Fraud & Internal Controls

46

Fraud & Internal Fraud & Internal Controls Controls Jonathan G. Kassouf, CPA Jonathan G. Kassouf, CPA L. Paul Kassouf & Co., L. Paul Kassouf & Co., P.C. P.C. 1

-

Upload

greenway-health -

Category

Technology

-

view

860 -

download

2

Transcript of Fraud & Internal Controls

Fraud & Internal ControlsFraud & Internal Controls

Jonathan G. Kassouf, CPAJonathan G. Kassouf, CPA

L. Paul Kassouf & Co., P.C.L. Paul Kassouf & Co., P.C.

1

Should you be concerned?Should you be concerned?

• 33% of all employees have stolen money or merchandise at least once

• The average company loses 6% of its annual revenue to fraud, committed by its own employees

• Theft occurs in 95% of companies

2

Should you be concerned?Should you be concerned?

• According to the Association of Certified Fraud Examiners, 3 out of 4 physicians will suffer a significant loss due to theft during their careers

3

Should you be concerned?Should you be concerned?

• On average, embezzlement takes 18 months to discover

• Average loss is estimated at $80,000

• Recent reports estimate losses as high as $500 billion annually among all businesses – half the projected cost of national health care reform!

4

Key PointsKey Points

• Physician practices are easy targets

• Knowledge of financial workings can greatly reduce embezzlement

• If someone wants to embezzle, they will

5

Key PointsKey Points

• True danger is that embezzlement is indicative of larger weaknesses– Patient data integrity– Payer information– Historical records

• Your goal? To make it difficult to embezzle

6

Is your practice at risk?Is your practice at risk?

• Donald Cressey– Indiana University student in the 1940s

seeking his Ph.D. in criminology– Dissertation on embezzlers– Interviewed 200 incarcerated inmates at

prisons in the Midwest– Referred to embezzlers as “trust

violators”

7

Is your practice at risk?Is your practice at risk?

• Cressey’s final hypothesis– “Trusted persons become trust violators when

they conceive of themselves as having a financial problem which is non-shareable, are aware this problem can be secretly resolved by violation of the position of financial trust, and are able to apply to their own conduct in that situation verbalizations which enable them to adjust their conceptions of themselves as trusted persons with their conceptions of themselves as usersof the entrusted funds or property.”

8

Is your practice at risk?Is your practice at risk?

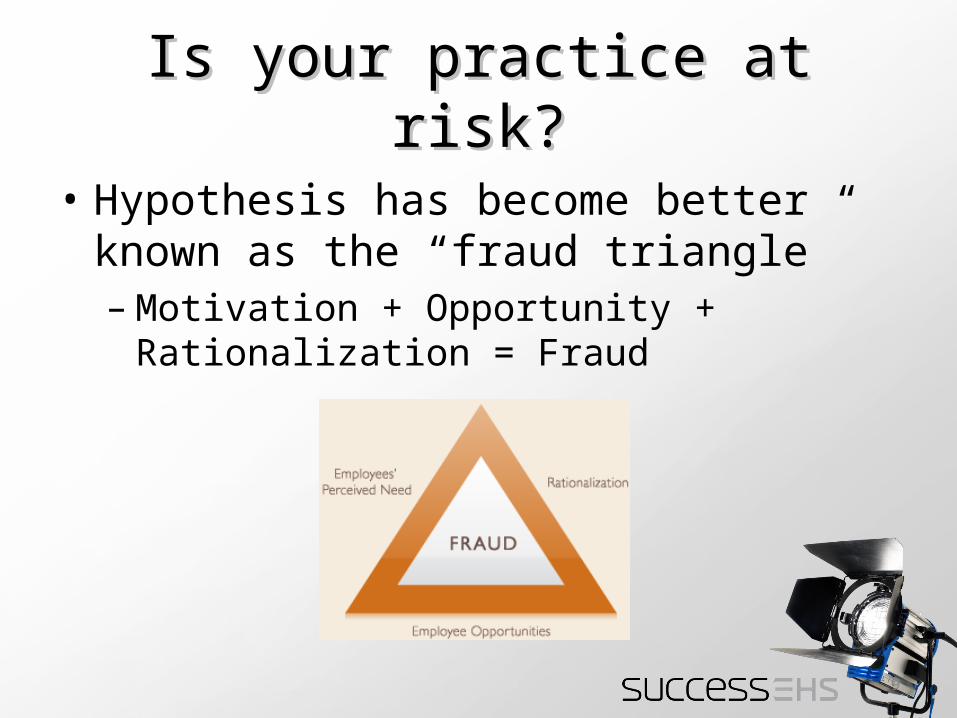

• Hypothesis has become better known as the “fraud triangle”–Motivation + Opportunity +

Rationalization = Fraud

9

Is your practice at risk?Is your practice at risk?

• Types of offenders– Active• Driven by motivation or greed

– Passive• Tempted by system weaknesses

10

Why do people embezzle?Why do people embezzle?

• Greed

• Support personal problems

• Jealous of physician’s earning capacity

• Angry at boss or co-workers

• Feel unappreciated

• For the challenge

11

Warning SignsWarning Signs

• Billing department– Cash flow– Changes in A/R statistics– Patient complaints about statements

12

Warning SignsWarning Signs

• Bookkeeper– Cash flow– Unexplained overhead increases– Incurring late charges/penalties–Missing sequence of checks– IRS notices– Untimely data– Unusual behavior

13

Which transactions are Which transactions are vulnerable?vulnerable?

• Cash receipts

• Cash disbursements

• Accounting adjustments

• Insurance filings

• All of the above

14

Embezzlement from Embezzlement from Cash Receipts CycleCash Receipts Cycle

• Employee pockets cash received from patient (skimming) – Higher deductibles and copays– Employee does not record patient visit or

payment

• Employee uses payment from Patient B to credit account of Patient A (lapping)– Complicated, time-consuming, and

lengthy15

How can you limit How can you limit embezzlement opportunities?embezzlement opportunities?

• Use internal controls:

– One employee collects receipts– Another employee makes the deposit– Another employee posts payments and

adjustments

16

How can you limit How can you limit embezzlement opportunities?embezzlement opportunities?

• Review and compare daily activity reports to bank deposits and vice versa

• Use EFTs whenever possible

17

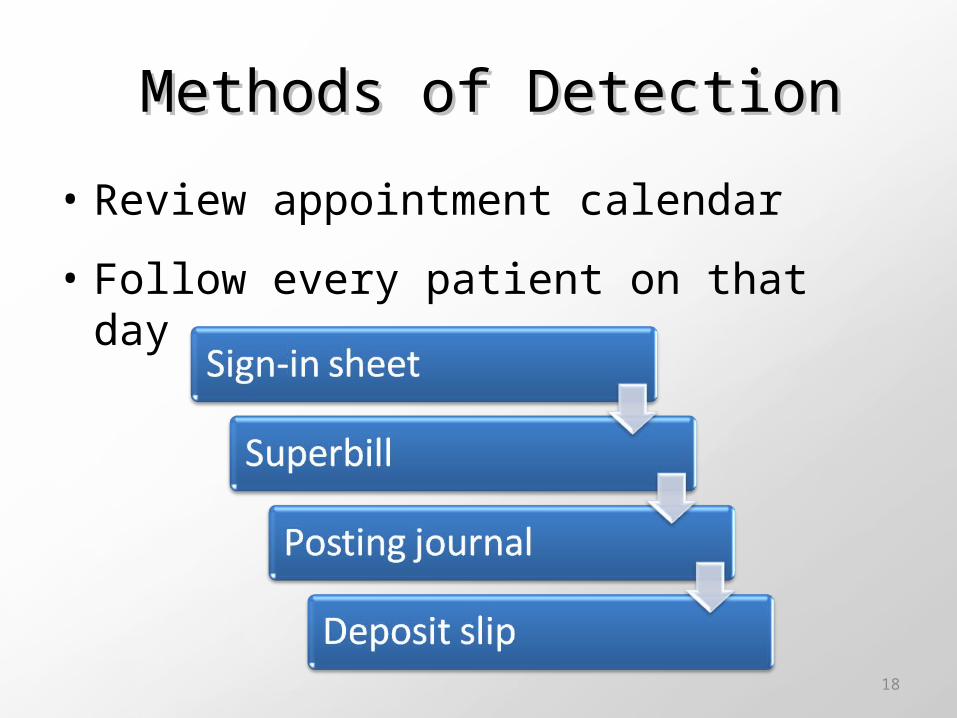

Methods of DetectionMethods of Detection

• Review appointment calendar

• Follow every patient on that day …

18

Methods of DetectionMethods of Detection

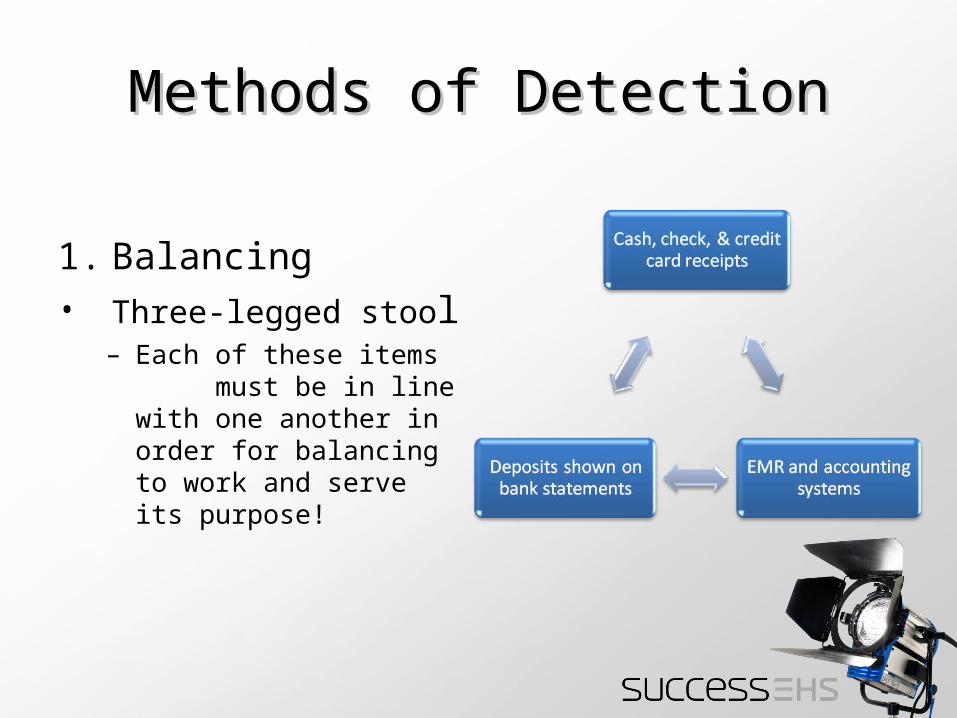

1. Balancing• Three-legged stool

– Each of these items must be in line with one another in order for balancing to work and serve its purpose!

19

Methods of DetectionMethods of Detection

• Balancing is a monthly, rolling process!

• Don’t neglect credit card reconciliation

Monthly Cash & A/R Reconciliation

Cash deposited XXX.XX

Less: A/R payments posted

(XXX.XX)

Difference XXX.XX

A/R posted last month, deposited this month

-

A/R posted this month, deposited next month

+

A/R posted this month, deposited last month

+

A/R posted next month, deposited this month

-

Subtotal XXX.XX

Non A/R income / bank adjustments

-

Net difference ZERO!

20

Methods of DetectionMethods of Detection

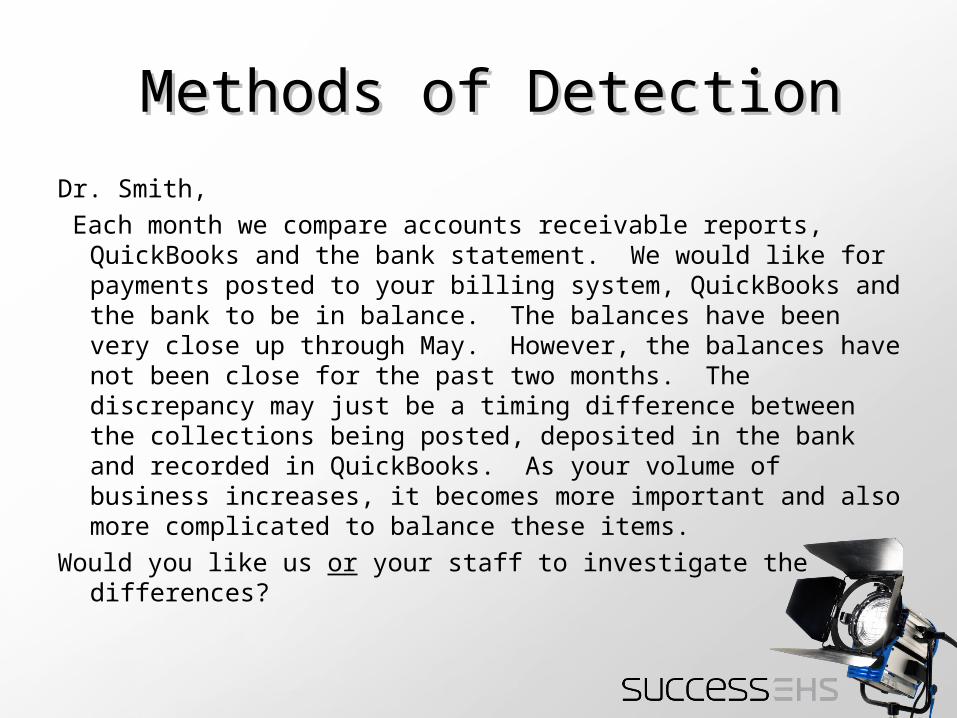

Dr. Smith, Each month we compare accounts receivable reports,

QuickBooks and the bank statement. We would like for payments posted to your billing system, QuickBooks and the bank to be in balance. The balances have been very close up through May. However, the balances have not been close for the past two months. The discrepancy may just be a timing difference between the collections being posted, deposited in the bank and recorded in QuickBooks. As your volume of business increases, it becomes more important and also more complicated to balance these items.

Would you like us or your staff to investigate the differences?

21

Methods of DetectionMethods of Detection

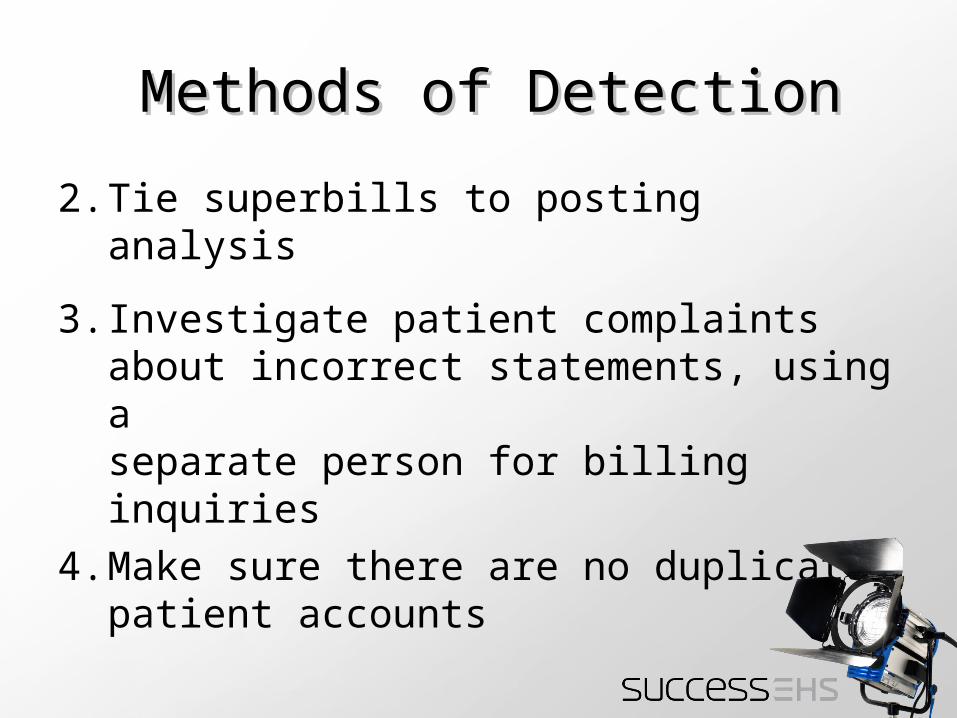

2. Tie superbills to posting analysis

3. Investigate patient complaints about incorrect statements, using aseparate person for billinginquiries

4. Make sure there are no duplicate patient accounts

22

Methods of DetectionMethods of Detection

5. Control hardcopy and electronic charge tickets and cash payments, so breaks in sequence can be monitored – follow through on monitoring

6. Review electronically generated missing and voided charge ticket report – check-ins must match check-outs

23

Embezzlement from Embezzlement from Cash Disbursements CycleCash Disbursements Cycle

• Invoices from fake company

• Paychecks to phantom employee

• Paychecks to existing employee– Employee increases gross pay and

withholdings, keeping net pay the same

24

Embezzlement from Embezzlement from Cash Disbursements CycleCash Disbursements Cycle

• Items purchased for personal use are coded as payments for supplies

• “Kickbacks” from suppliers– Over-ordering supplies and

accepting/cashing refund check after forging payee’s name

– ATM deposits

25

Embezzlement from Embezzlement from Cash Disbursements CycleCash Disbursements Cycle

• Know your vendors– Ask about new vendors and/or contact

them

– Sign checks only with proper documentation of shipping, service tickets, and invoices

– Review monthly bank statement(s) and cancelled checks, paying attention to endorsements

26

Embezzlement from Embezzlement from Cash Disbursements CycleCash Disbursements Cycle

• “Borrowing” money or non-receipted expenses from petty cash or change funds

• Non-specific or undocumented employee reimbursements

• Multiple bank accounts for practice

27

Embezzlement from Embezzlement from Cash Disbursements CycleCash Disbursements Cycle

• Patient and insurance refunds– Verify patient and review chart notes– Sign checks only with proper

documentation of patient account and insurance payments

• Credit card usage and misuse by employees

28

Other MethodsOther Methods

• More complex methods of embezzlement require access and knowledge

• Office pilferage– Postage, copies, time cards, long-

distance calls, medical supplies, medications

29

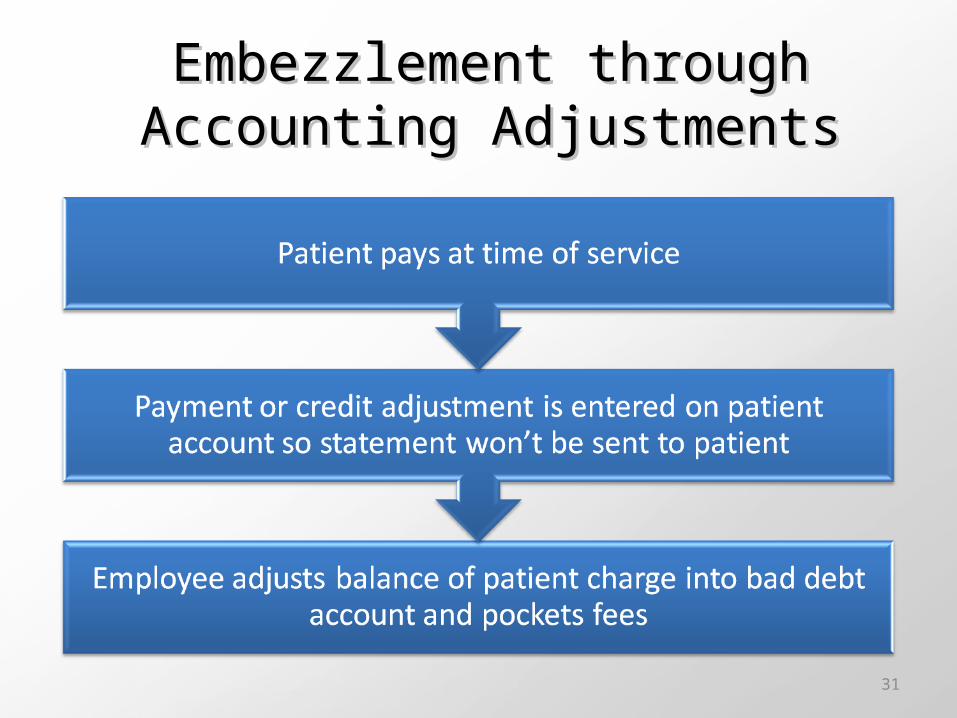

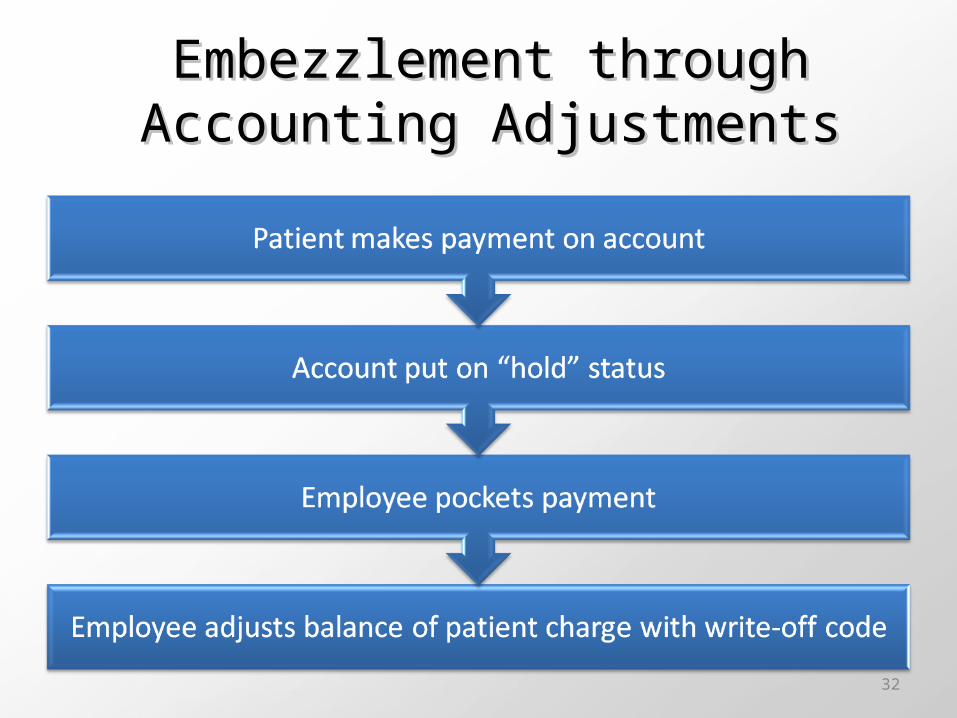

Embezzlement through Embezzlement through Accounting AdjustmentsAccounting Adjustments

• Using computer adjustments to bury embezzlement

• Bad debt expense account used to hide stolen amounts (debits)

30

Embezzlement through Embezzlement through Accounting AdjustmentsAccounting Adjustments

31

Embezzlement through Embezzlement through Accounting AdjustmentsAccounting Adjustments

32

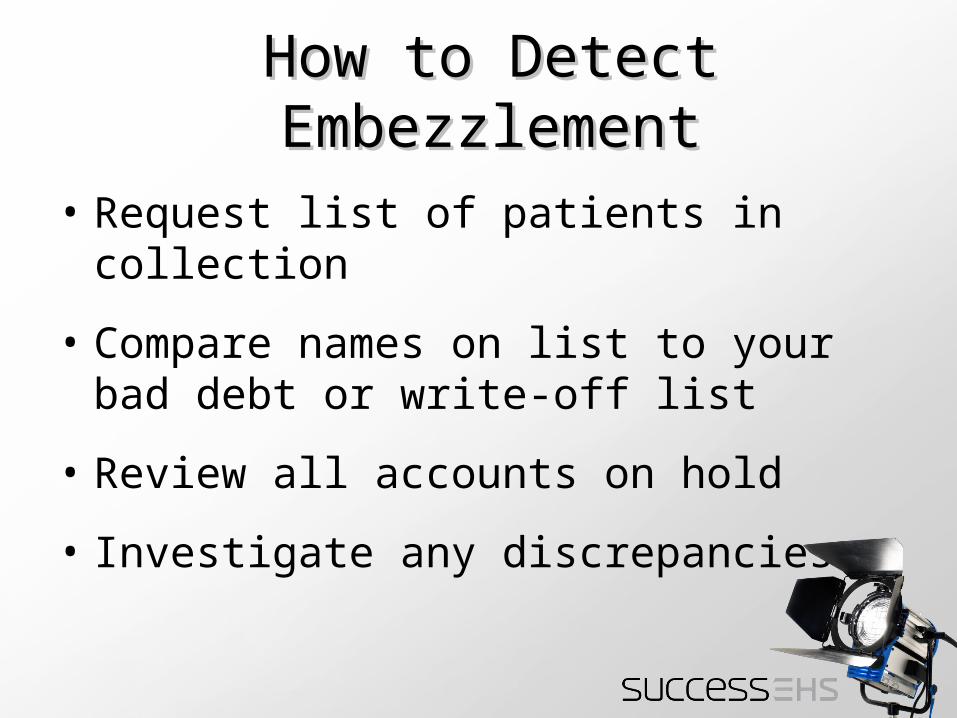

How to Detect How to Detect EmbezzlementEmbezzlement

• Request list of patients in collection

• Compare names on list to your bad debt or write-off list

• Review all accounts on hold

• Investigate any discrepancies

33

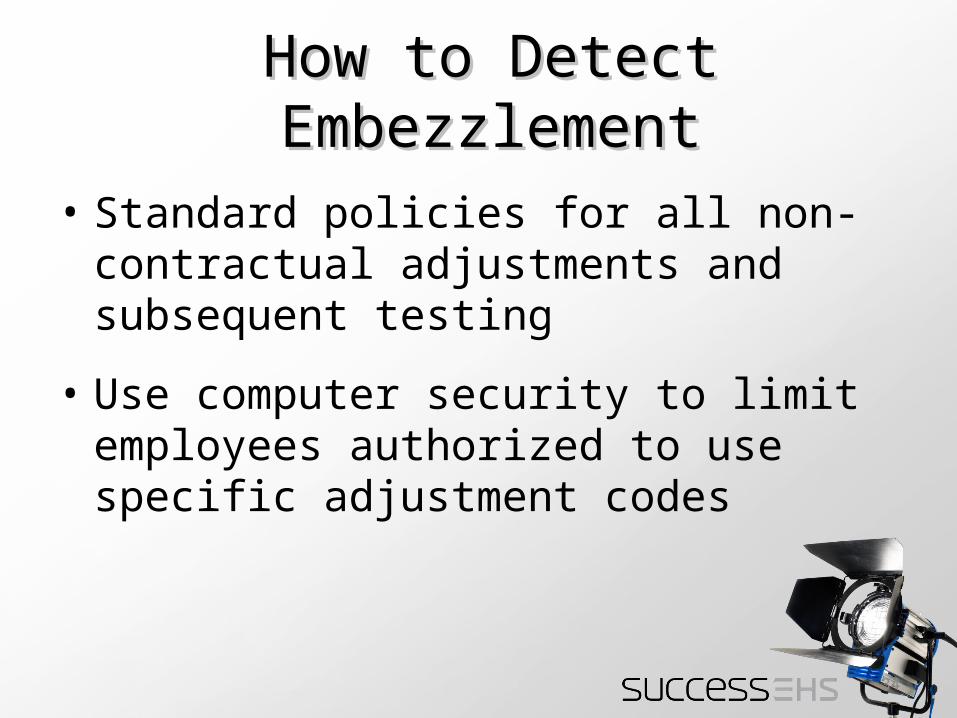

How to Detect How to Detect EmbezzlementEmbezzlement

• Standard policies for all non-contractual adjustments and subsequent testing

• Use computer security to limit employees authorized to use specific adjustment codes

34

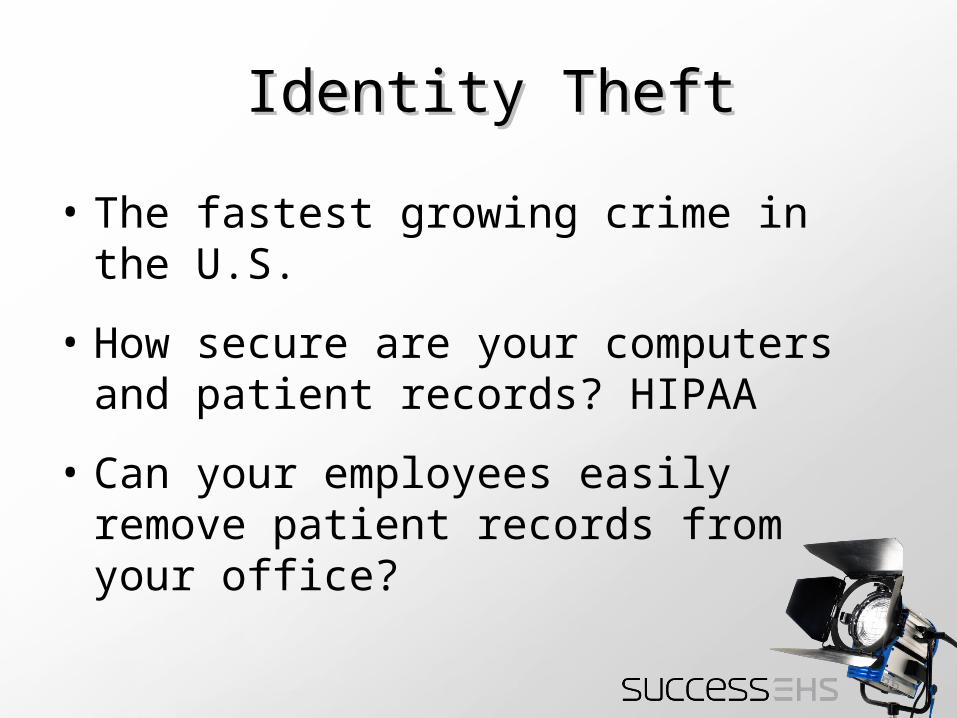

Identity TheftIdentity Theft

• The fastest growing crime in the U.S.

• How secure are your computers and patient records? HIPAA

• Can your employees easily remove patient records from your office?

35

Identity TheftIdentity Theft

• Do employees have remote access?

• Run report history and see what has been extracted

36

Protect Your CreditProtect Your Credit

37

What else can you do?What else can you do?

• Practitioner/employer should set a good example– Use of petty cash, for example– Establish policy of enforced accountability

• Use a complete practice management software system– Helps document records, evidence,

and losses

38

What else can you do?What else can you do?

• Investigate claim activity for patients who haven’t been seen recently or who are unfamiliar

• Consider lockbox

• Use passwords and log-ins to control who can make account adjustments

39

What else can you do?What else can you do?

• Require each employee to log on individually when working with records or data

• Utilize EFT whenever available

• Segregation of duties– No single employee should handle any

transaction from beginning to end

40

What else can you do?What else can you do?

• Fidelity Bond– $100,000 minimum or one month’s

collections– Add legal and accounting rider– Serves as deterrent to financial crime

because bonding companies prosecute perpetrators

41

What else can you do?What else can you do?

• Employee background checks– Incorporate on application–Watch– Employment screening service– References

42

What else can you do?What else can you do?

• Office of Inspector General– List of Excluded Individuals/Entities (LEIE)– No federal payment will be made by any

Federal health care program for any items or services furnished, ordered, or prescribed by an excluded individual or entity

– No program payment will be made for anything that an excluded person furnishes,orders, or prescribes

43

What else can you do?What else can you do?

• Eliminate all signature stamps– If not, contact stamp vendor to obtain

inventory of ordered stamps

• Require staff to take vacations

• Cross-train staff so multiple employees know how to balance books– Rotate job responsibilities periodically

44

What else can you do?What else can you do?

• Watch for suspicious behavior/lifestyle

• Give employees a way to report fraud

• QuickBooks– Turn on Audit Trail function

• Have certified public accountants set up record keeping and test for reliability and accuracy– Practice assessments

45

This PowerPoint was presented as part of the SuccessEHS 2011 Customer Conference.

www.successehs.com

46