Foreign Corrupt Practices Act in India...

39

Presenting a live 90‐minute webinar with interactive Q&A Foreign Corrupt Practices Act in India 2012 Compliance Strategies for India's Unique Cultural and Governmental Intricacies Today’ s faculty features: 1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific TUESDAY, MAY 8, 2012 Today s faculty features: Jay Holtmeier, Partner, Wilmer Cutler Pickering Hale and Dorr, New York Elizabeth D. Keating, Vice President, Legal Compliance/ Building Efficiency, Johnson Controls, Milwaukee, Wis. Jonathan C. Feig, Partner, Ernst & Young, Chicago The audio portion of the conference may be accessed via the telephone or by using your computer's speakers. Please refer to the instructions emailed to registrants for additional information. If you have any questions, please contact Customer Service at 1-800-926-7926 ext. 10.

Transcript of Foreign Corrupt Practices Act in India...

Presenting a live 90‐minute webinar with interactive Q&A

Foreign Corrupt Practices Act in India 2012Compliance Strategies for India's Unique Cultural and Governmental Intricacies

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

TUESDAY, MAY 8, 2012

Today s faculty features:

Jay Holtmeier, Partner, Wilmer Cutler Pickering Hale and Dorr, New York

Elizabeth D. Keating, Vice President, Legal Compliance/ Building Efficiency, Johnson Controls, Milwaukee, Wis.

Jonathan C. Feig, Partner, Ernst & Young, Chicago

The audio portion of the conference may be accessed via the telephone or by using your computer's speakers. Please refer to the instructions emailed to registrants for additional information. If you have any questions, please contact Customer Service at 1-800-926-7926 ext. 10.

Conference Materials

If you have not printed the conference materials for this program, please complete the following steps:

• Click on the + sign next to “Conference Materials” in the middle of the left-hand column on your screen hand column on your screen.

• Click on the tab labeled “Handouts” that appears, and there you will see a PDF of the slides for today's program.

• Double click on the PDF and a separate page will open. Double click on the PDF and a separate page will open.

• Print the slides by clicking on the printer icon.

Continuing Education Credits FOR LIVE EVENT ONLY

For CLE purposes, please let us know how many people are listening at your location by completing each of the following steps:

• In the chat box, type (1) your company name and (2) the number of attendees at your locationattendees at your location

• Click the SEND button beside the box

Tips for Optimal Quality

S d Q litSound QualityIf you are listening via your computer speakers, please note that the quality of your sound will vary depending on the speed and quality of your internet connection.

If the sound quality is not satisfactory and you are listening via your computer speakers, you may listen via the phone: dial 1-866-961-8499 and enter your PIN when prompted Otherwise please send us a chat or e mail PIN -when prompted. Otherwise, please send us a chat or e-mail [email protected] immediately so we can address the problem.

If you dialed in and have any difficulties during the call, press *0 for assistance.

Viewing QualityTo maximize your screen, press the F11 key on your keyboard. To exit full screen, press the F11 key againpress the F11 key again.

FCPA Compliance in India: Compliance Strategies Given India’sCompliance Strategies Given India sUnique Cultural and Governmental

Intricacies

Strafford Publications TeleconferenceMay 8 2012May 8, 2012

Jonathan C. FeigErnst & Young LLP

Jay HoltmeierWilmer Cutler Pickering Hale and Dorr LLP

Elizabeth D KeatingElizabeth D. KeatingJohnson Controls, Inc.

OVERALL FCPA ENFORCEMENT TRENDSOVERALL FCPA ENFORCEMENT TRENDS “In the Criminal Division, we have dramatically

increased our enforcement of the Foreign Corruptincreased our enforcement of the Foreign Corrupt Practices Act in recent years.... We recently promoted a [n]ew head of the Section’s FCPA Unit and two assistant chiefs, and we have also increased the ,number of line prosecutors in the Unit, attracting high caliber attorneys with extensive experience—including Assistant U.S. Attorneys with significant trial and y gprosecutorial experience and attorneys from private practice with defense-side knowledge and experience. These changes have significantly increased our FCPA enforcement capabilities.”

– Assistant Attorney General Lanny Breuer (Jan. 2011)

6

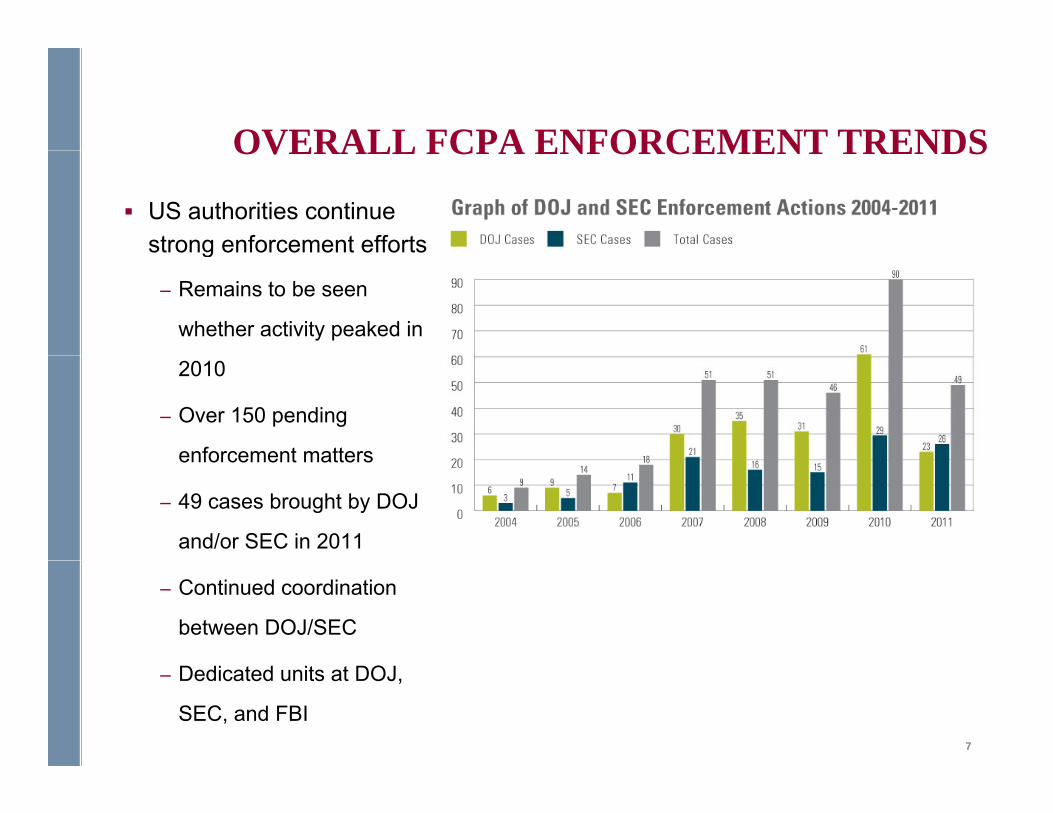

OVERALL FCPA ENFORCEMENT TRENDSOVERALL FCPA ENFORCEMENT TRENDS

US authorities continue strong enforcement efforts Reported FCPA Proceedingsg

– Remains to be seen

whether activity peaked in

Reported FCPA Proceedings

2010

– Over 150 pending

enforcement mattersenforcement matters

– 49 cases brought by DOJ

and/or SEC in 2011

– Continued coordination

between DOJ/SEC

7

– Dedicated units at DOJ,

SEC, and FBI

OVERALL FCPA ENFORCEMENT TRENDSOVERALL FCPA ENFORCEMENT TRENDS Large FCPA Sanctions Continue; Three of the Top 11 Corporate FCPA

Settlements Occurred in 2011

– JGC (Japan; $219M)

– Magyar Telekom/ Deutsche Telekom (Hungary/Germany; $95M)

J h & J h (US $70M)– Johnson & Johnson (US; $70M)

Prosecution of Individuals is Continued Priority

Third Party Risks (e.g., sales agents, intermediaries, consultants )

Travel and Entertainment in High-Risk Markets

Industry-Specific Risks (e.g., SEC probe of movie studios operating in China)

New Tool at the SEC – Deferred Prosecution Agreements New Tool at the SEC – Deferred Prosecution Agreements

Intersection of FCPA and Antitrust (e.g., Bridgestone Corporation settlement)

Shift Away from Compliance Monitors; Increased Use of Alternatives

New Developments – Morgan Stanley and Wal-Mart

8

FCPA ENFORCEMENT ACTIONS RELATED TO INDIA

Diageo (2011)Diageo is one of the orld’s largest prod cers of alcoholic– Diageo is one of the world’s largest producers of alcoholic beverages such as Johnnie Walker and Windsor Scotch whiskeys. From 2003 to mid-2009, Diageo’s Indian subsidiary made a number of illicit payments to government officials through thirdnumber of illicit payments to government officials through third parties totaling an estimated $1.7M.

– Diageo settled with the SEC for $16M including $11.3M in di t j d t i t t f $2 1M d f thdisgorgement, prejudgment interest of $2.1M, and a further penalty of $3M. The DOJ was not involved in this matter.

9

FCPA ENFORCEMENT ACTIONS RELATED TO INDIA

Pride International (2010)– Pride International is an oil and gas service company. Pride’s

Indian subsidiary paid $500K to judges of the Indian Customs, Excise, and Gold Appellate Tribunal for a favorable determination in a customs duties and penalties dispute. The estimated value of the favorable decision was approximately $1M.

– Pride’s Indian subsidiary pleaded guilty to criminal charges in the United States. Pride International and the Indian subsidiary ysettled with the SEC and agreed to pay a $32M criminal penalty. Pride International settled similar civil charges with the SEC and agreed to pay disgorgement of $19.3M plus pre-judgment interest of $4.2M.

10

FCPA ENFORCEMENT ACTIONS RELATED TO INDIA

Control Components, Inc. (2009)– CCI designs and manufactures valves used in the power, oil and

gas, and nuclear industries. CCI made payments of at least $4.9M from 2003 – 2007 to employees of state-owned companies in several countries, including in India to the Maharashtra State Electricity Board.

– CCI pleaded guilty to criminal charges and paid an $18.2M fine. Additionally, the company was placed on organizational probation y p y p g pfor three years and ordered to create and implement a compliance program and retain an independent compliance monitor for three years.

11

FCPA ENFORCEMENT ACTIONS RELATED TO INDIA

Westinghouse Air Brake Technologies (2008)– WABTEC manufactures brake subsystems and related products for

locomotives, freight cars, and passenger transit vehicles. From 2001 through 2005, WABTEC’s subsidiary paid approximately $137K in cash to the Indian Railway Board to obtain contracts, schedule inspections, obtain certificates, and avoid tax audits

– WABTEC and its subsidiary entered into settlement agreements with the DOJ and the SEC. WABTEC paid a $300K criminal penalty, $288K in p p ydisgorgement of profits including pre-judgment interest, and $89K in civil penalties (a total of approximately $677K).

12

FCPA ENFORCEMENT ACTIONS RELATED TO INDIA

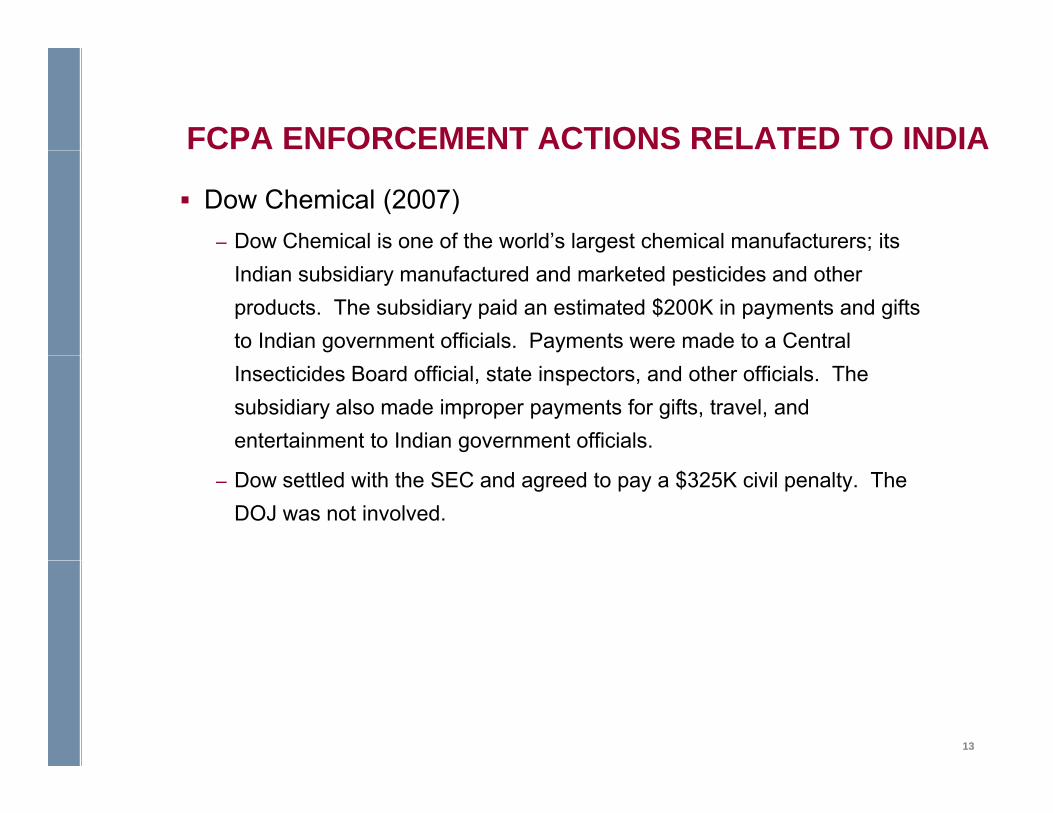

Dow Chemical (2007)– Dow Chemical is one of the world’s largest chemical manufacturers; its

Indian subsidiary manufactured and marketed pesticides and other products. The subsidiary paid an estimated $200K in payments and gifts to Indian government officials. Payments were made to a Central Insecticides Board official, state inspectors, and other officials. The subsidiary also made improper payments for gifts, travel, and entertainment to Indian government officials.

– Dow settled with the SEC and agreed to pay a $325K civil penalty. The DOJ was not involved.

13

FCPA ENFORCEMENT ACTIONS RELATED TO INDIA

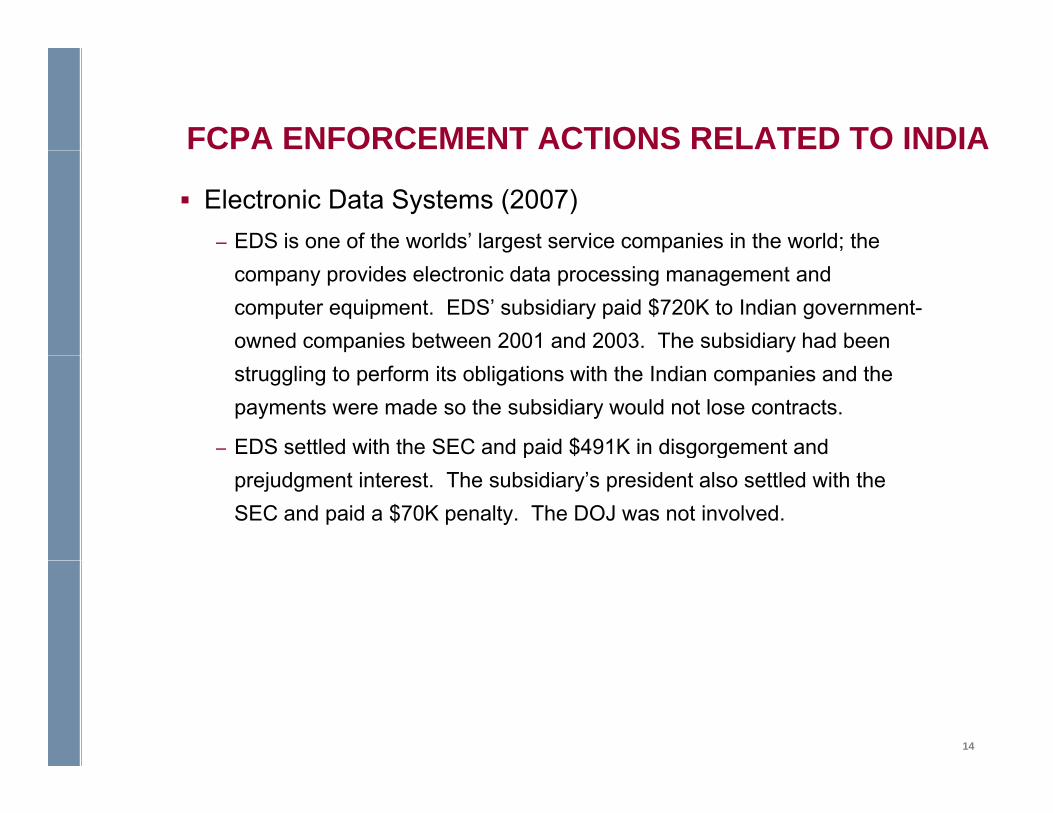

Electronic Data Systems (2007)– EDS is one of the worlds’ largest service companies in the world; the

company provides electronic data processing management and computer equipment. EDS’ subsidiary paid $720K to Indian government-owned companies between 2001 and 2003. The subsidiary had been struggling to perform its obligations with the Indian companies and the payments were made so the subsidiary would not lose contracts.

– EDS settled with the SEC and paid $491K in disgorgement and p g gprejudgment interest. The subsidiary’s president also settled with the SEC and paid a $70K penalty. The DOJ was not involved.

14

FCPA ENFORCEMENT ACTIONS RELATED TO INDIA

Textron Inc. (2007)– Textron is a global, multi-industry company which does work in aircraft,

defense and intelligence, industrial, and finance businesses. As part of an investigation into $700K in kickback payments related to its sale of humanitarian goods to Iraq under the UN’s oil for food program, Textron identified an illicit payment by an Indian subsidiary of approximately $52K to a non-government customer to obtain business.

– As part of a settlement, Textron agreed to disgorge $2.3M in profits, plus p g g g p p$450K in pre-judgment interest, and to pay a civil penalty of $800K. Textron was also ordered to comply with an FCPA compliance program. Textron was further ordered to pay a $1.15M fine pursuant to a non-prosecution agreement with the DOJ.

15

FCPA CURRENT INVESTIGATIONS RELATED TO INDIA

Kraft Foods– Kraft Foods, a food and beverage company, has disclosed that it is

currently being investigated by the SEC in connection with a facility in India that was part of its $19B acquisition of Cadbury in 2010. Kraft has disclosed that the SEC wants information about its "dealings with Indian governmental agencies and officials to obtain approvals related to the operation" of the India plant.

Avon Products– Avon Products, a cosmetics, perfume, and toy seller, has disclosed that

the SEC has issued a formal order of investigation into possible violations of the FCPA. According to Avon, the investigation is focused g , gon expenses and accounting for travel, entertainment, gifts, use of third-party vendors and consultants, and related due diligence, joint ventures, and acquisitions, and payments to third-party agents and others. q p y p y g

16

CONTACTS WITH GOVERNMENT OFFICIALS IN INDIA

Public procurement/contracting with government agenciesg g g

Customs clearance/importation of goods

Immigration processes

Real estate (both purchasing and leasing land) Real estate (both purchasing and leasing land)

Tax administration (excise and sales taxes, audits)

Obtaining certificates, registrations, permits, and licenses (approval from multiple officials often required to obtain one permit/license)

Gifts and entertainment (especially during religious festival, Diwali)

Scheduling/passing inspections (fire, environmental, building)

Government officials solicit donations for charitable/religious organizations

Interactions with police/judiciary

Third parties with ties to government departments/officials (consultants Third parties with ties to government departments/officials (consultants, agents, distributors, interns, and trainees)

17

FCPA Compliance Risks in India

Johnson Controls Confidential

Corruption Risk Profile - India

Transparency International - Corruption Perceptions Index (CPI) 2011 India ranked 95th out of 183 (tied with Albania, Swaziland and Tonga) Score of 3.1 out of 10 (0 = highly corrupt; 10=very clean) Down from 87th in 2010 In comparison: New Zealand ranked 1st; Somalia and North Korea ranked 182nd

TI Global Corruption Barometer 2010/2011 74% of those surveyed in India believed that corruption in their country had 74% of those surveyed in India believed that corruption in their country had

worsened Political parties, police, public officials, judiciary were all perceived to be affected

by corruption 44% believed that their government’s actions to fight corruption were ineffective

TI Bribe Payers Index 84% of Indian companies believe bribes or facilitation payments are being paid to

do businessdo business 30% of Indian companies reported paying bribes to government officials to

expedite government services 54% of individuals surveyed reported paying a bribe to obtain government services

Johnson Controls Confidential19

Risks in Dealing with India Bureaucracy

Challenges Presented by Regulatory and Business Environment Excessive bureaucracy and regulation Procedures are complicated and not transparent Procedures are complicated and not transparent Several layers of approvals required to obtain licenses/permits Practice of using “agents” to interface with government agencies

Ci il t l d id Civil servants grossly underpaid Accepted practice of “tips” or facilitation payments to civil servants in

order to obtain routine government services Seen as an accepted method of augmenting meager salaries Seen as an accepted method of augmenting meager salaries

Prevention of Corruption Act Prohibits public servants from accepting bribe P hibit i i f b ib t bli t Prohibits giving of bribes to public servants No exception for facilitation payments Inconsistent enforcement

Johnson Controls Confidential20

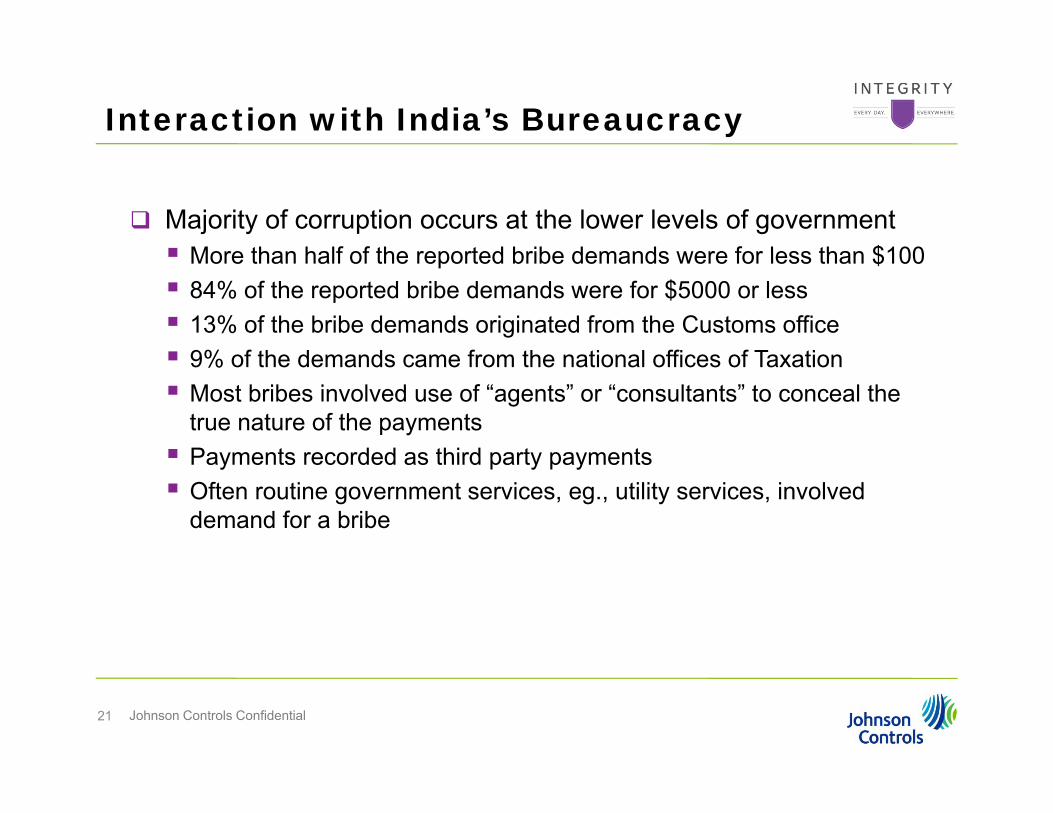

Interaction with India’s Bureaucracy

Majority of corruption occurs at the lower levels of government More than half of the reported bribe demands were for less than $100 More than half of the reported bribe demands were for less than $100 84% of the reported bribe demands were for $5000 or less 13% of the bribe demands originated from the Customs office 9% of the demands came from the national offices of Taxation 9% of the demands came from the national offices of Taxation Most bribes involved use of “agents” or “consultants” to conceal the

true nature of the payments Payments recorded as third party paymentsPayments recorded as third party payments Often routine government services, eg., utility services, involved

demand for a bribe

Johnson Controls Confidential21

Interaction with India’s Bureaucracy

Government Touch Points: Taxing Authorities Variety of taxing regimes provide “opportunities” for bribery Variety of taxing regimes provide opportunities for bribery Income taxes – tax on profits earned by business Tax Deducted at Source (TDS) – tax deducted from certain vendors.

Monthly returns and payments to the exchequerMonthly returns and payments to the exchequer Service taxes – central indirect tax on services rendered by company.

Monthly filings and payments to central treasury Value Added Tax (VAT) – state tax on sale of certain goodsValue Added Tax (VAT) state tax on sale of certain goods Works Contract Tax – part of VAT Tax law and applicable to specific

portion of contract Central Sales Tax – tax on sale of goods from one state to anotherg Central Excise – tax on manufactured goods Service Tax – tax on services provided to customer

Use of Consultants to prepare and file tax reports

Johnson Controls Confidential

Use of Consultants to prepare and file tax reports

22

Interaction with India’s Bureaucracy

Government Touch Points: Licenses, Permits and Inspections Licensing and permitting regulations are duplicated by national state Licensing and permitting regulations are duplicated by national, state

and local agencies Many licenses and permits require several visits to government offices Frequent requests for bribes from government employees to renderFrequent requests for bribes from government employees to render

routine government services Refusal to pay will often result in prolonged application process Many company employees do not distinguish between facilitationMany company employees do not distinguish between facilitation

payments and payments made to impact outcome of inspection report Government employees will often require that you make payment to a

“trusted” third party who will, in turn, funnel the money to the government employee “Government liaison” services offered by certain vendors Vendors will even provide a schedule of rates for amount of facilitation

payments required by the various agencies

Johnson Controls Confidential

payments required by the various agencies

23

Interaction with India’s Bureaucracy

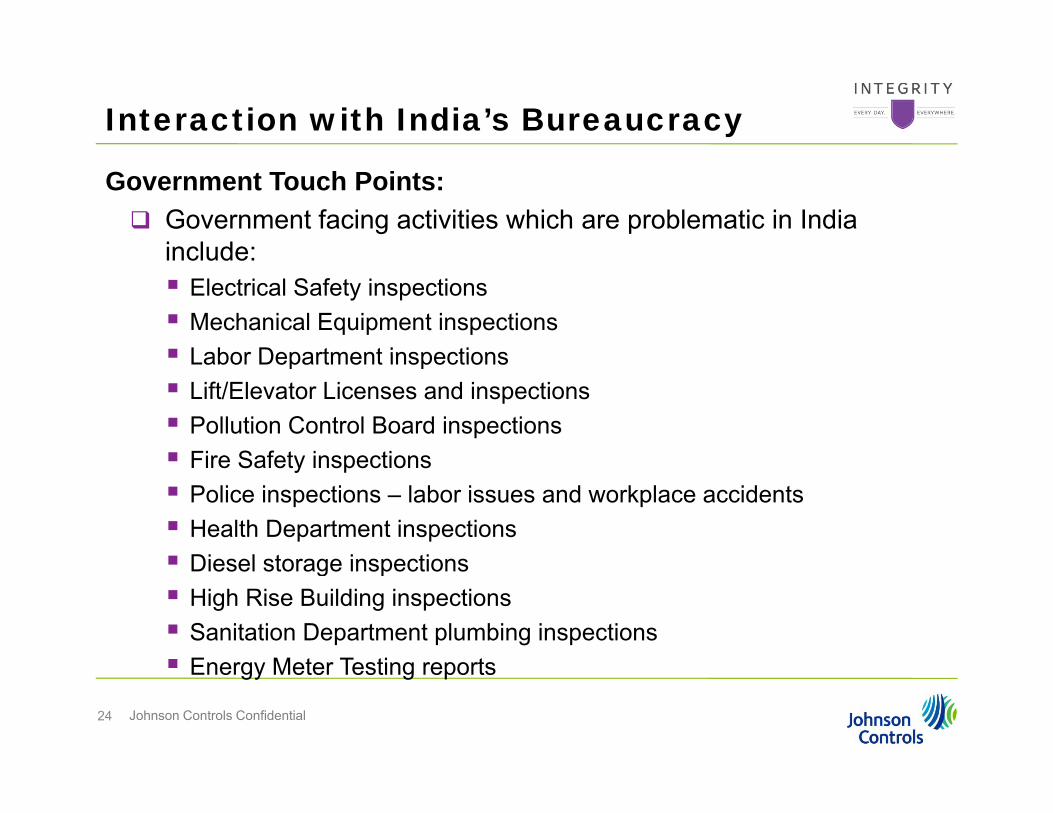

Government Touch Points: Government facing activities which are problematic in India

include:include: Electrical Safety inspections Mechanical Equipment inspections Labor Department inspections Labor Department inspections Lift/Elevator Licenses and inspections Pollution Control Board inspections Fire Safety inspections Fire Safety inspections Police inspections – labor issues and workplace accidents Health Department inspections Diesel storage inspections Diesel storage inspections High Rise Building inspections Sanitation Department plumbing inspections Energy Meter Testing reports

Johnson Controls Confidential

Energy Meter Testing reports

24

Interaction with India’s Bureaucracy

Government Touch Points: Government facing activities which are problematic in India

include:include: Environmental licenses CEIG Licenses for electrical systems Fire licenses Fire licenses Explosive licenses Commercial use clearances Air Consent (Operation & Establishment) Air Consent (Operation & Establishment) Occupation certificate from local authority Annual Operations renewal Structural certificate for floor load density Structural certificate for floor load density Water Consent Hazardous Waste Handling and Disposal Consent to Operate

Johnson Controls Confidential

Consent to Operate

25

Navigating the Risks

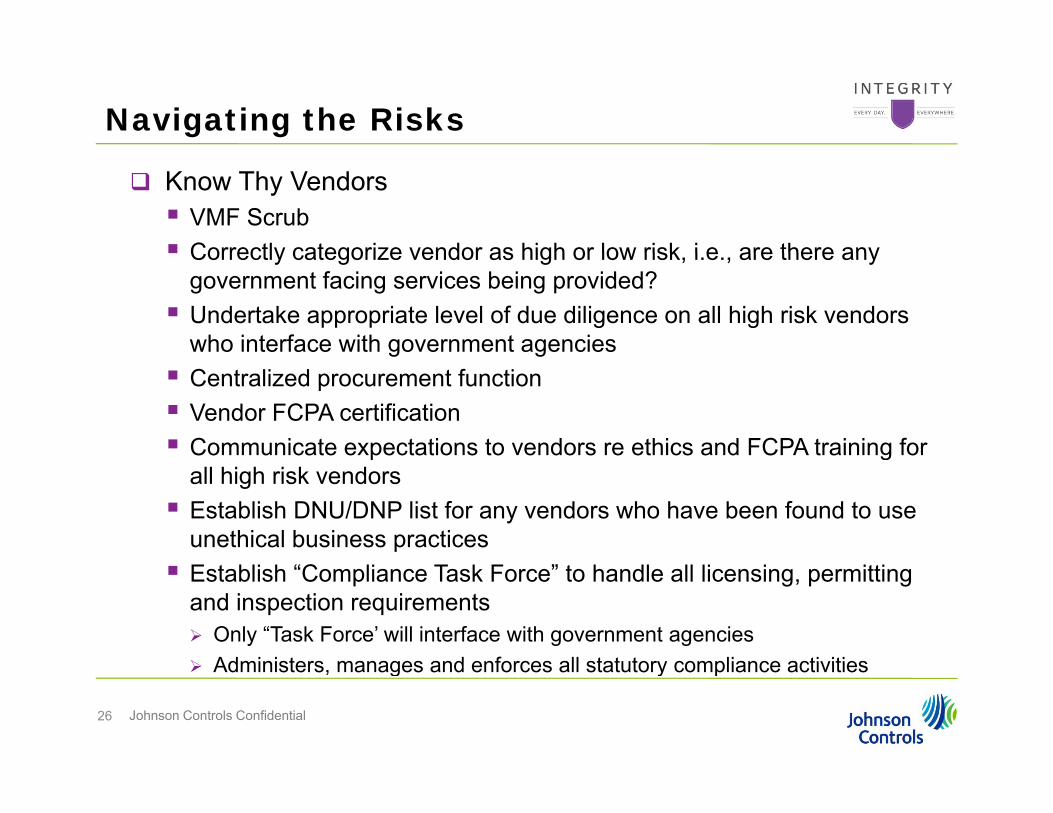

Know Thy Vendors VMF Scrub Correctly categorize vendor as high or low risk i e are there any Correctly categorize vendor as high or low risk, i.e., are there any

government facing services being provided? Undertake appropriate level of due diligence on all high risk vendors

who interface with government agenciesg g Centralized procurement function Vendor FCPA certification Communicate expectations to vendors re ethics and FCPA training for p g

all high risk vendors Establish DNU/DNP list for any vendors who have been found to use

unethical business practices Establish “Compliance Task Force” to handle all licensing, permitting

and inspection requirements Only “Task Force’ will interface with government agencies Administers manages and enforces all statutory compliance activities

Johnson Controls Confidential

Administers, manages and enforces all statutory compliance activities

26

Navigating the Risks

Contract Review Evaluate all contracts to ensure that the scope of services does not

provide inappropriate payments to government employeesprovide inappropriate payments to government employees “Outsourcing bribery” Do not undertake any government facing services on behalf of customers not

specifically provided for by contract

Financial Controls Establish monitoring process to ensure vendor transactions are for

legitimate services Stringent controls around employee advances and petty cash Red Flag training for all finance personnel

Monitor all Licensing/Permitting Activities Review all licenses and permits necessary to conduct business

Monitoring and Auditing Regular and periodic forensic reviews of business practices

Johnson Controls Confidential27

Fraud risks in India

April 2012

Jonathan C. Feig

Setting the context

The Indian Growth StoryThe Indian Growth Story

LargestLargest StrongStrong ConduciveConducive AbundantAbundantFast growing economy

Fast growing economy

Largest population of skilled workers

Largest population of skilled workers

Strong domestic demand

Strong domestic demand

Conducive investment environment

Conducive investment environment

Abundant natural resources

Abundant natural resources

The hurdles and show stoppersThe hurdles and show stoppers

Financial & accountingFinancial & accounting

Rampant corruption &

Rampant corruption &

Large number of commercialLarge number of commercial

Complex regulatoryComplex regulatoryaccounting

fraudsaccounting

fraudscorruption &

briberycorruption &

briberyof commercial

disputesof commercial

disputesregulatory

requirementsregulatory

requirements

Fraud risk scenario in IndiaPage 29

Key challenges in India

Key challenges in India► Large demographic area► Varied cultures & work practicesp► High levels of corruption

Financial misstatements /

occupational fraud / corruption & bribery

Corporate Culture

Local practices / customs

Underlying issues

Employee relationships with customer/ Vendor/

3rd parties

Inadequate privilege and data privacy

regulationsComplex web of

legislations

Fraud risk scenario in IndiaPage 30

g

Key factors leading to fraud and corruption

Significant 3rd partiesCorporate Culture

► Decentralized business► Aggressive sales culture and pressures to increase

in reach/penetration► Growth through acquisition or mergers► Operating through distributor or agent networks

► Agents/Facilitators► Resellers/Distributors► Consultants – tax/custom/licenses etc.► Staffing agencies

► Operating through distributor or agent networks► Employees with historical

relationships with vendors /customers

Key factors

► Government approvals► Fiercely competitive market► Size of emerging market

► Perception of employees – that is the way business is done thereg g

► Pricing pressures ► Distribution controlled by few

► Significant expenses on collaterals, gifts, business development and entertainment expenses

► Cash transactions

OthersMarket dynamics

Fraud risk scenario in IndiaPage 31

OthersMarket dynamics

Fraud risk challenges in IndiaBusiness environment is categorized by several fraud risk challenges such as Business environment is categorized by several fraud risk challenges such as

Procurement related frauds Conflict of InterestInflated sales revenue

Fictitious customer / sales orders

Vendor favoritism for awarding contractsOverstatement of expenses / duplicate claims

Lapping to Hide uncollectible receivables

unaccounted sales returns

Pilferage/theft of material

diversion of productsEmbezzlement of funds by employees Counterfeit

Potential corruption using third party service

providersBribery and inappropriate treatment of

government officials and other parties

Collusion with vendors

Fraud risk scenario in IndiaPage 32

How to Monitor for Corruption Risks?

► What kind of testing should be conducted?► Controls testing versus substantive testing► Controls testing versus substantive testing

► Why controls may not prevent fraud► Emphasis on controls without knowing vulnerabilities

“check box“ exercise does not mitigate risks

► False expectations from controls

controls do fail due to people, process and technology

► Management Override does not happen here!

the best policies, standards and monitoring fail if risk of management override not addressed or ignored

M i i k i li f ti ibilit► Managing risk is a compliance function responsibility

everyone is responsible to manage risk

Fraud risk scenario in IndiaPage 33

How to Monitor for Corruption Risks?continued

► How to choose a sampling methodology? Where are potential payments recorded?potential payments recorded?► Understand the business? Where are the customers? Where are the

government touch points?

► Choose accounts that could have risk – Commissions, permits, licenses, consultants, freight forwarding, customs clearance

► Choose T&E reports from individuals who direct or touch the risk?► Choose T&E reports from individuals who direct or touch the risk?► Who manages imports/exports?► Who entertains clients?

► Destination of cash? ► Is the payment going to a different country than the country in which the

services were rendered?

Fraud risk scenario in IndiaPage 34

How to Monitor for Corruption Risks? continued

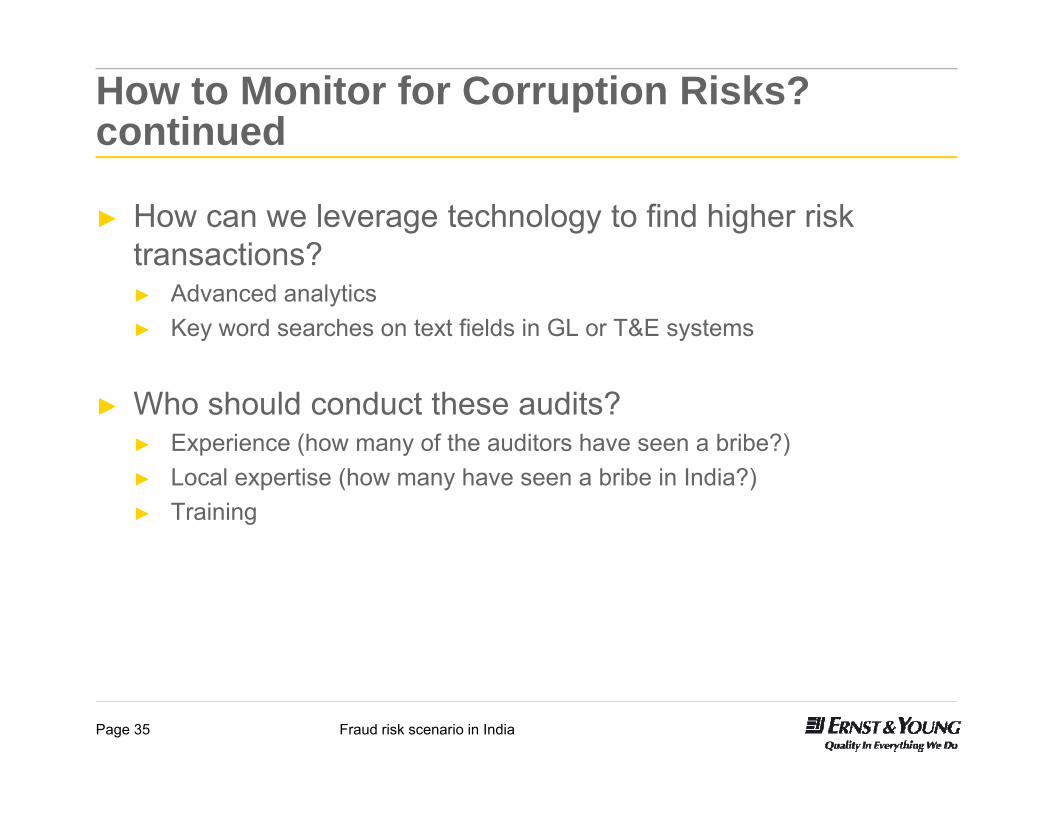

► How can we leverage technology to find higher risk transactions?transactions?► Advanced analytics ► Key word searches on text fields in GL or T&E systems

► Who should conduct these audits?► Experience (how many of the auditors have seen a bribe?)► Local expertise (how many have seen a bribe in India?)► Training

Fraud risk scenario in IndiaPage 35

What Companies should do?

Awareness

Every one is a compliance

Improve/ update Compliance program

Every one is a compliance officer - Training

Whistle blower policy Develop local language

compliance FAQs

Identify key risks Update policy & procedures

for Indian conditions Include key risks for

21

handbooks, handouts, etc

Risk assessment

ycontinuous monitoring/ assessments

Consider third party diligenceIt’s an

ongoing process

T ti / i di i Tone at the top Business landscape analysis Government interfaces Policy & procedures for other

34

Testing/ periodic reviews

Utilize advanced data analytics Select transactions for critical

areas – substantive and controlscompliance

Event based review: M&A

Incident Management / investigation5

areas substantive and controls based testing

Interviews of management/ employees

Fraud risk scenario in IndiaPage 36

Incident Management / investigation5

Some leading practices observed

► Communication on code of conduct, giving practical scenarios thus helping employee make the“desired” decision

► Regular training to increase awareness of code of conduct and whistle blower policy► Regular training to increase awareness of code of conduct and whistle blower policy

► Independent internal auditors reporting directly to the board/controls committee

► Before any vendor or agent is appointed, undertake a background check to assess the credentials,reputation and political affiliations if any based on public records and referencesreputation, and political affiliations, if any based on public records and references

► Rationalize the international approval matrix to customize the amounts to Indian environment.Expense limits are reduced and adjusted as per the need for a role

► Independent approval of expenses relating to activities like market research liaison fee consultancy► Independent approval of expenses relating to activities like market research, liaison fee, consultancycharges etc.

► Centralized procurement for all large amounts and all significant procurement/payments to be approved by an independent internal team/controls committee

► Restrict "emergency purchases" where requirements are seen to be circumvented.

► Cash transactions only in extreme cases

Fraud risk scenario in IndiaPage 37

Some leading practices observed

► Mandatory disclosure by employees on their other business interests and potential “related partytransaction”

► Review of SOPs and operating procedures from fraud risk perspective and make necessary► Review of SOPs and operating procedures from fraud risk perspective and make necessarymodifications in operating procedures

► Regular fraud analytics to identify deviations, if any

► Periodic sample (random) test of transactions (especially for gifts travel entertainment charitable► Periodic sample (random) test of transactions (especially for gifts, travel, entertainment, charitable contributions etc) to ascertain adherence to required policies and procedures. Specifically things reviewed are

► Compliance with mandated procedures, including approvals

► Correct depiction of nature of expenses

► Comparison of price and terms with prevalent market conditions

► Evidence to substantiate that product/services were actually required and receivedp y q

► While forming a joint venture or acquiring stake, undertake anti-corruption due diligence to assess ifthe target entity has been involved in bribery/corruption and it has necessary procedures to checkthe same

Fraud risk scenario in IndiaPage 38

CONCLUSION

Jonathan C. Feig

CONCLUSION

Ernst & Young LLP(312) [email protected]

Jay HoltmeierJay HoltmeierWilmer Cutler Pickering Hale and Dorr LLP(212) [email protected]

Elizabeth D. KeatingJohnson Controls, Inc.(414) 426-9506

li b th d k ti @j [email protected]

39