Foreign Exchange Healthcare Best Practices Discussion exchange transactions can be highly risky, and...

29

Foreign Exchange April 27, 2016 Healthcare Best Practices Discussion

Transcript of Foreign Exchange Healthcare Best Practices Discussion exchange transactions can be highly risky, and...

Arial 2015 4

:3

Foreign Exchange

April 27, 2016

Healthcare Best Practices Discussion

Arial 2015 4

:3

2

Today’s agenda

• Introduction

• Foreign Exchange Landscape

• Hedging 101

• Solutions

• Case Study

Arial 2015 4

:3

3

Foreign Exchange Landscape

Peter Compton Senior Foreign Exchange

Advisor

Arial 2015 4

:3

4 4

Euro - EUR/USD 1 Euro buys 1.13 US Dollars

British Pound - GBP/USD 1 Pound buys 1.43 US Dollars

Canadian Dollar - USD/CAD 1 US Dollar buys 1.28 Canadian Dollars

Swiss Franc - USD/CHF 1 US Dollar buys 0.97 Swiss Francs

Australian Dollar- AUD/USD 1 Australian Dollar buys 0.77 US Dollars

Swedish Krona - USD/SEK 1 US Dollar buys 8.14 Swedish Krona

Japanese Yen - USD/JPY 1 US Dollar buys 109 Japanese Yen

Frequently used Foreign Currencies for Life Sciences Companies

Arial 2015 4

:3

5 5

Life Sciences Company FX Exposure Causes BioTech Distributors, Partnerships, Materials

Drug Discovery International Clinical Trials

Medical Device Manufacturing Contracts, R&D

Healthcare IT Overseas Developers

Life Sciences Companies and Foreign Currencies

Most Companies Eventually Have FX Exposure: Sales/Receivables, Contractors, Vendors

Acquisitions

Investors

Funding Subsidiaries

Repatriating Profits

Arial 2015 4

:3

6

What Drives Currency Exchange Rates

• Economics

– GDP Growth

– Interest Rates Expectations (Higher Rate = Stronger Currency)

– Geopolitical Risks

• Market Participants in $5 Trillion Global Market

– Speculators

– Global Investors and Sovereign Wealth Funds

– Central Banks (Intervention)

– Corporations (8%)

Arial 2015 4

:3

7

EUR: European Economy Weaker than US Economy

‣ Deflation a problem in Europe. Quantitative easing negative for the euro.

‣ Euroland negative interest rates vs. the US where interest rates are headed higher.

‣ Geopolitical risks favor euro?

Source: Bloomberg.

Price of 1 euro in US Dollars

0.8

0.9

1

1.1

1.2

1.3

1.4

1.5

1.6

1.1262

+80.55% (+13.80% ann.)

-20.77%

Arial 2015 4

:3

8

GBP: It’s all about the “Brexit”

‣ June 23, 2016 referendum on UK remaining in EU. Uncertainty will lead to GBP weakness.

‣ The Fed raising rates ahead of the UK Monetary Policy Committee.

‣ Huge support at 1.40.

Source: Bloomberg.

1.35

1.4

1.45

1.5

1.55

1.6

1.65

1.7

1.75

1.4157 UK elections

Brexit uncertainty

Price of 1 Pound in US Dollars

Arial 2015 4

:3

9

Hedging 101

Nate Wyne Senior Foreign Exchange Advisor

Arial 2015 4

:3

10

FX Risk Management

• Primary Goal: Cash-flow / Earnings Certainty

– Mitigate fluctuations in the USD value of foreign denominated exposures

– NOT speculation on direction of foreign currency rates

• A prudently implemented risk management policy, consistently

applied, seeks to achieve discrete periods of cash flow certainty

More

Stable/Certain

Cash Flows

More

Stable/Certain

Earnings

Higher

Firm

Valuation

= =

Arial 2015 4

:3

11

Foreign Exchange Risk Management • Non-functional Currency Exposure

– Foreign revenue billed/collected out of US entity

• Fluctuations in FX rates cause significant false noise in financial statements

• Primary Concerns: Re-measurement Risk & Cash-flow Risk

• Control of Foreign Exchange G/L line

Key constraint: Lean finance team, fast moving company. Hedge program must be easy to administer.

• Isolate FX volatility from earnings to provide key business insights on core business

vs. market noise.

• Streamline FX operations to allow finance teams to focus on a way forward under a

solid policy with clearly defined roles/operations.

Arial 2015 4

:3

12

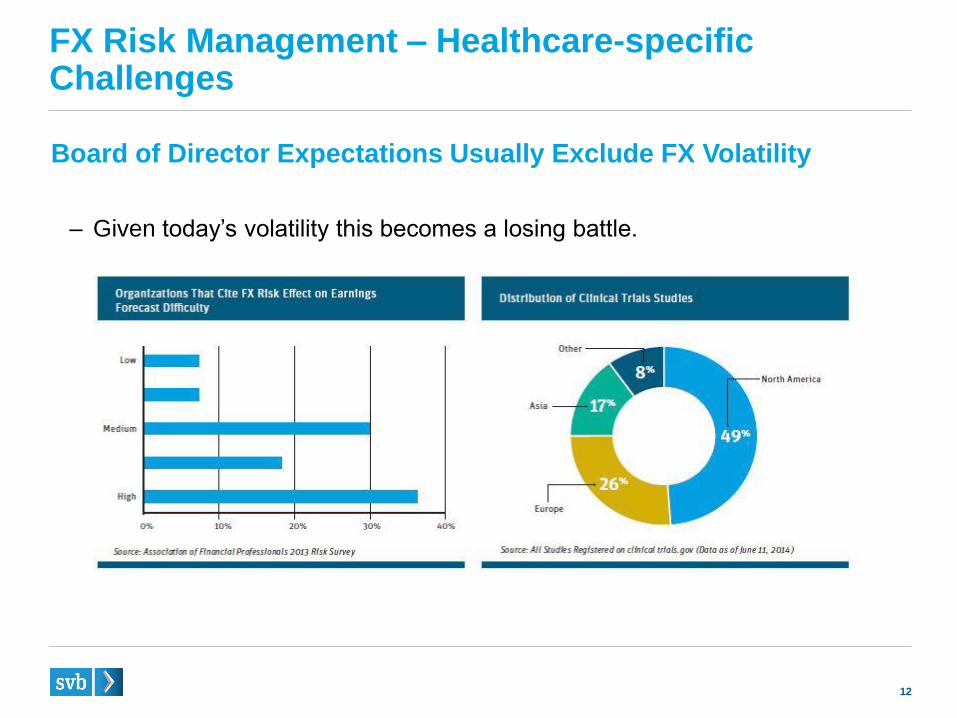

FX Risk Management – Healthcare-specific Challenges

Board of Director Expectations Usually Exclude FX Volatility

– Given today’s volatility this becomes a losing battle.

Arial 2015 4

:3

13

Hedging Foreign Exchange – Instruments Used

• FX Forwards / Swaps

– Traditional

– Window

– Non-Deliverable (NDF)

• FX Options

• Structured Products (combination of purchased/sold options)

Most (over 90%) hedging companies use forwards (and swaps) for hedging.

Simple, efficient, transparent, no upfront cost, simplifies hedge accounting treatment.

Arial 2015 4

:3

14

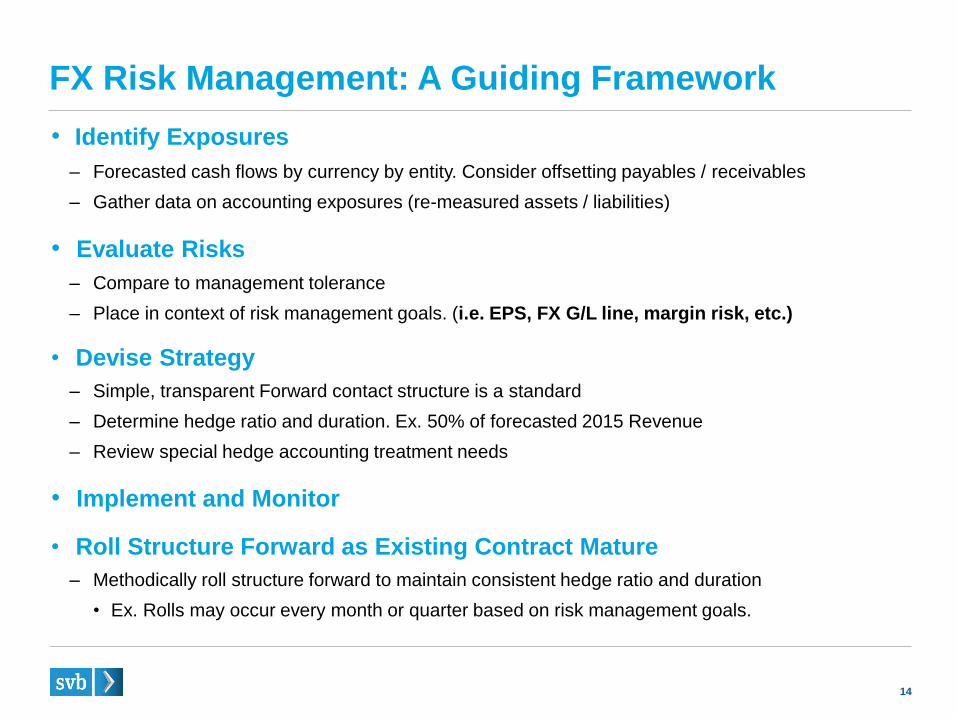

FX Risk Management: A Guiding Framework

• Identify Exposures

– Forecasted cash flows by currency by entity. Consider offsetting payables / receivables

– Gather data on accounting exposures (re-measured assets / liabilities)

• Evaluate Risks

– Compare to management tolerance

– Place in context of risk management goals. (i.e. EPS, FX G/L line, margin risk, etc.)

• Devise Strategy

– Simple, transparent Forward contact structure is a standard

– Determine hedge ratio and duration. Ex. 50% of forecasted 2015 Revenue

– Review special hedge accounting treatment needs

• Implement and Monitor

• Roll Structure Forward as Existing Contract Mature

– Methodically roll structure forward to maintain consistent hedge ratio and duration

• Ex. Rolls may occur every month or quarter based on risk management goals.

Arial 2015 4

:3

15

Solutions

Arial 2015 4

:3

16

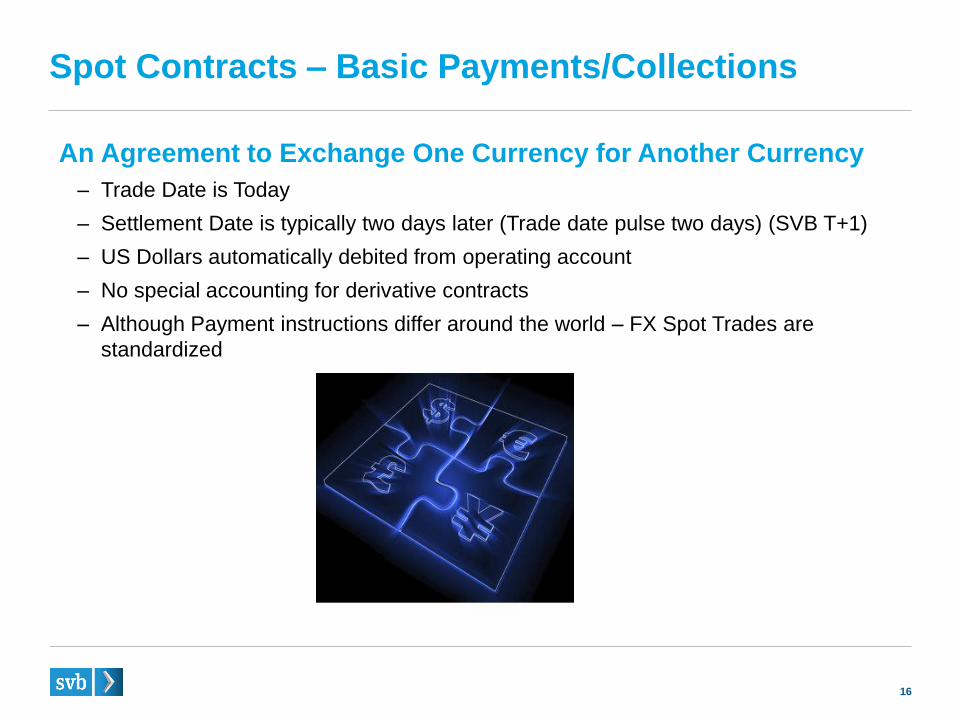

Spot Contracts – Basic Payments/Collections

An Agreement to Exchange One Currency for Another Currency

– Trade Date is Today

– Settlement Date is typically two days later (Trade date pulse two days) (SVB T+1)

– US Dollars automatically debited from operating account

– No special accounting for derivative contracts

– Although Payment instructions differ around the world – FX Spot Trades are

standardized

Arial 2015 4

:3

17

Forward and Forward Window Contracts Hedge currency exposure for more predictable cash flows

Benefits of using Forward Contract

– Can establish up to 100% certainty the

exchange or conversion rate of a currency on a

future settlement or delivery date

– Inexpensive method of managing currency risk

– Offers flexibility with regard to the amount of the

currency exposure to be hedged

– The buyer of the contract can exercise multiple

drawdowns until the contract amount is used

up.

Arial 2015 4

:3

18

Non-Deliverable Forward (NDF) Contacts

– Like an outright FX Forward only net settled in USD

– Some currencies don’t have an efficient outright FX Forward market (INR, BRL, CNY)

– Hedge a subsidiary’s FX exposure at parent level

– Balance Sheet hedging or Cash Flow hedging

Example: Hedge a Renminbi (Yuan) Expense at USD/CNY 6.5 due in 90 Days

Enter NDF to Buy CNY 6,500,000 and Sell USD 1,000,000

Calculation of NDF Net Settlement Amount

Arial 2015 4

:3

19

Swaps Manage Cash Flow & Maturity Dates for Foreign Currency Transactions

Benefits of FX Swaps

– Avoidance of unnecessary foreign exchange losses

– “Borrow” foreign currency by buying the currency spot and simultaneously agreeing to

sell the currency back at a future date

– Accelerate the settlement of an existing forward contract

– Extend or delay the settlement of an existing forward contract

Arial 2015 4

:3

20

Over-the-Counter Options Contract Hedge Currency Exposure with Tailored Options Contracts

Benefits of doing Over-the-Counter (OTC) Options

– Provides insurance against unfavorable currency movements

– Unlimited gains potential

– Hedge risk with the possibility to reduce or eliminate premiums

Arial 2015 4

:3

21

Foreign Currency Account (FCA):

A deposit account where funds can be held in a foreign currency

Buy and hold foreign currency until needed for expenses

Provides certainty with regard to FX rate (preserve cash, meet budget)

Domiciled in the Untied States

Able to wire currency into and out of FCA account

No need for derivative accounting/disclosures

Creates a foreign currency denominated asset which will gain/lose value

Does not allow for benefit of favorable movement in FX rate

Arial 2015 4

:3

22

Case Study

Arial 2015 4

:3

23

FX Healthcare Client Case Study - Tandem

Overview:

Tandem is a medical device company with an innovative approach to the design,

development and commercialization of a family of products for people with insulin-

dependent diabetes.

Tandem FX Hedging:

Why are we hedging our foreign currency exposures: one of our vendors is located in

Finland. We purchase high dollar large equipment form them. The EUR amount of these

purchases in known months in advance of payment. We enter into forward contracts to

protect our budget in hopes of avoiding budget variances due to fluctuations in the foreign

currency market.

Client:

Denise Lamas, Sr. Manager,

General Accounting

Arial 2015 4

:3

24

Questions?

Arial 2015 4

:3

25

Appendix

Arial 2015 4

:3

26

Peter Compton

Senior Foreign Exchange Advisor

Silicon Valley Bank

617-630-4136

Peter Compton is a senior foreign exchange advisor

for Silicon Valley Bank’s global financial services

group, and has been with SVB since 2007. He helps

clients design and implement hedging strategies for

foreign currency exposures. Compton has over 20

years experience in global financial markets.

Before joining Silicon Valley Bank, Compton spent

seven years working in the European equity markets.

Based in Germany, he spent four years with HSBC

and three years as Head of Equity Sales for ABN-

AMRO in Frankfurt. Prior to his work overseas,

Compton spent seven years with Bank of America in

San Francisco as an equity and fixed income

derivative specialist.

Compton holds a bachelor's degree in business and

management from the University of Rhode Island and

a Master's of Business Administration from San

Francisco State University.

Arial 2015 4

:3

27

Nate Wyne

Senior Foreign Exchange Advisor

Silicon Valley Bank

310.237.3489

Nate Wyne is the Southern California foreign

exchange advisor for Silicon Valley Bank. Nate hold a

bachelor’s degree from the University of Utah in

international studies for business.

Nate partners with his clients to create and implement

sound risk-management practices around foreign

exchange and cash management.

After completing his undergraduate degree, Nate

pursued a career in retail banking before moving to

commercial and eventually corporate banking. With

13 years of banking experience across the full gamut

of advisory roles – Nate enjoys helping growing

businesses focus on what they do best.

Arial 2015 4

:3

28

Disclaimer

Foreign exchange transactions can be highly risky, and losses may occur in short periods

of time if there is an adverse movement of exchange rates. Exchange rates can be highly

volatile and are impacted by numerous economic, political and social factors, as well as

supply and demand and governmental intervention, control and adjustments. Investments

in financial instruments carry significant risk, including the possible loss of the principal

amount invested. Before entering any foreign exchange transaction, you should obtain

advice from your own tax, financial, legal and other advisors, and only make investment

decisions on the basis of your own objectives, experience and resources. Opinions

expressed are our opinions as of the date of this content only. The material is based upon

information which we consider reliable, but we do not represent that it is accurate or

complete, and it should not be relied upon as such.

©2016 SVB Financial Group. All rights reserved. Silicon Valley Bank is a member of FDIC

and Federal Reserve System. SVB>, SVB Financial Group, and Silicon Valley Bank are

registered trademarks.

Arial 2015 4

:3

Thank you

www.svb.com