For personal use only - ASX · 2014-04-09 · Detached improving after jump in multi-res Detached...

6

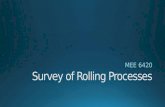

JP Morgan Building Forum Presentation CSR Limited – 10 April 2014 - 5,000 10,000 15,000 20,000 25,000 30,000 35,000 NSW/ ACT Vic/Tas Qld SA/NT WA Building approvals – growth continues across Australia All dwellings – six month rolling building approvals: s adj, Feb-14 2 Source: ABS For personal use only

Transcript of For personal use only - ASX · 2014-04-09 · Detached improving after jump in multi-res Detached...

JP Morgan Building ForumPresentation

CSR Limited – 10 April 2014

1

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

# Six month rolling building approvals: s adj, Feb-14

NSW/ ACT Vic/Tas Qld SA/NT WA

Building approvals – growth continues across Australia

All dwellings – six month rolling building approvals: s adj, Feb-14

2 Source: ABS

For

per

sona

l use

onl

y

Detached improving after jump in multi-res

Detached housesSix month rolling approvals: s adj, Feb-14

Multi-residentialSix month rolling approvals: s adj, Feb-14

3

-

2,500

5,000

7,500

10,000

12,500

15,000

17,500

20,000

22,500

#

NSW/ ACT Vic/Tas Qld SA/NT WA

-

2,500

5,000

7,500

10,000

12,500

15,000

17,500

20,000

#

NSW/ ACT Vic/Tas Qld SA/NT WA

Source: ABS

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Jun-2000 Jun-2002 Jun-2004 Jun-2006 Jun-2008 Jun-2010 Jun-2012

NSW Vic Qld

0%5%

10%15%20%25%30%35%40%45%50%

Jun-2000 Jun-2002 Jun-2004 Jun-2006 Jun-2008 Jun-2010 Jun-2012

medium density high rise Total Multi res

4

High rise gaining share of multi-res market

Multi-res now 44% of all dwelling approvals – historically 30%

– Consistent with international trends

Evenly split between high-rise and medium density

– Different demographic and geographic demands

High rise has been the growth segment

– Investor fuelled (both overseas and SMSF)

– >40% of all activity in NSW

– >20% of all national activity

High rise share of total approvals (MAT %, East Coast states)

Multi-res share of total approvals (MAT %, Australia)

Source: ABS

For

per

sona

l use

onl

y

0

20

40

60

80

100

120

140

400045005000550060006500700075008000

Co

nsu

mer

co

nfi

den

ce i

nd

ex

A&

A s

pen

d $

m

A&A (LHS) Consumer confidence index (RHS)

-

5,000

10,000

15,000

20,000

25,000

30,000

Commercial & Industrial Social & Institutional

Commercial up 22% MAT YoY

Social only up 8% MAT YoY

A&A and non-residential segments

Non-residential – swing from social to commercial

Commercial

– NSW & QLD lead commercial recovery; Vic flat

– Accommodation and office showing the strongest growth

Social

– Residual healthcare projects still in the pipeline

– Aged care targeted as major area for growth

Non-residential – Australia (MAT, $’m)

5

A&A – Australia (Quarterly, $’m)Alterations & additions market

Down from ~$8bn to ~$7bn a quarter

Yet to respond to lower interest rates and capital appreciation

Small scale renovations have held strong

Source: National accounts, Westpac MI and ABS approvals

Multi-res lag from commencement to completion is widening

6

2 year lag

Lag widening

Starts accelerating

Starts accelerating

Source: ABS, CSR analysis. Data shows MAT activity

For

per

sona

l use

onl

y

7

Lag time by construction segment

Segment Market size (A$bn)

Key drivers Lag trends

Growth outlook

Detached $26bn • First home buyers (FHB)• Upgrade/knockdown• Lot size/second storey

1-2Q lag • Recovery from record lows of 80k pa

• Land releases improving

Medium density• Semi

detached• Units 1-3

storey

$7bn • FHB• Empty nesters/retirees• Infill

2Q+ lag • Long term CAGR of ~7%• Trade-off between land/scale for

location

High density • Units 4+

storey

$12bn • Investors (Aus and overseas)

• FHB, students, empty nesters

4-8Q+ lag • Similar growth rates and market size to medium density

• Bias to metro markets

A&A $30bn • Capital growth• Housing activity

1-2Q • Positive long-term growth outlook• DIY trends

Non-residential $40bn • Social (Ageing, Health)• Commercial (Office, Retail)

2-8Q+ • Social investment declining

Source: ABS Building Approvals and National Accounts

8

CSR increasing exposure beyond detached housing

Gyprock Cemintel Bradford Hebel Bricks Roofing Viridian

Detached 1 to 1 High Moderate HighLow, but growing High High High Hebel, Cemintel

Medium density 2 to 1 Moderate Low Moderate Low Moderate Low Low Hebel, AFS

High density 3 - 5 to 1 Low Low Low High Nil Nil Low Hebel, AFS, Viridian

A&A n/a High High ModerateModerate,

growing Moderate Low Moderate Viridian

Non-residential n/a Moderate Moderate Low Low Moderate Low LowBradford Energy Solutions, Ceilector

Building segment OpportunitiesEquivalent house

(revenue)

Material penetration intensity

For

per

sona

l use

onl

y

9

Protect and invest in our businesses and people

Key initiative Progress

Improved margins • Price increases and cost savings delivered $11

million improvement in Building Products EBIT

for half year to Sept 13

Viridian turnaround on track

• Ingleburn glass site closed in July 2013 – with

no loss of major customers

• $5 million in lower costs following

shutdown

• Wetherill Park relocated ahead of schedule

Customer focus • CSR Connect online customer portal launched

in April last year – adding new functionality

• Progressing real time delivery updates,

improved sales force tools

Further rationalise operations

• East Coast Bricks JV with Boral announced –

ACCC review process underway

9

Strategic growth priorities

Key initiative Progress

Smarter, faster and easier

• Ongoing research and testing of pre-fabricated housing

systems – investment committed

• Hebel House construction time of two weeks

• Acquisition of AFS – leader in permanent formwork in

the multi-residential market

Adapting to the changing way we live and work

• Strong growth in Hebel through investment in

installation and inspection services - strong value

proposition for developers

Improvingcomfort, quality and energy efficiency

• Bradford expanding range of products and services in

ventilation, construction fabrics

• Acquisition of Martini to expand range into polyester

insulation

• Bradford Energy Solutions – energy efficient projects

initiated across all CSR sites and external consulting

services

10

For

per

sona

l use

onl

y

ACCC review process underway

Structure reflects relative valuation of the businesses

Initial overhead savings of $7-$10m pa

Longer term, opportunities to improve operational efficiencies and release high value land assets without impacting product range

11

East Coast Bricks Joint

Venture60% 40%

PGH bricks in NSW, Qld, Vic and SA

Schofields, NSW site used for the term of

an agreed lease period

Boral bricks in NSW, Qld and Vic

Scoresby, Vic site used for the term of

an agreed lease period

Retain Schofields, NSW land

title, lease to JV

Subdivide & retain

surplus land at Horsley Park, NSW and Oxley,

Qld

Retain Scoresby, Vic

land title, lease to JV

Subdivide & retain

surplus land at Bringelly,

NSW

East coast bricks JV transaction structure

Acquisition of AFS

Leader in load bearing permanent formwork walling solutions

Faster and less complex building solutions

– Increased speed of construction

– Lower labour costs and crane requirements

Logicwall® fibre cement based permanent formwork systems:

– Scalable production facility at Goulburn, NSW to meet growing demand in multi-residential market

– Over 30,000 multi-residential units completed to date

– CSR Cemintel current supplier of fibre cement products

Rediwall® polymer-based (PVC) permanent formwork system

– Concrete wall system that is water resistant

– Used in basement and retaining walls in multi-residential and commercial

AFS load bearing walling system complements CSR’s non-load bearing walling products (Gyprock, Bradford and Hebel)

12

For

per

sona

l use

onl

y