FULL YEAR 2014 RESULTS HEINEKEN N.V.€¦ · 3 2014 Key Highlights 1 Sol premium (volume outside...

26

1 Jean-François van Boxmeer FULL YEAR 2014 RESULTS HEINEKEN N.V. CHAIRMAN OF THE EXECUTIVE BOARD/CEO AMSTERDAM, 11 FEBRUARY 2015 Strong profit growth, delivering on strategic priorities

Transcript of FULL YEAR 2014 RESULTS HEINEKEN N.V.€¦ · 3 2014 Key Highlights 1 Sol premium (volume outside...

1

Jean-François van Boxmeer

FULL YEAR 2014 RESULTS HEINEKEN N.V.

CHAIRMAN OF THE EXECUTIVE BOARD/CEO

AMSTERDAM, 11 FEBRUARY 2015

Strong profit growth, delivering on strategic priorities

2

Disclaimer

This presentation contains forward-looking statements with regard to the financial position and results of HEINEKEN’s activities. These forward-looking statements are subject to risks and uncertainties that could cause actual results to differ materially from those expressed in the forward-looking statements.

Many of these risks and uncertainties relate to factors that are beyond HEINEKEN’s ability to control or estimate precisely, such as future market and economic conditions, the behaviour of other market participants, changes in consumer preferences, the ability to successfully integrate acquired businesses and achieve anticipated synergies, costs of raw materials, interest rate and foreign exchange fluctuations, change in tax rates, changes in law, changes in pension costs, the actions of government regulators and weather conditions. These and other risk factors are detailed in HEINEKEN’s publicly filed annual reports.

You are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date of this presentation. HEINEKEN does not undertake any obligation to publicly release any revisions to these forward-looking statements to reflect events or circumstances after the date of these materials.

Market share estimates contained in this presentation are based on outside sources such as specialised research institutes in combination with management estimates.

3

2014 Key Highlights

1 Sol premium (volume outside home market)

Strong performance reflects effectiveness of our strategy

Group revenue +3.3% organically with group rev/hl up +1.4%

Top and bottom line growth across the business

Heineken® volume +5.1% reporting positive growth in all regions

Double digit growth for global brands Desperados, Affligem and Sol1

Innovation contributed €1.5bn of revenue and rate accelerated to 7.7%

Consolidated operating profit (beia) margin up 90bps, well ahead of

medium term margin guidance (40bps)

Diluted EPS (beia) up 11%, proposed DPS up 24% (36% pay-out ratio)

4

Healthy growth across the business

2014FY Organic growth %

AFRICA MIDDLE

EASTAMERICAS

ASIA PACIFIC

CENTRAL & EASTERN EUROPE

WESTERN EUROPE

HEINEKENNV

Consolidated revenue 4.4 6.9 5.3 -3.7 2.2 3.0

Revenue per HL -3.1 3.2 0.4 1.4 0.5 1.2

Consolidated operating profit (beia) 8.8 16 5.4 -4.5 4.5 8.7

Group Beer volume 6.7 3.7 5.0 -4.2 2.3 2.0

5

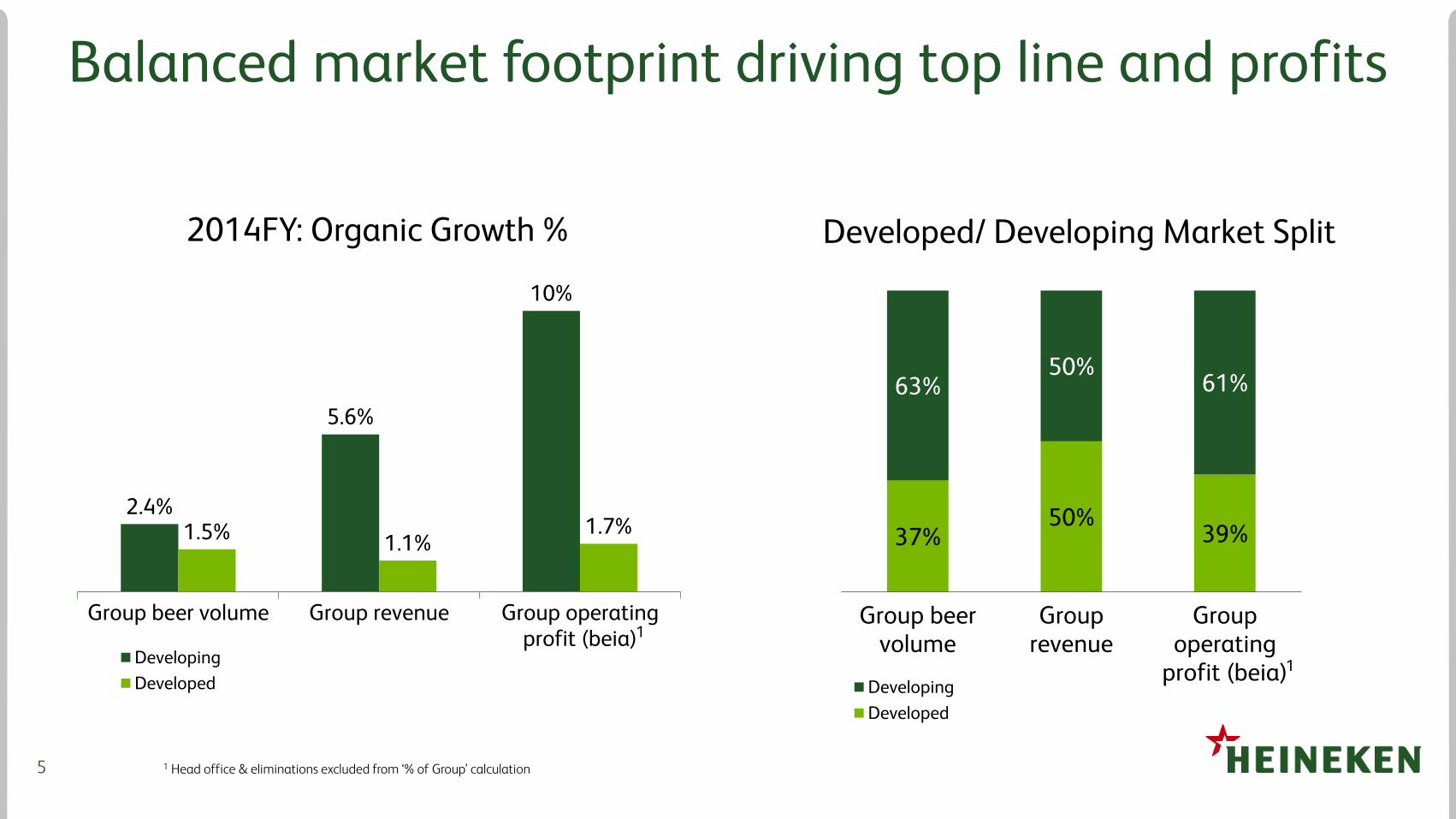

Balanced market footprint driving top line and profits

1 Head office & eliminations excluded from ‘% of Group’ calculation

37%50%

39%

63%50%

61%

Group beervolume

Grouprevenue

Groupoperating

profit (beia)Developing

Developed

Developed/ Developing Market Split2014FY: Organic Growth %

2.4%

5.6%

10%

1.5% 1.1%1.7%

Group beer volume Group revenue Group operatingprofit (beia)

Developing

Developed

1

1

6

Heineken® consistently outperforming premium

Source: Canadean – March 2014. FY2014 estimates on beer market and IPS * IPS = International Premium Segment (volume outside home market)

Heineken® premium volumes 2014FY

1.8%

4.0%

5.1%

Beer market IPS* Heineken®

Heineken® brand growing across all regions

Double digit growth in Brazil, China, France, the UK and Mexico

Encouraging progress in the US with positive Heineken® volume in Q4.

Successful ‘The City’ campaign, exciting pipeline for 2015 brand activation and marketing

7

Innovation delivered €1.5bn revenue, rate of 7.7%

From 1 January 2013, the innovation rate is calculated as revenues generated from innovation introduced in the past 40 quarters for a new category, 20 quarters for a new brand and 12 quarters for all other innovations, excluding packaging renovations divided by total revenue

Competitive advantage and sustainable contributor to profitability

Innovation rate1 New pack types Brand extensions

Innovation revenue Radler and alcohol free propositions Improving draught offer

3.0%

4.1%

5.3% 5.9%

7.7%

2010 2011 2012 2013 2014

2020 Target: 6%

€0.4bn

€1.5bn

2010 2014

40% CAGR

8

Continued focus on driving cost efficiencies

TCM2 completed in H1 2014 ahead of target and schedule.

Committed to driving further cost savings: Rightsizing the organisation to optimise cost structure Drive End2End productivity to grow topline and profits Leveraging global scale through Global Business Service organisation:

Additional efficiencies in HEINEKEN Global Procurement (HGP) Extending geographic scope and activities of HEINEKEN’s

Global Shared Services (HGSS)

Further cost savings are a key component of HEINEKEN’s medium term margin guidance

9

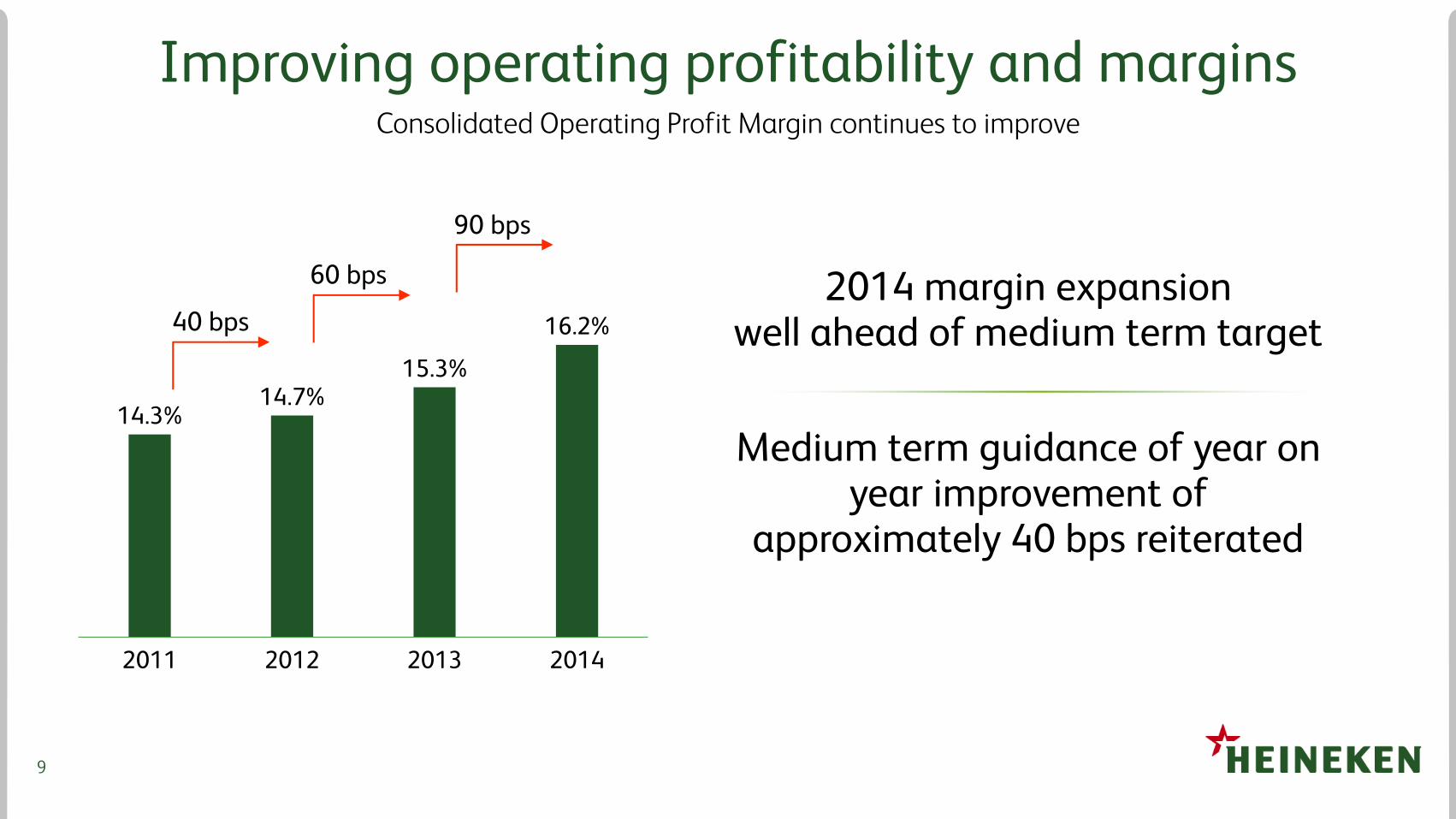

14.3%14.7%

15.3%

16.2%

2011 2012 2013 2014

Improving operating profitability and marginsConsolidated Operating Profit Margin continues to improve

90 bps

40 bps

60 bps 2014 margin expansion well ahead of medium term target

Medium term guidance of year on year improvement of

approximately 40 bps reiterated

10

2015 Full Year Outlook1

1 Based on consolidated reporting

Committed to delivering on strategic priorities – further revenue and profit growth in 2015

Continued challenging external environment

Positive organic revenue growth: Positive volume development more moderate than 2014 and weighted to H2 Revenue per hectolitre to increase driven by revenue management initiatives, pricing limited by

deflationary and off premise pressures in some markets

Slight increase in marketing and selling spend (beia) as percentage of revenue

Input cost prices to be slightly lower (excluding a foreign currency transactional effect)

Continue to target a year-on-year improvement in consolidated operating profit (beia) margin of around 40bps in the medium term. In 2015 consolidated operating profit (beia) margin will be adversely impacted by approximately 25bps from the disposal of EMPAQUE. HEINEKEN will partially but not fully offset this, such that in 2015 consolidated operating profit (beia) margin improvement will be somewhat below the 40bps medium term level

11

René Hooft Graafland

FULL YEAR 2014 RESULTS HEINEKEN N.V.

MEMBER OF THE EXECUTIVE BOARD/CFO

AMSTERDAM, 11 FEBRUARY 2015

12

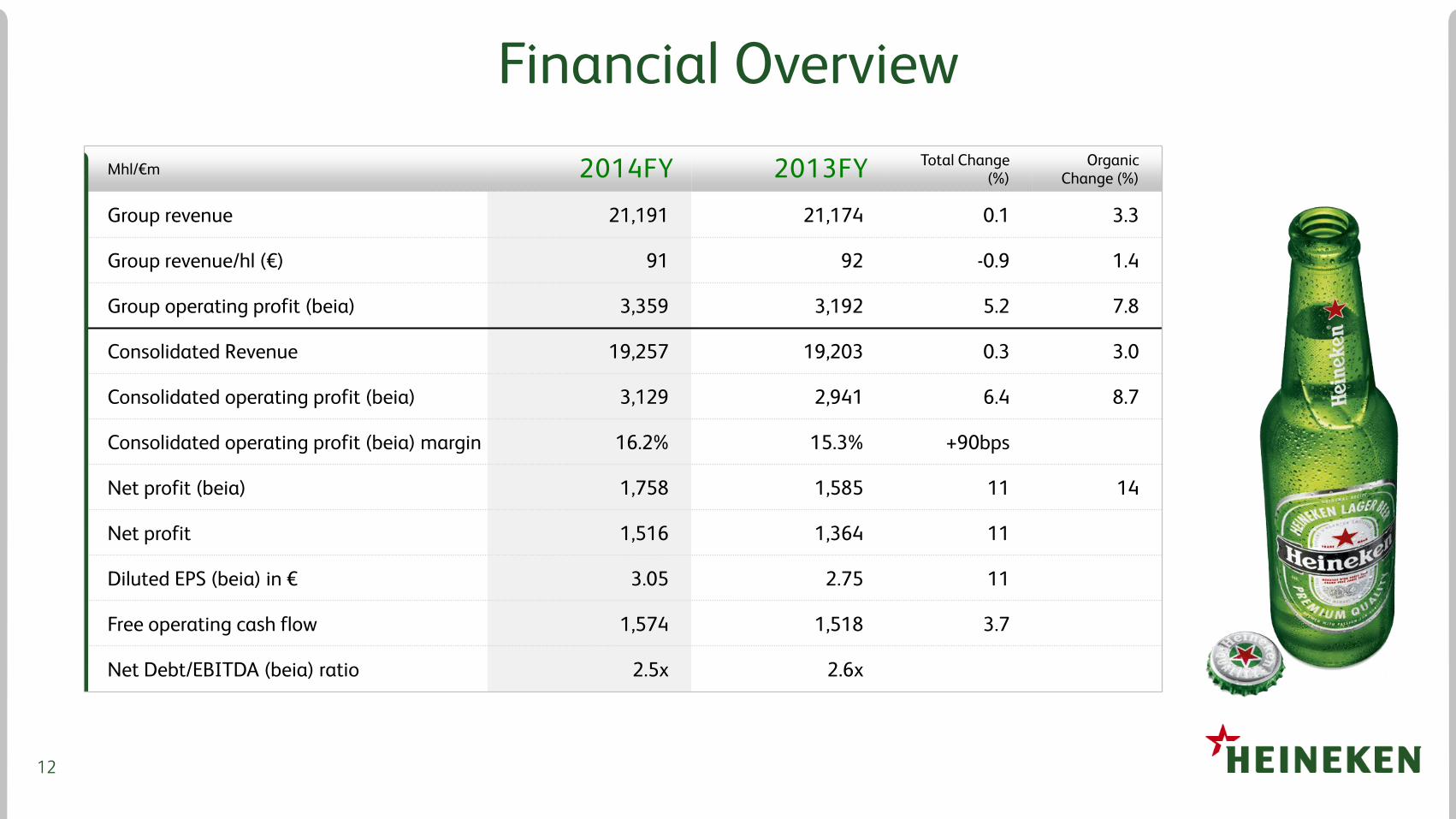

Financial Overview

Mhl/€m 2014FY 2013FY Total Change(%)

OrganicChange (%)

Group revenue 21,191 21,174 0.1 3.3

Group revenue/hl (€) 91 92 -0.9 1.4

Group operating profit (beia) 3,359 3,192 5.2 7.8

Consolidated Revenue 19,257 19,203 0.3 3.0

Consolidated operating profit (beia) 3,129 2,941 6.4 8.7

Consolidated operating profit (beia) margin 16.2% 15.3% +90bps

Net profit (beia) 1,758 1,585 11 14

Net profit 1,516 1,364 11

Diluted EPS (beia) in € 3.05 2.75 11

Free operating cash flow 1,574 1,518 3.7

Net Debt/EBITDA (beia) ratio 2.5x 2.6x

13

Group Organic Revenue Growth +3.3%

19,203 19,257

21,174

-1.1% -1.6%

+1.8% +1.2%

21,191

2013FY Revenue Consolidation impact Currency translation Total cons. volume Consol. rev/hl 2014FY Revenue

Group: organic +3.3%

Attributable share of joint ventures & associates

Consolidated

1,971 1,934

€m

14

Group Operating Profit (Beia) OG +7.8%

2,9413,129

3,192

-0.6% -1.7%

+8.7%

3,359

2013FY Operating profit (beia) Consolidation impact Currency translation Organic growth 2014FY Operating profit (beia)

Group: organic +7.8%

Attributable share of joint ventures & associates

Consolidated

251230

€m

15

Diluted EPS (beia) €3.05, +11%

€2.75

€3.05

-€0.02-€0.06

+€0.38

2013FY Diluted EPS (beia) Consolidation impact Currency translation Organic growth 2014FY Diluted EPS (beia)

EPS +11%

16

Strong Free Operating cash flow

1 Defined as cumulative amounts of year-on-year changes in the Total Working Capital starting from 20102 Capital expenditure related to property, plant and equipment

Net debt/EBITDA target achieved

2014FY 2013FY vs. LY

Cash flow from operations (before change in working capital)

4,279 3,990 289

Change in working capital 27 51 -24

Capital expenditure2 -1,494 -1,369 -125

Free operating cash flow 1,574 1,518 56

Net debt/EBITDA 2.5x 2.6x

4.7%

6.4%7.1%

7.8%

0

500

1,000

1,500

2011 2012 2013 2014

Capital Expenditure2 as % of Revenue (€ million)

Capex (€m) Capex (% of revenues)

0

100

200

300

400

500

2011 2012 2013 2014

Cumulative working capital contribution to cash flow1

(€ million)

17

Currency and further financial guidance

1 Based on consolidated reporting

Adverse currency impact more pronounced in H1

Assuming spot rates as at 6 Feb 2015 positive currency translational impact on consolidated operating profit (beia) €130 million and €80 million at net profit (beia)

Capital expenditure to be approximately €1.6 billion (2014: €1.5 billion)

Stable average interest rate 3.7%, effective tax rate (beia) broadly in line with 2014

Translational FX impact (€ million)1

1H14 2H14 FY14 FY15E

Consolidated revenue -376 61 -315

Consolidated operating profit (beia) -55 6 -49 130

Net profit (beia) -35 3 -32 80

18

Summary

HEINEKEN remains committed to delivering on its strategic priorities

Strong performance in 2014FY reassures strategy is working

Effective commercial investments in brands, strong execution and innovation

driving market share gains

Revenue management and further cost savings underpin confidence

in margin expansion of around 40bps year-on-year in the medium-term

19

Appendix

FULL YEAR 2014 RESULTS HEINEKEN N.V.

20

Africa Middle East

Consolidated

Strong results achieved amid volatile trading environment

Solid volume growth across most

markets, in particular Nigeria,

Ethiopia, Cameroon, Burundi, DRC

and Egypt

Organic consolidated revenue/hl

declined by 3.1%, due to high

license volumes, unfavourable

country and product mix

Continued capital investment

in new capacity across key

markets

Heineken® growth of 7.8%

driven by South Africa, Nigeria,

Cameroon and Algeria

100bps improvement on

consolidated operating profit

(beia) margin mainly from

cost efficiencies

Revenue 2,643 3.5 4.4 3,085 2.7

Revenue/hl (in €) 84 -3.8 -3.1 82 -3.7

Operating profit (beia) 655 7.9 8.8 700 5.2

Operating profit (beia) margin 24.8% +100bps 22.7% +60bps

Total volume 31.6 7.6 7.5 37.6 6.6 6.6

of which:Beer volume

25.0 7.4 7.3 29.3 6.8 6.7

Total Change (%)

Organic Change (%)

Mhl/€m 2014FY 2014FY Total Change (%)

Organic Change (%)

Group

21

Americas

Consolidated

Strong top and bottom line growth

Revenue 4,631 3.0 6.9 5,401 1.6

Revenue/hl (in €) 85 -0.7 3.2 87 -1.8

Operating profit (beia) 780 8.6 16 887 6.1

Operating profit (beia) margin 16.8% +80bps 16.4% +70bps

Total volume 54.6 3.8 3.7 62.3 3.5 3.7

of which:Beer volume

53.2 3.9 3.9 57.0 3.7 3.7

Total Change (%)

Organic Change (%)

Mhl/€m 2014FY 2014FY Total Change (%)

Organic Change (%)

Group

Solid growth in Brazil, Mexico,

Panama and export markets resulted

in 3.7% volume growth

Heineken® grew by 4.0% led

by Brazil, Mexico and export

markets

Mexico saw strong profit growth with

200bps of margin expansion due to

strong topline supported by ongoing

cost efficiencies

Operating profit (beia) increased

organically by 16% primarily due

to double digit growth in Mexico

and positive performance in Brazil

Continued strong growth

of Dos Equis and Tecate

brands in U.S and Mexico

22

Asia Pacific

Consolidated

H2 driving growth

Revenue 2,088 2.5 5.3 2,455 3.2

Revenue/hl (in €) 112 -1.4 0.4 100 -1.4

Operating profit (beia) 550 2.5 5.4 598 3.0

Operating profit (beia) margin 26.3% 0bps 24.4% 0bps

Total volume 18.7 4.0 4.9 24.5 4.7 4.8

of which:Beer volume

18.3 5.5 5.2 24.0 5.8 5.0

Total Change (%)

Organic Change (%)

Mhl/€m 2014FY 2014FY Total Change (%)

Organic Change (%)

Group

Volume growth accelerated in the

second half, with improved

trading conditions witnessed

across key markets

Production capacity expanded in

Vietnam and China, and new

greenfield underway in Myanmar

and East Timor

Market share gains

across key markets:

Vietnam, Taiwan,

Indonesia

Consolidated operating profit (beia) up

5.4% organically, with gains from Vietnam,

China, Singapore, Cambodia and export

markets

Strong double digit growth

of Tiger brand driven by

successful commercial

activation

23

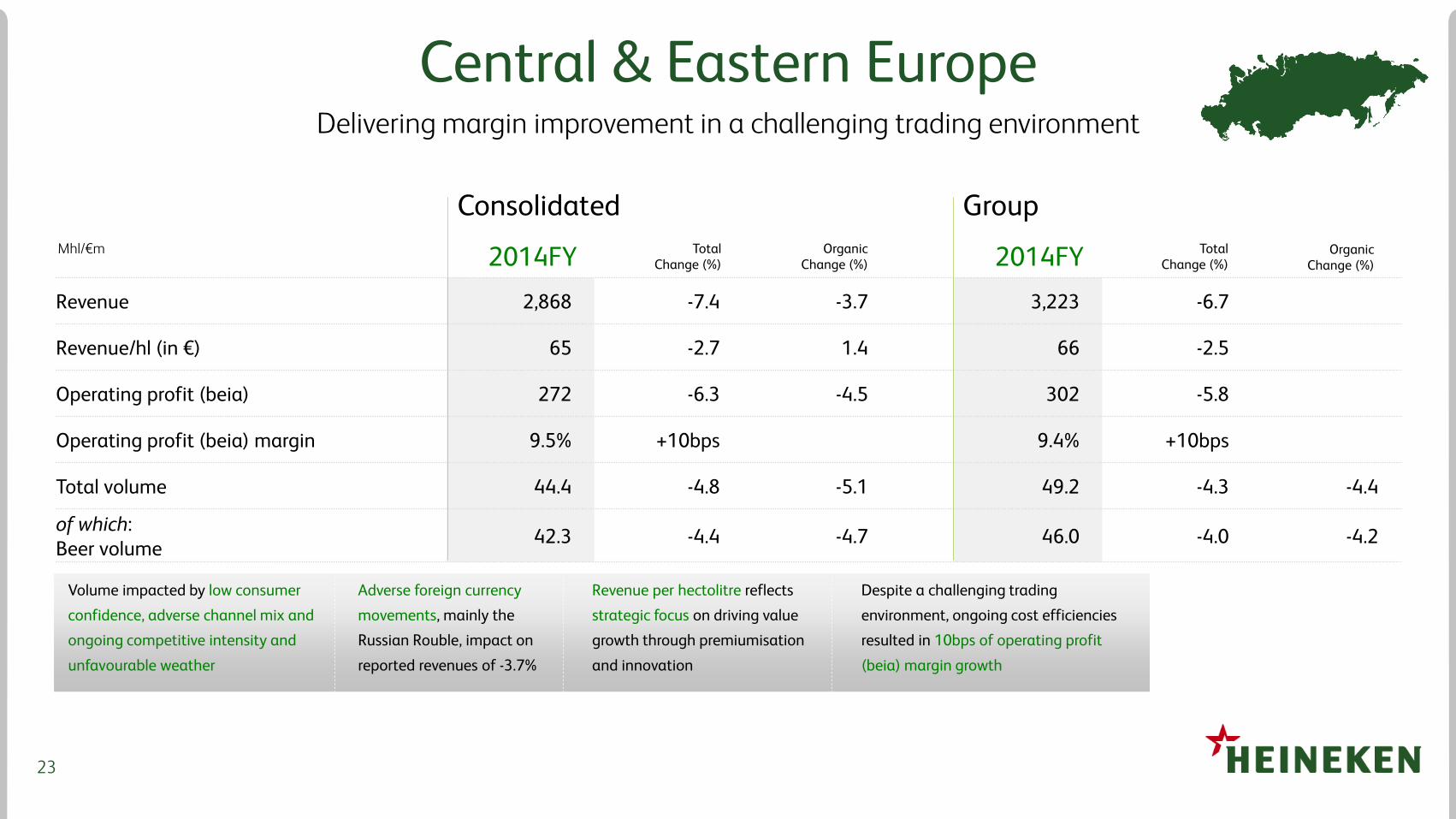

Central & Eastern Europe

Consolidated

Delivering margin improvement in a challenging trading environment

Revenue 2,868 -7.4 -3.7 3,223 -6.7

Revenue/hl (in €) 65 -2.7 1.4 66 -2.5

Operating profit (beia) 272 -6.3 -4.5 302 -5.8

Operating profit (beia) margin 9.5% +10bps 9.4% +10bps

Total volume 44.4 -4.8 -5.1 49.2 -4.3 -4.4

of which:Beer volume

42.3 -4.4 -4.7 46.0 -4.0 -4.2

Total Change (%)

Organic Change (%)

Mhl/€m 2014FY 2014FY Total Change (%)

Organic Change (%)

Group

Volume impacted by low consumer

confidence, adverse channel mix and

ongoing competitive intensity and

unfavourable weather

Adverse foreign currency

movements, mainly the

Russian Rouble, impact on

reported revenues of -3.7%

Despite a challenging trading

environment, ongoing cost efficiencies

resulted in 10bps of operating profit

(beia) margin growth

Revenue per hectolitre reflects

strategic focus on driving value

growth through premiumisation

and innovation

24

Western Europe

Consolidated & Group

Strong Execution & Higher Investments Driving Market Share Gains

Revenue 7,478 0.3 2.2

Revenue/hl (in €) 127 1.9 0.5

Operating profit (beia) 852 -0.1 4.5

Operating profit (beia) margin 11.4% 0bps

Total volume 59.0 -1.6 1.7

of which:Beer volume

42.5 0.5 2.3

Total Change (%)

Organic Change (%)

Mhl/€m 2014FY

Organic volume growth driven by broad-based market

share gains from focused commercial assertiveness,

increased brand investment and a clear consistent

strategy “Not An Inch Back” across the region

Organic revenue growth

supported by improving

volume and revenue per

hectolitre

Operating profit (beia)

grew 4.5% lead by

France, Spain, and the

Netherlands

The divestment of Oy

Hartwall Ab in Finland on

23 August 2013 is reported

as a consolidation impact

Strong focus on

innovation and

premiumisation

25

2012A 696 696 1.36

2013A 556 556 1.31

2014A 553 553 1.31

2015F 529 478 1.34

2016F 503 218 1.21

2012A -4

2013A 11

2014A 0

2015F* -1

2016F* 41

US Dollar Hedging

Position Impact

Net inflowIn USD mln

Hedged Part**Year Hedged Rate*** Year Net Profit

* Impact on open positions calculated by comparing spot rate with previous year’s hedging rate ** Hedging as at 6th February 2015*** Including the costs of hedging

26

Disposal of Empaque

Disposal announced on 1 September, for an EV of US $1,225 million to Crown Holdings Inc

Deal is subject to customary closing conditions and regulatory approval, and is expected to complete during Q1 2015

In 2014 EMPAQUE generated €515 million revenue mostly intercompany and €91 million EBIT (beia)

EMPAQUE results to date were included under ‘Head office’

In 2015 HEINEKEN consolidated operating profit (beia) margin will be adversely impacted by approximately 25bps from the disposal of EMPAQUE

HEINEKEN expects to record approximately €300 million post tax book gain, which will be treated as exceptional item in FY2015