TN Foundational Skills Curriculum Supplement Preschool Unit 1

For Producer or Broker/Dealer Use Only.

Not for Use with the General Public.

© 2019 MetLife Services and Solutions, LLC

FoundationalProduct Curriculum:Dental

L0919518486[exp1220][All States][DC,GU,MP,PR,VI]

Why the Need?

For Producer or Broker/Dealer Use Only.

Not for Use with the General Public.

Why the Need?

Employee

• Valued benefit

• Benefits defray costs

• Pre-tax (Section 125)

• Access to discounted care (in-network)

• Encourages oral health

Employer

• Attract and retain employees

• Total healthcare cost implications

• Productivity implications

For Producer or Broker/Dealer Use Only.

Not for Use with the General Public.

Objectives of a Dental Benefit PlanFor the Customer

To be effective, both Dental PPOs and DHMOs should accomplish these

essential things:

• Cost-effectively manage the services people need and want

• Promote oral health and standards of care

• Promote a healthy and safe environment for patient care

• Encourage preventive care and proactive treatment of disease

For Producer or Broker/Dealer Use Only.

Not for Use with the General Public.

Benefit ValueDental insurance enjoys a high demand in the market, consistently ranking among

the top 5 most valued benefits

Source: 15th Annual Employee Benefits Trends Study

For Producer or Broker/Dealer Use Only.

Not for Use with the General Public.

Oral Health Matters

It is important:

• To promote oral health improvements

• To educate and equip participants and dentists

• To drive more proactive behaviors

• To provide thoughtful, ongoing reporting and analysis

• To coordinate more robust health care interventions and analysis with data, insights tools

and tactics

• To leverage dental as a vehicle to promote overall well being

For Producer or Broker/Dealer Use Only.

Not for Use with the General Public.

Poor Oral Health has Broad Implications

• 51,540 people will get oral cavity or oropharyngeal cancer. From 2007 to 2013

there was a 65% – a 5 year survival rate.1

• There are meaningful connections between oral health and a variety of systemic

conditions and treatment modalities.

1) Cancer Facts and Figures 2015, American Cancer Society, https://cancerstatisticscenter.cancer.org/?_ga=2.139848819.1768896036 .1520013141-2119312434.1520013141#!/ accessed March 2, 2018.

Basic Plan Design Components

For Producer or Broker/Dealer Use Only.

Not for Use with the General Public.

What Makes up a Dental Program?

Types of Coverage

• Indemnity, PPO, DHMO

Dental Provider Network

Plan Design

• Schedule of Benefits (coinsurance, deductibles, maximums, etc.)

Rates

• 2 Tier, 3 Tier, 4 Tier

Contract (Policy and Certificate)

Underwriting

Claims Process and Payments

Customer Service

For Producer or Broker/Dealer Use Only.

Not for Use with the General Public.

Self-Insured vs. Fully-Insured

Fully-Insured Self-Insured

Who assumes the financial risk (bears risk of claims and/or expense fluctuations)?

Insurance Company Plan Sponsor

Plan funding Monthly Premium (rate)Monthly Administrative Fee

(daily bank funding for claims)

Who bears fiduciary liability for claims determinations?

Insurance CompanyPlan Sponsor and

Insurance Company

Are premium taxes paid? Yes No

For Producer or Broker/Dealer Use Only.

Not for Use with the General Public.

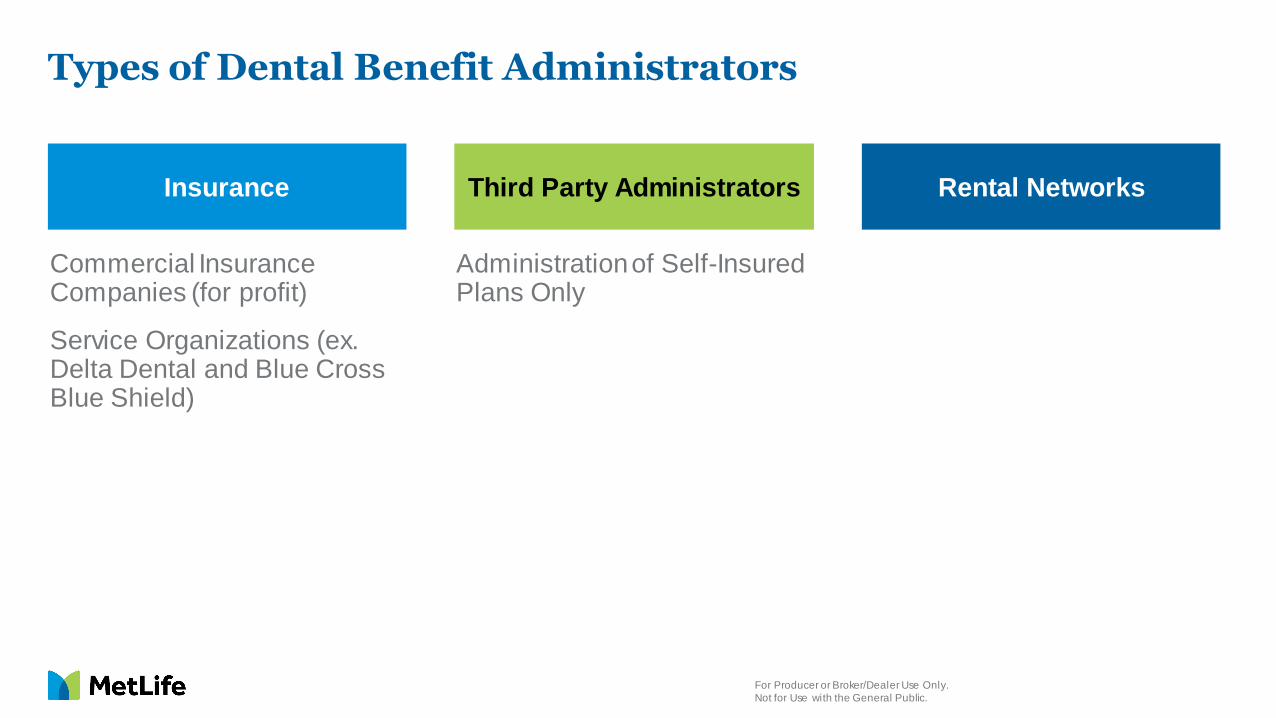

Types of Dental Benefit Administrators

Commercial Insurance Companies (for profit)

Service Organizations (ex. Delta Dental and Blue Cross Blue Shield)

Insurance Third Party Administrators Rental Networks

Administration of Self-Insured Plans Only

For Producer or Broker/Dealer Use Only.

Not for Use with the General Public.

Types of Dental Plans

• Fee for Service• Participants can go to any Provider and are

reimbursed at a set amount

Indemnity

• Participants have access to certain Providers within a network

• The network is made up of Providers that have agreed to lower their rates for participants and meet quality standards

Dental Health Maintenance Organization (DHMO)

• Participants can select Providers in or out of the carrier network and receive coverage

• Access to Dentists and Specialists without a referral from a General Dentist

Preferred Provider Organization (PPO)

• Direct Reimbursement: reimbursement based on dollar expenditures rather than the type of treatment (e.g. 100% coverage for the first $200 of care; 80% for the next $500 of care, etc.)

• Access Plans: discounts on Dental services without any “insurance coverage”

• Individual Plans: individually underwritten and administered plans; not group insurance

Other Types of Plans

For Producer or Broker/Dealer Use Only.

Not for Use with the General Public.

What is the Difference?

INDEMNITY PPO DHMO

Reimbursement Fee for Service Fee for ServiceCapitation +

Supplemental Payments

Plan DesignDeductible and coinsurance

applies to plan maximum

Deductible and

coinsurance/copays applies to

plan maximum

No deductible,

coinsurance/copays, or

plan maximum

Network No, visit any Dentist Yes, visit any DentistYes, out-of-network benefit

limited to emergencies

Network Access Does not Apply

Generally larger with nationwide

access; participants must select

Provider prior to care; No

Specialist referral required

Generally smaller with local

access defined by site;

participants must select Provider

prior to care; Specialist

referral required

Managed Care Low Moderate High

Premium High Moderate Low

For Producer or Broker/Dealer Use Only.

Not for Use with the General Public.

Allocation of Services

Type A

• Oral Exams

• X-Rays

• Prophylaxis

Type B Type C

• Fillings

• Extractions

• Sealants

• Crowns

• Dentures

• Implants

For Producer or Broker/Dealer Use Only.

Not for Use with the General Public.

PPO Schedule of BenefitsBENEFIT BENEFIT AMOUNT AND HIGHLIGHTS

Dental Insurance For You and Your Dependents

In-Network Out-of-Network

Covered Percentage for: Based on negotiated fee schedule Based on Reasonable and Customary (R&C)

Type A Services 100% 100%

Type B Services 80% 80%

Type C Services 50% 50%

Orthodontic Covered Services 50% 50%

Deductibles for:

Yearly Individual Deductible$50 for the following Covered Services

Combined: Type B; Type C

$50 for the following Covered Services

Combined: Type B; Type C

Yearly Family Deductible$150 for the following Covered Services

Combined: Type B; Type C

$150 for the following Covered Services

Combined: Type B; Type C

Maximum Benefit:

Yearly Individual Maximum$1,500 for the following Covered Services:

Type A; Type B; Type C

$1,000 for the following Covered Services:

Type A; Type B; Type C

Lifetime Individual Maximum for Orthodontic

Covered Services$1,000 $1,000

For Producer or Broker/Dealer Use Only.

Not for Use with the General Public.

Deductible

• Incurred expense paid by the plan participant before benefits are paid

• Annual deductible (calendar year or 12 month period)

• Individual vs. Family

• Passive vs. Steerage (In vs. Out-of-Network)

In/Out-of-Network• $50 per Individual• Applies to Type B & C Services• 3X (per individual) per Family

Standard Single / Family

VariationsSingle / Family

In/Out-of-Network• Range from $0 to $300 (in $5

increments)• Applies to: Type A,B,&C, or C Services

Only• 2x (per individual) per Family; 2x&3x

per Individual

Alternate Cost

Effective Example:

Type B & C $25 / $50

Type A, B & C $50 / $100

For Producer or Broker/Dealer Use Only.

Not for Use with the General Public.

Coinsurance

• Enables the insurance company and plan participant to share the risk and expenses associated with services

• Different coinsurance levels based on covered service

• Passive vs. Steerage (In vs. Out-of-Network)

Standard Variations

Alternate Cost

Effective Example:

100/80/50

In/Out-of-Network

100/80/50 In-Network

100/60/40 Out-of-Network

In-Network Out-of-Network

Type A 100% 100%

Type B 80% 80%

Type C 50% 50%

In-Network Out-of-Network

Range from 50% to 100% (in 5% increments)

Range from 25% to 100% (in 5% increments)

Range from 0% to 80% (in 5% increments)

For Producer or Broker/Dealer Use Only.

Not for Use with the General Public.

Orthodontia: Coinsurance & Lifetime Maximum

Alternate Cost

Effective Example:

$1,500

Lifetime Maximum

$1,000

Lifetime Maximum

Type D Co-Insurance

Lifetime Maximum

Type Standard Variations

In/Out-of-Network

50%

$1,500

In/Out-of-Network

Range from 20% to 80%

(in 5% increments)

Range from $250 to $3,000

(in $50 increments)

*MetLife: option to select either “To age 19” or “Dependent age Limit”

For Producer or Broker/Dealer Use Only.

Not for Use with the General Public.

Annual Maximum Benefits

• Benefit dollars to which a plan participant is entitled to for a stated period of time

• Calendar Year (consecutive)

- Applies to: Type A, B & C Services

• Passive vs. Steerage (In vs. Out-of-Network)

Standard Variations

Alternate Cost

Effective Example:

$1,500

In/Out-of-Network

1,500 In-Network

$1,000 Out-of-Network

In/Out-of-Network

$1,500

In/Out-of-Network

Range from $250 to $5,000

(in $50 increments)

For Producer or Broker/Dealer Use Only.

Not for Use with the General Public.

Frequency & Age Limitations

What is a Plan Frequency?

The frequency with which certain services will be covered

• Oral exam/cleaning (once every six months)

• Full mouth x-rays (once every five years)

Age Limitation Example:

Bitewings – variations between adult and child(ren)

• Adult: 1 per 12 months

• Children up to age 19: 1 per 6 months

• -OR- 1 per 12 for both adult and child(ren)

For Producer or Broker/Dealer Use Only.

Not for Use with the General Public.

In-Network & Out-of-Network

• Reimbursement based on network schedule

• Dentist may not bill more than schedule amount

In-Network Dentist Out-of-Network Dentist

• Reimbursement based on what is reasonable & customary (R&C) for service(s) provided

• Dentist may bill more than the reasonable & customary (R&C) amount

For Producer or Broker/Dealer Use Only.

Not for Use with the General Public.

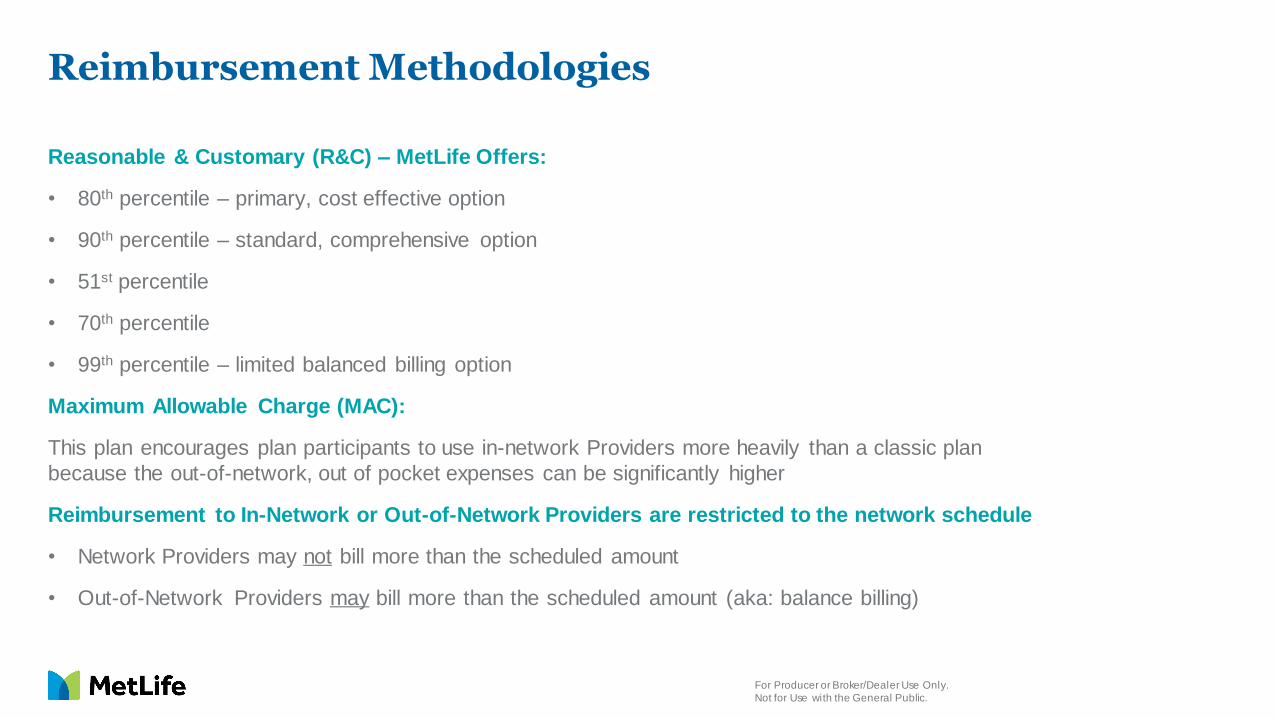

Reimbursement Methodologies

Reasonable & Customary (R&C) – MetLife Offers:

• 80th percentile – primary, cost effective option

• 90th percentile – standard, comprehensive option

• 51st percentile

• 70th percentile

• 99th percentile – limited balanced billing option

Maximum Allowable Charge (MAC):

This plan encourages plan participants to use in-network Providers more heavily than a classic plan

because the out-of-network, out of pocket expenses can be significantly higher

Reimbursement to In-Network or Out-of-Network Providers are restricted to the network schedule

• Network Providers may not bill more than the scheduled amount

• Out-of-Network Providers may bill more than the scheduled amount (aka: balance billing)

For Producer or Broker/Dealer Use Only.

Not for Use with the General Public.

Exclusions & Limitations

Designed to control claim cost and eliminate unnecessary dental care

Exclusions: non-covered services as defined in the contract/certificate

• Examples include: TMJ (in certain states) and cosmetic services

Limitations: limit the frequency with which certain services will be covered

• Examples include: - Oral exams/teeth cleanings (once every six months)

- Full mouth x-rays (once every five years)

For Producer or Broker/Dealer Use Only.

Not for Use with the General Public.

ContractPolicy & Certificate

Schedule of Benefits Exclusions

Covered Services Limitations

Predetermination of Benefits Continuity of Coverage

Coordination of Benefits Alternative Benefits

Late Entrant Penalty Extension of Benefits

For Producer or Broker/Dealer Use Only.

Not for Use with the General Public.

PPO vs. DHMO – How do they differ?

• Plan payments

• Patient out of pocket responsibility

• Charges for non-listed and excluded services

Dental PPO Dental HMO

• Capitation payments (fixed, per patient/month)

• Patient copayments

• Additional fees (labs, precious metals, porcelain) - should be pass through expense

• Encounter submission payment

• Supplemental schedule

• Specialty care (discounted fee for service)

• Charges for non-listed or excluded services (ex. implants and associated services)

For Producer or Broker/Dealer Use Only.

Not for Use with the General Public.

What Plan Provision Applies to which Type of Dental Plan?

Provision Indemnity Plan PPO Plan DHMO Plan

Deductible Yes Yes No

Coinsurance Yes Yes Not Generally

Copay Not Generally Not Generally Yes

Calendar Year Maximum Yes Yes Often unlimited

Orthodontic Lifetime

MaximumYes Yes Not Generally

Allocation of Services by

“Type of Service”Yes Yes Not Generally

Frequency & Age Limitations Yes Yes Yes

Specialist Referral Required No No Generally

Coordination of Benefits Yes Yes Yes

Missing Tooth Exclusion Yes Yes Yes

Alternate Benefit Provision Yes Yes Sometimes

Out-of-Network

Reimbursement

(Usual & Customary,

Schedule, MAC)

Yes YesGenerally very low benefit

limited to emergency care only

MetLife Differentiators & Marketplace Trends

For Producer or Broker/Dealer Use Only.

Not for Use with the General Public.

MetLife Dental

• #1 Dental benefit plan administrator among all single commercial carriers1

• 21 million covered Dental plan participants2

• Over 32,000 customers2

• 47 of the top 100 FORTUNE 500® companies offer MetLife Dental benefits3

• Nearly 370,000 PDP Plus Dental access points for customers2

• 126,000 Unique Dentists2

• Over 33,000 Dental DHMO access points2

1. LIMRA data, based on enrolled lives as of 12/31/17

2. MetLife Data as of February 2019

3. 2018 MetLife Market Research, FORTUNE 500®, April 2018. FORTUNE 500® is a registered trademark of FORTUNE® magazine, a divisi on of Time, Inc.

For Producer or Broker/Dealer Use Only.

Not for Use with the General Public.

For Producer or Broker/Dealer Use Only.

Not for Use with the General Public.

Dental Benefit Trends

▪ Variability in PPO network models is causing confusion in the industry for

employers and intermediaries.

▪ Regulatory discussions regarding carrier use of rented networks.

Networks

Technology and

Consumerism

▪ Recent dental carrier focus has been on improved service delivery through

technology. Use of mobile technology is now considered table stakes.

▪ Demand for consumer transparency tools is increasing.

▪ Increased consumerism, online enrollment, use of exchanges is making second

sale expertise critical

▪ Increased interest in dental disease management/data exchange/benefit

integration and wellness capabilities.

▪ Significant focus on how dental carriers are tackling the opioid crisis.

Employers want to insure that both medical and dental providers and patients

are being evaluated to reduce opioid abuse.

▪ Employers are looking for options for part time employees

▪ More interest in vendor consolidation in order to reduce administrative

impacts on HR staff and data exposure

▪ Increased focus on vendor data and system security capabilities.

Disease

Management

and

Wellness

Employer

Groups

Source: Industry Roundtable Discussions

For Producer or Broker/Dealer Use Only.

Not for Use with the General Public.

For Producer or Broker/Dealer Use Only.

Not for Use with the General Public.

Dental Benefit Trends

Benefits &

Plan

Designs

▪ Dental benefit plan designs, with the exception of a few features like extra

cleanings for certain conditions, max rollover, preventive not counting

toward deductible, etc., have largely remained unchanged for decades.

▪ The market still has many outdated plans that have not been modernized in

terms of what services are covered and how they are covered.

▪ Core benefits are continuing with little change; however, plan design

components are changing to control cost, offer consumer choice, and

meet market demand.

▪ There are more high deductible dental plans being offered to complement

the increase in high deductible health plans and higher annual maximums to

accommodate the overall cost increase in dental procedures.

▪ Continued increase in the shift towards voluntary dental coverage for

both active and retiree coverage, little/no change in participation

Benefits

and

Plan

Designs

Source: Industry Roundtable Discussions

For Producer or Broker/Dealer Use Only.

Not for Use with the General Public.

For Producer or Broker/Dealer Use Only.

Not for Use with the General Public.

Dental Industry Trends

9% 8% 8% 8% 7%

62% 67%74%

78%82% 81%

19% 14%

11%7%

6% 6%9% 10%

6% 6% 4% 5%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2006 2008 2010 2012 2014 2016

DHMO DEPO DPPO Indemnity Discount Direct Reimbursement

DPPO plans continue to be the most popular type

of dental benefit plan by a large margin.

Commercial Dental Benefits by Plan Type1

1 Source: NADP 2017 Dental Benefits Report: Enrollment

22%

10% 9% 5% 7% 7% 6%

67%

66% 67% 73% 70% 71%64%

10%

24% 24% 22% 24% 23%30%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2010 2011 2012 2013 2014 2015 2016

Employer Pays All Employee & EmployerShare Cost

Employee Pays All

Voluntary dental benefits (employee pays all) are

continuing to increase as a share of group dental.

Source of Premium Funding2

2 Source: NADP/DDPA 2011-2017 Dental Benefits Joint Report: Enrollment

8%

Underwriting Basics

For Producer or Broker/Dealer Use Only.

Not for Use with the General Public.

Components of a Dental Rate

An adequate Dental rate must fund THREE elements:

1. Incurred or Expected Claims (EC)

• Claims paid

• Incurred but not reported claims reserves

• Trend adjustment (unique to Dental and Medical)

2. Expenses

• Product and claim expenses, commissions, premium taxes, and other administrative

expenses

3. Margin

• Profit

For Producer or Broker/Dealer Use Only.

Not for Use with the General Public.

Information Needed to Quote Dental

• Full plan design

• 12-36 months of paid premium, claims and lives

• Current/Renewal rates and rate history

• Employer contributions

• Employee census

• To include: zip code, tier selection (EE, EE + one, etc.), and plan choice, if applicable

• Commissions – current and proposed

What We Would Like Why We Need It

• To know what is being quoted, and to determine the appropriate trend

• To effectively project future claims

• To perform a more accurate premium analysis

• To predict anti-selection

• To calculate manual rates and PDP savings

For Producer or Broker/Dealer Use Only.

Not for Use with the General Public.

Factors Influencing Manual Rate

• Area – zip code driven pricing

• Network Penetration

• Participation – selection risk

• Tier Mix – enrollment distribution

• Single option vs. Multiple option (ex. High/Low plan option)

• DHMO vs. PPO

For Producer or Broker/Dealer Use Only.

Not for Use with the General Public.

Factors Influencing Manual Rate Plan Design

• Deductible

• Co-insurance

• Maximum

• Reimbursement

• Allocations

• Limitations/Exclusions

State Approvals & Limitations

For Producer or Broker/Dealer Use Only.

Not for Use with the General Public.

Regulatory and Filing Considerations

• Plan Design Restrictions Non-Covered Services

• Other Restrictions:- Exclusive Provider Organization (EPO) – in only requires filing

- Preventive only → minimum loss ratio rate filing requirements

For Producer or Broker/Dealer Use Only.

Not for Use with the General Public.

DHMO Availability

NADP enrollment report August 2017

MetLife DHMO

availability1

Largest DHMO Enrollment Nationwide

1. MetLife does not currently offer DHMO in Maryland

Network Basics

For Producer or Broker/Dealer Use Only.

Not for Use with the General Public.

What is the Purpose of a Dental Network?

Savings*

Lower plan costs, save employers and employees

money

Quality

Promote health, evidence-based treatment, safety

Stability

Low turnover, satisfied brokers / consultants, employers, employees

and dentists

1 2 3

Do all networks accomplish these goals?

Do your network analyses reflect differences among carriers?

*Savings from enroll ing in a dental benefits plan will depend on various factors including the cost of the plan, how often pa rticipants visit the dentist and the cost of services rendered.

For Producer or Broker/Dealer Use Only.

Not for Use with the General Public.

What is the Purpose of a Dental Network?

Savings

Lower plan costs, save employers and employees money

Key Influencers:

• Network Access — Do employees have the opportunity to go in-network?

• Network Discounts / Negotiated Fees — Does going in-network result in

savings?

• Claim Utilization Controls / Plan Management — Does the network help control

costs?

• Plan Design — Does the network support steerage and voluntary plan designs?

For Producer or Broker/Dealer Use Only.

Not for Use with the General Public.

Network ComparisonsIs What You See, What You Get?

The problem with comparisons…

• Counting methodology; selection criteria inclusiveness

• Consideration for patient volume• Dentist selection and retention criteria

Count

• Match criteria; file limitations• Do dentists submit in the same way to all

administrators?

Disruption & Repricing

• Standard fees vs. special fee (or leasing) arrangements

• Tiered networks (especially Specialists)

Discount

• Comparable participant protections?• Comparable contracts and guidelines?

Other Considerations

For Producer or Broker/Dealer Use Only.

Not for Use with the General Public.

Network Access

• Compares the proximity of employees to participating Dentists within set criteria (e.g. 1 General Dentist within 5,10, or 20 miles)

What is it? Why is it important?

• Identifies where, and to what extent, employees will have the option to choose in-network Dentists

• Defines areas for network enhancement

• Assists in establishing plan designs

• Specialty care

• In and out-of-network differentials

For Producer or Broker/Dealer Use Only.

Not for Use with the General Public.

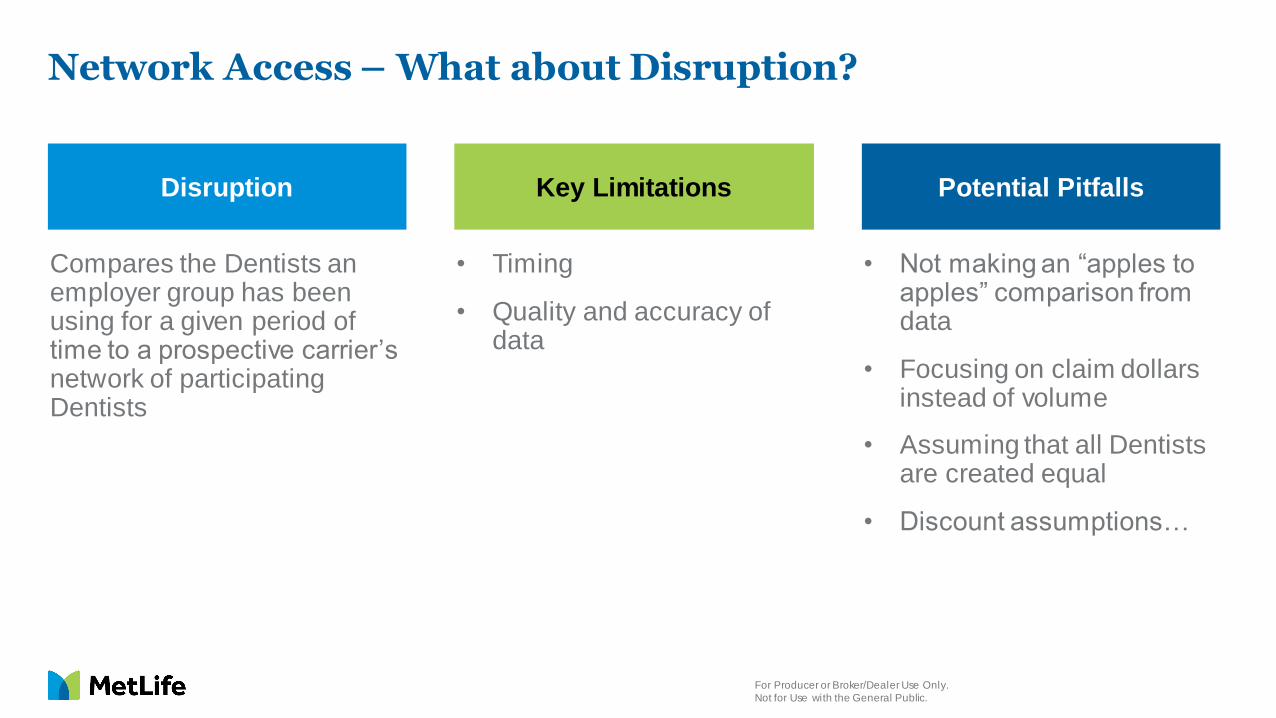

Network Access – What about Disruption?

Compares the Dentists an employer group has been using for a given period of time to a prospective carrier’s network of participating Dentists

Disruption Key Limitations Potential Pitfalls

• Timing

• Quality and accuracy of data

• Not making an “apples to apples” comparison from data

• Focusing on claim dollars instead of volume

• Assuming that all Dentists are created equal

• Discount assumptions…

For Producer or Broker/Dealer Use Only.

Not for Use with the General Public.

Disruption ReportsAre All Dentists Equal? Is 0% Disruption an Ideal Goal?

Disruption results show that Carrier B has 7 of top 10 most utilized Dentists.

Carrier A

Top 10 Utilized

Network Dentists

Carrier B

Network

Utilization

by Dentist

Schedule

Discount

Dentist 1 YES 10% 25%

Dentist 2 NO 9% 6%

Dentist 3 YES 8% 22%

Dentist 4 YES 7% 25%

Dentist 5 YES 6% 20%

Dentist 6 YES 5% 18%

Dentist 7 YES 4% 25%

Dentist 8 NO 3% 11%

Dentist 9 NO 2% 13%

Dentist 10 YES 1% 17%

Total: 7 of 10 55%

Which network uses benefit dollars most effectively?

• 10 Dentists

• 2 of the Dentists have low utilization

• 55% Plan Utilization

• 10.37% Weighted Avg. Discount

Carrier A Carrier B

• 7 Dentists

• 41% Plan Utilization

• 13.25% Weighted Avg. Discount

For Producer or Broker/Dealer Use Only.

Not for Use with the General Public.

Network Discounts

What are they?

• Reductions in the full amount that is usually charged for a service

Why are they important?

• When employees choose in-network Dentists, in-network discounts:

• Support lower plan costs

• Affect employee out-of-pocket savings

Do larger discounts always lead to lower rates and employer / employee savings?

How high or low should discounts go?

For Producer or Broker/Dealer Use Only.

Not for Use with the General Public.

Managing Costs

Who has the

best discounts?

Who has the

biggest network?

Who has the best combination of utilization and discounts?

Networks may be large, but do they include Dentists that participants visit?

For Producer or Broker/Dealer Use Only.

Not for Use with the General Public.

Network DiscountsUnderstand carrier’s calculations

Which discount is the largest? Look closer…

Carrier A Carrier B Carrier C

20% 27% 32%

In-Network(Schedule)

Basis of Discount (Carrier-Reported)

$100 $110 $125

$125 $150 $185

Can there be more than one average charge in an area?

Can carriers B and C have larger discounts if their in-network fee is higher?

For Producer or Broker/Dealer Use Only.

Not for Use with the General Public.

Network DiscountsUnderstand carrier’s calculations

Which discount is the largest? Look closer…

Carrier A Carrier B Carrier C

20% 12% 0%

In-Network(Schedule)

Basis of Discount (Carrier-Reported)

$100 $110 $125

$125 $125 $125

If basis of discount is equal….what is the effect on the discount?

For Producer or Broker/Dealer Use Only.

Not for Use with the General Public.

Effective DiscountsEvaluate network access and discounts together

• Area Discount — The total of all in-network covered fees for dental procedures

in a specific area divided by the total in-network submitted charges in that same

area for the same procedures, subtracted from 1.- e.g. $100 in-network fee, $125 average charge = 20% discount

• Network Utilization — The total of all submitted charges for procedures

performed by in-network providers divided by the total number of submitted

charges for services performed by both in- and out-of-network providers.

Effective

Discount=

Area Discount x Network Utilization (BEST)

Area Discount x Network Penetration (OK)

For Producer or Broker/Dealer Use Only.

Not for Use with the General Public.

Analyzing Networks & Discounts

A network is only as good as its

discounts

100% of Dentists in-network x 0% discount

= NO DISCOUNT

Discounts are only as good as the

network

100% discount x 0% in-network Dentists

= NO DISCOUNT

Find the right balance

Strong discounts x appropriate access

= VALUE & SAVINGS

Which is more important, access or discounts?

What drives plan value and employee savings?

For Producer or Broker/Dealer Use Only.

Not for Use with the General Public.

Effective DiscountsImpact on Plan Costs & Employee Savings

ABC Company has 1,000 employees who represent $625,000 in total

Dental claims. If you were their trusted advisor, which carrier would you

want to recommend that maximizes benefit dollars and provides value to

employees?

Carrier A Carrier B

Access Points 180,000 90,000

Aggregate Fee Schedule Discount 6% 25%

Total Claims ($) $625,000

In-Network Utilization (%) 80% 48%

In-Network Claims ($) $500,000 $300,000

In-Network Discount ($) $30,000 $75,000

Effective or Net Contracted Discount (%) 4.8% 12%

BUT…

smaller discounts decrease

plan value and increase

employee out-of-pocket costs!

Carrier A has 2x greater

access points!

Clinical Basics

For Producer or Broker/Dealer Use Only.

Not for Use with the General Public.

The Parts of a Tooth

For Producer or Broker/Dealer Use Only.

Not for Use with the General Public.

The Teeth

For Producer or Broker/Dealer Use Only.

Not for Use with the General Public.

The Types of Teeth

Primary Dentition (Deciduous/Baby Teeth)

• The first set of teeth that erupt in childhood, usually starting around 6-10 months

of age. Normally, there are 20 baby teeth.

Permanent Dentition (Adult Teeth)

• As the baby teeth fall out, the permanent teeth replace them. In addition, the

second and third permanent molars erupt behind the primary molars.

• Loss of primary teeth and replacement by permanent teeth usually begins at age

6. Normally, there are 32 permanent teeth.

For Producer or Broker/Dealer Use Only.

Not for Use with the General Public.

The Types of Teeth (cont.)

Primary (Deciduous) Teeth Permanent Teeth

For Producer or Broker/Dealer Use Only.

Not for Use with the General Public.

Classification of TeethArches & Quadrants

• There are two arches, upper (maxillary) and lower (mandibular) each having 16

adult teeth. Each arch is divided in half, and each half is called a quadrant.

• There are four quadrants in the mouth with eight teeth in each:- Upper Left (UL)

- Upper Right (UR)

- Lower Left (LL)

- Lower Right (LR)

• The term quadrant is also used to define certain dental procedures. (i.e. a

quadrant of gum surgery)

For Producer or Broker/Dealer Use Only.

Not for Use with the General Public.

Classification of Teeth (cont.)

ANTERIOR TEETH

• Incisors: the eight front teeth, four on top and four on the bottom. These teeth

are used for biting (incising) into food.

• Canines: also called “eye teeth”, canine teeth are in the corners of the mouth.

They are meant for grasping and tearing food and have very long roots.

POSTERIOR TEETH

• Bicuspids: the two teeth behind each canine for a total of eight teeth (two in

each quadrant). These teeth are meant for crushing food.

• Molars: usually three behind each 2nd bicuspid in the back of the mouth. There

are four teeth in each quadrant for a total of 12 molars. The last molar in each

quadrant is called the “wisdom” tooth.

For Producer or Broker/Dealer Use Only.

Not for Use with the General Public.

General Dental Terms and Meanings

• ENDODONTICS

• PERIODONTICS

• AMALGAM

• OCCLUSION

• PALLIATIVE

• RESTORATION

• PROPHYLAXIS

• PROSTHODONTICS

• BRUXING

Treatment of the Dental Pulp

Treatment of Gums (Gingiva)

Type of Restorative Material (“Silver Filling”)

The position of the teeth when the jaws are closed (Bite)

Treatment to relieve pain or alleviate a problem without dealing with the

underlying cause

Term to describe restoring the function of the tooth by replacing missing or

damaged tooth structure

Cleanings

Restoration and replacement of lost or damaged teeth

(Full and Partial Dentures/Bridges/Crowns/Veneers)

Grind

For Producer or Broker/Dealer Use Only.

Not for Use with the General Public.

Types of ProceduresDIAGNOSTIC SERVICES (Range of CDT Codes: D0100 – D0999)

Procedures that are necessary to recognize and identify any condition (and its causes) that

may not be normal. These are usually the initial services performed when a patient visits the

dentist for the first time or for a checkup.

• Periodic Exam: check-up visit. It is an exam of the head, neck, teeth and gums to see if

any conditions have developed since the last checkup which is usually performed within

the past year or six months.

• Comprehensive Exam: originally referred to as an initial exam. This is usually

performed on a new patient and includes recording and evaluation of existing dental work,

condition of teeth and gums. The new doctor then has a complete record of the patient’s

current oral condition.

• Consultation: an exam/evaluation that is performed by a doctor who will not actually treat

that patient.

• Bitewings: x-rays taken where a patient bites on a paper tab discloses the area in

between teeth that is difficult to visualize. Used to detect decay between the teeth.

For Producer or Broker/Dealer Use Only.

Not for Use with the General Public.

Types of Procedures (cont.)PREVENTIVE SERVICES (Range of CDT Codes: D1000 – D1999)

These procedures help a patient avoid, intercept, or minimize decay, and other diseases of

the oral cavity.

• Prophylaxis: includes removal of tarter and plaque above and below the gum line and

polishing the teeth, usually with a paste that includes fluoride.

• Fluoride Application: fluoride is applied to teeth to soak into the enamel and make it

more resistant to decay. This application of fluoride is apart from any fluoride in the prophy

paste.

• Sealants: thin, plastic coatings painted on the chewing surfaces of the back teeth from

getting in and causing decay.

• Space Maintainers: when a baby tooth is lost prematurely, a spacer is placed to prevent

adjoining teeth from shifting and blocking the proper eruption of the permanent tooth.

For Producer or Broker/Dealer Use Only.

Not for Use with the General Public.

Types of Procedures (cont.)RESTORATIVE SERVICES (Range of CDT Codes: D2000 – D2999)

The repair of teeth due to decay and trauma. The objective is to eliminate the disease,

restore the tooth to form and function, and to improve or regain appearance.

• Amalgam Filling: silver filling

• Resin/Composite Filling: tooth colored filling

• Inlay/Onlay: cast restorations constructed by a dental lab or a CAD/CAM machine in the

dental office that may be used instead of silver/white fillings to restore a tooth depending

on the extent of decay.

• Crown: a restoration that covers the part of the tooth visible in the mouth. Can be made

of various materials including precious (high noble) metal, semi-precious (noble) metal,

non-precious (base) metal, porcelain, ceramic, titanium, or acrylic (temporary).

• Post & Core: a type of dental restoration used to stabilize a weakened tooth or provide

an anchor for a crown. A metal, glass/ceramic or fiber post is placed in one of the roots of

a tooth that has had root canal treatment and the filling on top to provide support

for a crown.

For Producer or Broker/Dealer Use Only.

Not for Use with the General Public.

Types of Procedures (cont.)ENDODONTIC SERVICES (Range of CDT Codes: D3000 – D3999)

Dentistry that deals with treating the infected nerves of teeth.

• Pulpotomy: often referred to as a “baby root canal.” A pulpotomy removes the diseased

pulp tissue within the crown portion of the tooth.

• Pulp Cap: technique used to prevent the dental pulp from dying, after being exposed, or

nearly exposed during a cavity preparation. A dressing is placed over the pulp prior

placement of the dental restoration.

• Root Canal Therapy: removal of the nerve of an infected tooth and replacement of the

nerve with a bio-compatible material which allows for retention of the tooth rather than

extraction.

• Apicoectomy/Retrograde Amalgam: surgery to the root tips of a tooth that has not

responded favorably to root canal therapy because the infection has not gone away.

For Producer or Broker/Dealer Use Only.

Not for Use with the General Public.

Types of Procedures (cont.)PERIODONTIC SERVICES (Range of CDT Codes: D4000 – D4999)

Procedures that treat the gingiva (gums) and bone.

• Scaling and Root Planing: also known as non-surgical periodontal therapy, or deep cleaning, is the removal of plaque and calculus (tartar) above the gums and on the root surfaces to get rid of the bacteria that cause gum disease. It helps to reduce inflammation and allows the gum tissue to heal.

• Osseous Surgery: refers to a number of different periodontal surgeries aimed at gaining access to the tooth roots to remove tartar and bacteria. Done in cases where nonsurgical periodontal therapy was unsuccessful in resolving the disease.

• Periodontal Maintenance: follow-up to active nonsurgical and/or surgical periodontal therapy.

• After the disease has been controlled, the patient is put on 4910 (interval depends on condition

and dentist’s judgment).

• Includes evaluation, cleaning above and below the gum line, and smoothing of root surfaces (SCRP) as needed where there are

pockets.

• Localized Delivery of Antimicrobial Agents: medication that is inserted into periodontal pockets to suppress bacterial infection.

• Guided Tissue Regeneration: dental surgical procedures that use barrier membranes to direct the growth of new bone and gingival tissue

• Crown Lengthening: a surgical procedure for teeth that have broken and/or decayed below the bone level so that a filling/cap can be placed.

For Producer or Broker/Dealer Use Only.

Not for Use with the General Public.

Types of Procedures (cont.)PROSTHODONTIC SERVICES (Range of CDT Codes: D5000 – D5999; D6200 – D6999)

Dentistry that deals with replacement of missing teeth.

• Complete Dentures: replaces all teeth in the arch.

• Removable Partial Dentures: an appliance made of metal and /or plastic that replaces

missing teeth, but some natural teeth are still present.

• Abutment: a crown that supports a fixed bridge.

• Pontic: the false tooth on a fixed bridge.

• Fixed Bridge: a combination of abutments and pontics that replace missing teeth. Also

referred to as a fixed partial denture.

For Producer or Broker/Dealer Use Only.

Not for Use with the General Public.

Types of Procedures (cont.)IMPLANT SERVICES (Range of CDT Codes: D6000 – D6199)

• Implant: an artificial tooth root that is placed into the jaw to hold a

replacement tooth or bridge. It is usually made out of titanium.

For Producer or Broker/Dealer Use Only.

Not for Use with the General Public.

Types of Procedures (cont.)ORAL SURGERY (Range of CDT Codes: D7000 – D7999)

Removal of teeth.

• Extraction: extraction, erupted tooth or exposed root. It is the removal of a tooth where

most of the tooth is visible in the mouth.

• Extraction: removal of an erupted tooth requiring removal of bone and/or sectioning of

tooth, including elevation of flap if indicated . Includes related cutting of gingiva and bone,

removal of tooth structure, minor smoothing of socket bone and closure.

• Extraction of Impacted Teeth: removal of a tooth that is not erupted, and leaning against

another tooth or buried so deep in bone that it will probably not erupt on its own.

• Brush Biopsy: a noninvasive procedure to detect oral cancer during which a

sterile brush is rotated against a suspected lesion to obtain a tissue sample.

For Producer or Broker/Dealer Use Only.

Not for Use with the General Public.

Types of Procedures (cont.)ORTHODONTICS (Range of CDT Codes: D8000 – D8999)

Movement of teeth with metal/plastic brackets and rubber bands to improve

cosmetics and/or function. Also known as “braces.”

For Producer or Broker/Dealer Use Only.

Not for Use with the General Public.

Types of Procedures (cont.)ADJUNCTIVE GENERAL SERVICES (Range of CDT Codes: D9000 – D9999)

• Palliative Treatment of Pain: this is typically reported on a “per visit” basis for

emergency treatment of dental pain.

• Local Anesthesia: analgesic service that (a) doesn’t “sever” the pain response and (b) is

typically considered by code definitions to be a part of another billable service (such as a

filling or crown).

• Occlusal Adjustments: adjusting (or grinding) of the biting surface of the tooth/teeth.

• General Anesthesia and IV Sedation: anesthesia service that (a) does “sever” the pain

response and (b) is typically reimbursed in support of cutting services such as surgical

extractions and periodontal surgery.

• Occlusal Guard: removable dental appliances, which are designed to minimize the

effects of bruxism (grinding) and other occlusal factors.

Additional Dental Terminology

R&C (Reasonable and Customary) fee refers to the R&C charge, which is based on the lowest of (a) the dentist’s actual charge,(b) the dentist’s usual charge for the same or similar services, or (c) the charge

of most dentists in the same geographic area for the same or similar services as determined by MetLife.

Negotiated Fees refers to the fees that in-network dentists have agreed to accept as payment in full for covered services, subject to any co-payments, deductibles, cost sharing and benefits

maximums. Negotiated fees are subject to change.

For Producer or Broker/Dealer Use Only.

Not for Use with the General Public.

General Terminology

• Coinsurance: member’s share of the costs of a covered service calculated as a percent of the

allowed amount for the service.

• Copayment: a fixed amount that the member pays directly to a provider for a covered service.

• Deductible: The amount a member owes before the insurer makes payment for covered services.

The deductible applies before any coinsurance or copayment amounts are applied, and may not apply

to all covered services.

• Member: the subscriber or a covered dependent for whom required premiums have been paid.

Whenever a member is required to provide a notice; “member” also means the member’s designee.

Also referred to as the plan participant

• Non-Participating Provider: a provider who does not have a contract with the carrier.

• Participating Provider: provider who has a contract with the carrier to provide services to the

member.

• Physician or Physician Services: health care services a licensed medical Physician (M.D. –

Medical Doctor or D.O. – Doctor of Osteopathic Medicine) provides or coordinates.

• Plan Year: a 12 month period beginning on the effective date of the plan or the anniversary of the

effective date of the plan.

For Producer or Broker/Dealer Use Only.

Not for Use with the General Public.

General Terminology (cont.)

• Premium: amount that must be paid for Dental insurance coverage.

• Primary Care Dentist (“PCD”): participating dentist who directly provides or coordinates a range of

Dental services.

• Provider: appropriately licensed, registered or certified Dentist, Dental Hygienist, or Dental Assistant.

• Referral: authorization given to one participating provider from another participating provider (usually

from a PCD to a Specialist) in order to arrange for additional care for a member

• Schedule of Benefits: coinsurance/copayments, deductibles, and other limits on covered services.

• Specialist: Dentist who focuses on a specific area of Dentistry or a group of patients to diagnose,

manage, prevent or treat certain types of symptoms and conditions, such as: oral surgery,

endodontics, periodontics, orthodontia, and pediatric dentistry.

For Producer or Broker/Dealer Use Only.

Not for Use with the General Public.

General Terminology (cont.)

• Spouse: person to whom the subscriber is legally married, including a same sex spouse.

• Subscriber: person that is covered under the contract that is issued. Also referred to as the member

or plan participant

• UCR (Usual, Customary and Reasonable): cost of a dental service in a geographic area based on

what providers in the area usually charge for the same or similar service.

• Utilization Review: review to determine whether services are or were dentally necessary or

experimental or investigational.

For Producer or Broker/Dealer Use Only.

Not for Use with the General Public.

DHMO Specific Terminology

• Capitation: monthly fee paid to a general dentist under a Managed Care Plan based on the number of subscribers who have

selected that dentist as their primary care dentist. Capitation is based on the plan – richer plans have higher capitation to

offset lower co-pays, etc.

• Capitation Plan, DHMO, DMO, Managed Care Plan, Managed Dental Plan, Prepaid Plan: names for Dental HMOs.

Capitation is paid on a monthly basis, whether the patient is seen or not. These plans are sometimes referred to as “prepaid” ,

because the carrier pays the provider in advance.

• Direct Referral: specialty care on a DHMO plan is accessed through network specialists. A general dentist refers the patient

to a local contracted specialist, on most standard DHMO plans.

• Internal Note: the majority of specialty care referrals do not require approval from MetLife, with the exception of orthodontia and some periodontal referrals required in CA.

• DMHC: Department of Managed Health Care. Regulatory agency that oversees DHMO in CA.

• DHMO: Dental Health Maintenance Organization: most plans have in-network benefits only, do not have maximums,

deductibles, alternate treatment provisions, pre-existing condition exclusions, or require claim forms.

• Encounter Fee: the general dentist receives a fee for each subscriber they sees.

• Evidence of Coverage (EOC): the Managed Care Plan document equivalent to a certificate of insurance (or summary plan

description).

• Exclusions & Limitations (E&Ls): typically appear at the end of the Schedule of Benefits (SOB).

For Producer or Broker/Dealer Use Only.

Not for Use with the General Public.

DHMO Specific Terminology (cont.)

• Florida Department of Financial Services: Regulatory agency that oversees both PPO and DHMO in FL.

• New York Department of Financial Services: Regulatory agency that oversees both PPO and

Managed Dental plans in NY.

• New Jersey Department of Banking and Insurance: Regulatory agency that oversees both PPO

and DHMO plans in NJ.

• Office Visit Co-Payment: a nominal fee (usually $0-$5)the member pays that applies to every

office visit.

• Rosters: DHMO contracted General Dentists receive a monthly list of members/subscribers that are assigned to their office

and eligible for care.

• Schedule of Benefits (SOB): list of covered procedures with the CDT codes and co-pays or coinsurance percentages for

each plan.

• Self-Referral: “self-referral" plans (generally identified with a "D" in the SG plans) allow members to select a specialist from

the online directory and call directly for an appointment. These plans provide specialty care at a reduced fee, equal to 75% of

the provider's usual fee – rather than at a co-pay.

• Supplemental(s): a contracted fee paid to DHMO providers for complex services, not typically

included in the capitation assumption.

• Example: Crowns and bridges normally have an agreed upon supplemental.

• TDI: Texas Department of Insurance. Regulatory agency that oversees both PPO and DHMO in TX.

For Producer or Broker/Dealer Use Only.

Not for Use with the General Public.

Product and service disclosures

[GROUP DENTAL PLAN/PROGRAM benefits featuring the MetLife Preferred Dentist Program are provided by Metropolitan Life Insurance

Company, 200 Park Avenue, New York, NY 10166.]

[DENTAL MANAGED CARE PLAN/PROGRAM benefits are provided by Metropolitan Life Insurance Company, a New York corporation in

NY. Dental HMO plan/program benefits are provided by: SafeGuard Health Plans, Inc. a California corporation, in CA; SafeGuard Health

Plans, Inc. a Florida corporation, in FL; SafeGuard Health Plans, Inc., a Texas corporation, in TX; and MetLife Health Plans, Inc., a Delaware

corporation, and Metropolitan Life Insurance Company, a New York corporation, in NJ. The Dental HMO/Managed Care companies are part

of the MetLife family of companies. “DHMO” is used to refer to product designs that may differ by state of residence of the enrollee, including

but not limited to: “Specialized Health Care Service Plans” in California; “Prepaid Limited Health Service Organizations” as described in

Chapter 636 of the Florida statutes in Florida; “Single Service Health Maintenance Organizations” in Texas; and “Dental Plan Organizations”

as described in the Dental Plan Organization Act in New Jersey.]

[Availability of METLIFE TAKEALONG DENTALSM is based on MetLife’s guidelines, group size and state approvals. Contact your MetLife

representative for complete details. MetLife TakeAlong Dental is not COBRA coverage and does not affect any employer obligation to

provide COBRA coverage. Like most insurance policies/benefit programs, insurance policies/benefit programs offered by Metropolitan Life

Insurance Company (MetLife) and its affiliates contain certain exclusions, exceptions, reductions, limitations, waiting periods and terms for

keeping them in force. Certain administrative services are provided through Careington International Corporation, Frisco, TX (Careington).

Careington is not affiliated with Metropolitan Life Insurance Company or its affiliates. Please contact MetLife for costs and complete details.

In certain states, availability of MetLife’s individual dental product is subject to regulatory approval.]

For Producer or Broker/Dealer Use Only.

Not for Use with the General Public.

![dental foundation training curriculum 2015 [DRAFT]copdend.org/data/files/Foundation/DFTCurriculum... · DENTAL FOUNDATION TRAINING CURRICULUM ... Dental Foundation Training Curriculum](https://static.fdocuments.in/doc/165x107/5ae9bf757f8b9ab24d8c7b6b/dental-foundation-training-curriculum-2015-draft-foundation-training-curriculum.jpg)