Fnma 150418215501-conversion-gate01

57

John Connell | Angela Morisette | Parker Kim U N I V E R S I T Y O F T E A S

-

Upload

usittech -

Category

Investor Relations

-

view

2.323 -

download

0

Transcript of Fnma 150418215501-conversion-gate01

John Connell | Angela Morisette | Parker Kim

U N I V E R S I T Y O F T E A S

ConclusionInvestmentOverview

Valuation Considerations ConclusionLitigation

Par

ker

Kim

, Jo

hn

Co

nn

ell,

An

gela

Mo

rise

tte

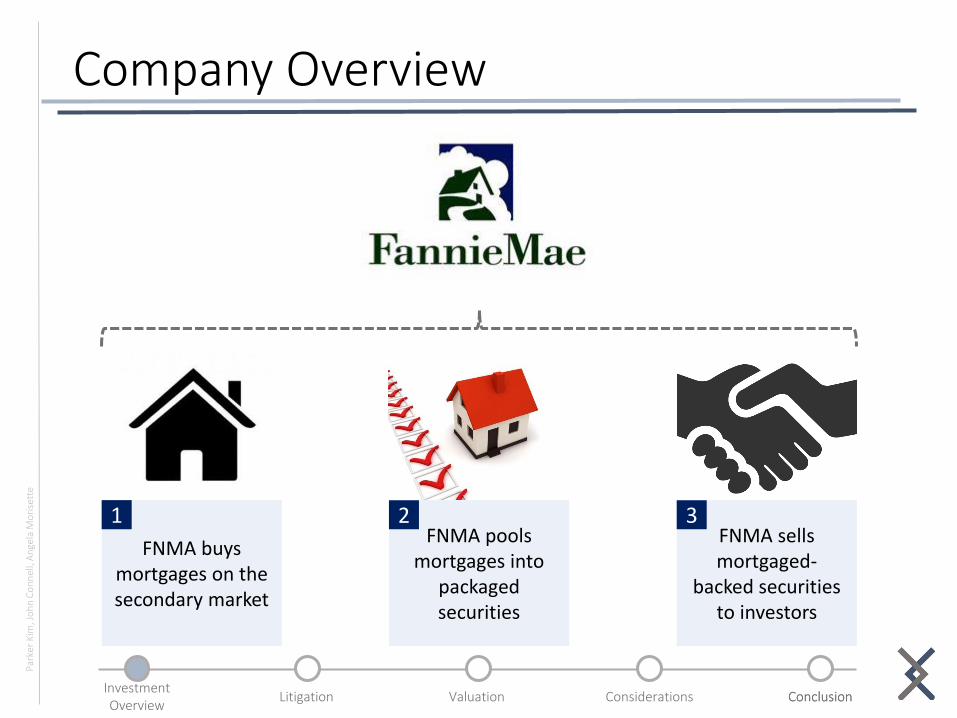

Company Overview

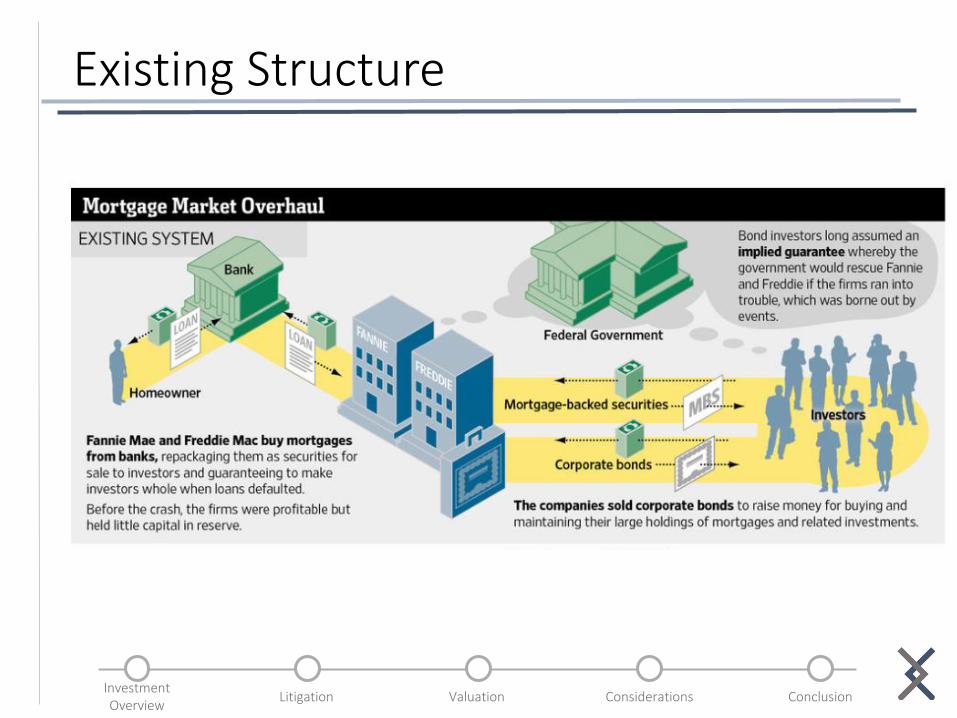

FNMA buys mortgages on the secondary market

1FNMA pools

mortgages into packaged securities

2FNMA sells mortgaged-

backed securities to investors

3

ConclusionInvestmentOverview

Valuation Considerations ConclusionLitigation

Par

ker

Kim

, Jo

hn

Co

nn

ell,

An

gela

Mo

rise

tte

Company Overview

FNMA buys mortgages on the secondary market

1FNMA pools

mortgages into packaged securities

2FNMA sells mortgaged-

backed securities to investors

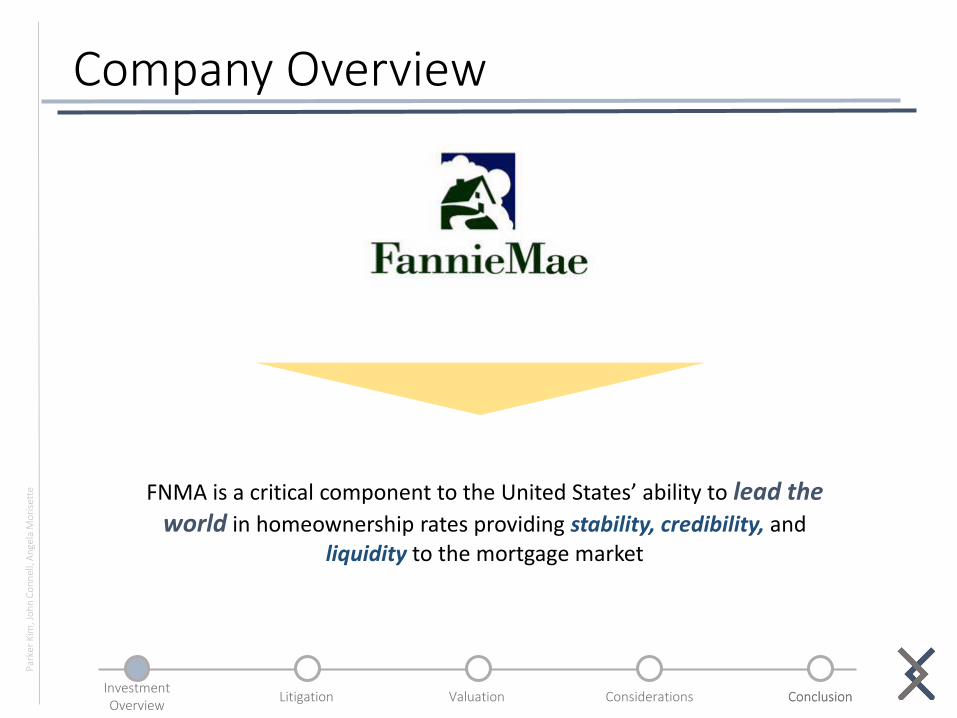

3FNMA is a critical component to the United States’ ability to lead the

world in homeownership rates providing stability, credibility, andliquidity to the mortgage market

ConclusionInvestmentOverview

Valuation Considerations ConclusionLitigation

Par

ker

Kim

, Jo

hn

Co

nn

ell,

An

gela

Mo

rise

tte

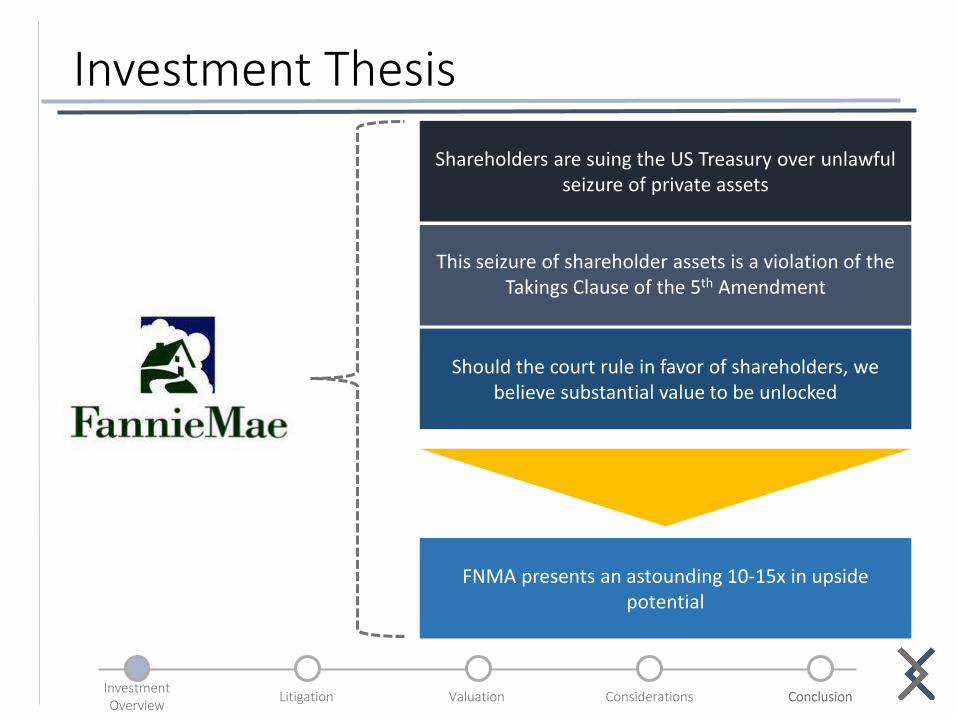

Investment Thesis

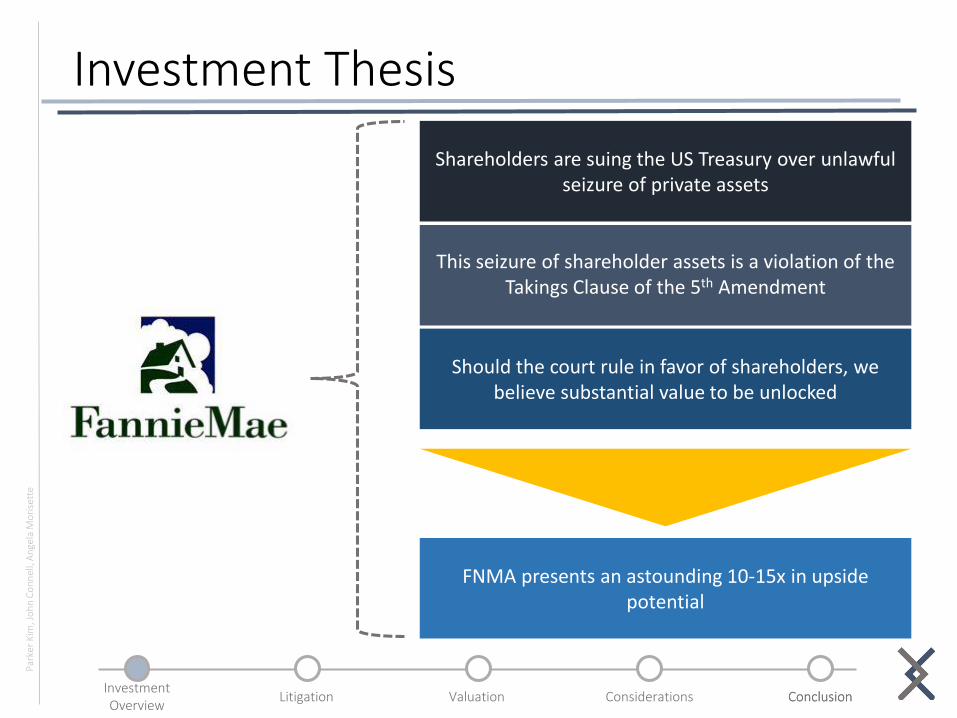

Shareholders are suing the US Treasury over unlawful seizure of private assets

This seizure of shareholder assets is a violation of the Takings Clause of the 5th Amendment

Should the court rule in favor of shareholders, we believe substantial value to be unlocked

FNMA presents an astounding 10-15x in upside potential

ConclusionInvestmentOverview

Valuation Considerations ConclusionLitigation

Par

ker

Kim

, Jo

hn

Co

nn

ell,

An

gela

Mo

rise

tte

FNMA Timeline

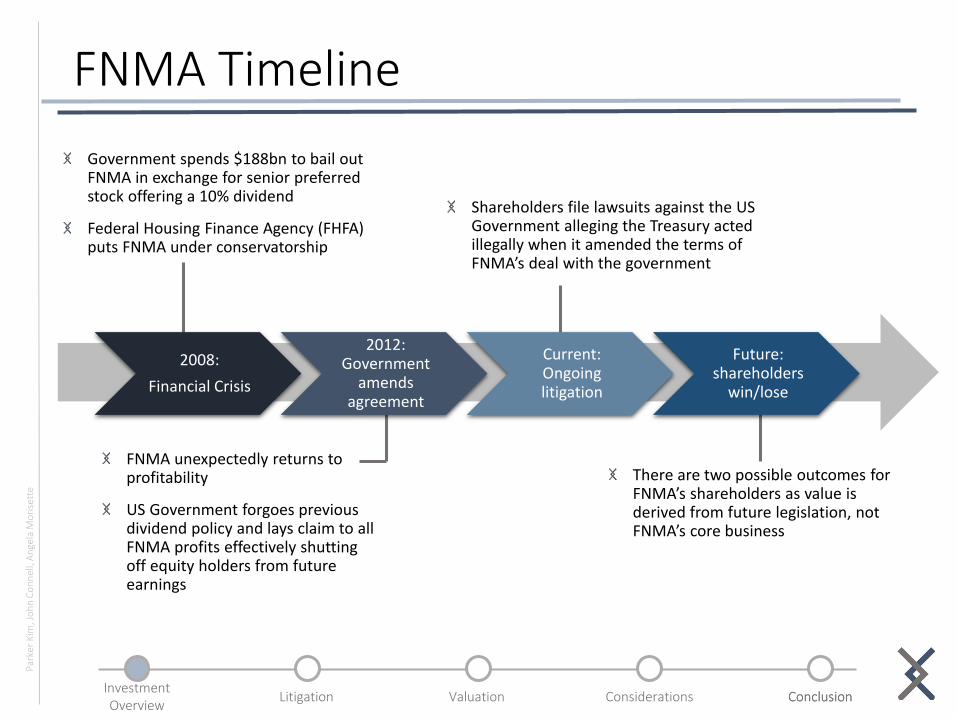

Government spends $188bn to bail out FNMA in exchange for senior preferred stock offering a 10% dividend

Federal Housing Finance Agency (FHFA) puts FNMA under conservatorship

2008:

Financial Crisis

2012: Government

amends agreement

Current: Ongoing litigation

Future: shareholders

win/lose

FNMA unexpectedly returns to profitability

US Government forgoes previous dividend policy and lays claim to all FNMA profits effectively shutting off equity holders from future earnings

Shareholders file lawsuits against the US Government alleging the Treasury acted illegally when it amended the terms of FNMA’s deal with the government

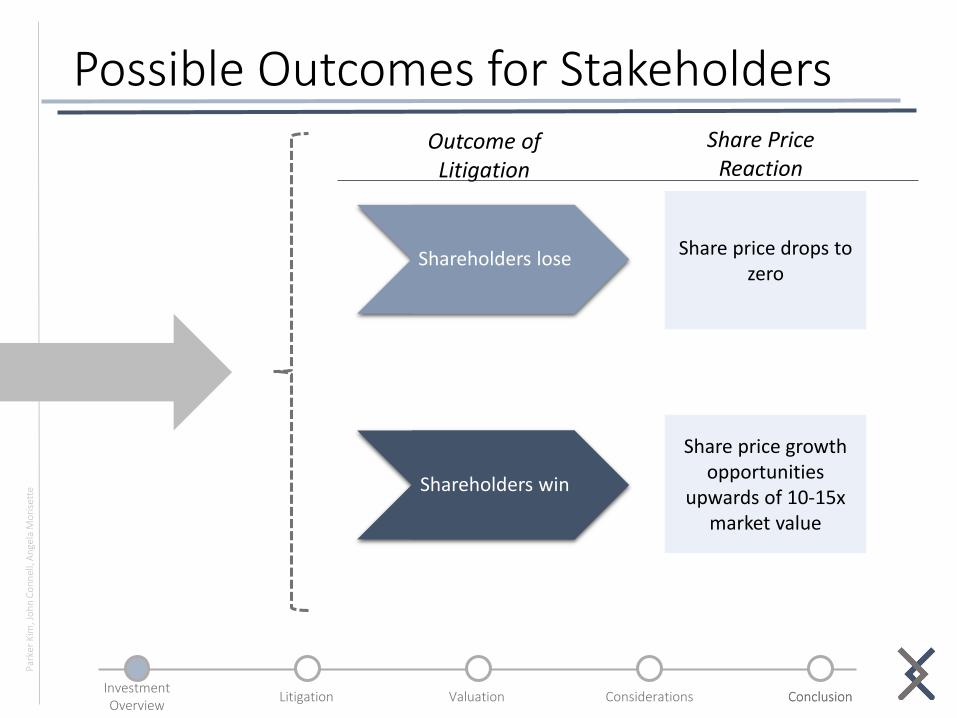

There are two possible outcomes for FNMA’s shareholders as value is derived from future legislation, not FNMA’s core business

ConclusionInvestmentOverview

Valuation Considerations ConclusionLitigation

Par

ker

Kim

, Jo

hn

Co

nn

ell,

An

gela

Mo

rise

tte

Possible Outcomes for Stakeholders

Shareholders lose

Shareholders win

Share price drops to zero

Share price growth opportunities

upwards of 10-15x market value

Share Price Reaction

Outcome of Litigation

itigation

InvestmentOverview

Valuation Considerations ConclusionLitigation

Par

ker

Kim

, Jo

hn

Co

nn

ell,

An

gela

Mo

rise

tte

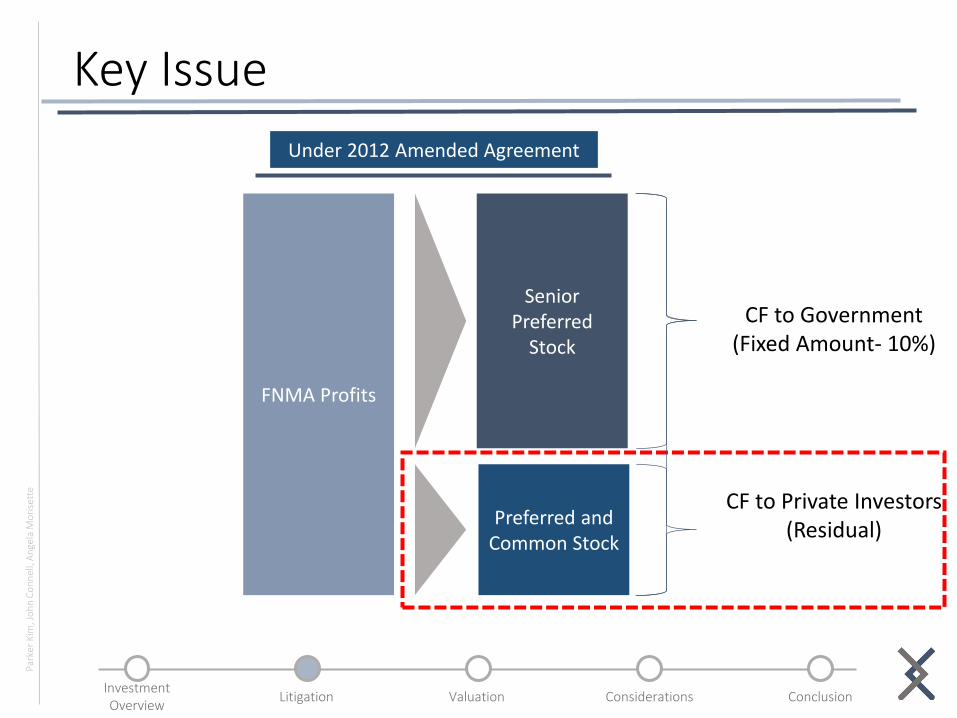

Key Issue

Under 2008 SPS Agreement

FNMA Profits

CF to Government(Fixed Amount- 10%)

CF to Private Investors(Residual)

Senior Preferred

Stock

Preferred and Common Stock

Under 2012 Amended Agreement

InvestmentOverview

Valuation Considerations ConclusionLitigation

Par

ker

Kim

, Jo

hn

Co

nn

ell,

An

gela

Mo

rise

tte

Key Issue

Under 2008 SPS Agreement

FNMA Profits

CF to Government(Fixed Amount- 10%)

CF to Private Investors(Residual)

Senior Preferred

Stock

Preferred and Common Stock

Senior Preferred

Stock

CF to GovernmentAll Profits

Under 2012 Amended Agreement

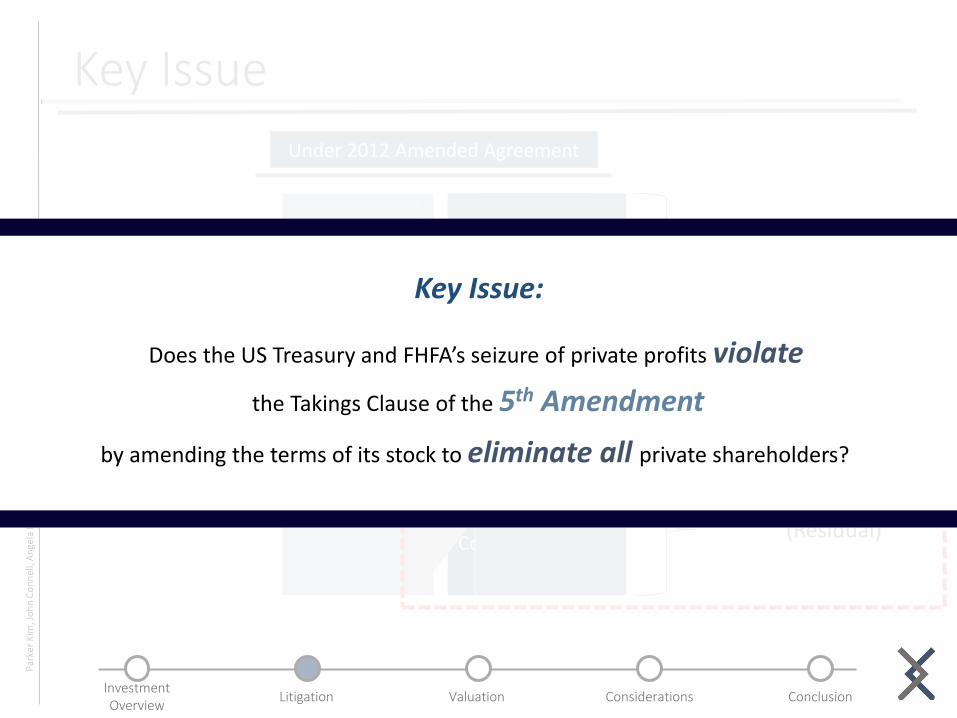

Key Issue:

Does the US Treasury and FHFA’s seizure of private profits violate

by amending the terms of its stock to eliminate all private shareholders?

the Takings Clause of the 5th Amendment

InvestmentOverview

Valuation Considerations ConclusionLitigation

Par

ker

Kim

, Jo

hn

Co

nn

ell,

An

gela

Mo

rise

tte

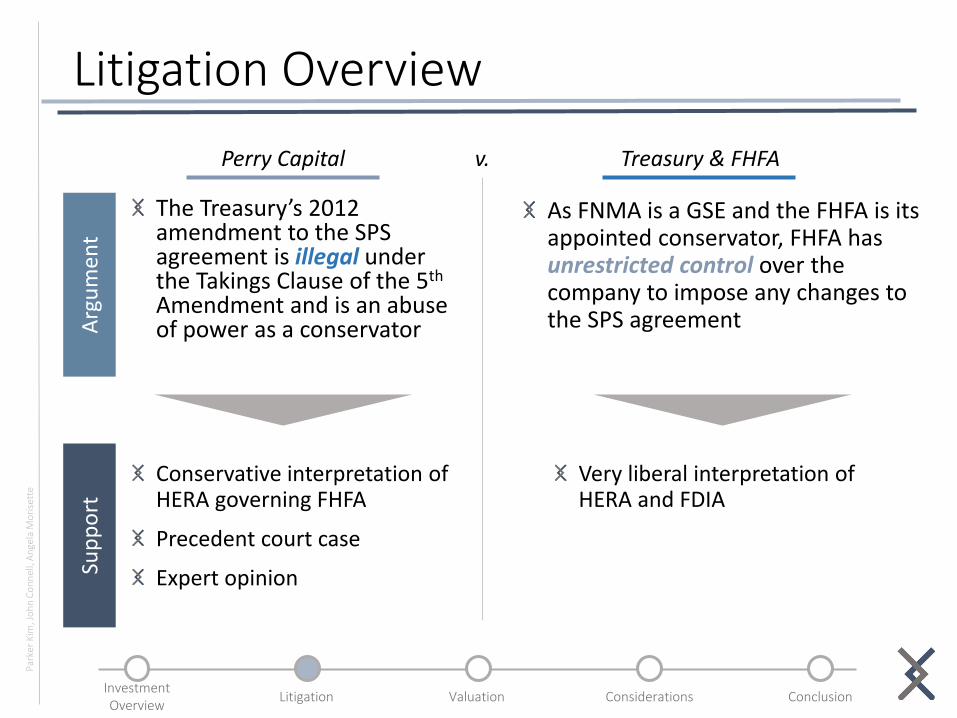

Litigation Overview

Perry Capital Treasury & FHFAv.

Arg

um

ent

Sup

po

rt

The Treasury’s 2012 amendment to the SPS agreement is illegal under the Takings Clause of the 5th

Amendment and is an abuse of power as a conservator

As FNMA is a GSE and the FHFA is its appointed conservator, FHFA has unrestricted control over the company to impose any changes to the SPS agreement

Conservative interpretation of HERA governing FHFA

Precedent court case

Expert opinion

Very liberal interpretation of HERA and FDIA

InvestmentOverview

Valuation Considerations ConclusionLitigation

Par

ker

Kim

, Jo

hn

Co

nn

ell,

An

gela

Mo

rise

tte

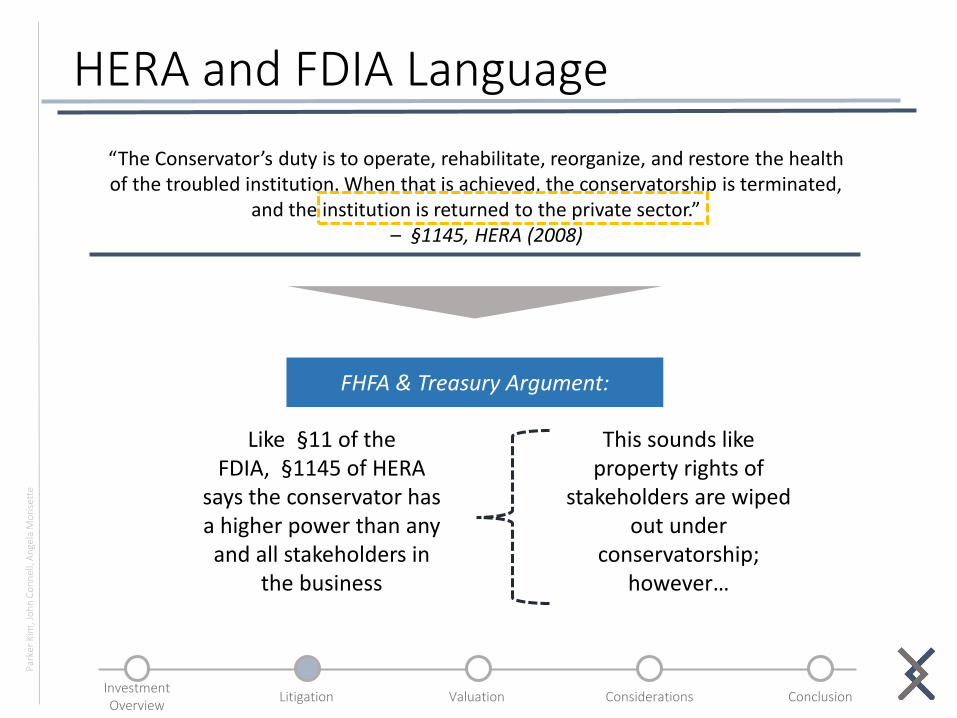

HERA and FDIA Language

“The Conservator’s duty is to operate, rehabilitate, reorganize, and restore the health of the troubled institution. When that is achieved, the conservatorship is terminated,

and the institution is returned to the private sector.” – §1145, HERA (2008)

FHFA & Treasury Argument:

Like §11 of the FDIA, §1145 of HERA

says the conservator has a higher power than any and all stakeholders in

the business

This sounds like property rights of

stakeholders are wiped out under

conservatorship; however…

InvestmentOverview

Valuation Considerations ConclusionLitigation

Par

ker

Kim

, Jo

hn

Co

nn

ell,

An

gela

Mo

rise

tte

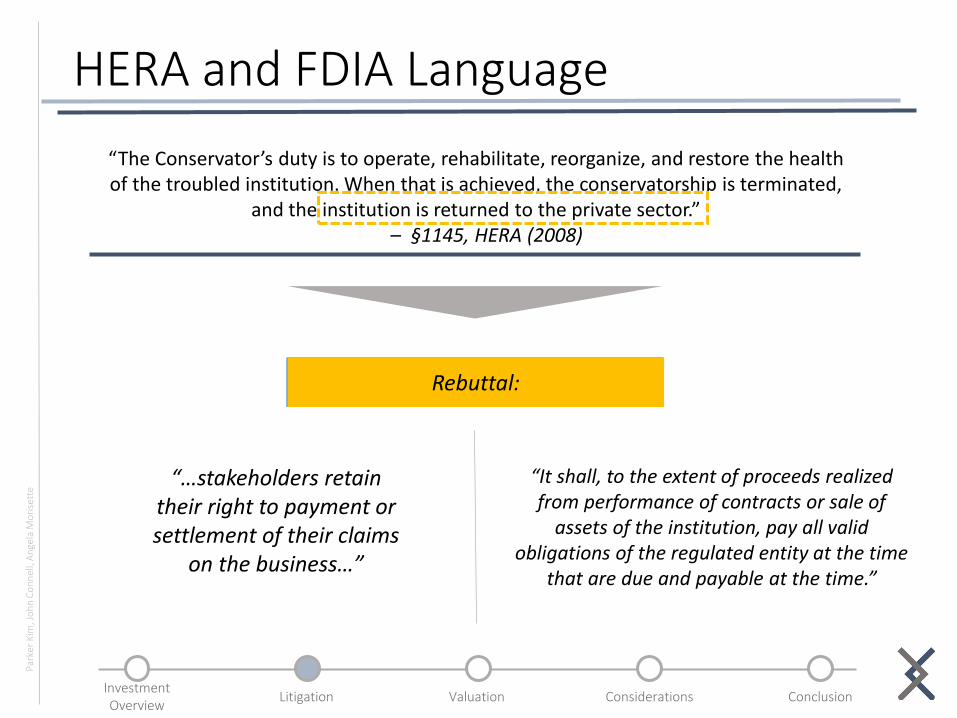

HERA and FDIA Language

“The Conservator’s duty is to operate, rehabilitate, reorganize, and restore the health of the troubled institution. When that is achieved, the conservatorship is terminated,

and the institution is returned to the private sector.” – §1145, HERA (2008)

FHFA & Treasury Argument:

Like §11 of the FDIA, §1145 of HERA

says the conservator has a higher power than any and all stakeholders in

the business

This sounds like property rights of

stakeholders are wiped out under

conservatorship; however…

“…stakeholders retain their right to payment or settlement of their claims

on the business…”

“It shall, to the extent of proceeds realized from performance of contracts or sale of

assets of the institution, pay all valid obligations of the regulated entity at the time

that are due and payable at the time.”

Rebuttal:

InvestmentOverview

Valuation Considerations ConclusionLitigation

Par

ker

Kim

, Jo

hn

Co

nn

ell,

An

gela

Mo

rise

tte

HERA and FDIA Language

“The Conservator’s duty is to operate, rehabilitate, reorganize, and restore the health of the troubled institution. When that is achieved, the conservatorship is terminated,

and the institution is returned to the private sector.” – §1145, HERA (2008)

FHFA & Treasury Argument:

Like §11 of the FDIA, §1145 of HERA

says the conservator has a higher power than any and all stakeholders in

the business

This sounds like property rights of

stakeholders are wiped out under

conservatorship; however…

“…stakeholders retain their right to payment or settlement of their claims

on the business…”

“It shall, to the extent of proceeds realized from performance of contracts or sale of

assets of the institution, pay all valid obligations of the regulated entity at the time

that are due and payable at the time.”

Rebuttal:

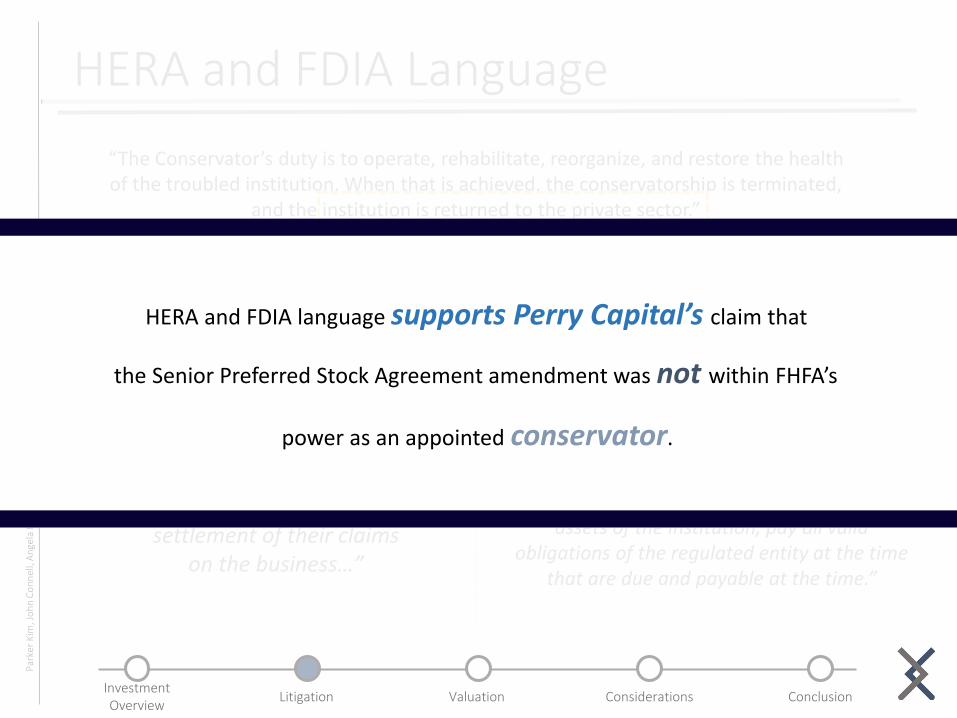

HERA and FDIA language supports Perry Capital’s claim that

the Senior Preferred Stock Agreement amendment was not within FHFA’s

power as an appointed conservator.

InvestmentOverview

Valuation Considerations ConclusionLitigation

Par

ker

Kim

, Jo

hn

Co

nn

ell,

An

gela

Mo

rise

tte

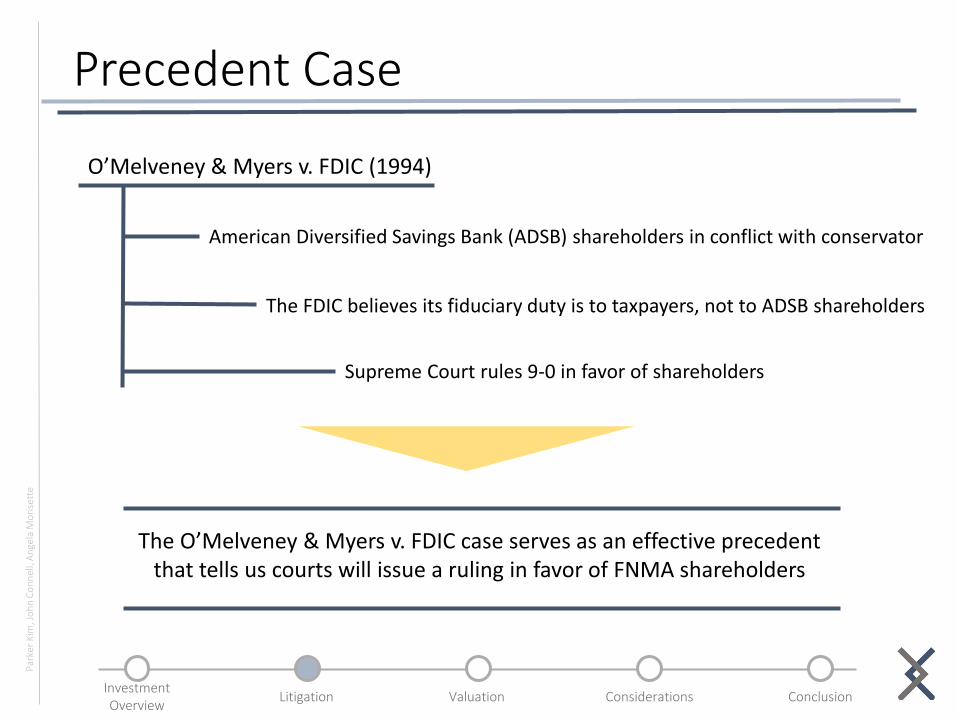

Precedent Case

O’Melveney & Myers v. FDIC (1994)

American Diversified Savings Bank (ADSB) shareholders in conflict with conservator

The FDIC believes its fiduciary duty is to taxpayers, not to ADSB shareholders

Supreme Court rules 9-0 in favor of shareholders

The O’Melveney & Myers v. FDIC case serves as an effective precedent that tells us courts will issue a ruling in favor of FNMA shareholders

InvestmentOverview

Valuation Considerations ConclusionLitigation

Par

ker

Kim

, Jo

hn

Co

nn

ell,

An

gela

Mo

rise

tte

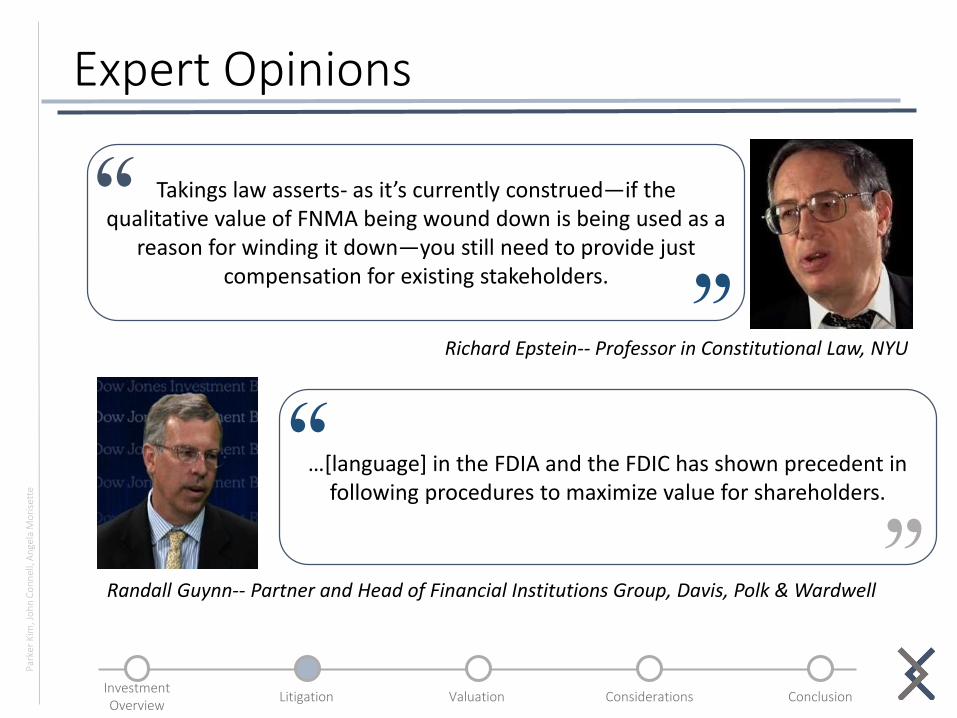

Expert Opinions

Takings law asserts- as it’s currently construed—if the qualitative value of FNMA being wound down is being used as a

reason for winding it down—you still need to provide just compensation for existing stakeholders.

““Richard Epstein-- Professor in Constitutional Law, NYU

…[language] in the FDIA and the FDIC has shown precedent in following procedures to maximize value for shareholders.

““Randall Guynn-- Partner and Head of Financial Institutions Group, Davis, Polk & Wardwell

InvestmentOverview

Valuation Considerations ConclusionLitigation

Par

ker

Kim

, Jo

hn

Co

nn

ell,

An

gela

Mo

rise

tte

Expert Opinions

If there is disclosure regarding future Fannie and Freddie earnings and the administration has a commitment that

existing Fannie and Freddie common equity holders will never receive any future positive earnings…this commitment would

be material to investors and should be disclosed.

“ “

Lewis Lowenfels-- Managing Partner, Tolins & Lowenfels

Takings law asserts- as it’s currently construed—if the qualitative value of FNMA being wound down is being used as a

reason for winding it down—you still need to provide just compensation for existing stakeholders.

““Richard Epstein-- Professor in Constitutional Law, NYU

…[language] in the FDIA and the FDIC has shown precedent in following procedures to maximize value for shareholders.

““Randall Guynn-- Partner and Head of Financial Institutions Group, Davis, Polk & Wardwell

Expert sentiment is overwhelmingly in favor of FNMA shareholders:

Additionally, experts agree that FNMA has a case on both a constitutional

and contractual basis.

aluation

InvestmentOverview

Valuation Considerations ConclusionLitigation

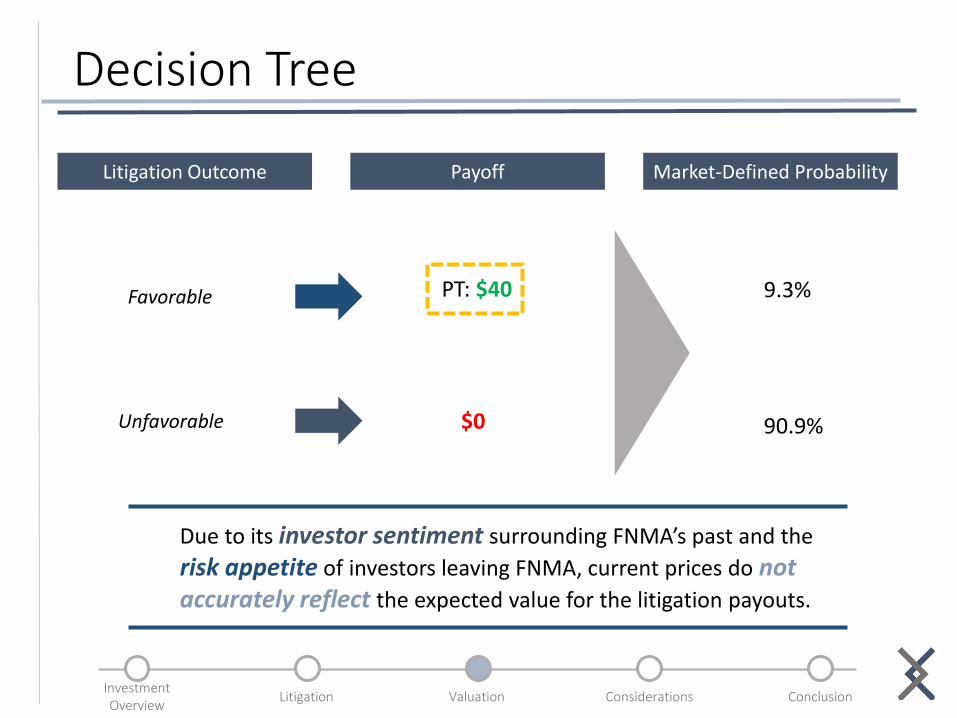

Decision Tree

Favorable

Unfavorable

PT: $40

$0

9.3%

90.9%

Litigation Outcome Payoff Market-Defined Probability

Due to its investor sentiment surrounding FNMA’s past and the

risk appetite of investors leaving FNMA, current prices do not accurately reflect the expected value for the litigation payouts.

InvestmentOverview

Valuation Considerations ConclusionLitigation

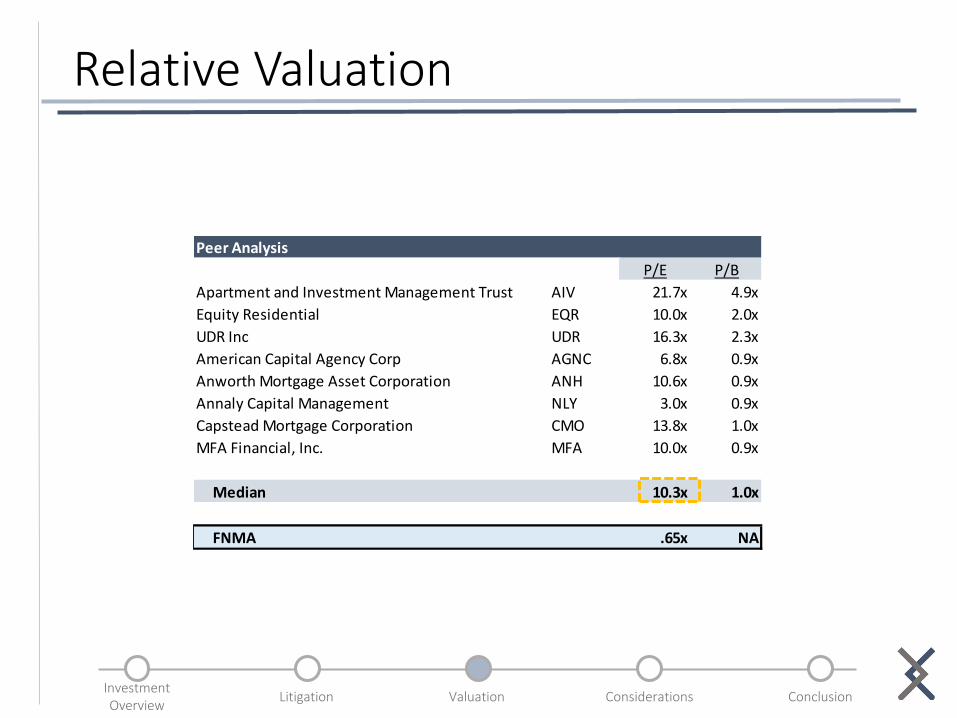

Peer Analysis

P/E P/B

Apartment and Investment Management Trust AIV 21.7x 4.9x

Equity Residential EQR 10.0x 2.0x

UDR Inc UDR 16.3x 2.3x

American Capital Agency Corp AGNC 6.8x 0.9x

Anworth Mortgage Asset Corporation ANH 10.6x 0.9x

Annaly Capital Management NLY 3.0x 0.9x

Capstead Mortgage Corporation CMO 13.8x 1.0x

MFA Financial, Inc. MFA 10.0x 0.9x

Median 10.3x 1.0x

FNMA .65x NA

Relative Valuation

InvestmentOverview

Valuation Considerations ConclusionLitigation

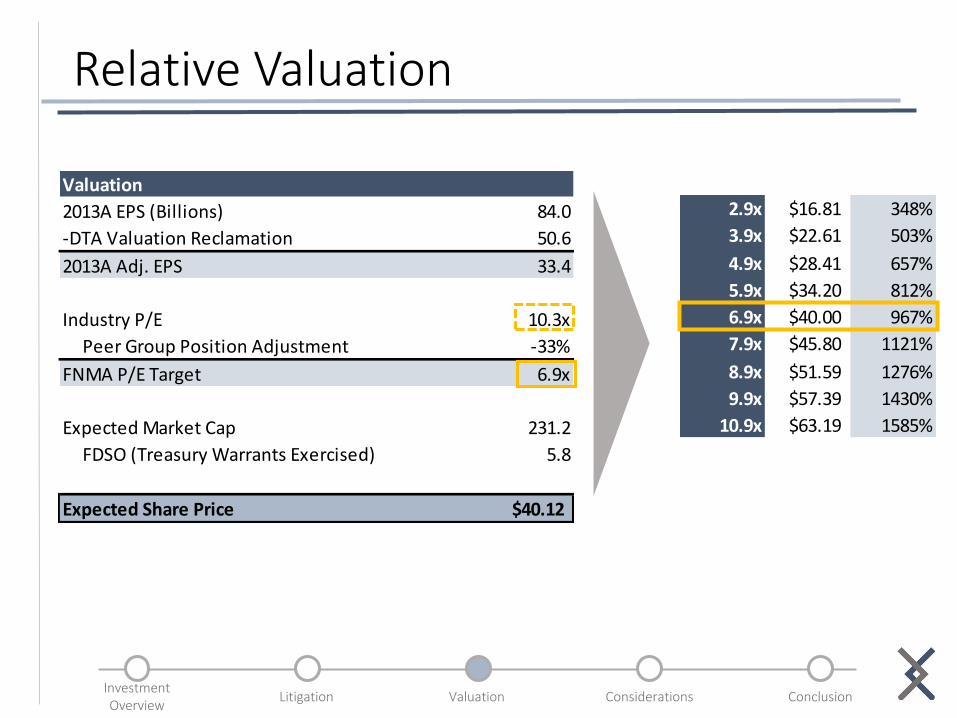

Relative Valuation

Valuation

2013A EPS (Billions) 84.0

-DTA Valuation Reclamation 50.6

2013A Adj. EPS 33.4

Industry P/E 10.3x

Peer Group Position Adjustment -33%

FNMA P/E Target 6.9x

Expected Market Cap 231.2

FDSO (Treasury Warrants Exercised) 5.8

Expected Share Price $40.12

2.9x $16.81 348%

3.9x $22.61 503%

4.9x $28.41 657%

5.9x $34.20 812%

6.9x $40.00 967%

7.9x $45.80 1121%

8.9x $51.59 1276%

9.9x $57.39 1430%

10.9x $63.19 1585%

InvestmentOverview

Valuation Considerations ConclusionLitigation

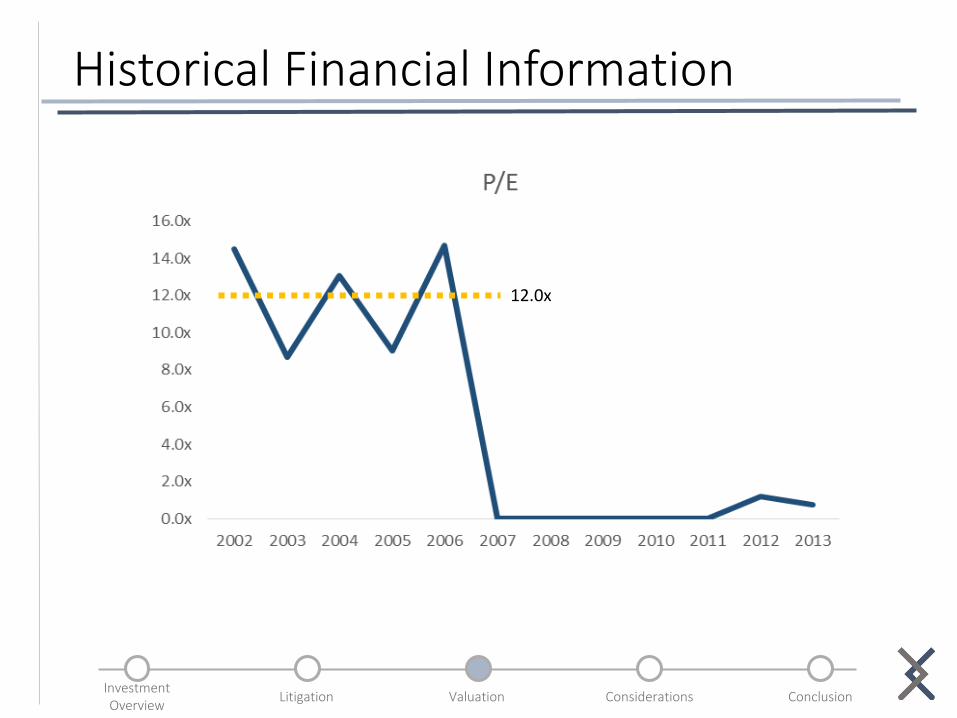

Historical Financial Information

12.0x

InvestmentOverview

Valuation Considerations ConclusionLitigation

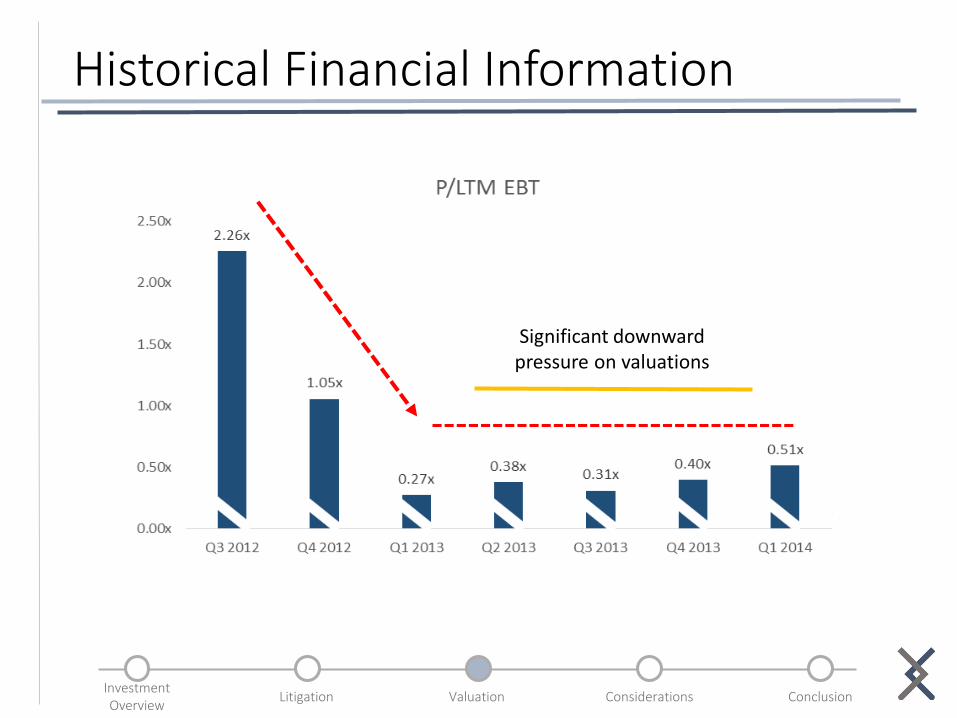

Historical Financial Information

12.0x

Significant downward pressure on valuations

InvestmentOverview

Valuation Considerations ConclusionLitigation

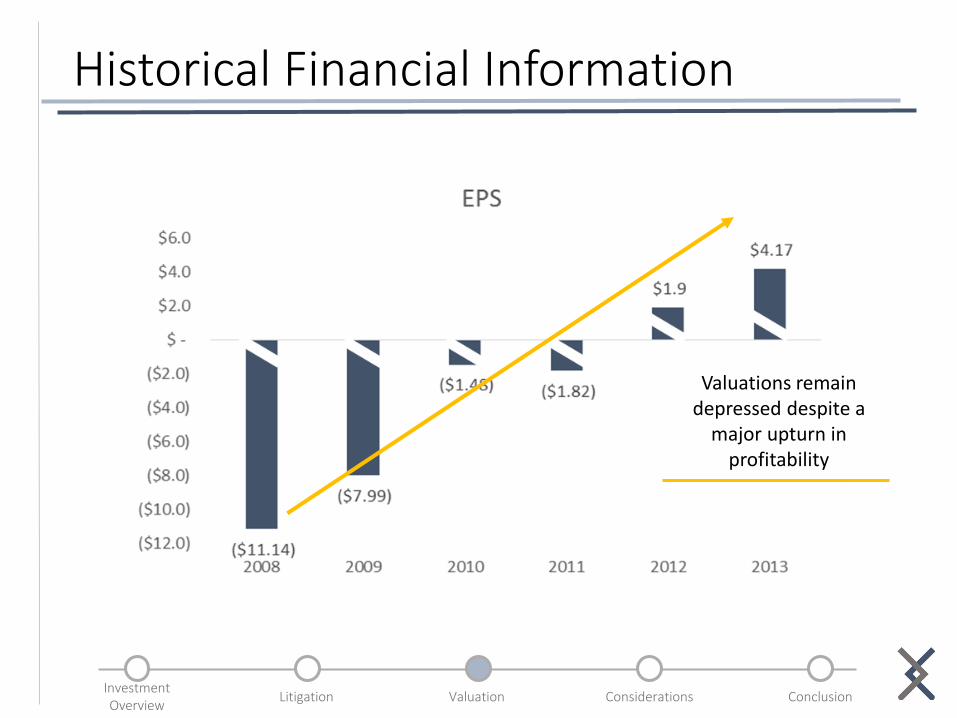

Historical Financial Information

12.0x

Significant downward pressure on valuations

Valuations remain depressed despite a

major upturn in profitability

onsiderations

InvestmentOverview

Valuation Considerations ConclusionLitigation

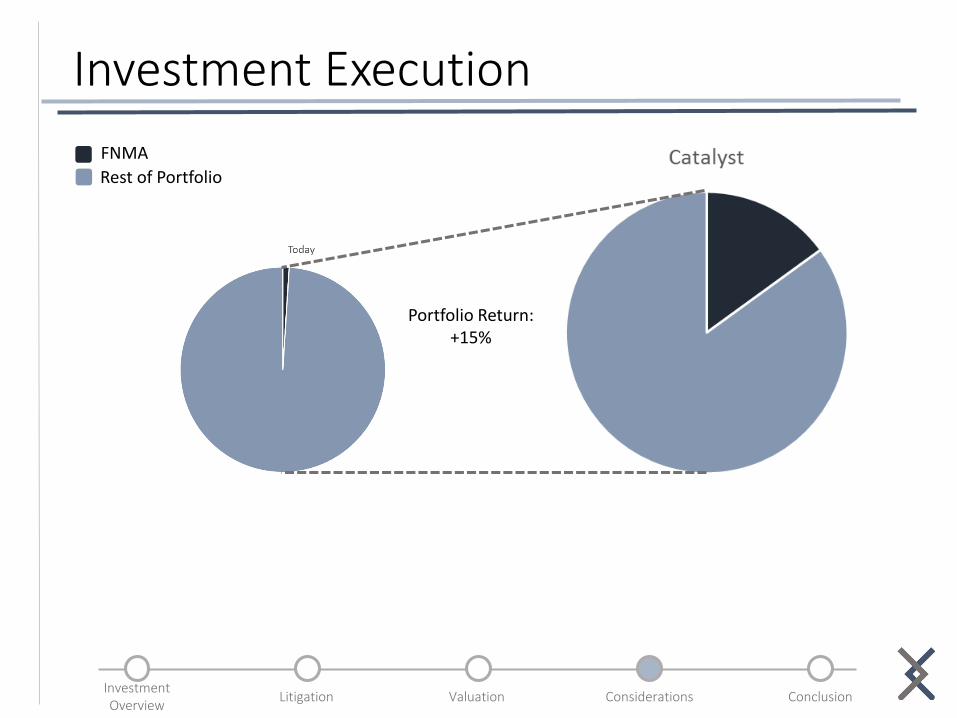

Investment Execution

Portfolio Return:+15%

FNMA

Rest of Portfolio

InvestmentOverview

Valuation Considerations ConclusionLitigation

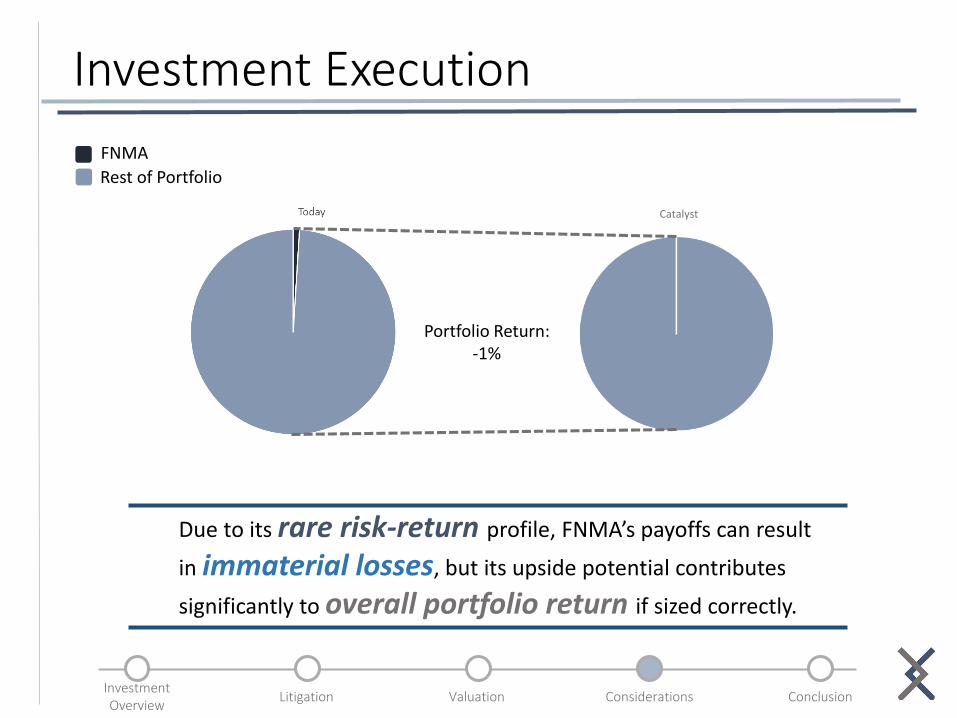

Investment Execution

Due to its rare risk-return profile, FNMA’s payoffs can result

in immaterial losses, but its upside potential contributes

significantly to overall portfolio return if sized correctly.

Portfolio Return:+15%Portfolio Return:

-1%

Catalyst

FNMA

Rest of Portfolio

InvestmentOverview

Valuation Considerations ConclusionLitigation

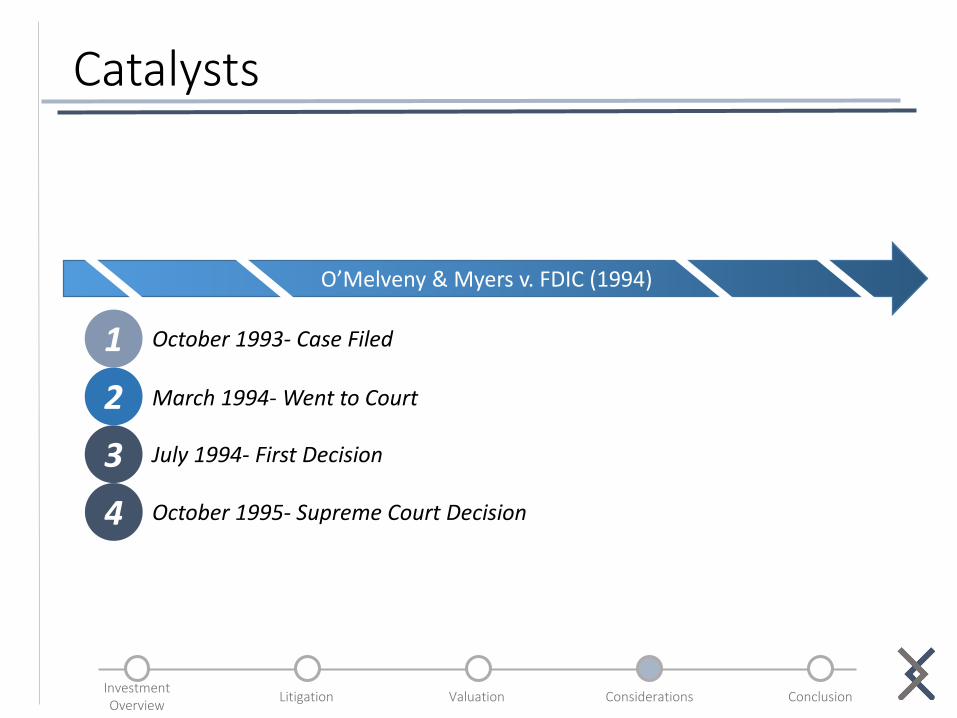

Catalysts

O’Melveny & Myers v. FDIC (1994)

1

3

2

4

October 1993- Case Filed

March 1994- Went to Court

July 1994- First Decision

October 1995- Supreme Court Decision

onclusion

ConclusionInvestmentOverview

Valuation Considerations ConclusionLitigation

Investment Thesis

Shareholders are suing the US Treasury over unlawful seizure of private assets

This seizure of shareholder assets is a violation of the Takings Clause of the 5th Amendment

Should the court rule in favor of shareholders, we believe substantial value to be unlocked

FNMA presents an astounding 10-15x in upside potential

Questions

InvestmentOverview

Valuation Considerations ConclusionLitigation

Appendix SlidesGovernment Plans for FNMA- 23Intrinsic Valuation- 24Legislation Current Progress- 25Capital Structure- 26Risks- 27Price Chart- One Year- 28Management- 29Circumstances Surrounding Entering Conservatorship- 30Capital Structure Breakdown over time- 31Shareholder Base- 32Senior Preferred Stock Agreement- 33Historical Interest Income- 34FDSO Calculation- 35DCF Flaws- 36Calculating Discount to P/E- 37Addressing the GSE- Ultimate Power- 38Theodore Olson – Strong Attorney- 39O’Melveny and Myers v. FDIC 1994- 40Existing FNMA Structure- 41Government Suggested Structure- 42Price Chart- Since 2007- 43Why is it Mispriced?- 44Recent News Decision Trees-45Housing Industry in Regards to FNMA- 46Credit Quality- 47Twitter Sentiment Analysis- 48

Litigation- 6Valuation- 12Conclusion- 19

InvestmentOverview

Valuation Considerations ConclusionLitigation

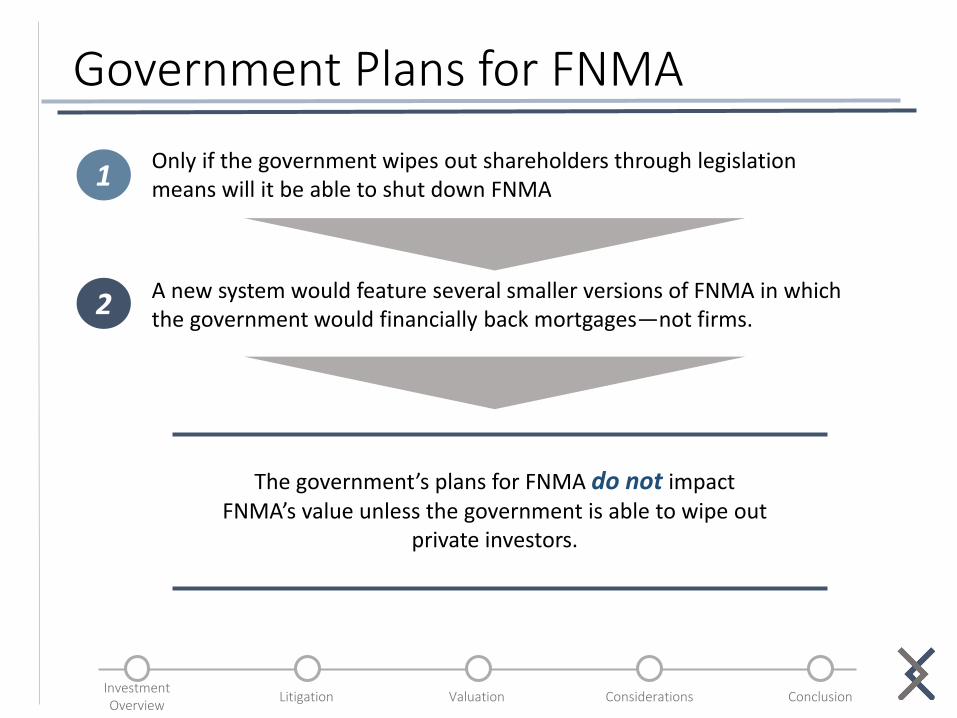

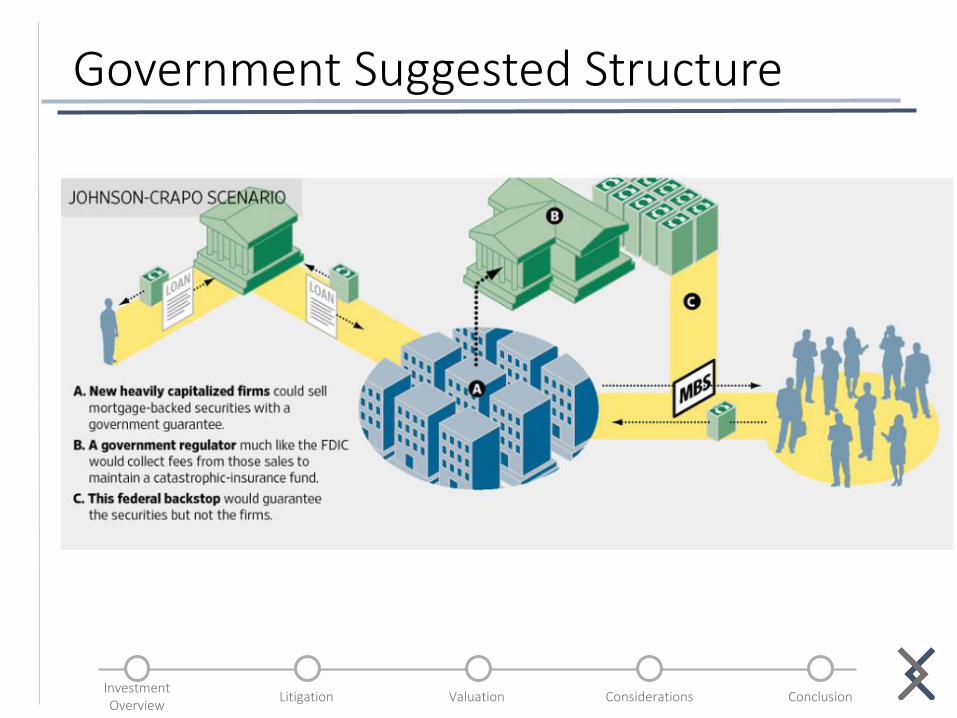

Government Plans for FNMA

1Only if the government wipes out shareholders through legislation means will it be able to shut down FNMA

2A new system would feature several smaller versions of FNMA in which the government would financially back mortgages—not firms.

The government’s plans for FNMA do not impact FNMA’s value unless the government is able to wipe out

private investors.

InvestmentOverview

Valuation Considerations ConclusionLitigation

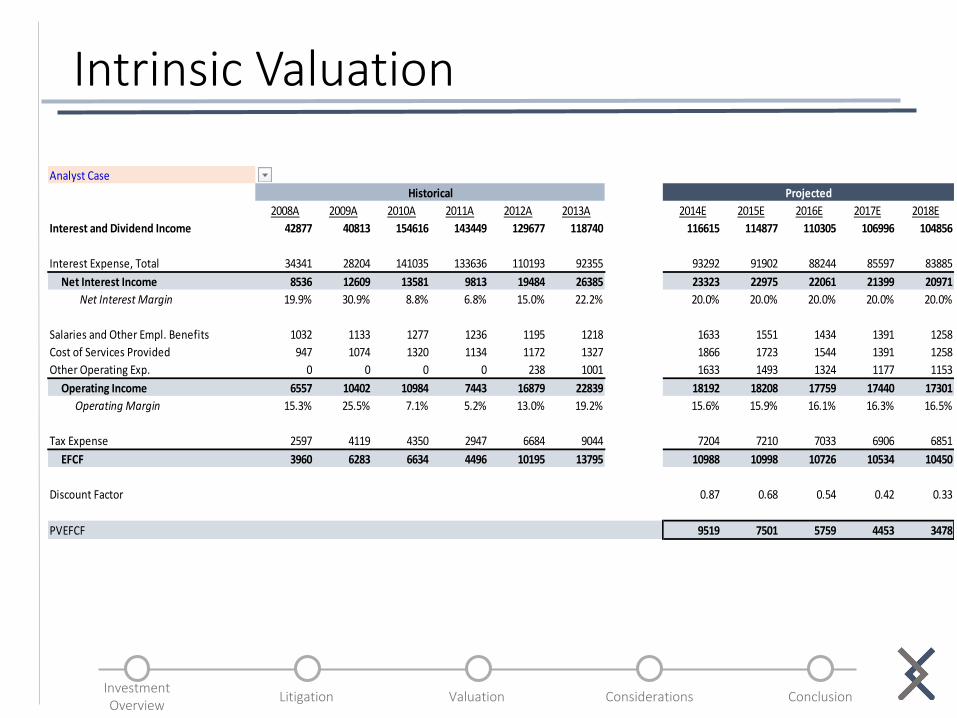

Intrinsic Valuation

Analyst Case

2008A 2009A 2010A 2011A 2012A 2013A 2014E 2015E 2016E 2017E 2018E

Interest and Dividend Income 42877 40813 154616 143449 129677 118740 116615 114877 110305 106996 104856

Interest Expense, Total 34341 28204 141035 133636 110193 92355 93292 91902 88244 85597 83885

Net Interest Income 8536 12609 13581 9813 19484 26385 23323 22975 22061 21399 20971

Net Interest Margin 19.9% 30.9% 8.8% 6.8% 15.0% 22.2% 20.0% 20.0% 20.0% 20.0% 20.0%

Salaries and Other Empl. Benefits 1032 1133 1277 1236 1195 1218 1633 1551 1434 1391 1258

Cost of Services Provided 947 1074 1320 1134 1172 1327 1866 1723 1544 1391 1258

Other Operating Exp. 0 0 0 0 238 1001 1633 1493 1324 1177 1153

Operating Income 6557 10402 10984 7443 16879 22839 18192 18208 17759 17440 17301

Operating Margin 15.3% 25.5% 7.1% 5.2% 13.0% 19.2% 15.6% 15.9% 16.1% 16.3% 16.5%

Tax Expense 2597 4119 4350 2947 6684 9044 7204 7210 7033 6906 6851

EFCF 3960 6283 6634 4496 10195 13795 10988 10998 10726 10534 10450

Discount Factor 0.87 0.68 0.54 0.42 0.33

PVEFCF 9519 7501 5759 4453 3478

Terminal Value 18,963

Exit Multiple (P/E) 6.0x

Equity Value 49,672

FDSO 5,762

Share Value $8.62

ProjectedHistorical

InvestmentOverview

Valuation Considerations ConclusionLitigation

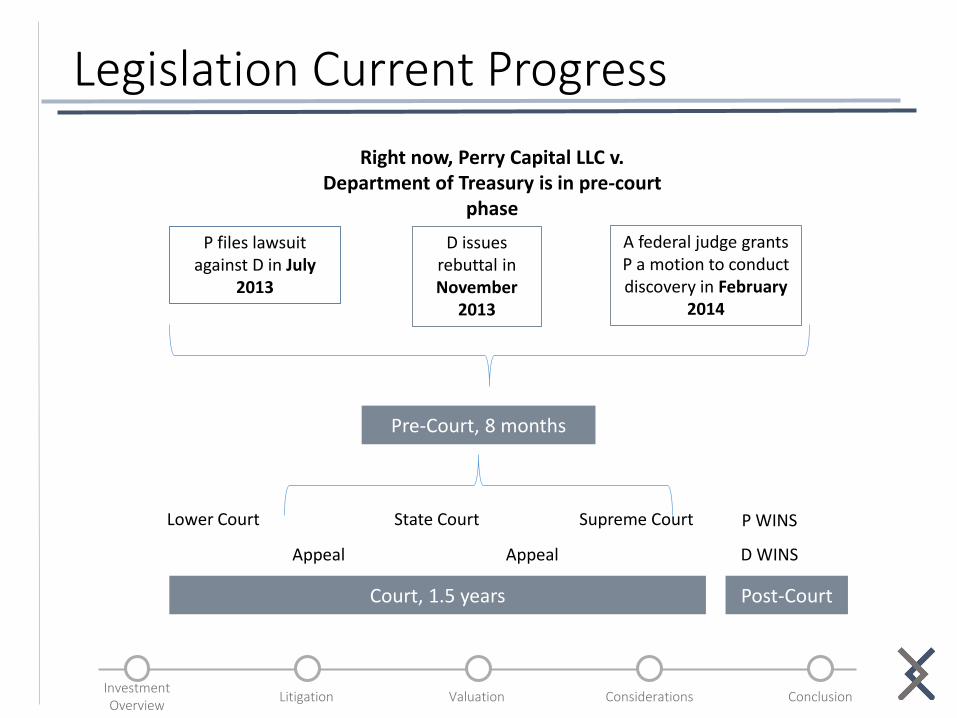

Legislation Current Progress

Post-CourtCourt, 1.5 years

D issues rebuttal in November

2013

P files lawsuit against D in July

2013

A federal judge grants P a motion to conduct discovery in February

2014

Lower Court Supreme Court P WINS

D WINSAppeal

State Court

Appeal

Right now, Perry Capital LLC v. Department of Treasury is in pre-court

phase

Pre-Court, 8 months

InvestmentOverview

Valuation Considerations ConclusionLitigation

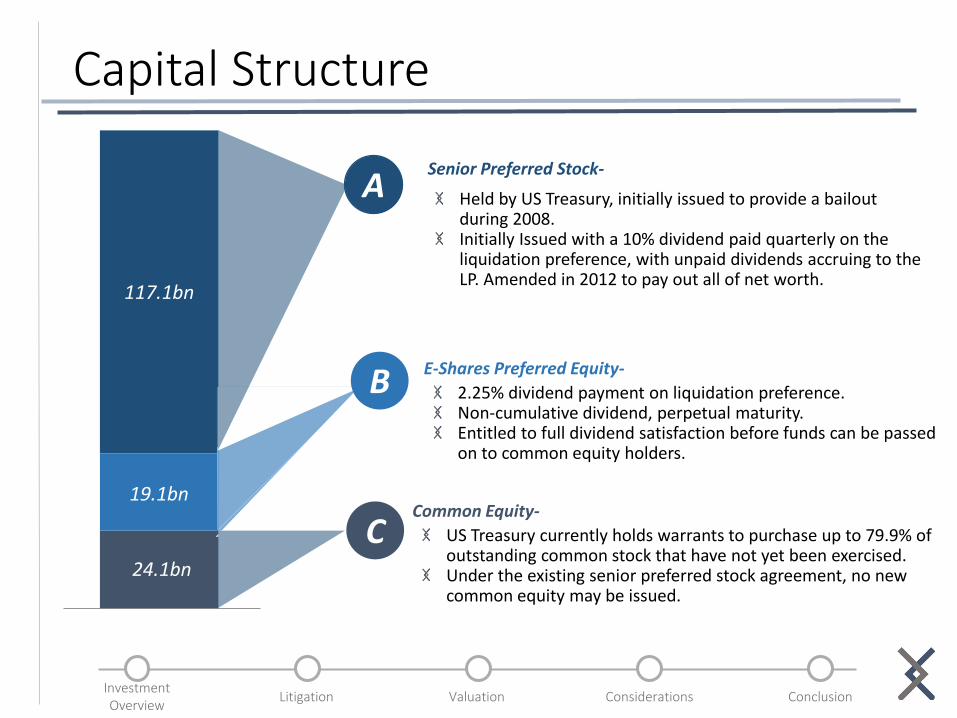

Capital Structure

Held by US Treasury, initially issued to provide a bailout during 2008.Initially Issued with a 10% dividend paid quarterly on the liquidation preference, with unpaid dividends accruing to the LP. Amended in 2012 to pay out all of net worth.

A

117.1bn

24.1bn

19.1bn

Senior Preferred Stock-

E-Shares Preferred Equity-

2.25% dividend payment on liquidation preference.Non-cumulative dividend, perpetual maturity.Entitled to full dividend satisfaction before funds can be passed on to common equity holders.

Common Equity-

US Treasury currently holds warrants to purchase up to 79.9% of outstanding common stock that have not yet been exercised. Under the existing senior preferred stock agreement, no new common equity may be issued.

C

B

InvestmentOverview

Valuation Considerations ConclusionLitigation

Risks

There is no precedent that dictates FHFA cannot abuse its conservator powers to eliminate equity holders

O’Melveney & Myers v. FDICGave a related decision that the

FDIC’s role as a conservator was to maximize firm value

FNMA’s stock price currently reflects concerns over distributable cash flows, not the fundamentals

of the core business

The core business will struggle if the overall housing market

deteriorates- eroding FNMA’s significant upside potential

InvestmentOverview

Valuation Considerations ConclusionLitigation

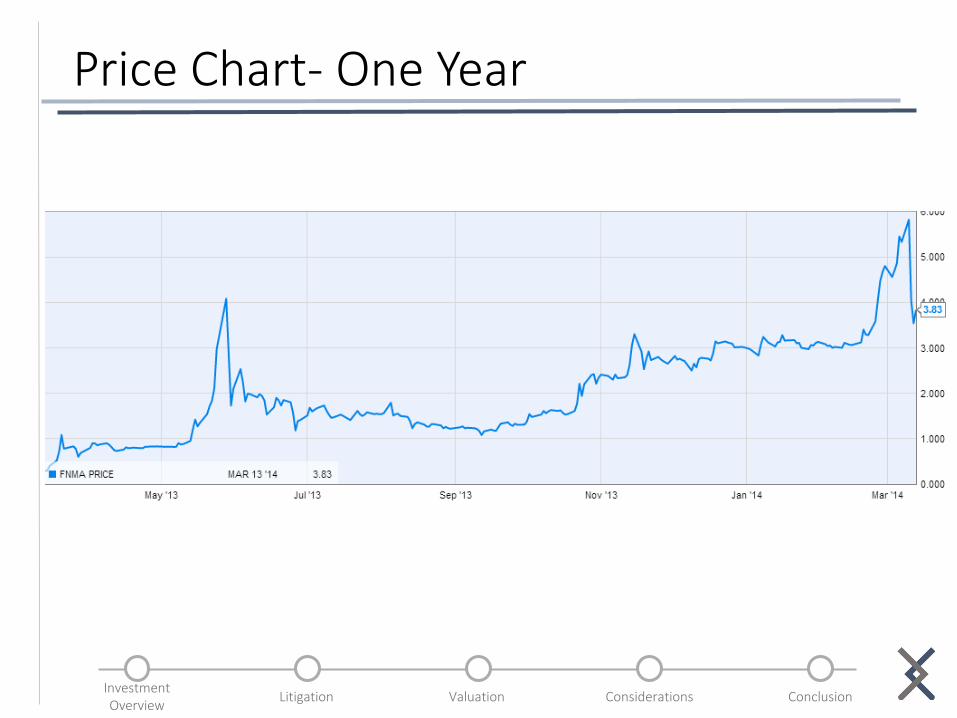

Price Chart- One Year

InvestmentOverview

Valuation Considerations ConclusionLitigation

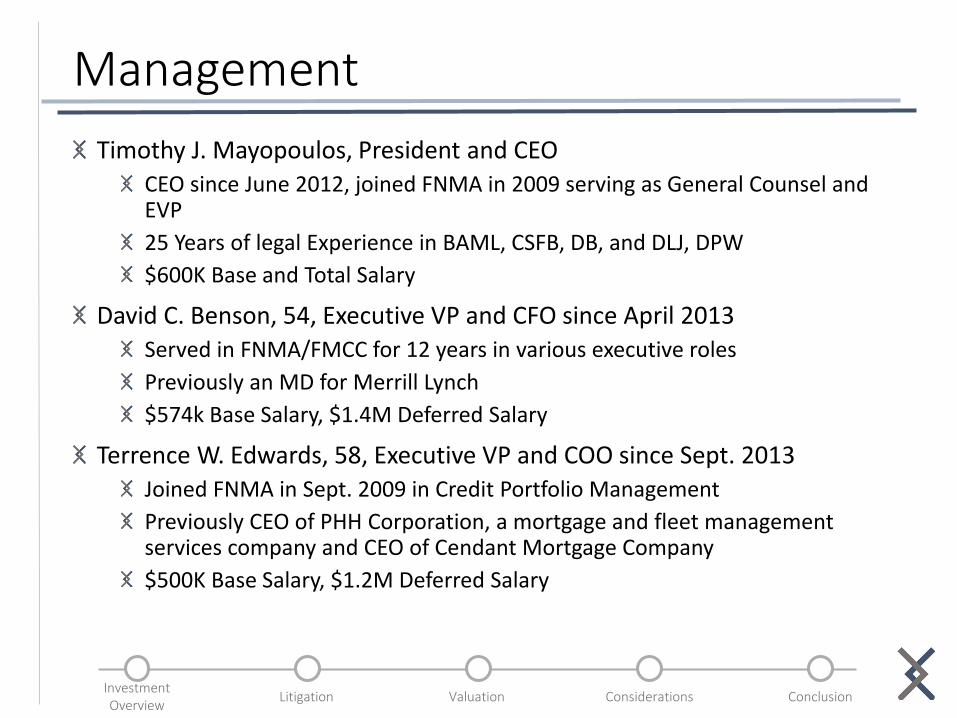

Management

Timothy J. Mayopoulos, President and CEOCEO since June 2012, joined FNMA in 2009 serving as General Counsel and EVP

25 Years of legal Experience in BAML, CSFB, DB, and DLJ, DPW

$600K Base and Total Salary

David C. Benson, 54, Executive VP and CFO since April 2013Served in FNMA/FMCC for 12 years in various executive roles

Previously an MD for Merrill Lynch

$574k Base Salary, $1.4M Deferred Salary

Terrence W. Edwards, 58, Executive VP and COO since Sept. 2013Joined FNMA in Sept. 2009 in Credit Portfolio Management

Previously CEO of PHH Corporation, a mortgage and fleet management services company and CEO of Cendant Mortgage Company

$500K Base Salary, $1.2M Deferred Salary

InvestmentOverview

Valuation Considerations ConclusionLitigation

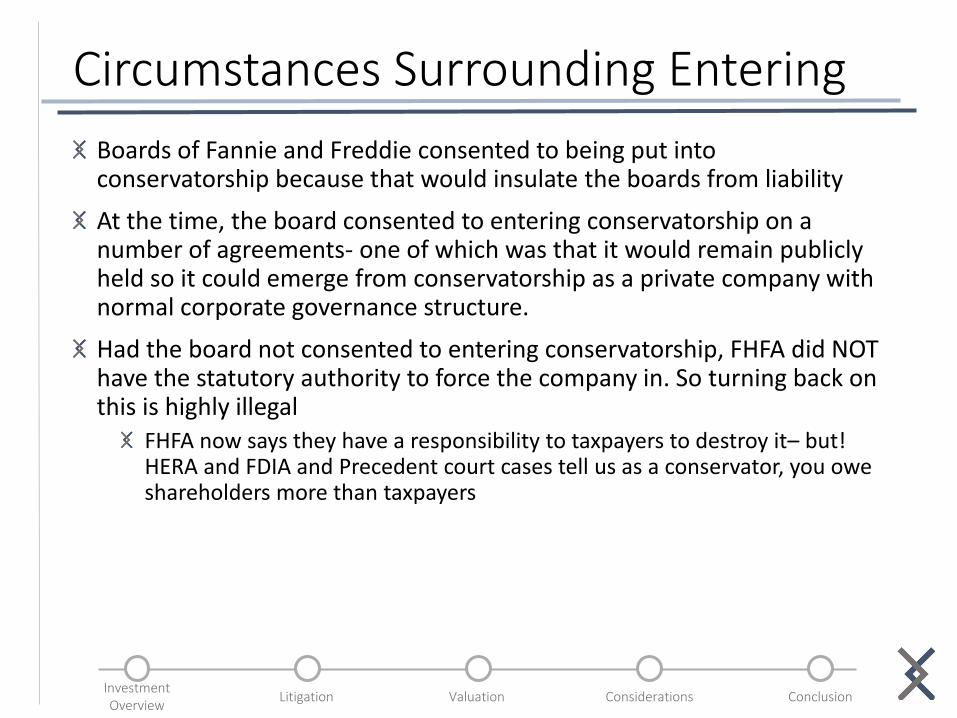

Circumstances Surrounding Entering

Boards of Fannie and Freddie consented to being put into conservatorship because that would insulate the boards from liability

At the time, the board consented to entering conservatorship on a number of agreements- one of which was that it would remain publicly held so it could emerge from conservatorship as a private company with normal corporate governance structure.

Had the board not consented to entering conservatorship, FHFA did NOT have the statutory authority to force the company in. So turning back on this is highly illegal

FHFA now says they have a responsibility to taxpayers to destroy it– but! HERA and FDIA and Precedent court cases tell us as a conservator, you owe shareholders more than taxpayers

InvestmentOverview

Valuation Considerations ConclusionLitigation

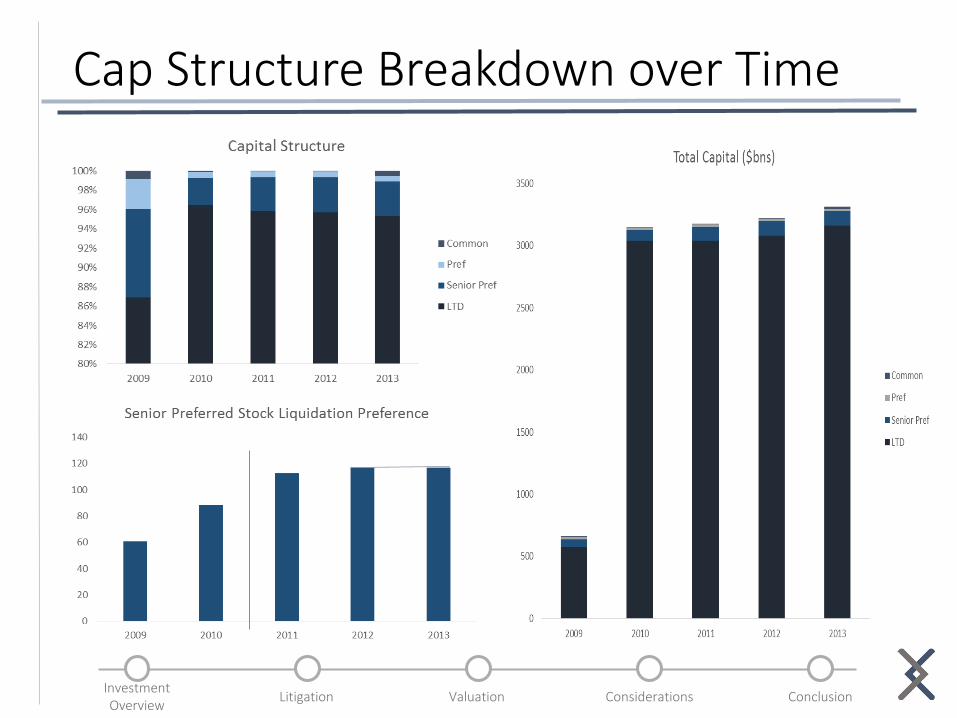

Cap Structure Breakdown over Time

InvestmentOverview

Valuation Considerations ConclusionLitigation

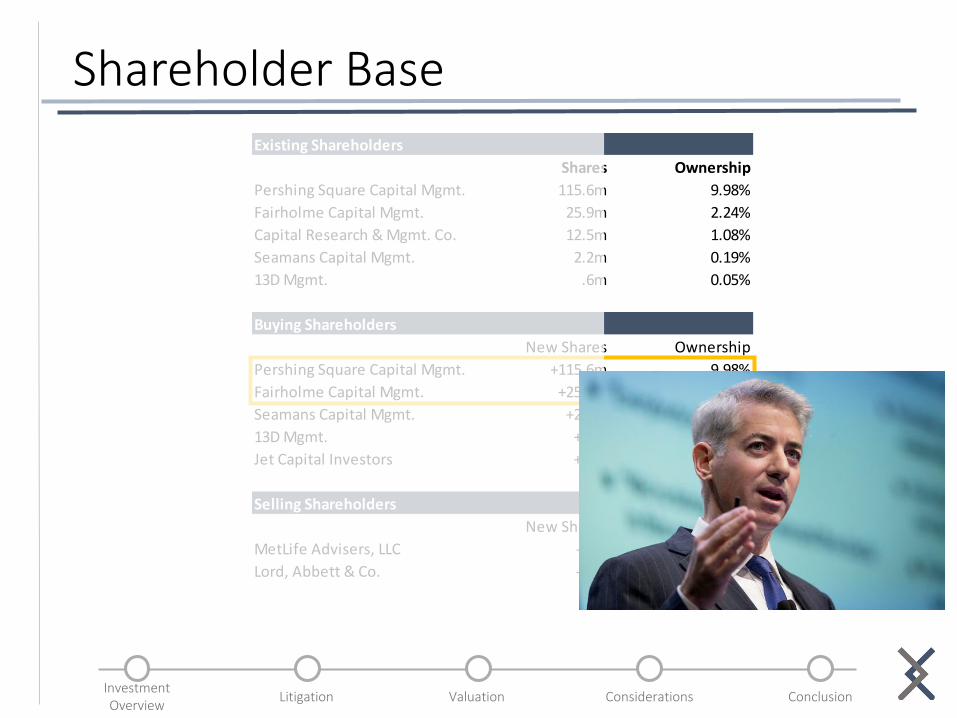

Shareholder BaseExisting Shareholders

Shares Ownership

Pershing Square Capital Mgmt. 115.6m 9.98%

Fairholme Capital Mgmt. 25.9m 2.24%

Capital Research & Mgmt. Co. 12.5m 1.08%

Seamans Capital Mgmt. 2.2m 0.19%

13D Mgmt. .6m 0.05%

Buying Shareholders

New Shares Ownership

Pershing Square Capital Mgmt. +115.6m 9.98%

Fairholme Capital Mgmt. +25.9m 2.24%

Seamans Capital Mgmt. +2.2m 0.19%

13D Mgmt. +.6m 0.05%

Jet Capital Investors +.4m 0.03%

Selling Shareholders

New Shares Ownership

MetLife Advisers, LLC -.2m 0.01%

Lord, Abbett & Co. -.1m 0.06%

InvestmentOverview

Valuation Considerations ConclusionLitigation

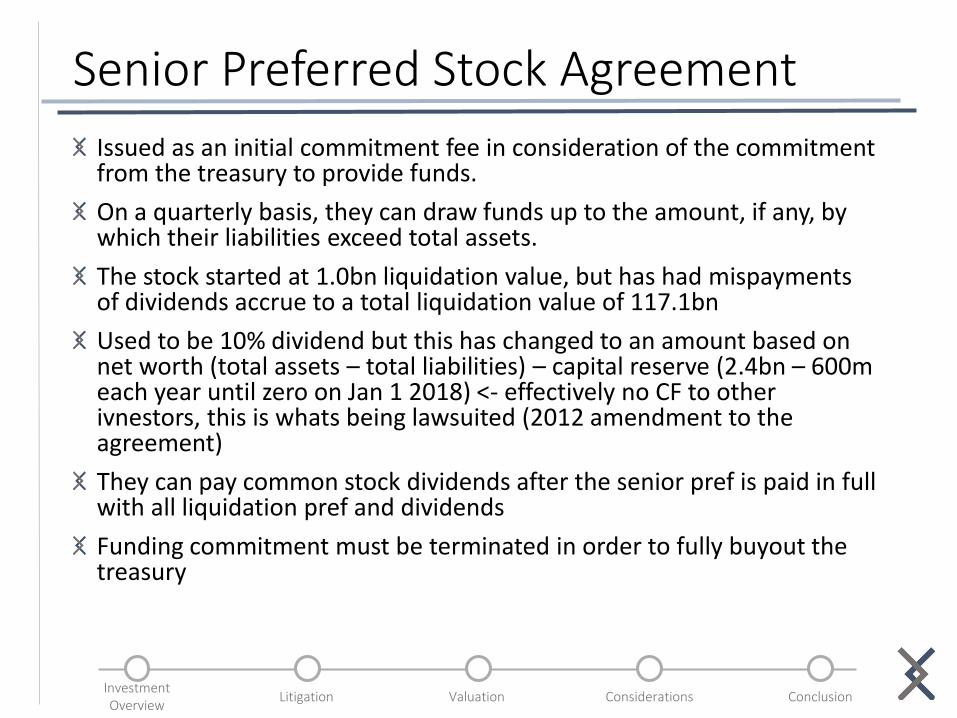

Senior Preferred Stock Agreement

Issued as an initial commitment fee in consideration of the commitment from the treasury to provide funds.

On a quarterly basis, they can draw funds up to the amount, if any, by which their liabilities exceed total assets.

The stock started at 1.0bn liquidation value, but has had mispaymentsof dividends accrue to a total liquidation value of 117.1bn

Used to be 10% dividend but this has changed to an amount based on net worth (total assets – total liabilities) – capital reserve (2.4bn – 600m each year until zero on Jan 1 2018) <- effectively no CF to other ivnestors, this is whats being lawsuited (2012 amendment to the agreement)

They can pay common stock dividends after the senior pref is paid in full with all liquidation pref and dividends

Funding commitment must be terminated in order to fully buyout the treasury

InvestmentOverview

Valuation Considerations ConclusionLitigation

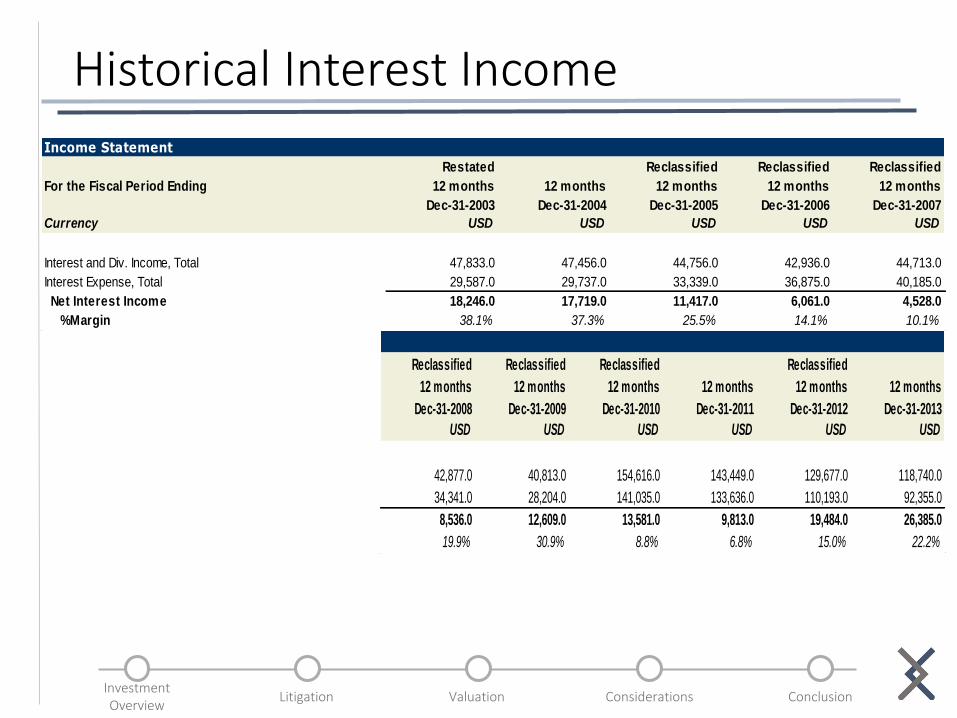

Historical Interest Income

Income Statement

For the Fiscal Period Ending

Restated

12 months

Dec-31-2003

12 months

Dec-31-2004

Reclassified

12 months

Dec-31-2005

Reclassified

12 months

Dec-31-2006

Reclassified

12 months

Dec-31-2007

Currency USD USD USD USD USD

Interest and Div. Income, Total 47,833.0 47,456.0 44,756.0 42,936.0 44,713.0

Interest Expense, Total 29,587.0 29,737.0 33,339.0 36,875.0 40,185.0

Net Interest Income 18,246.0 17,719.0 11,417.0 6,061.0 4,528.0

%Margin 38.1% 37.3% 25.5% 14.1% 10.1%

Reclassified

12 months

Dec-31-2008

Reclassified

12 months

Dec-31-2009

Reclassified

12 months

Dec-31-2010

12 months

Dec-31-2011

Reclassified

12 months

Dec-31-2012

12 months

Dec-31-2013

USD USD USD USD USD USD

42,877.0 40,813.0 154,616.0 143,449.0 129,677.0 118,740.0

34,341.0 28,204.0 141,035.0 133,636.0 110,193.0 92,355.0

8,536.0 12,609.0 13,581.0 9,813.0 19,484.0 26,385.0

19.9% 30.9% 8.8% 6.8% 15.0% 22.2%

InvestmentOverview

Valuation Considerations ConclusionLitigation

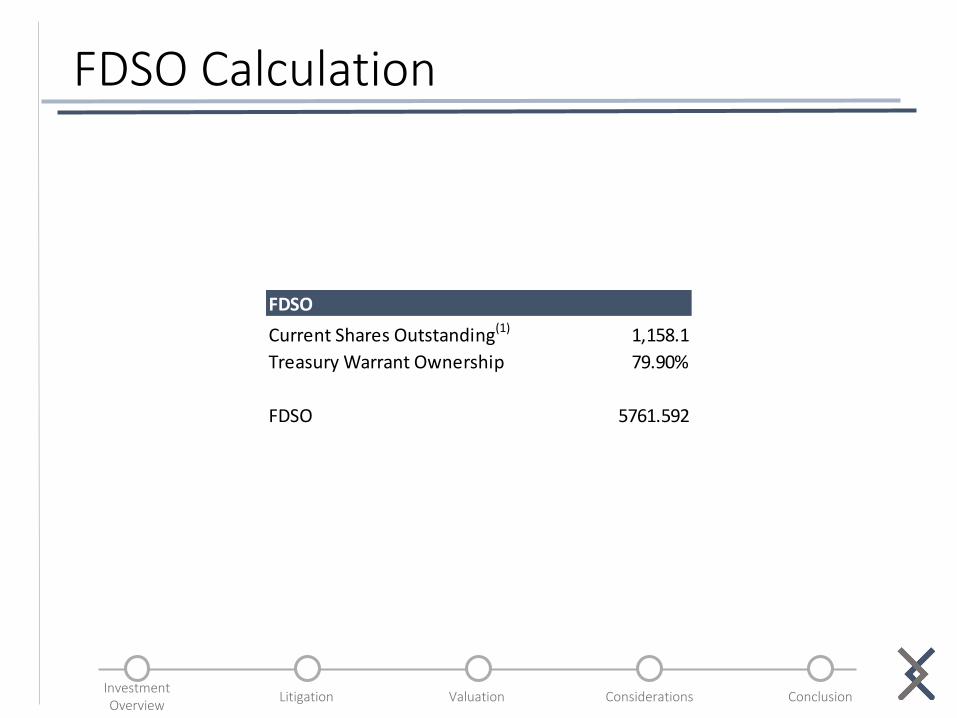

FDSO Calculation

FDSO

Current Shares Outstanding(1) 1,158.1

Treasury Warrant Ownership 79.90%

FDSO 5761.592

InvestmentOverview

Valuation Considerations ConclusionLitigation

DCF Flaws

We do not believe there is a material variant perspective when pricing the fundamentals of a $300bn secondary mortgage financing giant

Consequently, we believe analyst estimates serve as our best insight into the value of FNMA under normal capital payout structures

Additionally, applying a single WACC for FNMA is inappropriate, as the risk of FNMA is tied to its capital structure-related cash flow considerations, not the core fundamentals of the business.

InvestmentOverview

Valuation Considerations ConclusionLitigation

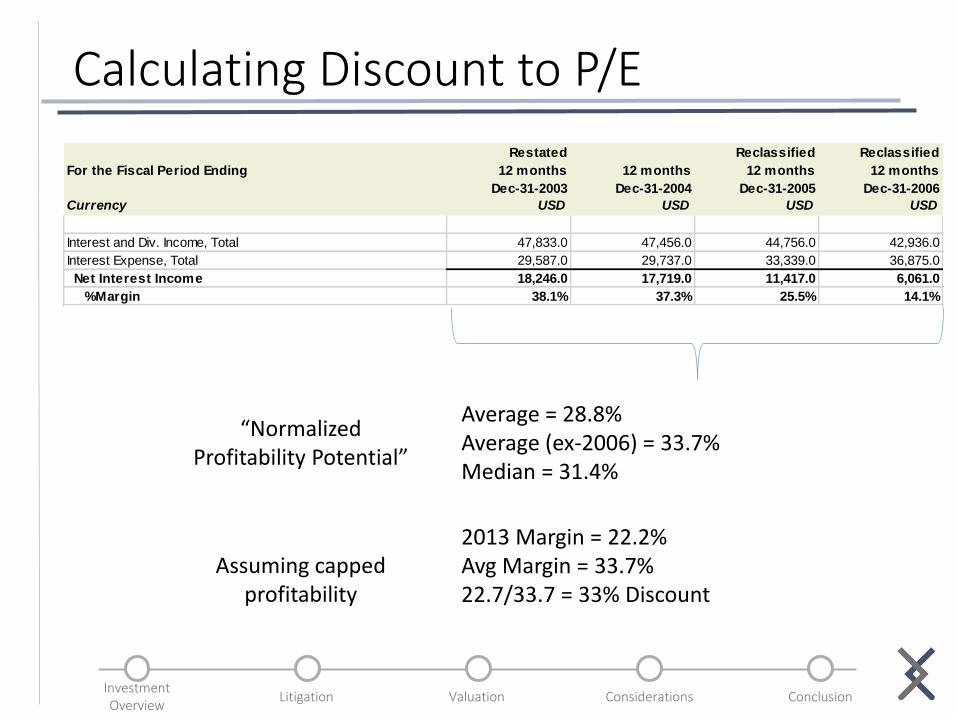

Calculating Discount to P/E

For the Fiscal Period Ending

Restated

12 months

Dec-31-2003

12 months

Dec-31-2004

Reclassified

12 months

Dec-31-2005

Reclassified

12 months

Dec-31-2006

Currency USD USD USD USD

Interest and Div. Income, Total 47,833.0 47,456.0 44,756.0 42,936.0

Interest Expense, Total 29,587.0 29,737.0 33,339.0 36,875.0

Net Interest Income 18,246.0 17,719.0 11,417.0 6,061.0

%Margin 38.1% 37.3% 25.5% 14.1%

Average = 28.8%Average (ex-2006) = 33.7%Median = 31.4%

2013 Margin = 22.2%Avg Margin = 33.7%22.7/33.7 = 33% Discount

“Normalized Profitability Potential”

Assuming capped profitability

InvestmentOverview

Valuation Considerations ConclusionLitigation

Addressing the GSE-Ultimate Power

Why we think being a GSE doesn’t necessarily give it ultimate power

InvestmentOverview

Valuation Considerations ConclusionLitigation

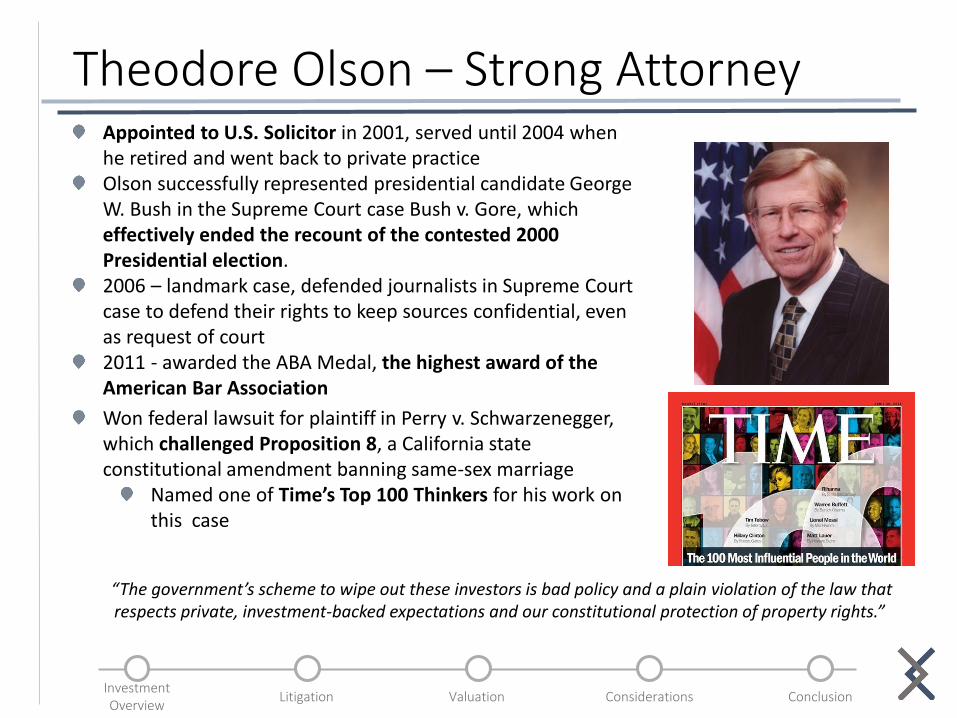

Theodore Olson – Strong Attorney Appointed to U.S. Solicitor in 2001, served until 2004 when he retired and went back to private practiceOlson successfully represented presidential candidate George W. Bush in the Supreme Court case Bush v. Gore, which effectively ended the recount of the contested 2000 Presidential election.2006 – landmark case, defended journalists in Supreme Court case to defend their rights to keep sources confidential, even as request of court2011 - awarded the ABA Medal, the highest award of the American Bar Association

Won federal lawsuit for plaintiff in Perry v. Schwarzenegger, which challenged Proposition 8, a California state constitutional amendment banning same-sex marriage

Named one of Time’s Top 100 Thinkers for his work on this case

“The government’s scheme to wipe out these investors is bad policy and a plain violation of the law that respects private, investment-backed expectations and our constitutional protection of property rights.”

InvestmentOverview

Valuation Considerations ConclusionLitigation

O’Melveny and Myers v. FDIC 1994

FDIC tried to show it had power beyond what the FDIA allowed for it in conservatorship, but the supreme court said under the statute, when you become a conservator, you step into the shoes as a stakeholder and have a duty to maximize value for the stakeholders.

InvestmentOverview

Valuation Considerations ConclusionLitigation

Existing Structure

InvestmentOverview

Valuation Considerations ConclusionLitigation

Government Suggested Structure

InvestmentOverview

Valuation Considerations ConclusionLitigation

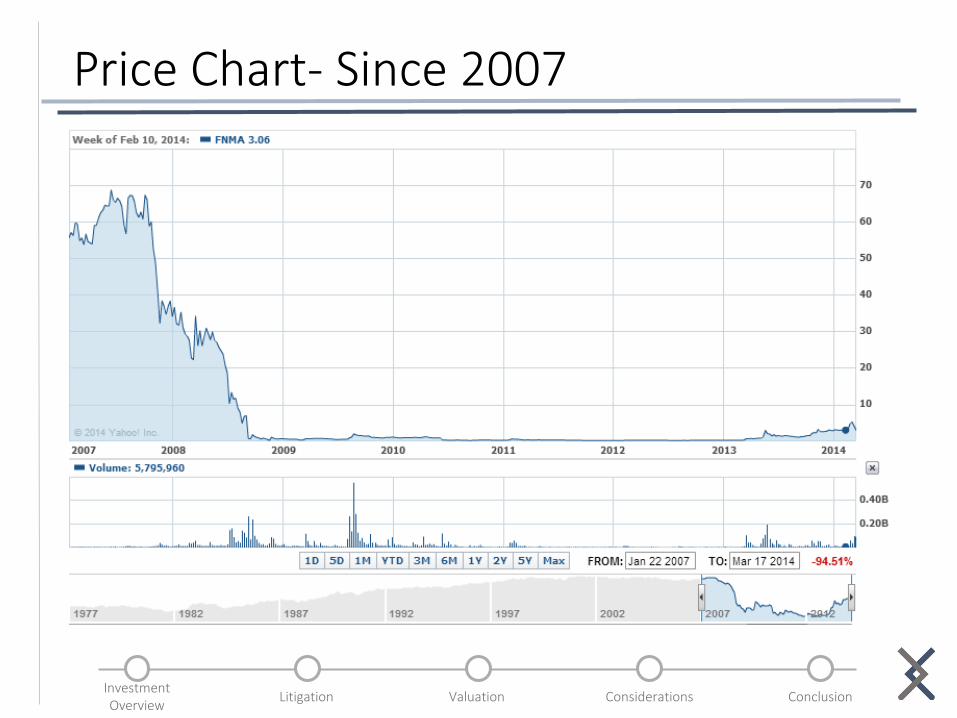

Price Chart- Since 2007

InvestmentOverview

Valuation Considerations ConclusionLitigation

Why is it mispriced?

Overly Negative Investor SentimentFew people want to be involved with a company that was at the headlines of 2008’s housing meltdown

2008 overshadows the litigation thesis

Unique Risk Appetite RequiredFew investors are willing to invest in something where a 100% loss is possible, ignoring the significant upside.

Litigation AnalysisOur precedent case is not a direct reference to the FHFA-HERA case, as it relates to FDIC-FDIA but given how FHFA-HERA are modeled after FDIC-FDIA we believe it is a perfect precedent case nonetheless.

InvestmentOverview

Valuation Considerations ConclusionLitigation

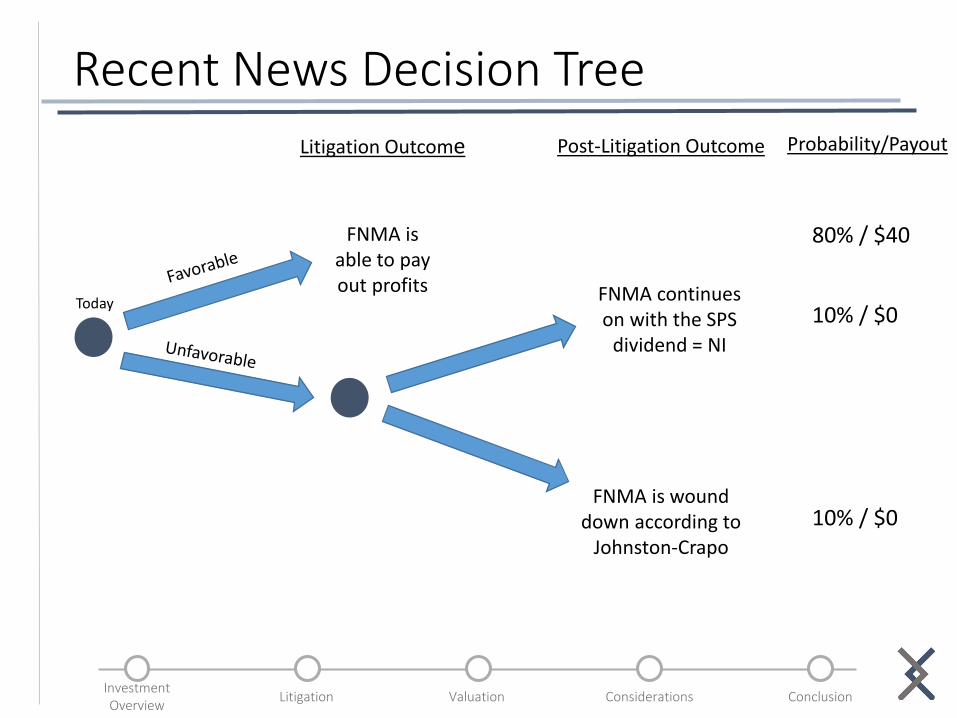

Recent News Decision Tree

Today

Litigation Outcome

FNMA is able to pay out profits

Post-Litigation Outcome

FNMA continues on with the SPS

dividend = NI

FNMA is wound down according to

Johnston-Crapo

Probability/Payout

80% / $40

10% / $0

10% / $0

InvestmentOverview

Valuation Considerations ConclusionLitigation

Housing Industry in Regards to FNMA

As rates rise, lenders will loosen rates and more mortgages will be available on the market

“Since 1999, mortgage purchase applications and all measures of sales activity have actually been higher when mortgage rates were higher.” -Forbes

In 2013, 2.5 million underwater homeowners regained positive equity status thanks to an increase in housing value which strengthens FNMA’s existing portfolio

Why? As default risk in FNMA’s portfolio decreases, FNMA’s investments are more likely to reach maturity

Forecasted market trends do not negatively affect FNMA’s business model

“Frankly, we see that our retail execution, selling individual homes to individual buyers, as still our best execution strategy. So, we will still continue to do the vast bulk of our executions in that way.” –FNMA CEO Timothy Mayopoulus (Q4 2013)

InvestmentOverview

Valuation Considerations ConclusionLitigation

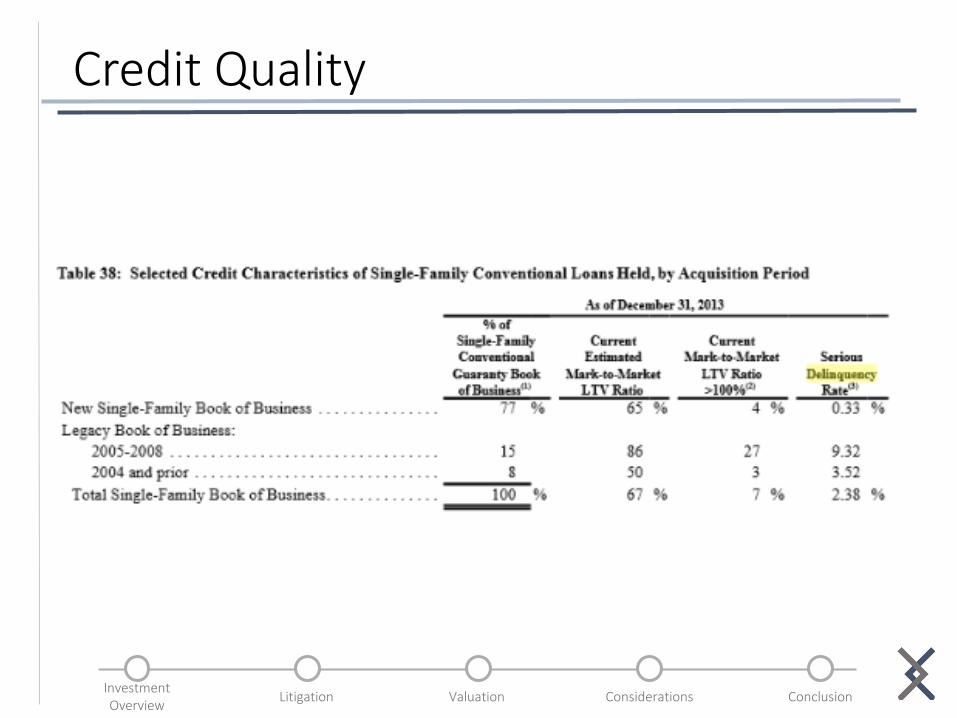

Credit Quality

InvestmentOverview

Valuation Considerations ConclusionLitigation

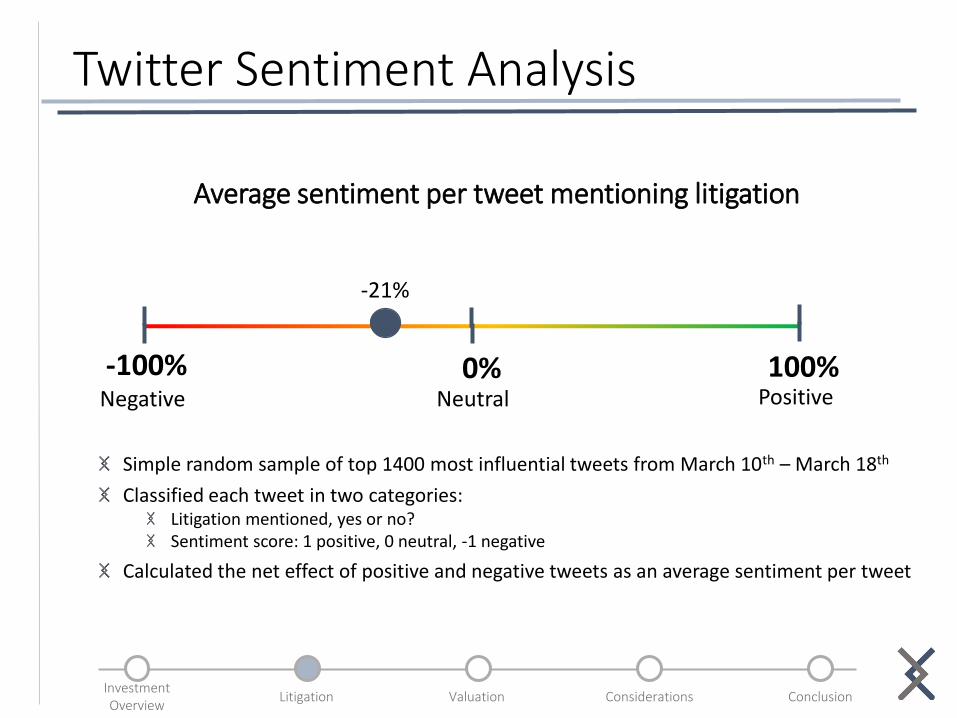

Twitter Sentiment Analysis

-100% 0% 100%Negative Neutral Positive

Average sentiment per tweet mentioning litigation

-21%

Simple random sample of top 1400 most influential tweets from March 10th – March 18th

Classified each tweet in two categories: Litigation mentioned, yes or no?Sentiment score: 1 positive, 0 neutral, -1 negative

Calculated the net effect of positive and negative tweets as an average sentiment per tweet