Frank Cowell: HMRC-HMT Economics of Taxation...

30

Frank Cowell: HMRC-HMT Economics of Taxation HMRC-HMT Economics of Taxation 2011 http://darp.lse.ac.uk/HMRC-HMT 10.2 Policy design 14 December 2011

Transcript of Frank Cowell: HMRC-HMT Economics of Taxation...

Frank Cow

ell: HM

RC-H

MT Econom

ics of Taxation

HMRC-HMT Economics of Taxation 2011

http://darp.lse.ac.uk/HMRC-HMT

10.2 Policy design

14 December 2011

Frank Cow

ell: HM

RC-H

MT Econom

ics of Taxation 2

Overview... Background

Objectives and constraints

Optimal policy C&B

Tax design

Policy Design

Locating the subject within public economics

Optimal policy Strategic

Frank Cow

ell: HM

RC-H

MT Econom

ics of Taxation 3

Issues in enforcement policy design

Identify main policy rules based on utilitarian ethics using the principal model types

Objectives reconcile with utilitarian goals? what guidance for tax agencies?

Implications for tax policy what guidance for tax agencies? impact of level and structure of income tax on tax evasion? and vice versa?

Feedback to tax design For overviews: Cowell (2004), Slemrod and Yitzhaki (2002)

Frank Cow

ell: HM

RC-H

MT Econom

ics of Taxation 4

Government

Taxpayers

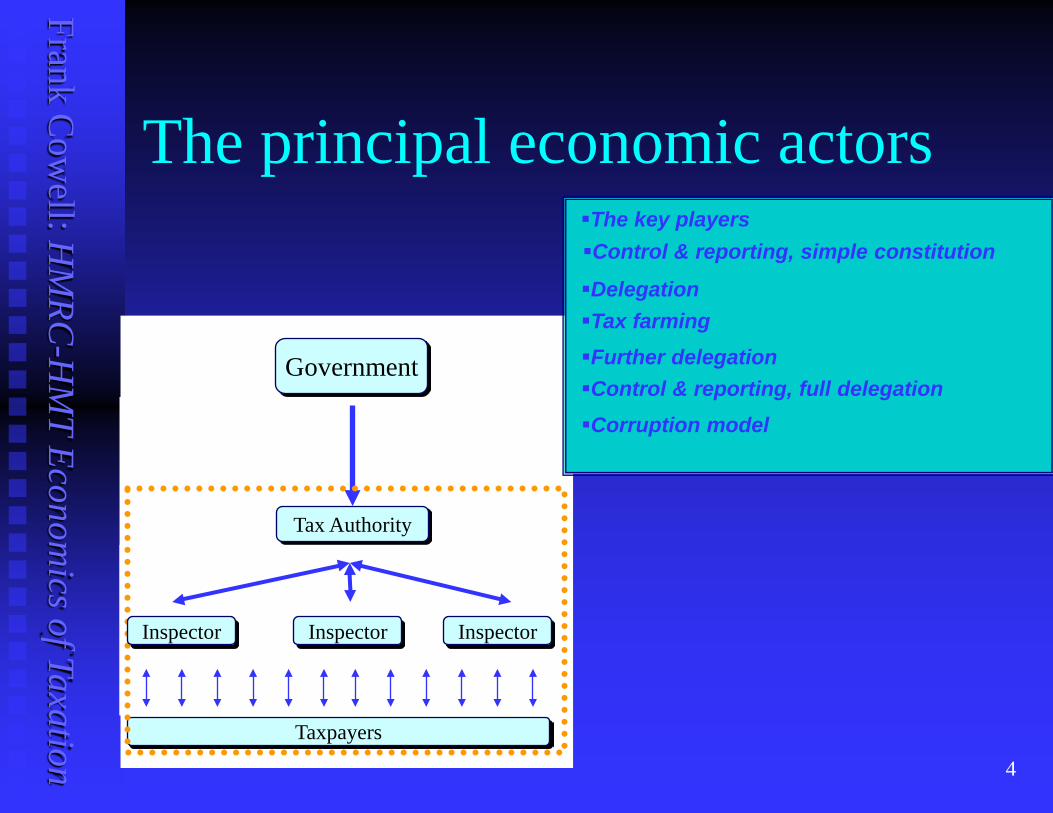

The principal economic actors

Tax Authority

The key players

Delegation Tax farming

Corruption model

Control & reporting, simple constitution

Further delegation

Inspector Inspector Inspector

Control & reporting, full delegation

Frank Cow

ell: HM

RC-H

MT Econom

ics of Taxation 5

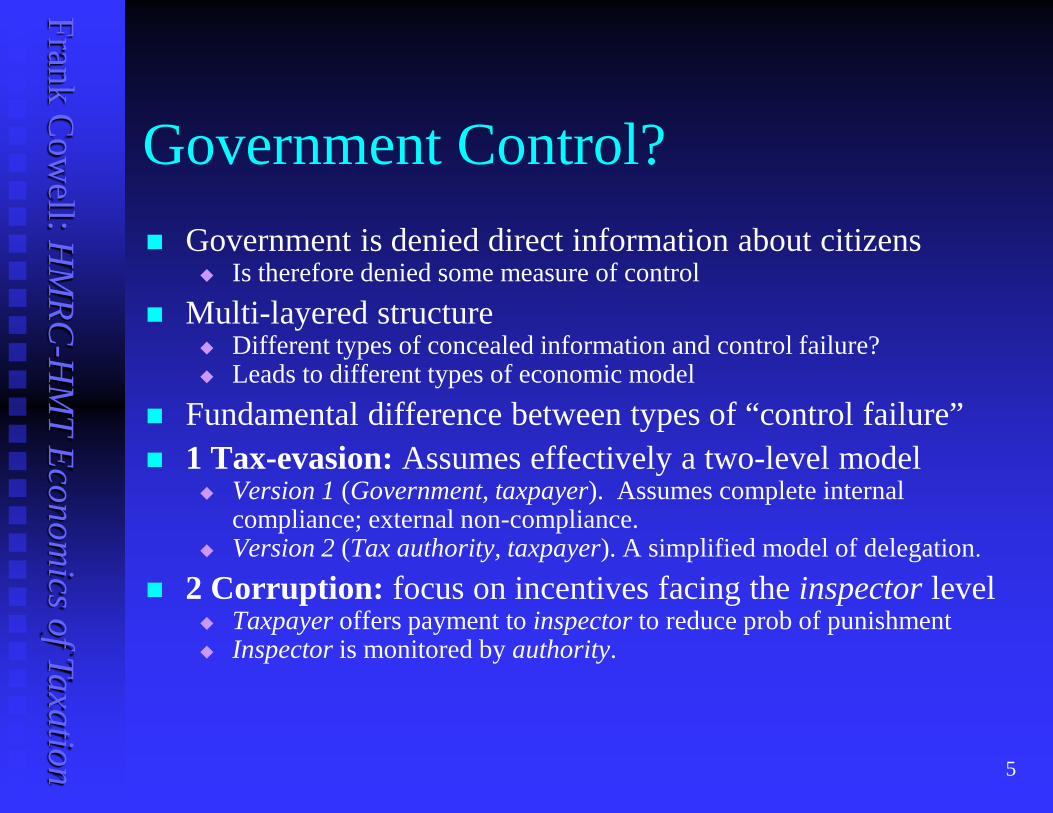

Government Control? Government is denied direct information about citizens

Is therefore denied some measure of control Multi-layered structure

Different types of concealed information and control failure? Leads to different types of economic model

Fundamental difference between types of “control failure” 1 Tax-evasion: Assumes effectively a two-level model

Version 1 (Government, taxpayer). Assumes complete internal compliance; external non-compliance.

Version 2 (Tax authority, taxpayer). A simplified model of delegation.

2 Corruption: focus on incentives facing the inspector level Taxpayer offers payment to inspector to reduce prob of punishment Inspector is monitored by authority.

Frank Cow

ell: HM

RC-H

MT Econom

ics of Taxation 6

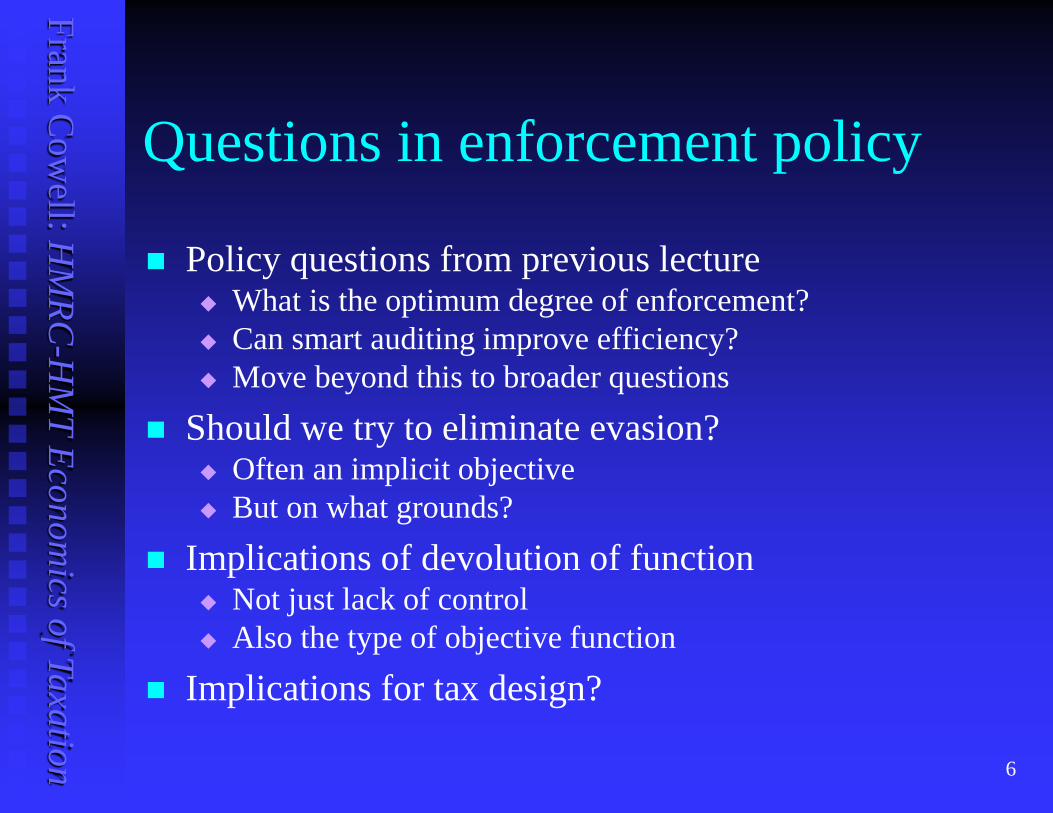

Questions in enforcement policy

Policy questions from previous lecture What is the optimum degree of enforcement? Can smart auditing improve efficiency? Move beyond this to broader questions

Should we try to eliminate evasion? Often an implicit objective But on what grounds?

Implications of devolution of function Not just lack of control Also the type of objective function

Implications for tax design?

Frank Cow

ell: HM

RC-H

MT Econom

ics of Taxation 7

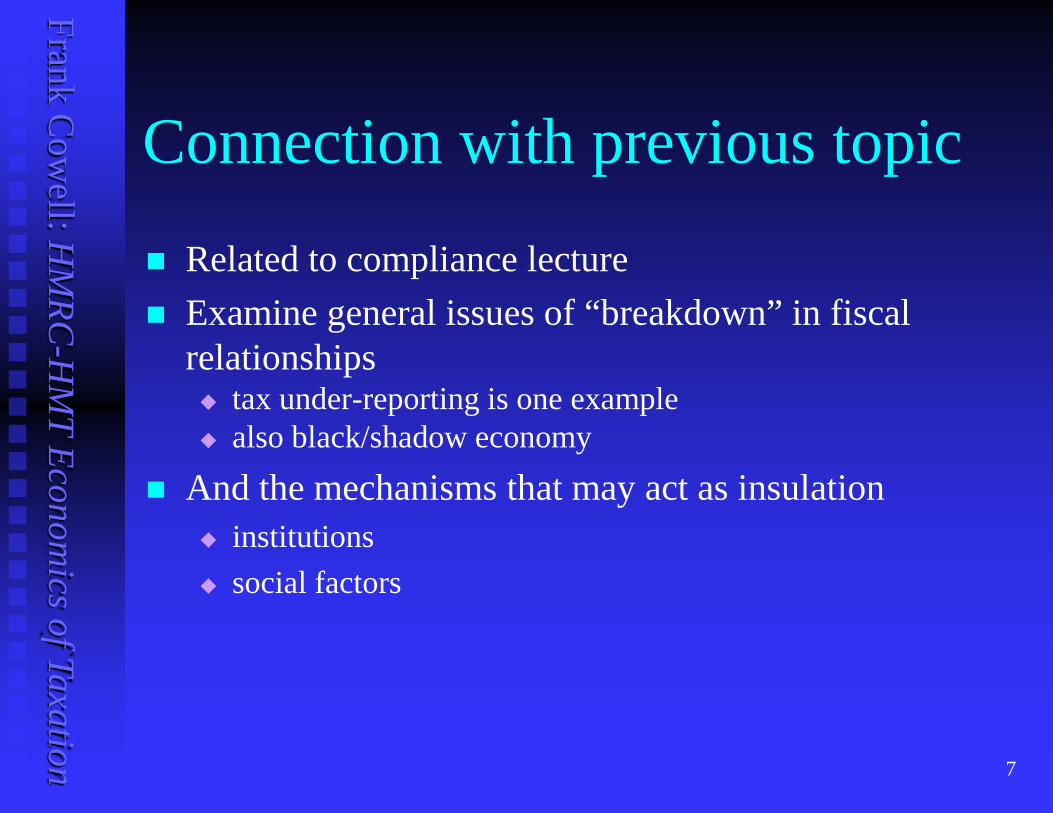

Connection with previous topic

Related to compliance lecture Examine general issues of “breakdown” in fiscal

relationships tax under-reporting is one example also black/shadow economy

And the mechanisms that may act as insulation institutions social factors

Frank Cow

ell: HM

RC-H

MT Econom

ics of Taxation 8

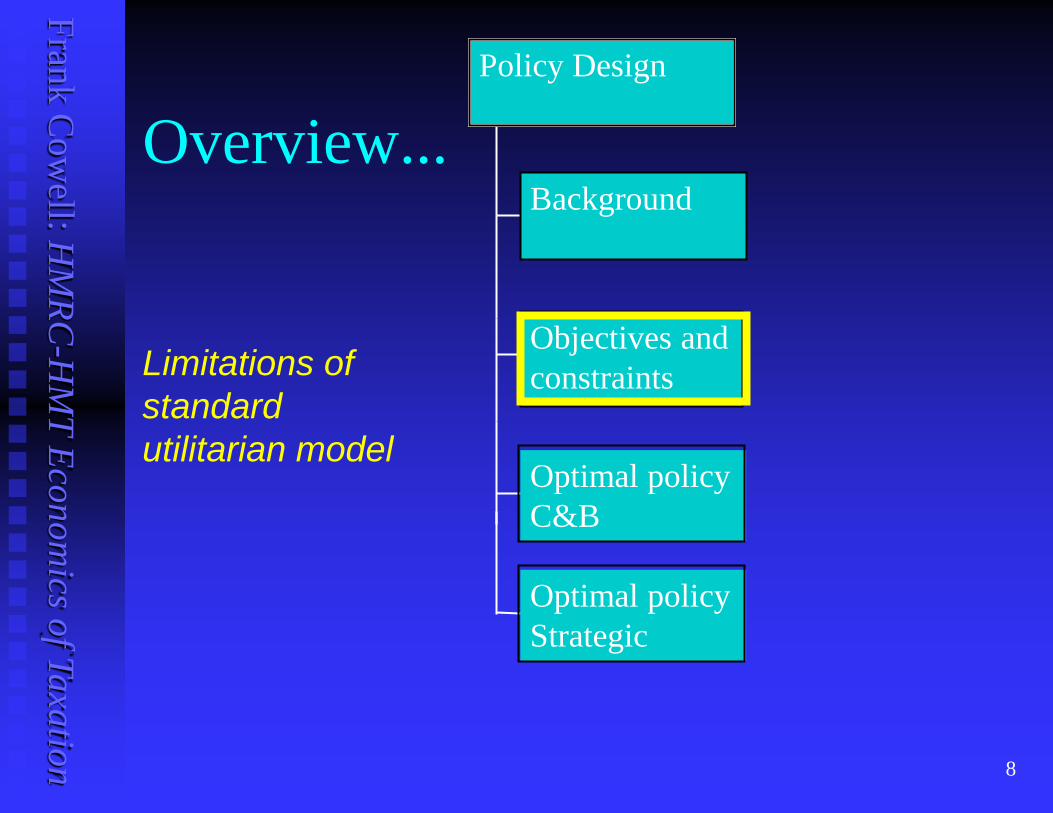

Overview... Background

Objectives and constraints

Optimal policy C&B

Policy Design

Limitations of standard utilitarian model

Optimal policy Strategic

Frank Cow

ell: HM

RC-H

MT Econom

ics of Taxation 9

Modelling issues

What is the appropriate objective? Law enforcement? Eliminate evasion? Welfare of law-abiding citizens? Utilitarianism?

What institutional structure? Direct government-taxpayer relation? Tax collection/enforcement agencies?

What components of the enforcement problem? requires a multi-stage approach see Cowell (1989)

Frank Cow

ell: HM

RC-H

MT Econom

ics of Taxation 10

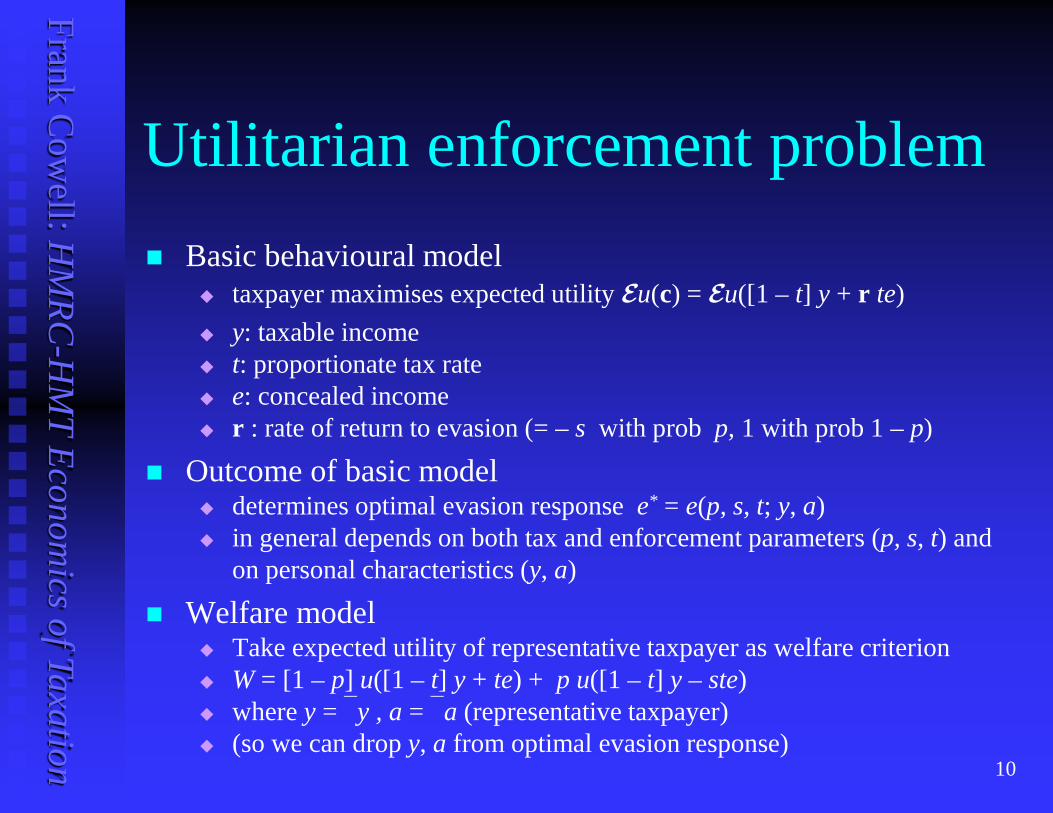

Utilitarian enforcement problem Basic behavioural model

taxpayer maximises expected utility Eu(c) = Eu([1 – t] y + r te) y: taxable income t: proportionate tax rate e: concealed income r : rate of return to evasion (= – s with prob p, 1 with prob 1 – p)

Outcome of basic model determines optimal evasion response e* = e(p, s, t; y, a) in general depends on both tax and enforcement parameters (p, s, t) and

on personal characteristics (y, a)

Welfare model Take expected utility of representative taxpayer as welfare criterion W = [1 – p] u([1 – t] y + te) + p u([1 – t] y – ste) where y = y , a = a (representative taxpayer) (so we can drop y, a from optimal evasion response)

Frank Cow

ell: HM

RC-H

MT Econom

ics of Taxation 11

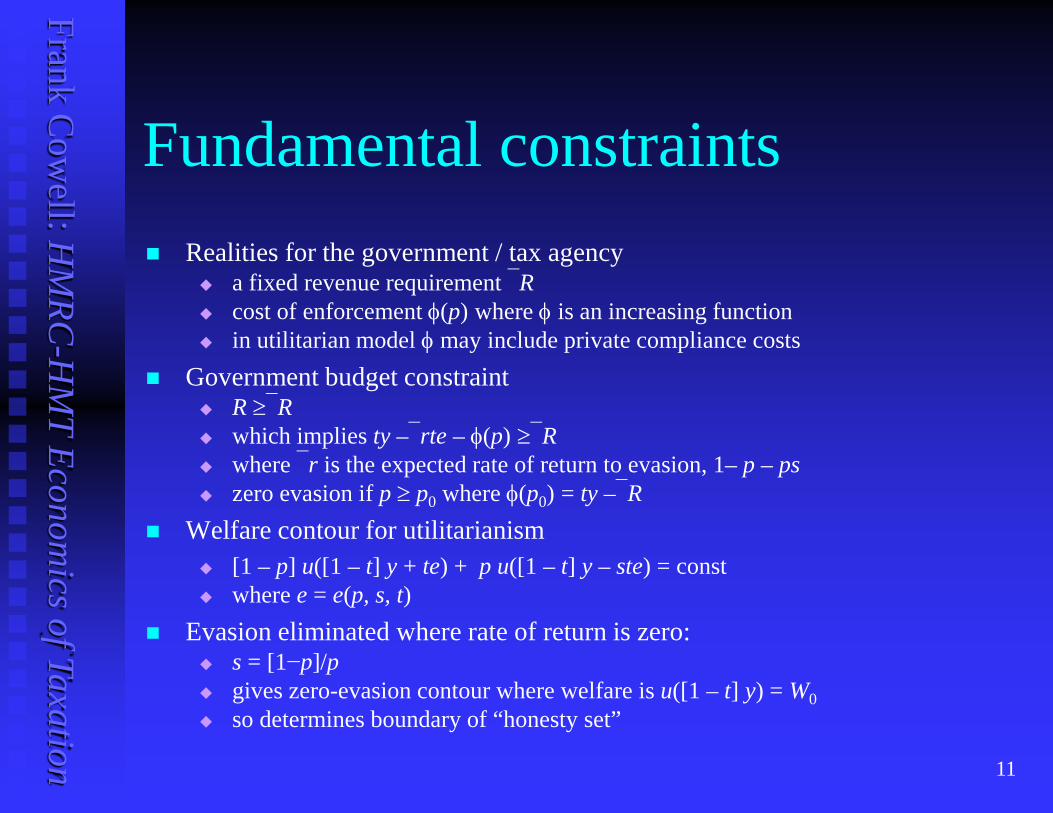

Fundamental constraints Realities for the government / tax agency

a fixed revenue requirement R cost of enforcement φ(p) where φ is an increasing function in utilitarian model φ may include private compliance costs

Government budget constraint R ≥R which implies ty –rte – φ(p) ≥R where r is the expected rate of return to evasion, 1– p – ps zero evasion if p ≥ p0 where φ(p0) = ty –R

Welfare contour for utilitarianism [1 – p] u([1 – t] y + te) + p u([1 – t] y – ste) = const where e = e(p, s, t)

Evasion eliminated where rate of return is zero: s = [1−p]/p gives zero-evasion contour where welfare is u([1 – t] y) = W0 so determines boundary of “honesty set”

Frank Cow

ell: HM

RC-H

MT Econom

ics of Taxation 12

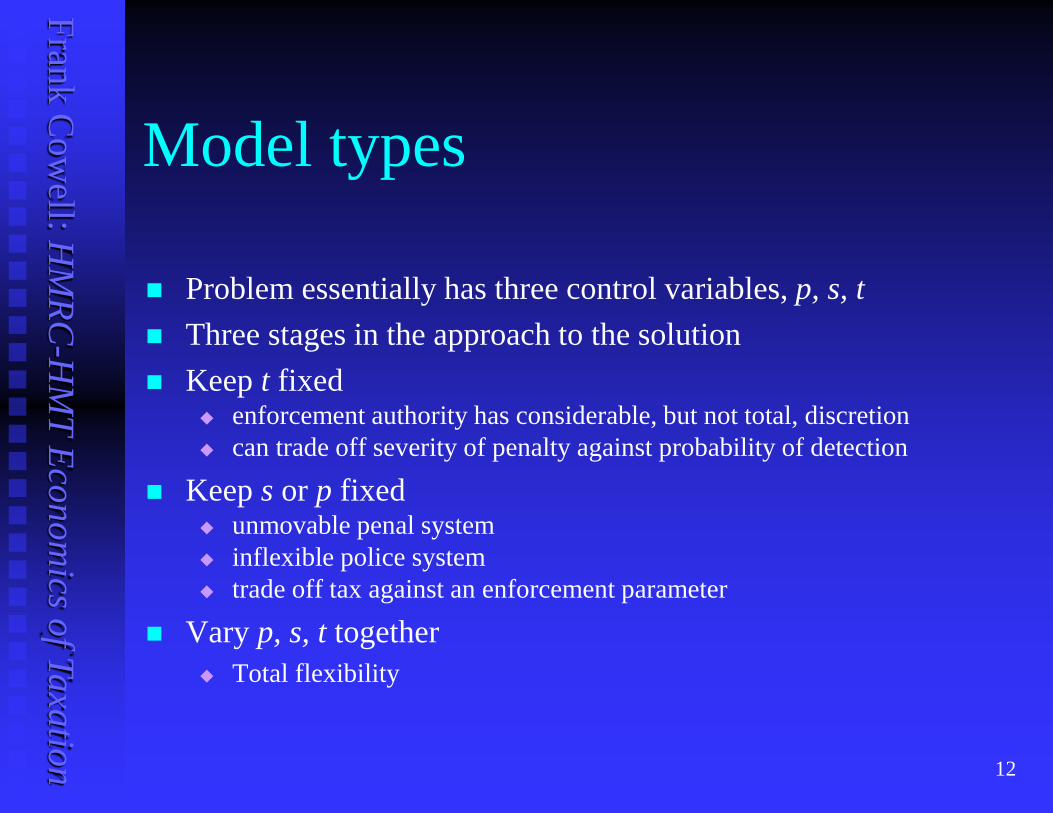

Model types

Problem essentially has three control variables, p, s, t Three stages in the approach to the solution Keep t fixed

enforcement authority has considerable, but not total, discretion can trade off severity of penalty against probability of detection

Keep s or p fixed unmovable penal system inflexible police system trade off tax against an enforcement parameter

Vary p, s, t together Total flexibility

Frank Cow

ell: HM

RC-H

MT Econom

ics of Taxation 13

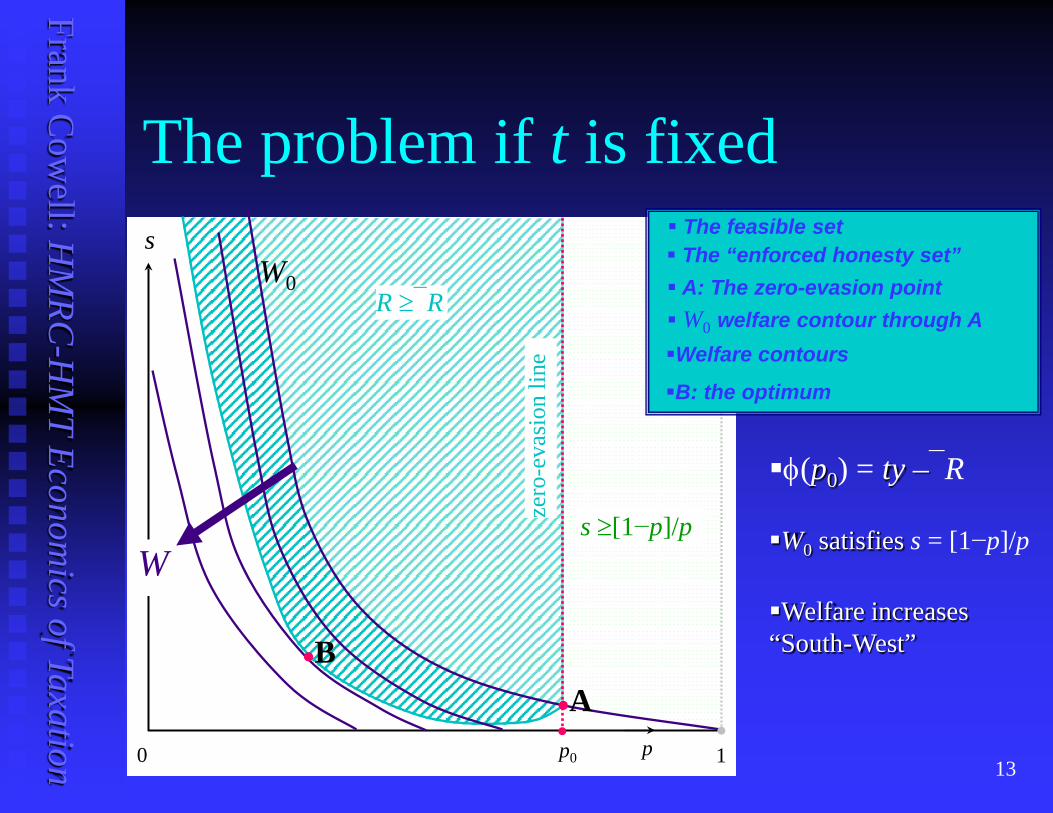

The problem if t is fixed

0 1

s

p

R ≥R

zero

-eva

sion

line

W

W0

s ≥[1−p]/p

p0

A B

The feasible set

A: The zero-evasion point W0 welfare contour through A Welfare contours

B: the optimum

The “enforced honesty set”

φ(p0) = ty –R

W0 satisfies s = [1−p]/p

Welfare increases “South-West”

Frank Cow

ell: HM

RC-H

MT Econom

ics of Taxation 14

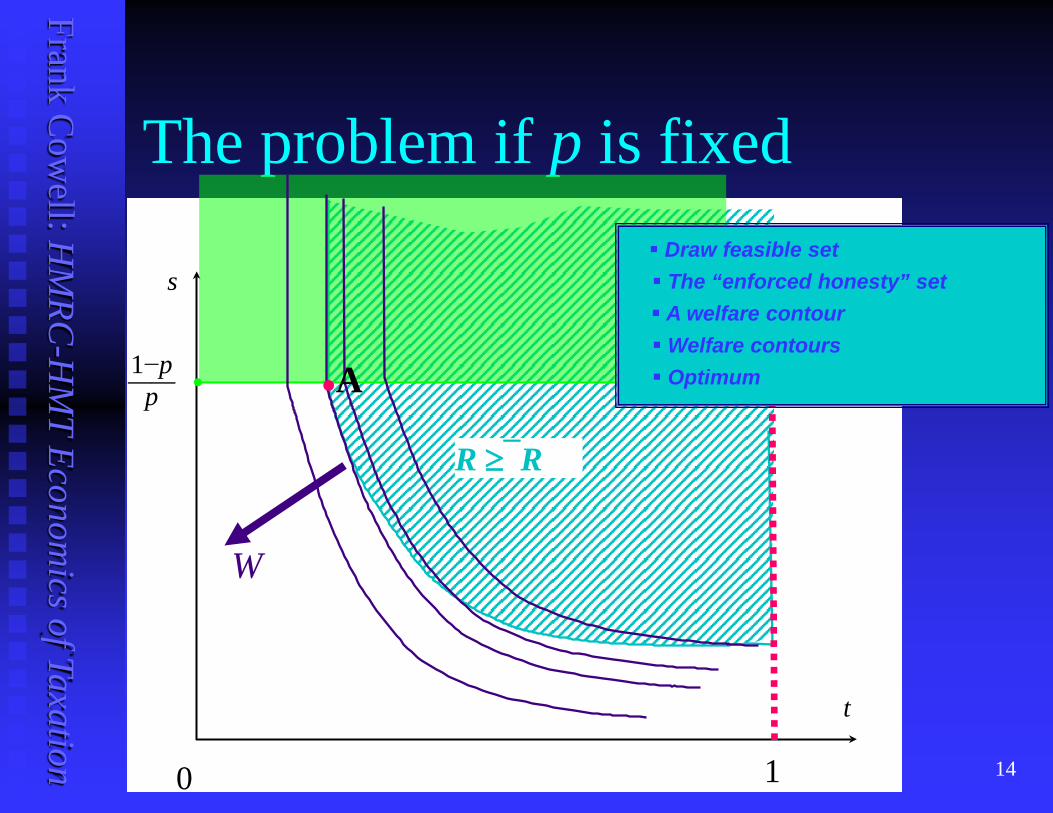

The problem if p is fixed

0 1

s

t

R ≥R

W

1−p —— p A

Draw feasible set

The “enforced honesty” set A welfare contour Welfare contours Optimum

Frank Cow

ell: HM

RC-H

MT Econom

ics of Taxation 15

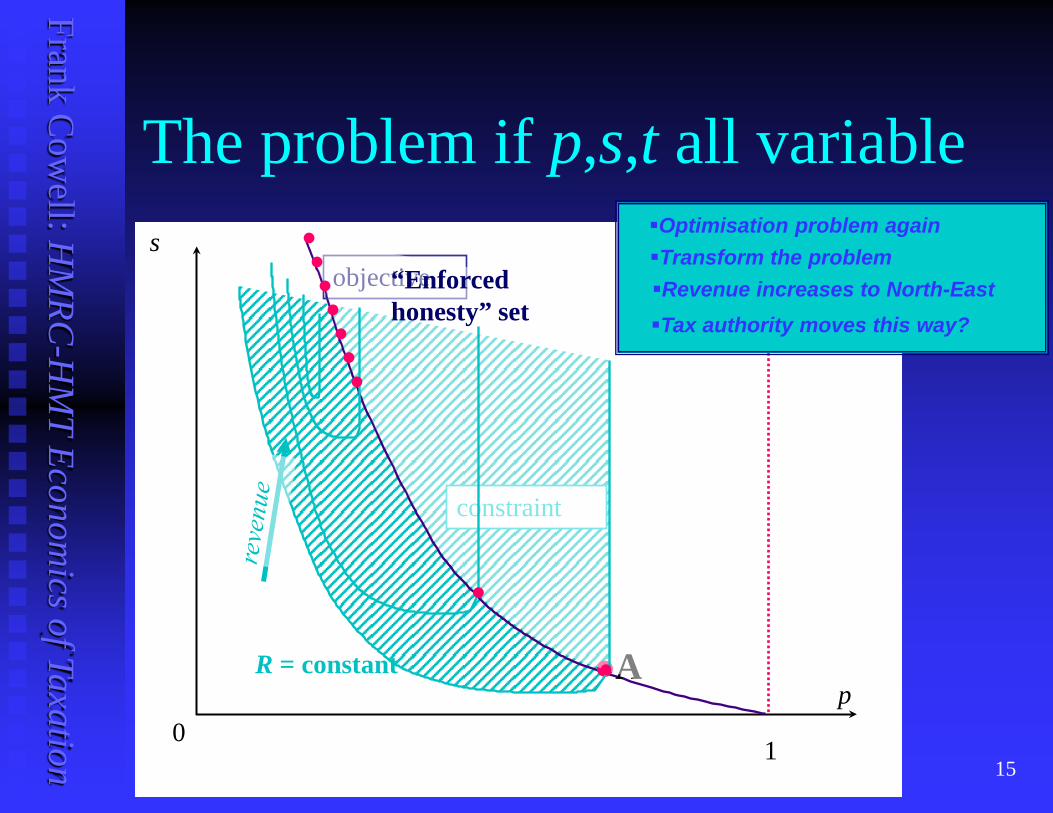

The problem if p,s,t all variable

0 1

s

p A

objective

constraint

Optimisation problem again Transform the problem

“Enforced honesty” set

Revenue increases to North-East

R = constant

Tax authority moves this way?

Frank Cow

ell: HM

RC-H

MT Econom

ics of Taxation 16

Overview... Background

Objectives and constraints

Optimal policy C&B

Policy Design

A utilitarian approach

Optimal policy Strategic

Frank Cow

ell: HM

RC-H

MT Econom

ics of Taxation 17

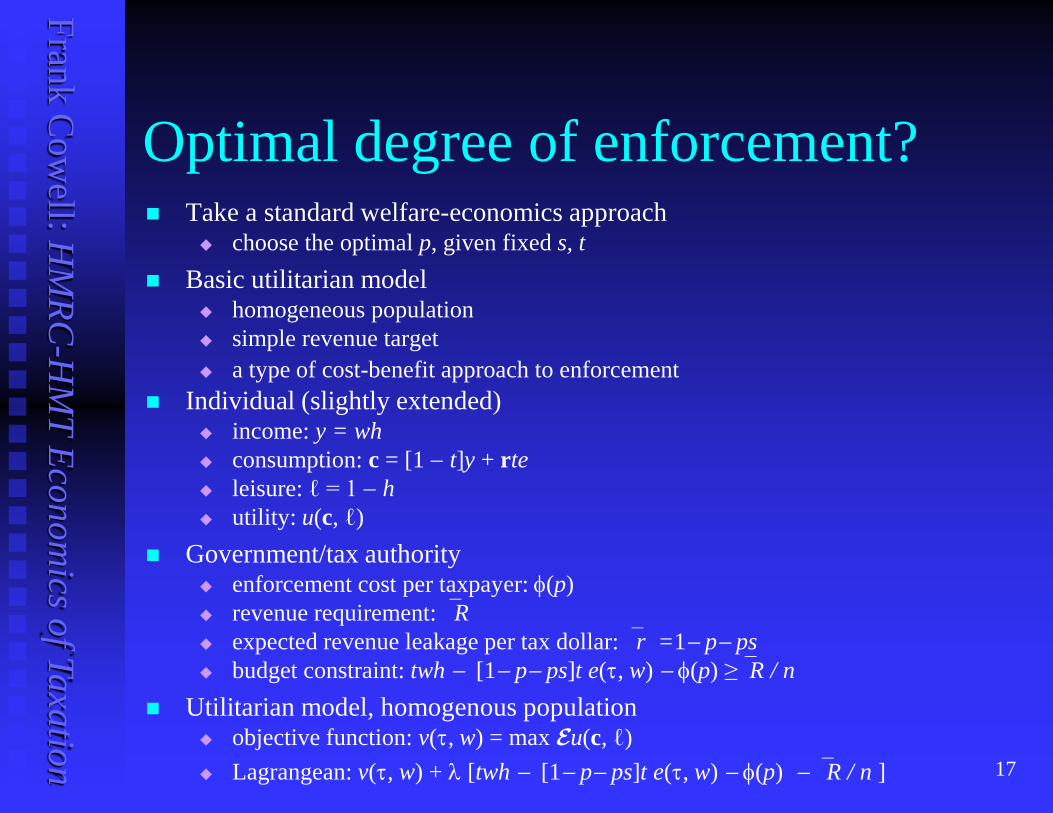

Optimal degree of enforcement? Take a standard welfare-economics approach

choose the optimal p, given fixed s, t Basic utilitarian model

homogeneous population simple revenue target a type of cost-benefit approach to enforcement

Individual (slightly extended) income: y = wh consumption: c = [1 − t]y + rte leisure: ℓ = 1 − h utility: u(c, ℓ)

Government/tax authority enforcement cost per taxpayer: φ(p) revenue requirement: R expected revenue leakage per tax dollar: r =1− p− ps budget constraint: twh − [1− p− ps]t e(τ, w) − φ(p) ≥R / n

Utilitarian model, homogenous population objective function: v(τ, w) = max Eu(c, ℓ) Lagrangean: v(τ, w) + λ [twh − [1− p− ps]t e(τ, w) − φ(p) − R / n ]

Frank Cow

ell: HM

RC-H

MT Econom

ics of Taxation 18

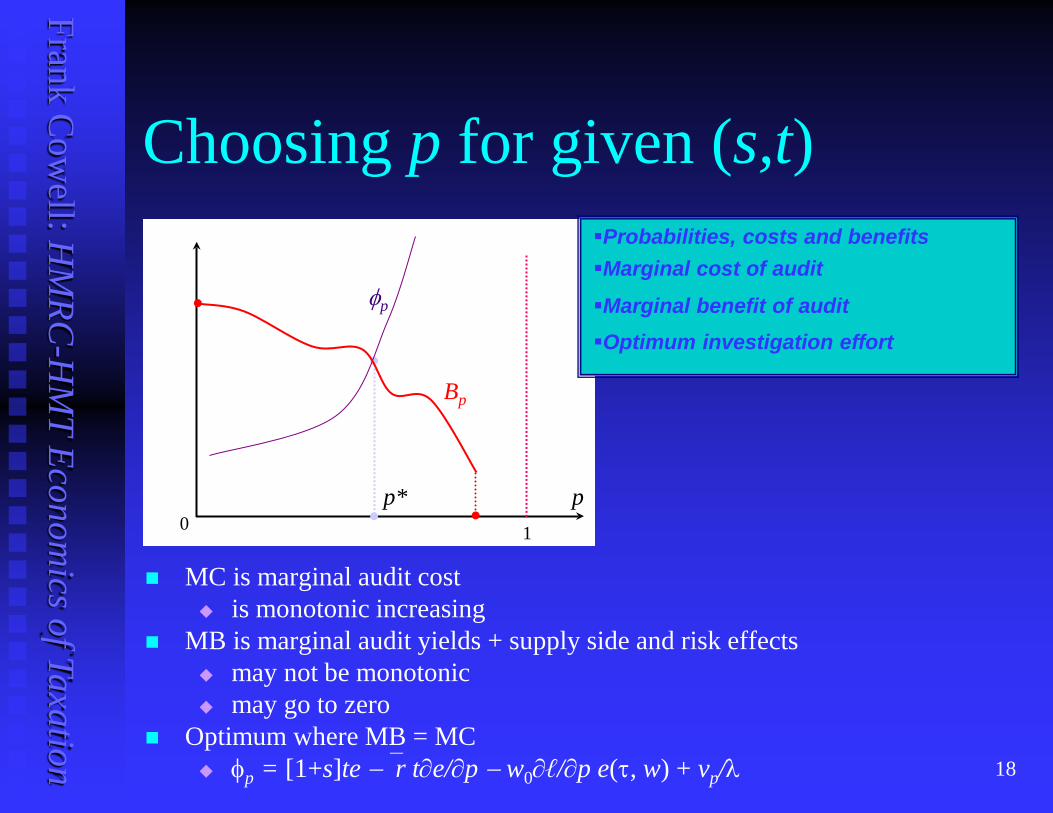

Choosing p for given (s,t)

MC is marginal audit cost

is monotonic increasing MB is marginal audit yields + supply side and risk effects

may not be monotonic may go to zero

Optimum where MB = MC φp = [1+s]te −r t∂e/∂p − w0∂ℓ/∂p e(τ, w) + vp/λ

0 1

p

φp

Bp

p*

Probabilities, costs and benefits Marginal cost of audit

Marginal benefit of audit Optimum investigation effort

Frank Cow

ell: HM

RC-H

MT Econom

ics of Taxation 19

Extensions – agent interaction Cost-benefit approach is essentially individualistic

compute MB for each agent Social interaction models

prevent epidemics? shift the equilibrium? manipulate expectations? Iyer et al 2010) raise search costs?

Focus on smart use of information recognise that agents may have better market information than tax authority exploit information about all agents’ behaviour

Example: tax compliance by firms use of information: compare simple auditing with relative auditing relationships amongst firms is essential to the impact of policy choice Cournot behaviour: get effect on output as well as tax receipts collusion amongst firms – smart auditing less effective (Bayer and Cowell 2009)

Examine smart auditing further in a reporting model

Frank Cow

ell: HM

RC-H

MT Econom

ics of Taxation 20

Overview... Background

Objectives and constraints

Optimal policy C&B

Policy Design

Strategic approach to audit policy

Optimal policy Strategic

Frank Cow

ell: HM

RC-H

MT Econom

ics of Taxation 21

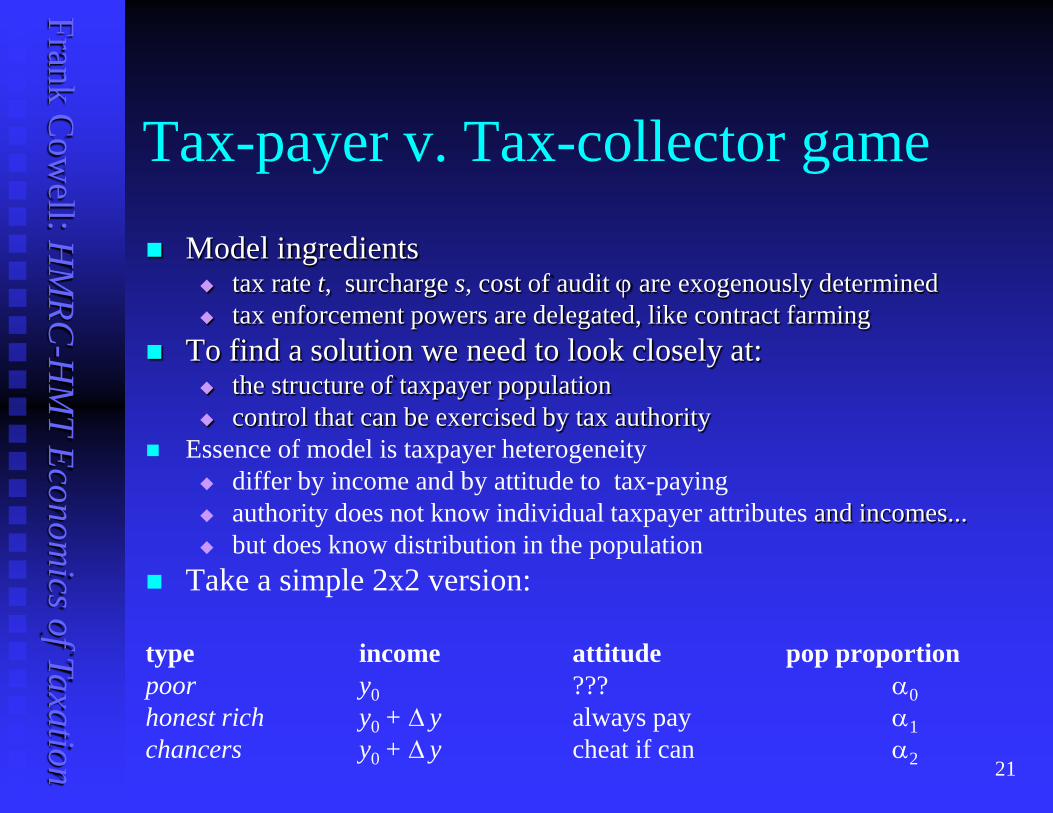

Tax-payer v. Tax-collector game Model ingredients

tax rate t, surcharge s, cost of audit ϕ are exogenously determined tax enforcement powers are delegated, like contract farming

To find a solution we need to look closely at: the structure of taxpayer population control that can be exercised by tax authority

Essence of model is taxpayer heterogeneity differ by income and by attitude to tax-paying authority does not know individual taxpayer attributes and incomes... but does know distribution in the population

Take a simple 2x2 version:

type income attitude pop proportion poor y0 ??? α0 honest rich y0 + ∆ y always pay α1 chancers y0 + ∆ y cheat if can α2

Frank Cow

ell: HM

RC-H

MT Econom

ics of Taxation 22

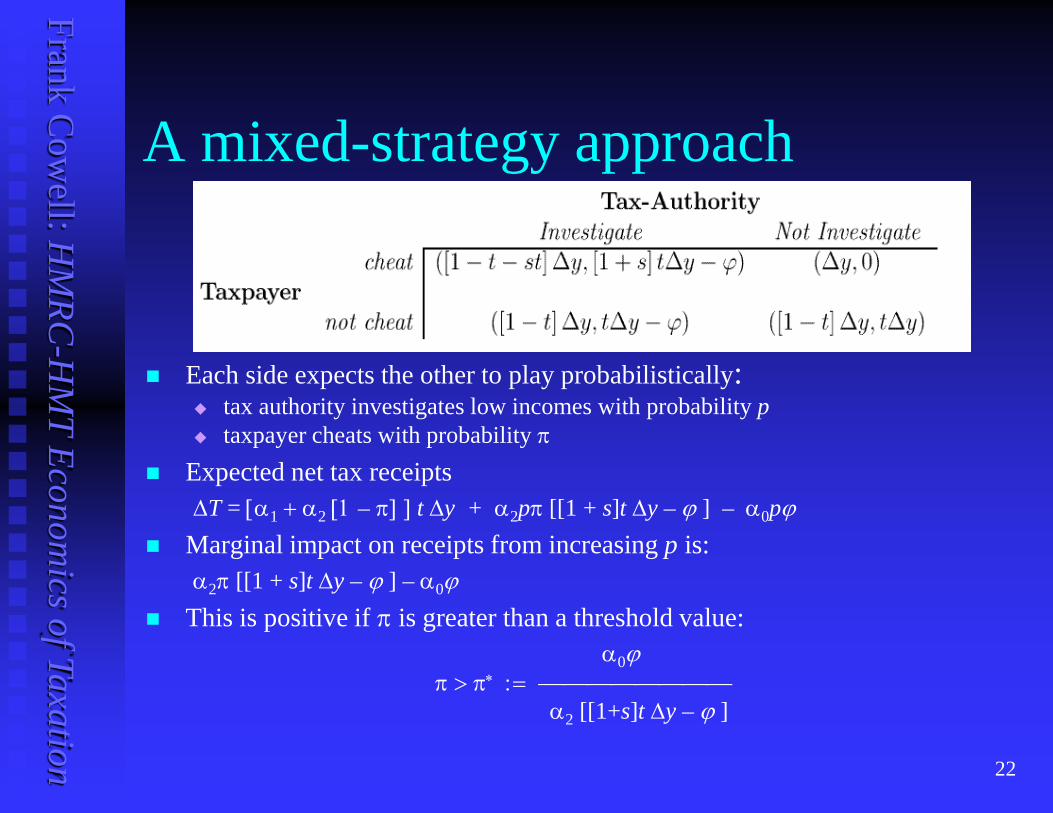

A mixed-strategy approach

Each side expects the other to play probabilistically: tax authority investigates low incomes with probability p taxpayer cheats with probability π

Expected net tax receipts ∆T = [α1 + α2 [1 – π] ] t ∆y + α2pπ [[1 + s]t ∆y – ϕ ] – α0pϕ

Marginal impact on receipts from increasing p is: α2π [[1 + s]t ∆y – ϕ ] – α0ϕ

This is positive if π is greater than a threshold value: α0ϕ

π > π∗ := α2 [[1+s]t ∆y – ϕ ]

Frank Cow

ell: HM

RC-H

MT Econom

ics of Taxation 23

Equilibrium concepts

Taxpayers and tax agency each form beliefs about the other’s actions

Equilibrium where each adopts a consistent set of beliefs

What is the optimal “tailored” audit strategy? Two types of relationship between taxpayer and tax

authority: tax authority precommits to a strategy tax authority does not precommit see Reinganum and Wilde (1985, 1986)

Frank Cow

ell: HM

RC-H

MT Econom

ics of Taxation 24

Precommitment: policy If the tax authority were permissive, net receipts would be low:

∆T|π=1,p=0 = α1 t ∆y

If authority can commit it ought to audit all low-income reports: p = 0 if report is y0 + ∆y p = 1 if report is y0

Tax receipts net of audit costs are ∆T|π=0,p=1 = [α1 + α2] t ∆y – α0ϕ

This amounts to a “Punish the poor” policy Is this in fact optimal?

viability credibility

Frank Cow

ell: HM

RC-H

MT Econom

ics of Taxation 25

Precommitment: optimality? Condition 1 for financial viability is:

∆T|π=0,p=1 ≥ ∆T|π=1,p=0 [α1 + α2] t ∆y – α0pϕ ≥ α1t ∆y α2t ∆y ≥ α0ϕ

Condition 2 for financial viability is: net return from investigating a false report must be non-negative [1 + s] t ∆y – ϕ ≥ 0

Combining the two conditions [1 + s] t ∆y – ϕ ≥ [1 + s – [α2/α0]]t ∆y satisfied if audit cost is not too high and there are not too many honest people

Credibility: everyone sees that only the genuinely poor people are audited no revenue is ever raised in equilibrium policy may not be credible in a repeated setting

Frank Cow

ell: HM

RC-H

MT Econom

ics of Taxation 26

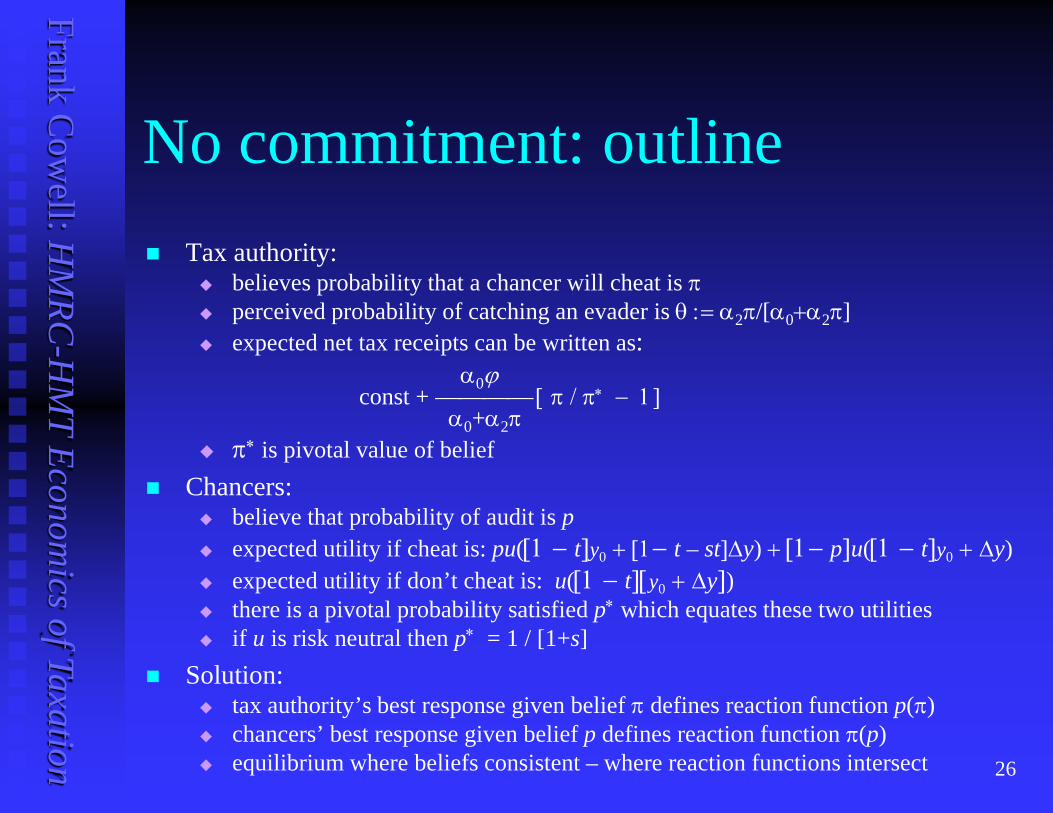

No commitment: outline Tax authority:

believes probability that a chancer will cheat is π perceived probability of catching an evader is θ := α2π/[α0+α2π] expected net tax receipts can be written as:

α0ϕ const + [ π / π∗ − 1] α0+α2π

π∗ is pivotal value of belief Chancers:

believe that probability of audit is p expected utility if cheat is: pu([1 − t]y0 + [1− t – st]∆y) + [1− p]u([1 − t]y0 + ∆y) expected utility if don’t cheat is: u([1 − t][y0 + ∆y]) there is a pivotal probability satisfied p∗ which equates these two utilities if u is risk neutral then p∗ = 1 / [1+s]

Solution: tax authority’s best response given belief π defines reaction function p(π) chancers’ best response given belief p defines reaction function π(p) equilibrium where beliefs consistent – where reaction functions intersect

Frank Cow

ell: HM

RC-H

MT Econom

ics of Taxation 27

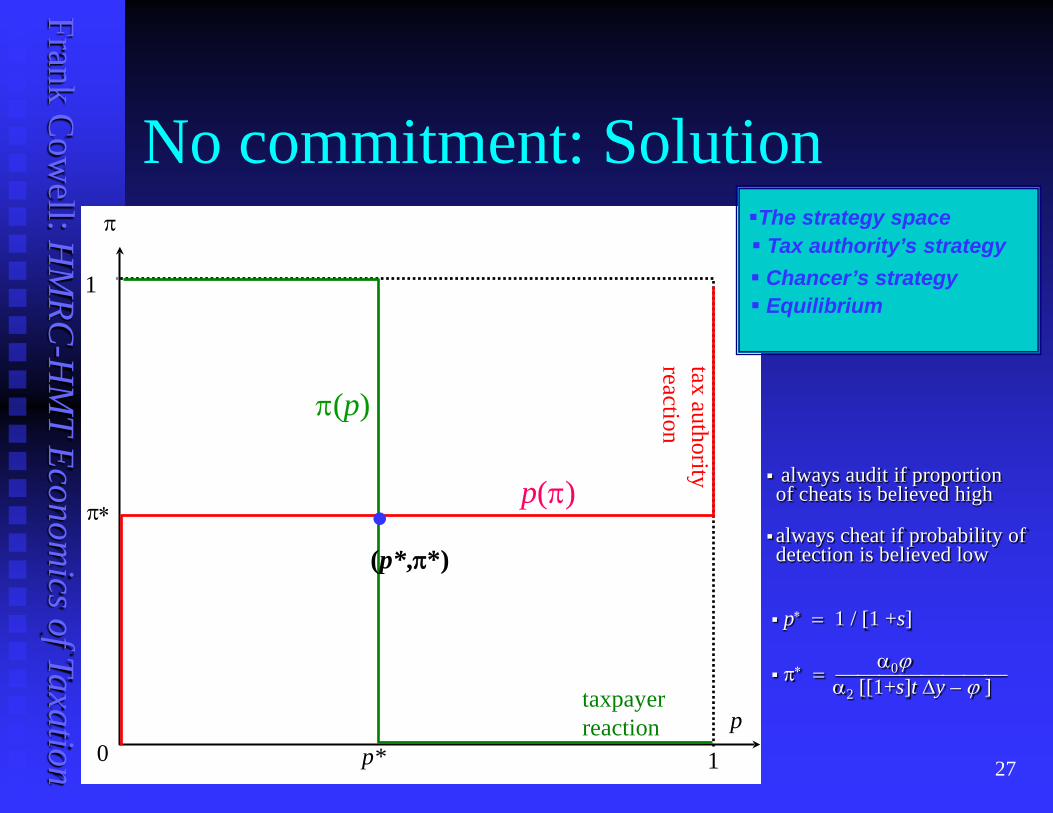

No commitment: Solution

1

0 1

π∗

p*

π

taxpayer reaction

tax authority reaction

p

p(π)

π(p)

• (p*,π*)

always audit if proportion of cheats is believed high

always cheat if probability of detection is believed low

The strategy space Tax authority’s strategy Chancer’s strategy Equilibrium

p∗ = 1 / [1 +s] α0ϕ π∗ =

α2 [[1+s]t ∆y – ϕ ]

Frank Cow

ell: HM

RC-H

MT Econom

ics of Taxation 28

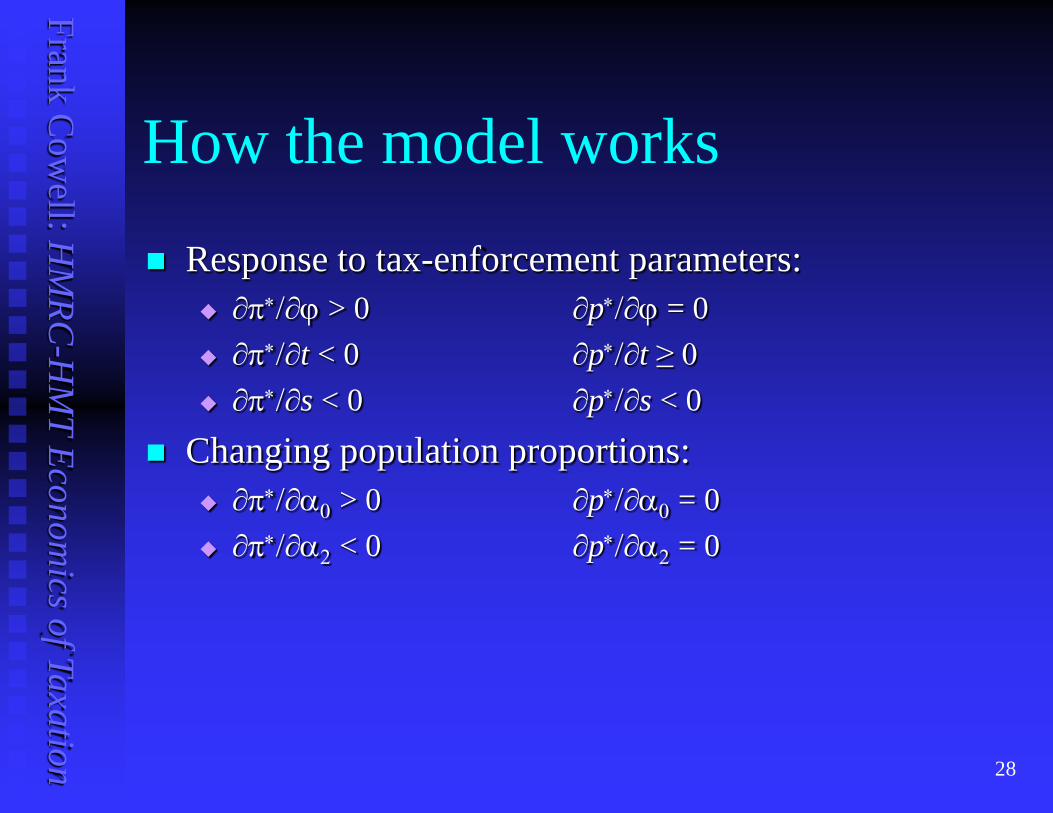

How the model works

Response to tax-enforcement parameters: ∂π∗/∂ϕ > 0 ∂p∗/∂ϕ = 0 ∂π∗/∂t < 0 ∂p∗/∂t ≥ 0 ∂π∗/∂s < 0 ∂p∗/∂s < 0

Changing population proportions: ∂π∗/∂α0 > 0 ∂p∗/∂α0 = 0 ∂π∗/∂α2 < 0 ∂p∗/∂α2 = 0

Frank Cow

ell: HM

RC-H

MT Econom

ics of Taxation 29

Assessment

Compliance is a central component of public economics Arises naturally from the issues concerning the provision of public

goods Analysed using standard microeconomic techniques

Incentives issues similar to those of labour supply Important to model the interactions involved in evasion

Perceptions of others’ behaviour may be important. Also interaction between tax-payers and enforcement agencies

Crucial issues on policy concern the institutional background What is the nature of the optimisation problem?

Is a standard reporting model appropriate? What information should each party be assumed to have?

Frank Cow

ell: HM

RC-H

MT Econom

ics of Taxation 30

References Cowell, F. A. (1989) “Honesty is sometimes the best policy,” European Economic

Review, 33,605-617 * Cowell, F. A. (2004) “Carrots and Sticks in Enforcement” in Aaron, H. J. and

Slemrod, J. (ed.) The Crisis in Tax Administration, The Brookings Institution, Washington DC, 230-275

Iyengar, R. (2008) “I'd rather be Hanged for a Sheep than a Lamb: The Unintended Consequences of 'Three-Strikes' Laws,” NBER Working Paper, 13784

Iyer, G.S. , Reckers, P.M.J. and Sanders, D.L. (2010) “Increasing Tax Compliance in Washington State: A Field Experiment,” National Tax Journal, 63,7-32,

Reinganum, J. F. and L. L. Wilde (1985) “Income tax compliance in a principal-agent framework ,” Journal of Public Economics, 26, 1-18.

Reinganum, J. F. and L. L. Wilde (1986) “Equilibrium verification and reporting policies in a model of tax compliance,” International Economic Review, 27, 739-760.

* Slemrod, J. and Yitzhaki, S. (2002) “Tax avoidance, evasion and administration,” Handbook of Public Economics, Volume 3, pp 1423-1470, North-Holland, Elsevier

![[PPT]No Slide Title - The Subjective Approach to Inequality ...darp.lse.ac.uk/.../HMRC-HMT/EconomicsTaxation_9_1.ppt · Web view* Frank Cowell: HMRC-HMT Economics of Taxation * Logic](https://static.fdocuments.in/doc/165x107/5aa2b4ac7f8b9a80378d5213/pptno-slide-title-the-subjective-approach-to-inequality-darplseacukhmrc-hmteconomicstaxation91pptweb.jpg)