From Goals to Reality - E

15

FDI policy in Japan from goals to reality

-

Upload

nicholas-benes -

Category

Documents

-

view

21 -

download

0

Transcript of From Goals to Reality - E

FDI policy in Japan

from goals to reality

2

Each year the American Chamber of Commerce in Japan (ACCJ) publishes at least one major policy document that we hope will make a positive contribution to improving Japan’s business climate for the benefit not only of our members but for all businesses in Japan.

This year the Chamber decided to focus on foreign direct investment into Japan in response to Prime Minister Junichiro Koizumi’s January speech to the Diet, in which he announced the government’s goal of doubling FDI in five years. A task force under the chairmanship of Nicholas Benes and Vice Chairs David Shuler, Thierry Porté, and Kumi Sato engaged the services of Japan’s most authoritative experts on FDI, Professor Kyoji Fukao of Hitotsubashi University and Tomofumi Amano of Toyo University, to conduct objective analysis and write a report illuminating the facts concerning FDI in Japan—including the kinds of benefits that it brings—and suggesting policy implications. Their extensive and excellent report was issued in Japanese on October 29, 2003, under the title ”Foreign Direct Investment and the Japanese Economy.”

In addition, the task force prepared the attached companion policy document, ”From Goals to Reality: FDI Policy in Japan.” This document builds on the facts and empirical analysis presented by Professors Fukao and Amano to dispel a number of myths and fears about FDI in Japan and offers a number of ACCJ policy recommendations for achieving the government’s goal of doubling FDI into Japan by 2008.

Finally, seven companies, including several ACCJ member companies, agreed to serve as case studies on how the process of inward direct investment into Japan actually occurs, and how it contributes to economic growth and the prosperity of the Japanese people.

I would like to express my appreciation on behalf of the ACCJ to Professors Fukao and Amano for their outstanding research and analysis, and especially to commend Chairman Benes for shepherding this complex and time-consuming project to fruition. In addition to overseeing the processes and inspiring his task force colleagues—who numbered almost 40—Mr. Benes also did much of the drafting for the general policy recommendations. His leadership, energy, and creativity were critical to the success of this undertaking.

I also would like especially to commend the work of the following task force members for their contributions of time and talent: Hidetoshi Asakura, Lawrence Bates, William Bishop, Andrew Conrad, John Diefenbach, Stephen Elliott, Robert Grondine, Toshi Hayami, Debbie Howard, Thomas Jordan, Masa Katsuyama, Terrie Lloyd, Mike Makino, Masa Matsushita, Takayuki Nakamura, David Sneider, Eric Sedlak, Linda Sherman, Gary Thomas, John Tofflemire, Kiyoshi Tsugawa, and Yasuaki Tsuchiya. Finally, I must extend our gratitude to the ACCJ staff members under Executive Director Donald Westmore who put in long hours and effort in support of this exceedingly complex project: Abby Pratt, Ryan Armstrong, Miho Yasuda, Emi Ogawa, Douglas Jackson, and Brechtje Zoet.

Sincerely,

Lance E. LeeACCJ President

letter from the president

1

ChairNicholas E. BenesJTP Corporation

Vice ChairsDavid L. ShulerGoldman Sachs (Japan) Ltd.

Thierry PortéMorgan Stanley Japan Ltd.

Vice Chair, Communications StrategyKumi Sato, Cosmo Public Relations

FDI task force team leadersNonperforming LoansYasu Tsuchiya and Masa Matsushita

Transparency and Corporate GovernanceDave Sneider, Hidetoshi Asakura, Nicholas Benes

Labor Mobility and Social Safety NetEric Sedlak and Larry Bates

Deregulation and Promoting EntrepreneurshipTed Johnson and Mike Makino

Stock SwapsBob Grondine, Gary Thomas, Eric Rouse

Cash MergersDave Sneider

the FDI task force of the american chamber of commerce in japan

FDI task force sponsorsGold SponsorsAFLACAIG CompaniesBaker & McKenzie/Tokyo Aoyama Aoki Law OfficeCitibank, N.A.The Coca-Cola CompanyEli Lilly Japan K.K.Federal Express CorporationGeneral Motors Asia Pacific (Japan) Ltd.General Electric Japan, Ltd.Goldman Sachs (Japan) Ltd.IBM World Trade Asia CorporationJapan External Trade Organization (JETRO)JTP CorporationMorgan Stanley Japan Ltd.Nestlé Japan GroupWhite & Case LLP

Silver SponsorsGMAC Commercial Mortgage Japan K.K.KPMGMIDAS Co. Ltd

Bronze SponsorsA. T. Kearney K.K. Cargill Japan Ltd.Deloitte Touche TohmatsuH&R ConsultantsHyogo Prefecture (Hyogo Prefectural Government Business Support Center, Tokyo)PricewaterhouseCoopers JapanSimpson Thacher & Bartlett LLPState Street JapanTemple University Japan

2

introductionIn his general policy speech to the Diet on January 31, 2003, Japanese Prime Minister Junichiro Koizumi unequivocally welcomed foreign direct investment (FDI) as a way to help revive the country’s economy and achieve sustained growth. In this first-ever reference to FDI in a Prime Minister’s opening annual policy address, he stated:

”Foreign direct investment in Japan will bring new technology and innovative management methods, and will also lead to greater employment opportunities. We will take measures to present Japan as an attractive destination for foreign firms, with the aim of doubling the cumulative amount of investment in five years.”

Doubling the nation’s FDI stock by 2008 is an ambitious target, considering Japan’s low ranking among major economies in inbound FDI levels. According to IMF statistics in the year 2000, Japan’s FDI stock stood at just 1.1 percent of GDP, lagging far behind the UK (32.4 percent), the United States (27.9 percent), and Germany (22.4 percent), among others. UNCTAD’s data show that China’s FDI inflows for 2002 ($52.7 billion) were almost six times as large as Japan’s ($9.3 billion), and were equivalent in size to Japan’s entire cumulative stock of FDI. China’s FDI stock already stood at $448 billion; Japan’s was less that one-seventh as large, at $60 billion.

Japan’s lonely single-digit cumulative FDI figure reflects postwar domestic policies that were designed to promote and develop local companies and industries to meet specific national industrial structure goals. In fact, it was only in 1990 that the government first issued a statement clearly inviting outside investment in Japan—long after formal barriers to foreign investment had been removed in 1980 with the major liberalization of the Foreign Investment and Foreign Exchange Control laws.

The new ”welcome FDI” policy in 1990 gained some momentum when the Japan Investment Council (JIC)—an advisory body to the Cabinet headed by the prime minister—was formed in 1994. The JIC, which includes an expert committee chaired by Keio University Professor

Haruo Shimada, regularly submits reports and recommendations to the Cabinet. These materials provide the base for current government policies welcoming and promoting inbound FDI.

There have been other positive moves made on the FDI front in both the public and private sectors. In September 2002, for example, a group of business leaders and prominent experts who share the view that expanding foreign direct investments will stimulate the economy launched the Invest Japan Forum (IJF). The IJF has since proposed a 12-point program to promote FDI in Japan. In April 2003, the Ministry of Economy, Trade and Industry (METI) announced a project to support regional activities to attract foreign enterprises, selecting five local areas with unique plans to promote FDI to serve as models for other local governments.

Another positive step was the May 2003 establishment of JETRO’s one-stop ”Invest Japan” center offering information and support to potential investors. Prime Minister Koizumi himself attended the opening ceremony to stress its importance. More recently, METI’s July 2003 ”White Paper on International Trade” recommended utilizing FDI as ”an effective method for vitalizing the Japanese economy,” and referred as follows to recommendations made by the JIC’s Expert Committee in April 2003:

”Inward FDI brings with it new capital, human resources, management know-how and technology that are free from existing organizations and practices. Cooperation with foreign enterprises can also enable companies to respond to the challenge of global competition in product development. [Foreign] companies can provide new products and services that do not exist in the domestic market and thus create a new market, enhancing competition and increasing benefits to consumers. In addition, foreign capital can serve as a provider of so-called risk money, which is not averse to taking proper risks. . . . Such new winds may become ’A Key to Revive Japan,’ revitalizing the economy and securing employment.”

foreign direct investment policy in japan: from goals to reality

2

mixed reactionsThe American Chamber of Commerce in Japan (ACCJ) applauds these forceful policy statements and the concrete reforms made in recent years to draw more FDI to Japan. We strongly believe that—as shown in the FDI study and accompanying case studies—foreign investment serves the interests not only of international businesses but also those of Japan’s economy, workers, consumers, and local governments.

That said, we recognize that the Prime Minister’s statement and policies on increasing FDI have drawn mixed reactions.

On the one hand, many mayors and prefectural governors have initiated programs or intensified existing efforts to attract FDI in an attempt to recharge their economies and generate new jobs through fresh investment. Quite a few Diet members endorse Prime Minister Koizumi’s goal as crucial to opening the nation’s economy to greater competition that would boost productivity and employment. Some are even contemplating starting an FDI promotion league within the Diet.

more data and analysis requiredBut in the absence of dependable data and analysis, some critics suggest that more FDI may mean fewer jobs rather than more. They fear that foreign companies acquiring Japanese companies will rationalize operations by cutting staff more than attrition, bankruptcy, or Japanese buyers would. Some simplistically assume that only greenfield investment—creating new manufacturing facilities where none currently exist—brings benefits. In this view, mergers and acquisitions (M&As) are unconnected to follow-on greenfield and expansion investment, and will be dominated by ”vulture” funds seeking to reap big, quick profits by taking advantage of troubled firms.

These downbeat outcomes are not borne out by the actual data on FDI flows. Further, opinion polls indicate that the Japanese public recognizes that, after more than a decade of economic stagnation, policy that is grounded more in emotion than reality cannot restore Japan to growth and sustainable prosperity. At the same time, many Japanese are understandably anxious about how they will be affected individually, how much change is really needed, and what role foreign investment should play. These issues are not unique to Japan; similar concerns were raised in the United States in the 1980s about the waves of Japanese investment during that time. The United States broadly welcomed FDI

from Japan and other countries, and the resulting inflows helped revive the U.S. economy.

The ACCJ fears that such varied reactions—and the lack of analysis about the positive benefits FDI has already brought to Japan—are having a chilling effect on the government’s ability to achieve its 2008 FDI target. Too little is known about FDI in Japan, and too much is incorrectly assumed without regard to the facts. Where is FDI growing, and why? How are the different types of flows interrelated, and what is their impact on the economy, growth, and jobs? If government policies are to be effective, they need to be supported by real-world data. And unless such policies produce concrete results, they will not be enough to counteract Japan’s past reputation as a nation that was for so long effectively closed to foreign investment.

the ACCJ’s FDI task force projectThe ACCJ’s FDI Task Force Project features an economic analysis by two respected academics, Professor Kyoji Fukao of Hitotsubashi University and Tomofumi Amano of Toyo University. This report–entitled the Fukao Report–evaluates the flows, dynamics, and impact of Japan’s FDI, and highlights the sort of policy changes that can realistically increase those flows. Supplementing their work are case studies describing successful investments already made by ACCJ member companies. The latter depict real-life examples of the process by which FDI actually occurs, based on the everyday experience and long-term commitment of typical ACCJ member firms.

By presenting a true and balanced picture of FDI in Japan based on a solid analysis of the data and actual case studies, we hope to dispel fears and misconceptions, and to offer a foundation for designing effective Japanese government policies that will increase FDI and benefit Japan’s economy and society.

the focus of this reportIn this document, based on the Fukao Report’s conclusions, we will examine the effects of foreign investment on the nation’s economy, and Japan’s experiences with FDI to date. We would also like to review some of the myths that surround the topic of FDI here, and suggest how Japan can foster a ”virtuous cycle” of investment by employing effective policies that will correct its historic reputation as a country that is unreceptive or resistant to foreign investment.

Specific recommendations on policy priority areas and policy changes that would significantly improve the attractiveness of the Japanese market to foreign investors—and hence to Japanese domestic investors as well—will be published in a forthcoming document.

the importance of market-based competitionIn previous publications such as The U.S.–Japan Business White Paper and ”The Long Road To Reform,” the ACCJ argued that, in a world of increasingly interdependent global markets, investment does not have a nationality. A healthy global economy that can eradicate poverty and raise standards of living requires the widest possible participation, and a world with some six billion inhabitants needs more than one engine of growth. The world has become too dependent on the economy of one nation: the United States. Without a vibrant and growing Japanese economy—which will remain the second largest in the world for some time to come—we are all vulnerable to severe trauma if the U.S. economy falters.

Regardless of the economic system a country adopts, investment drives economic growth and creates more jobs, and jobs of higher quality. That general understanding, however, does not pinpoint where investments should be made to produce the best results. Nor does it address the question of who should make the related policy and investment decisions, or how those decisions should be made.

The ACCJ has long asserted that the best way to achieve sustained, healthy growth is to foster an open, global economy that promotes market-based competition, meaning an economy characterized by access to reliable information, transparency, accountability in decision-making, and the ability to deploy financial, technological, and human resources to their most productive uses. The vitality of a nation’s economy and market lies in the productive jobs that the nation creates and sustains for its people. The ultimate goal is to increase productivity, enhance return on capital, and create value-added jobs that raise everyone’s standard of living.

Appropriate levels of government regulatory oversight are of course necessary to safeguard public health and safety in any economy. But the broader general rule should focus on and foster an open, competitive marketplace.

Although the subject of this study is how foreign direct investment benefits Japan, it is instructive to look at the experiences of other developed nations, including the United States, where FDI accounts for nearly 12 percent of the country’s output. Such examples indicate that the same conditions that attract foreign investors also help domestic investors and the economy by increasing returns on capital, productivity, incomes, and the number of value-added jobs. At the end of the day, the major growth drivers in very large economies such as Japan and the United States are domestic investors. The additional marginal stimulus from FDI assists in that process, however, smoothing out domestic downturns through international counter-cyclical investments, while delivering the extra benefits of know-how and productivity gains.

The financial ”Big Bang” and other regulatory reforms over the past few years indicate a profound shift in favor of Japan adopting these basic concepts. Japan’s more open and transparent business environment has already attracted substantial investment from abroad and enabled many Japanese corporations to re-examine corporate strategies and adopt new ones to meet the challenges of globalized markets and demographic changes in Japan.

maximizing positive changeWhen working properly, markets function as mechanisms to raise productivity, efficiency, and standards of living. In other words, markets can bring change for the better. But to be effective, they need the support of a complementary social, cultural, and political infrastructure. An effective social safety net, for example, ensures that the health and retirement needs of workers will be met, and that workers can get temporary financial relief when changes in the market cause their income to drop. Workers must have both the financial flexibility and opportunity to acquire new skills to master new technologies or meet changing consumer demand. Otherwise, the labor pool will not be mobile enough to ”retool” itself so that new companies will be able to enter industries and hire new staff as they invest. Likewise, the environment must be protected, food and workplace safety assured, and equitable taxation and income distribution promoted.

Similarly, foreign investment must always respect a country’s social, legal, and cultural systems—or risk failure. Japanese investors in the United States, for example, have adapted to the U.S. legal and social systems. Successful foreign companies operating in Japan are those well

4

5

schooled in such things as Japanese labor rules and consensus-based decision-making. In fact, almost all of their employees and managers are Japanese nationals. Successful future investors will have to follow these examples.

what is ”foreign direct investment”?

The Hierarchy of Investment Value

• Investment is good for an economy

• Direct investment creates jobs, stimulates growth, and fights deflation

• Foreign direct investment creates even more jobs, stimulates greater growth and productivity, and is even more effective at fighting deflation

FDI is direct investment, not portfolio investment.As described in the Fukao Report, direct investment entails the transfer of know-how and management resources to a recipient company from an investor with the ability and the incentive to make such transfers. FDI also tends to be much more committed and long-term capital than portfolio investment because the size of the investment outlays is large and liquidity is limited. This makes it much harder to pull back or retreat from direct investments.

So while all types of investment are generally good for an economy, direct investment offers extra benefits. It creates new employment and increases spending and aggregate demand, which helps fight deflation. It brings new business models, know-how, products, and management methods. In so doing, direct investment boosts productivity and supplies valuable risk capital to the market.

According to a May 2002 JETRO survey, foreign-owned and affiliated firms employ more than one million full-time employees, about 2.3 percent of Japan’s total labor force. Moreover, the employment contribution of foreign firms has been growing rapidly. The Fukao Report noted that employment due to FDI in Japan grew nearly fifty percent from 1997 to 2001. A relatively high proportion of these jobs were high-value-added positions.

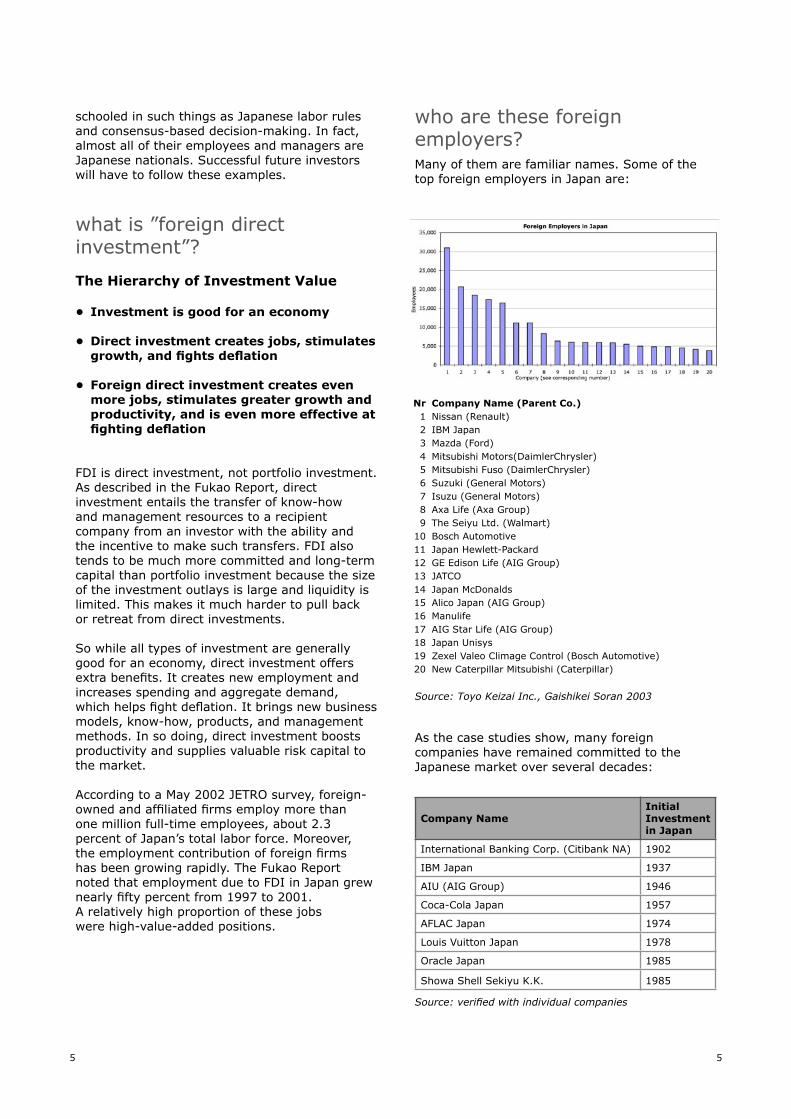

who are these foreign employers?Many of them are familiar names. Some of the top foreign employers in Japan are:

As the case studies show, many foreign companies have remained committed to the Japanese market over several decades:

Nr123456789

1011121314151617181920

Company Name (Parent Co.)Nissan (Renault)IBM JapanMazda (Ford)Mitsubishi Motors(DaimlerChrysler)Mitsubishi Fuso (DaimlerChrysler)Suzuki (General Motors)Isuzu (General Motors)Axa Life (Axa Group)The Seiyu Ltd. (Walmart)Bosch AutomotiveJapan Hewlett-PackardGE Edison Life (AIG Group)JATCOJapan McDonaldsAlico Japan (AIG Group)ManulifeAIG Star Life (AIG Group)Japan UnisysZexel Valeo Climage Control (Bosch Automotive)New Caterpillar Mitsubishi (Caterpillar)

5

Company NameInitial Investment in Japan

International Banking Corp. (Citibank NA) 1902

IBM Japan 1937

AIU (AIG Group) 1946

Coca-Cola Japan 1957

AFLAC Japan 1974

Louis Vuitton Japan 1978

Oracle Japan 1985

Showa Shell Sekiyu K.K. 1985

Source: verified with individual companies

Source: Toyo Keizai Inc., Gaishikei Soran 2003

6

As the Fukao Report points out, foreign direct investors create and establish new businesses. According to JETRO, from 1995 to 2000 (the last year for which data is available), 599 new businesses were established by foreign enterprises. On average, the revenues of foreign enterprises (and, consequently, employment) grow faster than those of domestic firms:

Productivity and jobs both increase after foreign companies enter markets in Japan. Once established, they consistently spend more per employee (including wages), make more capital investments, and are more profitable and efficient. Foreign firms bring direct and spillover benefits such as new know-how, business models, and different techniques that can help address low levels of productivity in all sectors of the economy–particularly in the service sector, where much of Japan’s future growth and job creation is likely to occur. It is no coincidence that Japan’s most productive industries are those that have been exposed to the greatest level of foreign competition. In general, deregulated sectors show higher levels of productivity, productivity improvement, and foreign investment than highly regulated sectors.

Foreign-affiliated companies also pay significant corporate taxes. Some of the largest foreign-affiliate corporate taxpayers are:

japan’s recent FDI experience: more jobs, better productivityAs many economists have noted, lagging productivity growth is one of Japan’s core problems. In its examination of Japan’s FDI flows, the Fukao Report analyzes the many contributions that FDI makes to job creation and improving productivity in Japan. The economic analysis shows that FDI boosts growth in jobs and the economy, not just because of the resources, support, and expansion it contributes, but also because it promotes longer-term productivity and sustainable corporate growth.

the fukao report’s conclusionsThe principal economic conclusions of the Fukao Report are both profound and worrisome:

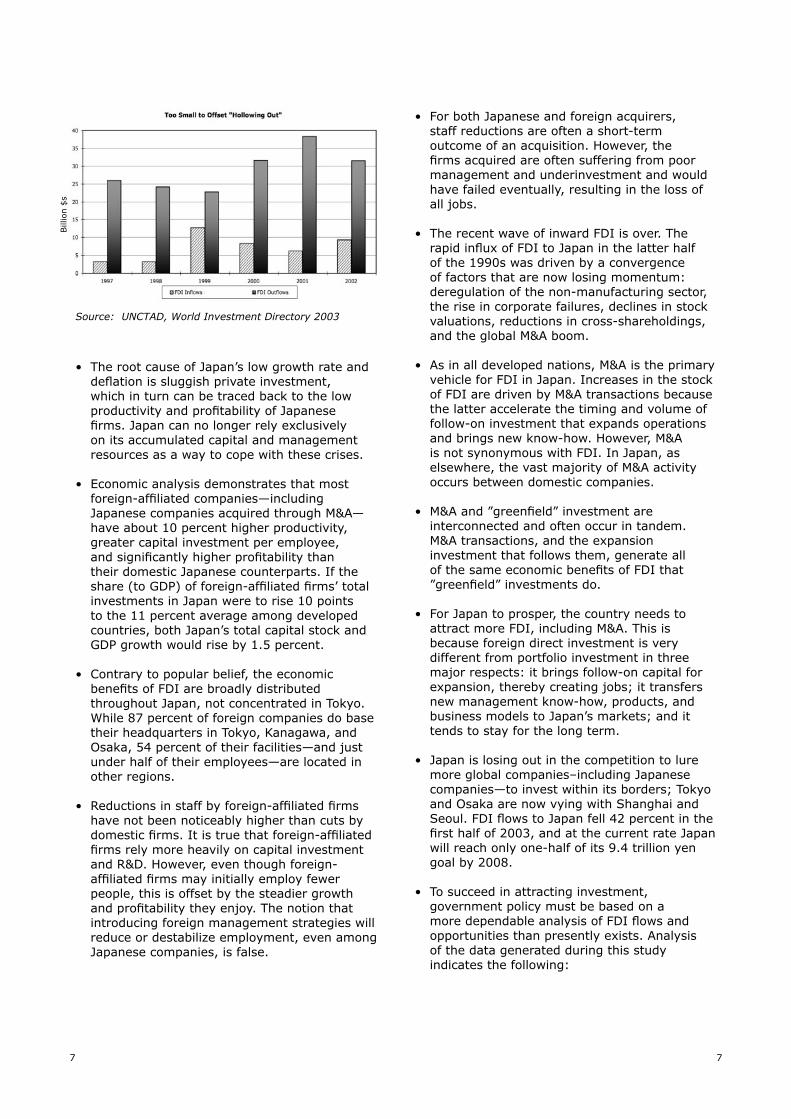

• Japan’s policies and practices have inhibited inward FDI for more than a hundred years. As a percentage of GDP, the country’s inward FDI stock is currently one-eleventh that of the United States and a twenty-eighth that of the U.K. Globalization has also rapidly pushed Japanese capital and management resources overseas as direct investment. Japan’s low FDI inflow level will not offset this ”hollowing out” of the country’s economy.

6

Taxable Income (millions of yen)

Company Name 2001 2000

IBM Japan 125,218 142,052

AFLAC Japan 110,651 95,385

Coca-Cola Japan 86,789 66,200

AIC Corp. 67,696 33,792

Nikko Citigroup 52,164 59,572

Showa Shell Sekiyu K.K. 50,352 18,715

Louis Vuitton Japan 32,405 25,648

Oracle Japan 30,958 18,751

Source: Toyo Keizai Inc., Gaishikei Soran 2003

Source: UNCTAD, World Investment Directory 2003. UNCTAD’s definition of ”foreign company” here is a bit narrower than JETRO’s and the Fukao Report, but the strong upward trend in the employment numbers is exactly the same.

Number of Foreign Enterprises Established

in Japan 1995 - 2000

Year 1995 1996 1997 1998 1999 2000

Number 116 116 92 73 95 107

Total: 599 companiesAve: 100 establishments / year

Source: METI, The 35th Survey of Trends in Business Activities of Foreign Affiliates

7

• The root cause of Japan’s low growth rate and deflation is sluggish private investment, which in turn can be traced back to the low productivity and profitability of Japanese firms. Japan can no longer rely exclusively on its accumulated capital and management resources as a way to cope with these crises.

• Economic analysis demonstrates that most foreign-affiliated companies—including Japanese companies acquired through M&A—have about 10 percent higher productivity, greater capital investment per employee, and significantly higher profitability than their domestic Japanese counterparts. If the share (to GDP) of foreign-affiliated firms’ total investments in Japan were to rise 10 points to the 11 percent average among developed countries, both Japan’s total capital stock and GDP growth would rise by 1.5 percent.

• Contrary to popular belief, the economic benefits of FDI are broadly distributed throughout Japan, not concentrated in Tokyo. While 87 percent of foreign companies do base their headquarters in Tokyo, Kanagawa, and Osaka, 54 percent of their facilities—and just under half of their employees—are located in other regions.

• Reductions in staff by foreign-affiliated firms have not been noticeably higher than cuts by domestic firms. It is true that foreign-affiliated firms rely more heavily on capital investment and R&D. However, even though foreign-affiliated firms may initially employ fewer people, this is offset by the steadier growth and profitability they enjoy. The notion that introducing foreign management strategies will reduce or destabilize employment, even among Japanese companies, is false.

• For both Japanese and foreign acquirers, staff reductions are often a short-term outcome of an acquisition. However, the firms acquired are often suffering from poor management and underinvestment and would have failed eventually, resulting in the loss of all jobs.

• The recent wave of inward FDI is over. The rapid influx of FDI to Japan in the latter half of the 1990s was driven by a convergence of factors that are now losing momentum: deregulation of the non-manufacturing sector, the rise in corporate failures, declines in stock valuations, reductions in cross-shareholdings, and the global M&A boom.

• As in all developed nations, M&A is the primary vehicle for FDI in Japan. Increases in the stock of FDI are driven by M&A transactions because the latter accelerate the timing and volume of follow-on investment that expands operations and brings new know-how. However, M&A is not synonymous with FDI. In Japan, as elsewhere, the vast majority of M&A activity occurs between domestic companies.

• M&A and ”greenfield” investment are interconnected and often occur in tandem. M&A transactions, and the expansion investment that follows them, generate all of the same economic benefits of FDI that ”greenfield” investments do.

• For Japan to prosper, the country needs to attract more FDI, including M&A. This is because foreign direct investment is very different from portfolio investment in three major respects: it brings follow-on capital for expansion, thereby creating jobs; it transfers new management know-how, products, and business models to Japan’s markets; and it tends to stay for the long term.

• Japan is losing out in the competition to lure more global companies–including Japanese companies—to invest within its borders; Tokyo and Osaka are now vying with Shanghai and Seoul. FDI flows to Japan fell 42 percent in the first half of 2003, and at the current rate Japan will reach only one-half of its 9.4 trillion yen goal by 2008.

• To succeed in attracting investment, government policy must be based on a more dependable analysis of FDI flows and opportunities than presently exists. Analysis of the data generated during this study indicates the following:

7

Source: UNCTAD, World Investment Directory 2003

Bill

ion $

s

8

a) Key industries must be deregulated or privatized to remove restrictions on market entry by all firms, whether foreign or domestic. This deregulation will not have sufficient impact unless it includes ”protected” areas such as healthcare services and education, and public corporations that are suitable for privatization.

b) Relevant laws must give more autonomy and resources to local governments so that they can differentiate themselves in front of investors, with incentives and infrastructure.

c) The legal framework must be improved to allow foreign firms to use convenient methods such as stock swaps in M&A transactions.

FDI is one of the keys to revitalizing Japan’s economy, and the success or failure of Japan’s inward direct investment policies will have a significant impact on the personal wealth of the Japanese people.

dispelling myths and fears about FDIPrime Minister Koizumi’s call to make Japan a place where foreigners would like to invest, live, and work signals a welcome change in attitude. But many concrete impediments to increasing Japan’s low cumulative FDI remain: excessive regulation, an overly centralized national policy, limited investment opportunities, restricted and nontransparent capital markets, high costs, and unfriendly legal regimes combine with other aspects of the investment environment to make investment time-consuming, disproportionately expensive, or simply unappealing.

Perhaps most damaging of all, however, are the many misperceptions and fears about how foreign companies and FDI affect Japan. Policy gaps that prevent Japan from attracting (or retaining) more investment with regard to FDI can often be traced to these mistaken beliefs and a lack of real-world exposure to the mechanisms and benefits of foreign investment. Indeed, it was to help dispel these misperceptions and fears that the ACCJ asked Professors Fukao and Amano to analyze the actual data on Japan’s FDI flows.

Below are several of the more pervasive myths about FDI, followed by some of the facts that disprove them.

Myth: Foreign companies cut jobs and do not expand.

Reality: According to JETRO, foreign companies and FDI have added 643,000 new jobs to Japan’s economy since 1993. Moreover, the Fukao Report shows that, over time, foreign companies grow faster, create more new jobs, and have faster job growth than domestic Japanese companies. In some cases the reason foreign companies are more productive than domestic companies is that they do more with fewer employees. Even when foreign companies reduce employment as a way to restore profitability, they usually rebound in subsequent years and enhance revenue and employment as a result.

Myth: FDI is a one-time event, and the investment is easily pulled back.

Reality: This pattern rarely occurs in real business. The FDI Task Force’s case studies and numerous other examples show that most FDI is an ongoing and committed process. Companies with no long-term commitment and no staying power seldom invest in the first place. Of all types of investment, including individual and institutional portfolio investment, direct investment is the least liquid and the hardest to pull out. Direct investment is committed investment.

Myth: Most FDI only benefits the Kanto and Kansai regions, not Japan’s other regions and local governments.

Reality: This is simply not true. Many corporate headquarters are indeed located in Tokyo, Kanagawa, and Osaka, but the data and analysis in the Fukao Report show that in terms of impact on employment, the benefits of FDI penetrate deeply and relatively evenly into Japan’s regions.

Source: Research Institute of Economy, Trade, and Industry, Research on the Impact of Quantitative Change in Foreign Direct Investment in Japan on Japan’s Economy and Employment, 2000. The primary source material is micro data from the 1996 Establishment and Enterprise Census.

This pattern does not mean, however, that opportunities for greenfield investments in Japan will not arise. The United States, which has high wages, has received significant amounts of greenfield FDI. The state of Illinois, for example, hosts 6,447 foreign firms that employ approximately 340,000 people. In the 1990s Indiana became the national leader in steel production, due largely to the investment by steel producers from around the world. In Indiana, over 40,000 residents currently work at Japanese-affiliated manufacturing plants, up from just over 7,000 in 1990.

Myth: Greenfield investment is preferable to M&A investment.

Reality: In fact, as our case studies show, the two are deeply interconnected and therefore hard to separate. Successful greenfield investment leads to M&A, and vice versa; both lead to follow-on expansion investment that creates new growth and new jobs. Focusing solely on one form would result in a less attractive investment environment and much less FDI overall. Promoting both is the only sensible strategy.

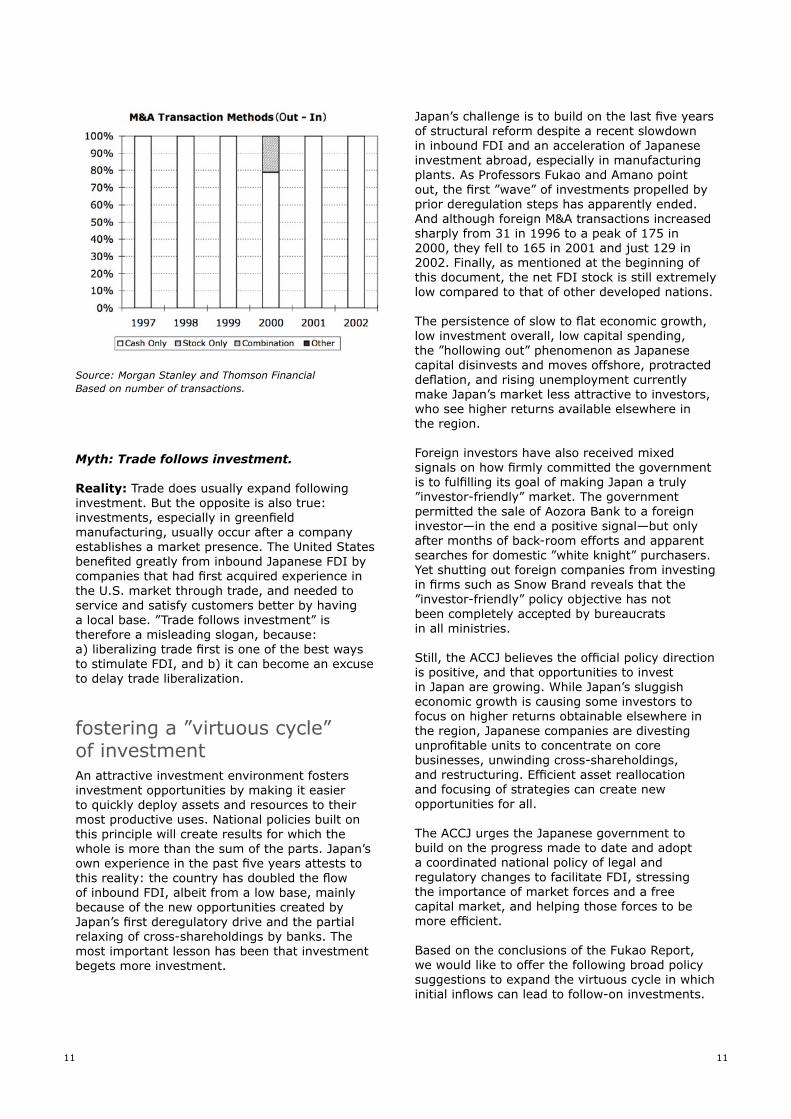

In developing countries, where labor costs are low, most investment is in manufacturing facilities to produce exports to richer countries. In most developed countries, however, some 80 percent of foreign investment occurs through M&A activities. Japan is no exception: the overwhelming portion of new investment since 1995 has been through M&As, particularly when the follow-on investment that occurs is considered. This will continue to be the case in Japan as well as globally. Investors like to acquire a larger ”base” that will generate larger investment opportunities and then expand faster and more efficiently. The quicker expansion and the new ownership of assets M&As cause can also help resolve the debt crisis.

Myth: Foreign firms just buy companies to suck out the value.

Reality: Even if an investor were tempted to do this, justifying acquisitions on such a basis would be extremely difficult. Foreign companies almost always need to have a growth strategy in mind so they can make profitability projections that justify the price paid for an acquisition. Most foreign M&A deals in Japan result in a turnaround of the company and faster subsequent growth in revenues, earnings, and jobs. To accomplish this, the foreign acquirer usually invests more funds after the initial deal. In fact, this has often been utterly essential because, on average, most companies acquired by foreign firms have been much more distressed than those bought by domestic acquirers.

Myth: Most FDI is short-term private equity (so-called vulture or turnaround funds).

Reality: First, most FDI comes from strategic investors and operating companies. Less than 5-10 percent has been investment by private

Source: UNCTAD, World Investment Report 2003

Data Source: Development Bank of Japan

Data Source: Development Bank of Japan

Years preceding/following transaction

-7 -6 -5 -4 -3 -2 -1 0 +1 +2 +3 +4 +5

-8 -7 -6 -5 -4 -3 -2 -1 0 +1 +2

Years preceding/following transaction

competitiveness, corporate governance practices, stock market returns, and the efficiency of asset allocation and reallocation. The analysis by Professors Fukao and Amano shows that M&A, asset reallocation, and ownership transfer transactions of any type (foreign or domestic) improve Japan’s economy in these ways.

The Fukao Report demonstrates that these benefits are even greater in the case of M&As by foreign companies. But M&A opportunities are much more limited for foreign firms. This is not just because of misconceptions and cross-shareholdings. It is also because corporate and tax laws in Japan still do not permit foreign companies to use most non-cash transaction methods in pursuing M&As. In contrast, domestic companies are free to utilize a variety of ”non-cash” transaction structures (such as stock swaps and mergers), and are actively taking advantage of that extra flexibility. This explains a significant portion of the recent boom in domestic M&A activity.

equity financial investors, sometimes referred to pejoratively and indiscriminately as ”vulture funds.” In actual fact, such funds bring in much-needed risk capital that provides support and growth opportunities for companies that are unable to find other backers. In fact, a large portion of money from such financial investors is not foreign money at all, but rather private equity investments by Japanese funds supported by domestic financial institutions. Moreover, a portion of the funds invested end up with Japanese sellers or lenders, who may then redeploy the funds elsewhere.

Analysis shows that all types of FDI increase productivity and efficiency of asset reallocation. Even when FDI is in the form of asset or debt purchases by financial investors for remarketing over a few years, these transactions get assets back into productive use, removing drags on economic growth. The ACCJ believes that, if anything, Japan needs much more private equity investment—both domestic and foreign money–and a more vibrant capital market.

*Values are based on public announcements and disclosures.*The ”PE % of Total M&A” is the proportion of total M&A transaction value comprised by both domestic and foreign PE fund investments.*The ”Foreign PE % of Foreign M&A” is calculated against total foreign M&A transaction value.*Source: PE and M&A transaction values, including foreign capital, were acquired from Thomson SDC Database or Recof Data.

Myth: Foreign companies make most M&A deals; Japanese companies do not make acquisitions.

Reality: Domestic acquirers actually make up the majority of M&A transactions in Japan, whether measured by volume or number. The dramatic increase in M&A transactions over the past fifteen years, led by domestic companies, is a positive development that will improve productivity,

Data Source: Recof M&A Databook 1988 - 2002

Source: Morgan Stanley and Thomson FinancialBased on number of transactions.

10

11

Myth: Trade follows investment.

Reality: Trade does usually expand following investment. But the opposite is also true: investments, especially in greenfield manufacturing, usually occur after a company establishes a market presence. The United States benefited greatly from inbound Japanese FDI by companies that had first acquired experience in the U.S. market through trade, and needed to service and satisfy customers better by having a local base. ”Trade follows investment” is therefore a misleading slogan, because: a) liberalizing trade first is one of the best ways to stimulate FDI, and b) it can become an excuse to delay trade liberalization.

fostering a ”virtuous cycle” of investmentAn attractive investment environment fosters investment opportunities by making it easier to quickly deploy assets and resources to their most productive uses. National policies built on this principle will create results for which the whole is more than the sum of the parts. Japan’s own experience in the past five years attests to this reality: the country has doubled the flow of inbound FDI, albeit from a low base, mainly because of the new opportunities created by Japan’s first deregulatory drive and the partial relaxing of cross-shareholdings by banks. The most important lesson has been that investment begets more investment.

Japan’s challenge is to build on the last five years of structural reform despite a recent slowdown in inbound FDI and an acceleration of Japanese investment abroad, especially in manufacturing plants. As Professors Fukao and Amano point out, the first ”wave” of investments propelled by prior deregulation steps has apparently ended. And although foreign M&A transactions increased sharply from 31 in 1996 to a peak of 175 in 2000, they fell to 165 in 2001 and just 129 in 2002. Finally, as mentioned at the beginning of this document, the net FDI stock is still extremely low compared to that of other developed nations.

The persistence of slow to flat economic growth, low investment overall, low capital spending, the ”hollowing out” phenomenon as Japanese capital disinvests and moves offshore, protracted deflation, and rising unemployment currently make Japan’s market less attractive to investors, who see higher returns available elsewhere in the region.

Foreign investors have also received mixed signals on how firmly committed the government is to fulfilling its goal of making Japan a truly ”investor-friendly” market. The government permitted the sale of Aozora Bank to a foreign investor—in the end a positive signal—but only after months of back-room efforts and apparent searches for domestic ”white knight” purchasers. Yet shutting out foreign companies from investing in firms such as Snow Brand reveals that the ”investor-friendly” policy objective has not been completely accepted by bureaucrats in all ministries.

Still, the ACCJ believes the official policy direction is positive, and that opportunities to invest in Japan are growing. While Japan’s sluggish economic growth is causing some investors to focus on higher returns obtainable elsewhere in the region, Japanese companies are divesting unprofitable units to concentrate on core businesses, unwinding cross-shareholdings, and restructuring. Efficient asset reallocation and focusing of strategies can create new opportunities for all.

The ACCJ urges the Japanese government to build on the progress made to date and adopt a coordinated national policy of legal and regulatory changes to facilitate FDI, stressing the importance of market forces and a free capital market, and helping those forces to be more efficient.

Based on the conclusions of the Fukao Report, we would like to offer the following broad policy suggestions to expand the virtuous cycle in which initial inflows can lead to follow-on investments.

Source: Morgan Stanley and Thomson FinancialBased on number of transactions.

11

12

We believe that such a virtuous cycle can strengthen Japan’s reputation as a market for investment and spur another doubling of FDI over the next five years:

• Prime Minister Koizumi, ministry officials, and other political leaders must continue to make forthright public statements both at home and abroad in support of foreign investment, and follow up with clear policies and concrete actions. Public statements should be frequent, and should focus on dispelling the many misconceptions about FDI that exist in Japan.

• Government bureaucracies should be made more accountable to advancing policy objectives for increasing FDI. A good start would be to educate the Japanese public on how the changes that make Japan an attractive place for foreign investors will not only help create jobs and sustainable growth, but will also help Japanese companies and industry to become productive so that the economy recovers.

• A campaign of advertising and events to increase interest, receptivity, and understanding about FDI and its benefits, dispel misconceptions, and to reach out to foreign investors to understand what concerns and obstacles they face.

• Lead a ”paradigm shift” toward greater reliance on market principles that encourage investment: free capital markets; transactions that are ”free” in principle with only a few exceptions that are clear and very limited; healthy corporate governance, transparency, and accountability; and regulatory and administrative simplicity. We suggest a Cabinet-level advisory group that would focus on recommending precise reforms that will reinforce healthy and competitive market principles.

• Accelerate deregulation and privatization. Unlock investment opportunities for both foreign and domestic firms in areas such as medical care, education, retailing, utilities, agriculture, professional services sectors, postal and delivery services, financial advisory and asset management sectors, and outsourcing of public services. Removing government institutions from a major role in the lending business would also be a key action.

• Make it easier for foreign investors to execute ownership transfers and M&A transactions. Change laws so that techniques such as cross-border stock swaps with tax deferral and ”cash

mergers” can be utilized. Educate the public and corporate managers about the benefits of timely M&A as a technique to help companies survive and maintain employment, and to ensure their sustainable long-term growth by securing access to new resources and know-how.

• Embark on a crash program to build a social safety net that improves labor mobility, facilitating faster entry to new industries and softening the impact of exits by inefficient competitors. Assist displaced workers financially and by training or subsidizing them to acquire value-added skills. Expand 401K pension benefit limits and features to enhance both attractiveness now and ”portability” over time.

• Strengthen and support the autonomy and authority of local governments to offer tax and other incentives so they can differentiate themselves and attract more FDI. Focus JETRO and key agencies such as METI on assisting local governments so that the latter can more actively seek investors for specific companies and situations in their jurisdictions, and can ”target” specific companies to urge them to make ”special zone” applications.

• Encourage and assist regional governments to design investment promotion programs that produce concrete results. It is particularly important that local governments:

a) Consult with foreign companies and the groups that represent them during the initial design phase to obtain detailed feedback on planned promotions

b) Target new investors to the region, and reward companies for growing their presence rather than focusing support and tax/subsidy benefits on companies already set up in the jurisdiction but which are not making new investments

c) Promote a mobile labor market by supporting training (especially, English-language training), and provide subsidies or tax benefits directly to individuals rather than to the companies that employ them

• Implement necessary policies and legal framework changes quickly, thereby creating early results and investment ”success stories.” Policies and changes should be based on dependable analysis of actual FDI flows, their drivers, and their dynamics.

12

13

In a follow-up report to be released in the coming months, the ACCJ will offer specific and concrete recommendations on the policies that can accomplish this, addressing the following issues:

• Deregulation and facilitating entrepreneurship

• Labor mobility and social safety net upgrades

• Accelerating the clearance of nonperforming loans

• Stock swaps and triangular mergers

• Cash mergers

• Corporate governance and transparency

• Strengthening education and medical services

conclusionJapan needs even more direct investment, and needs it now. Economic data clearly shows that foreign direct investment brings extra benefits to Japan, in terms of productivity, growth, and jobs. In fact, the analysis reveals that FDI is one of the most important keys to revitalizing Japan’s economy.

Japan has taken the first steps toward welcoming foreign investment, and the response by international investors has been very positive. However, the factors that drove the recent wave of FDI have ended. In the years to come, if Japan is to attract its fair share of FDI from the competitive global marketplace, the country will need to further accelerate reform and deregulation, improve laws that affect investment, and simplify procedures. It will need to do this with greater vigor, speed, and determination than in the past.

13