Food and Beverage - wholesale.wf.com · •Frozen Food 3Q’18 average unit price increased 0.6%...

18

August 2012 Industry Research Update: Food and Agribusiness 1 November 2018 © 2018 Wells Fargo Bank, N.A. All rights reserved. For public use. 1 Key Demand Developments • Wells Fargo Securities has the inflation forecast as largely unchanged for 2019 and 2020. Rising labor and material costs will likely continue to generate additional inflation pressures throughout 2019. We expect inflation to soften slightly in 2020 as energy prices begin to moderate. • Wells Fargo economists have updated the bank’s forecast for Q4-2018 U.S. real GDP growth to 2.5%. Government spending will continue to provide a boost to growth, and the bank expects a rebound in business fixed investment in Q4. For personal consumption growth, the bank feels a cool down from the third quarter pace is imminent, but that personal consumption will remain supportive of overall GDP growth. Residential construction is likely to remain a weak spot moving forward. • Wells Fargo economists have pared back expectations for global growth. Even with U.S. outperformance, growth continued to slow down in China and the Eurozone for Q3. A potential meeting at the G20 summit in late November between President Xi and President Trump will be key to the global trade outlook for growth. Consumer and Producer Price Indices • The Producer Price Index (PPI All Food) declined by 1.8% Y/Y for Sept 2018. The spread between restaurant and food retail pricing is steady for both Y/Y and M/M for September 2018, yet remains higher than the Jan 2018 low. Over the 3-5 year period, these trends appear to be demonstrating less volatility in macroeconomic indicators as CPI and PPI are moving in a smaller channel. • Restaurant pricing measured by the CPI Food Away from Home index (CPI-FAFH) grew 2.6% Y/Y in Sept 2018, which is outpacing the CPI Food At Home index with .3% growth Y/Y. Both of these measurements remain steady over the last several months. Industry Update Food and Agribusiness Price and Food Inflation Developments Food Retail Sales According to Nielsen, U.S. Food Retail sales growth increased in dollar volume by 1.3% Y/Y, while unit sales decreased 1.9% Y/Y. With overall value turning around since last month and unit sales decline decreasing, this begs the question of whether retail is beginning to find a strategic balance versus competition. Nielsen forecasts that fast-moving consumer goods (FMCG), including food, will continue to face growth headwinds through 2019 and 2020, notably for grocery, drug, and mass merchandise channels. -8% -6% -4% -2% 0% 2% 4% 6% 8% 10% Jan-14 Jul-14 Jan-15 Jul-15 Jan-16 Jul-16 Jan-17 Jul-17 Jan-18 Jul-18 Y/Y Change (%) CPI Food Away From Home CPI Food At Home PPI All Food Source: U.S. Bureau of Labor Statistics

Transcript of Food and Beverage - wholesale.wf.com · •Frozen Food 3Q’18 average unit price increased 0.6%...

August 2012

Industry Research Update: Food and Agribusiness 1

November 2018

© 2018 Wells Fargo Bank, N.A. All rights reserved. For public use.

1

Key Demand Developments

• Wells Fargo Securities has the inflation forecast as largely unchanged for 2019 and 2020. Rising labor and material costs will likely continue to generate additional inflation pressures throughout 2019. We expect inflation to soften slightly in 2020 as energy prices begin to moderate.

• Wells Fargo economists have updated the bank’s forecast for Q4-2018 U.S. real GDP growth to 2.5%. Government spending will continue to provide a boost to growth, and the bank expects a rebound in business fixed investment in Q4. For personal consumption growth, the bank feels a cool down from the third quarter pace is imminent, but that personal consumption will remain supportive of overall GDP growth. Residential construction is likely to remain a weak spot moving forward.

• Wells Fargo economists have pared back expectations for global growth. Even with U.S. outperformance, growth continued to slow down in China and the Eurozone for Q3. A potential meeting at the G20 summit in late November between President Xi and President Trump will be key to the global trade outlook for growth.

Consumer and Producer Price Indices

• The Producer Price Index (PPI All Food) declined

by 1.8% Y/Y for Sept 2018. The spread between

restaurant and food retail pricing is steady for

both Y/Y and M/M for September 2018, yet

remains higher than the Jan 2018 low. Over the

3-5 year period, these trends appear to be

demonstrating less volatility in macroeconomic

indicators as CPI and PPI are moving in a smaller

channel.

• Restaurant pricing measured by the CPI Food

Away from Home index (CPI-FAFH) grew 2.6%

Y/Y in Sept 2018, which is outpacing the CPI

Food At Home index with .3% growth Y/Y. Both

of these measurements remain steady over the

last several months.

Industry Update

Food and Agribusiness

Price and Food Inflation Developments

Food Retail Sales

According to Nielsen, U.S. Food Retail sales growth increased in dollar volume by 1.3% Y/Y, while unit sales decreased 1.9% Y/Y. With overall value turning around since last month and unit sales decline decreasing, this begs the question of whether retail is beginning to find a strategic balance versus competition. Nielsen forecasts that fast-moving consumer goods (FMCG), including food, will continue to face growth headwinds through 2019 and 2020, notably for grocery, drug, and mass merchandise channels.

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

Jan-14 Jul-14 Jan-15 Jul-15 Jan-16 Jul-16 Jan-17 Jul-17 Jan-18 Jul-18

Y/Y

Change (

%)

CPI Food Away From Home CPI Food At Home PPI All Food

Source: U.S. Bureau of Labor Statistics

August 2012

2

© 2018 Wells Fargo Bank, N.A. All rights reserved. For public use.

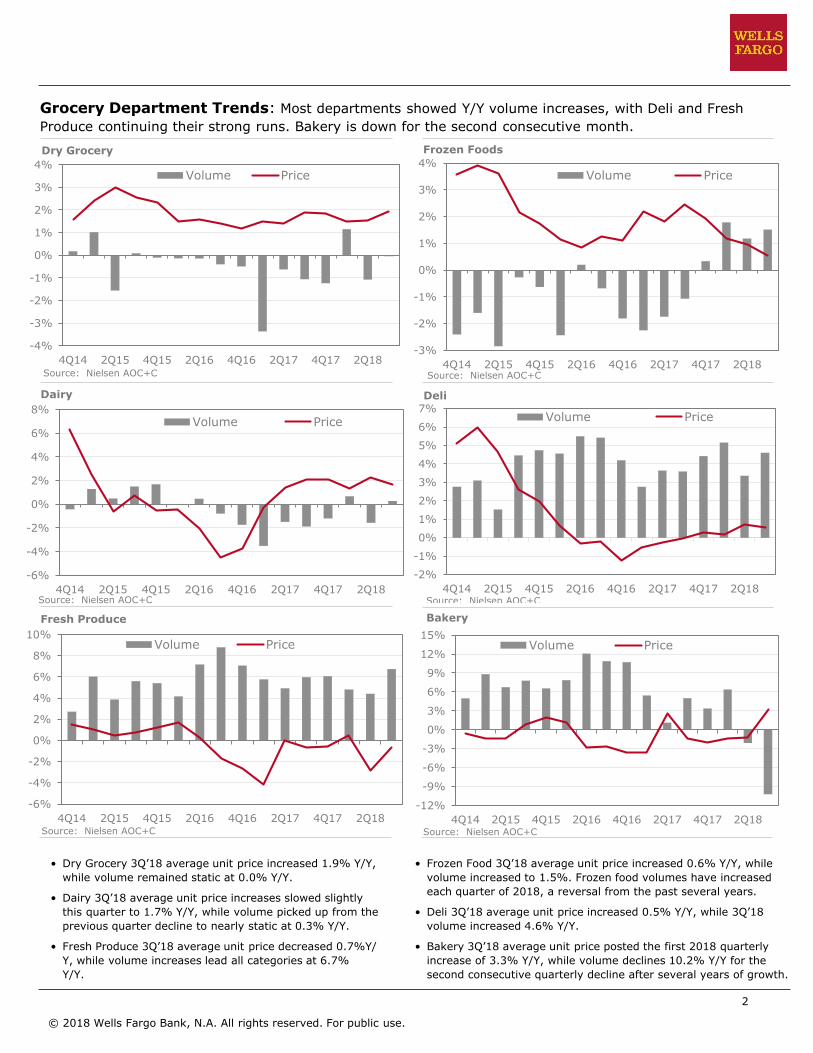

Grocery Department Trends: Most departments showed Y/Y volume increases, with Deli and Fresh

Produce continuing their strong runs. Bakery is down for the second consecutive month.

Dry Grocery Frozen Foods

Bakery

Deli

• Dry Grocery 3Q’18 average unit price increased 1.9% Y/Y,

while volume remained static at 0.0% Y/Y.

• Dairy 3Q’18 average unit price increases slowed slightly

this quarter to 1.7% Y/Y, while volume picked up from the

previous quarter decline to nearly static at 0.3% Y/Y.

• Fresh Produce 3Q’18 average unit price decreased 0.7%Y/

Y, while volume increases lead all categories at 6.7%

Y/Y.

Dairy

Fresh Produce

• Frozen Food 3Q’18 average unit price increased 0.6% Y/Y, while

volume increased to 1.5%. Frozen food volumes have increased

each quarter of 2018, a reversal from the past several years.

• Deli 3Q’18 average unit price increased 0.5% Y/Y, while 3Q’18

volume increased 4.6% Y/Y.

• Bakery 3Q’18 average unit price posted the first 2018 quarterly

increase of 3.3% Y/Y, while volume declines 10.2% Y/Y for thesecond consecutive quarterly decline after several years of growth.

-4%

-3%

-2%

-1%

0%

1%

2%

3%

4%

4Q14 2Q15 4Q15 2Q16 4Q16 2Q17 4Q17 2Q18

Volume Price

Source: Nielsen AOC+C

-6%

-4%

-2%

0%

2%

4%

6%

8%

4Q14 2Q15 4Q15 2Q16 4Q16 2Q17 4Q17 2Q18

Volume Price

Source: Nielsen AOC+C

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

4Q14 2Q15 4Q15 2Q16 4Q16 2Q17 4Q17 2Q18

Volume Price

Source: Nielsen AOC+C

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

7%

4Q14 2Q15 4Q15 2Q16 4Q16 2Q17 4Q17 2Q18

Volume Price

Source: Nielsen AOC+C

-3%

-2%

-1%

0%

1%

2%

3%

4%

4Q14 2Q15 4Q15 2Q16 4Q16 2Q17 4Q17 2Q18

Volume Price

Source: Nielsen AOC+C

-12%

-9%

-6%

-3%

0%

3%

6%

9%

12%

15%

4Q14 2Q15 4Q15 2Q16 4Q16 2Q17 4Q17 2Q18

Volume Price

Source: Nielsen AOC+C

August 2012

3

© 2018 Wells Fargo Bank, N.A. All rights reserved. For public use.

Monthly avg. corn, wheat, soybeans in $/bu; broilers, shrimp in $/lb; cattle, hogs, milk in $/cwt; salmon in $/kg; gas in $/Mct; oil in $/gal; electricity in $/kWh; labor in $/h

Sources: CBOT, USDA, Urner Barry, EIA, BLS

• Economic Backdrop: Wells Fargo’s updated forecast for

Q3-2018 U.S. real GDP growth is 3.3%, up from 3.1% in our

last monthly report. Real personal consumption appears to

be growing in excess of a 3% annualized rate, while federal,state and local government spending is likely to boost growth

in the quarter.

• Corn, Wheat & Soybeans: Corn and wheat prices are

above the past two years with U.S. and world stocks forecast

to moderate in 2018/19 from large levels in 2017/18.

Soybean prices remain low with the U.S. stocks/use ratio

projected the highest in 33 years on a large crop and small

exports to China.

• Chicken: Boneless, skinless breast prices dip down to 90

cents/lb., the lowest level in decades. Despite low grain

prices lending support, gross margins continue to drop for

producers.

• Beef: Demand remained strong in October, driven by export

sales to Asia. Beef production in 2018 was revised lower by

USDA on a slower than expected marketing pace for fed

cattle in the fourth quarter.

• Pork: African Swine Fever continues to spread in China,

creating uncertainty for global supplies into Q1. Lower prices

helped keep September exports above last year’s levels.

Seasonally higher hog supplies are expected to pressure

prices in the next couple of months.

• Packer Margin Environment: Pork, chicken and beef

packer margins followed their seasonal patterns in October.

Pork packers are gaining leverage against producers as plant

capacity is tested. Chicken margins struggle with low product

prices.

• Seafood: Prices continue to advance for both cod and

pollock on forecasted lower quotas in 2019. The expected

lower quota is overshadowing concerns about the U.S. 10%

import tariff on product brought back into the U.S. afterChinese processing.

• Dairy: Cheese prices moved lower in October due to higher

production. Dairy cow numbers are shrinking, but stronger

milk per cow growth is offsetting any potential production

declines.

• Specialty and Non-Grain Crops: U.S. spot sugar prices are

up roughly 9% Y/Y. Continued significant price advances are

unlikely.

• Nuts: California tree nut harvest is virtually complete with

processing continuing through end of year. Pecan harvest

has started in California and continues in Texas and the

Southeast. Georgia harvest has been hampered by the effect

of Hurricane Michael. The harvest has produced large crops

of excellent quality, but smaller nut sizing is being noted.

• Wine: Harvest is wrapping up in California, Oregon and

Washington with all areas reporting a large crop of good quality.

Expectations are in line with an approximate harvest in the 4MM

ton range for California. Bulk wine is available for purchase

depending on variety, quality and location. Industry is looking at

the possible effect of smoke taint in areas that experience

wildfires, and competition with legalized cannabis consumption.

• Fruit Crops: Table grape harvest will be winding down, although

fruit will continue to be sold out of cold storage. Apple harvest is

complete, with the U.S. crop down ~3MM boxes Y/Y. Fruits on

store shelves are transitioning to imported product, and citrus

growers are preparing to get harvest crews in the orchards.

• Vegetable Crops: Processing tomato harvest has wrapped up,

with an estimated 12.2MM tons delivered in CA. Cucumbers,

peppers, and tomatoes continue to be harvested in Tulare

County, with harvest expected to begin in FL soon. Lettuce

harvest is winding down in CA and moving to Arizona/Imperial

Valley. Sweet potato and sweet corn prices have increased

materially after weather issues in North Carolina.

• Forest Products: Lumber and structural panel prices fell sharply

in October to the lowest level in more than a year.

• Crop Inputs: Ammonia prices are the highest in 2½ years while

urea, DAP and potash prices are the highest in 3 years.

• Energy and Labor: The Energy Information Administration

estimates that U.S. crude oil production averaged 11.4MM barrels

per day in October, down from September levels because of

hurricane-related outages in the Gulf of Mexico.

Price vs. Volume Grain Protein Labor Energy

Constructive Mixed Mixed Inflationary Mixed

Food Company Margin Heat Map Y/Y

Food Company Input Cost Summary: As we end 3Q’18, commodity prices have been volatile when compared to 3Q’17 levels as M/M prices generally are up across the board. Commodity Price* Y/Y M/M

Corn $3.68 +5.4% +4.7%

HRW Wheat $5.14 +19.1% +1.3%

Soybeans $8.60 -12.0% +3.0%

Broilers $0.84 -1.5% +0.5%

Cattle $1.13 +0.7% +1.6%

Hogs $0.61 -1.4% +7.0%

Class III Milk $15.53 -7.0% -3.5%

Shrimp $4.00 -14.0% -1.2%

Salmon $5.66 +6.0% +0.5%

Natural Gas $8.93 +1.2% +4.0%

Electricity $10.97 -0.2% +1.4%

Heating Oil $3.23 +40.9% +0.3%

Restaurant Labor $13.94 +3.8% +0.4%

Supermarket Labor $13.45 +3.0% +0.4%

Food Labor $17.38 +3.9% +0.3%

Key Commodity Heat Map

*All prices for October except natural gas (July), Electricity (July),

heating oil (August) and supermarket labor (September)

August 2012

4

© 2018 Wells Fargo Bank, N.A. All rights reserved. For public use.

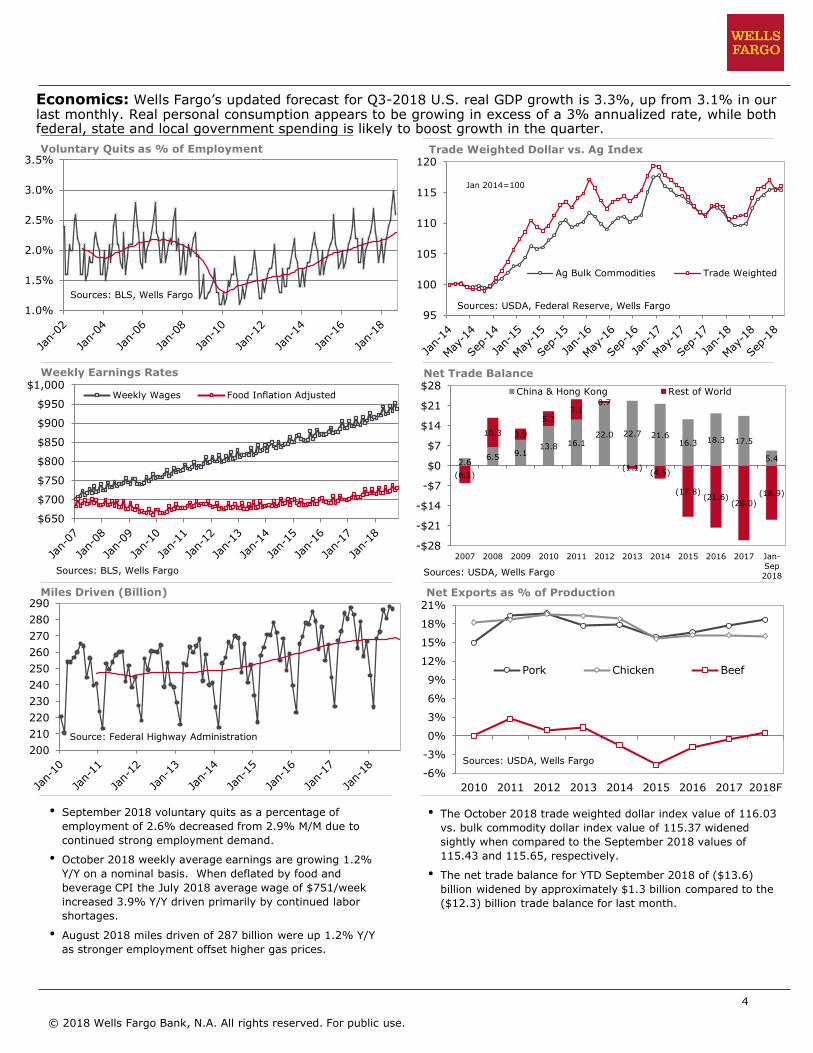

Economics: Wells Fargo’s updated forecast for Q3-2018 U.S. real GDP growth is 3.3%, up from 3.1% in our last monthly. Real personal consumption appears to be growing in excess of a 3% annualized rate, while both federal, state and local government spending is likely to boost growth in the quarter.

Miles Driven (Billion)

Trade Weighted Dollar vs. Ag Index

Net Exports as % of Production

Net Trade Balance

• September 2018 voluntary quits as a percentage of

employment of 2.6% decreased from 2.9% M/M due to

continued strong employment demand.

• October 2018 weekly average earnings are growing 1.2%

Y/Y on a nominal basis. When deflated by food and

beverage CPI the July 2018 average wage of $751/week

increased 3.9% Y/Y driven primarily by continued labor

shortages.

• August 2018 miles driven of 287 billion were up 1.2% Y/Y

as stronger employment offset higher gas prices.

• The October 2018 trade weighted dollar index value of 116.03

vs. bulk commodity dollar index value of 115.37 widenedsightly when compared to the September 2018 values of

115.43 and 115.65, respectively.

• The net trade balance for YTD September 2018 of ($13.6)

billion widened by approximately $1.3 billion compared to the

($12.3) billion trade balance for last month.

Voluntary Quits as % of Employment

Weekly Earnings Rates

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

Sources: BLS, Wells Fargo

$650

$700

$750

$800

$850

$900

$950

$1,000Weekly Wages Food Inflation Adjusted

Sources: BLS, Wells Fargo

200

210

220

230

240

250

260

270

280

290

Source: Federal Highway Administration

95

100

105

110

115

120

Ag Bulk Commodities Trade Weighted

Jan 2014=100

Sources: USDA, Federal Reserve, Wells Fargo

2.6 6.5 9.1

13.8 16.1 22.0 22.7 21.6

16.3 18.3 17.5

5.4

(6.1)

10.3 3.9

5.2 7.1

0.7

(1.1)(4.5)

(17.8)(21.6)

(26.0)

(18.9)

-$28

-$21

-$14

-$7

$0

$7

$14

$21

$28

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 Jan-

Sep

2018

China & Hong Kong Rest of World

Sources: USDA, Wells Fargo

-6%

-3%

0%

3%

6%

9%

12%

15%

18%

21%

2010 2011 2012 2013 2014 2015 2016 2017 2018F

Pork Chicken Beef

Sources: USDA, Wells Fargo

August 2012

5

© 2018 Wells Fargo Bank, N.A. All rights reserved. For public use.

• Nearby corn futures averaged $3.68

per bushel in October, up 17 cents

from September and up 19 cents Y/Y.

• Prices were supported by the USMCA

agreement and USDA’s smaller-than

expected U.S. production and ending

stocks forecasts released October 11.

• USDA’s world corn production and

stocks estimates were raised sharply

in November on adoption of higher

China production estimates back to

2007. For 2018/19, USDA now

forecasts world corn production up 2%

from 2017/18 and world stocks down

10% to the lowest level in four years.

• Nearby Kansas City wheat futures

averaged $5.14 per bushel in October.

This was up 7 cents from September

and up 82 cents from a year earlier.

• Support came from slow planting of

winter wheat amid wet conditions, but

gains were limited by a stronger U.S.

dollar and limited improvement in

export sales. The market received

some positive news late in the month

as Egypt bought a cargo U.S. wheat

for the first time in about 18 months.

• USDA projects global wheat production

down 4% in 2018/19 on large declines

in Russia, the EU and Australia. Global

stocks are forecast to fall 4% after

rising five straight years to a record.

Wheat

Grain Prices: Corn and wheat prices are above the past two years with U.S. and world stocks forecast

to decline in 2018/19. Soybean prices remain low with U.S. stocks/use projected the highest in 33 years.

Corn

Soybeans

• Nearby soybean futures averaged

$8.60 in October, which was up 25

cents from September but down $1.17

from October 2017.

• Support came from wet weather in the

Midwest, which slowed harvest and

brought concern about yields. Gains

were limited by export sales and

shipments that remind well below

recent years due to China’s high tariff.

• USDA projects world soybean

production up 9% in 2018/19 on this

year’s larger U.S. crop and an

assumed rebound in Argentina’s crop

in 2019. World stocks are projected to

jump 12% to a record level.

$3.20

$3.40

$3.60

$3.80

$4.00

$4.20

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2016 2017 2018 Futures

Source: CME

$/B

ushel

$3.90

$4.20

$4.50

$4.80

$5.10

$5.40

$5.70

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2016 2017 2018 Futures

Source: CME

$/B

ushel

$8.00

$8.50

$9.00

$9.50

$10.00

$10.50

$11.00

$11.50

$12.00

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2016 2017 2018 Futures

Source: CME

$/B

ushel

August 2012

6

© 2018 Wells Fargo Bank, N.A. All rights reserved. For public use.

Grain Fundamentals: U.S. corn and wheat stocks are forecast to moderate in 2018/19 from large levels

in 2017/18. U.S. soybean stocks are forecast to increase sharply on a large crop and small exports to China.

• USDA cut its U.S. corn crop estimate

152 million bushels in November on a

reduction in yield to 178.9 bushels,

which still would be a record.

• Projected ending stocks were lowered

77 million bushels with the smaller crop

partly offset by usage cuts. Feed and

residual usage was lowered 50 million

bushels due to the smaller crop and a

higher price outlook, while exports were

lowered 25 million on larger Ukrainian

production and exports. The implied

stocks-to-use ratio of 11.5% would be

below the past four years.

• USDA’s long-term projections released

in early November included 2019 corn

planted acres of 92 million, up 3% Y/Y.

Wheat

Corn

Soybeans

• USDA raised its forecast of 2018/19

seed usage of U.S. wheat by 7 million

bushels in November. This trimmed its

ending stocks projection to 949 million

bushels.

• USDA’s export forecast of 1,025 million

bushels could be too high if export sales

do not significantly improve soon.

• USDA’s long-term projections included

2019/20 wheat plantings of 51.0 million

acres, which would be up 7% Y/Y.

However, wet conditions this fall have

hindered winter wheat planting progress

and could limit the increase in acreage.

• USDA cut its U.S. soybean yield estimate

1.0 bushel per acre to 52.1 bushels,

which reduced its production estimate by

90 million bushels.

• The smaller crop and a 10-million-bushel

increase in crush were more than offset

by cuts in the other usage categories.

Exports were slashed 160 million bushels

as business to China remains minimal

due to the high tariff. USDA’s carryout

forecast increased 70 million bushels to

955 million, reflecting the largest stocks-

to-use ratio in 33 years.

• USDA’s long-term projections included

2019 soybean plantings of 82.5 million

acres, which would be down 7% Y/Y.

Source: USDA WASDE

Source: USDA WASDE

Source: USDA WASDE

2016/17 2017/18 2018/19F 2018/19F M/M Change Y/Y Change

October November 18/19 Forecast 18/19 Forecast

Acres Planted (mm) 94.0 90.2 89.1 89.1 0.0 -1.1

Acres Harvested 86.7 82.7 81.8 81.8 0.0 -0.9

Yield per Harvested Acre (bu) 174.6 176.6 180.7 178.9 -1.8 2.3

Beginning Stocks (mm bu) 1,737 2,293 2,140 2,140 0 -153

Production 15,148 14,604 14,778 14,626 -152 22

Imports 57 36 50 50 0 14

Total Supply 16,942 16,934 16,968 16,816 -152 -118

Feed and Residual 5,470 5,302 5,550 5,500 -50 198

Food, Seed & Industrial 6,885 7,054 7,130 7,130 0 76

Ethanol 5,432 5,601 5,650 5,650 0 49

Total Domestic 12,355 12,355 12,680 12,630 -50 275

Exports 2,294 2,438 2,475 2,450 -25 12

Total Use 14,649 14,793 15,155 15,080 -75 287

Ending Stocks 2,293 2,140 1,813 1,736 -77 -404

Stocks to Use (%) 15.7% 14.5% 12.0% 11.5% -0.5% -3.0%

Average Farm Price ($/bu) $3.36 $3.36 $3.50 $3.60 $0.10 $0.24

2016/17 2017/18 2018/19F 2018/19F M/M Change Y/Y Change

October November 18/19 Forecast 18/19 Forecast

Acres Planted (mm) 50.1 46.0 47.8 47.8 0.0 1.8

Acres Harvested 43.9 37.5 39.6 39.6 0.0 2.1

Yield per Harvested Acre (bu) 52.7 46.3 47.6 47.6 0.0 1.3

Beginning Stocks (mm bu) 976 1,181 1,099 1,099 0 -82

Production 2,309 1,740 1,884 1,884 0 144

Imports 118 157 140 140 0 -17

Total Supply 3,402 3,078 3,123 3,123 0 45

Food 949 964 970 970 0 6

Seed 61 63 62 69 7 6

Feed and Residual 161 50 110 110 0 60

Total Domestic 1,171 1,078 1,142 1,149 7 71

Exports 1,051 901 1,025 1,025 0 124

Total Use 2,222 1,979 2,167 2,174 7 195

Ending Stocks 1,181 1,099 956 949 -7 -150

Stocks to Use (%) 53.2% 55.5% 44.1% 43.7% -0.5% -11.9%

Average Farm Price ($/bu) $3.89 $4.72 $5.10 $5.10 $0.00 $0.38

2016/17 2017/18 2018/19F 2018/19F M/M Change Y/Y Change

October November 18/19 Forecast 18/19 Forecast

Acres Planted (mm) 83.4 90.1 89.1 89.1 0.0 -1.0

Acres Harvested 82.7 89.5 88.3 88.3 0.0 -1.2

Yield per Harvested Acre (bu) 52.0 49.3 53.1 52.1 -1.0 2.8

Beginning Stocks (mm bu) 197 302 438 438 0 136

Production 4,296 4,411 4,690 4,600 -90 189

Imports 22 22 25 25 0 3

Total Supply 4,515 4,734 5,153 5,063 -90 329

Crushings 1,899 2,055 2,070 2,080 10 25

Exports 2,174 2,129 2,060 1,900 -160 -229

Seed 105 104 103 96 -7 -8

Residual 35 8 34 32 -2 24

Total Use 4,213 4,296 4,268 4,107 -161 -189

Ending Stocks 302 438 885 955 70 517

Stocks to Use (%) 7.2% 10.2% 20.7% 23.3% 2.5% 13.1%

Average Farm Price ($/bu) $9.47 $9.33 $8.60 $8.60 $0.00 -$0.73

August 2012

7

© 2018 Wells Fargo Bank, N.A. All rights reserved. For public use.

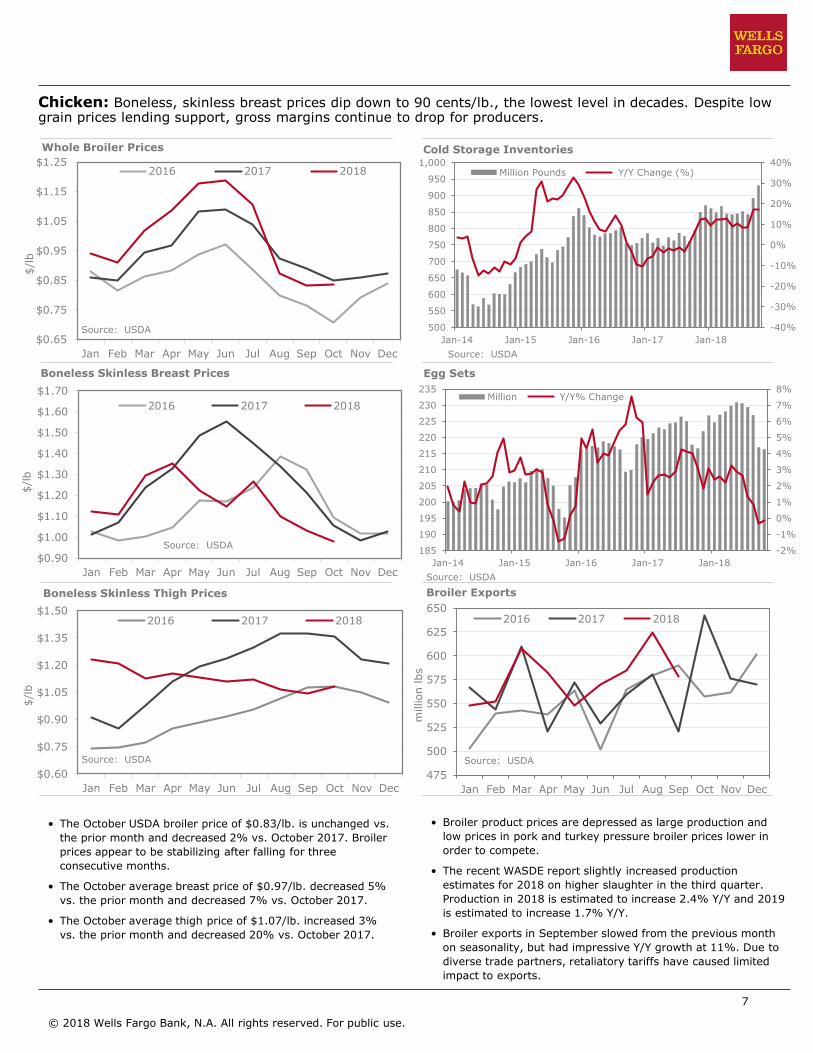

Chicken: Boneless, skinless breast prices dip down to 90 cents/lb., the lowest level in decades. Despite low grain prices lending support, gross margins continue to drop for producers.

Whole Broiler Prices Cold Storage Inventories

Broiler Exports

Egg Sets

• The October USDA broiler price of $0.83/lb. is unchanged vs.

the prior month and decreased 2% vs. October 2017. Broiler

prices appear to be stabilizing after falling for three

consecutive months.

• The October average breast price of $0.97/lb. decreased 5%

vs. the prior month and decreased 7% vs. October 2017.

• The October average thigh price of $1.07/lb. increased 3%

vs. the prior month and decreased 20% vs. October 2017.

• Broiler product prices are depressed as large production and

low prices in pork and turkey pressure broiler prices lower in

order to compete.

• The recent WASDE report slightly increased production

estimates for 2018 on higher slaughter in the third quarter.

Production in 2018 is estimated to increase 2.4% Y/Y and 2019

is estimated to increase 1.7% Y/Y.

• Broiler exports in September slowed from the previous month

on seasonality, but had impressive Y/Y growth at 11%. Due to

diverse trade partners, retaliatory tariffs have caused limited

impact to exports.

Boneless Skinless Breast Prices

Boneless Skinless Thigh Prices

$0.65

$0.75

$0.85

$0.95

$1.05

$1.15

$1.25

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

$/l

b

2016 2017 2018

Source: USDA

$0.90

$1.00

$1.10

$1.20

$1.30

$1.40

$1.50

$1.60

$1.70

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

$/l

b

2016 2017 2018

Source: USDA

$0.60

$0.75

$0.90

$1.05

$1.20

$1.35

$1.50

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

$/l

b

2016 2017 2018

Source: USDA

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

500

550

600

650

700

750

800

850

900

950

1,000

Jan-14 Jan-15 Jan-16 Jan-17 Jan-18

Million Pounds Y/Y Change (%)

Source: USDA

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

7%

8%

185

190

195

200

205

210

215

220

225

230

235

Jan-14 Jan-15 Jan-16 Jan-17 Jan-18

Million Y/Y% Change

Source: USDA

475

500

525

550

575

600

625

650

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

million lbs

2016 2017 2018

Source: USDA

August 2012

8

© 2018 Wells Fargo Bank, N.A. All rights reserved. For public use.

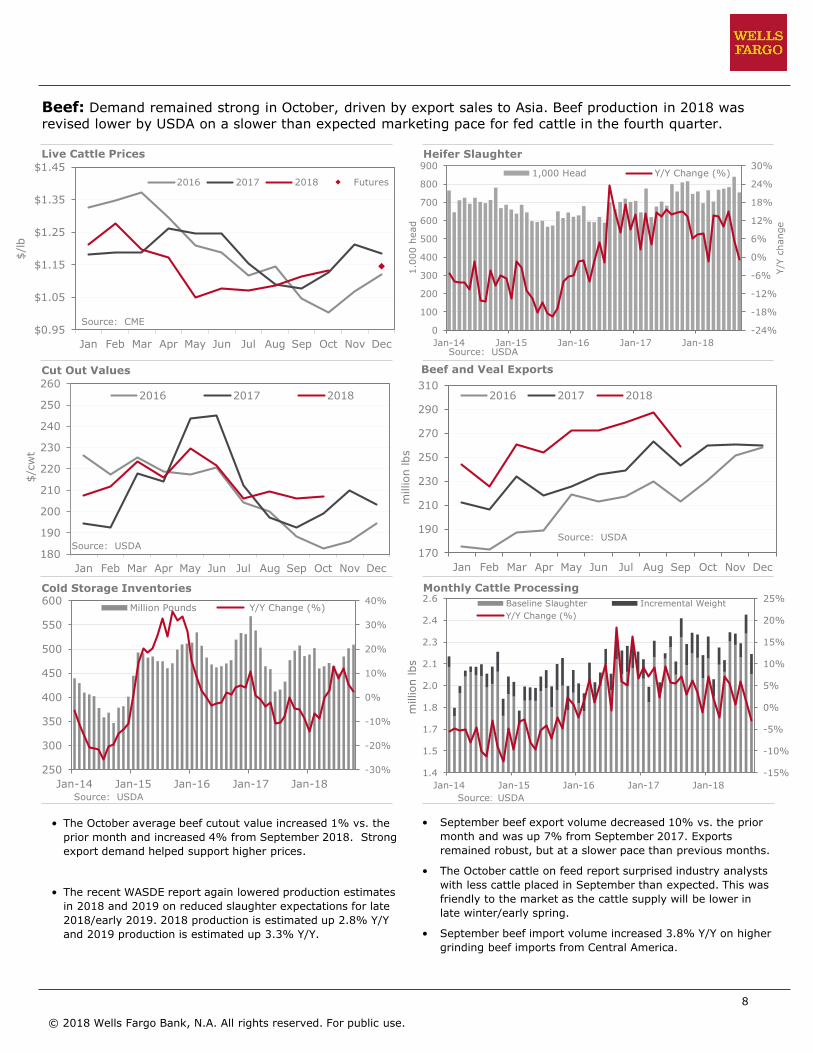

Beef: Demand remained strong in October, driven by export sales to Asia. Beef production in 2018 was

revised lower by USDA on a slower than expected marketing pace for fed cattle in the fourth quarter.

Cut Out Values

Cold Storage Inventories

Live Cattle Prices

Monthly Cattle Processing

Beef and Veal Exports

Heifer Slaughter

• The October average beef cutout value increased 1% vs. the

prior month and increased 4% from September 2018. Strong

export demand helped support higher prices.

• The recent WASDE report again lowered production estimates

in 2018 and 2019 on reduced slaughter expectations for late

2018/early 2019. 2018 production is estimated up 2.8% Y/Y

and 2019 production is estimated up 3.3% Y/Y.

• September beef export volume decreased 10% vs. the prior

month and was up 7% from September 2017. Exports

remained robust, but at a slower pace than previous months.

• The October cattle on feed report surprised industry analysts

with less cattle placed in September than expected. This was

friendly to the market as the cattle supply will be lower in

late winter/early spring.

• September beef import volume increased 3.8% Y/Y on higher

grinding beef imports from Central America.

$0.95

$1.05

$1.15

$1.25

$1.35

$1.45

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

$/l

b

2016 2017 2018 Futures

Source: CME

180

190

200

210

220

230

240

250

260

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

$/c

wt

2016 2017 2018

Source: USDA

-30%

-20%

-10%

0%

10%

20%

30%

40%

250

300

350

400

450

500

550

600

Jan-14 Jan-15 Jan-16 Jan-17 Jan-18

Million Pounds Y/Y Change (%)

Source: USDA

-24%

-18%

-12%

-6%

0%

6%

12%

18%

24%

30%

0

100

200

300

400

500

600

700

800

900

Jan-14 Jan-15 Jan-16 Jan-17 Jan-18

Y/Y

change

1.0

00 h

ead

1,000 Head Y/Y Change (%)

Source: USDA

170

190

210

230

250

270

290

310

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

million lbs

2016 2017 2018

Source: USDA

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

1.4

1.5

1.7

1.8

2.0

2.1

2.3

2.4

2.6

Jan-14 Jan-15 Jan-16 Jan-17 Jan-18

million lbs

Baseline Slaughter Incremental Weight

Y/Y Change (%)

Source: USDA

August 2012

9

© 2018 Wells Fargo Bank, N.A. All rights reserved. For public use.

Pork: African Swine Fever continues to spread in China, creating uncertainty for global supplies into Q1. Lower prices helped keep September exports above last year’s levels. Seasonally higher hog supplies are expected to pressure prices in the next couple of months.

Cut Out Values

Cold Storage Inventories

Lean Hog Prices

Pork Exports

Monthly Processing

Sow Slaughter

• Nearby lean hog futures averaged $0.61/lb. in October.This increased 7% from September, and decreased 1% Y/Y.

• The average cut-out value increased 6% in October, and wasup 5% Y/Y. Supply disruptions from Hurricane Michael gavesupport to cut-out prices.

• The recent WASDE report lowered production estimates in2018 and 2019 on reduced slaughter expectations and lowercarcass weights. 2018 production is estimated at 2.9% Y/Yand 2019 production is estimated at 5.3% Y/Y.

• Pork exports in September were 3% higher Y/Y, but haveslowed from their robust pace in the first half of the year.Although volume was higher, the dollar value was 3.5%lower Y/Y, indicating that cheaper product was needed toattracted buyers.

• Hog slaughter traditionally hits its seasonal highs in Q4.Record hog production in 2018 is challenging packerslaughter capacity.

$0.40

$0.50

$0.60

$0.70

$0.80

$0.90

$1.00

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

$/l

b

2016 2017 2018 Futures

Source: CME

60

70

80

90

100

110

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

$/c

wt

2016 2017 2018

Source: USDA

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

300

350

400

450

500

550

600

650

700

750

Jan-14 Jan-15 Jan-16 Jan-17 Jan-18

Million Pounds Y/Y Change (%)

Source: USDA

-12%

-8%

-4%

0%

4%

8%

12%

0

2

4

6

8

10

12

Jan-14 Jan-15 Jan-16 Jan-17 Jan-18

Y/Y

change

million h

ead

Million Head Y/Y Change

Source: USDA

360

390

420

450

480

510

540

570

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

million lbs

2016 2017 2018

Source: USDA

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

1.6

1.7

1.8

1.9

2.0

2.1

2.2

2.3

2.4

Jan-14 Jan-15 Jan-16 Jan-17 Jan-18

million lbs

Baseline Slaughter Incremental Weight

Y/Y Change (%)

Source: USDA

August 2012

10

© 2018 Wells Fargo Bank, N.A. All rights reserved. For public use.

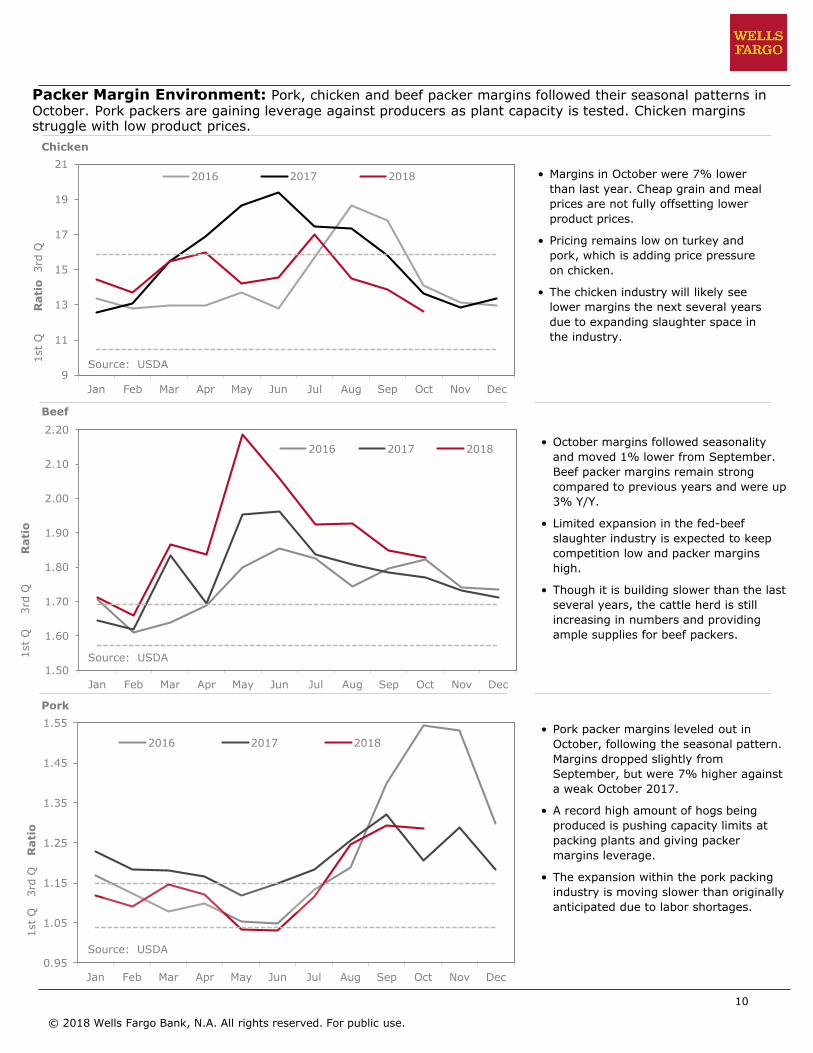

Packer Margin Environment: Pork, chicken and beef packer margins followed their seasonal patterns in October. Pork packers are gaining leverage against producers as plant capacity is tested. Chicken margins struggle with low product prices.

Beef

Chicken

Pork

• October margins followed seasonality

and moved 1% lower from September.

Beef packer margins remain strong

compared to previous years and were up3% Y/Y.

• Limited expansion in the fed-beef

slaughter industry is expected to keep

competition low and packer margins

high.

• Though it is building slower than the last

several years, the cattle herd is still

increasing in numbers and providing

ample supplies for beef packers.

• Pork packer margins leveled out in

October, following the seasonal pattern.

Margins dropped slightly from

September, but were 7% higher against

a weak October 2017.

• A record high amount of hogs being

produced is pushing capacity limits at

packing plants and giving packer

margins leverage.

• The expansion within the pork packing

industry is moving slower than originally

anticipated due to labor shortages.

• Margins in October were 7% lower

than last year. Cheap grain and meal

prices are not fully offsetting lower

product prices.

• Pricing remains low on turkey and

pork, which is adding price pressure

on chicken.

• The chicken industry will likely see

lower margins the next several years

due to expanding slaughter space in

the industry.

9

11

13

15

17

19

21

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

1st

Q

Rati

o3rd

Q

2016 2017 2018

Source: USDA

1.50

1.60

1.70

1.80

1.90

2.00

2.10

2.20

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

1st

Q

3rd

Q

Rati

o

2016 2017 2018

Source: USDA

0.95

1.05

1.15

1.25

1.35

1.45

1.55

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

1st

Q 3

rd Q

R

ati

o

2016 2017 2018

Source: USDA

August 2012

11

© 2018 Wells Fargo Bank, N.A. All rights reserved. For public use.

Seafood: Prices continue to advance for both cod and pollock on forecasted lower quotas in 2019. The

expected lower quota is overshadowing concerns about the U.S. 10% import tariff on product brought back into the U.S. after Chinese processing.

• The UB farm-raised white shrimp index in October was$4.00/lb., down 14% Y/Y. YTD ’18 shrimp imports are1,083MM lbs., up 4% Y/Y. Low prices continue to generateincreased demand for shrimp imports.

• The UB fresh-farmed salmon index was slightly higher inOctober at $5.66/lb., which is up 6% Y/Y. YTD Atlantic salmonimports through September totaled 537MM lbs., up 10% Y/Y.

• Pollock prices are expected to continue rising due to a 2.7%projected decline in global pollock supply in 2019. Alaskanpollock quota is expected to be cut by 6%. Russia will also seea decline in quota, but not until 2020.

Urner Barry Fresh Farmed Salmon Index

Urner Barry Farm-Raised White Shrimp Index Shrimp Import Volume

Alaskan Pollock Prices

Atlantic Salmon Import Volume

• Cod prices remained flat in October, but are 14% higher Y/Y.

The cod quota for 2019 was cut by 5%. The lower quota is

expected to support prices into early 2019.

• Live lobster prices averaged $8.66/lb. in October. This is up

slightly from September, and up 12% Y/Y. Lobster prices are

stable despite the Chinese tariff.

• Scallop prices jumped higher to $11.22/lb. in October, up 7%

from September and 7% higher Y/Y.

Scallop and Lobster Prices

3.80

3.95

4.10

4.25

4.40

4.55

4.70

4.85

5.00

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

$/l

b

2016 2017 2018

Source: Urner Barry

4.00

4.50

5.00

5.50

6.00

6.50

7.00

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

$/l

b

2016 2017 2018

Source: Urner Barry

0.60

0.75

0.90

1.05

1.20

1.35

1.50

1.65

Jan-16 Jul-16 Jan-17 Jul-17 Jan-18 Jul-18

$/l

b

Single Freeze Alaskan Minced

Source: Urner Barry

35

40

45

50

55

60

65

70

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

million k

g

2016 2017 2018

Source: NOAA

20

21

22

23

24

25

26

27

28

29

30

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

million k

g

2016 2017 2018

Source: NOAA

5

6

7

8

9

10

11

12

13

14

15

16

Jan-16 Jul-16 Jan-17 Jul-17 Jan-18 Jul-18

$

Scallops (US Natural, 10/20 ct)

Live Lobster (1 1/4 lb)

Source: Urner Barry

August 2012

12

© 2018 Wells Fargo Bank, N.A. All rights reserved. For public use.

Dairy: Cheese prices moved lower in October due to higher production. Dairy cow numbers are shrinking,but stronger milk per cow growth is offsetting any potential production declines.

Class I Milk

Cheddar Cheese, 40-lb. block

Milk Production

Dairy Product Exports

• The October USDA Class I milk price of $16.33/cwt increased

10% vs. the prior month and decreased 1% vs. October

2017. The October average Class III milk price of

$15.53/cwt. decreased 3% vs. the prior month and

decreased 7% vs. October 2017.

• The recent WASDE report slightly lowered production

estimates based on lower cow herd numbers. Stronger

growth in milk per cow is expected to partially offset lower

herd numbers. 2018 production is estimated up 1.1% Y/Y

and 2019 production is estimated up 1.4% Y/Y.

• U.S. milk production in September was up 1.3% Y/Y on stronger

milk per cow growth. The milk cow herd size was down slightly

vs. the prior year.

• Cheese production in September increased 3.1% Y/Y, a record

for the month. Butter production decreased slightly at 0.1%

Y/Y.

• The October USDA average cheddar cheese price of $1.59/lb.

decreased 3% vs. the prior month and decreased 8% Y/Y

• October average USDA Grade AA butter prices of $2.26/lb.

increased slightly at 0.2% vs. the prior month and decreased

3% vs. October 2017.

Class III Milk

Butter Prices, Grade AA

13

14

15

16

17

18

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

$/c

wt

2016 2017 2018

Source: USDA

12

13

14

15

16

17

18

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2016 2017 2018 Futures

Sources: USDA, CME

$/c

wt

1.3

1.4

1.5

1.6

1.7

1.8

1.9

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

$/l

b

2016 2017 2018

Source: USDA

-2%

-1%

0%

1%

2%

3%

4%

5%

13

14

15

16

17

18

19

20

Jan-14 Jan-15 Jan-16 Jan-17 Jan-18

billion lbs

Million Pounds Y/Y Change (%)

Source: USDA

1.6

1.8

2.0

2.2

2.4

2.6

2.8

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

$/l

b

2016 2017 2018

Source: USDA

300

350

400

450

500

550

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

million lbs

2016 2017 2018

Source: USDA

August 2012

13

© 2018 Wells Fargo Bank, N.A. All rights reserved. For public use.

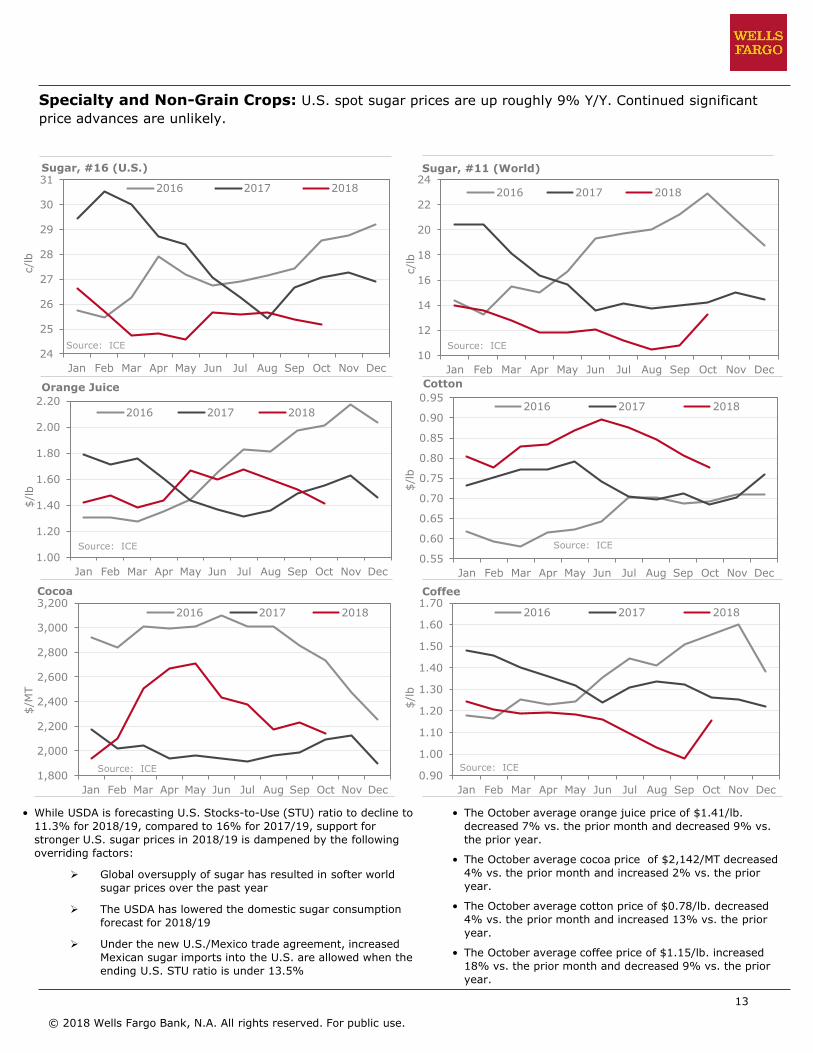

Specialty and Non-Grain Crops: U.S. spot sugar prices are up roughly 9% Y/Y. Continued significant

price advances are unlikely.

Sugar, #16 (U.S.)

Cocoa

Sugar, #11 (World)

CottonOrange Juice

Coffee

• While USDA is forecasting U.S. Stocks-to-Use (STU) ratio to decline to11.3% for 2018/19, compared to 16% for 2017/19, support for

stronger U.S. sugar prices in 2018/19 is dampened by the following

overriding factors:

Global oversupply of sugar has resulted in softer world

sugar prices over the past year

The USDA has lowered the domestic sugar consumption

forecast for 2018/19

Under the new U.S./Mexico trade agreement, increased

Mexican sugar imports into the U.S. are allowed when the

ending U.S. STU ratio is under 13.5%

• The October average orange juice price of $1.41/lb.

decreased 7% vs. the prior month and decreased 9% vs.

the prior year.

• The October average cocoa price of $2,142/MT decreased

4% vs. the prior month and increased 2% vs. the prior

year.

• The October average cotton price of $0.78/lb. decreased

4% vs. the prior month and increased 13% vs. the prior

year.

• The October average coffee price of $1.15/lb. increased

18% vs. the prior month and decreased 9% vs. the prior

year.

24

25

26

27

28

29

30

31

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

c/l

b

2016 2017 2018

Source: ICE

1.00

1.20

1.40

1.60

1.80

2.00

2.20

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

$/l

b

2016 2017 2018

Source: ICE

1,800

2,000

2,200

2,400

2,600

2,800

3,000

3,200

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

$/M

T

2016 2017 2018

Source: ICE

10

12

14

16

18

20

22

24

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

c/l

b

2016 2017 2018

Source: ICE

0.55

0.60

0.65

0.70

0.75

0.80

0.85

0.90

0.95

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

$/l

b2016 2017 2018

Source: ICE

0.90

1.00

1.10

1.20

1.30

1.40

1.50

1.60

1.70

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

$/l

b

2016 2017 2018

Source: ICE

August 2012

14

© 2018 Wells Fargo Bank, N.A. All rights reserved. For public use.

0

1

2

3

4

5

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

million t

ons

Grape Crush Trends, 2008 - 2017

Raisin Table Red White

Specialty and Non-Grain Crops: Tree Nut and Wine Grape Harvest are wrapping up. Nut harvest has produced large crops of excellent quality, but smaller nut sizing is being noted. West Coast wine grape areas report a large crop of good quality.Almonds

Walnuts Hazelnuts

• Almond, pistachio, and walnut harvest are wrapping up across

California with large crops being reported. Quality is very good,

although smaller than normal nut size is being reported.

• Almond pollinators were coming in heavier than the non-pareil

varietal. Early season indications are that crop will not meet

USDA 2.45B lb. projection. Prices stable at $2.00 to $2.50/lb.

depending on variety and size.

• Walnut harvest is wrapping up, and it is being reported that

yields may not reach the 680M lb. USDA projection. Walnut

prices continue to be reported in the $.90 to $.91 per pound for

new crop Jumbo Chandlers.

• Pistachio harvest is expected to come in heavy, around

900MM to 975MM pounds. Prices are holding firm within the

$2.50 to$3.00 range.

• Hurricane Michael has effected the Georgia Pecan crop.

Damage has been reported from trees blowing over and to

harvested nuts on the ground due to water damage. Damage

estimates are not yet available.

Pistachios

2017 Grape Crush Results

• Vintners reported abundant yields in line with the UnitedStates Department of Agriculture’s August forecast of 4.1 MMtons.

• Vintners are enthusiastic about both the quality and quantityof the 2018.

• Industry potentially feeling an oversupply issue as bulk wineprices are low to clear tanks for new harvest.

• Pricing in the spot market is trending down on most varietalsand locations.

Source: Gomberg Fredrikson and Wine Institute

0

60

120

180

240

300

360

420

480

0

150

300

450

600

750

900

1,050

1,200

80/81 85/86 90/91 95/96 00/01 05/06 10/11 15/16

c/l

b

1,0

00 a

cre

s

Bearing Acres Price

Source: USDA

0

70

140

210

280

350

420

490

0

50

100

150

200

250

300

350

80/81 85/86 90/91 95/96 00/01 05/06 10/11 15/16

c/l

b

1,0

00 a

cre

s

Bearing Acres Price

Source: USDA

0

100

200

300

400

500

600

700

800

0

40

80

120

160

200

240

280

320

80/81 85/86 90/91 95/96 00/01 05/06 10/11 15/16

c/l

b

1,0

00 a

cre

s

Bearing Acres Price

Source: USDA

0

70

140

210

280

350

420

490

560

0

5

10

15

20

25

30

35

40

80/81 85/86 90/91 95/96 00/01 05/06 10/11 15/16

c/l

b

1,0

00 a

cre

s

Bearing Acres Price

Source: USDA

August 2012

15

© 2018 Wells Fargo Bank, N.A. All rights reserved. For public use.

Framing Lumber Index U.S. Housing Starts

Repair & Remodel Expenditures (LTM total)

• The Framing Lumber Composite Index dropped another

15% in October to $367/thousand sq. ft. This was down

16% Y/Y and the lowest since January 2017 as demand has

not been strong enough to sustain prices at the lofty levels

seen during the first half of 2018. Despite the decline in

recent months, lumber prices are in line with levels seen

during much of 2016.

• The Structural Panel Composite Index fell 11% in October

to $419/thousand sq. ft. amid the drop in lumber prices.

This was down 22% Y/Y and the lowest since June 2017.

• U.S. housing starts of 1.20 million units in September

were up 4% Y/Y. Declines in lumber and structural panel

prices from their high levels during the first half of 2018

appear to have help housing starts rebound.

• LTM repair and remodel expenditures of $331.1 billion

during 3Q’18 were up 2% from the previous quarter and

up 7% Y/Y, reflecting the largest Y/Y increase since 2007.

Structural Panel Index

Forest Products: Lumber and structural panel prices fell sharply in October to the lowest level in over a year. September housing starts were up 4% Y/Y, and repair/remodel spending rose again in 3Q’18.

$280

$320

$360

$400

$440

$480

$520

$560

$600

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

$/1

,000 s

qft

2016 2017 2018

Source: Random Lengths

$320

$360

$400

$440

$480

$520

$560

$600

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

$/1

,000 s

qft

2016 2017 2018

Source: Random Lengths

-20%

-10%

0%

10%

20%

30%

40%

800

900

1,000

1,100

1,200

1,300

1,400

Jan-14 Jan-15 Jan-16 Jan-17 Jan-18

1,0

00 u

nits

New Units Y/Y Change (%)

Source: U.S. Fed

0%

1%

2%

3%

4%

5%

6%

7%

8%

200

220

240

260

280

300

320

340

1Q12 1Q13 1Q14 1Q15 1Q16 1Q17 1Q18

$ b

illion

$ Billion Y/Y Change (%)

Source: Harvard Joint Center for Housing Studies

August 2012

16

© 2018 Wells Fargo Bank, N.A. All rights reserved. For public use.

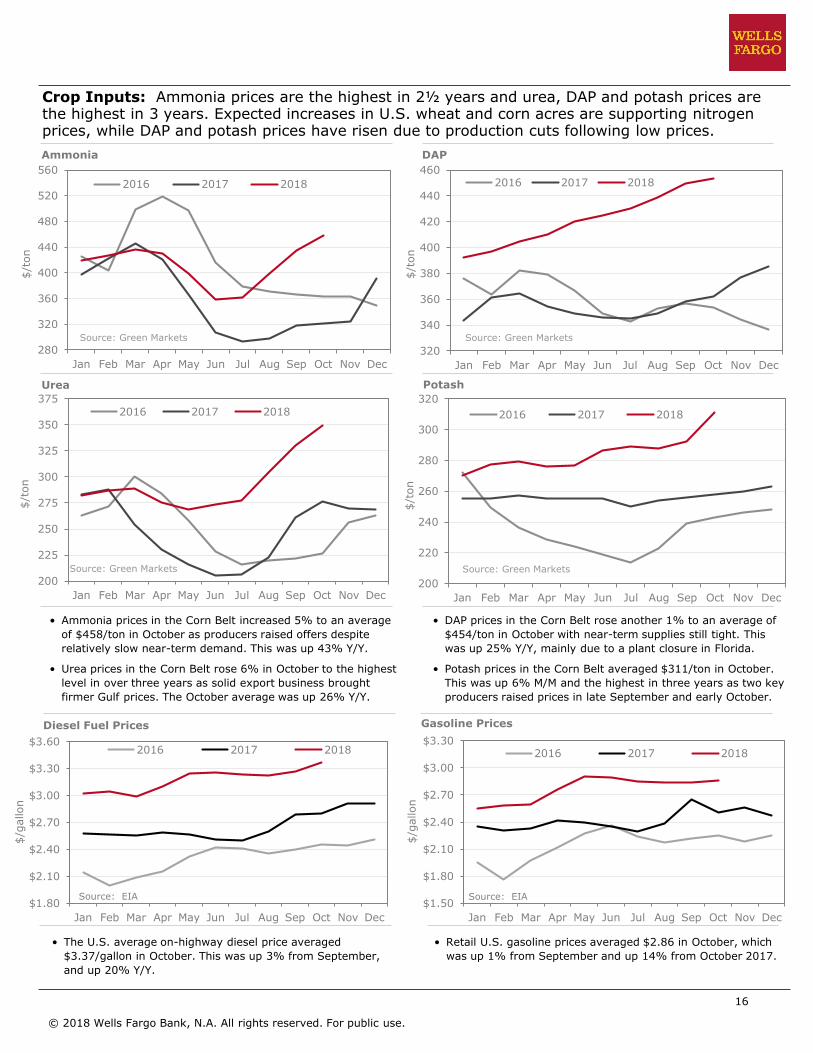

Crop Inputs: Ammonia prices are the highest in 2½ years and urea, DAP and potash prices are the highest in 3 years. Expected increases in U.S. wheat and corn acres are supporting nitrogen prices, while DAP and potash prices have risen due to production cuts following low prices.

Ammonia DAP

Urea Potash

• Ammonia prices in the Corn Belt increased 5% to an average

of $458/ton in October as producers raised offers despite

relatively slow near-term demand. This was up 43% Y/Y.

• Urea prices in the Corn Belt rose 6% in October to the highest

level in over three years as solid export business brought

firmer Gulf prices. The October average was up 26% Y/Y.

• DAP prices in the Corn Belt rose another 1% to an average of

$454/ton in October with near-term supplies still tight. This

was up 25% Y/Y, mainly due to a plant closure in Florida.

• Potash prices in the Corn Belt averaged $311/ton in October.

This was up 6% M/M and the highest in three years as two key

producers raised prices in late September and early October.

Diesel Fuel Prices Gasoline Prices

• The U.S. average on-highway diesel price averaged

$3.37/gallon in October. This was up 3% from September,

and up 20% Y/Y.

• Retail U.S. gasoline prices averaged $2.86 in October, which

was up 1% from September and up 14% from October 2017.

280

320

360

400

440

480

520

560

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

$/t

on

2016 2017 2018

Source: Green Markets

200

225

250

275

300

325

350

375

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

$/t

on

2016 2017 2018

Source: Green Markets

320

340

360

380

400

420

440

460

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

$/t

on

2016 2017 2018

Source: Green Markets

200

220

240

260

280

300

320

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

$/t

on

2016 2017 2018

Source: Green Markets

$1.80

$2.10

$2.40

$2.70

$3.00

$3.30

$3.60

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

$/g

allon

2016 2017 2018

Source: EIA$1.50

$1.80

$2.10

$2.40

$2.70

$3.00

$3.30

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

$/g

allon

2016 2017 2018

Source: EIA

August 2012

17

© 2018 Wells Fargo Bank, N.A. All rights reserved. For public use.

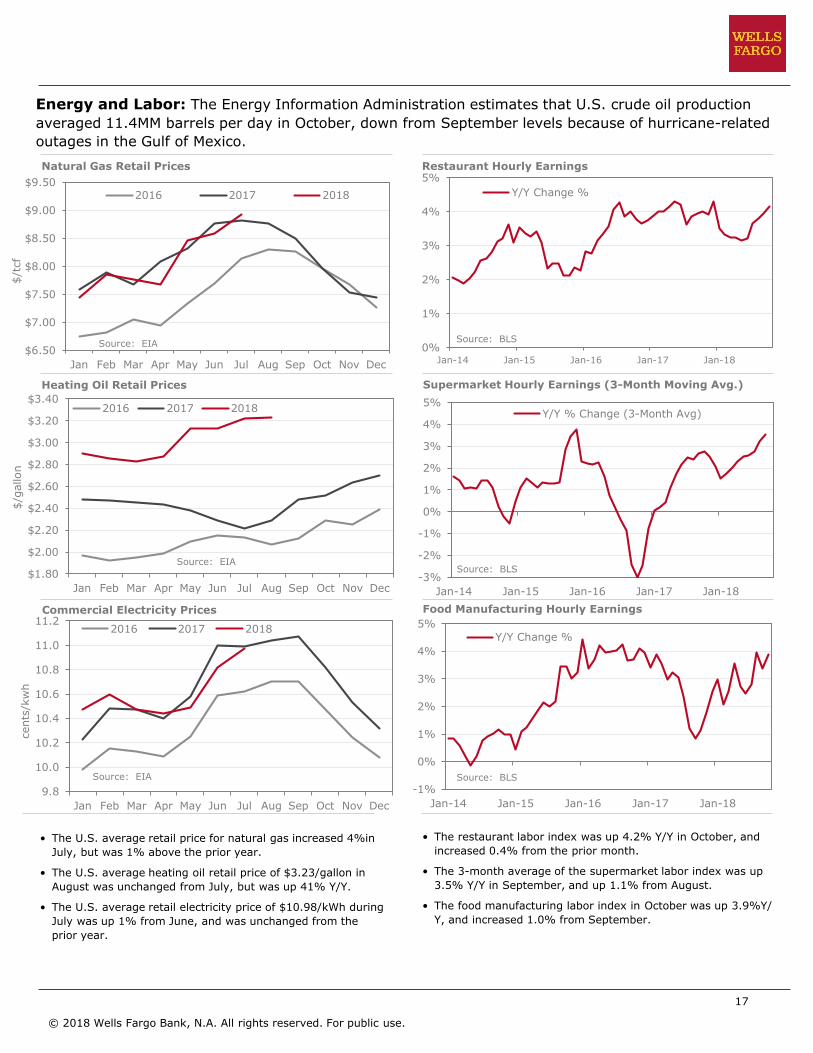

Energy and Labor: The Energy Information Administration estimates that U.S. crude oil production

averaged 11.4MM barrels per day in October, down from September levels because of hurricane-related

outages in the Gulf of Mexico.

Natural Gas Retail Prices Restaurant Hourly Earnings

Heating Oil Retail Prices Supermarket Hourly Earnings (3-Month Moving Avg.)

Commercial Electricity Prices Food Manufacturing Hourly Earnings

• The U.S. average retail price for natural gas increased 4%in

July, but was 1% above the prior year.

• The U.S. average heating oil retail price of $3.23/gallon in

August was unchanged from July, but was up 41% Y/Y.

• The U.S. average retail electricity price of $10.98/kWh during

July was up 1% from June, and was unchanged from the

prior year.

• The restaurant labor index was up 4.2% Y/Y in October, and

increased 0.4% from the prior month.

• The 3-month average of the supermarket labor index was up

3.5% Y/Y in September, and up 1.1% from August.

• The food manufacturing labor index in October was up 3.9%Y/

Y, and increased 1.0% from September.

$6.50

$7.00

$7.50

$8.00

$8.50

$9.00

$9.50

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

$/t

cf

2016 2017 2018

Source: EIA

$1.80

$2.00

$2.20

$2.40

$2.60

$2.80

$3.00

$3.20

$3.40

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

$/g

allon

2016 2017 2018

Source: EIA

9.8

10.0

10.2

10.4

10.6

10.8

11.0

11.2

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

cents

/kw

h

2016 2017 2018

Source: EIA

0%

1%

2%

3%

4%

5%

Jan-14 Jan-15 Jan-16 Jan-17 Jan-18

Y/Y Change %

Source: BLS

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

Jan-14 Jan-15 Jan-16 Jan-17 Jan-18

Y/Y % Change (3-Month Avg)

Source: BLS

-1%

0%

1%

2%

3%

4%

5%

Jan-14 Jan-15 Jan-16 Jan-17 Jan-18

Y/Y Change %

Source: BLS

August 2012

18

© 2018 Wells Fargo Bank, N.A. All rights reserved. For public use.

Food and Agribusiness Industry Advisors

General disclosuresThe views expressed are intended for Wells Fargo customers only. They present the opinions of the authors on prospective trends and related matters in food and agribusiness as of this date, and do not necessarily reflect the views of Wells Fargo & Co., its affiliates and subsidiaries. Opinions expressed are based on diverse sources that we believe to be reliable, though the information is not guaranteed and is subject to change without notice. This is not an offer to sell or the solicitation to buy or sell any security or foreign exchange product.

Karol Aure-FlynnSpecialty Crops Analyst, Analyst Team [email protected]

Chris EggermanSector Analyst: Grains, Crop Inputs, Forest Products [email protected]

Lakiesha McCainCredit Portfolio Consultant: Systems Administrator [email protected]

Brad RubinSector Analyst: Specialty and Non-Grain Crops [email protected]

Courtney SchmidtSector Analyst: Protein, [email protected]

Michael Swanson, Ph.D.Chief Agricultural Economist [email protected]

Kevin BergquistForest Products Sector [email protected]

Matt DusiSpecialty and Non-Grain Crops Sector Manager [email protected]

Scott EtzelProtein - Seafood and Sugar Sector [email protected]

Tim LuginslandGrains and Oilseeds Sector Manager [email protected]

Lee Ann PearceSpecialty and Non-Grain Crops Sector Manager [email protected]

Lon SwansonCrop Inputs/Feed Sector [email protected]

![[Frozen Food Market Research] Frozen Food Insights - Zpryme Research - July 2011](https://static.fdocuments.in/doc/165x107/5414026b8d7f7294698b47d5/frozen-food-market-research-frozen-food-insights-zpryme-research-july-2011.jpg)