Fm project

38

1 A PROJECT ON “A study of Derivatives Instrument in Indian Capital Market ” IN THE SUBJECT ADVANCE FINANCIAL MANAGEMENT SUBMITTED BY SOUMEET SARKAR A030 M.Com Part-II in Advance Accountancy UNDER THE GUIDANCE OF PROF. MEGHNA CHOTALIYA TO UNIVERSITY OF MUMBAI FOR MASTER OF COMMERCE PROGRAMME (SEMESTER - IV) In ADVANCE ACCOUNTANCY YEAR: 2014-15 SVKM’S NARSEE MONJEE COLLEGE OF COMMERCE &ECONOMICS VILE PARLE (W), MUMBAI – 400056

-

Upload

soumeet-sarkar -

Category

Education

-

view

111 -

download

3

Transcript of Fm project

1

A PROJECT ON

“A study of Derivatives Instrument in Indian Capital Market ”

IN THE SUBJECT

ADVANCE FINANCIAL MANAGEMENT

SUBMITTED BY

SOUMEET SARKAR

A030

M.Com Part-II in Advance Accountancy

UNDER THE GUIDANCE OF

PROF. MEGHNA CHOTALIYA

TO

UNIVERSITY OF MUMBAI

FOR

MASTER OF COMMERCE PROGRAMME

(SEMESTER - IV)

In

ADVANCE ACCOUNTANCY

YEAR: 2014-15

SVKM’S

NARSEE MONJEE COLLEGE OF COMMERCE &ECONOMICS

VILE PARLE (W), MUMBAI – 400056

2

EVALUATION CERTIFICATE

This is to certify that the undersigned have assessed and evaluated the project on

“A study of Derivatives Instrument in Indian Capital Market ”submitted

by SOUMEET SARKAR student of M.Com. – Part – II (Semester – IV) In

ADVANCE ACCOUNTANCY for the academic year 2014-15. This project is

original to the best of our knowledge and has been accepted for Internal

Assessment.

Name & Signature of Internal Examiner

Name & Signature of External Examiner

PRINCIPAL

Shri Sunil B. Mantri

3

DECLARATION BY THE STUDENT

I, SOUMEET SARKAR student of M.Com (Part – II) In ADVANCE

ACCOUNTANCY Roll No. A030 hereby declare that the project titled “ A study

of Derivatives Instrument in Indian Capital Market ” for the subject ADVANCE

FINANCIAL MANAGEMENT submitted by me for Semester – IV of the

academic year 2014-15, is based on actual work carried out by me under the

guidance and supervision of PROF. MEGHNA CHOTALIYA. I further state that this

work is original and not submitted anywhere else for any examination.

Place: MUMBAI

Date:

Name & Signature of Student:

Name: SOUMEET SARKAR

Signature

4

ACKNOWLEDGEMENT

It is indeed a great pleasure and proud privilege to present this project work.

I thank my project guide Prof. Meghna Chotaliya & my M.Com. Co-

ordinator Prof. Hardik Pathak of SVKM’s Narsee Monjee College of

Commerce and Economics. Their co-operation and guidance have helped me

to complete this project.

I would sincerely like to thank the principal of our college Shri Sunil B.

Mantri for his support and guidance.

I would also like to thank the college library and staff for helping and guiding

me, the class representatives and my family and friends who supported me in

this project.

THANK YOU

5

CONTENT

Sr. No. PARTICULARS Page No.

1 INTRODUCTION 6

2 STUDY of DERIVATIVE in DETAIL 8

3 HISTORICAL DEVELOPMENT OF

DERIVATIVE MARKET IN INDIA

20

4 GROWTH OF INDIAN DERIVATIVES

MARKET

23

5 CONCLUSION 35

6 BIBLIOGRAPHY 38

6

INTRODUCTION

While trading in derivatives products has grown tremendously in recent times, the earliest

evidence of these types of instruments can be traced back to ancient Greece. Even though

derivatives have been in existence in some form or the other since ancient times, the advent of

modern day derivatives contracts is attributed to farmers’ need to protect themselves against a

decline in crop prices due to various economic and environmental factors.

Thus, derivatives contracts initially developed in commodities. The first “futures” contracts can

be traced to the Yodoya rice market in Osaka, Japan around 1650. The farmers were afraid of

rice prices falling in the future at the time of harvesting. To lock in a price (that is, to sell the rice

at a predetermined fixed price in the future), the farmers entered into contracts with the buyers.

These were evidently standardized contracts, much like today’s futures contracts. In 1848, the

Chicago Board of Trade (CBOT) was established to facilitate trading of forward contracts on

various commodities. From then on, futures contracts on commodities have remained more or

less in the same form, as we know them today.

While the basics of derivatives are the same for all assets such as equities, bonds, currencies, and

commodities, we will focus on derivatives in the equity markets and all examples that we discuss

will use stocks and index (basket of stocks).

The global economic order that emerged after World War II was a system where many less

developed countries administered prices and centrally allocated resources. Even the developed

economies operated under the Bretton Woods system of fixed exchange rates.

The system of fixed prices came under stress from the 1970s onwards. High inflation and

unemployment rates made interest rates more volatile. The Bretton Woods system was

dismantled in 1971, freeing exchange rates to fluctuate. Less developed countries like India

began opening up their economies and allowing prices to vary with market conditions.

Price fluctuations make it hard for businesses to estimate their future production costs and

revenues. Derivative securities provide them a valuable set of tools for managing this risk. This

article describes the evolution of Indian derivatives markets, the popular derivatives instruments,

and the main users of derivatives in India.

7

A derivative security is a security whose value depends on the value of together more basic

underlying variable. These are also known as contingent claims. Derivatives securities have been

very successful in innovation in capital markets.

The emergence of the market for derivative products most notably forwards, futures and options

can be traced back to the willingness of risk adverse economic agents to guard themselves

against uncertainties arising out of fluctuations in asset prices. By their very nature, financial

markets are markets by a very high degree of volatility. Through the use of derivative products, it

is possible to partially or fully transfer price risks by locking – in asset prices. As instruments of

risk management these generally don’t influence the fluctuations in the underlying asset prices.

However, by locking-in asset prices, derivative products minimize the impact of fluctuations in

asset prices on the profitability and cash-flow situation of risk-averse investor. Derivatives are

risk management instruments which derives their value from an underlying asset. Underlying

asset can be Bullion, Index, Share, Currency, Bonds, Interest, etc.

Among all the innovations that have flooded the international financial markets, financial

derivatives occupy the driver's seat. These specialized instruments facilitate the shuffling and

redistribution of the risks that an investor faces. Thus aids in the process of diversifying ones

portfolio. The volatility in the equity markets over the past years has resulted in greater use of

equity derivatives. The volume of the exchange traded equity futures and options in most of the

mature markets have seen a significant growth. It goes beyond that the local derivative in the

emerging markets has witnessed widespread use of the derivative instrument for a variety of

reasons. This continuous growth and development by the emerging market participants has

resulted in capital inflows as well as helped the investors in risk protection through hedging.

The emergence of the market for derivatives products, most notably forwards, futures and

options, can be tracked back to the willingness of risk-averse economic agents to guard

themselves against uncertainties arising out of fluctuations in asset prices. By their very nature,

the financial markets are marked by a very high degree of volatility. Through the use of

derivative products, it is possible to partially or fully transfer price risks by locking-in asset

prices. As instruments of risk management, these generally do not influence the fluctuations in

the underlying asset prices. However, by locking-in asset prices, derivative product minimizes

8

the impact of fluctuations in asset prices on the profitability and cash flow situation of risk-

averse investors.

Derivatives are risk management instruments, which derive their value from an underlying asset.

The underlying asset can be bullion, index, share, bonds, currency, interest, etc. Banks,

Securities firms, companies and investors to hedge risks, to gain access to cheaper money and to

make profit, use derivatives. Derivatives are likely to grow even at a faster rate in future.

DERIVATIVES

With the opening of the economy to multinational and the adoption of the liberalized economic

policies the economy is driven more towards the free market economy. The complex nature of

the financial structuring is self involves the utilization of multicurrency transaction. It exposes

the clients, particularly corporate clients to various risks such as exchange rate risk, interest risk,

economic risk & political risk.

In the present state of the economy there is an imperative need for the corporate clients to protect

their operating profits by shifting some of the uncontrollable financial risk to those who are able

bear and manage them. Thus, risk management becomes a must for survival since there is a high

volatility in the present’s financial markets.

In the context, derivatives occupy an important place as a risk reducing machinery. Derivatives

are useful to reduce many of the risks. In fact, the financial service companies can play a very

dynamic role in dealing with such risk. They can ensure that the above risks are hedged by using

derivatives like forwards, futures, options, swaps In a broad sense, many commonly used

instruments can be called derivatives since they derive their value from underlying assets. For

instance, equity share its self is a derivatives, since it derives its value from the underlying assets.

Similarly one takes an insurance against his house covering all risks.

The emergence of the market for derivative products, most notably forwards, futures and options,

can be traced back to the willingness of risk-averse economic agents to guard themselves against

uncertainties arising out of fluctuations in asset prices. By their very nature, the financial markets

are marked by a very high degree of volatility. Through the use of derivative products, it is

9

possible to partially or fully transfer price risks by locking –in asset prices. As instruments of

risk management, these generally do not influence the fluctuations underlying prices. However,

by locking – in asset prices, derivative products minimizes the impact of fluctuations in asset

prices on the profitability and cash flow situation of risk–averse investors.

DEFINITION

Understanding the word itself, Derivatives is a key to mastery of the topic. The word originates

in mathematics and refers to a variable, which has been derived from another variable. For

example, a measure of weight in pound could be derived from a measure of weight in kilograms

by multiplying by two. In financial sense, these are contracts that derive their value from some

underlying asset. Without the underlying product and market it would have no independent

existence. Underlying asset can be a Stock, Bond, Currency, Index or a Commodity. Someone

may take an interest in the derivative products without having an interest in the underlying

product market, but the two are always related and may therefore interact with each other.

Derivatives are the financial instruments, which derive their value from some other financial

instruments, called the underlying. The foundation of all derivatives market is the underlying

market, which could be spot market for gold, or it could be a pure number such as the level of the

wholesale price index of a market price. A derivative is a financial instrument whose value

depends on the Value of other basic underlying variables.

The term Derivative has been defined in Securities Contracts (Regulation) Act 1956, as:-

A security derived from a debt instrument, share, loan whether secured or unsecured, risk

instrument or contract for differences or any other form of security.

A contract, which derives its value from the prices, or index of prices, of underlying

securities.

Therefore, derivatives are specialized contracts to facilitate temporarily for hedging which is

protection against losses resulting from unforeseen price or volatility changes. Thus, derivatives

are a very important tool of risk management. Derivatives perform a number of economic

functions like price discovery, risk transfer and market completion. The simplest kind of

10

derivative market is the forward market. Here a buyer and seller write a contract for delivery at a

specific future date and a specified future price. In India, a forward market exists in the form of

the dollar- rupee market. But forward market suffers from two serious problems; Counter party

risk resulting in comparatively high rate of contract non-compliance and poor liquidity.

Futures markets were invented to cope with these two difficulties of forward markets. Futures

are standardized forward contracts traded on an organized stock exchange. In essence, a future

contract is a derivative instrument whose value is derived from the expected price of the

underlying security or asset or index at a pre-determined future date.

Derivatives are financial contracts that are designed to create market price exposure to changes

in an underlying commodity, asset or event. In general they do not involve the exchange or

transfer of principal or title. Rather their purpose is to capture, in the form of price changes, some

underlying price change or event. The term derivative refers to how the prices of these contracts

are derived from the price of some underlying security or commodity or from some index,

interest rate, exchange rate or event. Examples of derivatives include futures, forwards; options

and swaps, and these can be combined with each other or traditional securities and loans in order

to create hybrid instruments or structured securities.

IMPORTANCE of DERIVATIVES

Derivatives are becoming increasingly important in world markets as a tool for risk management.

Derivatives instruments can be used to minimize risk. Derivatives are used to separate risks and

transfer them to parties willing to bear these risks. The kind of hedging that can be obtained by

using derivatives is cheaper and more convenient than what could be obtained by using cash

instruments. It is so because, when we use derivatives for hedging, actual delivery of the

underlying asset is not at all essential for settlement purposes.

Moreover, derivatives would not create any risk. They simply manipulate the risks and transfer

to those who are willing to bear these risks. For example,

Mr. A owns a bike If he does not take insurance, he runs a big risk. Suppose he buys insurance [a

derivative instrument on the bike] he reduces his risk. Thus, having an insurance policy reduces

11

the risk of owing a bike. Similarly, hedging through derivatives reduces the risk of owing a

specified asset, which may be a share, currency, etc.

CHARACTERISTICS of DERIVATIVES

Their value is derived from an underlying instrument such as stock index, currency, etc.

They are vehicles for transferring risk.

They are leveraged instruments.

RATIONALE BEHIND the DEVELOPMENT of DERIVATIVES

Holding portfolio of securities is associated with the risk of the possibility that the investor may

realize his returns, which would be much lesser than what he expected to get. There are various

influences, which affect the returns.

1. Price or dividend (interest).

2. Sum are internal to the firm like:-

a. Industry policy,

b. Management capabilities,

c. Consumer’s preference,

d. Labour strike, etc.

These forces are to a large extent controllable and are termed as “Non-systematic Risks”. An

investor can easily manage such non- systematic risks by having a well-diversified portfolio

spread across the companies, industries and groups so that a loss in one may easily be

compensated with a gain in other.

There are other types of influences, which are external to the firm, cannot be controlled, and they

are termed as “systematic risks”. Those are

Economic

Political

12

Sociological changes are sources of Systematic Risk

Their effect is to cause the prices of nearly all individual stocks to move together in the same

manner. We therefore quite often find stock prices falling from time to time in spite of

company’s earnings rising and vice –versa.

Rational behind the development of derivatives market is to manage this systematic risk,

liquidity. Liquidity means, being able to buy & sell relatively large amounts quickly without

substantial price concessions.

In debt market, a much larger portion of the total risk of securities is systematic. Debt

instruments are also finite life securities with limited marketability due to their small size relative

to many common stocks. These factors favor for the purpose of both portfolio hedging and

speculation.

India has vibrant securities market with strong retail participation that has evolved over the

years. It was until recently a cash market with facility to carry forward positions in actively

traded “A” group scripts from one settlement to another by paying the required margins and

borrowing money and securities in a separate carry forward sessions held for this purpose.

However, a need was felt to introduce financial products like other financial markets in the

world.

MAJOR PLAYERS in DERIVATIVE MARKET

There are three major players in the derivatives trading:-

1. Hedgers:- The party, which manages the risk, is known as “Hedger”. Hedgers seek to

protect themselves against price changes in a commodity in which they have an

interest. For protecting against adverse movement. Hedging is a mechanism to reduce

price risk inherent in open positions. Derivatives are widely used for hedging. A Hedge

can help lock in existing profits. Its purpose is to reduce the volatility of a portfolio, by

reducing the risk.

13

2. Speculators:- They are traders with a view and objective of making profits. They are

willing to take risks and they bet upon whether the markets would go up or come down.

To make quick fortune by anticipating/forecasting future market movements. Hedgers

wish to eliminate or reduce the price risk to which they are already exposed. Speculators,

on the other hand are those classes of investors who willingly take price risks to profit

from price changes in the underlying. While the need to provide hedging avenues by

means of derivative instruments is laudable, it calls for the existence of speculative

traders to play the role of counter-party to the hedgers. It is for this reason that the role of

speculators gains prominence in a derivatives market.

3. Arbitrageurs:- Risk less profit making is the prime goal of arbitrageurs. They could be

making money even without putting their own money in, and such opportunities often

come up in the market but last for very short time frames. They are specialized in making

purchases and sales in different markets at the same time and profits by the difference in

prices between the two centers. To earn risk-free profits by exploiting market

imperfections. Arbitrageurs profit from price differential existing in two markets by

simultaneously operating in the two different markets.

TYPES of DERIVATIVES:-

1. Forwards:- A forward contract or simply a forward is a contract between two parties to

buy or sell an asset at a certain future date for a certain price that is pre-decided on the

date of the contract. The future date is referred to as expiry date and the pre-decided price

is referred to as Forward Price. It may be noted that Forwards are private contracts and

their terms are determined by the parties involved.

A forward is thus an agreement between two parties in which one party, the buyer, enters

into an agreement with the other party, the seller that he would buy from the seller an

underlying asset on the expiry date at the forward price. Therefore, it is a commitment by

both the parties to engage in a transaction at a later date with the price set in advance.

This is different from a spot market contract, which involves immediate payment and

immediate transfer of asset. The party that agrees to buy the asset on a future date is

referred to as a long investor and is said to have a long position. Similarly the party that

14

agrees to sell the asset in a future date is referred to as a short investor and is said to have

a short position. The price agreed upon is called the delivery price or the Forward Price.

Forward contracts are traded only in Over the Counter (OTC) market and not in stock

exchanges. OTC market is a private market where individuals/institutions can trade

through negotiations on a one to one basis.

A forward contract is an agreement to buy or sell an asset on a specified date for a

specified price. One of the parties to the contract assumes a long position and agrees to

buy the underlying asset on a certain specified future date for a certain specified price.

The other party assumes a short position and agrees to sell the asset on the same date for

the same price; other contract details like delivery date, price and quantity are negotiated

bilaterally by the parties to the contract. The forward contracts are normally traded

outside the exchange.

The salient features of forward contracts are:-

They are bilateral contracts and hence exposed to counter-party risk,

Each contract is custom designed, and hence is unique in terms of contract size,

expiration date and the asset type and quality,

The contract price is generally not available in public domain,

On the expiration date, the contract has to be settled by delivery of the asset, or

net settlement.

The forward markets face certain limitations such as:-

Lack of centralization of trading,

Illiquidity, and

Counterparty risk

A forward contract is a customized contract between two entities where settlement takes

place on a specific date in the futures at today’s pre-agreed price. Forward contracts offer

tremendous flexibility to the party’s to design the contract in terms of the price, quantity,

quality, delivery, time and place. Liquidity and default risk are very high.

For example, on 1st June, X enters into an agreement to buy 50 bales of cotton for 1st

December at Rs.1000 per bale from Y, a cotton dealer. It is a case of a forward contract

where X has to pay Rs.50000 on 1st December to Y and Y has to supply 50 bales of

cotton.

15

2. Futures:- Like a forward contract, a futures contract is an agreement between two

parties in which the buyer agrees to buy an underlying asset from the seller, at a future

date at a price that is agreed upon today. However, unlike a forward contract, a futures

contract is not a private transaction but gets traded on a recognized stock exchange. In

addition, a futures contract is standardized by the exchange. All the terms, other than the

price, are set by the stock exchange (rather than by individual parties as in the case of a

forward contract). Also, both buyer and seller of the futures contracts are protected

against the counter party risk by an entity called the Clearing Corporation. The Clearing

Corporation provides this guarantee to ensure that the buyer or the seller of a futures

contract does not suffer as a result of the counter party defaulting on its obligation. In

case one of the parties defaults, the Clearing Corporation steps in to fulfill the obligation

of this party, so that the other party does not suffer due to non-fulfillment of the contract.

To be able to guarantee the fulfillment of the obligations under the contract, the Clearing

Corporation holds an amount as a security from both the parties. This amount is called

the Margin money and can be in the form of cash or other financial assets. Also, since the

futures contracts are traded on the stock exchanges, the parties have the flexibility of

closing out the contract prior to the maturity by squaring off the transactions in the

market. The basic flow of a transaction between three parties, namely Buyer, Seller and

Clearing Corporation is depicted in the diagram below:-

16

Futures contract is a standardized transaction taking place on the futures exchange.

Futures market was designed to solve the problems that exist in forward market. A

futures contract is an agreement between two parties, to buy or sell an asset at a certain

time in the future at a certain price, but unlike forward contracts, the futures contracts are

standardized and exchange traded To facilitate liquidity in the futures contracts, the

exchange specifies certain standard quantity and quality of the underlying instrument that

can be delivered, and a standard time for such a settlement. Futures’ exchange has a

division or subsidiary called a clearing house that performs the specific responsibilities of

paying and collecting daily gains and losses as well as guaranteeing performance of one

party to other. A futures' contract can be offset prior to maturity by entering into an equal

and opposite transaction. More than 99% of futures transactions are offset this way.

Yet another feature is that in a futures contract gains and losses on each party’s position

is credited or charged on a daily basis, this process is called daily settlement or marking

to market. Any person entering into a futures contract assumes a long or short position,

by a small amount to the clearing house called the margin money

The standardized items in a futures contract are:-

Quantity of the underlying,

Quality of the underlying,

The date and month of delivery,

The units of price quotation and minimum price change,

Location of settlement.

3. Options:- Like forwards and futures, options are derivative instruments that provide the

opportunity to buy or sell an underlying asset on a future date.

An option is a derivative contract between a buyer and a seller, where one party (say First

Party) gives to the other (say Second Party) the right, but not the obligation, to buy from

(or sell to) the First Party the underlying asset on or before a specific day at an agreed-

upon price. In return for granting the option, the party granting the option collects a

payment from the other party. This payment collected is called the “premium” or price of

the option.

An option is a contract, or a provision of a contract, that gives one party (the option

holder) the right, but not the obligation, to perform a specified transaction with another

17

party (the option issuer or option writer) according to the specified terms. The owner of a

property might sell another party an option to purchase the property any time during the

next three months at a specified price. For every buyer of an option there must be a seller.

The seller is often referred to as the writer. As with futures, options are brought into

existence by being traded, if none is traded, none exists; conversely, there is no limit to

the number of option contracts that can be in existence at any time. As with futures, the

process of closing out options positions will cause contracts to cease to exist, diminishing

the total number. Thus an option is the right to buy or sell a specified amount of a

financial instrument at a pre-arranged price on or before a particular date.

The right to buy or sell is held by the “option buyer” (also called the option holder); the

party granting the right is the “option seller” or “option writer”. Unlike forwards and

futures contracts, options require a cash payment (called the premium) upfront from the

option buyer to the option seller. This payment is called option premium or option price.

Options can be traded either on the stock exchange or in over the counter (OTC) markets.

Options traded on the exchanges are backed by the Clearing Corporation thereby

minimizing the risk arising due to default by the counter parties involved. Options traded

in the OTC market however are not backed by the Clearing Corporation.

There are two types of options:-

Call Option:- A call option is an option granting the right to the buyer of the

option to buy the underlying asset on a specific day at an agreed upon price, but

not the obligation to do so. It is the seller who grants this right to the buyer of the

option. It may be noted that the person who has the right to buy the underlying

asset is known as the “buyer of the call option”.

The price at which the buyer has the right to buy the asset is agreed upon at the

time of entering the contract. This price is known as the strike price of the

contract (call option strike price in this case).

Since the buyer of the call option has the right (but no obligation) to buy the

underlying asset, he will exercise his right to buy the underlying asset if and only

if the price of the underlying asset in the market is more than the strike price on or

before the expiry date of the contract. The buyer of the call option does not have

an obligation to buy if he does not want to.

18

Put Option:- A put option is a contract granting the right to the buyer of the

option to sell the underlying asset on or before a specific day at an agreed upon

price, but not the obligation to do so. It is the seller who grants this right to the

buyer of the option.

The person who has the right to sell the underlying asset is known as the “buyer

of the put option”. The price at which the buyer has the right to sell the asset is

agreed upon at the time of entering the contract. This price is known as the strike

price of the contract (put option strike price in this case).

Since the buyer of the put option has the right (but not the obligation) to sell the

underlying asset, he will exercise his right to sell the underlying asset if and only

if the price of the underlying asset in the market is less than the strike price on or

before the expiry date of the contract. The buyer of the put option does not have

the obligation to sell if he does not want to.

4. Warrants:- Longer – dated options are called warrants and are generally traded over the

counter. Options generally have life up to one year, the majority of options traded on

options exchanges having a maximum maturity of nine months.

5. Swaps Contract:- A swap is an agreement between two or more people or parties to

exchange sets of cash flows over a period in future. Swaps are agreements between two

parties to exchange assets at predetermined intervals. Swaps are generally customized

transactions. The swaps are innovative financing which reduces borrowing costs, and to

increase control over interest rate risk and FOREX exposure. The swap includes both

spot and forward transactions in a single agreement. Swaps are at the centre of the global

financial revolution. Swaps are useful in avoiding the problems of unfavorable

fluctuation in FOREX market. The parties that agree to the swap are known as counter

parties. The two commonly used swaps are interest rate swaps and currency swaps.

Interest rate swaps which entail swapping only the interest related cash flows between the

parties in the same currency. Currency swaps entail swapping both principal and interest

between the parties, with the cash flows in one direction being in a different currency

than the cash flows in the opposite direction.

19

Classification of Derivatives

Derivative Contracts Traded in India

Derivatives

Financial

Basic FD / FI

Futures Forwards Options Warrants & Convertibles

Complex FD / FI

Swaps & Swaptions

Exotic Non Standard Options

Commodity

Derivative

Equity

Index Futures & Options

Single Stock Futures & Options

Debt

Interest Rate

Futures & Forwards

Interest Rate Swaps

Commodity

Forward Contarcts

Cross Currency Swaps

Forex

Forward Futures

20

HISTORICAL DEVELOPMENT OF DERIVATIVE MARKET IN INDIA

The origin of derivatives can be traced back to the need of farmers to protect themselves against

fluctuations in the price of their crop. From the time it was sown to the time it was ready for

harvest, farmers would face price uncertainty. Through the use of simple derivative products, it

was possible for the farmer to partially or fully transfer price risks by locking-in asset prices.

These were simple contracts developed to meet the needs of farmers and were basically a means

of reducing risk.

Derivative markets in India have been in existence in one form or the other for a long time. In the

area of commodities, the Bombay Cotton Trade Association started future trading way back in

1875. This was the first organized futures market. Then Bombay Cotton Exchange Ltd. in 1893,

Gujarat Vyapari Mandall in 1900, Calcutta Hesstan Exchange Ltd. in 1919 had started future

market. After the country attained independence, derivative market came through a full circle

from prohibition of all sorts of derivative trades to their recent reintroduction. In 1952, the

government of India banned cash settlement and options trading, derivatives trading shifted to

informal forwards markets. In recent years government policy has shifted in favour of an

increased role at market based pricing and less suspicious derivatives trading. The first step

towards introduction of financial derivatives trading in India was the promulgation at the

securities laws (Amendment) ordinance 1995. It provided for withdrawal at prohibition on

options in securities. The last decade, beginning the year 2000, saw lifting of ban of futures

trading in many commodities. Around the same period, national electronic commodity

exchanges were also set up.

REGULATION OF DERIVATIVES TRADING IN INDIA

The regulatory frame work in India is based on L.C. Gupta Committee report and J.R. Varma

Committee report. It is mostly consistent with the international organization of securities

commission (IUSCO). The L.C. Gupta Committee report provides a perspective on division of

regulatory responsibility between the exchange and SEBI. It recommends that SEBI‟s role

should be restricted to approving rules, bye laws and regulations of a derivatives exchange as

21

also to approving the proposed derivatives contracts before commencement of their trading. It

emphasizes the supervisory and advisory role of SEBI. It also suggests establishment of a

separate clearing corporation.

DERIVATIVES MARKET IN INDIA

In India, there are two major markets namely National Stock Exchange (NSE) and Bombay

Stock Exchange (BSE) along with other Exchanges of India are the market for derivatives. Here

we may discuss the performance of derivatives products in Indian market.

DERIVATIVE PRODUCTS TRADED AT BSE

The BSE started derivatives trading on June 9, 2000 when it launched “Equity derivatives (Index

futures-SENSEX) first time. It was followed by launching various products as shown below.

They are index options, stock options, single stock futures, weekly options, stocks for: Satyam,

SBI, Reliance Industries, Tata Steel, Chhota (Mini) SENSEX, Currency futures, US dollar-rupee

future and BRICSMART indices derivatives.

Date of Commencement Derivative Product

9th

June 2000 Equity derivatives (Index futures - SENSEX)

1st June 2001 Index Options – S&P CNX Nifty

9th

July 2001 Stock options launched (Stock option on 109 stocks)

9th

Nov. 2002 Stock futures launched (Stock futures on 109 Stocks)

13th

Sep. 2004 Weekly options on 4 Stocks

1st Jan. 2008 Chhota (mini) SENSEX

NA Futures options on sectoral indices (namely BSE TECK, BSE

FMCG, BSE metal, BSE Bankex & BSE oil & gas)

1st Oct. 2008 Currency derivative introduced (currency futures on US Dollar)

30th

March 2012 Launched BRICSMART indices derivatives

22

DERIVATIVE PRODUCTS TRADED AT NSE

The NSE started derivatives trading on June 12, 2000 when it launched “Index Futures S & P

CNX Nifty” first time. It was followed by launching various derivative products which are

shown in table no.3. They are index options, stock options, stock future, interest rate, future

CNX IT future and options, Bank Nifty futures and options, CNX Nifty Junior futures and

options, CNX100 futures and options, Nifty Mid Cap-50 future and options, Mini index futures

and options, Long term options. Currency futures on USD-rupee, Defty future and options,

interest rate futures, SKP CNX Nifty futures on CME, European style stock options, currency

options on USD INR, 91 days GOI T.B. futures, and derivative global indices and infrastructures

indices.

Date of Introduction Derivative Product

12th

June 2000 Index futures – S&P CNX Nifty

4th

June 2001 Index Options – S&P CNX Nifty

2nd

July 2001 Stock options – on 233 stocks

9th

Nov. 2001 Stock futures on 233 stocks

23rd

June 2003 Interest rate futures – T. Bills & 10 years Bond

29th

Aug. 2003 CNX IT futures & options

13th

June 2005 Bank Nifty futures & options

1st June 2007 CNX Nifty Junior Futures & Options

1st June 2007 CNX 100 futures & options

5th

Oct. 2007 Nifty midcap – 50 futures & options

1st Jan. 2008 Mini index futures & options – S&P CNX Nifty Index

3rd

March 2008 Long term options contracts on – S&P CNX Nifty Index

29th

Aug. 2008 Currency futures on US Dollar Rupee

10th

Dec. 2008 S&P CNX Defty Futures & options

August 2009 Launch of Interest rate futures

February 2009 Launch of currency futures on additional currency pair

July 2010 S&P CNX Nifty futures on CME

October 2010 Introduction of European style stock options

23

October 2010 Introduction of Currency options on USD INR

July 2011 start 91 day GOI Treasury Bill-futures

August 2011 Launch of derivatives on global indices

September 2011 Launch of derivatives on CNX PSE & CNX Infrastructure indices

GROWTH OF INDIAN DERIVATIVES MARKET

The NSE and BSE are two major Indian markets have shown a remarkable growth both in terms

of volumes and numbers of traded contracts. Introduction of derivatives trading in 2000, in

Indian markets was the starting of equity derivative market which has registered on explosive

growth and is expected to continue the same in the years to come. NSE alone accounts 99% of

the derivatives trading in Indian markets. Introduction of derivatives has been well received by

stock market players. Derivatives trading gained popularity after its introduction in very short

time.

If we compare the business growth of NSE and BSE in terms of number of contracts traded and

volumes in all product categories it shows the NSE traded 636132957 total contracts whose total

turnover is Rs.16807782.22 cr in the year 2012-13 in futures and options segment while in

currency segment in 483212156 total contracts have traded whose total turnover is

Rs.2655474.26 cr in same year.

In case of BSE the total numbers of contracts traded are 150068157 whose total turnover is

Rs.3884370.96 Cr in the year 2012-13 for all segments. In the above case we can say that the

performance of BSE is not encouraging both in terms of volumes and numbers of contracts

traded in all product categories.

Year Total No. of

Contracts

Total Turnover (Rs.

Cr.)

Average Daily Turnover (Rs.

Cr.)

2013-2014 911118963 26444804.86 155557.68

2012-2013 1131467418 31533003.96 126638.57

24

2011-2012 1205045464 31349731.74 125902.54

2010-2011 1034212062 29248221.09 115150.48

2009-2010 679293922 17663664.57 72392.07

2008-2009 657390497 11010482.20 45310.63

2007-2008 425013200 13090477.75 52153.30

2006-2007 216883573 7356242 29543

2005-2006 157619271 4824174 19220

2004-2005 77017185 2546982 10107

2003-2004 56886776 2130610 8388

2002-2003 16768909 439862 1752

2001-2002 4196873 101926 410

2000-2001 90580 2365 11

Business Growth of NSE in CD Segment

Year Total Number of

Contracts

Total Turnover (Rs.

Crs)

Average Daily Turnover (Rs.

Crs)

2013-2014 54,88,48,391 32,94,408.65 19,727.00

2012-2013 95,92,43,448 52,74,464.65 21,705.62

2011-2012 97,33,44,132 46,74,989.91 19,479.12

2010-2011 74,96,02,075 34,49,787.72 13,854.57

2009-2010 37,86,06,983 17,82,608.04 7,427.53

2008-2009 3,26,72,768 1,62,272.43 1,167.43

Below their is statistical data or information about Indian derivatives markets namely: product

wise turnover of FO segment at NSE, product wise turnover of CD segment at NSE, Number of

contract traded at NSE in FO segment, number of contracts traded at NSE in CD segment,

Average daily transaction at NSE in FO segment, average daily transactions at NSE in CD

25

segment, Product wise turnover of futures at BSE, product wise turnover of options at BSE,

number of contract traded at BSE in future segment, number of contract, traded at BSE in option

segment and average daily transaction at BSE in all segments.

After analyzing the data given in table below we can say that they are encouraging growth and

developing. Industry analyst feels that the derivatives market has not yet, realized its full

potential in terms of growth and trading. Analyst points out that the equity derivative market on

the NSE and BSE has been limited to only four product Index-futures, index options and

individual stock future and options, which in turn are limited to certain select stock only.

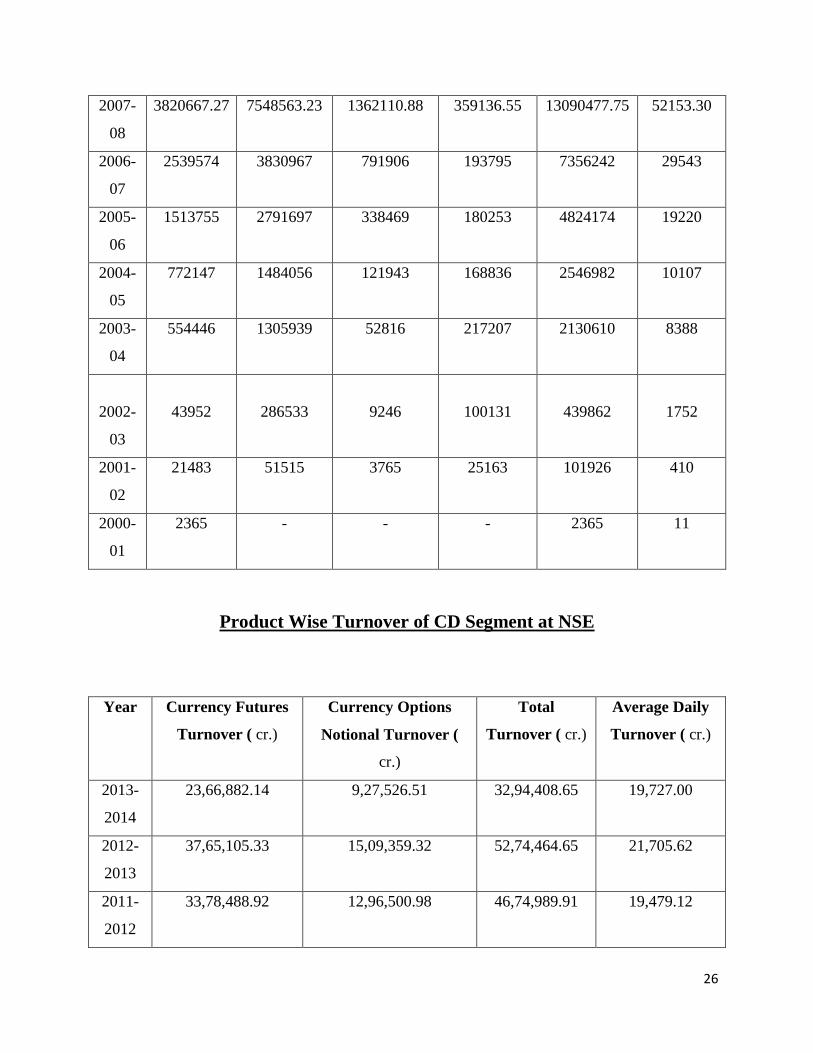

Product Wise Turnover at NSE

Year Index

Futures

Turnover (

cr.)

Stock

Returns

Turnover (

cr.)

Index

Options

Notional

Turnover (

cr.)

Stock

Options

Notional

Turnover (

cr.)

Total

Turnover (

cr.)

Average

Daily

Turnover

( cr.)

2013-

14

2176314.26 3203112.18 19462635.85 1602742.62 26444804.86 155557.68

2012-

13

2527130.76 4223872.02 22781574.14 2000427.29 31533003.96 126638.57

2011-

12

3577998.41 4074670.73 22720031.64 977031.13 31349731.74 125902.54

2010-

11

4356754.53 5495756.70 18365365.76 1030344.21 29248221.09 115150.48

2009-

10

3934388.67 5195246.64 8027964.20 506065.18 17663664.57 72392.07

2008-

09

3570111.40 3479642.12 3731501.84 229226.81 11010482.20 45310.63

26

2007-

08

3820667.27 7548563.23 1362110.88 359136.55 13090477.75 52153.30

2006-

07

2539574 3830967 791906 193795 7356242 29543

2005-

06

1513755 2791697 338469 180253 4824174 19220

2004-

05

772147 1484056 121943 168836 2546982 10107

2003-

04

554446 1305939 52816 217207 2130610 8388

2002-

03

43952

286533

9246

100131

439862

1752

2001-

02

21483 51515 3765 25163 101926 410

2000-

01

2365 - - - 2365 11

Product Wise Turnover of CD Segment at NSE

Year Currency Futures

Turnover ( cr.)

Currency Options

Notional Turnover (

cr.)

Total

Turnover ( cr.)

Average Daily

Turnover ( cr.)

2013-

2014

23,66,882.14 9,27,526.51 32,94,408.65 19,727.00

2012-

2013

37,65,105.33 15,09,359.32 52,74,464.65 21,705.62

2011-

2012

33,78,488.92 12,96,500.98 46,74,989.91 19,479.12

27

2010-

2011

32,79,002.13 1,70,785.59 34,49,787.72 13,854.57

2009-

2010

17,82,608.04 - 17,82,608.04 7,427.53

2008-

2009

1,62,272.43 - 1,62,272.43 1,167.43

Number of Contract Traded at NSE in FO Segment

Year Index Futures

No. of

contracts

Stock Futures

No. of

contracts

Index Options

No. of

contracts

Stock Options

No. of

contracts

Total No. of

contracts

2013-

14

75537352 116676854 663033020 55871737 911118963

2012-

13

96100385 147711691 820877149 66778193 1131467418

2011-

12

146188740 158344617 864017736 36494371 1205045464

2010-

11

165023653 186041459 650638557 32508393 1034212062

2009-

10

178306889 145591240 341379523 14016270 679293922

2008-

09

210428103 221577980 212088444 13295970 657390497

2007-

08

156598579 203587952 55366038 9460631 425013200

2006-

07

81487424 104955401 25157438 5283310 216883573

28

2005-

06

58537886 80905493 12935116 5240776 157619271

2004-

05

21635449 47043066 3293558 5045112 77017185

2003-

04

17191668 32368842 1732414 5583071 56886776

2002-

03

2126763 10676843 442241 3523062 16768909

2001-

02

1025588 1957856 175900 1037529 4196873

2000-

01

90580 - - - 90580

Number of Contract Traded at NSE in CD Segment

Year Currency Futures No. of

contracts

Currency Options No. of

contracts

Total No. of

contracts

2013-

2014

39,00,52,130 15,87,96,261 54,88,48,391

2012-

2013

68,41,59,263 27,50,84,185 95,92,43,448

2011-

2012

70,13,71,974 27,19,72,158 97,33,44,132

2010-

2011

71,21,81,928 3,74,20,147 74,96,02,075

2009-

2010

37,86,06,983 - 37,86,06,983

2008-

2009

3,26,72,768 - 3,26,72,768

29

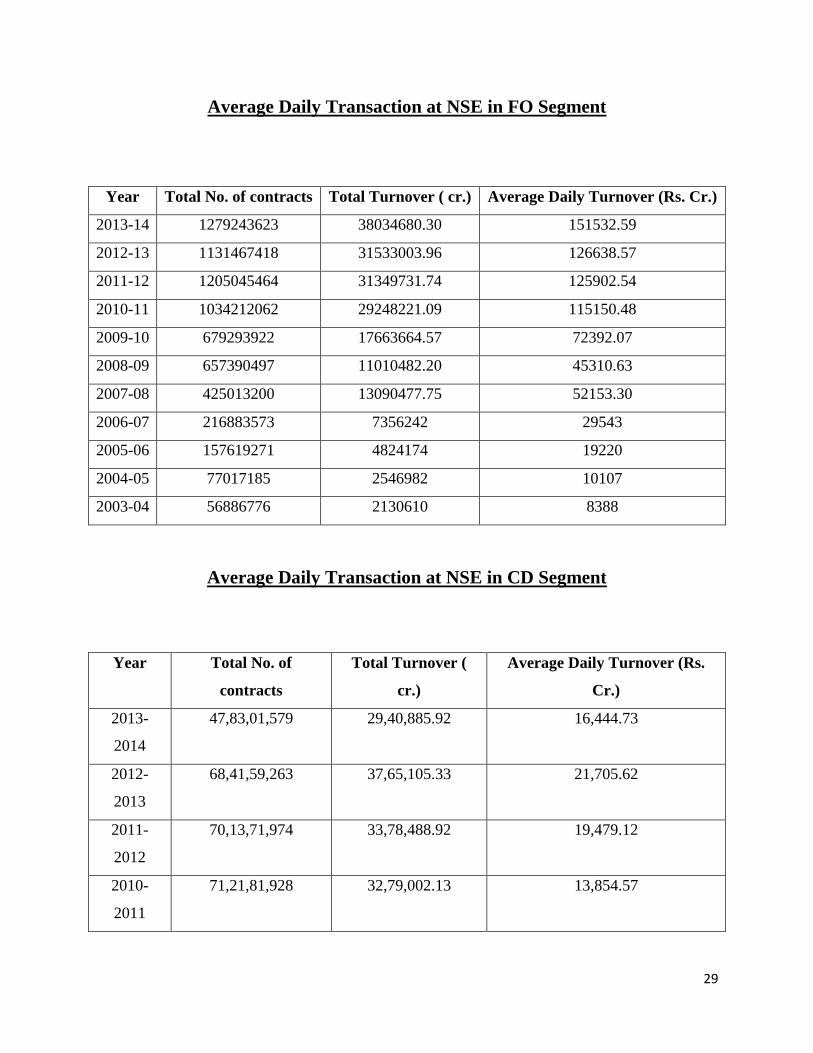

Average Daily Transaction at NSE in FO Segment

Year Total No. of contracts Total Turnover ( cr.) Average Daily Turnover (Rs. Cr.)

2013-14 1279243623 38034680.30 151532.59

2012-13 1131467418 31533003.96 126638.57

2011-12 1205045464 31349731.74 125902.54

2010-11 1034212062 29248221.09 115150.48

2009-10 679293922 17663664.57 72392.07

2008-09 657390497 11010482.20 45310.63

2007-08 425013200 13090477.75 52153.30

2006-07 216883573 7356242 29543

2005-06 157619271 4824174 19220

2004-05 77017185 2546982 10107

2003-04 56886776 2130610 8388

Average Daily Transaction at NSE in CD Segment

Year Total No. of

contracts

Total Turnover (

cr.)

Average Daily Turnover (Rs.

Cr.)

2013-

2014

47,83,01,579 29,40,885.92 16,444.73

2012-

2013

68,41,59,263 37,65,105.33 21,705.62

2011-

2012

70,13,71,974 33,78,488.92 19,479.12

2010-

2011

71,21,81,928 32,79,002.13 13,854.57

30

2009-

2010

37,86,06,983 17,82,608.04 7,427.53

2008-

2009

3,26,72,768 1,62,272.43 1,167.43

Business Growth at BSE in All Segments

Year Total

Contracts

Total Turnover (Rs

Cr)

Average Daily Turnover (Rs

Cr)

Trading

Days

2013-

14

7503405 19421854.8 308283.4 247

2012-

13

150068157 3884370.96 30828.34 241

2011-

12

32222825 808475.99 3246.89 249

2010-

11

5623 154.33 0.61 255

2009-

10

9028 234.06 1.04 224

2008-

09

496502 11774.83 48.46 243

2007-

08

7453371 242308.41 965.37 251

2006-

07

1781220 59006.62 259.94 227

2005-

06

203 8.78 0.14 61

2004-

05

531719 16112.32 77.09 209

31

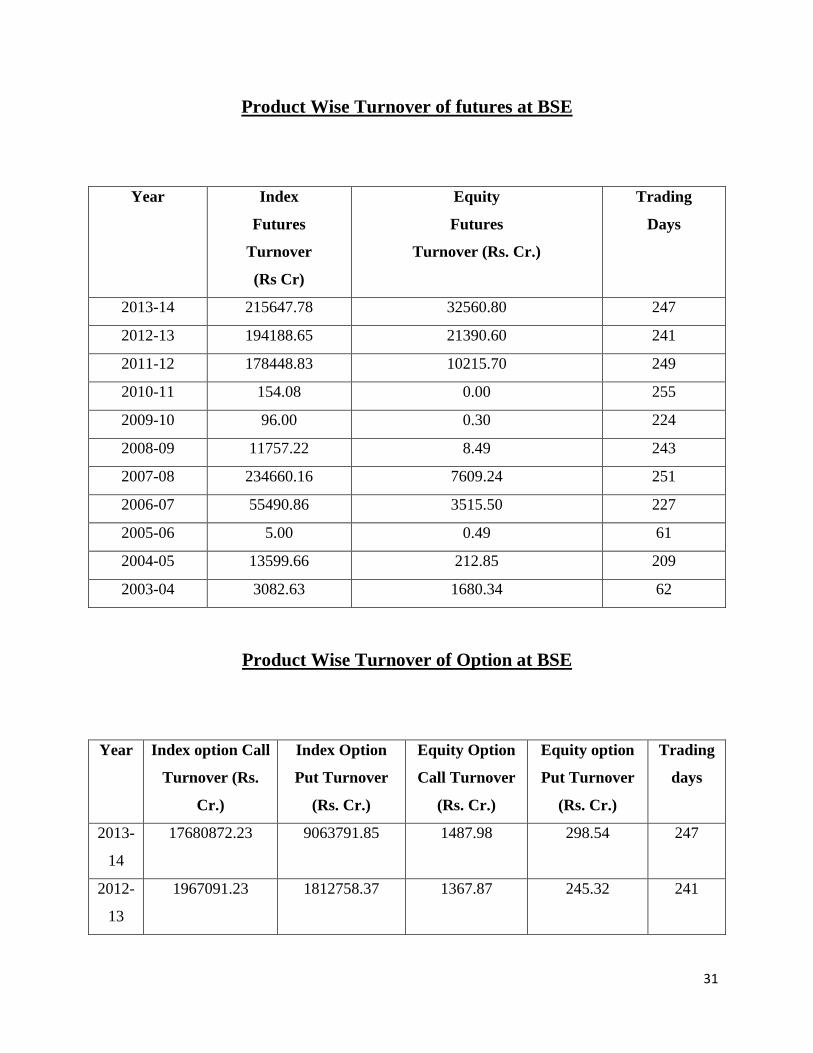

Product Wise Turnover of futures at BSE

Year Index

Futures

Turnover

(Rs Cr)

Equity

Futures

Turnover (Rs. Cr.)

Trading

Days

2013-14 215647.78 32560.80 247

2012-13 194188.65 21390.60 241

2011-12 178448.83 10215.70 249

2010-11 154.08 0.00 255

2009-10 96.00 0.30 224

2008-09 11757.22 8.49 243

2007-08 234660.16 7609.24 251

2006-07 55490.86 3515.50 227

2005-06 5.00 0.49 61

2004-05 13599.66 212.85 209

2003-04 3082.63 1680.34 62

Product Wise Turnover of Option at BSE

Year Index option Call

Turnover (Rs.

Cr.)

Index Option

Put Turnover

(Rs. Cr.)

Equity Option

Call Turnover

(Rs. Cr.)

Equity option

Put Turnover

(Rs. Cr.)

Trading

days

2013-

14

17680872.23 9063791.85 1487.98 298.54 247

2012-

13

1967091.23 1812758.37 1367.87 245.32 241

32

2011-

12

200089.57 418252.79 1277.27 191.82 249

2010-

11

0.00 0.25 0.00 0.00 255

2009-

10

137.76 0.00 0.00 0.00 224

2008-

09

6.11 3.01 0.00 0.00 243

2007-

08

31.00 7.66 0.21 0.14 251

2006-

07

0.06 0.00 0.16 0.04 227

2005-

06

3.20 0.00 0.09 0.00 61

2004-

05

1470.61 826.62 2.08 0.50 209

2003-

04

0.00 0.00 139.07 119.77 62

Number of Contracts Traded at BSE in Future Segment

Year Index Futures Contracts Equity Futures Contracts Trading Days

2013-14 42440004 1958052 247

2012-13 14146668 652684 241

2011-12 7073334 326342 249

2010-11 5613 0 255

2009-10 3744 8 224

2008-09 495830 299 243

33

2007-08 7157078 295117 251

2006-07 1638779 142433 227

2005-06 89 12 61

2004-05 44630 6725 209

2003-04 103777 33437 62

Number of Contracts Traded at BSE in Options Segment

Year Index Options

Call Contracts

Index Options

Put Contracts

Equity Options

Call Contracts

Equity Options

Put Contracts

Trading

Days

2013-

14

28387467 278474689 5425 39584 247

2012-

13

14413028 143044388 3498 15314 241

2011-

12

7206514 17569130 39848 7657 249

2010-

11

0 10 0 0 255

2009-

10

5276 0 0 0 224

2008-

09

251 122 0 0 243

2007-

08

951 210 9 6 251

2006-

07

2 0 5 1 227

2005-

06

100 0 2 0 61

2004-

48065

27210

72

17

209

34

05

2003-

04

0 0 3466 2544 62

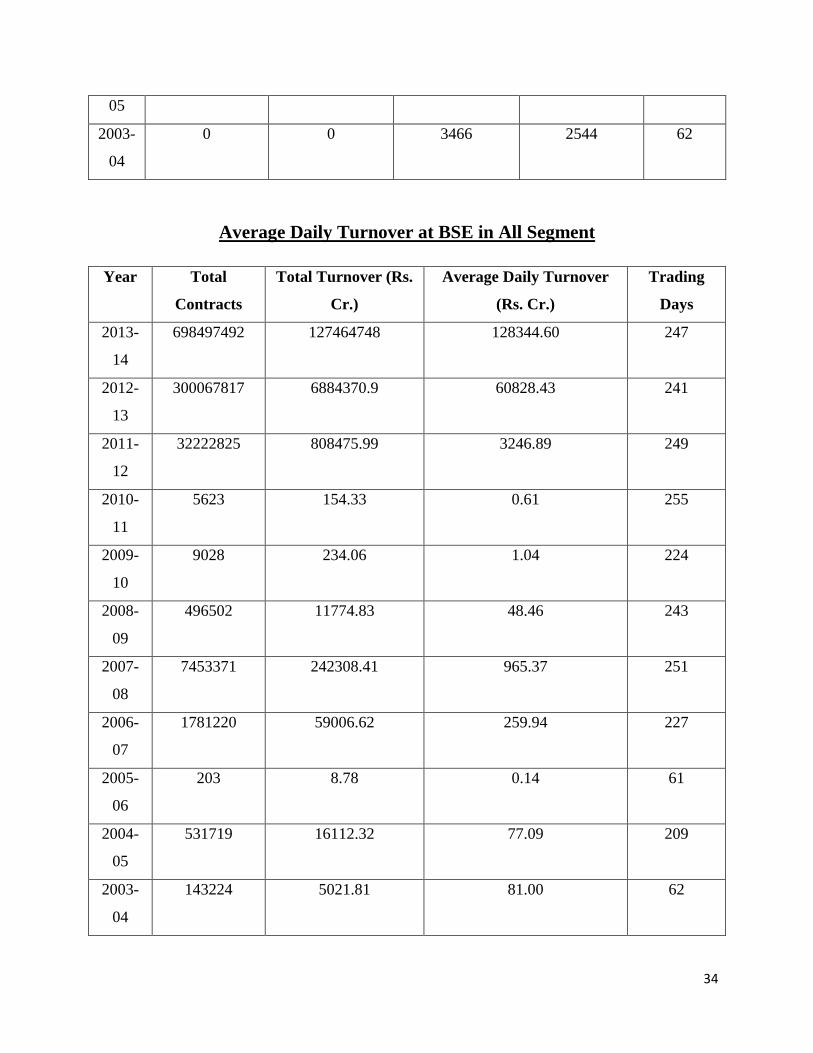

Average Daily Turnover at BSE in All Segment

Year Total

Contracts

Total Turnover (Rs.

Cr.)

Average Daily Turnover

(Rs. Cr.)

Trading

Days

2013-

14

698497492 127464748 128344.60 247

2012-

13

300067817 6884370.9 60828.43 241

2011-

12

32222825 808475.99 3246.89 249

2010-

11

5623 154.33 0.61 255

2009-

10

9028 234.06 1.04 224

2008-

09

496502 11774.83 48.46 243

2007-

08

7453371 242308.41 965.37 251

2006-

07

1781220 59006.62 259.94 227

2005-

06

203 8.78 0.14 61

2004-

05

531719 16112.32 77.09 209

2003-

04

143224 5021.81 81.00 62

35

CONCLUSION

Derivatives have existed and evolved over a long time, with roots in commodities market. In the

recent years advances in financial markets and the technology have made derivatives easy for the

investors. Derivatives market in India is growing rapidly unlike equity markets. Trading in

derivatives require more than average understanding of finance. Being new to markets maximum

number of investors have not yet understood the full implications of the trading in derivatives.

SEBI should take actions to create awareness in investors about the derivative market.

Introduction of derivatives implies better risk management. These markets can give greater

depth, stability and liquidity to Indian capital markets. Successful risk management with

derivatives requires a thorough understanding of principles that govern the pricing of financial

derivatives. In order to increase the derivatives market in India SEBI should revise some of their

regulation like contract size, participation of FII in the derivative market. Contract size should be

minimized because small investor cannot afford this much of huge premiums.

In cash market the profit/loss is limited but where in F & O an investor can enjoy unlimited

profits/loss. At present scenario the Derivatives market is increased to a great position. Its daily

turnover teaches to the equal stage of cash market. The derivatives are mainly used for hedging

purpose. In cash market the investor has to pay the total money, but in derivatives the investor

has to pay premiums or margins, which are some percentage of total money. In derivative

segment the profit/loss of the option holder/option writer is purely depended on the fluctuations

of the underlying asset.

In terms of the growth of derivatives markets, and the variety of derivatives users, the Indian

market has equalled or exceeded many other regional markets. While the growth is being

spearheaded mainly by retail investors, private sector institutions and large corporations, smaller

companies and state-owned institutions are gradually getting into the act. Foreign brokers such as

JP Morgan Chase are boosting their presence in India in reaction to the growth in derivatives.

The variety of derivatives instruments available for trading is also expanding.

There remain major areas of concern for Indian derivatives users. Large gaps exist in the range

of derivatives products that are traded actively. In equity derivatives, NSE figures show that

almost 90% of activity is due to stock futures or index futures, whereas trading in options is

36

limited to a few stocks, partly because they are settled in cash and not the underlying stocks.

Exchange-traded derivatives based on interest rates and currencies are virtually absent.

Liquidity and transparency are important properties of any developed market. Liquid markets

require market makers who are willing to buy and sell, and be patient while doing so. In India,

market making is primarily the province of Indian private and foreign banks, with public sector

banks lagging in this area. A lack of market liquidity may be responsible for inadequate trading

in some markets. Transparency is achieved partly through financial disclosure. Financial

statements currently provide misleading information on institutions’ use of derivatives. Further,

there is no consistent method of accounting for gains and losses from derivatives trading. Thus, a

proper framework to account for derivatives needs to be developed.

Further regulatory reform will help the markets grow faster. For example, Indian commodity

derivatives have great growth potential but government policies have resulted in the underlying

spot/physical market being fragmented (e.g. due to lack of free movement of commodities and

differential taxation within India). Similarly, credit derivatives, the fastest growing segment of

the market globally, are absent in India and require regulatory action if they are to develop.

As Indian derivatives markets grow more sophisticated, greater investor awareness will become

essential. NSE has programmes to inform and educate brokers, dealers, traders, and market

personnel. In addition, institutions will need to devote more resources to develop the business

processes and technology necessary for derivatives trading.

The investors can minimize risk by investing in derivatives. The use of derivative equips the

investor to face the risk, which is uncertain. Though the use of derivatives does not completely

eliminate the risk, but it certainly lessens the risk. It is advisable to the investor to invest in the

derivatives market because of the greater amount of liquidity offered by the financial derivatives

and the lower transactions costs associated with the trading of financial derivatives.

The derivatives products give the investor an option or choice whether to exercise the contract or

not. Options give the choice to the investor to either exercise his right or not. If on expiry date

the investor finds that the underlying asset in the option contract is traded at a less price in the

stock market then, he has the full liberty to get out of the option contract and go ahead and buy

the asset from the stock market. So in case of high uncertainty the investor can go for options.

37

However, these instruments act as a powerful instrument for knowledgeable traders to expose

them to the properly calculated and well understood risks in pursuit of reward, i.e., profit.

Financial derivatives have earned a well-deserved extremely significant place among all the

financial instruments (products), due to innovation and revolutionized the landscape. Derivatives

are tool for managing risk. Derivatives provide an opportunity to transfer risk from one to

another. Launch of equity derivatives in Indian market has been extremely encouraging and

successful. The growth of derivatives in the recent years has surpassed the growth of its

counterpart globally.

The Notional value of option on the NSE increased from 1195.691178 lakhs USD in 2003 to

354648.1941 lakhs USD in 2012 and notional value of NSE futures increased from 14329.35627

lakhs USD in 2003 to 39228.38563 lakhs USD in 2012. India is one of the most successful

developing country in terms of a vibrate market for exchange-traded derivatives. The equity

derivatives market is playing a major role in shaping price discovery. Volatility in financial asset

price, integration of financial market internationally, sophisticated risk management tools,

innovations in financial engineering and choices at risk management strategies have been driving

the growth of financial derivatives worldwide, also in India. Finally we can say there is big

significance and contribution of derivatives to financial system.

38

BIBLIOGRAPHY

1. www.bseindia.com

2. www.nseindia.com

3. www.world-exchanges.org

4. www.sebi.gov.in

5. Publications of National Stock Exchange