FOOD WHOLESALING IN THE UK - The National...

38

Page 1 of 38 FOOD AND DRINK WHOLESALING IN THE UK FOOD CHAIN ANALYSIS GROUP, DEFRA NOVEMBER 2008

Transcript of FOOD WHOLESALING IN THE UK - The National...

Page 1 of 38

FOOD AND DRINK WHOLESALING IN THE UK

FOOD CHAIN ANALYSIS GROUP, DEFRA

NOVEMBER 2008

Page 2 of 38

ONE PAGE SUMMARY

Food and drink wholesaling is an important segment of the UK food supply chain.

In 2006, the overall industry was worth £72.9bn, contributing 11% of the agri-food

contribution to GDP and employing 6% of its workforce.

Wholesalers link primary producers and manufacturers with small and large

retailers, foodservice outlets, and professional business users.

Wholesalers can be classified in terms of how they achieve this objective, who

they supply or what type of products they supply. The sector is very diverse.

At product level, there is a broad distinction between specialist and non-specialist

(or generalist) wholesalers. The latter tend to be larger scale and operate on

smaller margins.

In the past 10 years, definitions of wholesale operation have blurred. Substantial

consolidation (particularly in the non-specialist sub-sector), and changing

customer demands have lead to contrasting fortunes amongst specialist

wholesalers.

The customer base for wholesalers has shrunk as supermarkets have gained

market share forcing non-specialist wholesalers towards consolidation and

increasing the role of both buyer and symbol groups. The number of non-

specialist firms declined by around a third in the last ten years. In its latest

grocery market enquiry, the Competition Commission has considered the future

viability of the wholesale sector.

The environment in which wholesalers operate will continue to change. Important

factors are likely to be the outcome of the current competition investigation,

energy and producer price changes, increased food standards/ quality regulation

and most importantly, changing consumer preferences.

Page 3 of 38

CONTENTS

CONTENTS 3

1. INTRODUCTION 4

2. ECONOMIC SNAPSHOT 5

3. DEFINITIONS AND POSITION 8

4. MARKET STRUCTURE AND TRENDS 14

5. GENERAL GROCERY WHOLESALING: THE IGD PERSPECTIVE 19

6. COMPARING SUPERMARKET AND WHOLESALE SUPPLY CHAINS 29

7. CONCLUSION AND OUTLOOK 33

GLOSSARY 35

KEY SOURCES 36

LEADING UK WHOLESALERS 37

Page 4 of 38

1. INTRODUCTION

Food and drink wholesaling – selling goods in bulk quantities - plays a significant, varied

and sometimes overlooked role in Britain‟s food chain.1 This paper, produced by Defra‟s

Food Chain Economics team, describes key characteristics and trends within the food

and drink wholesaling sector in the UK. In particular, it:

gives an economic snapshot of the sector, relating to key variables such as

turnover, GVA, employment and productivity (section 2);

analyses the specific role of the sector and the different classifications of

wholesalers within it (section 3)

assesses key market characteristics and trends (section 4);

describes in more detail non-specialist wholesaling (section 5);

considers the increasing competition to its customer base and the general future

outlook for the sector (sections 6 and 7).

An annex provides brief company profiles of the top food wholesalers operating in the

UK. Readers may also wish to refer to our 2007 evidence paper on food service,

produced last year, given the degree of overlap between that sector and wholesaling.2

The paper draws heavily upon ONS‟s Annual Business Inquiry statistics (mostly

chapters 1 and 3) and IGD‟s wholesaling reports (chapter 4).3 These two sources define

the wholesale sector in different ways, reflecting its complex and evolving nature.

Underlined terms in the paper appear in the glossary, while references are cited in

footnotes with key documents listed in full at the end of the paper.

1 Note that this paper doesn‟t cover wholesaling within the agricultural sector.

2 Defra, Food service and eating out: an economic survey (January 2007),

http://statistics.defra.gov.uk/esg/reports/Food%20service%20paper%20Jan%202007.pdf

3 ONS data is analysed first as it gives a broad overview of the sector and allows consistent comparisons

with other areas of the food chain.

Page 5 of 38

2. ECONOMIC SNAPSHOT

2.1 According to the ONS, sales turnover in the wholesale of food, beverages and

tobacco was £72.9bn in 2006. Around 60% of this (£40.6 bn) is attributable to „specialist‟

wholesalers, and 40% (£29.0 bn) to „non-specialist‟ wholesale.

2.2 In 2006 the sector generated Gross Value Added (GVA) of £8.9 bn – around

11% of the total agri-food sector‟s contribution to UK GDP. This is larger than

agriculture‟s contribution but significantly less than the other downstream sectors, which

together comprise 80% of the food chain‟s total GVA of £79 bn (Figure 1). The ratio of

GVA to turnover (12%) is less than in other parts of the food industry. That reflects the

fact that wholesale activity, which largely revolves around consolidation and delivery,

does not typically add value to the goods themselves.

2.3 The food, beverage and tobacco wholesale sector employs around 206,000

people in over 14,000 enterprises (Table 1). Wholesaling is the smallest employer in

the food chain, accounting for only 6% of agri-food employment (Figure 1). But only one-

sixth of employees work part-time, compared with 60% of employees working part-time

in grocery retailing and one-tenth in food and drink manufacturing.

Figure 1 GVA and employment in the agri-food sector

0%

5%

10%

15%

20%

25%

30%

35%

40%

Agriculture Food and drink

manufacturing

Food and drink

wholesaling

Food and drink

retailing

Non-residential

catering

% o

f ag

ri-f

oo

d s

ecto

r to

tal

GVA Employment

Page 6 of 38

Table 1 Economic trends in Food, Drink and Tobacco wholesaling 1995 / 2000 - 2006

Sub-sector Turnover (£m) GVA (£m) Employees (000) Enterprises

1995 2006 Change 1995 2006 Change 1998 2006 Change 1995 2006 Change

Food, beverages & tobacco (total)

60,483 72,897 + 21% 5,341 8,908 +67% 223 206 -8% 15,829 14,142 -11%

Non-specialised wholesale of food, beverages & tobacco

19,058 29,324 +54% 1,270 2,951 +132% 81 83 +2 % 4,783 3,014 -37%

Fruit & vegetables 5,806 9,763 +68% 690 1,266 +83% 32 35 +9% 1,500 2,174 +45%

Meat & meat products 6,952 6,935 - 508 948 +87% 31 21 -32% 4,550 2,278 -49%

Dairy produce, eggs, & edible oils & fats

5,685 4,097 -28% 377 598 +59% 21 12 -43% 403 909 +126%

Alcohol & other beverages

9,372 11,182 +19% 1,744 1,508 -14% 29 26 -10% 2,665 2,882 +8%

Tobacco * 3,083 917 -70% 55 84 +53% 2 4 +100% 118 80 -32%

Chocolate & sugar confectionary *

2,498 4,031 +61% 120 316 +163% 3 4 +33% 397 470 +18%

Coffee, tea, cocoa & spices *

663 1,312 +98% 94 366 +289% 2 2 - 333 410 +23%

Fish, crustaceans & molluscs

3,549 5,335 +50% 386 944 +145% 19 19 - 1,559 1,925 +23%

* Shows figures and changes from 2000 to 2006 (not 1995). Red / green numbers indicate negative / positive growth Source: ABI (2007)

Source: ONS Labour Market Trends; Defra

Page 7 of 38

2.4 Labour productivity, measured by GVA per employee, has improved over the

years, as GVA has increased significantly whilst overall employment has fallen. (Table

1). Wholesaling Total Factor Productivity (TFP) – a more comprehensive indicator of

the efficiency of turning inputs into outputs – is estimated to have increased marginally

by an average of 0.12% per annum from 1998 to 2006. From 2005 to 2006 wholesaling

TFP increased by 3.4%, but there is no strong upward trend. The key driver of TFP is

how efficiently purchases are converted into sales: positive growth means that stock

control systems do not lead to wastage or delay, and that stock is aligned with customer

demand. Studies of US wholesaler and retailers suggest that greater and effective use of

IT is key to improving productivity performance (see below, para 4.6).4 The trends in

Table 1 are discussed further in para 4.6 below.

Figure 2 Total factor productivity across the food sector, 1998-2006

Source: Defra, Food Statistics Pocketbook, 2008(forthcoming)

4 Bloom, N., Sadun, R. & Van Reenen, J. (2005) „It ain‟t what you do it‟s the way that you do I.T. - testing

explanations of productivity growth using U.S. affiliates‟. Centre for Economic Performance, London School of Economics.

Page 8 of 38

3. DEFINITIONS AND POSITION

Background

3.1 Wholesaling is essentially an economic activity in which goods are sold in bulk

for resale. “Middlemen” have played a key role in food supply ever since Britain first

began to urbanise, in particular when the inland and coastal trade developed to supply

the expanding demands of early modern London.5 Basic wholesaling activity now

includes warehousing, transportation, product consolidation and inventory management

across the entire food supply chain.6 The advent of supermarkets has overcome the

dominance of traditional wholesaling, but the sector continues to play a significant and

varied role in food supply.

Position within the supply chain

3.2 Figure 3 offers a stylized view of the various routes to market. Wholesalers

connect producers and retail or foodservice customers outside the supermarket supply

chain (green arrows) and, logistically, perform a similar function to supermarket regional

distribution centres. Wholesalers give producers access to a large number of small

retailers and caterers, and in turn allow these outlets to access a wide range of products

from different suppliers, including imported goods. With their national distribution

networks, supermarkets generally by-pass wholesalers, as do parts of the foodservice

sector (orange arrows). However, some specialist wholesalers (e.g. importers of fresh

produce) will also supply supermarkets. For some small foodservice operators, it may be

cheaper to source some supplies, particularly smaller items, from supermarkets rather

than wholesalers (the purple arrow).

3.3 Contract distributors, unlike wholesalers, do not buy and sell goods, but simply

provide a specialist delivery service between different points of the supply chain (blue

arrows).7 They may act on behalf of individual producers or wholesalers. These

5 For a classic account of early developments in wholesaling, see R.B. Westerfield, Middlemen in English

business, particularly between 1660 and 1760 (1915; reprinted New York 1968). Also C. S. Smith, “The wholesale and retail markets of London, 1660-1840”, Economic History Review (Feb 2002), pp. 31-50.

6 IGD (2008)

7 IGD (2005) Understanding foodservice opportunities for farmers and small food producers.

http://www.defra.gov.uk/foodrin/foodname/foodservguide.pdf

Page 9 of 38

arrangements allow wholesalers to stock a limited range of products themselves, and to

provide drop-shipment schemes whereby certain perishable or temperature-controlled

goods (e.g. bread and milk) are delivered on behalf of the wholesaler or supplier. Major

contract distributors include Wincanton and Gist, whose clients lie within retail and

foodservice as well as producers themselves.

Figure 3 Routes to market in the food industry

Source: Adapted from IGD (2006)

Types of food wholesale

3.4 The modern food wholesale sector can be classified in a number of ways to

reflect its differing roles and relations. One approach is to classify by what products are

available and which markets are supplied. ONS‟ distinction between non-specialist and

specialist wholesalers is fairly clear, but the non-specialist sub-sector is not broken

down. IGD provides this further breakdown (see section 5 below). For now we can

distinguish three broad categories:

Manufacturer / Producer / Importer

Contract Distributor

Retail Foodservice

Wholesaler

Supermarket

Page 10 of 38

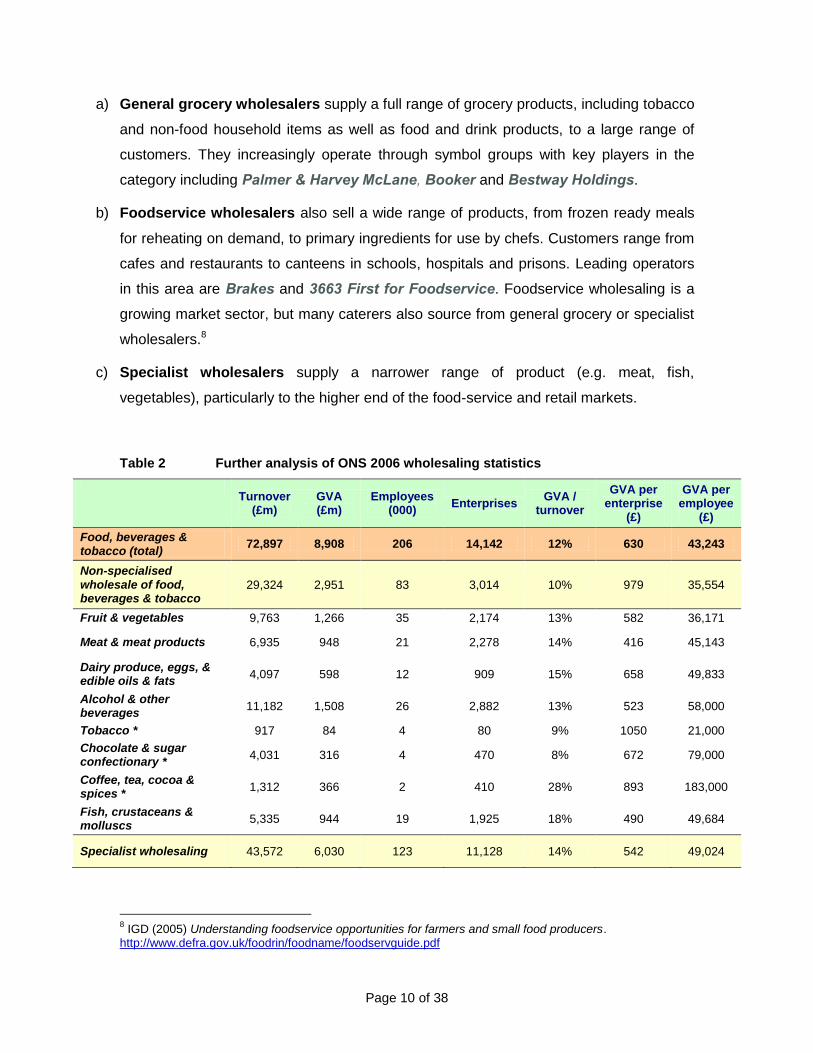

a) General grocery wholesalers supply a full range of grocery products, including tobacco

and non-food household items as well as food and drink products, to a large range of

customers. They increasingly operate through symbol groups with key players in the

category including Palmer & Harvey McLane, Booker and Bestway Holdings.

b) Foodservice wholesalers also sell a wide range of products, from frozen ready meals

for reheating on demand, to primary ingredients for use by chefs. Customers range from

cafes and restaurants to canteens in schools, hospitals and prisons. Leading operators

in this area are Brakes and 3663 First for Foodservice. Foodservice wholesaling is a

growing market sector, but many caterers also source from general grocery or specialist

wholesalers.8

c) Specialist wholesalers supply a narrower range of product (e.g. meat, fish,

vegetables), particularly to the higher end of the food-service and retail markets.

Table 2 Further analysis of ONS 2006 wholesaling statistics

Turnover

(£m) GVA (£m)

Employees (000)

Enterprises GVA /

turnover

GVA per enterprise

(£)

GVA per employee

(£)

Food, beverages & tobacco (total)

72,897 8,908 206 14,142 12% 630 43,243

Non-specialised wholesale of food, beverages & tobacco

29,324 2,951 83 3,014 10% 979 35,554

Fruit & vegetables 9,763 1,266 35 2,174 13% 582 36,171

Meat & meat products 6,935 948 21 2,278 14% 416 45,143

Dairy produce, eggs, & edible oils & fats

4,097 598 12 909 15% 658 49,833

Alcohol & other beverages

11,182 1,508 26 2,882 13% 523 58,000

Tobacco * 917 84 4 80 9% 1050 21,000

Chocolate & sugar confectionary *

4,031 316 4 470 8% 672 79,000

Coffee, tea, cocoa & spices *

1,312 366 2 410 28% 893 183,000

Fish, crustaceans & molluscs

5,335 944 19 1,925 18% 490 49,684

Specialist wholesaling 43,572 6,030 123 11,128 14% 542 49,024

8 IGD (2005) Understanding foodservice opportunities for farmers and small food producers.

http://www.defra.gov.uk/foodrin/foodname/foodservguide.pdf

Page 11 of 38

This higher value-added is evidenced by above-average labour productivity and

GVA‟s share of turnover (Table 2). On the other hand, GVA per enterprise tends

to be lower, suggesting many small firms are involved. The specialist sector is

highly diverse, ranging from traditional market-based wholesale traders to new

categories such as alcoholic drinks wholesalers (e.g. Bargain Booze and

Majestic Wine, who also operate a retail service), as well as ethnic food

wholesalers (e.g. SPL foods) and importers (e.g. Springbok wholesale).

3.5 A second approach is to consider how products are supplied to customers. There

are three broad modes of operation:

a) Traditional wholesale markets in which many traders assemble in a physical

market place to sell (usually specialist) product in bulk to independent retailers, other

wholesalers and food service operators (Table 3). The National Association of

British Market Authorities (NABMA) estimates annual total turnover for UK

wholesale markets at £2.5 - £3bn, around 10% of total specialist food wholesaling.

Wholesale markets employ some 10,000 people across the UK. Many of these have

a long history, such as Smithfield and Billingsgate in London. Many market-based

wholesalers are now diversifying and modernizing by operating directly from their

own premises, and offering delivery services, via telephone or internet with

customers generally being small independent shops (particularly for fruit and

Table 3 UK wholesale markets

London Outside London

Billingsgate (fish)

Belfast Bristol Hull Preston

Borough (fruit & veg)

Birmingham Cardiff Leicester Sheffield

New Spitalfields (fruit & veg)

Blackburn Derby Liverpool Southampton

Western International (fruit & veg)

Bradford Gateshead Manchester Wolverhampton

Smithfield (meat) Brighton Glasgow Nottingham

New Covent Garden (fruit & veg)

Source: NABMA

Page 12 of 38

vegetables) and foodservice outlets that use primary ingredients. As independent

shops have lost market share to supermarkets, traditional wholesale markets have

found their customer base shrinking and have sought to expand into the food-service

market, which is particularly vibrant in London. At New Covent Garden Market, 60-

80% of volumes handled by traditional fruit and vegetable wholesalers are sold to

these businesses, the remainder sold to the retail sector.9 The continued presence

of independent and niche retailers and food service outlets, combined with a desire

for a diversity of supply channels, is likely to ensure a continued demand for an

efficient food distribution system such as the wholesale markets, provided facilities

meet customer needs. According to Covent Garden market authority, its 240

businesses “between them supply about 40% of fresh fruit and vegetables eaten

outside the home in London.” A report commissioned by the GLA estimates that

total turnover of London wholesale markets will rise from £1.69 bn in 2006 (which is

over half estimated UK turnover) to £1.74 bn in 2026 (2004 prices). That translates

to 0.13% growth per annum over the period. Total turnover at Covent Garden

increased by 7% over 2007-8, largely driven by the wholesale distributor function.10

In view the relatively minor share of traditional market wholesaling (which accounts for

around 4% of total grocery wholesaling turnover and employment) and relative sparsity

of aggregate data, the rest of this paper focuses upon the two other, leading, modern

modes of operation:

b) Cash and carry outlets operate much like large supermarkets for registered

customers - typically independent retailers or caterers. Customers select goods from

the shelves, generally pay in “cash” (including card or cheque) rather than credit, and

are responsible for transporting their purchases away from the site. Examples

include Booker, Makro and Costco.

c) Delivered wholesalers, act as distributors as well as traders. Customers generally

have an account and pay for goods on provision of an invoice. Large-scale operators

use “their own fleet of vehicles to service customers from depots configured as

9 Covent Garden Market Authority. CGMA is owned by Defra

10 New Covent Garden Market, Annual Report 2007-8

http://www.newcoventgardenmarket.com/CGMA/ReportAccounts/tabid/95/Default.aspx; GLA, London

Wholesale Markets Review- June 2007. http://www.london.gov.uk/mayor/planning/industrial-land/docs/il-wholesale-markets-review.pdf

Page 13 of 38

distribution facilities, to which customers have no access”.11 Orders are made using

catalogues and product lists, via telephone, fax or the internet. Major delivered

wholesalers include Palmer & Harvey McLane and Musgrave Budgens Londis in

the general grocery sector, as well as the foodservice wholesalers Brakes and 3663

previously mentioned.

3.6 As retail markets become more competitive and wholesalers look to defend and

expand their business, these categories are starting to overlap. Traditional wholesale

markets are diversifying: at Covent Garden, for instance, many food service operators

are actually based in the market (generating 28% of its turnover), and offer a delivered

wholesale service to London restaurants, so the latter need not actually visit the market.

Some cash & carry wholesalers have decided to offer an optional delivery service, a

trend illustrated in the decision in 2006 by Blakemore Cash & Carry to restyle itself

Blakemore Wholesale to “reflect the changing nature of [its] business”.12 Additionally,

Booker – traditionally a cash and carry outlet – merged with internet grocery retailer

Blueheath in 2007, enabling them to offer “an unrivalled service of national delivery,

'top-up' delivery and cash and carry”.13

11

IGD (2006) p. 21

12 The Grocer (2006) The Big 30 Wholesalers, supplement to The Grocer, January 28

th 2006.

13 Talking retail (2007) „Booker and Blueheath to merge‟ http://www.talkingretail.com/news/5060/Booker-

and-Blueheath-to-merge.ehtml

Page 14 of 38

4. MARKET STRUCTURE AND TRENDS

4.1 The food wholesale sector – as elsewhere in the food chain - has undergone

significant change in recent years. This section begins to explore these patterns and

changes using ONS data, whilst the following section explores the IGD‟s analysis of the

non-specialist sector.

Consolidation and concentration

4.2 As elsewhere in the food chain, consolidation has been a major feature of the

wholesale sector, particularly the non-specialists, in recent years. Average turnover per

enterprise in the non-specialist sector rose from £4m in 1995 to £9.8m in 2006, as the

number of enterprises fell by more than a third to around 3000. In total wholesaling

enterprises fell by 11% over the same period (Table 1). High-profile acts of consolidation

in grocery wholesale include Blueheath’s acquisitions of CTM Wholesale and AC Ward

in 2005, Bestway’s take-over of rival Batleys in January 2005, and Booker’s merger

with Blueheath in May 2007.

4.3 Meanwhile, the number of unaffiliated convenience stores has shrunk

considerably, from 35,500 in 2000 to 25,893 in 2006. This has led some wholesalers to

develop their own symbol groups, in order to protect their customer base. A recent

example was Booker’s purchase of 2,000 independent stores for its own Premier

symbol group, thus securing a core customer base of £800m per annum.14

4.4 Wholesalers, particularly the non-specialists, have sought to benefit from

economies of scale and distributional efficiencies in order to remain cost competitive, not

only with each other but more so with the multiple retailers who are expanding their

share of the convenience and one-stop shopping sectors and thus putting pressure on

wholesalers‟ customer base, the small independents. The result is increased

concentration: seven firms now account for around two-thirds of the non-specialist

14

Competition Commission (2007a), p. 2

Page 15 of 38

market (Figure 4); and one or two firms represent a significant proportion of sales in

each market segment (Table 4).15

Figure 4 Company shares of the non-specialist grocery wholesale sector

Palmer &

Harvey McLane

17%

Booker

12%

Bestway/Batleys

8%

Brake Bros

7%3663

6%

Musgrave

5%

Costco

5%

Others

40%

Delivered

Cash & Carry

Foodservice

Mixed

Table 4 Large non-specialist wholesalers, 2007

Company Sales (£m) Share of relevant sub-sector

Delivered wholesale Palmer & Harvey McLane 3,983 46%

Cash & Carry Booker 3,036 37% Bestway/Batleys 1,850 30% Costco 1,128 7% Makro 1,040 4%

Foodservice wholesale Brake Bros 1,638 13% 3663 First for Foodservice 1,540

12%

Sources for figure 4 and table 4: The Grocer (2008), IGD (2008)

15

These do not necessarily represent distinct economic markets as defined by the competition authorities.

The Competition Commission recognises that the grocery wholesaling market consists of two segments, cash and carry and delivered; and that the line between these has become blurred in recent years. (para 3.28, CC Final Report (April2008))

Page 16 of 38

4.5 Specialist wholesalers rely less on economies of scale and direct competition

with supermarkets, hence are less concentrated. Many of them function best as smaller

enterprises due to their focus on local produce and supply, and an emphasis on value-

added goods and services, rather than the low margin bulk-buying and selling operations

that characterise general grocery wholesaling.

Other trends

4.6 In addition to consolidation, closer inspection of Table 1 suggests other notable

trends over the period since 1995:

Whilst aggregate turnover has risen 21% since 1995, this is less than overall

inflation (all items RPI increased by 33%), which means in real terms sales, and

possibly margins, are declining. That is another factor driving consolidation.

But this aggregate figure masks different fortunes across the sector. Non-

specialist wholesaling grew by 54% (outpacing inflation), while some specialist

sectors have struggled.

The fact that GVA has risen faster than turnover in most sub-sectors confirms

other evidence that wholesaling is becoming a more value-added activity both in

terms of goods and services.

Whilst output has increased, employment has generally fallen, reflecting an

uptake of new technology and improved labour productivity - a trend echoed in

the processing and retailing sectors. New technology has featured strongly in the

general wholesale sector, as the need for more efficient and timely logistics

intensifies. The spread of e-procurement, consolidation of warehouses (often

implemented with real time monitoring of supplier agreements) and

improvements in customer service have all involved greater use of IT. Large

wholesalers invested £12,836 per desktop on IT in 2005, more than investment

by food and drink retailers (£10,620) and significantly more than the average

£8,455 spent across all industries.16

16

Computer weekly (2006) „Food wholesalers spend heavily on IT‟ http://www.computerweekly.com/Articles/2006/11/07/219631/food-wholesalers-spend-heavily-on-it.htm

Page 17 of 38

In some specialist sectors, where firms are typically smaller than general grocery

wholesalers and there is less scope for improving technical efficiency, it may be

that workers are laid off as output falls.

Specialist sub-sectors

4.7 The fortunes of individual specialist sub-sectors in Table 1 are less easy to

generalise, and reflect a variety of trends and events. For instance:

The halving of enterprises in the meat sub-sector appears in part to reflect the

impact of BSE on abattoirs in the late 1990s (Figure 5). The number of

enterprises decreased by 28% in the 3 year period between 1995 and 1998, and

by only 26% in the much longer period between 1999 and 2005.

Figure 5 Numbers of wholesaling enterprises of meat and meat products, 1995-2005

0

1,000

2,000

3,000

4,000

5,000

1995 1997 1999 2001 2003 2005

A changing consumer culture that is increasingly focussed upon health, ethical

and convenience issues may help to explain the strong growth in the healthy fruit

and vegetable, fish, crustaceans and molluscs markets.

Similar drivers may help to explain the increases in GVA and enterprises within

industries where overall turnover is declining. For example, a decline in turnover

in the dairy sector has been accompanied by significant growth in GVA (59%)

and enterprise numbers (126%). This may reflect rising demand for organic or

quality regional products that command a higher premium, which in turn creates

attractive niche markets for new entrants.

Page 18 of 38

There are signs that some industries have been innovative. For example, in the

period 1999-2005, the number of fruit and vegetable wholesalers barely changed

whilst imports of fruit and vegetable rose by 37% - which suggests that the

wholesale sector has supplied a wider range of products contributing to rising

turnover and value-added.17

Tobacco wholesaling has shrunk significantly since 2000, as awareness of health

effects and rising taxes have reduced consumer demand.18 The ban on smoking

in indoor public places in England (2007) is likely to strengthen this trend.

17

AUK (2006). Table 8.1

18 According to The Grocer report – Focus On Tobacco, the UK tobacco market has been fairly flat, with total

tobacco volumes falling 3.9% year-on-year as of February 2008

Page 19 of 38

5. GENERAL GROCERY WHOLESALING: THE IGD PERSPECTIVE

5.1 Whereas the ONS provide a comprehensive and varied overview of different

forms of wholesale and highlight the specialist sectors, the IGD focus upon the general,

(“non-specialist”) sector, and, in their latest reports, upon the customer base for this

sector. In this section we summarise the key features of the generalist sector, drawing

heavily upon the IGD‟s 2006 and 2007 reports.

5.2 ONS figures show that in 2006 around 40% (£29bn) of the £73 bn UK food and

drink wholesale market was accounted for by the non-specialist sector (Table 1). In

contrast IGD measures the non-specialist UK food wholesaling sector at £24.1bn in

2007, an increase of 2% on 2006 (Figure 6). Although the exact reason for this

difference is unclear, it is most likely to be due to definitional differences.

Figure 6 Breakdown of food wholesale sector by turnover

Source: IGD (2008), ONS (2007)

5.3 IGD analysis reveals that nearly half of non-specialist wholesale sales are to

independent and convenience retailers, and just over a third to the foodservice market.

Other business and retail customers account for the remainder. We look at each of these

main outlets for non-specialist wholesaling as characterised by IGD.

Professional Business

Users £1.3bn

Independent and

convenience retail

£11.6bn

Foodservice market £8.6bn

Non-specialist wholesaling

£29.3bn

Specialist wholesaling

£43.6bn

UK food & drink wholesale £72.9bn

ONS breakdown

IGD breakdown

(£24.1 bn) Other retail

£2.6bn

Page 20 of 38

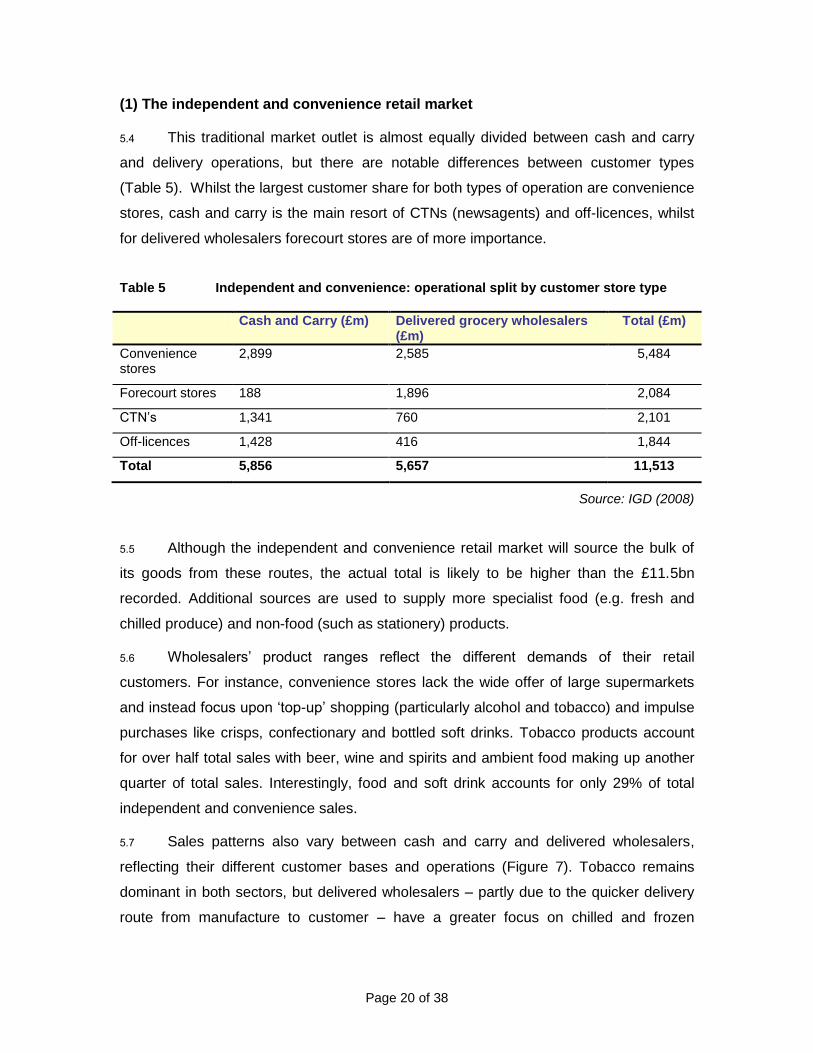

(1) The independent and convenience retail market

5.4 This traditional market outlet is almost equally divided between cash and carry

and delivery operations, but there are notable differences between customer types

(Table 5). Whilst the largest customer share for both types of operation are convenience

stores, cash and carry is the main resort of CTNs (newsagents) and off-licences, whilst

for delivered wholesalers forecourt stores are of more importance.

Table 5 Independent and convenience: operational split by customer store type

Cash and Carry (£m) Delivered grocery wholesalers (£m)

Total (£m)

Convenience stores

2,899 2,585 5,484

Forecourt stores 188 1,896 2,084

CTN‟s 1,341 760 2,101

Off-licences 1,428 416 1,844

Total 5,856 5,657 11,513

Source: IGD (2008)

5.5 Although the independent and convenience retail market will source the bulk of

its goods from these routes, the actual total is likely to be higher than the £11.5bn

recorded. Additional sources are used to supply more specialist food (e.g. fresh and

chilled produce) and non-food (such as stationery) products.

5.6 Wholesalers‟ product ranges reflect the different demands of their retail

customers. For instance, convenience stores lack the wide offer of large supermarkets

and instead focus upon „top-up‟ shopping (particularly alcohol and tobacco) and impulse

purchases like crisps, confectionary and bottled soft drinks. Tobacco products account

for over half total sales with beer, wine and spirits and ambient food making up another

quarter of total sales. Interestingly, food and soft drink accounts for only 29% of total

independent and convenience sales.

5.7 Sales patterns also vary between cash and carry and delivered wholesalers,

reflecting their different customer bases and operations (Figure 7). Tobacco remains

dominant in both sectors, but delivered wholesalers – partly due to the quicker delivery

route from manufacture to customer – have a greater focus on chilled and frozen

Page 21 of 38

foodstuffs, whereas beer, wine and spirits are relatively more important for cash and

carry wholesalers.

Figure 7 Independent and convenience: Breakdown by category sales, 2007

Source: IGD (2008)

5.8 Market concentration is relatively high. The three-firm concentration ratio in the

independent and convenience sector is estimated at 57%, with the five-firm ratio rising to

78%. The largest player P&H McLane – with a 23% share – is a delivered wholesaler,

whilst the second and third largest firms, Booker and Bestway – are traditionally cash

and carry wholesalers. However, the recent acquisition of internet based delivery

wholesaler Blueheath by Booker will change these dynamics.

Figure 8 Independent and convenience: Estimated wholesale shares, 2006

19%

15%

13%

8%

4%

18% 23%

P&H McLane Booker Bestway SPAR MRP Costco Others

Source: IGD (2008)

Cash and carry

59%

16%

13%

3%1%

5%3%0%

Tobacco Beers, w ines and spirits AmbientChilled and fresh Frozen Soft DrinksNon-Food Consumables Non-food Durables

Delivered grocery wholesalers

51%

9%

14%

9%

3%

7%

4% 3%

Page 22 of 38

5.9 In order to compete with larger firms entering and supplying the convenience

retail market, most non-specialist food wholesalers are members of one or more of the

wholesaler buyer groups (Table 6). These buying groups provide a range of services to

members, in particular:

negotiating trading terms with suppliers, to give members similar buying power to

larger businesses; and

providing services for marketing, promotional activity, own label development and

business support.

5.10 Some smaller buying groups offer a more limited range of services, and can

themselves be affiliated to the larger groups in order to give their members access to a

wide range of benefits. For example, Key Lekkerland and Costcutter are affiliated to

Today‟s, whilst Sterling is a member of Landmark.

5.11 Buying groups operate in different ways. One model is that adopted by SPAR,

whose six members are given the sole franchise of the SPAR brand within their given

region. These wholesalers are then entrusted to exclusively supply the SPAR retail

network through their own dedicated delivery service. A less rigid model, as adopted by

Landmark and Today’s, involves the buying group performing a variety of functions on

behalf of their wholesaler members, whilst leaving them free to serve whichever

customers they choose.

Table 6 UK Grocery Wholesaling Buyer Groups

Group Membership and operation Total Member Turnover

Today’s 350 companies; cash & carry, delivered and foodservice/catering

£5.0 bn

Landmark 29 companies; primarily cash and carry but also foodservice

£1.8 bn

SPAR 6 delivered wholesalers dedicated to SPAR retail network

£1.8 bn

Key Lekkerland 5 delivered wholesalers £500 m

Sugro 54 delivered wholesalers £500 m

Sterling Supergroup 52 mostly foodservice focussed wholesalers

£460 m

Source: IGD 2006

Page 23 of 38

5.12 Specialist wholesalers are less likely to require the services of a buyer group.

Rather than sourcing from a wide range of large national, branded suppliers, specialist

wholesalers are more likely to offer a route to market for suppliers that are smaller and

regional like the wholesaler. Because of this, there is less need to rely on using the

power of a larger organisation to deliver improved trading terms.

(2) The foodservice market

5.13 Around three-quarters (74%) of the food service market is supplied by

wholesalers operating a delivered service, with the remaining 26% supplied by cash and

carry. As Table 7 shows the main customers of this delivered service are restaurants,

pubs, hotels, workplaces, and public sector procurement for schools, hospitals and

prisons. Over half of cash and carry sales in this sector come from the pub / restaurant /

hotel sector.

Table 7 Food service: Operational split by customer store type

Cash and Carry (£m) Delivered foodservice wholesalers (£m)

Total (£m)

Restaurants, pubs, hotels etc

1,207 3,666 4,873

Education, health & welfare, workplace

427 2,101 2,528

Fast food, cafes etc 612 492 1,104

Total 2,246 6,259 8,505

Source: IGD (2007)

5.14 Unsurprisingly, food and soft drinks account for a larger share of food service

sales than convenience retail sales. The leading delivered wholesalers focus sales on

edible grocery, frozen, chilled/ fresh and impulse products, whilst a third of cash and

carry sales is in tobacco and beer, wine and spirits (Figure 9).

Page 24 of 38

Figure 9 Food service: Breakdown by category sales, 2006

Source: IGD (2008)

5.15 Concentration in the foodservice wholesaling market is relatively low (Figure 10)

The three firm market concentration (consisting of Brakes, 3663 and Booker) accounts

for just over a third of sales. Brakes and 3663 operate in the delivered sector, and

Figure 10 Food service: estimated wholesale shares, 2007

Brakes 13%

3663 12%

Booker 10%

Others 51%

Woodward/ DBC

4%Makro 4%

Costco 2%

Bestway 2%Caterforce 2%

Source: IGD (2008)

Cash and carry

8%

24%

28%

20%

4%

8%

2%6%

Tobacco Beers, wines and spirits AmbientChilled and fresh Frozen Soft DrinksNon-Food Consumables Non-Food Durables

Delivered foodservice

0%1%

44%

19%

23%

10%

3%

0%

Page 25 of 38

Booker in the cash and carry sector. The five-firm concentration is only 43%. “Others”

account for 51% of the market, and consist of „single ownership operations… [and] a

number of group organisations within the delivered foodservice wholesale sector,

bringing smaller businesses together in order to benefit from combined scale‟.19

5.16 The recent growth in the foodservice market represents an opportunity for food

wholesalers, with four-fifths of wholesalers surveyed by The Grocer agreeing that

„foodservice would form a major part of their plans to survive and grow their businesses

as the dominance of the multiples in the grocery sector continued to grow.‟ One of the

main reasons for this is the changing interests and demands of consumers. For

example, increased concern for food quality and origin (e.g. local, organic etc) have

prompted foodservice providers to react to this trend thereby supplying different products

(often of higher value). In terms of local produce, cash and carry operations are more

easily able to supply those goods due to their „presence in more localities‟.20 The ban on

smoking in public places may lead pubs to give greater emphasis to food, which in turn

is likely to increase the customer base for wholesalers.

5.17 But there are challenges too. Wholesalers, following retailers, need to respond to

the demand for healthier and ethical food standards. The prospect of an economic

slowdown and its impact on premium foodservice may serve to limit these growth

opportunities for wholesalers. For delivered wholesalers, the contractual style of

business – which can increase security and long-term planning – can also represent a

significant risk should contracts be lost or broken. Additionally, the „high frequency and

relatively small value of drops per site, means that there are more limited scale

opportunities to be found in foodservice distribution than in other sectors‟.21

(3) Professional Business Users and “Other Retail”

5.18 According to IGD, Professional Business Users (PBUs) are customers who are

not affiliated with convenience stores or foodservice providers, and usually have „more

miscellaneous requirements and in smaller volumes … purchasing as end users and not

for resale.‟ The sub-sector, worth £1.35 bn, is completely served by the cash and carry

19

IGD, UK Grocery and Foodservice Wholesaling (2007) para 3.1.4.

20 IGD, UK Grocery and Foodservice Wholesaling (2007) p. 63.

21 IGD, UK Grocery and Foodservice Wholesaling (2007) p. 57.

Page 26 of 38

route, owing to the more specialist and limited range of many delivered wholesalers, and

the inefficiency of delivery services for smaller orders. According to IGD, the PBU market

accounts for 6% of the total non-specialist sector and 14% of cash and carry sales.

5.19 Product sales to PBUs are quite diverse, with over half the categories accounting

for over 10% of total business. The largest three categories are non-food consumables

(33%), beer, wine and spirits (14%) and tobacco (12%), show that the focus is not on

food products, which make up less than a third of total sales.

5.20 Supply to the PBU market is dominated by Makro, which hold 46% of total

market sales. The three firm market concentration is estimated at 94%, with the largest

two firms (Makro and Costco) making up 80% of total sales (Figure 11).

Figure 11 Professional Business Users: estimated wholesale shares, 2006

Makro 46%

Costco 34%

Booker 14%

Others 2%

Blakemore 4%

Source: IGD (2008)

5.21 Whilst the PBU market gives access to a wide customer base, the diverse nature

of the products demanded may compromise scale economies.22 In most cases, PBU

purchases are for nothing more than final consumption, so average spends are usually

relatively low and the potential for cost-effective expansion of this sector is limited.

22

IGD, UK Grocery and Foodservice Wholesaling (2007) p. 72.

Page 27 of 38

5.22 The £2.6bn “Other Retail” element largely comprises the value of the business

that P&H McLane has with the likes of Tesco and Sainsbury‟s for whom it supplies

tobacco into the kiosks in their large stores.

Delivered versus cash and carry operations

5.23 Delivered wholesaling is clearly the major player in non-specialist wholesaling

(see summary figures in Table 8).

Table 8 Cash and Carry and Delivered Wholesale sales by market segment

Cash and carry Delivered wholesale Total

Independent and convenience retail 5.9 5.7 11.6

Food service 2.2 6.3 8.6

Professional Business Users 1.3 0 1.3

Other retail 0 2.6 2.6

Total 9.5 14.6 24.1

Based on IGD (2008)

5.24 Moreover, the delivered sector has grown at a faster rate than cash and carry over the past ten years (Figure 12). That reflects the gradual decline in cash and carry‟s

Figure 12 Sales by operational category, 1996-2007

IGD (2008)

Page 28 of 38

shrinking tobacco market also poses a challenge to the cash and carry sector. In

contrast, delivered wholesalers are more flexible and appeal to a wider customer base

main customer base - the non-affiliated independent retail sector. Reliance on a

including convenience store symbol groups, forecourt chains and foodservice outlets,

and hence have a number of growth opportunities.

5.25 With greater value placed on time by businesses as well as consumers, it can be

both desirable and cost-effective for many customers to pay a premium to have their

goods delivered to them. This increased emphasis on flexibility and service has brought

about a significant change in the customer base of the non-specialist wholesale sector.

Specialist wholesalers who supply the expanding foodservice sector have been under

less pressure to diversify and consolidate.

5.26 The rise of symbol groups - to which independent retailers have become

affiliated as a means of enhancing both their buying terms and their customer offer - has

led to increased demand for delivered wholesale services. Other than increasing their

share of symbol group customers, some cash and carry operators have focussed their

attention on areas including general business use (i.e. PBUs) and supplying retail outlets

in non-traditional locations like railway stations or tourist attractions.

5.27 Another potential challenge for both cash and carry and delivered wholesalers,

lies with transport. For cash and carry operators, the fact that customers are themselves

expected to transport goods to their premises (along with the expense of storing and

displaying such products) means that the potential for expansion into fresh and chilled

produce is limited. Whilst delivered wholesalers avoid this problem, the nature of their

business means that they are subject to the volatility of transport costs, and the

constraints introduced by the Working Time Directive.

5.28 Cash and carry operators remain the cheapest and most flexible source of supply

for the smallest foodservice businesses, with no „minimum order‟ levels. This wide reach

and high visit rates „a good platform for the development of incremental sales‟ according

to the IGD. On the other hand, the small nature of customer purchases and the inability

to stock wide ranges of fresh and frozen produce can limit sales. In contrast, delivered

wholesalers focus more on contractual agreements with larger clients (and with

consolidation average client sizes are rising) which allows for greater security and long

term planning.

Page 29 of 38

6. COMPARING SUPERMARKET AND WHOLESALE SUPPLY CHAINS

6.1 This section compares the supermarket and wholesale supply chains, and

summarises the effects of increased competition within the convenience retail market on

wholesalers.

Comparison of supermarket and wholesale supply chains

6.2 As Figure 13 shows, the supply chain structures for supermarkets and

wholesalers are similar. At primary and secondary level the formations are almost

identical, with goods channelled to regional distribution centres directly, or via primary

distribution centres. However, at the tertiary stage, the wholesale chain has an

additional link in order to supply independent or affiliated (via symbol groups) retailers

and catering outlets. This creates the need for double margins within retail pricing, with

wholesalers having to permit returns for themselves and the trade customer

6.3 Moreover, as the multiple retailers have moved into convenience retailing, the

number of unaffiliated convenience stores has fallen by around a quarter between 2000

and 2006. A convenience store supplied by the supermarket route has a shorter overall

supply chain, with goods being supplied direct from regional distribution centres. This

process has not only meant that the supermarkets and wholesalers are increasingly

competing for the same customer base, but has forced structural changes within the

traditional wholesale supplied convenience sector.

6.4 Thus the rise of buyer groups and symbol groups can be seen as a major

response of the wholesale chain to compete with supermarkets and to become more like

supermarket chains. Thus buyer groups allow several wholesalers to gain more

favourable terms from suppliers, and help them to compete with supermarkets at this

level. Symbol groups improve buying terms further downstream and allow for

convenience stores to trade under a common fascia so as to create a sense of familiarity

and „brand‟ loyalty (e.g. store formats, own-label products), in the same way that the

multiples‟ have extended their brand into the convenience market.

6.5 Unlike supermarkets, however, wholesalers are limited in terms of product resale

and customer feedback. Wholesalers typically have no direct control over the method in

Page 30 of 38

which their products are resold by retailers or catering outlets. And the fact that most

wholesalers do not directly retail, combined with the lack of IT capabilities within tertiary

outlets (e.g. bar scanners), creates a problem for those keen to implement customer

focussed strategies in order to drive product sales.

Figure 13 Illustrative comparison of supermarket and wholesaler supply chains

Source: Defra

6.6 A range of factors will affect the competitive pressure in the wholesale

convenience sector:

Production

Multiple retail outlets

Large wholesale/ cash and carry warehouse

Regional distribution centre (supermarket chain)

Regional distribution centre (large wholesaler)

Primary distribution centre

Independent or affiliated retail

outlet

Catering outlet

Pri

ma

ry

Se

co

nd

ary

T

ert

iary

Buyer group

Symbol group

Convenience stores

Page 31 of 38

The outcome of the Competition Commission inquiry into the grocery sector,

which could affect the ability of multiple retailers to expand into the convenience

sector;

A slowdown in supermarket sales could encourage multiples to expand more into

convenience retailing;

An economic slowdown could also make consumers more price sensitive, which

in turn could lead to slower growth in the convenience market, where mark-ups

have been significantly higher than in large stores.

Much will depend on the ability of general grocery wholesalers to enhance

productivity and realise economies of scale and the success of symbol groups

and buyer groups to achieve marketing efficiencies and meet final consumer

demands.

6.7 In contrast, major consolidation would not be expected in the specialist sector.

This is because their route to market, products supplied and customer base are more

distinct than supermarkets, plus evolving social trends and attitudes will always allow for

niche markets that continue to attract new entrants.

Concerns over wholesaler viability

6.8 The Association of Convenience Stores and the Federation of Wholesale

Distributors have in recent years raised concerns regarding the ongoing financial viability

of the UK‟s grocery wholesalers in the light of supermarket expansion into the

convenience market. A decline in the number of convenience stores was felt to increase

grocery wholesalers‟ unit costs as their fixed costs are spread over a smaller customer

base. As part of its inquiry into the groceries sector, the Competition Commission (CC)

reviewed the recent financial performance of the fifteen largest grocery wholesalers

(which account for approximately three-quarters of sector revenue) to assess whether

the industry may be approaching a “tipping point” in its financial viability.

6.9 Industry assessments generally point to growth in grocery wholesaler revenue in

the next few years. However, the CC assessed the extent to which grocery wholesalers

would need to lose sales before their financial viability came into question. The

wholesalers suggested that a 20 to 40 per cent reduction in turnover would be necessary

Page 32 of 38

to make their businesses unprofitable. Reductions in sales volumes of this order seem

unlikely when compared with industry assessments of growth in wholesale revenues.

Based on the current and projected financial performance of the grocery wholesaling

sector, the CC concluded that the financial viability of the sector as a whole was not

seriously threatened. To the extent that convenience store closures placed grocery

wholesalers under financial pressure the CC expected this would be addressed primarily

through industry consolidation.23

23

Competition Commission, Groceries Market Investigation, Final Report (2008) Appendix 5.5 “Grocery Wholesaler Profitability”

Page 33 of 38

7. CONCLUSION AND OUTLOOK

7.1 The food wholesaling sector is more complex than the supermarket sector, for it

supplies a variety of different retail and foodservice outlets, and food service itself is

highly differentiated. It combines both large-scale, supermarket-style logistical operations

and smaller specialised, wholesalers, as recorded in the ONS data. Because of this

complexity boundaries of type and operation are becoming blurred and classification of

the sector is becoming trickier. This is reflected in the IGD altering its own classification

methodology of the sector in 2007.

7.2 A number of interlinked trends and processes suggest that the food and drink

wholesaling sector is in a period of significant change:

● The customer base has shrunk as supermarkets have gained market share.

● This has pushed non-specialist wholesalers, in particular, towards consolidation:

their numbers have declined by 37% from 1995 to 2006, and seven firms now supply

60% of the non-specialist market.

● A shift in market share from cash and carry to delivered wholesaling, as firms seek to

offer greater convenience to the remaining customer base: symbol groups, forecourt

chains and foodservice outlets

● Specialist food wholesalers are more involved with premium produce, which has

grown more quickly than standard lines.

Table 9 summarises the main trends within the industry since 1995, which reflect

increased consolidation, productivity and value-added.

Table 9 Overall trends in food, beverage and tobacco wholesale, 1995- 2006

Turnover (£m)

GVA (£m)

Employees („000)

Enterprises

Average firm size

Food, beverages and tobacco

+21%

+67%

-7%

-11%

+36%

Source: Defra calculations/ ONS ABI (2007)

Page 34 of 38

7.3 Consolidation and differentiation are likely to continue in the future, and the

competitive challenges facing the sector are as strong as elsewhere in the food chain. In

view of the diverse nature of the food wholesale sector, it is difficult to generalise, but

issues facing and influencing the sector in the years to come include:

the competitiveness of independent, symbol group and convenience retailing,

particularly their response to economic slowdown;

the fortunes and format of the food service and eating out markets and specialist

premium produce generally, which may be particularly vulnerable to consumer belt-

tightening;

the implementation and impact of the Competition Commission Groceries Inquiry;

potential further regulation on food safety and standards;

energy and fuel prices (especially for delivered wholesalers);

the adaptability and modernisation of traditional wholesale markets

the future of tobacco consumption (traditionally a major element of non-specialist

wholesaling).

What is clear is that wholesaling in all its forms will continue to have a fundamental and

pervasive role in the UK food chain.

Food Chain Analysis Group

Defra

October 2008

Page 35 of 38

GLOSSARY

Buyer group Buyer groups are coalitions of one or more

wholesalers set up in order to obtain from suppliers

more favourable terms than each wholesaler could

obtain on its own. They can also provide a wide

range of other functions including marketing,

promotional activity, own label development and

business support.

Contract Distributors Firms that provide a logistics only service, as

opposed to a delivered wholesaler who deliver and

sell goods to the customer.

Delivered Wholesaler Wholesalers with whom customers generally have

an account and pay for goods on the provision of an

invoice, and act as distributors as well as

wholesalers.

Gross Value Added (GVA) The difference between the value of sales and the

value of purchased inputs.

Symbol group Term for a form of franchise in the retail sector. They

do not own or operate stores, but act as suppliers to

independent grocers and convenience stores, which

then trade under a common banner.

Total Factor Productivity A measure of productivity that incorporates both the

labour and capital used in the production process. Its

growth reflects the growth in output that is not

accounted for by the growth in inputs and is

considered a more balanced measure of productivity

than labour productivity.

Page 36 of 38

KEY SOURCES

Competition Commission, (2007). „Grocery Market Investigation: Emergent Thinking‟

http://www.competition-commission.org.uk/inquiries/ref2006/grocery/emerging_thinking.htm

Competition Commission, (2007a). „Working paper on grocery retailing‟

http://www.competition-commission.org.uk/inquiries/ref2006/grocery/index.htm

Competition Commission (2008). Grocery Market Investigation: Final Report

http://www.competition-commission.org.uk/rep_pub/reports/2008/fulltext/538.pdf

Europe Economics, (2005). „Impact of Supermarket Expansion in the Convenience Retailing Sector: A Report for the Association of Convenience Stores‟

Grocer, The, (2006). „The big 30 Wholesalers‟ supplement in The Grocer issued 28 January 2006.

Institute of Grocery Distribution (IGD), (2005). „Understanding foodservice opportunities for farmers and small food producers‟.

http://www.defra.gov.uk/foodrin/foodname/foodservguide.pdf

Institute of Grocery Distribution (IGD), (2006). „UK Grocery Wholesaling: A strategic guide‟

Institue of Grocery Distribution (IGD), (2008). „UK Grocery and Foodservice Wholesaling Outlook‟

Institute of Grocery Distribution (IGD), (2007). „UK Grocery and Foodservice wholesaling‟

Office of National Statistics (ONS), (2007). „Annual Business Inquiry‟

http://www.statistics.gov.uk/abi/

Page 37 of 38

LEADING UK WHOLESALERS

Founded in 1925 Palmer and Harvey McLane is the UK‟s 3rd largest private company with an annual turnover of £3.53bn. The non-specialist delivery wholesale provides over 9,000 different product lines, with a 28% shar of total tobacco market (54% of multiples) and 14% of total.

Founded in 1983, US based Costco currently has 19 locations in the U.K, and over 502 worldwide. Across the globe Costco employs 124,600 people and has a turnover of $58.96bn (2006).

Founded in 1925 Palmer and Harvey McLane is the UK‟s 3rd largest private company with an annual turnover of £3.53bn. The non-specialist delivery wholesaler provides over 9,000 different product lines, with a 28% share of total tobacco market (54% of multiples) and 14% of total confectionary.

Booker is the most prevalent Cash and carry chain in the UK with 172 stores nationwide. It was originally a sugar trade company but now concentrates on supplying the independent grocery sector. Previously part of the Iceland (supermarket) group it was acquired by the Baugur Group in February 2005. It employs over 8,000 people and has a turnover of £3.1 billion.

With the £100m acquisition of Batley's last year, Bestway is now the second-largest and most profitable cash and carry operator in the UK, with an annual turnover of £1.8bn. It serves 100,000 customers through its 50 branches and delivered services.

Founded in 1983, US based Costco currently has 19 locations in the U.K, and over 502 worldwide. It has 19 depots throughout the UK generating a company turnover of just over £1bn.

Page 38 of 38

Since opening its first outlet in 1971, Makro has expanded to 33 stores, employing 8,500 people with a turnover of £1.2bn. In 1998, it was acquired by Metro - one of Europe‟s biggest trading groups - which currently has 416 outlets in 24 countries.

Brakes are leading suppliers to caterers in the UK with a combined turnover from its UK and French operations in excess of £1.6 billion. They have 48,000 customers and 12,000 product lines.

Formed in 1999, 3663 First for Foodservice accounts for around 13% of the UK foodservice market, with turnover of £1.5bn. Customers include 30,000 independent outlets, national and multinational companies and Government bodies, and range from corner cafés to five-star restaurants.