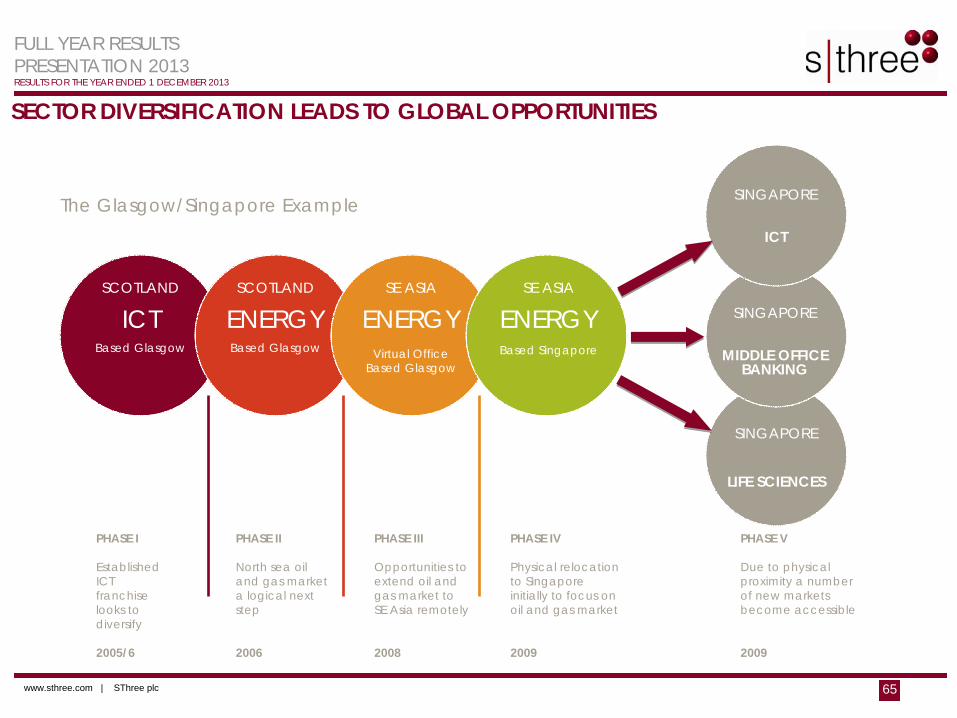

SECTOR DIVERSIFICATION LEADS TO GLOBAL OPPORTUNITIES

PHASE I

Established ICTfranchise looks todiversify

2005/6

SCOTLAND

ICTBased Glasgow

SCOTLAND

ENERGYBased Glasgow

SE ASIA

ENERGYVirtual Office

Based Glasgow

SE ASIA

ENERGYBased Singapore

SINGAPORE

ICT

SINGAPORE

MIDDLE OFFICEBANKING

SINGAPORE

LIFE SCIENCES

The Glasgow/Singapore Example

PHASE II

North sea oil and gas market a logical next step

2006

PHASE III

Opportunities toextend oil and gas market to SE Asia remotely

2008

PHASE IV

Physical relocationto Singaporeinitially to focus onoil and gas market

2009

PHASE V

Due to physicalproximity a numberof new marketsbecome accessible

2009

FULL YEAR RESULTSPRESENTATION 2013RESULTS FOR THE YEAR ENDED 1 DECEMBER 2013

www.sthree.com | SThree plc 66

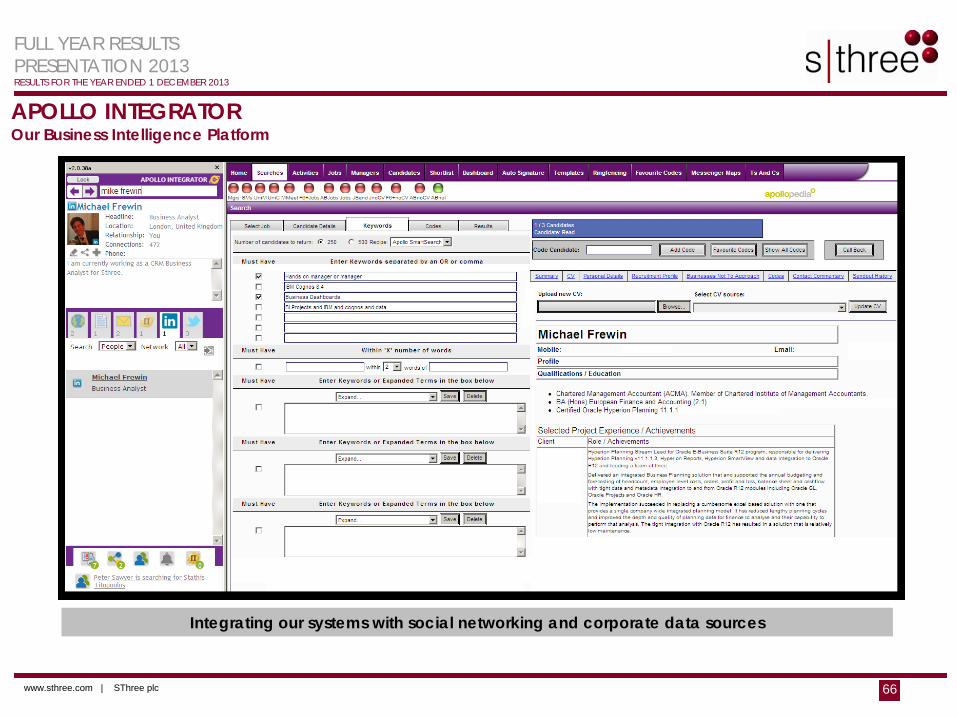

APOLLO INTEGRATOR

Integrating our systems with social networking and corporate data sources

Our Business Intelligence Platform

FULL YEAR RESULTSPRESENTATION 2013RESULTS FOR THE YEAR ENDED 1 DECEMBER 2013

www.sthree.com | SThree plc 67

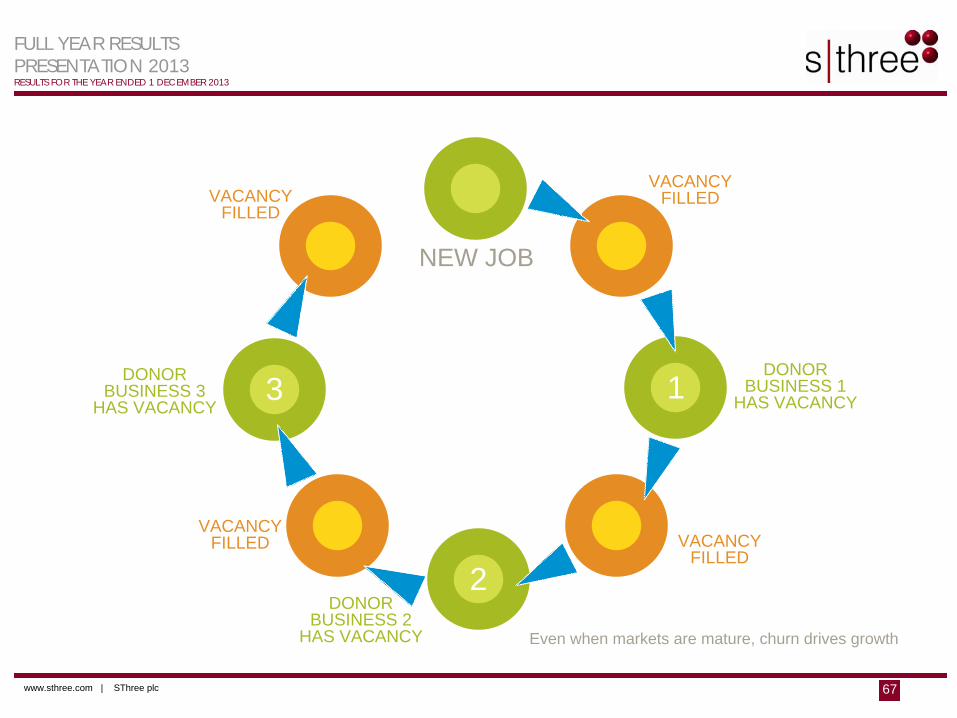

NEW JOB

Even when markets are mature, churn drives growth

VACANCY FILLED

DONOR BUSINESS 1

HAS VACANCY

VACANCY FILLED

DONOR BUSINESS 2

HAS VACANCY

VACANCY FILLED

VACANCY FILLED

DONOR BUSINESS 3

HAS VACANCY1

2

3