Formulating a strategic marketing plan for amana bank salary saving account

25

Amana bank Salary saving account Presented by M.S.Waseem Mohamed Reg.No-0000017138

-

Upload

royal-ceramics-lanka-plc -

Category

Marketing

-

view

68 -

download

2

Transcript of Formulating a strategic marketing plan for amana bank salary saving account

Amana bank Salary saving account

Presented byM.S.Waseem Mohamed

Reg.No-0000017138

Introduction The birth of Sri Lanka s first permit Islamic

banking products in Sri Lanka in 2005. In 2011 approved for Licensed commercial

bank which fully functions on the principles of Islamic finance.

Amana bank formed by Meeran sahib Alif, the former cabinet secretary. And Osman kassim, the banks current chairman.

Amana has 27 branches with total assets of over 65 billion rupees, employing about 650 people

Local brand name – Amana bank

Vision

To provide a differentiated banking experience in Sri Lanka, through an equitable financial system.

Mission

To share risk and rewards with all our customers by delivering sharia compliant financial solution based on innovation and technology.

Formal structure of Amana bank

M.D

C.O.O

v.p v.p v.p v.p v.p v.p v.p company v.p credit operating IT risk consumer banking audit legal secretary treasury

Marketing manager Manager direct sale

Executive 2 Team leaders

Executive 1 Business development officers

Junior executive

Assistant junior executive

C.M.T MEMBERS

M.D

The product – Amana salary saving account

Individual savings - the main category that generate normal saving account the saving account range comprise of individual saving s account available in both salary account and general saving account. The minimum initial deposit is LKR 2,500 and no wants minimum salary. And this account should maintain LKR1, 000 with in account. Personal salary saving account It’s maintaining individual customer, the customer who have a minimum salary LKR 10,000, he/she can open salary account without any initial deposit. This type account can maintain zero balance. Corporate salary saving accountThis type salary account should have an above 25 accounts, no want minimum salary, initial deposit and minimum balance. This type account focus for team workers and company’s whole employs.

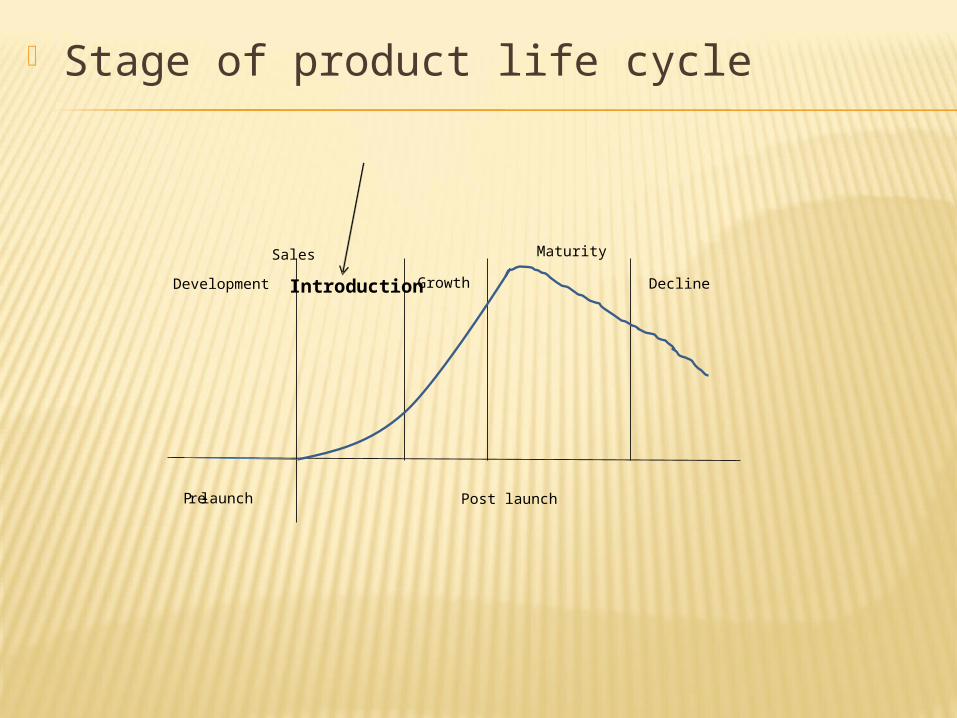

Stage of product life cycle

Development Introduction Growth

Maturity

Decline

Post launch Pre-launch

Sales

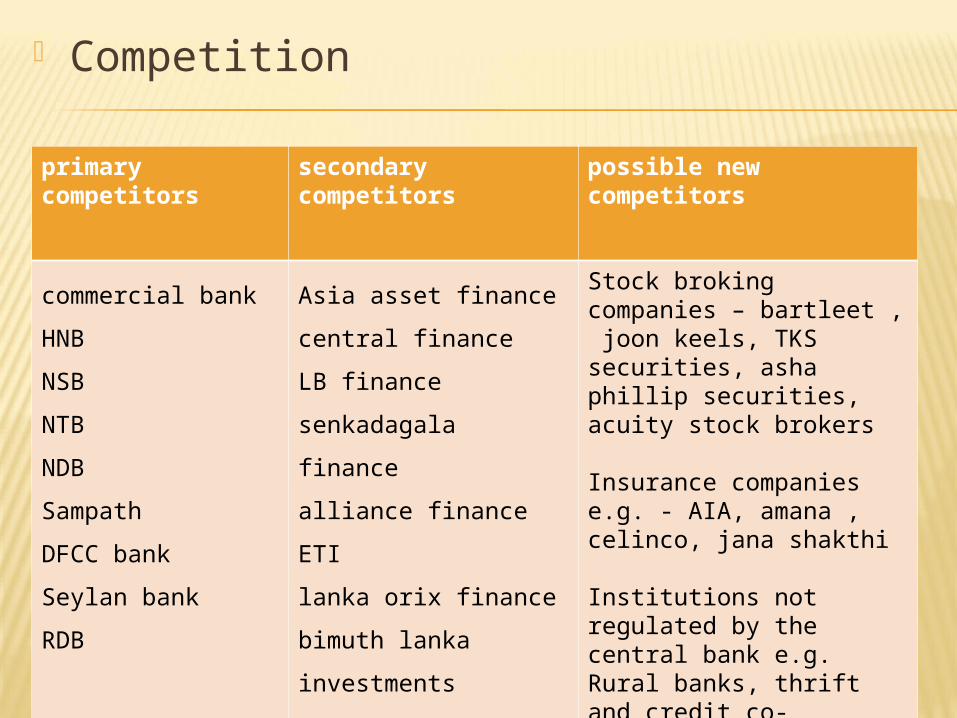

Competition

primary competitors

secondary competitors

possible new competitors

commercial bank

HNB

NSB

NTB

NDB

Sampath

DFCC bank

Seylan bank

RDB

Asia asset finance

central finance

LB finance

senkadagala finance

alliance finance

ETI

lanka orix finance

bimuth lanka

investments

Stock broking companies – bartleet , joon keels, TKS securities, asha phillip securities, acuity stock brokers

Insurance companies e.g. - AIA, amana , celinco, jana shakthi

Institutions not regulated by the central bank e.g. Rural banks, thrift and credit co-operative societies

Background of Competitors

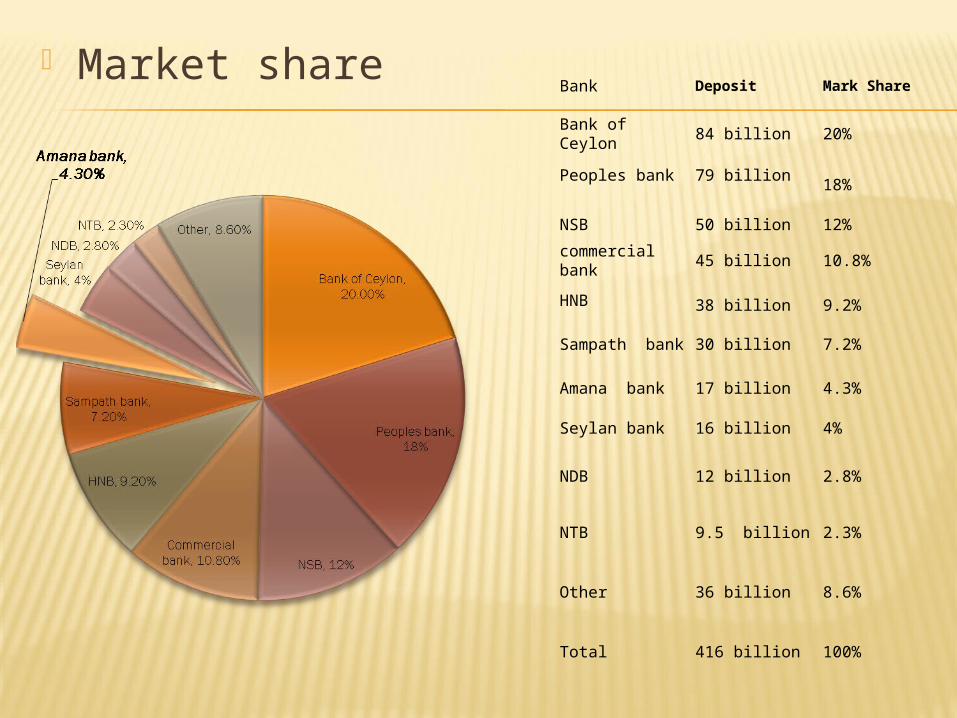

Market share Bank Deposit Mark Share

Bank of Ceylon 84 billion 20%

Peoples bank 79 billion18%

NSB 50 billion 12%

commercial bank 45 billion 10.8%

HNB 38 billion 9.2%

Sampath bank 30 billion 7.2%

Amana bank 17 billion 4.3%

Seylan bank 16 billion 4%

NDB 12 billion 2.8%

NTB 9.5 billion 2.3%

Other 36 billion 8.6%

Total 416 billion 100%

External Environment Factors

Political

Taxation, interest rate, especially interest rate will directly impact the purchasing of salary saving accounts. How the government takes measure to improve the economy etc.

Government imposes though rules and regulation

Economical

Cross national saving increased by 22.1% (2011), 24%(2012)and 27%(2013) of GDPInterest rate increased/decreased of savings,Decrease commodity prices(inflation rate) are decrease by 7.5%(2012) to 6.8%(2013)

Social

Change in social trends can impact the demand for salary saving accounts.Unemployment rate Increasing ageing population, it has the opportunity for bank industry to venture new segments into new

segments (salary saving account)

Technological

New technology in the firm of online banking account creation, online enquiry, money transfer, etc. are improved to facilitate user – friendly banking

e-bank cards management system platform upgraded to provide the infrastructural facilitates for the euro pay ,master card and visa upgrade.

Using mobile banking service vie a mobile internet connection by a mobile banking application

Strutted system training program for staff to develop their skills and knowledge.

Improvement of branch IT infrastructure including expansion of its service to newly open branches and

ATMs.

Ecological

Design and develop products such as slips, pass book, certificates and etc.. That has minimum environmental impact.

Use of environmentally friendly and easily disposable ATM cards, cards cover and ATM machine print receipt

In a “green” initiative, the printing of salary slip was discontinued and customers also enjoy the option of getting their monthly statement online.

Ethical

Product issue – the bank products should be making according to the model and if there any changes the bank must inform to the customers.

Product issue- the price (interest rate ) must be high to the brand value.

Details- so marketers make sure to put their product ingredient, profit sharing issue that is one of the ethics. That will build relationship with customer mostly.

Legal

Central bank rules and regulation

Government police for direct activities and exercise control over business activities, operating and risk management

Approve implementation of a policy of communication with all stakeholders, including depositors,

creditors, shareholders and borrowers

Swot analysis

Weaknesses•Banks under expansion in limited capital for promotional activity•Poor consideration on research and development•ATM machines are very low quantity •Limited market share growth•Poor consideration on motivation staff•Limited branches and lack of coverage area

• Lot of competitors • Substitutes (loan plan, local saving

plans)• Higher rules and regulation are

introduced by the government• External party have negative attitude

about the bank.

Sales objective

Amana bank expects to increase its deposit turnover further in order to achieve a higher growth rate and to achieve high profitability. The bank has achieved a deposit of Rs 17,983 million for the financial year of 2013/2014. Therefore it expects a higher sales turnover for the year 2014/2015, comparatively then the previous financial year. The sales objective has set as ,

“To achieve a saving accounts deposit turnover of Rs 21 billion for the financial year of 2014/2015 in all island”

Marketing objective

To be the fourth market leader in local saving market while increasing its market share and retaining the existing customers as mentioned below,

To be the fourth market leader in local saving all island market within next three years.

To increase the market share of saving account market by 4.3% to 6.5% within next three years.

Retaining 99% of existing customers and develop branch banking with 10 new branch of the year across.

.

Market segment geographic

Covered the full island wide coverage specially in town areas

Industrial areas who worked in private & government sectors

demographic Acceding to the age groupCompany sizeWho has a monthly income up to 10000/- RsWorking people in private and government sectors ReligionYoung generation

PsychographicSocial classLife style Personality characteristics

BehavioralProduct Benefits- Quality vies , interest rate, safety, durability, convenienceLoyalty statuesAttitude towards a product

Targetingfirst how well the existing segment are

served by others, secondly how do we enable to us to grape that market by differentiation.

Who are users and love the brand by nature which is a more behavioral segment and a combination of geo- demographical

Target market is a group of people / companies with a set of common characterizes, for Amana the target market will be the individuals/managements of organization

High service quality

High interest rate

low service quality

low interest rate

Amana salary saver

NTB salary saver

NDB salary max

Govt.banks

marketing mix strategy development product strategy

Amana salary saving account is in introduction stage there for penetration pricing is suit for the product

Also use Amana salary saving account price as competitive and economic pricing which is with the current market strategy to capture all level consumer and it is affordable to them

Promotional strategy

Sales promotion PR activities Free Gift

Radio, TV promotions Personal selling Facebook, Twitter & website

Distribution strategyAt present Amana bank have 27 branches in its branch network in Sri Lanka to distribute the salary saving account to its customers.

Secondly Amana bank use a set of competent sales staff with excellent interpersonal skills and PR is vital for the distribution to take place efficiently.

Physical evidence strategyCorporate ImageWeb page of Amana bank– user friendliness all the labors who works in Amana bank they ware Amana uniform

Process strategyLong term effects, efficiency, flexibility, cost and quality

People strategy

Staffing levelsWage/Benefit tradeoffsReward strategyTraining and Development

Budget and financial analysis Profit and lost statement for 2013/2014

Income Amounts percentage

Sales & Revenue

Expenditure

Operating expenses

Financial expense

Personal expense

Total expenditure

Profit before tax

Income tax expense

Net profit after tax

1,768,061,705

506,427,017

158,282,145

720,351,418

1,385,060,580

383,001,125

(120,971,087)

262,030,038

100%

28%

9%

40%

6%

14%

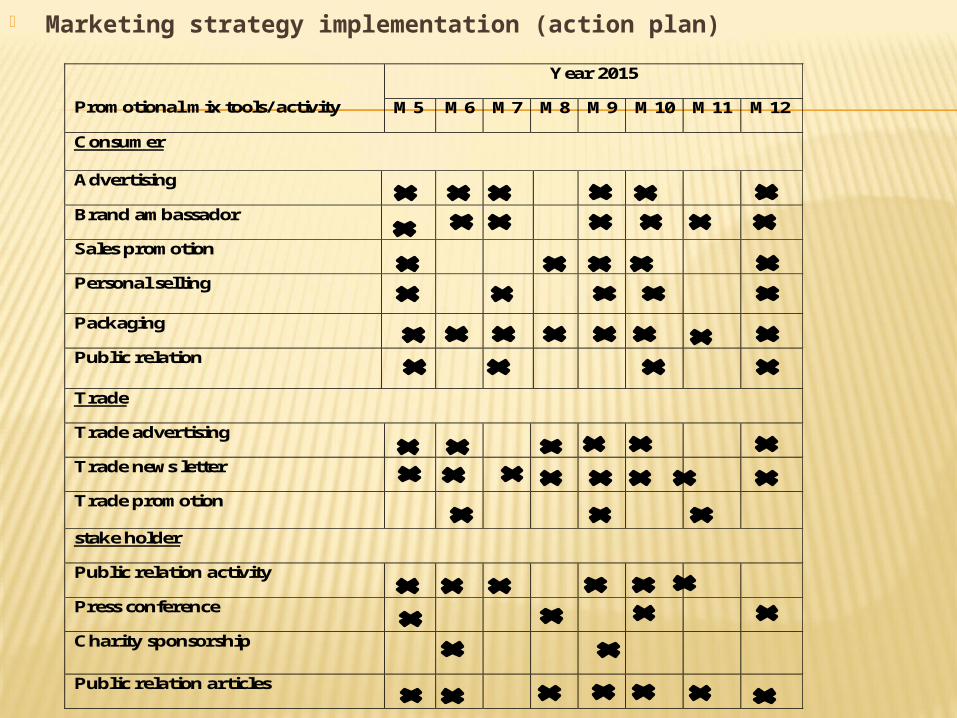

Marketing strategy implementation (action plan)

Promotional mix tools/ activity

Year 2015

M5 M6 M7 M8 M9 M10 M11 M12

Consumer

Advertising

Brand ambassador

Sales promotion

Personal selling

Packaging

Public relation

Trade

Trade advertising

Trade news letter

Trade promotion

stake holder

Public relation activity

Press conference

Charity sponsorship

Public relation articles

Monitoring and evaluation

Monitoring Conducting monthly sales review meetings

Building awareness among sales agents

If any drop in sales, corrective measures should be taken

Training the staff

Motivating the Amana customer service officers

Conducting customer researches

Conducting a market share analysis

Evaluation•Mail and e-mail surveys•Online samples•Communications audits•Telephone surveys•PR audits•CRM•Database searches