Forward-looking statements - InnVest Hotelsinnvesthotels.com/Userfiles/file/INN Q109 - ALL.pdf ·...

44

FIRST QUARTER REPORT 2009 1 Letter to unitholders The lodging industry continues to experience a slowdown in demand, reflecting broader economic trends and their impact on discretionary spending for travel. Diligent cost controls coupled with efforts to drive room rates throughout the portfolio helped mitigate the impact of reduced occupancies across the portfolio. Looking ahead, we continue to expect 2009 to be a difficult year for the hospitality sector. Our objectives through this period are to solidify our balance sheet liquidity and effectively manage our assets. First quarter earnings are not reflective of anticipated results for the annual period given the seasonality of operations. The first quarter is typically the weakest earnings period for the Trust. First quarter operating highlights p Average daily rate growth of 0.8% was offset by a 3.6 point decline in occupancy driven by the deteriorating economic environment and its impact on discretionary travel demand. As a result, revenue per available room (“RevPAR”) on a same-hotel basis declined 5.5%; p Overall, hotel revenues declined 6.1%, or $8.2 million, to $127.7 million. The revenue shortfall was somewhat offset by a 3.1% reduction in hotel expenses. Hotel operating income declined $4.8 million to $18.4 million; p The REIT generated a first quarter net loss of $15.4 million, relatively unchanged from the prior period; p The Trust maintained a prudent payout ratio of 87.5% on a trailing twelve month basis. Distributable loss and funds from operations both declined in the first quarter of 2009 as compared to 2008 reflecting the impact of lower revenues; and p Following the end of the first quarter of 2009, the Trust divested one hotel, previously classified as held for sale, for gross proceeds of $4.1 million. While credit markets appear to be stabilizing, significant uncertainty remains which leads us to maintain a cautious outlook in the near term. Building on our efforts in 2008, we have adapted our strategy to position the REIT to address the current environment with particular attention to our balance sheet and liquidity. Our priority in 2009 will be to continue to be proactive in our capital management initiatives including efforts to address debt maturities. We are continually seeking opportunities to recycle our capital efficiently and have actively expanded our sales efforts with respect to certain underperforming assets. Having developed and implemented contingency plans throughout the portfolio, we continue to manage our portfolio aggressively to maximize the performance of each hotel. Historically, the lodging industry performance has been highly correlated with the economy given the largely discretionary nature of leisure and business travel. While Canada cannot escape the impact of the volatile global trends, it remains fundamentally stronger than many other countries, including the U.S., as evidenced by national RevPAR performance over the last several months. Despite the near term operating environment, with new supply effectively constrained by the credit markets, InnVest is positioned for a stronger recovery when demand trends improve. InnVest’s current portfolio is diversified by geography, customer and brand. This diversity, combined with our partnership with experienced hotel operators, contributes to the resiliency of the portfolio and positions the REIT to effectively manage through the current economic environment. Kenneth Gibson President and Chief Executive Officer May 6, 2009 Q1 2009 First Quarter Report to Unitholders For the three months ended March 31, 2009.

Transcript of Forward-looking statements - InnVest Hotelsinnvesthotels.com/Userfiles/file/INN Q109 - ALL.pdf ·...

first quarter report 2009 1

Letter to unitholdersThe lodging industry continues to experience a slowdown in demand, reflecting broader economic trends and their impact on discretionary spending for travel. Diligent cost controls coupled with efforts to drive room rates throughout the portfolio helped mitigate the impact of reduced occupancies across the portfolio. Looking ahead, we continue to expect 2009 to be a difficult year for the hospitality sector. Our objectives through this period are to solidify our balance sheet liquidity and effectively manage our assets.

First quarter earnings are not reflective of anticipated results for the annual period given the seasonality of operations. The first quarter is typically the weakest earnings period for the Trust.

First quarter operating highlights p Average daily rate growth of 0.8% was offset by a 3.6 point

decline in occupancy driven by the deteriorating economic environment and its impact on discretionary travel demand. As a result, revenue per available room (“RevPAR”) on a same-hotel basis declined 5.5%;

p Overall, hotel revenues declined 6.1%, or $8.2 million, to $127.7 million. The revenue shortfall was somewhat offset by a 3.1% reduction in hotel expenses. Hotel operating income declined $4.8 million to $18.4 million;

p The REIT generated a first quarter net loss of $15.4 million, relatively unchanged from the prior period;

p The Trust maintained a prudent payout ratio of 87.5% on a trailing twelve month basis. Distributable loss and funds from operations both declined in the first quarter of 2009 as compared to 2008 reflecting the impact of lower revenues; and

p Following the end of the first quarter of 2009, the Trust divested one hotel, previously classified as held for sale, for gross proceeds of $4.1 million.

While credit markets appear to be stabilizing, significant uncertainty remains which leads us to maintain a cautious outlook in the near term.

Building on our efforts in 2008, we have adapted our strategy to position the REIT to address the current environment with particular attention to our balance sheet and liquidity. Our priority in 2009 will be to continue to be proactive in our capital management initiatives including efforts to address debt maturities. We are continually seeking opportunities to recycle our capital efficiently and have actively expanded our sales efforts with respect to certain underperforming assets. Having developed and implemented contingency plans throughout the portfolio, we continue to manage our portfolio aggressively to maximize the performance of each hotel.

Historically, the lodging industry performance has been highly correlated with the economy given the largely discretionary nature of leisure and business travel. While Canada cannot escape the impact of the volatile global trends, it remains fundamentally stronger than many other countries, including the U.S., as evidenced by national RevPAR performance over the last several months.

Despite the near term operating environment, with new supply effectively constrained by the credit markets, InnVest is positioned for a stronger recovery when demand trends improve. InnVest’s current portfolio is diversified by geography, customer and brand. This diversity, combined with our partnership with experienced hotel operators, contributes to the resiliency of the portfolio and positions the REIT to effectively manage through the current economic environment.

Kenneth Gibson President and Chief Executive Officer

May 6, 2009

Q12009 First Quarter Report to Unitholders For the three months ended March 31, 2009.

2 innVest real estate inVestment trust

management’s discussion and analysis

IntroductionInnVest Real Estate Investment Trust (“InnVest”, the “Trust”

or the “REIT”) is an unincorporated open-ended real estate

investment trust governed by the laws of Ontario and a

Declaration of Trust. It is publicly traded and listed on the

Toronto Stock Exchange under the symbol INN.UN. The

following is a discussion of the results of operations and

financial condition of InnVest for the three months ended

March 31, 2009.

The following management’s discussion and analysis (“MD&A”)

should be read in conjunction with the interim unaudited

financial statements and notes contained herein as at and

for the three months ended March 31, 2009. This MD&A

should also be read in conjunction with the REIT’s audited

consolidated financial statements for the year ended

December 31, 2008 and the MD&A for the year ended

December 31, 2008. The financial statements of InnVest are

prepared in accordance with Canadian generally accepted

accounting principles (“GAAP”) and are presented in Canadian

dollars. Monetary data in tabular form and in the text, unless

otherwise indicated, are in thousands of dollars, except for per

unit, average daily rate (“ADR”), and revenue per available

room (“RevPAR”) amounts. This MD&A is dated May 6, 2009.

Certain measures in this MD&A, such as hotel operating

income (“HOI”), funds from operations (“FFO”) and distributable

income, do not have any standardized meaning as prescribed

by GAAP, and therefore are considered non-GAAP measures.

InnVest uses non-GAAP financial measures to assess its

operating performance. Securities regulators require that

entities caution readers that earnings and other measures

adjusted to a basis other than GAAP do not have standardized

meanings and are unlikely to be comparable to similar

measures used by other companies. Please see Non-GAAP

Financial Measures for a discussion of certain non-GAAP

financial measures used by the Trust, including a reconciliation

to GAAP financial measures.

Additional information relating to InnVest, including its Annual

Information Form, can be accessed on the Canadian Securities

Administrators’ System for Electronic Document Analysis and

Retrieval (“SEDAR”) located at www.sedar.com and on the

Trust’s website at www.innvestreit.com.

Forward-looking statementsIn the interest of providing InnVest unitholders and potential

investors with information regarding the Trust, certain

statements contained in this M&DA constitute forward-looking

statements within the meaning of applicable securities laws.

These statements include, but are not limited to, statements

made concerning InnVest’s objectives, its strategies to achieve

those objectives, as well as other statements with respect to

management’s beliefs, plans, estimates and intentions, and

similar statements concerning anticipated future events,

results, circumstances and performance or expectations that

are not historical facts. Forward-looking information typically

contains statements with words such as “outlook”, “objective”,

“may”, “continue”, “anticipate”, “believe”, “expect”, “estimate”,

“plan”, “intend”, “forecast”, “project” or similar expressions

suggesting future outcomes or events. Such forward-looking

statements reflect management’s current beliefs and are based

on information currently available to management.

These forward-looking statements are not guarantees of future

events or performance and, by their nature, are based on

InnVest’s estimates and assumptions, which are subject to

risks and uncertainties, including those described under “Risks

and uncertainties” in this MD&A. Readers are cautioned not to

place undue reliance on forward-looking statements, as there

can be no assurance that the plans, intentions or expectations

upon which they are based will occur. By its nature, InnVest’s

forward-looking information involves numerous assumptions,

inherent risks and uncertainties, which may cause the Trust’s

actual performance and financial results in future periods to

differ materially from any estimates or projections of future

performance or results expressed or implied by such forward-

looking statements. Factors that could cause actual results,

performance, or achievements to differ materially from those

expressed or implied by forward-looking statements include,

but are not limited to, changes in business strategies; general

global economic and business conditions; general global credit

market conditions; the effects of competition and pricing

pressures; industry overcapacity; shifts in market demands;

changes in laws and regulations, including environmental and

regulatory laws; potential increases in maintenance and

operating costs; uncertainties of litigation; labour disputes;

timing of completion of capital or maintenance projects;

currency and interest rate fluctuations; various events which

could disrupt operations; and technological changes.

Although InnVest believes that the expectations represented by

such forward-looking statements are reasonable, there can be

no assurance that such expectations will be consistent with

first quarter report 2009 3

management’s discussion and analysis

InnVest REIT holds Canada’s largest hotel portfolio together

with a 50% interest in Choice Hotels Canada Inc., the largest

franchisor of hotels in Canada. InnVest’s portfolio is well

diversified across hotel accommodation categories, brands,

geography and customers.

Hotel real estate ownerAs at March 31, 2009, InnVest’s portfolio comprised

147 hotel properties, with 19,235 rooms, operated under

internationally recognized franchise brands. For the year ended

December 31, 2008, approximately 77% of InnVest’s hotel

revenues were generated from room revenues and 23% from

food and beverage services and other services including

parking, retail operations and telephone use.

InnVest’s hotels are operated by four hotel management

companies, which earn base and incentive fees related

to the revenues and profitability of each hotel. The hotels’

primary operating costs include wages, food costs, utilities,

management fees, and sales and marketing expenses. Other

property level expenses include property taxes, ground rent

for leasehold interests and property insurance. Many of these

property level expenses are relatively fixed and do not

necessarily change in accordance with revenue levels.

InnVest’s hotels are typically located near major thoroughfares

in urban and suburban areas, business centres, government

and manufacturing facilities, universities, airports and tourist

attractions. The hotels have a diverse customer base,

including business travellers, leisure travellers, tours,

associations, and corporate groups.

Business overview

Ontario Quebec Atlantic Western Total

% of

No. of No. of No. of No. of No. of total

No. of guest No. of guest No. of guest No. of guest No. of guest guest

hotels rooms hotels rooms hotels rooms hotels rooms hotels rooms rooms

Comfort Inn 38 3,155 22 1,754 15 1,126 9 745 84 6,780 35.3%

Delta Hotel 2 573 3 1,048 4 1,017 2 689 11 3,327 17.3%

Holiday Inn 14 2,376 – – 1 196 1 152 16 2,724 14.1%

Travelodge 4 552 – – – – 4 896 8 1,448 7.6%

Quality Suites/Inn 4 604 3 396 – – – – 7 1,000 5.2%

Quality Hotel 1 212 2 298 1 160 1 126 5 796 4.1%

Hilton Hotel – – 1 571 1 197 – – 2 768 4.0%

Radisson Hotel/Suites 3 532 1 175 – – – – 4 707 3.7%

Fairmont Hotels & Resorts – – – – – – 2 604 2 604 3.1%

Staybridge Suites 3 342 – – – – – – 3 342 1.8%

Sheraton Suites – – – – – – 1 323 1 323 1.7%

Best Western 1 130 – – – – – – 1 130 0.7%

Hilton Garden Inn 1 120 – – – – – – 1 120 0.6%

Hilton Homewood Suites 1 83 – – – – – – 1 83 0.4%

Independent 1 83 – – – – – – 1 83 0.4%

73 8,762 32 4,242 22 2,696 20 3,535 147 19,235 100.0%

these forward-looking statements. The forward-looking

statements contained in this MD&A are made as of the date

of this MD&A. Except as required by law, InnVest does not

undertake any obligation to publicly update or revise any

forward-looking statements, whether as a result of new

information, future events or otherwise. All forward-looking

statements contained in this MD&A are expressly qualified by

this cautionary statement.

4 innVest real estate inVestment trust

management’s discussion and analysis

Innvest’s franchise businessGenerating $3.8 million in other business income for the

year ended December 31, 2008 ($493 year-to-date in 2009),

InnVest owns 50% of Choice Hotels Canada Inc. (“CHC”),

which has franchise agreements with over 290 locations

representing over 24,500 guest rooms open and under

development in Canada. The remaining 50% interest is owned

by Choice Hotels International Inc. (“Choice International”),

one of the largest hotel franchise companies in the world.

In addition to strong international brand recognition, Choice

International has a centralized reservation system, sales

and marketing programs and proprietary property

management systems.

In 1993, CHC was granted a 99-year license to franchise all

Choice hotel brands in Canada, including Comfort Inn®, Quality

Suites® and Quality Hotels®. CHC earns franchise revenue

by charging hotel owners a monthly royalty fee based

on a percentage of the revenue generated by the licenced

properties and by selling franchises. InnVest’s proportionate

interest operating results are included in the consolidated

statements of income in other business income.

Office, retail and retirement home businessGenerating $1.8 million in other business income for the

year ended December 31, 2008 ($419 year-to-date in 2009),

InnVest owns office and retail real estate as well as a

retirement home. These real estate interests are adjacent

to owned hotels and were acquired as part of certain hotel

acquisitions. The operating results are included in the

consolidated statements of income in other business income.

51%Limited service

49%Full service

Rooms By Service Category

46%Ontario

22%Quebec

14%Atlantic

18%West

Rooms By Geography

35%Transient

10%Other

18%Group

2008 Room Revenues By Customer

37%Corporate

&Government

first quarter report 2009 5

management’s discussion and analysis

InnVest has adapted its strategy in response to the current

economic environment with a near term focus aimed at

preserving the REIT’s balance sheet stability. We believe

efforts to enhance liquidity, combined with our proven ability

to manage assets in difficult times, will differentiate the REIT

in this environment. InnVest employs operating and capital

allocation strategies to position the REIT to ensure the stability

of its balance sheet and to position it to take advantage of

opportunities which may exist.

Operating strategyInnVest’s operating focus aims to enhance the performance

of each hotel and improve its RevPAR penetration versus its

competitive set. Internal growth is maximized through the

following operating and strategic principles:

1. Partnering with leading hotel management groups and brands;

2. Implementing yield management and market strategies to

maximize RevPAR;

3. Leveraging InnVest’s size and industry experience to control

costs through operating efficiencies, as well as taking

advantage of buying power and economies of scale; and

4. Investing in the portfolio to drive higher returns and enhance

the value of the assets.

InnVest’s ability to deliver stable cash flow is largely achieved

through its diversification, by location, brand, customer and

market position. Since individual markets can be affected

by local events and economic conditions, geographic

diversification helps limit the impact of such factors on the

overall portfolio. Diversification across customers and brands

allows the Trust to effectively manage its rooms based on

changing demand drivers, thereby optimizing the financial

performance through improved occupancy and ADR.

The manager of all but 15 of InnVest’s hotels is Westmont

Hospitality Canada Ltd (“Westmont”), one of the largest

privately held managers of hotels in the world. The managers

of the REIT’s remaining 15 hotels are Delta Hotels (10),

Fairmont Hotels (3) and Hilton Hotels (2), each an experienced

hotel manager with recognized brands.

Capital allocation strategyIn order to drive the long-term profitability of the portfolio,

InnVest continually evaluates its capital allocation

opportunities. Over the last several years, InnVest has

significantly expanded its portfolio, broadening its market

base and diversifying its risk profile. Following this growth,

the Trust’s current capital allocation efforts are focused

on maximizing the potential of its existing portfolio.

The Trust constantly evaluates its current real estate holdings

to optimize diversification and capitalize on embedded value or

higher return opportunities. From time to time, certain assets

are identified that may not support the Trust’s long term

objectives given limited growth prospects in earnings and value.

In late 2007, InnVest reclassified four assets as held for sale.

Three of these hotels were sold in 2008. The remaining asset

was sold subsequent to the end of the first quarter in 2009.

In accordance with its capital allocation review, InnVest

identified five hotel properties to be held for sale in the

current quarter and wrote down the book value of these hotels

by $29.6 million during the fourth quarter of 2008 based

on expectations of sale proceeds. These hotel properties

contributed minimal hotel operating income of $1.6 million

to the REIT in 2008 and their sale should enable the successful

redeployment of funds into higher yielding opportunities.

Business strategy

Recent developmentsDuring the first quarter of 2009, InnVest successfully extended

two mortgages totalling $13.5 million which were originally

scheduled to mature in February 2010. One mortgage of

$6.9 million was extended to September 30, 2012, while

the second mortgage of $6.6 million was extended to

December 31, 2012 at a weighted average interest rate of

approximately 6.8% compared to the previous rate of 6.2%.

During the first quarter, InnVest classified five assets as held

for sale. The Trust recognized a non-cash impairment charge

of $29.6 million during the fourth quarter of 2008 based on the

anticipated fair value of these assets. The hotel properties

are primarily in tertiary markets impacted by the manufacturing

sector decline and which have also been particularly impacted

by new supply in recent years. In aggregate, six assets were

classified as discontinued operations as at March 31, 2009.

Following the end of the first quarter of 2009, InnVest

completed the divestiture of one hotel which had been

identified as held for sale since the end of 2007. The

transaction was completed for gross proceeds of

$4.1 million less closing costs.

6 innVest real estate inVestment trust

management’s discussion and analysis

First quarter operating highlights

OutlookWhile credit markets appear to be stabilizing, significant

uncertainty remains which leads us to maintain a cautious

outlook in the near term.

Building on our efforts in 2008, we have adapted our strategy

to position the REIT to address the current environment with

particular attention to our balance sheet and liquidity. Our

priority in 2009 will be to continue to be proactive in our

capital management initiatives including efforts to address

debt maturities. We are continually seeking opportunities

to recycle our capital efficiently and have actively expanded

our sales efforts with respect to certain underperforming

assets. Having developed and implemented contingency plans

throughout the portfolio, we continue to manage our portfolio

aggressively to maximize the performance of each hotel.

Historically, the lodging industry performance has been highly

correlated with the economy given the largely discretionary

nature of leisure and business travel. While Canada cannot

escape the impact of the volatile global trends, it remains

fundamentally stronger than many other countries, including

the U.S., as evidenced by national RevPAR performance over

the last several months.

Despite the near term operating environment, with new supply

effectively constrained by the credit markets, InnVest is

positioned for a stronger recovery when demand trends

improve. InnVest’s current portfolio is diversified by geography,

customer and brand. This diversity, combined with our

partnership with experienced hotel operators, contributes to

the resiliency of the portfolio and positions the REIT to

effectively manage through the current economic environment.

p First quarter earnings are not reflective of anticipated results

for the annual period given the seasonality of operations.

The first quarter is typically the weakest earnings period

for the Trust.

p ADR growth of 0.8% was offset by a 3.6 point decline

in occupancy driven by the deteriorating economic

environment and its impact on discretionary travel demand.

As a result, RevPAR on a same-hotel basis declined 5.5%.

This performance exceeds the RevPAR achieved across

the Canadian lodging industry during the quarter;

p Overall, hotel revenues declined 6.1%, or $8.2 million, to

$127.7 million. The revenue shortfall was somewhat offset

by a 3.1% reduction in hotel expenses. Overall, HOI

declined $4.8 million to $18.4 million;

p The REIT generated a first quarter net loss of $15.4 million,

relatively unchanged from the prior period;

p InnVest maintained a prudent payout ratio of 87.5% on a

trailing twelve month basis. Distributable loss and funds

from operations each declined in the first quarter of 2009

as compared to 2008 reflecting the impact of lower

revenues; and

p Following the end of the first quarter of 2009, the Trust

divested one hotel, previously classified as held for sale,

for gross proceeds of $4.1 million.

first quarter report 2009 7

management’s discussion and analysis

Hotel operating results comparisonThe REIT has classified 138 of its 144 hotels owned for the

entire current and comparative period as its “Base Portfolio”,

with the remaining six hotels being classified as discontinued

operations. Operating results for three assets acquired or

developed have been excluded since their results were

capitalized during a portion of the periods presented in

accordance with the REIT’s accounting policy.

Hotel revenues Hotel revenues consist primarily of revenue generated from

room occupancy. Non-room revenue from food and beverage

services and other miscellaneous revenue streams associated

with hotel operations such as space leases, vending

commissions, movie rentals, parking and telephone are

also included. For the first quarter of 2009, room revenues

accounted for approximately 77% of total hotel revenues.

Overall hotel portfolioFor the three months ended March 31, 2009, hotel revenues

decreased by $8.2 million, or 6.1%, to $127.7 million. First

quarter results were impacted by the deteriorating economic

environment and its impact on discretionary travel demand.

For the three months ended March 31, 2009, a 0.8% increase

in ADR was offset by a 3.6 point decline in overall occupancy.

The trend of ADR growth offsetting occupancy declines is

consistent with trends experienced through late 2008. Overall,

first quarter RevPAR decreased 5.5%. InnVest’s first quarter

RevPAR performance outperformed results achieved by the

broader Canadian hotel industry. RevPAR trends were

generally consistent across all service categories and brands.

Notably, RevPAR from the 2007 full-service portfolio additions

outperformed the RevPAR achieved across the balance

of the portfolio.

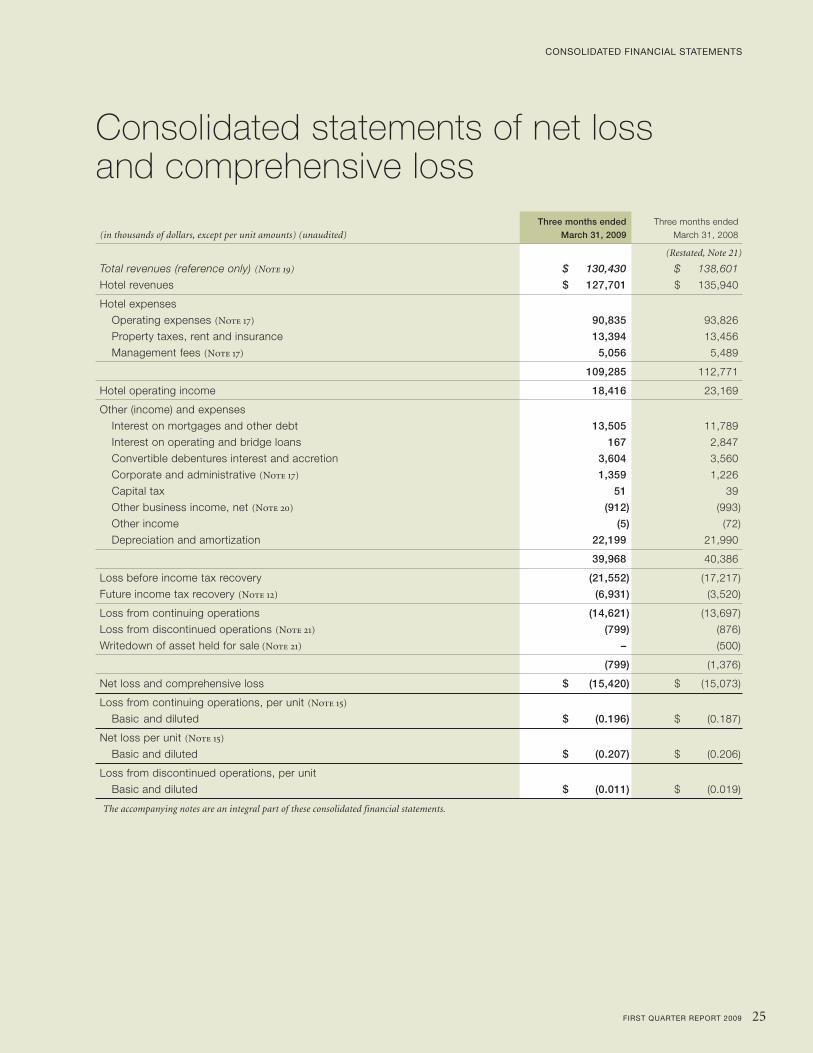

First quarter operating results reviewThree months ended March 31, 2009 2008

Hotel revenues $ 127,701 $ 135,940

Hotel expenses 109,285 112,771

Hotel operating income1 18,416 23,169

Net loss from continuing operations (14,621) (13,697)

Net loss and comprehensive loss (15,420) (15,073)

Funds from operations1 447 3,418

Distributable loss1 (3,753) (272)

Distributions declared2 13,956 20,618

Distributions per unit2 0.1875 0.28125

Per Unit:

Net loss from continuing operations per unit – basic and diluted (0.196) (0.187)

Net loss per unit – basic and diluted (0.207) (0.206)

Funds from operations per unit – basic and diluted 0.006 0.047

Distributable loss per unit3 – basic and diluted (0.050) (0.004)

1. See Non-GAAP Financial Measures.

2. Distributions and distributions per unit include cash distributions and distributions arising from the dividend reinvestment plan.

3. Distributable loss per unit is calculated on a basis consistent with that prescribed by GAAP for calculating net loss per unit.

Occupancy ADR RevPAR

% Variance to 2008 $ Variance to 2008 $ Variance to 2008

Ontario 51.1% (4.1 pts) $ 109.84 0.2% $ 56.11 (7.4%)

Quebec 52.2% (2.8 pts) $ 105.75 0.8% $ 55.21 (4.3%)

Atlantic 49.1% (4.4 pts) $ 104.47 1.3% $ 51.33 (7.0%)

Western 59.2% (2.3 pts) $ 137.03 1.0% $ 81.08 (2.9%)

Total 52.6% (3.6 pts) $ 114.19 0.8% $ 60.11 (5.5%)

Note: On a same-hotel basis, excluding the hotels that have been classified as discontinued operations, and the hotels which have not been included in the full

periods presented.

8 innVest real estate inVestment trust

management’s discussion and analysis

Room revenuesConsistent with RevPAR performance achieved during

the quarter, overall room revenues for the three months

ended March 31, 2009 decreased $5.8 million, or 5.6%, to

$98.1 million. Each region experienced modest ADR growth

which offset declines in occupancies. The overall declines in

occupancy are more broadly related to economic conditions

beyond the control of the Trust. As was noted in 2008,

Ontario continues to show the weakest performance given

its particular reliance on the manufacturing industry.

Three months ended March 31, 2009

Number of Variance

Room revenue variance hotel rooms $ Variance to 2008

Base Portfolio

Ontario 7,634 $ (3,527) (8.4)%

Quebec 4,080 (1,157) (5.4)%

Atlantic 2,696 (1,090) (8.0)%

West 3,535 (1,078) (4.0)%

Sub-total 17,945 (6,852) (6.6)%

Acquisitions 342 1,047 100.0%

Total 18,287 $ (5,805) (5.6)%

Consistent with broader economic activity and trends noted

through the end of 2008, demand was notably softer in the

first quarter of 2009 for the Ontario region. Ontario, particularly

southern Ontario, is impacted by the challenges experienced

in the manufacturing sector with declining production and job

losses resulting in slowing demand for accommodations.

Overall, first quarter room revenues for the region declined

$3.5 million or 8.4% based on occupancy declines. Almost

all of this decrease was realized in the Greater Toronto Area

and southern Ontario markets such as Burlington, Kitchener

and London.

InnVest’s Base Portfolio of Quebec hotels saw room revenues

decline $1.2 million or 5.4%. Modest rate growth achieved in

the region was offset by occupancy declines. As anticipated,

lower demand was experienced in Quebec City, which

benefitted from year-long festivities associated with the city’s

400th anniversary celebrations in 2008. We expect similar

trends for this city through the balance of 2009. The Montreal

area also experienced declining demand resulting from new

supply coupled with reduced group activity.

First quarter room revenues at InnVest’s Base Portfolio of

Atlantic hotels declined $1.1 million or 8.0%. Occupancies

were impacted by new supply in certain markets as the hotels

focused on maintaining room rate integrity. ADR increased

1.3% for the Atlantic region.

InnVest’s Base Portfolio of Western hotels realized a room

revenue decline of 4.0% or $1.1 million. This decline was

attributable to softness in Edmonton following a strong group

base in the comparative period. Results for the balance of the

region were in line with the prior year.

Non-room revenuesFor the three months ended March 31, 2009, non-room

revenues totalled $29.6 million, down $2.4 million or 7.6%

compared to the prior year. Non-room revenues are directly

impacted by overall occupancy. Lower occupancy results

in the reduced use of ancillary services offered at the hotel.

Hotel expensesIn periods of declining occupancies, the Trust is focused

on managing all costs to minimize the overall impact on

profitability. It should be noted that savings opportunities are

restricted during lower occupancy periods such as the first

quarter, particularly in smaller limited service hotels, given the

minimal infrastructure in place. Many property level expenses,

including property taxes, leasehold payments and insurance,

are relatively fixed and do not necessarily change in

accordance with overall demand levels.

Hotel expenses for the three months ended March 31, 2009

declined $3.5 million or 3.1% when compared to 2008. The

decrease reflects reduced occupancies as well as active steps

taken by the Trust to manage costs throughout the portfolio

in light of the softer economic environment. Some of these

initiatives, implemented in 2008, include hiring freezes and

salary freezes throughout most of the portfolio and at the

Trust’s corporate offices, as well as seeking to maximize value

from vendors through pricing concessions. These initiatives

should continue to benefit future periods.

Hotel operating incomeFor the three months ended March 31, 2009, the Trust

generated HOI of $18.4 million, down $4.8 million as

compared to the prior period. Typically, declining revenues,

or revenue growth below inflation, will result in a decline in

profitability given the considerable amount of operating fixed

costs, particularly at lower occupancy levels.

first quarter report 2009 9

management’s discussion and analysis

Net lossInnVest realized a net loss from continuing operations of

$14.6 million or a loss of $0.196 per unit basic and diluted.

These results were modestly lower then the loss of

$0.187 per unit basic and diluted in the prior year. The lower

HOI was offset by a higher future income tax recovery and

lower interest costs.

During the first quarter of 2009, InnVest reclassified five hotels

as discontinued operations. As at March 31, 2009, six assets

were held for sale. For the first quarter of 2009, discontinued

operations generated net losses of $799 compared to $876 in

the prior period. The prior year also includes a $500 writedown

of the book value of assets held for sale.

InnVest’s net loss for the first quarter totaled $15.4 million,

or a loss of $0.207 per unit basic and diluted, relatively

unchanged from the prior year.

Funds from operationsFor the three months ended March 31, 2009, InnVest

generated FFO of $447 ($0.006 per unit) compared to

$3.4 million in the prior period ($0.047 per unit). The decline

is primarily attributable to the $4.8 million reduction in HOI

for the first quarter. See Non-GAAP Financial Measures for

a reconciliation of GAAP net loss to FFO.

Distributable lossFor the three months ended March 31, 2009, InnVest

generated a distributable loss of $3.8 million (loss of

$0.050 per unit) compared to a distributable loss of $272 in

the prior year (loss of $0.004 per unit). The reduction reflects

lower HOI generated during the quarter. See Non-GAAP

Financial Measures for a reconciliation of GAAP net loss to

distributable loss.

Distributions declared during the first quarter of 2009 totalled

$14.0 million compared to $20.6 million in the prior period.

This reflected distributions of $0.1875 per unit (2008 –

$0.28125), reflecting the reduced level of monthly distributions

to $0.0625 per unit beginning in November 2008.

Three months ended March 31, 2009

Number of Variance

HOI variance hotel rooms $ Variance to 2008

Base Portfolio

Ontario 7,634 $ (2,653) (26.8)%

Quebec 4,080 (385) (14.9)%

Atlantic 2,696 (822) (59.1)%

West 3,535 (991) (10.7)%

Sub-total 17,945 (4,851) (20.9)%

Acquisitions 342 98 100.0%

Total 18,287 $ (4,753) (20.5)%

Hotel operating income margin analysisGiven the overall decline in revenues, hotel operating income

margins for the three months ended March 31, 2009, declined

to 14.4% as compared to 17.0% in 2008. First quarter margins

are not representative of annual margins achieved for the

portfolio given the seasonality of earnings. The first quarter

is historically the weakest earnings period for the Trust.

Other income and expensesOther income and expenses for the three months ended

March 31, 2009 totalled $40.0 million, down $418 as

compared to 2008. The decline is attributable to lower

overall interest incurred following the refinancing of the Trust’s

$215.0 million bridge loan in March 2008 with mortgage debt.

The REIT has benefitted from declines in overall floating

debt lending rates as compared to the prior year. At

March 31, 2009, approximately 9.7% of the REIT’s

outstanding debt is at floating rates.

Income taxesFor the three months ended March 31, 2009, the REIT

generated a future income tax recovery of $6.9 million,

as compared to $3.5 million in 2008. In addition to ongoing

operations and capital expenditures, the future income tax

recovery realized in the first quarter of 2009 reflects the

provincial SIFT tax rate change which was enacted in

March 2009 along with the impact of the reclassification

of certain assets as held for sale.

For 2009, the REIT estimates that the non-taxable portion of

the distributions made to unitholders during the year will be

approximately 40% (2008 – 44%).

10 innVest real estate inVestment trust

management’s discussion and analysis

Changes in financial conditionOperating activitiesFor the three months ended March 31, 2009, operating

activities used cash of $2.2 million, up $1.7 million from the

prior year. Lower cash earnings were somewhat offset by a

modest decline in working capital usage during the period

given tight cash management initiatives implemented to

conserve liquidity.

Financing activitiesFinancing activities reflect first quarter cash distributions

of $13.3 million (2008 – $16.7 million), which excludes the

distributions which were satisfied through the Trust’s dividend

reinvestment program (“DRIP”). Distributions declared for the

three months ended March 31, 2009 were $0.1875 per unit

compared to $0.28125 in 2008. In November 2008, the REIT

announced a reduction to its monthly distributions from

$0.09375 per unit to $0.0625 per unit. The Trust purchased

and cancelled 211,500 units for total proceeds of $689 during

the first quarter of 2009 in accordance with its normal course

issuer bid.

At March 31, 2009, the REIT had drawn $20.2 million from

its operating loan to finance the distribution and other capital

needs during the quarter. Given the seasonality of operations,

first quarter distributions are typically financed by drawing on

the Trust’s operating loan.

During the first quarter of 2008, InnVest completed

$390 million in aggregate mortgage financings, at a weighted

average blended interest rate of 5.6%, including new mortgage

debt and early refinancing of existing debt. Net proceeds were

used to repay the $215 million bridge loan incurred as part

of the acquisition of the Legacy Portfolio and to repay

$154.8 million in existing mortgages. InnVest fixed the

interest rates on $370 million of this debt.

During the prior period, the REIT also obtained

$17.3 million in financing to partially fund the acquisition

of one new hotel and the development of a second hotel.

Investing activitiesEach year, InnVest sets aside between 3% and 5% of total

hotel revenues at each hotel and certain amounts required for

hotel acquisitions for replacing furniture, fixtures and

equipment and capital improvements (the “FF&E reserve”).

Capital expenditures for the three months ended March 31,

2009 totalled $6.0 million (2008 – $5.9 million). This compares

to the Trust’s FF&E reserve of $5.4 million for the first quarter

of 2009 (2008 – $5.8 million).

Investing activities for the prior period reflect the acquisition

of a newly built hotel for $17.2 million and the completion

of a hotel under development.

SeasonalityInnVest’s operations are seasonal and as such its results are

not consistent throughout the year. Revenue earned from hotel

operations fluctuates throughout the year, with the third

quarter being the highest due to the increased level of leisure

travel in the summer months and the first quarter being the

lowest because leisure travel tends to be lower. The results

from operations vary materially from quarter to quarter

because of the seasonal nature of the revenue stream and the

fact that certain costs such as property taxes, insurance,

interest, depreciation and amortization, and corporate and

administrative expenses are fixed, or virtually fixed. Given their

lower relative contribution to results, weakness in the first and

fourth quarters will have a lesser impact on annual earnings.

Quarterly results

first quarter report 2009 11

management’s discussion and analysis

For each quarter ended (unaudited) (as reported)

March 31 Dec 31 Sept 30 June 30 March 31 Dec 31 Sept 30 June 30

2009 2008 2008 2008 2008 2007 2007 2007

Occupancy 52.6% 58.0% 72.1% 67.5% 55.9% 60.7% 72.8% 65.2%

ADR $ 114.09 $ 117.86 $ 125.86 $ 122.68 $ 112.89 $ 113.03 $ 105.17 $ 99.27

RevPAR $ 59.98 $ 68.33 $ 90.77 $ 82.84 $ 63.04 $ 68.56 $ 76.53 $ 64.70

Total revenues $ 127,701 $ 162,365 $ 193,832 $ 181,996 $ 140,529 $ 162,316 $ 135,982 $ 109,299

Hotel operating income $ 18,416 $ 36,871 $ 64,576 $ 56,152 $ 23,574 $ 38,130 $ 49,100 $ 33,959

Hotel operating income margin 14.4% 22.7% 33.3% 30.9% 16.8% 23.5% 36.1% 31.1%

Net (loss) income from

continuing operations $ (14,621) $ (28,329) $ 24,519 $ 17,186 $ (14,271) $ 24,510 $ 29,984 $ (113,270)

Distributable(loss) income $ (3,753) $ 13,340 $ 40,598 $ 31,874 $ (272) $ 13,686 $ 34,639 $ 19,892

Distributions $ 13,956 $ 16,277 $ 20,845 $ 20,733 $ 20,618 $ 21,572 $ 17,813 $ 15,793

Net (loss) income from

continuing operations

per unit

– basic $ (0.196) $ (0.381) $ 0.330 $ 0.233 $ (0.195) $ 0.337 $ 0.450 $ (2.023)

– diluted $ (0.196) $ (0.381) $ 0.320 $ 0.233 $ (0.195) $ 0.325 $ 0.420 $ (2.023)

Distributable (loss) income

per unit

– basic $ (0.050) $ 0.179 $ 0.547 $ 0.433 $ (0.004) $ 0.188 $ 0.520 $ 0.355

– diluted $ (0.050) $ 0.179 $ 0.497 $ 0.400 $ (0.004) $ 0.188 $ 0.474 $ 0.334

Trust units outstanding 74,434,338 74,412,317 74,249,239 73,849,170 73,447,668 73,000,694 72,610,235 56,265,058

Weighted average

trust units outstanding 74,439,594 74,373,530 74,222,761 73,647,417 73,234,488 72,795,804 66,566,306 56,002,020

Total assets $ 1,952,900 $ 1,977,104 $ 2,042,387 $ 2,060,807 $ 2,059,716 $ 2,062,279 $ 2,093,834 $ 1,210,338

Total long-term debt $ 938,774 $ 951,276 $ 948,318 $ 940,730 $ 939,582 $ 711,617 $ 728,817 $ 518,129

Liquidity and capital resourcesInnVest has several sources of liquidity including the following:

Cash generated from hotel operations

The REIT’s operations are seasonal with the first quarter

typically being the weakest earnings period given the low level

of business and leisure travel during these months. Over the

year, the REIT anticipates generating HOI sufficient to fund

distributions to unitholders, capital expenditures and debt

service requirements.

Lines of credit

InnVest has a line of credit with a major banking institution to

finance temporary shortfalls in cash resulting from business

seasonality and working capital fluctuations. The credit facility

may also be used to provide short-term financing in the event

of an acquisition of a new hotel.

Issuing additional debt

InnVest also has the ability to raise funds by mortgaging

its properties or by issuing either debt or convertible debt

securities. The Trust typically uses long-term debt financing to

refinance existing debt or to finance an acquisition. The choice

of debt instrument used is dependent on then-current market

conditions. The ability to secure debt financing on reasonable

terms is ultimately dependent on market conditions and

the lender’s determination of InnVest’s creditworthiness.

At March 31, 2009, substantially all of the REIT’s assets

have been pledged as security under debt agreements.

12 innVest real estate inVestment trust

management’s discussion and analysis

Issuing additional equity securities

InnVest’s listing on the Toronto Stock Exchange gives it the

ability to access, subject to market conditions, additional

equity through the issuance of additional units or other equity

instruments. When issued, additional equity is most often used

to finance an acquisition or repay debt. The REIT is subject to

certain restrictions on the issuance of equity as a result of

changes to the taxation of publicly traded trusts (refer to Risks

and Uncertainties – Proposed Tax Changes to Income Trusts).

Management believes that the REIT’s credit facilities,

cash on hand and expected cash flow from operations,

when combined with the potential to access debt and

equity markets, will allow InnVest to meet all of its

financial commitments.

Cash on hand At March 31, 2009, the REIT has cash on hand totaling

$12.9 million, of which $2.5 million is restricted under the

REIT’s Declaration of Trust for the replacement of furniture,

fixtures, and equipment and for capital improvements.

The REIT invests capital in its portfolio to maintain its

assets, and pursue repositioning opportunities to enhance

its competitive position. Capital expenditures for the three

months ended March 31, 2009 totalled $6.0 million (2008 –

$5.9 million). This compares to the Trust’s FF&E reserve of

$5.4 million for the first quarter of 2009 (2008 – $5.8 million).

Given the seasonality of hotel operations, revenues are

not earned evenly through the year. Conversely, capital

expenditures are typically scheduled during lower occupancy

periods to avoid guest displacement. However, in light of

the current operating environment, non-essential capital

investments during the first quarter of 2009 were limited in

order to meet the Trust’s desire to conserve liquidity. The Trust

expects its capital investment to be largely funded through

its FF&E reserve for the year 2009. Excess capital invested

above the FF&E reserve during the three months ended

March 31, 2009 was funded through cash from operations

or the REIT’s operating line.

The following table reconciles the change in restricted cash

during the three months ended March 31, 2009 and the

comparable period:

Three months ended March 31, 2009 2008

Opening balance $ 3,013 $ 2,995

FF&E Reserve 5,427 5,848

Capital expenditures (5,968) (5,919)

Closing balance $ 2,472 $ 2,924

Credit facility/bridge loanInnVest’s operations are seasonal (see Quarterly Results –

Seasonality). The REIT’s credit facility ensures that the

seasonal fluctuation in cash flows will not affect its ability

to operate in the normal course of business. The

Trust has a $40.0 million operating line secured by

14 unencumbered properties.

At March 31, 2009, $20.2 million was drawn on the credit

facility. In addition, letters of credit totaling $3.7 million were

drawn against the facility. The operating line bears interest at

the lesser of Canadian bank prime rate plus 0.5% or the

Canadian Bankers’ Acceptance rate plus 1.5%. This line of

credit expires in August 2009. Management anticipates that

the facility will be renewed in the normal course of business.

A $9.0 million bridge loan was scheduled to expire in

March 2009. Following the end of the quarter, management

successfully finalized an extension for $7.0 million of the bridge

through August 2009, bringing the maturity in line with the

REIT’s operating line with the same lender. The $2.0 million

difference was repaid in April 2009.

Mortgages payable and convertible debenturesAt March 31, 2009, InnVest had mortgages payable of

$945.4 million with a weighted average term of 3.5 years

and a weighted average effective interest rate of 5.6%.

Approximately 9.7% of the Trust’s mortgage debt is at floating

rate. In addition, the REIT has access to a loan facility, granted

in conjunction with property mortgages, for up to $36.1 million

to fund 50% to 100% of capital expenditures incurred

at individual hotels. At March 31, 2009, the REIT has

drawn $12.2 million on this facility (December 31, 2008 –

$12.2 million), such amounts being included in mortgages

payable. Remaining capacity under this facility at

March 31, 2009 approximated $23.9 million. In April 2009 an

additional amount of $6.9 million was funded under this facility.

InnVest also has three series of fixed-rate convertible

debentures which mature between 2011 and 2014.

At March 31, 2009, InnVest has $190.7 million

(December 31, 2008 – $190.8 million) in convertible

debentures outstanding.

InnVest’s debt obligations do not provide for any contractual

limitations on cash distributions to its unitholders.

first quarter report 2009 13

management’s discussion and analysis

During 2008, the global financial credit markets experienced

significant volatility. In general, the availability of credit has

deteriorated dramatically and credit spreads offered have

widened considerably. While credit spreads have widened, the

underlying bond yields have also decreased such that the

overall cost of debt, if available, remains relatively attractive.

The REIT’s strategy is to improve the performance of its hotels

and complete value-added capital investments as appropriate.

The resulting increased property values then enables the REIT

to obtain additional mortgage proceeds to finance additional

capital improvements or acquisitions. In light of the current

credit environment, the REIT’s near term focus is on preserving

its liquidity to help address future refinancing requirements,

including the potential that future refinancing proceeds are not

sufficient to satisfy mortgage debt maturities.

Adjusted debt to gross book valuesInnVest is not permitted to exceed certain financial leverage

amounts under the terms of the Declaration of Trust. The REIT

is permitted to hold indebtedness, excluding convertible

debentures, up to a level of 50% of gross asset value. Further,

the REIT is permitted to have indebtedness and convertible

debentures up to a level of 60% of gross asset value. InnVest

calculates indebtedness in accordance with GAAP excluding

non-interest bearing indebtedness, trade accounts payable,

and any future income tax liability. InnVest calculates gross

asset value as the total book value of assets on the REIT’s

balance sheet, plus the accumulated depreciation and

amortization, less any future income tax liabilities.

At March 31, 2009, the REIT’s leverage excluding

and including convertible debentures was 47.7%

(December 31, 2008 – 47.2%) and 57.0%

(December 31, 2008 – 56.5%), respectively.

Total assets per

Consolidated balance sheet $ 1,952,900

Accumulated depreciation

and amortization 295,696

Future income tax liability (204,046)

Future income tax liability

not included in assets 18,695

Gross asset value $ 2,063,245

Book value of mortgages

and other indebtedness1 $ 984,494 47.7%

Convertible debentures2 190,744 9.3%

Total debt $ 1,175,238 57.0%

1. Adjusted to eliminate financing issuance costs and include long-term debt

related to assets held for sale.

2. Adjusted to face value.

Long-term capital obligationsThe REIT’s long-term capital obligations consist primarily

of fixed-term mortgage financing and unsecured debentures.

The maturity dates for these obligations have been staggered

to lower the overall refinancing risk. The estimated interest

payments on mortgage debt and convertible debentures

include scheduled interest payments on fixed and variable rate

debt outstanding at March 31, 2009. The estimated interest

payment on variable rate mortgages is based on interest rates

prevailing at March 31, 2009.

Considering its overall leverage and demonstrated historical

access to capital markets, InnVest expects that all maturities

will be refinanced or repaid in the normal course of business.

InnVest has no mortgage maturities until mid-2010. In the

first quarter of 2009, the REIT successful extended the term

of two mortgages totalling $13.5 million which were originally

scheduled to mature in February 2010. One mortgage of

$6.9 million was extended to September 30, 2012, while

the second mortgage of $6.6 million was extended to

December 31, 2012 at a weighted average interest rate of

approximately 6.8% compared to the previous rate of 6.2%.

Following this extension, approximately $177.9 million in

mortgage debt with an average interest rate of 5.6% matures

in 2010. This debt represents one maturity with a large

Canadian institutional lender. Forty limited service hotels serve

as collateral on this debt. Mortgage maturities in 2011

approximate $321.5 million with an average interest rate

of 5.5%. This is made up of two separate maturities of

approximately $268.0 million and $53.5 million, both with a

large Canadian institutional lender. The $268.0 million maturity

includes two one-year extensions, at the REIT’s option, subject

to certain minimum thresholds at the time of maturity. In

aggregate, nine full service hotels serve as collateral on the

mortgages which mature in 2011. As at March 31, 2009, these

2010 and 2011 maturities are supported by strong debt

service coverage. InnVest’s outstanding Series A debentures

of $45.8 million also matures in April 2011. The REIT has

approximately $141.7 million of mortgages payable secured

by conduit financing with the relevant maturities in 2014

and beyond.

The REIT has leasehold interests in 13 of its hotels. The

leaseholds require minimum annual average lease payments

and expire between 2017 and 2088. There are also future

rental charges determined as a percentage of revenue that

are not included in the amounts reflected below. Capital

and operating leases primarily relate to equipment and

office leases.

In addition, capital expenditures committed, and yet to be

incurred, at March 31, 2009 approximated $405.

14 innVest real estate inVestment trust

management’s discussion and analysis

Remainder of 2014 and

2009 2010 2011 2012 2013 thereafter Total

Bank indebtedness – principal 9,000 – – – – – 9,000

Bank indebtedness – interest 94 – – – – – 94

Mortgages payable – principal 8,449 179,240 328,451 23,399 11,355 394,501 945,395

Mortgages payable – interest 41,187 50,229 28,066 25,385 23,956 17,612 186,435

Capital lease – principal 195 203 213 242 225 1,269 2,347

Capital lease – interest 176 239 239 239 239 60 1,192

Convertible debentures –

principal – – 45,764 – 74,980 70,000 190,744

Convertible debentures –

interest 9,408 11,455 10,025 8,595 6,345 4,095 49,923

Long-term land leases 3,670 4,945 4,492 4,492 4,492 89,933 112,024

Operating equipment

and office leases 473 392 172 50 35 – 1,122

72,652 246,703 417,422 62,402 121,627 577,470 1,498,276

Overall, the Trust has no significant current debt maturities,

minimal floating rate debt and appropriate leverage for its real

estate class. The Trust also has access to a credit facility to

fund short term fluctuations in earnings. If necessary, near

term disruptions to operating earnings and cash flow could

be addressed through reductions in discretionary capital

allocation decisions such as capital investments above the

FF&E reserve and/or distributions. Based on the current level

of distributions and current units outstanding, annual

distributions approximate $56 million. The Trust could also

generate liquidity through asset sales. At March 31, 2009,

six assets are classified as held for sale, one of which was

disposed of subsequent to the end of the first quarter of 2009.

As a result, management does not expect the current global

credit market environment to have a material impact on the

Trust’s ability to fund its commitments.

Distributions to unitholdersFor the three months ended March 31, 2009, the REIT

declared distributions of $14.0 million, of which $660,

was distributed in units as part of the DRIP. This represents

distributions declared of $0.1875 per unit, compared to

$0.28125 per unit for the first quarter of 2008. For the

twelve months ended March 31, 2009, InnVest’s payout

ratio was 87.5%, or 75.3% on a cash basis (excluding

the non-cash distributions made through the DRIP). This

payout ratio compares to a 91.7% annual payout for the year

ended December 31, 2008. The improved payout ratio reflects

the reduced level of distributions which offset the weaker hotel

operating environment.

In November 2008, the Trust announced a reduction in its

monthly distribution to $0.0625 per month, or $0.75 per unit

annually. This represented a one third reduction from annual

distributions of $1.125 per unit that had been paid since the

Trust’s inception in 2002. The reduction was implemented

based on the Board of Trustees’ decision to take a prudent

approach to distributions in light of current uncertain economic

conditions. The distribution reduction will enable InnVest to

conserve approximately $28 million annually and will help

enhance the REIT’s balance sheet and liquidity during the

current challenging credit environment. Based on current

market conditions, management expects the current level of

cash distributions to be sustainable. However, the potential

deterioration of business trends could impact future

distributions paid.

Liquidity to fund distributions is generated from cash flow

from operations, cash on hand, available bank operating

lines and by the ability to finance certain unencumbered or

under-leveraged assets. First and fourth quarter distributions

are typically partially funded through bank operating lines

given the seasonality of earnings through the year in contrast

to fixed costs.

Since 2006, the REIT’s annual distributions have been fully

funded by distributable income generated by the Trust.

first quarter report 2009 15

management’s discussion and analysis

12 months

ended

March 31, Years ended December 31

2009 2008 2007 2006 2005

Distributable income $ 82,059 $ 85,540 $ 71,995 $ 62,771 $ 48,721

Distributions 71,811 78,473 70,758 59,605 52,884

Distributable income in excess

of (less than) distributions 10,248 7,067 1,237 3,166 (4,163)

Non-cash distributions made

through the DRIP 10,021 13,234 10,606 4,166 3,303

Distributable income in excess

of (less than) cash distributions $ 20,269 $ 20,301 $ 11,843 $ 7,332 $ (860)

Payout ratios:

Total distributions 87.5% 91.7% 98.3% 95.0% 108.5%

Cash distributions (total

distributions minus DRIP) 75.3% 76.3% 83.6% 88.3% 101.8%

The REIT is required to pay distributions of not less than 80%

of the annual distributable income equally on a monthly basis.

Distributions to unitholders are approved by the REIT’s Board

of Trustees. In exercising their discretion to approve the level

of distributions, the Trustees use forecasts prepared by

management and other financial information to determine if

sufficient cash flow will be available to fund distributions. Such

financial information is subject to change due to the nature of

the Canadian hotel industry which can be difficult to predict,

even in the short-run (see Risks and Uncertainties).

Unit informationAt March 31, 2009, a total of 74,434,338 units of the REIT were outstanding. There is only one class of trust units, with each unit

eligible for one vote.

2009 2008

Units outstanding, January 1 74,412,317 73,000,694

Dividend reinvestment plan 202,067 427,230

Executive compensation plan 19,052 16,033

Trustee compensation plan 11,060 3,711

Conversion of debentures 1,342 –

Trust units cancelled pursuant to normal course issuer bid (211,500) –

Units outstanding, March 31 74,434,338 73,447,668

Commencing on November 11, 2008, InnVest initiated a

normal course issuer bid (“NCIB”) to purchase up to 5,924,617

trust units, representing approximately 10% of InnVest’s public

float. The NCIB expires on November 10, 2009. Under the

NCIB, units purchased will be cancelled. InnVest believes that

the market price of its units at certain times may be attractive

and that the purchase of units from time to time would be an

appropriate use of InnVest’s funds.

16 innVest real estate inVestment trust

management’s discussion and analysis

InnVest issues additional units each month through its DRIP.

Given its desire to conserve liquidity, to date, the REIT has

limited its NCIB purchases to satisfy those units issued

through the DRIP as to minimize their dilutive effect.

During the first quarter of 2009, the Trust purchased and

cancelled 211,500 trust units under the NCIB at an aggregate

cost of $689 (average cost of $3.26 per unit). Subsequent

to March 31, 2009, InnVest purchased and cancelled an

additional 70,000 units at an aggregate cost of $245 (average

cost of $3.49 per unit). In aggregate since implementing the

NCIB, the REIT has acquired 560,000 units at an aggregate

cost of $1.9 million (average cost of $3.34).

A total of $45.8 million of the Series A – 6.25% Debentures

remained outstanding at March 31, 2009. These debentures

are convertible into trust units at a strike price of $12.50,

bear interest at 6.25% per annum payable semi-annually on

April 15 and October 15 of each year and are due April 15, 2011.

At March 31, 2009, the trust units to be issued upon

conversion of the Series A – 6.25% Debentures are 3,661,120.

A total of $75.0 million of the Series B – 6.00% Debentures

remained outstanding at March 31, 2009. The Series B –

6.00% Debentures are convertible into trust units at a strike

price of $14.90, bear interest at 6.00% per annum payable

semi-annually on May 31 and November 30 of each year and

are due May 31, 2013. During the quarter, $20 convertible

debentures were converted into 1,342 units. At March 31, 2009,

the trust units to be issued upon conversion of the Series B –

6.00% Debentures total 5,032,215.

A total of $70.0 million of Series C – 5.85% Debentures

remained outstanding at March 31, 2009. These debentures

are convertible into trust units at a strike price of $14.70,

bear interest at 5.85% per annum payable semi-annually

on August 1 and February 1 of each year and are due

August 1, 2014. At March 31, 2009, the trust units to be

issued upon conversion of the Series C – 5.85% Debentures

total 4,761,905.

For each of its Series A, Series B and Series C debentures,

the REIT may elect, from time to time, to satisfy its obligation

to pay interest by delivering trust units. Also, for each of its

Series A, Series B and Series C debentures, the REIT may,

at its option, on not more than 60 days’ and not less than

30 days’ prior notice and subject to applicable regulatory

approval, elect to satisfy its obligation to repay all or any

option of the principal amount of the Series A, Series B and

Series C Debentures that are to be redeemed or that are to

mature, by issuing trust units. The number of trust units to be

issued in respect of each debenture will be determined by

dividing the principal amount by 95% of the volume-weighted

average trading price of the trust units on the Toronto Stock

Exchange for the 20 consecutive trading days ending on the

fifth trading day preceding the date fixed for redemption or

maturity, as the case may be.

At March 31, 2009, there were 81,922 (December 31, 2008 –

71,003) unvested executive units granted under the executive

compensation plan. Units granted vest equally on the third and

fourth anniversary of the effective date of grant.

On October 9, 2008, the REIT adopted a unitholder rights

plan, which expired April 9, 2009. On April 14, 2009,

unitholders of the REIT approved the adoption of the second

amended and restated unitholder rights plan, which will be

in effect for a period up to three years. InnVest did not adopt

either of the plans in response to any specific take-over

proposal, nor has it been made aware of any such proposal.

A unitholder right plan is intended to ensure that unitholders

receive fair treatment in the event of an unsolicited attempt

to gain control of InnVest and, in such event, to ensure

unitholders receive full value and that the Board of Trustees

has time to consider alternatives to maximize unitholder value.

The rights will only become exercisable upon the occurrence

of certain triggering events, including the acquisition by a

person or group of persons of 20% or more of the outstanding

units in a transaction not approved by InnVest’s Board

of Trustees.

Non-GAAP financial measuresIncluded in this MD&A are certain non-GAAP financial

measures, which are measures of InnVest’s historical or future

financial performance that are not calculated and presented in

accordance with GAAP. These non-GAAP financial measures

are unlikely to be comparable to similar measures presented

by other entities. The following discussion defines non-GAAP

measures used by InnVest and presents why management

believes they are useful supplemental measures of the

REIT’s performance.

Hotel operating incomeHOI is defined as hotel revenues less hotel expenses. HOI is a

commonly used measure by lodging real estate owners which,

when considered with GAAP measures, gives management a

more complete understanding of property level results before

debt service. It also facilitates comparisons between InnVest

and its competitors. Management believes that HOI is

one of InnVest’s key performance indicators since it helps

management, lenders and investors evaluate the ongoing hotel

profitability. Management believes hotel operating income to

be a meaningful indicator of hotel performance.

first quarter report 2009 17

management’s discussion and analysis

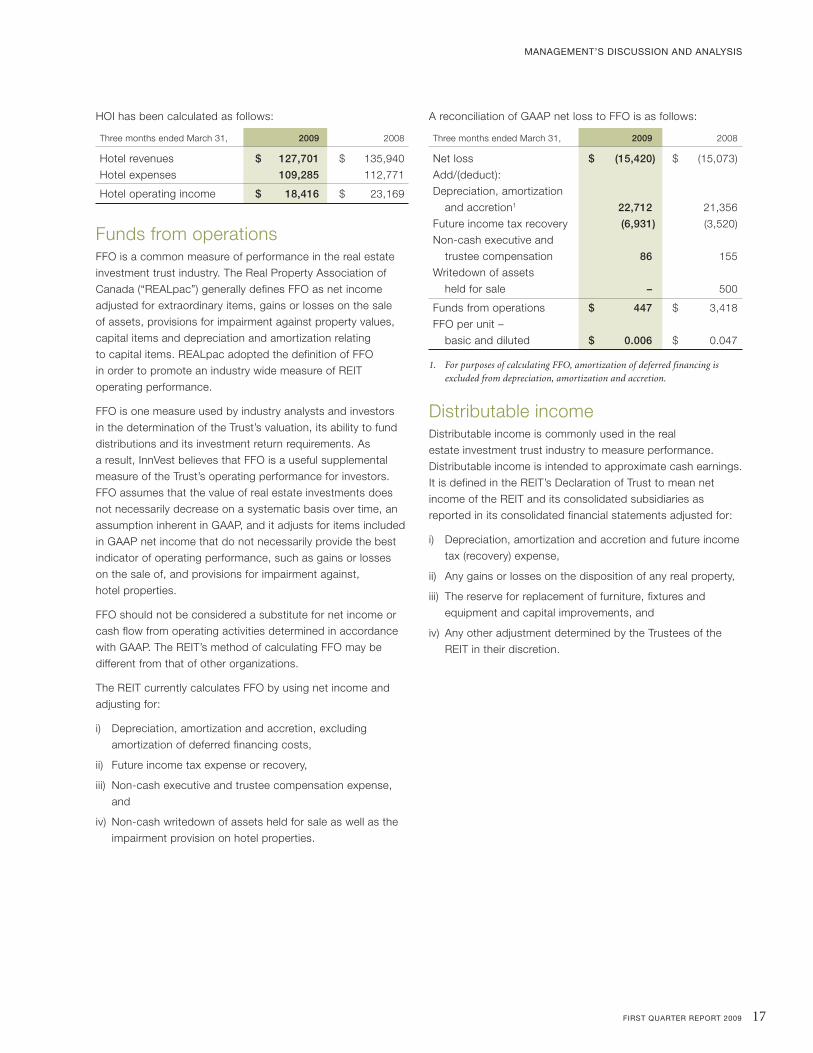

HOI has been calculated as follows:

Three months ended March 31, 2009 2008

Hotel revenues $ 127,701 $ 135,940

Hotel expenses 109,285 112,771

Hotel operating income $ 18,416 $ 23,169

Funds from operationsFFO is a common measure of performance in the real estate

investment trust industry. The Real Property Association of

Canada (“REALpac”) generally defines FFO as net income

adjusted for extraordinary items, gains or losses on the sale

of assets, provisions for impairment against property values,

capital items and depreciation and amortization relating

to capital items. REALpac adopted the definition of FFO

in order to promote an industry wide measure of REIT

operating performance.

FFO is one measure used by industry analysts and investors

in the determination of the Trust’s valuation, its ability to fund

distributions and its investment return requirements. As

a result, InnVest believes that FFO is a useful supplemental

measure of the Trust’s operating performance for investors.

FFO assumes that the value of real estate investments does

not necessarily decrease on a systematic basis over time, an

assumption inherent in GAAP, and it adjusts for items included

in GAAP net income that do not necessarily provide the best

indicator of operating performance, such as gains or losses

on the sale of, and provisions for impairment against,

hotel properties.

FFO should not be considered a substitute for net income or

cash flow from operating activities determined in accordance

with GAAP. The REIT’s method of calculating FFO may be

different from that of other organizations.

The REIT currently calculates FFO by using net income and

adjusting for:

i) Depreciation, amortization and accretion, excluding

amortization of deferred financing costs,

ii) Future income tax expense or recovery,

iii) Non-cash executive and trustee compensation expense,

and

iv) Non-cash writedown of assets held for sale as well as the

impairment provision on hotel properties.

A reconciliation of GAAP net loss to FFO is as follows:

Three months ended March 31, 2009 2008

Net loss $ (15,420) $ (15,073)

Add/(deduct):

Depreciation, amortization

and accretion1 22,712 21,356

Future income tax recovery (6,931) (3,520)

Non-cash executive and

trustee compensation 86 155

Writedown of assets

held for sale – 500

Funds from operations $ 447 $ 3,418

FFO per unit –

basic and diluted $ 0.006 $ 0.047

1. For purposes of calculating FFO, amortization of deferred financing is

excluded from depreciation, amortization and accretion.

Distributable incomeDistributable income is commonly used in the real

estate investment trust industry to measure performance.

Distributable income is intended to approximate cash earnings.

It is defined in the REIT’s Declaration of Trust to mean net

income of the REIT and its consolidated subsidiaries as

reported in its consolidated financial statements adjusted for:

i) Depreciation, amortization and accretion and future income

tax (recovery) expense,

ii) Any gains or losses on the disposition of any real property,

iii) The reserve for replacement of furniture, fixtures and

equipment and capital improvements, and

iv) Any other adjustment determined by the Trustees of the

REIT in their discretion.

18 innVest real estate inVestment trust

management’s discussion and analysis

Distributable income is one measure used by industry analysts

in the determination of the Trust’s per unit value, the ability

of the Trust to fund distributions and investment returns for

current or potential investors. As outlined in the Declaration of

Trust, the REIT is required to distribute monthly to unitholders

not less than one-twelfth of 80% of the estimated annualized

distributable income of the Trust for the calendar year.

Distributable income is not only used by management and

the Board of Trustees to determine the level of distributions

to unitholders, it also serves as an important measure

for investors in their evaluation of the performance

of management.

In addition, when evaluating acquisition opportunities, the

distributable income to be generated by the asset is reviewed

by management to determine whether a proposed acquisition

will generate an increase in distributable income per unit.

Therefore, distributable income is an important measure for

management as a guideline through which operating and

financial decisions are made and is an integral part of the

investment decision for investors and potential investors.

A reconciliation of GAAP net loss to distributable loss is as follows:

Three months ended March 31, 2009 2008

Net loss $ (15,420) $ (15,073)

Add/(deduct):

Depreciation and amortization 22,712 21,356

Future income tax recovery (6,931) (3,520)

FF&E Reserve (5,427) (5,848)

Non-cash portion of convertible debenture interest and accretion 784 578

Non-cash portion of mortgage interest expense 424 258

Non-cash executive and trustee compensation 86 155

Writedown of assets held for sale – 500

Amortization of deferred financing costs 17 1,314

Deferred land lease expense and retail lease income, net 2 8

Distributable loss $ (3,753) $ (272)

Distributable loss per unit – basic and diluted $ (0.050) $ (0.004)

The following table reconciles cash flows from operating activities to distributable loss in accordance with Canadian Securities

Administrators Staff Notice 41-201 Income Trusts and Other Indirect Offerings. Management considers distributable cash to be

equivalent to distributable income. The reconciliation has been prepared using reasonable and supportable assumptions which

reflect the REIT’s planned courses of action given management’s judgment about the most probable set of economic conditions.

Three months ended March 31, 2009 2008

Reconciliation of cash flow from operating activities to distributable loss

Cash flow from operating activities $ (2,185) $ (461)

Changes in non-cash working capital 3,562 6,152

Miscellaneous, including changes in non-cash working capital – discontinued operations 295 (123)

Deferred land lease expense and retail lease income, net 2 8

FF&E reserve (5,427) (5,848)

Distributable loss $ (3,753) $ (272)

first quarter report 2009 19

management’s discussion and analysis

Risks and uncertaintiesAll real estate investments are subject to a degree of risk.

The achievement of the REIT’s objectives is, in part, dependent

on successful mitigation of business risks. The following is

a discussion of some, but not all, of the risks which may

influence the REIT’s performance. Readers should also refer

to InnVest’s Annual Information Form, which is available on

SEDAR, for a more detailed discussion of risks.

Operating risksInnVest is subject to the normal operating risks consistent with

hotel ownership. The following is a discussion of key risks and

uncertainties facing the Trust on a day-to-day basis, and the

strategies adopted to mitigate such risks. The REIT has risk

management processes in place as well as restrictions,

limitations and policies placed upon it by its Declaration of

Trust. However, it should not be assumed that the following

discussion is exhaustive or that the strategies adopted to

mitigate these risks will be effective.

The REIT is subject to the operating risks inherent in the

Canadian hotel industry, including:

p Cyclical downturns arising from changes in general and local

economic conditions;

p Competition from other hotels;

p Seasonal fluctuations in hotel operating income generated

throughout the year;

p Changes in wages, prices, energy costs and construction

and maintenance costs that might result from inflation,

government regulation, changes in interest rates or

currency fluctuations;

p Changes in the level of business and commercial travel

and tourism;

p The recurring need for renovation, refurbishment and

improvement of hotel properties;

Related party transactionsFranchise businessInnVest owns 50% of CHC. The other 50% is owned by