Foundation Certificate Synoptic - osbornebooks.co.uk · Task 1 (a) Documents Finance function (b)...

9

Osborne Books Tutor Zone Foundation Certificate Synoptic Answers to practice assessment 2 © Osborne Books Limited, 2016

Transcript of Foundation Certificate Synoptic - osbornebooks.co.uk · Task 1 (a) Documents Finance function (b)...

Osborne Books Tutor Zone

FoundationCertificateSynoptic Answers to practice assessment 2

© Osborne Books Limited, 2016

Task 1(a)

Documents Finance function

(b) (a), (c) and (e)

(c) £99.30Workings: £147.60 – £48.30 = £99.30

(d)Amount £ Debit Credit100.70 4

Workings: £200.00 – £99.30 = £100.70

2 f o u n d a t i o n c e r t i f i c a t e s y n o p t i c t u t o r z o n e

Invoice to a customer

Credit note received from asupplier

Signed contract of employment

Purchase order from a customer

Notification of bank charges

Reimbursement of train ticket tomeeting

Purchase ledger

Sales Ledger

Human resources

Cashier

Payroll

Petty cashier

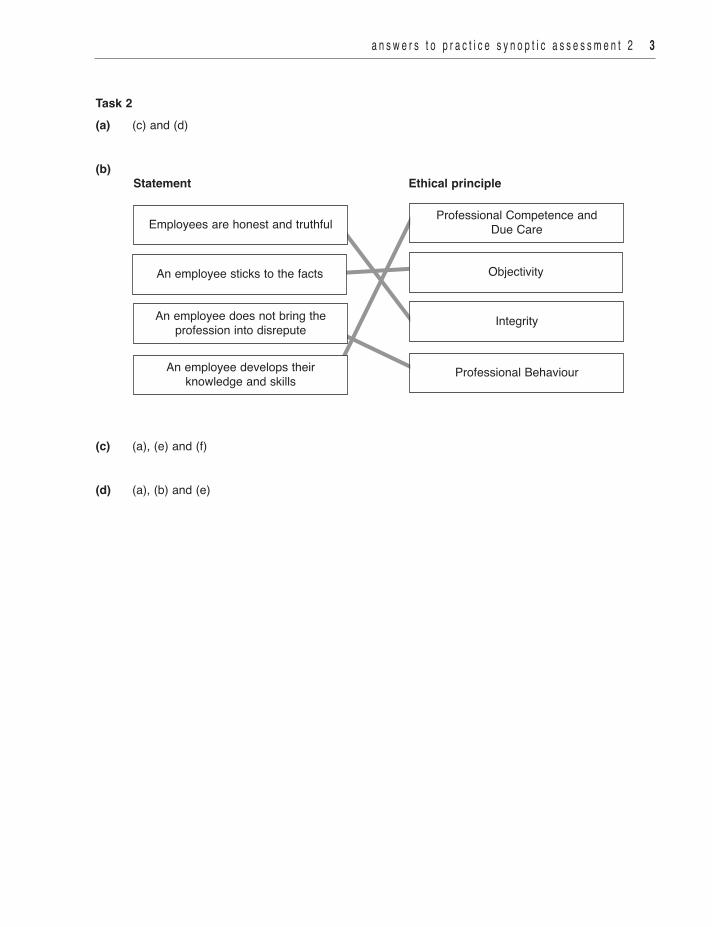

Task 2(a) (c) and (d)

(b)Statement Ethical principle

(c) (a), (e) and (f)

(d) (a), (b) and (e)

a n s w e r s t o p r a c t i c e s y n o p t i c a s s e s s m e n t 2 3

Employees are honest and truthful

An employee sticks to the facts

An employee does not bring theprofession into disrepute

An employee develops their knowledge and skills

Professional Competence and Due Care

Objectivity

Integrity

Professional Behaviour

Task 3(a)

Account name Amount £ Debit Credit Discount allowed 560 4 VAT 112 4 Sales ledger control 672 4

(b)Account name Amount £ Debit Credit Newtown Ltd 90 4

(c)Invoice/credit note number Amount £Invoice 4167 2089Invoice 4204 147Credit note SC501 303

(d)Amount Date to be paid by£811.44 1 August

Workings: £690.00 x 0.02 = £13.80£690.00 – £13.80 = £676.20£676.20 x 0.20 = £135.24£676.20 + £135.24 = £811.44

4 f o u n d a t i o n c e r t i f i c a t e s y n o p t i c t u t o r z o n e

a n s w e r s t o p r a c t i c e s y n o p t i c a s s e s s m e n t 2 5

Task 4(a)

Account name Amount £ Debit Credit VAT 544 4Sales 2,800 4Sales ledger control 3,540 4Purchases 80 4 Purchase ledger control 480 4

(b) Journal

Account name Amount £ Debit Credit Irrecoverable debts 12,875 4 VAT 2,575 4 Sales ledger control 15,450 4

Workings: £9,400 + £6,410 + £325 – £587 – £98 = £15,450

(c) Journal

Account name Amount £ Debit Credit Waverley Ltd 15,450 4

(d) Correct version (with errors in bold).

Hi Mrs SharpeOur sales ledger shows an outstanding balance on your account of £5,479. This has beenoutstanding for 60 days which has exceeded our 30 day payment terms.Please can you arrange payment as soon as possible and if you have any questions orqueries please do not hesitate to contact me.Kind regards

Tara

Sticky Note

See word file

6 f o u n d a t i o n c e r t i f i c a t e s y n o p t i c t u t o r z o n e

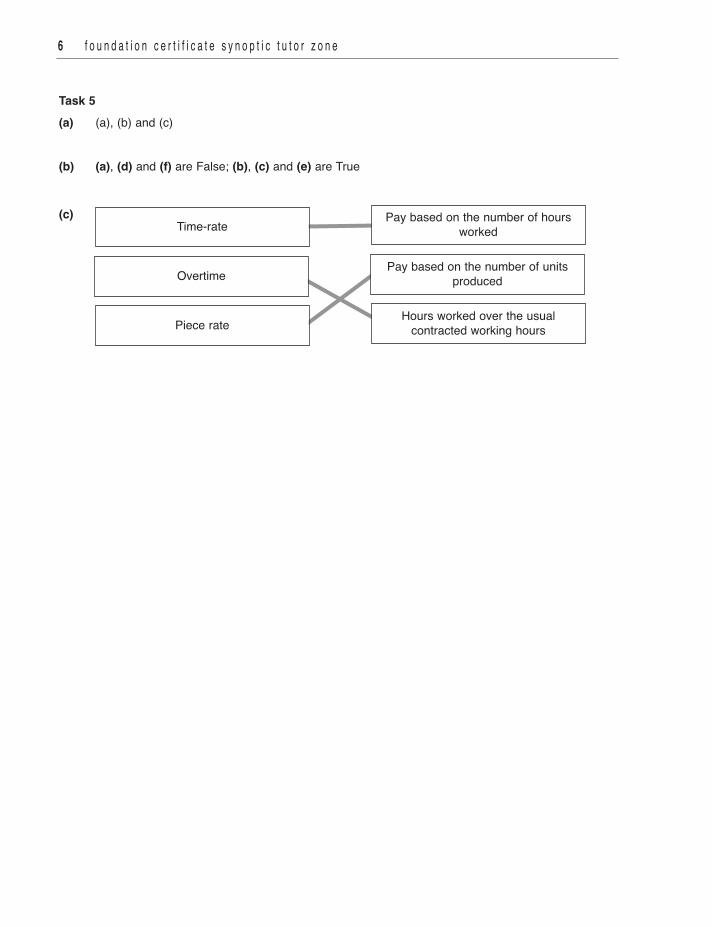

Time-rate

Overtime

Piece rate

Pay based on the number of hoursworked

Pay based on the number of unitsproduced

Hours worked over the usualcontracted working hours

Task 5(a) (a), (b) and (c)

(b) (a), (d) and (f) are False; (b), (c) and (e) are True

(c)

a n s w e r s t o p r a c t i c e s y n o p t i c a s s e s s m e n t 2 7

Task 6 (a)

Account name Amount £ Debit Credit Capital 20,000 4Bank (Overdrawn balance) 5,246 4Bank loan 21,200 4Sales ledger control 62,369 4

Vehicles 35,012 4

(b)Account name Amount £ Debit Credit

Entry from the sales day book 23,580 4

Entry from the sales returns day book 2,520 4

(c) Amount Debit Credit4,920 4

Workings: £4,100 x 1.20 = £4,920

(d) Amount Debit Credit46,319 4

Workings: £54,415 + £23,580 -£24,236 – £2,520 – £4,920 = £46,319

(e) £33,047

Workings: £23,245 + £9,407 – £240 + £635 = £33,047

(f) £853

Tara

Sticky Note

Delete the vehicles row

Tara

Sticky Note

Please delete part d)

8 f o u n d a t i o n c e r t i f i c a t e s y n o p t i c t u t o r z o n e

(g) This report is highlighting reasons as to discrepancies between the closing balance on thepurchase ledger control account (PLCA) and the closing balance of all the purchase ledger (PL)accounts.Reasons why the purchase ledger control account could be higher than the balance of thepurchase ledger accounts include: purchase invoices could have been understated in thepurchase ledger or entered twice or overstated in the PLCA. Purchase returns could have beenomitted or understated in the PLCA or entered twice or overstated in PL. Reasons why the purchase ledger control account could be lower than the balance of the purchaseledger accounts include: purchase invoices could have been omitted in the PLCA or entered twiceor overstated in the purchase ledger. Purchase returns could have been omitted or understated inthe purchase ledger or entered twice or overstated in PLCA. It is beneficial to complete control account reconciliations because it identifies any errors and canreduce fraud.

Task 7(a) (c) will NOT cause an imbalance; the remaining errors will cause an imbalance.

(b)Transactions: Type of error:

A cash payment to a supplier has notbeen entered into the accounts

A payment by cheque for advertisinghas been debited in the cash book andcredited to the advertising account

Wages account is overcast by £100and sales account is overcast by £100

The cost of stationery has beendebited to office furniture

An invoice to customer T James hasbeen debited to the account of L

James

Error of omission

Error of principle

Error of commission

Reversal of entries

Compensating error

Tara

Sticky Note

See word file for additional marking guidance.

(c) Potter Ltd

Date 20-X Details Amount £ Date 20-X Details Amount £

1 Sep Balance b/f 254.36 15 Sep Credit note 65 690.60

10 Sep Invoice 2410 1,980.70 20 Sep Bank 640.00

30 Sep Balance c/d 904.46

2,235.06 2,235.06

1 Oct Balance b/d 904.46

Askham Ltd

Date 20-X Details Amount £ Date 20-X Details Amount £

1 Sep Balance b/f 6,047.20 19 Sep Credit note 78 1,749.96

15 Sep Invoice 45892 7,740.36 29 Sep Bank 6,047.20

30 Sep Balance c/d 5,990.40

13,787.56 13,787.56

1 Oct Balance b/d 5,990.40

a n s w e r s t o p r a c t i c e s y n o p t i c a s s e s s m e n t 2 9