Fratelli Case

28

FRATELLI CARLI: GROWTH OPTIONS FOR A FAMIL Y BUSINESS Reference no 506-179-1 Technical assistance t +44 (0)1234 756410, e [email protected] North American customers: t + 1 781 2395884, e [email protected] If you are having problems opening this document visit www.ecch.com/ppdfhelp for guidance. Document ID: 11020-1388-18AFA-00018AFD ~ ethe case for learning Dlstrlbuted by eccb, UK and USA www.ecch.com All rights reserved North America t +17812395884 f +1 781 2395885 e [email protected] Rest of the world t +44 (0)1234 750903 f +44 (0)1234 751125 e [email protected]

Transcript of Fratelli Case

FRATELLI CARLI: GROWTH OPTIONS FOR AFAMIL Y BUSINESS

Reference no 506-179-1

Technical assistance

t +44 (0)1234 756410, e [email protected]

North American customers:t + 1 781 2395884, e [email protected]

If you are having problems opening this document visit www.ecch.com/ppdfhelp for guidance.

Document ID: 11020-1388-18AFA-00018AFD ~

ethe case for learning

Dlstrlbuted by eccb, UK and USAwww.ecch.comAll rights reserved

North Americat +17812395884f +1 781 2395885e [email protected]

Rest of the worldt +44 (0)1234 750903f +44 (0)1234 751125e [email protected]

llRII:-.,:TEIl .•"JI\TIONAl

UN IVERSITY OF MONACO

Fratelli CarliGrowth Options for a Family BusinessCase studyReference no 506-179-1

This case was written by Professor Marika Taishoff,Professor Sandrine Ricard andProfessor Francis R IlIe,lnternational University of Monaco.lt is intended to beused as the basis for class discussion rather than to illustrate either effective orineffective handling of a management situation.The case was made possible bythe co-operation of Fratelli Carli.

© 2006,1nternational University of Monaco.No part of this publication may be copied,stored,transmitted,reproducedor distributed in any form or medium whatsoever without the permissionof the copyright owner.

ethe case far learningDistributed by ecch, UK and USAwww.ecch.com·\11 r,qbt~ rl'~f'r'J('(j

Printed in UK and USA

North Americat +1 781 2395884f .; 7Rl 2l<J :'885

e eccbusegaecch.corn

Rest of the worldt +44 (0)1234 750903f •• l.~ 0112.1.1751 ;25e ecch@ec(h.com

506-179-1

lLN1ISIl;:IlNAnONAl

UN IVERSIlY' OF MONACO

FRATELLI eARLI: GROWTH OPTIONS FOR A FAMILY BUSINESS

This case was prepared byProfessor Marika Taishoff,Professor Sandrine Ricard,and Professor Francis Ille, asa basis for dass discussionrather than to illustrate eithereffective or ineffectivehandling 0/ a businesssituation.

On an unusually cold winter's day in early 2005, from his officeoverlooking the Mediterranean, Gianfranco Carli, grandson of thefounder ofthe Fratelli Carli Olive Oil Company, studied the firm'statest financial figures. Although it couldn't be said that businesswas bad, Mr. Carli was concemed, as he had been for severalyears now, about the direction the company needed to take tosustain its growth and profits into the future.

And once again his attention was focused on Carli's product line,and its distribution strategy: was the market for olive oil and oliveoil products changing? In wh ich ways, and how would it evolve inthe future? Should Carli's product line and direct-to-consumerdistribution strategy is adapted to these changes, or would suchmoves risk diluting the Carli brand's equity? And, finally, did thefamily owned company, with 250 employees and c\ose to onemillion customers across Italy, have the skills, infrastructure andcompetencies necessary to successfully implement, and sustain,any sweeping changes?

Signor Carli's office was just a few hundred meters away from thesea, and the view stretched over the gentle hills of Imperia, a smalltown in the Italian coastal region of Liguria where his grandfatherGiovanni Carli created the firm in 1911. In those early years itwas not unusual for landowning families in the area to seil the oilfrom their olive groves to neighbours, and Giovanni Carli did thison his bicyc\e, going from one neighbour to another.

In the course ofthat century, the small enterprise grew to becomeone of the leading olive oil distributors in Italy. It was number onein sales of regular olive oil, and the ninth largest distributor ofextra virgin olive oi!.

The family always believed that one of the reasons for Carli'ssuccess was its unique distribution system. Ever since itsinception, Carli only sold directly to its end users. Carlimanagement believed that this direct system not only allowed it to

Copyright © 2006 International University of Monaco 2

506-179-1

know and remain close to its customers, but also to avoid becoming dependent on retailers.And as the distribution landscape in Italy began to change in the late 1990s, with retailersconsolidating and acquiring ever-greater bargaining power, it seemed that Fratelli Carli'sstrategie option had been the right one.

Yet at the same time, the olive oil industry and its market had gone through severaltransformations in the past few years. Major fast moving consumer goods companies(FMCGs), such as Uni lever, had entered the market on the supply side, while on the retail sidethe large supermarket chains had intensified their hold on the market, and in the processchanged the purchase process for olive oil: by 2004, 75% of all the olive eil sold in Italy wassold because of a promotional offer in the supermarkets. The product category itself was nowconsidered a loss leader by the supermarket chains.

One of the issues wh ich had been vexing Gianfranco Carli for several years now was whetherhis firm's unyielding direct approach to distribution continued to be appropriate given theseevolving circumstances. Another issue, even more pressing he feit now in early 2005, waswhether the 1997 decision to diversify into olive oil based cosmetics had been the right one.For a family run firm, decisions about suitable avenues for growth were even more criticalthan they were for publicly held firms. Both the options for growth, as weil as the resourcesavailable to dedicate to it, were more limited, and therefore the choice had to be spot on.

Carli pondered the results from the direct sales of Carli olive oil cosmetics in ltaly, as weil asthird party sales from the 400 Spanish perfumeries that stocked Carli's olive oil cosmetics.Had the right decision been taken to diversify so dramatically from the company's corecompetence? Should Carli rather have focused on what it knew best-the manufacture anddistribution of olive oil, wh ich contributed 75% to its tumover, compared to only 4.4% fromcosmetics=and grow geographically? After all, its brand was one of the most recognisable inthe Italian olive oil market, and worldwide olive oil consumption had been growing at a rateof about 4%, with much higher growth rates in attractive markets like the United States andparts of Asia.

UNEXPECTED BEGINNINGS AND GROWTH

In the year 1911, the region of Liguria in northern Italy--bordering France and sharing thesame magnificent Mediterranean coastline-had an exceptional harvest of olives. The olivetrees belonging to the Carli family, who had a farm near the town of Irnperia, were soweighted down that Giovanni Carli, the youngest son in the family, decided to sell some ofthe family's olive oil to farming villages in the neighbouring Piedmont region of Italy to thenorth. He returned horne with such a huge list of orders that he had to enlist the support of hissister and three brothers to process and deliver them. And so the firm of Fratelli Carli (theCarli Brothers) was created in the year 1911-a memorable date which is still emblazoned onall the bottles of Fratelli Carli olive oil-"dal 1911".

From the very beginning, Fratelli Carli delivered directly to its custorners' hornes. Thecustomer base grew rapidly in those early years, as did the reputation of the firm. In 1926, theItalian royal family of the Savoys appointed Fratelli Carli as its official supplier; eleven yearslater so too did the Papal Establishment at the Vatican.

Copyright CD2006 Internationall!niversity ofMonaco 3

506-179-1

Growth in the number of orders continued steadily until the outbreak of WorId War 11.Duringthat time, the Fratelli Carli factory was destroyed during the heavy aerial bombardments ofthe region. It wouldn't be until eight years later that Fratelli Carli was back in operation. Andthen too, it continued with the same system it had used from the very outset: the hornedelivery of Frate 11i Carli olive oil.

PRODUCT AND PRODUCTION

By the late 1990s, the Fratelli CarIi plant had six to seven bottling lines producing severalhundred tons of olive oil per day.

Contrary to what many of Carli's loyalltalian customers believed, CarIi itself did not producethe olives from which its oils were made: it simply did not have enough trees! Instead it hadto import olives from which it then distilled the oil. This situation was not unique to Carli, butinstead characteristic of the olive oil industry in Italy, although it still comes as a surprise tomost olive oil purchasers the worId over.

In the US, the issue of misleading advertising was raised when it was learned that one of themost popular brands of olive oil in that country, Filippo Berio---a brand which portrayed itselfas an old-style favorite from Lucca, and whose label proclaimed it was 'Imported FromItaly'-was instead a composition of olive oils coming primarily from Spain, Greece andTunisia, and simply bottled in the celebrated olive growing tegion of Tuscany. As oneobserver put it, the "ltalian olive oil industry has long been built on this illusion; in truth, Italydoes not grow enough olives to meet even its own demand, let alone foreigners'."'

Quality Control from Beginning to End

Fratelli Carli sourced its olives from small producers in Spain, Greece and Italy. Its long termrelationships with these suppliers, based on years of working together and the ensuing trust,was considered an advantage especially in those years when there was shortage of goodsupply due to droughts or other factors. Even then CarIi could always count on getting thebest produce due to its good rapport with these farmers.

Carli would then proceed to crush the olives and assemble and refine the oils that resulted. Itconsidered this process of harmonizing the different oils, softening the acidities andsmoothing out tastes that were too strong, as one of its key competencies. As one of itsmanagers explained,

"Regardless of the source of the olives, the final, "Carli" product must have the sameexcellent quality, taste, and texture, year in year out. This is what our customers expectofus. And this is what we have to guarantee to them."

Accordingly, the Carli Quality Control Division established and monitored aseries ofstandards which began while the olives were still maturing on suppliers' trees; then on toprocessing plant and equipment; through to bulk storage-where the olive oil remained untilreceipt of orders from customers; then, based on customer orders, in the packing stage; andfinally in the shipping process.

I Levy, C. "The Olive Oil Seems Fine-Whether It's Italian is the Issue", The New York Times, 7 May 2004

Copyright © 2006 International University of Monaco 4

506-179-1

Fratellli Carli Olive Oil was packed in dark green glass bottles, as weil as in cans, both ofwhich offered a high degree of protection from light that deteriorated the quality of the oil.The bottles were strongly branded with the name and distinctive logo and font, along with thedate of creation, 1911. (See Exhibit 1 for an illustration of the Fratelli Carli Olive Oilglass bottles).

The Final Product

Although Carli sold the same product everywhere, its characteristics would be adapted to thetastes of specific regions. In terms of consumer preferences, the ltalian market wasfragmented and far from uniform in its taste: in Northern Italy custorners preferred olive oilwhose taste was not overly strong; in areas of the south like Naples and in the countrysidegenerally, people consumed more olive oil than anywhere else in Italy, and tended to look forthe cheapest products. Regardless of differences in taste however, the company abided by thestrict standards applied by the EU concerning what qualified as "Extra Virgin Olive Oil", and"100% Pure Olive Oil".

Fratelli Carli Extra Virgin Olive Oil

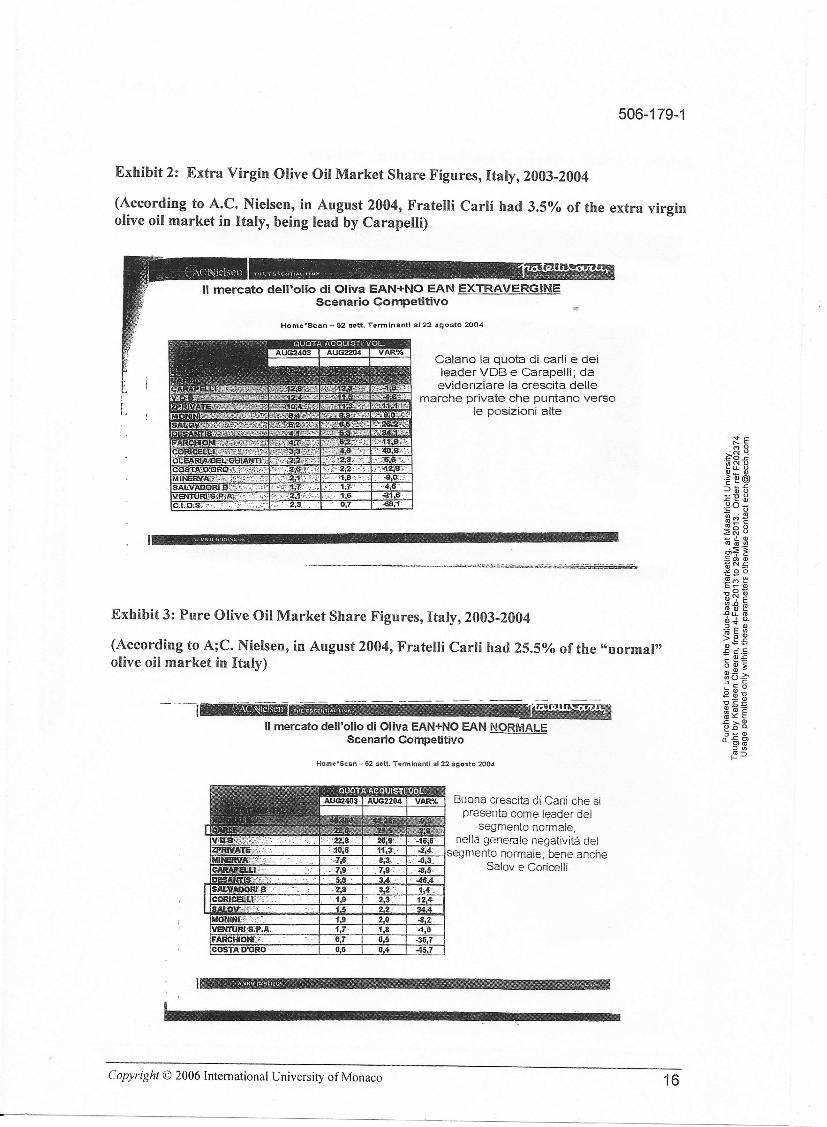

According to EU standards, to qualify as "extra virgin olive oil", an oil's acidity level couldnot go beyond the maximum legal limit of 1%. Fratelli Carli extra virgin olive oil had anacidity level that was consistently less that 0.3%; this was stated on the label of every bottle.Carli had 3.5% market share, which put it in ninth position. (See Exhibit 2 für Extra VirginOlive Oil market share figures) .

100% Pure Olive Oil (calIed Olio Carli)

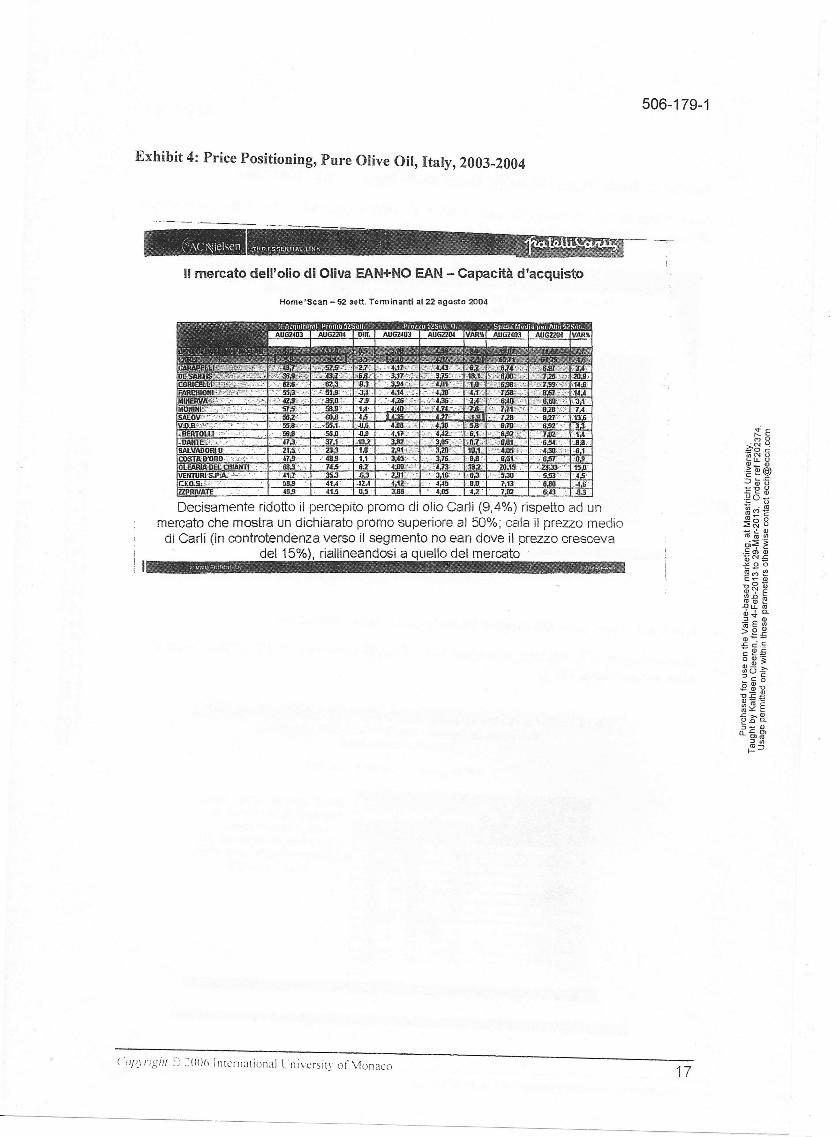

All brands of what is called "pure olive oil" are ablend of extra virgin or virgin olive oil andrefined olive oil; however, many brands contain 5% or less extra virgin or virgin olive oil.Carli's olive oil onee again had less that 0.3% acidity, and contained not less that 25% extravirgin olive oil. Contrary to most other brands, Carli specified the blend proportions on everylabel of its pure olive oil. Carli's Pure Olive Oil -simply called Olio Carli in Italy-was thatcountry's best-selling pure olive oil, with 25% market share. It cost more than practicallyevery brand of Extra Virgin Olive Oil in Italy. (See Exhibit 3 für Pure Olive Oil marketshare figures; see Exhibit 4 für price positioning in the Pure Olive Oil market).

CUSTOMERS, DISTRIBUTION AND PRESENCE

By the new millennium, Fratelli Carli had about 800,000 to 900,000 customers in Italy. Thisrepresented about 9% of the total market for Extra Virgin Olive Oils and the Pure Olive Oilsin Italy

These Carli eustomers were typically over 35 years of age, with families, living in thecountryside or in small towns. The average yearly purchase per customer was around 140Euros, with 35% of the customers representing 70% of turnover; Carli considered itscustomers to be very loyal to the brand. Ten times a year it would send its customers the Carlieatalogue. The company produced this catalogue in-house, and thanks to its significantinvestments in typography had what it called its own " printing factory" on site.

(uP) nghl S ::OO()International Lnivcrsity ol \lonaco 5

506-179-1

Customers could either phone in their orders, mail them, or use the Carli Web site. Sixtypercent of all orders were taken through the call centre, which was open from 8AM to 8PM,five days a week. Only 8% of orders were placed via the Internet. Once the order was taken -for free delivery a minimum order of six litres was necessary, otherwise there was a five eurodelivery charge=and then processed by the company's data centre, the oil would be packedand shipped from Imperia to distribution points throughout Italy; this network was composedof about 30 sorting points; from there, the orders would be picked up by horne delivery

-specialists, who would deliver the merchandise directly to customers' hornes in trucks ownedby Carli, and decorated with the company's trademarks and colours. (See Exhibit 5 for anillustration of the first Carli trucks, dating from the 1960s, and the most recent version).

These Carli owned trucks, which numbered 130, were used for the entire logistical process,from the factory, to the sorting points, and finally to the end users. They served 30-40customers a day across Italy; every day about 5000 to 6000 orders were delivered. In general,the length between a customer's time of order and delivery was three to seven days. The 30%price premium that Carli charged for its oils incorporated the direct delivery charges.

Carli's direct to the customer ordering and delivery system had long been unique in Italy, andits top management always believed it was areal source of competitive advantage for thefamily run firm: on the one hand it allowed the firm not to be reliant on intermediaries; on theother, the direct system also gave the company the potential to establish elose relationshipswith its almost one million Italian customers. Fratelli Carli tried to reinforce this relationshipby regularly sending out welcome gifts and fidelity gifts selected by Mrs. Renata Carli. Also,because Carli customers traditionally informed the company of such major family events asmarriages and births, Carli also sent out gifts for these special occasions. It also sent out aquarterly magazine, as weil as an annual calendar to all elients.

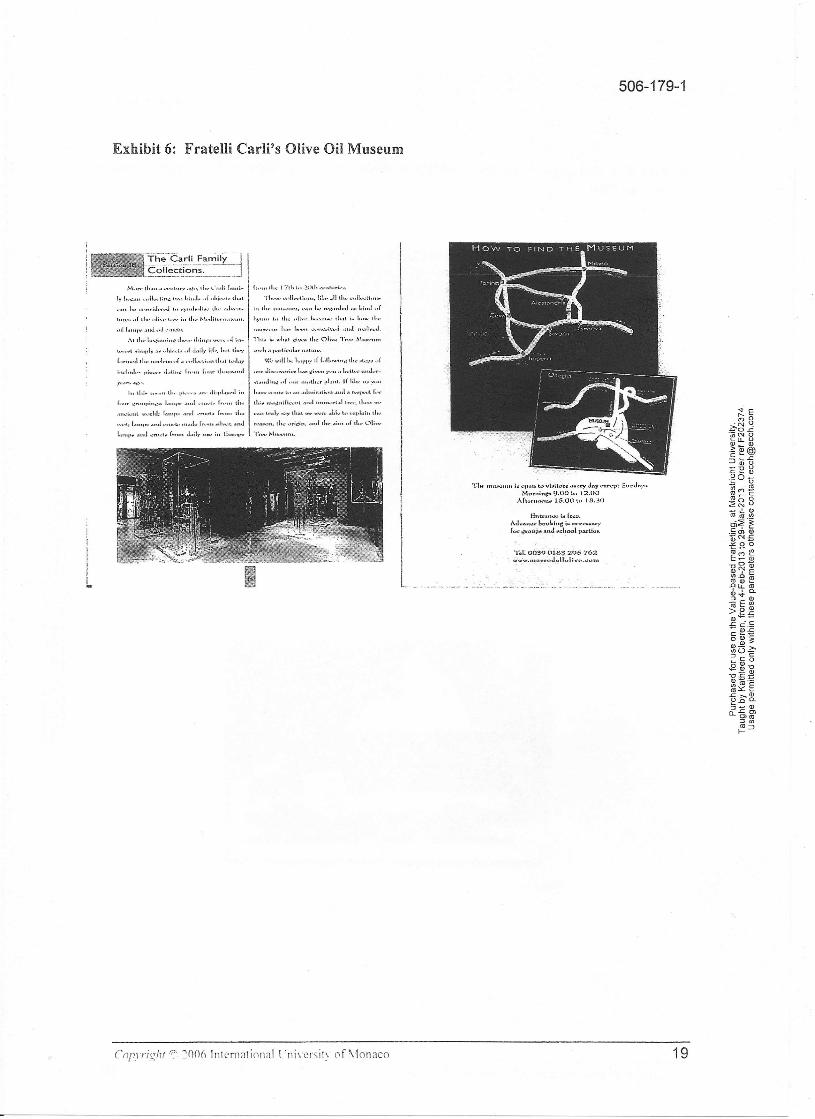

All told, a typical customer could expect to get something in themail from Fratelli Carli everymonth. The Carli brand became so synonymous with olive oil in Italy, that whenever theCarlis went to a hotel or restaurant, they would immediately be asked whether they were partofthe olive oil company. This association was further reinforced by the creation ofthe FratelliCarli Museum ofthe Olive, in Imperia. In 1993, it was given the European Museum Award asone of the most innovative museums on the Continent, and attracted 30,000 visitors a year.The idea for the museum came from Mr. Carli's father, who had over the years accumulatedan impressive collection of amphorae and oil jars as weil as other items related to olives andolive oi!. (See Exhibit 6 for images ofthe museum).

Households by far made up the bulk of Carli's customer base. However, the company alsosold to some top-notch restaurants. Entering the restaurant, cafe and hotel business on a largerscale was difficult however for Carli, since most firms selling to such establishments offered afull range of comestibles, such as coffee, sugar, salt, milk, etc., as weil as olive oil.

GROWING THE FRATELLI CARLI BRAND

Growth Through Product Diversification

The company's first product diversification was back in 1925, when it launched an olive oilbased soap. It wouldn't be until the 1960s however that Fratelli Carli embarked on a concertedeffort to diversify its product line. In 1964, the company launched its branded version of

Copyright © 2006 International University ofMonaco 6

506-179-1

Marsala. Thereafter, especially after the appointment of Gianfranco Carli as CEO in 1988, theolive oil based product line would be extended on a fairly regular basis, as shown below:

1925:1971 :1974:1981 :1983:1984:1996:1998:2003:

household soapvinegartoiletry soapextra virgin olive oiltuna fishpickled olivesred and white winesLinea Mediterranea cosmetics linetwo new types of olive oil launched: one called "Deciso", basically meaning"with more savour", and DOP olive oil (similar to AOC denominations inFrance), signifying that it came from a controlled and designated area ofproduction, and entirely made from Italian olives.

Notwithstanding this diversification, by 2005 almost three quarters of Fratelli Carli's turnoverstill stemmed from olive oil, as shown below:

Olive oil + extra virgin + aromatic oils 74%Tuna fish 10%Cosmetics (250 different products) 4.4%Pesto (basil and garlic sauce) 4%Vinegar 2%

With the remainder coming from pickled olives, wines, and soaps.

Growth Through Marker Expansion

Fratelli Carli also took its brand outside of Italy, going first to France in 1998 (but selling onlyin Paris and the neighbouring He de France). France was selected as the first "international"market for several reasons: the French consumer was considered similar in many ways to theItalians, both in their diets and eating habits (especially the case in Southern France), as weilas because of the steady growth in olive oil consumption in France. It was also a neighbouringcountry, and one the Carli family enjoyed visiting: several members of the Carli family spokefluent French. Despite the abundance of local competitors in France, and what it generallyperceived to be "nationalistic" preferences in France, Fratelli Carli broke even after fouryears.

In 2001, the company also decided to enter the German market. Several factors led to thisdecision: Germany had one of the highest rates of mailorder purchasing in Europe-theaverage German consumer purchased ten times as much through this channel than did theaverage Italian; Germany was a large market, and one where the consumption of olive oil wasincreasing; and, finally, because so many Germans spent their holidays in Italy, there was agrowing acceptance and interest amongst Germans in all things Italian, especially when itcame to food.

Copyright co 2006 International Univcrsity of Monaco 7

506~179-1

The Growing Market for Olive Oil

Olive oil was increasingly being praised in the international press, and even substantiated bystill scant yet growing scientific evidence, for its health and especially cardiovascular benefits.This was no doubt one of the reasons for the spurt in sales of olive oil in one of the largest--yet still untapped in tenns of olive oil consumption=rnarkets in the world, the United States.Between 1996 and 2002, sales of imported olive oil there doubled, from 1.2 billion litres to2.4 billion litres; between 2003 and 2004 alone sales of olive oil had increased by 16%, to$540 million; and olive oil imports from the Mediterranean region specifically had balloonedfrom64 million pounds in 1982, to 473 million pounds in 2003.2 Worldwide, growth ofoliveoil consumption was growing by about 4%.

Significant as it seemed, the American consumption of olive oil was only about .56 litres perpersonlyear, compared to the European consumption, wh ich ranged from 1.3 litres to 26 litresof oil per person per year, the case in parts of Greece.3 In Italy, the average consumption was11 to 12 litres per person per year.

The potential, and the trend in the US, amongst other countries, would no doubt acceleratefollowing the late 2004 decision of the influential Food and Drug Administration (FDA) toallow producers of olive oil, as weil as of foods containing olive oil, to tout on their labels andpackaging that the consumption of olive oil reduced the risk of coronary disease.4 Uni lever,which owned Bertoli Olive Oil, immediately forecast a significant increase in sales of thebrand as a result of this decision.'

In Italy as weil, 2004 saw a substantial increase in the consumption of olive oil: in the firstquarter of 2004 orders for Extra Virgin Olive rose by 20% year-on-year; orders for pure oliveoil increased by 26% year-on-year; while oil exports fell by 10%. And according to the Italianassociation of the oil production industry, Assitol, those brands unable to meet the increasingnumber of orders in Italy and from abroad faced many difficulties which could ultimatelyhave an effect on the entire oil production sector in Italy."

At the same time, both to meet and fuel the new sources of international demand, a newsupplier of olive oil emerged in the Pacific: notably, from Australia. In 2004, a milestone wasreached when one Australian olive oil producer sold 48,000 litres of its oil to Italy.'

In early 2005, Fratelli Carli was still deliberating whether it should pursue expansion intoother countries. It also continued to try to find new customers in Italy for its olive oil byincreased presence in leading fairs and exhibitions, such as SANA (the InternationalExhibition ofNatural Nutrition, Health and Environment) held in Bologna.

2 "US Expert Tips Olive Oil Market", The Australian Countryman, 25 November 20043 "US Expert Tips Olive Oil Market", The Australian Countryman, 25 November 20044 Zamiska, N. "Olive Oil Can Tout Heart Benefits", Wall Street Journal, 2 November 20045 Zamiska, N. "Olive Oil Can Tout Heart Benefits", Wall Street Journal, 2 November 20046 "Extra Virgin Olive Oil Orders in Italy Up 20% in Three Months", ANSA English Corporate News Service, 17May 20047 "Olive Oil to Italy a Milestone", The Australian Countryman, I July 2004

Copyright © 2006 International University ofMonaco 8

506-179-1

CHANGES ON THE HORIZON?

At the beginning of the new millennium, Gianfranco Carli believed that his firm's directmodel for the sale of olive oil in Italy was still valid, although he admitted it might becomemore difficult to profitably sustain into the future given changes in the market and competitiveenvironments.

Between 2000 and 2005, for instance, telemarketing in Italy had really taken off, with moreand more customers opting for this method of purchase, and ever more suppliers developingthe technological and logistical infrastructure to deliver accordingly. While this transitionbenefited Carli, it was an especial boon for competitors who had never before used thischannel.

In particular, many small olive oil producers and sellers in Italy began telemarketing activitiesin the first years of the new millennium; their prices were lower than Carli's for the productand for direct delivery. Additionally, thanks to the growth of Internet usage, manysupermarkets in Italy also began offering horne deliveries. Carli did not perceive thisparticular trend to be a threat since the large supermarket chains sold primarily to peopleliving in the larger cities-a segment which did not feature in Carli's core customer base.Moreover, customers of the supermarkets' Internet sites were primarily single, youngerpeople.

In 2004, Gianfranco Carli began studying the possibility of using different kinds ofdistribution channels to reach customers in those regions where the Carli brand was not sostrong, such as in eastern and southern Italy. (See Exhibit 7 für a breakdown of regionaland channel olive oil sales in Italy)

A NEW FACE FOR FRA TELLI CARLI?

While considering these competitive, technological, and market changes, Gianfranco Carligrew more and convinced that real and long term growth for his firm could only come fromproducts other than olive oil. And in particular, he had high expectations for the success ofFratelli Carli's cosmetics line that had been launched in 1997. The idea to diversify intocosmetics was the result of a conversation his wife, Renata Carli, had had with anacquaintance who was a researcher in a laboratory in Milan. It was possible, she learned, toproduce cosmetics from olive oil. And so the idea began. It seemed on the surface like aperfect fit: from time immemorial, Mediterranean women had applied olive oil as a skin andbeauty aid, and more recently some of toiletry and cosmetic giants had also begun using oliveoil as an ingredient in some of their products.

A New Role for Olive Oil: Beauty

The use of olive oil as an ingredient in cosmetics had been gaining increasing recognitionsince the late 1990s. One of the better-known producers and retailers of olive oil basedcosmetics, as weil as other natural and plant based cosmetics, was France's "L'Occitane"chain, which by 2005 had outlets the world over. Another venture created by the founder of"L'Occitane", Olivier Baussan, called "L'Olivier & Co.", stocked "all things olive oil", from

("o{J)liglll ':::~O()(, lntcmational tnivcrsity of x lonaco 9

506-179-1

25 vintage oils produced all over the Mediterranean, to vinegars, pesto sauces, and olive oilbased body, hair, and face care. This chain too rapidly expanded across Europe and the US.8

Yet another olive oil based cosmetics venture, which had grown rapidly since it was launchedin 1998, was "Cali Cosmetics". A joint venture between the Italian Baroness Consuelo Cali-whose family had owned a once weil known spa outside Rome called the Beauty Farm, whichshe had managed for ten years-- and an American businessman, the idea behind the venturewas to launch a line of beauty products based almost exclusively on olive oil extracts. Manyof these beauty treatments were "old family recipes" traditionally used in the Beauty Farm, Inthe US, there appeared to be a rapid take-up of the concept, with such large retailers asSephora and Nordstrom, as weil as smaller beauty boutiques, stocking the range. It was evenreported that such celebrities as Catherine Zeta-Jones, Sandra Bullock, and Joan Collins werefans ofthe brand.9

By 2002, Cali Cosmetics had grown better than expected and had about 25 stock keepingunits. The Baroness and her partner were now planning to open aseries of spas in the US, andthen later worldwide, offering beauty treatments, massage therapy -and lunch!--based onolive oil. The aim, according to the Baroness, was to provide a lifestyle experience, with oliveoil as the source. 10 While her partner managed the US office, she returned to Italy to head upItalian and European operations out of Milan.

Although "L'Occitane", "L'Olivier & Co.", and "Cali Cosmetics" were the cosmetics linesmost strongly associated with olive oil, by 2000 other manufacturers also started offeringolive oil based products, for instance: Amazing Grace, a perfumed olive oil body scrub fromPhilosophy; O-live a Little, a hand and body lotion from Bibo; The Olive Leaf line from TheThymes; and From Baudelaire, the Jardin de l'Olivier collection.!' Similarly there was apush towards natural ingredients generally speaking with the international success ofventures such as "The Body Shop".

FRA TELLI CARLI'S "LINEA MEDITERRANEA"

In 1997, Fratelli Carli launched eight olive oil based beauty products -including day andnight face creams, body oils, hand cream, and shower and bath gels-which it promotedthrough an annex to the olive oil catalogue sent to its existing customers. This new productline was called Linea Mediterranea. According to Mr. Carli, the brand Linea Med was to beclosely associated with nature and with innovation, with its core value built on the notion ofsuperior product quality. Fratelli Carli did not actually make the product line, but insteadoutsourced the production to several manufacturers in Milan who also worked for othercosmetics brands (one of them was the world' s largest manufacturer, who sold its products tothe leading international cosmetics companies, who then branded them accordingly).

Lucio Carli, the CEO's cousin, was appointed to manage this new activity. Lucio Carli hadbeen working in the family finn since 1990, first in the olive oil production facility (he had anengineering degree in food chemistry) and then rotating from one department to another every

8 Lane, M. "Olives Unlimited", The New York Times, 17 August 20009 "An Ancient Italian Recipe for Success", European Cosmetics Market, 1 November 200210 Chiaccio, c., "Cali Cosmetics Oliva Line Branches Out", Women's Wear Daily, 20 October 200011 Patteson, 1. "Beauty Tips from the Gladiators: Olive Oil is being Worked Into New Cosmetics", The TorontoStar, 26 July 2001

Copyright © 2006 International University of Monaco 10

506-179-1

two years so as to truly get to know all aspects of thecompany. In 1997, his uncle made hirnresponsible for the Internet site as weIl as for the cosmetics line.

In 2001, as a result of customer feedback and especially due to a drop in the number of newcustomers, management decided to totally revamp its strategy for Linea Med, specificallypositioning the brand now as "natural" yet with a strong element of feminine beauty andseduction. This, according to Lucio Carli, was really the serious launch of the brand. One ofthe outcomes of this repositioning was new packaging and, especiaIly, a new logo for the line.(See Exhibit 8 for these logos). The earlier association with Fratelli Carli on the packagingand advertisements was diminished; henceforth, there was no explicit.sendorsement madebetween the Frate Ili Carli brand, and the Linea Mediterranea brand. (See Exhibit 9· forrepresentative Linea Med catalogues pages). A beauty magazine was also launched, both inprint and on the Web, providing information, advice, and makeup tips. (See Exhibit 10 (a)for examples from the print version, and Exhibit 10 (b) for the Internet version).

In 2003, the company launched an intensive print advertising campaign in Italian magazines.There were several objectives for these campaigns-to build brand awareness as well provideproduct and channel information. (See Exhibits 11 (a) through (d) for examples of theseads)

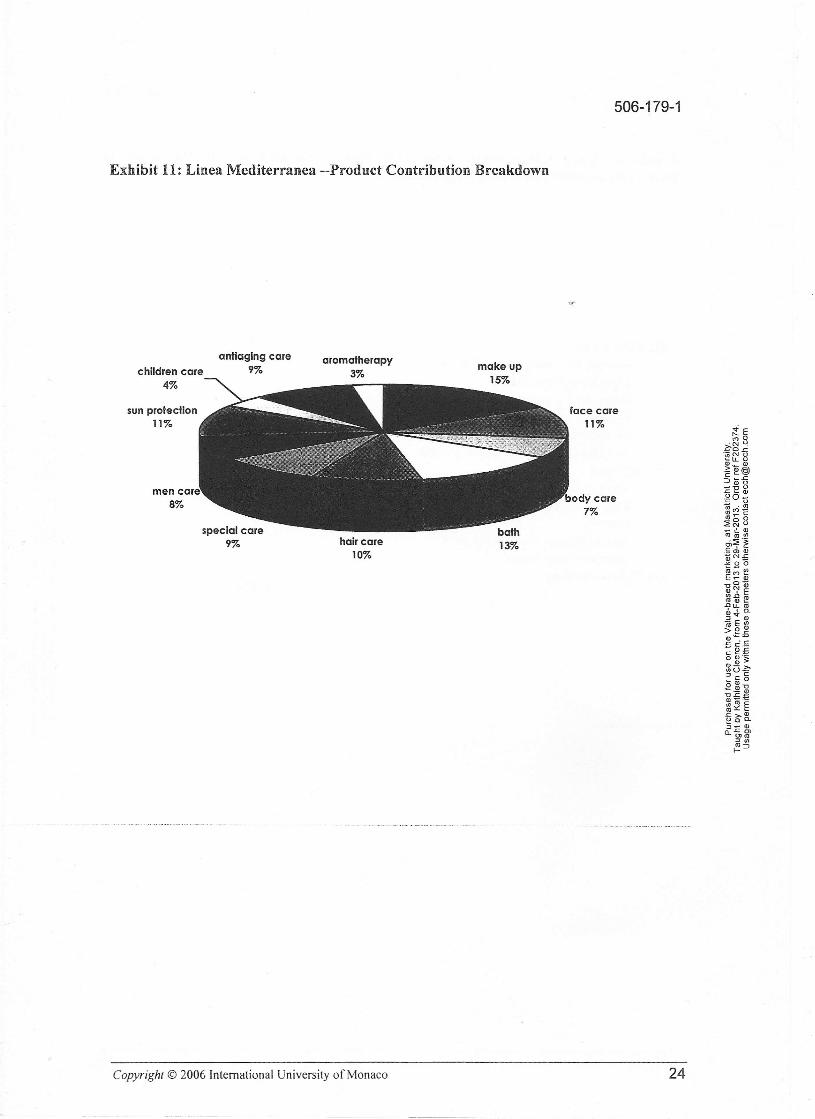

By 2005, the Linea Mediterranea line had 250 products in total. New products-- skin care, ha ircare, and body care lines for women as weIl as men, with sub-line products aimed specificallyat, for instance, young people, aging women, seniors, etc. -had been introduced on a regularbasis. (See Exhibit 12 for a breakdown of the cosmetic product market in Italy; seeExhibit 13 for a breakdown of contributions frorn Linea Med's different products), Ageneral catalogue of these products existed, as too did a specific one for infants, and one forseniors.

According to Lucio Carli, this continuous product development and promotion posed adifficult transition for the company. He explained:

"Cosmetics is a very fast moving industry; and it 's getting faster every day: it 's not atall like olive oill To succeed in cosmetics you have to create desires, and to do thatyou have to constantly launch new products. This is not something Fratelli Carli isused to doing=their view of business is very different. It takes a lot of time and energyto convince the other family members and employees that this is a whole new way ofworking. We 're fighting with them all the time, trying to get them to see andunderstand this!"

"Sometimes Ilike to remind my family about Nivea. It was also born in 1911. Andfordecades nothing ever changed about Nivea cream-same old blue box. Untiljive yearsago, when all of a sudden they realised that they needed to change if they were goingto survive. And, now? Now even Nivea is launehing new products evelY six months!"

Competitors, Channels and Customers

In the skincare market, Carli followed the trends set by such giants as L'Oreal and others; forinstance, they were planning to soon launch what they ca lied a revolutionary Botox skinlifting product; several of the major players had recently launched their own versions of sucha product. However, according to Mr. Carli, the line's key competitors were not the giants but

Copyright <0 2006 International University of Monaco 11

506-179-1

rather brands like Clinique, Biothenn and Clarins, all of which he saw as being associatedwith healthy, natural, innovative products.

For hirn, Cali Cosmetics was too focused on the US market, and therefore not really acompetitor. L'Occitane was weil known in France, he conceded, but not so weil known inSpain or elsewhere; another L'Occitane weakness in his view was that it launched very fewtruly "new" products-something he considered essential for success in the cosmeticsindustry-and thus did not really have a sophisticated, cutting edge image in skin and beauty,."products. L'Occitane was, in the end according to Carli, a gift and soap shop; it was not acosmetics company offering sophisticated products to solve beauty problems. As he put it,"No one buys L'Occitane products for themselves: they buy them as gifts."

As with its olive oil, Carli distributed its cosmetics directly to customers in Italy, who madetheir orders based on a catalogue, or via the Web site-although similarly to olive oilpurchases, very few purchased over the Web. (See Exhibit 14 for a breakdown ofdistribution networks for cosmetic products in Italy).

Nonetheless, the Internet site was a successful vehicle to capture customer feedback andsuggestions, and many of the ideas customers submitted were subsequently incorporatedsuccessfully into new products. Whenever the cosmetics line was presented in fairs,management reported a great deal of interest on the part of consumers.

Although Fratelli Carli's CRM program would only be operational in two years time, andtherefore management believed the market still couldn't be effectively segmented, they didhave some ideas as to who these customers should be. Lucio Carli and his team called them"The Sophisticates". These were women aged between 25 and 44, living primarily in thenorthern central part of Italy, who had a high level of education and an "interesting" socio-economic profile. Their lifestyle could be characterised primarily by the notion of"understatement": elegant, classy, and natural. These women consumed more than the averageamount of cosmetics, and were as focused on brand image, as on price. More than anythingelse, these women looked for practicality and simplicity when it came to their purchases.

More generally, they saw their potential buyers fall into two spheres: the very weaIthy, andless affluent who nonetheless desired quality products. The value proposition offered by LineaMediterranea - high quality products of the sort stocked in perfumeries and not insupennarkets, at the lowest possible price-was believed to hold equal appeal to both groups.

By the end of 2004, Linea Mediterranea was profitable in ltaly, with 80% of its purchasersalso Fratelli Carli Olive Oil customers. (See Exhibit 15 (a) for growth in LM customerfigures in Italy; see Exhibit 15(b) for revenue figures).

The Spanish Gambit

In 200 I, Lucio Carli decided to have some marketing research done in Spain. The countrywas a dynamic, young, and growing market and seemed to offer some potential for growth.Carli's aim for the research was twofold: to evaluate the possibility of success for an Italian,olive oil based cosmetics brand in the Spanish market; and to weigh the positioning optionssuch a brand could carve out for itself in an already crowded space.

Copyright © 2006 International University of Monaco 12

506-179-1

As for the first point, the initial results seemed prormsmg, with customers apparentlyaccepting a propostnon based on the following positive image criteria: olive oil and thebenefits generally associated with it; Italian brands, Italian style, Italian origins (Italian brandsranging from Dolce & Gabbana to Valentino were highly appreciated in Spain); and sharedMediterranean values between the Spanish and ltalian peoples and cultures.

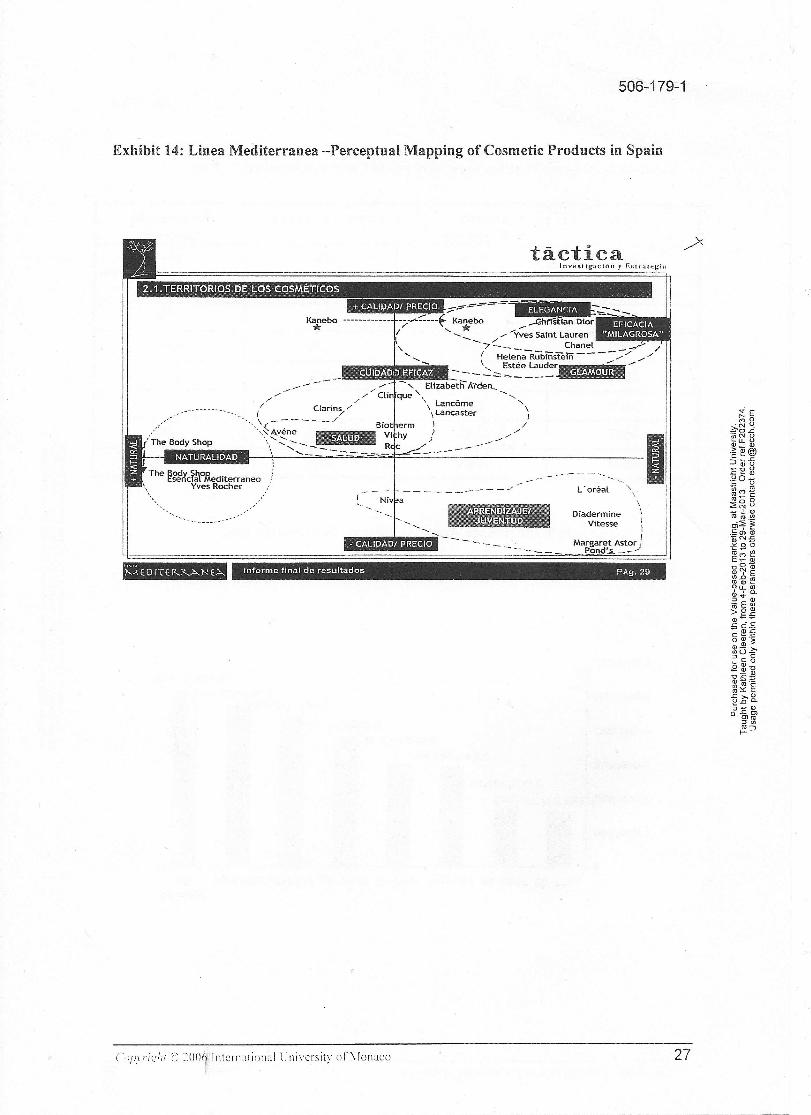

In terms of the other objective of the market research, it appeared that there could be a gapthat Linea Mediterranea could fill in the Spanish cosmetics market (See Exhibit 16 for aperceptual mapping of cosmetics brands in Spain derived from the market research)

Based on these findings, Lucio Carli decided to launch Linea Mediterranea in Spain in 1999,beginning only with face care products. He created a distribution company, and hired twoprofessionals-taking one from Lancome, and the other from Lancaster=-to organize andmanage the brand's Spanish activities. Their overriding target was to make the brand availablein the medium to high range perfumeries throughout Spain. Specifically, in five years time aturnover of six million Euros was expected, based on rapid and substantial growth of salespoints for the Linea Med line.

By the end of 2004, the brand could be found in over 400 sales points across Spain, both insuch international and pan-European retailers as Sephora and Marrionnaud, as weil as inleading Spanish perfumeries like Gilgo, Prieto and Valenci; Linea Med had achieved half amillion Euros in sales, and forecast sales of 1.4 million Euros by end 2005.

The brand had the same price positioning as weil as market positioning as Clarins. Carlidecided to rely more on PR than on advertising for promotion, and participated in numerousco-rnarketing activities with its selected distributors. Carli was also negotiating with EI CorteIngles-Spain's leading department store, equivalent to France's Galeries Lafayette orEngland's Harrods-to become a sales point.

By early 2005. Lucio Carli and his staff could state that they were more than pleased with theresults from Spain so far:

"For us, Spain is not just a pilot market. It is a kind oJ laboratory. And based on whatwe see developing in this laboratory, we will decide where else to take the brand, andhow quickly. "

"And so far, we are very happy with the results in the market. "

All told, by the beginning of 2005 sales of Linea Mediterrenea in Italy and Spain representedalmost 5% of all Fratelli Carli sales.

LOOKING INTO THE FUTURE

Fratelli Carli would soon be marking its centenary, and Gianfranco Carli had to decide whereto put his resources, energy, and focus for the future. Now, as he perused the overall financialresults for the company, and in particular those for Linea Mediterranea, he knew that optionshad to be weighed, and choices made. In Italy, Linea Mediterranea was profitable, althoughadmittedly cosmetics did bring in stronger margins than olive oil.

13

506-179-1

In terms of its core offering, Fratelli Carli's tumover has decreased over the last few years,and some in the company worried that it might become more difficult for the Fratelli Carlibrand to retain its position, and premiums, into the future.

As for the cosmetics industry, he knew it was highly competitive, but believed that the nichestrategy followed by Linea Mediterranea- cosmetic products with olive oil-would give theline a distinct edge in the crowded beauty care market. So far at least, the results from Spainseemed to confirm his assumptions.

But ifthe cosmetics option were to be pursued aggressively, would Fratelli Carli have to adaptits business and distribution models? If so, how? And did it have the right infrastructure andskills to do this effectively? And what about the role of its corporate brand: in Italy, the equityassociated with the Fratelli Carli brand was strong. What were the dominant characteristics ofthis brand identity, and should Carli try to leverage them into cosmetics, and perhaps eveninto other market spaces?

And, as Lucio Carli never tired of reminding the company's top management, did the familyfirm have the right culture to pull it through into this new venture-or would it instead hold itback and slow it down in an environment where speed, adaptability, creativity and continuousinnovation were necessary?

Or, perhaps there were other still growth options Fratelli Carli could consider to see it throughits second hundred years?

Copyright © 2006 International University ofMonaco 14

506-179-1

Exhibit 1: Illustration of the Fratelli Carli Olive Oil Glass Bottles

Copyright © 2006 International University ofMonaco 15

506-179-1

Exhibit 2: Extra Virgin Olive Oil Market Share Figures, Italy, 2003-2004

(According to A.C. Nielsen, in August 2004, Fratelli Carli had 3.5% of the extra virginolive oil market in Italy, being lead by Carapelli)

11mercato dell'olio di Oliva EAN+NO EAN EXTRAVERGINEScenario Competitivo

Hc me=Bc an - 52 sott. Terminsntl al22 agosto 2004

Calano la quota di carli e deileader VOB e Carapelli; daevidenziare la erescita delle

marche private ehe puntano versole posizioni alte

. .~:-...•.• vsn 1I1',\'~l ~.

Exhibit 3: Pure Olive Oil Market Share Figures, Italy, 2003-2004

(According to A;C. Nielsen, in August 2004, Fratelli Carli had 25.5% of the "normal"olive oil market in Italy)

-'-1--' --- ---.. - - - -·--.~r'1mpw••'9"WP12'P"M'j = .. 1 i _ C ~

11mercato dell'olio di Oliva EAN+NO EAN NORMALEScenario Competitivo

Hom(!'Scan - 52 sott. Tonnlnantl al 22 3g0'5'to 2004

Buona ereseita di Carii ehe sipresenta eome leader dei

segmento normale,nella generale negativita dei

-::-:'-"--,-:--:-:f,.,--:~,-,-t-~p--+~;:-:---,seg menta normale; bene ancheSalov e Coricelli

-821,7-.O~7 -36,7

COSTAD'ORO 06 4S.7

Copyright © 20061ntemational University ofMonaco 16

506-179-1

Exhibit 4: Price Positioning, Pure Olive Oil, Italy, 2003-2004

.._-.-._---.'

.' , C\C~iebcl1!.

11mercato dell'olio di Oliva EAN+NO EAN - Capacita d'acquisto

Home'Scan - 52 sett. Tonnlnanti al 22 agosto 2004

Decisamente ridotto il percepito promo di olio Carli (9,4%) rispetto ac! unmercato ehe mostra un dichiarato promo superiore al 50%; cala il prezzo medio

di Carli (in controtendenza verso il segmente no ean dove il prezzo crescevadei 15%), riallineandosi a quello dei mercato

(oP.lr:gll/:=: ~n()() lntcmuuonal Lniversily ofvlonaco17

506-179-1

Exhibit 5: Illustration ofthe first Carli truck, dating from the 1960s, and the most recentversion in 2004

Copyright © 2006 International University ofMonaco 18

Exhibit 6: Fratelli Carli's Olive Oil Museum

~~TI~~~~in;~~~~I.\.\•••.•..,1..,,,.,,.•·"tt.rv .•\!••, .1••·~:.,~Iir.••"i- h"I" 11,,, 1711 • .,.2thl, ,,~.,,!•••.i.·,..

I.••I••~." ••. "" •..•.•;,,.! h•••, Li".!" "r ,.I.;.-d •• lh,'l TI"""" ...·,.11•..•:1;••,,'" 1,[,,· .•11t1••....·••I1•..•.:ti ••" ••

,",,,' I•.•, ......••n ••iJ.·r •.•.1 (•••. y",l",li~,. LI••..•• 1•..•·,,_ i" t/ ••, ,,,,, •.•. ,,," • .:.". 1,., r•.~., •.J..J ".. ki ••.! "rt"rn •• ,r 11•••· •• Ii~" t ••.• · iu 11••• "h·,Ii'"rl·'''''"''''' \'v"", I •• d,e ,.Ii, .•.· I••.•..·.,,,•••.· 11•.•1 ,•• I",", !I ••·

"ili .••",,>, ""J •.,1.-,."",... ", ••,••."". I",~ I••.••" ,x "".".·<,· •.•1 .•oJ (l'.lli.""J .

.\, tI ••...l ••.~i.",;"..: 11".".· 11,;",:., ,....,••· ••f i,,- TI" •• i••,,·1•••, ~iv",' 11,." (;.Ii"", TI..,.- M"~""I1'"

1.,•.•",1 /O;",,,ly .", •• 1,;".;1.,;"r .1.,il}.li(.-. \",1 tI ••.y ••tI~·h., p.lr1in,l"r .,,\lu ••.·,

r..~"•..J 11". ""~·I<·t,,••• f .••.•• 11•.•.·1;•• 11t!, .•1 h ••I••y \'(',•••••111••..1•.".1' .•••,r f ••I1,,,,,,·i,,~tll~' ~t"I'".,1

;•••:I".I.·~ 1"",-"..,. .1..1••••.• (,-,.". (''''1' ~I" ••••••" ••I ••,,~ Ji-: ••~·"ri,·..I, .•••~i-. ••Y'••••• 1••.·U~·r 'lOul •.·r-

.•t. •••~I;".: .,r ." .• n•••d ••..~ 1,1.•••1. If 1.1••. "'" Y''''

1•• tI,i~ n••••••11••· 1';•......•.•" .• I;~I'I.•.•••.•I i.. I" •••.•••.•"n••t •••• n ."1" ••,,.•\;. •••.•• ,,1.1 r~·"l'•..•.,1 ("1'

[••"r ..:n'",';"""" 1.••.,••" .••••1 .·r.,..I .• (,.",,, 11." 11,;" tI ••• ,.!"ifk,·nl .",,1 i""".,,.t .•II •.•.••.·.II,,, ••••.•..

""~'icHI ••.•.'rIJ; I.,,,•••.•.,,,.1 .·n ••.t .•• (n"" 11... 0.:,'" l".lr ":':-'11•••, \W' ••,,"' .J.I•.•tu ,.••••1.,;" \I".~·.,,.tl I.••••,••..••.•I.·•.•••.L. ", .••k· fr •••••••• 1_·1'•.•••• 1 n.·ol••''''. rl ••.· ,'rici ••.• ,n,III,,· .•ion ••r 11,•.· .;,...•1••.•.,1.•••• 1•••••• ,,1 .:nl"''' (•.•••••J .•il) •••• " iu I.: ••••• "••., 'rn .•' i\-\".,.. .•'n•.

t

l

506-179-1

'1'1"1 "', ••..,,,,,. l" '''I!lUt 1:0'Yi"l!..ar!l' e •••<"..)' Jny •.·,U.••.·pl' SunJ"",,, ..M"rllin~ 9.00 t •.• 12.0{)

Ah •.••.Il•••,U. 15.00 h. 18.30

Entll'lInuu I••{n:u.

AJIfAII"'" bOQblll~ i•.1U."CUo' •••••• yf.•.•l'..:roup. ••nd ..clu'Iol[l.1l!lic ••.

141: 009<;1 orss 296 762.;;.•i••••.•,,'\~.J:oJ~liuli_v<:o.C'unt

('nplrighr0 ~()()(i lntcrnational I 'niversitv of vlonaco 19

506-179-1

Exhibit 7: Regional and Channel Sales of Olive Oil in Italy

11mercato dell'olio di Oliva 52 weeksHome'Scan - 52 seit. Terminanti al 22 aqosto 2004

Nella generale neqativita, spicca I'ottima performance dell'area 4,in termini di volumi, malgrado il calo di penetrazione; stabili i volumiweicolati

dalla grande distribuzione

I Acaulstl 52S,Gtt. Q.

Var% Var%AUG2403 AUG2204 04 vs03 AUG2403 AUG2204 04vs03

~~-.LJ.~;;-L!Y~~::C·..r~:-:~~,:.::::;}:t6~w~rAREA1 22,0 20,7 ·7,9 5,319:898 5.205.435 -2,2AREA2 170 16,4 -5,6 3.476:379 3.355.757 -3,2AREA3 24.9 23,8 -5,4 3.732.164 3.721.406 -o.aAREA4 36,2 39,1 6,3 4.512.1184 4.474.956 -o.aSUPERMERCATI + IPERMERCATI 47,4 48,5 0,0 13.739.156 13;609.165 -o.sUBERI SERVIZI 3,1 2.8 -12.6 1:598;1160' 1.473,608 -7,7DISCOUNTS 3,6 3,8 4,2 2.0'13.660 2.218.842. 10,2TOTALE.TRADI2JONAU AUMENTARI CONFEZ 28,8 27,1 -8,3- 5;;664.025 5.140.007 -7,6CASH & CARRY I GROSSISTA I SPACCIO PROD 3,4 3,2 -7,3 451".128 458.260 1,6AMSUUNTl 1,5 2,3 52.6 440.570 426.540 -3,2PRODUZIONE PROPRIA 12,2 12,2 ·2,3 1.379,106 1.256.834 -8,9

(Sales volumes per geographical areas in Italy showing the declines in sales except forthe South of Italy larea4)

Copyright © 2006 International University of Monaco 20

506-179-1

Exhibit 8: Linea Mediterranea Logos

LINEA

MED1TE~~ANEAI CO S"MET I C I Al PP-..lN Cl PI A TT I V I 0 EL L' 0 Ll 0 0 I 0 Ll VA

21

506-179-1

Exhibit 9: Representative Catalogue Pages, Linea Mediterranea

NUQva PromQzloneRagai01WVi iI betloss~ at

N~ov"i.~~otti.:~:;t-~.)-J.f I: ITI: t...•fI.... ••.•. " t Ä

Triltl<:Jmonlo contcrno I.abbrnlteee 100tl

.1mUQH1Q. ~-!l!'-lm.'..U<lmo~.crernu contorno ecent

tuMl$ml

l~t~r-bnH~ lI"'lif\lOllQ.....,."....

Pa'!!.!.1pretcutvalutl",l~l'l\l

'<tt;';<;OIj::it;<cl,~IO'U':lft\l:,.,ti~

KU 'J1Ji.O~''ilftHn('J• $(}"'Q~lI~

jW;f UI'ltr'\..l.~C!utltU.ln.sult:ato,<1Ip<:CC.,)!).'!<I~

Copyright © 2006 International University of Monaco 22

506-179-1

Exhibit 10 (a): Linea Mediterranea, Representative Pages from the Beauty MagazineSent to Customers

J•~;' ..,.";)

_"'" ••.•• '."d'~"f'oo •••~'" "'_"'~'''''''-' •• ..,...,.· ••••• <'"I ••••• ..-~.

...,.,...........•;

Exhibit 10 (b): Linea Mediterranea, Internet Beauty Magazine

~Ic."/lU Fh~,,".I,.,C'.fI,"~IUn.

el ,nl~" trn: •••• ..t•.t • N::Iu.•• LI,.. •.•• ,La1.:to!!lwl.Ft...cl ••,,"••.•(c-"h~

~ln'1:I=-C, S::t.:t..':OS'.Ul-f!UI. ,nd~u._~,~ UllH~O'1OH1fI ••

<hu!e .aU>ltf<'>'11 ,u..UIN.lb,..,.. ••11 4. ~rMI'\l1:' • 4;"u~11"O =.•4,1fa , •• ft '(~r.w.

b fUW d Il'.KGUlt Ku. rtt lqi

~;:::;~~~ l/'clt rllttibta .»~~~',p!c(,mjt1EmJi

"' rn(ntf !bunt

'I'fH!'~ '~UJ"1<Ih".ri~ ~.r1.~•.tI.• pu h\\v, Tran t.'"'~"!'.t1.~n.,.Q.('o,rt"'o'neto41u,,!d.A.-.cb.~IrdJ,,~.X' •• n*4.u:.411 •• r",t,.tW\ll'CI"~"'Ii~U cl, •.•"",••.". ~""""rj,,,,"h..,4<I.b. .•1u.~'t•••,••••.t UI ~-.. ~I , .•~

1~IrUIn.'afI"~'t'tI,u.u." 01=.~.-.

-•• " ••• - •••••••• 1.1 I"~

I•••••.•••·.~·~.- •••.•••. 1.,...4.1_ ••••••.•.•. _

,r •••••••••• -._" •. - ~ •.•.• ,., •••..•.--- •• <. ".- ••••••••• - ••• _-

__•••1.1:•••• _ •••••••••.;.. •••.•••.•.-..L_.>..c... ..•, •..•• '"'--" •..l.o.~\ •

••~••ul •.·.,•••.••.•I••.---.- ,.•...~,.~....•-' .•...~.•. ;..~...,...•. ~._-I"~_ .••••/"••- •.•..,.,. -.-...•~"'- _.._--I.~.._-.~.•,.•._.I""~'HI'4_ .....~.""_~••

_1·· ••••••••-01••.... ,......•.........••. _ •.....,.....•..•••..•*•••,.r """.II.t"MtA .u-4r ••

23

506-179-1

Exhibit 11: Linea Mediterranea --Product Contribution Breakdown

children care4%

antlaglng care9%

sun protectlon11%

face care11%

men care8%

halr care10%

Copyright © 2006 International University ofMonaco 24

506-179-1

Exhibit 12: Linea Mediterranea -Analysis of Direct Channel Cosmetics Purchasers inItaly (total number purchasers = 23, 162,00)

Via Catalogueswomen between ages of 18-24high school educationliving in the south, on the islands, orin towns with less than 10,000inhabitantshouseholds with at least 3 people

Via the Webwomen between the ages of 18 and 34high socio-economic and culturalleveluniversity graduate and post-graduate education

Via Telemarketing

2.8%

0.7%

0.9%

Source: Eurisko

Co/))nghl =: ~()(I() lntcrnauonal t.nivcrsity of~lonaco 25

506-179-1

Exhibit 13 (a): Linea Mediterranea -Growth in Customer Numbers in Italy

Year Existing FC New Customers Existing LMCustomers customers

1997 96% 4% 0%

1998 69% 7% 24%

1999 55% 7% 38%

2000 40% 12% 49%

2001 34% 14% 52%

2002 22% 8% 70%

2003 25% 12% 63%

2004 15% 12% 73%

Exhibit 13(b) Linea Mediterranea -Revenue Figures, Italy (Italian Lire)

6,000,0005,100,000.00

4,701,446.404,364,957.76

3,810,544.102,976,013.76

2,892,841.89

5,000,000

4,000,000

3,000,000

2,000,000:1.

1,000,000

o1997-98 1998-99 1999-00 2000-01 2001-02 2002-03 2003-04 HP

2004-05

Copyright © 2006 International University ofMonaco 26

506-179-1

Exhibit 14: Linea Mediterranea -Perceptual Mapping of Cosmetic Products in Spain

täctical n ve at igu c Iö n y EHlr;llc:gia

2.1. TERRITORIOS OE LOS COSMETICOS

Kanebo oooooooooooo••'\

<,

'-/' "Elizab';:~~:"':::: "'" - - - -IEl!llmi11

//-- /// Cli que '\ <,

Lancörne -,(" Ctarins.>" \ t.ancaster ;

'",,\(------/ Biat erm I /'-_" A.vene Vi I -"'-."'::--- ""]'\1'1"" ),/ I~!!~~~--_\t'__'~'~O=~~-~-~-~-~-~-~-=-~-~~~~~~-~-~-~-----------------------------·0·

Ii • . • _.--- ...•----

"- \\

Diadermine \Vitesse :

1'_ _ _ Margare;t Asta')--==-==----=- PaQJ:.I..s.__

CUIDADiJ EFICAZ

I

The ~Xc~~aß.editerraneaYves Rocher ___ ~ J

Niv a

• CALIDADI PRECIO

'ME0 IH I'..I'..ÄN EÄ lnforrne final de resultados Päg, 29

C'J/>lrig/]r er; 2()() lntcm.uional Lnivcrsitv of\lonaco 27