Frankfurt’s Changing Role in the European Financial …€™s Changing Role in the European...

24

1 Frankfurt’s Changing Role in the European Financial Center System – A Value Chain Approach to Financial Services – by Michael H. Grote * , Sofia Harrschar-Ehrnborg ** , Vivien Lo *** May 2000 * Goethe-University Frankfurt, Department of Economics ** Goethe-University Frankfurt, Wilhelm Merton-Chair of International Banking and Finance *** Goethe-University Frankfurt, Institute for Economic and Social Geography & DFG Special Research Program 403 ‘Competitive Advantage by Networking’ Abstract The main argument in this paper is that new information and communication technologies (ICT) in the financial industry will increase specialization and competition within the European financial center system and thereby lead to a ‘re-bundling’ of functions of the various financial centers. Frankfurt plays an interesting role in this development as it is one of the main development centers for ‘financial technology’. With these technologies, e.g. remote access to the Frankfurt stock exchange is now feasible from most European cities. This leads to a reduced need for physical presence, which opens up new possibilities for the financial sector’s spatial organization. However, as financial production is information- and knowledge-intensive, spatial and other types of proximity between financial actors and clients are still essential in many stages. We examine the value chains of three different products (advisory, lending, trading) with regard to different proximities, in order to identify possible patterns of their spatial (re)organization. From these findings, inferences are drawn for a ‘new’ role for Frankfurt in the European financial center system.

Transcript of Frankfurt’s Changing Role in the European Financial …€™s Changing Role in the European...

1

Frankfurt’s Changing Role in the European Financial Center System

– A Value Chain Approach to Financial Services –

byMichael H. Grote*, Sofia Harrschar-Ehrnborg**, Vivien Lo***

May 2000

* Goethe-University Frankfurt, Department of Economics** Goethe-University Frankfurt, Wilhelm Merton-Chair of International Banking and Finance

*** Goethe-University Frankfurt, Institute for Economic and Social Geography & DFG Special

Research Program 403 ‘Competitive Advantage by Networking’

Abstract

The main argument in this paper is that new information and communication technologies (ICT) in the

financial industry will increase specialization and competition within the European financial center

system and thereby lead to a ‘re-bundling’ of functions of the various financial centers. Frankfurt

plays an interesting role in this development as it is one of the main development centers for ‘financial

technology’. With these technologies, e.g. remote access to the Frankfurt stock exchange is now

feasible from most European cities. This leads to a reduced need for physical presence, which opens

up new possibilities for the financial sector’s spatial organization. However, as financial production is

information- and knowledge-intensive, spatial and other types of proximity between financial actors

and clients are still essential in many stages. We examine the value chains of three different products

(advisory, lending, trading) with regard to different proximities, in order to identify possible patterns

of their spatial (re)organization. From these findings, inferences are drawn for a ‘new’ role for

Frankfurt in the European financial center system.

2

‘Every cheapening of the means of communication,

every new facility for the free interchange of ideas between distant places

alters the action of the forces which tend to localise industries.’

Alfred Marshall

1 Introduction

Global economic integration has increased the flows of goods, information and capital whichare being guided to and from different regions around the world. These globe-spanning ac-tivities follow certain patterns which can be interpreted as networks where cities act as nodes.Except for a handful of ‘truly’ global cities, the rest are competing within subsystems of theworld economy, delimited by space, sector, culture etc. (Grasland and Jensen-Butler, 1997;Knox, 1995; Sassen, 1991). The scope of this paper is the subsystem of the Europeanfinancial center system with a particular focus on Frankfurt, the „premier German global city“(Friedmann, 1995, p. 35) and one of the main development centers for ‘financial technology’.The main argument in our paper is that new information and communication technologies(ICT) in the financial industry enable the splitting up of existing value chains, therebyincreasing specialization and competition within the European financial center system, whichcan lead to a ‘re-bundling’ of functions of the various financial centers. The assumptionbehind this is that financial centers will remain important, due to the need for proximity infinancial production, one of the main determinants of its spatial organization and theanalytical focus of this paper. Because financial services are too diverse for simplisticgeneralizations, we examine financial production on the basis of different value chains. Fromthis micro perspective we try to gather evidence for the macro perspective, i.e. changes in theEuropean financial center system and Frankfurt’s position in it. Although the hierarchy offinancial centers appears to be relatively stable over long periods of time, „(t)he sense ofpermanence of financial centers is one that often deceives“ (Budd, 1995, p. 354).

The remainder of this paper is organized as follows: After a brief introduction into the natureof financial centers, we introduce ‘financial technologies’ and examine the connectionbetween new ICT and the need for different types of proximity. These concepts are thenapplied to the value chains of three different financial products. From this analysisimplications for the spatial organization of the financial sector are drawn and in conclusion,applied to Frankfurt with regard to its position in the European financial center system.

2 Financial centers and financial technology

Studying financial centers raises the question of what a financial center actually is. A reviewof the existing literature is of little help, as there is little common ground on a definition.Following Kindleberger (1974), Reed (1981) and Rose (1994) we regard a financial center as

3

a) a location of important actors (mostly banks and stock exchanges, but also funds and otherfinancial services) and linked and supporting services for the financial sector, b) which servesas a point of origin and destination of financial flows, and c) acts as the control center for thedirection of these flows.

Financial centers, like other agglomerations, are the outcome of both centripetal and centrifu-gal forces. These “shape the the evolving geographies of domestic and global finance”(Martin 1999, p. 15; see also Martin 1994). In the case of financial production, centripetalforces are linked to labor market externalities, easy access to intermediate services,technological spillovers, informational spillovers and socio-institutional and cultural factors(Porteous, 1999). Centrifugal forces, on the other hand, are related to congestion, high rentsand other costs, the lack of local knowledge specific to other places and – provided that not allbanks are located in the same financial center – internal economies of scale and scope.Internal economies occur when individual banks gain from concentrating their activities inone place, usually their respective headquarters.

These forces operate at least on three levels:- firm level (relocation of departments between headquarter and other locations),- financial center level (relocation between financial center and periphery)- and financial center system level (relocation between different centers).

For the purpose of this paper, we concentrate on the first and third level, disregarding the sec-ond, thus taking into account solely the respective leading financial center in a country (asshown in table 1). Since the products we look at are almost exclusively produced in the majorfinancial centers, this abstraction can be done without harm for our analysis.

Table 1 gives an impression of the current European financial center system. The cities areranked by their number of branches or other types of representation of the Top 500-banks.

4

Table 1: European national financial centers

Group City Number ofTop 500 Banks

Group 1 London 201Group 2 Frankfurt 107

Paris 90Group 3 Milan 77

Madrid 75Luxembourg 67Brussels 63Zurich 53

Group 4 Amsterdam 40Geneva 40Vienna 32Warsaw 31

Group 5 Lisbon 26Prague 25Athens 24Stockholm 22Copenhagen 20Dublin 19Oslo 14Helsinki 11

Source: The Bankers’ Almanac (1998), Institutional Investor (1998), own calculations.

Interestingly, there is a clear ranking which also allows for the clustering of centers in groups.The table displays the top financial centers of 19 European countries. Only Switzerlandharbors two financial centers of similar importance, Zurich and Geneva, which is most likelydue to Swiss bilingualism. The European financial centers form a decentralized system,particularly in comparison to the United States which have a similar capital market size, butfewer financial centers. This difference becomes obvious when the numbers of stock andfutures exchanges are used as an indicator for the number of financial centres: whereas thereare 32 stock exchanges and 23 futures exchanges in Europe, there are only 8 stock and 7futures exchanges in the USA (Frankel 1996).

The spatial structure of financial centers has proved very stable over time. The top position inthe European financial center hierarchy has changed only three times in the last 500 years.Shifts in the financial center system have always occurred in connection to major political ortechnological changes (Harrschar-Ehrnborg, 1999). With Europe undergoing major politicaland technological changes at the moment, the question is how these will affect the financialcenter system. The most important effect of ICTs with regard to financial centers is that theyreduce the necessity of a presence on-site. This implies that they weaken the forces that havehitherto brought financial actors together in central places of the world economy.

The proximity to the stock exchange has always counted among the strongest determinantsfor the emergence of central places for financial transactions (Rose, 1994). Consequently, the

5

virtualization of stock exchanges, the change from ‘open outcry’-floor trading to computer-based, quote-driven market systems has made a lot of headlines. Some of the new tradingsystems allow for a remote access option, i.e. participation from anywhere in the world viacomputer terminal. This is leading to unprecedented competition between stock exchanges. InEurope, Frankfurt is at the forefront of these technological developments. The Frankfurt-based German Stock Exchange ‘Deutsche Börse’ has developed a spot-market tradingplatform for shares (Xetra) and together with the Swiss Stock Exchange a common tradingplatform for derivatives (Eurex). Both systems provide remote access facilities and areextremely successful in acquiring new participants in other (mostly European) countries. Bythe end of 1998, more than 60% of traders in the Eurex System were located outside Germany(Deutsche Börse AG, 1999).

The production of financial services is of course also influenced by other moderncommunication technologies such as E-mail or Internet. In many cases these technologieshave been further developed to suit the specific needs of communication in the financialindustry. An interesting example are secure web-based environments, that allow tocommunicate and exchange data. Virtual data rooms and deal spaces with restricted entryfacilitate distribution and revision of documents and thereby reduce the need for direct contactin order to exchange data. The basis for any use of such technologies is a technologicalinfrastructure that allows for quick and stable connections. So it is not surprising thatFrankfurt is the central node for Internet-transactions in Germany with 85% of all Internet-transmissions being routed via Frankfurt (Wirtschaftswoche, 1999; Frankfurter AllgemeineZeitung, 1999).

These developments in financial technology will obviously have great effects on the existenceof financial centers. The digitalization and the so-called distanciation of communicationmedia have immediate consequences for the need for proximity to other financial actors, andtherefore work against agglomeration tendencies.

3 A value chain approach to financial centers

As the importance of financial centers depends on the location choices of individual actors, ananalysis of the financial center system has to take into account changes at firm and even de-partment level. Moreover, the same technologies that enable centralization of functions atfirm level can work in favor of a decentralization from the viewpoint of the financial centersystem. Because of this complexity, we use the concept of value chains of individual productswhich is well suited for the analysis of geographical embeddedness of production systems(Schoenberger, 1994). The approach of using the production process to draw inferences forthe spatial organization of the financial industry is in the tradition of the writings of Ter Hart

6

and Piersma (1990), Lee and Schmidt-Marwede (1993), Thrift (1994), Clark and O’Connor(1997) and Walter (1998).

Following Walter (1988), Lee and Schmidt-Marwede (1993) stress that different financialservices require different competitive resources, or „conditions of production“. The extent towhich the production of specific financial services is „open to [...] the choice of global loca-tion“ (ibid., p. 513) determines the outcome of financial center competition. On a differenttrack, Ter Hart and Piersma (1990) concentrate on the determinants for physical, or spatialproximity in the financial sector: intensity of face-to-face-contacts, importance of rapidity orintensity of contact, scale of the transaction and acquaintance with the other party. They alsogive a list of banking transactions ranked by their sensitivity to spatial proximity. The morecomplex and the closer to the customer the transactions are, the more spatial proximity isneeded.

A similar approach with a more exhaustive terminology was chosen by Clark and O’Connor(1997). They divide financial products into three categories, i.e. transparent, translucent andopaque, mainly by looking at the kind and specificity of information that is required to tradethese products. Opaque products will be traded in sub-national centers, because of the localknowledge that is needed, translucent products mostly in national centers and transparentproducts in the global financial centers.

Walter (1998) goes one step further. He states that technology permits the ‘unbundling’ offinancial activities, thereby increasing the centrifugal forces in financial centers. Differentfinancial products are allocated within a range according to the need for personal contactswith customers, other players or service firms. Walter states that technology reduces thethreshold beyond which the internal economies of scale outweigh the benefits of being closeto the financial center where the business originates.

We suggest that it is not only necessary to grapple with individual products as „differentfinancial services have different conditions of existence“ (Lee and Schmidt-Marwede, 1993,p. 502), but with individual production stages in the process in order to analyze the changingspatial organization of financial production. We therefore examine the value chains ofdifferent financial products, stressing the kinds of proximity to other actors or institutionsneeded for their production at each stage.

The concept of value chains permits the disaggregation of the production process into itsrelevant activities (Porter, 1985) in a way that allows a simultaneous analysis of process andactors. It therefore becomes possible to highlight those junctures in the value chain where newtechnologies can be used to spatially separate production stages that hitherto had to be locatedin the same place. Although the value chain approach basically is a microeconomic concept, it

7

also allows for an analysis of meso- and macroeconomic phenomena (Gereffi et al., 1994), i.e.financial centers.

Value chains have been used widely in business literature and economic geography, albeitwith varying terminology – e.g. production chain (Dicken), global commodity chain (Gereffi)or value added chain (Porter). Its most common use is in the analysis of the organization ofproduction systems (Dicken, 1998; Gereffi and Korzeniewicz, 1994; Gereffi, 1999; Johnstonand Lawrence, 1988; Porter, 1985 and 1990; Storper, 1992; Walker, 1988). While a widearray of subjects have been analyzed with this concept (see Leslie and Reimer, 1999), servicesin general are seen only as links between different nodes of the value chain and as facilitatingthe production of goods (Dicken, 1998; Rabach and Kim, 1994). In this paper, the valuechain-framework is extended to cover financial services. The provision of financial services istherefore regarded as a production process.

One critical issue about value chain analysis is that the focus on linkages between differentproduction stages stresses vertical relationships between firms and neglects horizontal links(Leslie and Reimer, 1999). For the spatialization of value chains, the localization ofproduction stages, however, the forging of horizontal relationships with co-operating firms indistinct places is of eminent relevance. These horizontal linkages differ between productionstages which in turn suggests the importance of study in a vertical direction. In this paper, wetherefore utilize a combination of vertical analysis with horizontal connections in order tolocalize the different stages of financial production. This coincides with Appelbaum, Smithand Christerson (1994, p. 188) who see each production stage as a node which „is in itself anetwork connected to other nodes concerned with related activities“. Our argument is that it isthe need for proximity in these horizontal connections that is one of the most importantfactors for the localization of the respective activity.

4 Proximities in financial production

For the financial industry, proximity is especially important because financial production isbased mainly on knowledge and information exchange. The need for the procurement ofinformation and knowledge is generally seen as one of the main driving forces behind thecentralization of financial actors. As Thrift (1994, p. 334) points out, the culture ofinternational financial centers can be summarized by „the need for information, for theexpertise that allows that information to be interpreted and for the social contacts thatgenerate trust, information, interpretive schemes – and business“.

When analyzing the consequences of ICT, it is important to note the distinction betweeninformation and knowledge: While information and codified knowledge can be transferredover spatial distances via telecommunication technologies, tacit knowledge is alwaysconnected to subject and context, and cannot be removed from these connections without

8

difficulties (Nonaka and Takeuchi, 1995; Willke, 1998). Because of the context-intensity,tacit knowledge exchange is facilitated and sometimes only possible in close proximity (thisrefers not only to spatial but also to other types of proximity). Boden and Molotch (1994, p.274) point out that „(t)he more information produced by the new technologies, the higher thepremium on copresence needed to design, interpret and implement the knowledge gained.“

According to Giddens (1990, p. 28), ICT function as disembedding mechanisms which„remove social relations from the immediacies of context“. For Giddens, trust is the criticalissue for the functioning of disembedding mechanisms like ICT, and trust can only be built upthrough proximity. In this context, many authors suggest that it is not only spatial proximity,but also various other forms of proximity (i.e. social, cultural, organizational, technological,relational, institutional, temporal...) that form the basis for trust in business interaction (Blancand Sierra, 1999; Lundvall, 1988; Malmberg and Maskell, 1997). In this paper, we argue thatfour kinds of proximities are important for understanding the geographical organization ofvalue chains in the financial sector: spatial, organizational, cultural and vocational proximity.

Spatial proximity refers to the geographical distance between actors. Depending on the con-text, this can mean walking distance or the distance to any point that can be reached within acertain time span (Thierstein, 1996). Spatial proximity incites personal contacts (Daniels,1985), and fosters knowledge transmission and collective learning processes, often incombination with cultural and organizational proximity (Keeble and Wilkinson, 1999;Malmberg and Maskell, 1999). Spatial proximity is of great importance if the need forspontaneous meetings or/and regular informal contacts is high. It also offers opportunities forgetting aside information out of conventional channels. For our purposes later on in the valuechain analysis, we understand spatial proximity as location in the same financial center.

In the definition of cultural proximity we include sharing common cultural background andlanguage (Lundvall, 1988), values, norms, conventions and ways of doing business (Saxenian,1994) and institutional characteristics of nation-states (Berndt, 1996). All these aspectsfacilitate and foster interaction and communication between actors located in the samenational territory. The reference to national territories in cultural proximity is of importancebecause the financial business is highly dependent on national regulation. Sharing experiencein the established law therefore provides a common frame of reference. As Gertler (1993, p.676) puts it: „This argument thus ascribes considerable importance to national boundariesbecause nation-states create those institutions which actively define and maintain distinctindustrial practices [...]“. Cultural proximity gains in importance with the degree ofcomplexity of the transaction (Bathelt, 1995) and is essential to ensure adequate qualitativecommunication (Gregersen and Johnson, 1997).

A lack in spatial or cultural proximity can be partly substituted by vertical integration ororganizational proximity (Lundvall, 1988). This becomes even more relevant with the

9

implementation of new ICT (Bathelt, 2000). Organizational proximity exists between actorsworking in the same company regardless of their geographical location. It refers to corporateidentity, corporate philosophy, organizational rules and codes (Blanc and Sierra, 1999). In asimilar manner, proximity between actors in the same type of job can bridge spatial andcultural distance. Our interviews have shown that this vocational proximity, is of considerableimportance in the financial sector. Actors with strong vocational proximity possess anunderstanding of each others methods and aims, share similar interests and the vocationallanguage. This proximity is especially intense in vocations that have a high code of ethics,like law or accountancy.

Organizational and vocational proximity are important for financial production because theyfacilitate the building of trust and provide context, thus simplifying knowledge exchange. Thereason for this is that they are based on sharing conventions, thus providing a common„framework of action [...] with other actors engaged in that activity“ (Storper, 1997, p. 45). Inthe case of organizational and vocational proximity, ICT can be used to bridge great spatialdistances, because they provide trust that enables the disembedding mechanism. In contrast tothat, the need for spatial and cultural proximity still entails spatial boundaries. Culturalproximity impedes the extension beyond national and language borders and therefore keepsproduction within a certain territory.

In the following chapter we will use this concept of proximities in connection with technolo-gies to discuss financial production by means of three different value chains. We argue thatthis analytical tool can be used to explain the development of the spatial organization of thefinancial production which in turn leads to the location of functions in different financialcenters.

5 Value chains of different financial products

In this section we discuss consultancy for the acquisition of a firm, loan syndication, andstock trading. While these three products cover only part of the range of financial trans-actions, they are exemplary for the three kinds of business typically performed by banks:advisory, lending and trading, and they are usually located in financial centers. In order to beable to compare three different products we have included only the main parts of theproduction process in the stylized value chains.

For empirical evidence, we have drawn extensively on the preliminary results of three on-going research projects at Frankfurt University. The projects included 128 semi-structuredinterviews with banks and related services (lawyers, accountants) which took place betweenFebruary 1998 and December 1999. The interviews focused on location behavior, andrelationships with clients and other firms during production process. The firms that wereinterviewed represent major players in European banking, and are multilocational firms in the

10

sense that they are all located in several European financial centers which allows them tomove departments between financial centers easily. The enterprises were chosen on the basisof size, business activity and diversity of geographic origin. In nearly all cases, the interviewswere conducted with high-level executives. The data was collected in the three mostprominent European financial centers (with a bias on Frankfurt): Frankfurt (92 interviews),London (19) and Paris (17).

In the following chapters, we will show (1) which production stages can be spatiallyreorganized with ICTs and (2) what kind of proximity is required for production and thereforeinfluences the new location of this activity. 1

Acquisition of a firm

In merger and acquisition (M&A)-transactions, personal contact is crucial in many stages ofthe value chain. In this production process, ICT has until now been implemented almostsolely as a complement and not as a substitute for face-to-face contact. In our analysis, weconsider three typical stages of the acquisition of a firm which are shown in Figure 1: Firstly,the selection of and first contact with the target firm (the firm that is to be bought). Secondly,the evaluation of the target firm and thirdly, the negotiations about the conclusion of the deal.

Figure 1: Acquisition of a firm

value chain bankdepartment

kind ofproximity

correspondingactor

selection &first contact

evaluation

negotiation

M&Adepartment

client

target firm

M&Adepartment

accountants

target firm

M&Adepartment

client

lawyers

target firm

culturalvocational

culturalvocational

spatialcultural

vocational

1 For analytical purposes we assume that the need for organisational proximity between the steps of the valuechain remains constant. This will not influence our conclusions concerning the mobility of certain departmentsor functions.

11

In the first stage, the M&A-department has to understand a) what kind of target firm will beappropriate for the client and b) how to convince the target of the attractiveness of their offer.Thus, a shared frame of reference, i.e. cultural proximity between bank and client and bankand target is of great importance for the build up of trust, the contact approach and thefollowing exchange of sensitive information. Firms involved in M&A-transactions aretherefore advised and approached almost exclusively by the respective domestic branches ofinvestment banks.

The second stage contains the evaluation of the target firm. This is done directly at the targetfirm’s headquarter, with the help of specialized accountants under the supervision of theM&A-department. (The need of the accountants to work in spatial proximity to the target firmis indicated by a dotted rectangle.) In this stage, the communication relationship betweenaccountants and M&A-department is crucial. The bank must be able to understand andprocess the information and knowledge produced by the accountants, thus the need forcultural proximity. Furthermore, the bank has to trust the accountants that they will inform itof any difficulty or irregularity in the balance sheets which presupposes similar vocationalethics, i.e. vocational proximity.

The third stage includes extensive negotiations about contract details and the conclusion ofthe deal among M&A-department, lawyers, tax consultants, client and target firm. Culturalproximity between these actors makes communication easier and helps to avoid time-consuming misunderstandings. Continuity and length of the negotiations is also greatlyinfluenced by the degree of vocational proximity between M&A-departments, tax consultantsand lawyers on both sides. The higher this proximity, the closer they will work together forthe collective goal: conclusion of the contract. The speed and smoothness of the settlement isalso dependent on the possibility for frequent, spontaneous (and sometimes informal)meetings, i.e. spatial proximity. Therefore, location in the national financial center isattractive for the M&A-department because of spatial proximity to specialized tax consultantsand lawyers.

In M&A-transactions, technology’s role is mainly focused on the supply with information andless on the production process and interaction between the actors. The ‘getting to know eachother’ in close personal interactions cannot be replaced by telecommunications, but onlycomplemented by it. Mergers & acquisitions is still very much a ‘person business’ where‘thick communication’ is essential for conducting the transaction (Lo, 1999).

Loan syndication

Syndicated loans are provided when the capital needed by a client exceeds the amount a sin-gle bank can or wants to supply. Thus, through syndication the amount and risk of the loan isshared between a certain number of banks. The success of the syndication relies on first-hand

12

information about 'the market', i.e. other banks' strategies in order to find out which banks toinvite for participation etc. Furthermore, the process involves extensive negotiations betweenboth lead bank(s) and client, and lead bank(s) and participating banks. The latter are oftenvery intensive, as all participating banks have to sign the same contract.

The loan syndication process can be divided roughly into three stages, as shown in Figure 2:

Figure 2: Lead management of a syndicated loan arrangement

value chain bankdepartment

kind ofproximity

correspondingactor

deal-structuring

credit-worthiness

check

arrangement

syndicationdepartment client

credit riskdepartment

(usuallyheadquarter)

other banks

lawyers

syndicationdepartment

syndicationdepartment

spatialvocational

spatial

cultural

In the first stage, the leading bank structures the deal according to the client's needs. As in thecase of M&A-transactions, the negotiation between the lead bank and the client is simplifiedby cultural proximity which establishes a common frame of reference. Secondly, thecreditworthiness of the client is being checked by the in-house credit department. The resultof this check is of significant importance for the participation in the deal. As many variablesin the check are subject to interpretation, intensive contact between the two departments aboutdetails of the deal are important. This contact is best achieved trough spatial proximity. In thethird stage, the actual syndication takes place. This process includes the gathering andprocessing of information about possible participants and the arrangement of the syndicate(including negotiations about the final loan). This stage requires intense negotiations withparticipating banks and their lawyers which often are held at short notice. Furthermore, thegathering of information about possible participating banks involves frequent informalmeetings. Such contacts can be best achieved with spatial proximity. Vocational proximity isnecessary to ensure a common understanding in the process of negotiation between banks andlawyers. The essential part of the syndication process consists of close contact to other banks.Therefore most banks have located the whole syndication department in a financial center

13

with a large market for syndicated loans, even though, as can be seen from the value chain,not all stages require close proximity to other banks. In the first and second stage, spatial andcultural proximity to the client and the headquarter are equally important.

Only recently, new Internet-based firms are emerging that are changing the way in which thethird stage is organized. These firms provide virtual data rooms with high security standards,where participating banks can download information about the deal and which substantiallyreduce administrative costs of both co-ordinating and supervising data flows. This has alreadyled some banks to split up the third stage into two, leaving a small number of employees inthe main financial center in order to keep close contact to other banks and to keep track ofmarket developments. The larger part of the syndication department is then relocated to theheadquarter in order to simplify the internal co-ordination processes.

Stock trading

In former times, physical presence was required at each stock exchange in order to participatein the respective market. The different stages of conventional stock trading at foreign stockexchanges – on behalf of a client – are shown in Figure 3:

Figure 3: Conventional stock trading at a foreign European stock exchange

value chain bankdepartment

kind ofproximity

correspondingactor

customeradvisoryservice

order routing

trading

salesdepartment client

foreign stockexchange

domestictrading office

foreigntrading office

spatialcultural

vocational

cultural

In the first stage the appropriate country, amount and company to invest in is chosen. Sinceduring the advisory process not only the events of the day, the market mood and rumors butalso the specific needs of the client (only large clients are regarded here) are discussed,cultural proximity to the client is required. In the second stage, the sales department gives the

14

order to its domestic trading office, where the processing is done and the order is routed to therespective foreign trading office. This office has to be vocationally, culturally and spatiallyclose to the foreign stock exchange, where – in the third stage – the trading takes place.Vocational proximity is necessary as, by law, only locally trained dealers are allowed toparticipate in stock exchange dealings, and cultural proximity is needed to understand thecomplex and partly unwritten rules of dealing in specific stock exchanges. Spatial proximityis needed because ‘conventional’ stock trading implies that there is no remote access.

The virtualization of stock exchanges is probably one of the most profound changes for finan-cial centers. With the implementation of remote access facilities, European stock exchangescan be reached via computer from any country. This eliminates the necessity for physicalpresence. At present, this technology is not very wide-spread, but it is generally expected tobecome ubiquitous in only a few years. Figure 4 shows stock trading with remote access.Compared to conventional trading, the actual trading now requires only vocational proximity– at the domestic trading office. The foreign trading department is no longer necessary.

Figure 4: Stock trading with remote access to an European stock exchange network

value chain bankdepartment

kind ofproximity

correspondingactor

customeradvisoryservice

trading

salesdepartment client

stockexchangenetwork

domestictrading office

cultural

vocational

This reflects what is actually happening in Frankfurt, where sophisticated stock exchangetechnology has been developed and implemented: Non-German banks have started tradingfrom London and relocated their local traders. Since the actual trading process involves onlythe transfer of information, remote access to other stock exchanges is possible withoutdifficulties. Still, the need for cultural proximity to the client continues to exist because of the

15

intensive advisory service that banks offer and the high degree of tacit knowledge involved inthat service.

However, if clients are willing to inform themselves and even buy and sell stocks on theInternet, every single step of the production chain becomes ‘virtual’. As already shown inFigure 4, the trading office does not have to be located close to any other department or stockexchange anymore, the homepage can be provided elsewhere and now even the clients loosetheir importance as a ‘fixing point’.

6 From value chains to financial centers

From the micro level of value chains we now take a big step to the macro level, the Europeanfinancial center system. The next question is, what are the inferences for financial centers?The reason why we introduced the concept of different proximities in connection with tech-nologies is that we try to assess whether certain types of activity have a tendency to centralizein specific financial centers. We are aware that this is a very narrow view of the determinantsfor spatial organization, but nevertheless assume that the need for proximities is one of themajor factors for location of financial actors.

The aim of this chapter is to show in which stages of the value chain the implementation oftechnologies allows a delocalization, and where the following relocalization, either in a differ-ent national financial center or centralized in just one financial center in Europe, is probableto take place according to the necessity of different types of proximity.

Acquisition of a firm

The analysis of the value chain in acquisitions has shown that the arrival of new telecommu-nications is not leading to a split up of different stages or activities. This means that there willbe no relocation of single activities, the entire production process will stay in one place. Atthe moment, the bulk of acquisition activities are concentrated in the respective national fi-nancial centers and this is unlikely to change. As we have shown above, cultural proximity tocustomers and target firms is so important that presence within the same national/cultural ter-ritory is essential for doing business.

Most of the firms choose the national financial center, because of the high contact frequencyto related services (spatial proximity to lawyers, accountants). Another point in favor offinancial centers is their (usually) high standard of transportation infrastructure which isneeded for travelling to client and target firms. Therefore, we conclude that the location of theM&A-function is unlikely to change in the next few years, and there will be no single highlyspecialized European M&A-center, but one within each national/cultural territory.

16

Loan syndication

In the case of syndicated loans, new ICT is starting to change the spatial organization of fi-nancial actors. The activities of information gathering, contacting other banks and processingof the transaction need no longer stay in one place. These activities have so far beenconcentrated in the biggest financial centers. The reason for this was the need for spatialproximity to other banks, because of the frequency of copresent interaction for contact main-tenance, information exchange and co-ordination. Therefore, the syndication business had atendency to locate within the financial center with the highest number of banks, which isLondon.

With the event of new telecommunications, the need for spatial proximity to other banks forco-ordination purposes has abated. Thus, the syndication department can now be split up intoinformation gatherers (which includes maintenance of contact with other banks), who stillhave to be where the biggest agglomeration of banks is, and in transaction processors (whostructure the loan), who gain a certain level of 'footlooseness'. Again, the question is, whereare they most likely to go? For the structuring activity, spatial proximity to the headquarter isthe next priority. It is therefore likely, that there will be a centralization on a firm level and atthe same time a decentralization on a financial center level. That means that, for syndicatedloans, the leading European financial center is likely to keep the information activity but loosesome of the processing activity to the respective national financial centers, where headquar-ters are usually located.

Stock trading

In the case of stock trading, the location of the traders is affected to a great extent by the de-velopment of new technologies, i.e. trading-systems with remote access. The need for spatialand cultural proximity has so far led to locations close to the respective stock exchanges,which in most cases is equal with presence in the various national financial centers. In thefuture, this will not be necessary, because each bank can concentrate their traders in oneplace. There are two possible directions for relocation: (1) centralization within Europe in justone financial center or, as in the case of processing syndicated loans, (2) concentration on thefirm level close to the respective headquarters. This depends on whether there is morenecessity to be culturally, vocationally and spatially close to traders from other firms or to beorganizationally and spatially close to the headquarters. Or, to look at it from a different per-spective, it depends on whether the gains from external economies of scale are greater orsmaller than those from internal economies of scope and scale.

Contrary to that, the advisory activity will have to stay close to the customer, i.e. dispersed inthe different national territories, to maintain cultural proximity. On the level of financialcenters, this implies that while there is no locational change for advisory, trading might

17

centralize within Europe in just one financial center. Because of London’s prominent positionin Europe and the trading knowledge already accumulated there, London would then be theprobable location for this function.

As we have shown, the implementation of new information and communication technologieshas very different effects on the spatial organization of the activities in each value chain.From a financial center perspective, the relocation tendencies can be summarized asfollowing: (a) products that will not relocate, as for example acquisitions; (b) activities, likeprocessing syndicated loans, that might decentralize from a leading financial center to therespective bank headquarters and (c) activities that can centralize in just one leading financialcenter in Europe, e.g. stock trading. We will now leave this rather abstract level and applythese findings to a concrete example, Frankfurt’s role in the European financial center system.

7 Frankfurt’s new role in the European financial center system

Frankfurt is the most important German and one of the most important European financialcenters. As the host city of the European Central Bank (ECB), it is also the center of Euro-pean monetary policy. The decision to locate the ECB in Frankfurt raised huge expectationsabout Frankfurt’s future, forecasting an increasing inflow of foreign bankers and experts(Frankfurter Allgemeine Zeitung, 1998). So far, these expectations have not been fulfilled andlikewise Frankfurt has not reached the aspired position as a gateway to Eastern Europe(Schamp and Grote, 1999). In terms of financial center resources, compared to London,Frankfurt has less innovative and liquid financial markets, less qualified labor and less flexi-ble regulation (Dietl, Pauli and Royer, 1999). Yet, in recent years, Frankfurt’s efforts havegone far to ameliorate its regulatory and technological framework and the city has become aleader in the development of financial technology, notably trading and settlement systems.

Hence, the opinion about Frankfurt’s future is changing: A study from 1990 expected thatLondon and (to some respect) Paris would dominate Frankfurt (Häuser et al., 1990).However, a recent survey by the news channel CNBC states that 39% of European bankersinterviewed see Frankfurt as the primary financial center in Europe in 2005, even ahead ofLondon (Metzler, 1999). So while formerly Frankfurt was competing with Paris for secondplace in the European financial center hierarchy, now the competition seems to be betweenLondon and Frankfurt, with Paris being left behind.

Such general assessments may hint at future developments, but fail to give an idea of the on-going relocations of different functions between the financial centers. Therefore, we base thefollowing predications about the new role of Frankfurt in the European financial center sys-tem on our findings from the value chain approach.

18

As shown above, M&A-business is likely to stay in the respective national markets. Europeanintegration has put high competitive pressure on firms operating in the EU and is one of thereasons for the increasing number of M&A deals. This is particularly true for the Germaneconomy with its high percentage of medium-sized firms (‘Mittelstand’). This clientele re-quires advisors who are not only spatially but also culturally close. Thus, the volume of M&Adeals executed in Frankfurt is rising steadily and the headcount of M&A experts is increasing.Frankfurt’s specialization as a center for advisory services related to the German market isalso reflected in the strategy of foreign banks in Frankfurt. While there is a general trend forforeign banks to reduce their headcount in trading and back-office, they are increasing it inadvisory and sales (Grote, 1998).

Although, Frankfurt mainly serves as a gateway to the German market, the importance of thisfunction should not be underestimated, since the German economy represents a large part ofthe EU economy. Contrary to the past, Frankfurt now plays a considerable part in advisory-related investment banking products. This is an important change for Frankfurt which used torely mainly on commercial banking.

Notwithstanding its strength in commercial banking, Frankfurt has never been a center forinternational syndicated loans. The European and global center for syndication is London,which has the largest agglomeration of specialists and expertise. As shown above, it has nowbecome possible to relocate the processing activities in the syndication process closer to therespective headquarters. Since almost all headquarters of the major German banks are locatedin Frankfurt, such a relocation process would enhance its position in the field of internationalcommercial banking.

Contrary to the examples above, all of which have positive implications for Frankfurt, theconsequences of new ICT on trading are double-edged. During the last few years the develop-ment of Frankfurt has been closely linked to that of the Frankfurt stock exchange and its in-vestment in new technologies. Judged by the turnover on the Frankfurt markets, this has beena clear success: Frankfurt’s futures exchange Eurex is the largest futures market in the world,whilst the stock market ranks fourth. Both have gained a reputation for highly reliable andquick settlement of deals. Nevertheless, the implications of the stock market technology onFrankfurt’s position are not solely positive: While Frankfurt is the European center for thedevelopment of stock market technology, this still might not make Frankfurt a trading center;at least not in the sense that traders are actually located here. On the contrary, at first therewas a clear trend of traders relocating to London, while using the Frankfurt trading infra-structure. This has changed in the last year, reflecting the conflicting effects of internal andexternal economies of scale as well as the need for different proximities: Since traders needproximity to both other traders and locally available knowledge about the stocks they trade,the final location remains uncertain. London has a much larger agglomeration of traders,

19

leading to larger benefits from externalities, which gives it a competitive edge over Frankfurt.However, several German banks have concentrated their trading activities for the Germanmarket in Frankfurt, and recently one of the largest American investment banks has followedtheir example.

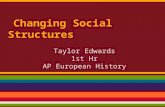

A particularly apt example for the ambivalence of technological development is the ‘battle forthe Bund-future’ between London’s Liffe and Frankfurt’s Eurex. The Bund-future is the mosttraded derivative in the world. As it is based on German federal bonds, it could be expectedthat it were traded in its ‘home-country’ Germany. However, as German regulation did notallow trading of derivatives until 1990, the market emerged at Liffe and the relevant expertisewas concentrated in London. The efforts of the German Derivatives Exchange – after theirformation in the early 90s – to transfer Bund-future trading volume to Frankfurt were of littlesuccess despite their comparatively low trading costs. Due to prevailing lock-in effects(mostly concerning market liquidity), a large extent of the trade still took place at London'sLiffe. Only after Eurex terminals with remote-access facility were installed in the City andGerman banks shifted their trading volume to Eurex, London traders began using theFrankfurt-based system, too. Eurex' market-share in Bund-future trading now amounts to99.9%. Figure 5 shows that Eurex’ gain in the trading volume of the Bund-future coincideswith an increase in the number of traders from abroad. Thus, the trading system is now thecentral marketplace for Bund-futures, but most of the traders are using the system fromforeign financial centers, mainly London.

20

Figure 5: Market Share in Bund-Future Trading

Source: Verband der Auslandsbanken in Deutschland 1999, p. 33 and Finanzplatz e.V. 1999, p. 33.

Thus, from the viewpoint of Frankfurt, its leadership in remote access technology has someunwelcome side effects, as many of the advantages of being a financial center are related tothe income that is generated in that center. Frankfurt might become a leader in technology,but not in people. The gains from Frankfurt’s position as a center for trading technology thusdepend on whether further business is attracted which necessitates the physical presence ofbankers, i.e. spatial proximity to the technology center.

Acknowledgements

Part of this work – especially the interviews – has been done while the authors have beenworking at different projects at Johann Wolfgang Goethe-University Frankfurt. Michael Grotewas funded by German Israeli Foundation Jerusalem, research project no. I-0404-003 04/95;Sofia Harrschar-Ehrnborg was funded by Centre for Financial Studies Frankfurt, researchproject “The European financial centre competition – the case of London, Frankfurt andParis” and Vivien Lo was funded by DFG Deutsche Forschungsgemeinschaft Bonn, specialresearch programme SFB 403, project “Networking of knowledge intensive services as afactor of innovativeness in metropolitan regions” and by Institute for Economic and SocialGeography, Frankfurt. The funding is gratefully acknowledged.

0

10

20

30

40

50

60

70

80

90

100

Mrz 96

Apr 9

6Mai 9

6Jun

96Jul

96Au

g 96

Sep 9

6Okt 9

6No

v 96

Dez 9

6Jan

97Fe

b 97

Mrz 97

Apr 9

7Mai 9

7Jun

97Jul

97Au

g 97

Sep 9

7Okt 9

7No

v 97

Dez 9

7Jan

98Feb

98Mrz 9

8Ap

r 98Mai 9

8Jun

98Jul

98Au

g 98

Sep 9

8Okt 9

8No

v 98

Time

Mar

ket S

har

e in

Per

cen

t

0

20

40

60

80

100

120

140

Nu

mb

er o

f Rem

ote

-Acc

ess

Mem

ber

s at

Eu

rex

Number of Remote-Access Members at Eurex (right scale) Market Share Eurex (left scale, in Percent)

21

The authors would like to thank Sam Ock Park, Eike W. Schamp and Reinhard Schmidt fortheir insightful and inspiring comments and the participants of the conference “Cities in theGlobal Information Society: An International Perspective” in Newcastle for their clarifyingremarks. Remaining errors are of course solely in our responsibility.

References

Appelbaum R, Smith D, Christerson B, 1994, “Commodity Chains and Industrial Restructuring in thePacific Rim: Garment Trade and Manufacturing”, in Commodity Chains and GlobalCapitalism Eds G Gereffi, M Korzeniewicz (Westport, Greenwood) pp 187-198.

Bathelt H, 1995, “Der Einfluss von Flexibilisierungsprozessen auf industrielle Produktionsstrukturenam Beispiel der chemischen Industrie“ Erdkunde 49 176-196.

Bathelt H, 2000, “Räumliche Produktions- und Marktbeziehungen zwischen Globalisierung undRegionalisierung – Konzeptioneller Überblick und ausgewählte Beispiele“ Berichte zurdeutschen Landeskunde 74 (2) forthcoming.

Berndt C, 1996, “Arbeitsteilung, institutionelle Distanz und Ortsgebundenheit: StrategischeAnpassung an veränderte Rahmenbedingungen am Beispiel mittelständischer Unternehmen imRuhrgebiet“ Geographische Zeitschrift 84 (4) 220-237.

Blanc H, Sierra C, 1999, “The internationalisation of R&D by multinationals: a trade-off betweenexternal and internal proximity“ Cambridge Journal of Economics 23 187-206.

Boden D, Molotch H, 1994, “The compulsion of proximity“, in NowHere: Space, Time and ModernityEds R Friedland, D Boden (University of California Press, California) pp 257-286.

Budd L, 1995, “Globalisation, Territory and Strategic Alliances in Different Financial Centres“ UrbanStudies 32 (2) 345-360.

Clark G, O'Connor K, 1997, “The Informational Content of Financial Products and the SpatialStructure of the Global Finance Industry“, in Spaces of Globalization Ed K R Cox (GuilfordPress, London, New York) pp 89-114.

Daniels P W, 1985, “Standorte von Bürobetrieben“ in Standorte und Einzugsbereiche tertiärerEinrichtungen Ed G Heinritz (Wissenschaftliche Buchgesellschaft, Darmstadt ) pp 218-262.

Deutsche Börse AG, 1999 Facts and Figures, 60284 Frankfurt/M.

Dicken P, 1998 Global Shift, 3rd edition (Paul Chapman, London).

Dietl H, Pauli M, Royer S, 1999, “Frankfurts Position im internationalen Finanzplatzwettbewerb: Eineressourcenorientierte Analyse”, Working Paper No 1999/10, Centre for financial studies,60054 Frankfurt/M.

Eurex, 1999 Eurex – der europäische Derivatemarkt, Eurex Frankfurt AG, Börsenplatz 7-11, 60313Frankfurt/M.

Finanzplatz e.V., 1999 Der Euro ist da – Neue Währung, neue Märkte, neue Benchmarks, Finanzplatze.V., Börsenplatz 7-11, 60313 Frankfurt/M.

Frankel J A, 1996, “Exchange Rates and the Single Currency”, in The European Equity Markets Ed BSteil (European Capital Markets Institute, London) pp 355-393.

22

Frankfurter Allgemeine Zeitung, 1998, “Frankfurt profitiert von der neuen Zentralbank” FrankfurterAllgemeine Zeitung, 29 May, p 25.

Frankfurter Allgemeine Zeitung, 1999, “Der zentrale Knoten des deutschen Internet zieht um”Frankfurter Allgemeine Zeitung, 27 May, p 27.

Friedmann J, 1995, “Where we stand: a decade of world city research“, in World cities in a world-system Eds P Knox, P Taylor (Cambridge University Press, Cambridge) pp 21-47.

Gereffi G, 1999, “International trade and industrial upgrading in the apparel commodity chain”Journal of International Economics 48 37-70.

Gereffi G, Korzeniewicz M, Korzeniewicz R P, 1994, “Introduction: Global Commodity Chains”, inCommodity chains and global capitalism Eds G Gereffi, M Korzeniewicz (Praeger, Westport)pp 1-14.

Gertler M, 1993, “Implementing Advanced Manufacturing Technologies in Mature Industrial Regions:Towards a Social Model of Technology Production“ Regional Studies 27 (7) 665-680.

Giddens A, 1990 The Consequences of Modernity (University Press, Stanford).

Grasland L, Jensen-Butler Ch, 1997, “The set of cities“, in European cities in competition Eds ChJensen-Butler, A Shachar, J Weesep (Brookfield, Aldershot) pp 43-78.

Gregersen B, Johnson B, 1997, “Learning Economies, Innovation Systems and European Integration“Regional Studies 31 (5) 479-490.

Grote M, 1998 Foreign Banks in Frankfurt, Mimeo, Institute for Economic and Social Geography,Johann Wolfgang Goethe-Universität, Frankfurt/M.

Harrschar-Ehrnborg S, 1999 Die Entwicklung von Finanzzentren. Eine historische Betrachtung,Mimeo, Wilhelm Merton-Chair for International Banking and Finance, Johann WolfgangGoethe-Universität, Frankfurt/M.

Häuser K et al., 1990, “Frankfurts Wettbewerbslage als europäisches Finanzzentrum – Eine empiri-sche Untersuchung”, Informationsschrift 8, Institut für Kapitalmarktforschung, 60054 Frank-furt/M.

Institutional Investor, 1998, “The world's largest banks“ The Institutional Investor (August) 41-74.

Johnston R, Lawrence P R, 1988, “Beyond vertical integration – the rise of the value-addingpartnership” Harvard Business Review (July-August) 94-101.

Keeble D, Wilkinson F, 1999, “Collective Learning and Knowledge Development in the Evolution ofRegional Clusters of High Technology SMEs in Europe“ Regional Studies 33 (4) 295-303.

Kindleberger C, 1974, “The Formation of Financial Centers: A Study in Comparative EconomicHistory“ Princeton Studies in International Finance 36.

Knox P, 1995, “World cities in a world-system“, in World cities in a world-system Eds P Knox, PTaylor (Cambridge University Press, Cambridge) pp 3-20.

Lee R, Schmidt-Marwede U, 1993, “Interurban competition? Financial centres and the geography offinancial production“ International Journal of Urban and Regional Research 17 (4) 492-515.

Leslie D, Reimer S, 1999, “Spatializing commodity chains” Progress in Human Geography 23 (3)401-420.

23

Lo V, 1999, “Der M&A-Markt in Deutschland” Working Paper No 4, SFB 403 AB-99-24, Institutefor Economic and Social Geography, Johann Wolfgang Goethe- Universität, 60054 Frank-furt/M.

Lundvall B-A, 1988, “Innovation as an interactive process: from user-producer interaction to thenational system of innovation“, in Technical change and economic theory Eds G Dosi et al.(Pinter, London New York) pp 349-369.

Malmberg A, Maskell P, 1997, “Toward an explanation of regional specialization and industryagglomeration“ European Planning Studies 5 (1) 25-41.

Malmberg A, Maskell P, 1999, “Localised learning and industrial competitiveness“ CambridgeJournal of Economics 23 167-185.

Martin R, 1994, “Stateless Monies, Global Financial Integration and National Economic Autonomy:The End of Geography?“, in Money, Power and Space Eds S Corbridge, RL Martin, N Thrift(Blackwell, Oxford) pp 253-278.

Martin R, 1999, “The New Economic Geography of Money“, in Money and the Space Economy Ed RMartin (John Wiley & Sons, Chichester et al.) pp 3-27.

Metzler F, 1999, “Aufbruch ins 21. Jahrhundert“, in Finanzplatz Frankfurt. Von der mittelalterlichenMessestadt zum europäischen Bankenzentrum Ed C-L Holtfrerich (C.H. Beck, München) pp297-312.

Nonaka I, Takeuchi I, 1995 The Knowledge-Creating Company: How Japanese Companies Create theDynamics (University Press, Oxford).

Porteous D, 1999, “The Development of Financial Centres: Location, Information Externalities andPath Dependence“, in Money and the Space Economy Ed R Martin (John Wiley & Sons,Chichester et al.) pp 95-114.

Porter M E, 1985 Competitive Advantage (Free Press, New York).

Porter M E, 1990 The Competitive Advantage of Nations (Free Press, New York).

Rabach E, Kim E M, 1994, “Where Is the Chain in Commodity Chains? The Service Sector Nexus”,in Commodity chains and global capitalism Eds G Gereffi, M Korzeniewicz (Praeger,Westport) pp 123-141.

Reed H C, 1981 The preeminence of international financial centers (Praeger, New York).

Rose H, 1994, “London as an International Financial Centre. A Narrative History”, The City ResearchProject, Subject Report XIII (London).

Sassen S, 1991 The Global City: New York, London, Tokyo (Princeton University Press, Princeton,NJ).

Saxenian A, 1994 Regional Advantage: Culture and competition in Silicon Valley and Route 128(Harvard University Press, Cambridge London).

Schamp E, Grote M, 1999, “An emerging Node in the World System: Frankfurt/Rhine-Main Region“,Mimeo, Institute for Economic and Social Geography, Johann Wolfgang Goethe-Universität,60054 Frankfurt/M.

Schoenberger E, 1994, “Competition, Time and Space in Industrial Change“, in Commodity Chainsand Global Capitalism Eds G Gereffi, M Korzeniewicz(Greenwood, Westport) pp 51-66.

24

Storper M, 1992, “The limits to globalization: technology districts and international trade” EconomicGeography 68 60-93.

Storper M, 1997 The regional world: territorial development in a global economy (The GuilfordPress, New York).

Ter Hart H, Piersma J, 1990, “Direct representation in international financial markets: The case offoreign banks in Amsterdam“ Tijdschrift voor Economische en Sociale Geografie 81 (2) 82-92.

The Bankers’ Almanac, 1998 The Bankers’ Almanac (Reed Business Information Ltd, EastGrinstead).

Thierstein A, 1996, “Auf der Suche nach der regionalen Wettbewerbsfähigkeit – Schlüsselfaktorenund Einflußmöglichkeiten“ Raumforschung und Raumordnung (2/3) 193-202.

Thrift N, 1994, “On the Social and Cultural Determinants of International Financial Centres: The Caseof the City of London“, in Money, Power and Space Eds S Corbridge, RL Martin, N Thrift(Blackwell, Oxford) pp 327-355.

Verband der Auslandsbanken e.V., 1999 Die Auslandsbanken in Deutschland 1999, Verband derAuslandsbanken in Deutschland e.V., Savignystr. 53-55, 60325 Frankfurt/M.

Walker R, 1988, “The geographical organization of production systems” Environment and Planning A6 377-408.

Walter I, 1988 Global competition in financial services: market structure, protection and trade lib-eralization (American Enterprise Institute/Ballinger Publishing Co, Cambridge, MA).

Walter I, 1998, “Globalization of Markets and Financial-Center Competition“, paper presented at theSymposium Challenges for Highly Developed Countries in the Global Economy, Institut fürWeltwirtschaft, March, Kiel.

Willke H, 1998 Systemisches Wissensmanagement (Lucius und Lucius, Stuttgart).

Wirtschaftswoche, 1999, “Netzminuten statt Schweinehälften” Wirtschaftswoche (24) p 120.