Forward and Futures

65

Forward and Futures Adler Haymans Manurung Guru Besar Pasar Modal dan Perbankan FE Universitas Bina Nusantara Advisor PT Bursa Berjangka Jakarta

-

Upload

iwan-suryadi -

Category

Economy & Finance

-

view

268 -

download

6

Transcript of Forward and Futures

Forward and Futures

Adler Haymans Manurung

Guru Besar Pasar Modal dan Perbankan

FE Universitas Bina Nusantara

Advisor PT Bursa Berjangka Jakarta

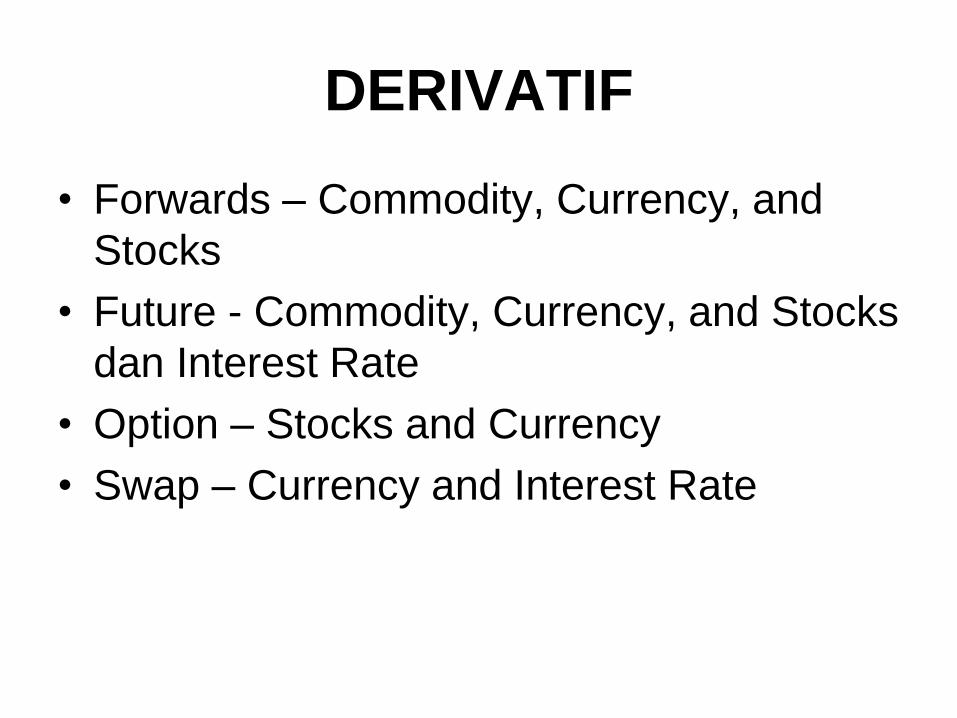

DERIVATIF

• Forwards – Commodity, Currency, and

Stocks

• Future - Commodity, Currency, and Stocks

dan Interest Rate

• Option – Stocks and Currency

• Swap – Currency and Interest Rate

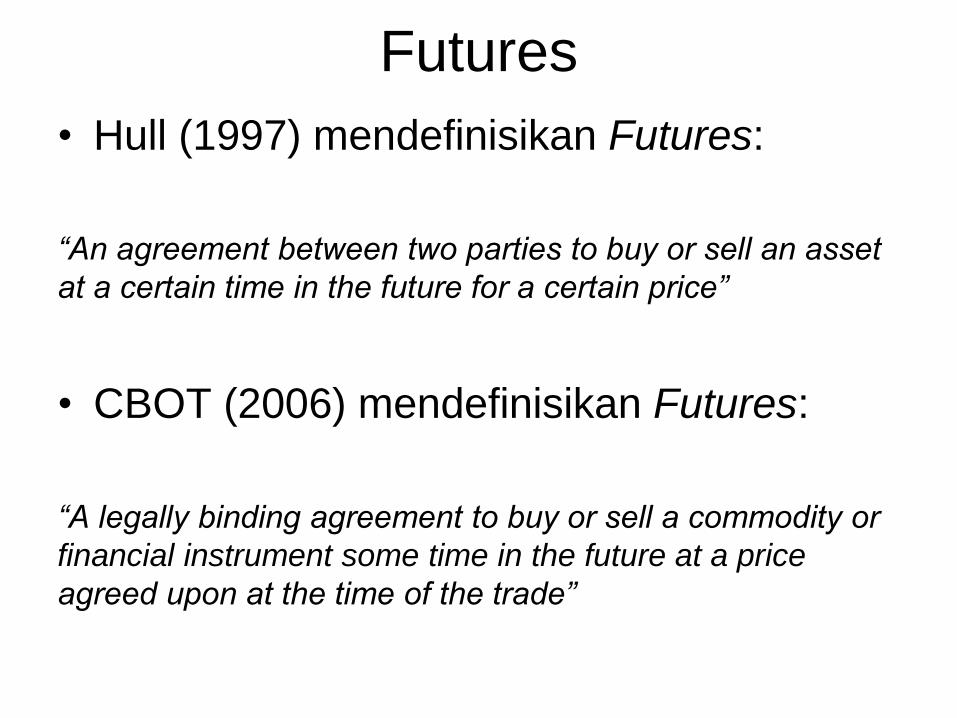

Futures

• Hull (1997) mendefinisikan Futures:

“An agreement between two parties to buy or sell an asset

at a certain time in the future for a certain price”

• CBOT (2006) mendefinisikan Futures:

“A legally binding agreement to buy or sell a commodity or

financial instrument some time in the future at a price

agreed upon at the time of the trade”

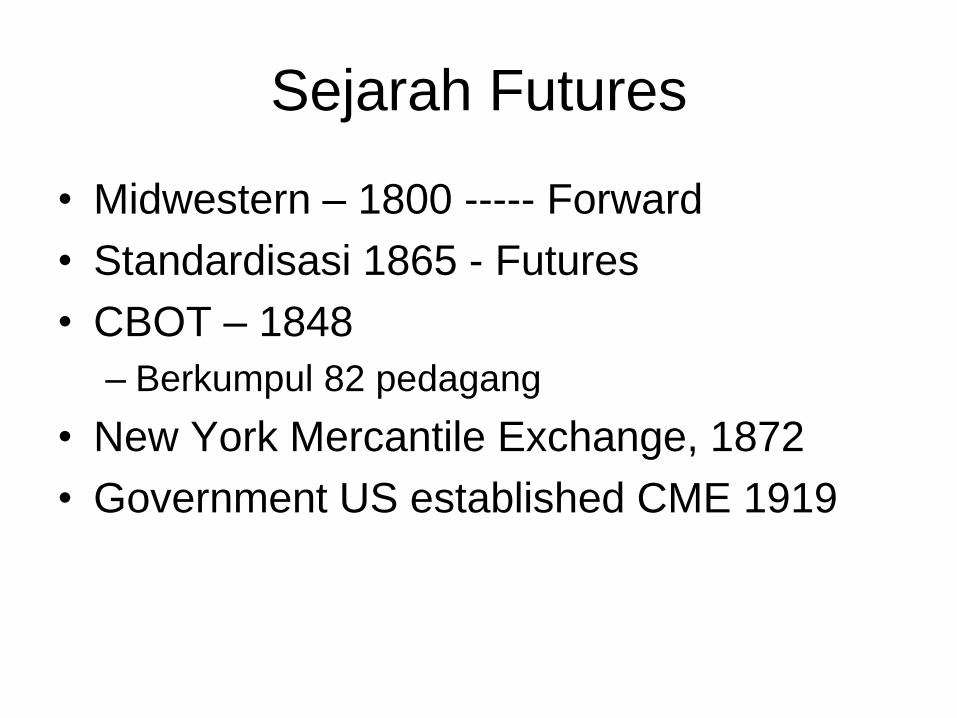

Sejarah Futures

• Midwestern – 1800 ----- Forward

• Standardisasi 1865 - Futures

• CBOT – 1848

– Berkumpul 82 pedagang

• New York Mercantile Exchange, 1872

• Government US established CME 1919

Forwards

• Contract between two parties at specific

on certain date

• Non Bourse – Non regulated

• Delivery System – depend on contract

Futures

• Contract between two parties at specific

on certain date

• Bourse – Regulated

• Clearing Settlement

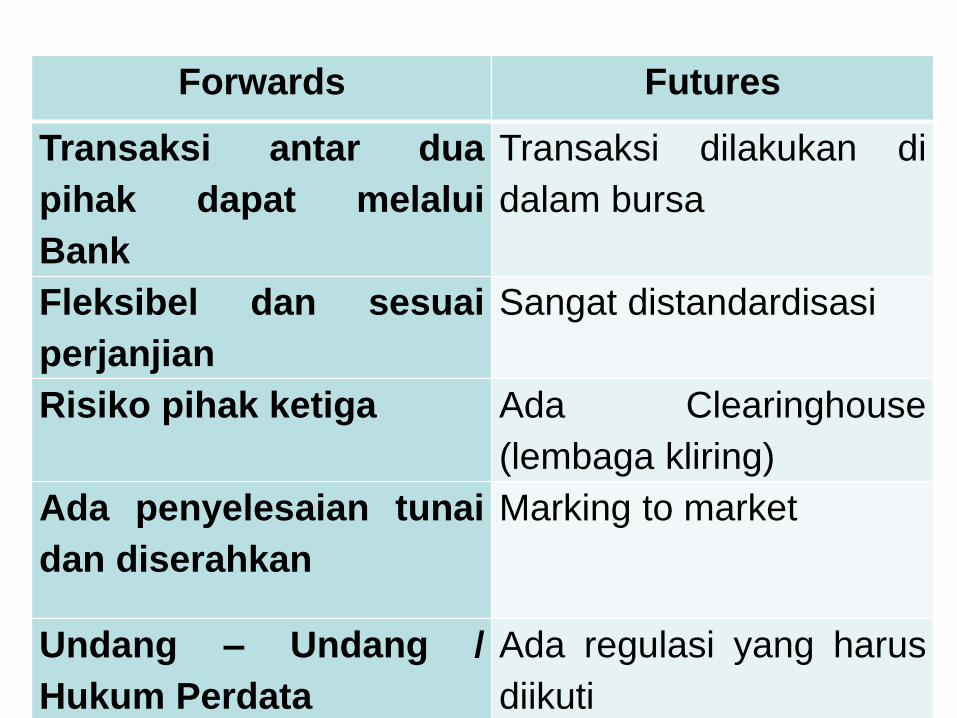

Forwards Futures

Transaksi antar dua

pihak dapat melalui

Bank

Transaksi dilakukan di

dalam bursa

Fleksibel dan sesuai

perjanjian

Sangat distandardisasi

Risiko pihak ketiga Ada Clearinghouse

(lembaga kliring)

Ada penyelesaian tunai

dan diserahkan

Marking to market

Undang – Undang /

Hukum Perdata

Ada regulasi yang harus

diikuti

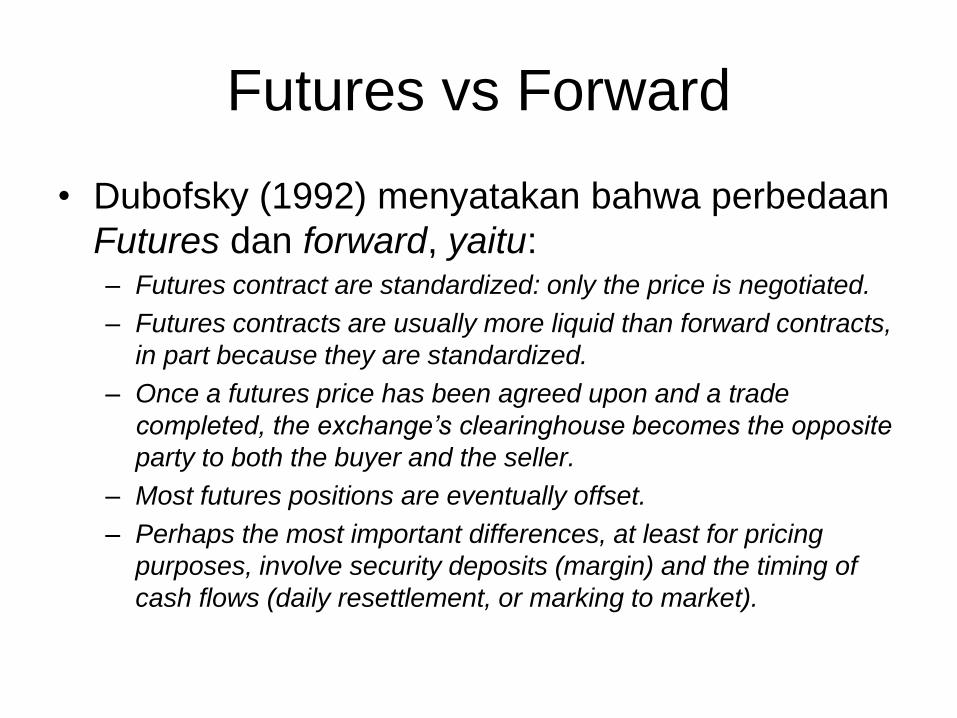

Futures vs Forward

• Dubofsky (1992) menyatakan bahwa perbedaan

Futures dan forward, yaitu: – Futures contract are standardized: only the price is negotiated.

– Futures contracts are usually more liquid than forward contracts,

in part because they are standardized.

– Once a futures price has been agreed upon and a trade

completed, the exchange’s clearinghouse becomes the opposite

party to both the buyer and the seller.

– Most futures positions are eventually offset.

– Perhaps the most important differences, at least for pricing

purposes, involve security deposits (margin) and the timing of

cash flows (daily resettlement, or marking to market).

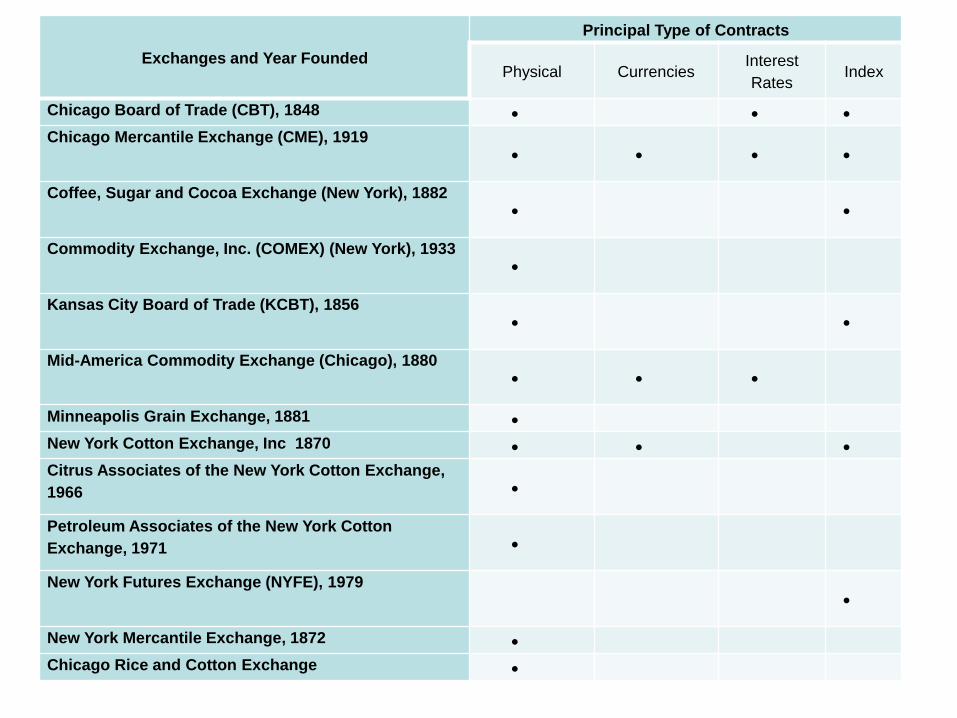

Exchanges and Year Founded

Principal Type of Contracts

Physical Currencies Interest

Rates Index

Chicago Board of Trade (CBT), 1848

Chicago Mercantile Exchange (CME), 1919

Coffee, Sugar and Cocoa Exchange (New York), 1882

Commodity Exchange, Inc. (COMEX) (New York), 1933

Kansas City Board of Trade (KCBT), 1856

Mid-America Commodity Exchange (Chicago), 1880

Minneapolis Grain Exchange, 1881

New York Cotton Exchange, Inc 1870

Citrus Associates of the New York Cotton Exchange,

1966

Petroleum Associates of the New York Cotton

Exchange, 1971

New York Futures Exchange (NYFE), 1979

New York Mercantile Exchange, 1872

Chicago Rice and Cotton Exchange

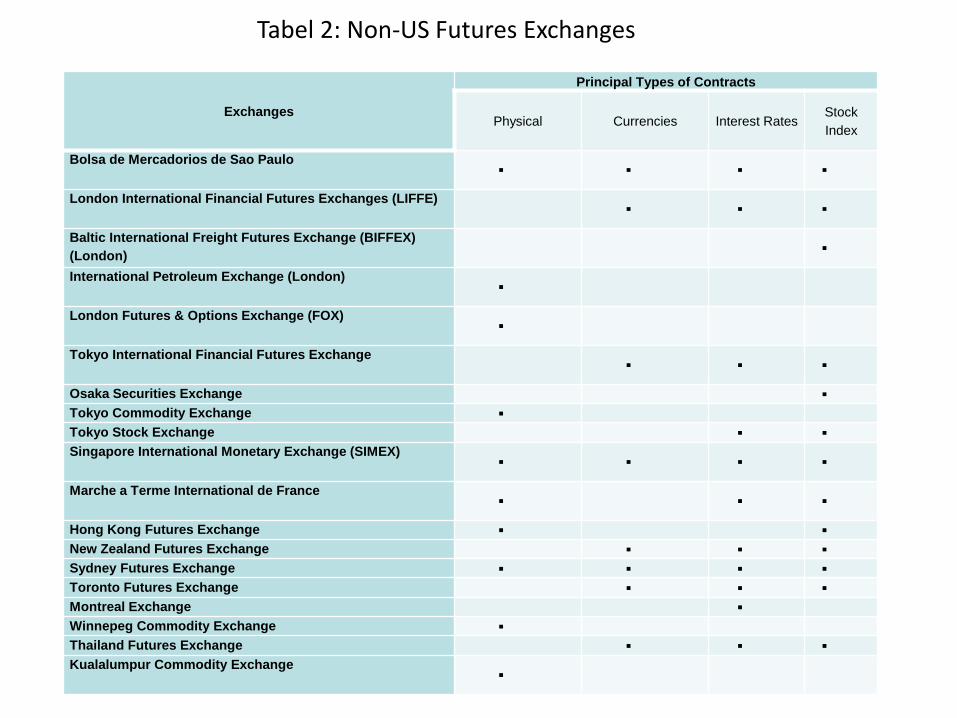

Exchanges

Principal Types of Contracts

Physical Currencies Interest Rates Stock

Index

Bolsa de Mercadorios de Sao Paulo

London International Financial Futures Exchanges (LIFFE)

Baltic International Freight Futures Exchange (BIFFEX)

(London)

International Petroleum Exchange (London)

London Futures & Options Exchange (FOX)

Tokyo International Financial Futures Exchange

Osaka Securities Exchange

Tokyo Commodity Exchange

Tokyo Stock Exchange

Singapore International Monetary Exchange (SIMEX)

Marche a Terme International de France

Hong Kong Futures Exchange

New Zealand Futures Exchange

Sydney Futures Exchange

Toronto Futures Exchange

Montreal Exchange

Winnepeg Commodity Exchange

Thailand Futures Exchange

Kualalumpur Commodity Exchange

Tabel 2: Non-US Futures Exchanges

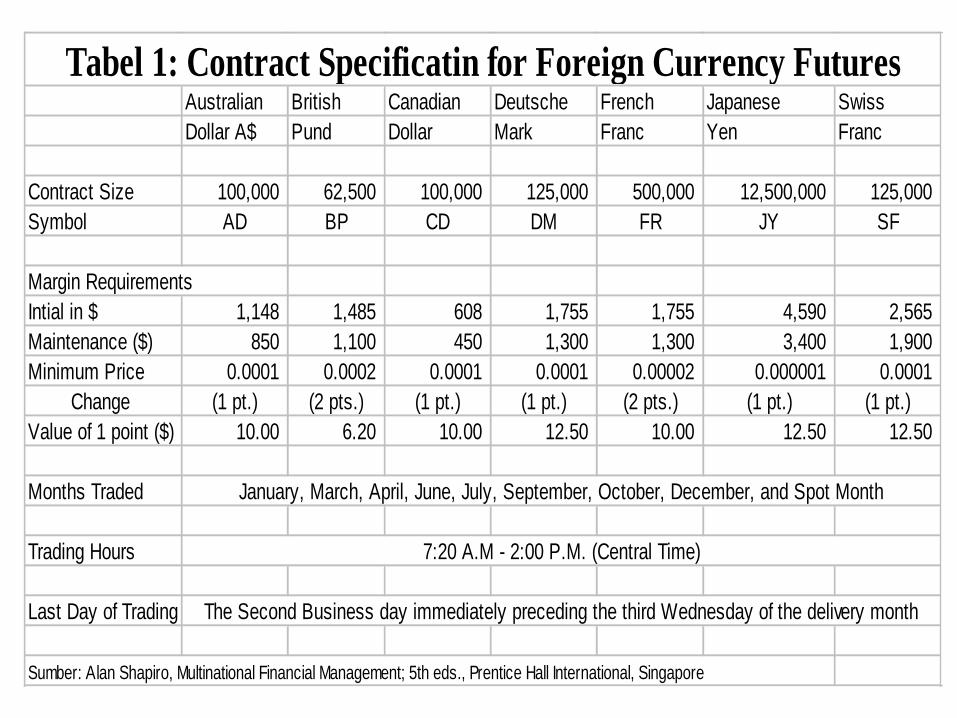

Australian British Canadian Deutsche French Japanese Swiss

Dollar A$ Pund Dollar Mark Franc Yen Franc

Contract Size 100,000 62,500 100,000 125,000 500,000 12,500,000 125,000

Symbol AD BP CD DM FR JY SF

Margin Requirements

Intial in $ 1,148 1,485 608 1,755 1,755 4,590 2,565

Maintenance ($) 850 1,100 450 1,300 1,300 3,400 1,900

Minimum Price 0.0001 0.0002 0.0001 0.0001 0.00002 0.000001 0.0001

Change (1 pt.) (2 pts.) (1 pt.) (1 pt.) (2 pts.) (1 pt.) (1 pt.)

Value of 1 point ($) 10.00 6.20 10.00 12.50 10.00 12.50 12.50

Months Traded

Trading Hours

Last Day of Trading

Sumber: Alan Shapiro, Multinational Financial Management; 5th eds., Prentice Hall International, Singapore

January, March, April, June, July, September, October, December, and Spot Month

7:20 A.M - 2:00 P.M. (Central Time)

The Second Business day immediately preceding the third Wednesday of the delivery month

Tabel 1: Contract Specificatin for Foreign Currency Futures

Bank Indonesia @ 2006

Market Participants

Hedgers

• Hedging is the opposite of speculation and describes the process

of managing the price risk inherent in a business by offsetting

that risk in the futures and options market. It can vary in

complexity from a relatively simple activity through to a highly

complex operation.

• Managing price risk means:

maintaining greater control of the cost of inputs or revenues

from sales, or both planning for the future based on assured

costs and revenues

• Eliminating concerns that a sharply adverse move in a metal's

price could turn an otherwise flourishing and efficient business into

a loss maker

• Example A copper mining firm may sell copper futures to fix a sale price today for future copper production. By selling the futures, the firm protects profit margins and sales revenues against a potential decline in the copper price thus offsetting the price risk in the futures market.

• Mutually compensatory movements in his cash and futures holdings should have cancelled out any change of price that occurred during the interval. If the grain price has dropped, the operator buys back the futures contract at less than the sale price, and the profit from doing so will be offset by the loss on the grain.

Market Participants

Bank Indonesia @ 2006

Bank Indonesia @ 2006

Market Participants

SPECULATORS

Speculators buy and sell futures and options contracts in an

effort to profit from price trends.

If speculators believe that prices will rise, they buy futures

contracts. If prices do indeed rise, the speculator profits by

selling the contract at the higher price. If prices fall, the

speculator stands to make a loss.

Typically, speculators have no desire to actually own the

physical commodity. They assume market price risk and

add liquidity and capital to the futures markets.

Types of Traders

• Commission Brokers – are following the instructions from their clients and charge a commission for doing so

• Locals – are trading for their own account

• Types of Speculators: – Scalpers – attempt to profit for small changes in

contract price (hold position only for minutes)

– Day Traders – hold their position for less than one trading day

– Position Traders – hold positions for much longer period of time

Bank Indonesia @ 2006

Market Participants

ARBITRAGEURS

• Arbitrage is the process of simultaneously buying and selling a

product in related markets to earn a risk-free profit.

• Arbitrageurs bridge the gap between the cash and futures market, by

maintaining the price relationship between the underlying physical

commodity and its futures market.

• Arbitrage in commodity futures markets takes the form of cash and

carry arbitrage.

• This exploits a situation where the price of a particular future is higher

than the spot price of the underlying commodity plus the costs of holding

the commodity until delivery, i.e, storage, insurance, interest costs, etc.

In this case, cash and carry arbitrage involves purchasing the underlying

physical commodity and simultaneously selling its corresponding futures

contract.

Bank Indonesia @ 2006

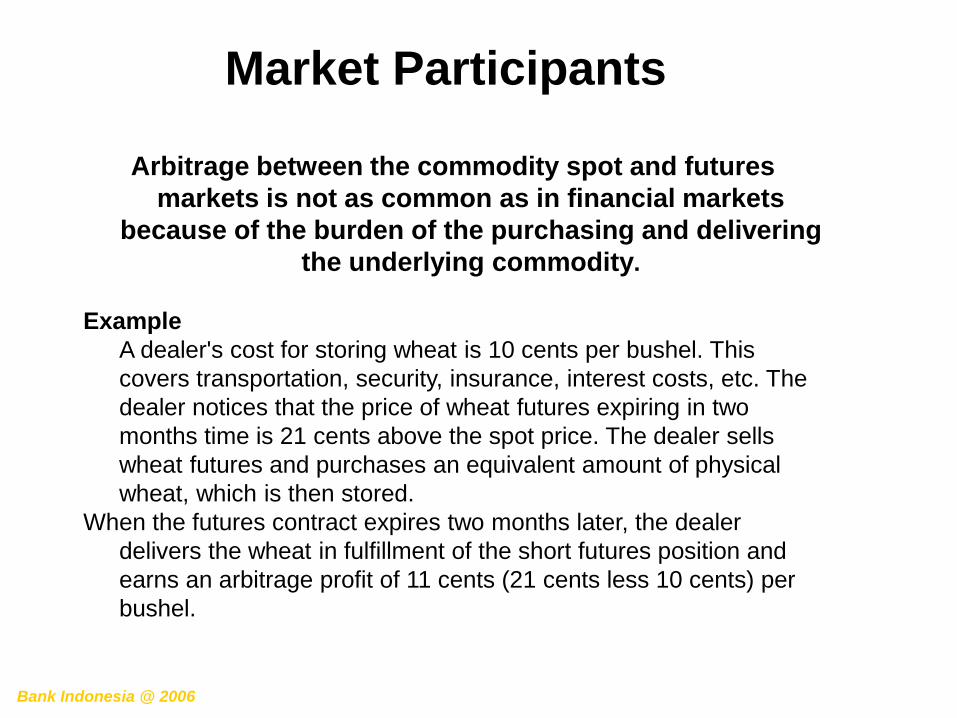

Market Participants

Arbitrage between the commodity spot and futures

markets is not as common as in financial markets

because of the burden of the purchasing and delivering

the underlying commodity.

Example

A dealer's cost for storing wheat is 10 cents per bushel. This

covers transportation, security, insurance, interest costs, etc. The

dealer notices that the price of wheat futures expiring in two

months time is 21 cents above the spot price. The dealer sells

wheat futures and purchases an equivalent amount of physical

wheat, which is then stored.

When the futures contract expires two months later, the dealer

delivers the wheat in fulfillment of the short futures position and

earns an arbitrage profit of 11 cents (21 cents less 10 cents) per

bushel.

Bank Indonesia @ 2006

Market Participants

The Hedgers pass off the risk of

price variation to the

Speculators, who is better able,

or at least more willing to bear

the risk

Hedgers Speculators

Risk

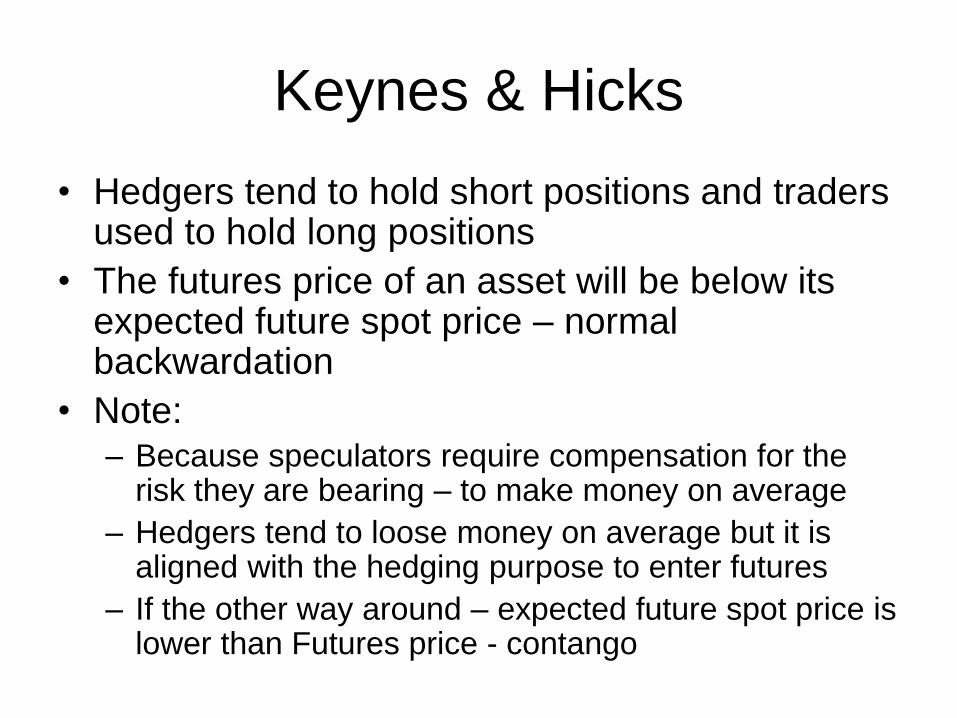

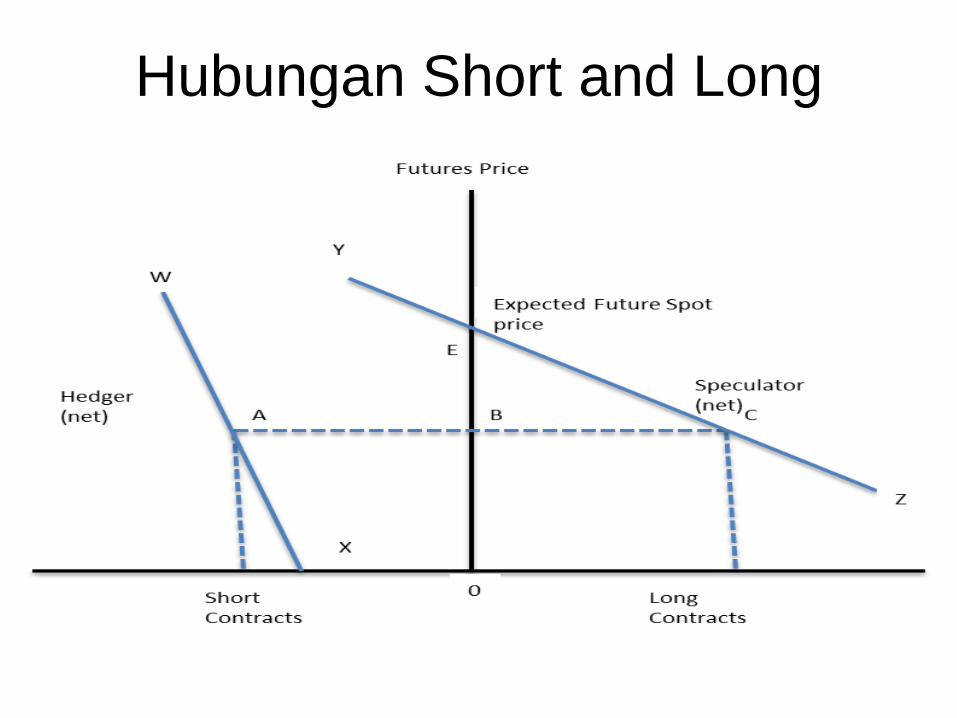

Keynes & Hicks

• Hedgers tend to hold short positions and traders used to hold long positions

• The futures price of an asset will be below its expected future spot price – normal backwardation

• Note: – Because speculators require compensation for the

risk they are bearing – to make money on average

– Hedgers tend to loose money on average but it is aligned with the hedging purpose to enter futures

– If the other way around – expected future spot price is lower than Futures price - contango

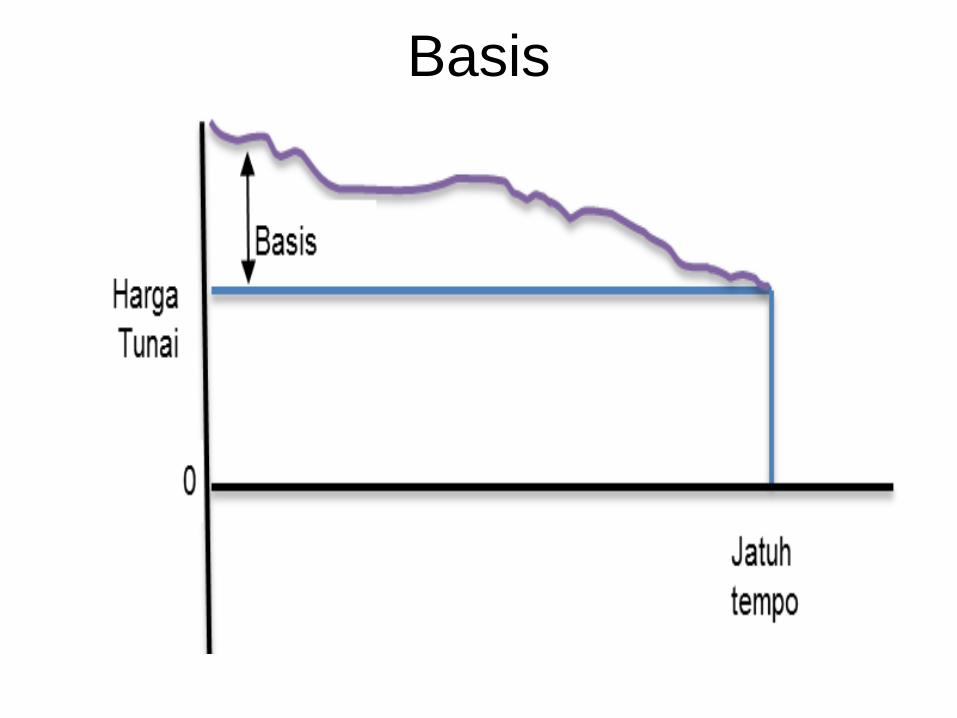

Hubungan Short and Long

Basis

Market Mechanics

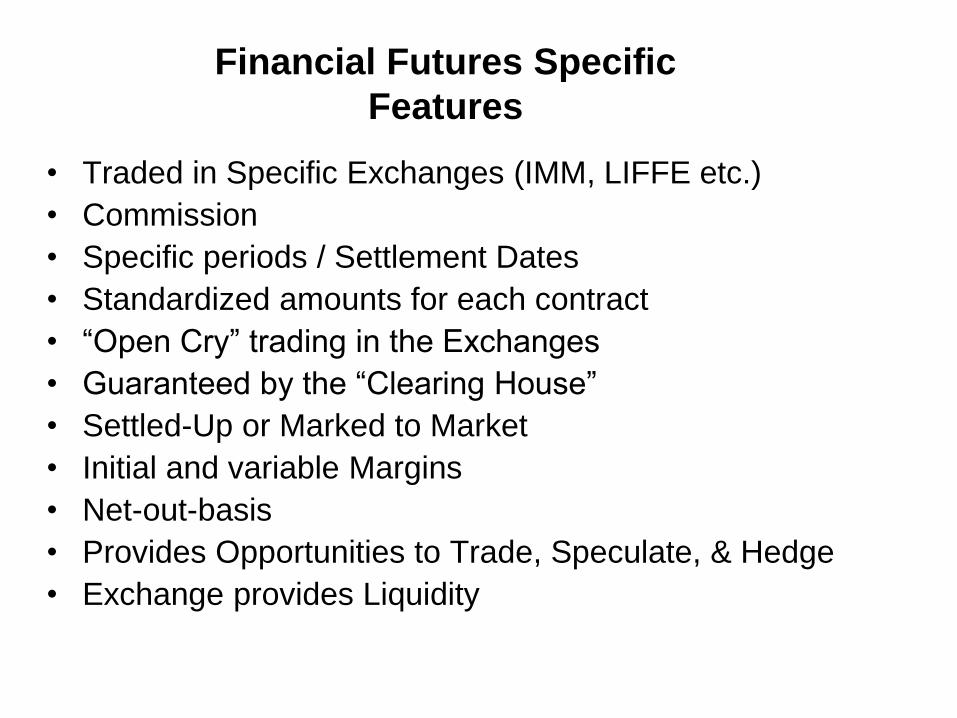

Financial Futures Specific

Features

• Traded in Specific Exchanges (IMM, LIFFE etc.)

• Commission

• Specific periods / Settlement Dates

• Standardized amounts for each contract

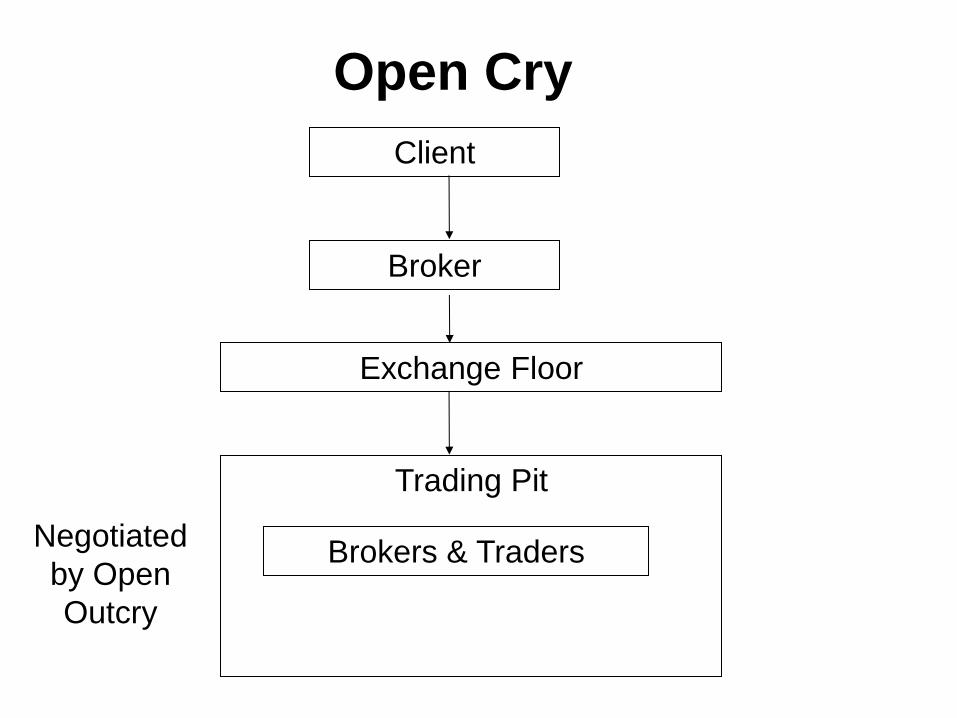

• “Open Cry” trading in the Exchanges

• Guaranteed by the “Clearing House”

• Settled-Up or Marked to Market

• Initial and variable Margins

• Net-out-basis

• Provides Opportunities to Trade, Speculate, & Hedge

• Exchange provides Liquidity

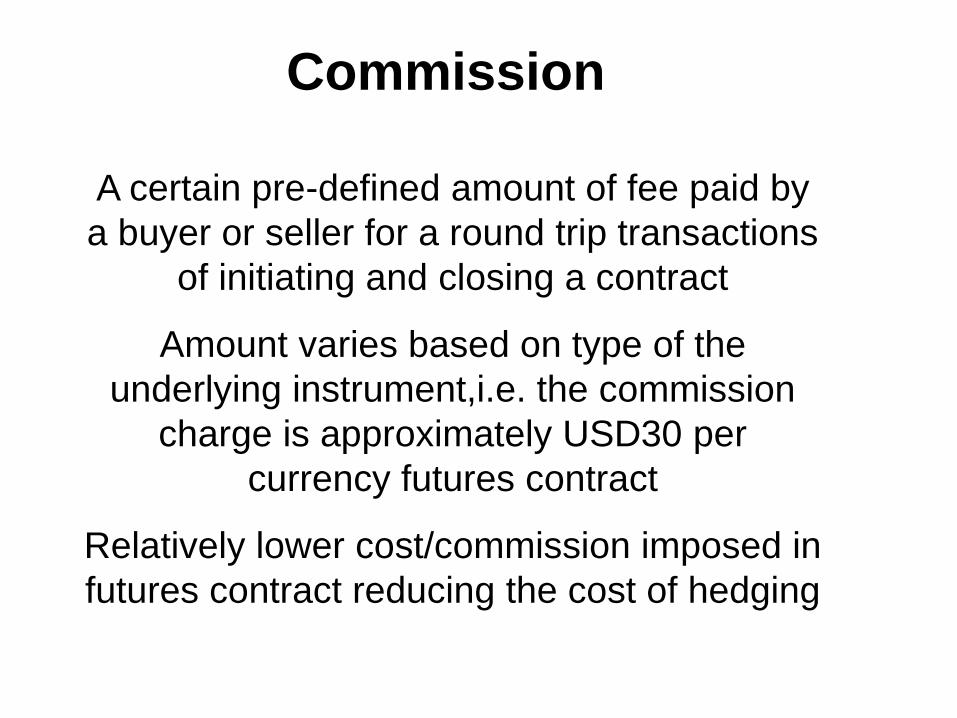

Commission

A certain pre-defined amount of fee paid by

a buyer or seller for a round trip transactions

of initiating and closing a contract

Amount varies based on type of the

underlying instrument,i.e. the commission

charge is approximately USD30 per

currency futures contract

Relatively lower cost/commission imposed in

futures contract reducing the cost of hedging

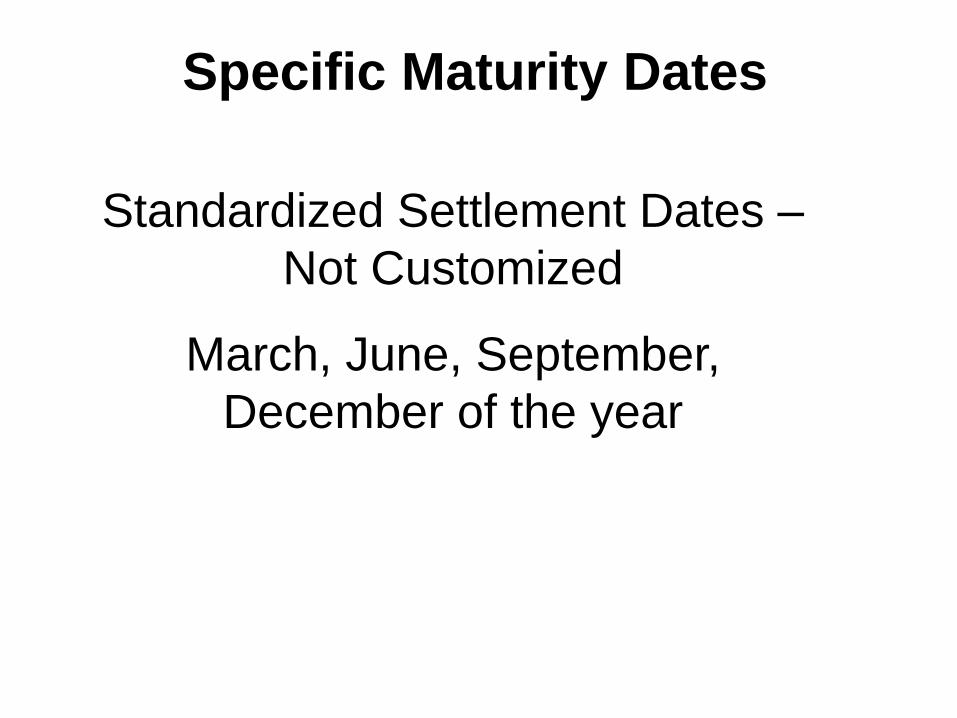

Specific Maturity Dates

Standardized Settlement Dates –

Not Customized

March, June, September,

December of the year

Standardized Amount

Standardized Contract Amount – Not

Customized (Exchange Traded Vs

OTC)

Position in multiple contracts might be

necessary to establish a hedge

Open Cry

Client

Broker

Exchange Floor

Trading Pit

Brokers & Traders Negotiated

by Open

Outcry

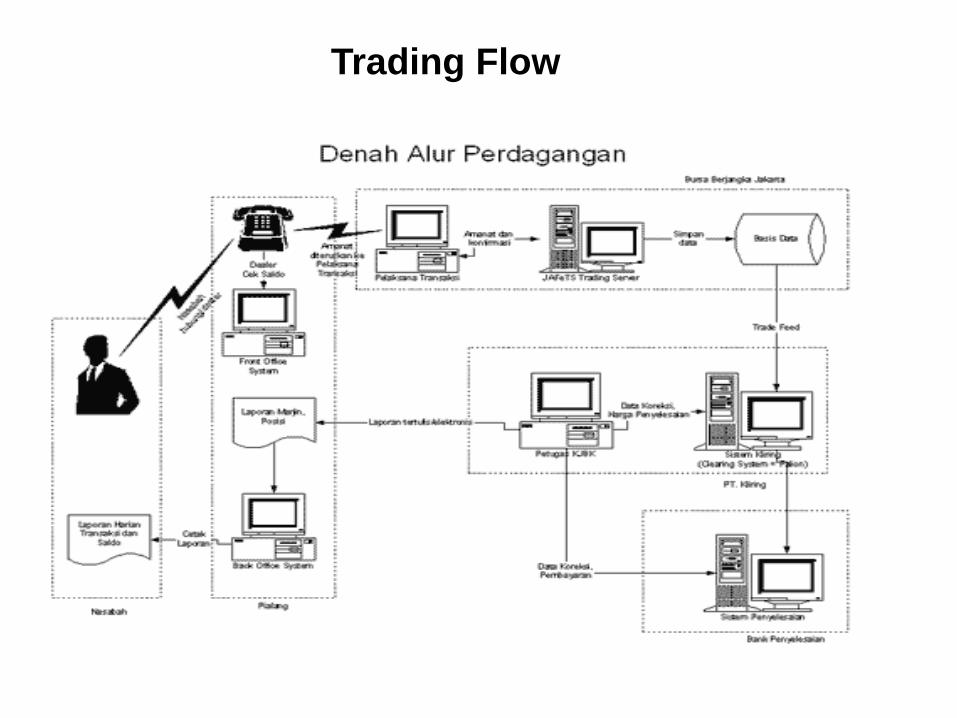

Trading Flow

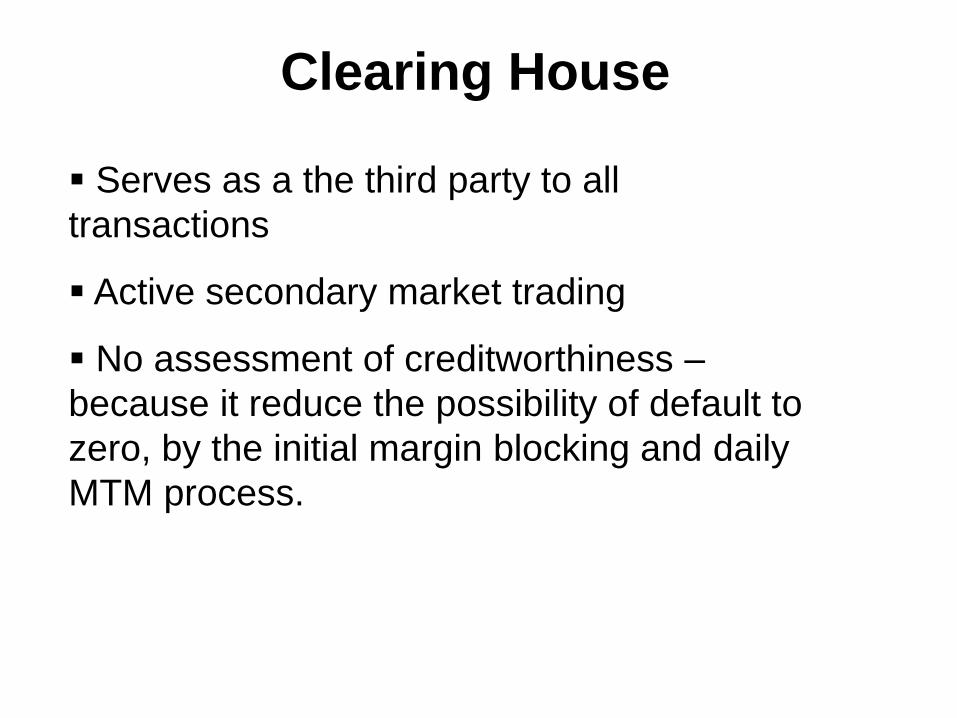

Clearing House

Serves as a the third party to all

transactions

Active secondary market trading

No assessment of creditworthiness –

because it reduce the possibility of default to

zero, by the initial margin blocking and daily

MTM process.

Mark to Market

• Realization of profit or loss on a day to day basis

• Contract Rate Vs End of Day (Closing) Rate (multiplied by respective notional)

• Profit/Loss will be added/subtracted from the initial margin deposited

• If initial margin minus accumulated loss < maintenance margin (75% of initial margin) – top up/liquidation

Initial & Variable Margin

• 4%-10% of contract value – Initial Margin – amount of funds pledged for holding a position

• Notional of Variable Margin will vary depends on the MTM profit/loss added/subtracted daily from your account

• Enable Investor/Hedger to enter the whole contract amount by depositing significantly smaller margin (Leverage)

Net Out Basis

• More than 90% of Futures Contracts are closed out before Settlement Date (standardized/un-customized tenor)

• Without the necessity of delivery (no real position in underlying assets)

Long & Short

Position

Long Vs Short

A buyer of futures contract (one who holds long

position) in which the settlement price is higher

(lower) than the previous day’s settlement price has

a positive (negative) settlement for the day.

Since a long position entitles the owner to purchase

the underlying asset, a higher (lower) settlement

price means the futures price of the underlying

asset has increased (decreased). Consequently a

long position in the contract is worth more (less).

Long Vs Short

Futures trading between the long

and short is a zero sum game;

that is the sum of the long’s and

short’s daily settlement is zero.

Long Vs Short

Futures trading allows Investor to do a

“short selling” (you can sell first even if you

do not have the underlying)

Regulators in US at the moment allow a

stock to be shorted only on an uptick – that

is when the most recent movement in the

price of the stock was an increase

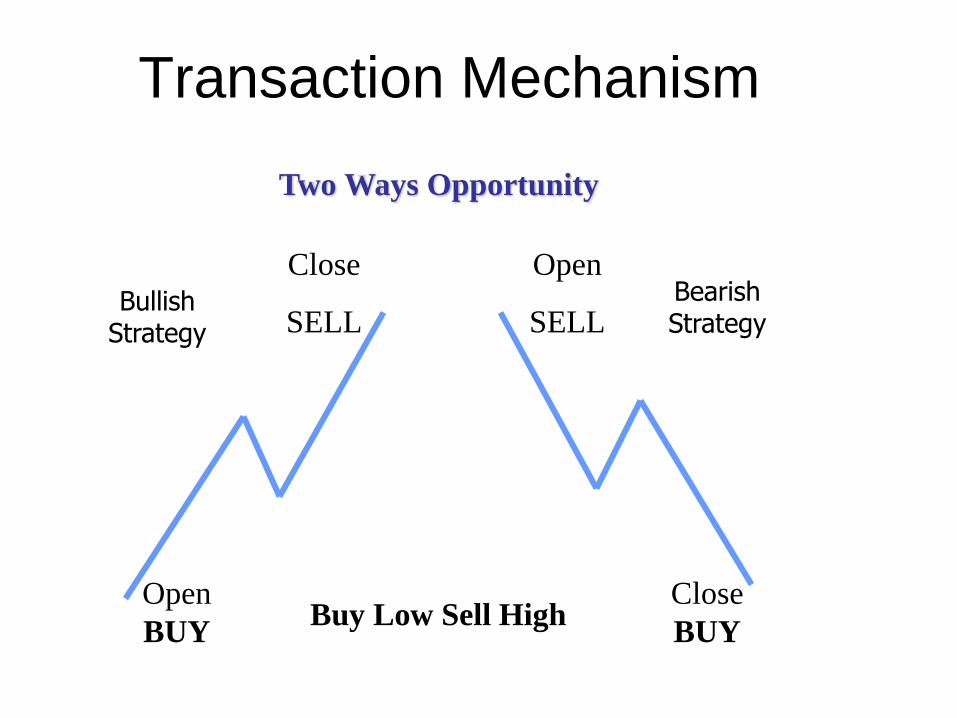

Transaction Mechanism

Open

BUY

Close

SELL

Open

SELL

Close

BUY

Buy Low Sell High

Two Ways Opportunity

Bullish Strategy

Bearish Strategy

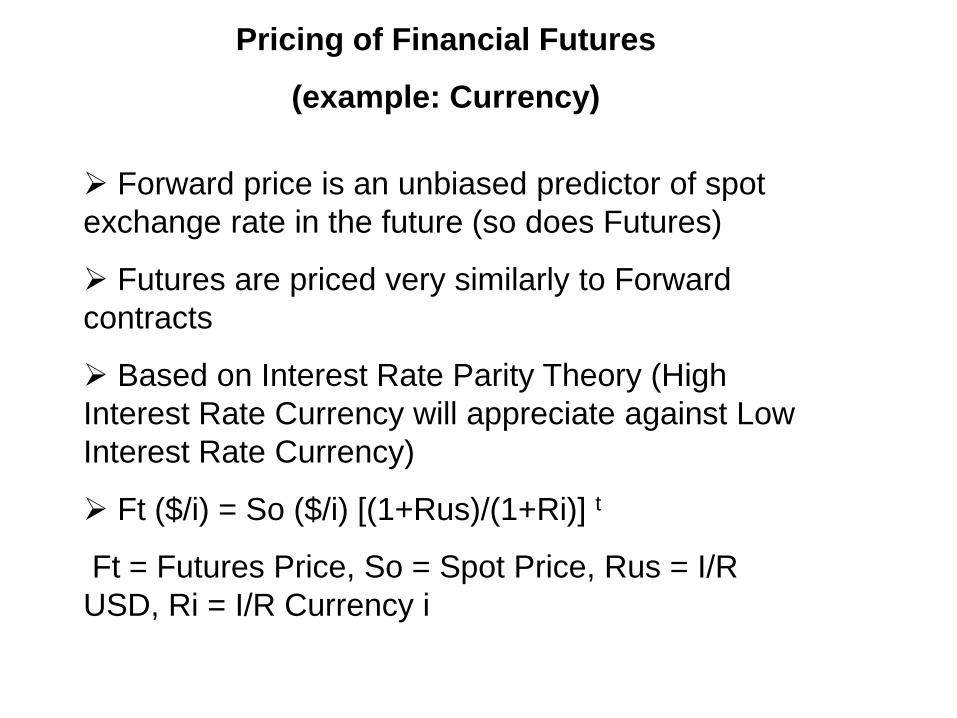

Pricing of Financial Futures

(example: Currency)

Forward price is an unbiased predictor of spot

exchange rate in the future (so does Futures)

Futures are priced very similarly to Forward

contracts

Based on Interest Rate Parity Theory (High

Interest Rate Currency will appreciate against Low

Interest Rate Currency)

Ft ($/i) = So ($/i) [(1+Rus)/(1+Ri)] t

Ft = Futures Price, So = Spot Price, Rus = I/R

USD, Ri = I/R Currency i

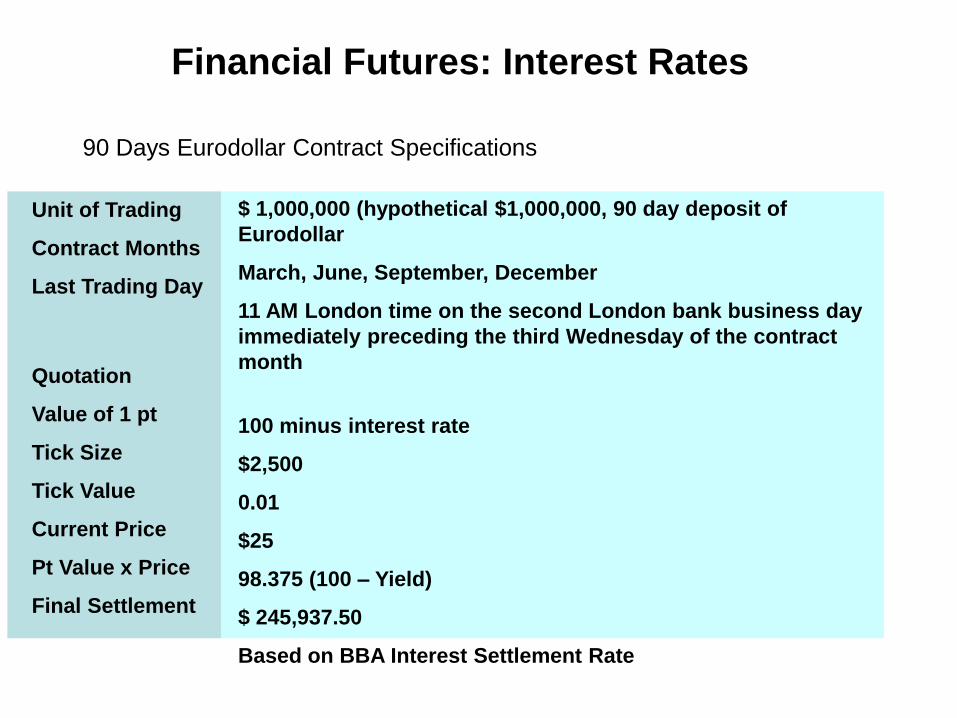

Financial Futures: Interest Rates

90 Days Eurodollar Contract Specifications

Unit of Trading

Contract Months

Last Trading Day

Quotation

Value of 1 pt

Tick Size

Tick Value

Current Price

Pt Value x Price

Final Settlement

$ 1,000,000 (hypothetical $1,000,000, 90 day deposit of

Eurodollar

March, June, September, December

11 AM London time on the second London bank business day

immediately preceding the third Wednesday of the contract

month

100 minus interest rate

$2,500

0.01

$25

98.375 (100 – Yield)

$ 245,937.50

Based on BBA Interest Settlement Rate

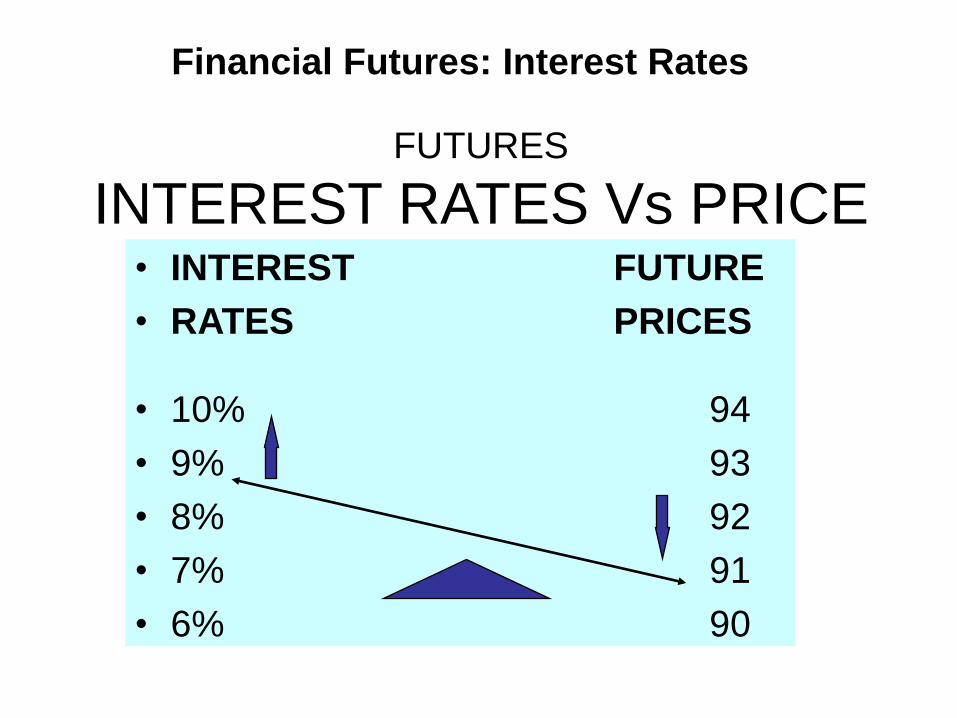

Financial Futures: Interest Rates

FUTURES

INTEREST RATES Vs PRICE • INTEREST FUTURE

• RATES PRICES

• 10% 94

• 9% 93

• 8% 92

• 7% 91

• 6% 90

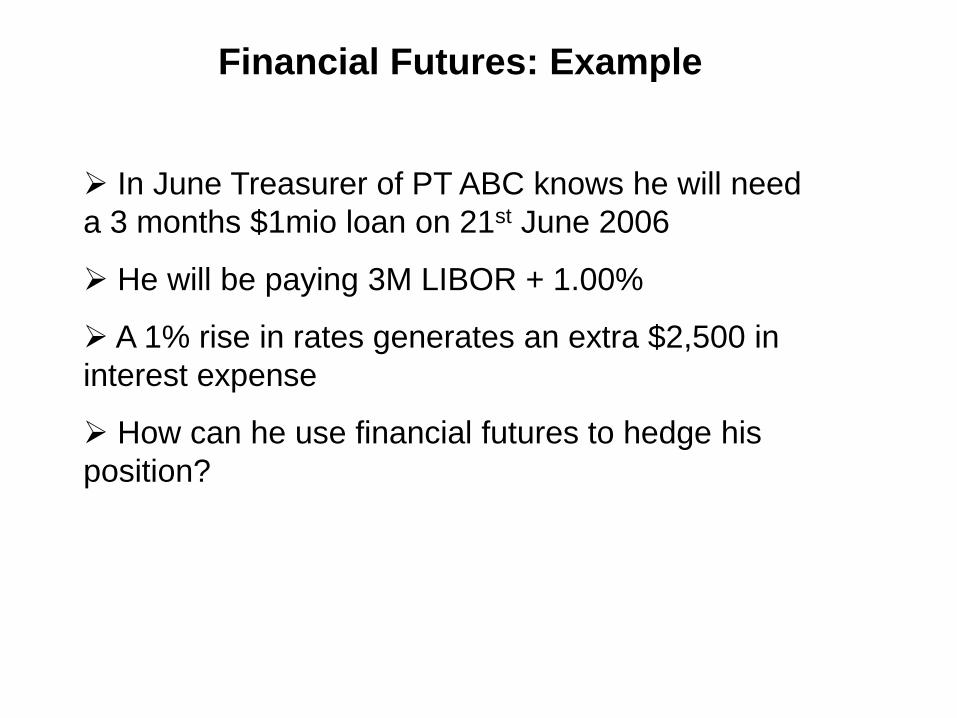

Financial Futures: Example

In June Treasurer of PT ABC knows he will need

a 3 months $1mio loan on 21st June 2006

He will be paying 3M LIBOR + 1.00%

A 1% rise in rates generates an extra $2,500 in

interest expense

How can he use financial futures to hedge his

position?

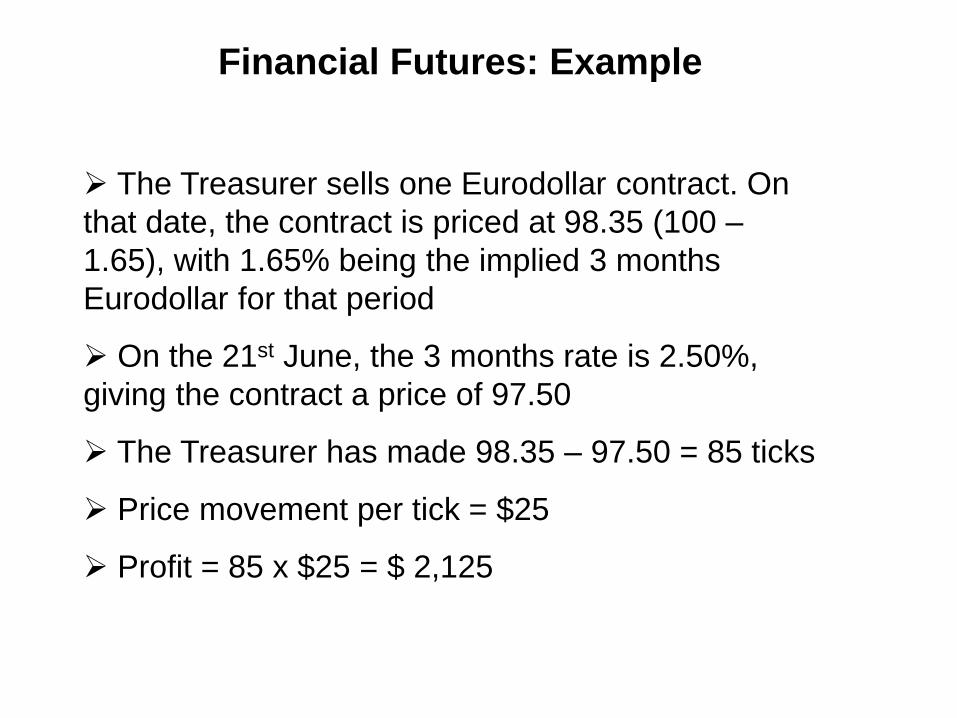

Financial Futures: Example

The Treasurer sells one Eurodollar contract. On

that date, the contract is priced at 98.35 (100 –

1.65), with 1.65% being the implied 3 months

Eurodollar for that period

On the 21st June, the 3 months rate is 2.50%,

giving the contract a price of 97.50

The Treasurer has made 98.35 – 97.50 = 85 ticks

Price movement per tick = $25

Profit = 85 x $25 = $ 2,125

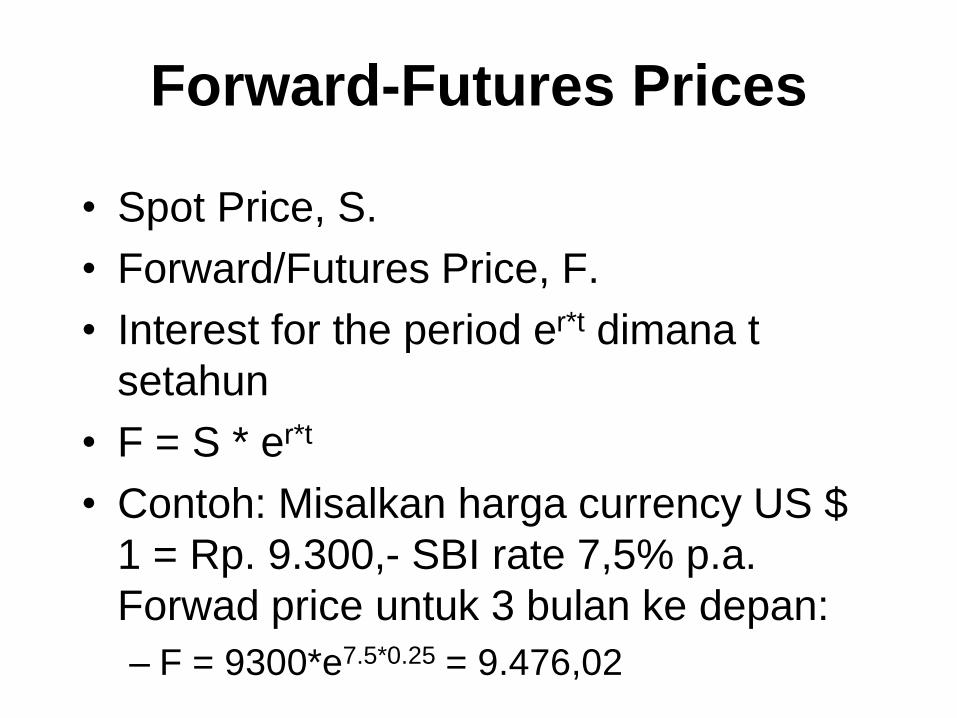

Forward-Futures Prices

• Spot Price, S.

• Forward/Futures Price, F.

• Interest for the period er*t dimana t

setahun

• F = S * er*t

• Contoh: Misalkan harga currency US $

1 = Rp. 9.300,- SBI rate 7,5% p.a.

Forwad price untuk 3 bulan ke depan:

– F = 9300*e7.5*0.25 = 9.476,02

Long Forward Contract

Prices • Spot Price, S. Delivery Price, K.

• Forward Price, F.

• f = long forward contract prices

• Interest for the period er*t dimana t setahun

• f = S - K * e-r*t

• Contoh: Misalkan harga currency US $ 1 = Rp. 9.300,- SBI rate 7,5% p.a. Forwad Contract price untuk 3 bulan ke depan bila delivery price Rp. 9.300,-: – f = 9300 - 9300*e-7.5*0.25 = 172,75

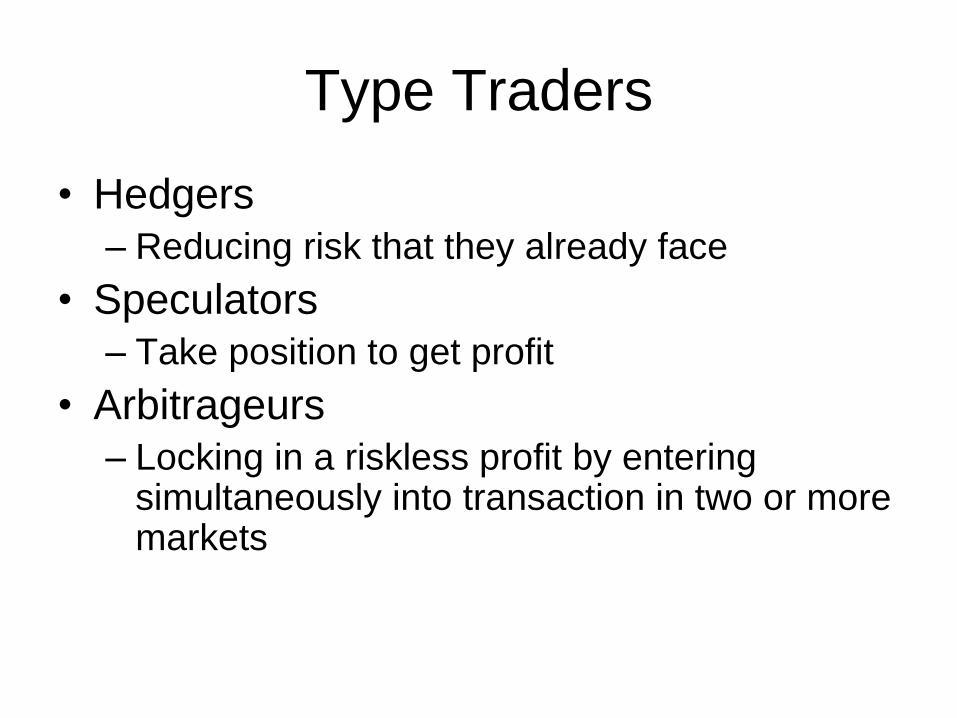

Type Traders

• Hedgers

– Reducing risk that they already face

• Speculators

– Take position to get profit

• Arbitrageurs

– Locking in a riskless profit by entering simultaneously into transaction in two or more markets

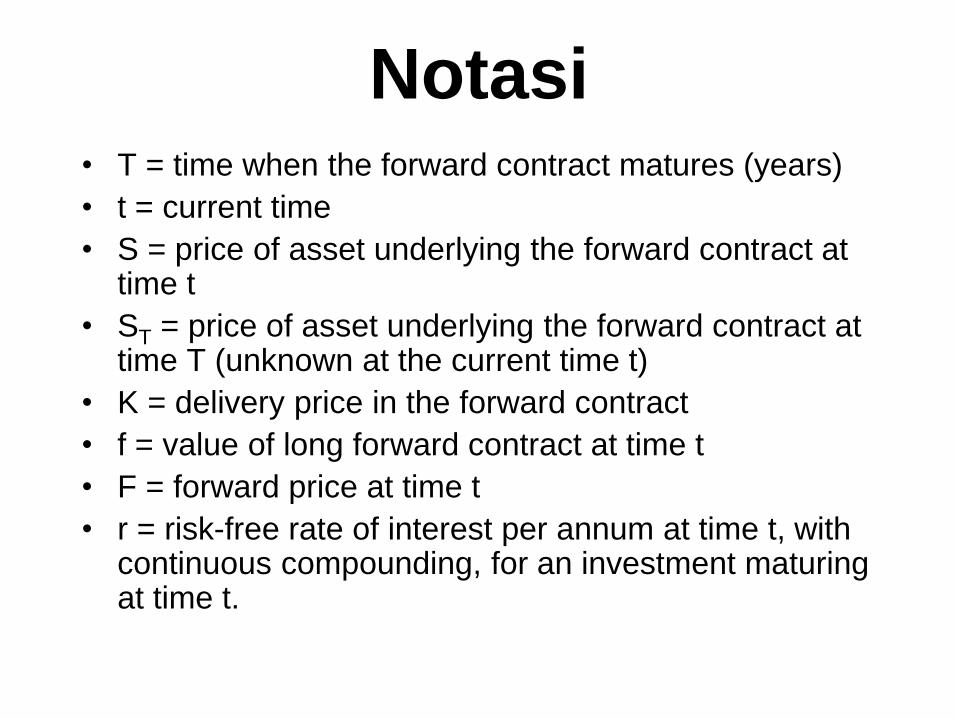

Notasi • T = time when the forward contract matures (years)

• t = current time

• S = price of asset underlying the forward contract at time t

• ST = price of asset underlying the forward contract at time T (unknown at the current time t)

• K = delivery price in the forward contract

• f = value of long forward contract at time t

• F = forward price at time t

• r = risk-free rate of interest per annum at time t, with continuous compounding, for an investment maturing at time t.

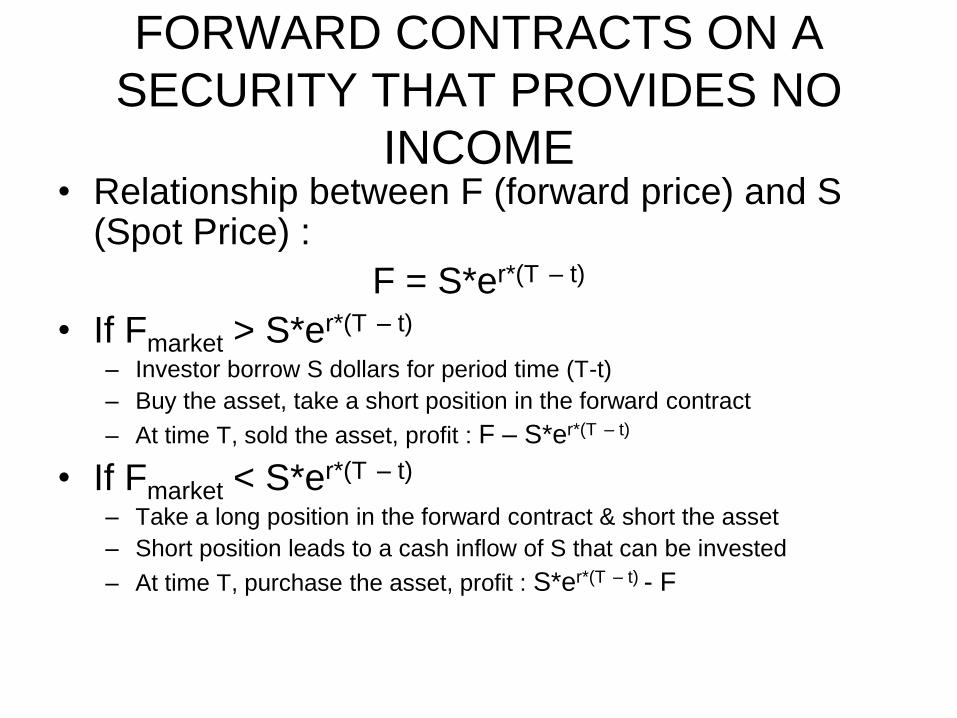

FORWARD CONTRACTS ON A

SECURITY THAT PROVIDES NO

INCOME • Relationship between F (forward price) and S

(Spot Price) :

F = S*er*(T – t)

• If Fmarket > S*er*(T – t)

– Investor borrow S dollars for period time (T-t)

– Buy the asset, take a short position in the forward contract

– At time T, sold the asset, profit : F – S*er*(T – t)

• If Fmarket < S*er*(T – t)

– Take a long position in the forward contract & short the asset

– Short position leads to a cash inflow of S that can be invested

– At time T, purchase the asset, profit : S*er*(T – t) - F

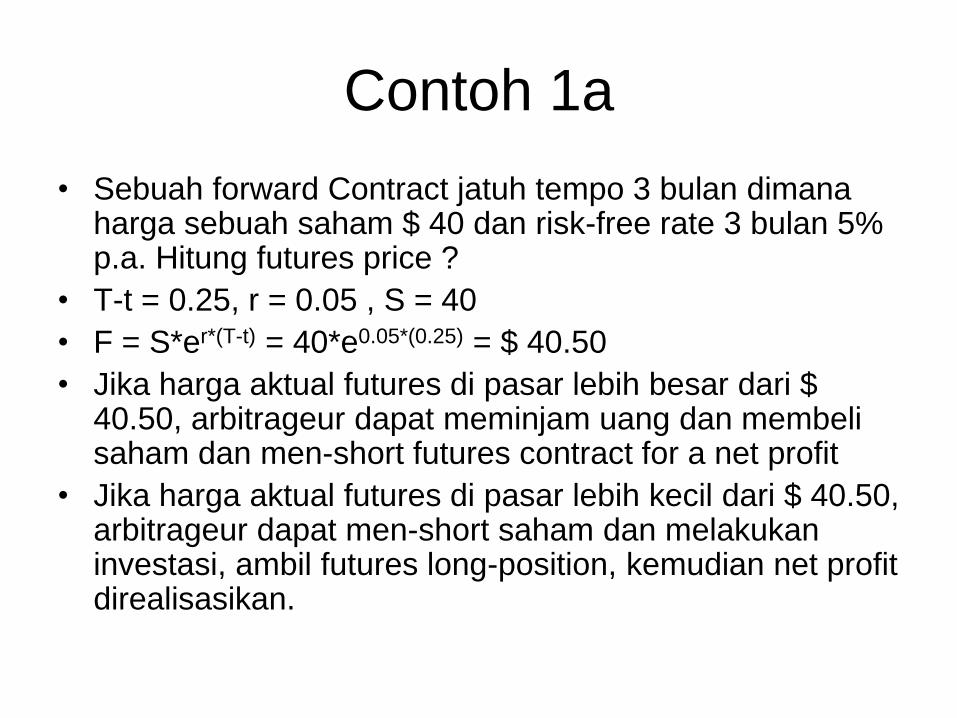

Contoh 1a

• Sebuah forward Contract jatuh tempo 3 bulan dimana harga sebuah saham $ 40 dan risk-free rate 3 bulan 5% p.a. Hitung futures price ?

• T-t = 0.25, r = 0.05 , S = 40

• F = S*er*(T-t) = 40*e0.05*(0.25) = $ 40.50

• Jika harga aktual futures di pasar lebih besar dari $ 40.50, arbitrageur dapat meminjam uang dan membeli saham dan men-short futures contract for a net profit

• Jika harga aktual futures di pasar lebih kecil dari $ 40.50, arbitrageur dapat men-short saham dan melakukan investasi, ambil futures long-position, kemudian net profit direalisasikan.

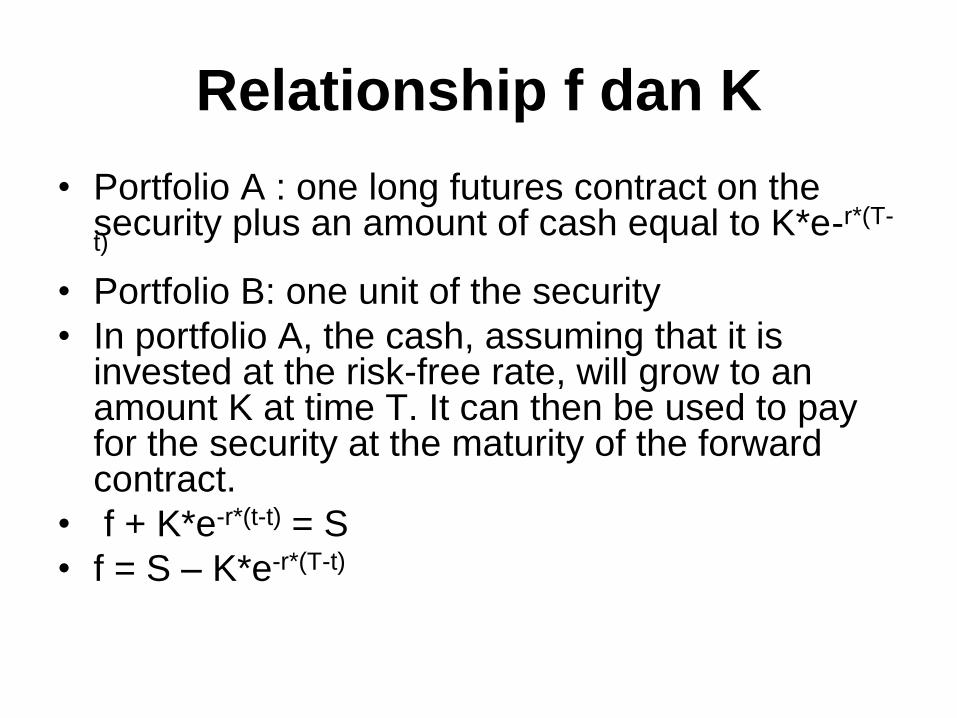

Relationship f dan K

• Portfolio A : one long futures contract on the security plus an amount of cash equal to K*e-r*(T-t)

• Portfolio B: one unit of the security

• In portfolio A, the cash, assuming that it is invested at the risk-free rate, will grow to an amount K at time T. It can then be used to pay for the security at the maturity of the forward contract.

• f + K*e-r*(t-t) = S

• f = S – K*e-r*(T-t)

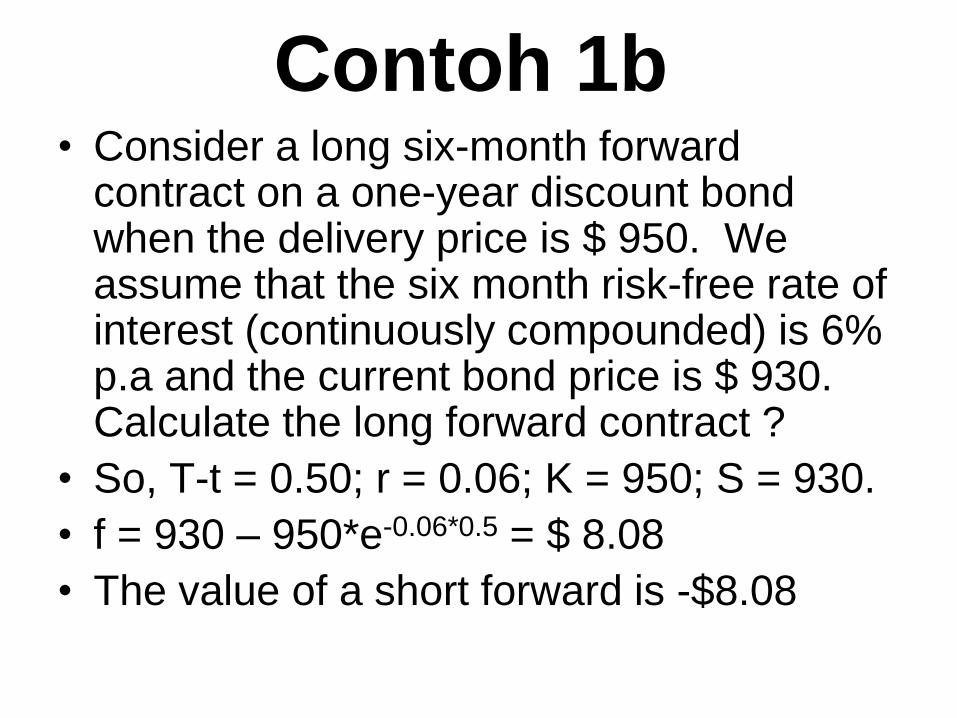

Contoh 1b • Consider a long six-month forward

contract on a one-year discount bond when the delivery price is $ 950. We assume that the six month risk-free rate of interest (continuously compounded) is 6% p.a and the current bond price is $ 930. Calculate the long forward contract ?

• So, T-t = 0.50; r = 0.06; K = 950; S = 930.

• f = 930 – 950*e-0.06*0.5 = $ 8.08

• The value of a short forward is -$8.08

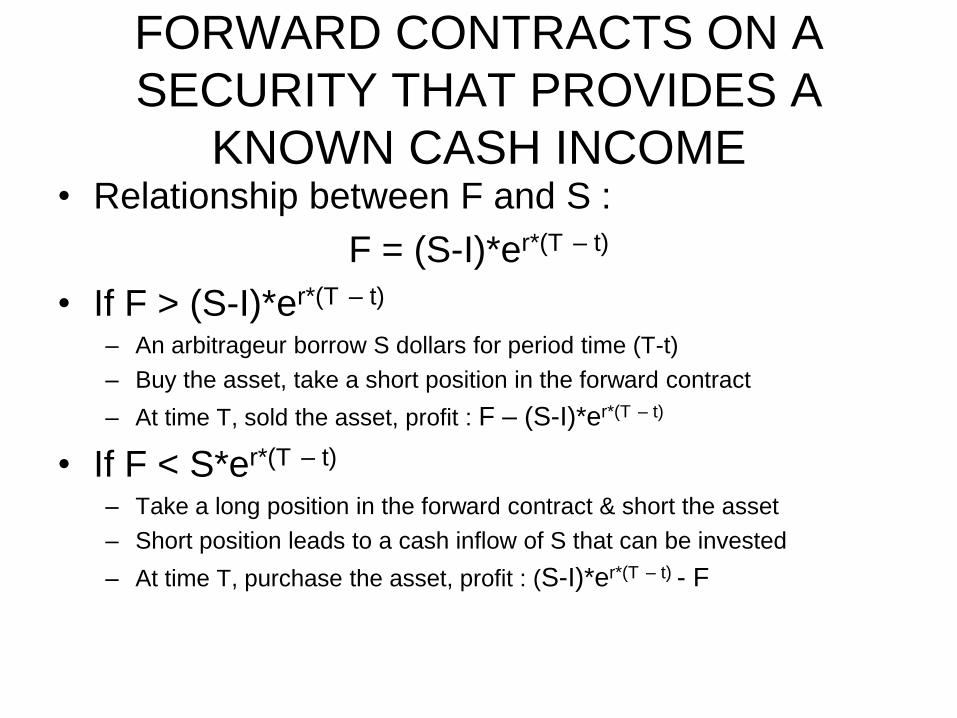

FORWARD CONTRACTS ON A

SECURITY THAT PROVIDES A

KNOWN CASH INCOME • Relationship between F and S :

F = (S-I)*er*(T – t)

• If F > (S-I)*er*(T – t)

– An arbitrageur borrow S dollars for period time (T-t)

– Buy the asset, take a short position in the forward contract

– At time T, sold the asset, profit : F – (S-I)*er*(T – t)

• If F < S*er*(T – t)

– Take a long position in the forward contract & short the asset

– Short position leads to a cash inflow of S that can be invested

– At time T, purchase the asset, profit : (S-I)*er*(T – t) - F

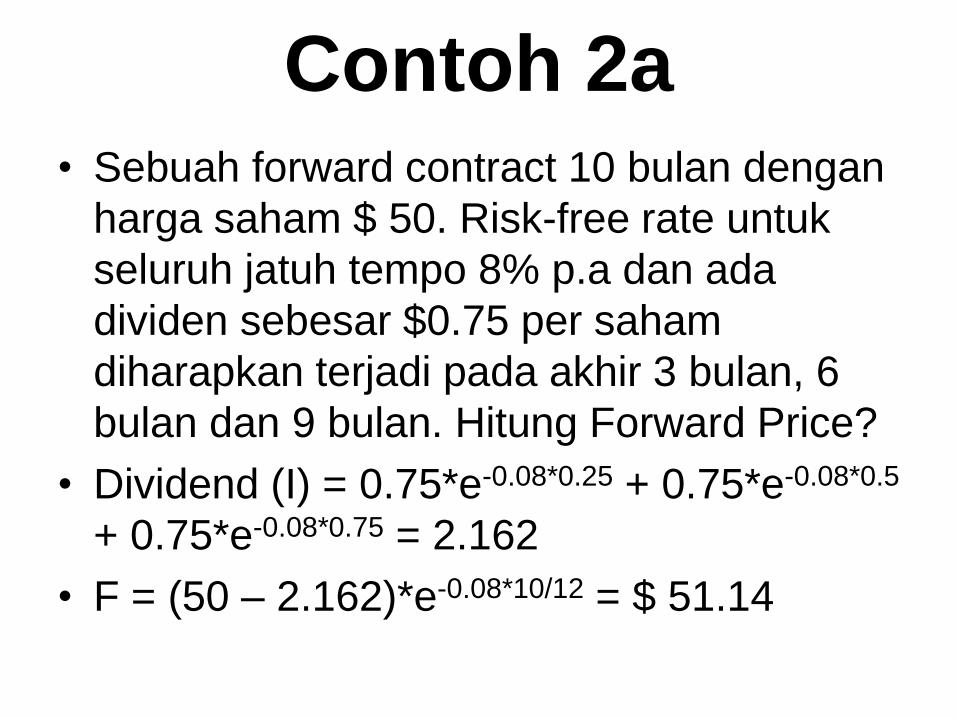

Contoh 2a • Sebuah forward contract 10 bulan dengan

harga saham $ 50. Risk-free rate untuk

seluruh jatuh tempo 8% p.a dan ada

dividen sebesar $0.75 per saham

diharapkan terjadi pada akhir 3 bulan, 6

bulan dan 9 bulan. Hitung Forward Price?

• Dividend (I) = 0.75*e-0.08*0.25 + 0.75*e-0.08*0.5

+ 0.75*e-0.08*0.75 = 2.162

• F = (50 – 2.162)*e-0.08*10/12 = $ 51.14

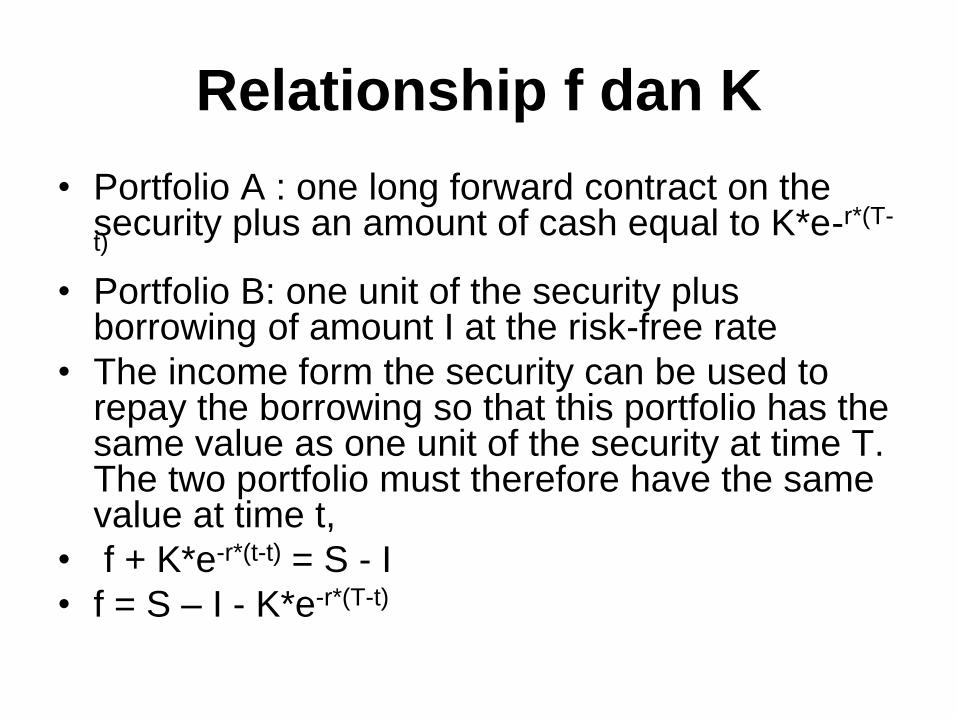

Relationship f dan K

• Portfolio A : one long forward contract on the security plus an amount of cash equal to K*e-r*(T-t)

• Portfolio B: one unit of the security plus borrowing of amount I at the risk-free rate

• The income form the security can be used to repay the borrowing so that this portfolio has the same value as one unit of the security at time T. The two portfolio must therefore have the same value at time t,

• f + K*e-r*(t-t) = S - I

• f = S – I - K*e-r*(T-t)

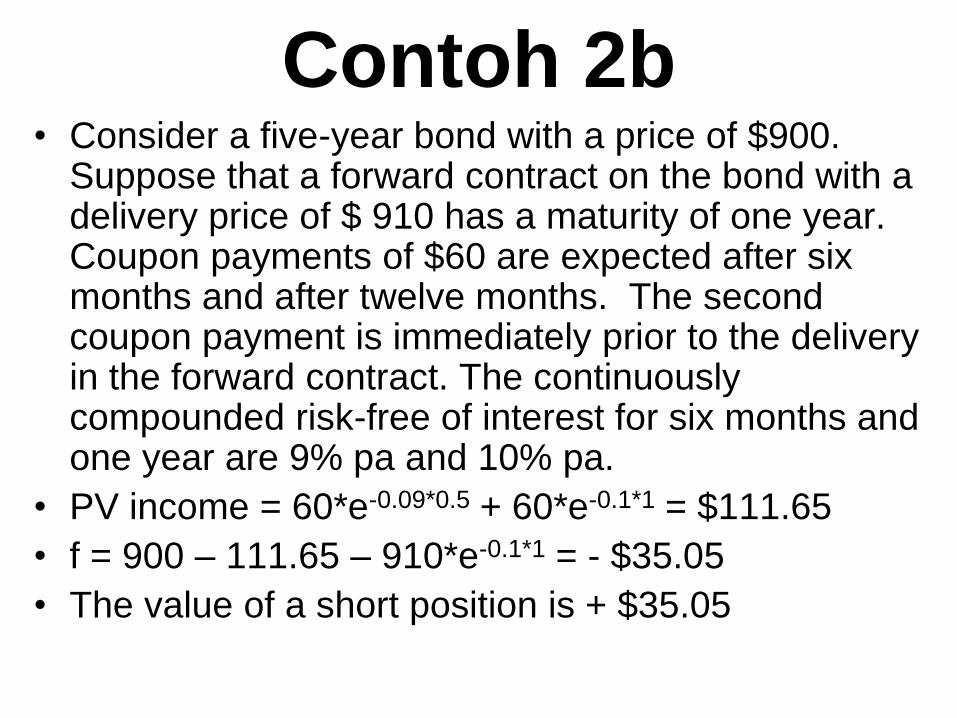

Contoh 2b • Consider a five-year bond with a price of $900.

Suppose that a forward contract on the bond with a delivery price of $ 910 has a maturity of one year. Coupon payments of $60 are expected after six months and after twelve months. The second coupon payment is immediately prior to the delivery in the forward contract. The continuously compounded risk-free of interest for six months and one year are 9% pa and 10% pa.

• PV income = 60*e-0.09*0.5 + 60*e-0.1*1 = $111.65

• f = 900 – 111.65 – 910*e-0.1*1 = - $35.05

• The value of a short position is + $35.05

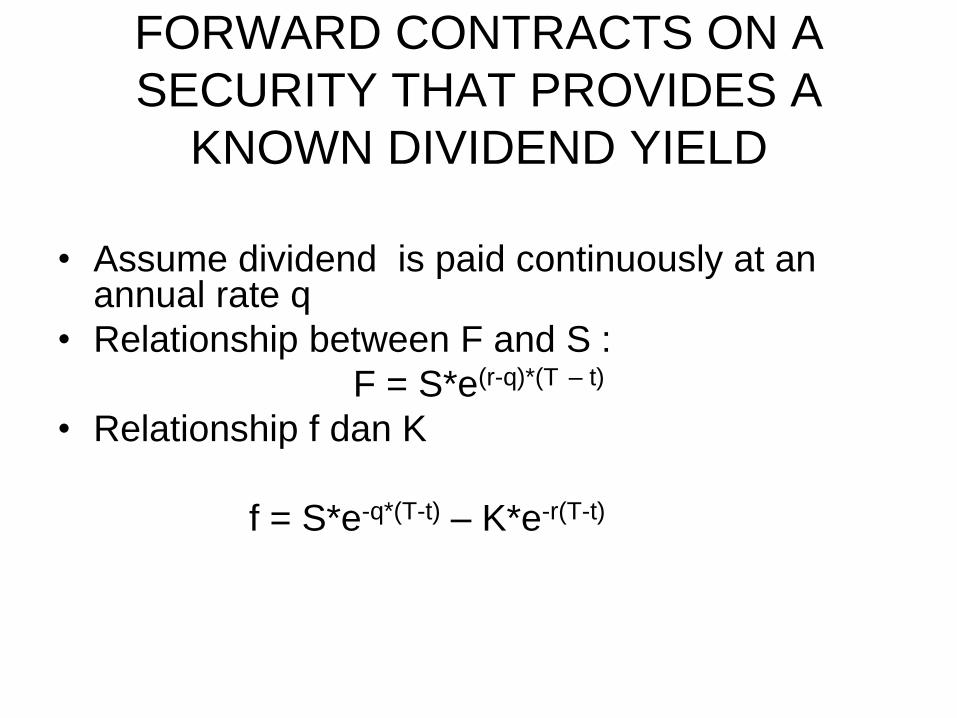

FORWARD CONTRACTS ON A

SECURITY THAT PROVIDES A

KNOWN DIVIDEND YIELD

• Assume dividend is paid continuously at an annual rate q

• Relationship between F and S :

F = S*e(r-q)*(T – t)

• Relationship f dan K

f = S*e-q*(T-t) – K*e-r(T-t)

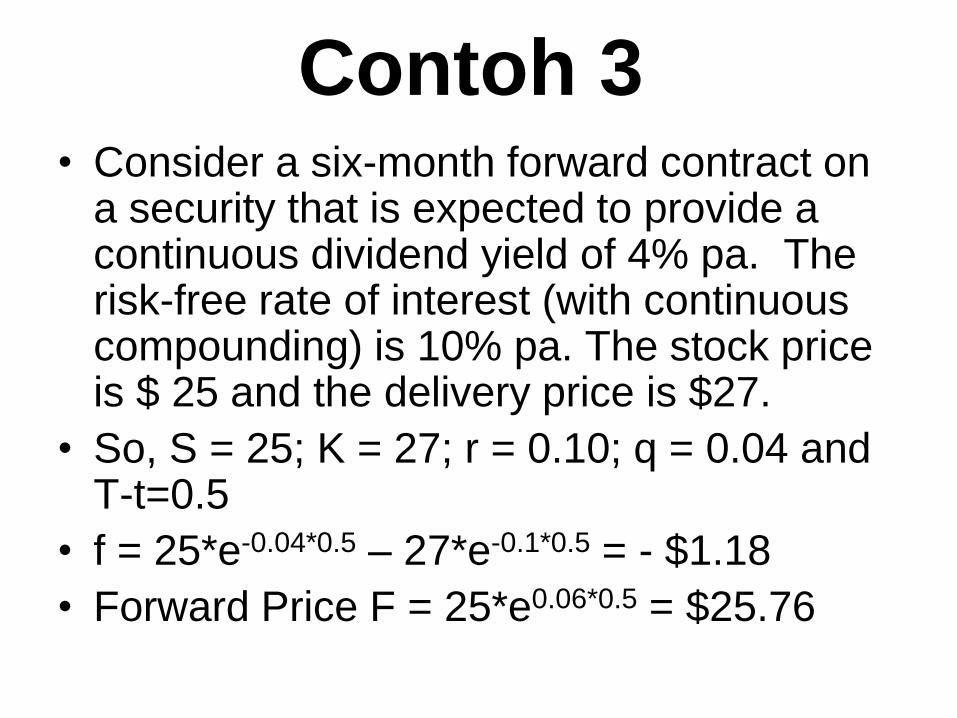

Contoh 3 • Consider a six-month forward contract on

a security that is expected to provide a continuous dividend yield of 4% pa. The risk-free rate of interest (with continuous compounding) is 10% pa. The stock price is $ 25 and the delivery price is $27.

• So, S = 25; K = 27; r = 0.10; q = 0.04 and T-t=0.5

• f = 25*e-0.04*0.5 – 27*e-0.1*0.5 = - $1.18

• Forward Price F = 25*e0.06*0.5 = $25.76

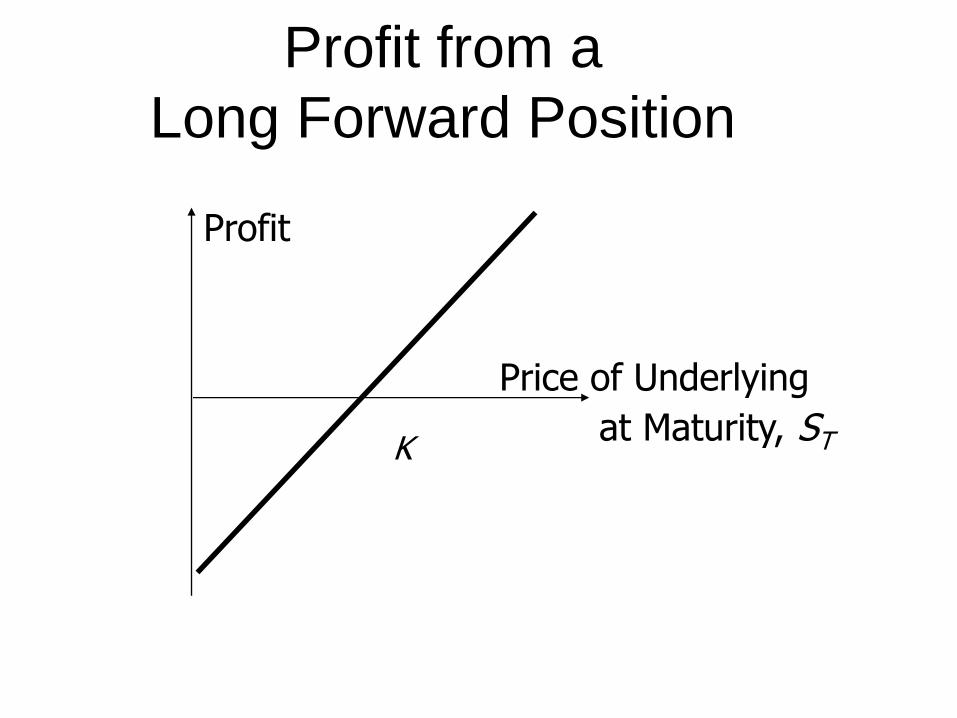

Profit from a

Long Forward Position

Profit

Price of Underlying

at Maturity, ST K

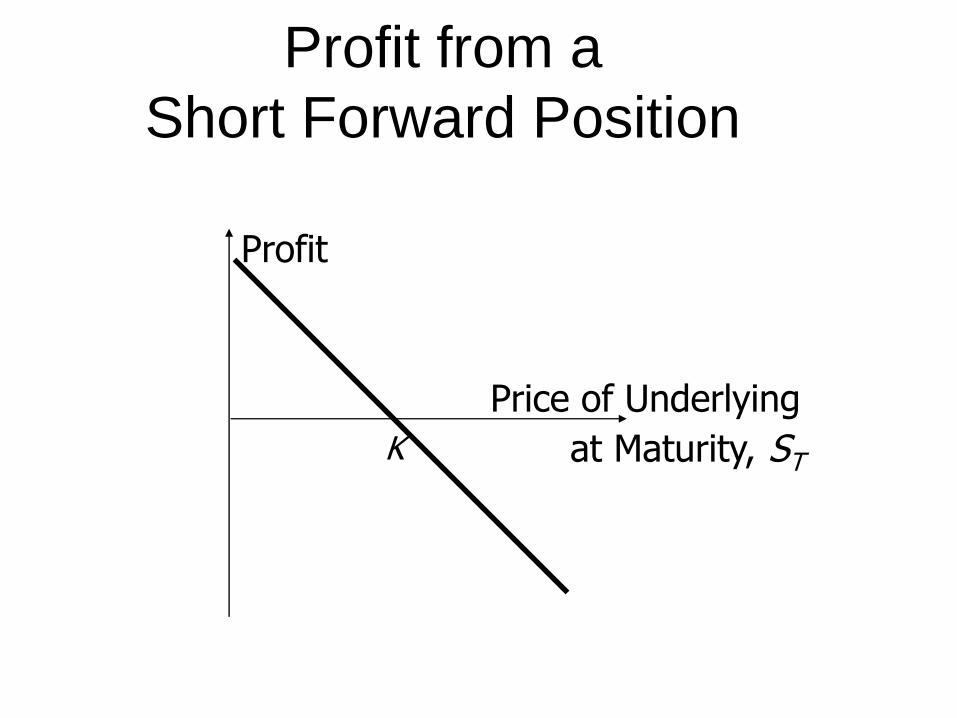

Profit from a

Short Forward Position

Profit

Price of Underlying

at Maturity, ST K

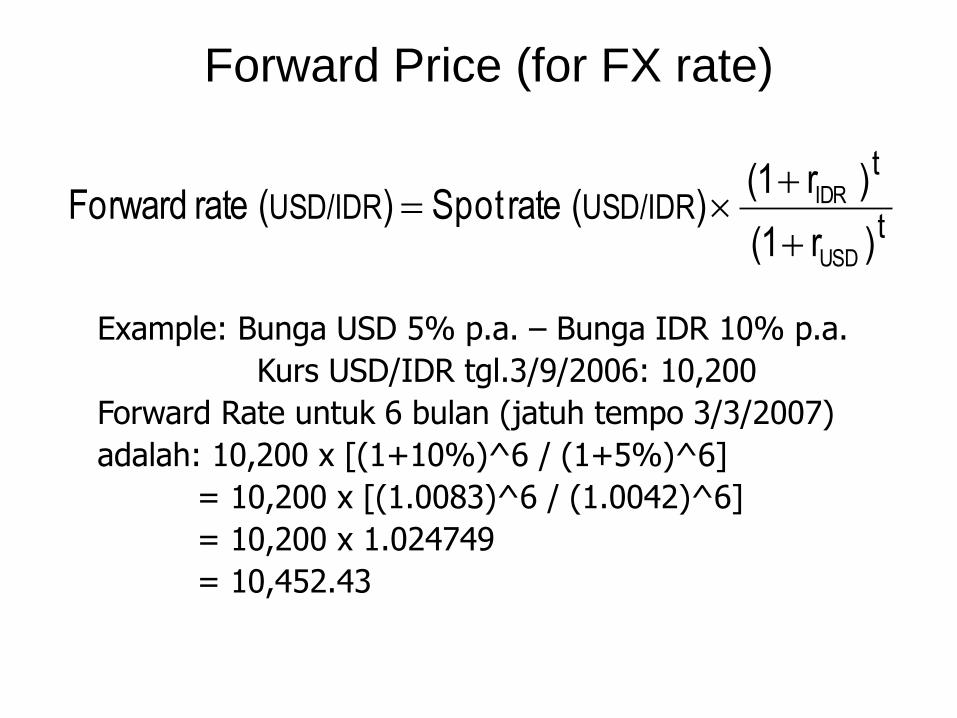

Example: Bunga USD 5% p.a. – Bunga IDR 10% p.a.

Kurs USD/IDR tgl.3/9/2006: 10,200

Forward Rate untuk 6 bulan (jatuh tempo 3/3/2007)

adalah: 10,200 x [(1+10%)^6 / (1+5%)^6]

= 10,200 x [(1.0083)^6 / (1.0042)^6]

= 10,200 x 1.024749

= 10,452.43

Forward Price (for FX rate)

t

t

USD/IDRUSD/IDR)r(1

)r(1)( rateSpot )( rate Forward

USD

IDR

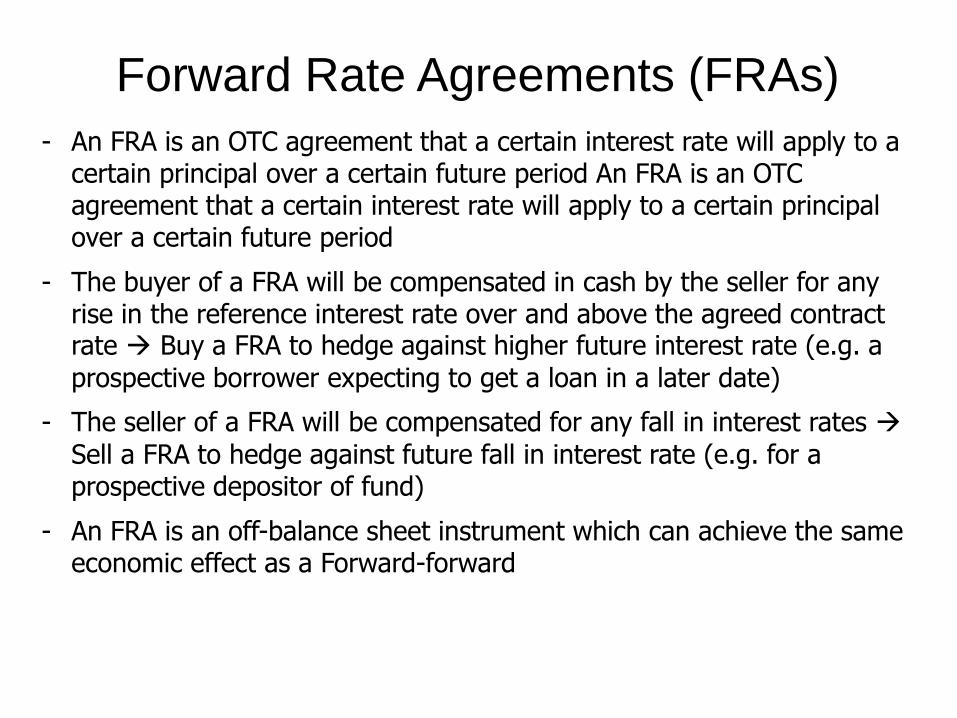

- An FRA is an OTC agreement that a certain interest rate will apply to a certain principal over a certain future period An FRA is an OTC agreement that a certain interest rate will apply to a certain principal over a certain future period

- The buyer of a FRA will be compensated in cash by the seller for any rise in the reference interest rate over and above the agreed contract rate Buy a FRA to hedge against higher future interest rate (e.g. a

prospective borrower expecting to get a loan in a later date)

- The seller of a FRA will be compensated for any fall in interest rates

Sell a FRA to hedge against future fall in interest rate (e.g. for a prospective depositor of fund)

- An FRA is an off-balance sheet instrument which can achieve the same economic effect as a Forward-forward

Forward Rate Agreements (FRAs)

Forward Rate Agreements (FRAs)

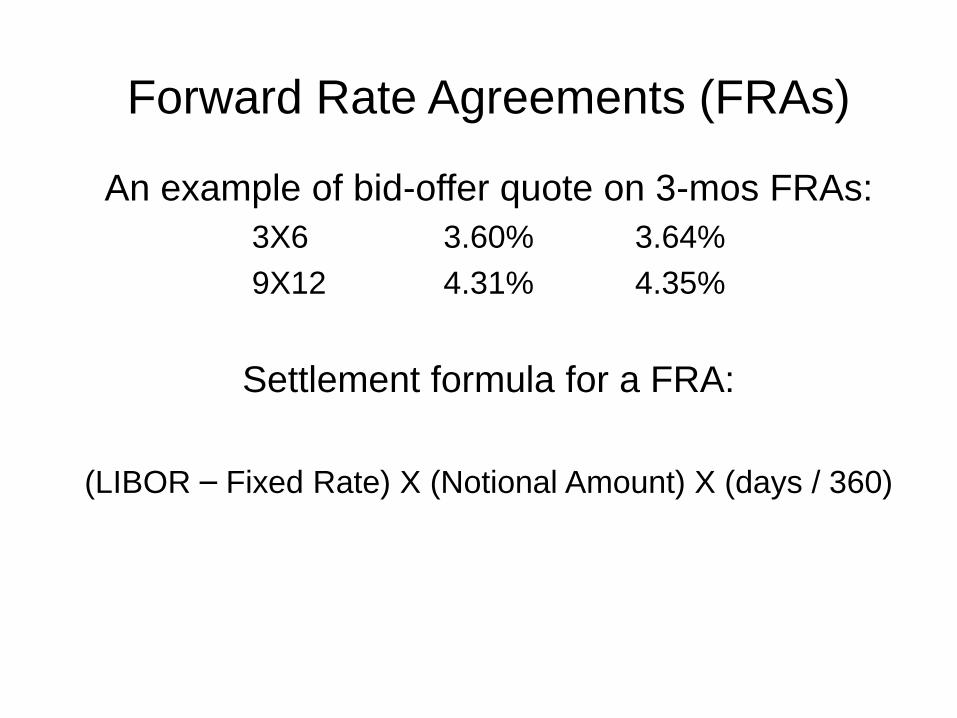

An example of bid-offer quote on 3-mos FRAs:

3X6 3.60% 3.64%

9X12 4.31% 4.35%

Settlement formula for a FRA:

(LIBOR – Fixed Rate) X (Notional Amount) X (days / 360)

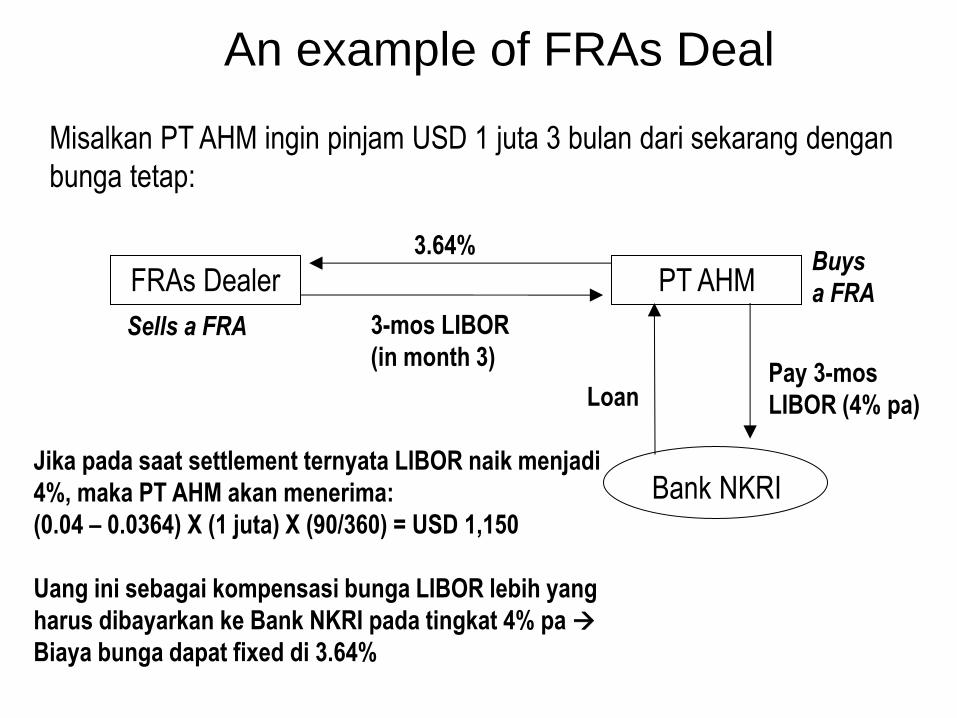

An example of FRAs Deal

PT AHM

Bank NKRI

3.64%

3-mos LIBOR

(in month 3)

Loan Pay 3-mos

LIBOR (4% pa)

FRAs Dealer

Jika pada saat settlement ternyata LIBOR naik menjadi

4%, maka PT AHM akan menerima:

(0.04 – 0.0364) X (1 juta) X (90/360) = USD 1,150

Uang ini sebagai kompensasi bunga LIBOR lebih yang

harus dibayarkan ke Bank NKRI pada tingkat 4% pa

Biaya bunga dapat fixed di 3.64%

Misalkan PT AHM ingin pinjam USD 1 juta 3 bulan dari sekarang dengan

bunga tetap:

Sells a FRA

Buys

a FRA

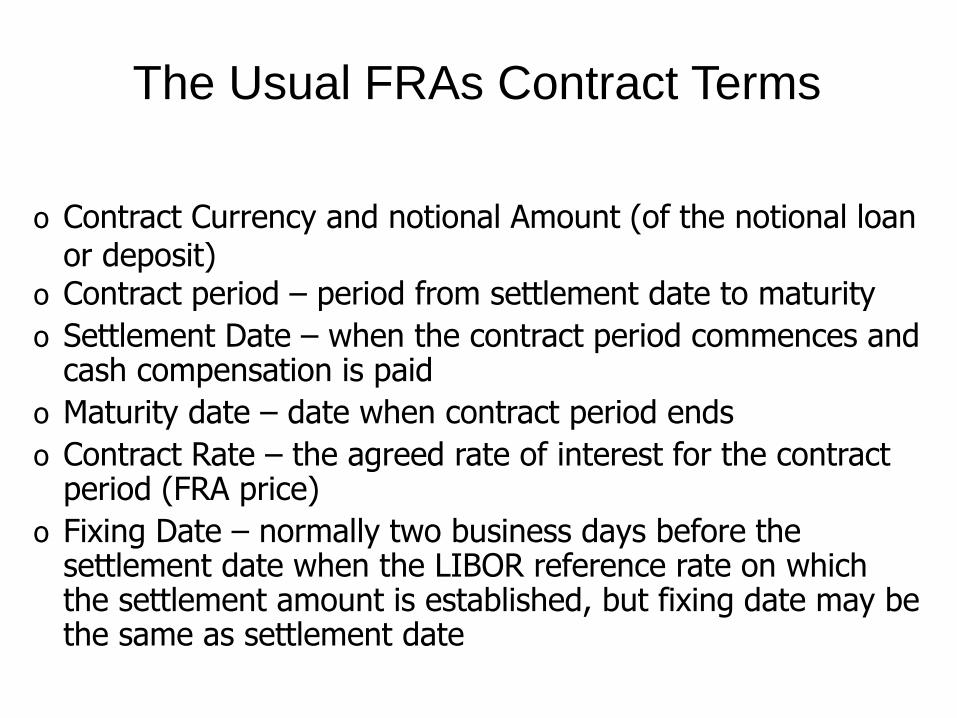

o Contract Currency and notional Amount (of the notional loan or deposit)

o Contract period – period from settlement date to maturity

o Settlement Date – when the contract period commences and cash compensation is paid

o Maturity date – date when contract period ends

o Contract Rate – the agreed rate of interest for the contract period (FRA price)

o Fixing Date – normally two business days before the settlement date when the LIBOR reference rate on which the settlement amount is established, but fixing date may be the same as settlement date

The Usual FRAs Contract Terms

Forwards vs FRAs

• Forwards Hedging against Market Risk (price

fluctuations)

• FRAs Hedging against Interest Rate Risk

Terima kasih