Freight and Logistics Council Presentation 26 March 15 Peter Parolo, Executive Director Ports and...

15

Freight and Logistics Council Presentation 26 March 15 Peter Parolo, Executive Director Ports and Maritime

-

Upload

joel-mathews -

Category

Documents

-

view

218 -

download

1

Transcript of Freight and Logistics Council Presentation 26 March 15 Peter Parolo, Executive Director Ports and...

Freight and Logistics Council Presentation 26 March 15

Peter Parolo, Executive Director Ports and Maritime

1. State Budget Framework/Process

2. Port Tariffs, Fees and Charges (TF&C’s)

3. National Tax Equivalent Regime (NTER)

4. Rate of Return (ROR) and Dividend set by Government

5. Port Authorities (PA’s) Financials and Impact on State Net Debt

Topics of my presentation

• PA’s develop budgets which are integrated into their statutory planning documents under the Port Authorities Act 1999 (the Act).

• Budgets are integrated into the State’s financial framework and once approved, the port authority has little discretion for reallocation without Government support.

• Port financials directly impact the State’s financial targets.

1. State Budget Framework

• WA PA’s are governed by the Act. The primary functions of a PA are

• (a) to facilitate trade within and through the port and plan for future growth and development of the port; and

• (b) to undertake or arrange for activities that will encourage and facilitate the development of trade and commerce generally for the economic benefit of the State through the use of the port and related facilities.

• The State’s PA’s operate as Government Trading Enterprises (GTE’s) and they have the legislative authority under section 37 of the Act to establish port fees and charges on a commercial basis that allows for the making of a profit.

1. Budget Process

• The Minister with the concurrence of the Treasurer sets targets through the policies established by Government via the PA’s 5-year Strategic Development Plans (SDP) and annual Statement of Corporate Intent (SCI).

• The Treasurer and Minister endorse the PA’s budget and seek final approval of the Economic Expenditure Reform Committee (EERC) that may include new capital expenditure proposals.

• The SCI is tabled in Parliament.

1. Budget Process

• Financials are consolidated into State’s Budget for 4 years and reviewed twice yearly (Budget and Mid Year Review).

• All Budgets and changes must be approved by Government.

• Cash at bank in a port is seen as State funds and these funds can only be spent if spending is approved as part of the budget process.

1. Budget Process

• Government in recent times has been focused on

– PA’s achieving sustainable cash flows for the port’s operational needs and,

– ensuring reasonable returns to Government.

• PA’s have been subjected to mandated cost saving reductions by Government in recent years as per the general government sector.

1. Budget Process

• The 2012-13 budget included a provision for improved financial rate of return for 2012-13 and forward estimates to 2015-16 inclusive.

• A target was set for all the port authorities of an additional $145m operating profit and $84.9m tax and dividends over four years. This was an approximate 20% increase on submitted figures and was based on volume increases and port efficiencies.

1. Budget Process Setting

• The Treasurer concurs with the Minister on Port’s annual SCI and 5-year SDP plans, which includes financials and Return on Assets.

• All fees and charges are tied to the financials, but fee increases (%), CPI or other are identified in the PA’s SCI.

• Additionally and separate to the above, PA’s are required to make a separate Tariffs Fees & Charges (TFCs) submission to be approved by the Minister as per the Treasurer’s instructions.

2. Port Tariffs, Fees and Charges

• PA’s need to assess that TF&Cs have been set at a level that is reflective of full costs incurred in the provision of various services, plus a rate of return.

• PA’s are required to provide information on the results of their reviews for consideration by the EERC as part of the budget process.

• Port’s provide a schedule of fees and charges online.

2. Port Charges, Tariffs and Fees

• The tax laws are set by the Commonwealth Government and applied to the State’s GTEs through the National Tax Equivalent Regime.

• The 30% Tax liability is to be factored as a cost component in PA’s cost assessments.

• The State Government will not, in‑principle, fund tax liabilities resulting from commercial decisions by GTEs.

3. National Tax Equivalent Regime (NTER)

• Under the State Government’s financial policy PA’s are required to pay a dividend equivalent to 65% of after tax profit for the financial year.

• In December 2012, the Economic Expenditure Reform Committee (EERC) endorsed the recommendations in the Port Authority Revenue and Pricing Framework paper, but clarified that any ROR target is not considered a ceiling or barrier to PA’s achieving higher RORs where deemed appropriate.

• DoT continues to work with the Western Australian Treasury Corporation (WATC) and each of the port authorities on determining an appropriate ROR level acceptable to Government.

4. Rate of Return(ROR) and Dividend set by Government

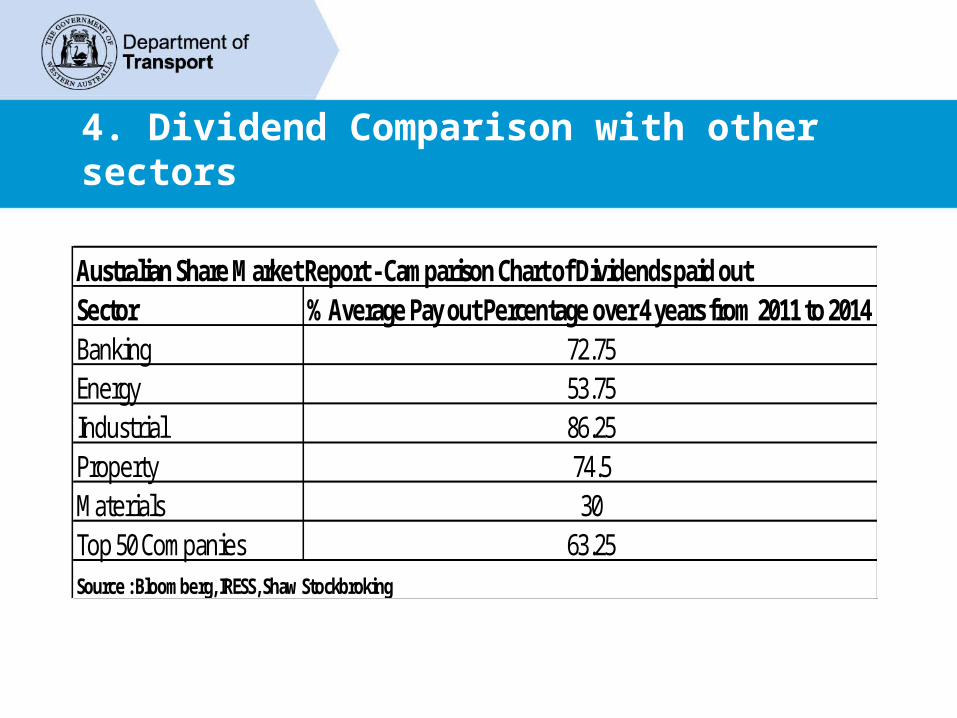

4. Dividend Comparison with other sectors

Australian Share Market Report - Camparison Chart of Dividends paid outSector % Average Pay out Percentage over 4 years from 2011 to 2014Banking 72.75Energy 53.75Industrial 86.25Property 74.5Materials 30Top 50 Companies 63.25Source : Bloomberg, IRESS, Shaw Stockbroking

5. Port Authority Financials and Impact on State Net Debt

• Net debt directly impacts on the State credit rating.

• Ports financial results affect net debt and hence Treasury closely scrutinises any changes in these results.

• Any change in the impact on net debt has to be approved by EERC or Government.

• Notably, if a port wishes to purchase a non-current asset from cash reserves this will have an adverse net debt impact.

• One sample paragraph

• Two sample paragraphs

• Three sample paragraphs

• Four sample paragraphs

• Six sample paragraphs

– Sublevel

QUESTIONS?