Fourth-Quarter and Full-Year 2017 Results - Cabot Oil & Gas · Fourth-Quarter and Full-Year 2017...

28

A decade of progress and perseverance in the Marcellus Shale. February 23, 2018 Fourth-Quarter and Full-Year 2017 Results

Transcript of Fourth-Quarter and Full-Year 2017 Results - Cabot Oil & Gas · Fourth-Quarter and Full-Year 2017...

A decade of progress and perseverance in the Marcellus Shale.

February 23, 2018

Fourth-Quarter and Full-Year 2017 Results

2

This presentation includes forward‐looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and

Section 21E of the Securities Exchange Act of 1934, as amended. The statements regarding future financial and operating performance and

results, strategic pursuits and goals, market prices, future hedging and risk management activities, and other statements that are not historical

facts contained in this report are forward-looking statements. The words “expect”, “project”, “estimate”, “believe”, “anticipate”, “intend”, “budget”,

“plan”, “forecast”, “outlook”, “target”, “predict”, “may”, “should”, “could”, “will” and similar expressions are also intended to identify forward-looking

statements. Such statements involve risks and uncertainties, including, but not limited to, market factors, market prices (including geographic

basis differentials) of natural gas and crude oil, results of future drilling and marketing activity, future production and costs, legislative and

regulatory initiatives, electronic, cyber or physical security breaches and other factors detailed herein and in our other Securities and Exchange

Commission (SEC) filings. See “Risk Factors” in Item 1A of the Form 10-K and subsequent public filings for additional information about these

risks and uncertainties. Should one or more of these risks or uncertainties materialize, or should underlying assumptions prove incorrect, actual

outcomes may vary materially from those indicated. Any forward-looking statement speaks only as of the date on which such statement is

made, and Cabot Oil & Gas (the “Company” or “Cabot”) does not undertake any obligation to correct or update any forward-looking statement,

whether as the result of new information, future events or otherwise, except as required by applicable law.

This presentation may contain certain terms, such as resource potential, risked or unrisked resources, potential locations, risked or unrisked

locations, EUR (estimated ultimate recovery) and other similar terms that describe estimates of potentially recoverable hydrocarbons that the

SEC rules prohibit from being included in filings with the SEC. These estimates are by their nature more speculative than estimates of proved,

probable and possible reserves and may not constitute “reserves” within the meaning of SEC rules and accordingly, are subject to substantially

greater risk of being actually realized. These estimates are based on the Company’s existing models and internal estimates. Actual locations

drilled and quantities that may be ultimately recovered from the Company’s interests could differ substantially. Factors affecting ultimate

recovery include the scope of the Company’s ongoing drilling program, which will be directly affected by the availability of capital, drilling and

production costs, availably of drilling services and equipment, drilling results, lease expirations, transportation constraints, regulatory approvals,

actual drilling results, including geological and mechanical factors affecting recovery rates, and other factors. These estimates may change

significantly as development of the Company’s assets provide additional data. Investors are urged to consider carefully the disclosures and risk

factors about Cabot’s reserves in the Form 10‐K and other reports on file with the SEC.

This presentation also refers to Discretionary Cash Flow, EBITDAX, Free Cash Flow, Adjusted Net Income (Loss), Return on Capital Employed

(ROCE) and Net Debt calculations and ratios. These non-GAAP financial measures are not alternatives to GAAP measures, and should not be

considered in isolation or as an alternative for analysis of the Company’s results as reported under GAAP. For additional disclosure regarding

such non-GAAP measures, including definitions of these terms and reconciliations to the most directly comparable GAAP measures, please

refer to Cabot’s most recent earnings release at www.cabotog.com and the Company’s related 8-K on file with the SEC.

Forward-Looking Statements and Other Disclaimers

3

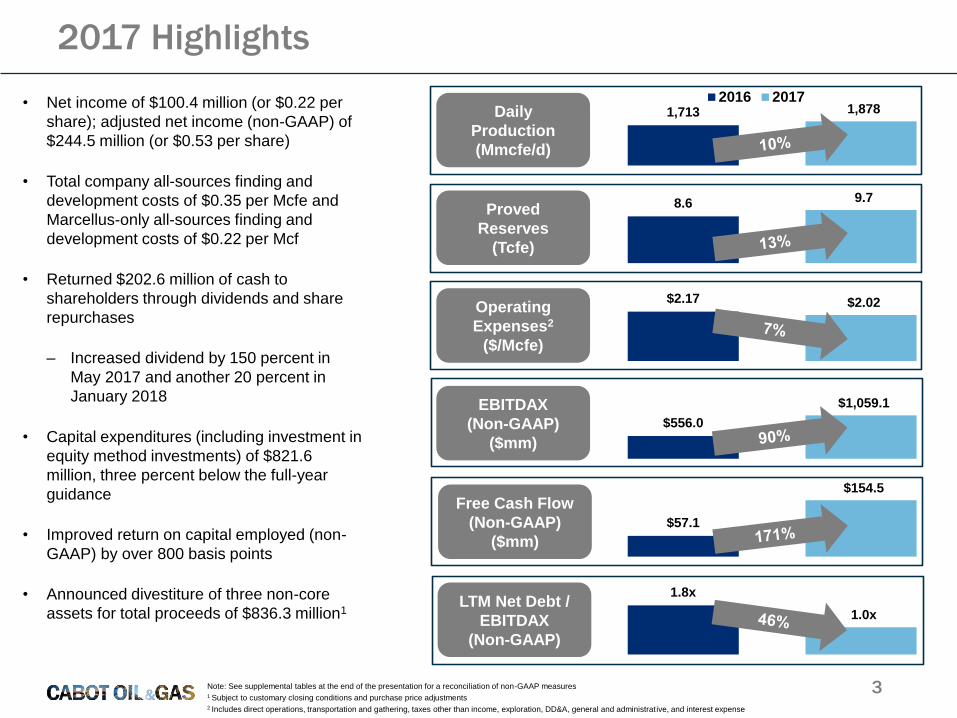

• Net income of $100.4 million (or $0.22 per

share); adjusted net income (non-GAAP) of

$244.5 million (or $0.53 per share)

• Total company all-sources finding and

development costs of $0.35 per Mcfe and

Marcellus-only all-sources finding and

development costs of $0.22 per Mcf

• Returned $202.6 million of cash to

shareholders through dividends and share

repurchases

– Increased dividend by 150 percent in

May 2017 and another 20 percent in

January 2018

• Capital expenditures (including investment in

equity method investments) of $821.6

million, three percent below the full-year

guidance

• Improved return on capital employed (non-

GAAP) by over 800 basis points

• Announced divestiture of three non-core

assets for total proceeds of $836.3 million1

Note: See supplemental tables at the end of the presentation for a reconciliation of non-GAAP measures1 Subject to customary closing conditions and purchase price adjustments2 Includes direct operations, transportation and gathering, taxes other than income, exploration, DD&A, general and administrat ive, and interest expense

Daily

Production

(Mmcfe/d)

1,713 1,8782016 2017

Proved

Reserves

(Tcfe)

8.6 9.7

Operating

Expenses2

($/Mcfe)

$2.17 $2.02

EBITDAX

(Non-GAAP)

($mm)

$556.0

$1,059.1

Free Cash Flow

(Non-GAAP)

($mm)

$57.1

$154.5

1.8x

1.0xLTM Net Debt /

EBITDAX

(Non-GAAP)

2017 Highlights

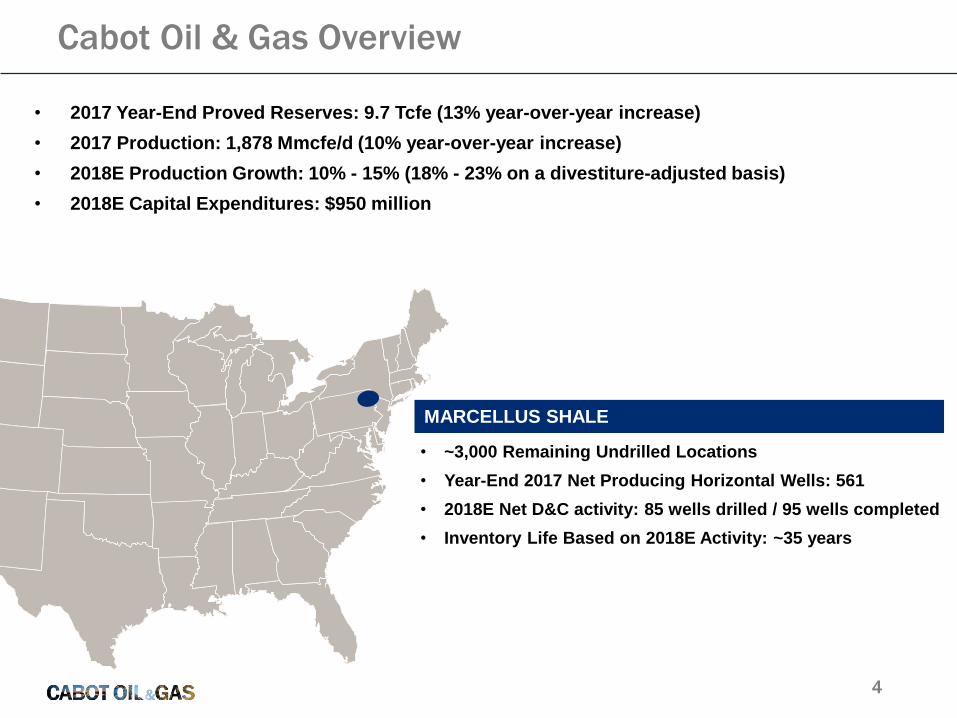

• ~3,000 Remaining Undrilled Locations

• Year-End 2017 Net Producing Horizontal Wells: 561

• 2018E Net D&C activity: 85 wells drilled / 95 wells completed

• Inventory Life Based on 2018E Activity: ~35 years

• 2017 Year-End Proved Reserves: 9.7 Tcfe (13% year-over-year increase)

• 2017 Production: 1,878 Mmcfe/d (10% year-over-year increase)

• 2018E Production Growth: 10% - 15% (18% - 23% on a divestiture-adjusted basis)

• 2018E Capital Expenditures: $950 million

4

MARCELLUS SHALE

Cabot Oil & Gas Overview

5

Cabot Oil & Gas Strategy

Deliver growth in production and

reserves per debt-adjusted share while

generating positive free cash flow

Generate an improving return on

capital employed (ROCE) that

exceeds our cost of capital

Increase the return of capital to

shareholders through dividends

and share repurchases

Maintain a strong balance sheet

to maximize financial flexibility

• 20%+ CAGR in production and reserves per debt-adjusted share from

2011 – 2017

• Three-year plan production CAGR of 17% - 21% (20% - 24% on a

divestiture-adjusted basis)

• Forecasted cumulative free cash flow of $1.6 bn - $2.5 bn from 2018 – 2020

allows for potential share repurchases and/or debt reduction, furthering

enhancing debt-adjusted per share growth

• Anticipate ROCE increasing from 7.3% in 2017 to 18% - 23% by 2020

(based on a $2.75 - $3.25 NYMEX price range)

• ROCE would be further enhanced by future share repurchases or debt

reduction

• Returned over $200 mm of capital to shareholders in 2017

– $124 mm of share repurchases (~5 mm shares)

– $79 mm of dividends

• Increased dividend by 150 percent in 2017 and 20 percent in 2018

• Increased share repurchase program authorization to 30 mm shares

(~6.5% of current shares outstanding)

• Net debt / LTM EBITDAX of 1.0x (target of 1.0x - 1.5x)

– Forecasted deleveraging during the three-year plan allows for potential

incremental balance sheet capacity in the future

• Current liquidity of ~$2.2 bn including cash on hand of $480 mm as of

12/31/2017, with further proceeds from Eagle Ford divestiture anticipated

in Q1 20181

Disciplined capital allocation focused on delivering debt-adjusted per share growth,

generating positive free cash flow, improving corporate returns on capital employed,

increasing return of capital to shareholders, and maintaining a strong balance sheet

Note: See supplemental tables at the end of the presentation for a reconciliation of non-GAAP measures1 Subject to customary closing conditions and purchase price adjustments

• Increased share repurchase program authorization to 30 million shares (~6.5% of current shares outstanding)

• Debt-adjusted per share growth and ROCE metrics added to the 2018 incentive compensation plan

2011 2012 2013 2014 2015 2016 2017

6

Daily Production Per Debt-Adjusted Share

2011 2012 2013 2014 2015 2016 2017

Year-End Proved Reserves Per Debt-Adjusted Share

Proven Track Record of Debt-Adjusted per Share Growth

Note: Debt-adjusted share count is calculated as the sum of the annual weighted average shares outstanding plus the incremental “debt shares” by dividing total debt by the average

annual share price.

7

$1.21

$0.87

$0.55

$0.71 $0.57

$0.37 $0.35

2011 2012 2013 2014 2015 2016 2017

Total Company All-Sources Finding & Development Costs ($/Mcfe)

Marcellus All-Sources Finding & Development Costs ($/Mcf)

$0.65

$0.49

$0.40 $0.43

$0.31 $0.26

$0.22

2011 2012 2013 2014 2015 2016 2017

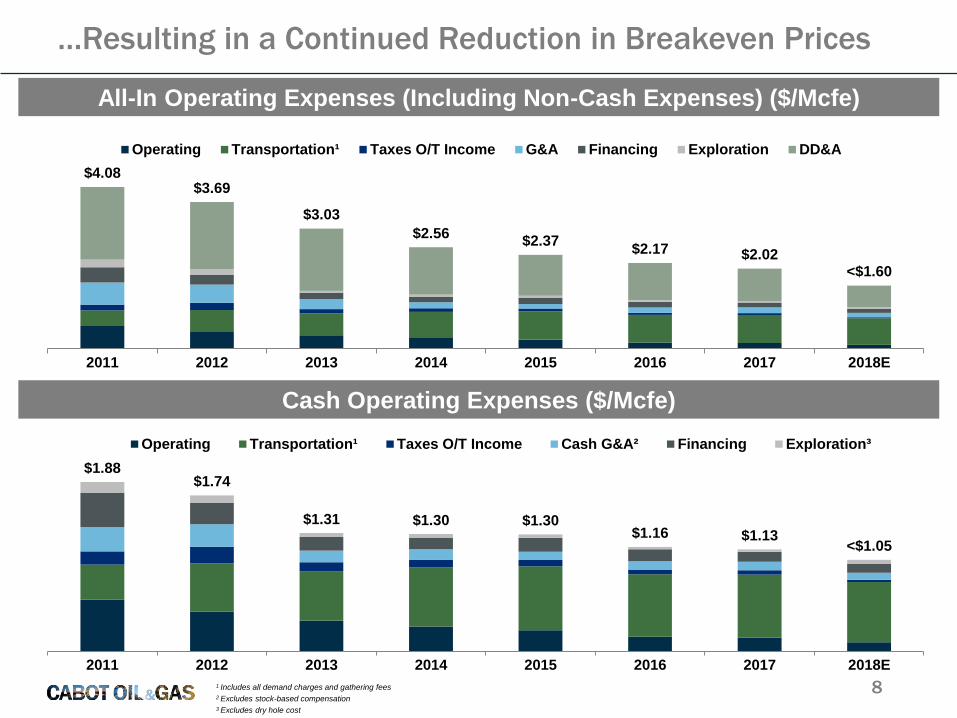

Industry-Leading Cost Structure Continues to Improve…

8

$1.88$1.74

$1.31 $1.30 $1.30$1.16 $1.13

<$1.05

2011 2012 2013 2014 2015 2016 2017 2018E

Operating Transportation¹ Taxes O/T Income Cash G&A² Financing Exploration³

1 Includes all demand charges and gathering fees

2 Excludes stock-based compensation

3 Excludes dry hole cost

Cash Operating Expenses ($/Mcfe)

…Resulting in a Continued Reduction in Breakeven Prices

$4.08$3.69

$3.03

$2.56$2.37

$2.17 $2.02<$1.60

2011 2012 2013 2014 2015 2016 2017 2018E

Operating Transportation¹ Taxes O/T Income G&A Financing Exploration DD&A

All-In Operating Expenses (Including Non-Cash Expenses) ($/Mcfe)

9

Net Debt to LTM EBITDAX

1.4x 1.4x

0.9x

1.2x

2.5x

1.8x

1.0x

2011 2012 2013 2014 2015 2016 2017

Cabot’s Balance Sheet is Well-Positioned to Provide Financial Flexibility Through the Commodity Price Cycle

Target Leverage Ratio:

1.0x – 1.5x

Note: See supplemental tables at the end of the presentation for a reconciliation of non-GAAP measures

84%

8%

6%2%

Marcellus Shale Exploration Areas

Pipeline Investments Corporate

2018 Capital Budget and Operating Plan

10

2018E Production Growth: 10% - 15% (18% - 23% on a divestiture-adjusted basis)

Marcellus Net D&C Activity by Quarter2018E Total Program Spending: $950 mm

(includes $60 mm of equity pipeline investments)

Net Production by Quarter (Mmcfe/d)1

20 23 22 2020 2327 25

0

24

36

23

Q1 2018 Q2 2018 Q3 2018 Q4 2018

Wells Drilled Wells Completed Wells TIL

Q1 2018 Q2 2018 Q3 2018 Q4 2018

~1,825 –

1,875

+6%+11%

+13%

• Assumes Gen 5 Completion Design Across the Majority of the 2018 Program

• 2018 Drilling Program Average Lateral Length: 8,300 feet

• 2018 Average Well Cost (Including Facilities): $8.3 million ($1,000 per lateral foot)

1 Q2 – Q4 production forecasts are subject to change based on the in-service timing of new infrastructure projects and takeaway capacity. Sequential growth rates are based on the midpoint of guidance.

Note: Due to larger pad sizes in Q1 and the 2nd completion crew not coming online until February 2018, wells

completed in Q1 will not be turned-in-line (TIL) until early-to-mid April 2018

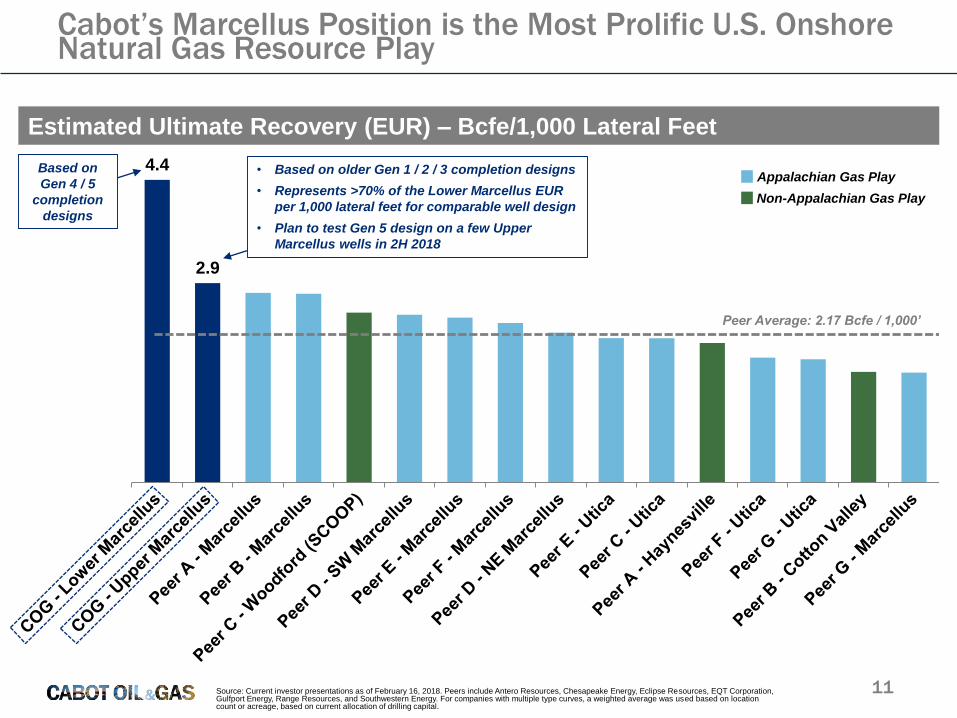

4.4

2.9

Appalachian Gas Play

Non-Appalachian Gas Play

Peer Average: 2.17 Bcfe / 1,000’

11

Estimated Ultimate Recovery (EUR) – Bcfe/1,000 Lateral Feet

Source: Current investor presentations as of February 16, 2018. Peers include Antero Resources, Chesapeake Energy, Eclipse Resources, EQT Corporation, Gulfport Energy, Range Resources, and Southwestern Energy. For companies with multiple type curves, a weighted average was used based on location count or acreage, based on current allocation of drilling capital.

Cabot’s Marcellus Position is the Most Prolific U.S. Onshore Natural Gas Resource Play

Based on

Gen 4 / 5

completion

designs

• Based on older Gen 1 / 2 / 3 completion designs

• Represents >70% of the Lower Marcellus EUR

per 1,000 lateral feet for comparable well design

• Plan to test Gen 5 design on a few Upper

Marcellus wells in 2H 2018

12

~2.15Bcf/d

2.2 2.32.6

3.6~3.7Bcf/d

165 Mmcf/d

240Mmcf/d

1 Bcf/d

150Mmcf/d

Current GrossProduction Capacity

Moxie FreedomPower Plant

(June 2018 - currentlyunder construction)

Lackawanna EnergyCenter Power Plant(June to December

2018 - currently underconstruction)

Atlantic Sunrise(Mid-2018 - currentlyunder construction)

PennEast(2019)

Future GrossProduction Capacity

Cabot continues to evaluate new opportunities to increase firm transport capacity / firm sales and remains

confident it can organically grow its production base above 3.7 Bcf/d through the following opportunities:

1) additional sales on currently approved takeaway projects (i.e. Atlantic Sunrise / PennEast)

2) incremental sales on potential future expansion projects

3) increasing in-basin market share

4) new in-basin demand projects

5) future greenfield takeaway projects (including Constitution Pipeline)

•350 Mmcf/d (COG transport capacity): 20 years

•500 Mmcf/d (COG transport capacity): 15 years

•150 Mmcf/d (3rd party transport capacity): 3 years

Note: COG firm transport capacity / firm sales are stated on a gross basis before royalties

2018 is an Inflection Year for Cabot

13

Cabot is committed to returning capital to shareholders

Return of Capital to Shareholders ($mm)

$13 $17 $25 $33 $33 $36

$79

$111

$165$139

$124

$0

$25

$50

$75

$100

$125

$150

$175

$200

$225

2011 2012 2013 2014 2015 2016 2017 2018E

Dividends Share Repurchases

Increased

Dividend

33%

Increased

Dividend

100%

Increased

Dividend

150%

Increased

Dividend

20%

Commodity Price

Downturn

Recently

increased

share

repurchase

authorization

to 30mm

shares

($~720mm1)

1As of February 22, 2018Note: The chart above excludes the Company’s 2016 equity issuance

3.8%

1.5%1.3%

1.0%0.7% 0.6% 0.5%

0.3% 0.2% 0.2% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

Peer A Peer B Peer C COG Peer D Peer E Peer F Peer G Peer H Peer I Peer J Peer K Peer L Peer M Peer N Peer O Peer P

14Source: FactSet as of 02/19/2018; peers include: AR, CHK, XEC, CXO, CLR, DVN, ECA, EQT, MRO, MUR, NFX, NBL, PXD, QEP, RRC, SWN.

1 Free cash flow yield is calculated as consensus estimates for cash from operations less capital expenditures

2 EQT pro forma for Rice Energy acquisition

Current Dividend Yield

Cabot offers a compelling combination of top-tier yield, free cash flow and growth

2019E Free Cash Flow Yield1

2017 – 2019E Production CAGR2

5.4% 5.3% 5.1% 4.5% 4.1% 3.8% 3.5% 2.9% 2.4% 1.7% 0.9% 0.8% 0.6%

(0.7%)(2.6%)

(4.3%)

(7.3%)

COG Peer F Peer C Peer J Peer D Peer A Peer M Peer H Peer E Peer I Peer N Peer G Peer L Peer B Peer K Peer P Peer O

21.8% 20.7% 19.9% 19.7% 18.7%16.9% 16.8% 16.6%

15.0%

11.1% 9.9%

7.0% 6.1%4.6% 4.0% 3.5%

1.5%

COG Peer J Peer L Peer M Peer F Peer I Peer G Peer H Peer N Peer E Peer C Peer P Peer D Peer B Peer A Peer O Peer K

$245

2017 Actual 2018E 2019E 2020E

$2.75 NYMEX $3.00 NYMEX $3.25 NYMEX

15Note: See the assumptions slide in the appendix for further detail and definitions.

1 Based on midpoint of production guidance. The CAGRs and improvement in ROCE represented in the arrows above are based on the $2.75 NYMEX case.

Adjusted Net Income ($mm)1 Discretionary Cash Flow ($mm)1

Free Cash Flow ($mm)1

7.3%

2017 Actual 2018E 2019E 2020E

$2.75 NYMEX $3.00 NYMEX $3.25 NYMEX

Return on Capital Employed1

$976

2017 Actual 2018E 2019E 2020E

$2.75 NYMEX $3.00 NYMEX $3.25 NYMEX

$155

2017 Actual 2018E 2019E 2020E

$2.75 NYMEX $3.00 NYMEX $3.25 NYMEX

Three-Year Cabot Oil & Gas Outlook

$1.6 bn - $2.5 bn of estimated cumulative after-tax

free cash flow from 2018 – 2020 to reinvest in

the business and return capital to shareholders

Three-Year Production CAGR: 17% - 21% (20% - 24% on a divestiture-adjusted basis)

Incremental share repurchases and debt reduction would further enhance the

growth of these metrics on a debt-adjusted per share basis and improve ROCE

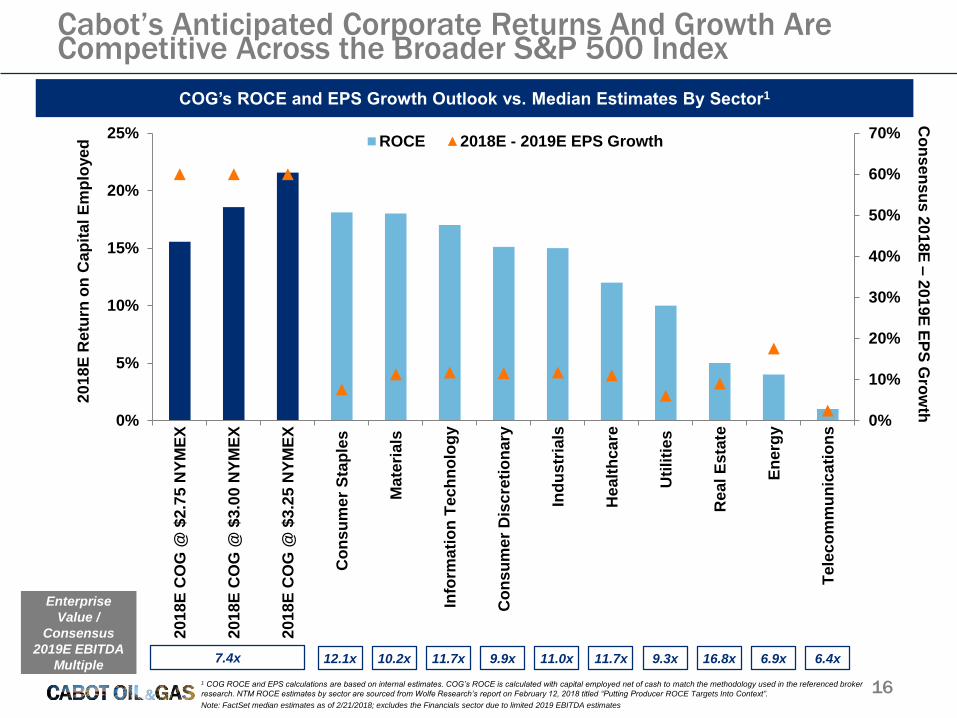

0%

10%

20%

30%

40%

50%

60%

70%

0%

5%

10%

15%

20%

25%

201

8E

CO

G @

$2.7

5 N

YM

EX

201

8E

CO

G @

$3.0

0 N

YM

EX

201

8E

CO

G @

$3.2

5 N

YM

EX

Co

ns

um

er

Sta

ple

s

Ma

teri

als

Info

rma

tio

n T

ec

hn

olo

gy

Co

ns

um

er

Dis

cre

tio

nary

Ind

us

tria

ls

Healt

hca

re

Uti

liti

es

Real

Esta

te

En

erg

y

Te

lec

om

mu

nic

ati

on

s

ROCE 2018E - 2019E EPS Growth

161 COG ROCE and EPS calculations are based on internal estimates. COG’s ROCE is calculated with capital employed net of cash to match the methodology used in the referenced broker

research. NTM ROCE estimates by sector are sourced from Wolfe Research’s report on February 12, 2018 titled “Putting Producer ROCE Targets Into Context”.

Note: FactSet median estimates as of 2/21/2018; excludes the Financials sector due to limited 2019 EBITDA estimates

COG’s ROCE and EPS Growth Outlook vs. Median Estimates By Sector1

Cabot’s Anticipated Corporate Returns And Growth Are Competitive Across the Broader S&P 500 Index

Enterprise

Value /

Consensus

2019E EBITDA

Multiple7.4x 12.1x

20

18

E R

etu

rn o

n C

ap

ital E

mp

loye

d

Co

ns

en

su

s 2

01

8E

–2

01

9E

EP

S G

row

th

10.2x 11.7x 9.9x 11.0x 11.7x 9.3x 16.8x 6.9x 6.4x

17

Illustrative Average Annual After-Tax Corporate Free Cash Flow at 3.7 Bcf/d Flat ($bn)

$1.0

$1.2

$1.4

$2.75 NYMEX $3.00 NYMEX $3.25 NYMEX

Average Annual Maintenance Capital: ~$500mm

Implied FCF Yield

Based on Current

Market Cap1:

9%

Implied FCF Yield

Based on Current

Market Cap1:

11%

Implied FCF Yield

Based on Current

Market Cap1:

13%

Best-in-Class Marcellus Capital Efficiency

1 Based on market capitalization as of February 22, 2018

Note: Assumes ($0.35) long-term weighted-average differential to NYMEX

Cabot’s expects to reach 3.7 Bcf/d of gross production in 2020

Cabot management expects to grow volumes above this illustrative 3.7 Bcf/d maintenance level by securing

incremental firm transport capacity / firm sales and / or increasing in-basin market share

Cabot would generate $1.6bn - $2.5bn of cumulative after-tax corporate free cash flow from 2018 – 2020 before

getting to this maintenance level (based on a $2.75 - $3.25 NYMEX price range in 2018 – 2020)

The illustrative annual free cash flow estimates below include the impact of income taxes, corporate overhead, and

interest expense

Appendix

Full-year 2018 total company daily production growth

guidance: 10% - 15% (18% - 23% on a divestiture-adjusted

basis to reflect the impact of the previously announced

Eagle Ford, East Texas, and West Virginia dispositions)

– 2018 exit-to-exit divestiture-adjusted production

growth guidance: 35%+

– Q1 2018 production guidance: 1,825 – 1,875 Mmcfe/d

(97% natural gas)

2018 total program spending: $950 million

– Marcellus Shale: $800 million

– Exploration Areas: $75 million

– Pipeline Investments: $60 million

– Corporate: $15 million

2018 Marcellus Shale drilling and completion activity:

– 85 net wells drilled / 95 net wells completed

2018 income tax rate guidance: 23% - 24%

2018 deferred tax rate guidance: 100%+ (The Company

expects to receive a refund in 2018 associated with the

recent repeal of the corporate alternative minimum tax)

2018E Differential Guidance (Before the Impact of Derivatives)

Q1 2018 FY 2018

Natural Gas ($/Mcf) ($0.40) – ($0.45) ($0.45) – ($0.50)

2018E Natural Gas Price Exposure By Index

Q1 2018 FY 2018

Fixed Price (~$2.75/Mcf) 24% 20%

NYMEX 24% 21%

TGP Zone 4 – 300 Leg 19% 21%

Leidy Line Receipts 18% 14%

Millennium East 7% 6%

Dominion 6% 6%

Columbia 2% 3%

D.C. Area Market NA 8%

PJM Power Market NA 1%

Note: Fixed price percentages above include volumes associated with

sales agreements that have floor prices. An additional deduct of ~$0.05

per Mcf should be applied to account for fuel use.

FY 2018E Cost Assumptions ($/Mcfe, unless otherwise noted)

Direct operations $0.09 - $0.11

Transportation and gathering $0.66 - $0.68

Taxes other than income $0.02 - $0.03

Depreciation, depletion and amortization $0.50 - $0.60

Interest expense $0.09 - $0.11

General and administrative ($mm)1 $60

Exploration ($mm)2 $35(1) Excluding stock-based compensation(2) Excluding exploratory dry hole costs; includes exploration

administration expense and geophysical expenses

2018 Guidance

20

$304

$87$188

$62

$575

$312

$0

$100

$200

$300

$400

$500

$600

2018 2019 2020 2021 2022 2023 2024 2025 2026

7.2%

6.5%

4.3%

6.2%

3.7%

Natural Gas (NYMEX) Swaps

Total Volume (Bcf)

Average Price per Mcf

Natural Gas (NYMEX) Basis Swaps

Total Volume - Leidy (Bcf)

Average Price per Mcf (Leidy)

Total Volume – Transco (Bcf)

Average Price per Mcf (Transco)

98.0

$2.87

34.1

($0.68)

10.7

$0.41

As of 12/31/2017 $bn

Cash and Cash Equivalents $0.5

Debt $1.5

Net Debt $1.0

Net Capitalization $3.6

Liquidity $2.2

Net Debt / Capitalization 29.2%

Net Debt / LTM EBITDAX 1.0x

2018 Hedge Position1

Debt Maturity Schedule ($mm) (Including Weighted Average Coupon Rate)

Capitalization / Liquidity

4.2%

Financial Position and Risk Management Profile

1As of February 22, 20182Based on the midpoint of the production guidance range

Approximately 34% of Cabot’s forecasted 2018 natural gas

volumes are locked-in at an average price of ~$2.80 per Mcf

(includes NYMEX swaps and fixed price contracts)2

21

2018 – 2019 Hedge Summary

2018 Natural Gas Swaps

# of Total $/Mcf

Pricing Index Contracts Mcf/Day Fixed Price Duration

LDS NYMEX 26 252,574 $2.93 Feb-18 Dec-18

LDS NYMEX 5 48,572 $3.10 Feb-18 Oct-18

2018 Natural Gas Basis Swaps

# of Total $/Mcf

Pricing Index Contracts Mcf/Day Fixed Price Duration

Leidy 5 48,572 ($0.71) Jan-18 Dec-18

Leidy 5 48,572 ($0.68) Feb-18 Dec-18

2018-2019 Natural Gas Basis Swaps

# of Total $/Mcf

Pricing Index Contracts Mcf/Day Fixed Price Duration

Transco 3 29,143 $0.42 Jan-18 Dec-19

Note: As of February 22, 2018

The table above does not include fixed price deals that cover ~20%

of Cabot’s forecasted 2018 natural gas volumes at ~$2.75 per Mcf

22

Three-Year Outlook Assumptions

Three-Year Outlook Assumptions (Slide 15)

• ~($0.50) per Mcf weighted-average basis differential in 2018 and ~($0.35) per Mcf weighted-average basis differential in 2019

and 2020

• ~$850 million of annual total company capital spending in 2019 and 2020 (no investments in equity pipelines in 2019 and

2020 as Constitution is not included in this three-year outlook)

• No capital associated with exploration activity in 2019 and 2020; however, assumes ~$35 million of corporate exploration

expense annually. This assumption is subject to change based on the initial results from the ongoing testing in the

Company’s exploratory areas

• Refinancing of notes at maturity based on current market indications

• For purposes of this illustrative analysis, free cash flow is maintained on the balance sheet (ROCE outlook does not reflect

the benefit of this free cash flow)

• Corporate tax rate between 23% and 24% in 2018 – 2020

• Deferred tax rates dependent on NYMEX price assumptions—100%+ in 2018 for all three price cases; a range of 70% to

100%+ in 2019 and 25% to 50% in 2020

• Service cost inflation of 5%+ annually in 2019 and 2020 (subject to market conditions)

• Cash G&A expense increases of 3% and 4% in 2019 and 2020, respectively

• No change to the current Pennsylvania state Impact Fee

23

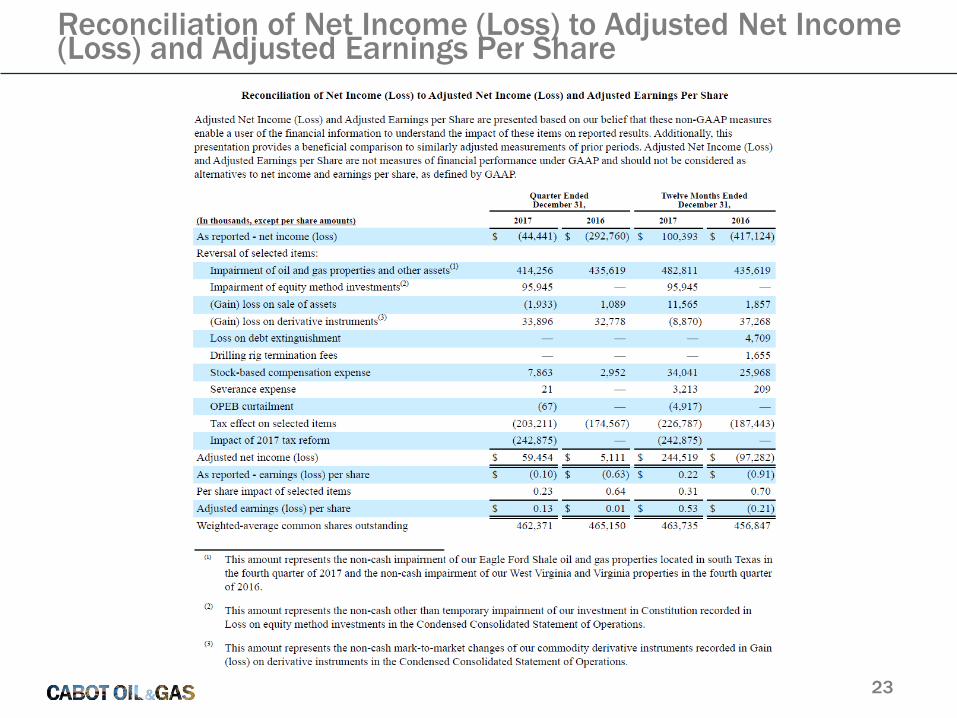

Reconciliation of Net Income (Loss) to Adjusted Net Income (Loss) and Adjusted Earnings Per Share

24

EBITDAX Calculation and Reconciliation

25

Net Debt Reconciliation

26

Discretionary Cash Flow and Free Cash Flow Calculation and Reconciliation

27

Return on Capital Employed (ROCE) Calculation and Reconciliation

A decade of progress and perseverance in the Marcellus Shale.