Impact of USDA's Supplemental Nutrition Assistance Program ...

FOOD PROCUREMENT BY

USDA�s FARM SERVICE AGENCY

Economic Research Service, U.S. Department of Agriculture. AgriculturalEconomic Report No. 766.

Abstract

USDA�s Farm Service Agency (FSA) purchases food products for distributionthrough several of the Department�s food assistance programs. This report describesFSA purchase methods and compares them to procurement strategies used by otherFederal agencies and by private sector firms. It summarizes the principal policyissues faced by FSA in designing procurement strategies. Finally, it uses a detailedstatistical analysis to compare FSA prices to those realized in the private sector, andto identify the separate effects of agricultural commodity prices, seasonality, clientlocation, purchase volumes, product characteristics, and competition on FSA prod-uct prices.

Keywords: procurement, auctions, food assistance, competition

This report was prepared by James M. MacDonald [202-694-5391], Charles R.Handy [202-694-5385], and Gerald E. Plato [202-694-5383]

Washington, DC 20036-5831 September 1998

Contents

Executive Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .iii

Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1

An Overview of Federal Food Procurement Programs . . . . . . . . . . . . . . . . . . . . 3

USDA Domestic Food Procurement: Programs and Expenditures . . . . . . . . . . . 9

FSA Procurement Auctions: How the Process Works . . . . . . . . . . . . . . . . . . . . 15

Issues in USDA Procurement Policies . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

Data for Empirical Analyses of FSA Auctions . . . . . . . . . . . . . . . . . . . . . . . . . 27

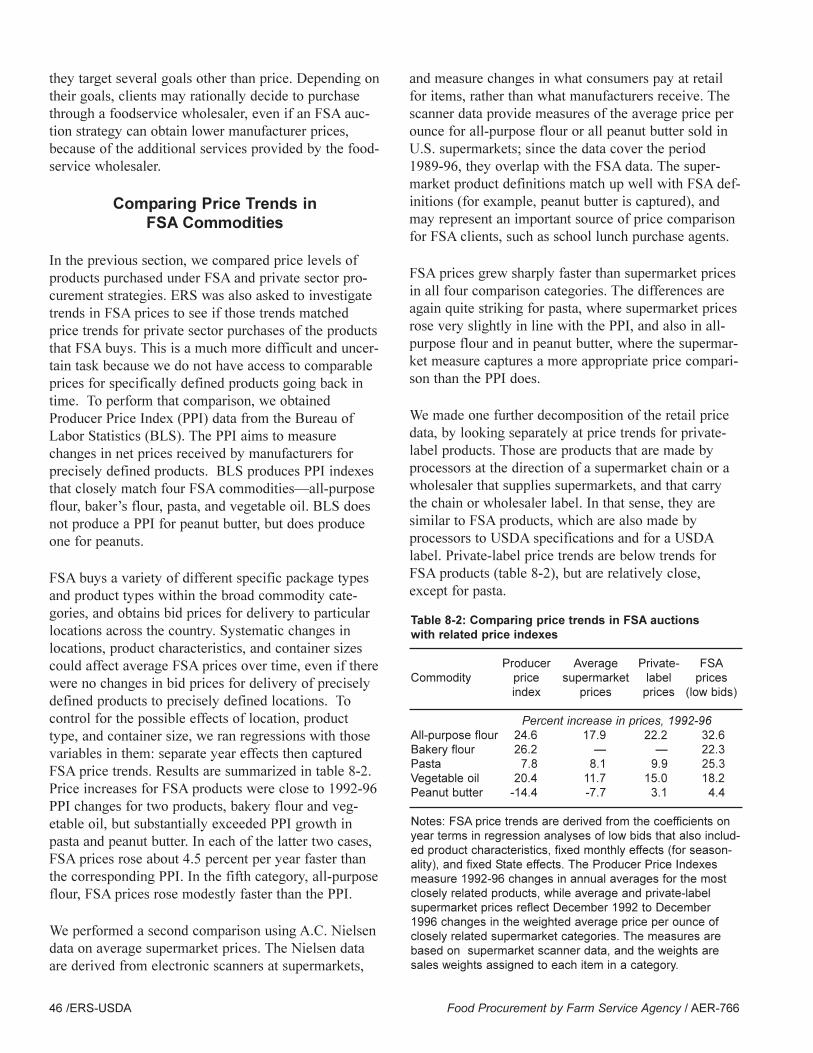

Statistical Analysis of Bid Prices for Five FSA Commodities . . . . . . . . . . . . . 33

Comparing FSA to Commercial Prices . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 43

Conclusions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 49

References . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 53

Appendix A � Glossary of Acronyms . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 54

Appendix B � Detailed Regression Results�Analyses of Low Bids . . . . . . . 55

ii

EXECUTIVE SUMMARY

The U.S. Department of Agriculture�s Farm Service Agency (FSA) purchases foodproducts for distribution through several of the Department�s food assistance pro-grams. FSA purchases food throughout the year, using methods that economistsrefer to as auctions. The food products are then delivered to States for distribution toclient agencies, such as school systems and social service organizations, which inturn distribute the products to needy households.

In the fall of 1996, FSA asked the Department�s Economic Research Service (ERS)to evaluate the agency�s procurement system. This report summarizes that work,based on three sources of information: 1) interviews with participants, includingFSA employees and clients, other government agencies with responsibilities forfood procurement, and private sector food processors and distributors; 2) summaryFSA expenditure and quantity data; and 3) an extensive statistical analysis of dataon individual FSA auctions, focusing on the determinants of FSA bid prices and oncomparisons with commercial prices for the same products.

FSA Obtains Highly Competitive Prices

FSA�s system aims to elicit low-price bids for the delivery of large volumes of alimited number of food products. The system works well in reaching those goals:FSA prices are substantially lower than those paid by private sector buyers for cor-responding products. Moreover, processing margins for FSA products are quite low;FSA stretches USDA budget dollars by purchasing substantial volumes of foodproducts for any given budget allocation.

Experience at other major Federal procurement agencies, such as the Department ofDefense and the Department of Veterans Affairs, shows that ultimate consumerswant more than low prices. Along with nutrition, they are also interested in timelydelivery and product variety. FSA does not act as a full-line food distributor for itsclients, and hence does not focus on wide variety and rapid delivery. Rather, it pro-vides clients with the opportunity to obtain large volumes of a few items at veryfavorable prices, by limiting product variety and by responding more slowly toorders than full-line distributors. Clients can more effectively spend the rest of theirbudgets on a variety of products.

But Clients Cite Four Problems in USDA Service Quality

1. Unreliable Delivery. Because of FSA�s long lead times for delivery, client agen-cies must plan meals well in advance. If deliveries arrive late, meal plans are upset,meal quality can suffer, and client agency costs can rise sharply when they mustreplace FSA�s orders quickly. Interviewees cited several sources of delivery delays:lags due to USDA inspection delays (typically at small plants), cancellation of auc-tions, and vendor noncompliance.

iii

2. Product Selection. Client agencies feel that surplus removal goals often drive theselection and distribution of bonus commodities that clients frequently have littleinterest in, although this problem relates more to the distribution of bonus commodi-ties through the Agricultural Marketing Service.

3. Product Deterioration. USDA products follow a long distribution chain betweenordering and eating. A client first places an order with USDA, which arranges forproduction. A vendor then manufactures the product, and arranges for delivery fromthe processing plant to a State warehouse or to another processing site. The productis then delivered to the client�s central facilities, before being distributed to diningfacilities, where further preparation and holding may occur before serving.Deterioration may occur at any point in the chain.

4. Problem resolution. The client may interact with State government agencies inordering and final delivery, and may be unaware that up to five different USDAagencies may be involved in their order for food, as well as private vendors, truck-ers, and warehouses.

What Drives FSA Bids? Observations and Recommendations

1. Agricultural Commodity Prices. FSA bids are far more sensitive to agriculturalprice movements than are wholesale and retail food prices. Because FSA prices areso sensitive to agricultural prices, they will fall more than wholesale and retailprices when agricultural prices decline, and they will rise more when agriculturalprices rise. The gap between FSA and corresponding retail and wholesale pricesshould therefore be largest during periods of relatively low agricultural prices, andsmallest during periods of high agricultural prices.

2. Competition. We found that competition matters in FSA auctions, but it matters alot only in some circumstances. As an approximate rule of thumb, FSA can do asmuch for its clients by attracting a second bidder to a monopoly auction (reducingprices by 4-7 percent), as by finding four more bidders for an auction that alreadyhas two. Consequently, we recommend that FSA focus its efforts on adding biddersat those auctions that typically attract only 1 or 2 bidders.

The number of bidders in FSA auctions varies substantially by product and overtime. Where are the most serious competitive problems? The data suggest that sea-sonality is important for some products: for example, over three-quarters of monop-oly auctions in flour occur in the fall, when mills operate near peak capacity.Monopoly auctions are also more likely among products with limited FSA volume,because of unusual package sizes or product characteristics.

In those cases, FSA can counteract monopoly by conveying accurate price informa-tion to clients�for example, that FSA�s price advantages over commercial flourproviders are weakest in the fall and strongest in other periods, or that FSA�s priceadvantages are strongest in high-volume products. We recommend that FSA exploreways to counteract seasonal variations in monopoly by extending the experimentwith rolling contracts, currently in use with cheese, to other products.

iv

Participation in FSA bidding has a distinctive �all or nothing� character to it�bid-ders typically commit to being active in FSA auctions, in which case they bidactively each month on auctions for a variety of locations and products. Auctionparticipation then does not typically decline because bidders reduce the number ofauctions they are active in; rather, firms decide to get out of FSA bidding entirely.Our present research has not aimed to uncover the reasons why firms decide to enteror leave FSA�s bidding process. But efforts to increase competition should empha-size research into the reasons for entry and exit by those firms, and the researchshould generate strategies to attract participation by more firms.

3. Product Volumes. Monthly FSA purchase volumes have dropped substantially asa result of changes in USDA commodity support programs. But declining volumeshave not yet had any substantive effects on FSA prices. Purchase volumes have onlysmall direct effects on prices, and those effects are not always in the same direction.Moreover, the monthly volumes that matter are total USDA purchases (foreign anddomestic), and not simply domestic purchases. The most important effects on pricesoccur in months in which large PL480 purchases are occurring�in those months,coincident large domestic purchases can lead to FSA price increases of 2-4 percent.The driving factor in these instances are PL480 purchases, which vary quite sharplyfrom month to month. FSA should initiate strategies to get better prices on domesticflour and vegetable oil, either by smoothing PL480 purchases, or by timing domes-tic purchases to avoid peaks in PL480 purchases.

Order volumes (the amount going to a specific destination in a specific order) havevery small effects on prices. Larger orders generally draw more aggressive bidding,but prices only fall by less than 1 percent�combining orders into multiple truck-loads yields very limited savings. Major gains in price likely come as one goes totruckload volumes from smaller orders, and FSA already acts to combine smallorders into orders of at least truckload sizes.

Service Quality Observations and Recommendations

FSA�s procurement system is designed to obtain good-quality products at very com-petitive prices. But at times, FSA may sacrifice service quality in the form of reli-able delivery and in the pursuit of advantageous prices:

1. Canceled Auctions. There may be a problem in Kansas City Commodity Office�s(KCCO) calculation of constructed prices, used in deciding whether to cancel anauction and shift purchases to a later month. In particular, because constructedprices seem to be less sensitive to underlying agricultural prices than actual bidprices are, constructed prices may give insufficient weight to agricultural prices.Now, the threat of cancellation can be useful� auction theory suggests that thethreat can lead to more competitive bidding, and the threat of cancellation is onlycredible if it is actually used at times. But actual cancellations lead to lags in prod-uct deliveries, and can therefore impose substantial costs on clients. We thereforerecommend that FSA review its procedures for calculating constructed prices, with aparticular focus on the weight given to agricultural prices.

2. Penalties. Vendors have traditionally faced weak penalties for failures to meetFSA delivery dates. Our statistical analysis shows that vendors are very sensitive to

v

economic incentives�they revise bids quickly to changes in materials costs, trans-port costs, and capacity utilization. Stronger penalties for noncompliance, in theform of financial penalties or suspension of later contracts, should lead to improvedvendor compliance.

3. USDA Inspection and Labels. Under existing rules, FSA products undergo onsiteUSDA inspection and must carry USDA, rather than commercial, labels. The rulesare related: reliance on USDA labels and packaging shifts some risks of poor prod-uct quality to USDA, and consequently creates a need for USDA inspection.Inspection, along with occasional unusual packaging requirements, can raise vendorcosts by 1-2 percent; USDA inspection and testing can also lead to lags in productdelivery, which clients cite as a persistent problem. Some vendors, especially rela-tively small plants, cite inspection and packaging requirements as deterrents to par-ticipation in FSA auctions, because of the effects on cost and on timely delivery ofproducts.

The current system results in very competitive prices, and the insistence on USDAlabels may contribute to the competition that leads to those prices�some firms maynot wish to bid aggressively on their own branded products. In some products, inother words, the net effect of USDA labels and inspection may be lower prices. Butthe insistence on USDA labels may, in other products, limit opportunities to obtainsurplus stocks of commercially labeled products and may deter additional biddersfrom participating.

FSA currently purchases commercially labeled products in a few commodity cate-gories. In markets with only a few vendors, FSA may be able to obtain more prod-uct variety and greater competition by opening auctions to commercially labeledproducts�the clear examples include the current experiments in ready-to-eat cerealand infant formula. Those two cases illustrate a dilemma for the agency. A principalargument made for USDA labels is that they limit brand loyalty on the part of con-sumers and therefore allow for more competitive bidding, but brand loyalty isimportant in those two products (especially ready-to-eat cereal).

FSA�s shift to purchase of commercial labels reflects the agency�s judgment that theshift may introduce greater competition into two highly concentrated markets. ButFSA also purchases products for other markets in which brand loyalty is far lessimportant, because the brands are never seen by ultimate consumers and because theproducts are used as ingredients in final servings, not as the serving itself. We rec-ommend that FSA carefully evaluate its current experiments and consider a gradualexpansion of commercial labels (especially including high-quality private label andwholesalers� own-brand products), especially in products with limited existing brandloyalty and low vendor participation.

The research for this report relied primarily on paper reports, whose data were reen-tered into an electronic format, because FSA disposes of the electronic records ofauctions after 1 year. Electronic data retention grows cheaper every year, as domethods for analyzing data. Moreover, because of steady improvements in dataretention and analysis, undergraduate business and economics majors now routinelylearn almost all of the techniques used in this report. KCCO commodity analystsshould in the future be able to easily call up 5 years� worth of past auction data (forexample); they should be able to quickly summarize key data patterns, and can easi-

vi

ly be provided with expert summaries of more subtle issues. They should be able touse that information in making auction decisions and in delivering timely informa-tion and advice to client agencies. We recommend that KCCO�s future strategy forinformation technology include steps to retain electronic auction records and todevelop those records into easily accessible databases.

vii

The U.S. Department of Agriculture�s Farm ServiceAgency (FSA) purchases food products for distributionthrough several of the Department�s food assistanceprograms. The products are then delivered to clientagencies, such as school systems and social serviceorganizations, which in turn distribute the products toneedy households. FSA purchases food productsthroughout the year, using methods that economistsrefer to as auctions. An auction is a bidding mechanismthat encompasses a set of auction rules, which in turnspecify how potential bidders may participate in theauction; how the winner is determined; and how much,in the case of procurement auctions, the winner is to bepaid (McAfee and McMillan, 1987; Wolfstetter, 1996).Auctions are widely used in government procurementactivities, and are also used to distribute oil drilling andtimber harvesting rights on Federal property, and tofinance Federal activities through the sale of Treasurybills. In the private sector, auctions are used to sell suchproducts as wine, art, flowers, fish, and tobacco, and tosolicit delivery price offers for products ranging fromoffice supplies to tires to construction jobs.

In the fall of 1996, FSA asked the Department�sEconomic Research Service (ERS) to evaluate theagency�s system for procuring and distributing foodproducts. This report summarizes that work, and isbased on three sources of information. First, ERSresearchers conducted a series of interviews with partic-ipants in the process, including FSA employees andclients, people at other government agencies withresponsibilities for food procurement, and private sectorfood processors and distributors. Second, we acquired

summary expenditure and quantity data from FSA andfrom other government agencies. Finally, we developeda large database, using FSA administrative records, onthe results of separate procurement auctions and per-formed extensive statistical analyses of those auctions.We focused particularly on the determinants of bidprices in FSA auctions and compared those prices tocommercial prices for the same products.

Chapters 2 through 4 describe the environment withinwhich FSA carries out its procurement activities. Wefirst provide an overview of the largest Federal foodprocurement agencies. In particular, we describe thedifferences among USDA, the Department of Defense,and the Department of Veterans Affairs in procurementgoals and methods, and describe recent major changesin procurement methods at the latter two Departments.We then detail, in Chapter 3, USDA�s food procurementprograms�the agencies and food assistance programsinvolved, the statutory framework that drives USDAprograms, and recent expenditure patterns. Chapter 4provides a detailed description of the actual stepsinvolved in purchases administered by FSA.

In the fifth chapter, we build on the material intro-duced earlier, and describe a set of policy issues thatrelate to FSA procurement. That is, a set of specificrules currently constrains FSA to purchase quite specif-ic products, with customized packaging, and requires anextensive system of onsite inspection of USDA�s foodproducts. We summarize those rules, identify theirinterlinkages, and discuss potential alternatives.

Food Procurement by Farm Service Agency / AER-766 USDA-ERS / 1

CHAPTER 1

INTRODUCTION

Moreover, current FSA procedures could be modified ina variety of ways. We discuss potential modificationsand their possible effects.

Chapters 6 through 8 rely on the large database of FSApurchase records. We first discuss the construction ofthe database in chapter 6, and summarize the key price,volume, competition, and product measures in the data.In chapter 7, we report the results of our statisticalanalysis of bid prices in FSA purchases. We estimatethe effects of agricultural commodity prices, productand packaging characteristics, purchase volumes, andcompetition on bid prices in five FSA commodity cate-gories over a 5-year period. The results should helpFSA to identify the major factors behind actual andforecast changes in product prices and to plan for tacti-

cal changes in policies aimed at improving perfor-mance.

We use the analyses of chapters 6 and 7 to developmeasures of average FSA prices in chapter 8, measuredat particular times and locations. The chapter then com-pares those average prices to commercial price quotesfor those products, times, and locations. The data pro-vide evidence of the price advantages that FSA candeliver to its clients, as well as the sources of thoseadvantages; in short, it summarizes FSA�s relativestrengths and weaknesses in food procurement and dis-tribution. A concluding chapter summarizes our majorpositive and negative findings, and offers some recom-mendations for FSA auction strategy.

2 /ERS-USDA Food Procurement by Farm Service Agency / AER-766

Introduction

Several government agencies administer large-scalefood procurement programs. At the U.S. Department ofAgriculture (USDA), two agencies�the Farm ServiceAgency (FSA) and the Agricultural Marketing Service(AMS)�purchase food products for domestic distribu-tion on behalf of a third�the Food and NutritionService (FNS). Those products are distributed throughdomestic food assistance programs, such as theNational School Lunch Program (NSLP) or TheEmergency Food Assistance Program, which arefinanced by FNS. About three-quarters of the food pur-chased under domestic food assistance programs is dis-tributed to school districts under the NSLP, while therest is distributed through a variety of smaller pro-grams, described more fully in chapter 3. The twoUSDA agencies spent $849 million on food purchasesfor domestic programs in 1996.

Food procurement forms a small part (less than 2 per-cent) of total FNS expenditures on domestic food assis-tance. Most of the total FNS food assistance budget of$38 billion goes to support direct cash transfers, such aspayments to foodstores for redemption of coupons andvouchers under the Food Stamp and Women, Infants,and Children Programs, or cash payments to schools forsubsidized meals under the NSLP. Schools receiveabout 20 percent of their USDA support in the form ofcommodities, with the rest in cash support.

FSA also purchases and ships food and agricultural

commodities to foreign countries under the Food forPeace program (PL480) and other international assis-tance programs. The programs are administered andfinanced by the State Department�s Agency forInternational Development (AID) or another USDAagency, the Foreign Agricultural Service (FAS), forwhich FSA acts as the buying agent. FAS expendituresfor PL480 programs were $1.21 billion in 1996. Inaddition, FAS spent another $84 million on food expen-ditures for the Food for Progress program. Under thisprogram, U.S. agricultural commodities are provided todeveloping countries and emerging democracies thathave commitments to introduce and expand free enter-prise in their agricultural economies.

At the U.S. Department of Defense (DoD), the DefensePersonnel Support Center (DPSC) purchases food formilitary bases, ships, and other military facilities.DPSC purchases for all four branches of the military,acting as the buying agent for the Defense LogisticsAgency (DLA). In addition, DPSC has contracts to actas purchasing agent for the U.S. Coast Guard, someprisons, and some school systems. DPSC food purchas-es amounted to approximately $525 million in 1996,and the agency also provided $115 million in other con-tract services.

At the Department of Veterans Affairs (VA), the Officeof Acquisition and Materials Management (OAMM)purchases food for 173 VA facilities, primarily medicalcenters. OAMM food expenditures amounted to $60million in 1996, along with another $12 million in food

Food Procurement by Farm Service Agency / AER-766 USDA-ERS / 3

CHAPTER 2

AN OVERVIEW OF FEDERAL FOOD

PROCUREMENT PROGRAMS

equipment and supplies. The agency also aims to obtaincontracts to act as purchasing agent for other entities;for example, OAMM handles food purchases for med-ical facilities in the U.S. Army Medical Command.

Program Goals

Each agency tries to reach several primary and sec-ondary goals through their procurement strategies. Forexample, the USDA agencies traditionally have haddual goals�surplus removal and food assistance.USDA has historically purchased substantial volumesof agricultural commodities in order to support pricesfor �program crops,� such as wheat, corn, and dairyproducts. The Department has then had to find ways todispose of the accumulated surpluses, and one way hasbeen to distribute them outside of normal commercialchannels through food assistance programs to low-income households and countries. Surplus removal,used for Section 32 purchases by AMS, often empha-sizes the rapid distribution of large volumes of particu-lar commodities, those that have had large harvests andfalling prices, in order to support producer prices. As aresult, AMS procurement has generally emphasizedagricultural commodities and less processed food prod-ucts because of their closer link to the farm sector.

Food assistance programs include the distribution ofemergency supplies of staple food items to areas hit bysuch natural disasters as floods, hurricanes, and earth-quakes, and the regular distribution of food products tomembers of low-income households. Assistance goalsinclude the assurance of nutritionally adequate dietsamong client groups, as well as income support forfood assistance recipients. Because most expenditureshave been aimed at staple food products that are oftenstorable for extended periods, procurement procedureshave emphasized the acquisition of simple, nutritionallysound foods at competitive prices.

DoD and VA purchasing agencies do not operate undersurplus removal expectations. Because they provide asubstantial share (up to 100 percent, for some) of thefood consumed by their clients, they are under greaterpressure to provide for product variety, and not simplynutritional adequacy. Moreover, because DoD clientfood demands may fluctuate sharply (for example,when a ship arrives at a base or when a reserve unit isactivated), DPSC�DoD�s procurement agency�mustrespond rapidly to unexpected service demands. As aresult, the agencies� procurement strategies emphasize

quick delivery of a wide variety of food products.

Food procurement agencies also aim to realize somesecondary goals that often are imposed by statute. Eachis required to support small businesses by setting asidea certain percentage of purchases for firms that are des-ignated as small businesses. USDA is required to buyfoods that use products from American farms, and theMerchant Marine Act requires FSA to arrange for oceanshipment in American ships. VA medical centers areexpected to purchase a percentage of food in local areasin order to support local economic development. USDAagencies often attempt to encourage good dietary andpurchase habits through example, by offering low-fatversions of food products and by forgoing more expen-sive commercially branded products.

Procurement Methods

USDA, DoD, and VA use different procurement meth-ods. Most USDA procurement is done through sealed-bid auctions for the delivery of a limited variety of foodcommodities to central warehouses or further proces-sors. Client agencies then generally take responsibilityfor distribution from warehouses, reprocessing somecommodities (such as cheese and flour) into more high-ly processed foods (such as pizza), delivery to points ofconsumption, and local preparation. By contrast, DoDand VA have recently introduced �prime vendor pro-grams,� in which a private firm (the prime vendor) isresponsible for ordering products from processors, pro-viding storage for an inventory of products, and deliv-ering a wide variety of food products to all facilitieswithin a region, with clients then responsible only fortheir own ordering and for local preparation.

A Brief Description of USDA Procurement Methods

FNS receives the appropriation for USDA programs; italso allocates funds to the client State and tribal distrib-uting agencies, collects food commodity and productorders from these agencies, and ensures their compli-ance with program requirements. State and tribal agen-cies use FNS program guidelines to determine if indi-viduals are eligible to receive food products and todeliver products from warehouses to the targeted popu-lation.

Client agencies place orders for food products, workingfrom product lists (with likely price ranges) provided

4 /ERS-USDA Food Procurement by Farm Service Agency / AER-766

by FNS. USDA�s procurement agencies, FSA and AMS,then aggregate the orders to truckload quantities, andproduce invitations for vendors to enter bids to producethe orders. An invitation usually includes multiple auc-tions, where each auction is for the award of an orderfor delivery of truckload quantities of a preciselydefined food product to a distribution point within adefined time period. The time period is usually a 2-week span, the distribution point is usually a warehousein reasonable proximity to the client, and food productsare defined as to type (say, all-purpose flour or breadflour), package size, and ingredient requirements.

USDA distributes invitations and runs auctions once amonth for some products, while auctions for others areheld weekly (ground beef), seasonally (some fruit prod-ucts), or annually (infant formula). Vendors (food pro-cessing firms) respond by submitting sealed bids;sealed bids are not known or observed by rivals, aswould occur in the sort of open verbal auctions used atart auction houses. Vendors typically do not offer bidson all auctions in an invitation, but frequently enterbids on more than one. A bidder may place a maximumon the total quantity that they would be willing to pro-duce from all the bids entered in an auction, and bid-ders in some auctions may also place minimum quanti-ties, below which they will accept no awards.

USDA aims to award the order to the best bid in anauction, subject to several constraints. For internationalshipments, USDA considers ocean transport charges aswell as the vendor�s quoted prices for delivery of aproduct to a domestic port�that is, the winner is deter-mined by the lowest total cost to USDA. When lowbidders are above their maximum or below their mini-mum total quantities, agencies will attempt to makeawards in ways that will minimize invitation-wide totalcosts to USDA. Finally, some orders are set aside forsmall businesses, as long as a qualified small businessenters a bid that is within 5 percent of the lowest bid.

Vendors are expected to arrange for transportation towarehouse points or, in the case of international ship-ments, to ports. Commercial freight forwarders arrangefor ocean shipping to international clients, whiledomestic clients arrange for transportation from ware-houses. USDA requires onsite inspection of all prod-ucts; inspectors for some products are employed byAMS, while another USDA agency, GIPSA (the GrainInspection, Packers and Stockyards Administration),provides inspectors for other commodities. Laboratory

testing services supplement the onsite inspectors andare supplied by AMS and GIPSA.

Prime Vendor Programs

USDA�s procurement auctions rely on competitionamong processors to obtain precisely defined foodproducts at favorable prices. Prime vendor programsalso rely on competition, but for a different sort ofaward.

Under the DoD program, the country is divided intoregions, and in each region, a single prime vendor sup-plies military facilities with food products. DoD nowhas 50 Prime Vendor contracts in the continental UnitedStates. Contracts are for a single base year, with provi-sions for three or four 1-year extensions. The primevendor is generally not itself a manufacturer; most arefoodservice wholesalers. Prime vendors offer distribu-tion facilities and choices from a wide range of fooditems. They obtain products from processors, assembleloads for clients, and deliver from the prime vendor�swarehouses directly to ships, base dining halls, andother locations. Prime vendors also provide a centralpoint of contact for problems with deliveries, productquality, or errors in orders.

Prime vendors in the VA program perform a similarfunction, but the VA divides the country into 16regions. The geographically larger VA regions are ableto combine hospital purchases into a large enoughaggregate to correspond to the business opportunitiesoffered to prime vendors in DoD regions.

Prime vendor contracts are awarded after competitivebidding among potential vendors. The contracts are forindefinite quantities because base food demands are notperfectly predictable far in advance. The DoD procure-ment agency, DPSC, provides bidders with a list ofitems wanted, along with estimated quantities and like-ly minima and maxima; the agency also estimates thelikely dollar volume of sales for each region. Inresponse to the invitation, and after pre-proposal con-ferences, bidders submit very large and extensive pro-posals. DPSC then evaluates the proposals. It considersa business segment of the proposal, in which it asks forprice quotes on a sample of items, as well as the bid-der�s fee per item. The agency also assembles a techni-cal panel to make site visits and to review the bidder�sordering systems, inventory controls, and delivery tech-nologies.

Food Procurement by Farm Service Agency / AER-766 USDA-ERS / 5

VA technical panels review the size of bidder ware-houses, the variety of products and the capability to addnew items, transport options, and purchase and account-ing systems. Price quotes are also included for evalua-tion in the business segment of bidder proposals.

Contract awards are made on the basis of the lowestpriced, technically feasible, proposal. DPSC managersexpect, however, that the basis for awards will shiftsomewhat toward best value, which would add consid-erations of past performance and service quality to theawards decision.

DPSC purchases some military-unique food items,including those with special packaging to withstandshipboard or airborne conditions as well as foods thatare prepared for field consumption. DPSC runs compe-titions to select a single manufacturer for each military-unique item, and handles orders and payment to themanufacturer. Prime vendors then assemble and delivermilitary-unique items to bases.

DoD and VA procurement agencies do not rely onextensive onsite inspection to provide quality controlsas USDA does. Instead, pressures to maintain qualityand to meet contractual obligations arise from severalsources. First, contracts are renewable, and past perfor-mance becomes a factor in competitions for renewedawards. Second, military facilities are not obliged tospend all of their food dollars at prime vendors; theymay also purchase from local vendors. Third, messhalls and other dining facilities are not obliged toaccept deliveries from prime vendors; they may rejectand return unacceptable products. Fourth, the agenciesretain the right to audit the relevant records of primevendors during the course of the contract. Finally, mostprime vendor food products are identical to those thevendor supplies to its other commercial clients. Vendorshave incentives to maintain and assure the quality oftheir private-label brands and services; if quality deteri-orates, they risk losing not only DoD and VA business,but commercial sales as well.

Causes of the Shift to Prime Vendor Programs

DoD prime vendors supplanted a system of militarydepots. Prior to the shift to prime vendors in 1995,DPSC ordered food products on behalf of military facil-ities, much as USDA�s agencies now order on behalf ofschool districts and other clients. Food products were

then delivered to depots operated by the DefenseLogistics Agency (DLA), and from there were distrib-uted to base warehouses. Finally, products were deliv-ered to mess halls, ships, and other dining facilitiesfrom the base warehouses.

Two problems drove the shift to a prime vendor system.First, aging military depots and warehouses were inneed of substantial investments in construction andmaintenance. Second, food deliveries required longlead times, 45 days between order and delivery. Primevendors provide substantially improved service to din-ing facilities; over 99 percent of orders are deliveredwithin 2 days, if substitution among brands and pack-age sizes is allowed. Vendors operate 7 days a week,and offer a wide variety of products. The military hasbeen able to consolidate depots and warehouses, and torealize substantial savings in the costs of carrying foodinventories, which fell from $230 million prior to initia-tion of the program to $69 million in late 1996, with agoal of $15 million after full implementation.

Of course, the need for warehouse space does not dis-appear with the introduction of the program�primevendors now provide services of storage, repackaging,delivery, and administration that the military used to doby itself. DPSC managers estimate that vendor fees forthese services amount to 11-12 percent of commoditysales. DPSC receives additional payments equal to 6percent of total expenditures for prime vendor com-modities and services. DPSC provides translation soft-ware to enable the different services to order through aconsistent computer system, advises facility managerson sound purchasing strategies, handles the flow ofpayments from bases and DLA through DPSC to thevendors, and administers the system of prime vendorcontracts.

Procurement agencies and clients must make someadjustments under prime vendor programs. With awider range of available products, clients must learnmore about the products that are commercially avail-able, and they need to invest in learning about electron-ic ordering and tracking systems. Agencies assumegreater responsibility for advising clients and forreviewing and supervising vendors.

The VA�s 1995 shift to a prime vendor program cameslightly before DoD�s did. Before then, VA purchasedabout 300 different food items distributed through adepot system. In the view of VA managers, vendor

6 /ERS-USDA Food Procurement by Farm Service Agency / AER-766

prices were relatively high, and delivery times throughthe depot system were poor. Food item distributioncosts appear to have been subsidized by pharmaceuticalitems in the VA depot system. When pharmaceuticalprocurement was pulled out of the depot system, thefood procurement program came under substantialfinancial pressure, leading to a search for alternatives.In the VA case, managers cite lower product prices,wider variety, more timely delivery, and the eliminationof depot facilities, along with their associated expenses,as advantages of the new system. Prime vendor feesaverage 9-12 percent of food product costs, and theVA�s procurement office, the Office of Acquisition andMaterial Management (OAMM), charges a one-half-percent fee for its services.

The VA provides some volume guarantees to primevendors by committing at least half of a region�s pur-chases to the prime vendor. Clients may also reducecosts on some items by providing volume commitmentson specific products to the manufacturer/vendor fromwhich the prime vendor purchases.

Conclusions

USDA�s procurement programs are designed to obtain alimited variety of precisely defined food products at thelowest possible cost to USDA for delivery to warehous-es. As we shall see in later sections, USDA relies ontight specifications and direct inspection to ensure prod-uct quality. The system is decentralized in that finaldelivery, reprocessing, and distribution to dining facili-ties are the responsibility of the client. The prime ven-dor programs used by DoD and the VA are designed toobtain important services, such as variety (and associat-ed inventory) and rapid delivery, in addition to foodcommodities. Vendors are expected to compete to offerpackages of service and price. DoD and VA aim toensure product quality through reliance on commerciallabels and continued competition among vendors forcontract renewals.

Food Procurement by Farm Service Agency / AER-766 USDA-ERS / 7

Introduction

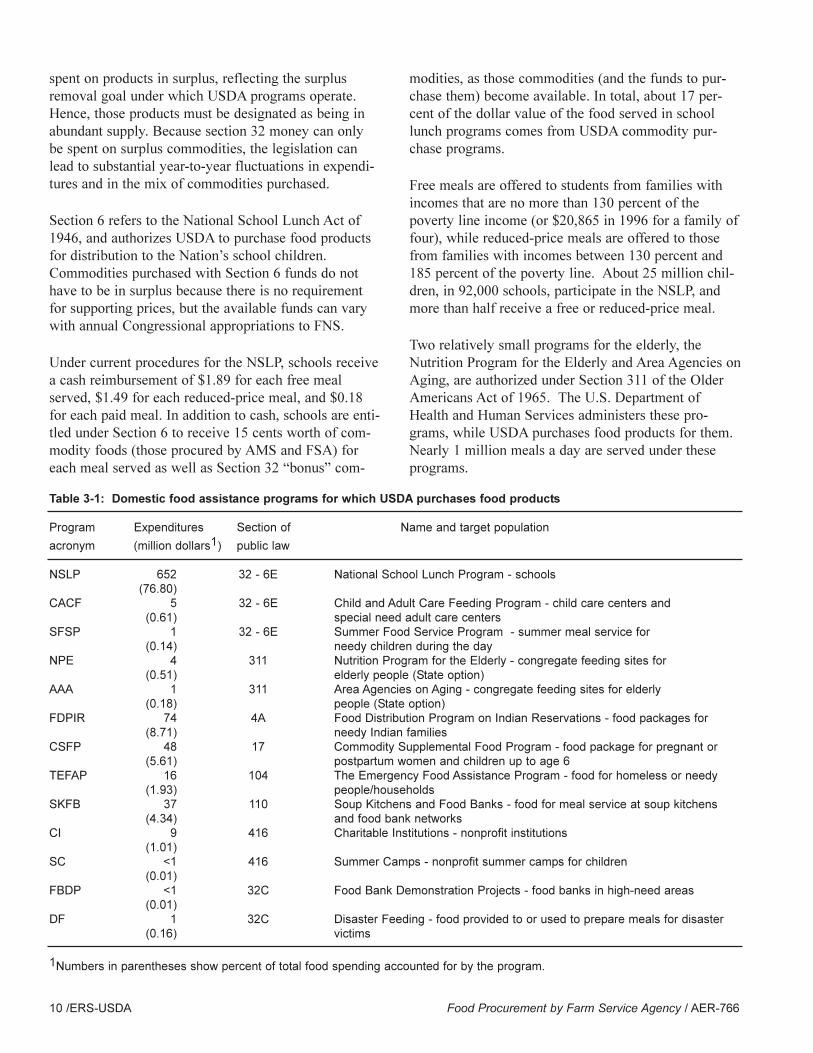

USDA purchases and distributes food commoditiesthrough 13 food assistance programs. Purchase and dis-tribution activities are essentially the same for each pro-gram, but spending authorities, target populations, andprogram goals differ. The collective goals of the pro-grams are to provide needy people with access to amore nutritious diet, to improve the eating habits of theNation�s children, and to stabilize farm prices throughthe distribution of surplus foods. This chapter summa-rizes USDA�s food procurement programs, identifiestheir authorizing legislation, and details the recent his-tory of annual expenditures under these programs.

Programs and Supporting Legislation

Table 3-1 lists the 13 programs, identifies their targetpopulations, links them to their supporting legislation,and shows the amounts spent on food procurement infiscal 1996. The column headed �Section of publiclaw� lists numbers that refer to the sections of the origi-nal legislation that authorize each program�s procure-ment activity; those numbers are common referencesfor program administrators.

The 13 programs spent a total of $849 million on foodprocurement in fiscal 1996. The four largest pro-grams�the National School Lunch Program (NSLP),the Food Distribution Program on Indian Reservations,the Commodity Supplemental Food Program, and Soup

Kitchens and Food Banks�purchased more than 95percent of the total, about $811 million. The NSLPalone accounted for almost 77 percent of the 1996 total,or $652 million.

The 13 programs are authorized under several differentstatutes, which create a variety of funding sources andfunding constraints for USDA. The first three programsin table 3-1, including the NSLP, are primarily support-ed by two separate congressional laws and subsequentamendments to these laws.

Section 32 refers to that section of the AgriculturalAdjustment Act of 1935. The Section authorizesUSDA to support prices of commodities in surplus bypurchasing them in the marketplace, and also authorizesUSDA to distribute commodities domestically. The leg-islation authorizes the funding of these activities withmoney collected from customs receipts; this funding isprimarily administered by AMS to purchase meat andlivestock, fruit and vegetable commodities, usuallyabout $400 million annually.

Funds used under section 32 are designed to supportagricultural markets. As a result, the funds are to beapplied to the purchase of relatively unprocessed foodproducts that are close to agricultural commodities inthe distribution chain. That is, the funds can be used topurchase pork but not frozen sausage pizza, and theycan be used to purchase chicken but cannot be appliedto paying for processing the chicken into chickennuggets. In addition, section 32 money is intended to be

Food Procurement by Farm Service Agency / AER-766 USDA-ERS / 9

CHAPTER 3

USDA DOMESTIC FOOD PROCUREMENT: PROGRAMS AND EXPENDITURES

spent on products in surplus, reflecting the surplusremoval goal under which USDA programs operate.Hence, those products must be designated as being inabundant supply. Because section 32 money can onlybe spent on surplus commodities, the legislation canlead to substantial year-to-year fluctuations in expendi-tures and in the mix of commodities purchased.

Section 6 refers to the National School Lunch Act of1946, and authorizes USDA to purchase food productsfor distribution to the Nation�s school children.Commodities purchased with Section 6 funds do nothave to be in surplus because there is no requirementfor supporting prices, but the available funds can varywith annual Congressional appropriations to FNS.

Under current procedures for the NSLP, schools receivea cash reimbursement of $1.89 for each free mealserved, $1.49 for each reduced-price meal, and $0.18for each paid meal. In addition to cash, schools are enti-tled under Section 6 to receive 15 cents worth of com-modity foods (those procured by AMS and FSA) foreach meal served as well as Section 32 �bonus� com-

modities, as those commodities (and the funds to pur-chase them) become available. In total, about 17 per-cent of the dollar value of the food served in schoollunch programs comes from USDA commodity pur-chase programs.

Free meals are offered to students from families withincomes that are no more than 130 percent of thepoverty line income (or $20,865 in 1996 for a family offour), while reduced-price meals are offered to thosefrom families with incomes between 130 percent and185 percent of the poverty line. About 25 million chil-dren, in 92,000 schools, participate in the NSLP, andmore than half receive a free or reduced-price meal.

Two relatively small programs for the elderly, theNutrition Program for the Elderly and Area Agencies onAging, are authorized under Section 311 of the OlderAmericans Act of 1965. The U.S. Department ofHealth and Human Services administers these pro-grams, while USDA purchases food products for them.Nearly 1 million meals a day are served under theseprograms.

10 /ERS-USDA Food Procurement by Farm Service Agency / AER-766

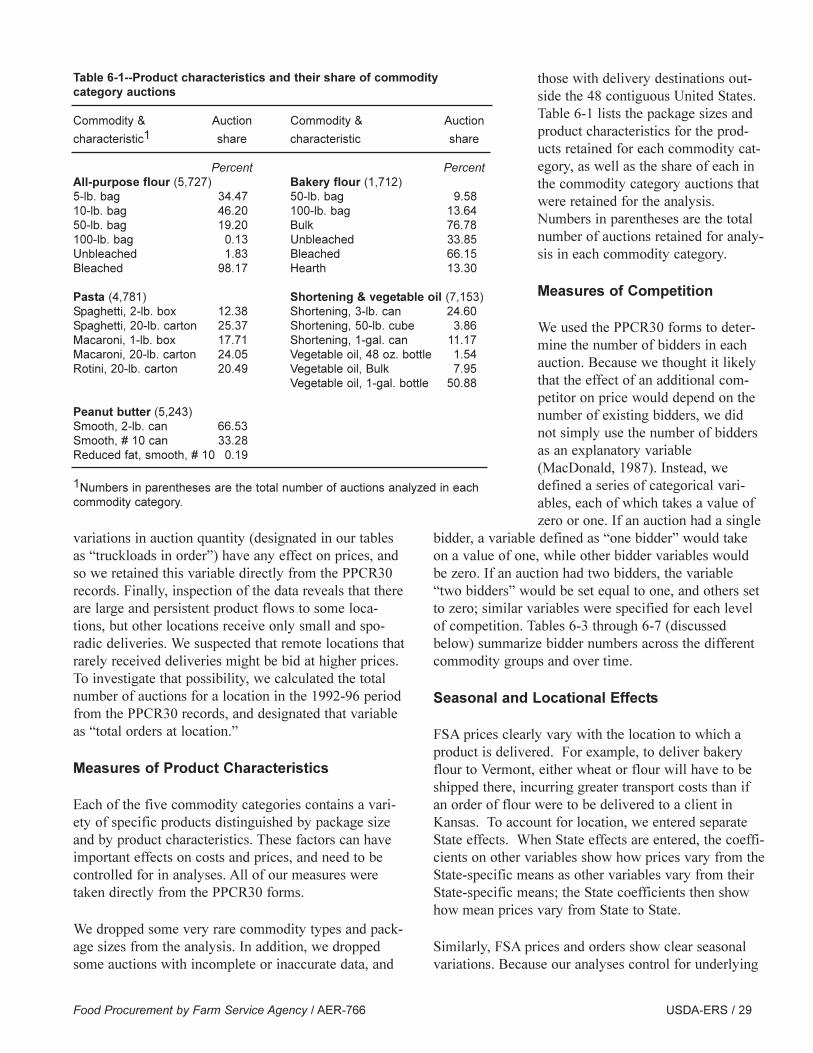

Table 3-1: Domestic food assistance programs for which USDA purchases food products

Program Expenditures Section of Name and target population

acronym (million dollars1) public law

NSLP 652 32 - 6E National School Lunch Program - schools(76.80)

CACF 5 32 - 6E Child and Adult Care Feeding Program - child care centers and(0.61) special need adult care centers

SFSP 1 32 - 6E Summer Food Service Program - summer meal service for (0.14) needy children during the day

NPE 4 311 Nutrition Program for the Elderly - congregate feeding sites for (0.51) elderly people (State option)

AAA 1 311 Area Agencies on Aging - congregate feeding sites for elderly (0.18) people (State option)

FDPIR 74 4A Food Distribution Program on Indian Reservations - food packages for (8.71) needy Indian families

CSFP 48 17 Commodity Supplemental Food Program - food package for pregnant or (5.61) postpartum women and children up to age 6

TEFAP 16 104 The Emergency Food Assistance Program - food for homeless or needy (1.93) people/households

SKFB 37 110 Soup Kitchens and Food Banks - food for meal service at soup kitchens (4.34) and food bank networks

CI 9 416 Charitable Institutions - nonprofit institutions(1.01)

SC <1 416 Summer Camps - nonprofit summer camps for children(0.01)

FBDP <1 32C Food Bank Demonstration Projects - food banks in high-need areas(0.01)

DF 1 32C Disaster Feeding - food provided to or used to prepare meals for disaster (0.16) victims

1Numbers in parentheses show percent of total food spending accounted for by the program.

Sections 4A and 17 refer to those sections in theAgriculture and Consumer Protection Act of 1973.This law authorizes the Food Distribution Program onIndian Reservations and the Commodity SupplementalFood Program. Each distributes food packages; about115,000 people participate in the first, and about400,000 in the second. These programs received thesecond and third largest amounts spent for commodityand product in fiscal 1996, over $120 million.

Two programs were authorized through the HungerPrevention Act of 1988. Section 104 authorizes USDAto distribute surplus commodities to needy individualsor households, while Section 110 authorizes USDA topurchase and distribute commodities and food productsto soup kitchens and food banks.

Section 416 of the Agricultural Adjustment Act of 1949authorizes the Commodity Credit Corporation (CCC) tomake available CCC-owned commodities for distribu-tion. FSA administers the CCC�a public corporationthat supports the prices of commodities through nonre-course commodity loans and manages commoditiesacquired by the agency. The commodities providedunder Section 416 may be in private stocks or in publicstocks that were acquired through forfeiture of nonre-course commodity loans. Commodities donated underthis legislation are known as bonus commodities, and

may be used in any of these programs.

Section 32C also refers to Section 32 in the AgriculturalAdjustment Act of 1935. Section 32C funds are fundsset aside by the Secretary for use in extreme surplus orto provide for disaster relief. These funds also comefrom customs receipts, and may also be used in any ofthe other programs in table 3-1. They are the primarysource for the Food Demonstration Projects andDisaster Feeding Programs. Section 32C funds areused primarily for purchasing and distributing AMScommodities.

Program Expenditures

FSA and AMS purchase different products. AMS isresponsible for purchasing �Group A� commodities,which include poultry, red meat, fish, eggs, and freshand processed fruits and vegetables. FSA purchases�Group B� commodities, which include dairy products(primarily cheese but also including butter and evapo-rated milk), grain-based products (such as wheat flour,corn products, pasta and ready-to-eat cereal), peanutproducts, honey, vegetable oil, rice, and infant formula.Most Group B products are derived from agriculturalproducts that are or have been subject to agriculturalsupport programs also administered by FSA.

Food Procurement by Farm Service Agency / AER-766 USDA-ERS / 11

Million dollars

Total

Group A

Group B

1979 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 960

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2,200

Figure 1

USDA food purchases for domestic feeding programs, 1979-96

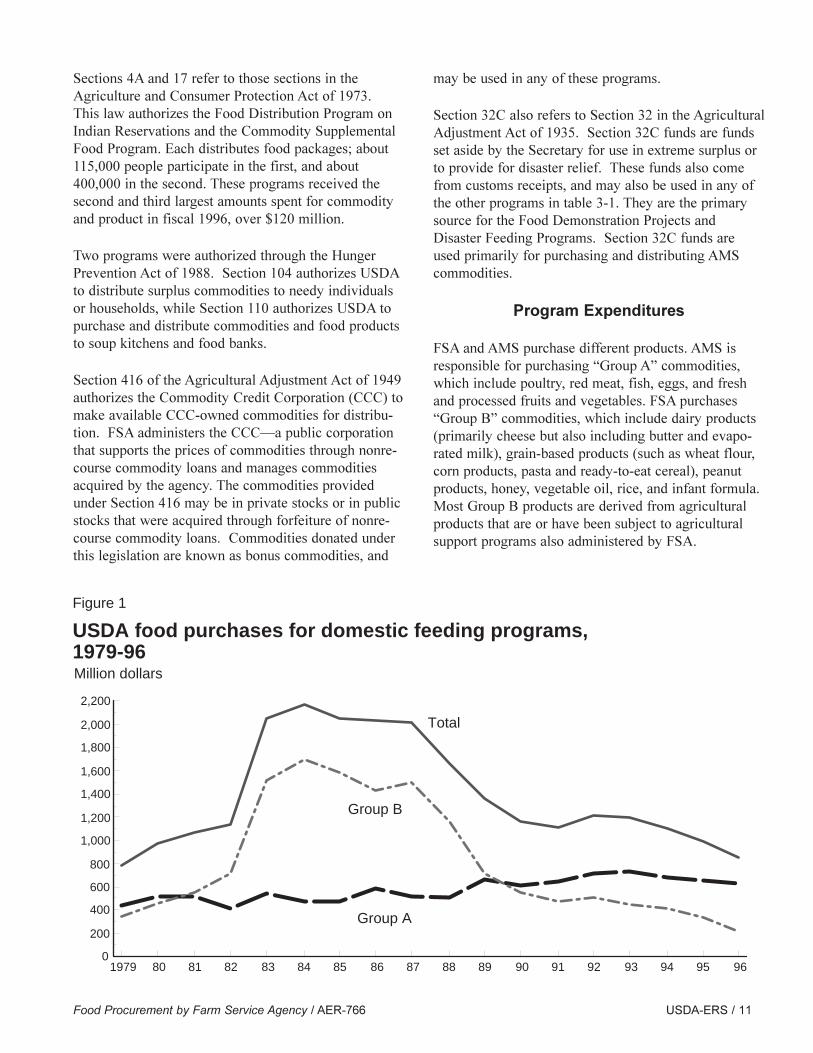

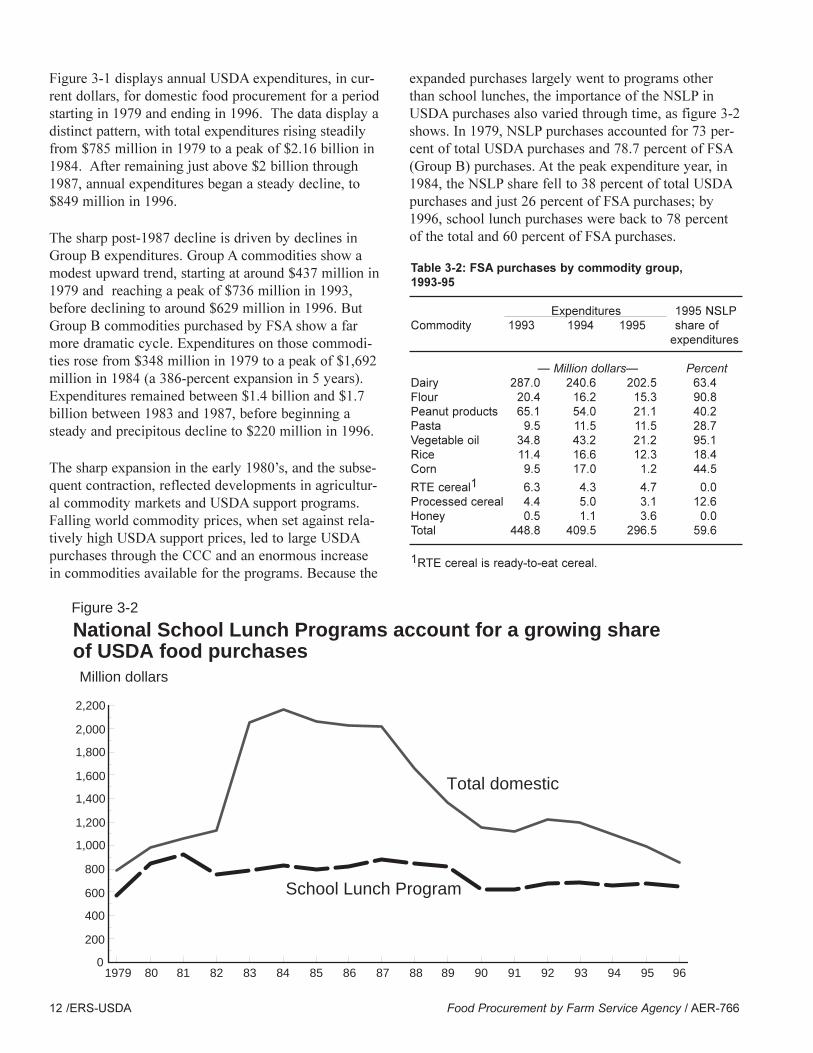

Figure 3-1 displays annual USDA expenditures, in cur-rent dollars, for domestic food procurement for a periodstarting in 1979 and ending in 1996. The data display adistinct pattern, with total expenditures rising steadilyfrom $785 million in 1979 to a peak of $2.16 billion in1984. After remaining just above $2 billion through1987, annual expenditures began a steady decline, to$849 million in 1996.

The sharp post-1987 decline is driven by declines inGroup B expenditures. Group A commodities show amodest upward trend, starting at around $437 million in1979 and reaching a peak of $736 million in 1993,before declining to around $629 million in 1996. ButGroup B commodities purchased by FSA show a farmore dramatic cycle. Expenditures on those commodi-ties rose from $348 million in 1979 to a peak of $1,692million in 1984 (a 386-percent expansion in 5 years).Expenditures remained between $1.4 billion and $1.7billion between 1983 and 1987, before beginning asteady and precipitous decline to $220 million in 1996.

The sharp expansion in the early 1980�s, and the subse-quent contraction, reflected developments in agricultur-al commodity markets and USDA support programs.Falling world commodity prices, when set against rela-tively high USDA support prices, led to large USDApurchases through the CCC and an enormous increasein commodities available for the programs. Because the

expanded purchases largely went to programs otherthan school lunches, the importance of the NSLP inUSDA purchases also varied through time, as figure 3-2shows. In 1979, NSLP purchases accounted for 73 per-cent of total USDA purchases and 78.7 percent of FSA(Group B) purchases. At the peak expenditure year, in1984, the NSLP share fell to 38 percent of total USDApurchases and just 26 percent of FSA purchases; by1996, school lunch purchases were back to 78 percentof the total and 60 percent of FSA purchases.

12 /ERS-USDA Food Procurement by Farm Service Agency / AER-766

National School Lunch Programs account for a growing share of USDA food purchases

1979 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 960

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2,200

Million dollars

Total domestic

School Lunch Program

Figure 3-2

Table 3-2: FSA purchases by commodity group, 1993-95

Expenditures 1995 NSLPCommodity 1993 1994 1995 share of

expenditures

� Million dollars� PercentDairy 287.0 240.6 202.5 63.4 Flour 20.4 16.2 15.3 90.8 Peanut products 65.1 54.0 21.1 40.2 Pasta 9.5 11.5 11.5 28.7 Vegetable oil 34.8 43.2 21.2 95.1 Rice 11.4 16.6 12.3 18.4 Corn 9.5 17.0 1.2 44.5

RTE cereal1 6.3 4.3 4.7 0.0 Processed cereal 4.4 5.0 3.1 12.6 Honey 0.5 1.1 3.6 0.0 Total 448.8 409.5 296.5 59.6

1RTE cereal is ready-to-eat cereal.

At present, FSA purchases of Group B commodities areincreasingly concentrated on one major program, andare also concentrated on a major commodity group.Table 3-2 shows that dairy purchases now account forover 68 percent of FSA purchases, and for nearly two-thirds of the agency�s NSLP purchases. In turn, cheeseaccounts for the major share of dairy purchases.

U.S. agricultural policy, as set in 1996 farm legislation,has moved away from a reliance on price supports forprogram commodities. If that policy continues, thenprocurement of bonus commodities under Section 416legislation will become a less important driver ofUSDA procurement. In turn, annual entitlement appro-priations will become more important, and the NSLPwill continue to be the primary recipient of USDAfoods.

Food Procurement by Farm Service Agency / AER-766 USDA-ERS / 13

Introduction

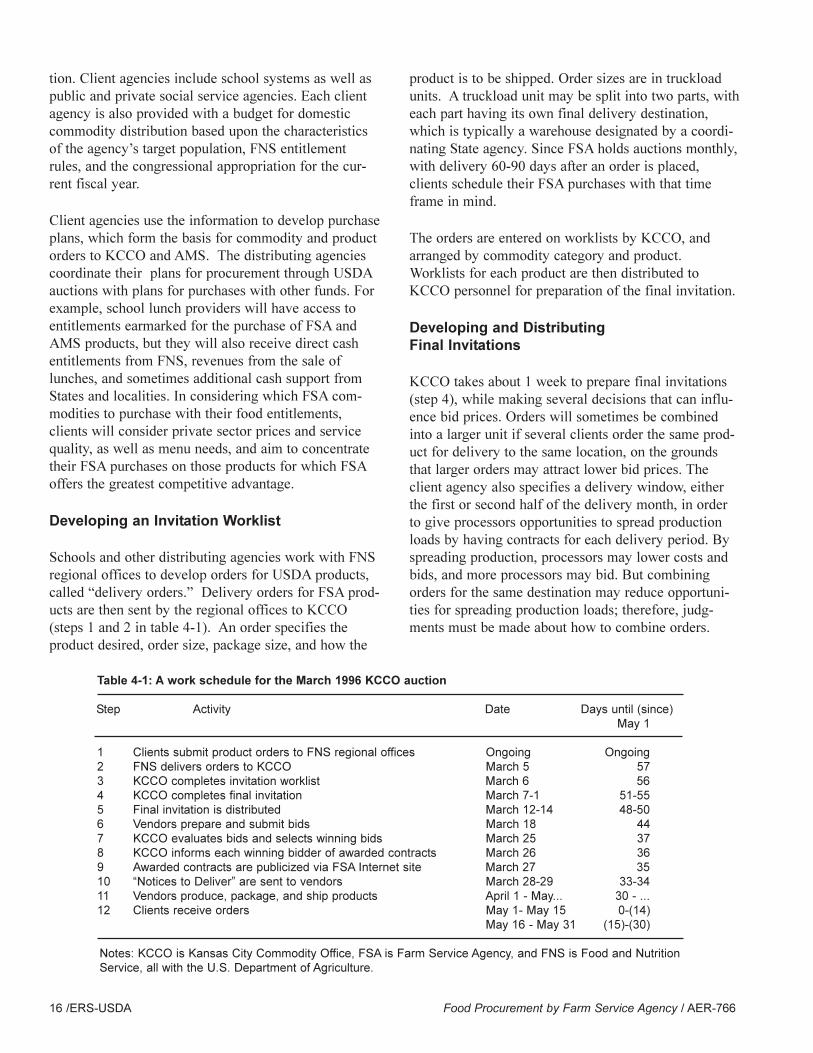

To understand the issues involved in structuring FSAauctions, one needs to understand how the existingprocess works. This chapter describes the stepsinvolved in administering an FSA auction, using as anexample an auction held by FSA�s Kansas CityCommodity Office (KCCO) in late March 1996 forproducts to be delivered to distributing agencies duringMay 1996. That auction is representative of most FSAauctions, but, at the close of the chapter, we discussrecent auction changes for some commodities.

Table 4-1 summarizes the auction; column 2 defines thekey steps in the auction, while column 3 lists the asso-ciated dates. Column 4 lists the time remaining, at eachstep, until the beginning of the delivery month (May 1,in this case). Auctions for other months frequently haveslightly different days of the month for the procurementactivities, but essentially the same time remaining, afteraccounting for weekends and holidays, until the begin-ning of the delivery month. In a typical auction, KCCOaims to schedule dates for each step by working back-ward from the beginning of the delivery month. Forexample, KCCO aims to receive bids and select andinform auction winners during a period that is typically5 to 6 weeks prior to the opening of the delivery month.Actual deliveries can be scheduled for two periods�thefirst or second half of the delivery month.

KCCO aims to prepare final invitations about 8 weeks(55 days) before the beginning of a delivery month. A

final invitation is FSA�s notice of intent to purchaseproducts, and is sent to vendors and the trade; it is a listof the tendered contracts for purchasing products. The55-day span reflects auction experience: a shorter spanwould result in more failures to complete the remainingsteps on time and could increase the cost of completingthese activities.

FSA excludes product orders that do not arrive by thedeadline. Excluded orders may sometimes be includedin a special supplemental invitation and auction, withdelivery in the same month as the current auction.Otherwise, late orders are held for the next month�sauction.

A supplemental auction includes all the steps in otherauctions, but with the time until the beginning of thedelivery month compressed for steps 4 through 11.Generally, deliveries for a supplemental auction are inthe latter half of the delivery month to ease the schedul-ing problems caused by missing the 55-day deadline.The current or regular auction has deliveries in both thefirst and second halves of the delivery month.

The FSA Auction Process

Information and Client Planning

USDA�s Food and Nutrition Service (FNS) providesclient agencies with a list of products that can beobtained from FSA and AMS auctions along with theirexpected prices, based on experience and forecast infla-

Food Procurement by Farm Service Agency / AER-766 USDA-ERS / 15

CHAPTER 4

FSA PROCUREMENT AUCTIONS: HOW THE PROCESS WORKS

tion. Client agencies include school systems as well aspublic and private social service agencies. Each clientagency is also provided with a budget for domesticcommodity distribution based upon the characteristicsof the agency�s target population, FNS entitlementrules, and the congressional appropriation for the cur-rent fiscal year.

Client agencies use the information to develop purchaseplans, which form the basis for commodity and productorders to KCCO and AMS. The distributing agenciescoordinate their plans for procurement through USDAauctions with plans for purchases with other funds. Forexample, school lunch providers will have access toentitlements earmarked for the purchase of FSA andAMS products, but they will also receive direct cashentitlements from FNS, revenues from the sale oflunches, and sometimes additional cash support fromStates and localities. In considering which FSA com-modities to purchase with their food entitlements,clients will consider private sector prices and servicequality, as well as menu needs, and aim to concentratetheir FSA purchases on those products for which FSAoffers the greatest competitive advantage.

Developing an Invitation Worklist

Schools and other distributing agencies work with FNSregional offices to develop orders for USDA products,called �delivery orders.� Delivery orders for FSA prod-ucts are then sent by the regional offices to KCCO(steps 1 and 2 in table 4-1). An order specifies theproduct desired, order size, package size, and how the

product is to be shipped. Order sizes are in truckloadunits. A truckload unit may be split into two parts, witheach part having its own final delivery destination,which is typically a warehouse designated by a coordi-nating State agency. Since FSA holds auctions monthly,with delivery 60-90 days after an order is placed,clients schedule their FSA purchases with that timeframe in mind.

The orders are entered on worklists by KCCO, andarranged by commodity category and product.Worklists for each product are then distributed toKCCO personnel for preparation of the final invitation.

Developing and Distributing Final Invitations

KCCO takes about 1 week to prepare final invitations(step 4), while making several decisions that can influ-ence bid prices. Orders will sometimes be combinedinto a larger unit if several clients order the same prod-uct for delivery to the same location, on the groundsthat larger orders may attract lower bid prices. Theclient agency also specifies a delivery window, eitherthe first or second half of the delivery month, in orderto give processors opportunities to spread productionloads by having contracts for each delivery period. Byspreading production, processors may lower costs andbids, and more processors may bid. But combiningorders for the same destination may reduce opportuni-ties for spreading production loads; therefore, judg-ments must be made about how to combine orders.

16 /ERS-USDA Food Procurement by Farm Service Agency / AER-766

Table 4-1: A work schedule for the March 1996 KCCO auction

Step Activity Date Days until (since) May 1

1 Clients submit product orders to FNS regional offices Ongoing Ongoing2 FNS delivers orders to KCCO March 5 573 KCCO completes invitation worklist March 6 564 KCCO completes final invitation March 7-1 51-555 Final invitation is distributed March 12-14 48-506 Vendors prepare and submit bids March 18 447 KCCO evaluates bids and selects winning bids March 25 378 KCCO informs each winning bidder of awarded contracts March 26 369 Awarded contracts are publicized via FSA Internet site March 27 3510 �Notices to Deliver� are sent to vendors March 28-29 33-3411 Vendors produce, package, and ship products April 1 - May... 30 - ...12 Clients receive orders May 1- May 15 0-(14)

May 16 - May 31 (15)-(30)

Notes: KCCO is Kansas City Commodity Office, FSA is Farm Service Agency, and FNS is Food and Nutrition Service, all with the U.S. Department of Agriculture.

Some orders are selected as small-business set asides.Set-aside contracts give qualified small businesses a 5percent bidding advantage; that is, the award will bemade to a small firm if its bid is no more than 5 percentgreater than the best bid.

A final invitation for a particular commodity group,such as flour, will often cover many specific orders.That is, it will separately list each delivery of a specificproduct, distinguished by package size and precisecharacteristics. For each product order, it will list a cityor town to which the product is to be delivered (some-times, two will be listed for a split load). The invitationwill specify the quantity being sought for each productand destination, and it will identify any specific trans-portation or distinctive packaging requirements.

KCCO solicits bids by sending the final invitation foreach commodity category to the appropriate vendors(step 5). The agency also publicizes the final invitationto the trade and to the public for each product throughmailings and through electronic postings on the Inter-net. After receiving the solicitation, vendors have about1 week to prepare their bids and return them to KCCO.

Bid Preparation and Selection

In preparing bids (step 6), vendors account for expectedcompetition as well as product costs. Costs include theexpected costs of processing, including labor, energy,and packaging materials, and also must reflect expectedprices for the agricultural commodities that will beprocessed into FSA products. Bidders are generallyfairly certain of future agricultural prices because bid-ding occurs only 1 to 6 weeks before processing andbecause many FSA products are based on agriculturalcommodities that have deep futures markets.

Bid prices are FOB destination at the warehouse andprocessor locations are specified by distributing agen-cies. Vendors pay transportation costs to receiving loca-tions and, therefore, account for likely transportationcosts when preparing bids. Bids also reflect distinctiveUSDA requirements, such as USDA labels, unusualpackaging or product standards, and inspections.

Finally, bidders consider likely capacity utilizationwhen preparing bids. Those who expect to have excesscapacity at the time of processing are likely to bidaggressively (low). Since they will need to pay capitaland other fixed costs whether they win the bid or not,

they will seek to win the bid as long as the revenuesfrom winning exceed only the additional variable costsassociated with filling an order. By contrast, firms thatexpect to be producing near full capacity will bid high-er; for a winning bid to be worthwhile, it will have toreturn more to the firm than the production that it sup-plants. In short, firms will be more likely to add�capacity charges� to the bid when they are alreadyproducing near full capacity.

A vendor can specify a total quantity restriction; that is,the vendor can be awarded contracts only up to therestriction quantity, even if the vendor is the low bidderon other contracts. In addition, a vendor may submit aminimum quantity restriction that specifies the lowestquantity of product the vendor is willing to supply. Theminimum restriction means that the vendor chooses notto be awarded any contracts if the total quantity won isless than the specified minimum.

Bids submitted by a vendor can vary among contracts,even among contracts for the same product to the samedestination. However, a vendor can bid only one pricefor an entire contract. Frequently, bidders submitrevised bids just before they are opened to reflect thelatest market information.

Bid Evaluation and Selection of Winners

KCCO opens all the bids at the same time (step 7). Norevised bids are accepted after the envelopes areopened. The bids are evaluated and winners are select-ed on the day the envelopes are opened so that vendorscan be notified the next day. Bids are binding contracts;selection of a winner obligates the winner to fulfill thecontract even before being notified.

The bid evaluation is complicated because of the mini-mum and maximum quantity restrictions and the 5-per-cent bidding advantage given to small businesses. Asearch procedure implemented on the KCCO computer,known as linear programming, is used to select thecombination of contract winners that yields the lowesttotal procurement costs while satisfying the restrictions.

Winning bids that are greater than a maximum purchase(constructed) price are reviewed. Constructed prices arebased on prior experience and expectations of inflation,and are developed by KCCO commodity analysts priorto bid evaluation. KCCO may decide to accept the bid,

Food Procurement by Farm Service Agency / AER-766 USDA-ERS / 17

or they may approach the winning bidder and attemptto get the bid reduced, or they may reject the bid andcancel the contract. Orders in canceled contracts maybe reintroduced in the next auction round, and thoseorders are delivered late to clients, or KCCO may issuea supplemental invitation to purchase the orders for thesame delivery period.

Announcement of Awards

Winning vendors are notified quickly, the day afterselection, since those who have not already purchasedmaterials (step 8) may consequently be placed in specu-lative positions. The price risks from these speculativepositions increase in direct proportion to the elapsedtime between bid submission and notification of con-tract awards. Winning bidders then have about 5-7weeks to fulfill contracts with delivery in the first halfof the delivery month, and about 7-9 weeks for con-tracts with delivery in the second half.

KCCO provides public notice of the auction results 2days after bid openings and evaluations (step 9). Theresults revealed include the price and winning bidder oneach contract. Releasing this information helps ensurethe public that the auction is competitive and providesvendors that did not win with information about howmuch they must lower their bids to win at the next auc-tion. It is important to release the information quicklybecause some losing bidders may have purchased mate-rials in anticipation of winning contracts, and quickrelease allows for easier reallocation of materials.Finally, quick public release via electronic means savesresources for FSA and KCCO; agency personnel nolonger have to respond directly to frequent requests forinformation.

Notices to Deliver

KCCO produces a document for each contract, calledthe Notice to Deliver, and sends it to the winning bid-der (step 10). The notice includes the product descrip-tion (for example, rice, milled U.S. No. 2 medium), aswell as the contract number, invitation number, deliveryorder number, commodity code, contract size, packagesize, and shipment mode. Notices also list the name,address, and telephone number of the vendor, the dis-tributing agency, and the designated agency personresponsible for receiving the product (the consignee).The notice to deliver provides the vendor with all theinformation necessary for fulfilling the contract.

Production and Shipping

The vendor produces the product and ships it to theconsignee (step 11). Contracts call for USDA inspectorsto be on site at the plant during production runs forUSDA commodities. Vendors must, therefore, arrangefor inspection by personnel from AMS (peanut anddairy products and salad dressing) or GIPSA (all otheritems), and must generally time production runs fortheir presence. For remote or small plants, this cansometimes lead to delays. Inspectors monitor produc-tion processes and may perform some onsite tests. Theycertify product type, quality (through lab tests), andweight, and also certify that packaging meets contractstandards for information, strength, and sanitaryrequirements. Most USDA products must be shippedwith USDA labels, instead of the processor�s normalbrands or private labels.

Contracts also require that product samples be sent toUSDA-approved labs for testing. Required tests varywith the product. For example, USDA aims for certainnutritional goals in cheese purchases, and also prefers aproduct that will melt properly when cooked, whilestretching across a pizza or hamburger. Precise lab testsfor cheese include tests of fat, moisture, salt, and acidcontent. Inspection procedures can also sometimes leadto delays, and products are sometimes shipped pendingreceipt of test results, at the vendor�s risk.

Delays are not always due to USDA inspection andtesting requirements. Sometimes processors will delib-erately delay production because an unexpected, morelucrative, order came in. USDA can impose fines forlate delivery, and can also suspend contracts for ven-dors that are chronically late. If USDA does not use thetools at its disposal, vendors can have strong incentivesfor late delivery, especially when vendors are producingnear full capacity.

Distribution

The vendor informs the distributing agency by fax thatthe product order is being shipped (step 12). This noti-fication must be given on the date the product isshipped. The trucker or a rail employee calls the con-signee, at least 24 hours prior to delivery, to scheduledelivery. FSA products are often shipped to a manufac-turing plant for further processing. For example, schooldistricts often use FSA entitlements to purchase flourand cheese, which are then shipped to nearby proces-

18 /ERS-USDA Food Procurement by Farm Service Agency / AER-766

sors who make them into frozen pizza or other morehighly processed foods.

Title to the product is transferred from vendor to dis-tributing agency at the receiving location when the con-signee signs for the product. At this stage, USDA�sresponsibility for product quality ends. The consignee isthen responsible for any further processing, as well asproduct transportation to client facilities and handling atdining facilities.

Recent Variants on the FSAAuction Process

FSA has altered the typical process in recent auctionsfor several commodities. The alterations affect the tim-ing of the auction process, the use of USDA labels, andthe reliance on USDA inspection.

Commercially labeled items in five product cate-gories�infant formula, evaporated milk, instant nonfatdry milk, ready-to-eat cereal, and rice cereal�are beingpurchased under a 5-year pilot program. The productsare purchased not for the school lunch program but fortwo smaller programs�the Commodity SupplementalFood Program (CSFP) and the Food DistributionProgram on Indian Reservations (FDPIR).

By purchasing commercially labeled products, vendorsmay supply USDA programs out of existing inventory,thus altering the production process outlined in step 11.Moreover, with commercial labels, FSA now relies onvendor certification of quality, since the vendor�s brandis on the package. As a result, USDA inspection (also instep 11) is forgone.

The process outlined in table 4-1 uses a series ofmonthly auctions to procure products to be delivered toclients 5-9 weeks after the selection of winning bids. In

infant formula, KCCO has lengthened the contract to afull year, while at the same time allowing commerciallabels on formula. Invitations now specify an indefinitequantity to be delivered throughout the year, instead ofspecifying precise quantities to be delivered to specificlocations each month. Contracts can be less precise ininfant formula because bids show no geographic varia-tion. Because of the longer contract duration, the vol-ume at bid is considerably larger, and KCCO hopes thatlarger volume will induce more competitive biddingamong the small number of manufacturers. Similarly,KCCO has lengthened contract durations for ready-to-eat cereal purchases as part of the experiment in pur-chasing commercially labeled products.

KCCO has altered the bidding process in another wayfor cheese purchases. It now issues rolling invitations,covering several months, for deliveries of cheese. Forexample, KCCO will issue an invitation in July to bidon deliveries of cheese in specified 2-week windowsfrom September through December. The August invita-tion will then include any new school orders forOctober through January deliveries. In essence, the newcheese process adds certain elements of flexibility:firms can now place bids further in the future than theydid under the prior system, and they can achieve morecertainty, in that they can commit to USDA productionfor a quarter of a year at a time instead of a month.Rolling contracts also provide KCCO with the opportu-nity to reject winning bids that are above constructedprices, and still deliver products on time.

Under the cheese experiment, KCCO enters orders asthey come in. Clients now have some reason to enterearly orders, since KCCO will act upon them. In addi-tion, KCCO can use rolling contracts to encourageclient agencies to shift the temporal pattern of theirorders, away from peak and toward off-peak periods, totake advantage of seasonal price fluctuations.

Food Procurement by Farm Service Agency / AER-766 USDA-ERS / 19

Introduction

FSA sets precise requirements for the commodities thatit buys for food assistance programs. Those require-ments include product specifications (such as nutrition-al guidelines), packaging and labeling standards, andrules for product testing and onsite product inspectionto ensure compliance with specifications. From thoseprocessors who are willing to offer products that meetFSA requirements, the agency then chooses vendors byusing a bidding process, as outlined in chapter 4, that isdesigned to use competition to purchase products at thelowest feasible prices.

When FSA chooses a specific bidding process, it makesseveral other choices. It specifies the timing of theprocess: FSA decides when invitations to bid will beannounced, when they will be closed, how quickly theaward will be made upon closure, and how quickly theproduct must be delivered upon award. In defining theaward and the bidding process, FSA also specifies anytransportation requirements, plans solicitation of poten-tial bidders, formulates procedures for aiding smallbusinesses, sets damages for noncompliance with awardrequirements, and sets policies for cancellation of aninvitation if bids appear to be noncompetitive.

Most awards are for precisely defined quantities (say,42,800 pounds) of a precisely defined product (all-pur-pose bleached wheat flour in 50-pound bags) to bedelivered to a precise location (a warehouse in Omaha,Nebraska) during a set time (between November 1 and

November 15). But in principle, the award could alsobe for the delivery of an indefinite quantity (with, forexample, a minimum of 1 million pounds and a maxi-mum of 25 million) throughout a year. In other words,FSA can also choose the duration and quantity of theaward at bid.

FSA acts on behalf of other clients, such as State dis-tributing agencies. When it designs the bidding process,FSA must also specify the timing that clients must fol-low to place orders. That is, client agencies must deliv-er food orders to FSA 55 days prior to the deliverymonth in order to be included in an invitation order toreceive delivery in a specified time window. FSA�s pol-icy choices for order, auction, and delivery timing ulti-mately drive one dimension of service quality�tempo-ral responsiveness to client orders.

These are all policy choices. FSA could choose otherproduct requirements or other auction designs; alterna-tive choices could affect processor costs, productprices, product quality, and FSA service quality. Actualchoices often can involve a tradeoff of a gain in onedimension of performance against a loss in another(McAfee and McMillan, 1987; Laffont and Tirole,1993; Wolfstetter, 1996). Key FSA decisions revolvearound four interlinked areas: product packaging andlabeling requirements, inspection requirements, the tim-ing of order, bid, and delivery stages, and the design ofprocurement auctions. We discuss the issues surround-ing these areas in this chapter, and begin by showingwhy we say these issues are interlinked.

Food Procurement by Farm Service Agency / AER-766 USDA-ERS / 21

CHAPTER 5

ISSUES IN USDA PROCUREMENT POLICIES

Labels Require Inspection: The Need for Quality Certification

in USDA Procurement

FSA food procurement procedures are not unique, butthey do differ in important ways from those used bycommercial buyers, as well as some other governmentagencies. For example, some private firms (such asnational fast food chains, retail supermarket firms, orwholesalers arranging for private-label products) willselect a small set of qualified suppliers through anintense search. Once selected, a qualified supplier willreceive a large volume of orders from the firm, at rela-tively profitable prices. Because the status of qualifiedsupplier is so important to a supplier�s profits, the sup-plier will have strong incentives to maintain agreed lev-els of quality and therefore to retain qualified supplierstatus. Firms using that procurement strategy, which isquite similar to prime vendor programs, trade off higherproduct prices to gain greater supplier efforts to main-tain product quality and to provide timely service.

FSA uses auctions to procure food commodities, andthe auctions are designed to get favorable prices forFSA clients by relying on price competition among bid-ders. That is, FSA does not form long-term relationswith suppliers. Moreover, FSA generally does not pur-chase products with commercial labels (that is, com-mon supermarket brands). Instead, USDA requires thatall USDA products be packaged according to specificUSDA directions and carry USDA labels. While theprocedure can generate strong price competition amongbidders, resulting in lower FSA costs, it also providesbidders with incentives to reduce their own costs bydelivering low-quality products. Since the products donot carry commercial labels, quality problems will notdamage the reputations of vendors� commerciallylabeled products; instead, USDA and its client agenciesbear the risks of poor product quality.

FSA aims to control those risks by setting precise prod-uct specifications, by requiring the presence of USDAinspectors on site during production of USDA products,and by performing laboratory tests of product samples,to ensure that delivered products adhere to contractspecifications. In short, FSA�s inspection requirementsfollow from the use of USDA labeling requirementsand a competitive bidding process.

Critics note four potential problems with current USDAproduct requirements. They may increase costs, both to