cu.clarkson.educu.clarkson.edu/tcs/2016-2017 Clarkson School Handb… · Web viewcu.clarkson.edu

Prepared byINSTATE Pty Ltd

D E P A R T M E N T O F A G R I C U L T U R E , F I S H E R I E S A N D F O R E S T R Y

Food Exporters’ Guide to INDONESIA

Ha

nd

bo

ok

Prepared for the Australian Government Department ofAgriculture, Fisheries and Forestry

by INSTATE Pty Ltd

Food Exporters’Guide to INDONESIA

Ha

nd

bo

ok

© Commonwealth of Australia 2004All photographs © Peter Dawson, 2003

This work is copyright. The Copyright Act 1968 1968 permits fair dealing for study, research, newsreporting, criticism or review. Selected passages, tables or diagrams may be reproduced for suchpurposes provided acknowledgment of the source is included. Major extracts or the entire document may not be reproduced by any process without the written permission of the Executive Manager, Food and Agriculture Business, Australian Government Department of Agriculture, Fisheries and Forestry,GPO Box 858, Canberra ACT 2601.

ISBN 0 642 539197

Disclaimer

This report was prepared by INSTATE Pty Ltd for the Food Policy and Safety Branch of the AustralianGovernment Department of Agriculture, Fisheries and Forestry. It should be cited as:

Smith, L and Dawson, P, Food Exporters’ Guide to Indonesia, Australian Government Department ofAgriculture, Fisheries and Forestry, Canberra, 2004.

INSTATE Pty Ltd is an Australian advisory firm, headquartered in Sydney, which specialises in Asian marketstrategies.

The views expressed in this publication are not necessarily the views of the Commonwealth. Thispublication is made available on the understanding that the Commonwealth is not thereby engaged inrendering professional advice. Before relying on material in this publication, users should independentlyverify the accuracy, currency, completeness and relevance of the information for their purposes and obtainany appropriate professional advice. References to non-Commonwealth organisations do not constituteendorsement by the Commonwealth of those organisations or any associated product or service.

The Australian Government Department of Agriculture, Fisheries and Forestry seeks to publish its work tothe highest professional standards. However, it cannot accept responsibility for any consequences arisingfrom the use of information herein. Readers should rely on their own skill and judgement in applying anyinformation for analysis to particular issues or circumstances.

Design and formatting by Mirrabooka Marketing & Design Pty Ltd.

Acknowledgements

The authors wish to thank PJ Dawson and Associates, Thomas Darmalan (GAPMMI), staff in the FoodPolicy and Communications Section of the Australian Government Department Agriculture, Fisheries andForestry’s Food and Agriculture Business Group who managed the project and edited the handbook, andthe numerous Australian and Indonesian company representatives and government officials who gavegenerously of their time for interviews and assistance.

The authors also wish to thank Nicole Maron, Andrew Campion and Denis Gastin of INSTATE for theirresearch and editorial input.

Cover images courtesy of P J Dawson and P T Davids Distribution Indonesia.CLOCKWISE FROM TOP LEFT: Fruit stalls, Jakarta; Carrefours checkouts, Jakarta; Davids dry warehouse,Jakarta; fruit & vegetables, Alfa hypermarket; Alfa hypermarket, Surabaya.

FOO D E XPORTER S’ GUIDE TO INDONESIAii

Chapter title

FOOD AND AGRICULTURE BUSINESS GROUP

The Australian Government Department of Agriculture Fisheries and Forestry is theCommonwealth agency with portfolio responsibility for food production and processing policy.The Food and Agriculture Business Group facilitates integrated policy development, innovationand stakeholder engagement across the agriculture and food industries.

The Food Policy and Safety Branch of the Group, which includes the Food Policy andCommunications Section, develops and implements policy with the aim of facilitating a globallycompetitive, innovative and export oriented food processing and beverage industry. Thesection works cooperatively with and has regard to the mandates of the National Food IndustryCouncil (NFIC), National Food Industry Strategy Ltd (NFIS Ltd), the Primary Industry MinisterialCouncil’s food sub-committee, and industry.

The section is also responsible for disseminating information to food industry stakeholders onissues of interest and importance including sectoral profiles, international and domestictrends, emerging issues, statistics, developments in food policy and programs, and decisionsby government and food agencies.

Other portfolio publications of possible interest include:Spencer S, Price Determination in the Australian Food Industry: A Report, AustralianGovernment Department of Agriculture, Fisheries and Forestry, Canberra, 2004.

Department of Agriculture, Fisheries and Forestry, Australian Food Statistics 2003, reportprepared by ABARE, Canberra, 2003.

Food News Bulletin (published quarterly), produced by the Australian Government Departmentof Agriculture, Fisheries and Forestry, Canberra.

Department of Agriculture, Fisheries and Forestry, Exporting Australian Processed Foods,report prepared by INSTATE Pty Ltd, Milsons Point, NSW, 2000.

Department of Agriculture, Fisheries and Forestry, Chains of Success, Canberra, 1998.

Most portfolio publications can be accessed via:http://www.daff.gov.au/content/publications.cfm

Contact details

Food Policy and CommunicationsAustralian Government Department of Agriculture, Fisheries and ForestryGPO Box 858CANBERRA ACT 2601

Telephone: +61 2 6272 4161

Email: mailto:[email protected]

Internet site: http://www.daff.gov.au/foodinfo

FOO D E XPORTER S’ GUIDE TO INDONESIA iii

Chapter title

FOO D E XPORTER S’ GUIDE TO INDONESIAiv

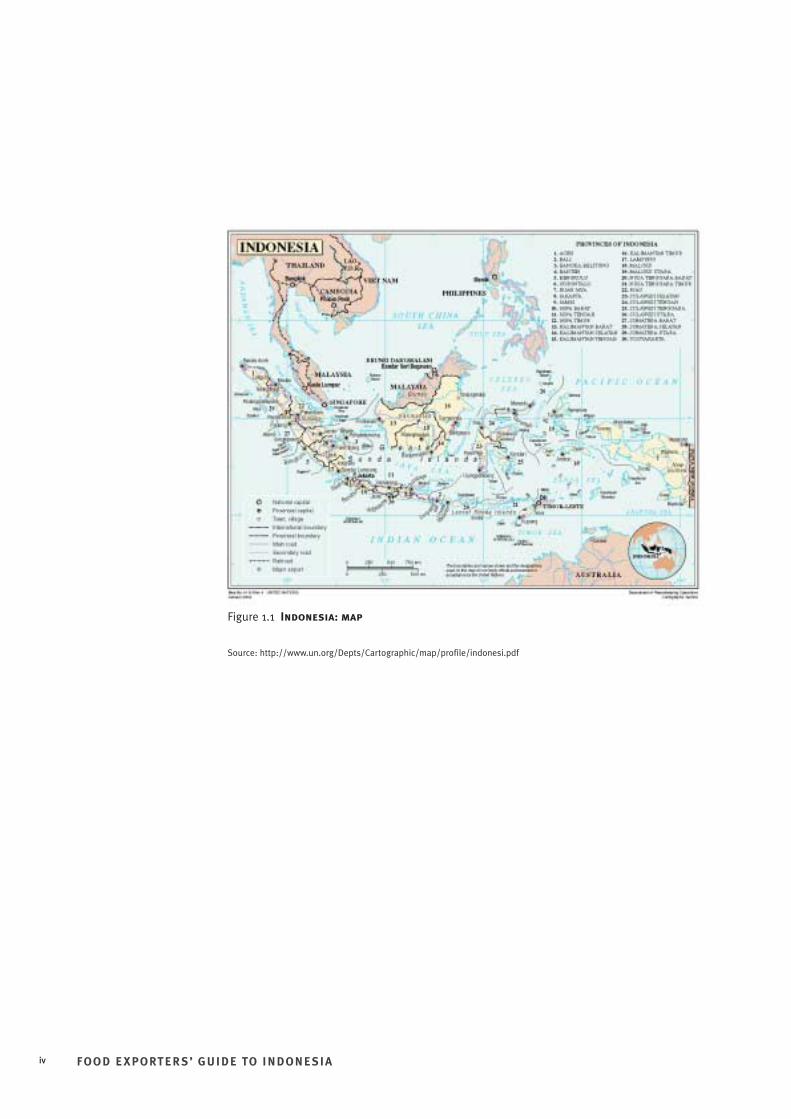

Figure 1.1 Indonesia: map

Source: http://www.un.org/Depts/Cartographic/map/profile/indonesi.pdf

Chapter title

FOO D E XPORTER S’ GUIDE TO INDONESIA v

CONTENTS

Indonesia: Map iv

Abbreviations/Acronyms ix

Indonesia: Facts in Brief xi

Chapter 1 Introduction 1

Chapter 2 Indonesian consumers 3

Chapter 3 Retail and food service 13

Chapter 4 Supply chains 27

Chapter 5 Business environment 43

Chapter 6 Australian food exports 57

Chapter 7 Political and economic environment 63

Appendixes 69

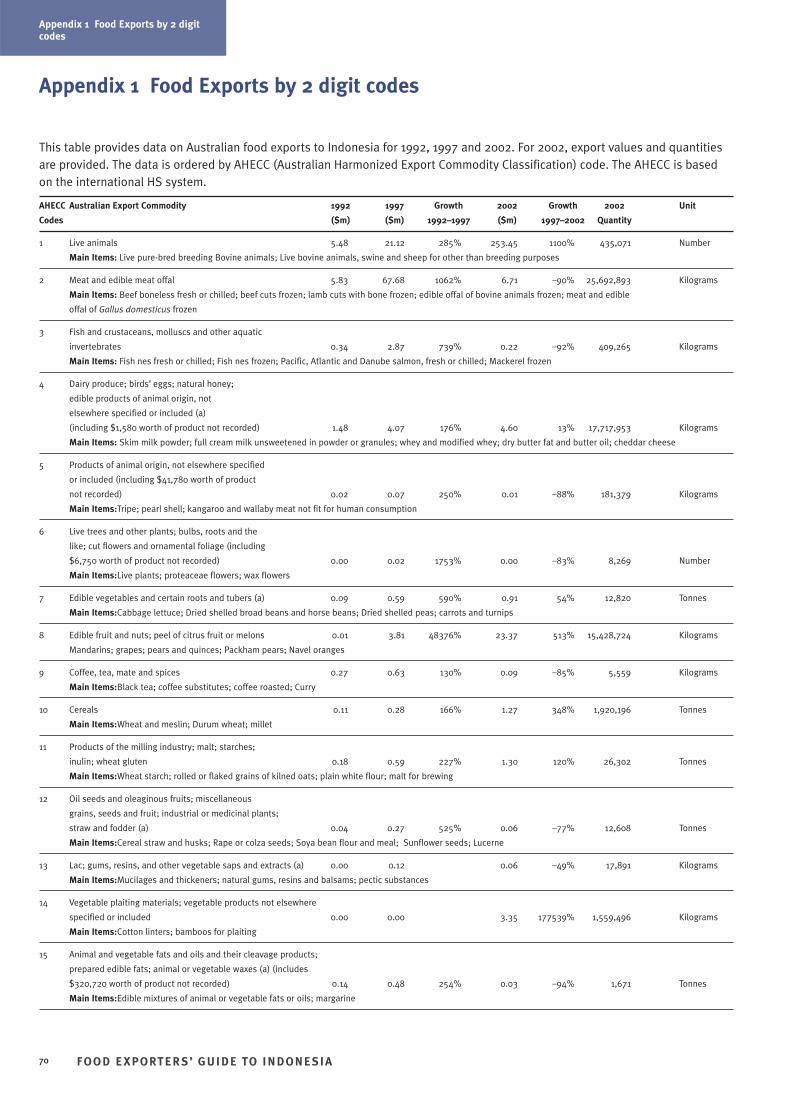

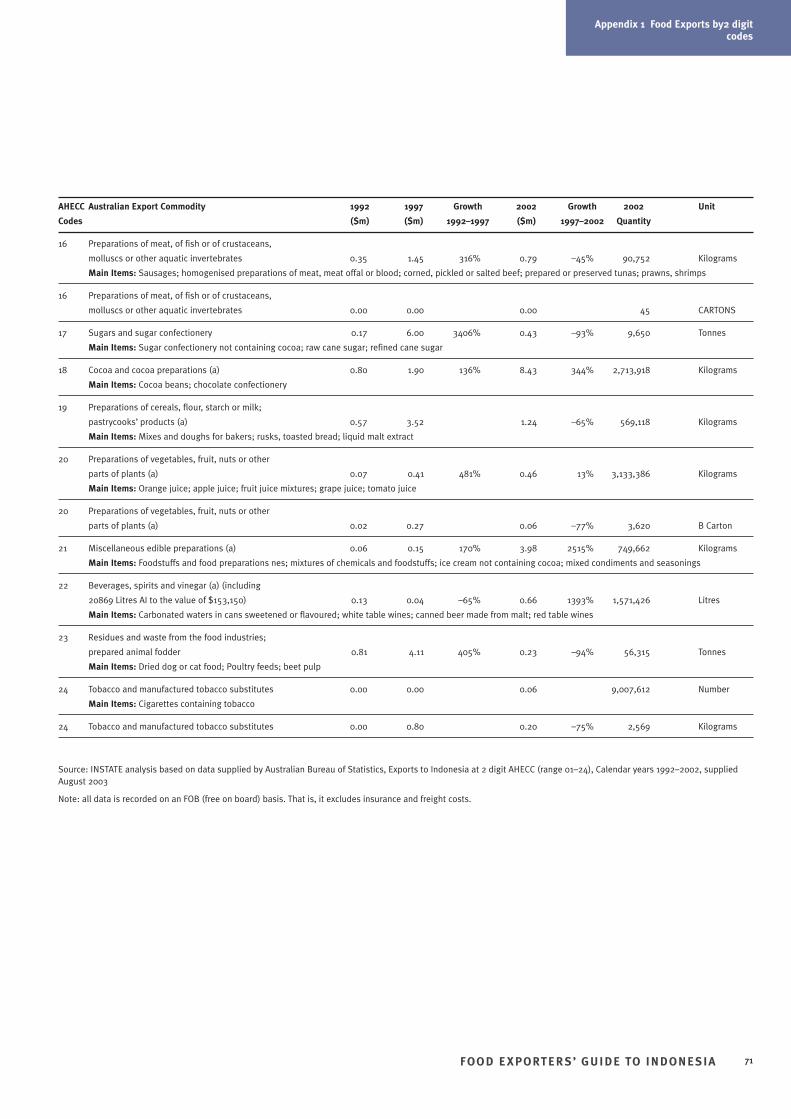

Appendix 1 Food exports by 2 digit codes 70

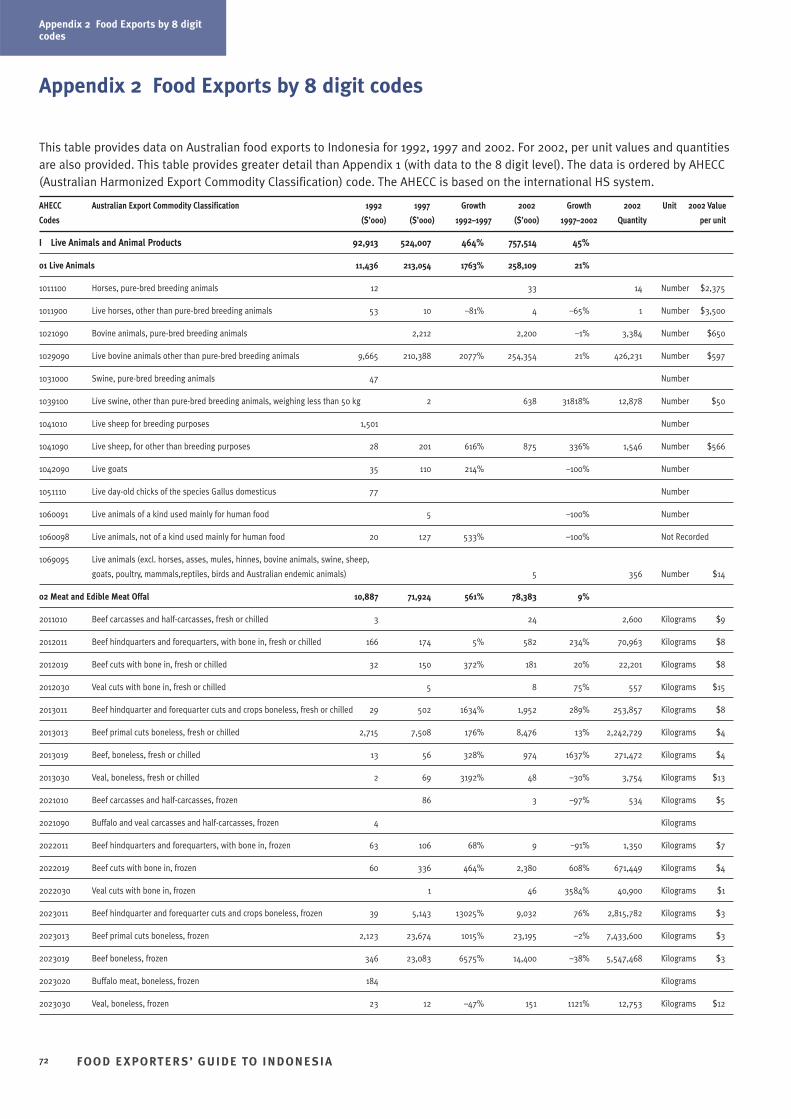

Appendix 2 Food exports by 8 digit codes 72

Appendix 3 Exports – by port of discharge 93

Appendix 4 Tariffs 98

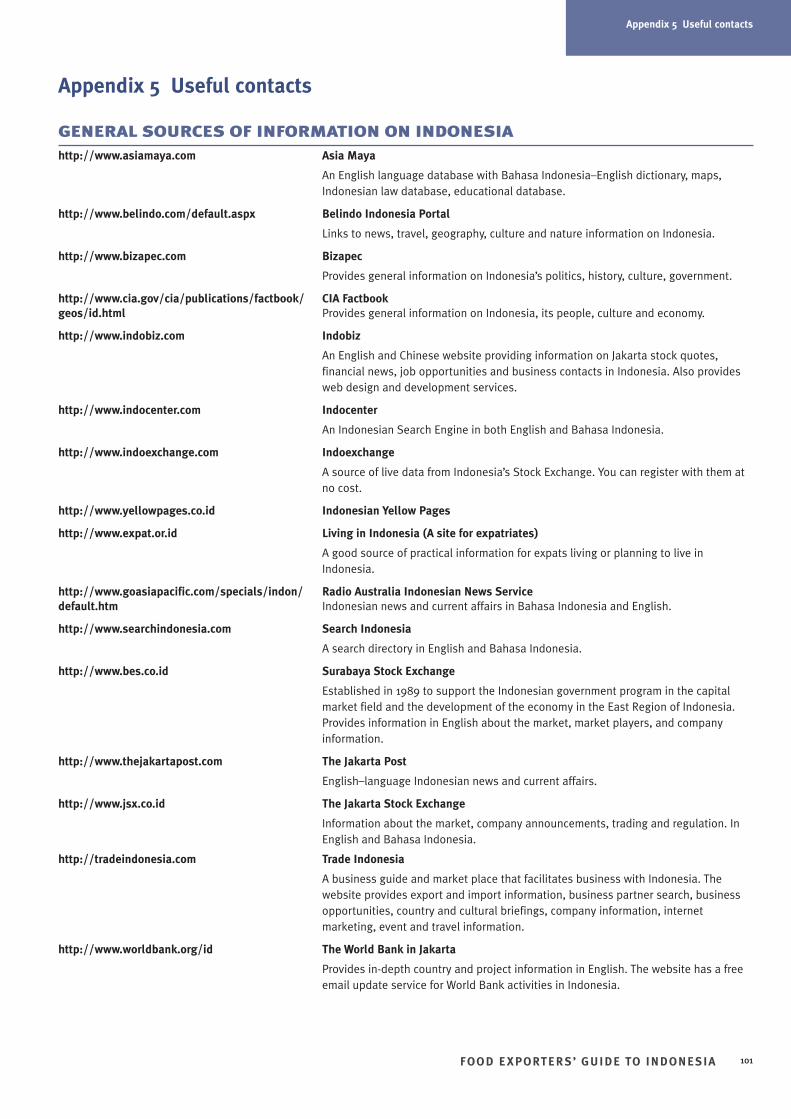

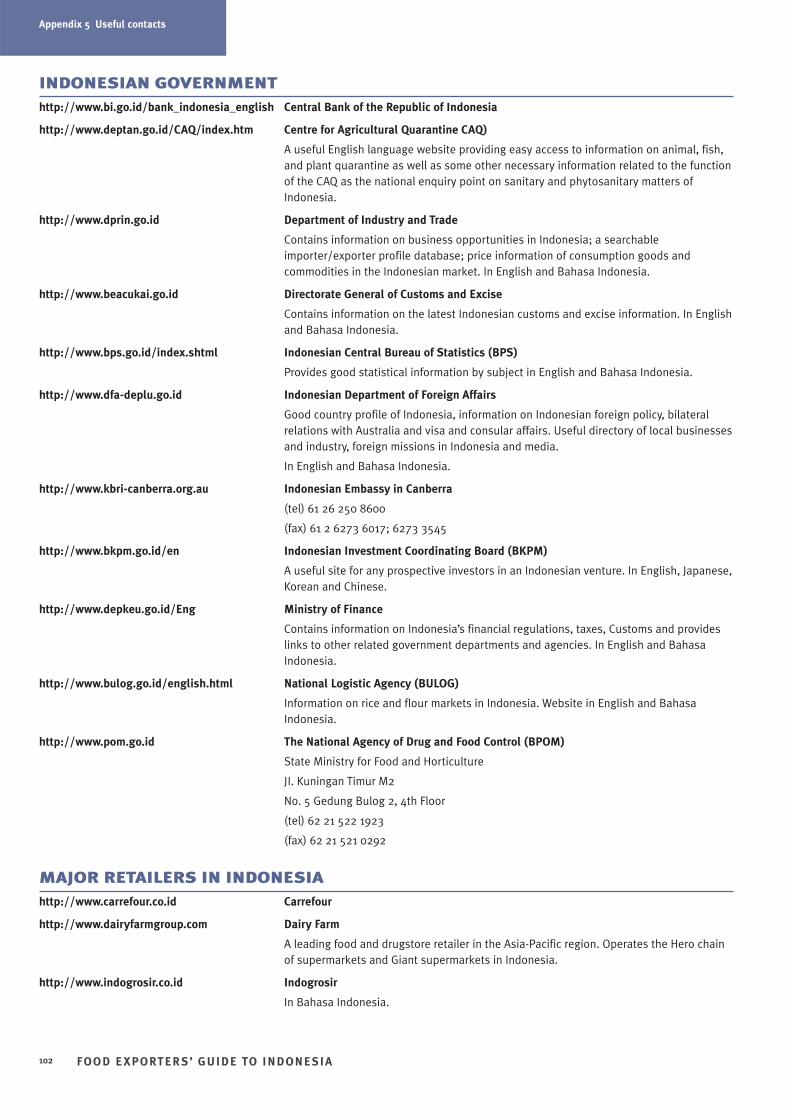

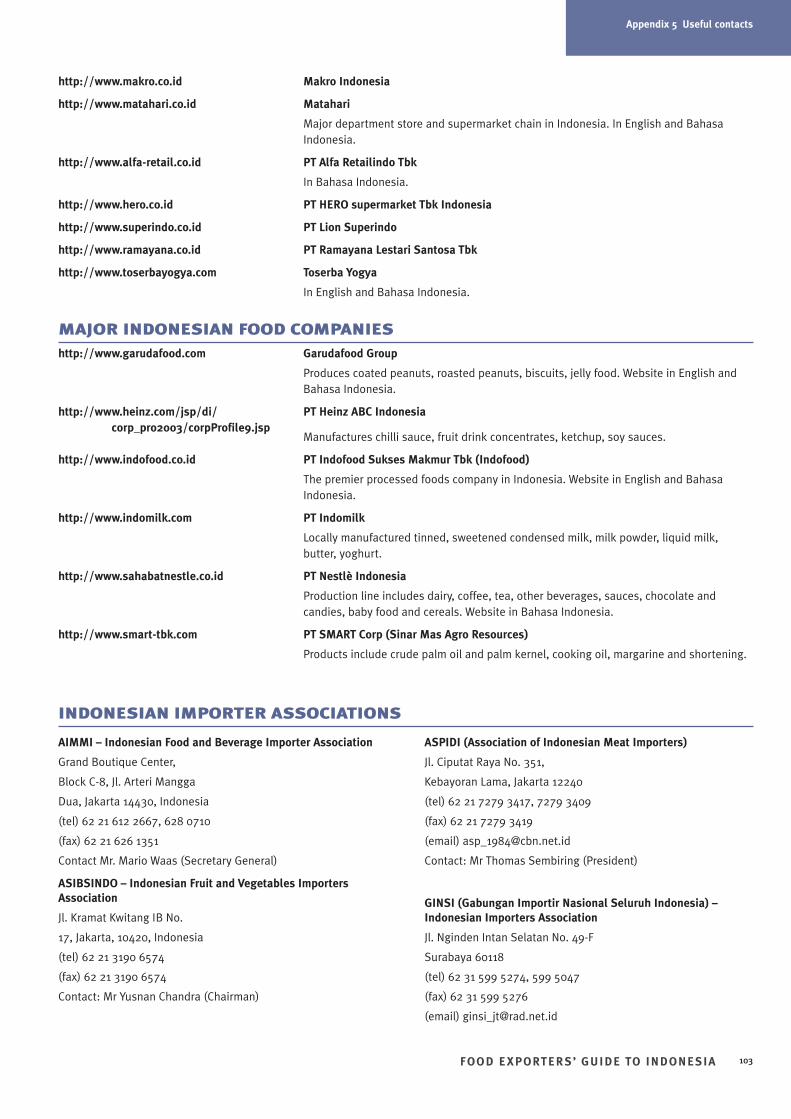

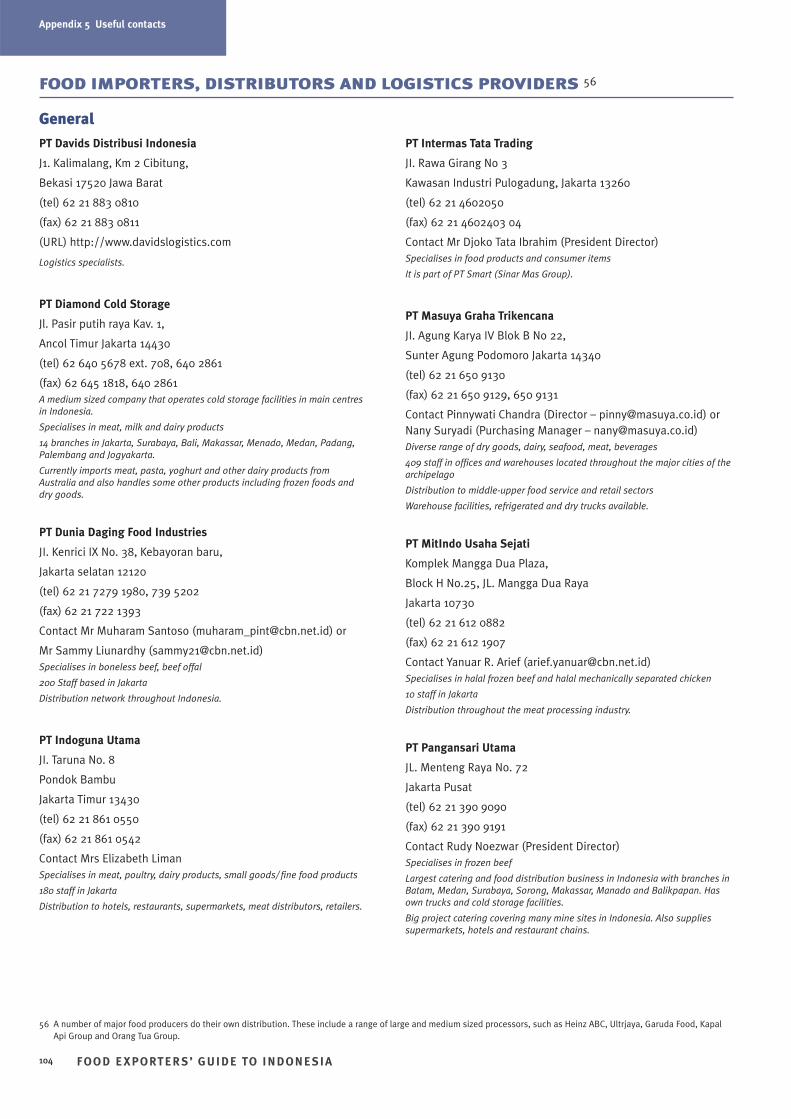

Appendix 5 Useful contacts 101General sources of information on Indonesia 101Indonesian Government 102Major retailers in Indonesia 102Major Indonesian food companies 103Indonesian importer associations 103Food importers, distributors and logistics providers 104Indonesian industry associations 106Australia-Indonesia business and other links 106Australian Government 107Islamic associations in Australia 107

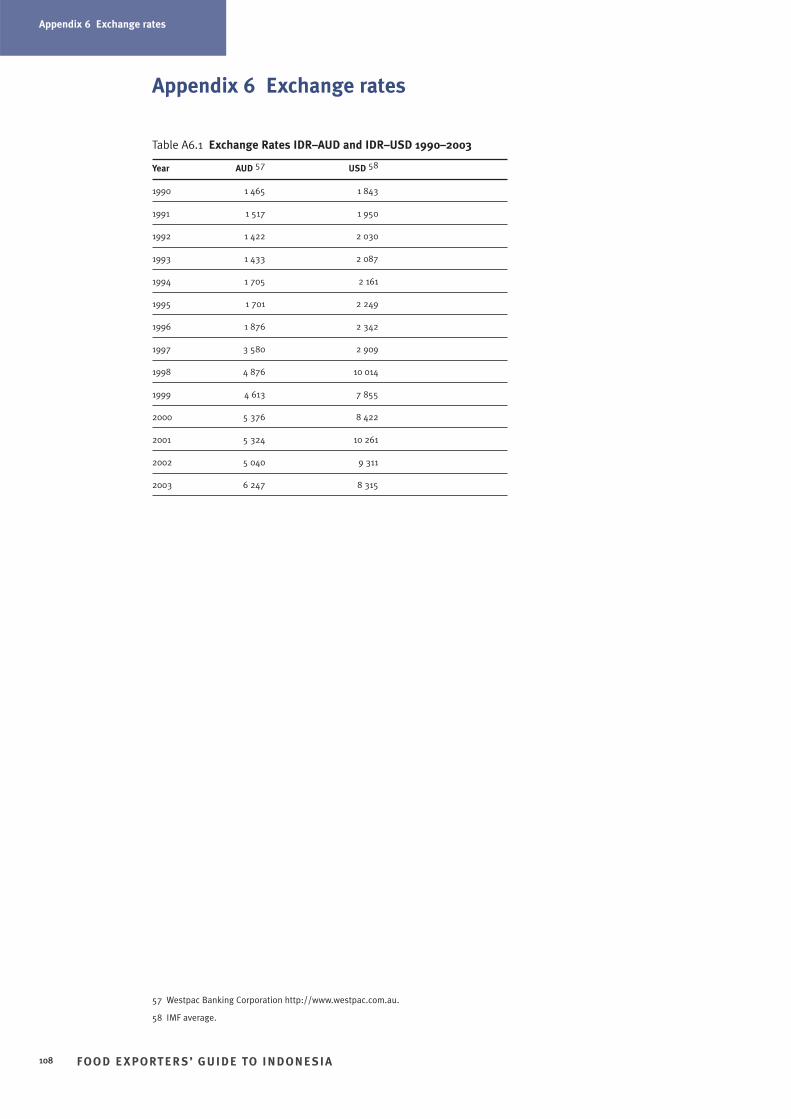

Appendix 6 Exchange rates 108

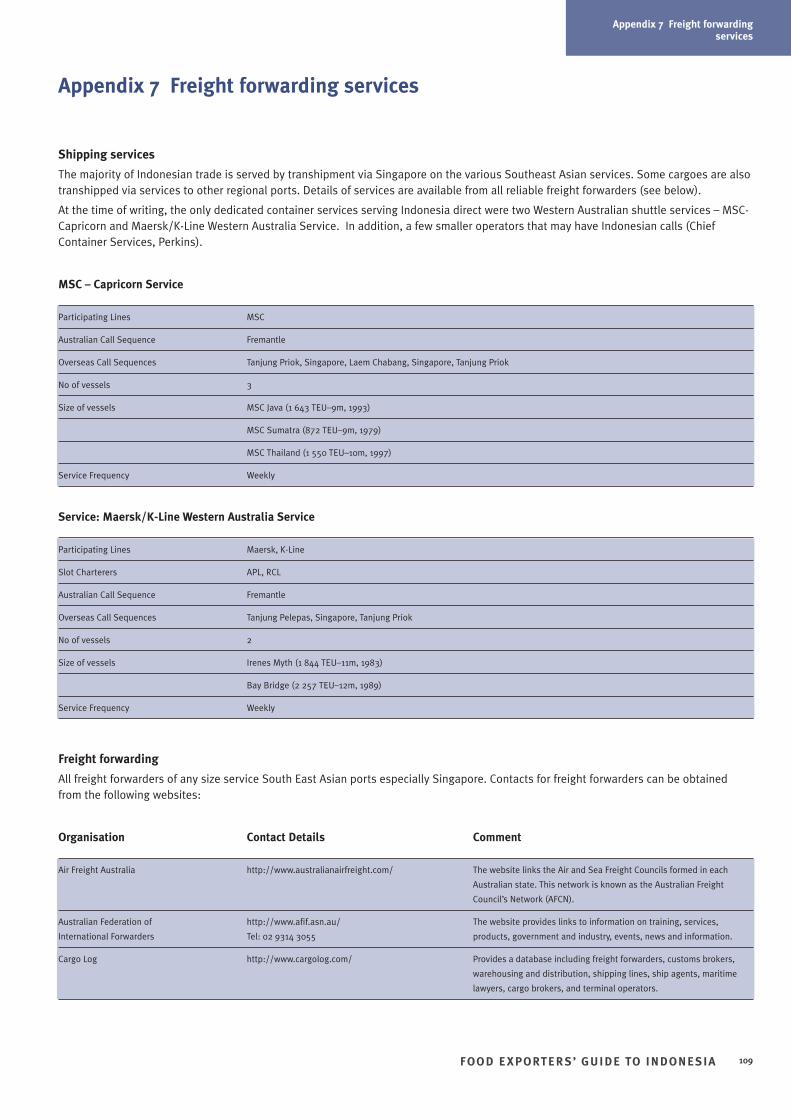

Appendix 7 Freight forwarding services 109

Bibliography 110

FIGURES, TABLES AND IMAGES

Figures

1.1. Indonesia: map iv

2.1. Indonesia: age distribution 3

2.2. Indonesia: population distribution 4

2.3. Monthly per capita expenditure (Rp/month) 4

2.4. Consumer spending on food: urban rural differences 5

2.5. Indonesia: religious beliefs 5

2.6. Indonesia: GDP growth, 1970–2003 6

2.7. Demographic distribution: AC Nielsen data (Rp/month) 7

3.1. Where Indonesians shop 13

3.2. Average number of people per retail outlet 14

3.3. Top five grocery chains’ market share: share of all category volume (%) 15

3.4. Indonesia: retail trade shares 16

4.1. Indonesia and Australia: composition of GDP 27

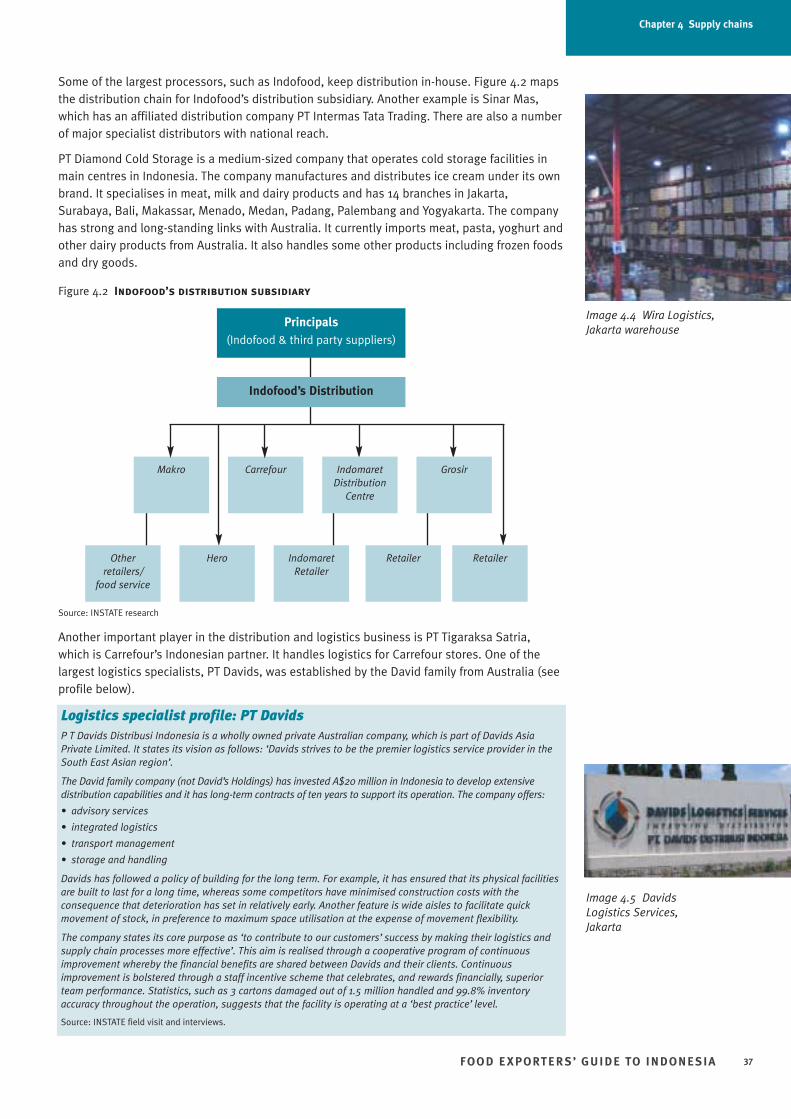

4.2. Indofood’s distribution subsidiary 37

4.3. Typical distribution network for cooking oil 41

Tables

2.1. Demographic segments 7

2.2. Indonesia: size and distribution of demographic segments (% total in city) 7

2.3. Average per capita monthly expenditure by commodity group, 2002 (Rp) 8

2.4. Average per capita monthly expenditure by commodity group, 2002 (% share of total spending on food) 9

3.1. Indonesia: estimated growth in number of retail food outlets, 1997–2003 15

3.2. Retail food sales by type of outlet Rp trillion (% share) 15

3.3. Indonesia: an overview of the modern retail sector 16

3.4. Indonesia: major supermarket chains, 2001 18

3.5. Indonesia: major warehouse / cash and carry operators, 2001 19

3.6. Indonesia: hypermarket chains, 2003 20

3.7. Indonesia: international tourism industry key projections 23

3.8. Indonesia: hotels 24

3.9. Indonesia: selected food outlet franchises, 2002 25

4.1. Indonesia: ten largest packaged food companies by market share (%) 29

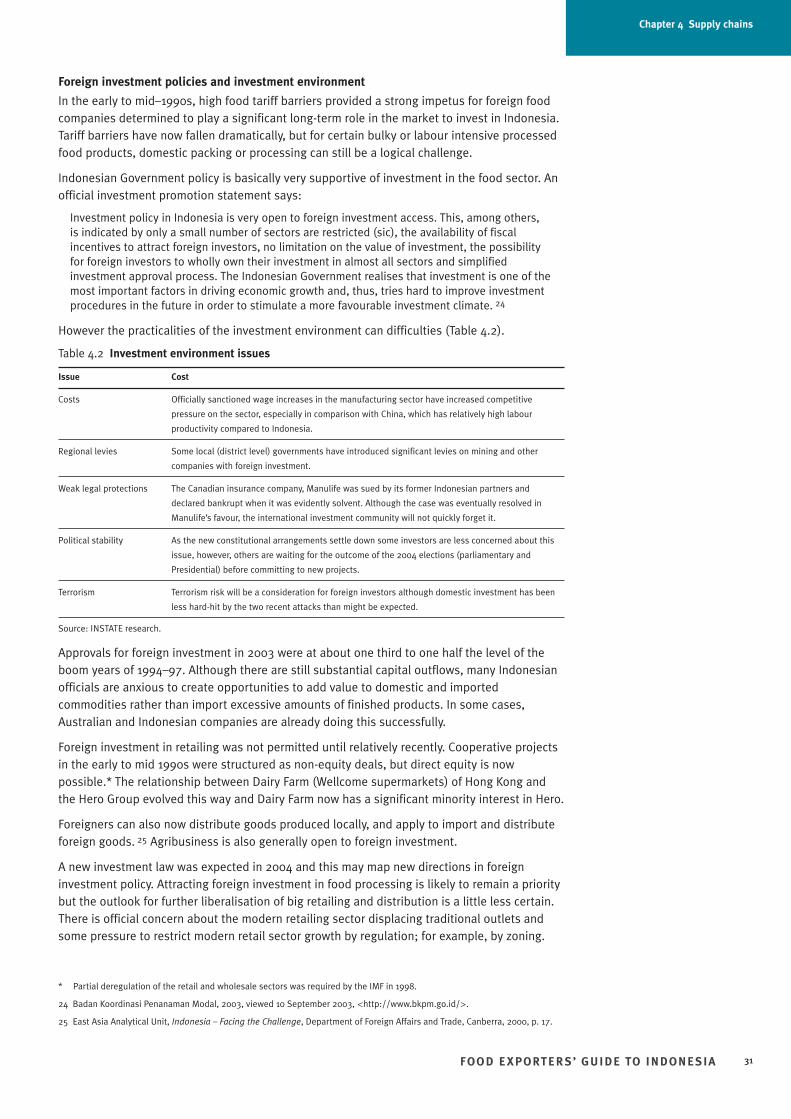

4.2. Investment environment issues 31

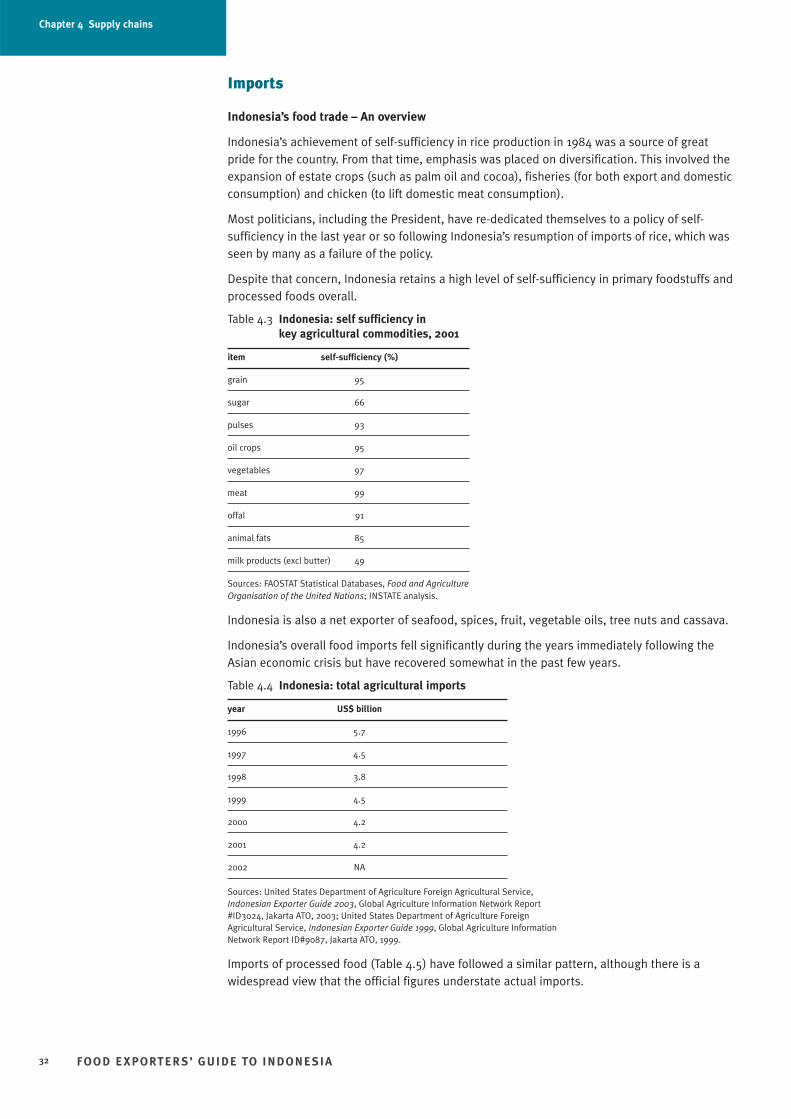

4.3. Indonesia: self-sufficiency in key agricultural commodities, 2001 32

4.4. Indonesia: total agricultural imports 32

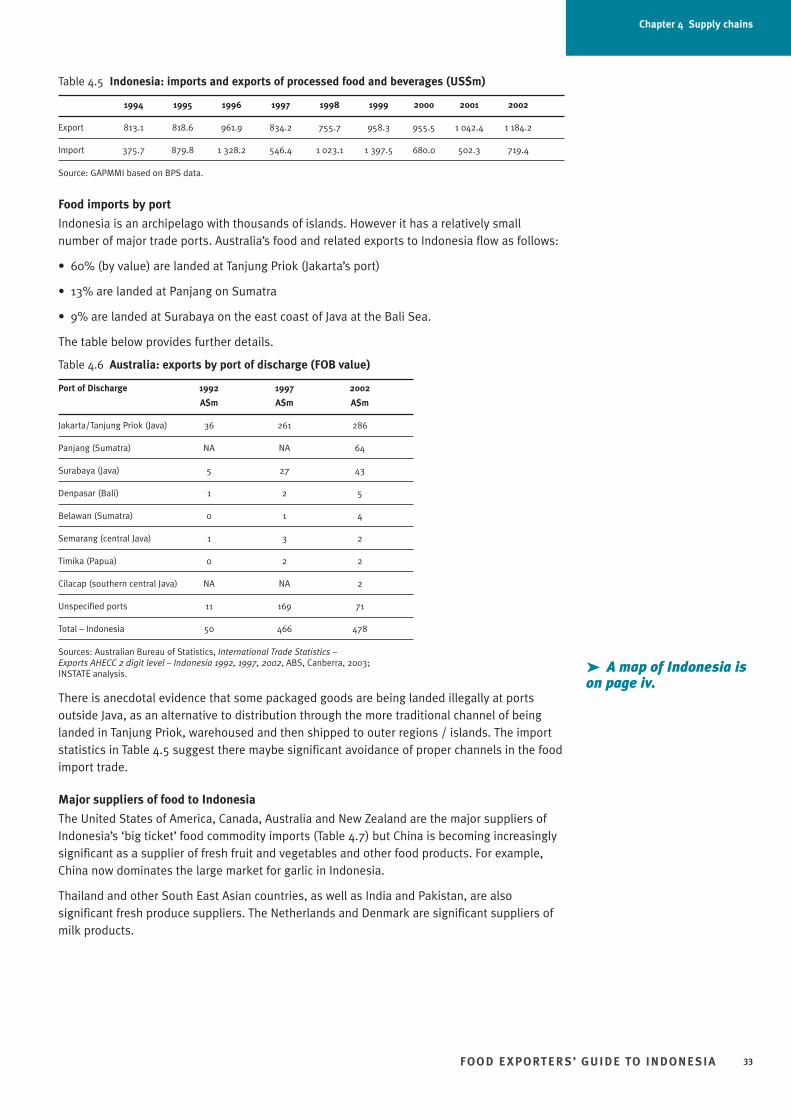

4.5. Indonesia: imports and exports of processed food and beverages (US$m) 33

4.6. Australia: exports by port of discharge (FOB value) 33

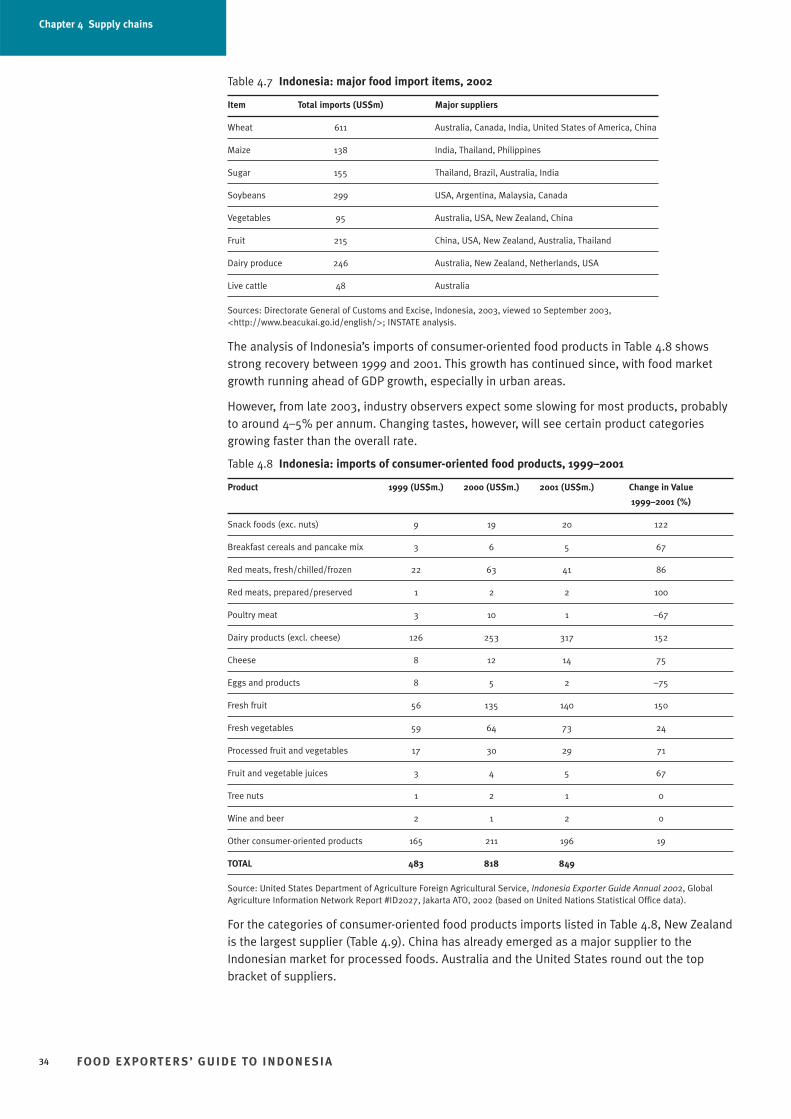

4.7. Indonesia: major food import items, 2002 34

4.8. Indonesia: imports of consumer-oriented food products, 1999–2001 34

FOO D E XPORTER S’ GUIDE TO INDONESIAvi

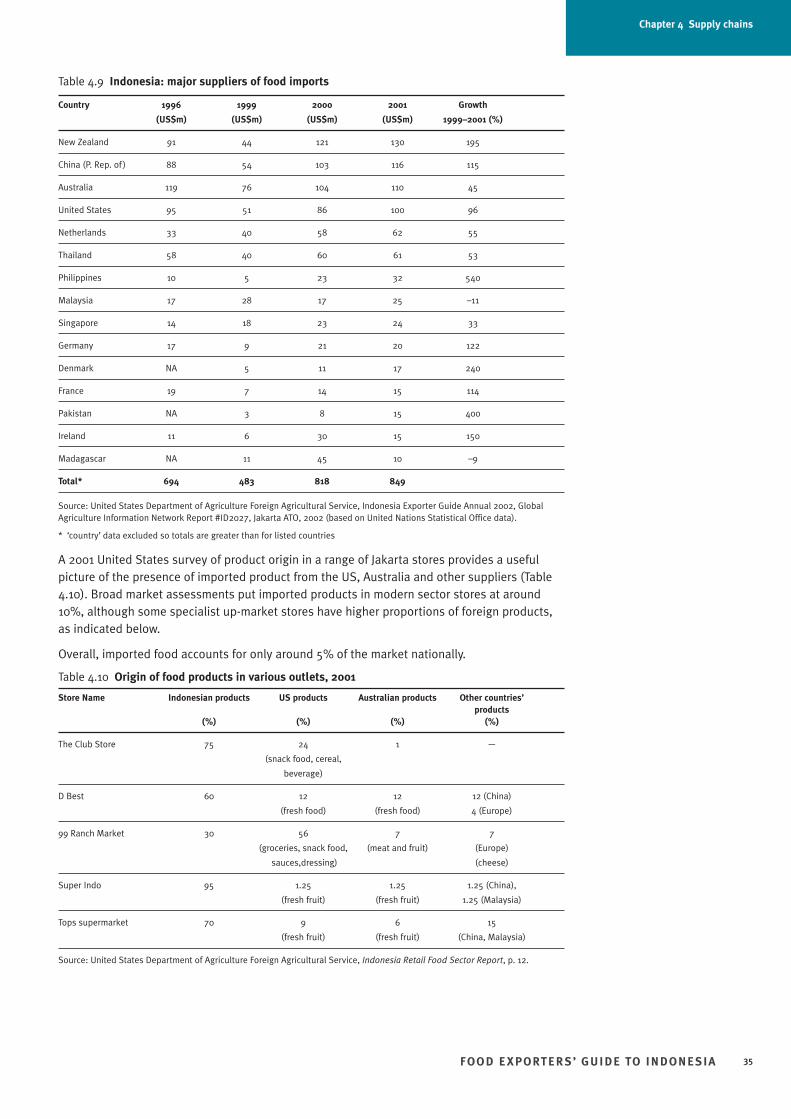

4.9. Indonesia: major suppliers of food imports 35

4.10. Origin of food products in various outlets, 2001 35

4.11. Indonesia: food distribution by retail / trade channel 38

4.12. Indonesia: food distribution by geographic region 38

4.13. Supply chain development: challenges and constraints 41

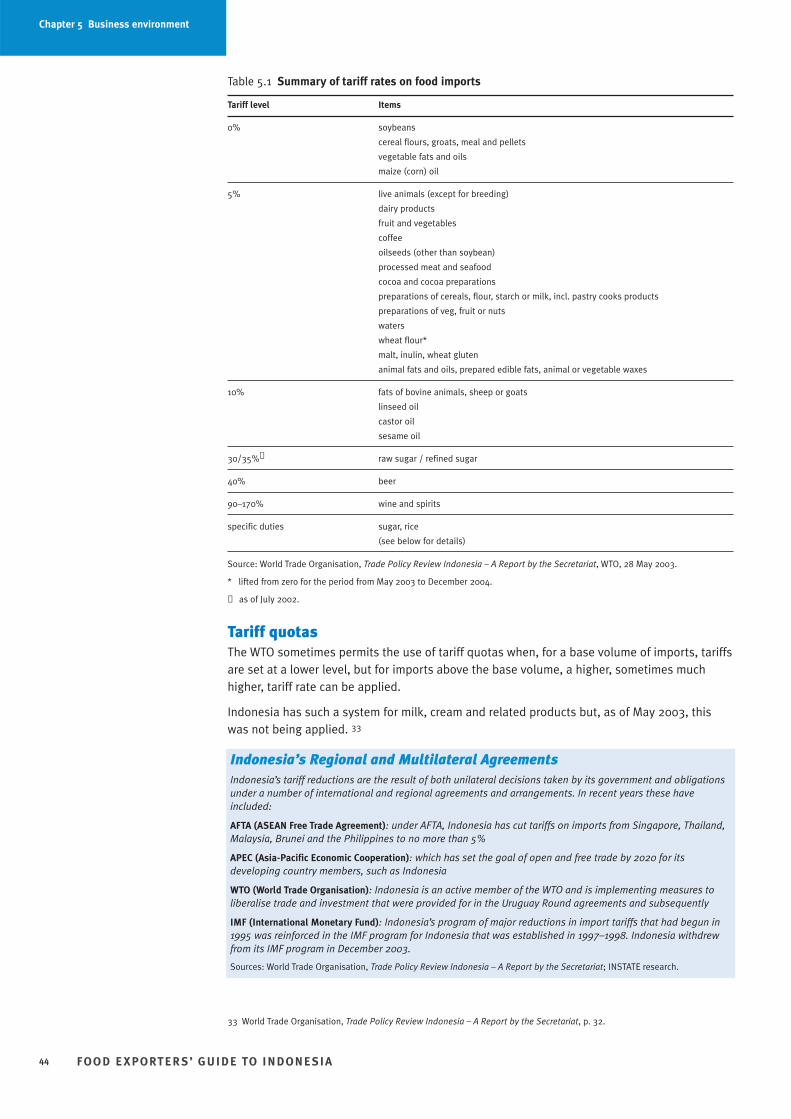

5.1. Summary of tariff rates on food imports 44

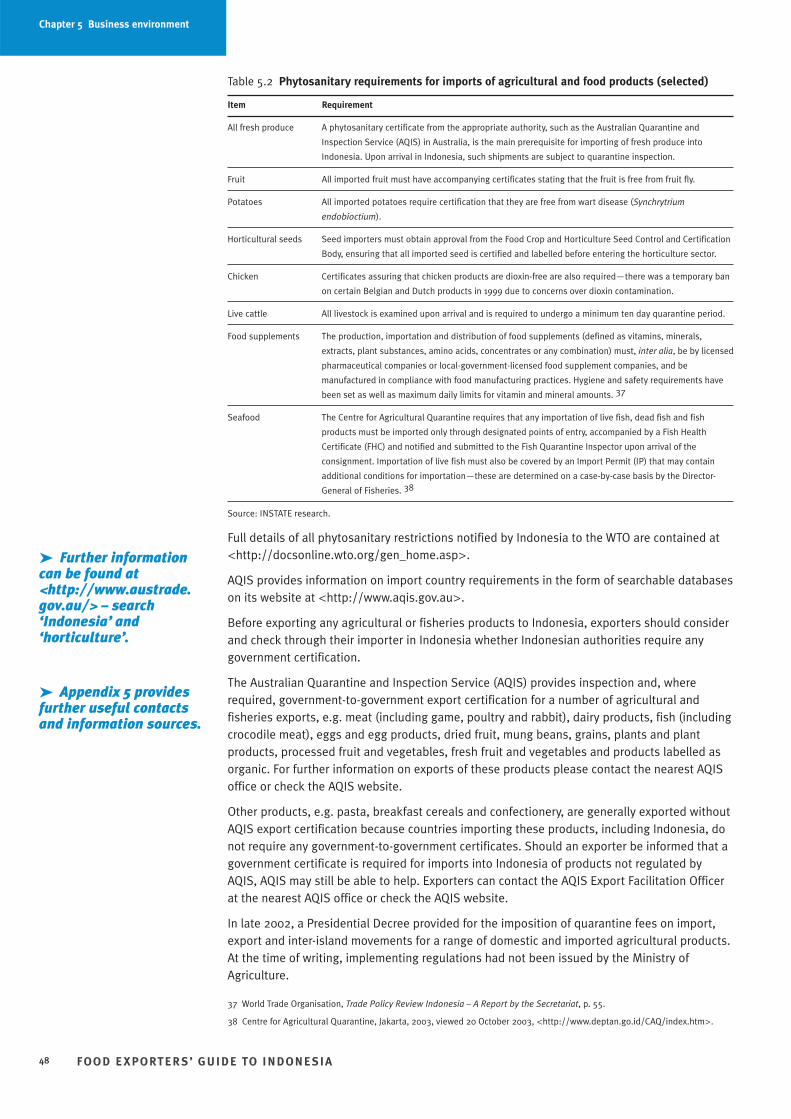

5.2. Phytosanitary requirements for imports of agricultural and food products (selected) 48

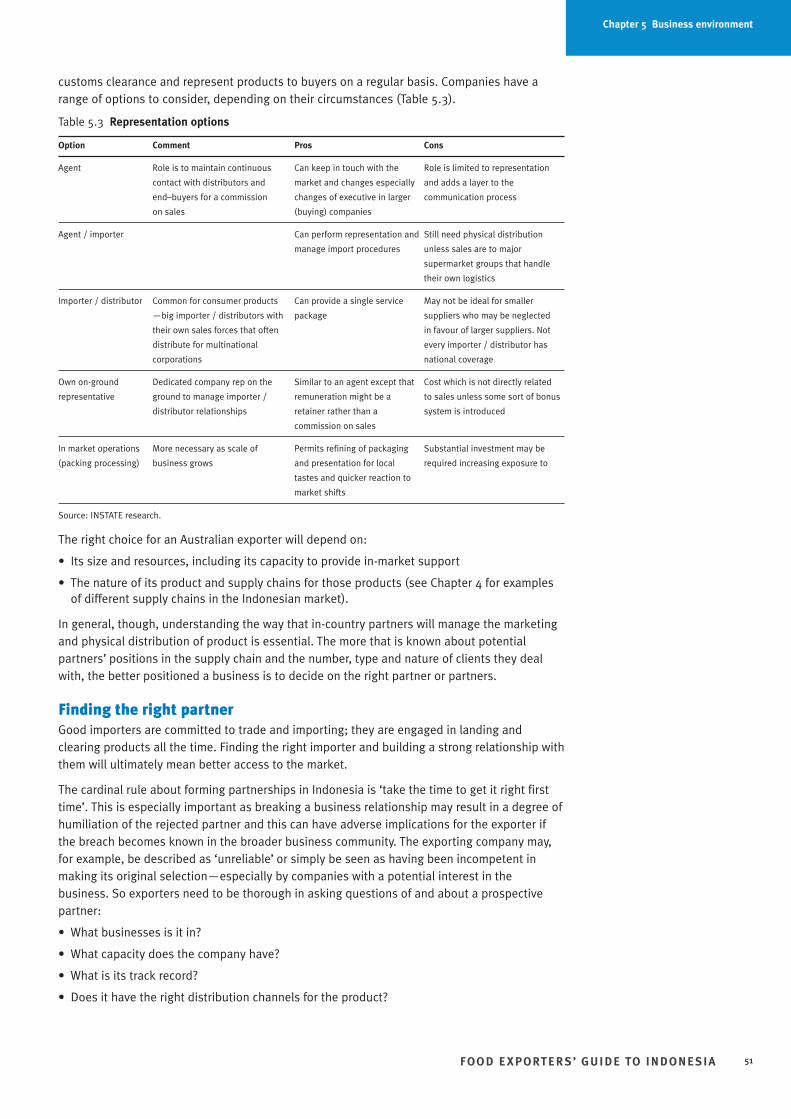

5.3. Representation options 51

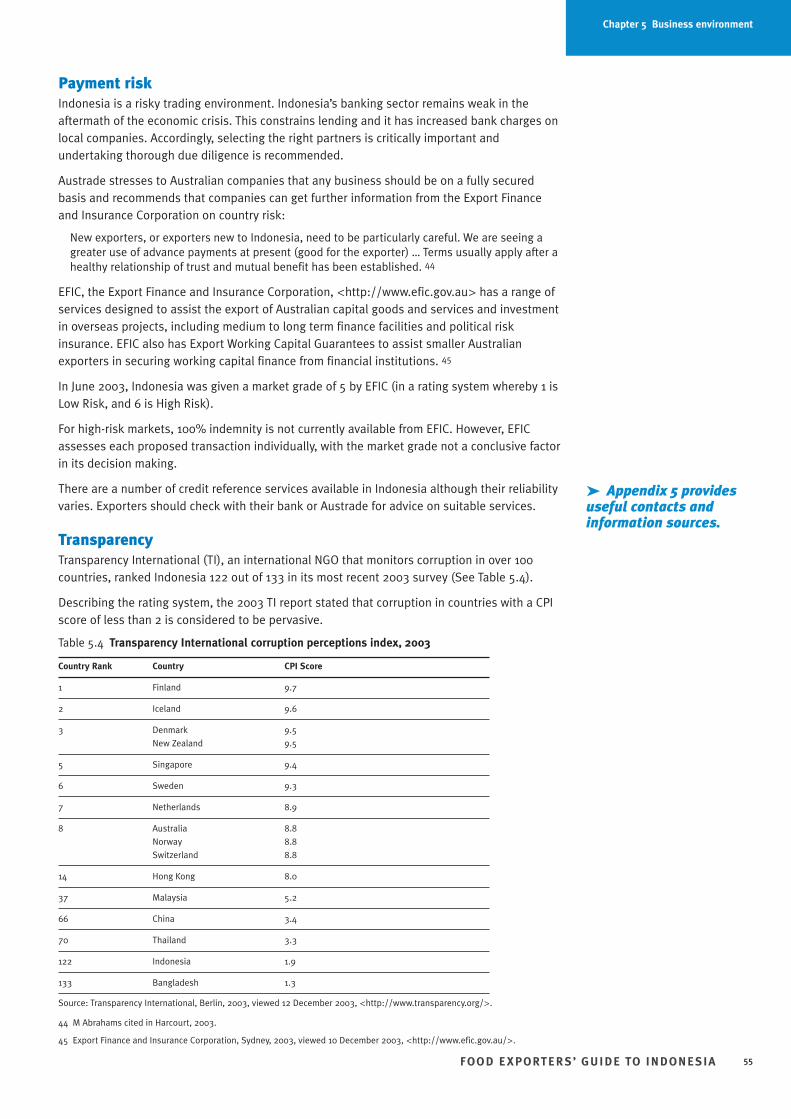

5.4. Transparency International corruption perceptions index, 2003 55

6.1. Australia’s major food markets: selected years (ranking / exports in A$bn) 57

6.2. Select Australian exports to Indonesia, 1992–2002 by value ($,000 FOB) 58

6.3. Australian food exports to Indonesia: growing niche markets 60

6.4. Australian product shares of the Indonesian market, 2002 60

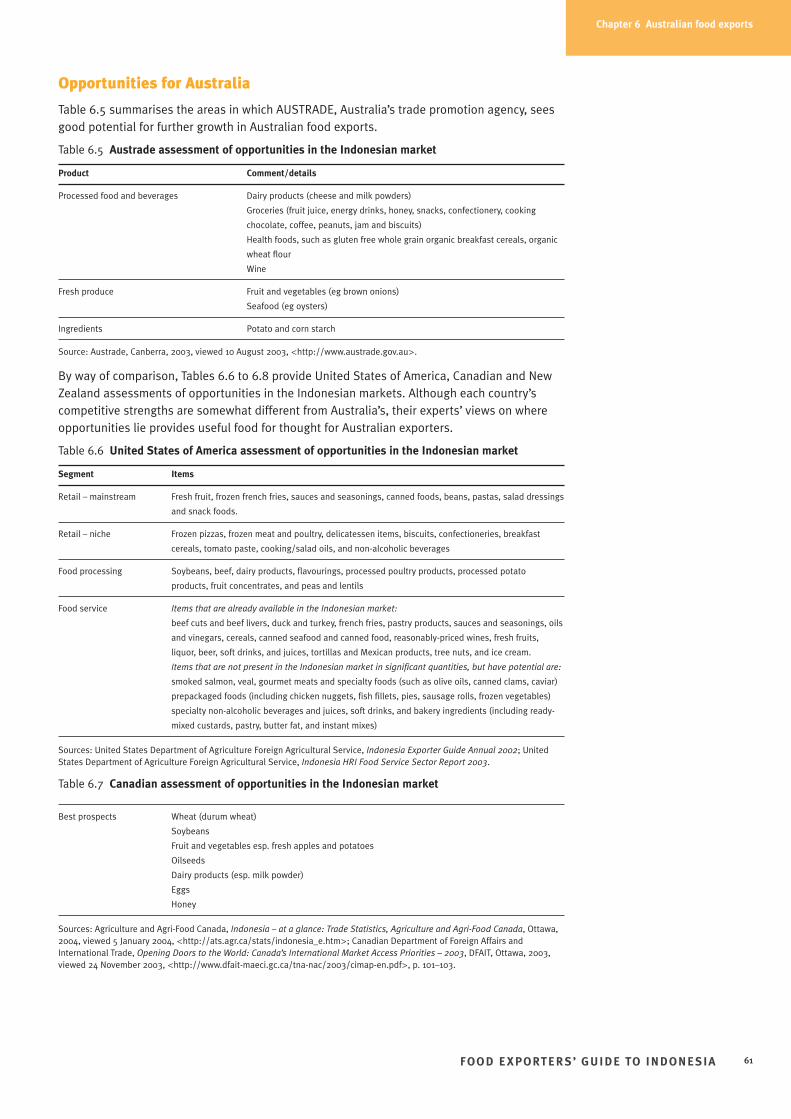

6.5. Austrade assessment of opportunities in the Indonesian market 61

6.6. United States assessment of opportunities in the Indonesian market 61

6.7. Canadian assessment of opportunities in the Indonesian market 61

6.8. New Zealand assessment of opportunities in the Indonesian market 62

A6.1. Exchange Rates IDR–AUD and IDR–USD, 1990–2003 108

Images

1.1. Fresh fruit street stall, Jakarta 1

1.2. Makro store, Jakarta 1

1.3. Australian fresh fruit display, Sogo Supermarket, Plaza Indonesia 1

2.1. Meat display, Hero supermarket 9

2.2. Indomilk display, Kemang 9

2.3. Fruit display, Jakarta supermarket 10

2.4. Durian fruit, Carrefour, Jakarta 10

2.5. In-store bakery, Carrefour, Jakarta 10

3.1. Wet market, Malang, East Java 14

3.2. Plaza Indonesia, Central Jakarta 15

3.3. Alfa Store, Surabaya 17

3.4. Fruit display, Hero supermarket, Kemang 18

3.5. Australian carrots, D’Best supermarket, Jakarta 19

3.6. Makro Store, Jakarta 20

3.7. Carrefour checkouts, Jakarta 21

3.8. Carrefour fruit section, Jakarta 21

3.9. Alfa minimart, Malang, East Java 22

3.10. Alfa minimart, Malang, East Java 22

3.11. Arnott’s biscuits, Hero supermarket, Kemang 23

3.12. Australian fruit display, Hero supermarket, Kemang 23

FOO D E XPORTER S’ GUIDE TO INDONESIA vii

Chapter title

3.13. Giant hypermarket under construction, Kelapa Gading, Jakarta 23

3.14. Shoppers in World Trade Centre, Mangga Dua 24

4.1. Japfa products, Jakarta hypermarket 28

4.2. Nestle cereal, Makro store, Jakarta 30

4.3. Wira Logistics, Jakarta 36

4.4. Wira Logistics, Jakarta warehouse 37

4.5. Davids Logistics Services, Jakarta 37

4.6. Davids 25 000 m2 dry warehouse, Jakarta 38

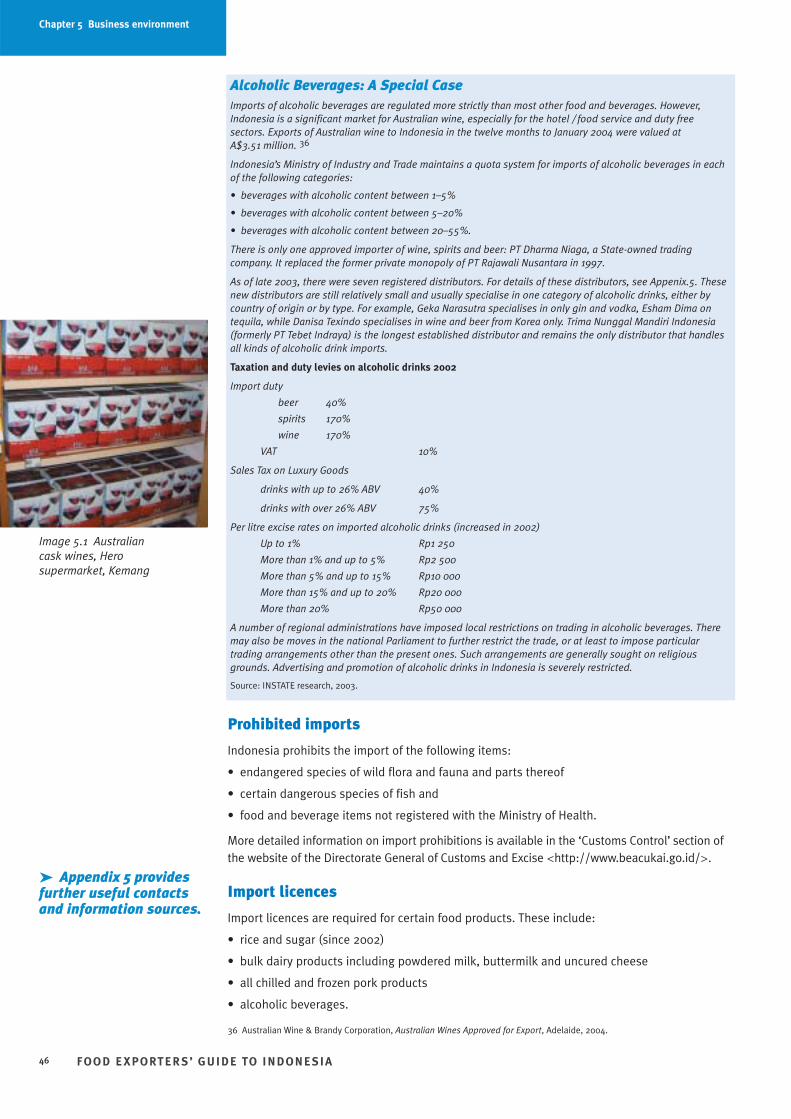

5.1. Australian cask wines, Hero supermarket, Kemang 46

5.2. Lebaran gift packs, hypermarket, Bekasi, Jakarta 53

5.3. Indonesian syrups and noodles, Ramadan stock 53

6.1. Capilano Honey, Hero supermarket, Kemang 58

6.2. Australian yoghurt, Hero supermarket, Kemang 59

6.3. Berri Juice counter, Kelapa Gading Mall 59

FOO D E XPORTER S’ GUIDE TO INDONESIAviii

Chapter title

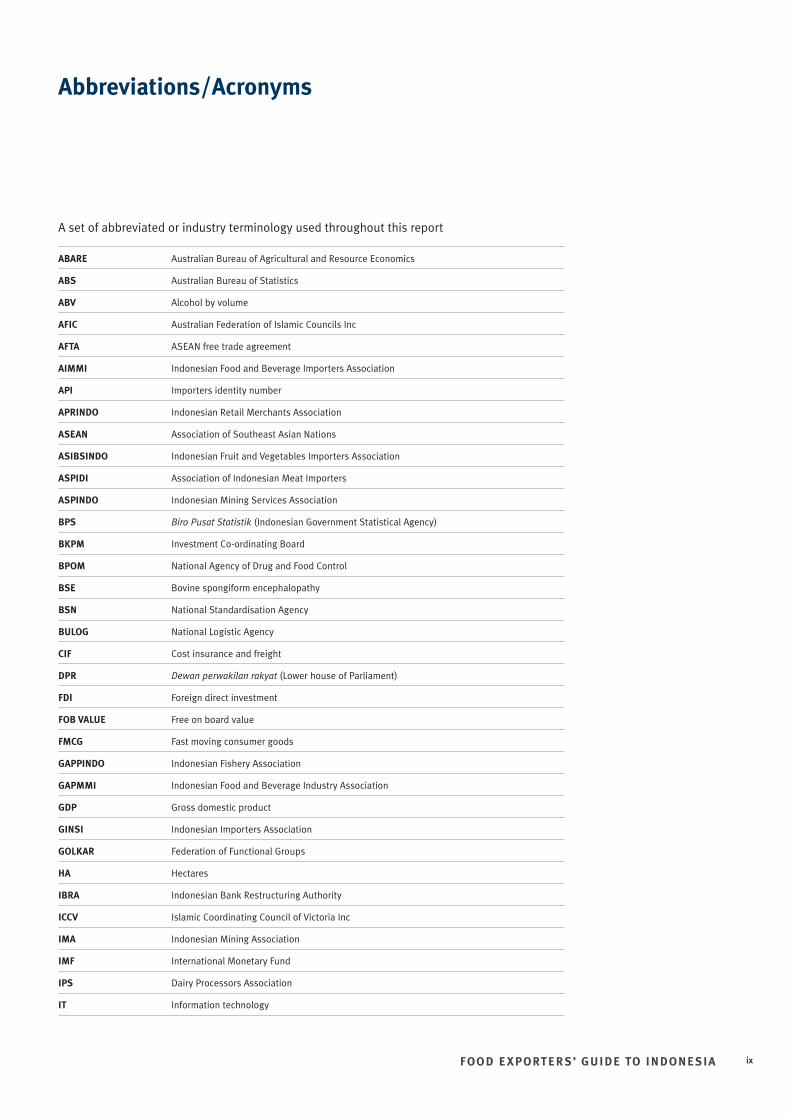

Abbreviations/Acronyms

A set of abbreviated or industry terminology used throughout this report

ABARE Australian Bureau of Agricultural and Resource Economics

ABS Australian Bureau of Statistics

ABV Alcohol by volume

AFIC Australian Federation of Islamic Councils Inc

AFTA ASEAN free trade agreement

AIMMI Indonesian Food and Beverage Importers Association

API Importers identity number

APRINDO Indonesian Retail Merchants Association

ASEAN Association of Southeast Asian Nations

ASIBSINDO Indonesian Fruit and Vegetables Importers Association

ASPIDI Association of Indonesian Meat Importers

ASPINDO Indonesian Mining Services Association

BPS Biro Pusat Statistik (Indonesian Government Statistical Agency)

BKPM Investment Co-ordinating Board

BPOM National Agency of Drug and Food Control

BSE Bovine spongiform encephalopathy

BSN National Standardisation Agency

BULOG National Logistic Agency

CIF Cost insurance and freight

DPR Dewan perwakilan rakyat (Lower house of Parliament)

FDI Foreign direct investment

FOB VALUE Free on board value

FMCG Fast moving consumer goods

GAPPINDO Indonesian Fishery Association

GAPMMI Indonesian Food and Beverage Industry Association

GDP Gross domestic product

GINSI Indonesian Importers Association

GOLKAR Federation of Functional Groups

HA Hectares

IBRA Indonesian Bank Restructuring Authority

ICCV Islamic Coordinating Council of Victoria Inc

IMA Indonesian Mining Association

IMF International Monetary Fund

IPS Dairy Processors Association

IT Information technology

FOO D E XPORTER S’ GUIDE TO INDONESIA ix

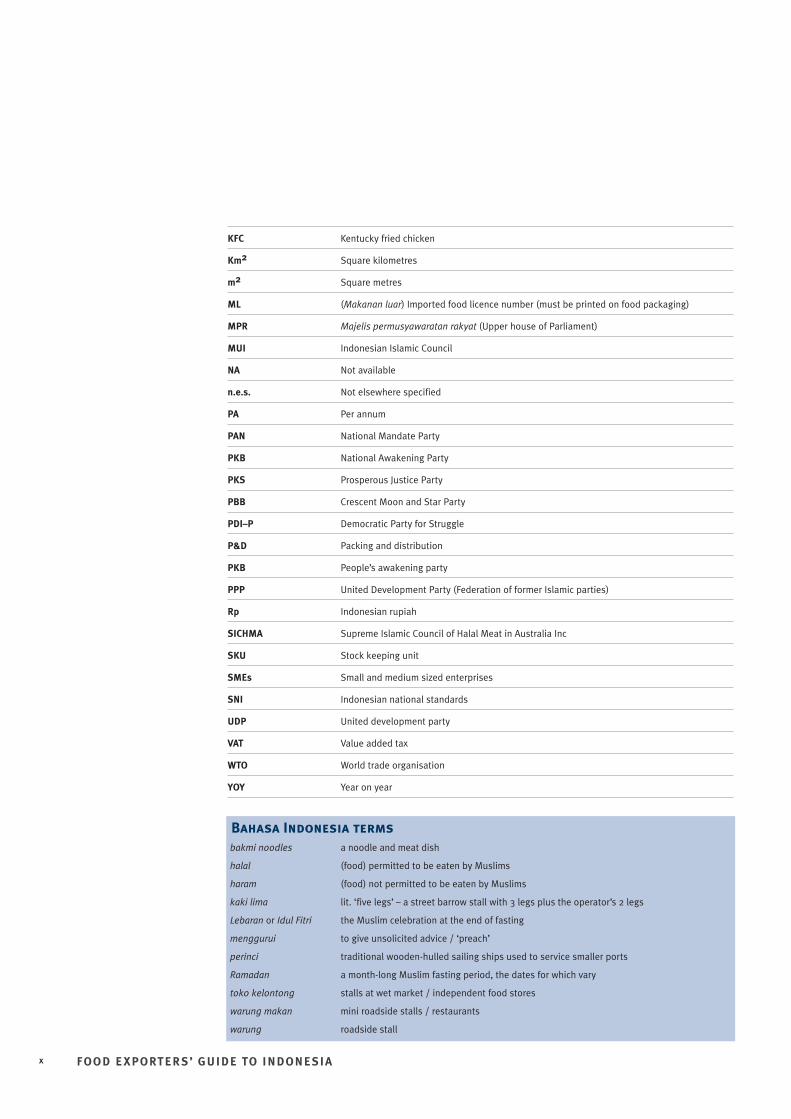

KFC Kentucky fried chicken

Km2 Square kilometres

m2 Square metres

ML (Makanan luar) Imported food licence number (must be printed on food packaging)

MPR Majelis permusyawaratan rakyat (Upper house of Parliament)

MUI Indonesian Islamic Council

NA Not available

n.e.s. Not elsewhere specified

PA Per annum

PAN National Mandate Party

PKB National Awakening Party

PKS Prosperous Justice Party

PBB Crescent Moon and Star Party

PDI–P Democratic Party for Struggle

P&D Packing and distribution

PKB People’s awakening party

PPP United Development Party (Federation of former Islamic parties)

Rp Indonesian rupiah

SICHMA Supreme Islamic Council of Halal Meat in Australia Inc

SKU Stock keeping unit

SMEs Small and medium sized enterprises

SNI Indonesian national standards

UDP United development party

VAT Value added tax

WTO World trade organisation

YOY Year on year

Bahasa Indonesia termsbakmi noodles a noodle and meat dish

halal (food) permitted to be eaten by Muslims

haram (food) not permitted to be eaten by Muslims

kaki lima lit. ‘five legs’ – a street barrow stall with 3 legs plus the operator’s 2 legs

Lebaran or Idul Fitri the Muslim celebration at the end of fasting

menggurui to give unsolicited advice / ‘preach’

perinci traditional wooden-hulled sailing ships used to service smaller ports

Ramadan a month-long Muslim fasting period, the dates for which vary

toko kelontong stalls at wet market / independent food stores

warung makan mini roadside stalls / restaurants

warung roadside stall

FOO D E XPORTER S’ GUIDE TO INDONESIAx

Chapter title

FOO D E XPORTER S’ GUIDE TO INDONESIA xi

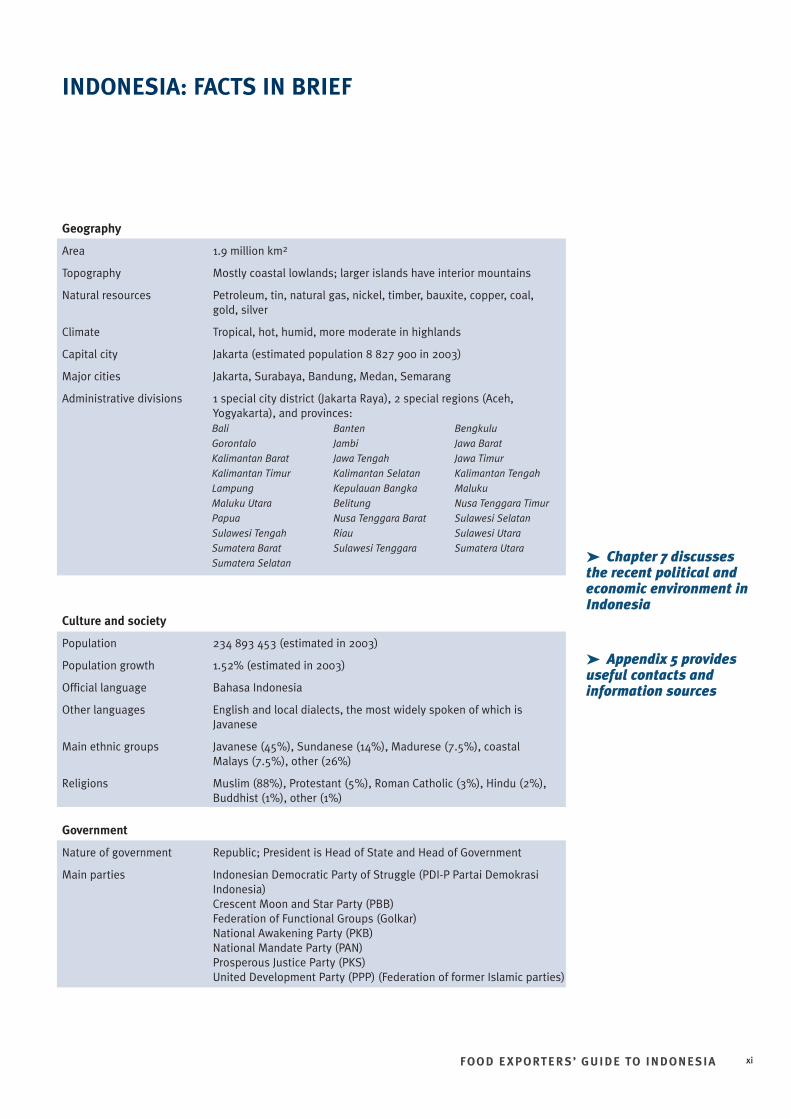

➤ Chapter 7 discussesthe recent political andeconomic environment inIndonesia

➤ Appendix 5 providesuseful contacts andinformation sources

INDONESIA: FACTS IN BRIEF

Geography

Area 1.9 million km2

Topography Mostly coastal lowlands; larger islands have interior mountains

Natural resources Petroleum, tin, natural gas, nickel, timber, bauxite, copper, coal, gold, silver

Climate Tropical, hot, humid, more moderate in highlands

Capital city Jakarta (estimated population 8 827 900 in 2003)

Major cities Jakarta, Surabaya, Bandung, Medan, Semarang

Administrative divisions 1 special city district (Jakarta Raya), 2 special regions (Aceh,Yogyakarta), and provinces:

Culture and society

Population 234 893 453 (estimated in 2003)

Population growth 1.52% (estimated in 2003)

Official language Bahasa Indonesia

Other languages English and local dialects, the most widely spoken of which isJavanese

Main ethnic groups Javanese (45%), Sundanese (14%), Madurese (7.5%), coastal Malays (7.5%), other (26%)

Religions Muslim (88%), Protestant (5%), Roman Catholic (3%), Hindu (2%),Buddhist (1%), other (1%)

Government

Nature of government Republic; President is Head of State and Head of Government

Main parties Indonesian Democratic Party of Struggle (PDI-P Partai DemokrasiIndonesia) Crescent Moon and Star Party (PBB)Federation of Functional Groups (Golkar)National Awakening Party (PKB)National Mandate Party (PAN)Prosperous Justice Party (PKS)United Development Party (PPP) (Federation of former Islamic parties)

Bali GorontaloKalimantan BaratKalimantan TimurLampungMaluku UtaraPapuaSulawesi TengahSumatera BaratSumatera Selatan

BantenJambiJawa TengahKalimantan SelatanKepulauan BangkaBelitungNusa Tenggara BaratRiauSulawesi Tenggara

BengkuluJawa BaratJawa TimurKalimantan TengahMalukuNusa Tenggara TimurSulawesi SelatanSulawesi UtaraSumatera Utara

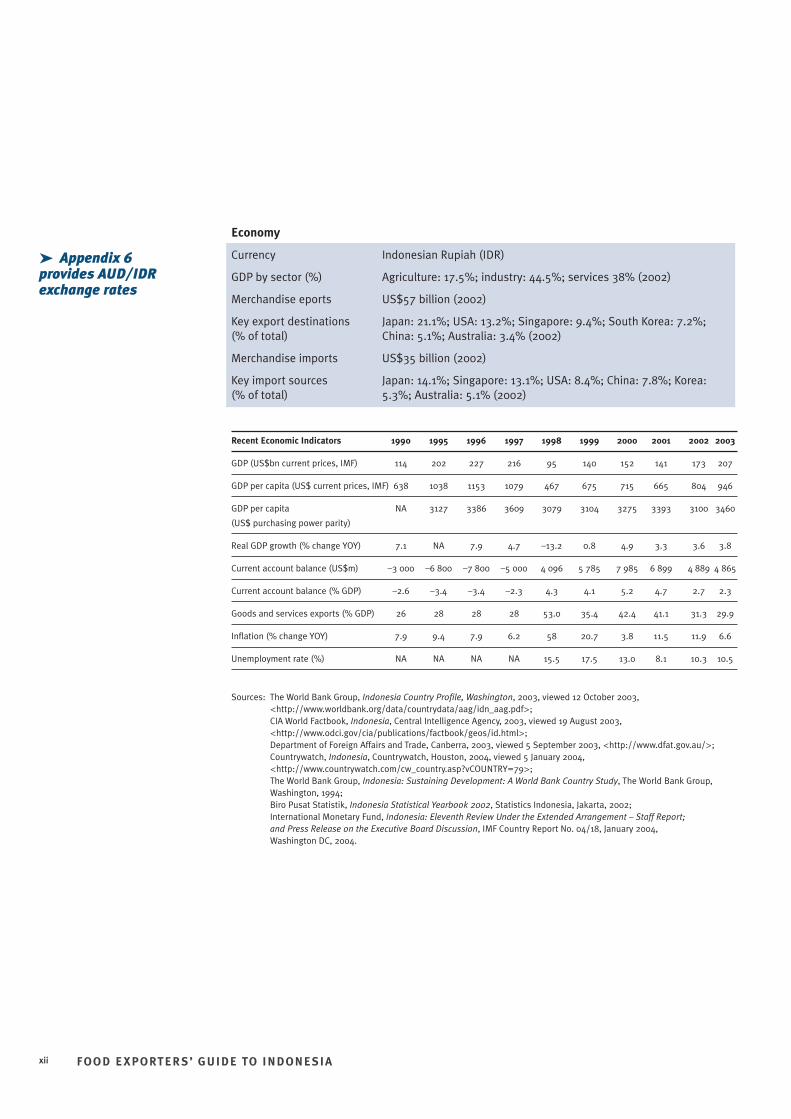

Economy

Currency Indonesian Rupiah (IDR)

GDP by sector (%) Agriculture: 17.5%; industry: 44.5%; services 38% (2002)

Merchandise eports US$57 billion (2002)

Key export destinations Japan: 21.1%; USA: 13.2%; Singapore: 9.4%; South Korea: 7.2%;(% of total) China: 5.1%; Australia: 3.4% (2002)

Merchandise imports US$35 billion (2002)

Key import sources Japan: 14.1%; Singapore: 13.1%; USA: 8.4%; China: 7.8%; Korea: (% of total) 5.3%; Australia: 5.1% (2002)

Recent Economic Indicators 1990 1995 1996 1997 1998 1999 2000 2001 2002 2003

GDP (US$bn current prices, IMF) 114 202 227 216 95 140 152 141 173 207

GDP per capita (US$ current prices, IMF) 638 1038 1153 1079 467 675 715 665 804 946

GDP per capita NA 3127 3386 3609 3079 3104 3275 3393 3100 3460

(US$ purchasing power parity)

Real GDP growth (% change YOY) 7.1 NA 7.9 4.7 –13.2 0.8 4.9 3.3 3.6 3.8

Current account balance (US$m) –3 000 –6 800 –7 800 –5 000 4 096 5 785 7 985 6 899 4 889 4 865

Current account balance (% GDP) –2.6 –3.4 –3.4 –2.3 4.3 4.1 5.2 4.7 2.7 2.3

Goods and services exports (% GDP) 26 28 28 28 53.0 35.4 42.4 41.1 31.3 29.9

Inflation (% change YOY) 7.9 9.4 7.9 6.2 58 20.7 3.8 11.5 11.9 6.6

Unemployment rate (%) NA NA NA NA 15.5 17.5 13.0 8.1 10.3 10.5

Sources: The World Bank Group, Indonesia Country Profile, Washington, 2003, viewed 12 October 2003,<http://www.worldbank.org/data/countrydata/aag/idn_aag.pdf>; CIA World Factbook, Indonesia, Central Intelligence Agency, 2003, viewed 19 August 2003,<http://www.odci.gov/cia/publications/factbook/geos/id.html>; Department of Foreign Affairs and Trade, Canberra, 2003, viewed 5 September 2003, <http://www.dfat.gov.au/>;Countrywatch, Indonesia, Countrywatch, Houston, 2004, viewed 5 January 2004,<http://www.countrywatch.com/cw_country.asp?vCOUNTRY=79>; The World Bank Group, Indonesia: Sustaining Development: A World Bank Country Study, The World Bank Group,Washington, 1994; Biro Pusat Statistik, Indonesia Statistical Yearbook 2002, Statistics Indonesia, Jakarta, 2002; International Monetary Fund, Indonesia: Eleventh Review Under the Extended Arrangement – Staff Report; and Press Release on the Executive Board Discussion, IMF Country Report No. 04/18, January 2004, Washington DC, 2004.

FOO D E XPORTER S’ GUIDE TO INDONESIAxii

➤ Appendix 6provides AUD/IDRexchange rates

Chapter title

1. INTRODUCTION

INTRODUCTION

Indonesia is an important neighbour and trading partner for Australia. It has faced manychallenges during the past decade and more undoubtedly lie ahead. But economic growthhas recovered quite strongly and Indonesia has returned to the top tier of Australian foodexport markets, ranking 6th as an export market for Australia in 2002–3. In both 2001–2 and2002–3 Indonesia outstripped China as a market for Australian food exports.

The scale of the trading relationship is reflected in the large number of Australian companies,big and small, that are represented in Indonesia. Healthy two-way trade and investment tiesare an important element in the broader Australia-Indonesia relationship.

The aim of this handbook is to bring together in a single, concise document a comprehensiveoverview of the Indonesian food market that provides Australian exporters with practical andrealistic information on this important market. It will better equip Australian food exporters toexplore new opportunities to work with local partners in the Indonesian market for theirmutual benefit.

Australia’s food exports to Indonesia are dominated by live cattle, beef, dairy products andwheat and flour. But a host of niche high value-added products, many produced by small andmedium sized Australian companies, find good markets in Indonesia and Austrade seespromising potential for further growth in a range of food product segments.

The handbook provides description and analysis of:

• The Indonesian consumer (Chapter 2)

• Retail and food service trends (Chapter 3)

• Supply chain issues (Chapter 4)

• The business environment (Chapter 5)

• Australian food exports to Indonesia (Chapter 6)

• The political and economic environment (Chapter 7)

Following the main chapters of the handbook, a series of appendices provide more detaileddata on:

• Australian food exports to Indonesia (Appendices 1–3)

• Indonesian tariffs on agricultural and food products (Appendix 4)

• Other useful contacts, information and information sources (Appendices 5–7)

The information in the handbook draws on a mix of fieldwork, conducted in July andSeptember/October 2003, and a wide range of Indonesian, Australian and internationalsources. The bibliography contains a listing of the sources used in compiling the handbook.

The handbook was commissioned by the Australian Department of Agriculture, Fisheries andForestry in June 2003 as part of its work in support of the Australia – Indonesia MinisterialForum’s Working Group on Agriculture and Food Cooperation. Since 1992, the Working Grouphas provided an enduring and valuable mechanism for developing linkages between thegovernment and private sectors in Indonesia and Australia. There is a continuing strong level ofmutual commitment to this bilateral agricultural and food forum and its work programs.

FOO D E XPORTER S’ GUIDE TO INDONESIA 1

Chapter 1 Introduction

Image 1.2 Makro store, Jakarta

Image 1.1 Fresh fruit street stall,Jakarta

Image 1.3 Australian fresh fruitdisplay, Sogo Supermarket,Plaza Indonesia

FOO D E XPORTER S’ GUIDE TO INDONESIA2

Chapter 1 Introduction

2. INDONESIAN CONSUMERS

Overview• Indonesia has a young and increasing population. Half of the population is under 25 and

30% are under 14. Purchasing power has recovered in recent years as solid economicgrowth has been restored.

• The country is urbanising rapidly, which is leading to mixing and melding of many traditions.It is also exposing consumers to international tastes and trends.

• In 2003, households with average monthly spending over Rp1 250 000 (approx.A$200/month) accounted for 12% of households nationally and 26% of households inJakarta.

• At lower incomes, typical diets include rice with some modest garnishing and vegetables.Moderately higher incomes permit a more varied diet with a significantly higher share ofspending on fish, meat, eggs, dairy and fruit. Spending on prepared foods rises rapidly with income.

• Urban Indonesians have traditionally eaten out a lot. Their spending on convenience foodsis also rising strongly.

• Almost 90% of Indonesians are Muslim. Most observe Islamic dietary laws.

• Although the Indonesian economy is recovering and growing steadily, the Asian economiccrisis has left consumers with a stronger focus on value for money.

• Looking to the future, and assuming moderate economic growth, per capita consumption of temperate fruit, poultry, beef, other meat, baked products and dairy goods will grow most rapidly. Consumption of cereals will grow slowly, except for wheat (and flour-basedproducts).

• Packaged goods likely to enjoy strong growth include baby food and confectionery. Sales of frozen and chilled foods as well as ready to eat meals will also grow, although off a low base.

Basic indicatorsIndonesia is multi-ethnic with many languages and cultures, wide regional differences and fast-changing political and economic circumstances. However, modernisation is bringing thelifestyles of Indonesian urban consumers across the country closer together.

Internationalisation is also creating some similarities between consumption patterns inIndonesia and countries like Australia, although many big differences remain. Indonesia’sdiversity means that its people’s eating habits defy any neat categorisation except in suchobvious respects as the fact that Muslims generally adhere strictly to halal food rules.

While tradition exists and is important in Indonesia, its society is mobile both vertically andlaterally. People move around the country and up and down the social ladder. Jakarta, thebiggest single market, has people from every ethnic group in Indonesia. In this sense it is agood market to learn in.

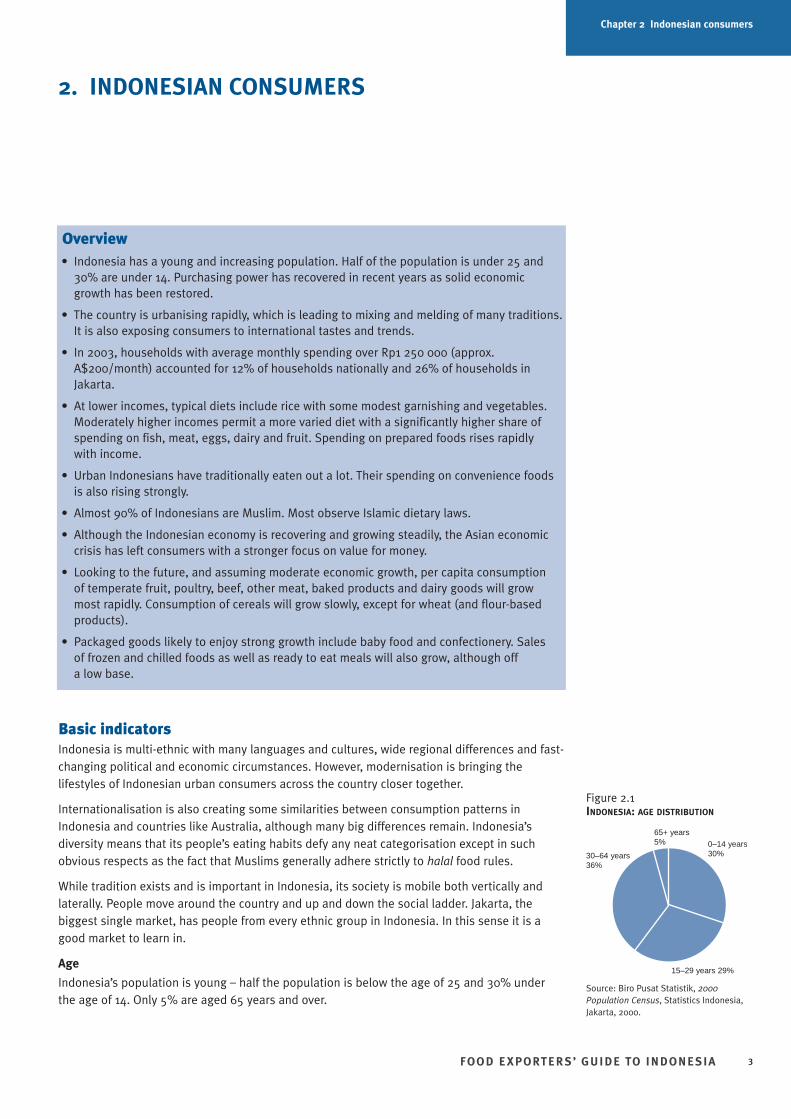

Age

Indonesia’s population is young – half the population is below the age of 25 and 30% underthe age of 14. Only 5% are aged 65 years and over.

FOO D E XPORTER S’ GUIDE TO INDONESIA 3

Chapter 2 Indonesian consumers

Figure 2.1INDONESIA: AGE DISTRIBUTION

Source: Biro Pusat Statistik, 2000Population Census, Statistics Indonesia,Jakarta, 2000.

0–14 years30%

65+ years5%

15–29 years 29%

30–64 years36%

Chapter 2 Indonesian consumers

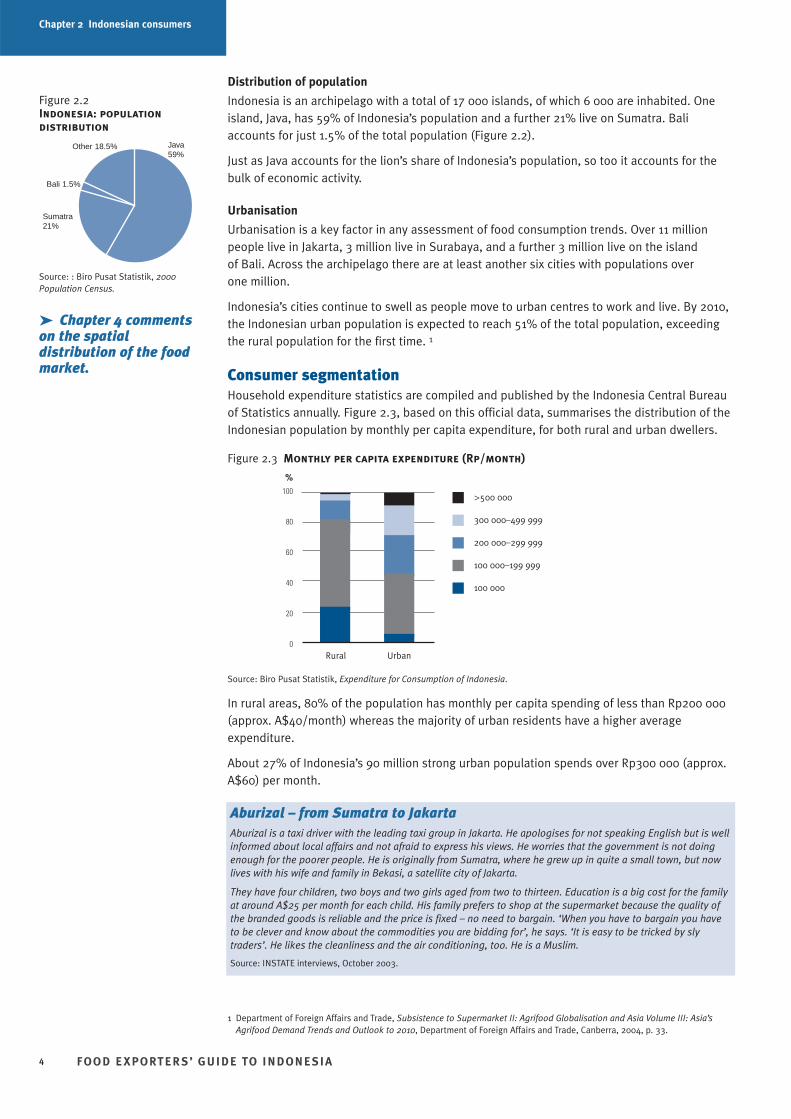

Distribution of population

Indonesia is an archipelago with a total of 17 000 islands, of which 6 000 are inhabited. Oneisland, Java, has 59% of Indonesia’s population and a further 21% live on Sumatra. Baliaccounts for just 1.5% of the total population (Figure 2.2).

Just as Java accounts for the lion’s share of Indonesia’s population, so too it accounts for thebulk of economic activity.

Urbanisation

Urbanisation is a key factor in any assessment of food consumption trends. Over 11 millionpeople live in Jakarta, 3 million live in Surabaya, and a further 3 million live on the island of Bali. Across the archipelago there are at least another six cities with populations over one million.

Indonesia’s cities continue to swell as people move to urban centres to work and live. By 2010,the Indonesian urban population is expected to reach 51% of the total population, exceedingthe rural population for the first time. 1

Consumer segmentationHousehold expenditure statistics are compiled and published by the Indonesia Central Bureauof Statistics annually. Figure 2.3, based on this official data, summarises the distribution of theIndonesian population by monthly per capita expenditure, for both rural and urban dwellers.

Figure 2.3 Monthly per capita expenditure (Rp/month)

Source: Biro Pusat Statistik, Expenditure for Consumption of Indonesia.

In rural areas, 80% of the population has monthly per capita spending of less than Rp200 000(approx. A$40/month) whereas the majority of urban residents have a higher averageexpenditure.

About 27% of Indonesia’s 90 million strong urban population spends over Rp300 000 (approx.A$60) per month.

FOO D E XPORTER S’ GUIDE TO INDONESIA4

Aburizal – from Sumatra to JakartaAburizal is a taxi driver with the leading taxi group in Jakarta. He apologises for not speaking English but is wellinformed about local affairs and not afraid to express his views. He worries that the government is not doingenough for the poorer people. He is originally from Sumatra, where he grew up in quite a small town, but nowlives with his wife and family in Bekasi, a satellite city of Jakarta.

They have four children, two boys and two girls aged from two to thirteen. Education is a big cost for the familyat around A$25 per month for each child. His family prefers to shop at the supermarket because the quality ofthe branded goods is reliable and the price is fixed – no need to bargain. ‘When you have to bargain you haveto be clever and know about the commodities you are bidding for’, he says. ‘It is easy to be tricked by slytraders’. He likes the cleanliness and the air conditioning, too. He is a Muslim.

Source: INSTATE interviews, October 2003.

Figure 2.2Indonesia: populationdistribution

Source: : Biro Pusat Statistik, 2000Population Census.

%100

80

60

40

20

0UrbanRural

>500 000

300 000–499 999

200 000–299 999

100 000–199 999

100 000

Java59%

Other 18.5%

Sumatra21%

Bali 1.5%

1 Department of Foreign Affairs and Trade, Subsistence to Supermarket II: Agrifood Globalisation and Asia Volume III: Asia’sAgrifood Demand Trends and Outlook to 2010, Department of Foreign Affairs and Trade, Canberra, 2004, p. 33.

➤ Chapter 4 commentson the spatialdistribution of the foodmarket.

Chapter 2 Indonesian consumers

Urbanisation and the rise in income associated with this transition is leading to lifestylechanges that are influencing consumer purchases and food and entertainment choices.

Households are shrinking due to the smaller number of children per family as well as the trendaway from extended families. Today, meals in urban families are more likely to include justparents and children rather than a larger extended family. Single and married women areworking more, leaving less time for shopping and cooking. This drives convenience shoppingand eating.

Urban – rural differences

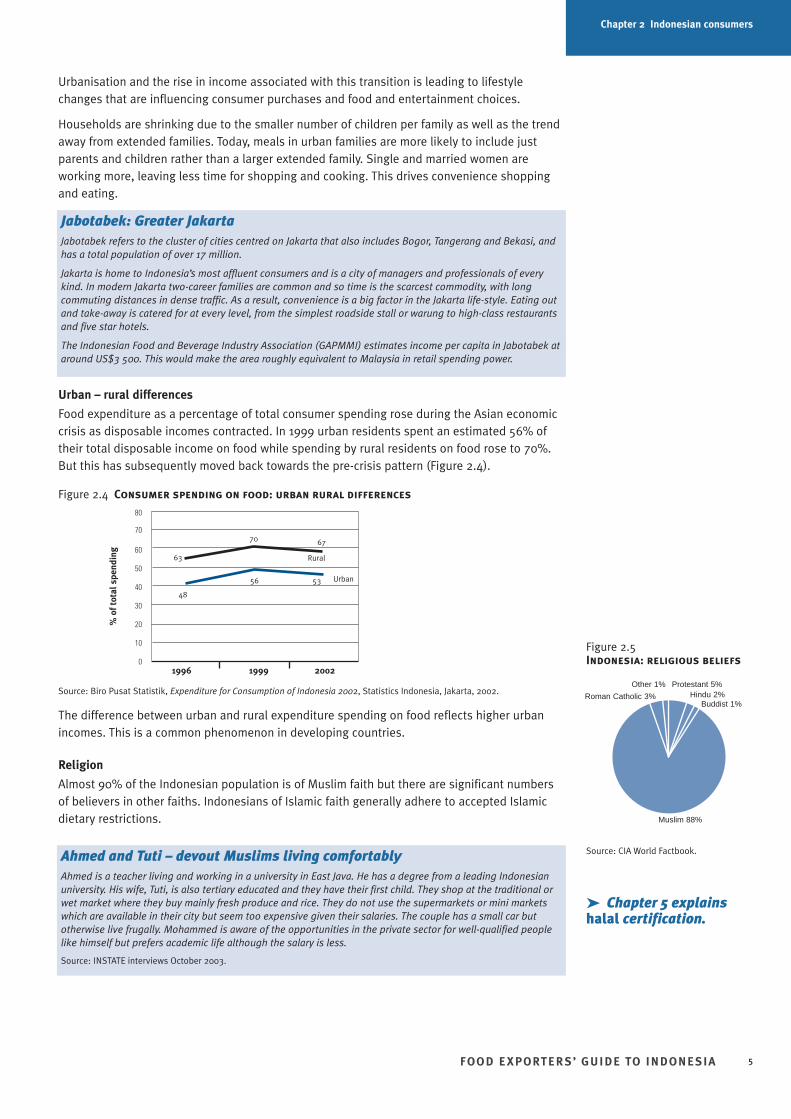

Food expenditure as a percentage of total consumer spending rose during the Asian economiccrisis as disposable incomes contracted. In 1999 urban residents spent an estimated 56% oftheir total disposable income on food while spending by rural residents on food rose to 70%.But this has subsequently moved back towards the pre-crisis pattern (Figure 2.4).

Figure 2.4 Consumer spending on food: urban rural differences

Source: Biro Pusat Statistik, Expenditure for Consumption of Indonesia 2002, Statistics Indonesia, Jakarta, 2002.

The difference between urban and rural expenditure spending on food reflects higher urbanincomes. This is a common phenomenon in developing countries.

Religion

Almost 90% of the Indonesian population is of Muslim faith but there are significant numbersof believers in other faiths. Indonesians of Islamic faith generally adhere to accepted Islamicdietary restrictions.

FOO D E XPORTER S’ GUIDE TO INDONESIA 5

Jabotabek: Greater JakartaJabotabek refers to the cluster of cities centred on Jakarta that also includes Bogor, Tangerang and Bekasi, andhas a total population of over 17 million.

Jakarta is home to Indonesia’s most affluent consumers and is a city of managers and professionals of everykind. In modern Jakarta two-career families are common and so time is the scarcest commodity, with longcommuting distances in dense traffic. As a result, convenience is a big factor in the Jakarta life-style. Eating outand take-away is catered for at every level, from the simplest roadside stall or warung to high-class restaurantsand five star hotels.

The Indonesian Food and Beverage Industry Association (GAPMMI) estimates income per capita in Jabotabek ataround US$3 500. This would make the area roughly equivalent to Malaysia in retail spending power.

➤ Chapter 5 explainshalal certification.

Figure 2.5Indonesia: religious beliefs

Source: CIA World Factbook.

Buddist 1%

Protestant 5%

Muslim 88%

Hindu 2%Other 1%

80

70

60

50

40

30

20

10

01996 1999 2002

Urban

Rural63

% o

f tot

al s

pend

ing

48

56

70 67

53

Ahmed and Tuti – devout Muslims living comfortablyAhmed is a teacher living and working in a university in East Java. He has a degree from a leading Indonesianuniversity. His wife, Tuti, is also tertiary educated and they have their first child. They shop at the traditional orwet market where they buy mainly fresh produce and rice. They do not use the supermarkets or mini marketswhich are available in their city but seem too expensive given their salaries. The couple has a small car butotherwise live frugally. Mohammed is aware of the opportunities in the private sector for well-qualified peoplelike himself but prefers academic life although the salary is less.

Source: INSTATE interviews October 2003.

Roman Catholic 3%

Indonesians of Hindu belief do not follow a central set of dietary rules, but devout Hindus arelacto-vegetarian. That is, they consume no red meat, especially not pork or beef, and onlyconsume milk-related livestock products, such as milk, curd, cheese and yoghurt. SomeIndonesian Hindus do eat poultry and fish. 2

The peak business periods for the food industry are during the religious holiday periods whenconsumer spending increases, driving up demand for basics such as flour, sugar, eggs, freshand dried fruits, poultry and meat, and luxury and snack items such as cheese, cakes, cookiesand pastries. The most important holiday periods are:

• Ramadan – the month-long Muslim fasting period in which, surprisingly, food consumptiongoes up significantly

• Lebaran (also known as Idul Fitri) – the celebration of the end of Ramadan

• Chinese New Year.

Stores also take advantage of the Christmas season and decorate and promote festive foodssuch as special fruits, sweets and pastries. Western celebrations, such as Valentine’s Day, havealso become trendy among upper-level restaurants in Indonesia. 3

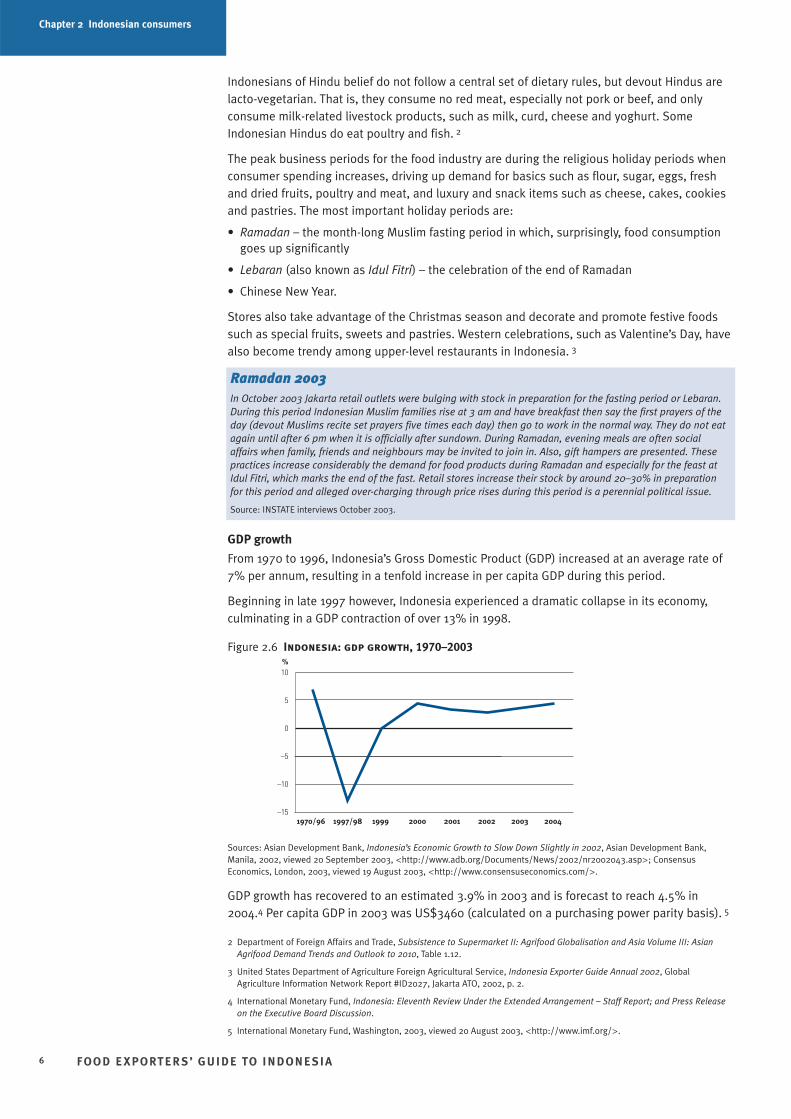

GDP growth

From 1970 to 1996, Indonesia’s Gross Domestic Product (GDP) increased at an average rate of7% per annum, resulting in a tenfold increase in per capita GDP during this period.

Beginning in late 1997 however, Indonesia experienced a dramatic collapse in its economy,culminating in a GDP contraction of over 13% in 1998.

Figure 2.6 Indonesia: gdp growth, 1970–2003

Sources: Asian Development Bank, Indonesia’s Economic Growth to Slow Down Slightly in 2002, Asian Development Bank,Manila, 2002, viewed 20 September 2003, <http://www.adb.org/Documents/News/2002/nr2002043.asp>; ConsensusEconomics, London, 2003, viewed 19 August 2003, <http://www.consensuseconomics.com/>.

GDP growth has recovered to an estimated 3.9% in 2003 and is forecast to reach 4.5% in2004.4 Per capita GDP in 2003 was US$3460 (calculated on a purchasing power parity basis). 5

FOO D E XPORTER S’ GUIDE TO INDONESIA6

Chapter 2 Indonesian consumers

2 Department of Foreign Affairs and Trade, Subsistence to Supermarket II: Agrifood Globalisation and Asia Volume III: AsianAgrifood Demand Trends and Outlook to 2010, Table 1.12.

3 United States Department of Agriculture Foreign Agricultural Service, Indonesia Exporter Guide Annual 2002, GlobalAgriculture Information Network Report #ID2027, Jakarta ATO, 2002, p. 2.

4 International Monetary Fund, Indonesia: Eleventh Review Under the Extended Arrangement – Staff Report; and Press Releaseon the Executive Board Discussion.

5 International Monetary Fund, Washington, 2003, viewed 20 August 2003, <http://www.imf.org/>.

Ramadan 2003In October 2003 Jakarta retail outlets were bulging with stock in preparation for the fasting period or Lebaran.During this period Indonesian Muslim families rise at 3 am and have breakfast then say the first prayers of theday (devout Muslims recite set prayers five times each day) then go to work in the normal way. They do not eatagain until after 6 pm when it is officially after sundown. During Ramadan, evening meals are often socialaffairs when family, friends and neighbours may be invited to join in. Also, gift hampers are presented. Thesepractices increase considerably the demand for food products during Ramadan and especially for the feast atIdul Fitri, which marks the end of the fast. Retail stores increase their stock by around 20–30% in preparationfor this period and alleged over-charging through price rises during this period is a perennial political issue.

Source: INSTATE interviews October 2003.

%10

5

0

–5

–10

–151970/96 1997/98 1999 2000 2001 2002 2003 2004

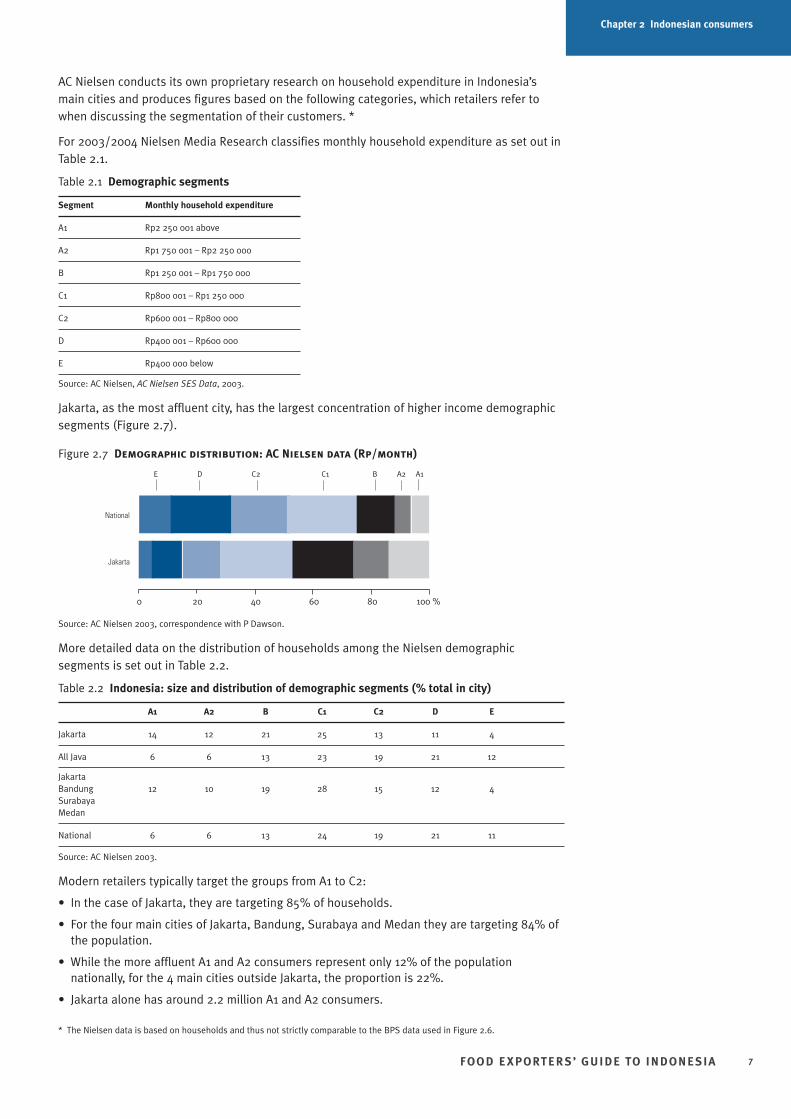

AC Nielsen conducts its own proprietary research on household expenditure in Indonesia’smain cities and produces figures based on the following categories, which retailers refer towhen discussing the segmentation of their customers. *

For 2003/2004 Nielsen Media Research classifies monthly household expenditure as set out inTable 2.1.

Table 2.1 Demographic segments

Segment Monthly household expenditure

A1 Rp2 250 001 above

A2 Rp1 750 001 – Rp2 250 000

B Rp1 250 001 – Rp1 750 000

C1 Rp800 001 – Rp1 250 000

C2 Rp600 001 – Rp800 000

D Rp400 001 – Rp600 000

E Rp400 000 below

Source: AC Nielsen, AC Nielsen SES Data, 2003.

Jakarta, as the most affluent city, has the largest concentration of higher income demographicsegments (Figure 2.7).

Figure 2.7 Demographic distribution: AC Nielsen data (Rp/month)

Source: AC Nielsen 2003, correspondence with P Dawson.

More detailed data on the distribution of households among the Nielsen demographicsegments is set out in Table 2.2.

Table 2.2 Indonesia: size and distribution of demographic segments (% total in city)

A1 A2 B C1 C2 D E

Jakarta 14 12 21 25 13 11 4

All Java 6 6 13 23 19 21 12

JakartaBandung 12 10 19 28 15 12 4SurabayaMedan

National 6 6 13 24 19 21 11

Source: AC Nielsen 2003.

Modern retailers typically target the groups from A1 to C2:

• In the case of Jakarta, they are targeting 85% of households.

• For the four main cities of Jakarta, Bandung, Surabaya and Medan they are targeting 84% ofthe population.

• While the more affluent A1 and A2 consumers represent only 12% of the populationnationally, for the 4 main cities outside Jakarta, the proportion is 22%.

• Jakarta alone has around 2.2 million A1 and A2 consumers.

FOO D E XPORTER S’ GUIDE TO INDONESIA 7

Chapter 2 Indonesian consumers

E D C2 C1 B A2 A1

0 20 40 60 80 100 %

National

Jakarta

* The Nielsen data is based on households and thus not strictly comparable to the BPS data used in Figure 2.6.

What Indonesians eat

Differences among income groups

Table 2.3 sets out data on food spending for a range of different income and spending groups.

Key points to note include:

• At lower incomes typical diets include rice with some modest garnishing and vegetables.

• Moderately higher incomes permit a more varied diet with a significantly higher share ofspending on fish, meat, eggs, dairy and fruit.

Table 2.3 Average per capita monthly expenditure by commodity group, 2002 (Rp)

Expenditure ClassCommodity Group 80 000– 100 000– 150 000– 200 000– 300 000–

99 999 149 999 199 999 299 999 499 999 >500 000

cereals 22 334 22 770 23 750 24 215 24 287 22 851

tubers 620 762 978 1 323 1 775 2 258

fish 4 061 6 744 9 708 12 910 17 289 23 253

meat 1 004 2 456 4 919 8 651 15 050 26 165

eggs and milk 2 275 4 154 6 147 9 807 14 880 24 887

vegetables 6 221 7 441 9 262 11 468 14 174 17 315

legumes 3 332 3 986 4 430 4 915 5 776 6 269

fruits 1 623 2 886 4 598 7 176 12 229 22 782

oil and fats 2 913 3 547 4 356 5 179 6 236 7 561

beverages 3 230 4 167 5 119 6 195 7 568 10 087

spices 1 777 2 361 3 038 3 771 4 901 6 148

other food items 1 108 1 866 2 622 3 941 5 771 8 443

prepared food and beverages 7 099 12 156 18 023 27 460 46 792 89 187

alcoholic beverages 23 37 108 133 206 702

tobacco and betel 5 447 9 022 13 052 16 623 21 103 25 643

Total av. food spending (Rp / month) 63 067 84 355 110 110 143 767 198 037 293 551

Source: Biro Pusat Statistik, Expenditure for Consumption of Indonesia.

• Spending on prepared foods rises steadily with income: the top income group spends 12 times as much as the bottom income group in money terms and three times as much interms of the share of food spending.

• Cereals, including wheat, corn flour and rice, remain the staple for all groups and spendingon these staples in money terms is quite steady at all income levels.

Table 2.4 below presents the percentage shares of spending on various commodity groups foreach income group.

FOO D E XPORTER S’ GUIDE TO INDONESIA8

Chapter 2 Indonesian consumers

Halimah – a commuting professional in JakartaHalimah is a young graduate, still single. She commutes each day from one of Jakarta’s satellite towns toJakarta to work each day in a commercial research organisation. It takes two hours in the morning to get towork and three hours in the evening to get home. ‘The buses are really crowded,’ she says, ‘so sometimes youhave to stand up all the way.’

She shops at the nearest supermarket, Hero, in her home town. Halimah says: ‘I just don’t have the time toshop around’. She likes the cleanliness, too. Halimah is a Muslim so she checks packages to see what theingredients are and to see if the product is certified halal. She says her Muslim friends do the same. Halimah’smother still does most of her shopping at the wet markets where she can get things more cheaply.

Halimah and her family are in the B demographic.

Source: INSTATE interview, October 2003.

Table 2.4 Average per capita monthly expenditure by commodity group, 2002 (% share of total spending on food)

Expenditure ClassCommodity Group 80 000– 100 000– 150 000– 200 000– 300 000–

99 999 149 999 199 999 299 999 499 999 >500 000

cereals 35% 27% 22% 17% 12% 8%

tubers 1% 1% 1% 1% 1% 1%

fish 6% 8% 9% 9% 9% 8%

meat 2% 3% 4% 6% 8% 9%

eggs and milk 4% 5% 6% 7% 8% 8%

vegetables 10% 9% 8% 8% 7% 6%

legumes 5% 5% 4% 3% 3% 2%

fruits 3% 3% 4% 5% 6% 8%

oil and fats 5% 4% 4% 4% 3% 3%

beverages 5% 5% 5% 4% 4% 3%

spices 3% 3% 3% 3% 2% 2%

other food items 2% 2% 2% 3% 3% 3%

prepared food and beverages 11% 14% 16% 19% 24% 30%

alcoholic beverages 0% 0% 0% 0% 0% 0%

tobacco and betel 9% 11% 12% 12% 11% 9%

Total 100% 100% 100% 100% 100% 100%

Share of income on food spending in each class 70% 67% 63% 58% 50% < 50%

Source: Biro Pusat Statistik, Expenditure for Consumption of Indonesia.

Recent growth trends

Consumption of meat has grown steadily in line with economic development. Chicken inparticular is the meat of choice — Indonesians now eat twice as much chicken as beef. Beefconsumption fell sharply during the late 1990s but has since recovered quite strongly.

Consumption of milk almost tripled in the three decades to 1997. Consumption of other dairyproducts has increased significantly, but from a tiny base (see Table 2.5).

Fruit, and temperate fruit in particular, represents an increasing part of the diet of urbanIndonesians. 6

Packaged food sales have grown quite strongly in nominal terms during the past five years. 7

However a good part of this nominal growth has been offset by inflation. Per capita sales of

FOO D E XPORTER S’ GUIDE TO INDONESIA 9

Chapter 2 Indonesian consumers

The Tanujaja family – affluent but careful Iwan Tanujaja and his wife, Dewi, operate a furniture manufacturing and export business based in a satellitetown of Jakarta. They have two daughters. Iwan’s father is Javanese and a Muslim so Iwan is a Muslim too andDewi has converted to Islam although her parents are Chinese Indonesians, as is Iwan’s mother. They observethe main Muslim practices including the fast of Ramadan.

Dewi mainly shops at Matahari and Makro. Makro prices are good, possibly cheaper than Hero and both storesare close to her house. They eat Chinese and Indonesian dishes with more chicken than beef or lamb. She buyssome imported meat when that is the best kind for the recipe – also sometimes, imported fruit. They are in theA1 demographic but they live simply outside the main city. ‘It is important for our girls to get a good education’,says Iwan, ‘and that is very expensive.’

Source: INSTATE interview, October 2003.

Image 2.1 Meat display, Herosupermarket

Image 2.2 Indomilk display,Kemang

6 FAOSTAT Statistical Databases, Food and Agriculture Organisation of the United Nations, 2003, viewed 2 October 2003,<http://apps.fao.org/>.

7 Euromonitor, Packaged Food in Indonesia, London, 2003, viewed October 2003,<http://www.euromonitor.com/Packaged_Food_in_Indonesia>.

Chapter 2 Indonesian consumers

packaged food in 2002 were estimated at US$29, just over 10% the level of nearby Singapore.That said, packaged food sales are growing very rapidly. Between 1998 and 2002, sales ofbakery products grew by 31% in value terms (32% in volume terms). Other fast-growingcategories during that time included:

• packaged noodles: sales up 31% (39% volume growth).

• confectionery: sales up 83% (36% volume growth).

• savoury snacks: sales up 88% (42% volume growth).

• oils and fats: sales up 21% (39% volume growth).

Smaller categories that have grown strongly include:

• baby food: sales up 90% (50% volume growth).

• ice-cream: sales up 70% (22% volume growth).

• ready-to-eat meals: sales up 37% (36 volume growth).

Convenience foods

Indonesian consumers are increasingly purchasing convenience food. More urban women areentering the workforce and working after marriage and having children. With less timeavailable for shopping and cooking, they have a growing focus on convenience.

More generally, the rising pace of modern life in urban centres is driving up demand for ready-to-cook / ready-to-eat food, and Indonesians returning from study or work abroad are alsoimporting the tendency to eat on-the-run. The increase in sales of prepared foods evident inTables 2.3 and 2.4 above illustrates this fast growing trend.

The trend towards convenience foods is also consistent with the traditional Indonesian love ofsnacking. Markets and shops offer a wide range of snacks, such as fried, baked and sweetfoods, including many traditional cakes and jellies.

Eating out

The number of household appliances in Indonesia for cooking is low. For example, in thecapital city of Jakarta, only an estimated 43% of households have a refrigerator, 27% have agas stove and 10% have a microwave oven. 8 So Indonesians eat a lot away from home.

FOO D E XPORTER S’ GUIDE TO INDONESIA10

Image 2.4 Durian fruit,Carrefour, Jakarta

Image 2.3 Fruit display, Jakartasupermarket

Image 2.5 In-store bakery,Carrefour, Jakarta

Hot climate, cold refreshment‘Walls’ ice cream dominates the local market with over 40% market share. Its competitors are local brand icecreams including ‘Diamond’ and ‘Campina’.

Walls is manufactured by Unilever which, as in many other markets, has a very diversified operation inIndonesia producing oils and fats, ice cream and sauces, dressings and condiments.

Source: INSTATE research.

Instant noodlesConsumption of instant noodles grew strongly during the first half of the 1990s, rising from 4.7 billion packs in1992 to almost 8.6 billion packs by 1997, making Indonesia the world’s second largest consumer of instantnoodles, behind only China.

Consumption was hit by the economic crisis and fell from 42 packs per capita in 1997 to 39 packs in 1998, buthas since bounced back strongly and reached 48 packs per capita by 2002.

Indofood, the market leader, has the factory capacity to make 13 billion packs of instant noodles per year(which would weigh in at 3.6 million tonnes). Indofood had a market share of 88% in 2002.

During the lean times, Indofood produced cheaper products, to retain what market share it could, but morerecently it has been concentrating on premium products more precisely targeted to market segments toincrease its margins. One successful strategy has been to offer instant noodle flavours based on traditionalflavours from the various regions of Indonesia.

Sources: United States Department of Agriculture Foreign Agricultural Service, Indonesian Grain and Feed Annual 1999, GlobalAgriculture Information Network Report #ID9031, Jakarta ATO, 1999; Euromonitor, Packaged Food in Indonesia, London, 2003,viewed October 2003, <http://www.euromonitor.com/Packaged_Food_in_Indonesia>; PT Indofood Sukses Makmur Tbk, PTIndofood Sukses Makmur Tbk Annual Report 2002, Jakarta, 2002; INSTATE interview; Department of Foreign Affairs and Trade,Subsistence to Supermarket II: Agrifood Globalisation and Asia Volume III: Asian Agrifood Demand Trends and Outlook to 2010.

➤ Chapter 3 alsoidentifies productssought by particularcompanies and outlettypes.

8 United States Department of Agriculture Foreign Agricultural Service, Indonesia Exporter Guide Annual 2002, p. 3.

Chapter 2 Indonesian consumers

This is partly traditional, roadside food stalls for example, have always been common inIndonesian cities.

In Jakarta it is also a matter of the lifestyle imposed by the nature of the city. Many workers inJakarta have left families behind in Central Java, East Java, even Sumatra, and visit them only afew times each year. In the meantime they live in boarding houses or dormitory-typeaccommodation in Jakarta. Often employers provide such accommodation to their staff and, insome cases, meals are provided at a dining hall. If not, then out-of-town employees eat at foodstalls or restaurants of various kinds, depending upon income.

Many more Jakarta residents, including many middle-class professionals, live in satellite townssuch as Bogor, Tangerang or Bekasi. It is quite usual for these workers to commute two ormore hours in each direction to attend work. They are natural customers for prepared foodoutlets of various kinds, depending upon income.

Urban and higher income Indonesians are eclectic eaters who try the 30 or more differentcuisines from within the huge archipelago as well as imported tastes, including Asian andwestern flavours.

Fast food boomed in the early and mid–1990s as the population developed a taste for Westernfoods and food on-the-run. Fast food, and especially higher end food service outlets declinedfor several years following the Asian economic crisis and were again buffeted by more recentevents such as the Bali bombings.

Packaging

The Asian economic crisis caused consumers to be much more price-conscious than previouslyand they remain so. Suppliers and retailers have addressed this challenge in various ways:

• Products have been offered in smaller packs—an example is the sale of disposable nappiesin single unit packs. Packs of many other personal products including cosmetics remainsmall.

• Large ‘economy packs’ of daily essentials have become popular with lower incomeconsumers.

• New forms of cheap packaging for products traditionally bought in bulk have gainedpopularity—for example, soft pouch packs of cooking oil.

• Cheaper alternatives to foreign-made or foreign-branded products with simpler packaginghave emerged. The energy drink powder Hema, which is a substitute for canned soft drink, isenjoying increasing market share and is a good example of this phenomenon.

More generally, however, the trend in consumer preference to packaged and branded productstill has strong momentum, even for staple products that were traditionally sold in bulk at thewet markets. Branded product is perceived as carrying an assurance of quality and healthprotection.

Future trends

A recent Australian Government report, Subsistence to Supermarket II: Agrifood Globalisationand Asia Volume III: Asian Agrifood Demand Trends and Outlook to 2010, provides estimates oflikely per capita consumption growth trends to 2010.

FOO D E XPORTER S’ GUIDE TO INDONESIA 11

Shinta – A taste for styleShinta, a young Indonesian mother, settles in to study the menu at Tony Roma’s, an upscale restaurant chain,while her nursemaid attends to her baby. She has been married for only a year. Her father is a general in thearmy and they live in a big house in Menteng. There is a flat for her and her young husband and the baby. Herhusband works in the finance industry in Jakarta. Soon he joins her. The restaurant is fairly full by 8pm and themanager says it will improve after that time. This is a restaurant for the A1 demographic. This group can also befound in the stylish restaurants and coffee shops of five star hotels like the Grand Hyatt and the Regent and inthe designer label stores of Plaza Indonesia.

Source: INSTATE interview, October 2003.

Chapter 2 Indonesian consumers

Under its medium growth scenario the report forecasts that growth will be strongest in percapita consumption of:

• temperate fruit

• poultry, beef and other meat

• dairy products.

Growth is likely to be slowest in consumption of cereals, although wheat consumption isforecast to grow considerably more rapidly than rice.

According to Euromonitor,11 in the packaged goods segment, likely trends include:

• steady but not spectacular growth in staples such as grains and oils

• moderating growth in sales of noodles

• continuing growth in sales of baked products

• strong growth in sales of dairy products, baby food and confectionery

• in smaller categories, reasonable, but not spectacular growth in sales of frozen and chilledfoods as well as ready-to-eat meals.

The next chapter describes trends in retail and food service in Indonesia, while Chapter 4describes the supply chains to the Indonesian market.

FOO D E XPORTER S’ GUIDE TO INDONESIA12

➤ The food servicesector is described inmore detail in Chapter 3.

Impact of the Asian economic crisisA lot of publicly available commentary on the Indonesian food market highlights the impact of the crisis onfood consumption patterns. Some of the effects were relatively short-lived and have now faded. These include:

• compression of urban income levels (as the more affluent were hardest hit)

• a lessened focus on nutrition versus price*

• a downturn in eating out

• a slowing in modern retail development as shoppers sought cheaper products through traditional shops andmarkets

Other changes have been more long lasting. These include:

• an increased consumer focus on value for money

• the continued growth of generic brands

• a wider range of packaging options—including smaller packages

• a reduction in brand loyalty. 9

Prior to the crisis, affluent Indonesians were described as more concerned about taste, freshness andpackaging than price. 10 Whether or not that was true then, it applies to few Indonesians now. One in-marketoperator commented recently that ‘The market is very price sensitive. Although Australian beef sold insupermarkets is of better quality, wealthy shoppers will readily go to the wet market if the price climbs toohigh.’

Source: INSTATE research and interviews, October 2003.

* see for example, the assessments in United States Department of Agriculture Foreign Agricultural Service, Indonesia ExporterGuide Annual 2002, p 4.

9 United States Department of Agriculture Foreign Agricultural Service, Indonesia Exporter Guide Annual 2002, GlobalAgriculture Information Network Report #ID2027, Jakarta ATO, 2002, p 2.

10 K Easton, G Bell & F Ng, Exporting Food to Indonesia: A Guide for Australian Small to Medim Enterprises, CSIRO and RIRDC,Sydney, 1997.

11 Euromonitor, 2003.

3. RETAIL AND FOOD SERVICE

Overview• The average Indonesian shops mostly at traditional outlets—large wet markets and smaller

provision stores.

• Large local food producers—whether domestic or foreign-owned—rely on traditionalchannels to achieve mainstream market penetration.

• Modern retail continues to grow strongly, especially in Jakarta and other major cities. Thetop 5 chains account for 11% of retail sales so modern retailing is more concentrated inIndonesia than, say, China (though not Australia).

• Supermarkets were the pioneers but hypermarkets, mini marts and warehouse stores arenow sharing the growth. Within the modern sector, supermarkets are under the mostcompetitive pressure. Hero (Dairy Farm), Carrefour and Makro lead the supermarket,hypermarket and warehouse sectors respectively.

• Hotels and fast food chains dominate the modern food service sector and account for mostfood service imports. Other food service niches include airline catering and servicing ofmining communities.

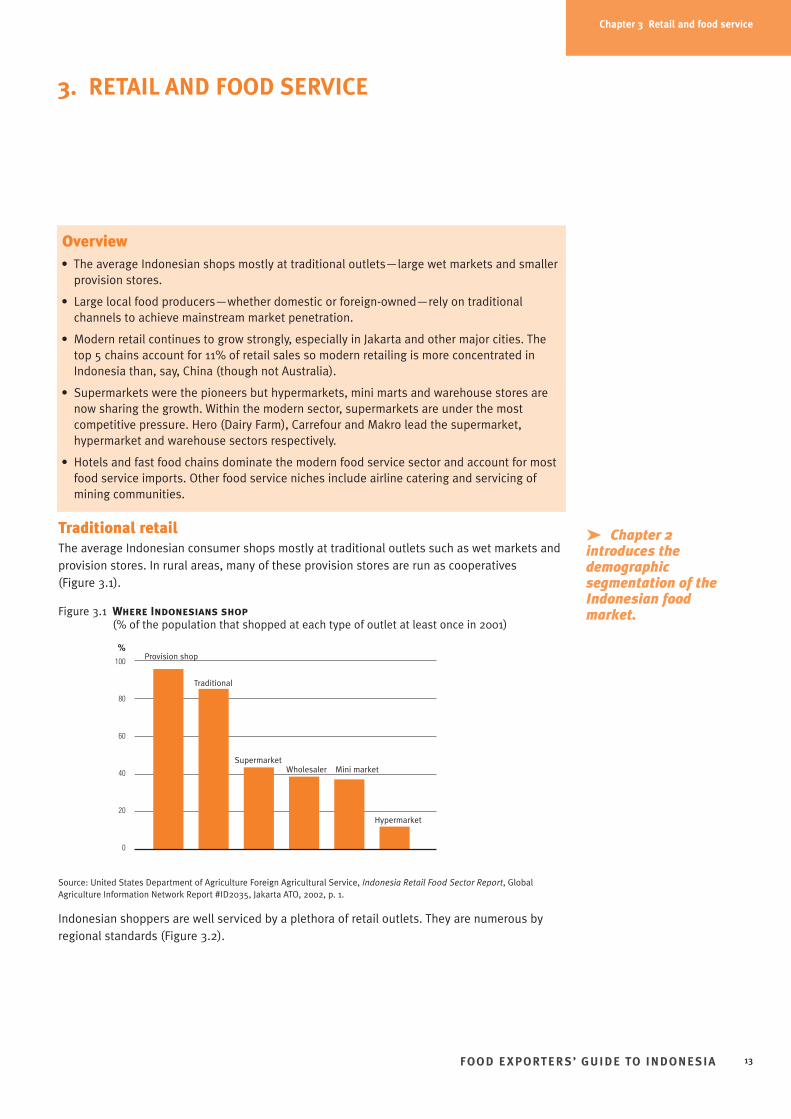

Traditional retail The average Indonesian consumer shops mostly at traditional outlets such as wet markets andprovision stores. In rural areas, many of these provision stores are run as cooperatives (Figure 3.1).

Figure 3.1 Where Indonesians shop(% of the population that shopped at each type of outlet at least once in 2001)

Source: United States Department of Agriculture Foreign Agricultural Service, Indonesia Retail Food Sector Report, GlobalAgriculture Information Network Report #ID2035, Jakarta ATO, 2002, p. 1.

Indonesian shoppers are well serviced by a plethora of retail outlets. They are numerous byregional standards (Figure 3.2).

FOO D E XPORTER S’ GUIDE TO INDONESIA 13

➤ Chapter 2introduces thedemographicsegmentation of theIndonesian foodmarket.

Chapter 3 Retail and food service

%100

80

60

40

20

0

Provision shop

Traditional

SupermarketWholesaler Mini market

Hypermarket

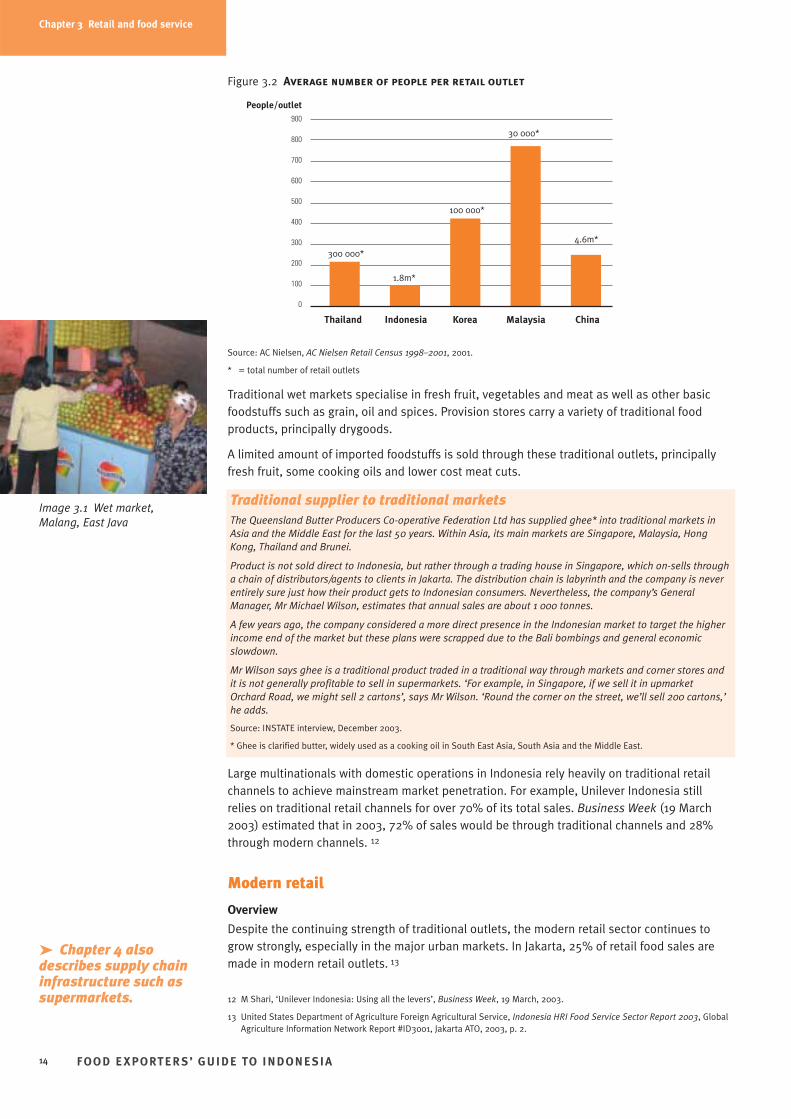

Figure 3.2 Average number of people per retail outlet

Source: AC Nielsen, AC Nielsen Retail Census 1998–2001, 2001.

* = total number of retail outlets

Traditional wet markets specialise in fresh fruit, vegetables and meat as well as other basicfoodstuffs such as grain, oil and spices. Provision stores carry a variety of traditional foodproducts, principally drygoods.

A limited amount of imported foodstuffs is sold through these traditional outlets, principallyfresh fruit, some cooking oils and lower cost meat cuts.

Large multinationals with domestic operations in Indonesia rely heavily on traditional retailchannels to achieve mainstream market penetration. For example, Unilever Indonesia stillrelies on traditional retail channels for over 70% of its total sales. Business Week (19 March2003) estimated that in 2003, 72% of sales would be through traditional channels and 28%through modern channels. 12

Modern retail

Overview

Despite the continuing strength of traditional outlets, the modern retail sector continues togrow strongly, especially in the major urban markets. In Jakarta, 25% of retail food sales aremade in modern retail outlets. 13

FOO D E XPORTER S’ GUIDE TO INDONESIA14

➤ Chapter 4 alsodescribes supply chaininfrastructure such assupermarkets.

Image 3.1 Wet market,Malang, East Java

Chapter 3 Retail and food service

People/outlet900

800

700

600

500

400

300

200

100

0

300 000*

Thailand Indonesia Korea Malaysia China

1.8m*

100 000*

30 000*

Traditional supplier to traditional marketsThe Queensland Butter Producers Co-operative Federation Ltd has supplied ghee* into traditional markets inAsia and the Middle East for the last 50 years. Within Asia, its main markets are Singapore, Malaysia, HongKong, Thailand and Brunei.

Product is not sold direct to Indonesia, but rather through a trading house in Singapore, which on-sells througha chain of distributors/agents to clients in Jakarta. The distribution chain is labyrinth and the company is neverentirely sure just how their product gets to Indonesian consumers. Nevertheless, the company’s GeneralManager, Mr Michael Wilson, estimates that annual sales are about 1 000 tonnes.

A few years ago, the company considered a more direct presence in the Indonesian market to target the higherincome end of the market but these plans were scrapped due to the Bali bombings and general economicslowdown.

Mr Wilson says ghee is a traditional product traded in a traditional way through markets and corner stores andit is not generally profitable to sell in supermarkets. ‘For example, in Singapore, if we sell it in upmarketOrchard Road, we might sell 2 cartons’, says Mr Wilson. ‘Round the corner on the street, we’ll sell 200 cartons,’he adds.

Source: INSTATE interview, December 2003.

* Ghee is clarified butter, widely used as a cooking oil in South East Asia, South Asia and the Middle East.

12 M Shari, ‘Unilever Indonesia: Using all the levers’, Business Week, 19 March, 2003.

13 United States Department of Agriculture Foreign Agricultural Service, Indonesia HRI Food Service Sector Report 2003, GlobalAgriculture Information Network Report #ID3001, Jakarta ATO, 2003, p. 2.

4.6m*

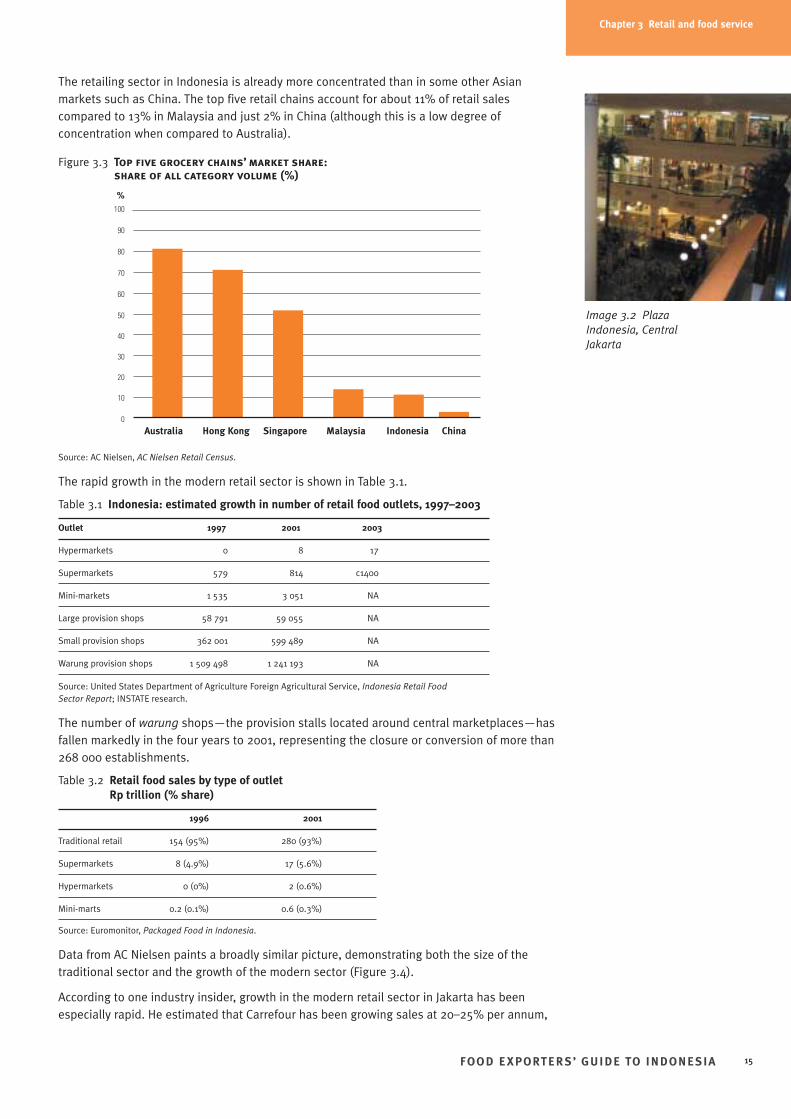

The retailing sector in Indonesia is already more concentrated than in some other Asianmarkets such as China. The top five retail chains account for about 11% of retail salescompared to 13% in Malaysia and just 2% in China (although this is a low degree ofconcentration when compared to Australia).

Figure 3.3 Top five grocery chains’ market share:share of all category volume (%)

Source: AC Nielsen, AC Nielsen Retail Census.

The rapid growth in the modern retail sector is shown in Table 3.1.

Table 3.1 Indonesia: estimated growth in number of retail food outlets, 1997–2003

Outlet 1997 2001 2003

Hypermarkets 0 8 17

Supermarkets 579 814 c1400

Mini-markets 1 535 3 051 NA

Large provision shops 58 791 59 055 NA

Small provision shops 362 001 599 489 NA

Warung provision shops 1 509 498 1 241 193 NA

Source: United States Department of Agriculture Foreign Agricultural Service, Indonesia Retail Food Sector Report; INSTATE research.

The number of warung shops—the provision stalls located around central marketplaces—hasfallen markedly in the four years to 2001, representing the closure or conversion of more than268 000 establishments.

Table 3.2 Retail food sales by type of outlet Rp trillion (% share)

1996 2001

Traditional retail 154 (95%) 280 (93%)

Supermarkets 8 (4.9%) 17 (5.6%)

Hypermarkets 0 (0%) 2 (0.6%)

Mini-marts 0.2 (0.1%) 0.6 (0.3%)

Source: Euromonitor, Packaged Food in Indonesia.

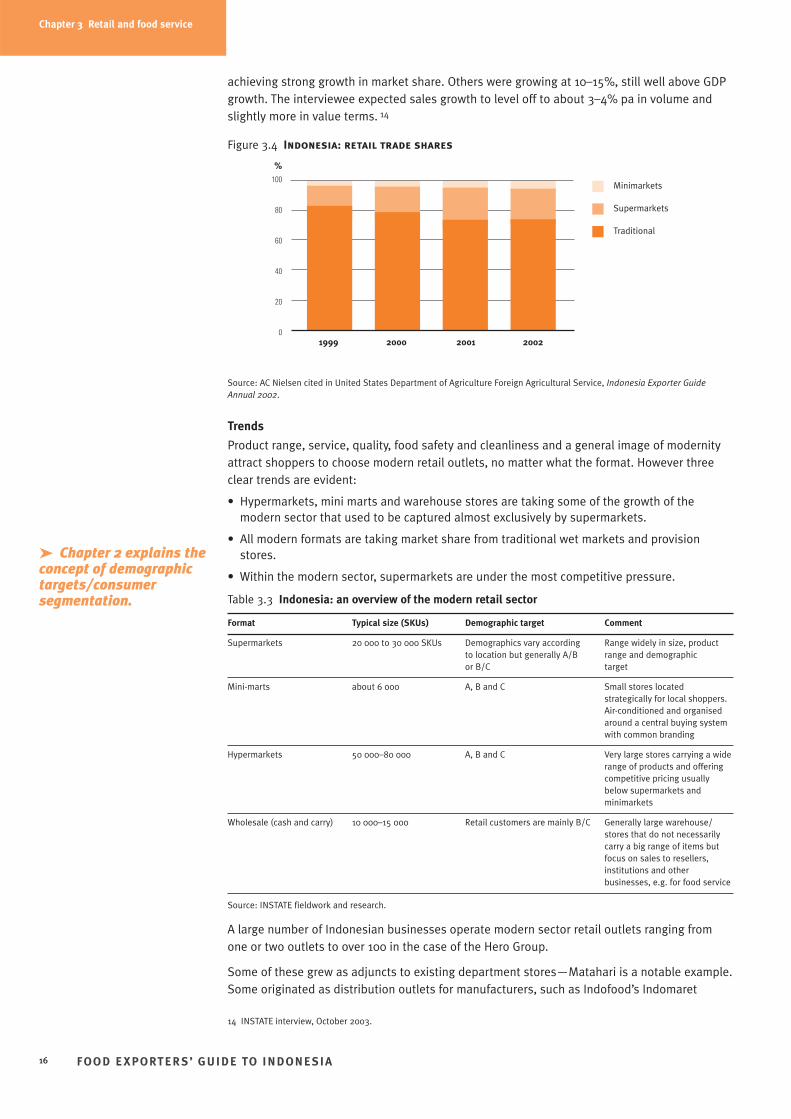

Data from AC Nielsen paints a broadly similar picture, demonstrating both the size of thetraditional sector and the growth of the modern sector (Figure 3.4).

According to one industry insider, growth in the modern retail sector in Jakarta has beenespecially rapid. He estimated that Carrefour has been growing sales at 20–25% per annum,

FOO D E XPORTER S’ GUIDE TO INDONESIA 15

Image 3.2 PlazaIndonesia, CentralJakarta

Chapter 3 Retail and food service

%100

90

80

70

60

50

40

30

20

10

0

Australia Hong Kong Singapore Malaysia Indonesia China

achieving strong growth in market share. Others were growing at 10–15%, still well above GDPgrowth. The interviewee expected sales growth to level off to about 3–4% pa in volume andslightly more in value terms. 14

Figure 3.4 Indonesia: retail trade shares

Source: AC Nielsen cited in United States Department of Agriculture Foreign Agricultural Service, Indonesia Exporter GuideAnnual 2002.

Trends

Product range, service, quality, food safety and cleanliness and a general image of modernityattract shoppers to choose modern retail outlets, no matter what the format. However threeclear trends are evident:

• Hypermarkets, mini marts and warehouse stores are taking some of the growth of themodern sector that used to be captured almost exclusively by supermarkets.

• All modern formats are taking market share from traditional wet markets and provisionstores.

• Within the modern sector, supermarkets are under the most competitive pressure.

Table 3.3 Indonesia: an overview of the modern retail sector

Format Typical size (SKUs) Demographic target Comment

Supermarkets 20 000 to 30 000 SKUs Demographics vary according Range widely in size, product to location but generally A/B range and demographic or B/C target

Mini-marts about 6 000 A, B and C Small stores locatedstrategically for local shoppers.Air-conditioned and organisedaround a central buying systemwith common branding

Hypermarkets 50 000–80 000 A, B and C Very large stores carrying a widerange of products and offeringcompetitive pricing usuallybelow supermarkets andminimarkets

Wholesale (cash and carry) 10 000–15 000 Retail customers are mainly B/C Generally large warehouse/stores that do not necessarilycarry a big range of items butfocus on sales to resellers,institutions and otherbusinesses, e.g. for food service

Source: INSTATE fieldwork and research.

A large number of Indonesian businesses operate modern sector retail outlets ranging fromone or two outlets to over 100 in the case of the Hero Group.

Some of these grew as adjuncts to existing department stores—Matahari is a notable example.Some originated as distribution outlets for manufacturers, such as Indofood’s Indomaret

FOO D E XPORTER S’ GUIDE TO INDONESIA16

➤ Chapter 2 explains theconcept of demographictargets/consumersegmentation.

Chapter 3 Retail and food service

%100

80

60

40

20

0

Minimarkets

Supermarkets

Traditional

1999 2000 2001 2002

14 INSTATE interview, October 2003.

minimarket chain and some as downstream diversifications by distributor groups such asWicaksana’s Club Stores.

Crossover: what format is that?

The distinctions between different retail formats are not always absolute. For example, it isdifficult to distinguish precisely between smaller supermarkets and convenience stores or minimarkets, and wholesale stores and hypermarkets:

• Although Carrefour is primarily focused on individual customers, its broad product range andattractive pricing also attracts purchases for re-sale and food service.

• Similarly, although Makro is geared to serve resellers and institutions it also has a greatnumber of retail customers who are attracted by the competitive pricing and pleasantshopping conditions.

• Alfa’s larger outlets and Wicaksana’s Club Stores are also hard to classify, some comparingthe former to hybrid supermarket/wholesale stores and the latter to hybridhypermarkets/wholesale stores.

FOO D E XPORTER S’ GUIDE TO INDONESIA 17

Image 3.3 Alfa store,Surabaya

Chapter 3 Retail and food service

Retail operator profile: HeroHero began as a family company and has operated retail stores in Indonesia since the 1970s. It was a pioneer ofsupermarkets in Indonesia, especially at the upper end of the market.

Hero became a publicly listed company after the economic crisis. Dairy Farm of Hong Kong has taken a 32% shareholding. Dairy Farm is understood to now be the driving force in the management of the group. Thecompany employs many expatriate managers, including Australians.

It has been expanding aggressively and Hero now operates 107 stores including stores taken over from RoyalAhold under the Tops brand.

By mid 2003, Hero had 89 supermarkets, up from 70 in 1999. Of these, there are 36 outlets in Jakarta, of which 17are in the wealthy south Jakarta area. Supermarkets are being ‘re-engineered’ to remain competitive and DairyFarm concepts have been used in newer supermarket designs. Some stores are focused on A and B customers,others on B and C (e.g. Tangerang). Supermarkets average about 6 000 m2 of floor area.

Hero opened its first hypermarket under the Giant brand in September 2002 and now has three in Jakarta (inBekasi, Cemanggis (Depok) and Tangerang) and one in Surabaya. It expects to have five operating by the end of2004. These stores tend to be located close to competing Carrefour stores. They have developed a slightlydifferent style from Carrefour—more like the wet markets and more informal in style. Spruikers are used as in wetmarkets. Hero targets the C and D demographic buyers. The stores are around 9 000 m2 in area.

Hero is spending a lot of money going head-to-head with Carrefour and this has had a dramatic negative short-term effect upon financial results. The company believes, however, that its strategy will pay off in the longer term.

Hero does not normally buy direct from suppliers. The main reason for this is to avoid the problem of having toapply for an imported food licence number (ML or makanan luar) through the National Agency of Drug and FoodControl (BPOM). Hero does, however, import directly to a facility at the major mining town of Freeport in Papua(bringing in 5 containers every 10 days).

Source: INSTATE field visit and interviews, September–October 2003.

Medium-sized retail operator profile: Alfa GroupThe Alfa group is Indonesian-owned. It is a subsidiary of PT Sampoerna, one of the leading manufacturers ofcigarettes in Indonesia. The group does not have a foreign partner and relies on Indonesian expertise. Itsfinancial returns are reported to have been good, with net profit rising even as the group has expanded rapidlyin recent years.

Mini-marts under the Alfamart banner have increased in number from 16 in 1998 to 300 in 2002, with a target of1 000 by 2004. The group is the second largest operator of mini-marts behind Indofood’s Indomaret group thathad 750 stores in 2002.

The group’s larger stores have also expanded in number, from 7 in 1999 to 29 in 2003.15 Some describe them assupermarkets (see Table 3.3) while they are also similar in some ways to warehouse stores. As in the case ofMakro, these stores sell to the public as well as to resellers, food service and institutions.

An Alfa supermarket/wholesale store in Surabaya, 6 000 m2 in area. While displays are of a good standard andcompetitive with other outlets the environment is fairly basic, with air conditioning turned down low to savecost. Offices tend to be spartan, indicating this is a company focused on tight cost management. The success ofthis group is a sign that modern retailing in Indonesia is maturing in terms of local management expertise.

Source: INSTATE field visit and interviews, September–October 2003.

➤ Chapter 5 explainsprocedures for sellingfood products inIndonesia.

15 Indocommercial, N.322, Jakarta, 4 June, 2003.

Chapter 3 Retail and food service

FOO D E XPORTER S’ GUIDE TO INDONESIA18

Image 3.4 Fruit display,Hero supermarket,Kemang

Winners and losers

Among the foreign companies, Carrefour’s success no doubt owes something to its Frenchtechnology and management systems but what stands out is how well it has adapted its styleand offering to address local needs and customs. It has also benefited from its quickadaptation to the crisis situation of the late 1990s.

On the other hand, the local industry believes there are obvious reasons for the failure andsubsequent withdrawal from the market in the late 1990s of Wal Mart and J C Penney. Theseincluded their attempts to transfer existing business models and product lines to Indonesia,including a high proportion of imported products, and store locations that were less than optimal.

SupermarketsThe number of supermarkets has grown rapidly in the past 3 to 4 years and now stands ataround 1400 country wide. The biggest players in supermarkets are Hero, Matahari andRamayana (Table 3.4).

Table 3.4 Indonesia: major supermarket chains, 2001

Retail Name Ownership Outlets Locations

Hero Indonesian Hong Kong 83* Jakarta, Java, Bali, Sumatra, Kalimantan

Matahari Indonesian 61 Jakarta, Java, Bali, Sumatra, Kalimantan, Sulawesi, Ambon

Ramayana Indonesian 65 Jakarta, Java, Bali, Batam, Sumatra, Kalimantan

Super Indo Indonesian Belgium 34 Jakarta, Bogor, Tangerang, Bekasi, Bandung, Surabaya, Palembang,

Yogyakarta

Yogya Indonesian 33 Jakarta, West Java

Alfa Indonesian 29 Jakarta, Java, Bali, Medan, Makassar

Tops Dutch 24 Jakarta, Java

Gelael Indonesian 11 Jakarta, Jawa, Bali, Sumatra, Sulawesi, Batam

Nina Fair Price Indonesian, Singapore 5 Surabaya

Pantry Indonesian 5 Jakarta

Sinar Indonesian 5 Surabaya

Sogo Indonesian Japan 4 Jakarta, Surabaya

Tiara Dewata Indonesian 3 Bali

Tragia Indonesian 5 Bali

Source: United States Department of Agriculture Foreign Agricultural Service, Indonesia Retail Food Sector Report, p. 8.

* 89 stores by mid 2003.

Affluence and urbanisation are two key underlying factors driving the development of modernretail. Younger shoppers in particular prefer the modern retail experience, and a majority ofsupermarket shoppers are female.

Supermarkets are busy after work, from 5 pm through till about 9 pm and on weekends.Families often make a day of it on Saturdays or Sundays.

Before the crisis, up to half the product on supermarket shelves was imported. In today’sbigger supermarket sector, imports typically account for 5–10% of SKUs.

Supermarkets that cater to higher income residential areas with wealthy local and expatriatecustomers tend to carry a higher percentage of imported products, stocking specialist brandsat higher prices. Conversely, the proportion of imported product sold tends be less in outletsoutside of the capital as well as in the less affluent areas of Jakarta where shoppers are moreprice sensitive.

Chapter 3 Retail and food service

Wholesale (cash and carry)Wholesale or cash and carry outlets are a popular and fast growing type of outlet. Despite theirname, they attract a considerable flow of retail customers as well as trade customers lookingto stock small shops or buying for a food service outlet or street stall.

Table 3.5 Indonesia: major warehouse / cash and carry operators, 2001

Retail Name Ownership Outlets Locations

Makro (wholesale) Dutch 13* Jakarta, Surabaya, Medan, Bandung, Bali, Semarang

Indo Grosir (wholesale) Indonesian Belgian 6 Jakarta, Bandung, Yogyakarta, Surabaya

Goro (wholesale) Indonesian 5 Jakarta, Solo, Makassar

Club Store Indonesian 2 Jakarta, Medan

Club Grosir (wholesale) Indonesian 2 Jakarta

Sources: United States Department of Agriculture Foreign Agricultural Service, Indonesia Retail Food Sector Report; INSTATE research.

* 2003 data

These large warehouse/stores do not necessarily carry a big range of items. For example,Makro carries around 11 000 SKUs but intends to reduce its range further (see profile below).

FOO D E XPORTER S’ GUIDE TO INDONESIA 19

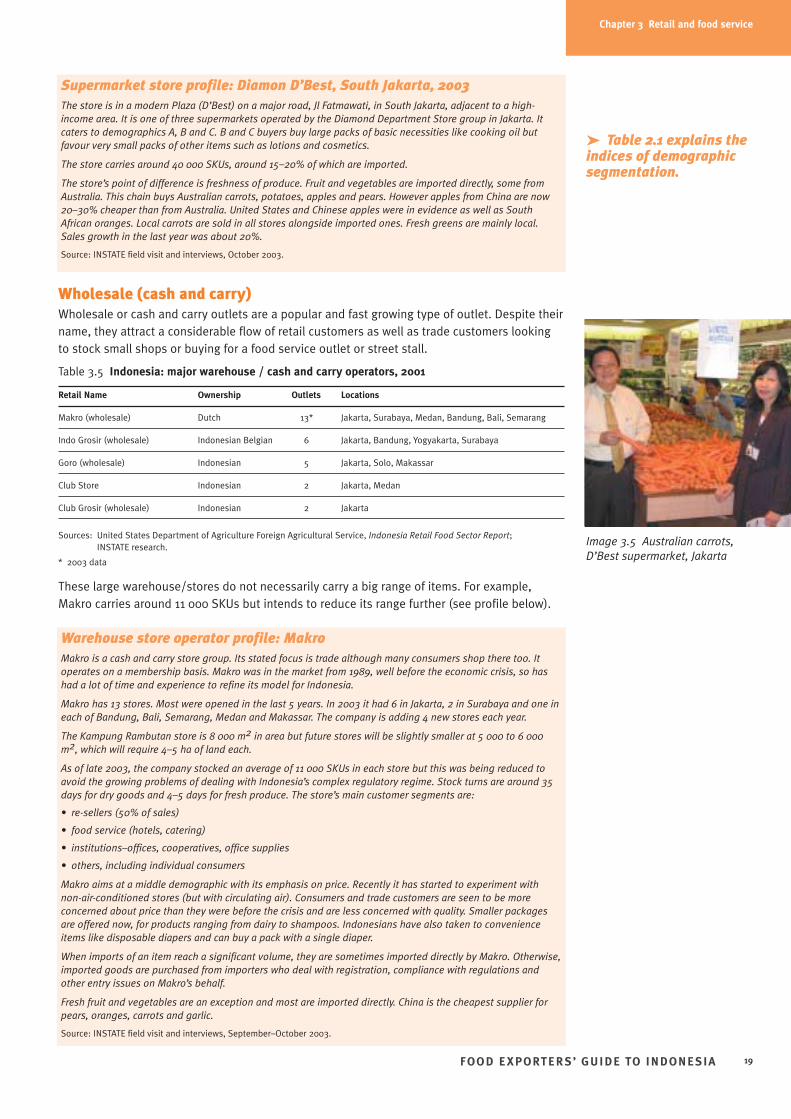

Supermarket store profile: Diamon D’Best, South Jakarta, 2003The store is in a modern Plaza (D’Best) on a major road, Jl Fatmawati, in South Jakarta, adjacent to a high-income area. It is one of three supermarkets operated by the Diamond Department Store group in Jakarta. Itcaters to demographics A, B and C. B and C buyers buy large packs of basic necessities like cooking oil butfavour very small packs of other items such as lotions and cosmetics.

The store carries around 40 000 SKUs, around 15–20% of which are imported.

The store’s point of difference is freshness of produce. Fruit and vegetables are imported directly, some fromAustralia. This chain buys Australian carrots, potatoes, apples and pears. However apples from China are now20–30% cheaper than from Australia. United States and Chinese apples were in evidence as well as SouthAfrican oranges. Local carrots are sold in all stores alongside imported ones. Fresh greens are mainly local.Sales growth in the last year was about 20%.

Source: INSTATE field visit and interviews, October 2003.

Warehouse store operator profile: MakroMakro is a cash and carry store group. Its stated focus is trade although many consumers shop there too. Itoperates on a membership basis. Makro was in the market from 1989, well before the economic crisis, so hashad a lot of time and experience to refine its model for Indonesia.

Makro has 13 stores. Most were opened in the last 5 years. In 2003 it had 6 in Jakarta, 2 in Surabaya and one ineach of Bandung, Bali, Semarang, Medan and Makassar. The company is adding 4 new stores each year.

The Kampung Rambutan store is 8 000 m2 in area but future stores will be slightly smaller at 5 000 to 6 000m2, which will require 4–5 ha of land each.

As of late 2003, the company stocked an average of 11 000 SKUs in each store but this was being reduced toavoid the growing problems of dealing with Indonesia’s complex regulatory regime. Stock turns are around 35days for dry goods and 4–5 days for fresh produce. The store’s main customer segments are:

• re-sellers (50% of sales)

• food service (hotels, catering)

• institutions–offices, cooperatives, office supplies

• others, including individual consumers

Makro aims at a middle demographic with its emphasis on price. Recently it has started to experiment withnon-air-conditioned stores (but with circulating air). Consumers and trade customers are seen to be moreconcerned about price than they were before the crisis and are less concerned with quality. Smaller packagesare offered now, for products ranging from dairy to shampoos. Indonesians have also taken to convenienceitems like disposable diapers and can buy a pack with a single diaper.