Fostering Investment in Infrastructure - · PDF fileFostering Investment in Infrastructure...

60

Fostering Investment in Infrastructure Lessons learned from OECD Investment Policy Reviews JANUARY 2015

-

Upload

phungtuyen -

Category

Documents

-

view

226 -

download

3

Transcript of Fostering Investment in Infrastructure - · PDF fileFostering Investment in Infrastructure...

Fostering Investment in Infrastructure

Lessons learned from

OECD Investment Policy Reviews

JANUARY 2015

You can copy, download or print OECD content for your own use, and you can include excerpts from OECD publications, databases and

multimedia products in your own documents, presentations, blogs, websites and teaching materials, provided that suitable acknowledgment of the

source and copyright owner is given. All requests for public or commercial use and translation rights should be submitted to [email protected].

Requests for permission to photocopy portions of this material for public or commercial use shall be addressed directly to the Copyright Clearance

Center (CCC) at [email protected] or the Centre français d’exploitation du droit de copie (CFC) at [email protected].

OECD Investment Policy Reviews (IPRs) present an analysis of investment trends and policies in the countries reviewed. The reviews are based on the Policy Framework for Investment which raises issues for policy makers in ten policy areas which are widely recognised, including in the Monterrey Consensus, as underpinning a healthy environment for all investors, from small- and medium-sized firms to multinational enterprises. One of these key areas is infrastructure.

This paper draws on 22 reviews undertaken in developing and emerging economies. It identifies actionable policy options to enhance the enabling environment for infrastructure investment, for the consideration of both host-country governments and their international partners.

In 2014 this paper was contributed to the G20 Development Working Group (DWG). As a result, it is being used by the DWG as the starting point for initiating work on policy indicators on the enabling environment for infrastructure investment.

This report has been prepared by the OECD with contributions from, among others:

a network of high-level infrastructure practitioners gathered by the OECD and the African Development Bank (including institutional investors, infrastructure utilities, fund managers, regulators, Multilateral Development Banks and Development Finance Institutions);

Southern African Development Community (SADC); and

Asia-Pacific Economic Cooperation (APEC).

The opinions expressed and arguments employed within this report are those of the authors and are published to stimulate discussion on a broad range of issues on which the OECD works. Comments on the report are welcomed, and may be sent to Karim Dahou or Carole Biau of the OECD Investment Division [ [email protected] | [email protected] ].

More information about our work on infrastructure investment is available online at http://oe.cd/QF.

Fostering Investment in Infrastructure © OECD 2015 3

TABLE OF CONTENTS

EXECUTIVE SUMMARY: OVERVIEW OF KEY FINDINGS ................................................................... 5

INTRODUCTION ........................................................................................................................................... 9

1. THE INVESTMENT REGIME UNDERPINNING INFRASTRUCTURE INVESTMENT ............... 11

1.1 National infrastructure planning ................................................................................................ 11 1.2 Access to land and protection against expropriation ................................................................. 12 1.3 Contract renegotiation ............................................................................................................... 13 1.4 Settlement of infrastructure investment disputes ....................................................................... 15 1.5 Legal and regulatory coherence, including at regional level ..................................................... 15 1.6 Key policy takeaways ................................................................................................................ 16

2. ENSURING SUCCESSFUL AND LONG-LIVED PROJECTS: MITIGATING PROJECT RISKS

AND OBTAINING VALUE-FOR-MONEY ........................................................................................ 19

2.1. Upstream contract preparation: national investment plans and feasibility studies .................... 19 2.2 Risk allocation ........................................................................................................................... 20 2.3. Financing infrastructure programmes ........................................................................................ 22 2.4. Project monitoring ..................................................................................................................... 23 2.5. Key policy takeaways ................................................................................................................ 24

3. INSTITUTIONAL ENVIRONMENT FOR SOUND PRIVATE PARTICIPATION IN

INFRASTRUCTURE MARKETS ........................................................................................................ 25

3.1. Role of PPP Units, procurement entities, and privatisation authorities ..................................... 25 3.2 Peer-learning and training for managing private participation in infrastructure projects .......... 26 3.3. Key policy takeaways ................................................................................................................ 27

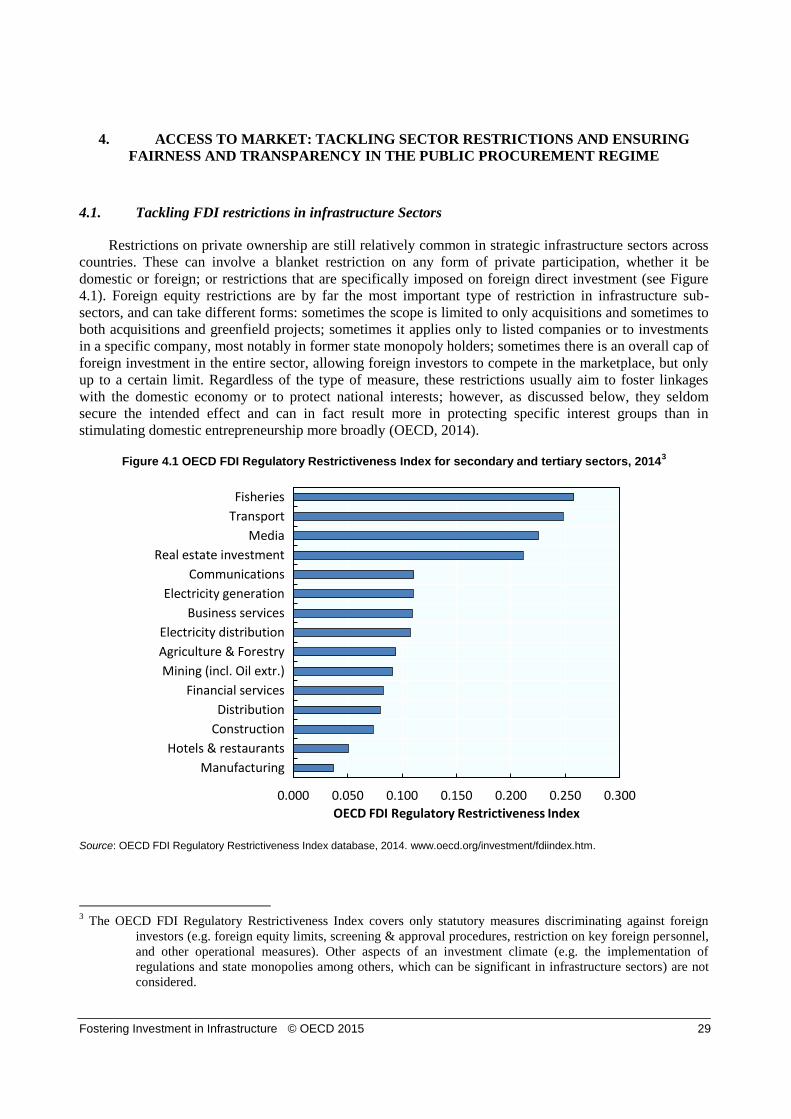

4. ACCESS TO MARKET: TACKLING SECTOR RESTRICTIONS AND ENSURING FAIRNESS

AND TRANSPARENCY IN THE PUBLIC PROCUREMENT REGIME .......................................... 29

4.1. Tackling FDI restrictions in infrastructure sectors .................................................................... 29 4.2. Transparency and predictability of the procurement regime ..................................................... 30 4.3. SOE governance and competition in infrastructure markets ..................................................... 31 4.4. Key policy takeaways ................................................................................................................ 33

5. PRIVATISATION, RESTRUCTURATION, AND STRUCTURAL SEPARATION OF

INFRASTRUCTURE NETWORKS ..................................................................................................... 35

5.1 Privatisation and restructuration experiences ............................................................................ 35 5.2 Experiences in structural separation .......................................................................................... 36 5.3 Key policy takeaways ................................................................................................................ 37

6. REGULATION AND PRICE-SETTING IN INFRASTRUCTURE MARKETS ................................. 40

6.1. Price-setting for infrastructure markets ..................................................................................... 40 6.2. Infrastructure sector regulators .................................................................................................. 41 6.3 Key policy takeaways ................................................................................................................ 43

7. INVESTING IN LOW-CARBON INFRASTRUCTURE ..................................................................... 49

7.1. Regulatory reform in the energy sector ..................................................................................... 49 7.2 Key policy takeaways ................................................................................................................ 51

ANNEX A: OECD GUIDANCE .................................................................................................................. 53

REFERENCES .............................................................................................................................................. 55

Fostering Investment in Infrastructure © OECD 2015 5

EXECUTIVE SUMMARY

Infrastructure investment needs to be substantially increased in most developing and emerging

economies to meet social needs and support more rapid economic growth. According to the OECD, total

global infrastructure investment requirements by 2030 for transport, electricity generation, transmission

and distribution, water and telecommunications will come to USD 71tn. This figure represents about 3.5%

of the annual World GDP from 2007 to 2030. There is a widespread recognition that governments cannot

afford to bridge these growing infrastructure gaps through tax revenues and aid alone, and that greater

private investment in infrastructure is needed. Private sector participation in infrastructure can help reduce

pressure on public finances and increase the portfolio of projects in the public sector investment

programme. Governments can also benefit from private sector skills and reap cost and efficiency gains by

delegating the construction and oftentimes the management of infrastructure projects to private investors.

From an economic growth perspective, infrastructure is not only an enabling factor for development and

for facilitating private investments and competitiveness across all sectors of national and regional

economies, but can also be an attractive investment opportunity in itself.

Although infrastructure investment opportunities are plentiful across developing countries,

investors are not fully seizing them – often due to gaps in the enabling environment for such

investment. The infrastructure sector presents specific risks to private investors, and since private

participation in infrastructure delivery is a relatively recent form of procurement in many countries,

governments do not necessarily have the experience and capacity needed to effectively manage these risks.

Beyond case-by-case project preparation and financing, concrete, implementation-oriented guidance that

can help governments identify and manage reforms is needed to make the broader infrastructure

investment environment more open to private participation. Well-targeted policy reforms can increase the

quality and quantity of private investment in infrastructure, a significant complement to public investment.

Country-specific experiences reported in OECD Investment Policy Reviews provide examples of

good practice in a number of policy areas, as well as risks to be avoided. Country cases help shed light

on the complex links among regulatory and institutional frameworks that make private investment in

infrastructure possible. Securing necessary resources and making infrastructure networks more attractive

for private involvement is possible by improving the efficiency of service delivery, facilitating investor

access to land, and establishing a more level playing field between State-owned infrastructure operators

and private investors. In addition improving procurement processes can help ensure that projects are long-

lived and secure the expected performance gains. Countries are also reforming their regulatory regimes in

order to strike a balance between cost-recovery needs of public and private investors on the one hand, and

end-user affordability on the other. More generally, developing national infrastructure plans, improving

core standards of investor protection, establishing a clear and well-implemented land policy, and refining

mechanisms for dispute resolution and contract renegotiation, are means through which governments can

bolster investor confidence, mitigate project risks, and secure responsible investment.

Lessons learned from country experiences for enhancing private participation and end-user

affordability in infrastructure sectors

Country experiences provide a variety of options for ensuring that infrastructure projects are

competitive, result in value-for-money for governments, and are ultimately acceptable and affordable for

end-users. A few of these policy options are highlighted below, and expanded in further detail at the end of

each chapter of this paper.

6 Fostering Investment in Infrastructure © OECD 2015

Increasing private participation in infrastructure investment requires an investment regime that

provides clarity and predictability for investors, in particular protection against expropriation

and provisions for dispute resolution and contract negotiation. A supportive institutional

environment is also needed. PPP units, procurement entities, and privatisation authorities need to

be provided with adequate numbers of well trained staff, and have well defined responsibilities

and co-ordination mechanisms, including for managing cross-border projects.

Careful project preparation is essential to ensure efficient public sector investment in

infrastructure. Project appraisal should include cost-benefit analysis and environmental impact

assessment; it should also analyse the suitability of projects for private sector participation,

making use of the public sector comparator approach combined with a careful analysis of value-

for-money and of the risks to be borne by the public and private sector partners. Project proposals

which survive initial screening should be included in medium-term public investment

programmes, and be coherent with long term strategic visions at national and sector level.

Sources of project finance should be as varied as possible, and include innovative sources such

as national and municipal bonds. Special purpose funds for infrastructure maintenance and for

addressing social objectives such as universal service provision, or SME development, can also

be critical to a successful infrastructure development programme.

Improving the public procurement regime is of particular importance for increasing value for

money in the use of public funds for infrastructure investment. This entails, inter alia, increasing

transparency in the bidding process (including through E-Procurement). Increasing the number of

bidders is important for reducing the costs of infrastructure projects. Reducing any remaining

restrictions on foreign direct investment in infrastructure – or at minimum assessing the rationale

for and impact of such restrictions on a regular basis – would notably help to increase the number

of bidders.

Improving SOE governance is of crucial importance for meeting infrastructure investment

goals. SOEs in many countries have shown improved performance when they have adopted

reforms that include: converting them into corporatised enterprises; separating the ownership and

management functions in their governing bodies; subjecting them to the authority of auditing

bodies and competition authorities; and ensuring that they follow the same financial accounting

and other corporate governance standards as private enterprises.

Unbundling vertically integrated supply chains in network infrastructure sectors (ICT,

transport, energy, and water and sanitation) can remove public monopolies and create more space

for enterprises to compete. Countries have also often reduced or eliminated restrictions on foreign

direct investment. The remaining restrictions can usefully be detailed in so-called “negative

lists”, together with explanations justifying their continuation and plans to gradually reduce them.

Changes in regulatory regimes may be necessary to safeguard user affordability alongside cost

recovery for private participants. In an increasing number of countries independent regulators are

being established to reduce the advantages of incumbent enterprises and to set tariffs for

infrastructure services; competition authorities can also be strengthened and mechanisms for co-

ordination with sector regulators established.

Reforming pricing structures in infrastructure networks remains necessary in many

countries, so as to move these sectors closer to cost-recovery levels. Where this has been possible

and politically acceptable (such as in several transport sub-sectors, or the ICT sector and in

particular mobile telephony), private sector participation has often substantially increased. Fewer

Fostering Investment in Infrastructure © OECD 2015 7

countries have managed to reform pricing in the electricity and water sectors. Often stepped

tariffs or cross-subsidisation are used as an alternative, to move to cost-recovery levels for

business and higher income households while continuing to subsidise low income families.

Identifying and analysing these different responses to common policy challenges can be useful not

only for developing country governments, but also for the donor community. This can support efforts to

better co-ordinate and align development partner support for infrastructure development, in view of greater

competitiveness and social wellbeing in developing countries.

Fostering Investment in Infrastructure © OECD 2015 9

INTRODUCTION

Infrastructure networks are likely to have a strong impact on the investment attractiveness of host

countries, most evidently as key variables within the production function of firms operating in the country.

The extensiveness of the road network, together with the efficacy of the port system and length of

container wait times for instance have clear implications for the timely and cost-effective delivery of goods

– each day in transit is estimated to cost between 0.6 and 2% of the value of traded goods (Hummels and

Schaur, 2012). Likewise, access to water infrastructure has a significant impact on the capacity for

agricultural production and innovation, in addition to substantial health impacts on the domestic

population. As regards electricity in Nigeria, for instance, it is estimated that private generators (used to

compensate for an unreliable grid electricity system) add about 40% to the cost of goods and services

produced and that adequate power supplies could boost annual GDP growth by 3-4 percentage points

(OBG, 2012).

In addition to being a key enabler of investment, infrastructure can also be a significant and lucrative

recipient of investment inflows. Private investment in infrastructure networks, alongside or in place of

state-owned operators, has been on the rise worldwide for several decades. However, since the global

financial crisis, this momentum has faltered somewhat: in 2010-2012 an average of only 8% of FDI

inflows received by OECD countries ended up in infrastructure sectors, as opposed to more than 10% in

2007-2009 (OECD, 2013a). The same applies to developing countries: apart from exceptional investments

in energy in Morocco and South Africa, Africa has seen a regular decline in private capital for

infrastructure projects, year after year, from 2008 to 2012 (ICA, 2013). The attractiveness of infrastructure

as an investment recipient varies significantly among countries: within the OECD in 2012 for instance, the

share of infrastructure in total inward FDI stocks for individual countries ranged from less than 1% in

Israel to 20% in Spain and 28% in Turkey (OECD, 2013a).

Addressing infrastructure constraints is a priority for the majority of developing country governments.

Worldwide, consensus is growing that mobilising private investors to finance and participate in national

infrastructure maintenance and development can ease the pressure on public funds and supplement

resources for investment. Globally governments have found it more difficult to raise financing for

infrastructure in the wake of the 2008-09 crisis and the 2011 downturn. Private sector participation in

infrastructure is thus often sought to broaden the resources available for financing the portfolio of projects

in the national infrastructural development programme.

By delegating the construction and oftentimes the management of infrastructure projects to private

investors, governments are also likely to reap cost and efficiency gains. Evidence collected from the

performance of more than 1 200 water and energy utilities in 71 developing and transition economies

between 1990 and 2002 indicates that greater degrees of private participation are associated with stronger

gains in productivity and service quality. These gains include a 12% increase in the average number of

residential water connections, a 32% rise in electricity sold per worker, a 19% increase in the residential

coverage of sanitation services, a 45% improvement in the electricity bill-collection rate, an 11% drop in

electricity distribution losses, and a 41% increase in hours of daily water service (World Bank PPIAF,

2009).

Indeed besides financing issues, infrastructure development in many developing countries has

traditionally been confronted with a problem of investment effectiveness, including poor management and

underperforming service provision. Inefficiently-run SOEs, in particular, can adversely affect the quality of

network management and subsequently deter private investment. Inefficiencies such as overemployment,

poor bill collection, system losses, and irregular maintenance practices by SOEs in infrastructure markets

cost about USD 12 billion annually in Africa – detracting public resources from amelioration of

10 Fostering Investment in Infrastructure © OECD 2015

infrastructure networks (Trebilcock et al, 2011). Conversely and in somewhat of a virtuous circle, if

efficiency and cost gains are obtained via private participation in infrastructure, these can contribute

towards reducing the amount of subsidies required to support infrastructure service provision when full

cost recovery pricing cannot be achieved.

Augmenting private sector participation in infrastructure requires addressing not only constraints on

the financing of infrastructure – the “push” factors – but also country specific issues – the “pull” factors –

including host countries’ investment climates. Numerous work streams have been initiated by the OECD

Investment Committee to partner with developing countries in improving the enabling environment for

infrastructure investment. For example, the infrastructure chapters of Investment Policy Reviews draw on

the Policy Framework for Investment (PFI) to analyse infrastructure investment policy, highlight funding

gaps, and identify reforms that governments can take to increase the quality and quantity of both private

and public investment in different infrastructure sub-sectors. 22 such Reviews have been conducted to

date. These country-specific experiences have shed light on the complex and significant links among the

regulatory and institutional frameworks that impact private participation in infrastructure networks,

including in green infrastructure. These include frameworks for: investor protection; contract design and

renegotiation; infrastructure procurement and public-private partnerships (PPPs); regulation and pricing of

infrastructure markets; competition policy; and corporate governance of state-owned enterprises, which

often dominate infrastructure markets in both developed and developing regions.

Drawing on the policy experience accumulated through the application of the PFI across developing

and emerging economies, this paper highlights transversal policy bottlenecks and priority areas of action

necessary for stimulating further private investment in infrastructure. The policy areas considered include:

the investment regime underpinning infrastructure investment; mitigating project risks and obtaining value-

for-money; the institutional environment for sound private participation in infrastructure markets; market

structure considerations, including the regime for SOE governance and competition in infrastructure

markets; fairness and transparency in the public procurement regime; and price-setting and regulation in

infrastructure markets. Key policy takeaways for consideration by governments are proposed at the end of

each section.

The OECD launched an update of the PFI in 2013. The country experiences in this paper will

contribute to strengthening the policy relevance of the PFI’s infrastructure chapter.

Fostering Investment in Infrastructure © OECD 2015 11

1. THE INVESTMENT REGIME UNDERPINNING INFRASTRUCTURE INVESTMENT

The infrastructure sector presents specific risks to private investors. Not only do projects tend to be

large-scale, capital intensive and with long development timelines, but it can also be difficult for the

private party to transfer asset ownership. To a greater extent than in other sectors of the economy, investors

in infrastructure are also particularly vulnerable to changes in government regulations (such as a

modification in infrastructure tariffs) that can undermine their profitability. In addition as infrastructure

development is a critical means of supporting economic growth and catering to essential social needs,

government decisions on how much, where and what kind of infrastructure to build are politically charged.

As a result governments have traditionally built, owned and managed infrastructure capital themselves.

For all these reasons, making the transition towards more private participation in national

infrastructure provision carries a number of risks. Moreover, since certain forms of private participation

(such as public-private partnerships or PPPs) are relatively recent in many countries, governments do not

necessarily have the experience and capacity needed to effectively manage the risks entailed. Over the past

two decades, 37% of PPP projects have thus been conducted in “lower middle income” countries, and 4%

only in “low income” developing countries (Trebilcock et al, 2011). Yet public sector capacity for project

design and implementation is indispensable in order to obtain value-for-money from infrastructure projects

and to avoid unbalanced risk-sharing arrangements which can result in fiscally unsustainable contracts and

costly contract renegotiations.

In such a delicate context, investors considering a country’s infrastructure investment opportunities

are especially attentive to what in economic terms (in the words of Paul Collier) comes down to

government “commitment technologies” – essentially all measures, be they economy-wide, sector-specific

or even contract-specific, that make it more difficult for governments to renege ex-post on the

commitments made within an infrastructure project.

1.1 National infrastructure planning

Government procedures to decide how much to spend on public infrastructure and how to allocate

spending, as expressed in medium-term development plans or strategies at the national or sector level, are

one such “commitment technology”. These plans are likely to receive careful scrutiny from any domestic

or international investor considering investment in the country’s infrastructure networks. Investors will pay

particular attention to government intentions to promote private participation, be it in specific utility

markets (for instance, plans to increase the number of independent power providers connected to the

national electricity grid or to embrace more forms of renewable energy) or through a particular contract

structure (as embodied in a PPP Policy for instance). Political commitment is critical for assuring private

investors that their investments in national infrastructure will be promoted, and that institutional and

regulatory obstacles will be mitigated by government.

Public discussion of national infrastructure plans and other strategy documents is especially important

when a shift towards enhanced private participation is undertaken, as this can help modify embedded ways

of thinking among government officials and the general public. Indeed investors expect the consistency of

the regulatory framework to transcend any given government. In Mauritius, which is a model in this

regard, since 2005 the National Development Strategy provides a framework for all public sector

investment programmes – including for transport, water and energy utilities; and the Mauritian

“Government Programme 2012-2015 for Moving the Nation Forward” sets the objective of ensuring that at

least 10% of the financing for major public infrastructure over 2012-2015 should come from Foreign

Direct Investment flows.

12 Fostering Investment in Infrastructure © OECD 2015

By contrast in many countries there is a confusing multiplicity of such plans or strategies, which are

seldom accompanied by a formal public sector investment programme or by a strategic approach to attract

private investment to key sectors. In Colombia for instance, although the project cycle begins coherently

with the elaboration of a national development programme (NDP) that determines multi-year investment

plans, significant deficiencies include: the absence within the NDP of clearly set priorities as regards PPP

projects; key differences between the proposal of projects by the government and the approval by Congress

of NDPs (with some concessions being dropped and others appearing without adequate ex-ante

evaluation); and lack of coherence between decentralisation policies and national planning policies as

regards infrastructure. These shortcomings in turn affect the execution of policies, and may be partly

responsible for the high levels of renegotiation of PPP contracts in Colombia relative to other Latin

American economies (OECD, 2013h).

National infrastructure plans can also be an opportunity to make space for innovative forms of

infrastructure expansion – for instance through shared use of infrastructure networks. Indeed especially in

the extractive industries, large-scale projects undertaken in areas that are poorly serviced by existing

infrastructure networks often require heavy private infrastructure investments, which have considerable

spare capacity. As a result, in several African countries such as Mozambique and Tanzania, the

exploitation of natural resources has coincided with a burst of accompanying infrastructure investment. It

is becoming increasingly urgent for governments to carefully monitor the development of such ancillary

infrastructure: these projects should not be undertaken by individual companies in isolation, but rather

within a coherent national framework, which would build on joint economies of scale, tackle coverage

gaps in the national network, and address the needs of the domestic population. Protocols could also

usefully be established for these mining companies to open their infrastructure to wider use. Governments

could also more proactively encourage shared use of infrastructure networks even outside of the extractive

sector. For instance internet and telecom operators can ‘piggy-back’ on fibre optic cables pre-installed by

rail, road and electricity companies – an advantage that Tunisia is beginning to exploit in the rail sector.

The formulation of reliable national infrastructure plans, or more specifically PPP or privatisation

policies, is also especially necessary to reassure investors in contexts where initially divested enterprises

have been subsequently re-possessed. Indeed in several countries the strength of the political commitment

to private participation in infrastructure has sometimes been ambiguous. In such cases, countries have at

times cancelled contracts and retaken possession of facilities (Tanzania, Zambia). In Tanzania, although

five major utilities (in electricity, harbours, water, ICT and air travel) involved some private participation

by 2003, most of these companies were re-possessed by Government in 2010-2011 for pricing

considerations.

Whether politically or socially motivated, such changes in government positions (within a single

administration but also across election periods and beyond party lines) send conflicting and deterrent

messages to private investors potentially interested in infrastructure investment. Such evolutions confirm

that to back national plans and policies, it is paramount that laws, regulations and agreements governing

infrastructure sectors are clearly defined and transparent, as well as adequately enforced. These elements

are addressed in the following section.

1.2 Access to land and protection against expropriation

Land acquisition is often a major obstacle in infrastructure projects and countries have initiated

reforms accordingly. A peculiarity of Indonesian PPP regulations in the past was that projects could be

tendered before the necessary land had been acquired, leading to costly delays as landowners held out for

higher prices. Following incremental improvements to land procurement regulations, a 2010 regulation

ensures that land is procured before the tender process commences. In 2012, a new law on Land Provision

Fostering Investment in Infrastructure © OECD 2015 13

for the Public Interest was also enacted, which facilitates the adoption of a court-led land consignment

scheme and reduces by half the time spent negotiating such schemes.

In Myanmar land leasing, from either a public or private owner, remains subject to prior approval by

the Myanmar Investment Commission (MIC). When foreign investors lease land directly from the

government, it is most often done through a Build-Operate-Transfer agreement, which also requires MIC

approval. Most frequently, foreign investors use land through joint ventures with Myanmar nationals who

have already leased land from the state. Beginning in 2013, the MIC can also issue permits for sub-leases

of land, provided that the land is used for the same investment project as initially planned (OECD, 2014d).

However, the difficulties in the achieving the full completion of special economic zones illustrate the

challenges in improving land policy and its implementation.

In Zambia strides have been taken to improve access to land for investment purposes, involving close

collaboration with traditional local rulers. Improvements in the systems of processing land acquisition

applications and registration of titles are being implemented, including through the decentralisation of the

Lands Department (OECD, 2012d). Like in Mozambique however, the award and administration of land

use rights at the local government level remains a challenge.

The question of access to land is intimately tied to that of protection of property rights – and by

extension, expropriation procedures. In the interest of attracting more long-term investment, including in

infrastructure, domestic legal frameworks must contain a sound, clear and detailed provision that lays

down the obligation for compensation in the event of an expropriation and that clearly sets out the public

benefit purposes for which an expropriation can lawfully occur. In Indonesia, the 2012 law on Land

Provision for the Public Interest introduces safeguards for more transparent and fair expropriation

procedures, including in cases where the government exercises the right of eminent domain. The 2012

provisions: provide a clear definition of public interest; require public and stakeholder consultation from

the time when the location is initially designated; secure just and fair compensation through independent

appraisal; and establish a single institution responsible for land acquisition, together with a dedicated fund.

In many countries, the protection against expropriation is laid out not only within the national law, but

also within international investment agreements (IIAs) signed between the host and home countries. For

several decades, IIAs have been designed with a view to nurture investor-state relationships, to attract new

investors and reduce perceived risks that can deter investment. They therefore often provide an additional

layer of “commitment”, beyond domestic regulations pertaining to investment. However, in order for

governments to fully reinforce the credibility of these commitments vis-à-vis all kinds of investors, be they

foreign or domestic, they should address potential inconsistencies between levels of protection provided by

domestic laws and regulations and within IIAs. Otherwise, discrepancies regarding investment protection

can impede legal predictability and transparency for investors. Moreover and as IIAs mostly grant investor

protection on a bilateral basis, such disparity risks creating an uneven playing field between investors

based on whether or not their home countries have signed IIAs with the host country. This also raises the

importance of building domestic capacity for IIA negotiation in developing countries, and raising internal

awareness of the commitments to which these countries are agreeing.

1.3 Contract renegotiation

Given the long time-lines of infrastructure projects and the unpredictable nature and variability of

many of the risks involved (such as commercial or demand risk), it is highly likely that most infrastructure

contracts will have to be renegotiated at least once during their lifetime. Out of 1 000 Latin American

concession contracts awarded between the mid-1980s and 2000, 30% were renegotiated. This proportion

reaches 54.4% in transport contracts and 74.4% in water contracts. Interestingly, renegotiations often

favour the concessionaire: in Latin America, 62% of renegotiation cases studied led to tariff increases, 38%

14 Fostering Investment in Infrastructure © OECD 2015

to extensions of the concession term and 62% to reductions in investment obligations (Guasch, 2004). Such

high renegotiation rates point to the importance of adequately addressing the need for contract

renegotiation in long-term contractual arrangements – through flexible contracts and renegotiation

structures on the one hand, and appropriate mechanisms for dispute settlement in case of disagreement

between public and private parties on the other hand.

Most often and provided that the contract structure is flexible enough, these renegotiations take place

smoothly and do not lead to disputes between the investor and the state. When disputes do arise, they are in

majority settled privately or dealt with by the national courts. The legal framework for concessions and

PPPs currently under preparation in Tunisia provides an example of how a degree of contract flexibility

can help address demand and revenue risks so as to ensure that projects are resilient to changing economic

conditions. Both the forthcoming regulations for Tunisia’s PPP law (currently in draft form) and the

November 2013 decree relative to concessions require that project contracts contain clauses specifying in

which cases their terms can be revised (for instance in response to unforeseen changes in the needs of the

public party or in the financing conditions). Meanwhile in Peru, a single state agency, ProInversión,

handles all nationwide public infrastructure and utilities, as well as concession and public tender processes.

All concession agreements must include a clause on the projects’ economic balance, which means that if –

due to the legislative changes – the concessionaire’s profit decreases or its costs increase, economic

balance should be re-established. The private investor has a guarantee that if the State executes the

redemption clause, which allows it to terminate the concession unilaterally, the State shall pay to the

concessionaire the total invested amount and the loss of potential profit (OECD, 2008a).

The Peruvian case provides an interesting example of mitigating political risk and enabling more

flexible contract renegotiation. Nevertheless excessive flexibility on renegotiation can also be dangerous,

as it can encourage private bidders to deliberately underestimate costs in their offers so as to win the bid,

while expecting to break even through subsequent renegotiation. A 2009 econometric evaluation of PPP

renegotiations suggests that this is a common tendency. Out of 50 concessions awarded in Chile between

1993 and 2006, total investment increased by nearly one-third via renegotiation – from USD 8.4 billion to

USD 11.3 billion (Engel et al, 2009). This in part resulted from weaknesses in the regulatory framework

which: allowed for unlimited addition of complementary works under direct negotiation and agreement by

both parties; and established an excessively general clause allowing the concessionaire to request

compensations when adverse contingencies affected the contract, thus transferring too much commercial

risk back to the government (OECD, 2013g). Alongside and as experienced in several other countries,

renegotiation was in some cases used to increase spending while shifting the burden of payments to future

administrations. Thus the majority of renegotiation costs in Chile were not borne by the administration that

renegotiated (Engel et al, 2009). The OECD Principles for Public Governance of Public-Private

Partnerships seek to help avoid such fiscal mismanagement, by providing concrete guidance to policy

makers on how to ensure that PPPs represent value-for-money (VFM) for the public sector.

In view of such risks, Tunisia’s decrees relative to concessions and PPPs (forthcoming) also define in

which cases contract modifications are considered to be “substantial” and therefore require launching a

new bidding procedure (substantial modifications for instance include: the introduction of contract

conditions that would have enabled alternative bidders to be selected initially; a modification of the

contract’s economic balance in favour of either public or private party; or a change in the scope of the

contract which results in the coverage of services or works not originally included in the contract).

Likewise Chile improved the transparency of its concession framework in 2007, with new administrative

regulations requiring that any substantive construction work derived from contract renegotiation be

subjected to auction. In addition the new concessions law enacted in 2010 established more transparent

rules for renegotiation that levelled the field between concessionaires and other potential contractors of

complementary works (OECD, 2013g).

Fostering Investment in Infrastructure © OECD 2015 15

Such efforts can help strike a balance between contract resilience and excess flexibility in the

contractual terms, so as to ensure that VFM and competitiveness are retained as priorities throughout the

lifetime of the infrastructure project. Specifying limits to the financial amounts that can be renegotiated

within concessions laws is another frequent approach, although in several countries insufficient

enforcement and budgetary oversight has allowed these limits to be frequently exceeded. Indeed as Section

3.2 details further, even in the best of cases well-written contracts cannot overcome institutional

weaknesses (Trebilcock et al, 2013).

1.4 Settlement of infrastructure investment disputes

Alongside a balanced approach to contract renegotiation, a reliable structure for domestic arbitration

can help settle public-private disputes. In the Chilean case above, while 83% of the renegotiation volume

was settled bilaterally between the contracting parties, the rest resulted from decisions from arbitral panels.

However domestic arbitration is not always a sufficient or satisfactory recourse, and in some cases

infrastructure investment cases are taken to international arbitration fora. Whether a dispute can be taken to

international arbitration or not is dependent on the parties’ consent to arbitral jurisdiction, which is often

contained within an IIA (although consent to arbitration may also be included in an investment contract or

within domestic legislation). For these reasons, alongside addressing expropriation risks, domestic legal

frameworks can also include as another core standard of treatment the right to resolve through arbitration

any disputes that may arise in the course of project operation.

Overall prior to 2003 at least 28 cases relative to arbitrations and settlement agreements in

infrastructure projects (involving telecommunications, transportation, water and sanitation, and energy)

have been taken to the ICSID tribunal. Out of these, five disputes pertained to concession contracts, six to

construction contracts, and seven involved infrastructure privatisation agreements. In a significant number

of these cases the disputes have related to tariff adjustments, often triggered by public resistance to cost-

reflective pricing (see section 6.1 below). In construction contracts, disputes most frequently relate to

allegations of breach of contractual stipulations, or to the final payments due under the contract (OECD,

2006). More rarely the case may relate to repossessions of divested infrastructure services – Tanzania has

been involved in four such ICSID cases to date. Most recently the ongoing case between Standard

Chartered Bank (Hong Kong) Limited and the state-owned electricity utility TANESCO sheds light on

inconsistencies remaining between Tanzania’s national framework and its international commitments.1

These court and arbitration procedures are extremely lengthy and costly, including for the host

country concerned, and also send out negative signals to potential future investors. This highlights the

necessity of providing sufficiently protective domestic frameworks, consistent with host countries’

international commitments, so as to anticipate and manage potential investment disputes in infrastructure

projects without necessarily having to refer them to international arbitration.

1.5 Legal and regulatory coherence, including at regional level

More generally and beyond these core standards of investor protection, the clarity and predictability

of the infrastructure investment regime may require legal and regulatory harmonisation. Introducing a PPP

law is an option, not a requirement, for developing a PPP programme: Indonesia, Thailand, and Brazil have

1 ICSID proceedings between Standard Chartered Bank (Hong Kong) Limited (SCB HK) and the Tanzania Electric

Supply Company (TANESCO, the state-owned operator) were commenced in 2010. In the PPA Tanzania

consented to ICSID arbitration. On 12 February 2014 the Tribunal concluded that it had jurisdiction over

the dispute and ordered the parties in the light of its findings to renegotiate the disputed tariff. However on

23 April 2014, the Tanzanian High Court ordered both parties (TANESCO and SCB HK) to refrain from

“enforcing, complying with or operationalising” the Tribunal’s decision.

16 Fostering Investment in Infrastructure © OECD 2015

such laws, while for example Botswana, the UK, Australia, South Africa, and Mexico do not.

Nevertheless, dedicated PPP laws can help regulate more specific elements necessary to ensure the success

of PPP contracts, as long as they are made ‘user-friendly’ so as to avoid excessive complexity which can

otherwise deter public entities from adopting the PPP route. In countries newly seeking to attract investors

to PPP projects, the elaboration of a PPP Policy and PPP Law can also be a useful mechanism for guiding

procurement agencies, raising awareness, and reflecting the government’s policy stance with respect to

private participation in infrastructure (as an additional form of “commitment technology”).

Yet as PPPs are a nascent form of procurement in many countries, pre-existing legislation on

investment, procurement and concessions is not always entirely consistent with the new laws. The

definition of PPPs, relative to other forms of infrastructure procurement, can especially be subject to

confusion for both public and private actors. The conditions for undertaking a PPP may also be too

restrictive and give excessive preference to less innovative forms of procurement. For instance Article 14

of Tunisia’s draft PPP law sets the condition that PPPs are to be undertaken only under three conditions: if

the contract is too complex (financially or technically) for the public authority to shoulder it; under matters

of urgency; or in case of failure or underperformance of similar projects having espoused different

contractual forms in the past.

Regulations at sector level may likewise come into conflict with the new PPP or procurement regime.

Alongside, some institutional overlap may also occur regarding which authorities are responsible along the

different steps of the infrastructure project’s life cycle. Mauritius has for instance sought to overcome this

risk by establishing Memoranda of Understanding among the different agencies tasked with the oversight

of concession procedures and of infrastructure sectors: MoUs thus exist among the Competition

Commission, the Public Procurement Office, and various sector regulators.

Legal and regulatory harmonisation also has implications for projects undertaken at the regional level.

Countries can for instance make progress towards common criteria for bid selection and for evaluation of

value-for-money and PPP viability. Joint projects could also be facilitated via shared standards for

transparency of the procurement process, as well as shared rules on project cancelation and compensation.

To avoid ‘free-rider’ risks during project implementation, it is moreover crucial for the governments of all

countries involved to commit ex-ante to a sufficient allocation of budgetary resources, and to agree on

shared development priorities that should be upheld throughout the course of the project. Country

collaboration could be further supported by inter-country Memoranda of Agreement, as well as by

mechanisms for regular dialogue between the public parties involved.

1.6 Key policy takeaways

Changes in government positions on private sector participation in infrastructure (within a single

administration but also across election periods and beyond party lines) can severely shake

investor confidence. Where they take place, they should be clearly explained and delineated in

the interest of preserving future policy predictability. Moreover clear and holistic long-term

infrastructure and development plans (which firmly emphasise the role of private sector

participation) can help regain investor confidence.

Governments could take more proactive measures to encourage shared-use of infrastructure

networks, through protocols established with private companies and with existing rail, road and

electricity operators to open their infrastructure to wider use on appropriate terms. This will be

particularly important for countries experiencing a boom in extractive industry investments.

The legal framework for investment (including such as is established through international

agreements, IIAs) must contain a sound, clear and detailed provision that lays down the

Fostering Investment in Infrastructure © OECD 2015 17

obligation for compensation in the event of an expropriation. Other core standards of treatment

include a well-defined fair and equitable treatment provision, and a right to resolve through

arbitration any disputes that may arise in the course of the project operation. Parties to cross-

border projects should agree on a framework for dispute resolution and contract re-negotiation.

By clearly delineating investment protection principles, countries can also better protect

themselves from costly cases of international arbitration. Large discrepancies between what is

provided for in the domestic regime and the country’s international commitments should be

avoided in the interest of clarity and reliability for investors and host governments alike.

PPP laws can help manage the transition towards greater private participation in infrastructure.

PPP laws should usefully include: the definition and scope of a PPP (contractual attributes, size

and duration of PPP contracts); the principles by which PPP contracts will be structured,

procured, managed, and reported; the modalities by which projects risks will be allocated; and the

institutional structure and processes established for managing and overseeing PPPs.

To give optimal results, PPP legislations must also be consistent with pre-existing and broader-

spectrum legislations on investment. They should also be ‘user-friendly’ for procuring entities;

procurement manuals, tailored to country context, can provide valuable help in this regard.

Fostering Investment in Infrastructure © OECD 2015 19

2. ENSURING SUCCESSFUL AND LONG-LIVED PROJECTS: MITIGATING PROJECT

RISKS AND OBTAINING VALUE-FOR-MONEY

2.1. Upstream contract preparation: national investment plans and feasibility studies

Once national infrastructure development strategies are in place, the next stage is infrastructure

investment programming, whereby a preliminary list of priority projects is developed. Colombia and

Mauritius provide useful examples of how to embed infrastructure projects within broader public sector

investment plans. Colombia’s National Development Plan (NDP) includes a multi-year Investment Plan,

the main tool for determining the country’s investment needs in infrastructure. To monitor the NDP’s

objectives, a dedicated information system keeps track of the life cycle of the country’s public investment

projects, from their formulation to budget programming, execution and monitoring (OECD, 2012a).

Similarly, the Mauritius Public Sector Investment Programme (PSIP) serves as a basis for Performance

Based Budgeting (PBB) by government agencies, identifies possible areas for private domestic and

international investment, and highlights policy changes required for encouraging inflows into these areas

(OECD, 2014c). Beyond keeping track of public spending, well-organised infrastructure investment

programming ensures the coherence of long-term infrastructure development plans, and helps delineate the

respective roles of public procurement and private participation in this regard.

Before they are included in finalised public sector investment plan however, and regardless of the

degree of private investment, priority projects must be evaluated using such tools as cost-benefit analysis,

to ensure that the social, environmental and economic benefits justify the use of public funds, and that the

annual costs fit within the budgetary envelope. The evaluation process for each project begins with a pre-

feasibility study, followed by full appraisal for projects that survive an initial screening. The latter should

consider all relevant aspects of sustainable development, including the environmental and social

repercussions of large-scale infrastructure projects. In China, Environmental Impact Assessment (EIA) is a

requirement for all development projects under the EIA Law 2002. This law also provides for a strategic

environmental assessment to complement the project-oriented EIA process in regional and sector plans and

programmes (OECD, 2008c). Finally these evaluation procedures need to be complemented by financial

sustainability analysis.

Feasibility studies are particularly useful tools to determine the extent and desirability of public

participation in a given infrastructure project – that is, whether the project is amenable to private sector

involvement or whether it would be better suited to traditional infrastructure procurement (based on the

“design-bid-build” approach). The feasibility study should therefore include a complete risk analysis.

Indeed the greater the degree of private sector involvement, the larger the transfer of risks from the public

to the private actor (see Figure 2.1). As further detailed in the next section, this large spectrum of risks

(from design and construction risk, through demand risk, and to early termination risk2) must be

appropriately allocated among public and private parties. The OECD Principles for the Governance of

PPPs provide guidance on how governments can help secure value-for-money (VFM) when making these

infrastructure investment decisions, from the project prioritisation and pre-feasibility stages through to the

operational phase.

As noted by the Collaborative Africa Budget Reform Initiative (CABRI), infrastructure project

appraisal represents both a useful toolkit and a challenge for decision makers due to the profusion of

2 Key project risks include: design and construction risk; operation risk; demand risk; maintenance risk; residual

value risk; exchange rate risk; interest rate risk; contractor failure risk; renegotiation risk; early termination

risk; force majeure (civil disturbance/ war/ security); technology risk; expropriation risk; breach of contract

/ non-honouring of sovereign financial obligations.

20 Fostering Investment in Infrastructure © OECD 2015

information needed to conduct a rigorous approach (OECD/CABRI, 2014). Careful upstream project

preparation is indeed resource-intensive, and dedicated sources of finance can be a useful way of meeting

these costs. India, for example, has established the India Infrastructure Project Development Fund (IIPDF),

a revolving fund with an initial budgetary outlay of 1 billion rupees, replenished through fees earned from

successful bidders. The IIPDF ordinarily assists up to 75% of project development expenses in the form of

interest-free loans (OECD, 2009b).

Figure 2.1. Spectrum of private participation and risk transfer in infrastructure provision

Source: OECD Investment Division, adapted from: Straub, S. (2009). Governance in Water Supply. Thematic paper for the Global Development Network project.

Project preparation should also involve adequate consultations with end-users and other stakeholders

prior to the initiation of the project, preferably at the planning stage. Indeed private participation in

infrastructure is unlikely to be successful unless authorities have assured themselves beforehand that the

envisaged undertakings are in the public interest and are acceptable to consumers and other stakeholders.

Among the countries considered in this report, Colombia, Indonesia, Malaysia, Mozambique, Nigeria, and

Zambia have all made use of BOT modalities to encourage private sector investment in highways financed

by tolls. Not all of these projects have met expectations, in part due to weak communication ex-ante which

resulted in public resistance once the roads and their tolls became operational. Particularly where

newcomers are expected to address long-standing problems of inefficiency or mismanagement, or if the

transfer of infrastructure services to the private domain is linked with the introduction of user fees or

reduction of subsidies, public consultations can help establish a realistic expectation of what the private

sector can achieve.

2.2 Risk allocation

According to the OECD Principles for Private Participation in Infrastructure, infrastructure project

risks should be allocated to the party who can best control it or bear it at least cost. The private partner is

best suited to assume the commercial risk (linked to variations in demand and revenue from users), while

the public partner is better able to assume the legal, regulatory and political risks. The balance of risks

differs across infrastructure sectors. When a sector is politically sensitive, as the case with water and

sanitation for instance, the revenue risk (due to variability in user fees and government subsidies) and sub-

Fostering Investment in Infrastructure © OECD 2015 21

sovereign risks (due to management at local level where capacity may be weak) are greater. When the

quality of the existing infrastructure cannot be adequately assessed (e.g. water mains), the possible hidden

costs of maintenance and rehabilitation can represent significant contractual risks.

There are four broad types of PPP modalities: management contracts, lease contract, concessions, and

build-operate-transfer (BOT) schemes and its many variants. Figure 2.2, adapted from the website of

Nigeria’s Infrastructure Concessions Regulatory Commission, illustrates how these different forms of

project delivery vary in terms of asset ownership, risk transfer, contract duration, and the share of

responsibilities among public and private parties. The Government of India likewise provides a good

explanation of these modalities in its on-line toolkit for solid waste management. As these different project

types consist in various risk-sharing arrangements that all have their own costs and benefits, it is crucial to

ensure that the choice among them will arrive at the most cost-effective option of infrastructure provision

that provides the most value for money for end-users.

Figure 2.2. Forms of PPP Delivery: differences in asset ownership, risks, and contract duration

Source: OECD Investment Division, adapted from: Nigeria Public-Private Partnerships Manual, “Overview of PPP Delivery Models”. Nigeria Infrastructure Concessions Regulatory Commission (ICRC, 2012).

This choice on the extent of private participation in infrastructure can be facilitated by transparent

public procurement and PPP frameworks, and should be based on assessing the comparative advantage of

each potential actor in providing the service. This can include calculating a Public Sector Comparator

(PSC), which estimates the hypothetical risk-adjusted cost of a project if it were to be wholly financed,

owned and implemented by government and any relevant SOE. ProInversión has also developed risk

matrices to identify, assign and mitigate possible risks related to concession agreements based on the

principle that risk should be assumed by the party that can manage it better (OECD, 2008a). The public

sector’s participation in infrastructure project finance should also be fully reflected in the government

budget.

22 Fostering Investment in Infrastructure © OECD 2015

In most countries, bid evaluation procedures as well as value-for-money and fiscal viability

assessments are explained in guidance manuals provided by a central body, while the actual procurement is

usually decentralized to the relevant ministry or local authority. These guidance manuals cover every step

of the contract preparation and bidding process, and can easily draw on those developed by international

financial institutions. The 2008 ‘Manual on Standard Operating Policies and Procedures’ of Botswana’s

Public Procurement and Asset Disposal Board (PPADB), and the 2006 PPP Guidance Manual released by

the Mauritian PPP Unit, are two useful – if somewhat dated – examples of such manuals.

In the interest of legibility and relevance for public authorities, this guidance must carefully be

tailored to individual country specificities. For instance Nigeria’s Infrastructure Concession Regulatory

Commission (ICRC) makes a very user-friendly website available to public authorities, adapted to both

federal and state-level infrastructure procurement needs in Nigeria. In addition the Lagos State Office of

PPPs details the conditions under which various forms of tendering can take place – from international and

national competitive bidding, to two-stage bidding, restricted or selective bidding, single source

procurement or framework contracting – together with the recommended timeframe for each method.

2.3. Financing infrastructure programmes

According to the World Economic Forum, an estimated USD 60 trillion needs to be invested in global

infrastructure between 2013 and 2030 to support growing population needs. Of this amount, only about

USD 24 trillion is currently earmarked for the infrastructure sector (WEF, 2013). In developing countries,

filling coverage gaps and sustaining growth will imply a doubling of current infrastructure investment

levels (EIB, 2010). Although private participation in infrastructure has fallen in recent years due to the

global financial crisis, with appropriate incentives it could be returned at least to the previous levels.

Alongside these private inflows, public sector investment itself should be increased and better allocated.

On the private sector side, bank financing is difficult in many developing countries due to the narrow,

concentrated and illiquid nature of the domestic banking sector. The tightening of banking regulations in

the aftermath of the financial crisis could also impede international financing of infrastructure projects. In

addition, large banks might also prefer to come in as “brown-field investors”, that is after the field has been

tested by other investors. Examples from India show that involving local banks in the early phases of the

investment was useful as their knowledge proved critical in assessing the risks. Once the projects proved to

be viable, large international players were more likely to come in. Besides, some countries have

successfully made use of bank lending secured by companies’ balance sheets: such ‘asset finance’ has been

the second biggest contributor to renewable energy financing in Malaysia.

Provided that a stream of revenues from the project can be estimated within a reasonable degree of

accuracy, project financing is another option. Since the underlying assets of infrastructure projects are

long-lived, these projects lend themselves to long-term financing which usually takes the form of bonds or

long-term institutional investment (on behalf of pension funds and insurance companies, or by establishing

Special Purpose Vehicles for instance). Malaysia’s Employees Provident Fund (EPF) is the sixth largest

sovereign pension fund in the world with over a third of its investment portfolio in loans and bonds, used

in part to finance infrastructure projects. The picture is also promising in Africa, where by 2050, USD 7

trillion of assets will be managed by pension funds. In order to tap into this vast latent capacity, national

regulations need revisiting. In Nigeria for instance investment in private equity (which usually finances

infrastructure) is capped at only 5% for pension funds. Developing a domestic base of institutional

investors, with appropriate savings incentives and a proper capital market, can play a decisive role in

national growth and enhance domestic capability to address infrastructure needs.

Institutional investors outside of the ‘host country’ (such as pension funds and insurance funds based

in OECD countries) also represent a vast and rapidly-growing pool of finance for infrastructure projects in

Fostering Investment in Infrastructure © OECD 2015 23

developing and emerging economies. In principle, infrastructure utilities are an asset class which suits the

long-term nature of the liabilities of such funds. Yet worldwide, less than 1% of the assets of insurers,

pension funds and sovereign wealth funds are invested in infrastructure. This is in part explained by

regulatory constraints: some home countries impose strict controls on the investment of such funds in

infrastructure and utilities, especially outside the home country. To overcome such obstacles, in 2014, the

OECD has delivered the G20/OECD High-Level Principles for Long-Term Investment Financing by

Institutional Investors. A voluntary checklist has also been developed against these Principles, to assist

governments in self-assessing their support schemes for long-term investment financing. Developing

appropriate investment vehicles to access long-term investments, and promoting infrastructure as an asset

class for long-term investors, is important. Institutional (and other) investors for instance need a sufficient

pipeline of projects in which to invest over the long-term. Currently, however, project financing often

requires an ‘investment grade’ credit rating (be it at the project or country level); this can be particularly

difficult to secure for developing countries, of which only a minority are comprehensively assessed by

international credit rating institutions.

On the public sector side and to complement private inflows, finance can be provided by government

budgets, bilateral or multilateral development finance institutions, export credit or guarantee agencies, and

development assistance agencies. Public sector finance can also be used to leverage private sector finance,

so as to support a portfolio of infrastructure projects substantially larger than if all the finance had to come

from the public sector and development partners. Malaysia released its first infrastructure-related bonds in

the mid-1990s (OECD, 2013d). Meanwhile Namibia has successfully issued corporate bonds, South Africa

has issued municipal bonds and equity, and Mozambique, Uganda and Zambia among others have issued

bonds for power sector projects (EIB, 2010). In addition to address the financing needs of infrastructure

PPP projects, the government of India has established the India Infrastructure Finance Company Limited

(IIFCL) to provide long-tenor debt to infrastructure projects. The government has also launched a scheme

for financial support to PPPs to provide “viability-gap” funding to PPP projects that would otherwise not

be financially viable (OECD, 2009b).

2.4. Project monitoring

During project roll-out, it is necessary to regularly check to what extent the assumptions made during

project preparation align with reality. Ensuring quality delivery during project roll-out requires dedicated

staff. They may be a temporary team drawn from the agency in charge of procuring the project or they may

be in a permanent unit of government that can be drawn upon for this purpose. For instance India has an

independent project monitoring unit in the Ministry of Statistics and Programme Implementation, which

can provide monitoring services to other units of government based on MoUs. In the case of PPPs, project

monitoring may be done in a dedicated PPP unit. Given the variety of oversight options available, the legal

regime for public procurement needs to specify who will be responsible for monitoring project

implementation.

For effective monitoring, the procurement contracts themselves must also specify timelines,

deliverables, and metrics with enough precision for the monitoring unit to validate the performance of the

contractor. In cross-border projects these must be agreed upon by all public parties. Among other methods,

contracts can be settled through performance-based procurement (PBP). Under PBPs payments are made

based on the quantity delivered during specified time periods subject to a quality standard. In the bidding

process the inputs are not specified, as it is up to the contractors to specify how they intend to achieve the

desired results. Payments to private providers often take the form of fixed monthly payments plus a

variable amount based on performance standards set in the contract. Some contracts also call for retention

of payments if results fall short of the quantities specified, or for premium payments in the inverse case.

24 Fostering Investment in Infrastructure © OECD 2015

Various developing and emerging economies have attempted PBP contracts relatively early on (for

instance Venezuela in 1997 with Aguas de Monagay, or Jordan in 1999 with Aman Water and Sewerage

Management). Some others have attempted a slightly different form of performance contracting, by

defining performance targets in terms of improvement rates relative to a benchmark, rather than in absolute

levels. For instance in Chile performance of water concessions is measured against a model company,

while water sector contracts in both Manila and Jakarta have been segmented into East and West Zones,

allowing for direct performance comparisons (OECD, 2009a). By contrast more traditional forms of

infrastructure procurement tend to include detailed technical specifications related not only to expected

outputs but also to inputs, with less room for innovation (but also less risk transfer) for the private party

(see Figure 2.2 above).

The advantages of PBP are their greater cost-effectiveness, and scope for technological innovation.

However, there are disadvantages. The need for higher performance security (shifting risk for delivery of

outcomes to the private partner) may mean higher project costs and thus may result in fewer qualified

bidders; the preparation of functional specifications may require sector-specific specialised training; and

the evaluation of options using different engineering specifications may require hiring external expertise.

Section 3.2 below addresses in more detail the importance of adequate public sector capacity for managing

private participation in infrastructure projects, from conception to contract termination.

2.5. Key policy takeaways

Investment projects and infrastructure priorities should be developed in co-operation with local

and regional authorities, involve public consultations, and be aligned with the strategic needs of

specific sectors of the economy. These national strategies and plans should clearly identify the

expected role for private investors to play across different infrastructure networks.

Investment projects should be carefully evaluated by first requiring pre-feasibility studies, and –

after screening – be subject to full project appraisal including cost-benefit analysis and

sustainability impact analysis to ensure value for money. The public expenditure component of

infrastructure investment projects should also fit within the government’s budget envelope.

Risks should be allocated appropriately between the contracting parties in public private

partnerships, as well as among countries in regional projects. The contract modality chosen for a

particular project will have implications in terms of asset ownership, project duration, and the

degree of technological innovation required in the project. It should also to a large extent

determine the degree of risk transfer.

Sources of finance for infrastructure projects should be as varied as possible, and governments

should make optimal use of national and municipal bonds (among other innovative sources).

Home countries have a role to play in creating a more enabling regulatory framework that can

allow investment by pension funds and other institutional investors overseas. Meanwhile host

developing countries can seek to create more avenues for infrastructure bank financing, by

improving the liquidity and breadth of domestic financial markets.

Monitoring project roll-out requires skilled and dedicated staff in dedicated PPP Units, or other

agencies responsible for project monitoring. Performance criteria can be specified in the contract

and be associated with a system of penalties and rewards based on the level of performance.

Fostering Investment in Infrastructure © OECD 2015 25

3. INSTITUTIONAL ENVIRONMENT FOR SOUND PRIVATE PARTICIPATION IN

INFRASTRUCTURE MARKETS

3.1. Role of PPP Units, procurement entities, and privatisation authorities

The shift towards private sector participation in infrastructure places new demands on government

agencies and involves the responsibilities of multiple bodies (see Figure 3.1). Most countries have

established a public authority for co-ordinating public procurement at the national level, as well as

authorities for receiving appeals of procurement procedures and for overseeing privatisation processes.

Many have also established specific PPP units, although with differing levels of capacity.

Figure 3.1: Implication of public agencies in the roll-out of public procurement infrastructure projects

Source: NEPAD-OECD Africa Investment Initiative (created by author)

Together with Ministries of Finance, various oversight and management authorities are frequently

established in order to secure an efficient use of public funds, and to ensure that public procurement is

carried out in a fair and transparent manner. Most frequently this includes: central procurement authorities,