Foodservice Opportunities for Beef, Pork, Bison & Lamb in

105

Foodservice Opportunities (in Hotels, High-end Restaurants, Chains, & Universities) for Beef, Pork, Bison & Lamb in Saskatchewan & Alberta FINAL REPORT Submitted By: Hodgins & Company 105 – 111 Research Drive Saskatoon, Saskatchewan CANADA S7N 3R2 December 2002

Transcript of Foodservice Opportunities for Beef, Pork, Bison & Lamb in

Foodservice Opportunities(in Hotels, High-end Restaurants,

Chains, & Universities) for Beef, Pork, Bison & Lambin Saskatchewan & Alberta

FINAL REPORT

Submitted By: Hodgins & Company

105 – 111 Research Drive Saskatoon, Saskatchewan

CANADA S7N 3R2

December 2002

TABLE OF CONTENTS PAGE

EXECUTIVE SUMMARY PART ONE – Background Information 1 1. Introduction 2 2. Objectives 2 3. Methodology 3 PART TWO – Publications and Internet Review 4 4. Publications and Internet Review 5 4.1 Description of the Foodservice Industry 5 4.2 The Market 6 4.3 Market Drivers 10 4.4 Trends 12 4.5 Consumers 15 4.6 Products 16 4.7 Price 23 4.8 Promotion 23 4.9 Competition 24 4.10 Distribution 27

4.11 Issues 32 4.12 Critical Success Factors 34 4.13 The Future 35 4.14 Conclusion 36

PART THREE – Interview Findings 37 5. Interview Findings 38

5.1 Overview 38 5.2 Trends 39 5.3 Foodservice Customers 40 5.4 Products 41 5.5 Product Usage 47 5.6 Pricing 48 5.7 Promotion 49 5.8 Suppliers 50 5.9 Universities 57 5.10 Issues 62 5.11 Critical Success Factors 63

PART FOUR – Market Viability & Conclusions 65 6. Market Viability 66 6.1 Conclusions 66 6.2 The Opportunity 70 APPENDIX A – List of Interviews APPENDIX B – List of Restaurants APPENDIX C – Typical Weekly Meat Requirements at

University of Saskatchewan APPENDIX D – Western Canadian Imports of New Zealand and

Australian Beef

Foodservice Opportunities – Beef, Pork, Bison, Lamb

Executive Summary i

EXECUTIVE SUMMARY Saskatchewan Agriculture Food and Rural Revitalization contracted Hodgins & Company Management Consultants Inc. to undertake a study to assess and identify the market potential for beef, pork, bison and lamb products in the high end and chain foodservice industry in Saskatchewan and Alberta. The study was to provide processors and suppliers with an understanding of the market’s supply chain and its requirements for entry. Specifically, the attached report reviews:

• A market assessment; • A competitive analysis of the distributors and suppliers to the market; • Specific opportunities; and • Market viability.

The scope of the project was limited to foodservice outlets in hotels and high end restaurants and chains in the two provinces. In addition, four prairie universities were included in the project in order to understand their foodservice needs (universities of Saskatchewan, Regina, Calgary and Alberta). The research methodology for this study included a publications’ and internet review as well as 59 interviews with representatives from restaurants, distribution centers, foodservice management groups, and processor/distributors. The Industry The foodservice industry represents an important component of the economy. In Canada, sales in the industry were valued at $41.1B in 2001 and is expected to reach $42.6B in 2002 according to the Canadian Foodservice and Restaurant Association (CFRA). As well, the industry represents a major source of employment for youth between the ages of 15 and 24. 2001 represented the eight consecutive year that the sector has gained share from supermarkets and other food retailers. The CFRA states that of every dollar spent on food in Canada in 2001, 41.1 cents went to foodservice (compared to 46.1 cents in the U.S.). By 2007 the figure is expected to exceed 50% of the consumer food dollar. Trends affecting the industry include:

• The changing life situation in households with more households reporting “no children” (recent research identifies the presence or absence of children as a major determinant of food and beverage choices for a household);

Foodservice Opportunities – Beef, Pork, Bison, Lamb

Executive Summary ii

• The growth of dual income households reflecting the growing affluence (increased disposable income to spend on food outside the home) and the need for convenience in food offerings;

• Increasing concern about nutrition affecting the menu choices available (chicken sales are now on par with beef sales at foodservice outlets);

• Increasing diversity of the Canadian population reflecting the rise in foodservice menu offerings of ethnic foods;

• Product branding where menus sport brands recognizable to consumers (e.g. Alberta Beef, Maverick Natural Beef, Neilson’s Ice Cream);

• Supermarkets expanding into commercial foodservice outlets where food retailers are offering full-service dining opportunities; and

• The growth of the “fast and easy dining chains” in Western Canada (e.g. Moxie’s, Earl’s, etc.) that are gradually securing market share from the fine dining outlets as well as the independent outlets.

Based on the interviews, the foodservice consumer segments in Alberta and Saskatchewan are (in priority):

• The business and professional customer (particularly “the lunch crowd”);

• Tourists (particularly in Alberta); • Families; • “Locals”; and • “The young crowd” (23-35 years old).

In order to service these segments, foodservice outlets in Saskatchewan and Alberta offer a variety of protein sources. Without a doubt, the main protein sources being sold are beef and poultry. Pork is a distant third in the rankings overall (with about 50% of sales being bacon for breakfasts), and lamb and bison an even more distant fourth and fifth. Very little value adding of product by processors is being done to target this industry in the two provinces although the smaller distributors such as Prairie Meats and Chef-Redi offer products such as kabobs, marinated steaks, and dry ribs. Most outlets add the value themselves due to the perception that portion steaks do not meet the quality standards. In addition, there is concern about potential labour strife at the outlet(s) if products are used that may result in a reduced workforce. A major issue for the foodservice operators is the cost of protein on any given menu offering (“centre-of-the-plate” pricing). On average, the food share of total foodservice cost runs about 30-33% (although the highest noted was 45% for Boffins in Saskatoon and the lowest being 29% at the Elephant & Castle). The centre-of-the-plate cost (protein cost) was then identified as being anywhere between 50-88% (average being 63%) of the total cost of food depending on the level, quality and distinctiveness of their garnishes.

Foodservice Opportunities – Beef, Pork, Bison, Lamb

Executive Summary iii

The foodservice outlets in Saskatchewan are primarily using the following distributors:

• SYSCO/Serca; • Centennial Meats; • Prairie Meats; • Chef-Redi Meats; and • Sunspun.

The foodservice outlets in Alberta are primarily using the following distributors:

• Bridge Brand/Gordon Foods; • SYSCO/Serca; • Western Quality Meats; • Centennial Meats; • Intercity Meats; and • Edmonton Meat Packing Ltd..

Note that SYSCO is the distributor of choice to the Universities of Saskatchewan, Regina, Calgary and Alberta. Foodservice outlets, even the independents (except in small rural areas distant from distribution centres) usually use the services of several suppliers, even for the same commodity in order to get the best price (e.g. two or three suppliers for beef). Some foodservice outlets, and in particular the chains, often enter in a contract with the larger distributors. For example, most chains are either using SYSCO or Gordon Foods. The contract is based on expected volumes. Any foodservice outlet that exceeds those volumes can source product from other suppliers for reasons such as a better price, quality, etc. Or the contract may be for a minimum order thus allowing outlets to use other sources. In the case of universities/hotels/food chains, it is often the practice to choose the end supplier and then direct the distributor to use that supplier. Contracts are usually entered into anywhere from six months to 2 years. The smaller independents however do not work on contract. Conclusions The foodservice industry on the prairies as examined for this report will be very difficult to penetrate and make substantial gains. Any processing facility or producer wishing to penetrate the industry is faced with the following situation.

• The foodservice market on the prairies is extremely competitive. The market is mature with growing competition from the chains classed as casual or licensed (e.g. Moxie’s, Earl’s, Tony Roma’s, etc.). Smaller independent restaurants and local chains are having an increasingly

Foodservice Opportunities – Beef, Pork, Bison, Lamb

Executive Summary iv

difficult time competing as it is more difficult for them to receive the volume discounts that the chains can garner.

• This is a price driven industry: While the ability to provide the

type of product with the desired quality attributes at the volume required is the “admission price” to being a supplier to the foodservice industry, once those requirements are met, price is the primary consideration with service being a close second.

Margins are small and volume sales are required to make a profit.

The industry as examined for this project is comprised of high end restaurants, casual chains and independent restaurants. The following table outlines what each of these categories demand from their suppliers. The points are listed in priority.

Supplier Requirements - Foodservice Outlets High End Chains (Casual) Independent (Casual)

Top quality meat (and if in Alberta – must be Alberta beef)

Ability to supply entire chain consistently

Best price

Consistent quality Best price Appropriate sizing of the meat

Trusted supplier (often deals with large distributor)

Appropriate sizing of the meat

Consistent supply

Best price Meet specifications Ability to deliver a couple of times a week if required

Ability to deliver daily if required

Consistent quality & size Will deal with smaller distributors

Deals with large distributor Ability to deliver daily if

required

While “price” may not have been listed as the most important factor in supplying all categories, it is still a critical issue. This entire industry appears to be price driven. This is a result of the high degree of competition in the marketplace as well as consumer resistance to menu price increases.

• Consumers in the two provinces are classed generally as being

the “meat and potatoes” crowd. And until Saskatchewan is deemed a destination place for tourists, it likely will not have the level of high end restaurants that Alberta enjoys. Generally Saskatchewan foodservice consumers are more price sensitive than their Alberta neighbours.

• The main protein items in demand for this market are beef and

chicken. With particular focus on beef, the market issues on the prairies are:

Consumer concern over health: beef vs. chicken;

Foodservice Opportunities – Beef, Pork, Bison, Lamb

Executive Summary v

Quality perceptions: beef vs. “Alberta Beef”; Size requirements: Canadian beef vs. Australian/New Zealand

beef; and Price considerations: Canadian beef vs. Australian/New

Zealand beef.

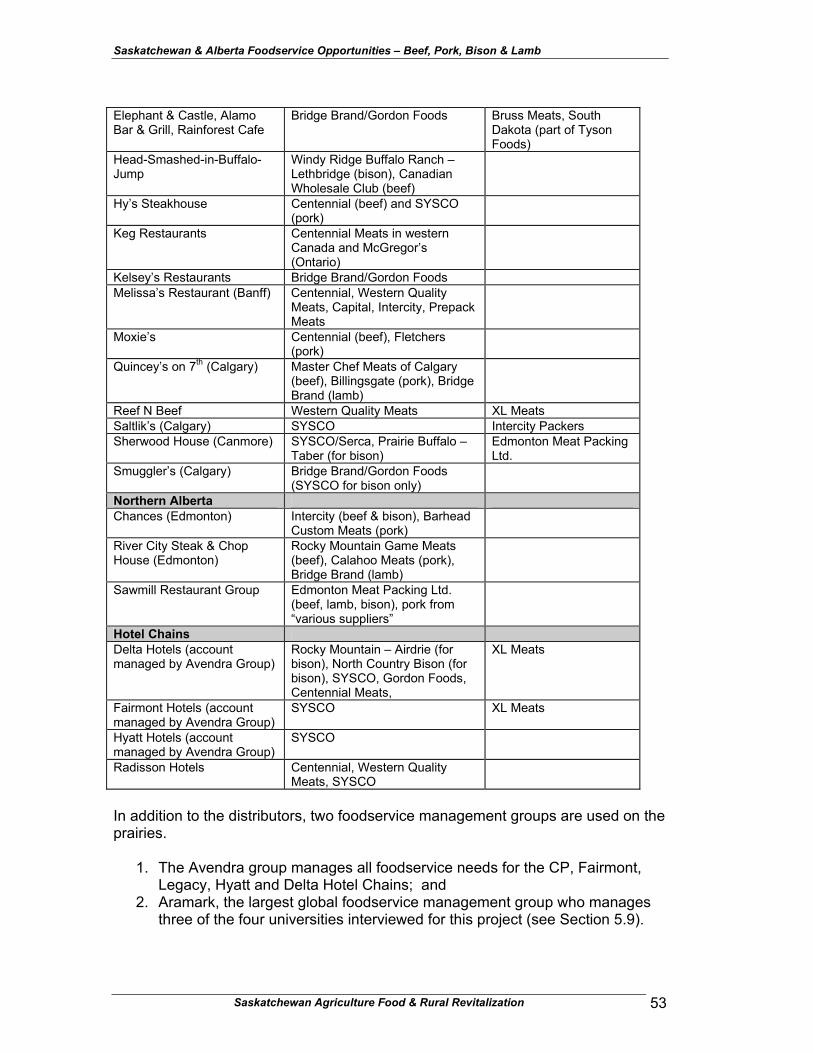

Alberta Beef: The Alberta producers enjoy a marketing advantage by having successfully built a brand that is recognized internationally and equates to top quality beef. Regardless of whether the meat is in fact top quality or just perceived to be, it would be difficult at this point to build a Saskatchewan brand that would rival the reputation of the Alberta product. In addition, the cost to build a brand is significant (anywhere from $2M to $30M). New Zealand/Australian beef: The market in Western Canada for New Zealand and Australian beef has increased significantly over the past four years. The following chart illustrates the value of the imports to this region. [Note however that it is not possible given this information to determine where the product is used (e.g. retail, foodservice, etc.).]

Value of Beef Imports to Western Canada Australia and New Zealand – Value in $ ‘000s

$0$10,000$20,000$30,000$40,000$50,000$60,000$70,000$80,000

1998 1999 2000 2001

AustraliaNew Zealand

Source: Statistics Canada

In other words, the market for Australian and New Zealand beef in Western Canada has doubled in just four years.

• The current suppliers are meeting the demand for pork. One

area that requires monitoring however is the demand for back ribs. Only one distributor claimed to have had difficulty in sourcing that particular product last year.

• Alberta and New Zealand producers are currently meeting the

demand for lamb. As with beef, the smaller size of the New Zealand racks as well as their lower price, make it suitable for the foodservice market. Since the demand for lamb in foodservice is

Foodservice Opportunities – Beef, Pork, Bison, Lamb

Executive Summary vi

very small, it is likely not a market that warrants examining for import displacement until lamb producers can influence consumers to purchase it for more meal occasions (in other words, producers must work to create demand for their product).

In addition, if lamb producers wish to supply this market, they must be prepared to find markets for the lesser quality cuts.

• Bison represents a specialty product at this time. While bison

burgers and some high value cuts are used in tourist areas as well as “specials” on fine dining menus, the market is limited. The restaurants and distributors that are using the product have found suppliers that offer consistent quality and most buyers are not prepared to try new suppliers for this product. In addition, bison producers must decide who their market is. They have damaged their reputation by selling to (or attempting to sell to) distributors and then directly to the restaurants to whom the distributors supply.

The Saskatchewan Opportunity There are three ways in which to participate as a supplier to the foodservice industry:

• As a distributor; • As a processor; or • As a producer.

It would be very difficult for a new processor to penetrate this market as a distributor to the foodservice industry. Competition is fierce. The large established players are consolidating. Due to their size, they bring massive buying power and can secure lower prices based on volume purchases which are then passed off to the restaurants. They are now going after the markets of the smaller distributors who are experiencing increasing pressure from the large distributors. Indications are that these large distributors are determined to fight among themselves over the smaller market share. Saskatchewan processors then have two potential markets:

1. To supply the larger distributors (e.g. SYSCO, Gordon Foods) who have the contracts with the chains or the high end restaurants (they must be able to meet the requirements of the distribution company); or

2. To supply the high end restaurants or the independents directly. Saskatchewan processors will be challenged to penetrate the market (as examined in this report) beyond its borders and even within its borders given the competitive nature of the business.

Foodservice Opportunities – Beef, Pork, Bison, Lamb

Executive Summary vii

In consultation with a member of the Steering Committee who has in-depth knowledge of the Saskatchewan meat processing industry, it became clear that the processors either are currently providing some supply to the foodservice industry or are devoting their production and marketing efforts elsewhere. They are likely not in a position (have the resources) or have the interest to penetrate this market due to their current strategies. The option for consideration at the processor level may be for three or four smaller processors to form some sort of cooperative action to supply a distributor already servicing this industry. The cooperative action of course provides them the opportunity of supplying the quantities required to enter the market. The challenge in that scenario is that the alliance would require common standards and strict adherence to quality demands, pricing strategies and meeting delivery schedules. The producers may represent the best opportunity to supplying this market. That opportunity is import replacement of the Australian and New Zealand products. Before examining this market, producers must understand that the smaller size of the cut is not the only reason that the off-shore product is in demand. It is a combination of size AND price. In order to determine if the import replacement option is a viable opportunity, there needs to be a good understanding of the production processes and transportation of the Australian and New Zealand products. In other words, how can that smaller cattle be produced, processed, shipped to Western Canada and still be priced at or lower than Canadian beef. In addition, the examination should consider the appropriate size of herd(s) that would be required to fill the demand. This does not likely represent an opportunity for all beef producers but rather a small group. Therefore, if a Canadian product can be produced (e.g. a ten pound and under striploin) that meets the price and at least meets the quality, then it will be the product of choice. The other area where opportunity may exist but was not examined, is for value added products targeted at foodservice outlets where food is not the primary source of revenues and who have limited food preparation space (e.g. bars). Small processors are encouraged to examine this market segment to determine if the option is viable.

Foodservice Opportunities – Beef, Pork, Bison, Lamb

Saskatchewan Agriculture Food and Rural Revitalization 1

PART ONE BACKGROUND INFORMATION

Foodservice Opportunities – Beef, Pork, Bison, Lamb

Saskatchewan Agriculture Food and Rural Revitalization 2

1. INTRODUCTION Agricultural producers and food processors in Saskatchewan are seeking new markets or growth areas in current markets for their products. The foodservice industry may be such a market as it represents 4% of Canada’s gross domestic product.1 In addition, certain segments within foodservice are realizing significant growth. Saskatchewan Agriculture Food and Rural Revitalization (SAFRR) therefore wishes to explore the foodservice industry on the prairies to evaluate its true potential with particular focus on the red meat products. This report examines and assesses the opportunities available for both small processors and livestock producers in the province. SAFRR contracted with Hodgins & Company Management Consultants Inc. to undertake the market study. 2. OBJECTIVES The overall objective of this study was to assess and identify the market potential for beef, pork, bison and lamb products in the Saskatchewan and Alberta restaurant, hotel and university segments of the foodservice market in order to provide processors and suppliers with an understanding of that market’s supply chain and its requirements for entry. More specifically, the objectives were to:

1. Undertake a market assessment: • Quantify the market for beef, pork, bison and lamb products

in Saskatchewan and Alberta; • Detail foodservice trends; • Outline products served (including relative pricing and

consumption patterns); • Storage and shipping requirements; and • Outline the critical success factors for entry and

sustainability.

2. Undertake a competitive analysis of the distributors and suppliers to the market that will: • Provide an overview of the distributors and meat suppliers

currently servicing the market.

3. Identify specific opportunities including identification of: • Pricing requirements; • Buyers; • Product forms required; and • Procurement policies.

1 www.crfa.com

Foodservice Opportunities – Beef, Pork, Bison, Lamb

Saskatchewan Agriculture Food and Rural Revitalization 3

4. Assess market viability (e.g. identify if the market can be

penetrated). The scope of the project was limited to foodservice outlets in hotels and high end restaurants and chains. In addition, four prairie universities were included in the project in order to understand their foodservice needs (universities of Saskatchewan, Regina, Calgary and Alberta). A list of interviewees was provided to the steering committee for approval. 3. METHODOLOGY The research methodology for this study included:

• A publications and internet review;

• Interviews: In total 59 representatives from restaurants, distribution centers, foodservice management groups, and processor/distributors were interviewed during the course of the project. See Appendix A for a list of interviewees. Note that some distributors asked that specific quantity information not be included in this report but was provided to give perspective to the consultants.

The results of the study are outlined in the following report. The findings are summarized in:

Part Two: Publications and Internet Review; Part Three: Interviews With Industry Stakeholders; Part Four: Market Viability and Conclusions

Foodservice Opportunities – Beef, Pork, Bison, Lamb

Saskatchewan Agriculture Food and Rural Revitalization 4

PART TWO PUBLICATIONS & INTERNET REVIEW

Foodservice Opportunities – Beef, Pork, Bison, Lamb

Saskatchewan Agriculture Food and Rural Revitalization 5

4. PUBLICATIONS & INTERNET REVIEW 4.1. Description of the Foodservice Industry The foodservice industry is typically categorized into two major areas, commercial and non-commercial. The division is usually dependant on whether the food purchase is the primary purpose of the business.2 The commercial segment of the foodservice industry is the sub-sector most often seen by consumers. Statistics Canada defines the commercial sectors as being comprised of the following five business segments:

1. Licensed restaurants: The largest segment holds a liquor license and predominantly serves food.

2. Unlicensed restaurants (known in the U.S. as “fast casual”): The second largest segment does not serve alcohol but has seats for their guests and is usually quick service restaurants (e.g. MacDonald’s, Harvey’s).

3. Take-out and delivery: This segment does not serve alcohol and provides very limited seating for guests (e.g. Pizza Pizza, KFC).

4. Social and contract caterers: Companies that cater cafeterias in schools, hospitals, homes for the aged, etc. (e.g. Versa Services, Beaver Foods).

5. Pubs and taverns: While these enterprises serve food, most sales are derived from alcoholic beverages.

For perspective, the non-commercial foodservice sector serves food as a necessity to “quasi-captive” clientele. This sector includes all food sold through hotels, motels and resorts including fine dining, catering and quick-service at these establishments. As well as hospitals, schools and prisons (definitely a captive customer), food sold through outlets at leisure venues such as movie theatre snack bars, ball parks, arenas, vending machines, department stores and institutions are also included in the non-commercial sector.3 The commercial foodservice sector represents an important component of the economy. Figures from the United States indicate that for every dollar spent dining out, another $2 in business is generated for other industries. While not confirmed, it is likely that the multiplier effect is similar for Canada. It is little wonder that the foodservice industry has been dubbed “the cornerstone of the economy”.4

2 www.agr.gov.ca/food/industryinfo/distribution/distribution.pdf 3 Ibid. 4 www.restaurant.org/cornerstone/economy.cfm

Foodservice Opportunities – Beef, Pork, Bison, Lamb

Saskatchewan Agriculture Food and Rural Revitalization 6

4.2 The Market The global foodservice industry is currently valued at US$1.2 trillion5 and is considered to be “the most dynamic sector of the food market” given that it is growing at a rate five times that of retail. Even with the high value of the industry, 2001 represented what one industry CEO considered to be “the worst demand situation in 10 years”.6 The combined effects of the recession and the terrorist events of September 11, 2001 in New York, kept customers away from the commercial restaurants. This was mainly due to the slowdown of business and leisure travel. Over 2001, most establishments saw sales down anywhere from 5%-20% on average. 7 While many articles noted that business has come back in 2002, others indicated that sales from tourism are still down. The Canadian Restaurant and Foodservice Association (CRFA) credits this sector (tourism) as comprising 22% of commercial foodservice sales. Therefore, if tourism decreases, then commercial foodservice take a direct hit. Another effect of the difficult 2001 year is that while customers are back to eating out, many have turned from the upscale restaurants to more moderately priced restaurants.8 The CRFA states that the current value of foodservice (including both commercial and non-commercial) in Canada was valued at $41.1B in 2001 and is expected to reach $42.6B in 2002. It is the single biggest customer for many food producers and processors. The following chart provides an overview of the foodservice industry in Canada. It is evident that the commercial sector makes up the lion’s share of the industry.

5 http://just-food.com/features_detail.asp?art=452 6 “Steakhouse Trendsetters: Sizzle and Substance”, Meat Marketing & Technology, March 2002. 7 Ibid. 8 Ibid.

Foodservice Opportunities – Beef, Pork, Bison, Lamb

Saskatchewan Agriculture Food and Rural Revitalization 7

Table One: The Foodservice Market in Canada - 2001

Full Service Rest.37%

Retail2%Other

4%

Institutional6%

Accomoda-tions11%

Bars5%

Caterers7%

Limited Service Rest.

28%

Source: Foreign Agricultural Service/USDA

The special foodservice sectors that include foodservice contractors, social caterers and mobile foodservice registered the largest growth rate in 2001 with an 18.5% increase in revenues with limited service restaurants enjoying an 8% growth rate. And pubs, bars and full service restaurants grew by 7% in 2001.9 The CRFA expects that consumer preference will make the full service restaurant the fastest growing channel over the next decade.10 However, limited service restaurants like Burger King are showing less robust growth with some exceptions such as Subway.11 Canadian consumers spent $29.9 B in various commercial foodservice outlets in 2001.12 For this industry in Canada, operators purchase annually:13

• $14.7 B worth of food and beverage products including: o $2.6B worth of beef; and o $2.5B worth of chicken.

The following table provides an overview of the Canadian industry and for comparison purposes, also provides a picture of the industry in the United States. 9 www.statcan.ca/daily/English/020628/d0206281.htm 10ww.crfa.ca/research/foodservicetrends/research_foodservicetrends_foodservice2010.htm 11 Davis, David; Stewart, Hayden, “Changing Consumer Demands Create Opportunities for U.S. Food System”, Economic Research Service, USDA, FoodReview, Spring 2002. 12 www.agr.gco.ca/food/consumer/mrkreports/consumers_e.html 13 Source: Canadian Restaurant and Foodservice Association.

Foodservice Opportunities – Beef, Pork, Bison, Lamb

Saskatchewan Agriculture Food and Rural Revitalization 8

Table Two: The Canadian Foodservice Sector - 2001 Description Canada

(CDN$) U.S.

(CDN$) Foodservice sales 2001 $41.1 B

(commercial & non-commercial))

$611.5B (commercial

only) Food purchases (@32% of sales) $13.2 B Alcoholic beverage purchases (@3.7% of $41.1B in sales)

$ 1.5 B

Employment in foodservice sector * 978,700 11.66M Commercial sector sales 2001 $29.9B $408B Forecasted annual commercial sector sales growth to 2005 (in 2001 dollars)

2.5%

Number of restaurants, caterers, pubs, bars and nightclubs

64,000 850,000

Average sales per commercial unit 2001 $576,000 Food purchases per commercial unit $184,000 Profit margin before taxes 6.6% Source (Canadian figures): Canadian Restaurant and Foodservice Association

Source (US Figures): www.restaurant.org * The commercial foodservice industry employs 42% of employed youth between the ages of 15 and 24 (CRFA). Regionally, Western Canada represented 34.6% of national food services in 1999 according to the United States Department of Agriculture (USDA). There are over 40,000 commercial outlets in western Canada with the chains and their associated franchisees dominating the independents. In 1999 terms British Columbia enjoyed 15.9% of national sales, Alberta 13%, Saskatchewan 3% and Manitoba 2.8%.14 In general, the CRFA has updated its forecast for commercial foodservice sales for 2002 as a result of an apparent stronger economy in Canada than the U.S. and gains in the labour market. While the revised forecast for 2002 is for a 4% growth, higher menu prices are expected to hinder real sales growth reducing real foodservice sales to just 1.2%. The growth is expected to be a result of the recovery in the second half of the year as many of the provinces showed a dramatic decrease in the first quarter. Alberta led the way in a 10.5% decline in real foodservice sales and Saskatchewan was down 6.6% during that time period. In 2003 however sales are expected to result in a 4.3% real growth.15 The foodservice share of the total food dollar spent by consumers is also an important perspective when examining the growth of the industry. 2001 represented the eighth consecutive year that the sector has gained share from supermarkets and other food retailers. BUT, the figures reflect the devastation felt by Canadian foodservice operators as a result of the introduction of the GST. Of every dollar spent on food in Canada, 41.1 14 Woodcock, B., USA Food Export, Inc., “Canada HRI Food Service Sector – Hotel, Restaurant, Institutional Sector Report – Western Canada, 2000”, Foreign Agricultural Service/USDA, August 2000. 15 www.crfa.ca/research/research_foodservicealestoheatup.htm

Foodservice Opportunities – Beef, Pork, Bison, Lamb

Saskatchewan Agriculture Food and Rural Revitalization 9

cents16 (compared to 46.1 cents in the U.S. 17) went to foodservice in 2001 up slightly from 40.7 cents in 2000 but below the 42.1 cents back in 1989 prior to the GST. The GST and a recession resulted in the foodservice market share to fall to a low of 37.1% of the total food dollar in 1993. The following table provides an overview of the past decade of the share of the total food dollar spent in the foodservice sector for both Canada and the U.S. (the rest being spent for food in the home).

Table Three: Foodservice Share of the Total Food Dollar

0%

10%

20%

30%

40%

50%

1989 1993 1997 2001

CanadaUnited States

Source: Foodservice Facts 2002

Expectations are that by 2007 the foodservice share will exceed 50%. This is important to note as the USDA’s Economic Research Service predicts U.S. food expenditures will increase 26% over the next 20 years. 18 As illustrated above, Canadian figures usually lag but do follow the trends in the U.S. When examining the potential growth of the industry, consideration should be given to factors such as population growth, greater service costs and food price inflation which can skew the figures.19 In other words, real growth figures will likely be less than projected. In addition to the commercial foodservice sector, the non-commercial sector is an important growth area. In fact institutional foodservice is forecast to be the fastest growing foodservice sector in 2002 with 4.1% increase over 2001. The highest growth area in the institutional sector is “education” with a forecasted growth of 7.3%. The growth is a result of an increase in enrollment at colleges and universities which “will make self-operated education foodservice the fastest growing sub-sector”.20

16 According to the CRFA, the foodservice share of the stomach is based on total foodservice spending in Canada at the consumer level, as well as by foreign visitors, business, industry and government. 17 www.cfra.ca/research/research_foodserviceharerises.htm 18 Davis, David; Stewart, Hayden, “Changing Consumer Demands Create Opportunities for U.S. Food System”, Economic Research Service, USDA, FoodReview, Spring 2002. 19 www.agr.gco.ca/food/consumer/mrkreports/consumers_e.html 20 www.crfa.ca/research/research_institutionalgrowth.htm

Foodservice Opportunities – Beef, Pork, Bison, Lamb

Saskatchewan Agriculture Food and Rural Revitalization 10

In Canada, the education market is currently valued at CDN$361M (2001 figure) and projected to be CDN$387M in 2002. This figure includes private schools, high schools, colleges and universities with the majority accredited to the latter segments.21 In other words, the education market represents less than 1% of the total foodservice industry. And in 2000, foodservice sales at U.S. colleges and universities accounted for US$10.8B (or CDN$16.9B). Educational consumers are seen to be a “captive market”. Due to increasing competition for students, the institutions recognize that having efficient, high-quality foodservice options are a necessity. Many educational institutions have recently privatized foodservice or contracted them out. In order to capture a larger share of the students’ food dollars, including those who live off campus, the operators are offering more of a varied menu such as adding more nutritious meals (e.g. more fruits, vegetables and vegetarian meals).22 4.3 Market Drivers Most articles agreed that economic growth is the primary determinant of consumer expenditures on away-from-home foods23. And the two major economic variables that drive the commercial foodservice industry are the Gross Domestic Product (GDP) and Disposable Income (DI). To put this in perspective, the CRFA calculates that a one percent increase in DI results in a 1.1% increase in commercial foodservice sales.24 In addition, the stronger showing of the Canadian economy in recent months has led to a decision by CRFA to increase its forecast for the industry for 2002 as outlined in the previous section. Other factors that were identified as currently driving the commercial foodservice industry are:

• The maturity of the retail market: The retail market for food (e.g. supermarkets, convenience stores, etc.) is considered to be mature and growing at a rate that is only a fifth of the rate of growth of the foodservice sector. Since it is becoming more and more difficult to secure significant margins out of the retail market, large food companies are turning to the foodservice industry in order to maximize value for the companies.25

21 LBC Consulting Services, “Canada HRI Food Service Sector, An Overview of the Institutional Foodservice Market in Canada 2002, Foreign Agricultural Service/USDA. 22 “The United Sates Foodservice Market (FaxLink no. 34119)”, The Team Canada Market Research Centre, August 2000. 23 Davis, David; Stewart, Hayden, “Changing Consumer Demands Create Opportunities for U.S. Food System”, Economic Research Service, USDA, FoodReview, Spring 2002. 24 Gain Report #CA0047, Foreign Agricultural Service, USDA. 25 Woodcock, B., USA Food Export, Inc., “Canada HRI Food Service Sector – Hotel, Restaurant, Institutional Sector Report – Western Canada, 2000”, Foreign Agricultural Service/USDA, August 2000.

Foodservice Opportunities – Beef, Pork, Bison, Lamb

Saskatchewan Agriculture Food and Rural Revitalization 11

• Knowledgeable and demanding consumers: Consumers are more knowledgeable than in the past and are demanding; 26

Variety; Quality and freshness (and willing to pay for it); Convenience due to time pressures; Health and nutrition (particularly the aging baby boomers); Environmental sensitivity (with the primary drivers, the

youth); Safe food as a result of heightened media attention; and Access to information.

In addition, increasing consolidation within the foodservice sector and an increasingly competitive climate means consumers will continue to drive the market.27

• Smaller households: Smaller households are driving North

Americans to eat away from home on more occasions. The studies indicate that the smaller households eat out more often because of economies. For example, the time spent preparing food per family member and the cost of the meal, increases as the size of the family decreases.28 Therefore as households decrease in size, consumers eat out more often.

• Proximity to restaurants and quick service: Lunchtime represents

an important segment of the foodservice industry. For the luncheon segment, the main drivers are proximity to the restaurant and how long it takes to get in and out of the restaurant. “After than comes value. Quality is the expectation and it is imperative”.29

In summary, there appears to be support for the premise that the commercial foodservice industry will soon secure more of the consumers’ food dollar due to the following drivers/factors:

1. Continued economic growth, particularly increases in per capita income;

2. The shift to smaller households; and 3. Increasing numbers of empty nesters and single person

households.

Note however that income growth may result in increases in the per capita quantities of some food items consumed. For example, the USDA predicts that higher incomes will likely lower consumption of pork (down 3%), beef (down 2.8% - if the same decrease occurs in Canada, results in a decrease in beef sales to commercial foodservices of $72.8M) and other meat and eggs, and it will result in an increase in consumption of fruits, vegetables, cheese, yogurt and fish.

26 www.agr.gco.ca/food/consumer/mrkreports/consumers_e.html 27 http://just-food/features_detail.asp?art=452 28 Davis, David; Stewart, Hayden, “Changing Consumer Demands Create Opportunities for U.S. Food System”, Economic Research Service, USDA, FoodReview, Spring 2002. 29 www.rimag.com/1402/Food.htm

Foodservice Opportunities – Beef, Pork, Bison, Lamb

Saskatchewan Agriculture Food and Rural Revitalization 12

4.4 Trends In addition to the current drivers, trends were also identified as having an influence of the growth of the foodservice industry. They include:

• The changing life situation in households: In the short term, the largest growth market will be the 50-64 year old age-group which by 2011 will be 40% larger than it is today. (U.S. figures note that 32% of Americans 55 and older currently dine out three times a week or more.30) There is a growing body of research that finds that food and beverage choices are more determined by the presence or absence of children in the home and whether or not a couple is retired. Once children have left home, the tight food budget is no longer as important. As well, this group is tired of years of meal preparation and prefers to eat out more often. In other words, eating patterns appear to be more dictated by life situation rather than age. So, while older consumers may have more time to prepare meals, they actually eat out more before and after retirement. This group is known as the WOOFs (Well off Older Folks). 31

Life situation not only affects households where children have grown and left home, but also the growing number of single adults or couples who opt out or delay parenthood. This group is also a high frequenter of commercial foodservice operations.

• Growth of dual income households: Two income-earner

households mean more income (increased affluence) resulting in: Consumer demand for convenience; 32 Consumers increasingly opting out of household tasks such as

meal preparation and eating away from home; A greater emphasis being placed on leisure activities in which

dining away from home plays an important part; and Increased foreign travel, broadening consumer tastes for a

greater variety of global cuisine. 33

The increased affluence has not only affected the wage earners, it has also affected their children. In the 15-24 year old age group, approximately 40% eat their main meal out of the home three or more times a week. “Our customers of tomorrow are growing into adulthood by cultivating the habit of eating away from home”. 34

• Increasing concerns about nutrition: Nutrition becomes increasingly

important as people age. Mature adults are as receptive to new foods as their children. As consumers age however, they are more

30 Gain Report #CA0047, Foreign Agricultural Service, USDA. 31 www.foodincanada.com/index.cgi?pcode-0122FCEF7C6681786128B916CD7CE968 32 Davis, David; Stewart, Hayden, “Changing Consumer Demands Create Opportunities for U.S. Food System”, Economic Research Service, USDA, FoodReview, Spring 2002. 33 http://just-food/features_detail.asp?art=452 34 www.meatingplace.com/meatingplace/Archives/oop/qnohit_g.asp.ID=5364

Foodservice Opportunities – Beef, Pork, Bison, Lamb

Saskatchewan Agriculture Food and Rural Revitalization 13

interested in nutritious foods that will assist them to maintain their health longer. 35 Many restaurants and even fast food chains have addressed this trend by offering lighter or heart healthy menu offerings.

In addition, as adults mature/grow older, they tend to eat less. Projections are that this will result in downward demand pressure on per capita quantities of beef and poultry.36 The older population is not the only group who are eating healthier. The American Dietetic Association states that 38% of Americans are actually eating more healthy, a significant increase from 28% in 1999.37

• The changing face of the Canadian (North American) population:

The growth of the Canadian population is slow (expected to be 1.2% annually over the next decade). It is expected that in order to make up for the slow growth, immigration will increase. This will likely occur in the U.S. as well. And in order to address the tastes of the new population, restaurants that meet the demands of the new population make-up will be in demand. 38

It should also be noted however that minority groups are not as inclined to dine out as the majority of the population in North America. 39

• Growth in demand for personal chefs: Personal chefs are a growing

trend in North America. The chefs interview family members concerning meal preferences and then shop for, make meals and stock them in the client’s fridge/freezer. The U.S. Personal Chef Association states that if people eat out at least three times a week they can afford the services of a personal chef and are likely to realize savings using their services rather than eating in restaurants. Currently, there are personal chefs in nearly every city in the U.S. with a population of more than 50,000 people. In fact, “there are about 6,000 in the U.S. with some 80-100 new people getting into the business every month”. The client groups are predominantly:

Working professionals; People with special diets (weight-loss diets, weight-gain diet

or doctor imposed diet); Seniors seeking a healthy meal that tastes good; Widow or widower who does not feel like cooking for him or

herself.40

35 http://just-food/features_detail.asp?art=452 36 Blisard, Noel; Lin, Biing-Hwan; Cromartie, John; Ballenger, Nicole; “America’s Changing Appetite: Food Consumption and Spending to 2020”, Economic Research Service, USDA, FoodReview, Vol. 25, Issue 1. 37 Functional Foodwire, August 19, 2002. 38 www.agr.gov.ca/food/consumer/mrkreports/consumers_e.html 39 Davis, David; Stewart, Hayden, “Changing Consumer Demands Create Opportunities for U.S. Food System”, Economic Research Service, USDA, FoodReview, Spring 2002. 40 Anderson, Mark, “Dinner is Served”, Sacramento Business Journal, August 8, 2002.

Foodservice Opportunities – Beef, Pork, Bison, Lamb

Saskatchewan Agriculture Food and Rural Revitalization 14

• Branding and multi-branding at commercial foodservice outlets: This growing trend in foodservice is two-fold. Not only are products that are recognizable to consumers offered on the menu (e.g. Maverick Natural Beef, or Neilson’s ice cream products) but also food companies producing private label products for the foodservice industry. 41

• Supermarkets expanding into commercial foodservice outlets:

The U.S. is realizing a growing trend towards grocery stores adding a full-service fine dining restaurant (e.g. Tastings Restaurant a 114 seat fine dining restaurant attached to Wegman’s Food Market in Rochester, N.Y.) The concept is that products including alcoholic beverages offered on the menu are available in the grocery store and can be purchased prior to the customer leaving the building. 42

• “Going up – as in upscale”: Restaurant chains are moving

towards offering a higher quality dining experience. While new menu items are sourced in researching the most popular food trends, these chains are also offering old menu favourites which are considered “the comfort zone of loyal customers”. The concept is considered to be risk taking but the goal is to increase traffic into their locations.43 Even MacDonald’s has attempted to attract new customers with their more up-scale menu offerings of healthier meals.

• Food as entertainment: Since the market is highly competitive,

distinguishing features are added in order to attract market share. For example, at Chi-Chi’s, a Louisville, Kentucky chain, fajitas now get a splash of tequila and are flamed tableside. The chain has added this feature specifically to tap into this trend.44

• Focus on quality, rather than quantity: Quality describes the

demand for a wide array of food characteristics such as taste, nutritional content, safety and convenience. Consumers are turning away from the huge super-sized meals of the past at restaurants and turning to quality.45

• More natural and organic products on the menu: The

foodservice industry appears to be increasingly interested in offering natural and organic products, particularly in meat and poultry. (Note: The challenge is that natural and organic brokers are not foodservice oriented. It [the foodservice industry] is a “whole different sales game than the specialty retail market”. In

41 http://just-food/features_detail.asp?art=452 42 www.democratandchronicle.com/biznews/forprint/0810story5_business.shtml 43 Yee, Laura, “Stepping Up”, R&I, July 15, 2002. 44 http://www.rimag.com/1402/Food.htm 45 Blisard, Noel; Lin, Biing-Hwan; Cromartie, John; Ballenger, Nicole; “America’s Changing Appetite: Food Consumption and Spending to 2020”, Economic Research Service, USDA, FoodReview, Vol. 25, Issue 1.

Foodservice Opportunities – Beef, Pork, Bison, Lamb

Saskatchewan Agriculture Food and Rural Revitalization 15

other words, the foodservice industry demands a much higher level of service than retail as well as being more price sensitive.)46

Interestingly, the combined result of many of the trends is that there is a growing percentage of the population who have either not developed or have lost their cooking skills.47 In addition, it should also be noted that the current downturn in the economy has affected some trends. For example, according to the USDA for example, many retirees are currently considered time rich but cash poor due to the reduction in income from the low interest received (if any) from their savings and investments. This group is now looking for value and bargains. It is unclear as to whether this current situation will turn into a trend in the future and will therefore have an on-going effect on the foodservice industry.

4.5 Consumers The consumers of Canada and the U.S. are generally wealthier, older, more educated, and more ethnically diverse than in the past. While the population cannot be viewed as a homogenous group, the following description typifies the household that spends the most money on commercial foodservice outlets: 48

• Household income is $70,000 or more; • Age of the head of the household is between 45-54; and • The oldest child is 18 or older.

While the above description fits the households with the highest overall spending on foodservice, other consumer groups represent a strong segment of the market. For example, households headed by a person under age 25 spends a higher percentage of their food dollar on food away from home but their total spending is lower. As well, households consisting of only a husband and wife have the highest average per capita expenditure on food away from home.49 Consumers are looking for an experience that addresses one or a combination of convenience, quality (tasty, good value, safe food) and service. Depending on the consumer’s situation, they may want quick service that will send them on their way to the soccer game. Others prefer a dining experience. For example, seniors’ eating patterns run contrary to eating on the run trend. They are more likely to perceive mealtime as traditional and wish an enjoyable, social event rather than quick replenishment prior to

46 Lipson, Elaine, “The Foodservice Frontier”, The Natural Foods Merchandiser, March 1999. 47 http://just-food/features_detail.asp?art=452 48 National Restaurant Association, “Restaurant Spending”, 2000. 49 www.restaurant.org/research/spending.cfm

Foodservice Opportunities – Beef, Pork, Bison, Lamb

Saskatchewan Agriculture Food and Rural Revitalization 16

running off to the next event. This segment wants good service and to be served with respect.50 There is a growing number of references in the publications questioning past perceptions of the “wealthy gray market”. The older baby boomers have been referred to as the affluent, with significant disposable income, thus having the ability to buy what they want when they want. With the downturn in the economy, government spending tightening, and a growing number of people living longer, many futurists are re-examining the impact of the trend. “Facing an extended old age with disappointing holes in savings and pensions, many consumers must cope on a low income”. 51 In other words, the segment comprised of older consumers with high disposable income may be much smaller than predicted. The impact to the foodservice industry is that this group, while still wanting a social event, will likely decrease the number of eating away-from-home occasions and spend more time cooking and entertaining at home. According to Statistics Canada, the average Canadian household spent CDN$1,536 on food and alcohol in commercial foodservice outlets in 2001. Figures from the U.S. indicate a much higher level of household spending of U.S. $2,137 (or CDN$3,333.72) in these outlets.52 Closer to home, Western Canadians tend to spend more on “away from home” eating than their counterparts in the other areas of the country. British Columbia in fact has Canada’s highest per capita foodservice spending at 1.31 (restaurant/population development index).53 While consumers have a wealth of venues from which to eat, when dining out they are more likely to do so at table service or fast-food outlets rather than in cafeterias.54 And while the evening meal still represents the meal most often served at foodservice outlets, the fastest growing meal occasion is breakfast. In two years, the share of restaurant traffic for breakfast and/or morning snacks has increased from 16.1% to 17.1% while lunch and supper have in fact fallen.55 4.6 Products Food is only one of the categories of goods sold in the foodservice industry representing 32% of sales as opposed to over 90% of the cost of sales in the retail grocery sector.56

50 www.crfa.ca/research/foodservicetrends/research_foodservicetrends_servingseniors.htm 51 http://just-food.com/features_detail.asp?art=661&app=1&fotw.sct 52 www.restaurant.org/research/spending.cfm 53 Source: Statistics Canada 54 www.agr.gco.ca/food/consumer/mrkreports/consumers_e.html 55 www.crfa.ca/research/foodservicetrends/research_foodservicetrends_consumerbreakfast.html 56 Source: Canadian Restaurant and Foodservice Association.

Foodservice Opportunities – Beef, Pork, Bison, Lamb

Saskatchewan Agriculture Food and Rural Revitalization 17

Restaurants aim to offer variety in their menus and are increasingly offering new foods in order to attract new customers. The trick for the outlets is to continue offering a core set of products that will keep their old customers coming to the restaurant while offering new products and menu items that attract new diners. However, the new products need to be significantly different so that they will not cannibalize existing options.57 As well as new product offerings that provide a “solution” for the foodservice industry, many food companies use restaurants to launch and experiment with new product ideas. The food companies see this market as a ready test market for consumers’ constantly changing tastes and one that provides quick feedback prior to introduction at the retail level. 58 Even though restaurants aim to offer new products, the “old standbys” seem to be entrenched in the hearts of the consumers. The following table outlines the top food items purchased at foodservice outlets in Canada.

Table Four: Top Ten Foods & Beverages at Canadian Foodservice Outlets - 2001

Food Category Share of Occasions

French Fries 22% Hamburgers 11% Unsweetened Baked Goods 11% Salads 11% Chicken 11% Pizza 10% Sandwiches 10% Sweetened Baked Goods 7% Desserts 6% Ice Cream/Frozen Yogurt 5%

Source: Canadian Restaurant and Foodservice Association While a growing number of seniors enjoy trying new foods, the major target market for familiar foods is usually the senior. This group often avoids experimenting if faced with digestive or health problems. The Canadian Restaurant and Foodservice Association has noted that this group is more likely to want dishes they grew up with and have meat as the major feature of the meal. 59 Restaurants have accommodated the older market segment in order to “provide a point-of-difference” for their outlet by updating recipes or “adding a twist” to it such as new spices. This is done for three reasons as the restaurants aim to: 60

1. Attract the seniors with familiar food but in a manner that they would not make at home;

57 Yee, Laura, “Stepping Up”, R&I, July 15, 2002. 58 www.foodincanada.com/index.cgi? 59 www.crfa.ca/research/foodservicetrends/research_foodservicetrends_servingseniors.htm 60 Ibid.

Foodservice Opportunities – Beef, Pork, Bison, Lamb

Saskatchewan Agriculture Food and Rural Revitalization 18

2. Offer traditional menu items that have been made “healthier” (a critical criteria for many seniors); and

3. Increase taste intensity (sense of taste decreases with age). As well, chefs are looking for ideas that are driven by seasonality, ethnic flavours and the popularity of comfort food.61 Most of the fine dining segment employ chefs. This group is particular and often works on “creative urges”. Chefs direct their sous-chefs to create (or will create themselves) a dish with only certain ingredients in mind.62 In other words, they wish to use ingredients where they will add the value. The rest of the industry usually employ “cooks”, people who follow specific recipes and produce the same item exactly the same each time. This group may be more inclined or required to use value added products that provide the consistency from meal to meal. Except for the very high fine dining restaurants, the publications indicated that the foodservice industry (with less of an emphasis on the fine dining operations) is looking for:

1. Pre cut meat that is exactly the same size and weight so that cooks know exactly how long to cook the portion.63 Processors will need to be cognisant therefore of the need to cut and portion each piece of meat exactly the same.

2. Food product solutions such as partially baked foods (cold plated/ready-to-heat and serve) that are easy to store, require limited heating before serving. These products save time by reducing the labour (and therefore labour costs) required to make the products from scratch.64

While food processors receive better returns at the retail level than in foodservice, most also produce for the HRI trade. A representative of Unilver Bestfoods noted it is critical to be in the foodservice channel or forego dollars spent on food purchased away from home. “We’d be shooting ourselves in the foot if we weren’t in foodservice”.65 An example of the importance of foodservice to the food industry is the emphasis that the transnational food company Nestle places on foodservice. Nestle Foodservice introduced a comprehensive program called NIMS (Nestle Integrated Menu System). It is a selection of more than 125 fully prepared frozen meal components.

61 www.rimag.com/1402/Food/htm 62 Harvard Business Review, “Management By Fire”, July 2002, p.60. 63 Yee, Laura, “Stepping Up”, R&I Magazine, July 15, 2002. 64 Woodcock, B., USA Food Export, Inc., “Canada HRI Food Service Sector – Hotel, Restaurant, Institutional Sector Report – Western Canada, 2000”, Foreign Agricultural Service/USDA, August 2000. 65 Burn, Doug, “Carving Up the Pie”, Food in Canada, May 2002.

Foodservice Opportunities – Beef, Pork, Bison, Lamb

Saskatchewan Agriculture Food and Rural Revitalization 19

To illustrate the growing importance of the foodservice industry to the major food companies, three of Nestle Canada’s eight manufacturing plants are now dedicated exclusively to making products for the foodservice industry. 66 A key strategy for both the food processing and foodservice industries to pursue is constant experimentation with new food concepts to address changing consumer tastes.67 Other food companies are also preparing products targeted at the foodservice industry. California based Fernando’s Foods Corp. has developed Southwestern and Latin American entrees, signature dishes and appetizers for foodservice menus. The products are specially seasoned and prepared and are individually quick-frozen and heat-sealed in portion-controlled bags. Red meat offerings include grilled steak strips, “shredded mexicana, and carnitas” (pulled pork). FoodMasters Inc., a Missouri based company has introduced “Country Creations Natural Slab of Pre-Cooked Boneless Loin Back Ribs with Savory BBQ Sauce” for the food service industry. 68 In addition, many value added meat products are designed solely for the foodservice industry. One article noted that most pre-marinated, pre-seasoned steaks are processed for the family style restaurant chains who “need signature, value-added steaks on their menus to create points of difference that are more affordable and unique (different flavour profiles)”. Many of the food companies are working with spice companies to develop unique flavour profiles for meat products.69 Marinated brands specifically developed for the foodservice industry are also becoming available at the retail level. Tyson Prepared Foods/IBP for example sells its brands, Black Diamond and Black Gold, a line of pre-seasoned frozen steaks, to both the foodservice industry and club stores. 70 Branding of products by the large distributors is also gaining strength. Consumers however have been turning to other sources of protein over the years. The following table indicates that per capita consumption of chicken has taken away market share from the beef industry. Pork on the other hand has remained fairly stable.

66 www.foodincanada.com/index.cgi? 67 Ibid. 68 www.meatingplace.com/meatingplace/Archives/oop/qfullhit_m.htw? 69 Salvage, Bryan, “Pre-Seasoned Steaks: A Product for the Times”, Meat Marketing & Technology, March 2002. 70 Ibid.

Foodservice Opportunities – Beef, Pork, Bison, Lamb

Saskatchewan Agriculture Food and Rural Revitalization 20

Table Five: The U.S. Average Annual Per Capita Consumption In Pounds of Beef, Chicken and Pork

0102030405060708090

1980

1984

1988

1992

1996

2000

BeefChickenPork

Source: USDA

It appears that any growth in beef would need to come from population growth. The following sections provide an overview of information specific to each product category. Beef Within the red meat food group, consumers with a higher disposable income often choose beef steak as their menu item. While steak is usually the highest price point on the menu there appears to be an increasing demand for quality over quantity of steak in restaurants. Restaurants often see a really unique, signature steak as their competitive advantage. The “au jus flavor” is the most requested steak flavor. 71 While overall population growth in North America results in a projection of a 15% increased consumption in beef by 2020, the per capita beef consumption in fact is expected to drop as identified above. The USDA attributes the projected decrease to an aging population, an increasingly educated population (which heightens awareness of the health risks of excess saturated fat) and income growth (indicates a shift towards poultry and fish). The expectation is future consumers of red meat (not just beef) will demand a higher quality, more expensive product. 72 71 Salvage, Bryan, “Pre-Seasoned Steaks: A Product for the Times”, Meat Marketing & Technology, March 2002. 72 Blisard, Noel; Lin, Biing-Hwan; Cromartie, John; Ballenger, Nicole; “America’s Changing Appetite: Food Consumption and Spending to 2020”, Economic Research Service, USDA, FoodReview, Vol. 25, Issue 1.

Foodservice Opportunities – Beef, Pork, Bison, Lamb

Saskatchewan Agriculture Food and Rural Revitalization 21

Bison Bison has had some difficulties getting onto the menu. Its higher price and its “exotic” image have been barriers to increased consumption.73 As well, it has been difficult to translate the message of the health benefits (high protein, lean meat) into sales.74 It appears however that bison meat is “making a comeback as an alternative to beef”.75 Previously it was known as being “dry, overdone, chewy hockey puck…served in a tourist trap”. The industry is working hard to overcome that reputation.76 The Canadian Bison Marketing Council appears to be promoting bison as a “healthy and safe meat” with the following attributes: 77

• “Bison is leaner than beef, chicken or pork and has about 30% more protein than beef”;

• It is “grassfed and the use of antibiotics and hormones is avoided”; and

• Programs have been developed that “include implementing industry standards that provide consistent product and food safety with its ‘On Farm Food Safety Plan’”.

Bison is also being promoted to those who wish to eat kosher foods. Bison is now being featured on the menus of many kosher restaurants across the country. Kosherbison.com offers burgers, roasts, steaks, ribs and deli meats from bison meat.78 Note that “kosherbison.com is available in the U.S. only. The main issue however noted in the publications is that bison lacks market penetration and that there may be too much production given the size of the market. Any market growth has been achieved through sales to the white tablecloth restaurants (account for about one third of the all sales). Of the 660,000 pounds of dressed meat produced last year for the market (valued at CDN$40M and representing one quarter of the North America production), about 90% was exported to the U.S. where consumption is higher. In parts of the U.S., such as Colorado (population 4.4 million), the per capita consumption is 6 pounds of bison per year while the average per capita consumption in Canada is .45 pounds.79 The biggest challenge to increasing the market for bison however may be the differing names used causing confusion. The U.S. restaurants usually use the term buffalo while Canadians use bison or buffalo. In reference to the term

73 www.web5.infotrac.galegroup.com 74 http://just-food.com/features_detail.asp?art=660&app+1&fotw=sct 75 www.web5.infotrac.galegroup.com 76http://just-food.com/features_detail.asp?art=660&app+1&fotw=sct 77 Ibid. 78 www.meatingplace.com/meatingplace/Archives/oop/qnohit_g.asp?ID=6533 79 http://just-food.com/features_detail.asp?art=660&app+1&fotw=sct

Foodservice Opportunities – Beef, Pork, Bison, Lamb

Saskatchewan Agriculture Food and Rural Revitalization 22

buffalo, water buffalo is enjoying a small but growing market in North America. In the U.S. specialty meat market the concern is that there will be consumer confusion.80 Pork While beef has realized a decrease in per capita consumption since 1970, per capita pork consumption has remained relatively flat at about 50 pounds per year (U.S. figures).81 Rather than discuss pork in general, articles mainly focused on value-added pork products. New flavours and ready-to-serve items are being developed for foodservice such as:

• SiouxPreme Packing Company that offers 50 different pork products targeting restaurants;

• Swift’s ready-to-cook pork product “offering 10 different flavours”; and • Godshall’s Smoked Pork products.

Since breakfast is the meal occasion that appears to be growing the fastest, pork may be a product to watch to see if an increased demand for bacon and sausages is evident. Lamb Due to the strong U.S. dollar and the lack of quotas on lamb imports into the U.S., the Australian and New Zealand producers have taken the upper hand in the U.S. Meatingplace.com points out that “if you can find lamb, it likely isn’t North American”. 82 Lamb does not seem to enjoy the consumer acceptance of either beef or pork at the foodservice or retail sectors. The lack of product promotion has left most consumers thinking of lamb primarily as an entrée at holiday meals or at white tablecloth restaurants. There may be an increase in the demand for lamb in the future. The USDA is currently in the process of approving a check-off that would result in an annual US$3.5M marketing campaign to increase sales. In addition, new pre-cooked products are being tested on the market in response to consumer confusion as to cooking methods. 83 80 Ibid. 81 www.meatingplace.com 82 www.meatingplace.com/meatingplace/Archives/oop/qnohit_g.asp?ID=8981 83 Ibid.

Foodservice Opportunities – Beef, Pork, Bison, Lamb

Saskatchewan Agriculture Food and Rural Revitalization 23

As it relates to products in general, a recent USDA report describing the HRI trade in Canada stated that there is a “foodservice predisposition to buy Canadian first”.84 Therefore home-grown products may in this instance have a competitive advantage over their American competition. However countries that can supply products that meet Canadian foodservice quality standards and are lower priced will still likely have the advantage in this market segment. 4.7 Price Price was not discussed extensively in the publications. Most references were to bison where its 20-50% price premium is perceived as being too high for the average Canadian consumer.85 4.8 Promotion If the commercial foodservice industry is viewed on a continuum with the white table cloth restaurant being at one end and the take-out and delivery outlets at the other end, the closer to the takeout and delivery, the higher the use of promotional activities directly to consumers to grow sales, particularly with the chains.86 The following table illustrates the intensity of the promotion activities by segment.

Table Six: Promotional Activities

Increases Promotional Decreases Activity

Take-out & / Unlicensed Licensed Delivers / (Family Dining) (White Table-Cloth) The internet is also used as a promotional tool for restaurants. However, many small independent restaurants do not appear to use this form of advertising. The internet is also used to promote specific forms of non traditional meat products at restaurants. For example, restaurants offering organic meat (e.g. www.allorganiclinks.com/restaurants, www.berettafarms.com, www.organicbreadbasket.com/profiles.htm, http://santacruz.about.com/library/blcuisine4.htm) and bison meat (e.g.

84 Woodcock, B, USA Food Export, Inc., “Canada HRI Food Service Sector – Hotel, Restaurant, Institutional Sector Report, Western Canada, 2000”, Foreign Agricultural Service, USDA, August 2000. 85 http://just-food.com/features_detail.asp?art=660&app+1&fotw=sct 86 http://just-food/features_detail.asp?art=452

Foodservice Opportunities – Beef, Pork, Bison, Lamb

Saskatchewan Agriculture Food and Rural Revitalization 24

www.albertabuffalo.com) are featured on either producer or industry websites. This channel is targeted directly at consumers. Promotional activities are also conducted by commodity groups and targeted at restaurants themselves. This is particularly true of the white table-cloth outlets where chefs often do the ordering. For example, new beef menu ideas were offered at a chef education seminar conducted at a leading culinary school to key menu decision-makers in the restaurant and related industries. The second annual “Beef, It’s What’s on the Menu” seminar was held at the Culinary Institute of America Greystone Campus in St. Helena, California and funded by the National Cattlemen’s Beef Association (NCBA). The Association sponsored the program in order to “allow us opportunities to reach those individuals who decide what goes on the menus in America’s restaurants, and to increase beef’s presence on those menus”.87 This example may represent an opportunity for Saskatchewan producers and processors to promote and test their products with the foodservice industry. 4.9 Competition The publications identified specific examples of restaurants or chains that have achieved some success in the marketplace and the reason for the success. The ones to which reference was made are in the U.S. and are:

• The Outback Steakhouse: This casual dining chain was identified as “one of the most successful chains in the country …with its commitment to service and passion for creating serious food ”.88 As well, the article noted the strategic alliance that the company has built with its meat suppliers, IBP Inc., and Excel. Another feature of the Outback Steakhouse is that it introduced the “Curbside Take-Away Program” where servers take dinners to their customers who wait in their cars.

• Ruth’s Chris Steak House: This fine dining chain is located in

Louisiana and is “one of the most successful in the world”. Its commitment to quality control where steaks are monitored from all suppliers has been the major contributing factor to its success. While the company did meat cutting in-house at each site, it is now turning to pre-cut and pre-seasoned steaks for all cuts, done at a central cutting house.89

• Morton’s of Chicago: This internationally known restaurant built its

reputation on top quality service and the “best prime steaks in town”.90 .

• T.G.I. Friday’s: This growing full-service chain bases its offerings on the consumer demand for convenience as well as demand for dining amenities and a diverse menu offering.91

87 www.beef.org/dsp/dsp_content.cfm?locationID=45&contentID=319&contentTypeID=2 88 www.meatingplace.com 89 Ibid. 90 Ibid.

Foodservice Opportunities – Beef, Pork, Bison, Lamb

Saskatchewan Agriculture Food and Rural Revitalization 25

• Ted’s Montana Grills: Media mogul Ted Turner is growing a chain of

burger restaurants that use bison meat from his own ranches (a good example of vertical integration). The chain features freshly cooked bison burgers and chili.92

The growing competition is actually coming from retail grocery outlets. Retailers are trying to stem the flow of customers and their food dollars to the foodservice industry by offering home meal replacements and deli sections. And in some instances, these retailers are developing restaurants as a complementary service at the grocery store.93 Closer to home, competition abounds. Appendix B provides lists of restaurants in Saskatchewan and Alberta sourced on the internet. In addition, chains, both foodservice and hotels, provide competition. The major chains that have operations in Western Canada and their affiliations in the foodservice industry were identified and are outlined in the following table:

91 Davis, David; Stewart, Hayden, “Changing Consumer Demands Create Opportunities for U.S. Food System”, Economic Research Service, USDA, FoodReview, Spring 2002. 92 www.web5.infotrac.galegroup.com 93 Davis, David; Stewart, Hayden, “Changing Consumer Demands Create Opportunities for U.S. Food System”, Economic Research Service, USDA, FoodReview, Spring 2002.

Foodservice Opportunities – Beef, Pork, Bison, Lamb

Saskatchewan Agriculture Food and Rural Revitalization 26

Table Seven: Chains in Western Canada With Foodservice Outlets CHAIN AFFILIATE HEAD OFFICE

Four Seasons Hotels & Resorts

Don Mills, Ontario

McDonald’s Restaurants of Canada

Toronto, Ontario

#TDL Group Ltd. Subsidiary of Wendy’s International; Licenses Tim Hortons.

Oakville, Ontario

Cara Operations Ltd. Harvey’s; Swiss Chalet; Summit Food Distributors; Beaver Foods and Airport Services.

Mississauga, Ontario

Canadian Pacific Hotels Delta Hotels Fairmont Hotels.

Toronto, Ontario

Tricon Global Restaurants (Canada Inc.)

KFC; Pizza Hut; Taco Bell.

Rexdale, Ontario

Starwood Hotels & Resorts Worldwide Inc.

Sheraton Hotels; Westin Hotels & Resorts; Four Points Hotels

Toronto, Ontario

Best Western International, Inc.

Phoenix, Arizona

Subway Franchise Systems of Canada, Ltd.

Milford, Connecticut

Choice Hotels Canada Inc. Clarion Hotels; Quality Hotels; Comfort Hotels; Economy Lodge; Rodeway Inns.

Mississauga, Ontario

Burger King Restaurants of Canada Inc.

Etobickoke, Ontario

A&W Food Services of Canada Inc.

Vancouver, British Columbia

Bass Hotels & Resorts Holiday Inn Express. Atlanta, Georgia Royal Host Travelodge Canada;

Thriftlodge. Calgary, Alberta

The Second Cup Ltd. Toronto, Ontario UniHost Corporation Journey’s End;

Holiday Inn; Comfort Inn.

Mississauga, Ontario

Keg Restaurants Group Inc., Richmond, British Columbia Boston Pizza International Inc.

Richmond, British Columbia

Kelsey’s International Inc. Kelsey’s; Montana’s Cookhouse Saloon; Outback Steakhouse.

Oakville, Ontario

Mr. Sub Toronto, Ontario Northland Properties Ltd. Sandman Hotels and Inns;

Denny’s Restaurants; Moxie’s Restaurants.

Vancouver, British Columbia

#SIR Corp. Armadillo steakhouse; Papa Leoni’s; Canyon Creek; Alic Fazooli’s Italian Crabshack;

Burlington, Ontario

Foodservice Opportunities – Beef, Pork, Bison, Lamb

Saskatchewan Agriculture Food and Rural Revitalization 27

Al Frisco’s; Far Niente; Jack Astor’s.

Darden Restaurants Red Lobster; Olive Garden

Mississauga, Ontario

Coma Food Group Inc. Company’s Coming Bakery Café; Grabbajabba Gourmet Coffee Stores; Pastel’s Restaurants.

Calgary, Alberta

Coast Hotels Limited Vancouver, British Columbia White Spot Restaurants Triple O’s Vancouver, British Columbia Smitty’s Canada Ltd. Calgary, Alberta Arby’s Canada Inc. TJ Cinnamon’s. Mississauga, Ontario The Spectra Group of Great Restaurants Inc.

Milestone’s; The Bread Garden; The Boathouse; Roman’s Macaroni Grill.

Vancouver, British Columbia

Hospitality Corp. of Manitoba Inc.

Windsor Park Inn; Garden City Inn; Express Fort Garry Inn; Transcona Inn; Fort Garry Inn.

Winnipeg, Manitoba

ABC Country Restaurants Inc.

Surrey, British Columbia

Humpty’s Restaurant International

Rockin’ Robin’s Diner. Calgary, Alberta

Red Robin Restaurants of Canada Ltd.

North Vancouver, British Columbia

Taco Time Canada Ltd. Calgary, Alberta Elephant & Castle Group Inc. Rosie’s and Alamo Bar &

Grill; Rainforest Café.

Vancouver, British Columbia

Donato Food Corporation Mrs. Vanelli’s; Made in Japan.

Mississauga, Ontario

#Joey’s Only Seafood Calgary, Alberta Edo Japan Calgary, Alberta Husky Oil Marketing Company Ltd.

Husky House Restaurants Calgary, Alberta

Source: USDA/Foreign Agricultural Service As noted above, many of the foodservice operations own/franchise several concepts (e.g. Red Lobster and Olive Garden). The rationale is the need for diversification in order to capture different markets.94 4.10 Distribution Within the distribution, chain three groups play a key role in linking the processors and the foodservice outlets:

1. Distributors; 2. Brokers; and 3. Buying groups.

94 www.meatingplace.com/meatingplace/Archives/oop/qfullhit_m.htw?

Foodservice Opportunities – Beef, Pork, Bison, Lamb

Saskatchewan Agriculture Food and Rural Revitalization 28

Most larger restaurants and chains are supplied by established agents/brokers/distributors. Smaller operations often purchase their requirements through large retail and wholesale outlets such as Costco or Walmart to maximize their individual buying efficiencies. 95 Distributors Distributors are the logistic link that warehouse and deliver food and beverage products to foodservice operators. The publications identified three types of distributors: 96

• Broadline distributors (also known as full service distributors): The broadline distributor purchases products from numerous processors, stocks the goods in a warehouse, and delivers the ordered products to the restaurants. It is the most comprehensive type of distributor and tends to serve single unit restaurants and small-scale chains. Examples of this type of distributor are SYSCO, Gordon Foods and Sunspun (a division of Westfair Foods).

• Specialty distributors (also known as niche distributors or

shortliners): As the name suggests, the specialty distributor deals with a narrow range of products only, such as meats or produce (e.g. Prairie Meats, Chef-Redi Meats).

• Systems distributors serve mostly chain restaurants that centralize