Commodity Specific Food Safety Guidelines for the Fresh Tomato ...

Fresh Tomato Trends in the N.

American Market

DR. ROBERTA COOK Dept. of Ag and Resource Economics

University of California Davis for

America Trades Produce Conference Tubac, AZ

March 13, 2014

Agenda • Overview of US fresh tomato market supply

and consumption • Retail market shares by key tomato type • Historical trends • Update on US fresh tomato imports • Canadian greenhouse tomato trends • Protected culture in Mexico changes market

dynamics

Important Considerations • Comparing trends DOES NOT necessarily imply

causality. • Concept of with and without analysis. • Too soon to draw conclusions about the impact

of the higher prices under the new suspension agreement (in effect since March 2013)

• Restricting supply can lead to higher prices (due to relatively inelastic demand) but these may be difficult to sustain without acreage controls due to “supply response” dynamics; barriers to entry play a role

0

1000

2000

3000

4000

5000

6000

7000

1990

19

91

1992

19

93

1994

19

95

1996

19

97

1998

19

99

2000

20

01

2002

20

03

2004

20

05

2006

20

07

2008

20

09

2010

20

11

2012

20

13P

U.S. Fresh Tomatoes: Production, Consumption, Imports, and Exports, 1990-2013p

million pounds

Consumption

Production

Imports Exports

Sources: USDA/ERS, Vegetables and Pulses Yearbook Data May 31, 2013 and unpublished update for 2013. (includes estimate of US GH production)

Pounds per capita

P=Preliminary Sources: USDA/ERS, Vegetables and Pulses Yearbook Data May 31, 2013 and unpublished update for 2013.

0

5

10

15

20

25

US Per Capita Utilization/Consumption of Fresh Tomatoes (1985-2013P)

US Retail Fresh Tomato Trends

• Remember – scanner data excludes foodservice tomatoes!

• Foodservice is likely over half of tomato volume sold in the USA and relies on mature green tomatoes. Foodservice sales also took a hit during the economic downturn.

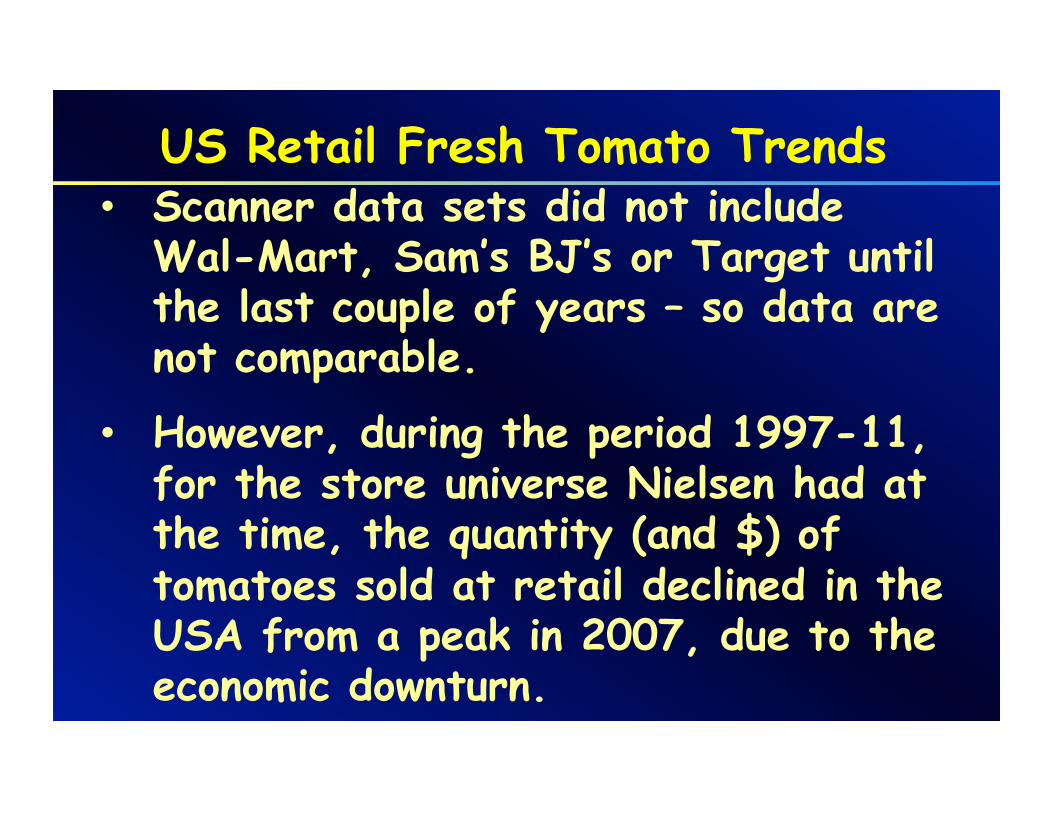

US Retail Fresh Tomato Trends • Scanner data sets did not include

Wal-Mart, Sam’s BJ’s or Target until the last couple of years – so data are not comparable.

• However, during the period 1997-11, for the store universe Nielsen had at the time, the quantity (and $) of tomatoes sold at retail declined in the USA from a peak in 2007, due to the economic downturn.

US Fresh Tomato Retail Market Shares (in Lbs) by Key Type, 2013

Source: FreshLook Marketing

Roma 27%

TOV 22% Grape

14%

Vine Ripe 12%

GH 9%

[CATEGORY NAME] [VALUE]

[CATEGORY NAME] [VALUE]

[CATEGORY NAME] [VALUE]

US Fresh Tomato Retail Market Shares (in $) by Key Type, 2013

Source: FreshLook Marketing

TOV 23%

Grape 22%

Roma 16%

Vine Ripe 11%

Mini, excl grape 10%

[CATEGORY NAME] [VALUE]

[CATEGORY NAME] [VALUE]

[CATEGORY NAME] [VALUE]

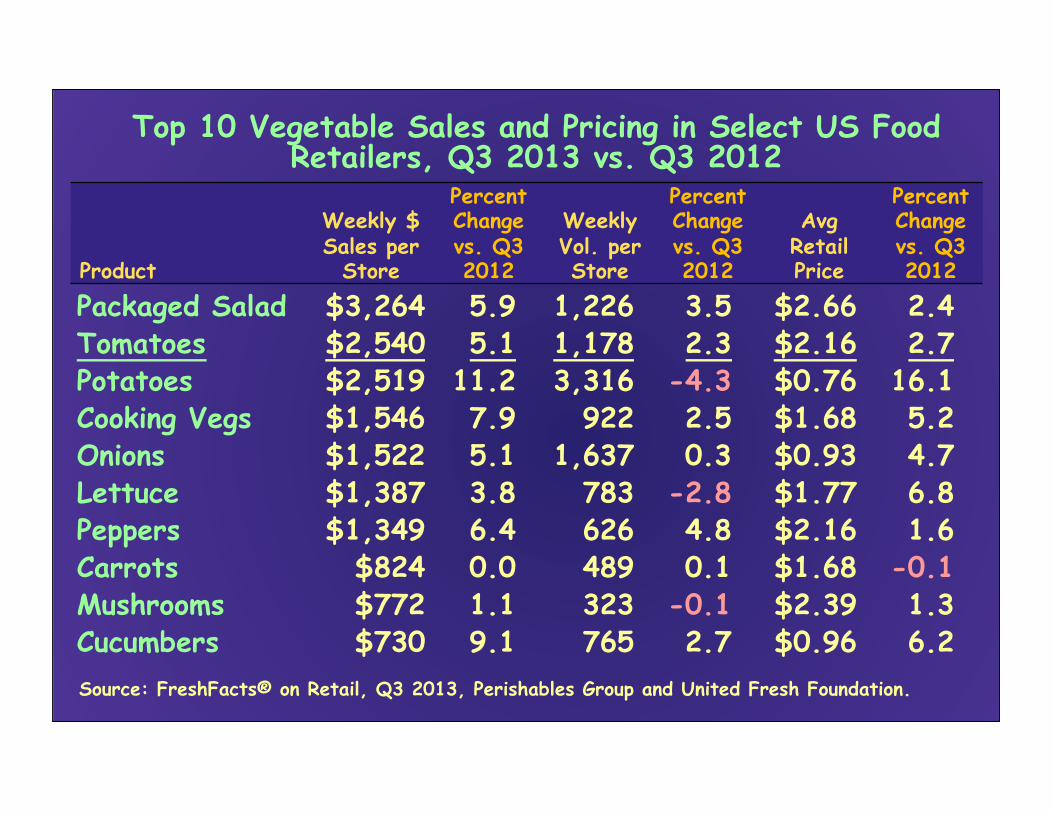

Top 10 Vegetable Sales and Pricing in Select US Food Retailers, Q3 2013 vs. Q3 2012

Product

Weekly $ Sales per

Store

Percent Change vs. Q3 2012

Weekly Vol. per Store

Percent Change vs. Q3 2012

Avg

Retail Price

Percent Change vs. Q3 2012

Packaged Salad $3,264 5.9 1,226 3.5 $2.66 2.4 Tomatoes $2,540 5.1 1,178 2.3 $2.16 2.7 Potatoes $2,519 11.2 3,316 -4.3 $0.76 16.1 Cooking Vegs $1,546 7.9 922 2.5 $1.68 5.2 Onions $1,522 5.1 1,637 0.3 $0.93 4.7 Lettuce $1,387 3.8 783 -2.8 $1.77 6.8 Peppers $1,349 6.4 626 4.8 $2.16 1.6 Carrots $824 0.0 489 0.1 $1.68 -0.1 Mushrooms $772 1.1 323 -0.1 $2.39 1.3 Cucumbers $730 9.1 765 2.7 $0.96 6.2 Source: FreshFacts® on Retail, Q3 2013, Perishables Group and United Fresh Foundation.

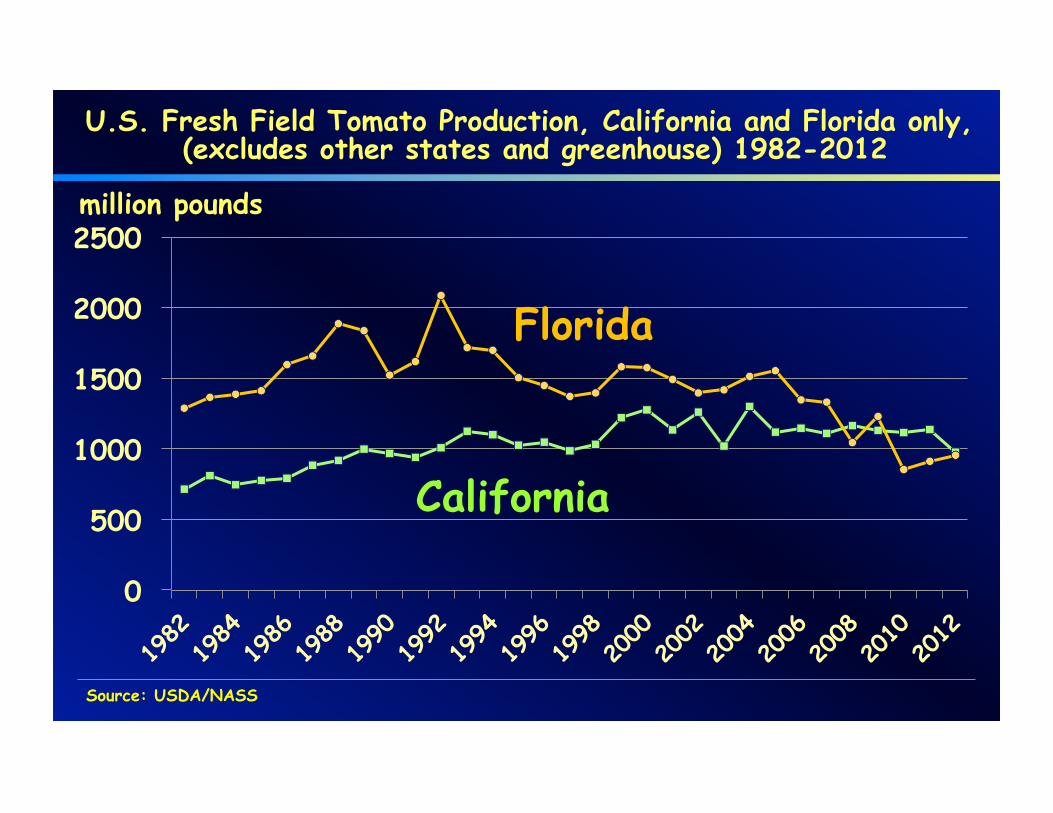

Historical Perspective

0

500

1000

1500

2000

2500

U.S. Fresh Field Tomato Production, California and Florida only, (excludes other states and greenhouse) 1982-2012

million pounds

Florida

California

Source: USDA/NASS

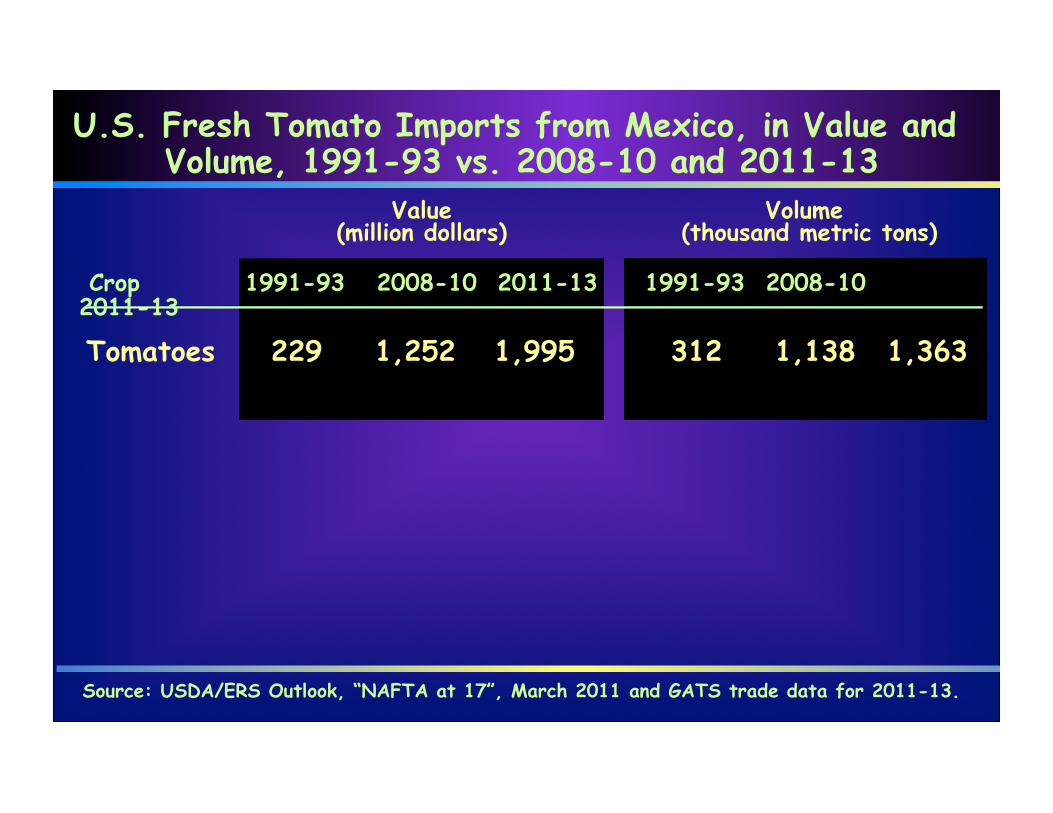

Source: USDA/ERS Outlook, “NAFTA at 17”, March 2011 and GATS trade data for 2011-13.

Tomatoes 229 1,252 1,995 312 1,138 1,363

U.S. Fresh Tomato Imports from Mexico, in Value and Volume, 1991-93 vs. 2008-10 and 2011-13

Crop 1991-93 2008-10 2011-13 1991-93 2008-10 2011-13

Volume (thousand metric tons)

Value (million dollars)

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

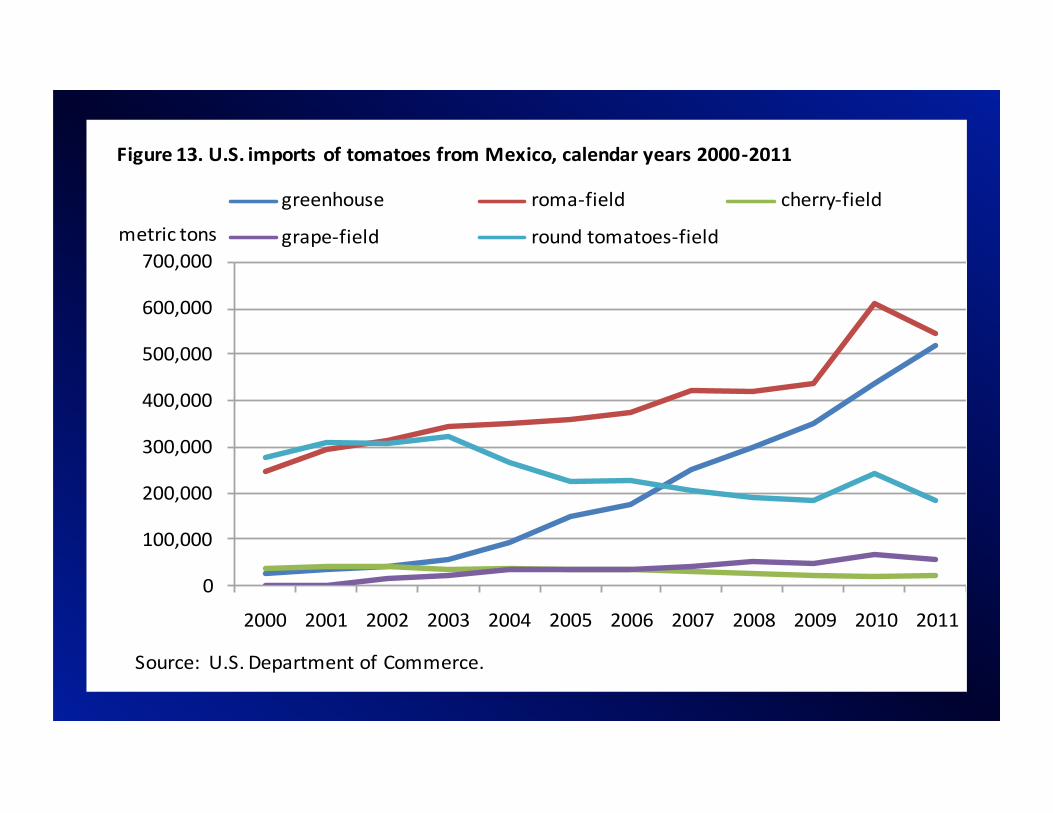

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Figure 13. U.S. imports of tomatoes from Mexico, calendar years 2000-‐2011

greenhouse roma-‐field cherry-‐field

grape-‐field round tomatoes-‐fieldmetric tons

Source: U.S. Department of Commerce.

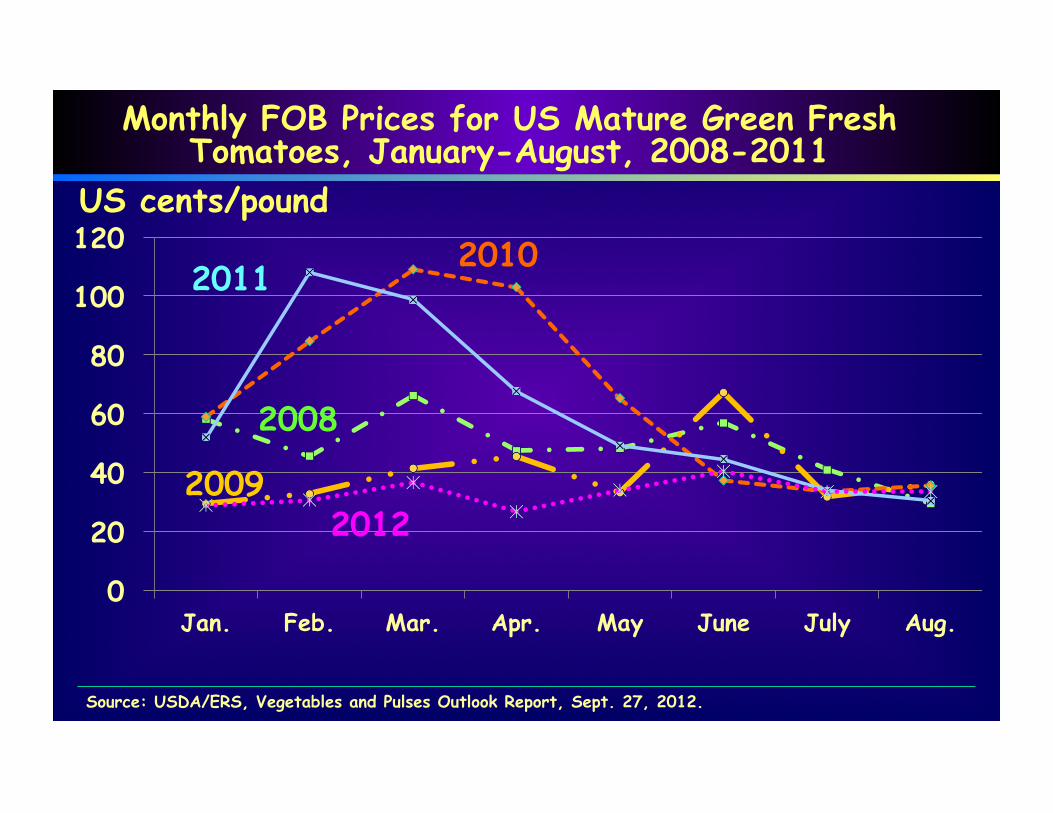

0

20

40

60

80

100

120

Jan. Feb. Mar. Apr. May June July Aug.

2012

Monthly FOB Prices for US Mature Green Fresh Tomatoes, January-August, 2008-2011

US cents/pound

2011

2008

2009

2010

Source: USDA/ERS, Vegetables and Pulses Outlook Report, Sept. 27, 2012.

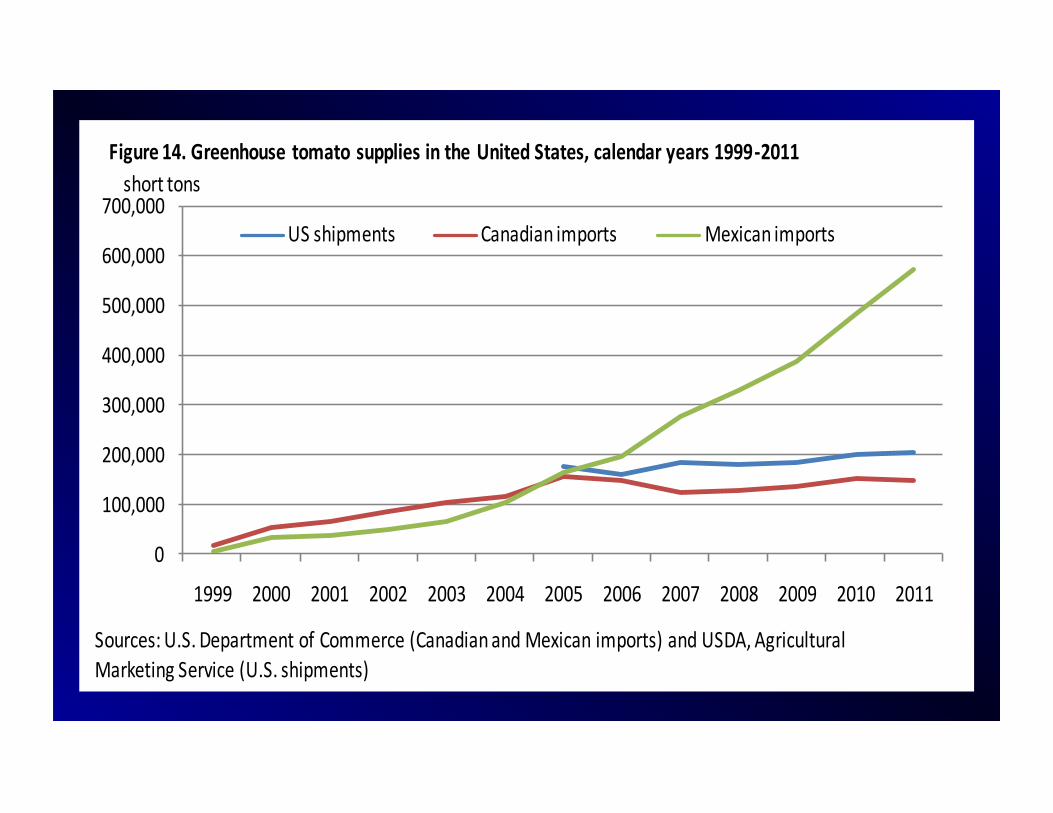

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Figure 14. Greenhouse tomato supplies in the United States, calendar years 1999-‐2011

US shipments Canadian imports Mexican imports

short tons

Sources: U.S. Department of Commerce (Canadian and Mexican imports) and USDA, Agricultural Marketing Service (U.S. shipments)

Update on US Fresh Greenhouse Industry

Over 1100 acres in 2013 among the main players, Eurofresh Farms, Village Farms, Windset Farms, Houweling’s, and Backyard Farms. Part of capacity not utilized in 2013 (Eurofresh, Village, Backyard Farms). Latter two will be back up but Eurofresh will be down more in 2014. Some growth in controlled environment among major players, and small urban players – “local.”

Update on US Fresh Tomato Imports

US Fresh Tomato Imports, All Types, by Key Country, 2009-2013, million pounds

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

Mexico Canada Other Countries Total

Millions

2009 2010 2011 2012 2013

Sources: US Department of Commerce. US Census Bureau, Foreign Trade Statistics and ERS calculations.

US Fresh Tomato Imports, All Types, by Key Country, 2008-2013, million dollars

0

500

1,000

1,500

2,000

2,500

Mexico Canada Other countries Total

Millions

2008 2009 2010 2011 2012 2013

Sources: US Department of Commerce.

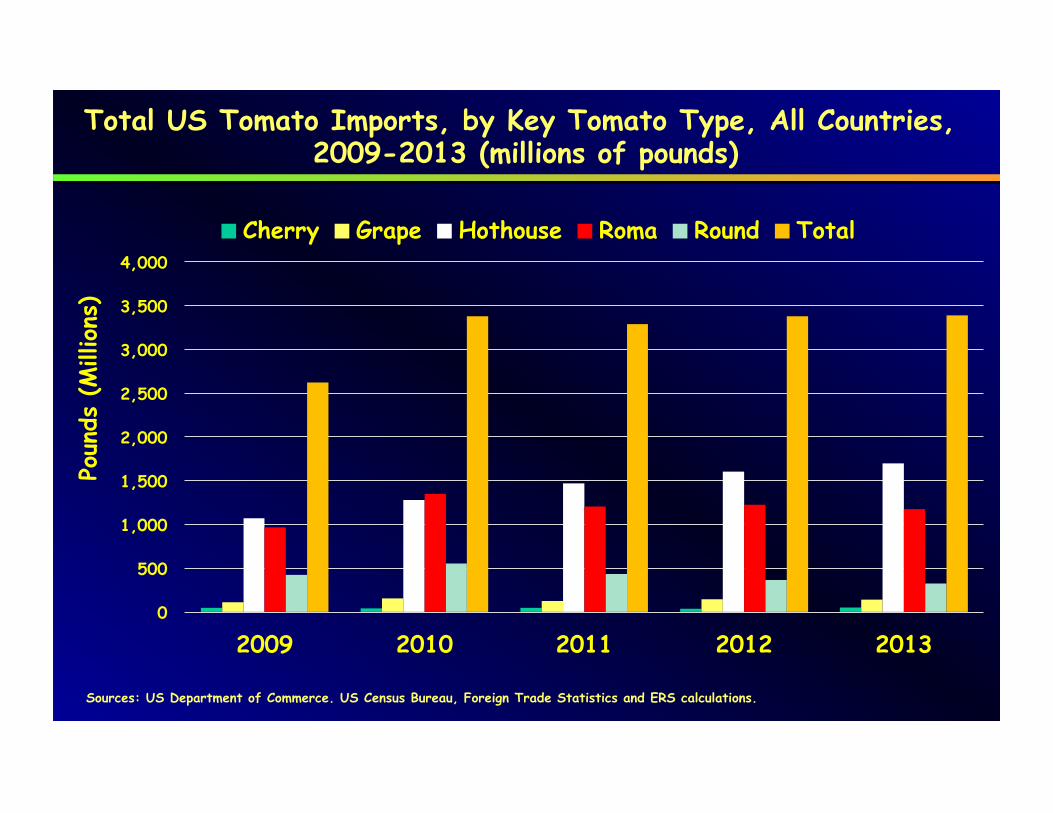

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

2009 2010 2011 2012 2013

Poun

ds (M

illions

)

Cherry Grape Hothouse Roma Round Total

Sources: US Department of Commerce. US Census Bureau, Foreign Trade Statistics and ERS calculations.

Total US Tomato Imports, by Key Tomato Type, All Countries, 2009-2013 (millions of pounds)

0

500

1,000

1,500

2,000

2,500

2008 2009 2010 2011 2012 2013

US

Dollars

(M

illions

)

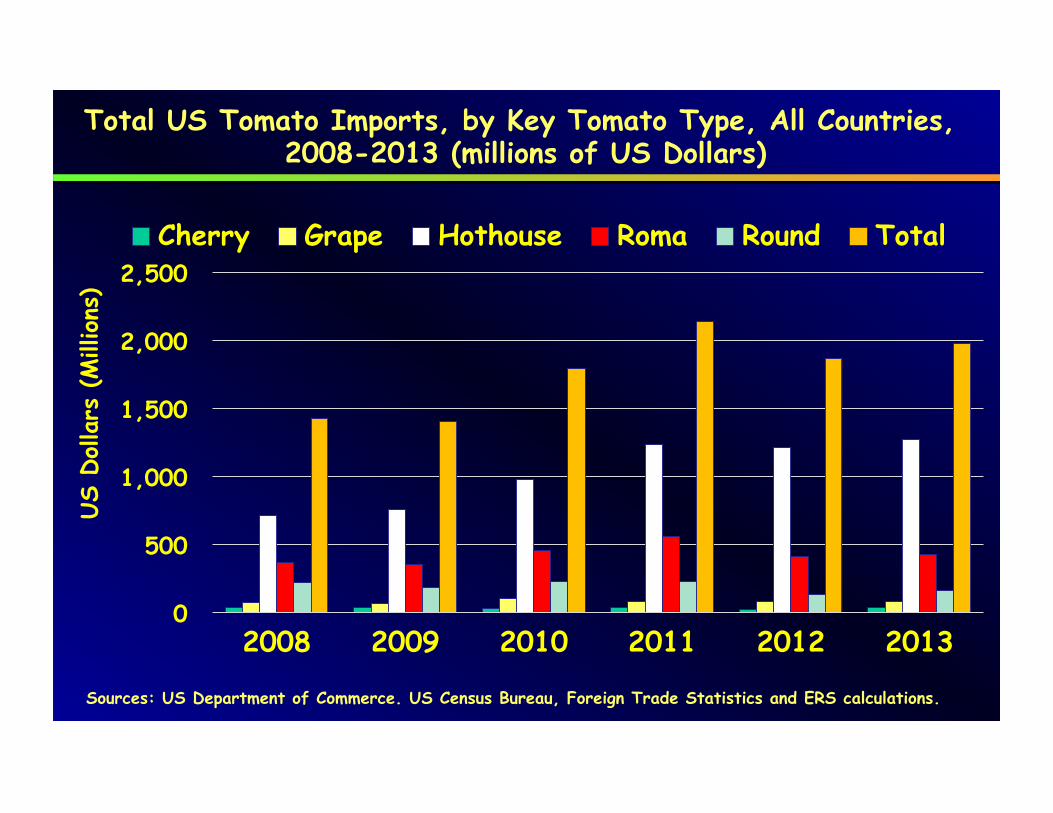

Cherry Grape Hothouse Roma Round Total

Sources: US Department of Commerce. US Census Bureau, Foreign Trade Statistics and ERS calculations.

Total US Tomato Imports, by Key Tomato Type, All Countries, 2008-2013 (millions of US Dollars)

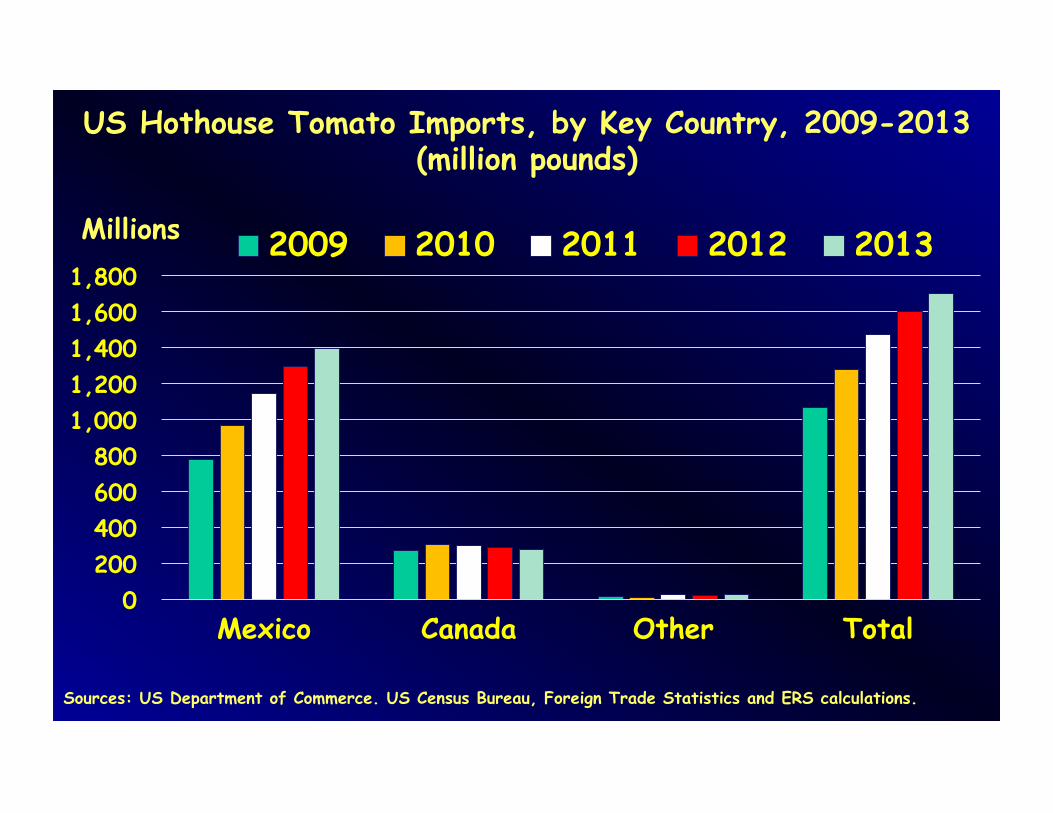

US Hothouse Tomato Imports, by Key Country, 2009-2013 (million pounds)

0 200 400 600 800

1,000 1,200 1,400 1,600 1,800

Mexico Canada Other Total

Millions 2009 2010 2011 2012 2013

Sources: US Department of Commerce. US Census Bureau, Foreign Trade Statistics and ERS calculations.

0

100

200

300

400

500

600

Mexico Canada Other Total

Millions

2009 2010 2011 2012 2013

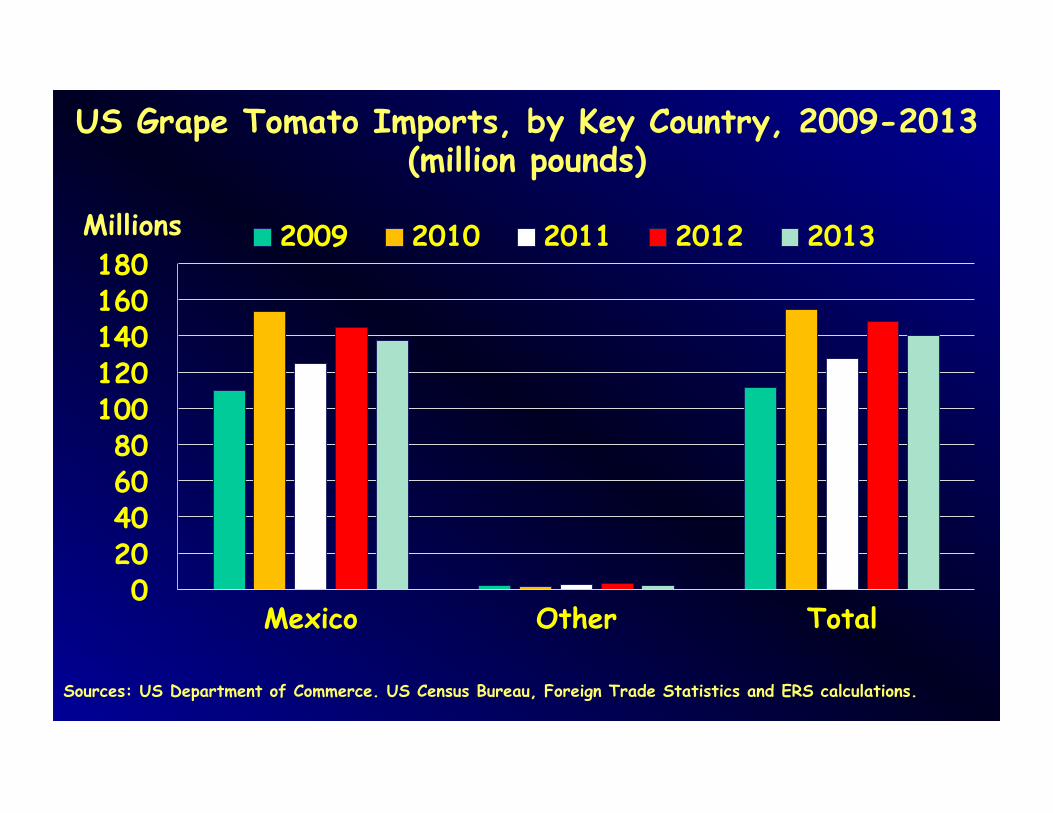

Sources: US Department of Commerce. US Census Bureau, Foreign Trade Statistics and ERS calculations.

US Round Tomato Imports, by Key Country, 2009-2013 (million pounds)

Import volume by country, Roma Tomatoes 2009-2013 (million pounds)

0

200

400

600

800

1,000

1,200

1,400

1,600

Mexico Other Countries Total

Millions 2009 2010 2011 2012 2013

Sources: US Department of Commerce. US Census Bureau, Foreign Trade Statistics and ERS calculations.

0

10

20

30

40

50

60

Mexico Canada Other Total

Millions 2009 2010 2011 2012 2013

Sources: US Department of Commerce. US Census Bureau, Foreign Trade Statistics and ERS calculations.

US Cherry Tomato Imports, by Key Country, 2009-2013 million pounds

0 20 40 60 80

100 120 140 160 180

Mexico Other Total

Millions 2009 2010 2011 2012 2013

Sources: US Department of Commerce. US Census Bureau, Foreign Trade Statistics and ERS calculations.

US Grape Tomato Imports, by Key Country, 2009-2013 (million pounds)

Average annual import unit value by fresh tomato variety, 2009-2013, US Dollars per pound

0.00

0.20

0.40

0.60

0.80

1.00

Cherry Grape Hothouse Roma Round

2009 2010 2011 2012 2013

Sources: US Department of Commerce. US Census Bureau, Foreign Trade Statistics and ERS calculations.

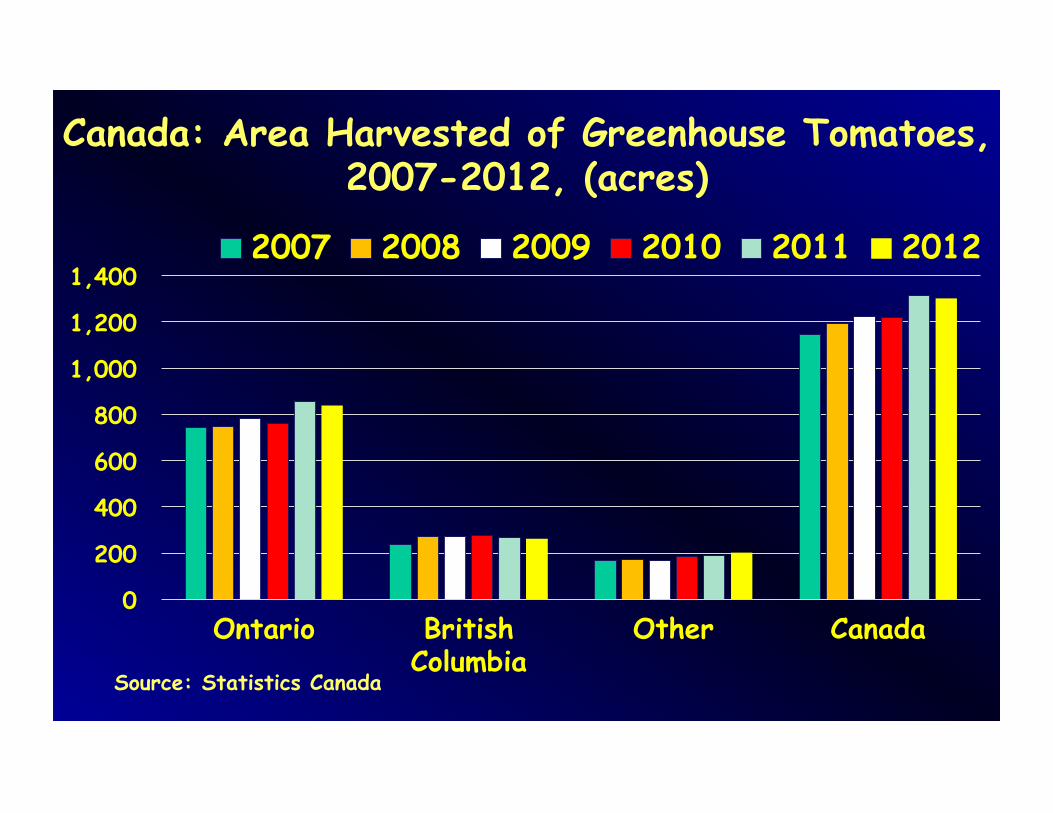

Canada: Greenhouse Tomato Trends • Interviews indicate that acreage in BC is

stable while it grows in Ontario. • In Jan. 2011 according to the OGVG, there

were 404 acres of clusters/specialties in Ont. plus 378 acres of beefs (total 782), vs in Jan. 2014 there were 543 plus 378 acres, respectively, (total 920). Specialties! And over half is high tech glass.

• Following trends are from Statistics Canada, 2013 data not yet available.

Canada: Area Harvested of Greenhouse Tomatoes, 2007-2012, (acres)

0

200

400

600

800

1,000

1,200

1,400

Ontario British Columbia

Other Canada

2007 2008 2009 2010 2011 2012

Source: Statistics Canada

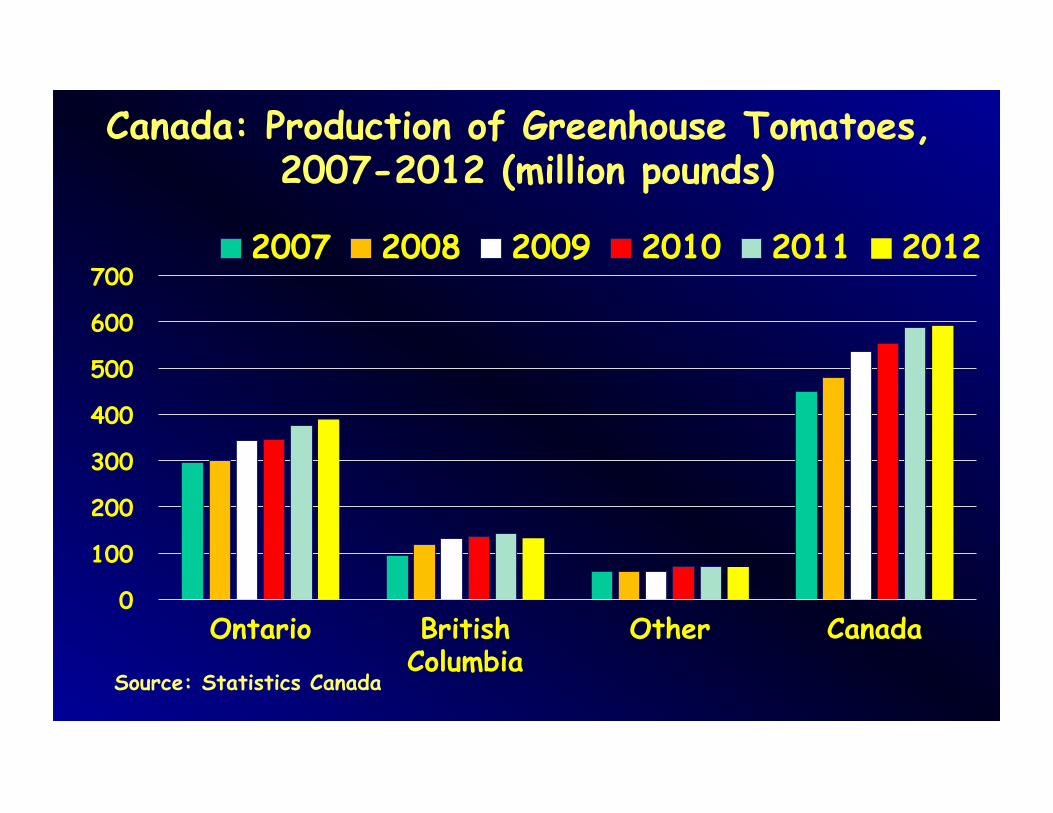

Canada: Production of Greenhouse Tomatoes, 2007-2012 (million pounds)

0

100

200

300

400

500

600

700

Ontario British Columbia

Other Canada

2007 2008 2009 2010 2011 2012

Source: Statistics Canada

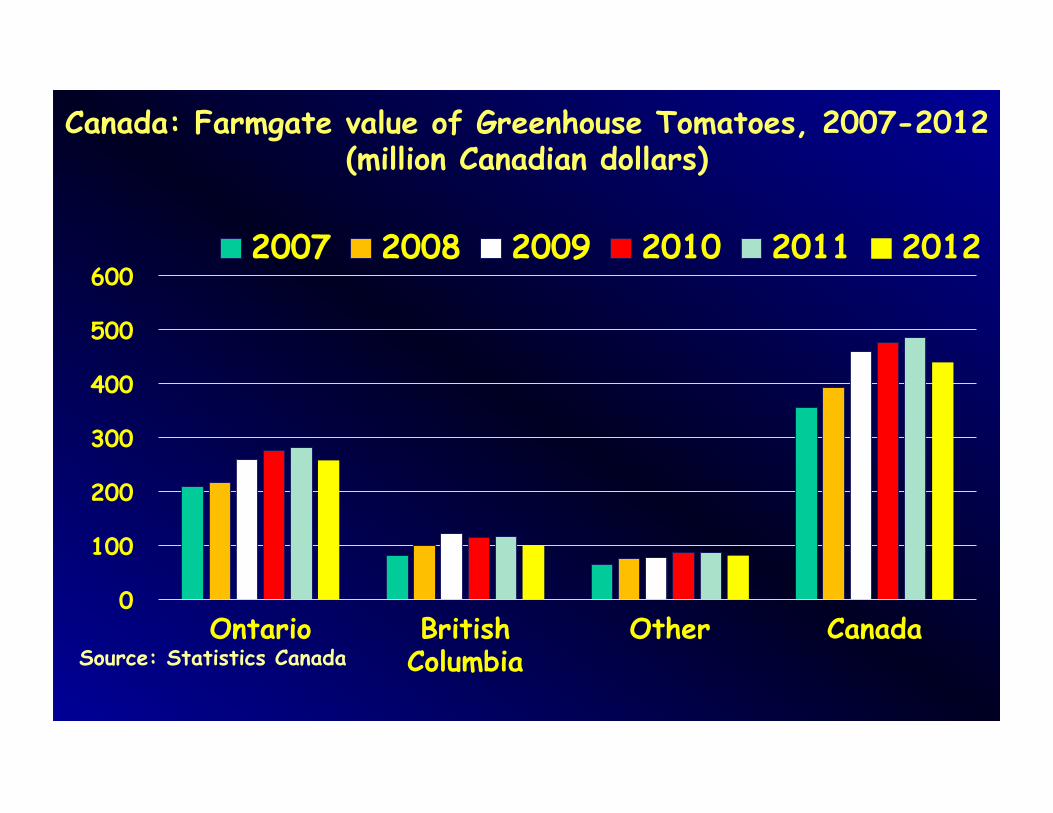

Canada: Farmgate value of Greenhouse Tomatoes, 2007-2012 (million Canadian dollars)

0

100

200

300

400

500

600

Ontario British Columbia

Other Canada

2007 2008 2009 2010 2011 2012

Source: Statistics Canada

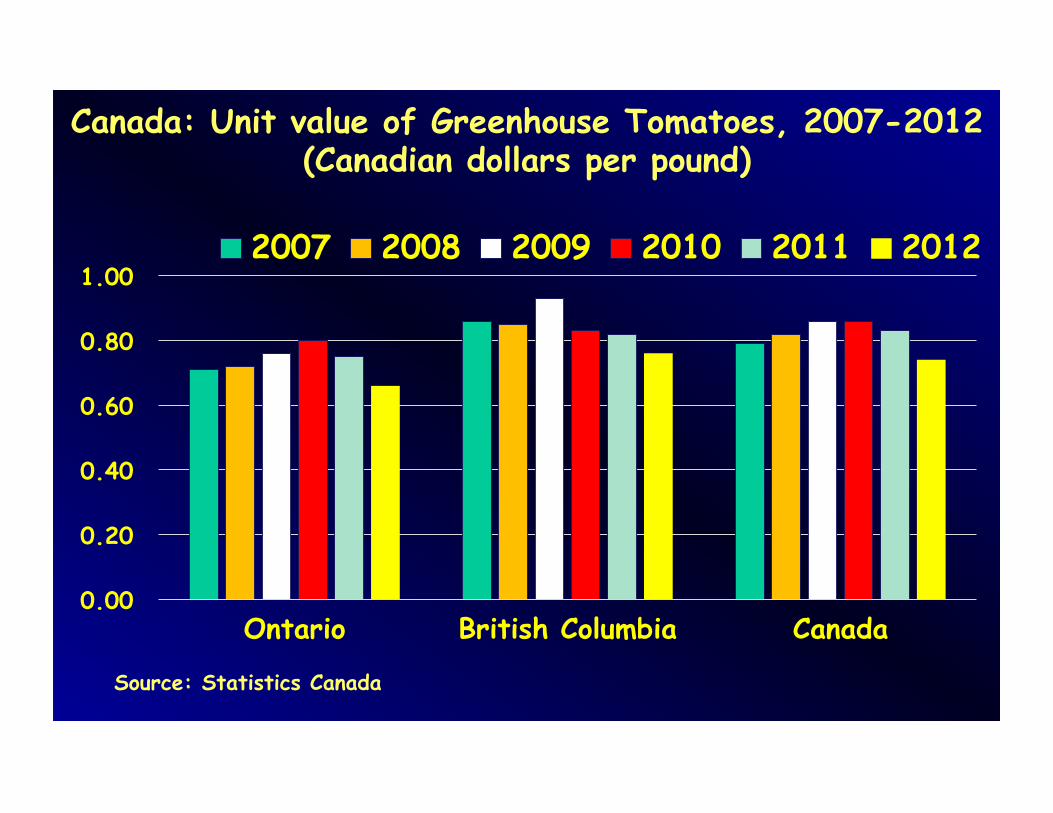

Canada: Unit value of Greenhouse Tomatoes, 2007-2012 (Canadian dollars per pound)

0.00

0.20

0.40

0.60

0.80

1.00

Ontario British Columbia Canada

2007 2008 2009 2010 2011 2012

Source: Statistics Canada

• The relatively strong competitiveness of the US veg industry is because more than being labor-intensive, fruit/veg are knowledge, technology, capital, and marketing-intensive.

• However, protected culture, which is technology and capital-intensive is emerging elsewhere.

• US growers face an ever more complex regulatory environment. • Labor availability is increasingly problematic, everywhere.

Relative Competitiveness of US Veg Industry

Mexico

• 77% of US fresh veg exports go to Canada, followed by Mexico with 8%.

• Mexico supplies 68% of U.S. fresh veg imports.

• Mexico is a powerhouse produce exporter; $6.649 billion fruit/veg exports to the world, 2010.

• US is Mexico’s predominant market.

N. American Fresh Veg Trade Mainly Intra-NAFTA

Mexican Tomato Industry • The development of new PC producers

throughout Mexico is bringing new tomato products into the domestic market, competing both with traditional small producers in central Mexico and growers in Sinaloa and Baja in their seasons.

• PC is a major new force for this dual market

crop (export and domestic markets are both important to profitability for some grower-exporters), and may become more important with the higher suspension prices.

Protected Culture in Mexico

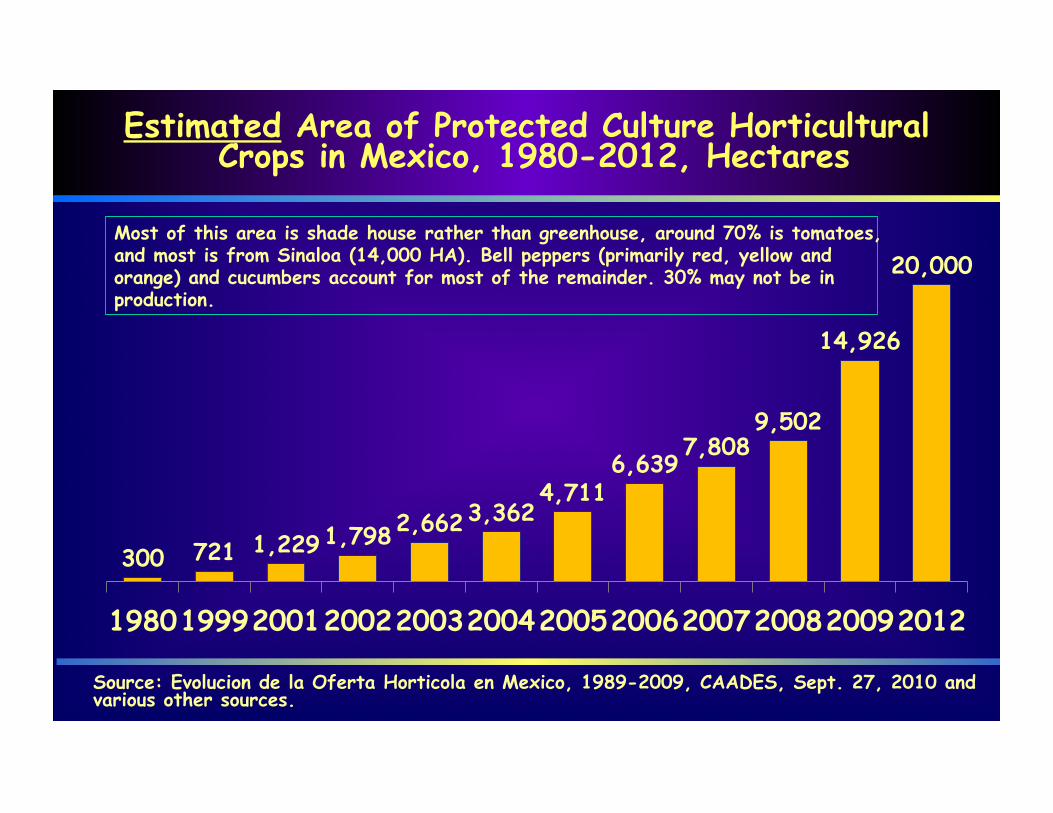

Estimated Area of Protected Culture Horticultural Crops in Mexico, 1980-2012, Hectares

300 721 1,229 1,798 2,662 3,362

4,711 6,639

7,808 9,502

14,926

20,000

1980 1999 2001 2002 2003 2004 2005 2006 2007 2008 2009 2012

Most of this area is shade house rather than greenhouse, around 70% is tomatoes, and most is from Sinaloa (14,000 HA). Bell peppers (primarily red, yellow and orange) and cucumbers account for most of the remainder. 30% may not be in production.

Source: Evolucion de la Oferta Horticola en Mexico, 1989-2009, CAADES, Sept. 27, 2010 and various other sources.

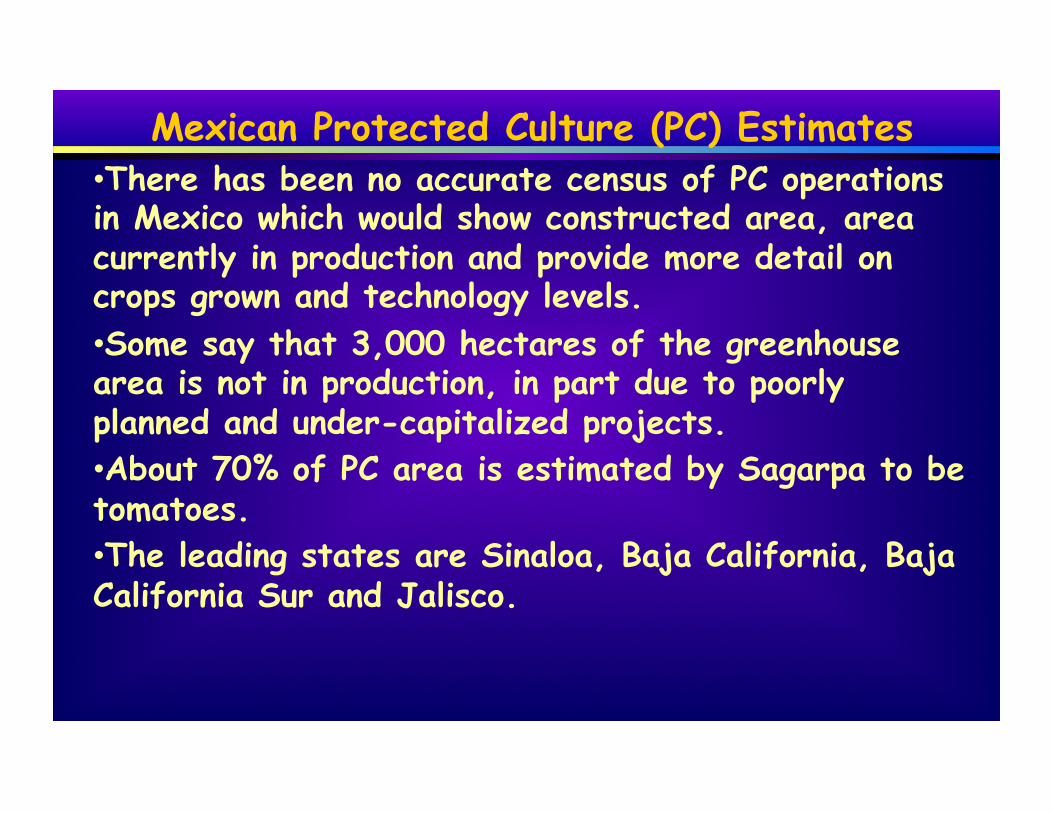

Mexican Protected Culture (PC) Estimates • There has been no accurate census of PC operations in Mexico which would show constructed area, area currently in production and provide more detail on crops grown and technology levels. • Some say that 3,000 hectares of the greenhouse area is not in production, in part due to poorly planned and under-capitalized projects. • About 70% of PC area is estimated by Sagarpa to be tomatoes. • The leading states are Sinaloa, Baja California, Baja California Sur and Jalisco.

Mexico’s Farm Workforce Has Declined between 1995 and 2010 – No panacea there either

Source: ARE Update May/Apr 2013 16(4):1-4

7.9

7.7

8.7

7.4

7.9

7.1 7.1

7.2

6.8

6.9

6.4

6.3

6.1 6.1 6.1 6.2

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Workforce in millions

Conclusions • Tomato market focusing more on quality, with

emphasis on flavor, aided by seed innovation • Export marketing from Mexico still too

fragmented, remainder of N. American industry, whether GH or open field is relatively concentrated

• Growers must be market-driven in their planting decisions

• Higher suspension prices may impose more market orderliness, to the benefit of most

Conclusions • Producers must think carefully about scaling

their operations to meet market demand • Foodservice is beginning to take more PC

tomatoes, if successful this could offer another period of expansion in demand at the expense of mature green (cost and food safety both important factors weighed by operators)

• Demand is maturing for tomatoes and cannibalization is rampant, across tomato types and sectors

Conclusions • Ongoing retail consolidation is leading to even

fewer, larger buyers, often seeking secure sources of year-round supply and contracts

• Growing use of contracts may smooth out the highs and lows of market prices

• Seems to be some growing consumer awareness of the term greenhouse and association with environmental sustainability, may follow organic trend/cache among same consumer segment (18% of households)

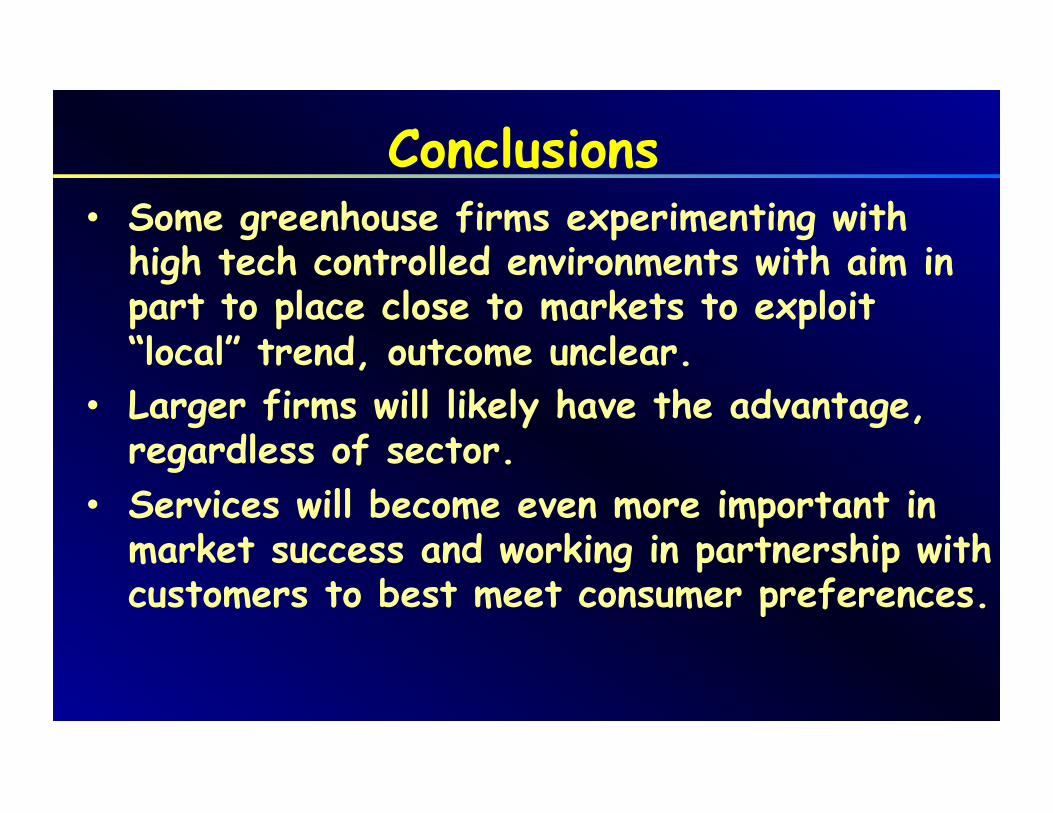

Conclusions • Some greenhouse firms experimenting with

high tech controlled environments with aim in part to place close to markets to exploit “local” trend, outcome unclear.

• Larger firms will likely have the advantage, regardless of sector.

• Services will become even more important in market success and working in partnership with customers to best meet consumer preferences.

Supplemental Information

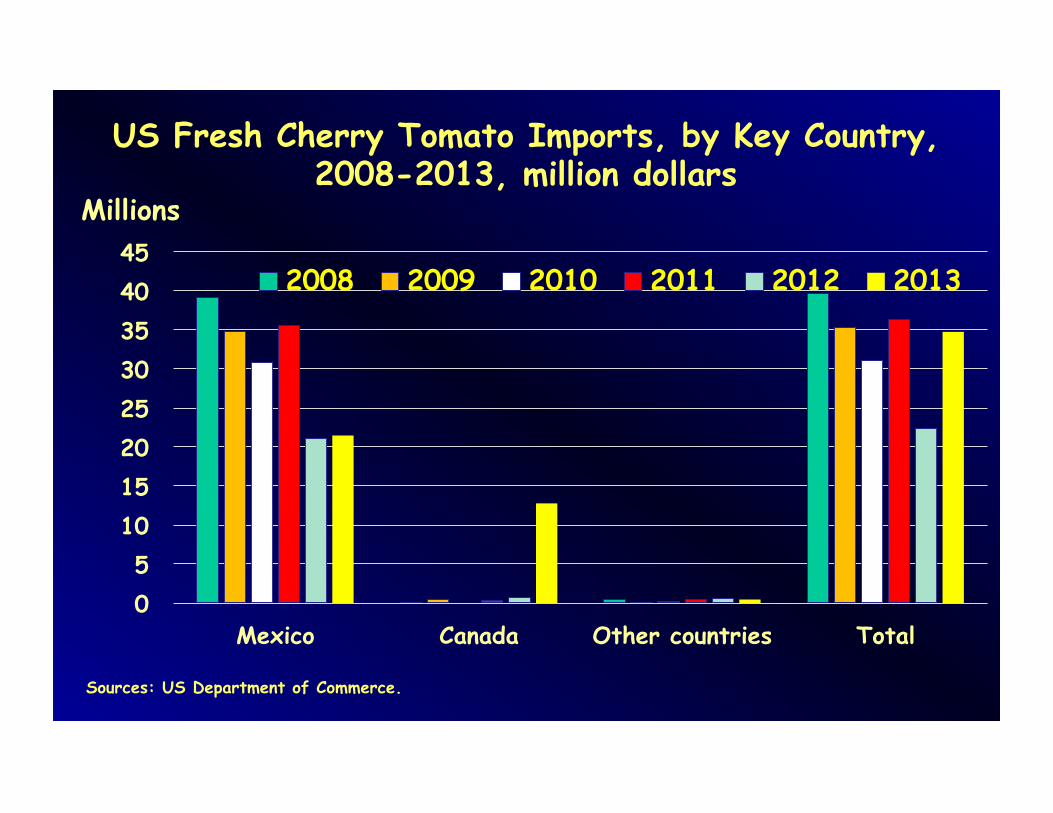

US Fresh Cherry Tomato Imports, by Key Country, 2008-2013, million dollars

0 5

10 15 20 25 30 35 40 45

Mexico Canada Other countries Total

Millions

2008 2009 2010 2011 2012 2013

Sources: US Department of Commerce.

US Fresh Grape Tomato Imports, by Key Country, 2008-2013, million dollars

0

20

40

60

80

100

120

Mexico Canada Other countries Total

Millions

2008 2009 2010 2011 2012 2013

Sources: US Department of Commerce.

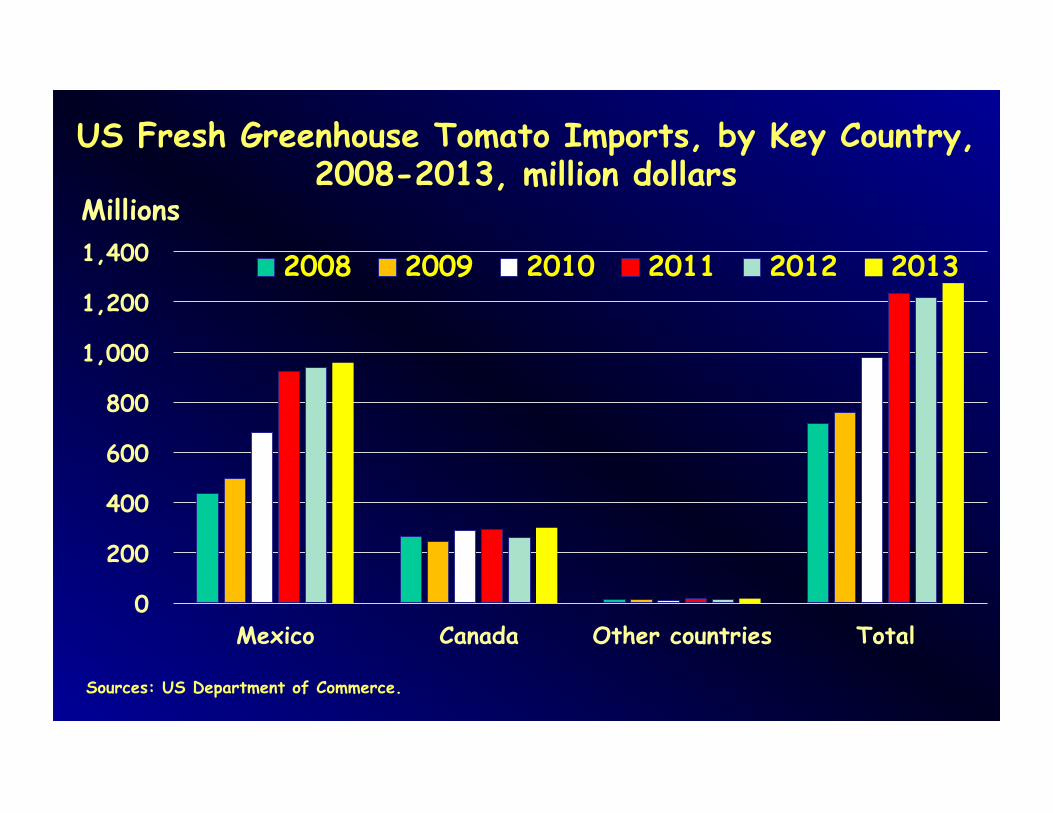

US Fresh Greenhouse Tomato Imports, by Key Country, 2008-2013, million dollars

0

200

400

600

800

1,000

1,200

1,400

Mexico Canada Other countries Total

Millions

2008 2009 2010 2011 2012 2013

Sources: US Department of Commerce.

US Fresh Roma Tomato Imports, by Key Country, 2008-2013, million dollars

0

100

200

300

400

500

600

Mexico Canada Other countries Total

Millions

2008 2009 2010 2011 2012 2013

Sources: US Department of Commerce.

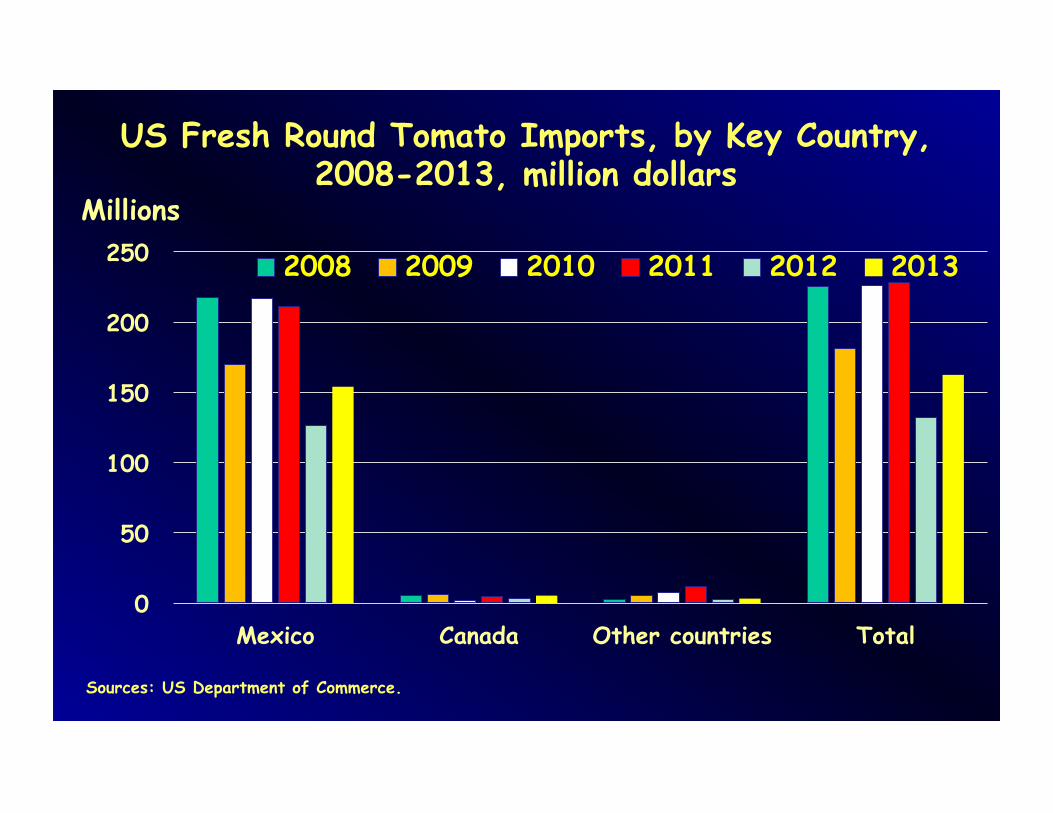

US Fresh Round Tomato Imports, by Key Country, 2008-2013, million dollars

0

50

100

150

200

250

Mexico Canada Other countries Total

Millions

2008 2009 2010 2011 2012 2013

Sources: US Department of Commerce.