Foreclosure INDIRECT LENDING - · PDF fileForeclosure INDIRECT LENDING: LITIGATION AND ......

40

Foreclosure INDIRECT LENDING: LITIGATION AND REGULATORY ISSUES 2015 MCUL Lending & Marketing Conference Patricia Corkery, Esq. Holzman Corkery PLLC [email protected] 248-352-4340 ext. 238

Transcript of Foreclosure INDIRECT LENDING - · PDF fileForeclosure INDIRECT LENDING: LITIGATION AND ......

ForeclosureINDIRECT LENDING:LITIGATION AND

REGULATORY ISSUES

2015 MCUL Lending & Marketing ConferencePatricia Corkery, Esq.

Holzman Corkery [email protected]

248-352-4340 ext. 238

BENEFITS OF INDIRECT LENDING

Expand lending volume.

Create membership growth.

Enhance member retention and loyalty.

Help credit union bottom line.

Cross-selling products to new members.

RISKS – RED FLAGS

Examiners look at call reports for increased repossessions, increased delinquency and increased loan loss

Key Red Flags – High concentration of indirect loans to total loans or

net worth without adequate controls Incentive programs tying loan officer bonuses to

indirect loan volume Inadequate analysis of indirect portfolio

performance High first payment defaults, payment deferment Frequent re-fi of past due interest Insufficient loan documentation Poor dealer management

NCUA RECOMMENDATIONS FOR IDL Successful Planning Process

Establish goals for IDL program; monitoring

Consistent Underwriting Standards

Clear Vendor Policies

Formalized Contracts and Written Agreements

Effective Risk Management

Preventing and Defecting Fraud

HOW TO MITIGATE ADDITIONAL RISKSWITH INDIRECT LENDING:

Monitor dealer and credit union employees working with dealer.

Updated and comprehensive policies. Lending AND Collection/Recovery

Strong lending department. Strong collection department. Training. Pricing the deal. Recognizing fraud and poor lending decisions.

DEALER CONTRACT. Credit union has sole lending discretion. Dealer provided membership criteria but credit

union must confirm eligible. Dealer warranties:

› Information true and accurate› Cash down, trade-in and rebates

Dealer agrees to buy back paper if breach. Comply with law and privacy. Attorney review and negotiate with dealer. Reg E Issues – Discussed later.

DEALER CONTRACT TERMS. In the event Buyer defaults on the Contract, or for any reason

should Credit Union be entitled to a refund of any unused premium for service warranties, GAP or other product sold by

Dealer to Customer, Dealer shall assist Credit Union in obtaining refund from third party provider.

Dealer represents and warrants to Credit Union:

All down payments reflected as cash in the Contract are cash directly from the Buyer received on or before the date of the Contract and are not rebates, loans or contributions from Dealer or a manufacturer. Dealer, in conjunction with the sale of the Vehicle and/or Recreational Vehicle sold under the Contract, did not purchase any Vehicle and/or Recreational Vehicle other than indicated as a trade-in on the Contract. Any form of rebate (including manufacturer) applied to the Contract shall be identified as a rebate and not cash on all documents.

DEALER CONTRACT TERMS CONT. The Dealer has confirmed the identity of each Buyer and that

each Buyer is a bona fide person. Dealer has met face-to-face with Buyer in connection with the application.

Dealer has not communicated to Credit Union any incorrect information related to Buyer’s application or credit statement, or failed to communicate financial or personal information provided by Buyer.

KNOW THY DEALER. Great contract with a lot of protection not worth

anything if dealer is broke. As part of dealer contract require review of

financials. Dealer must agree to provide information on its

corporate structure and allow review of files at dealership.

Take advantage of right to review deal files.

LICENSE - MVSFA Michigan Motor Vehicle Sales Finance Act – governs

financing of auto loans DIFS requires that dealers in Michigan only sell or

assign loans to entities licensed under MVSFA Argument can be made that credit union does not

have to be licensed to buy auto loans, but dealers being told they can only sell to licensed entities.

License fee = $30.00› www.michigan.gov/dleg

CUSO OR THIRD PARTY PROVIDER

Most credit unions contract with CUSO or third party to provide services.

Credit Union still required to meet all consumer laws and privacy regs

All contracts need legal review NCUA leery of outsourcing

› NCUA looks for documented due diligence and monitoring

LENDING POLICY Separate indirect lending policy Key components to policy:

› Term – higher risk, shorter the term Higher the mileage – shorter the term

› Employment – Income verification› Rebate – separate from cash› Collateral value – new cars get MSRP – used and trade in

– get book value including mileage and options› Spot check collateral! Call member. › Inspect sales contract

WHAT DEALERS ARE LOOKING FOR. Credit union to buy deep – 125 – 150% LTV Long finance terms – for used cars too. Insurance and add-on income. Pay them for deals. Up charge. Provide instant approvals with little

verification. Take more risk than anyone else. Fast approvals.

COMMON CHARACTERISTICS OFINDIRECT LENDING GONE BAD:

Program grew too fast.

Credit union not staffed for growth.

No increase in collection staff to deal with influx of

problems.

Lending and collection have issues.

Waiting to long to stop program.

No contract with dealer.

EMPLOYEE TOO CLOSE TO DEALER? Lending employee working with dealerships –

risky if only one person If one employee running program – watch for

them: Waiving stipulations Becoming defensive Wants deals to go through them Overrides decisions on declines Intimidates other employees

STRONG COLLECTORS A MUST FORSUCCESSFUL INDIRECT PROGRAM.

Collectors on indirect must be highly trained.

Must understand scoring models.

Must be able to know fraud when they see and

promptly report to management.

Dealer fraud is caught by collectors – if asleep –

fraud continues.

COLLECTION POLICY – PART OFLENDING.

Aggressive collection needed on indirect loans. Faster calls – shorter delinquent status Faster letters

Strong repo timelines. Fast notices to members and pro-active on first-

payment defaults. GPS trackers? Disposition of collateral – do what can be done to

cut losses Monitor sale process Recondition cars?

WHAT EXAMINERS WILL REVIEW & CONSIDER:

Strategic Red Flags

Transaction Red Flags

Credit Risk Red Flags

STRATEGIC RED FLAGS FLAGS

High program exposure with no concentration parameters Concentration of credit quality and to individual dealers

No portfolio credit quality standards High LTVs (need skin in the game!) Inadequate staffing, program analysis and board

reporting Unusual Trends (high ROA, first payment defaults)

TRANSACTION RED FLAGSE FLAGS

Inadequate segregation of duties Separate people to approve and cut checks Don’t assign one person to particular dealer

Lack of internal controls for: Loan documentation – funding Dealer reserves (flat fee vs. int rate mark-up) Lien placement FOM eligibility

TRANSACTION FLAGS CONT. No follow up procedures –

CALL NEW MEMBERS Ensure contract terms Review contract and optional car features Cross-sell Ensure lien is perfected

Improper Incentives Don’t encourage risky loans

CREDIT RISK RED FLAGSFLAG

Inadequate Review of Underwriting 3rd party provider lending policy CU must do quality control review to assure loan

compliance Review exception reports Loan Autopsy

High Default Rates

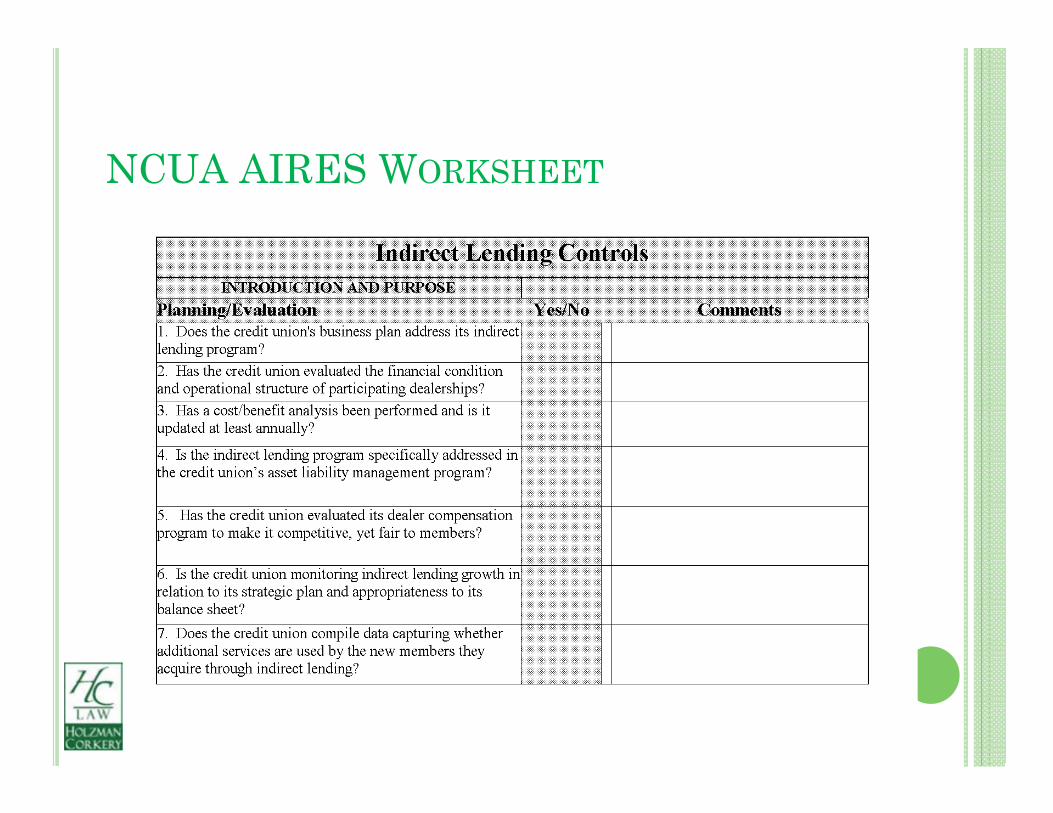

NCUA AIRES WORKSHEET

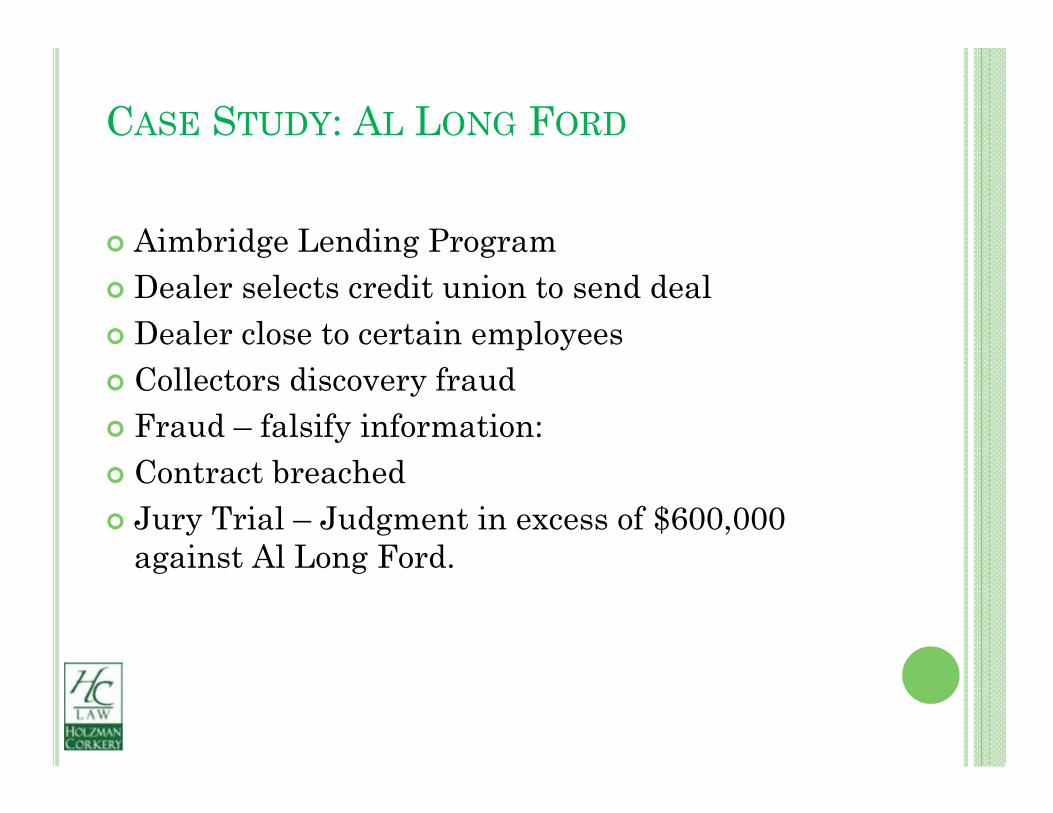

CASE STUDY: AL LONG FORD: AL LONGFORD

Aimbridge Lending Program Dealer selects credit union to send deal Dealer close to certain employees Collectors discovery fraud Fraud – falsify information: Contract breached Jury Trial – Judgment in excess of $600,000

against Al Long Ford.

REPORTS TO DECREASE RISK: TODECREASE RISK. First payment defaults – review all loans.

Policy violations? Bond claim? Mandatory loan autopsy. Review of member contact. Monitor dealership. Loans to individual dealers:

First payment defaults Charge-offs One dealer more than others bringing in bad loans.

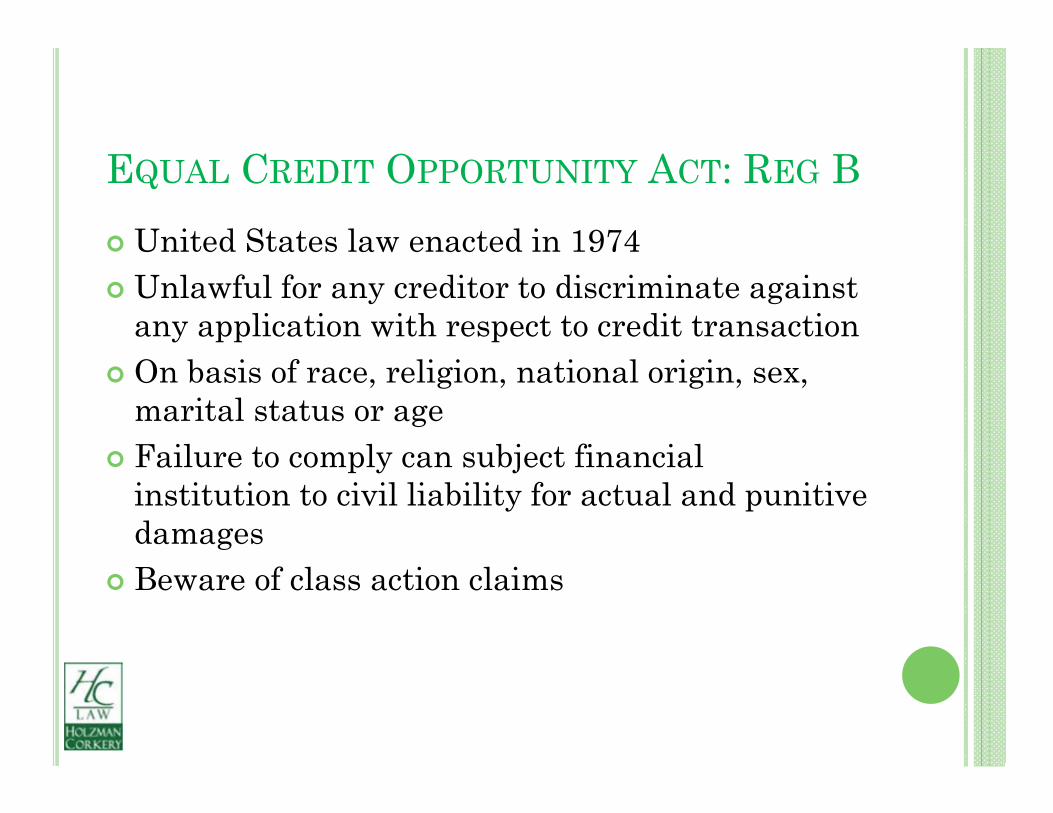

EQUAL CREDIT OPPORTUNITY ACT: REG B United States law enacted in 1974 Unlawful for any creditor to discriminate against

any application with respect to credit transaction On basis of race, religion, national origin, sex,

marital status or age Failure to comply can subject financial

institution to civil liability for actual and punitive damages

Beware of class action claims

CFPB DISCRIMINATORY MARK-UPS

Consumer Financial Protection Bureau Bulletin Subject – IDL and compliance with Equal Credit

Opportunity Act (ECOA or Reg B) Concerns allowing dealers to increase interest

rates – dealer “mark-up” or “reserve” Risk that pricing disparities will result because of

race, national origin, etc. CFPB recommends controls on dealer markups,

monitor mark-up policies and eliminate discretion to mark up rates

BREAKDOWN OF CFPB CONCERNS: ALLONG FORD

Indirect auto lender’s markup and compensation policies may trigger liability under ECOA/REG B

Dealer’s practices may result in disparity of rates and cost to protected class of borrowers

As credit union is assigned paper, credit union is lender

CFPB looking for controls on dealer markup and compensation policies

Looking for dealers and creditors to address effects of policies that may violate ECOA

Looking to eliminate dealer discretion to mark up buy rates and go to flat fee.

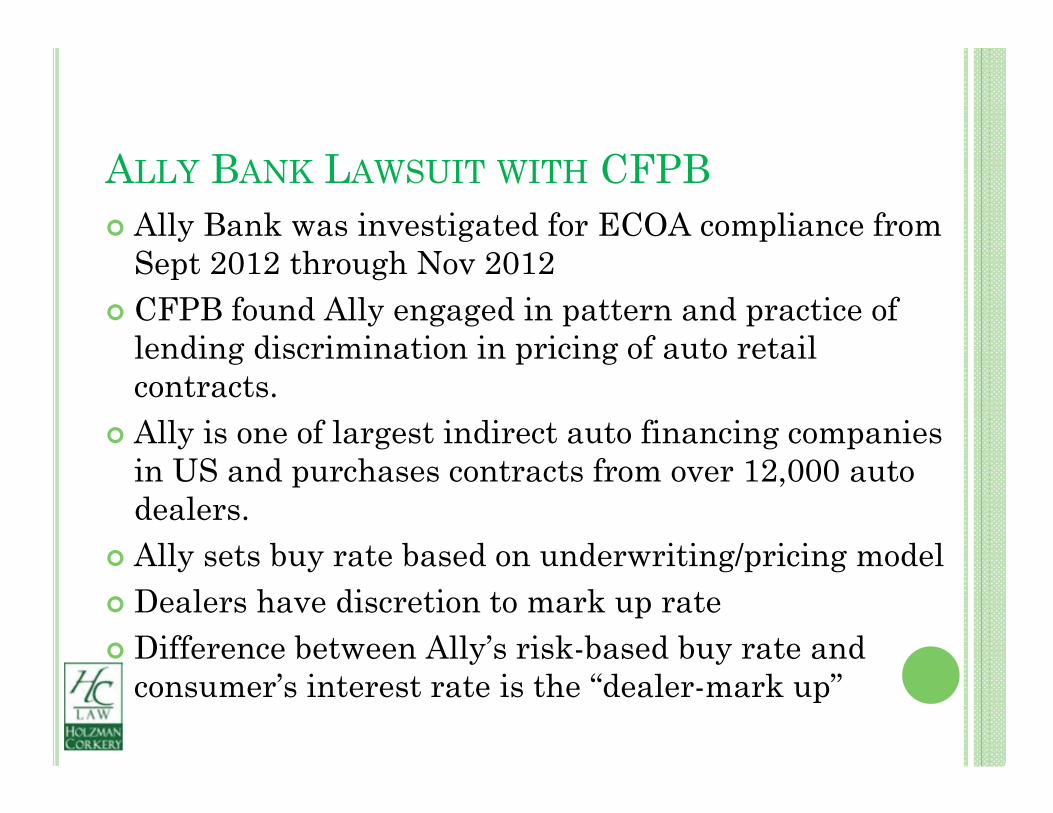

ALLY BANK LAWSUIT WITH CFPB-ACTIVE. Ally Bank was investigated for ECOA compliance from

Sept 2012 through Nov 2012 CFPB found Ally engaged in pattern and practice of

lending discrimination in pricing of auto retail contracts.

Ally is one of largest indirect auto financing companies in US and purchases contracts from over 12,000 auto dealers.

Ally sets buy rate based on underwriting/pricing model Dealers have discretion to mark up rate Difference between Ally’s risk-based buy rate and

consumer’s interest rate is the “dealer-mark up”

ALLY CASE CONT. ACTIVE. CFPB and DOJ reviewed dealer markup on deals

purchased between April 1 and March 31, 2012. Results were that on average African-American

borrowers were charged approx 29 basis points more than similarly-situated non-Hispanic whites. Differences were based on race and not credit.

During review time period, approx 100,000 African-American borrowers paid higher mark-ups than whites and, on average, paid $300 more each in interest.

Study found similar problems for Hispanic and Asian/Pacific Islander borrowers.

ALLY CONT.-ACTIVE. Ally did not monitor whether discrimination was

occurring and did not offer fair lending training to dealers.

In Dec 2013 Ally agreed to numerous items in consent order: Set up a Compliance Committee Form Compliance Plan Reporting Requirements Record Keeping Requirements Monetary fine - $80 million into a Settlement Fund Pay $18 million to CFPB as a civil penalty

WHAT TO DO IN WAKE OF ALLY BANKACTIVE. First – remember that your IDL program is a small

fish in the pond. ALLY Financial had $182 billion in assets and Ally

Financial (subsidiary) $94.8 billion in assets ALLY is one of largest auto finance companies in US Things to consider for your program: Fair lending statement to dealers Fair lending training for your staff and dealer Fair lending review of lending policies Statistical analysis applies to only very large portfolios

BE PRO-ACTIVE!-ACTIVE. Set short-term and long-term goals. Assess risk before launching program or signing on

new dealer. Staffing – collection and lending. Training – Internal and Dealerships. Policies in place. Procedures in place. Assess viability of dealership. Contract review.

RRESOURCES

Your credit union attorney experienced in indirect lending.

NCUA August 2010 – LCU 10-CU-15 Due diligence over 3rd Party Providers

LCU 01-CU-20 Evaluating Third Party Relationships

LCU 07-CU-13 Specialized Lending Activity – Subprime indirect

– 05-Risk-01 NCUA Examiner’s Guide – Appendix on IDL CFPB Bulletin 2013-02/Ally Consent Order 2013-

CFPB-0010