For personal use only - ASX · 2017. 6. 12. · Rhyolite Ridge Nevada Clay Open pit 393Mt at 0.34%...

25

The Next Player in European Lithium Production + a Globally Significant Potash Project Investor Presentation June 2017 ASX.PLH For personal use only

Transcript of For personal use only - ASX · 2017. 6. 12. · Rhyolite Ridge Nevada Clay Open pit 393Mt at 0.34%...

The Next Player in European Lithium Production+ a Globally Significant Potash Project

Investor Presentation June 2017

ASX.PLH

For

per

sona

l use

onl

y

Disclaimer

Plymouth Minerals Limited ASX: PLH | 2

For Consideration

This presentation has been prepared by Plymouth Minerals Ltd “Plymouth”. This document contains background information about Plymouth current at the

date of this presentation. The presentation is in summary form and does not purport to be all inclusive or complete. Recipients should conduct their own

investigations and perform their own analysis in order to satisfy themselves as to the accuracy and completeness of the information, statements and opinions

contained in this presentation.

This presentation is for information purposes only. Neither this presentation nor the information contained in it constitutes an offer, invitation, solicitation orrecommendation in relation to the purchase or sales of shares in any jurisdiction.

This presentation does not constitute investment advice and has been prepared without taking into account the recipient’s investment objectives, financialcircumstances or particular needs and the opinions and recommendations in this presentation are not intended to represent recommendations of particularinvestments to particular persons. Recipients should seek professional advice when deciding if an investment is appropriate. All securities involve risks whichinclude (among others) the risk of adverse or unanticipated market, financial or political developments.

To the fullest extent permitted by law, Plymouth, its officers, employees, agents and advisors do not make any representation or warranty, express or implied,

as to the currency, accuracy, reliability or completeness of any information, statements, opinions, estimates, forecasts or other representations contained in

this presentation. No responsibility for any errors or omissions from this presentation arising out of negligence or otherwise are accepted.

This presentation may include forward-looking statements. Forward-looking statements are only predictions and are subject to risks, uncertainties and

assumptions which are outside the control of Plymouth. Actual values, results or events may be materially different to those expressed or implied in this

presentation. Given these uncertainties, recipients are cautioned not to place reliance on forward looking statements. Any forward looking statements in this

presentation speak only at the date of issue of this presentation. Subject to any continuing obligations under applicable law, Plymouth does not undertaken

any obligation to update or revise any information or any of the forward looking statements in this presentation or any changes in events, conditions, or

circumstances on which any such forward looking statement is based.

Competent Persons Statement

Competent Person Statement: The information in this report related to Exploration Results, Exploration Targets, Mineral Resources or Ore Reserves is based on

information compiled by Mr A Byass, B.Sc Hons (Geol), B.Econ, FSEG, MAIG an employee of Plymouth Minerals Limited. Mr Byass has sufficient experience

relevant to the style of mineralisation and type of deposit under consideration and to the activity which he is undertaking to qualify as a Competent Person as

defined in the 2012 Edition of the Australasian Code for Reporting of Exploration Results, Exploration Targets, Mineral Resources and Ore Reserves. Mr Byass

consents to the inclusion in the report of the matters based on this information in the form and context in which it appear.

The information in this report that relates to Exploration Targets and Mineral Resources for the San Jose project is based on the information compiled by Mr

Jeremy Peters, FAusIMM CP (Mining, Geology). Mr Peters has sufficient relevant professional experience with open pit and underground mining, exploration

and development of mineral deposits similar to the style of mineralisation and type of deposit under consideration and to the activity which he is undertaking

to qualify as a Competent Person as defined in the 2012 Edition of JORC Code He has visited the project area and observed drilling, logging and sampling

techniques used by Plymouth in collection of data used in the preparation of this report. Mr Peters is an employee of Snowden Mining industry Consultants and

consents to be named in this release and the report as it is presented.

For

per

sona

l use

onl

y

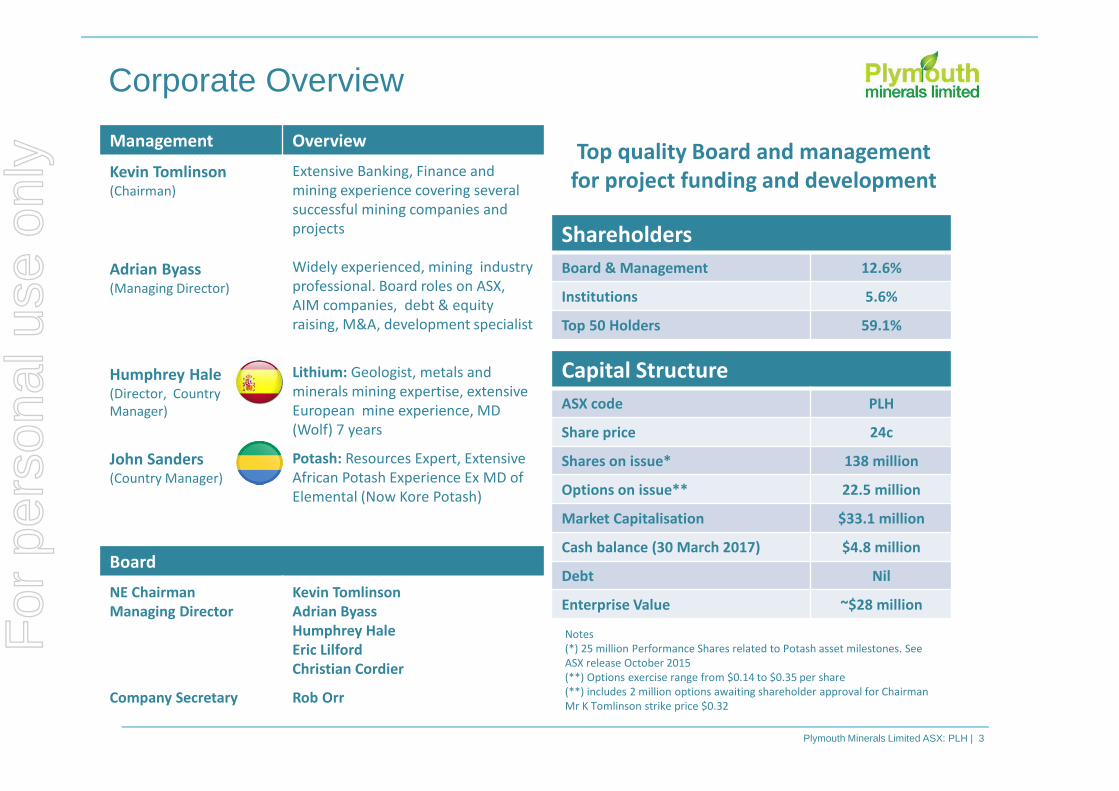

Corporate Overview

Plymouth Minerals Limited ASX: PLH | 3

Capital Structure

ASX code PLH

Share price 24c

Shares on issue* 138 million

Options on issue** 22.5 million

Market Capitalisation $33.1 million

Cash balance (30 March 2017) $4.8 million

Debt Nil

Enterprise Value ~$28 million

Shareholders

Board & Management 12.6%

Institutions 5.6%

Top 50 Holders 59.1%

Management Overview

Kevin Tomlinson(Chairman)

Adrian Byass(Managing Director)

Extensive Banking, Finance and

mining experience covering several

successful mining companies and

projects

Widely experienced, mining industry

professional. Board roles on ASX,

AIM companies, debt & equity

raising, M&A, development specialist

Humphrey Hale (Director, Country

Manager)

Lithium: Geologist, metals and

minerals mining expertise, extensive

European mine experience, MD

(Wolf) 7 years

John Sanders(Country Manager)

Potash: Resources Expert, Extensive

African Potash Experience Ex MD of

Elemental (Now Kore Potash)

Board

NE Chairman

Managing Director

Kevin Tomlinson

Adrian Byass

Humphrey Hale

Eric Lilford

Christian Cordier

Company Secretary Rob Orr

Notes

(*) 25 million Performance Shares related to Potash asset milestones. See

ASX release October 2015

(**) Options exercise range from $0.14 to $0.35 per share

(**) includes 2 million options awaiting shareholder approval for Chairman

Mr K Tomlinson strike price $0.32

Top quality Board and management

for project funding and development

For

per

sona

l use

onl

y

Experience in Financing & Developing in Europe and Globally – A Board for building value

Plymouth Minerals Limited ASX: PLH | 4

� Investment Banking, finance and M&A, development and mining

� Multiple Project Financing (Debt and Equity deals up to +$500 million

each), Several hundred million in equity raisings

� 2013 European Mining and Metals “Deal of the Year”

� Syndicated bank debt facilities, Government subordinated bank debt

facilities, off-take and Specialist project finance

� AIM, ASX, TSX listings and Directorships

� Project permitting and planning permissions

� Offtake agreements (including Euro consumers)

� Commercial, Acquisition, Drilling and government liaison strengths with

high calibre in-country staff – Spain since 2013

Deal of the year

Hemerdon Tungsten-Tin mine England

Centamins gold mine, Egypt

For

per

sona

l use

onl

y

Lithium/Tin in SpainEarning 75% of San Jose (Sacyr 25% contributing)

Plymouth Minerals Limited ASX: PLH | 5

For

per

sona

l use

onl

y

Valoriza Mineria Senior Management team

$200 million facility

with Macquarie Bank for

project development

IBEX 35, +$billion market capitalisationMajor international engineering,

construction and water treatment operations

100%

Sacyr - Top Tier Partners – Strong Local Advantage

Ni, Cu, W, Li,

Mining subsidiary

Plymouth Minerals Limited ASX: PLH | 6

San Jose

Lithium-Tin

Project

Earning 75%

Diluting to 25%

contributing

partner

Plymouth + Sacyr = Won a Public Tender for

the development of the San Jose lithium deposit.

The Government of Extremadura awarded the

tender and is the same government which awards

development and mining permits

* Also refer to ASX 20 April 2017 in respect of a transaction with Reabold Resources

For

per

sona

l use

onl

y

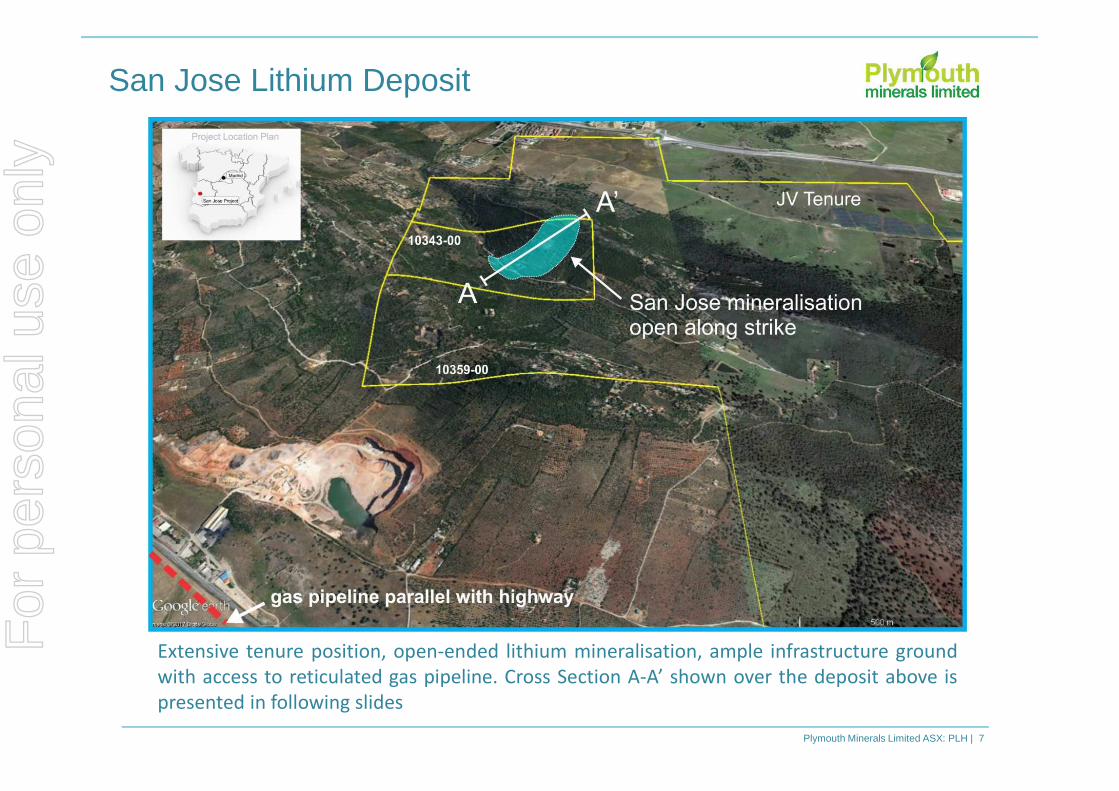

San Jose Lithium Deposit

Plymouth Minerals Limited ASX: PLH | 7

A

A’

Extensive tenure position, open-ended lithium mineralisation, ample infrastructure ground

with access to reticulated gas pipeline. Cross Section A-A’ shown over the deposit above is

presented in following slides

For

per

sona

l use

onl

y

Plymouth Minerals Limited ASX: PLH | 8

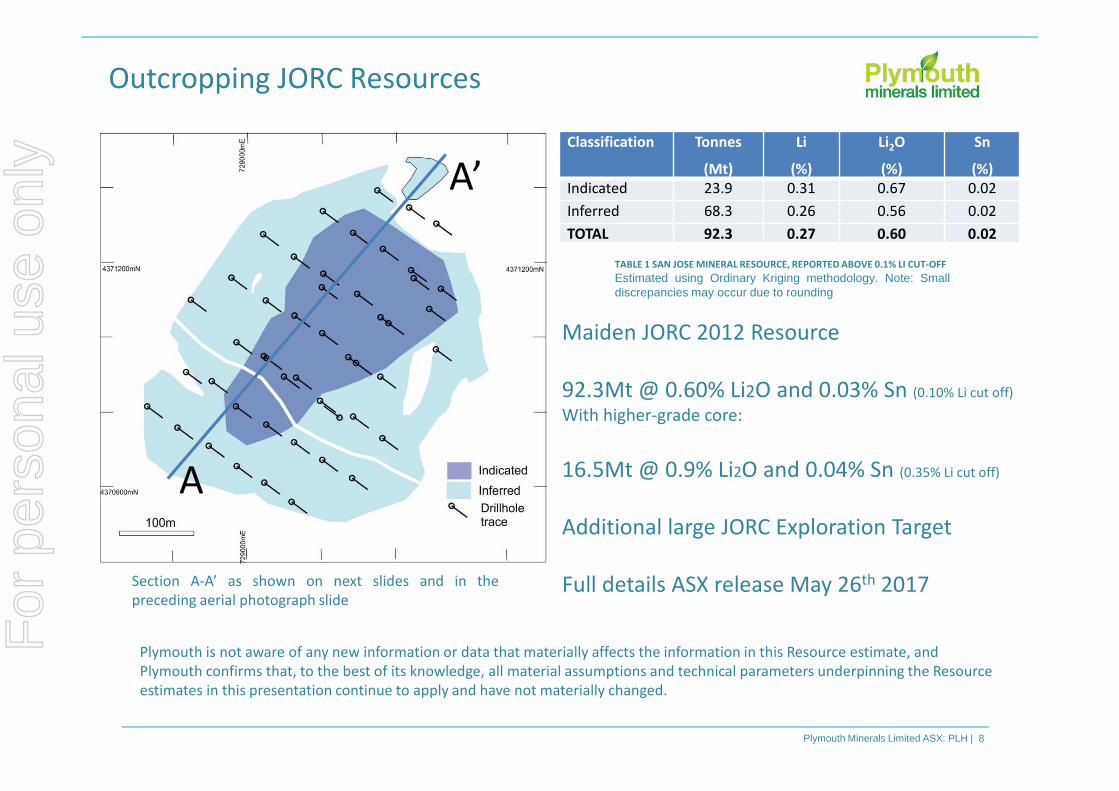

Outcropping JORC Resources

A

A’

Section A-A’ as shown on next slides and in the

preceding aerial photograph slide

Maiden JORC 2012 Resource

92.3Mt @ 0.60% Li2O and 0.03% Sn (0.10% Li cut off)

With higher-grade core:

16.5Mt @ 0.9% Li2O and 0.04% Sn (0.35% Li cut off)

Additional large JORC Exploration Target

Full details ASX release May 26th 2017

Classification Tonnes

(Mt)

Li

(%)

Li2O

(%)

Sn

(%)

Indicated 23.9 0.31 0.67 0.02

Inferred 68.3 0.26 0.56 0.02

TOTAL 92.3 0.27 0.60 0.02

TABLE 1 SAN JOSE MINERAL RESOURCE, REPORTED ABOVE 0.1% LI CUT-OFF

Estimated using Ordinary Kriging methodology. Note: Smalldiscrepancies may occur due to rounding

Plymouth is not aware of any new information or data that materially affects the information in this Resource estimate, and

Plymouth confirms that, to the best of its knowledge, all material assumptions and technical parameters underpinning the Resource

estimates in this presentation continue to apply and have not materially changed.

For

per

sona

l use

onl

y

Plymouth Minerals Limited ASX: PLH | 9

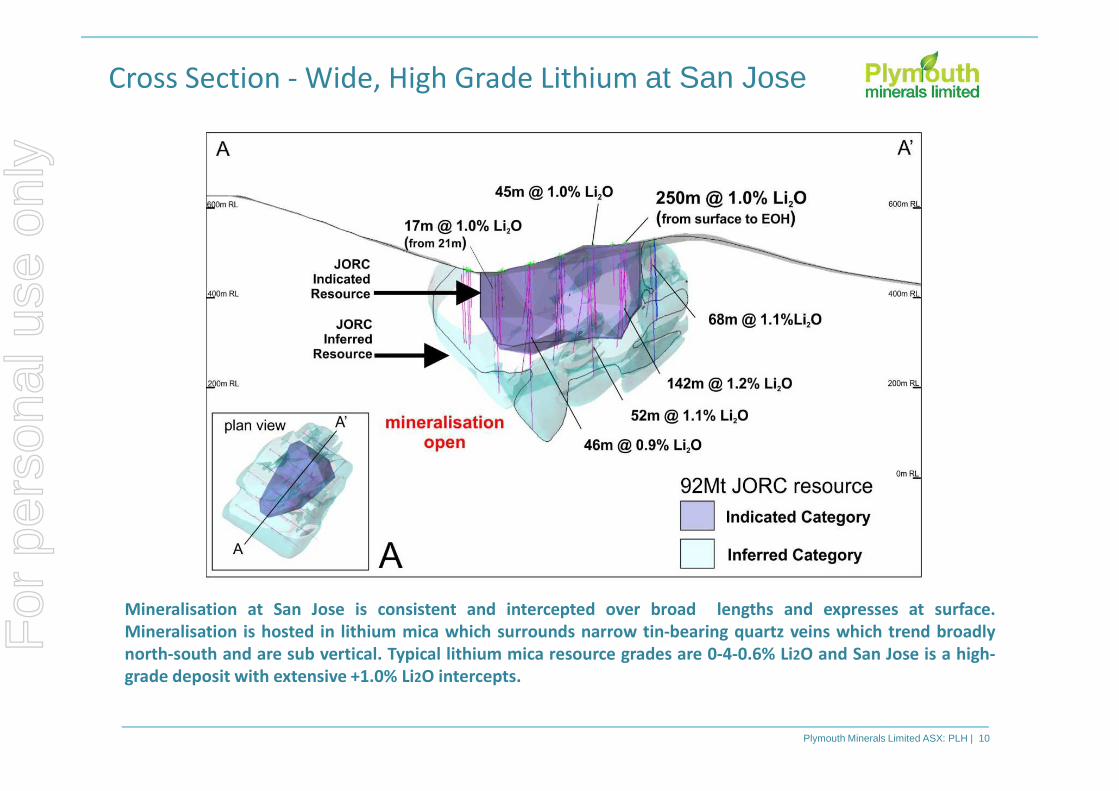

Cross Section - Wide, High Grade Lithium at San Jose

For

per

sona

l use

onl

y

Plymouth Minerals Limited ASX: PLH | 10

Cross Section - Wide, High Grade Lithium at San Jose

Mineralisation at San Jose is consistent and intercepted over broad lengths and expresses at surface.

Mineralisation is hosted in lithium mica which surrounds narrow tin-bearing quartz veins which trend broadly

north-south and are sub vertical. Typical lithium mica resource grades are 0-4-0.6% Li2O and San Jose is a high-

grade deposit with extensive +1.0% Li2O intercepts.

For

per

sona

l use

onl

y

Plymouth Minerals Limited ASX: PLH | 11

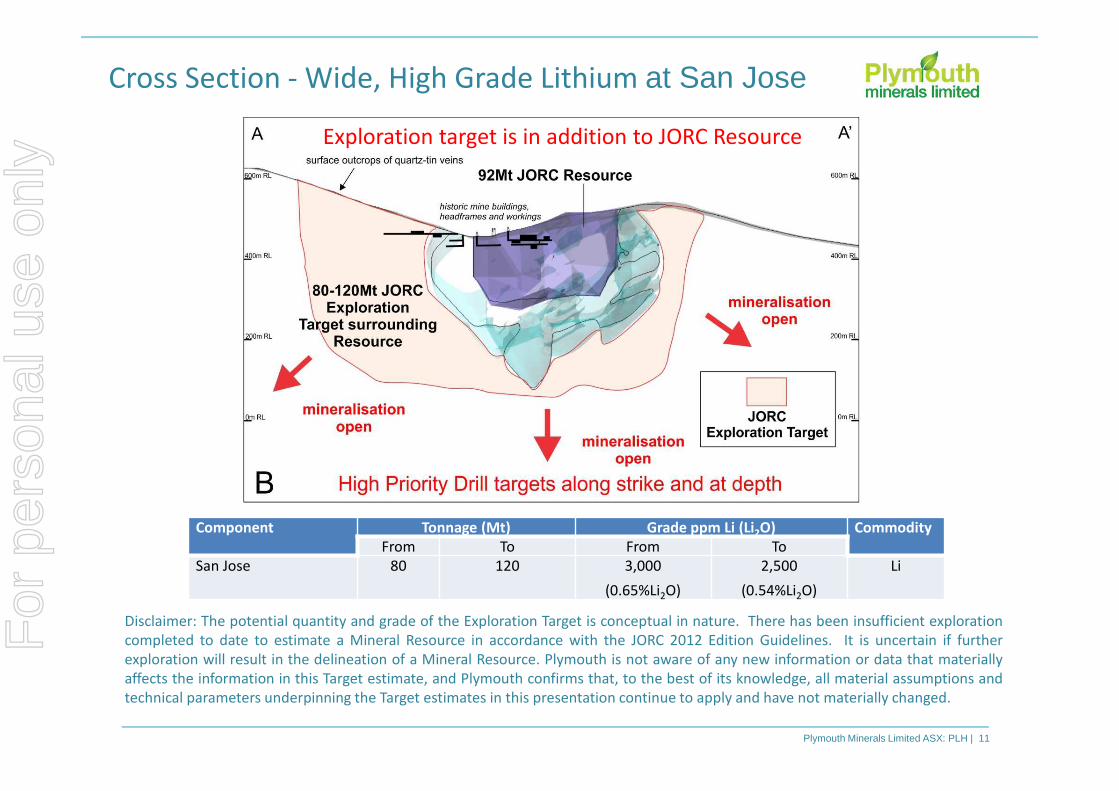

Cross Section - Wide, High Grade Lithium at San Jose

Exploration target is in addition to JORC Resource

Disclaimer: The potential quantity and grade of the Exploration Target is conceptual in nature. There has been insufficient exploration

completed to date to estimate a Mineral Resource in accordance with the JORC 2012 Edition Guidelines. It is uncertain if further

exploration will result in the delineation of a Mineral Resource. Plymouth is not aware of any new information or data that materially

affects the information in this Target estimate, and Plymouth confirms that, to the best of its knowledge, all material assumptions and

technical parameters underpinning the Target estimates in this presentation continue to apply and have not materially changed.

Component Tonnage (Mt) Grade ppm Li (Li2O) Commodity

From To From To

San Jose 80 120 3,000

(0.65%Li2O)

2,500

(0.54%Li2O)

Li

For

per

sona

l use

onl

y

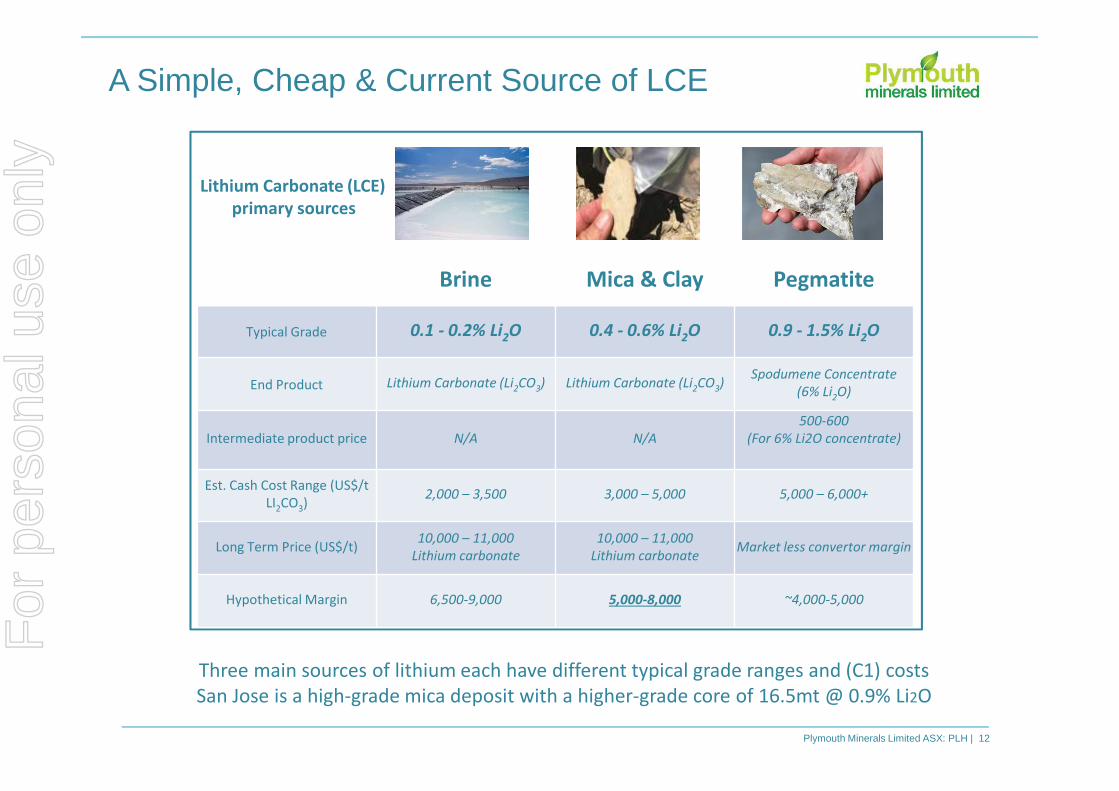

A Simple, Cheap & Current Source of LCE

Plymouth Minerals Limited ASX: PLH | 12

Brine Mica & Clay Pegmatite

Typical Grade 0.1 - 0.2% Li2O 0.4 - 0.6% Li

2O 0.9 - 1.5% Li

2O

End Product Lithium Carbonate (Li2CO3) Lithium Carbonate (Li2CO3)Spodumene Concentrate

(6% Li2O)

Intermediate product price N/A N/A

500-600

(For 6% Li2O concentrate)

Est. Cash Cost Range (US$/t

LI2CO3)2,000 – 3,500 3,000 – 5,000 5,000 – 6,000+

Long Term Price (US$/t)10,000 – 11,000

Lithium carbonate

10,000 – 11,000

Lithium carbonateMarket less convertor margin

Hypothetical Margin 6,500-9,000 5,000-8,000 ~4,000-5,000

Three main sources of lithium each have different typical grade ranges and (C1) costs

San Jose is a high-grade mica deposit with a higher-grade core of 16.5mt @ 0.9% Li2O

Lithium Carbonate (LCE)

primary sources

For

per

sona

l use

onl

y

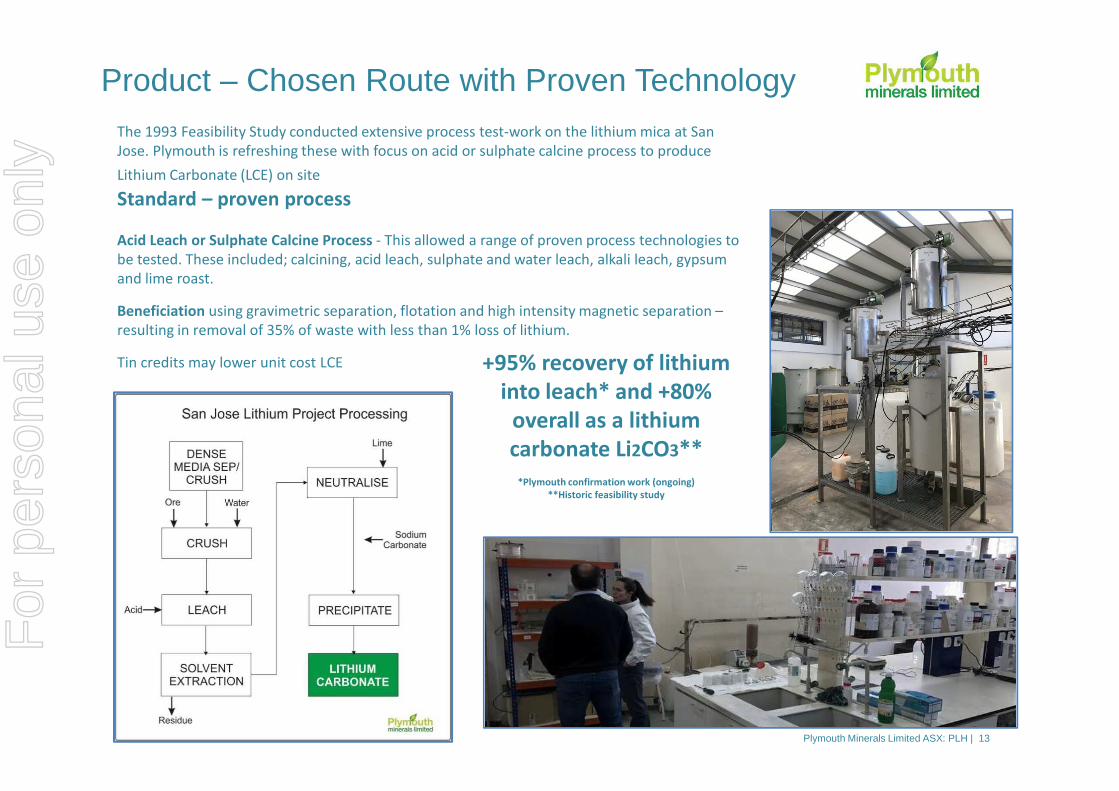

Product – Chosen Route with Proven Technology The 1993 Feasibility Study conducted extensive process test-work on the lithium mica at San

Jose. Plymouth is refreshing these with focus on acid or sulphate calcine process to produce

Lithium Carbonate (LCE) on site

Standard – proven process

Acid Leach or Sulphate Calcine Process - This allowed a range of proven process technologies to

be tested. These included; calcining, acid leach, sulphate and water leach, alkali leach, gypsum

and lime roast.

Beneficiation using gravimetric separation, flotation and high intensity magnetic separation –

resulting in removal of 35% of waste with less than 1% loss of lithium.

Tin credits may lower unit cost LCE +95% recovery of lithium

into leach* and +80%

overall as a lithium

carbonate Li2CO3**

*Plymouth confirmation work (ongoing)

**Historic feasibility study

Plymouth Minerals Limited ASX: PLH | 13

For

per

sona

l use

onl

y

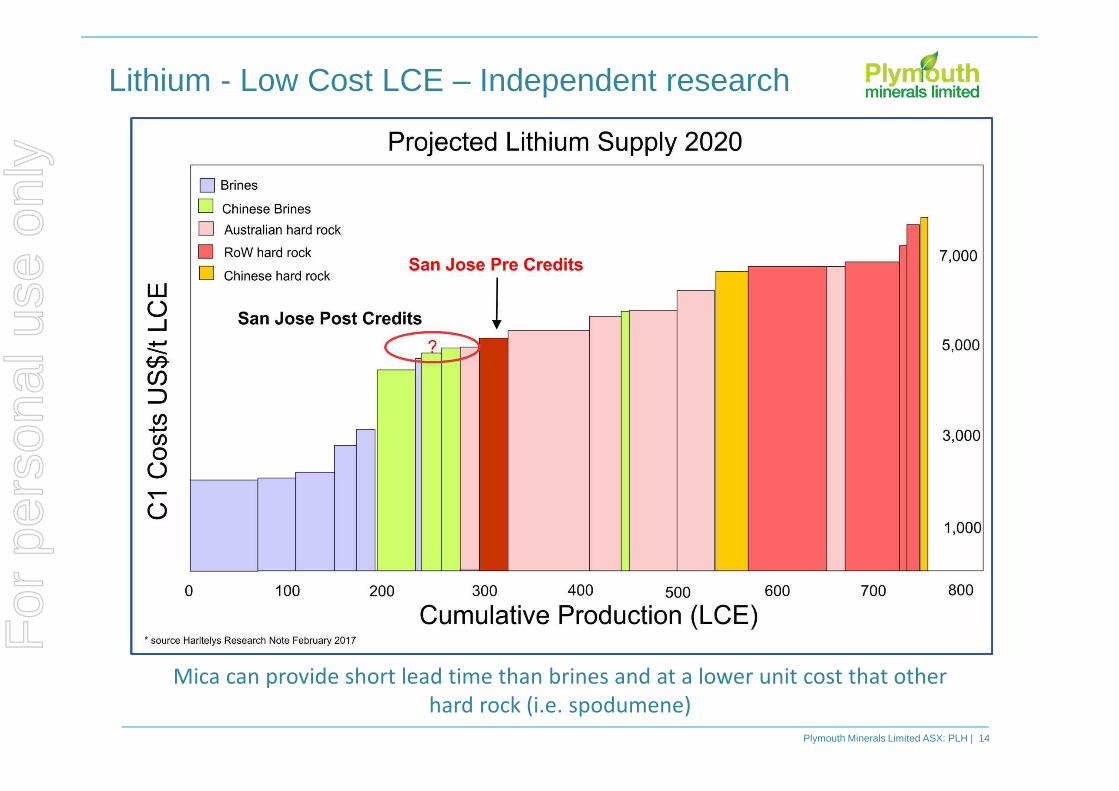

Lithium - Low Cost LCE – Independent research

Plymouth Minerals Limited ASX: PLH | 14

Mica can provide short lead time than brines and at a lower unit cost that other

hard rock (i.e. spodumene)

For

per

sona

l use

onl

y

Peer Comparatives – Lithium

Plymouth Minerals Limited ASX: PLH | 15

Company Deposit Location Host Mineral Mining Style Resource Mkt Cap*

Plymouth Minerals

(ASX: PLH)San Jose Spain Mica Open pit

92.3Mt at

0.6% Li20$32m

Tawana Resources

(ASX: TAW)Bald Hill Western Aust. Pegmatite Open pit

Exploration Target

30Mt-50Mt at

0.9-1.4% Li20

$100m

European Metals

(ASX/AIM: EMH)Cinovec Czech Republic Mica Underground

~650Mt at

~0.4% Li20$120m

Bacanora Minerals

(AIM/TSX: BCN)Zinnwald Germany Mica Underground

39.4Mt at

0.79% Li20GBP 104m

$184mBacanora Minerals

(AIM/TSX: BCN)Sonora Mexico Clay Open pit

420Mt at

0.68% Li20

Global Geoscience

(ASX: GSC)Rhyolite Ridge Nevada Clay Open pit

393Mt at

0.34% Li20 and

0.51% boron

$209m

* Approximate market capitalisations in 6 June 2017 (GBPAUD 1.75)

Source: Company announcements on ASX and AIM

For

per

sona

l use

onl

y

San Jose Lithium/Tin – the next 6 months

Plymouth Minerals Limited ASX: PLH | 16

Finalisation of Process Met early Q3 2017

Scoping Study Q3 2017

Mining Lease Application to be lodged late Q3 2017

PFS as early as Q4 2017

For

per

sona

l use

onl

y

Potash in Gabon100% of a major potash project on the coast

Plymouth Minerals Limited ASX: PLH | 17

For

per

sona

l use

onl

y

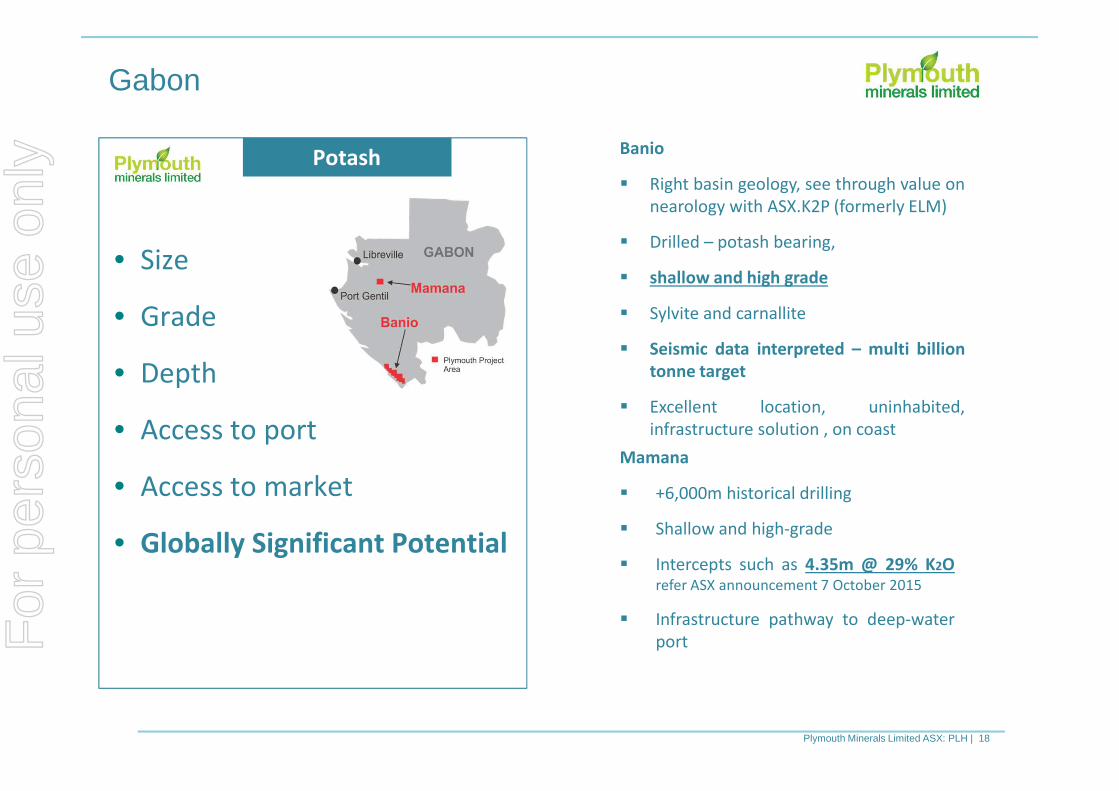

Gabon

Plymouth Minerals Limited ASX: PLH | 18

• Size

• Grade

• Depth

• Access to port

• Access to market

• Globally Significant Potential

Potash Banio

� Right basin geology, see through value on

nearology with ASX.K2P (formerly ELM)

� Drilled – potash bearing,

� shallow and high grade

� Sylvite and carnallite

� Seismic data interpreted – multi billion

tonne target

� Excellent location, uninhabited,

infrastructure solution , on coast

Mamana

� +6,000m historical drilling

� Shallow and high-grade

� Intercepts such as 4.35m @ 29% K2Orefer ASX announcement 7 October 2015

� Infrastructure pathway to deep-water

portFor

per

sona

l use

onl

y

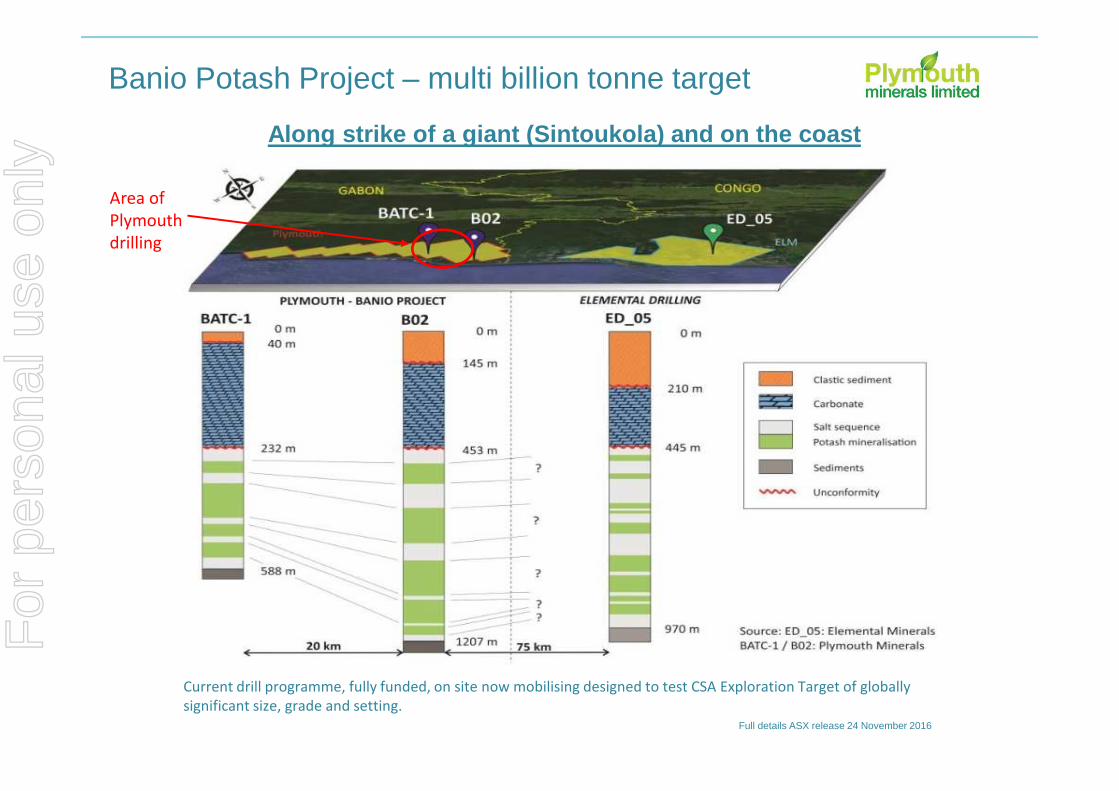

Banio Potash Project – multi billion tonne target

Current drill programme, fully funded, on site now mobilising designed to test CSA Exploration Target of globally

significant size, grade and setting.Full details ASX release 24 November 2016

Along strike of a giant (Sintoukola) and on the coast

Area of

Plymouth

drilling

For

per

sona

l use

onl

y

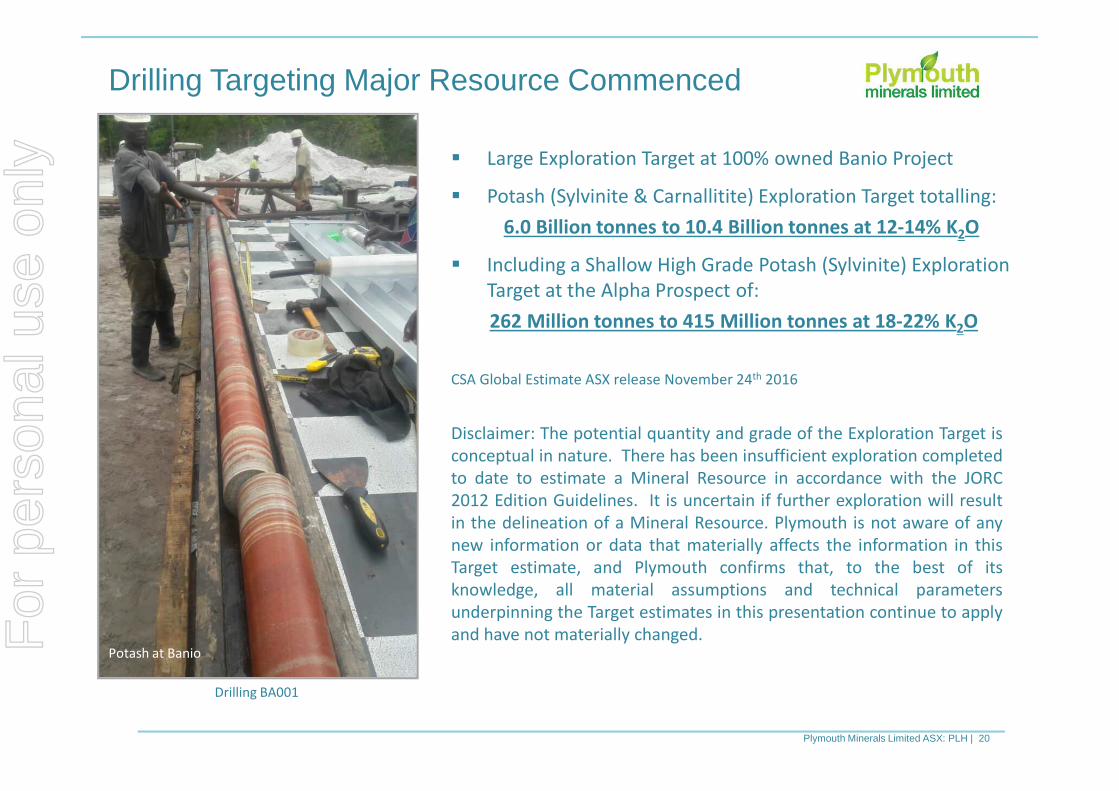

Drilling Targeting Major Resource Commenced

Plymouth Minerals Limited ASX: PLH | 20

� Large Exploration Target at 100% owned Banio Project

� Potash (Sylvinite & Carnallitite) Exploration Target totalling:

6.0 Billion tonnes to 10.4 Billion tonnes at 12-14% K2O

� Including a Shallow High Grade Potash (Sylvinite) Exploration

Target at the Alpha Prospect of:

262 Million tonnes to 415 Million tonnes at 18-22% K2O

CSA Global Estimate ASX release November 24th 2016

Drilling BA001

Potash at Banio

Disclaimer: The potential quantity and grade of the Exploration Target is

conceptual in nature. There has been insufficient exploration completed

to date to estimate a Mineral Resource in accordance with the JORC

2012 Edition Guidelines. It is uncertain if further exploration will result

in the delineation of a Mineral Resource. Plymouth is not aware of any

new information or data that materially affects the information in this

Target estimate, and Plymouth confirms that, to the best of its

knowledge, all material assumptions and technical parameters

underpinning the Target estimates in this presentation continue to apply

and have not materially changed.For

per

sona

l use

onl

y

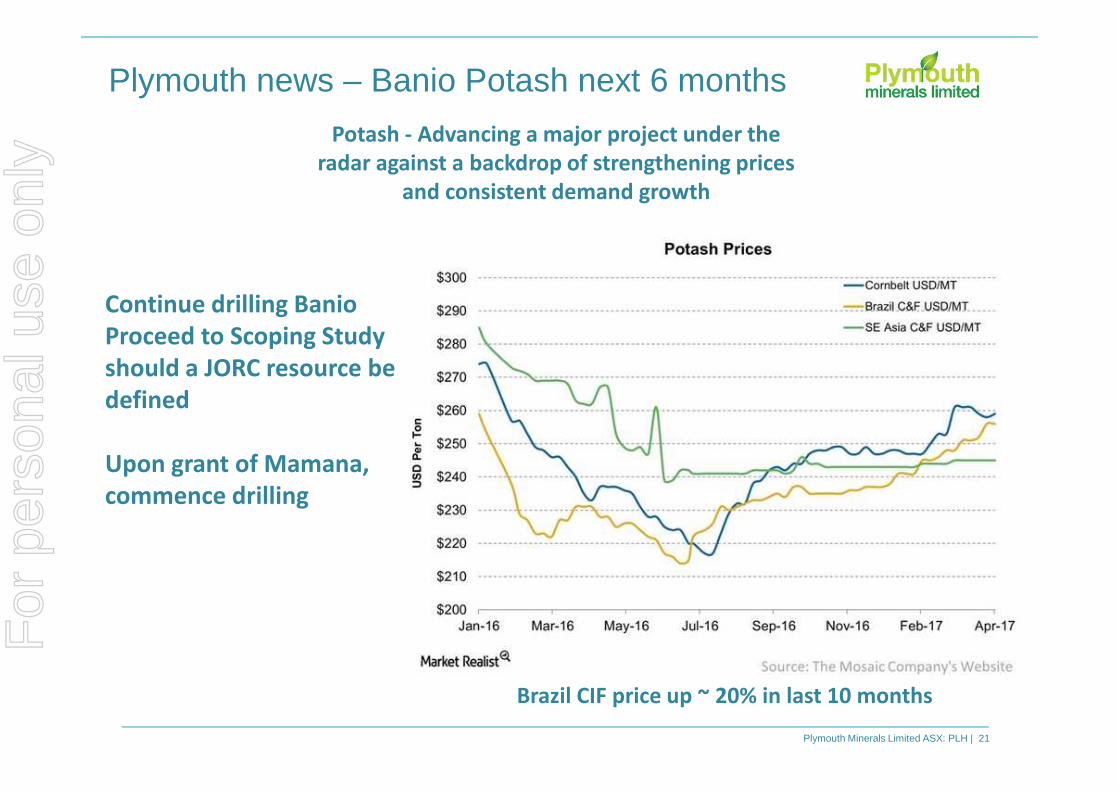

Plymouth news – Banio Potash next 6 months

Plymouth Minerals Limited ASX: PLH | 21

Continue drilling Banio

Proceed to Scoping Study

should a JORC resource be

defined

Upon grant of Mamana,

commence drilling

Potash - Advancing a major project under the

radar against a backdrop of strengthening prices

and consistent demand growth

Brazil CIF price up ~ 20% in last 10 months

For

per

sona

l use

onl

y

$28

100

115

$0

$20

$40

$60

$80

$100

$120

$140

Plymouth – Unlocking Significant Value

Plymouth Minerals Limited ASX: PLH | 22

� Entry into Plymouth today is effectively

“a ground floor entry” – given the

enterprise valuation of $28 million

today

� London direction for value unlocking

evolving

� San Jose Lithium - Right management,

Right Partners in Spain, Quality project

� Banio Potash – world class, see through

value, top quality African management

Banio Potash

� Large

� African Potash

� Neighbouring

Kore Potash

San Jose Lithium

� Large

� Lithium in Mica

� Open pit

� European

� Lithium in Mica

� Underground

� European� African Potash

� Neighbouring

project

� Extension of

potash

Enterprise

Value A$m

Prices as per ASX 12/6/17

For

per

sona

l use

onl

y

Thank you Plymouth Minerals Limited

T: +61 8 6461 6350 (AUS)A: Level 1, 329 Hay Street, Subiaco,

WA Australia, 6008W: www.plymouthminerals.com

CONTACT: Adrian Byass Managing DirectorP: +61 410 305 685E: [email protected]

For

per

sona

l use

onl

y

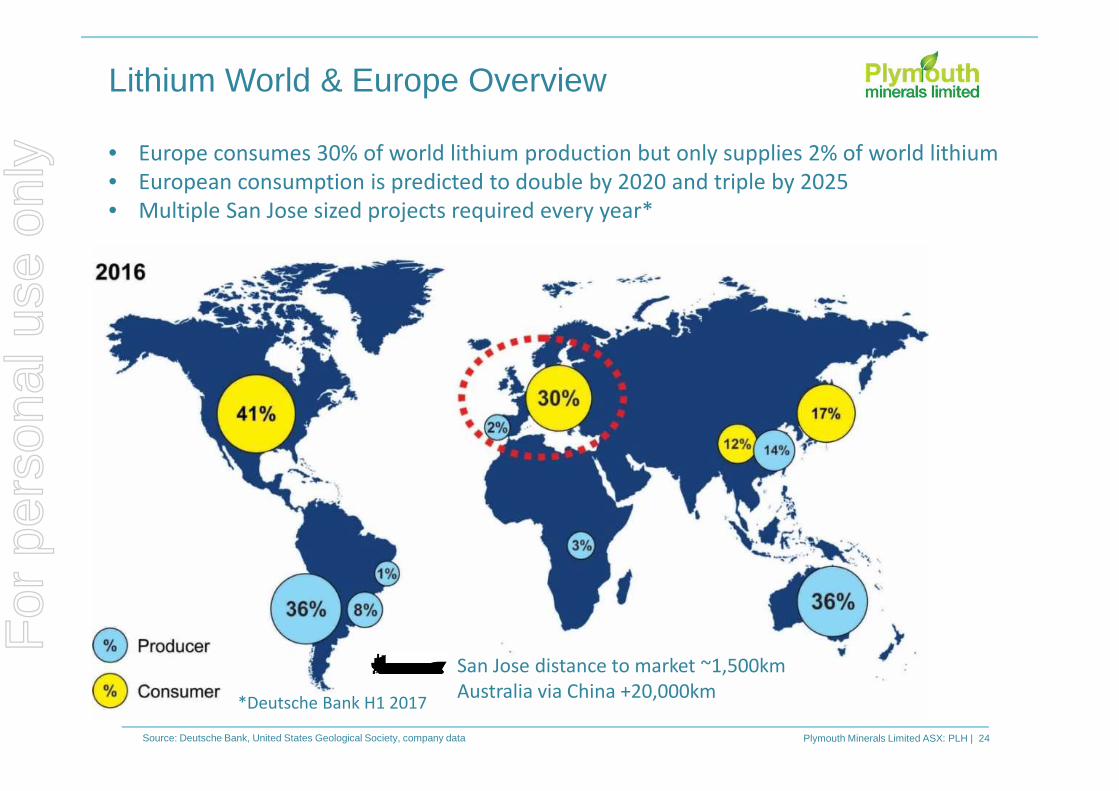

Lithium World & Europe Overview

Source: Deutsche Bank, United States Geological Society, company data Plymouth Minerals Limited ASX: PLH | 24

• Europe consumes 30% of world lithium production but only supplies 2% of world lithium

• European consumption is predicted to double by 2020 and triple by 2025

• Multiple San Jose sized projects required every year*

San Jose distance to market ~1,500km

Australia via China +20,000km*Deutsche Bank H1 2017

For

per

sona

l use

onl

y

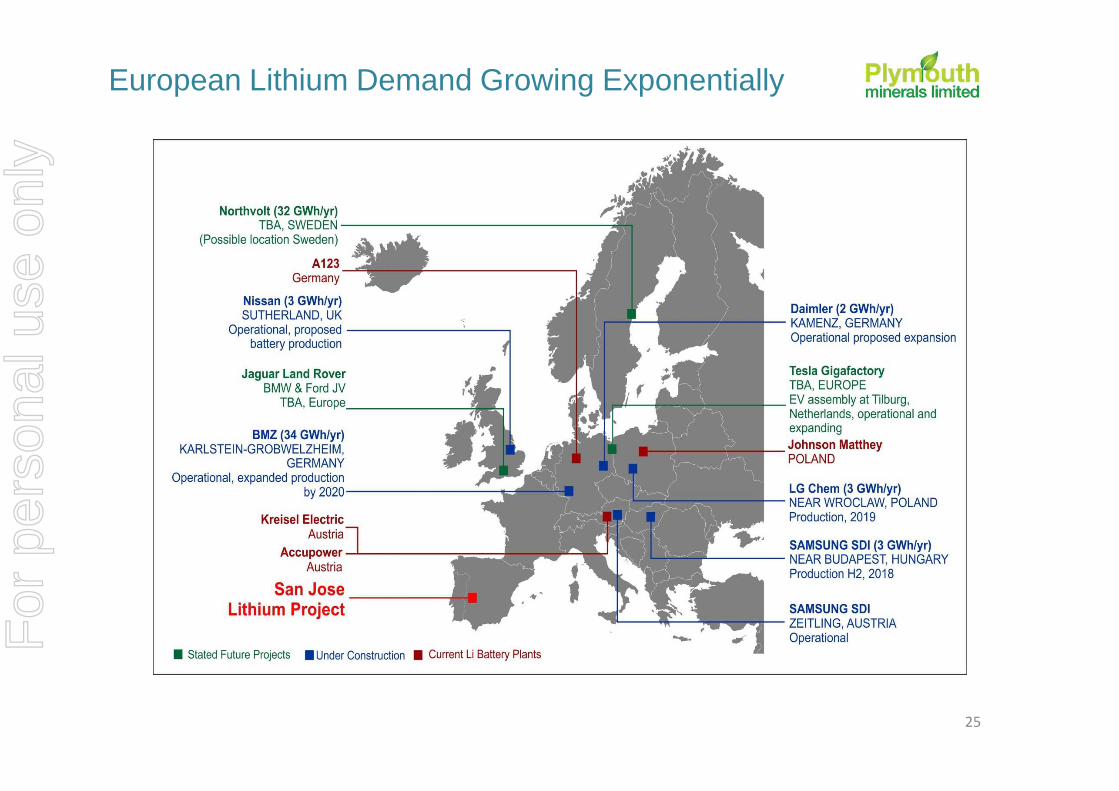

25

European Lithium Demand Growing Exponentially

For

per

sona

l use

onl

y