Foreign Profitability and Dividend Policy Robert JOLIET FNRS Research Fellow Université de Liège...

18

Foreign Foreign Profitability and Profitability and Dividend Policy Dividend Policy Robert JOLIET Robert JOLIET FNRS Research Fellow FNRS Research Fellow Université de Liège Université de Liège Séminaires de Gestion Séminaires de Gestion

-

Upload

earl-walton -

Category

Documents

-

view

216 -

download

1

Transcript of Foreign Profitability and Dividend Policy Robert JOLIET FNRS Research Fellow Université de Liège...

Foreign Profitability and Foreign Profitability and Dividend PolicyDividend Policy

Robert JOLIETRobert JOLIET

FNRS Research FellowFNRS Research Fellow

Université de LiègeUniversité de Liège

Séminaires de GestionSéminaires de Gestion

22

Multinational Firms & Segmental Financial Multinational Firms & Segmental Financial PerformancePerformance

• Typically, the long-term growth rate of a project will be highly correlated with economic growth in the country, specially in the long-run and according to the firm’s business.

Percentage profitability and earnings vary from one Percentage profitability and earnings vary from one country to another. A relatively “low” profitability in one country to another. A relatively “low” profitability in one country might be acceptable in a different one. country might be acceptable in a different one.

International diversification smoothing effect vs. specific International diversification smoothing effect vs. specific regional effect.regional effect.

33

The Value of Foreign OperationsThe Value of Foreign Operations

Operations in different countries present the firm with different Operations in different countries present the firm with different costs, barriers, political climates and legal restrictions costs, barriers, political climates and legal restrictions Operating regions/countries usually experience varied rates of Operating regions/countries usually experience varied rates of profitability, risk and growth.profitability, risk and growth.

Valuation likely varies depending upon the location of the Valuation likely varies depending upon the location of the operations operations disaggregation needed disaggregation needed

A geographical breakdown of firms’ operations may A geographical breakdown of firms’ operations may provides investors with useful information.provides investors with useful information.

Investors may not fully understand the benefits and risks Investors may not fully understand the benefits and risks involved in the heterogeneous foreign operations involved in the heterogeneous foreign operations tend to tend to underestimate the persistence of foreign earnings.underestimate the persistence of foreign earnings.

IS THERE INTERACTION WITH DIVIDEND POLICY ?IS THERE INTERACTION WITH DIVIDEND POLICY ?

44

The Effect of Segmental Profitability on The Effect of Segmental Profitability on Stock ReturnsStock Returns

Corporate Profitability is an essential key component in Corporate Profitability is an essential key component in the computation of the cost of equity.the computation of the cost of equity.

Expected Dividend Yield Future Growth RateExpected Dividend Yield Future Growth Rate

for a multinational firm for a multinational firm ii, operating in , operating in nn foreign region foreign region jj

55

The Effect of Segmental Profitability on The Effect of Segmental Profitability on Stock Returns (2)Stock Returns (2)

Assuming a changing profitabilityAssuming a changing profitability

associated with associated with associated with associated with

forthcomingforthcoming projects projects existingexisting projects projects

66

Dividend Yield & Segmental ProfitabilityDividend Yield & Segmental Profitability

Depends on the investment growth opportunities available Depends on the investment growth opportunities available (investors’ expectations & agency costs problems)(investors’ expectations & agency costs problems)

Signalling effectsSignalling effects

77

Empirical AnalysisEmpirical Analysis388 firms from North America, Europe, and Australasia388 firms from North America, Europe, and AustralasiaStudy on a 10 year period (1993-2003)Study on a 10 year period (1993-2003)Based on incremental regional accounting profitability Based on incremental regional accounting profitability (ROIC) with respect to the domestic one (levels and (ROIC) with respect to the domestic one (levels and changes).changes).Regional and Country-specific analysisRegional and Country-specific analysisSimultaneous and lagged stock returns, following the Simultaneous and lagged stock returns, following the firm’s fiscal yearfirm’s fiscal yearDividend-paying stocks vs. Non-dividend-paying stocksDividend-paying stocks vs. Non-dividend-paying stocksDividend per share adjusted for stock splitsDividend per share adjusted for stock splitsYear, industry and firm’s nationality (fixed) effects.Year, industry and firm’s nationality (fixed) effects.

88

A. Dividend-Paying StocksA. Dividend-Paying Stocks

99

Empirical Analysis (1) : Empirical Analysis (1) : Dividend-Paying stocksDividend-Paying stocks – –SimultaneousSimultaneous Stock Returns & Segmental Profitability Stock Returns & Segmental Profitability

1010

Empirical Analysis (2) : Empirical Analysis (2) : Dividend-Paying stocksDividend-Paying stocks – – LaggedLagged Stock Returns & Segmental Profitability Stock Returns & Segmental Profitability

1111

Empirical Analysis (3) : Empirical Analysis (3) : Dividend-paying stocksDividend-paying stocks – – LaggedLagged Stock Stock Returns & Segmental Profitability Variation, Dividend YieldReturns & Segmental Profitability Variation, Dividend Yield

1212

Empirical Analysis (4) : Empirical Analysis (4) : Dividend-payingDividend-paying stocks – stocks – Expected Expected Dividend YieldDividend Yield & Segmental Profitability & Segmental Profitability

1313

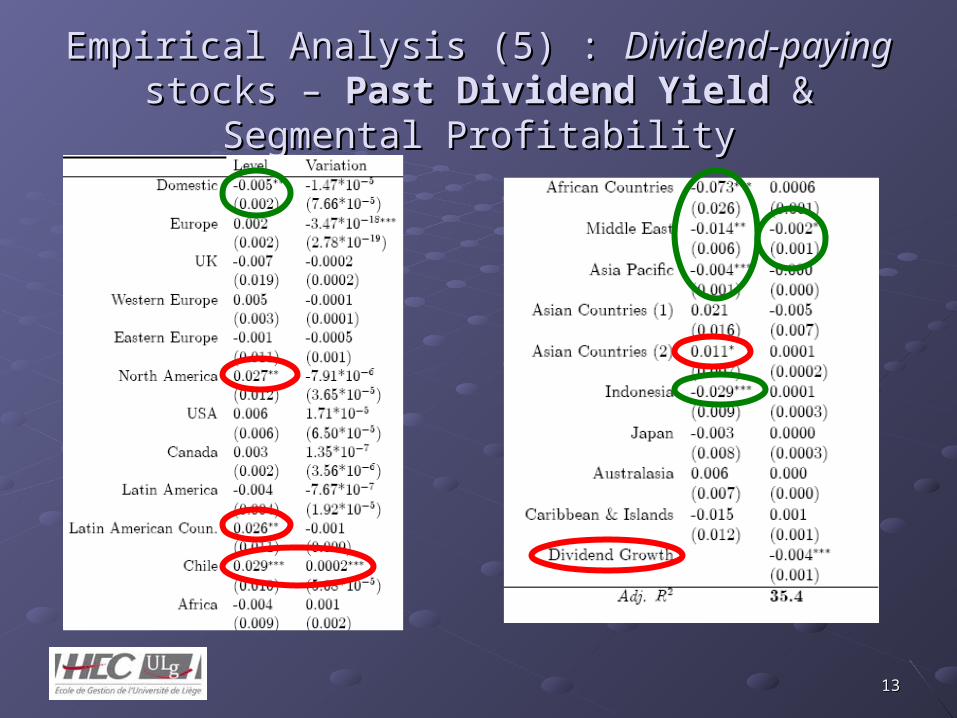

Empirical Analysis (5) : Empirical Analysis (5) : Dividend-payingDividend-paying stocks – stocks – Past Dividend YieldPast Dividend Yield & Segmental Profitability & Segmental Profitability

1414

B. Non-Dividend-Paying StocksB. Non-Dividend-Paying Stocks

1515

Empirical Analysis (6) : Empirical Analysis (6) : Non-Dividend-payingNon-Dividend-paying stocks – stocks – SimultaneousSimultaneous Stock Returns & Segmental Profitability Stock Returns & Segmental Profitability

1616

Empirical Analysis (7) : Empirical Analysis (7) : Non-Dividend-payingNon-Dividend-paying stocks – stocks – LaggedLagged Stock Returns & Segmental Profitability Stock Returns & Segmental Profitability

1717

Concluding RemarksConcluding Remarks

The relation between geographical profitability The relation between geographical profitability and common equity valuation depends on and common equity valuation depends on investors’ expectations and whether a firm pays investors’ expectations and whether a firm pays dividends.dividends.

Dividend Policy seems to give a sign to investors Dividend Policy seems to give a sign to investors about the profitability and the investment about the profitability and the investment opportunities in the different area of opportunities in the different area of operations.The dividend yield tends to be operations.The dividend yield tends to be pushed down by operating regions/countries pushed down by operating regions/countries with sustainable growth opportunities.with sustainable growth opportunities.

1818

Thank you for your attentionThank you for your attention