Frank Cowell: EC426 Public Economics MSc Public Economics 2011/12 Commodity Taxation Frank A....

30

Frank Cowell: Frank Cowell: EC426 EC426 Public Economics Public Economics MSc Public Economics 2011/12 http://darp.lse.ac.uk/ec426/ Commodity Taxation Commodity Taxation Frank A. Cowell Frank A. Cowell 31 October 2011

Transcript of Frank Cowell: EC426 Public Economics MSc Public Economics 2011/12 Commodity Taxation Frank A....

Frank C

owell:

Frank C

owell: E

C426

EC

426 Public E

conomics

Public E

conomics

MSc Public Economics 2011/12

http://darp.lse.ac.uk/ec426/

Commodity TaxationCommodity Taxation

Frank A. Cowell Frank A. Cowell

31 October 2011

Frank C

owell:

Frank C

owell: E

C426

EC

426 Public E

conomics

Public E

conomics

Reusing what we know

General results – what do we know?General results – what do we know? On commodity taxationOn commodity taxation On personal income taxOn personal income tax

Derive “optimal” commodity tax rulesDerive “optimal” commodity tax rules using standard second-best techniquesusing standard second-best techniques a case for simplification?a case for simplification?

Commodity tax rules on reformCommodity tax rules on reform Integration with income tax?Integration with income tax?

Issues of informationIssues of information Modelling of incentivesModelling of incentives

For overview and introductionFor overview and introduction Salanié, B. (2003)Salanié, B. (2003) Kaplow ((2008b), pp125-136

Frank C

owell:

Frank C

owell: E

C426

EC

426 Public E

conomics

Public E

conomics

Overview...

Optimal tax rules

Commodity Taxation

An application of standard efficiency analysis

Commodity tax reform

Commodity tax and income tax

Frank C

owell:

Frank C

owell: E

C426

EC

426 Public E

conomics

Public E

conomics

Commodity tax: approach

Basic questions:Basic questions: Can we set up a well-defined optimisation problem?Can we set up a well-defined optimisation problem? If so, what criteria should be applied to the problem?If so, what criteria should be applied to the problem? Is there a case for taxing all commodities at the same rate?Is there a case for taxing all commodities at the same rate? If not, on which commodities should the tax burden fall more heavily?If not, on which commodities should the tax burden fall more heavily?

Model role of the government as intervention in the price systemModel role of the government as intervention in the price system Price “wedges” are used to raise the required revenuePrice “wedges” are used to raise the required revenue

Taxes expressed as either Taxes expressed as either An absolute addition to the producer price (a “specific tax” rate An absolute addition to the producer price (a “specific tax” rate tt)) A percentage increase in the price (an “ad valorem tax” rate A percentage increase in the price (an “ad valorem tax” rate ))

Proceed in stagesProceed in stages Start with heuristic argument based on standard applied welfare Start with heuristic argument based on standard applied welfare

economics (Cf economics (Cf Coady and Drèze 2002)) Then Ramsey modelThen Ramsey model Then generalisationsThen generalisations

Frank C

owell:

Frank C

owell: E

C426

EC

426 Public E

conomics

Public E

conomics

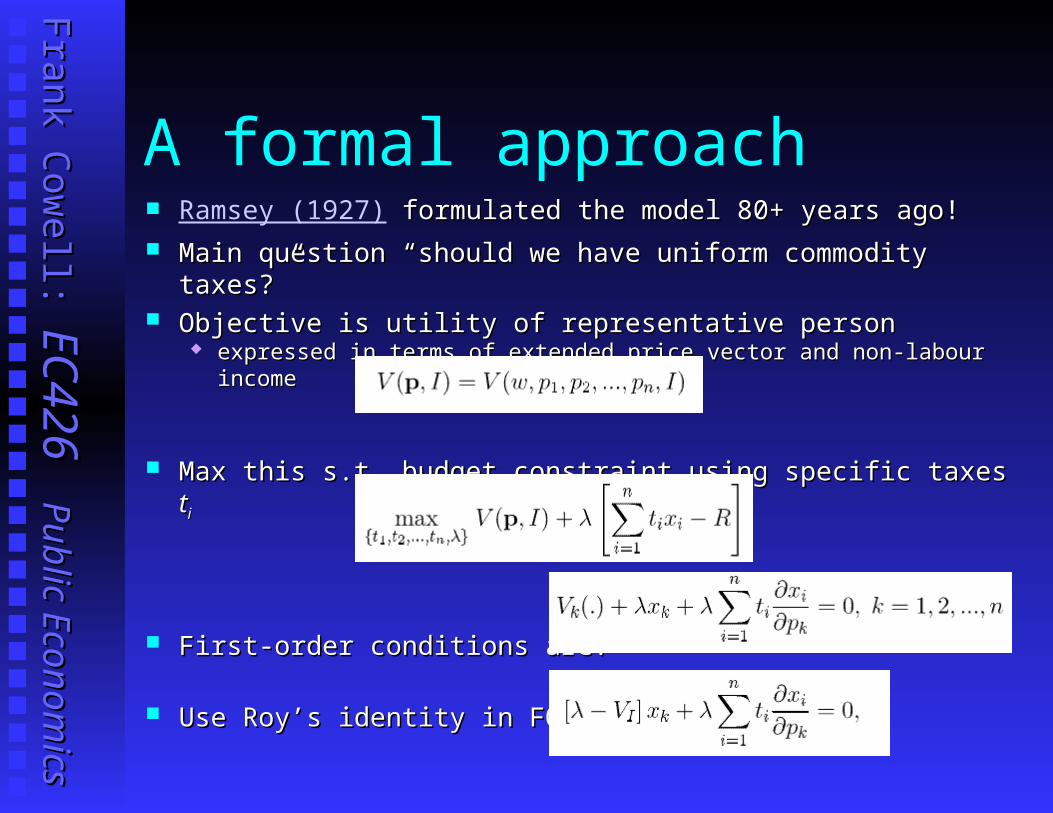

A formal approach Ramsey (1927) formulated the model 80+ years ago! formulated the model 80+ years ago! Main question “should we have uniform commodity taxes?”Main question “should we have uniform commodity taxes?” Objective is utility of representative person Objective is utility of representative person

expressed in terms of extended price vector and non-labour incomeexpressed in terms of extended price vector and non-labour income

Max this s.t. budget constraint using specific taxes Max this s.t. budget constraint using specific taxes ttii

First-order conditions are:First-order conditions are:

Use Roy’s identity in FOC:Use Roy’s identity in FOC:

Frank C

owell:

Frank C

owell: E

C426

EC

426 Public E

conomics

Public E

conomics

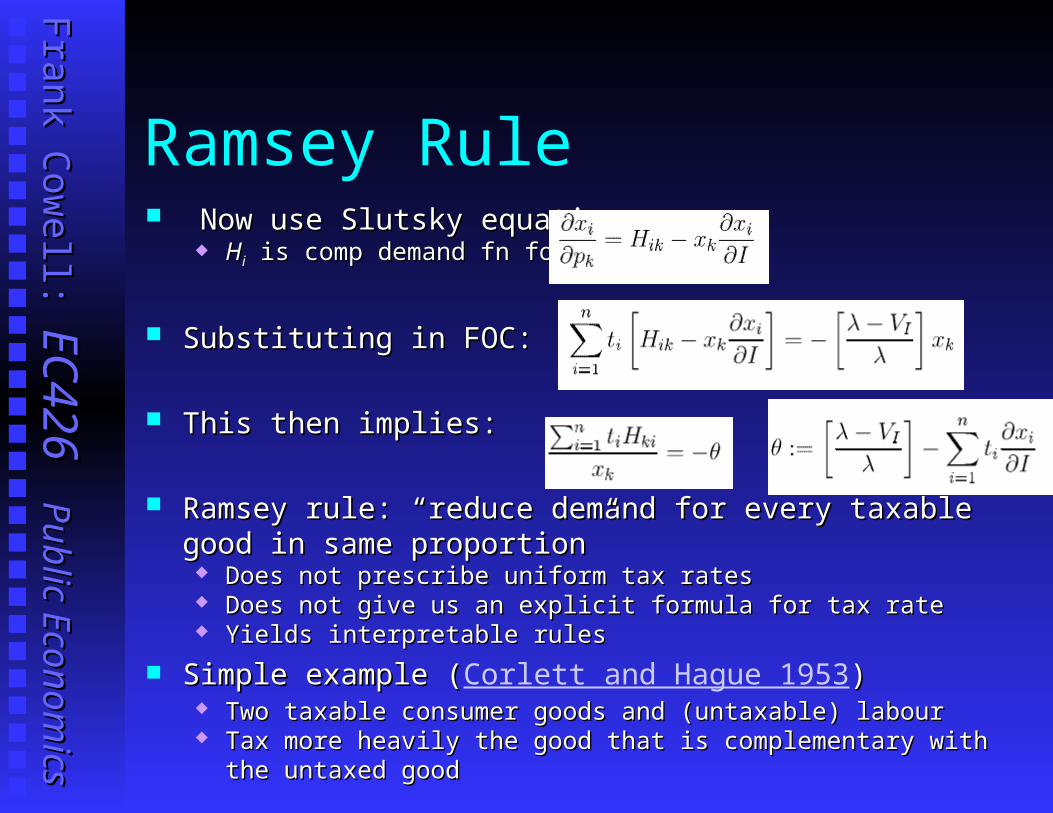

Ramsey Rule Now use Slutsky equation:Now use Slutsky equation:

HHii is comp demand fn for is comp demand fn for ii

Substituting in FOC:Substituting in FOC:

This then implies:This then implies:

Ramsey rule: “reduce demand for every taxable good in same Ramsey rule: “reduce demand for every taxable good in same proportion”proportion”

Does not prescribe uniform tax ratesDoes not prescribe uniform tax rates Does not give us an explicit formula for tax rateDoes not give us an explicit formula for tax rate Yields interpretable rulesYields interpretable rules

Simple example (Simple example (Corlett and Hague 1953)) Two taxable consumer goods and (untaxable) labourTwo taxable consumer goods and (untaxable) labour Tax more heavily the good that is complementary with the untaxed goodTax more heavily the good that is complementary with the untaxed good

Frank C

owell:

Frank C

owell: E

C426

EC

426 Public E

conomics

Public E

conomics

Atkinson-Stiglitz interpretation

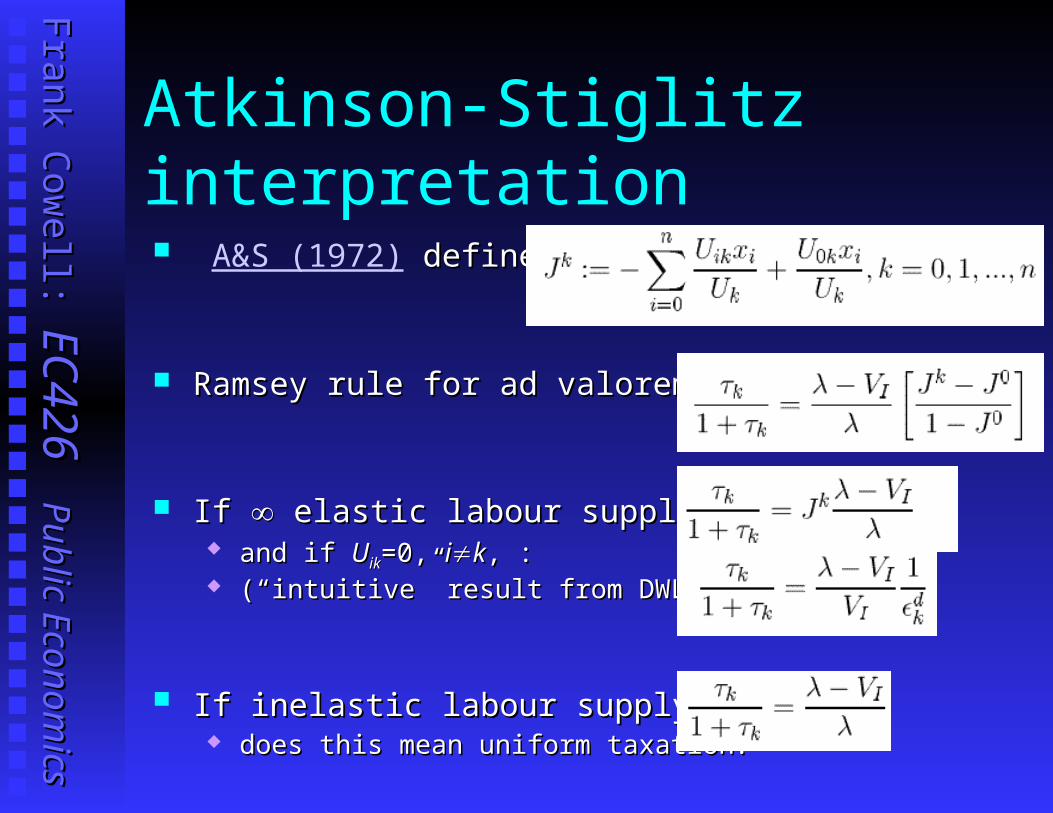

A&S (1972) d define:efine:

Ramsey rule for ad valorem taxes:Ramsey rule for ad valorem taxes:

If If elastic labour supply ( elastic labour supply (JJ00=0) =0) and if and if UUikik=0, =0, iikk, :, : (“intuitive” result from DWL argument)(“intuitive” result from DWL argument)

If inelastic labour supply (If inelastic labour supply (JJ00==)) does this mean uniform taxation?does this mean uniform taxation?

Frank C

owell:

Frank C

owell: E

C426

EC

426 Public E

conomics

Public E

conomics

Uniform Taxation? The basis for a “common sense” guideline?The basis for a “common sense” guideline? Consider budget constraint in Ramsey-type model ifConsider budget constraint in Ramsey-type model if

good 0 (labour) is untaxable good 0 (labour) is untaxable and the amount of labour is fixed at and the amount of labour is fixed at KK

So budget constraint isSo budget constraint is nn

qqii[1+[1+ii]]xxii wKwK

ii=1=1

qqii is producer price of good is producer price of good ii i i is ad valorem tax on good is ad valorem tax on good ii

Under uniform commodity taxation this becomes:Under uniform commodity taxation this becomes: nn

qqiixxii wKwK / [1+ / [1+]]

ii=1=1

But this is equivalent to lump-sum taxation of labour!But this is equivalent to lump-sum taxation of labour!

Frank C

owell:

Frank C

owell: E

C426

EC

426 Public E

conomics

Public E

conomics

Arguments for Uniform Taxation?1.1. Invention of new commoditiesInvention of new commodities

Substitutability may make it difficult to specify robust “boundaries” Substitutability may make it difficult to specify robust “boundaries” between commodities. between commodities.

But such boundaries are essential for differential tax rates.But such boundaries are essential for differential tax rates. ““Fine-tuning” of tax rates may be infeasible.Fine-tuning” of tax rates may be infeasible.

2.2. Administration costAdministration cost Formal model of Formal model of complexitycomplexity?? Degree of disaggregation of the tax-collecting processDegree of disaggregation of the tax-collecting process Minimisation of errors (Minimisation of errors (Dhami and Al-Nowaihi 2006))

3.3. Perceived equityPerceived equity Special taxes for “special” goods : OKSpecial taxes for “special” goods : OK Higher taxes for “luxuries” : OKHigher taxes for “luxuries” : OK But, “discriminatory” taxes elsewhere?But, “discriminatory” taxes elsewhere?

Frank C

owell:

Frank C

owell: E

C426

EC

426 Public E

conomics

Public E

conomics

Heterogeneous consumers

Broader social objectives need to be considered.Broader social objectives need to be considered. With representative consumer distributional equity is assumed awayWith representative consumer distributional equity is assumed away Concentration on efficiency makes sense.Concentration on efficiency makes sense.

Pattern of demand may vary with incomePattern of demand may vary with income distinguish between “luxury items” and conventional goods?distinguish between “luxury items” and conventional goods? a basis for discriminatory taxation?a basis for discriminatory taxation?

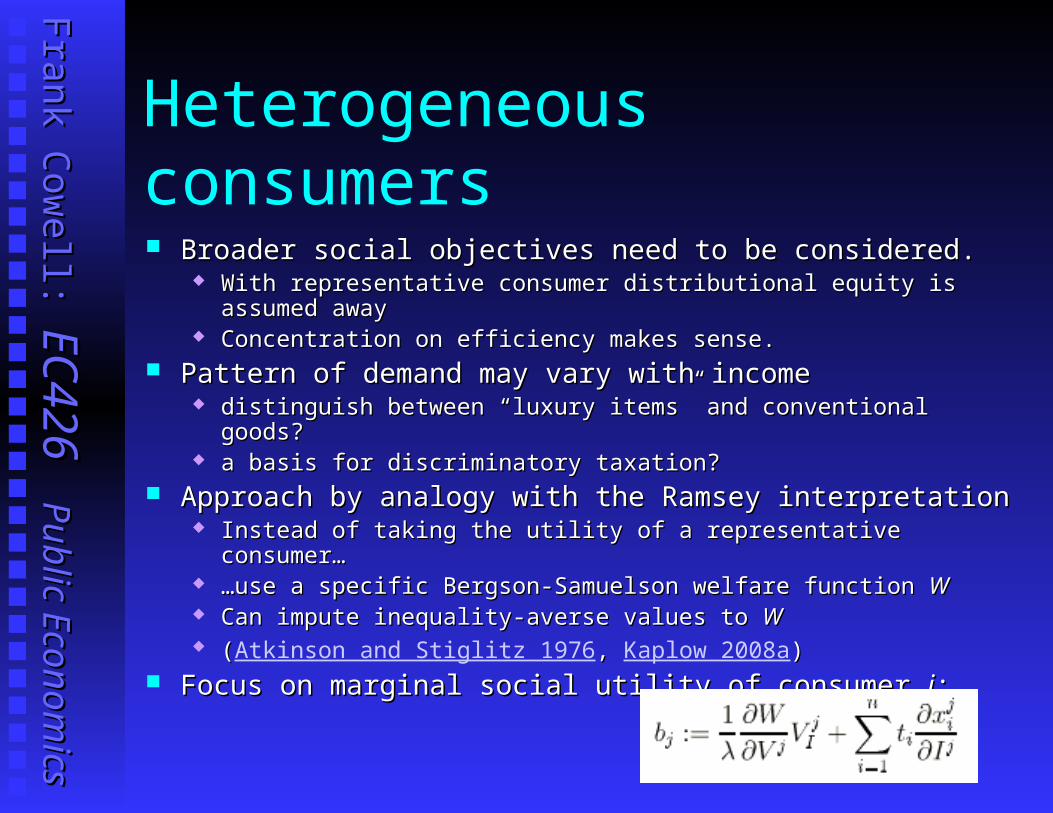

Approach by analogy with the Ramsey interpretationApproach by analogy with the Ramsey interpretation Instead of taking the utility of a representative consumer…Instead of taking the utility of a representative consumer… ……use a specific Bergson-Samuelson welfare function use a specific Bergson-Samuelson welfare function WW Can impute inequality-averse values to Can impute inequality-averse values to WW ((Atkinson and Stiglitz 1976, , Kaplow 2008a))

Focus on Focus on marginal social utility of consumer marginal social utility of consumer jj::

Frank C

owell:

Frank C

owell: E

C426

EC

426 Public E

conomics

Public E

conomics

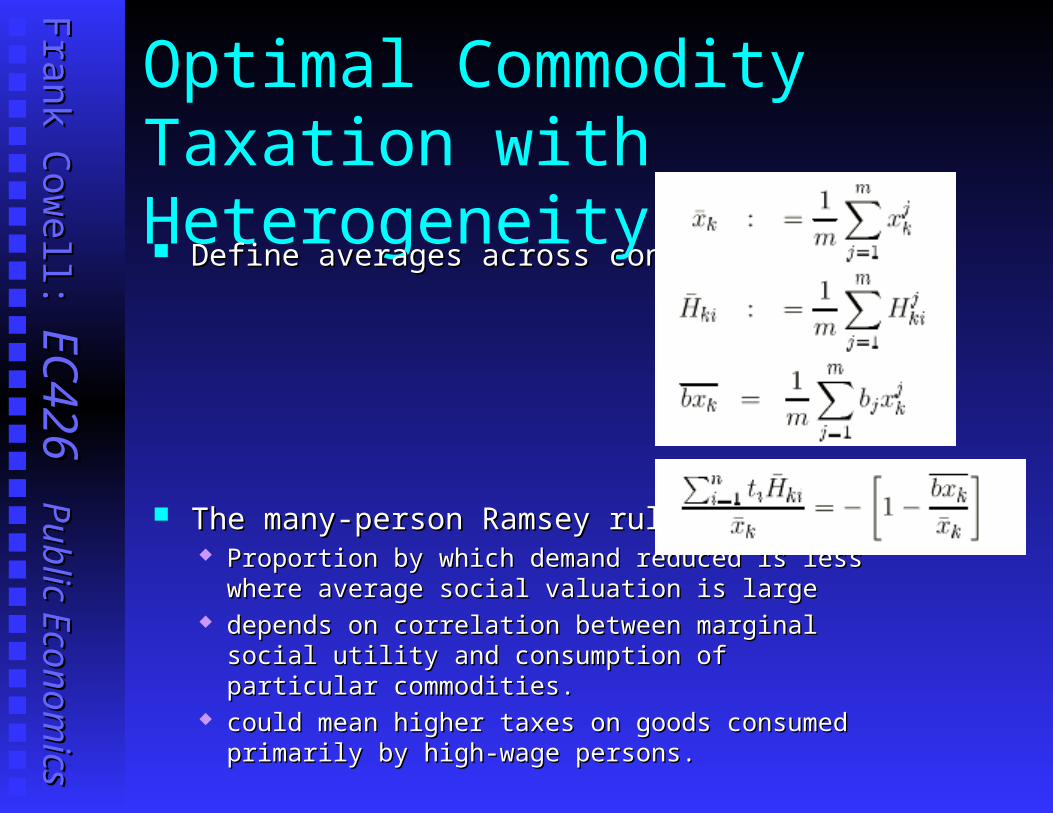

Optimal Commodity Taxation with Heterogeneity Define averages across consumers:Define averages across consumers:

The many-person Ramsey rule:The many-person Ramsey rule: Proportion by which demand reduced is less where average Proportion by which demand reduced is less where average

social valuation is large social valuation is large depends on correlation between marginal social utility and depends on correlation between marginal social utility and

consumption of particular commodities.consumption of particular commodities. could mean higher taxes on goods consumed primarily by could mean higher taxes on goods consumed primarily by

high-wage persons.high-wage persons.

Frank C

owell:

Frank C

owell: E

C426

EC

426 Public E

conomics

Public E

conomics

Indirect tax: summary

Elementary micro-economics appears to give us a Elementary micro-economics appears to give us a powerful analytical toolpowerful analytical tool

Using standard results get a neat characterisation of tax Using standard results get a neat characterisation of tax structure in terms of elasticitiesstructure in terms of elasticities

The approach can be generalised to many consumersThe approach can be generalised to many consumers But assumes away some things that may be crucial in But assumes away some things that may be crucial in

actual tax designactual tax design Determinants of commodity boundariesDeterminants of commodity boundaries Administrative costsAdministrative costs

Is there a case for simplified taxation?Is there a case for simplified taxation? Can we use the analysis for guidance on tax reform?Can we use the analysis for guidance on tax reform?

Frank C

owell:

Frank C

owell: E

C426

EC

426 Public E

conomics

Public E

conomics

Overview...

Optimal tax rules

Commodity Taxation

Use principle to indicate beneficial changes

Commodity tax reform

Commodity tax and income tax

Frank C

owell:

Frank C

owell: E

C426

EC

426 Public E

conomics

Public E

conomics

Commodity tax reform: an approach In evaluating a proposed tax reform, need to consider:In evaluating a proposed tax reform, need to consider:

Impact on tax revenues. Impact on tax revenues. Effect on the welfare of each household. Effect on the welfare of each household. Effect on social welfareEffect on social welfare

Can fairly easily evaluate first two:Can fairly easily evaluate first two: Use household expenditure surveys to estimate demandUse household expenditure surveys to estimate demand Microsimulation model to determine tax effectMicrosimulation model to determine tax effect

What about third point?What about third point? impute social welfare weight to each household…impute social welfare weight to each household… ……then aggregate gains and losses of householdsthen aggregate gains and losses of households difficult: embodies normative value judgmentsdifficult: embodies normative value judgments

Frank C

owell:

Frank C

owell: E

C426

EC

426 Public E

conomics

Public E

conomics

Tax reform problem (1)

Simple approach to tax reform focuses just on welfare Simple approach to tax reform focuses just on welfare improvementimprovement

This requires full comparability of householdsThis requires full comparability of households ReformReform must be must be achievable within existing resources achievable within existing resources So a favourable tax reform So a favourable tax reform requiresrequires

no decrease in tax revenues: no decrease in tax revenues: ddRR = = ii MR MRi i ddttii ≥≥ 0 0 no decrease in social welfare: no decrease in social welfare: ddWW ≥≥ 0 0

Obvious problem with this approachObvious problem with this approach High informational requirements on individual welfareHigh informational requirements on individual welfare Specification of social welfare functionSpecification of social welfare function

Frank C

owell:

Frank C

owell: E

C426

EC

426 Public E

conomics

Public E

conomics

Tax reform problem (2)

To avoid imposing a specific structure on social To avoid imposing a specific structure on social welfare…welfare…

… … just just try to find try to find Pareto-improvingPareto-improving tax reforms tax reforms Pareto improvement requires:Pareto improvement requires:

achievable within existing resourcesachievable within existing resources Pareto superiority of after-reform outcomePareto superiority of after-reform outcome

Translated this meansTranslated this means non negative impact on tax revenuesnon negative impact on tax revenues must harm no onemust harm no one benefit at least one personbenefit at least one person

Frank C

owell:

Frank C

owell: E

C426

EC

426 Public E

conomics

Public E

conomics

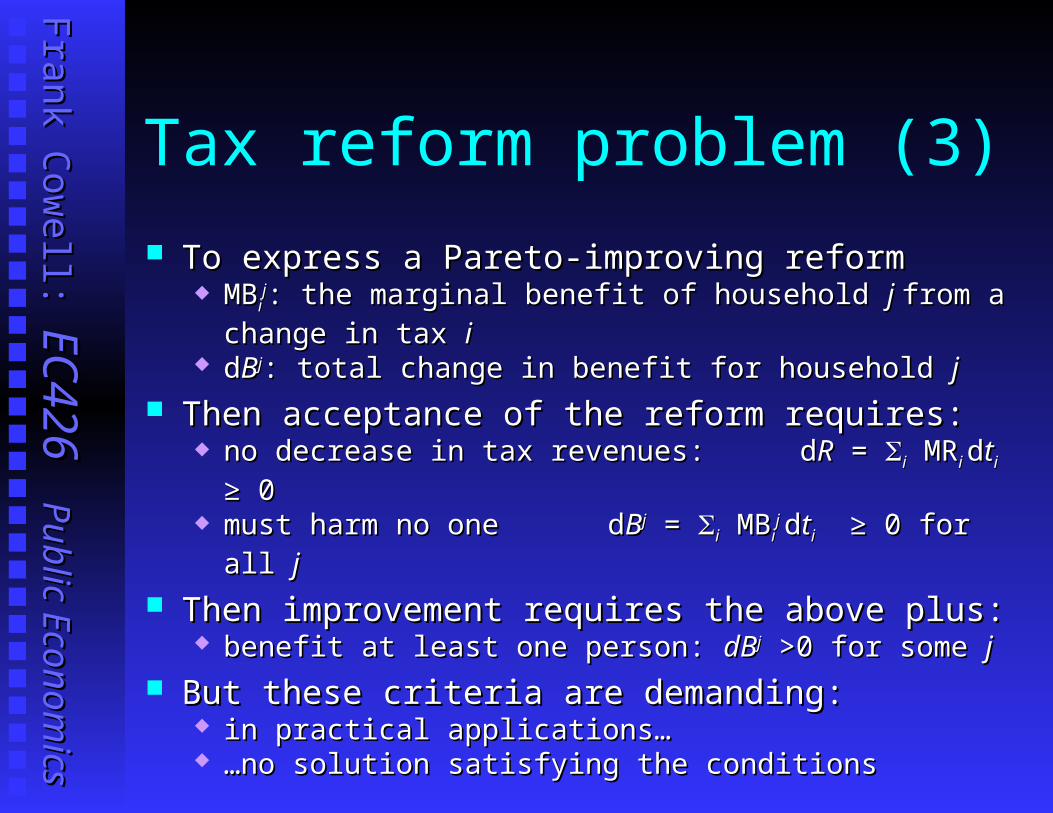

Tax reform problem (3)

To express a Pareto-improving reform To express a Pareto-improving reform MBMBii

jj: the marginal benefit of household : the marginal benefit of household j j from a change in from a change in

tax tax ii ddBBjj: total change in benefit for household : total change in benefit for household jj

Then acceptance of the reform requires:Then acceptance of the reform requires: no decrease in tax revenues: no decrease in tax revenues: ddRR = = ii MR MRi i ddttii ≥≥ 0 0 must harm no onemust harm no one ddBBjj = = ii MB MBii

jj ddttii ≥≥ 0 for all 0 for all jj

Then improvement requires the above plus:Then improvement requires the above plus: benefit at least one person: benefit at least one person: dBdBjj >0 for some >0 for some jj

But these criteria are demanding:But these criteria are demanding: in practical applications…in practical applications… ……no solution satisfying the conditionsno solution satisfying the conditions

Frank C

owell:

Frank C

owell: E

C426

EC

426 Public E

conomics

Public E

conomics

A refined approach

Because of indecisiveness of Paretian approach, try a modified Because of indecisiveness of Paretian approach, try a modified criterioncriterion

Mayshar and Yitzhaki (Mayshar and Yitzhaki (1995, , 1996 ) )

Base this on the “transfer principle” (Base this on the “transfer principle” (Dalton 1920) ) Assume a prior (welfare) ranking of householdsAssume a prior (welfare) ranking of households A transfer is approved if A transfer is approved if

it distributes from the low ranking (rich)…it distributes from the low ranking (rich)… ……to the high ranking (poor)to the high ranking (poor) ……without altering the ranking itself without altering the ranking itself

Logic behind this:Logic behind this: Similar to dominance criteriaSimilar to dominance criteria Difficult to find first-order dominance?Difficult to find first-order dominance? Therefore worth looking at second-order dominanceTherefore worth looking at second-order dominance

Frank C

owell:

Frank C

owell: E

C426

EC

426 Public E

conomics

Public E

conomics

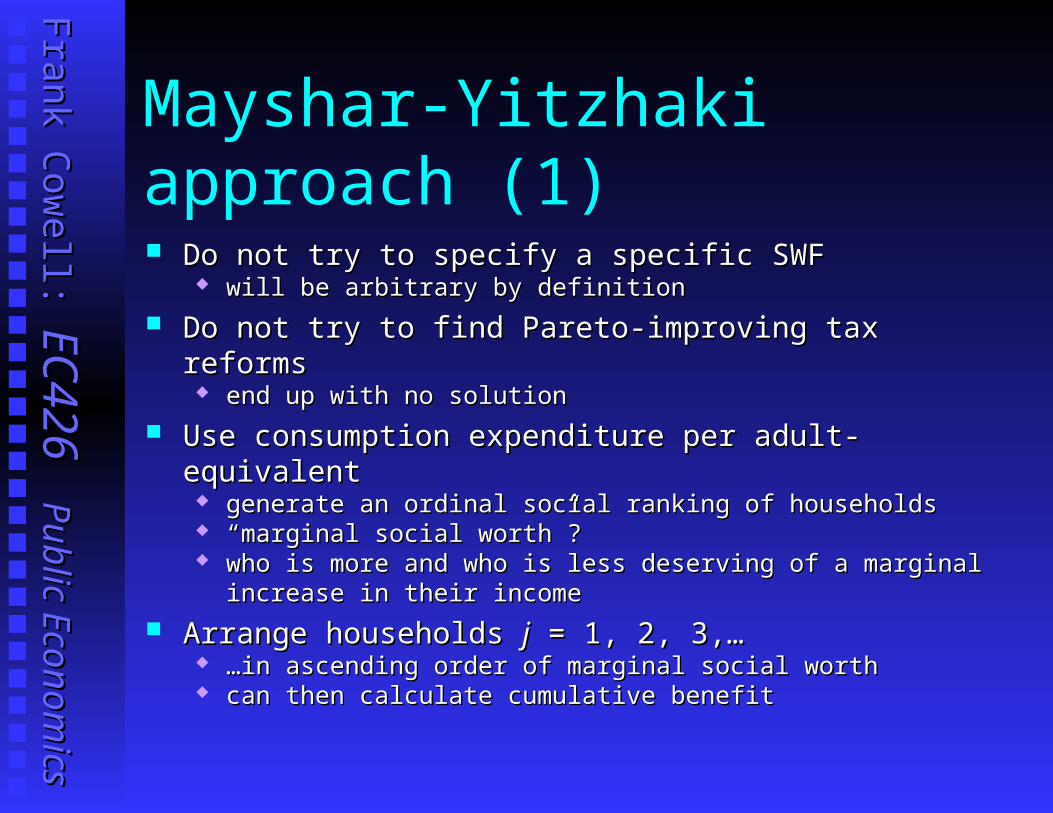

Mayshar-Yitzhaki approach (1)

Do not try to specify a specific SWFDo not try to specify a specific SWF will be arbitrary by definitionwill be arbitrary by definition

Do not try to find Pareto-improving tax reformsDo not try to find Pareto-improving tax reforms end up with no solution end up with no solution

Use consumption expenditure per adult-equivalentUse consumption expenditure per adult-equivalent generate an ordinal social ranking of householdsgenerate an ordinal social ranking of households ““marginal social worth”?marginal social worth”? who is more and who is less deserving of a marginal increase in their who is more and who is less deserving of a marginal increase in their

incomeincome

Arrange households Arrange households jj = 1, 2, 3,… = 1, 2, 3,… ……in ascending order of marginal social worthin ascending order of marginal social worth can then calculate cumulative benefitcan then calculate cumulative benefit

Frank C

owell:

Frank C

owell: E

C426

EC

426 Public E

conomics

Public E

conomics

Mayshar-Yitzhaki approach (2)

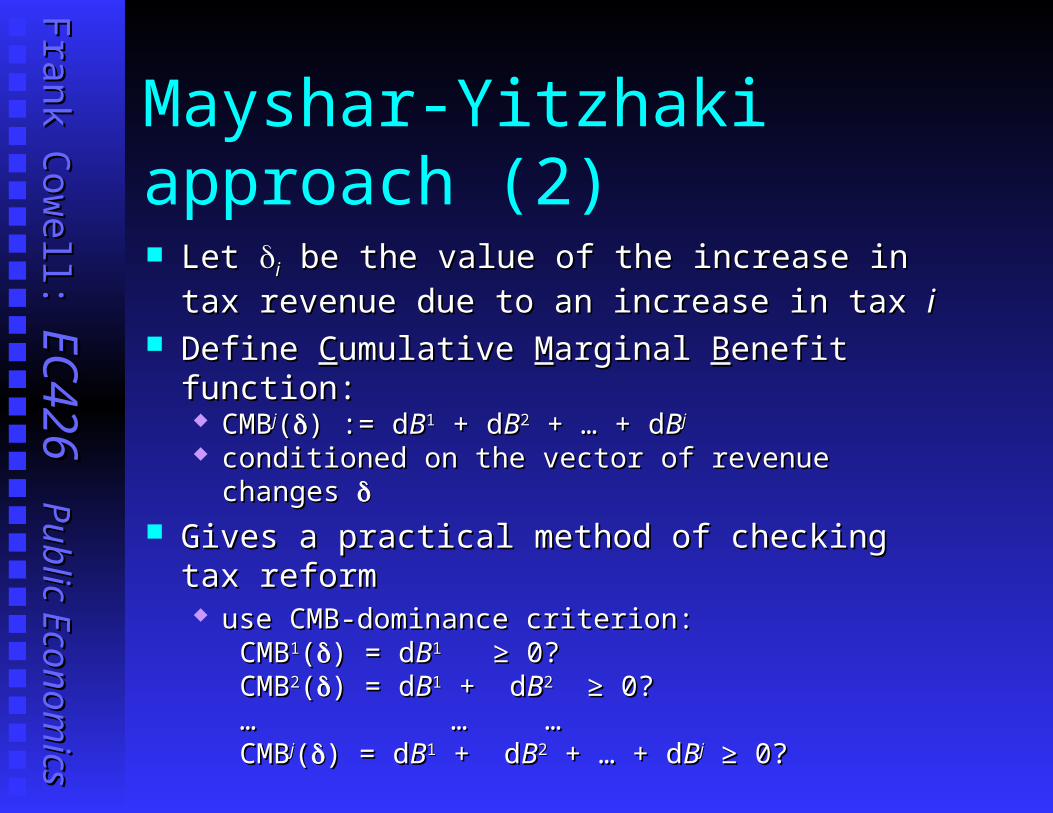

Let Let ii be the value of the increase in tax revenue be the value of the increase in tax revenue

due to an increase in tax due to an increase in tax ii Define Define CCumulative umulative MMarginal arginal BBenefit function:enefit function:

CMBCMBjj(() := d) := dBB11 + d + dBB22 + … + d + … + dBBjj conditioned on the vector of revenue changes conditioned on the vector of revenue changes

Gives a practical method of checking tax reformGives a practical method of checking tax reform use CMB-dominance criterion:use CMB-dominance criterion:

CMBCMB11(() = d) = dBB11 ≥ 0?≥ 0?CMBCMB22(() = d) = dBB11 + d + dBB22 ≥ 0?≥ 0?… … …… ……CMBCMBjj(() = d) = dBB11 + d + dBB22 + … + d + … + dBBjj ≥ 0?≥ 0?

Frank C

owell:

Frank C

owell: E

C426

EC

426 Public E

conomics

Public E

conomics

Mayshar-Yitzhaki criterion

Gives simple principle for reform of commodity taxationGives simple principle for reform of commodity taxation Accept the reform if and only if:Accept the reform if and only if:::

no decrease in tax revenues: no decrease in tax revenues: ddRR = = i i ii ≥≥ 0 0 dominance resultdominance result holds: holds: CMBCMBjj(() ) ≥≥ 0 for all 0 for all jj

Simple relationship between criteria:Simple relationship between criteria: Pareto-improving criterion implies Dalton-improving Pareto-improving criterion implies Dalton-improving but not vice versabut not vice versa

Dalton-improving is more likely to result in a non-empty Dalton-improving is more likely to result in a non-empty solution set solution set

Frank C

owell:

Frank C

owell: E

C426

EC

426 Public E

conomics

Public E

conomics

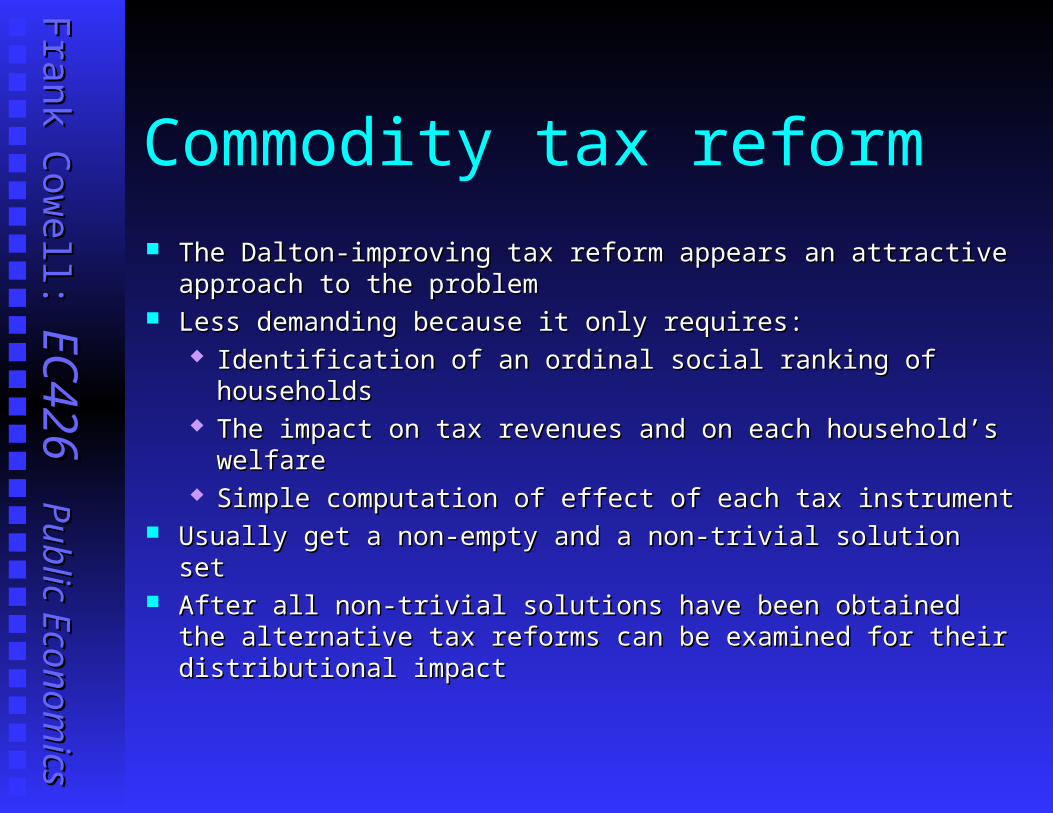

Commodity tax reform

The Dalton-improving tax reform appears an attractive approach The Dalton-improving tax reform appears an attractive approach to the problemto the problem

Less demanding because it only requires: Less demanding because it only requires: Identification of an ordinal social ranking of householdsIdentification of an ordinal social ranking of households The impact on tax revenues and on each household’s welfare The impact on tax revenues and on each household’s welfare

Simple computation of effect of each tax instrumentSimple computation of effect of each tax instrument

Usually get a non-empty and a non-trivial solution set Usually get a non-empty and a non-trivial solution set After all non-trivial solutions have been obtained the alternative After all non-trivial solutions have been obtained the alternative

tax reforms can be examined for their distributional impact tax reforms can be examined for their distributional impact

Frank C

owell:

Frank C

owell: E

C426

EC

426 Public E

conomics

Public E

conomics

Overview...

Optimal tax rules

Commodity Taxation

An integrated approach – do we need commodity taxes?

Commodity tax reform

Commodity tax and income tax

Frank C

owell:

Frank C

owell: E

C426

EC

426 Public E

conomics

Public E

conomics

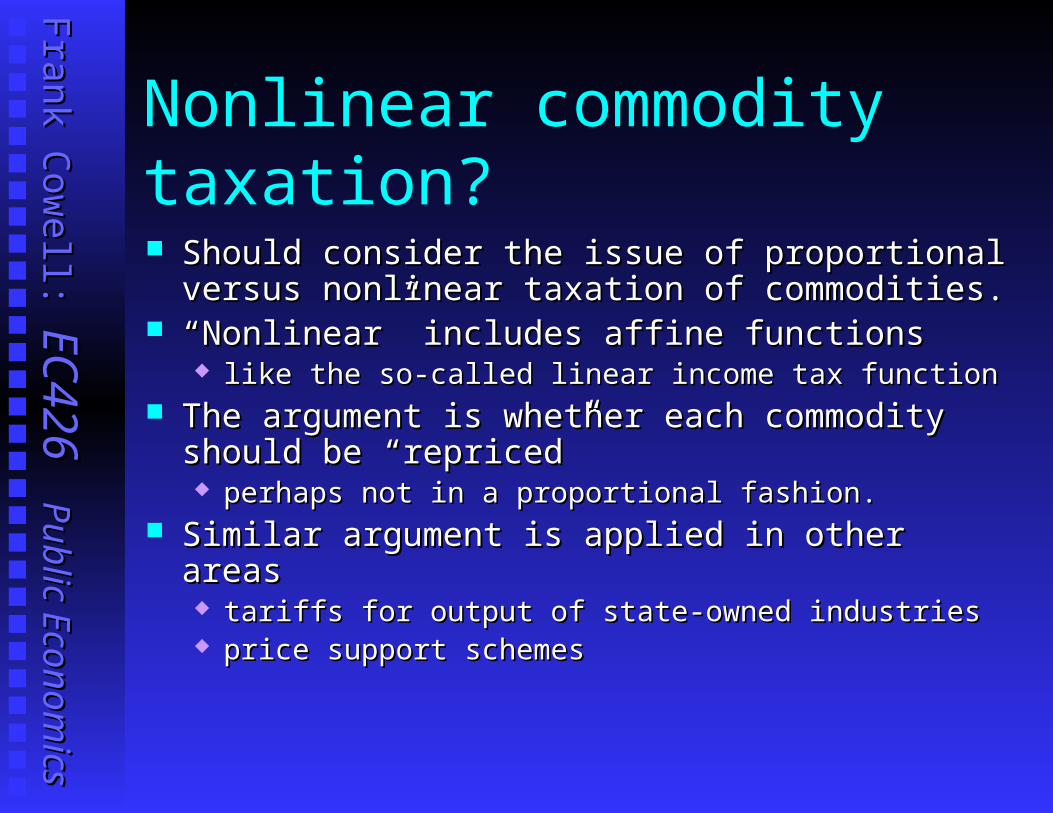

Nonlinear commodity taxation?

Should consider the issue of proportional versus Should consider the issue of proportional versus nonlinear taxation of commodities. nonlinear taxation of commodities.

““Nonlinear” includes affine functions Nonlinear” includes affine functions like the so-called linear income tax function like the so-called linear income tax function

The argument is whether each commodity should be The argument is whether each commodity should be “repriced”“repriced” perhaps not in a proportional fashion.perhaps not in a proportional fashion.

Similar argument is applied in other areasSimilar argument is applied in other areas tariffs for output of state-owned industriestariffs for output of state-owned industries price support schemesprice support schemes

Frank C

owell:

Frank C

owell: E

C426

EC

426 Public E

conomics

Public E

conomics

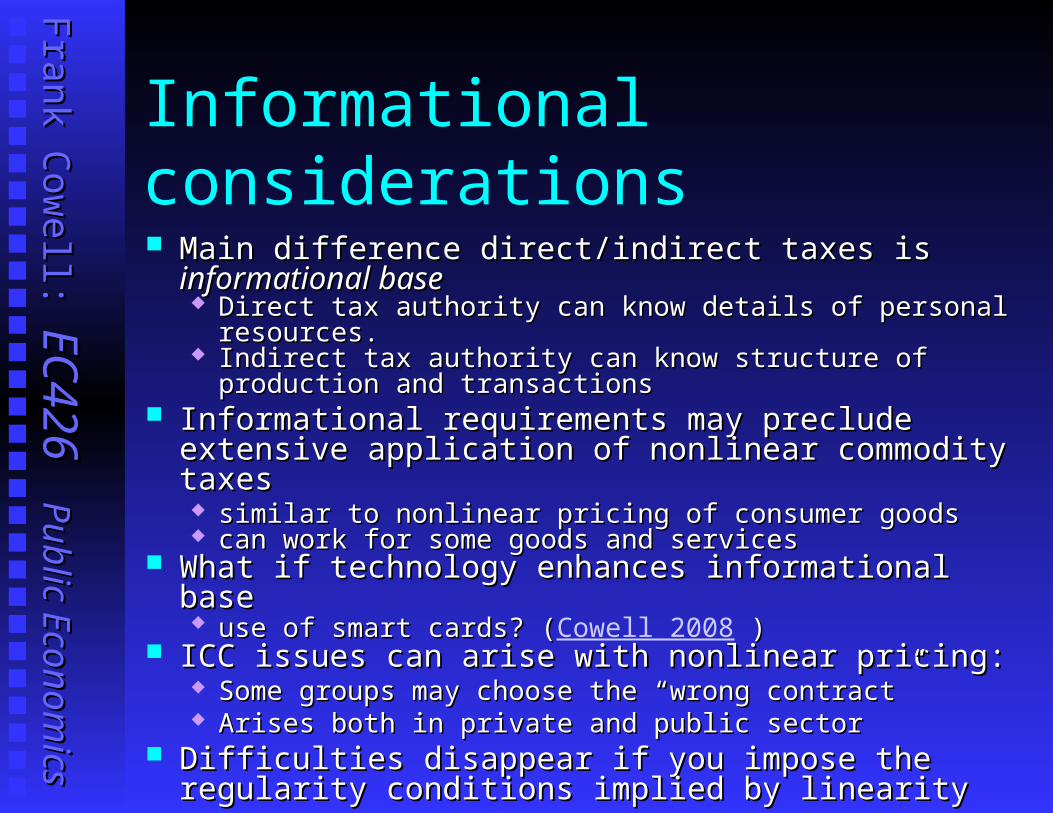

Informational considerations Main difference direct/indirect taxes is Main difference direct/indirect taxes is informational informational

basebase Direct tax authority can know details of personal resources.Direct tax authority can know details of personal resources. Indirect tax authority can know structure of production and Indirect tax authority can know structure of production and

transactionstransactions Informational requirements may preclude extensive Informational requirements may preclude extensive

application of nonlinear commodity taxesapplication of nonlinear commodity taxes similar to nonlinear pricing of consumer goodssimilar to nonlinear pricing of consumer goods can work for some goods and servicescan work for some goods and services

What if technology enhances informational baseWhat if technology enhances informational base use of smart cards? (use of smart cards? (Cowell 2008 ) )

ICC issues can arise with nonlinear pricing: ICC issues can arise with nonlinear pricing: Some groups may choose the “wrong contract”Some groups may choose the “wrong contract” Arises both in private and public sectorArises both in private and public sector

Difficulties disappear if you impose the regularity Difficulties disappear if you impose the regularity conditions implied by linearityconditions implied by linearity

Frank C

owell:

Frank C

owell: E

C426

EC

426 Public E

conomics

Public E

conomics

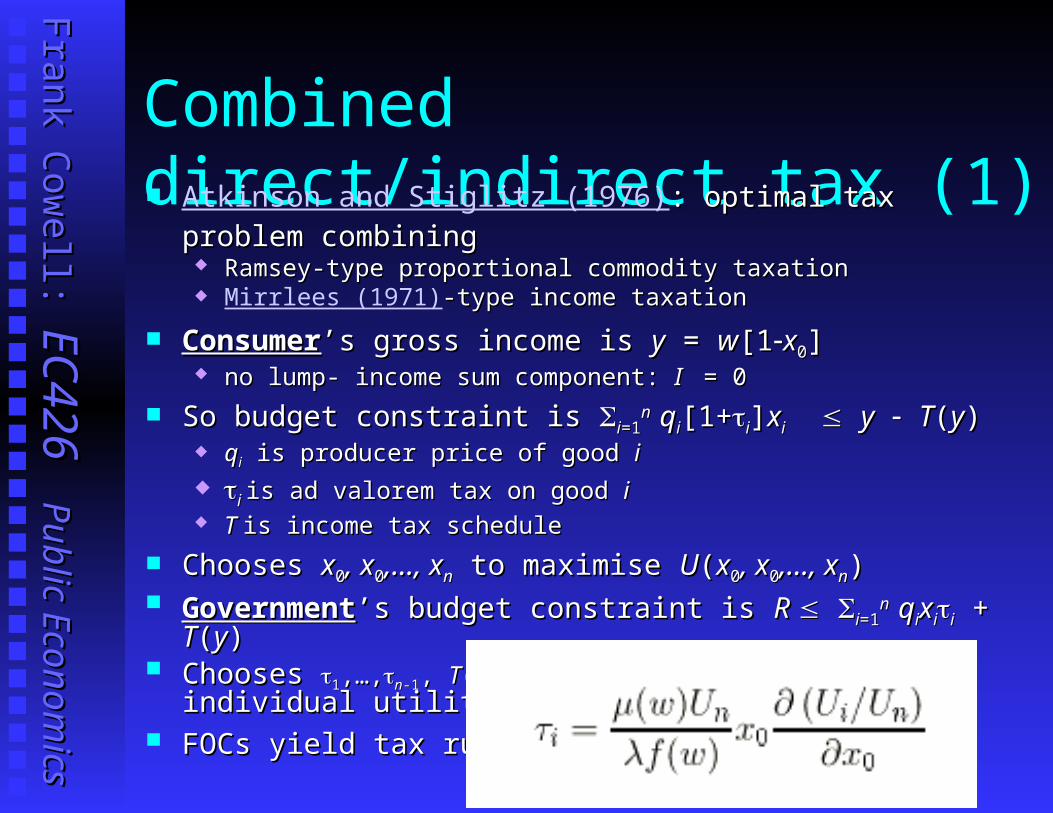

Combined direct/indirect tax (1) Atkinson and Stiglitz (1976): optimal tax problem combining: optimal tax problem combining

Ramsey-type proportional commodity taxationRamsey-type proportional commodity taxation Mirrlees (1971)-type income taxation-type income taxation

ConsumerConsumer’s gross income is ’s gross income is yy = = ww[1[1xx00]] no lump- income sum component: no lump- income sum component: I I = 0 = 0

So budget constraint is So budget constraint is ii=1=1n n qqii[1+[1+ii]]xxii yy TT((yy))

qqii is producer price of good is producer price of good ii i i is ad valorem tax on good is ad valorem tax on good ii T T is income tax scheduleis income tax schedule

Chooses Chooses xx00, x, x00,…, x,…, xnn to maximise to maximise UU((xx00, x, x00,…, x,…, xnn) ) GovernmentGovernment’s budget constraint is’s budget constraint is R R ii=1=1

n n qqiixxiiii + + TT((yy)) Chooses Chooses 11,…,,…,nn-1-1, , TT(.) (.) to max SWF (function of individual utility) to max SWF (function of individual utility) FOCs yield tax ruleFOCs yield tax rule

Frank C

owell:

Frank C

owell: E

C426

EC

426 Public E

conomics

Public E

conomics

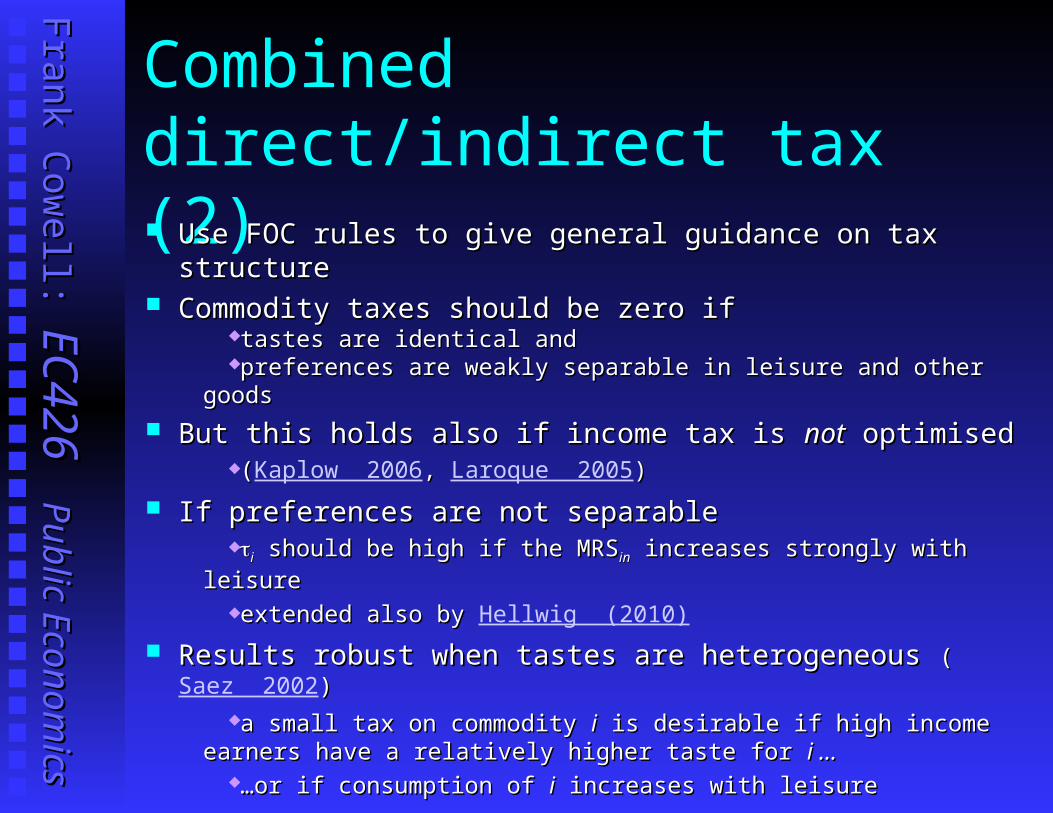

Combined direct/indirect tax (2) Use FOC rules to give general guidance on tax structureUse FOC rules to give general guidance on tax structure Commodity taxes should be zero if Commodity taxes should be zero if

tastes are identical andtastes are identical andpreferences are weakly separable in leisure and other goodspreferences are weakly separable in leisure and other goods

But this holds also if income tax is But this holds also if income tax is notnot optimised optimised((Kaplow 2006,, Laroque 2005))

If preferences are not separableIf preferences are not separableii should be high if the MRSshould be high if the MRSinin increases strongly with leisure increases strongly with leisureextended also by extended also by Hellwig (2010)

Results robust when tastes are heterogeneous Results robust when tastes are heterogeneous ((Saez 2002))a small tax on commodity a small tax on commodity ii is desirable if high income earners have a is desirable if high income earners have a

relatively higher taste for relatively higher taste for i …i ………or if consumption of or if consumption of ii increases with leisure increases with leisure

Frank C

owell:

Frank C

owell: E

C426

EC

426 Public E

conomics

Public E

conomics

Conclusions

Direct versus indirectDirect versus indirect Distinction between the two is essentially an issue of Distinction between the two is essentially an issue of

information.information. Big differences in terms of distributional effect.Big differences in terms of distributional effect.

Uniform commodity taxationUniform commodity taxation No compelling case within the context of the modelNo compelling case within the context of the model There may be a case if you appeal to other factorsThere may be a case if you appeal to other factors

Do we need commodity taxes?Do we need commodity taxes? depends on way incentives and information are modelleddepends on way incentives and information are modelled also depends on structure of preferencesalso depends on structure of preferences

Frank C

owell:

Frank C

owell: E

C426

EC

426 Public E

conomics

Public E

conomics

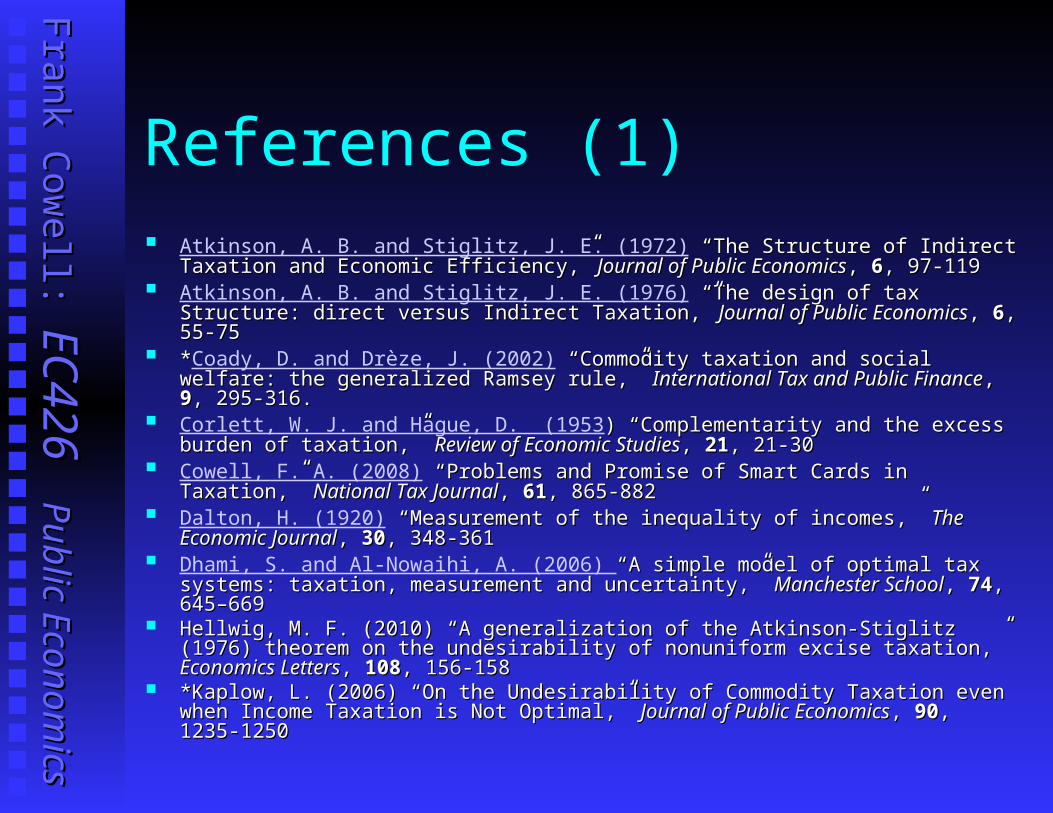

References (1) Atkinson, A. B. and Stiglitz, J. E. (1972) “ “The Structure of Indirect Taxation and The Structure of Indirect Taxation and

Economic EfficiencyEconomic Efficiency,”,” Journal of Public Economics Journal of Public Economics, , 66, , 97-11997-119 Atkinson, A. B. and Stiglitz, J. E. (1976) “The design of tax Structure: direct versus “The design of tax Structure: direct versus

Indirect Taxation,”Indirect Taxation,” Journal of Public Economics Journal of Public Economics, , 66, 55-75, 55-75 **Coady, D. and Drèze, J. (2002) “Commodity taxation and social welfare: the “Commodity taxation and social welfare: the

generalized Ramsey rule,” generalized Ramsey rule,” International Tax and Public FinanceInternational Tax and Public Finance, , 99, 295-316., 295-316. Corlett, W. J. and Hague, D. (1953) “) “Complementarity and the excess burden of Complementarity and the excess burden of

taxation,” taxation,” Review of Economic StudiesReview of Economic Studies, , 2121, 21-30, 21-30 Cowell, F. A. (2008) “Problems and Promise of Smart Cards in Taxation,” “Problems and Promise of Smart Cards in Taxation,” National National

Tax JournalTax Journal, , 6161, 865-882, 865-882 Dalton, H. (1920) “ “Measurement of the inequality of incomes,” Measurement of the inequality of incomes,” The Economic The Economic

JournalJournal, , 3030, 348-361, 348-361 Dhami, S. and Al-Nowaihi, A. (2006) “A simple model of optimal tax systems: “A simple model of optimal tax systems:

taxation, measurement and uncertainty,” taxation, measurement and uncertainty,” Manchester SchoolManchester School, , 7474, 645–669, 645–669 Hellwig, M. F. (2010) “A generalization of the Atkinson-Stiglitz (1976) theorem on Hellwig, M. F. (2010) “A generalization of the Atkinson-Stiglitz (1976) theorem on

the undesirability of nonuniform excise taxation,” the undesirability of nonuniform excise taxation,” Economics LettersEconomics Letters, , 108108, 156-158 , 156-158 *Kaplow, L. (2006) “On the Undesirability of Commodity Taxation even when *Kaplow, L. (2006) “On the Undesirability of Commodity Taxation even when

Income Taxation is Not Optimal,” Income Taxation is Not Optimal,” Journal of Public EconomicsJournal of Public Economics, , 9090, 1235-1250, 1235-1250

Frank C

owell:

Frank C

owell: E

C426

EC

426 Public E

conomics

Public E

conomics

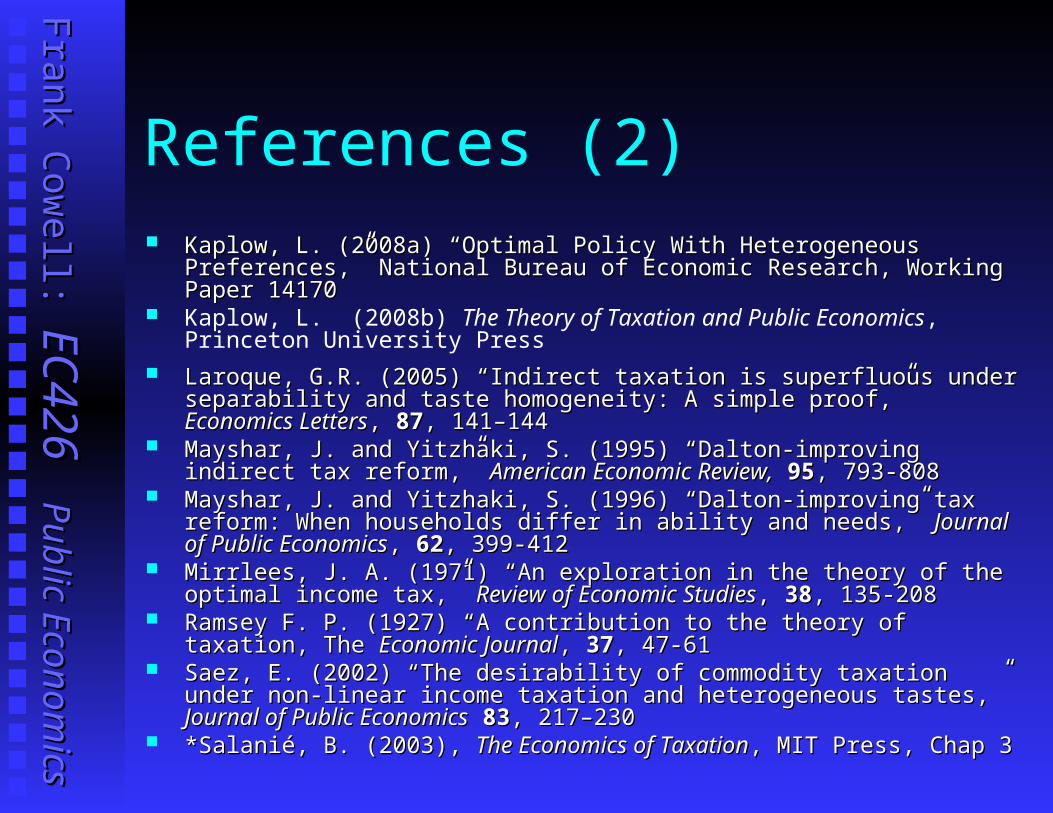

References (2) Kaplow, L. (2008a) “Optimal Policy With Heterogeneous Preferences,” National Kaplow, L. (2008a) “Optimal Policy With Heterogeneous Preferences,” National

Bureau of Economic Research, Working Paper 14170Bureau of Economic Research, Working Paper 14170 Kaplow, L. (2008b) The Theory of Taxation and Public Economics, Princeton

University Press Laroque, G.R. (2005) “Indirect taxation is superfluous under separability and taste Laroque, G.R. (2005) “Indirect taxation is superfluous under separability and taste

homogeneity: A simple proof,” homogeneity: A simple proof,” Economics LettersEconomics Letters, , 8787, 141–144 , 141–144 Mayshar, J. and Yitzhaki, S. (1995) “Dalton-improving indirect tax reform,” Mayshar, J. and Yitzhaki, S. (1995) “Dalton-improving indirect tax reform,”

American Economic Review,American Economic Review, 9595, 793-808, 793-808 Mayshar, J. and Yitzhaki, S. (1996) “Dalton-improving tax reform: When households Mayshar, J. and Yitzhaki, S. (1996) “Dalton-improving tax reform: When households

differ in ability and needs,” differ in ability and needs,” Journal of Public EconomicsJournal of Public Economics, , 6262, 399-412 , 399-412 Mirrlees, J. A. (1971) “An exploration in the theory of the optimal income tax,” Mirrlees, J. A. (1971) “An exploration in the theory of the optimal income tax,”

Review of Economic StudiesReview of Economic Studies, , 3838, 135-208, 135-208 Ramsey F. P. (1927) Ramsey F. P. (1927) “A contribution to the theory of taxation, The “A contribution to the theory of taxation, The Economic JournalEconomic Journal, ,

3737, 47-61, 47-61 Saez, E. (2002) “The desirability of commodity taxation under non-linear income Saez, E. (2002) “The desirability of commodity taxation under non-linear income

taxation and heterogeneous tastes,” taxation and heterogeneous tastes,” Journal of Public EconomicsJournal of Public Economics 8383, 217–230, 217–230 *Salanié, B. (2003), *Salanié, B. (2003), The Economics of TaxationThe Economics of Taxation, MIT Press, Chap 3, MIT Press, Chap 3