Food Innovation Trend & Beverage Market: Size and Growth by Segment, Global, 2014-2015 Speciality...

56

1 Food Innovation Trend –In collaboration with Intesa Sanpaolo Innovation Center– August 2016

Transcript of Food Innovation Trend & Beverage Market: Size and Growth by Segment, Global, 2014-2015 Speciality...

1

Food Innovation Trend–In collaboration with Intesa Sanpaolo Innovation Center–

August 2016

2

Context and Headlines (1/4)

• Frost & Sullivan breaks the Food & Beverage market out into three main segments which include

speciality ingredients, enabling technologies and processed products. In terms of their potential, health

ingredients and safety products are the two most attractive elements of the value chain with growth

rates of 8.5% and 7.5% (2014-2020) respectively

1. Health Ingredients: a) Proteins

• The protein ingredients for human nutrition market can be segmented according the feedstock from

which the proteins stem, with plant proteins representing 24% and animal 76% of the total in unit terms

in 2014. Globally, the market was valued at $28.37 billion in 2014 and will expand to reach $42.99

billion by 2020, a 7.2% CAGR

• End-users’ focus on health and fitness is driving demand for functional foods, meat analogues, sports

nutrition and subsequently proteins

• Overall, the supply side is highly fragmented with backwards vertical integration one of the key

characteristics that distinguishes top participants from smaller and emerging players in the space.

Nonetheless, there are leaders in specific product categories – Fronterra notably has a strong

presence in animal proteins and Cargill is similarly positioned on the plant side owing to its global

reach and access to raw materials

• Protein ingredients find their main application in foods & beverages but sports nutrition is a pillar of

growth and medical nutrition is emerging

• From a feedstock point of view, egg, soy, and dairy will continue to dominate the market, but novel

ingredient sources like algae and pea have been shaking up the space in recent years Frost & Sullivan

3

Context and Headlines (2/4)

o Whole Algae Protein in the US is an example of an young company which is developing innovative

algae-based “Alga Via” protein solutions

o Globally, 8.98 million MT of peas are produced annually but, once they have been cleaned, dried,

de-hulled, milled, fractionated and purified, this translates into 20.70 thousand MT of pea protein

ingredients. The rising demand for pea protein in existing and new food applications (e.g. medical

foods) will sustain utilization rates of around 90%

o The pea protein value chain is similar to that of other plant-based proteins with the main

stakeholders specialised in storage and processing. There is significant vertical integration between

pea processors, elevators and traders/brokers

o Frost & Sullivan finds that 67% of pea protein is retained from a milled pea in the final concentrate

form, amounting to a 29% price mark-up

1. Health Ingredients: b) Omega-3

• The Omega-3 ingredients market can be segmented according the source from which the fatty acids

stem, with microalgae oils representing 35%. Globally, the omega-3 market was valued at $1.83 billion

in 2014 and will expand to reach $2.88 billion by 2025, a 4.2% CAGR

• An increase in the number of reported health benefits backed by scientific findings is driving the

adoption of omega-3 but concerns about the sustainability and quality of the ingredients as well as

price volatility remain an issue

• Regulations governing omega-3 ingredients intended for human consumption are stringent and vary

across countriesFrost & Sullivan

4

Context and Headlines (3/4)

• The global omega-3 ingredients market is moderately competitive, but has areas of concentration

depending on the end-market application. Overall, the top 3 tier I companies, DSM, BASF and Wuxi

Xunda, account for 52% of the global market and consolidation is expected to continue

• From an application perspective, dietary supplements lead in terms of volume and revenue, but the

pet food industry is expected to grow at a CAGR of 5.3% due to the rapid and continued growth in pet

ownership across the globe

• On the technology side, US firm Ocean Omega has developed a micro-emulsion solution which

makes omega-3 available to fortify functional beverages. Sweden-based Simiris is working to farm

algae with a view to providing a safe and environmentally friendly alternative to the omega-3 oils

extracts which typically stem from wild fatty fish

2. Safety Products

• Globally, the food safety market was valued at $20.50 billion in 2015 and will expand to reach $29.73

billion by 2025, with double digit growth expected in the software, test kits & consumables and

systems & equipment categories

• The market is expanding rapidly due to a combination of macro and micro factors on the demand

and supply side with regulation is creating challenges but also opportunities to transform the way in

which food safety is managed from a technology perspective

• Digital transformation in the sector is rooted in sustainable industry trends with particular progress

being made on leveraging electronic traceability, cloud-based and automation & robotics solutions

Frost & Sullivan

5

Context and Headlines (4/4)

3. Medical Foods

• Medical foods fall between pharmaceuticals and nutraceuticals and can be segmented into

prescription and non-prescription products. Globally, the medical foods market was valued at $9.36

billion in 2013 and will expand to reach $13.34 billion by 2018, a 7.3% CAGR

• Despite the robust growth and presence of strong underlying drivers, up-take of medical foods

faces supply and demand side challenges. Medical foods are notably tightly regulated, by the Food

and Drug Administration in the US and a European Commission Directive in the EU

• From a competitive point of view, the market is highly concentrated with Abbot, Nestle and Danone

leading the way in APAC and globally

• Diabetes, oncology and metabolic health are the most significant application areas, while immune and

cardiovascular promise high growth

Frost & Sullivan

6

Introduction

7

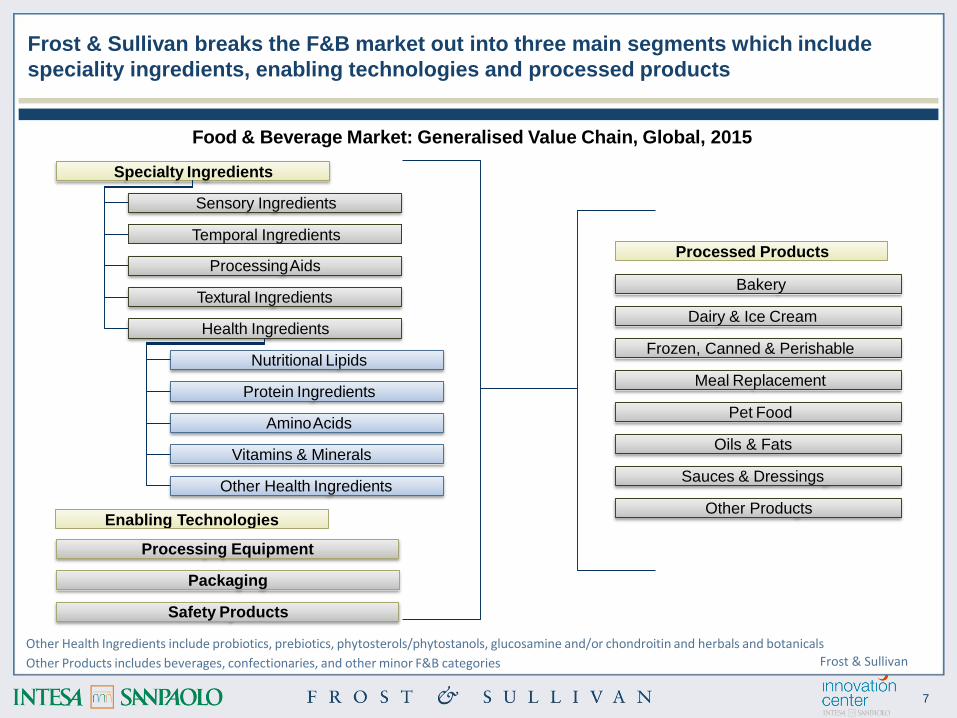

Frost & Sullivan breaks the F&B market out into three main segments which include

speciality ingredients, enabling technologies and processed products

Health Ingredients

Specialty Ingredients

ProcessingAids

Textural Ingredients

Other Health Ingredients

AminoAcids

Nutritional Lipids

Vitamins & Minerals

Protein Ingredients

Processing Equipment

Packaging

Safety Products

Meal Replacement

Pet Food

Oils & Fats

Sauces & Dressings

Bakery

Dairy & Ice Cream

Frozen, Canned & Perishable

Other Products

Other Health Ingredients include probiotics, prebiotics, phytosterols/phytostanols, glucosamine and/or chondroitin and herbals and botanicals

Other Products includes beverages, confectionaries, and other minor F&B categories

Food & Beverage Market: Generalised Value Chain, Global, 2015

Temporal Ingredients

Sensory Ingredients

Enabling Technologies

Processed Products

Frost & Sullivan

8

In terms of their growth potential, health ingredients and safety products are the two

most attractive elements of the value chain

9.0%

8.0%

7.0%

6.0%

5.0%

4.0%

3.0%

2.0%

1.0%

0.0%0.0 50.0 100.0 350.0

An

nu

al

Gro

wth

(20

14

–2015)

Safety

Products

Specialty

Ingredients

Packaging

150.0 200.0 250.0 300.0

All figures are rounded. Base year = 2014

Health

Ingredients

Food & Beverage Market: Size and Growth by Segment, Global, 2014-2015

Speciality Ingredients includes Health Ingredients

Processing

Equipment

Market Size, 2015 ($ Billion)

Frost & Sullivan

9

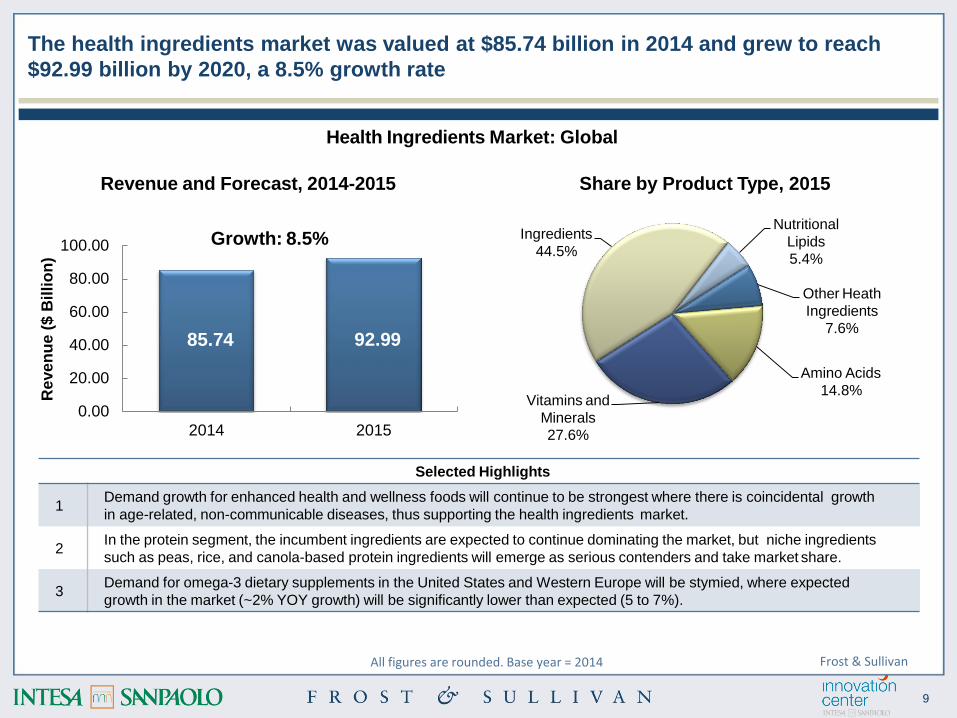

The health ingredients market was valued at $85.74 billion in 2014 and grew to reach

$92.99 billion by 2020, a 8.5% growth rate

Selected Highlights

1Demand growth for enhanced health and wellness foods will continue to be strongest where there is coincidental growth

in age-related, non-communicable diseases, thus supporting the health ingredients market.

2In the protein segment, the incumbent ingredients are expected to continue dominating the market, but niche ingredients

such as peas, rice, and canola-based protein ingredients will emerge as serious contenders and take market share.

3Demand for omega-3 dietary supplements in the United States and Western Europe will be stymied, where expected

growth in the market (~2% YOY growth) will be significantly lower than expected (5 to 7%).

Revenue and Forecast, 2014-2015

Growth: 8.5%

85.74 92.99

0.00

20.00

40.00

60.00

80.00

100.00

2014 2015

Re

ve

nu

e($

Bil

lio

n)

Nutritional

Lipids

5.4%

Other Heath

Ingredients

7.6%

Amino Acids

14.8%Vitamins and

Minerals

27.6%

Ingredients

44.5%

All figures are rounded. Base year = 2014

Health Ingredients Market: Global

Share by Product Type, 2015

Frost & Sullivan

10

The safety products market was valued at $15.53 billion in 2014 and grew to reach $16.69

billion by 2020, a 7.5% growth rate

Selected Highlights

1 Increasing demand for verifiable and assured food safety is growing worldwide.

2Disinfection equipment and food safety testing products are expected to see the greatest growth in demand through 2015

and 2016, relative to the other segments in this market.

3 On average, there are about 30 recalls per week in the United States in 2015.

Revenue and Forecast, 2014-2015

All figures are rounded. Base year = 2014

Safety Products Market: Global

Share by Product Type, 2015

15.53 16.6910.00

15.00

20.00

5.00

0.002014 2015

Re

ve

nu

e($

Bil

lio

n)

Growth: 7.5%PPE35%

Disenfect’ &

SanitiserChemicals

24%

Disenfect’ Equipment

10%

Safety Software

8%

Others23%

Frost & Sullivan

11

1. Health ingredients

12

Proteins

13

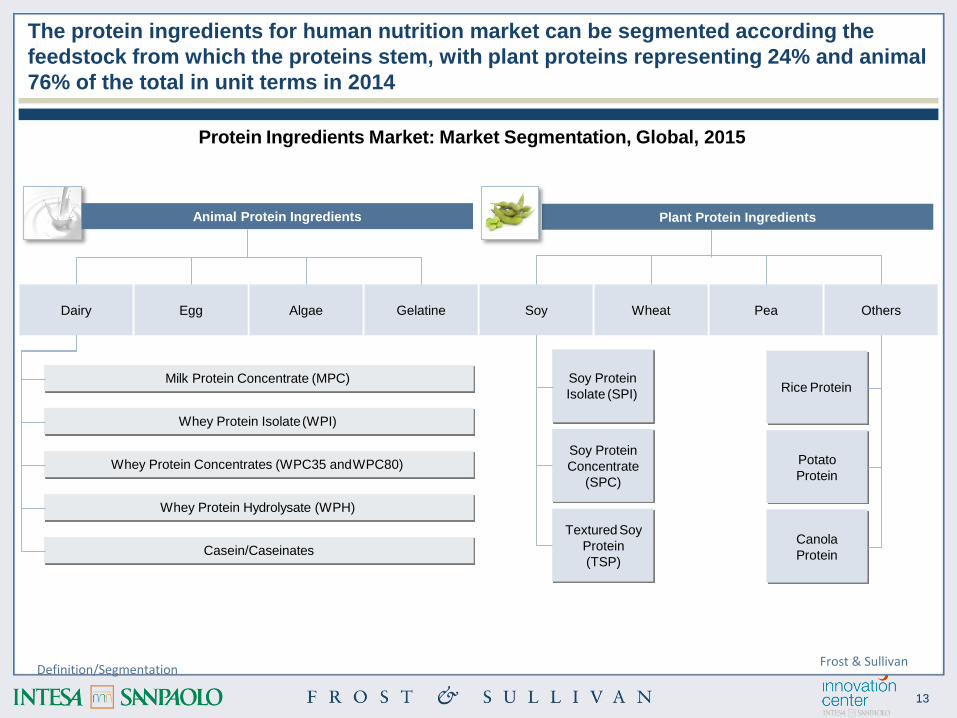

The protein ingredients for human nutrition market can be segmented according the

feedstock from which the proteins stem, with plant proteins representing 24% and animal

76% of the total in unit terms in 2014

Definition/Segmentation

Protein Ingredients Market: Market Segmentation, Global, 2015

Plant Protein Ingredients

Rice Protein

Potato

Protein

Canola

Protein

Soy Protein

Isolate (SPI)

Soy Protein

Concentrate

(SPC)

Textured Soy

Protein

(TSP)

Milk Protein Concentrate (MPC)

Whey Protein Isolate(WPI)

Whey Protein Concentrates (WPC35 andWPC80)

Whey Protein Hydrolysate (WPH)

Casein/Caseinates

Dairy Egg Algae Gelatine Soy Wheat Pea Others

Animal Protein Ingredients

Frost & Sullivan

14

Globally, the protein ingredients market was valued at $28.37 billion in 2014 and will

expand to reach $42.99 billion by 2020, a 7.2% CAGR

Market Analysis & ForecastAll figures are rounded. Base year = 2014

Protein Ingredients Market: Revenue Forecast, Global, 2014-2020

0.00

45.00

40.00

35.00

30.00

25.00

20.00

15.00

10.00

5.00

50.00

Plant Protein

2014

6.82

2015

7.25

2016

7.72

2017

8.21

2018

8.77

2019

9.38

2020

10.04

CAGR

(2014–2020)

6.7%

Animal Protein 21.55 22.96 24.52 26.27 28.24 30.45 32.95 7.3%

Reve

nu

e($

Bil

lio

n)

Frost & Sullivan

15

Drivers Short Mid Long

Rising End-user Focus on Health and Fitness Drive Protein Fortification of Foods H H H

Growing Demand for Functional Foods and Protein Supplements H H H

Increasing Shift Toward Vegetarianism Drives Market Growth for Meat Analogues M H H

Flourishing Sports Nutrition Market Drives Growth in the Proteins Market M M M

End-users’ focus on health and fitness is driving demand for functional foods, meat

analogues, sports nutrition and subsequently proteins

Market Trends

Protein Ingredients Market: Key Market Drivers and Restraints, North America, 2015–2020

Restraints Short Mid Long

Growth of Freedom Food Restrains the Wheat Gluten Market H H H

Concerns Over Animal and Bird Diseases Restrain Growth of Animal Proteins M M M

Flavour Challenges With High Protein Content Restrain Volume Usage of Proteins M M M

Anti-GMO Activism Restrain Growth of Plant Proteins L L L

Frost & Sullivan

16

Overall, the protein ingredients market is highly fragmented with backwards vertical

integration one of the key characteristics that distinguishes top participants from smaller

and emerging players in the space

Key Players & Forecast

Protein Ingredients Market: Competitive Structure, Global, 2015

Number of Companies in the Market >100

Competitive Factors

Product innovations, supply chain efficiency, application

diversity, multi-product presence, supply security, monitoring

consumer trends

Key End-user Groups Dairy, baked goods, processed food (dry goods), beverages

Major Market Participants

(selected)

ADM, Arla Foods, Cargill, DuPont/Solae, Fonterra, Friesland

Campina, Glanbia Nutritionals, Hilmar Ingredients, Kerry

Ingredients, Roquette, Solbar Ingredients

Market Share of Top 3 Competitors >30% in revenue terms

Emerging Market Participants

(selected)

Arnhem Group, Ballas Egg Products, California Natural

Products, Delta Protein, Erie Foods International, Marron

Foods, MGP Ingredients, World Food Processing

Frost & Sullivan

17

Nonetheless, there are leaders in specific productcategories; Fronterra notably has a

strong presence in animal proteins and Cargill is similarly positioned on the plant side

owing to their global reach and access to raw materials

Key Players & Forecast

Protein Ingredients Market: Competitive Structure, Global, 2015

Animal

Dairy

Whey Protein

Bongards' Creameries, Davisco, Fonterra, Glanbia, Hilmar Cheese,

Leprino Foods Company, Protient

Milk Protein ConcentrateDavisco, Erie Foods, Fonterra, Glanbia, Idaho Food Products, Kerry

Group

Casein and Caseinates Arla Foods, DMV International, Fonterra, Glanbia, Kerry Group

Egg ProteinBallas Egg Products, Henningsen Foods, Michael Foods, Moark, Rose

Acre Farms, Sonstegard Foods

Algae Proteins Aurora Algae, Solazyme (Algavia)

Gelatin Gelita, Kraft Foods, PB Leiner, Rousselo, Nitta

Plant

Soy Protein Archer Daniels, Cargill, Dupont (Solae)

Wheat GlutenArcher Daniels, Cargill, Manildra Group, MGP Ingredients, Roquette,

Syral, White Energy

Pea ProteinAxiom Foods, Burcon Nutrascience, Farbest Brands, Nutri-Pea,

Roquette Frères,

Others Rice and Canola Protein Axiom Foods, Burcon Nutrascience, BioExx

Frost & Sullivan

18

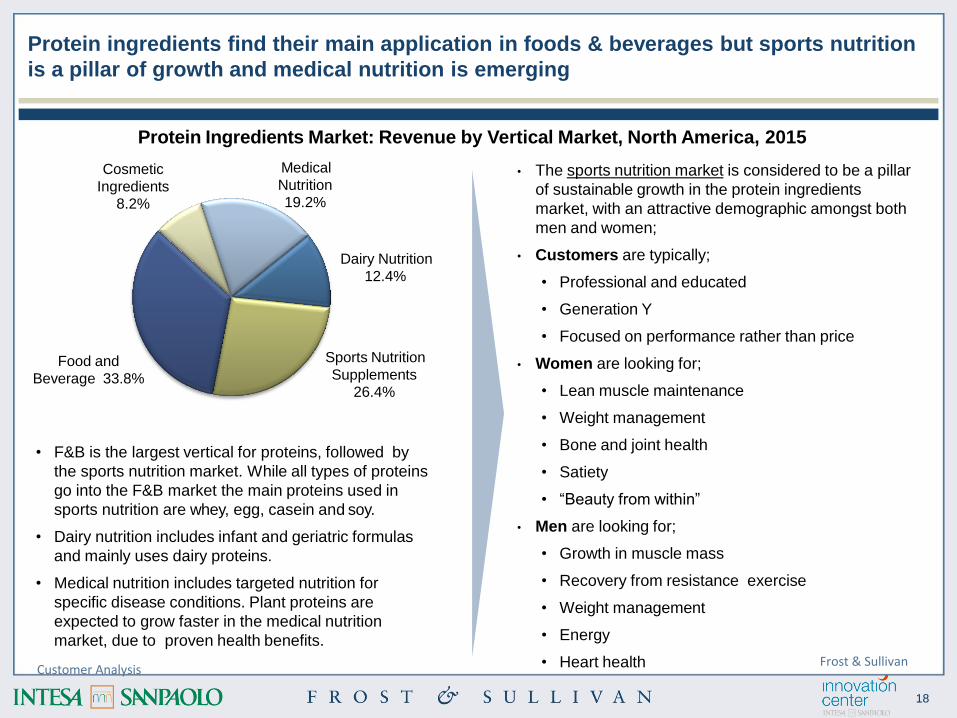

Protein ingredients find their main application in foods & beverages but sports nutrition

is a pillar of growth and medical nutrition is emerging

• The sports nutrition market is considered to be a pillar

of sustainable growth in the protein ingredients

market, with an attractive demographic amongst both

men and women;

• Customers are typically;

• Professional and educated

• Generation Y

• Focused on performance rather than price

• Women are looking for;

• Lean muscle maintenance

• Weight management

• Bone and joint health

• Satiety

• “Beauty from within”

• Men are looking for;

• Growth in muscle mass

• Recovery from resistance exercise

• Weight management

• Energy

• Heart health

Medical

Nutrition

19.2%

Cosmetic

Ingredients

8.2%

• F&B is the largest vertical for proteins, followed by

the sports nutrition market. While all types of proteins

go into the F&B market the main proteins used in

sports nutrition are whey, egg, casein and soy.

• Dairy nutrition includes infant and geriatric formulas

and mainly uses dairy proteins.

• Medical nutrition includes targeted nutrition for

specific disease conditions. Plant proteins are

expected to grow faster in the medical nutrition

market, due to proven health benefits.

Dairy Nutrition

12.4%

Sports Nutrition

Supplements

26.4%

Food and

Beverage 33.8%

Protein Ingredients Market: Revenue by Vertical Market, North America, 2015

Customer AnalysisFrost & Sullivan

19

From a feedstock point of view, egg, soy, and dairy will continue to dominate the

market, but novel ingredient sources like algae and pea have been shaking up the space

in recent years with growth in excess of 24% and 13%

Technology

30%

25%

20%

15%

10%

5%

0%0

2,000

4,000

6,000

8,000

Revenue CAGR

Reven

ue

($M

illio

n)

CA

GR

,2014–2020

(%)

0

5

10

15

20

10,000 25

Protein Ingredients Market: Revenue Forecast for Selected Proteins, Global, 2014-2020

All figures are rounded. Base year = 2014 Frost & Sullivan

20

Whole Algae Protein in the US is an example of an young company which is developing

innovative algae-based “Alga Via” protein solutions

Problem Statement

Innovation Attributes

Technology Profile

The production of animal protein is unsustainable at its current

rate due to a global population rise and the livestock farming

industry’s negative effects on the environment and public health.

The rising demand for alternative protein strongly influences

market shift from animal sources.

Consumers demand for vegan, non-allergenic, and non-

genetically modified (non-GM) sources of protein, which animal-

based protein could not fulfill.

Market Applications

Future Outlook

Algae cell wall helps limit protein interaction with other

ingredients, allowing easier formulation

Consists of 65% protein and is gluten-free

Contains high amino acids, lipids, fiber and micronutrients such

as lutein and zeaxanthin

Able to reduce fat and calorie content in formulations

Maintain favorable and delicious, nutty taste

Enhanced taste and texture, easily digestible

Indifferent tasting variant (developed through drying process

modification)

No beverage stabilizer is needed, allow fortifications

Steady in various temperatures and pH conditions

No formation of grittiness or extra viscosity on end products

Cater to a wide range of food preparations due to the oil, fiber

content, and micronized particles - a multifunctional food

ingredient

Highly adaptive to industrial applications

Target markets are the beverage industry, sports nutrition, and

sauce, snack, bread, and cereal products

Looking toward products that could enhance or replace

emulsifiers, fats, oils, polysaccharides, and oligosaccharides

Development of light-colored protein powder to improve end-

product physical appearance

In the production process, a native strain of the microalgae is thawed

and then inoculated in a flask filled with broth that is rich in simple

sugars and nutrients. The microalgae will then convert the simple

sugars into protein-rich whole food ingredients via fermentation. The

controlled variables are temperature, pH, agitation, and aeration. To

end the process, the fermentation broth is harvested, concentrated,

washed, dried, and milled into a fine powder. The use of a non-GM

sugar source for fermentation is done at the client’s request, but

only natural supplies such as corn, sugar beet, and sugarcane

dextrose are used for the process.

Whole Algae Protein, Frost & SullivanAlgae protein

21

8.98 Million

MT

Harvested Yellow Peas Production

North America produces 42% of the world’s yellow peas (3.67

million MT) and Canada accounts for 89% of North America’s

production.

94

Thousand

MT

1.62 Million

MT

Total Yellow Pea Protein Ingredients

24% of milled pea flour is attributed to pea protein. 46% of that

flour is a starch by-product. For starch processing, the same split

applies aftermilling.

Yellow Pea Product Processing

709 thousand MT is processed for flour, 394 thousand MT for

starch, and 512 thousand MT forprotein.

20.7

Thousand

MT

Dry Fractionated (DF) Yellow Pea Protein Ingredients

67% pea protein is retained from milling after fractionationand

purification. Solvents and/or additives are added, resulting in a final

product that ranges from 80% to 90% peaprotein.

Globally, 8.98 million MT of peas are produced annually but, once they have been

cleaned, dried, de-hulled, milled, fractionated and purified, this translates into 20.70

thousand MT of pea protein ingredients

Whole Yellow Pea and Pea Protein Ingredients Market: Percent of Harvested Peas Used inthe

Production of Value-added Pea Products, Global, 2014

Pea proteinFrost & Sullivan

22

0

20

40

60

80

0

5

10

15

20

Production Capacity

2008

17.9

2009

18.7

2010

19.9

2011

20.4

2012

20.7

2013

21.3

2014

23.5

Unit Shipment 14.3 14.9 16.2 17.8 17.7 18.6 20.7

Utilization 80 80 81 87 86 87 88

Uti

liza

tio

n (

%)

Pro

du

cti

on

Cap

ac

ity/U

nit

Sh

ipm

en

t(M

etr

ic T

on

s)

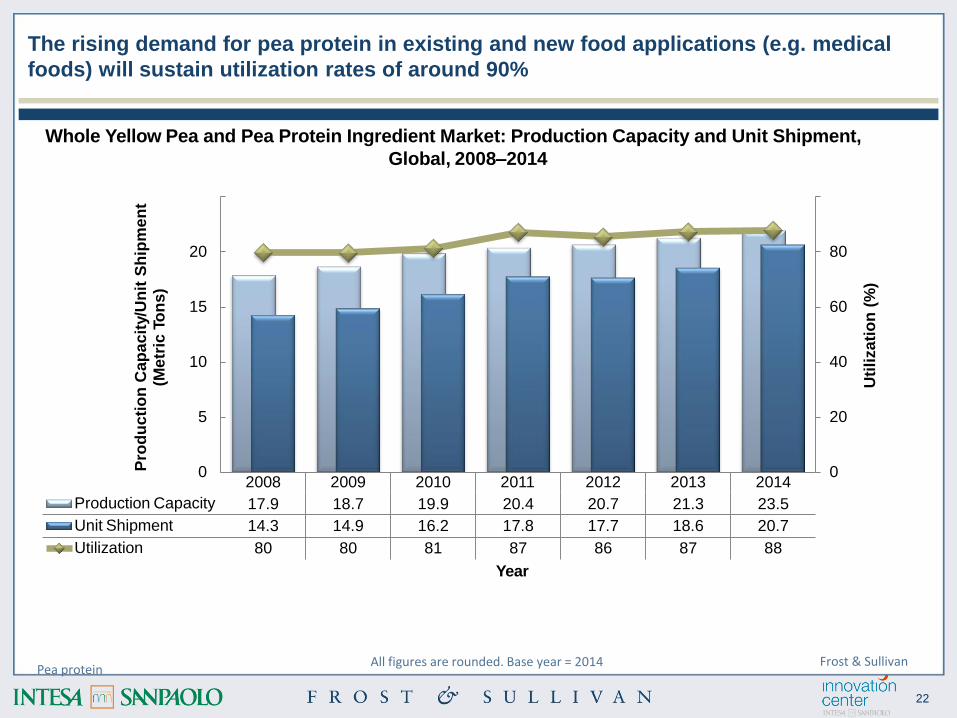

The rising demand for pea protein in existing and new food applications (e.g. medical

foods) will sustain utilization rates of around 90%

Year

Whole Yellow Pea and Pea Protein Ingredient Market: Production Capacity and Unit Shipment,

Global, 2008–2014

All figures are rounded. Base year = 2014Pea protein

Frost & Sullivan

23

End-user

IndustriesElevator

Whole

Yellow Pea

Crop Grower

Processor

Whole Yellow Pea and Pea Protein Ingredients Market: Industry Supply Chain, Global,2014

Pea and Food

Ingredient

Processor and

ManufacturerWholesale and

Retail

Distributors

The pea protein value chain is similar to that of other plant-based proteins with the main

stakeholders specialised in storage and processing

The market comprises a wide range of participants. It can be roughly grouped intothe

following classifications:

• Companies that specialize in storage: These purchase harvested peas directly from the grower or trader

and store the same in a holding facility.

• Companies that specialize in pea processing: These purchase harvested peas directly from a grower, a

pulse elevator, or a trader. The peas undergo various levels of processing, which is subject to the

company’s end markets.

• Companies that specialize in pea protein processing: These undertake pea milling and additional

processing activities, such as fractionating flour into protein, starch, fiber, andfat.

Pea proteinFrost & Sullivan

24

There is a significant level of vertical integration between pea processors, elevators

and traders/brokers whereas the pea ingredient processors, which develop the protein,

consist of a separate group of companies

• Pea processors purchase harvested peas directly from a grower and/or pulse elevator and/or

trader/broker. The peas undergo various levels of processing depending on the end market

• Examples include Besopke Group LLC, Columbia Grain International, Coop Ag Producers, Inc.,

Northwest Pea & Bean Co, George F. Brocke & Sons, Inc., Spokane Seed, Co, Legume Matrix,

Alliance Grain Traders, 3D Corporate Solutions, Legumex Walker, Inc. and Tumac Commodities

• Pea elevators purchase harvested peas directly from a grower and/or trader/broker and store them in a

holding facility. In some cases, these organizations are also processors and traders/brokers

• Examples include Bespoke Group LLC, Columbia Grain International, Cooperative Agricultural

Producers, Inc., Northwest Pea & Bean Company, George F. Brooke & Sons, Inc., Spokane Seed

Company, 3D Corporate Solutions, and Tumac Commodities

• Pea traders/brokers buy and sell harvested and/or processed peas and other pulses

• Example include Besopke Group LLC, Columbia Grain International, Legume Matrix, Alliance Grain

Traders, JM Grain, 3D Corporate Solutions, Bridgewell Resources LLC, California Exim, Inc.,

Commercial Lynks, Inc., Globeways, Inc., Legumex Walker, Inc., Maviga and Nexus Trading, Inc

• Pea ingredient processors undertake pea milling and additional processing activities, such as

fractionating flour into protein, starch, fiber, and fat. In some cases, this processor is a multi-purpose food

and feed ingredient processor and manufacturer

• Example include Meelunie America, Inc., Harvest Innovations, Zumbro River Brand, Inc., Roquette,

Nutri-Pea Limited, Axiom Foods, Inc., Burcon Nutrascience, Cosucra, and Alliance Grain Traders, and

a large number of Chinese and Asian-based pea protein ingredient processors.Pea protein

Frost & Sullivan

25

• Harvest

Harvested Peas

• Sorting

20% VAM

Clean and Dry Peas

•De-husking

•39% VAM

De-hulled Peas

•Milling

32% VAM

Milled Peas

• Fractionation• Concentration• Isolation

75% VAM

Pea Proteins

1.00 ton 0.77 ton

<0.12 ton

Pea Product by Relative Weight

Frost & Sullivan finds that 67% of pea protein is retained from a milled pea in the final

concentrate form, amounting to a 29% price mark-up

Whole Yellow Pea and Pea Protein Ingredients Market: Production Value Chain, Global,2014

Key: VAM=Value-added Markup

0.77 ton0.9 ton

Pea proteinFrost & Sullivan

26

Omega-3

27

Omega-3 Ingredients Market: Percent

Revenue by Ingredient Type, Global, 2014

30% Natural Fish/18:12 Oils

16.3%

50 to 55% Fish Oil Concentrates

4.0%60 to 70% Fish Oil

Concentrates 11.0%

75%+ Fish Oil Concentrates

13.0%

Krill Oils 7.1%

Microalgae Oils 34.8% Specialty Fish Oils

13.8%

The Omega-3 ingredients market can be segmented according the source from which the

fatty acids stem, with microalgae oils representing 35%

• Omega-3 Polyunsaturated Fatty Acids (PUFA)

continue to be one of the most researched and

scientifically proven functional ingredients in the

marketplace. Hundreds of scientific papers have

been published about Omega-3’s benefits to both

human and animal nutrition, which greatly

enhances the credibility of omega-3 as a vital

functional ingredient.

• The main sources of Omega-3 PUFAs are cold-

water marine fish and microalgae algae, which are

both rich in eicosapentaenoic acid (EPA),

docosahexaenoic acid (DHA), or both;

o 30% EPA+DHA Natural Fish/18:12 Oils

o 50 to 55% EPA+DHA Fish Oil Concentrates

o 60 to 70% EPA+DHA Fish Oil Concentrates

o 75%+ EPA+DHA Fish Oil Concentrates

o Krill oils

o Microalgae oils

o Specialty fish oils

All figures are rounded. Base year = 2014Definition/Segmentation

Frost & Sullivan

28

0

50

100

150

200

2503,500

3,000

2,500

2,000

1,500

1,000

500

Revenue CAGR (2014–2025) = 4.2%; Units CAGR (2014–2025) = 4.1%

0 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Revenue 1,766.1 1,809.5 1,830.8 1,958.8 2,089.9 2,221.2 2,343.6 2,451.7 2,546.5 2,632.9 2,711.0 2,778.5 2,834.1 2,878.2

Units 117 126 136 144 152 161 169 177 184 190 197 203 208 212

Un

its

('0

00

Metr

icT

on

s)

Rev

en

ue

($M

illio

n)

Year

Globally, the omega-3 market was valued at $1.83 billion in 2014 and will expand to reach

$2.88 billion by 2025, a 4.2% CAGR

Omega-3 Ingredients Market: Revenue Forecast, Global, 2014-2020

Market Analysis & ForecastAll figures are rounded. Base year = 2014 Frost & Sullivan

29

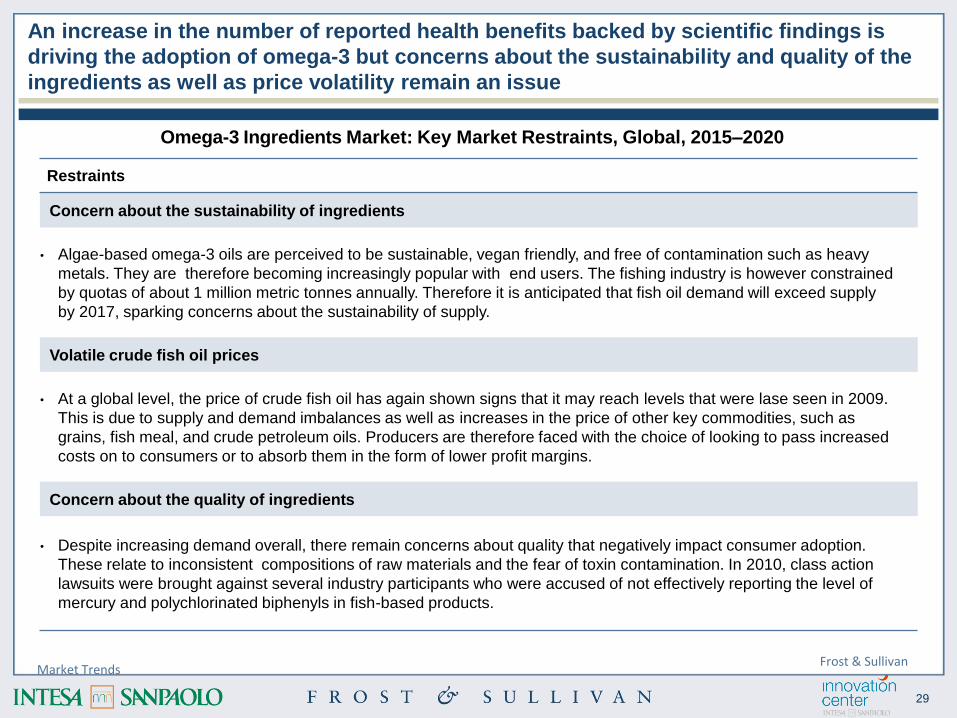

Restraints

Concern about the sustainability of ingredients

• Algae-based omega-3 oils are perceived to be sustainable, vegan friendly, and free of contamination such as heavy

metals. They are therefore becoming increasingly popular with end users. The fishing industry is however constrained

by quotas of about 1 million metric tonnes annually. Therefore it is anticipated that fish oil demand will exceed supply

by 2017, sparking concerns about the sustainability of supply.

Volatile crude fish oil prices

• At a global level, the price of crude fish oil has again shown signs that it may reach levels that were lase seen in 2009.

This is due to supply and demand imbalances as well as increases in the price of other key commodities, such as

grains, fish meal, and crude petroleum oils. Producers are therefore faced with the choice of looking to pass increased

costs on to consumers or to absorb them in the form of lower profit margins.

Concern about the quality of ingredients

• Despite increasing demand overall, there remain concerns about quality that negatively impact consumer adoption.

These relate to inconsistent compositions of raw materials and the fear of toxin contamination. In 2010, class action

lawsuits were brought against several industry participants who were accused of not effectively reporting the level of

mercury and polychlorinated biphenyls in fish-based products.

An increase in the number of reported health benefits backed by scientific findings is

driving the adoption of omega-3 but concerns about the sustainability and quality of the

ingredients as well as price volatility remain an issue

Market Trends

Omega-3 Ingredients Market: Key Market Restraints, Global, 2015–2020

Frost & Sullivan

30

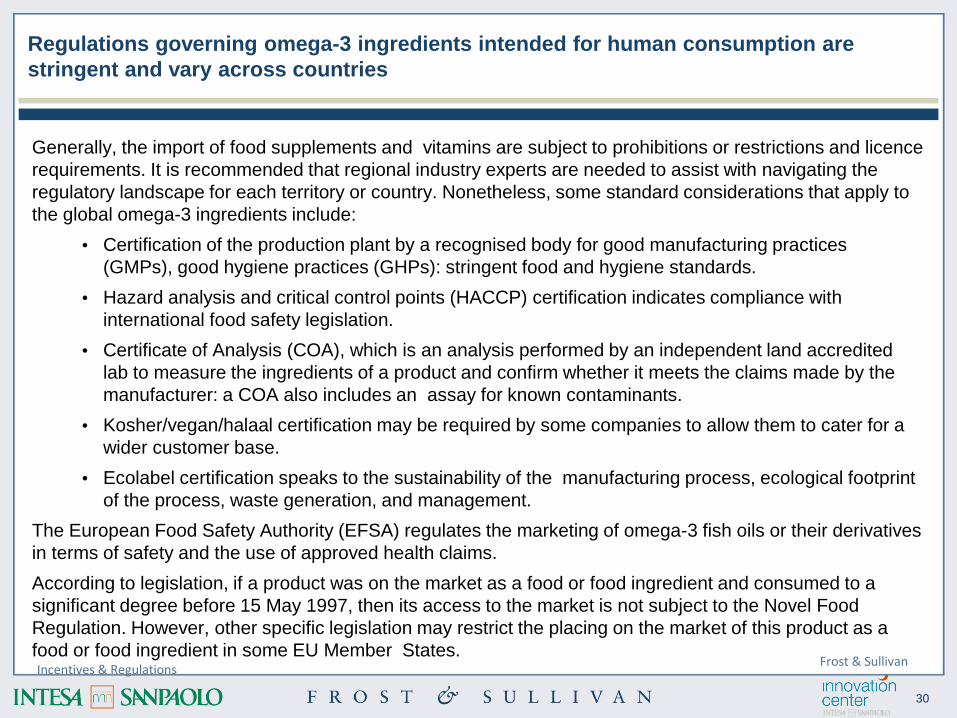

Regulations governing omega-3 ingredients intended for human consumption are

stringent and vary across countries

Generally, the import of food supplements and vitamins are subject to prohibitions or restrictions and licence

requirements. It is recommended that regional industry experts are needed to assist with navigating the

regulatory landscape for each territory or country. Nonetheless, some standard considerations that apply to

the global omega-3 ingredients include:

• Certification of the production plant by a recognised body for good manufacturing practices

(GMPs), good hygiene practices (GHPs): stringent food and hygiene standards.

• Hazard analysis and critical control points (HACCP) certification indicates compliance with

international food safety legislation.

• Certificate of Analysis (COA), which is an analysis performed by an independent land accredited

lab to measure the ingredients of a product and confirm whether it meets the claims made by the

manufacturer: a COA also includes an assay for known contaminants.

• Kosher/vegan/halaal certification may be required by some companies to allow them to cater for a

wider customer base.

• Ecolabel certification speaks to the sustainability of the manufacturing process, ecological footprint

of the process, waste generation, and management.

The European Food Safety Authority (EFSA) regulates the marketing of omega-3 fish oils or their derivatives

in terms of safety and the use of approved health claims.

According to legislation, if a product was on the market as a food or food ingredient and consumed to a

significant degree before 15 May 1997, then its access to the market is not subject to the Novel Food

Regulation. However, other specific legislation may restrict the placing on the market of this product as a

food or food ingredient in some EU Member States.Incentives & Regulations

Frost & Sullivan

31

The global omega-3 ingredients market is moderately competitive, but has areas of real

concentration depending on the end-market application

The omega-3 PUFA ingredients market is multi-layered. It starts with the raw material supplier. The actual

competition begins at the next level: the oil extractor or the PUFA ingredient supplier. At this stage, the PUFA

oil may be further refined depending on the specific needs of the manufacturer. PUFA ingredients are then

traded through distributors or regional offices to supplement or F&B manufacturers. Finally they reach the end

consumer via a number of PUFA-enriched products.

The market is continually facing competition from other nutritional ingredients. However, the wide range of

health benefits offered by PUFA ingredients is unmatched.

The challenge is to sustain popularity and consumer interest in omega-3 fatty acids.

A sustainable competitive advantage stems from having –

• a strong scientific focus in this industry

• third party certifiers (TPC) confirm that production processes and products conform to consumer

expectations and protects consumers from ambiguous product information. Standardization through

TPCs creates an barrier to entry for nonconforming competitors

The global omega-3 ingredients market (oil refiners) is moderately competitive, but has areas of extreme

market concentration depending on the end-market application. There are over 40 manufacturers (refiners)

active in this market. Frost & Sullivan expects the level of competition to increase thereby decreasing the

price of omega-3 products.

In November 2014, BASF sold its Brattvag plant in Norway to food industry supplier Marine Ingredients. The

sale confirms the anticipated industry shift from low concentration omega-3s to high concentrated

pharmaceutical grade products. Competitors in the high concentrates segment of the omega-3 market are

characterized by strong R&D capabilities, product differentiation, and regulatory know-how.Key Players & Forecast

Frost & Sullivan

32

Tier III and Other Companies

(5)24%

DSM (2)

23%

BASF(1)

20%

Products (China)

9%

GC Rieber Oils (Norway)

4%

Chemport (Korea)

3%

Clover

Corporation (4)

2%

FMC Corporation (3)

6%

Croda International (UK)

2%

Guangdong Runke Biological

Eng. Co. (China)2%

Hubei Fuxing Biotechnology

Co.,Ltd2%

Omega Protein Corporation

2%

Orkla Health (Norway)

1%Tier II Companies

18%

Wuxi Xunda Marine Biological

Notes:1) Includes Pronova BioPharma, Equateq, Callanish, and Cognis2) Includes Martek and Ocean Nutrition Canada3) Former Epax4) Former Nu-Mega5) Others include Axellus, Denomega, Lonza Group, Neptune Biotech, Omega Protein, Alltech, Rishon International Group, Seambiotic Ltd, Hubei YouzhiyouBiotechnology Co., Ltd, Shantou Runke Biological EngineeringCompany, and Wuhan Bioco Sci & Tech Dev Co.Ltd.

Overall, the top 3 tier I companies, DSM, BASF and Wuxi Xunda, account for 52% of the

global market and consolidation is expected to continue

Omega-3 Ingredients Market: Competitive Structure, Global, 2014

Key Players & ForecastFrost & Sullivan

33

Pet Food2.6%

Dietary Supplements

46.8%

Food & Beverage 10.9%

Infant Formula 26.9%

Pharmaceuticals 11.7%

Other End Markets 1.2%

End Application

2014

Revenue

($ Million)

Revenue

CAGR

(2014-2025)

2014 Units

(Metric Tons

000s)Units CAGR

(2014-2025)

Pet Food 46.7 5.3% 23.1 1.5%

Dietary

Supplements856.3 4.8% 82.4 4.6%

Food & Beverage 199.3 5.2% 18.5 5.4%

Infant Formula 493.0 1.8% 8.2 3.0%

Pharmaceuticals 22.1 5.6% 1.0 5.7%

Other End Markets 213.5 5.2% 2.3 4.3%

Total 1,830.8 4.2% 135.6 4.1%

From an application perspective, dietary supplements lead in terms of volume and

revenue, but the pet food industry is expected to grow at a CAGR of 5.3% due to rapid

and continued growth in pet ownership across the globe

Omega-3 Ingredients Market: Revenue by End Application, Global, 2014

All figures are rounded. Base year = 2014

Customer AnalysisOther end markets include personal care and other minor non-human nutrition applications

Frost & Sullivan

34

On the technology side, US firm Ocean Omega has developed a micro-emulsion solution

which makes omega-3 available to fortify functional beverages

1

2

Omega-3 has poor oxidative stability and variable

bioavailability, which limits its use in beverages.

Problem

StatementTech

Profile

Oceans Omega LLC has invented water‐soluble omega‐3 EPA

(eicosapentaenoic acid) and DHA (docosahexaenoic acid) ingredients

for the fortification of beverage products.

Oceans Omega LLC is located at Paramus, New Jersey, USA. It is a

wholly owned subsidiary of Mycell Technologies LLC.

The omega-3 micro-emulsion technology produces a stable emulsion

that decelerates the breakdown of nutritional content of omega-3 oil,

allowing for easy incorporation of omega-3 in beverages. The water-

soluble omega-3 emulsion has been commercialized as OTEC™

250CL-K and OTEC™ 300LDHA-S35.

Innovation

Attributes

pasteurization, cold-fill and

carbonation

Future

Plans

Omega Brands Corporation has purchased the omega-3 micro-

emulsion technology from Mycell Technologies LLC. It has entered into

a supply agreement with Oceans Omega LLC for distributing specialty

beverages fortified with Oceans Omega’s water-soluble omega-3

across North America and selected international markets.the finished product.

There is a need to address the low consumption of

omega-3 in the people’s daily diets, especially for

children and the elderly population.

Finished products are self-

stable underunrefrigerated

conditions

Incorporation of emulsion

through common beverage

manufacturing processes

such as hot-fill pasteurization,

cold-fill and carbonation

Emulsions are water- soluble

and highly translucent, thus

can fortify clear beverages

The omega-3 emulsion tastes

natural, is odorless, and has

no impact on the texture and

appearance on the finished

product.

Key Players & ForecastOceans Omega, Frost & Sullivan

35

Sweden-based Simiris is working to farm algae with a view to providing a safe and

environmentally friendly alternative to the omega-3 oils extracts which typically stem

from wild fatty fish

1

2

There are high levels of environmental toxins and

heavy metals in wild fatty fish.

Problem

StatementTech

Profile

The technology involves natural and prime processes starting with

farming, harvesting, and production. Algae are grown in photo-

bioreactors. The technology that is routinely used is both energy and

performance efficient in order to maintain the algae’s freshness. As a

result, algae nutrients can be reserved and protected.

The algae farm is located in Hammenhög, Sweden with 2,000 square

meters of greenhouses and laboratories

• Genetically modified organism (GMO)-free creation

• Free from solvent-based extractions

• Vegetarian omega-3 fatty acids

• Use of home-grown algae starter cultures

• No allergens

• Algae cultivation under supervised conditions

Innovation

Attributes

pasteurization, cold-fill and

carbonation

Future

Plans

• The improvement of the organoleptic property (taste) of omega-3 oil

• Microencapsulation of oil into powder

• Emulsification of algal oil for liquid application

• Estimated omega-3 EPA and DHA market growth to USD$2.7 billion

between 2014 and 2020 (at consumer level)the finished product.

The market is moving towards high-value,

sustainable, bioavailable and vegetarian omega-3s,

especially from highly concentrated algal oil.

Algae omega-3 oils DHA and

EPA extracts are

indistinguishable from high-fat

fish - In the food chain, algae

is a source of omega-3 for fish

Fish oil alternative - 100%

plant-based omega-3 fatty

acids

Algae are farmed in closed

system, greenhouses - Free

from environmental toxins,

controlled safety, and purity

Ecologically sustainable

omega-3 oil - Reduce

overfishing activities, maintain

natural ecology balance

Key Players & ForecastSimiris, Frost & Sullivan

36

2. Safety Products

37

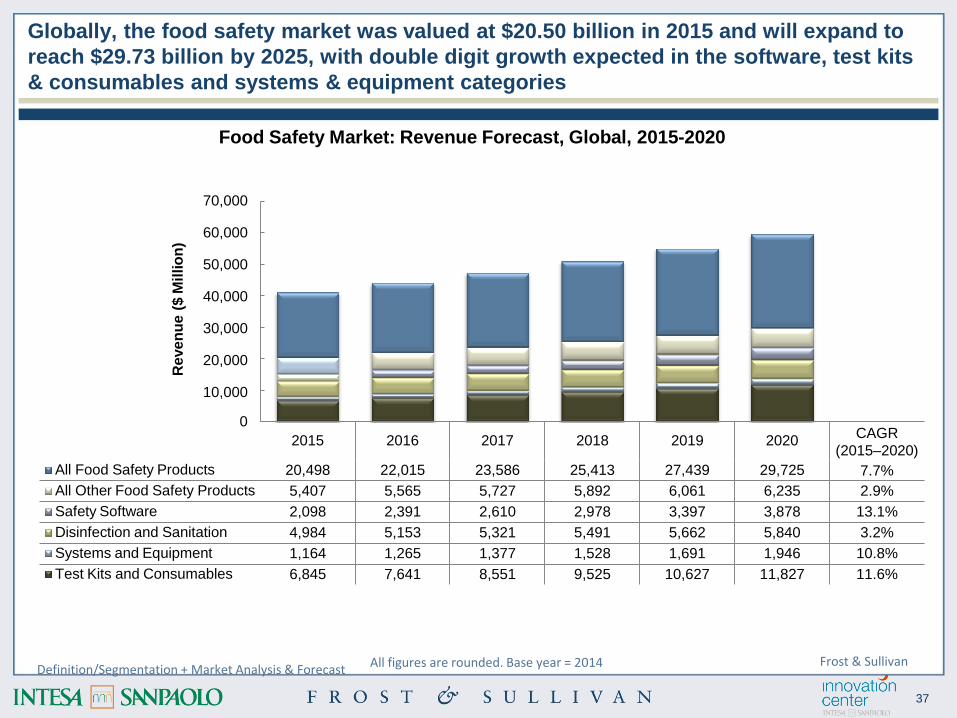

Globally, the food safety market was valued at $20.50 billion in 2015 and will expand to

reach $29.73 billion by 2025, with double digit growth expected in the software, test kits

& consumables and systems & equipment categories

Reven

ue

($M

illio

n)

0

All Food Safety Products

2015

20,498

2016

22,015

2017

23,586

2018

25,413

2019

27,439

2020

29,725

CAGR

(2015–2020)

7.7%

All Other Food Safety Products 5,407 5,565 5,727 5,892 6,061 6,235 2.9%

Safety Software 2,098 2,391 2,610 2,978 3,397 3,878 13.1%

Disinfection and Sanitation 4,984 5,153 5,321 5,491 5,662 5,840 3.2%

Systems and Equipment 1,164 1,265 1,377 1,528 1,691 1,946 10.8%

Test Kits and Consumables 6,845 7,641 8,551 9,525 10,627 11,827 11.6%

70,000

60,000

50,000

40,000

30,000

20,000

10,000

Food Safety Market: Revenue Forecast, Global, 2015-2020

All figures are rounded. Base year = 2014Definition/Segmentation + Market Analysis & Forecast

Frost & Sullivan

38

The market is expanding rapidly due to a combination of macro and micro factors on

both the demand and supply side

3Increasing volumes of data related to food safety (e.g., foodborne outbreaks, molecular

epidemiology) are being generated by government, industrial, and academic organizations, which

necessitates innovative enabling technologies to provide instantaneous and actionable insight.

4Research and development of rapid detection methods used for isolation, early detection, profiling,

and listing of pathogens and their metabolites in food safety diagnostics is stimulating the need

for higher efficiency of digital data management.

5Efficient software makes much-needed interoperability possible in the food & beverage industry,

and will increase the efficiencies of proactive monitoring for expired, spoiled, or tainted foods;

traceability; tracking; alerts; recalls; and corrective actions throughout the value chain.

The burden of food safety breaches is significant; consequently, the need for food security

solutions is only expected to increase. Demand will increase for enabling technologies that

address this challenge in the most cost-effective way possible.

1

2

Globalization and the demand for novel and exotic food have increased food safety concerns,

especially in a world with major differences in regulations and national enforcement. Demand is

growing for technologies that can track product and production information and share it across

regions and throughout the value chain.

Market TrendsFrost & Sullivan

39

Implementation

Challenges That

Should Be Addressed

Digitally

• Industry, government, and other external stakeholders have recognized the deficiency in the

US food safety system and have supported the passage of the FMSA, but implementation

challenges remain.

• While large companies are becoming digitalized, the FDA continues to require data to be

sent as scanned documents in PDF and fax formats.

• In general, the US food safety system has been relatively ineffective in ensuring the general

safety of the US food supply chain.

Food Safety

Management Systems

That Need Big Data

• The industry relies on food safety management systems—defined as the application of

processes and systems in a food business to prevent food-borne illness and to protect

consumer health. System objectives are to improve food safety, ensure consumer

protection, boost consumer confidence, improve efficiency throughout the supply chain,

benchmark parameters for food safety management, and provide an action plan to counter

problems.

• Food safety management systems active in the global food market include the Dutch

HACCP, International Organization for Standardization (ISO 22000), British Retail

Consortium (BRC), International Featured Standards (IFS), and Safe Quality Food Initiative

(SQF). Independent national and international standards also exist.

GFSI Calls For

Efficient Data

Management

• The Global Food Safety Initiative (GFSI) is a food safety trade standard organization founded

by large retailers including Carrefour, Tesco PLC, Metro AG, Migros, Royal Ahold, Walmart,

and Delhaize.

• GFSI’s vision is to have a standard that, once certified, is accepted everywhere.• Launched in 2000, the GFSI does not undertake any accreditation or certification activities.

Certification is based on BRC, IFS, and SQF food safety schemes.

Regulation is creating challenges but also opportunities to transform the way in which

food safety is managed from a technology perspective

Incentives & RegulationsFrost & Sullivan

40

Digital transformation in the sector is rooted in sustainable industry trends with

particular progress being made on leveraging electronic traceability, cloud-based and

automation & robotics solutions

Global Food

Trade/Imported

Foods

Demand for

Novel/Exotic

Foods

Need for Less-

Processed Foods

Harmonized

Food Safety

Information

Voluminous Data

on Outbreaks &

Epidemiology

Multiple Big Data

Banks

Diverse Big Data

at End Market &

Consumer Levels

Big Data

Analytics

Immunoassays

Biosensors

DNA-Based

Assays

Rapid

Detection

Methods

Expansion of

Software

Features

Interface with

Tracking &

Traceability

Cloud-Based

Technologies

Advanced Food

Safety Software

as a Service

Interventional

Technologies

Electronic

Traceability

Automation &

Robotics

Emerging

Technological

Innovations

Food Safety Market : Top 5 Trends, Global, 2015-2020

Enabling InfrastructureFrost & Sullivan

41

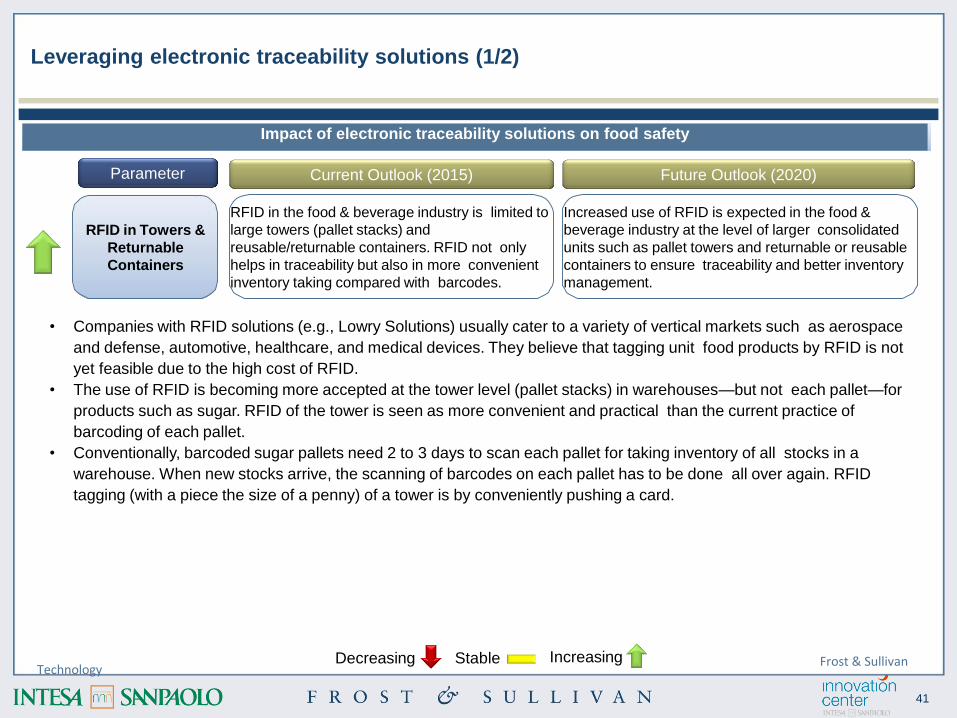

Leveraging electronic traceability solutions (1/2)

RFID in Towers &

Returnable

Containers

Parameter

RFID in the food & beverage industry is limited to

large towers (pallet stacks) and

reusable/returnable containers. RFID not only

helps in traceability but also in more convenient

inventory taking compared with barcodes.

Current Outlook (2015) Future Outlook (2020)

Increased use of RFID is expected in the food &

beverage industry at the level of larger consolidated

units such as pallet towers and returnable or reusable

containers to ensure traceability and better inventory

management.

Impact of electronic traceability solutions on food safety

IncreasingDecreasing StableTechnology

• Companies with RFID solutions (e.g., Lowry Solutions) usually cater to a variety of vertical markets such as aerospace

and defense, automotive, healthcare, and medical devices. They believe that tagging unit food products by RFID is not

yet feasible due to the high cost of RFID.

• The use of RFID is becoming more accepted at the tower level (pallet stacks) in warehouses—but not each pallet—for

products such as sugar. RFID of the tower is seen as more convenient and practical than the current practice of

barcoding of each pallet.

• Conventionally, barcoded sugar pallets need 2 to 3 days to scan each pallet for taking inventory of all stocks in a

warehouse. When new stocks arrive, the scanning of barcodes on each pallet has to be done all over again. RFID

tagging (with a piece the size of a penny) of a tower is by conveniently pushing a card.

Frost & Sullivan

42

Leveraging electronic traceability solutions (2/2)

Barcodes in

Packaged Foods

Parameter

Barcoding technologies interface with food

safety software, mainly at the packaged food

product manufacturing, logistics, and

retailing levels

Current Outlook (2015) Future Outlook (2020)

Barcode applications will increase in tune with

market expansion of food & beverage

manufacturing, warehousing, transportation, and

retailing (groceries and supermarkets) activities.

Impact of electronic traceability solutions on food safety

Technology

RFID in Food-

Allied Industries

RFID is becoming important in tracking of fishing

boats (tuna and shrimp) by the US government. It

is also likely to become more significant in the

traceability of food safety- related diagnostic kits

due to their high value and critical contents.

RFID is expected to become diverse in fishing boat

applications. Diagnostic kit suppliers for the food &

beverage industry will rely more on RFID for their

tracking and inventory management of expensive

materials that are also at risk of health and safety

breaches.

• Recent US regulations will require RFID or electronic tracking of fishing boats - private and corporate - that are used in

tuna and shrimp fishing. Information to be included are the ocean area in which the fish are caught, date, time, and

fishing boat details. Information must be reported to the government electronically (via document imaging) and

uploaded on a protected government Web site.

• According to companies with traceability software with barcode labeling compliance, barcode applications only start at

the level of downstream companies that manufacture packaged food products (e.g., Hershey’s, Kraft, Nestlé) that sell to

wholesalers such as Kroger, Walmart, or Costco that have larger staff, networks, and software for ERP, traceability, and

warehouse and inventory management.

IncreasingDecreasing Stable Frost & Sullivan

43

Leveraging cloud-based solutions (1/2)

Cloud-based Tech

for Large

Processors

Parameter

Cloud-based technologies are being accepted by

large international food processors for enterprise

resource planning (ERP), customer relationship

management (CRM), traceability, and food safety

management.

Current Outlook (2015) Future Outlook (2020)

Penetration of cloud-based technologies is expected

to expand at the level of global food & beverage

product manufacturers, while making strides in

company-owned system efficiencies of accuracy and

security.

Impact of cloud-based solutions on food safety

Technology

• Use of tablets and mobile devices is on the rise. Software providers with content and auditing products for preventing

food safety breaches and unwanted incidents, regulatory compliance, record keeping, and supply chain management

are upgrading their software interfacing with tablets, mobile devices, and cloud-based technologies.

• Large franchise operations with many locations globally can use mobile technologies to audit all locations

simultaneously and make prompt and meaningful decisions.

“These days, I would say, almost everybody is looking for it (cloud-based software). I think it's become fairly cost-effective

— lower capital expenditures, that kind of shifting things to your operating costs, as well as just the flexibility in an agility

that you have with cloud. First of all, if you’re running a global business, a global distributive basic business, or a

federated business like Nestlé, it allows you a true central repository, which is easily accessed. It also allows you the

ability to scale very easily. So, one area where you see quite a lot of success, not only in freedom beverages, but just

generally across our client base, is particularly in those federated-type businesses, because it allows us as a vendor to

be able to begin with smaller implementations or more concentrated implementations at a particular brand segment. And

then once we see success — joint success — we establish a partnership, and then we can cut across the remainder of

the organization.” — Provider of mainly environmental health and safety (EHS) software solutions for a variety of

industries (e.g., food & beverage, healthcare, oil & gas, automotive)

IncreasingDecreasing Stable Frost & Sullivan

44

Leveraging cloud-based solutions (2/2)

Cloud-based Tech

for Software

Providers

Parameter

Food software providers have mostly customized

their products to be compatible with cloud

platforms, with clients (especially large clients

with confidence in the security of their company-

owned servers) requesting this feature.

Current Outlook (2015) Future Outlook (2020)

Moving on from providing customized cloud-based

software for large clients with their own secure

servers, more food safety providers globally will

develop software that will be compatible with public

domains (e.g., Microsoft catering to the needs of small

to medium clients).

Impact of cloud-based solutions on food safety

Technology

• Updates in the form of dashboard graphs and summaries can be received in just 10 to 20 seconds from scores of

locations simultaneously (compared with conventional systems that can deliver information in a few hours, for one

location at a time).

• From a typical EHS software provider (e.g., Intelex) perspective, cloud-based systems have become pervasive. EHS

software is provided on a cloud-based platform since it has become cost-effective and efficient. Clients, especially large

companies with many locations, are demanding cloud-based EHS systems, and the provider is able to consider the

cloud in its software innovation.

• From the perspective of a food safety software specialist, cloud-based systems are here to stay and will grow in

application. Food safety software providers offer cloud systems in applications for seasonal businesses, large firms in

the United States, and large growers with fields that are scattered and sometimes remote. For example, farm-related

software systems run on iPads can be deployed in North America to fruit and vegetable fields. With cloud, the corporate

office is able to connect to workers with iPads, capture a lot of information from the fields during harvest and growing

cycles, and update it quickly.

IncreasingDecreasing Stable Frost & Sullivan

45

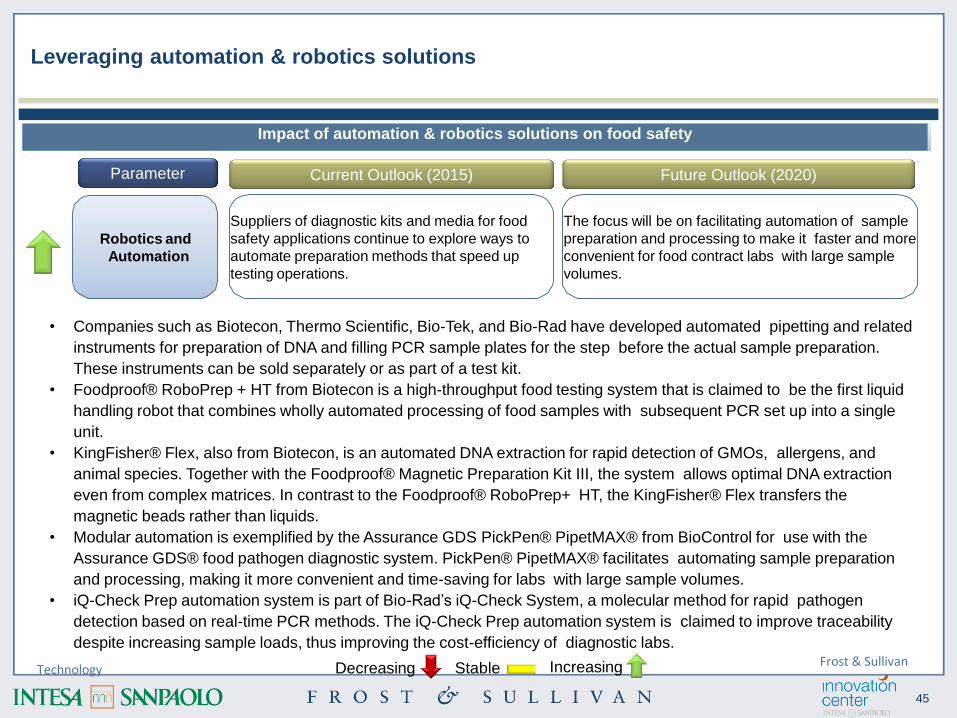

Leveraging automation & robotics solutions

Robotics and

Automation

Parameter

Suppliers of diagnostic kits and media for food

safety applications continue to explore ways to

automate preparation methods that speed up

testing operations.

Current Outlook (2015) Future Outlook (2020)

The focus will be on facilitating automation of sample

preparation and processing to make it faster and more

convenient for food contract labs with large sample

volumes.

Impact of automation & robotics solutions on food safety

Technology

• Companies such as Biotecon, Thermo Scientific, Bio-Tek, and Bio-Rad have developed automated pipetting and related

instruments for preparation of DNA and filling PCR sample plates for the step before the actual sample preparation.

These instruments can be sold separately or as part of a test kit.

• Foodproof® RoboPrep + HT from Biotecon is a high-throughput food testing system that is claimed to be the first liquid

handling robot that combines wholly automated processing of food samples with subsequent PCR set up into a single

unit.

• KingFisher® Flex, also from Biotecon, is an automated DNA extraction for rapid detection of GMOs, allergens, and

animal species. Together with the Foodproof® Magnetic Preparation Kit III, the system allows optimal DNA extraction

even from complex matrices. In contrast to the Foodproof® RoboPrep+ HT, the KingFisher® Flex transfers the

magnetic beads rather than liquids.

• Modular automation is exemplified by the Assurance GDS PickPen® PipetMAX® from BioControl for use with the

Assurance GDS® food pathogen diagnostic system. PickPen® PipetMAX® facilitates automating sample preparation

and processing, making it more convenient and time-saving for labs with large sample volumes.

• iQ-Check Prep automation system is part of Bio-Rad’s iQ-Check System, a molecular method for rapid pathogen

detection based on real-time PCR methods. The iQ-Check Prep automation system is claimed to improve traceability

despite increasing sample loads, thus improving the cost-efficiency of diagnostic labs.

IncreasingDecreasing StableFrost & Sullivan

46

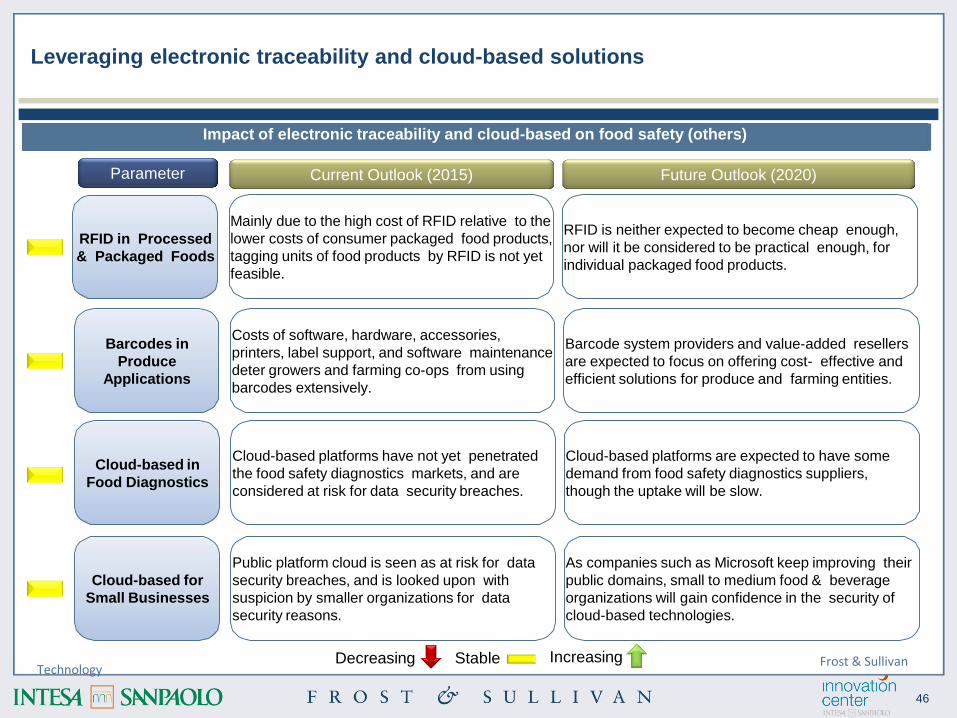

Leveraging electronic traceability and cloud-based solutions

RFID in Processed

& Packaged Foods

Cloud-based in

Food Diagnostics

Barcodes in

Produce

Applications

Parameter

Mainly due to the high cost of RFID relative to the

lower costs of consumer packaged food products,

tagging units of food products by RFID is not yet

feasible.

Cloud-based platforms have not yet penetrated

the food safety diagnostics markets, and are

considered at risk for data security breaches.

Costs of software, hardware, accessories,

printers, label support, and software maintenance

deter growers and farming co-ops from using

barcodes extensively.

Current Outlook (2015) Future Outlook (2020)

RFID is neither expected to become cheap enough,

nor will it be considered to be practical enough, for

individual packaged food products.

Cloud-based platforms are expected to have some

demand from food safety diagnostics suppliers,

though the uptake will be slow.

Barcode system providers and value-added resellers

are expected to focus on offering cost- effective and

efficient solutions for produce and farming entities.

Impact of electronic traceability and cloud-based on food safety (others)

Cloud-based for

Small Businesses

Public platform cloud is seen as at risk for data

security breaches, and is looked upon with

suspicion by smaller organizations for data

security reasons.

As companies such as Microsoft keep improving their

public domains, small to medium food & beverage

organizations will gain confidence in the security of

cloud-based technologies.

TechnologyIncreasingDecreasing Stable Frost & Sullivan

47

3. Medical Foods

48

Medical foods fall between pharmaceuticals and nutraceuticals and can be segmented

into prescription and non-prescription products

Definition/Segmentation

Medical Foods Market: Market Segmentation, Global, 2015

Pharmaceuticals

(Disease-specific)

Medical Foods

Nutraceuticals

(Address nutritional

requirements)

Prescription

Medical Foods

Non- prescription

Medical Foods

• Medical foods are essentially a product group wedged between pharmaceuticals and nutraceuticals.

• The only requirement for medical foods stipulated by the FDA is that the active ingredient be generally

recognized as safe (GRAS) and that the product be administered under medical supervision.

• This has paved the way for 2 sectors of medical foods;

• Prescription medical foods, more drug-like in nature, are administered in a capsule or tablet form and

are made available only in pharmacies and hospitals.

• Non-prescription medical foods, closer to nutraceuticals, are complete or partially complete nutrition

products available as concentrates or ready-to-consume formulations.

Frost & Sullivan

49

Globally, the medical foods market was valued at $9.36 billion in 2013 and will expand to

reach $13.34 billion by 2018, a 7.3% CAGR

Market Analysis & ForecastAll figures are rounded. Base year = 2013

Medical Foods Market: Revenue Forecast, Global, 2014-2018

5.0

6.0

7.0

8.0

9.0

10.0

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

Revenue

2013

9.36

2014

9.95

2015

10.61

2016

11.39

2017

12.30

2018

13.34

Growth Rate - 6.3 6.7 7.3 8.0 8.4

Gro

wth

Ra

te (

%)

Re

ve

nu

e($

Billi

on

)

Frost & Sullivan

50

Drivers Short Mid Long

Lifestyle Changes and R&D Resulting in Newer Disease Targets H H H

Improving Healthcare Systems and Life Expectancy M M M

Ageing World Population L L M

Despite the robust growth and presence of strong underlying drivers, up-take of medical

foods faces supply and demand side challenges

Market Trends

Medical Foods Market: Key Market Drivers and Restraints, Global, 2014-2018

Restraints Short Mid Long

Lack of Insurance Coverage for Medical Foods in Some Regions H H H

Low Physician Awareness of Medical Foods H H M

Poor Medical Adherence of the Regional Population M M M

High Level of Clinical Trials and Medical Evaluation Required L L L

Use of Alternative Medicine Hinders Adoption of Medical Foods L L L

Frost & Sullivan

51

Medical foods are quite tightly regulated, by the Food and Drug Administration in the US

and a European Commission Directive in the EU

Incentives & Regulations

No pre-market approval is needed for marketing medical foods. However, in the US, the FDA keeps a check

on all existing and new products in the market and sends out warnings to any spurious or wrongly defined

products. Under regulation 21 CFR 101.9(j)(8), the US FDA has established the criteria to clarify the statutory

definition of medical foods as outlined below.

• It is a specially formulated and processed product (as opposed to a naturally occurring foodstuff used in

its natural state) for the partial or exclusive feeding of a patient by means of oral intake or enteral feeding

by tube.

• It is intended for the dietary management of a patient who, because of therapeutic or chronic medical

needs, has limited or impaired capacity to ingest, digest, absorb, or metabolize ordinary foodstuffs or

certain nutrients, or who has other special medically determined nutrient requirements, the dietary

management of which cannot be achieved by the modification of the normal diet alone.

• It provides nutritional support specifically modified for the management of the unique nutrient needs that

result from the specific disease or condition, as determined by medical evaluation.

• It is intended to be used under medical supervision; and

• It is intended only for a patient receiving active and ongoing medical supervision, wherein the patient

requires medical care on a recurring basis for, among other things, instructions on the use of the medical

food.

In Europe, the European Commission Directive 1999/21/EC of 25 March 1999 on dietary foods for special

medical purposes (as amended by Directive 2006/141/EC) outlines specifications for medical foods.

Regulations for medical foods are still under development in other parts of the world.Frost & Sullivan

52

Diabetes

Health

Oncology

Health

Metabolic

Health

Digestive

Health

Immune

Health

Musculoskeletal

Health

Critical Care/

Trauma

Diabetes

Health

Oncology

Health

Metabolic

Health

Digestive

Health

Immune

Health

Musculoskeletal

Health

Critical Care/

Trauma

From a competitive point of view, the market is highly concentrated with Abbot, Nestle

and Danone leading the way in APAC and globally

Key Players & Forecast

Abbot (45-55% share in APAC)

Leading Brands Ensure®, Glucerna®, Vital®, Juven®

Nestle (18-22% share in APAC)

Leading Brands: DIABETISHIELD®, PEPTAMEN®, RENALCAL®

Danone (15-18% share in APAC)

Leading Brands: FortiFit®, Souvenaid®, Nutrison®

Others include Fresenius-Kabi, Mead Johnson, Kalbe, Nutrifood and Vinamilk

Medical Foods Market: Competitive Structure, Global, 2013

Diabetes

Health

Oncology

Health

Metabolic

Health

Digestive

Health

Immune

Health

Musculoskeletal

Health

Critical Care/

Trauma

Frost & Sullivan

53

Diabetes, oncology and metabolic health are the most significant application areas, while

immune and cardiovascular promise high growth

Medical Foods Market: Principal Applications, Global, 2013

Customer Analysis

Foods targeted for type 1 and type 2 diabetes mellitusDiabetes

Foods targeted at different types of cancerOncology

Foods for metabolic disorders such as in-born errors of metabolism, hypoglycemia, milk

protein intolerance, and chronic liver diseaseMetabolic

Foods targeted for malabsorption in gastrointestinal and renal diseases such as inflammatory

bowel disease, short bowel syndrome, leaky gut syndrome, dysphagia, renal disease, and

renal failure.

Digestive

Foods for bone, muscle and joint health and musculoskeletal disorders such as osteoporosis,

sarcopenia, and fibromyalgiaMusculo-

skeletal

Frost & Sullivan

54

Appendices

55

Principal abbreviations

BRC British Retail Consortium

CAGR Compound Average Growth Rate

COA Certificate of Analysis

CRM Customer Relationship Management

DHA Docosahexaenoic Acid

EFSA European Food Safety Authority

EPA Eicosapentaenoic Acid

ERP Enterprise Resource Planning

EU European Union

F&B Food & Beverage

FDA Food and Drug Administration

FMSA Food Safety Modernization Act

GFSI Global Food Safety Initiative

GHP Good Hygiene Practice

GMP Good Manufacturing Practice

HACCP Hazard Analysis and Critical Control Points

IFS International Featured Standards

ISO International Organization for Standardization

MPC Milk Protein Concentrate

PUFA Polyunsaturated Fatty Acids

RFID Radio-Frequency Identification

SPC Soy Protein Concentrate

SPI Soy Protein Isolate

SQF Safe Quality Food Initiative

TPC Third Party Certifiers

TSP Textured Soy Protein

WPC Whey Protein Concentrate

WPH Whey Protein Hydrolysate

WPI Whey Protein Isolate

YoY Year On Year

56

Frost & Sullivan

www.frost.com

August 2016

In exclusive for Intesa Sanpaolo

All rights reserved.

The partial or full reproduction, use, distribution, publication, transmission, amendment or sale of

all or part of these document by any means and for any reason whatsoever is forbidden.

For any request, please contact [email protected]