“Flowpolis: The Form of Nodal Space” Las Palmas de Gran Canaria, November 2-4 2006 Intermodal...

27

“ “ Flowpolis: The Form of Nodal Space” Flowpolis: The Form of Nodal Space” Las Palmas de Gran Canaria, November 2-4 2006 Las Palmas de Gran Canaria, November 2-4 2006 Intermodal Intermodal Transportation and Transportation and Integrated Transport Integrated Transport Systems: Spaces, Systems: Spaces, Networks and Flows Networks and Flows Jean-Paul Rodrigue Associate Professor, Dept. of Economics & Geography, Hofstra University, New York, USA “There’s no business like flow business” Email: [email protected] Paper available at: http://people.hofstra.edu/faculty/Jean- paul_Rodrigue

-

date post

21-Dec-2015 -

Category

Documents

-

view

212 -

download

0

Transcript of “Flowpolis: The Form of Nodal Space” Las Palmas de Gran Canaria, November 2-4 2006 Intermodal...

““Flowpolis: The Form of Nodal Space”Flowpolis: The Form of Nodal Space”Las Palmas de Gran Canaria, November 2-4 2006Las Palmas de Gran Canaria, November 2-4 2006

Intermodal Intermodal Transportation and Transportation and Integrated Transport Integrated Transport Systems: Spaces, Systems: Spaces, Networks and FlowsNetworks and FlowsJean-Paul RodrigueAssociate Professor, Dept. of Economics & Geography, Hofstra University, New York, USA

“There’s no business like flow business”

Email: [email protected] available at:http://people.hofstra.edu/faculty/Jean-paul_Rodrigue

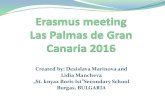

Spaces, Networks and Flows in a Global Economy

■ Globalization; a clustered and spatially diffused process• In terms of production and

consumption.• Distribution is reconciling

spatially diverse demands for raw materials, parts and finished goods.

■ The backbone of globalization• Networks are established to

support distribution.• Nodes are regulating the flows

within networks.• As international trade increases,

nodes have become strategic locations.

The Emergence of a Nodal Space: First Phase

■ The Transshipment Node• Conventional international trade

environment.• Some mobility of raw materials,

parts and finished goods.• Many impediments (tariffs and

regulations).• Trade as an attempt to cope with

scarcity.• Nodes as constrained

locations for transshipment.• Load break functions.• Industrial clusters next to rail

yards.• Port industrial complexes.

Load

Bre

ak Warehousing lag

Industrialcluster

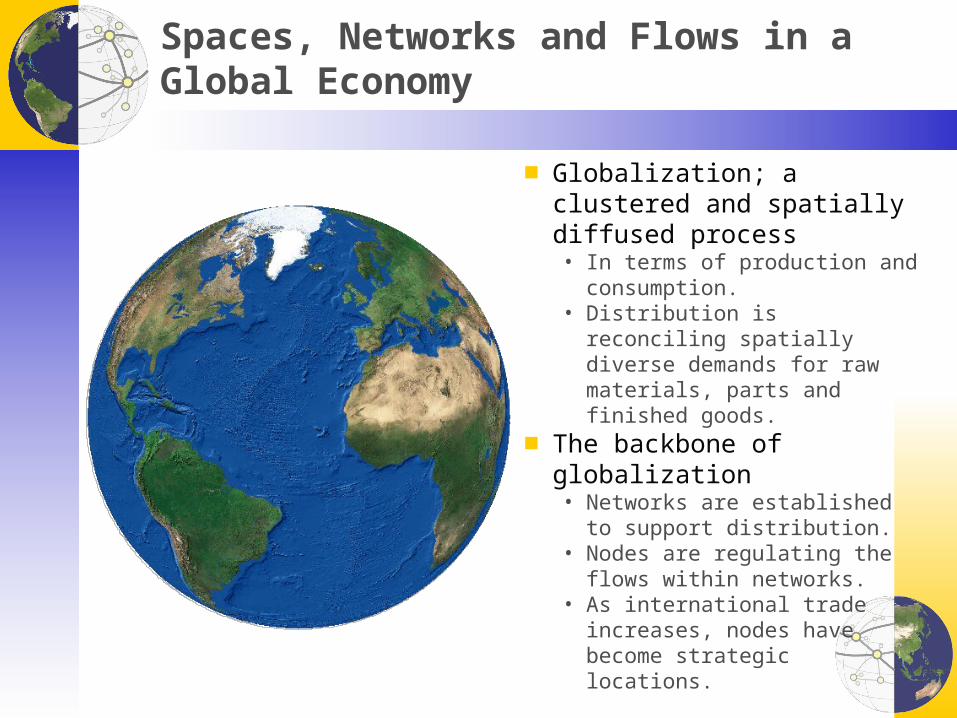

Harbor Types of the World's Large and Medium Sized Ports

Coastal Natural Coastal Breakwater

Coastal Tide Gates River Natural

River Basins River Tide Gates

Canal or Lake Open Roadstead

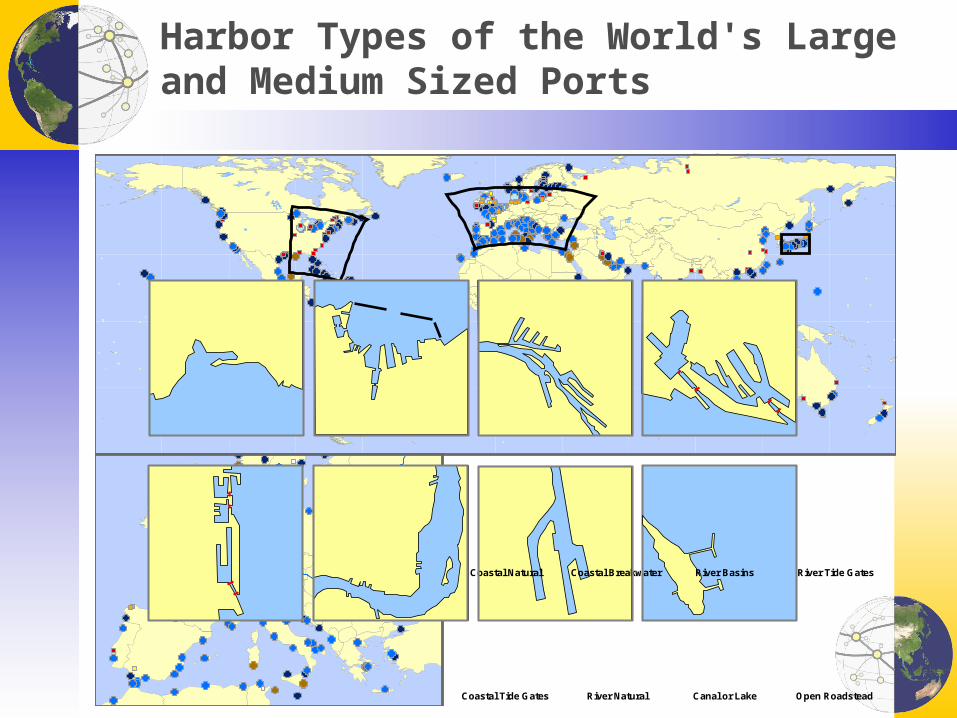

The Emergence of a Nodal Space: Second Phase

■ The Intermodal Node• Higher mobility of the factors of

production (particularly capital).• Better realization of comparative

advantages (mainly labor).• Strengthening of the

transactional and legal setting.• Emergence of intermodal

transportation, mainly containerization.

• Nodes as locations promoting the efficiency of different transport networks.

• New terminals and new locations.

• Increased velocity of the flows.

Composition

Transfer

Interchange

Decomposition

Tra

nsp

ort C

hain

‘First mile’

‘Last mile’

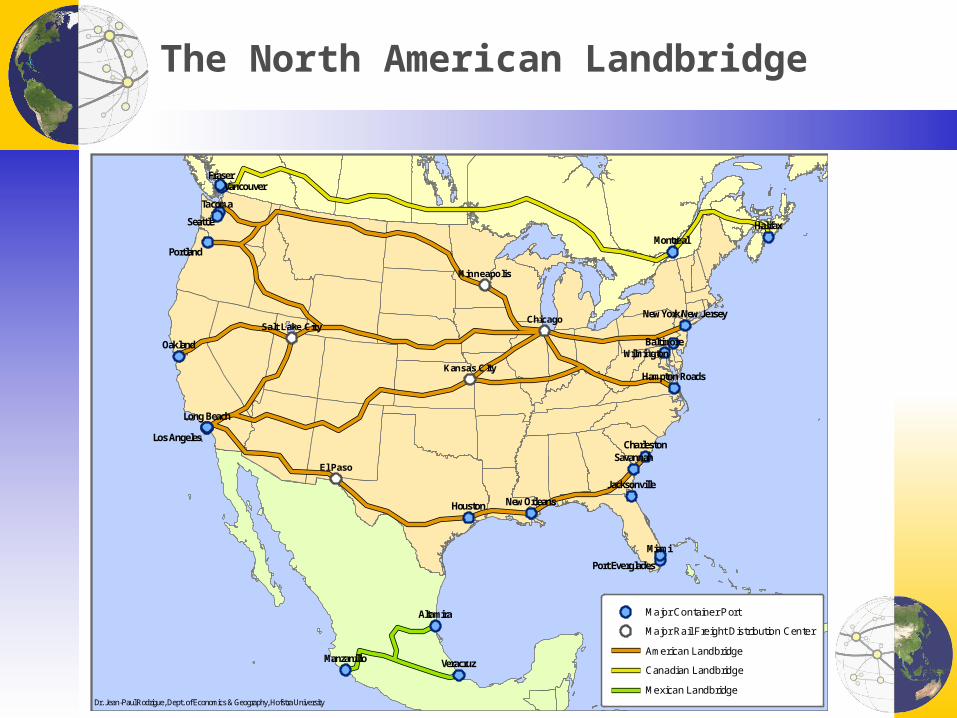

The North American Landbridge

El Paso

Chicago

Kansas CIty

Minneapolis

Salt Lake City

Miami

Tacoma

Fraser

Seattle

Oakland

Houston

Halifax

Veracruz

Altamira

Savannah

PortlandMontreal

Vancouver

Baltimore

Manzanillo

Wilmington

Long Beach

Charleston

New Orleans

Los Angeles

Jacksonville

Hampton Roads

Port Everglades

New York/New Jersey

The North American Landbridge

Major Container Port

Major Rail Freight Distribution Center

American Landbridge

Canadian Landbridge

Mexican LandbridgeDr. Jean-Paul Rodrigue, Dept. of Economics & Geography, Hofstra University

The Emergence of a Nodal Space: Third Phase

■ The Logistical Node• Fast growth of international trade

with the full realization of comparative advantages.

• Geographical and functional integration of production, distribution and consumption.

• Commodity / Supply Chains.• Transportation integrated in the

production / retailing process.• Global Production Networks

(GPN).• Nodes as logistical poles

where value added activities are performed.

• Entirely new nodal locations.

Su

pp

ly C

hain

Flows

Market

Transport Chain

Parts and rawmaterials

Manufacturingand assembly

Distribution

Market

Stage

Bulk shipping

Unit shipping

High volumesLow frequency

Low volumesHigh frequency

LTL shipping

Average volumesHigh frequency

Network

GPN

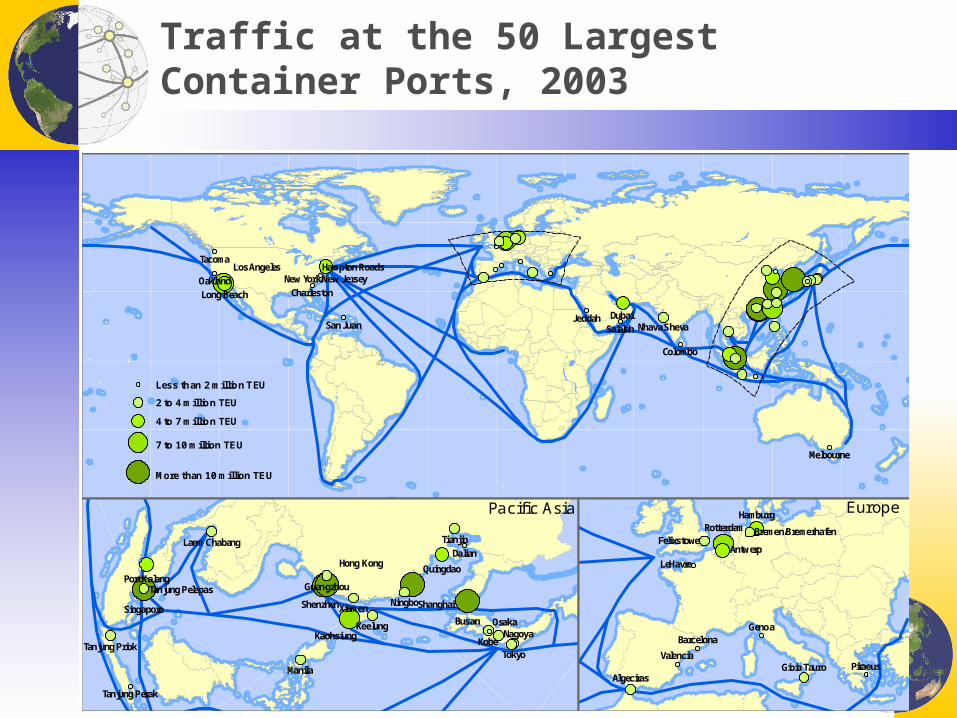

Traffic at the 50 Largest Container Ports, 2003

DubaiJeddah

Tacoma

Colombo

Salalah

Oakland

San Juan

Melbourne

Long Beach Charleston

Nhava Sheva

Los Angeles Hampton RoadsNew York/New Jersey

Kobe

Osaka

Tokyo

BusanNagoya

Dalian

Ningbo

Manila

Xiamen

Tianjin

Keelung

Quingdao

ShanghaiShenzhen

Kaohsiung

Hong Kong

Guangzhou

Singapore

Port Kalang

Laem Chabang

Tanjung Perak

Tanjung Priok

Tanjung Pelepas

Less than 2 million TEU

2 to 4 million TEU

4 to 7 million TEU

7 to 10 million TEU

More than 10 million TEU

Genoa

PiraeusValencia

Barcelona

AlgecirasGioia Tauro

LeHavre

FelixstoweAntwerp

Bremen/Bremerhafen

HamburgRotterdam

Pacific Asia Europe

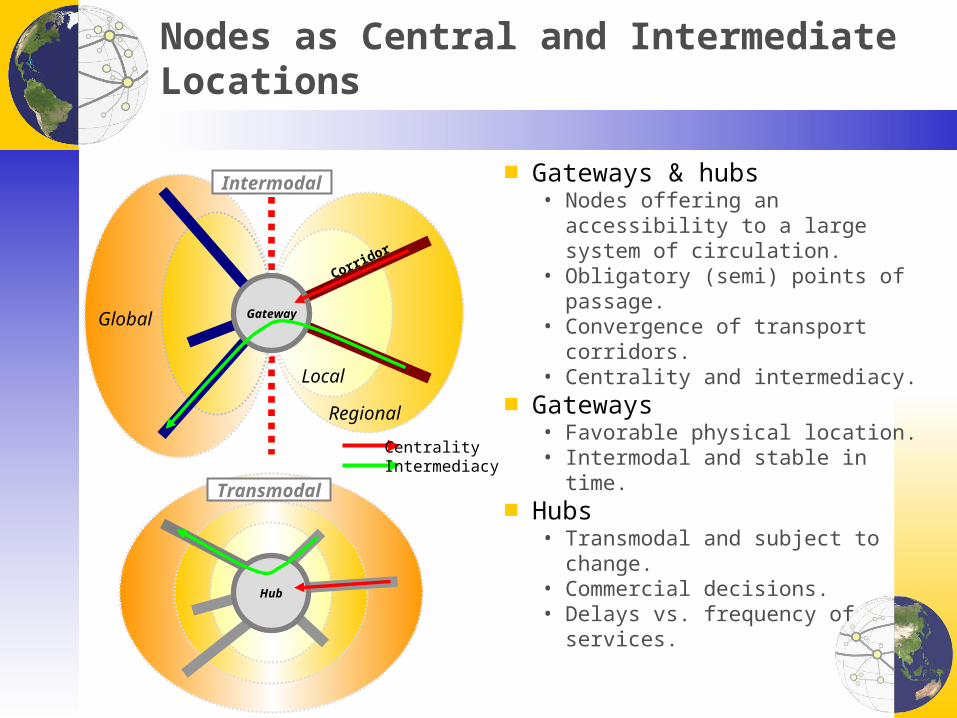

Nodes as Central and Intermediate Locations

■ Gateways & hubs• Nodes offering an accessibility to a

large system of circulation.• Obligatory (semi) points of

passage.• Convergence of transport

corridors.• Centrality and intermediacy.

■ Gateways• Favorable physical location.• Intermodal and stable in time.

■ Hubs• Transmodal and subject to change.• Commercial decisions.• Delays vs. frequency of services.

Gateway

Local

Regional

Global

Corridor

CentralityIntermediacy

Intermodal

Hub

Transmodal

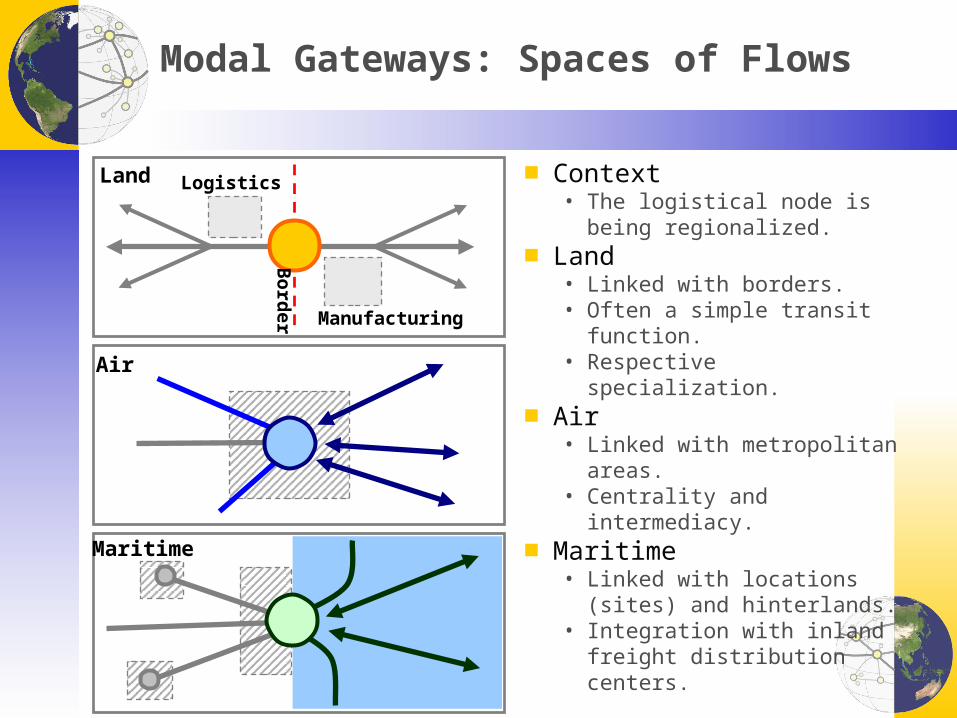

Modal Gateways: Spaces of Flows

■ Context• The logistical node is being

regionalized.■ Land

• Linked with borders.• Often a simple transit function.• Respective specialization.

■ Air• Linked with metropolitan areas.• Centrality and intermediacy.

■ Maritime• Linked with locations (sites) and

hinterlands.• Integration with inland freight

distribution centers.B

order

Logistics

Manufacturing

Land

Air

Maritime

Major US Modal Gateways, 2004

Port of Miami

Port of Tacoma

Port of Seattle

Port of Houston

Port of Oakland

Port of Beaumont

Port of Portland

Port of New York

Port of Savannah

Port of Baltimore

Port of CharlestonPort of Long Beach

Port of New Orleans

Port of Morgan City

Port of Los Angeles

Port of Philadelphia

Port of Jacksonville

Port of Norfolk Harbor

Port of Corpus ChristiPort of Port Everglades

Port of Huron

Port of Blaine

Port of Laredo

Port of Hidalgo

Port of El Paso

Port of Pembina

Port of Detroit

Port of Nogales

Port of Sweetgrass

Port of Calexico-East

Port of Alexandria Bay

Port of Otay Mesa Station

Port of Brownsville-Cameron

Port of Champlain-Rouses Pt.

Port of Buffalo-Niagara Falls

Chicago

Atlanta

Cleveland

New Orleans

Dallas-Fort Worth

Boston Logan Airport

JFK International Airport

Seattle-Tacoma International

Miami International Airport,

Los Angeles International Airport

San Francisco International Airpor

Air Gateways

$68 Billion

Exports

Imports

Land Gateways

$64 Billion

Exports

Imports

Port Gateways

$81 Billion

Exports

Imports

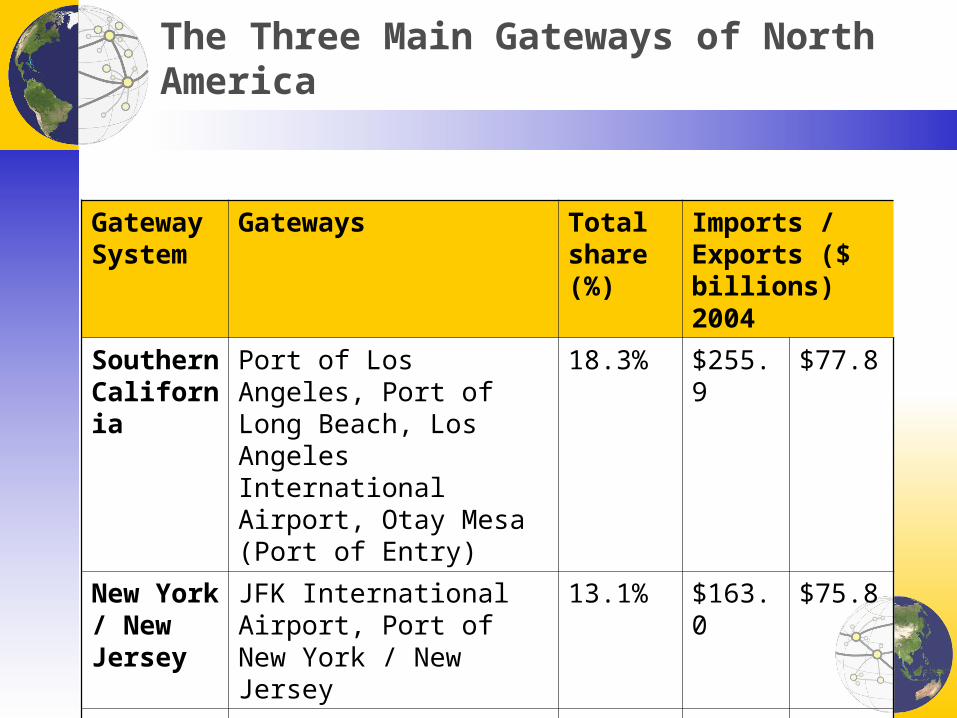

The Three Main Gateways of North America

Gateway System

Gateways Total share (%)

Imports / Exports ($ billions) 2004

Southern California

Port of Los Angeles, Port of Long Beach, Los Angeles International Airport, Otay Mesa (Port of Entry)

18.3% $255.9 $77.8

New York / New Jersey

JFK International Airport, Port of New York / New Jersey

13.1% $163.0 $75.8

Detroit Detroit (Port of Entry), Huron (Port of Entry)

9.8% $97.9 $81.8

Integrated Transport Systems: From Fragmentation to Coordination

Factor Cause Consequence

Technology Containerization & IT Modal and intermodal innovations; Tracking shipments and managing fleets

Capital investments Returns on investments

Highs costs and long amortization; Improve utilization to lessen capital costs

Alliances and M & A Deregulation Easier contractual agreements; joint ownership

Commodity chains Globalization Coordination of transportation and production (integrated demand)

Networks Consolidation and interconnection

Multiplying effect

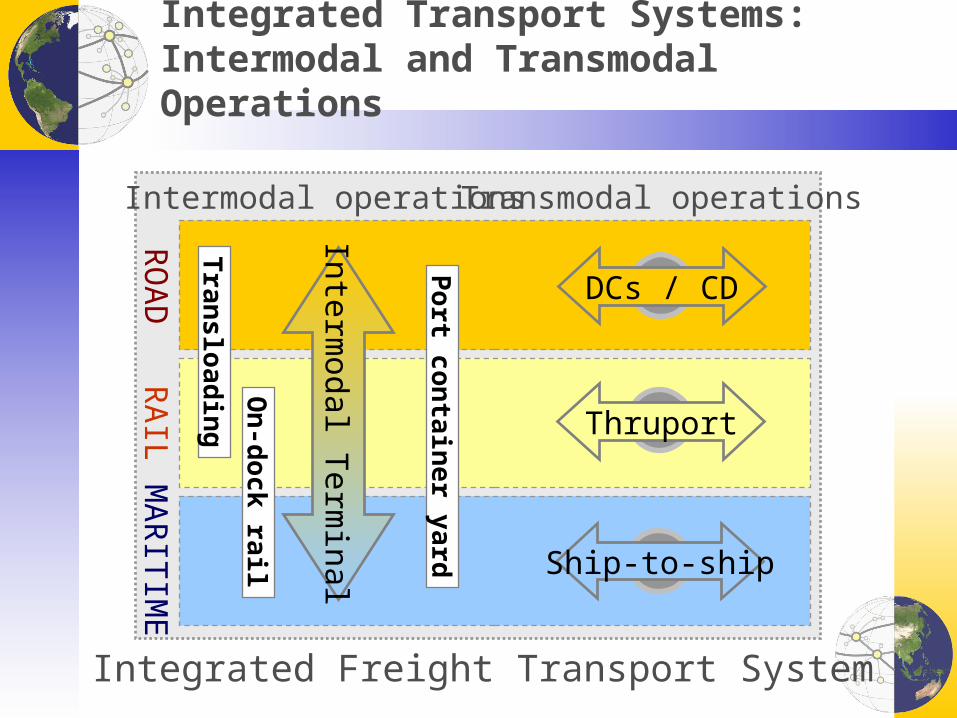

Integrated Transport Systems: Intermodal and Transmodal Operations

RO

AD

RA

ILM

AR

ITIM

E

Inte

rmod

al T

erm

inal

Thruport

Ship-to-ship

DCs / CD

Intermodal operationsTransmodal operations

On-dock rail

Transloading

Integrated Freight Transport System

Port container yard

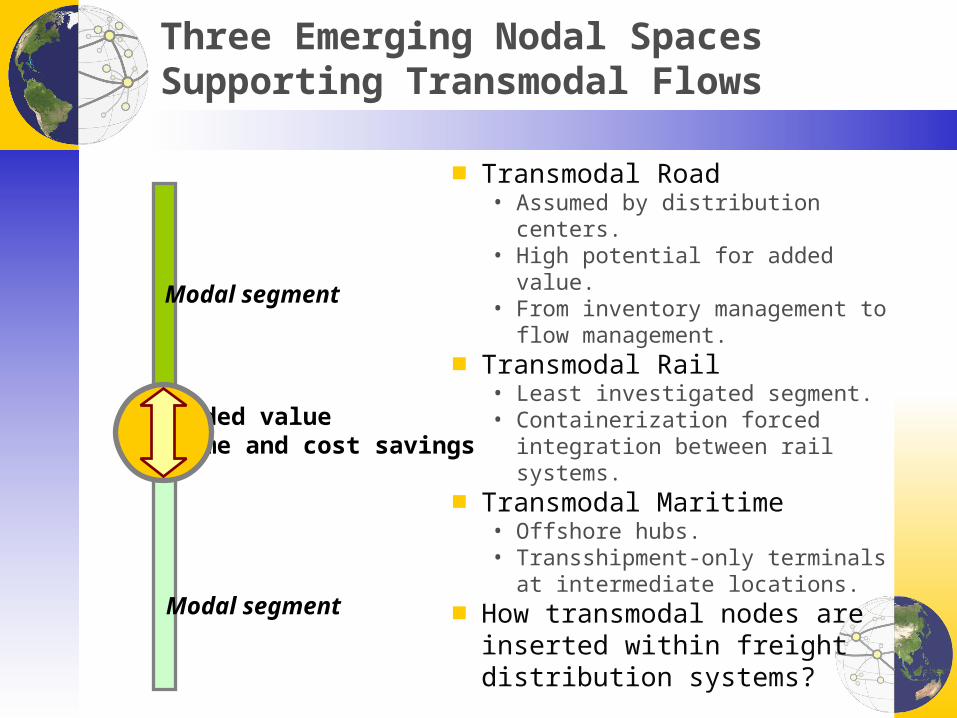

Three Emerging Nodal Spaces Supporting Transmodal Flows

■ Transmodal Road• Assumed by distribution centers.• High potential for added value.• From inventory management to flow

management.■ Transmodal Rail

• Least investigated segment.• Containerization forced integration

between rail systems.■ Transmodal Maritime

• Offshore hubs.• Transshipment-only terminals at

intermediate locations.■ How transmodal nodes are inserted

within freight distribution systems?

Modal segment

Modal segment

Added valueTime and cost savings

Cross-Docking Distribution Center

Suppliers

Customers

Receiving

Shipping

Sorting

Distribution Center Before Cross-Docking

LTL

Suppliers

Customers

After Cross-Docking

TL

TL

Cross-Docking DC

UPS Willow Springs Distribution Center, Chicago

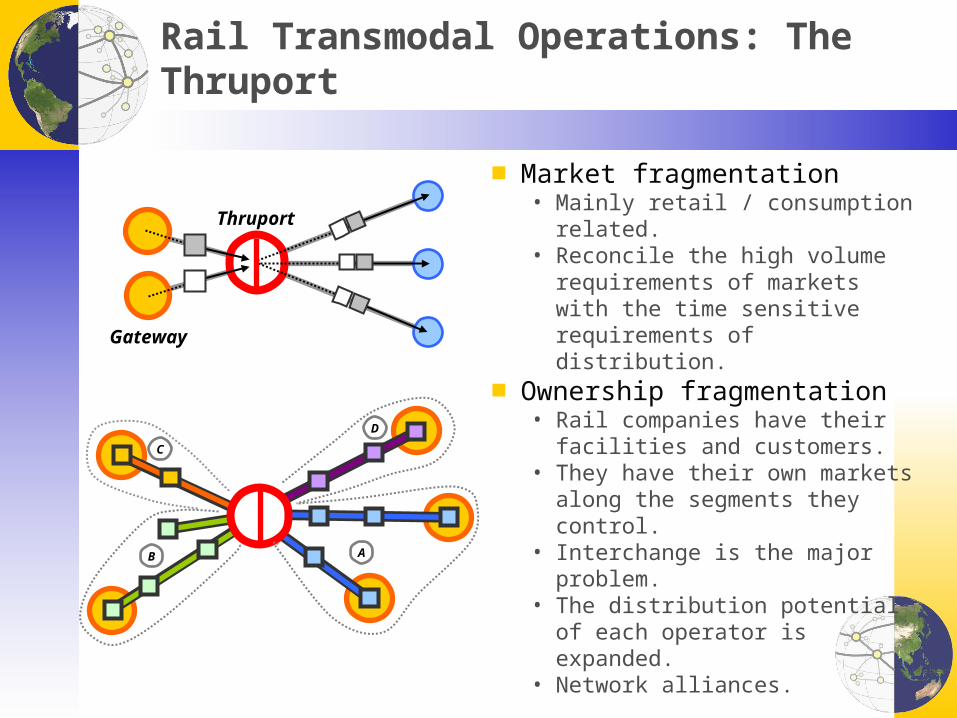

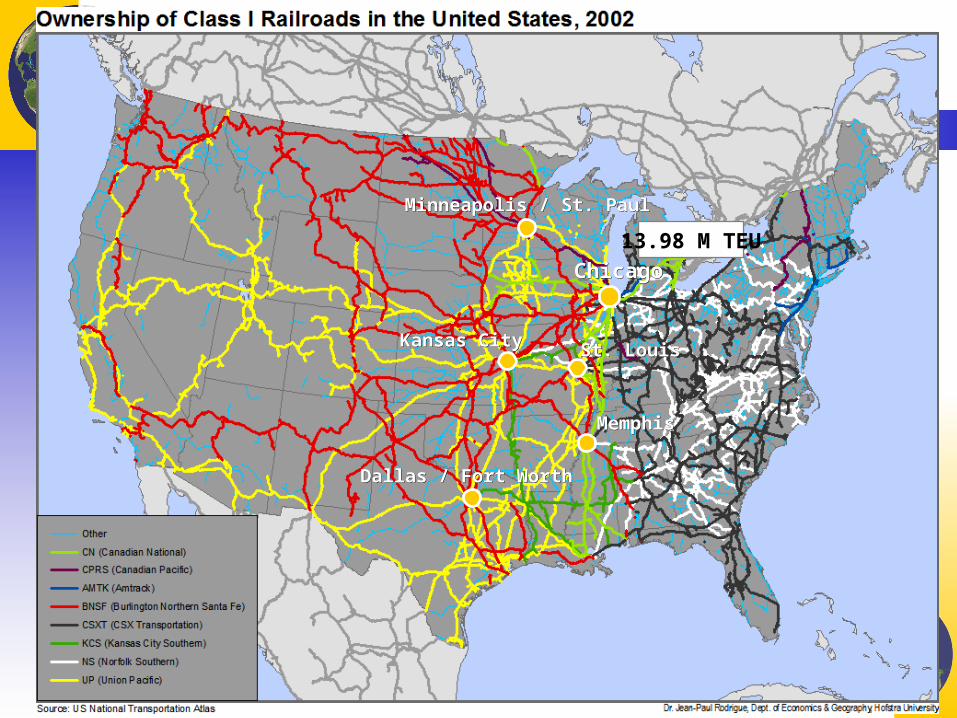

Rail Transmodal Operations: The Thruport

■ Market fragmentation• Mainly retail / consumption related.• Reconcile the high volume

requirements of markets with the time sensitive requirements of distribution.

■ Ownership fragmentation• Rail companies have their facilities

and customers.• They have their own markets along

the segments they control.• Interchange is the major problem.• The distribution potential of each

operator is expanded.• Network alliances.

Thruport

Gateway

B A

C

D

ChicagoChicago

Minneapolis / St. PaulMinneapolis / St. Paul

Dallas / Fort WorthDallas / Fort Worth

MemphisMemphis

Kansas CityKansas City St. LouisSt. Louis

13.98 M TEU

Mi-Jack Stack-Packer (Thruport Terminal)

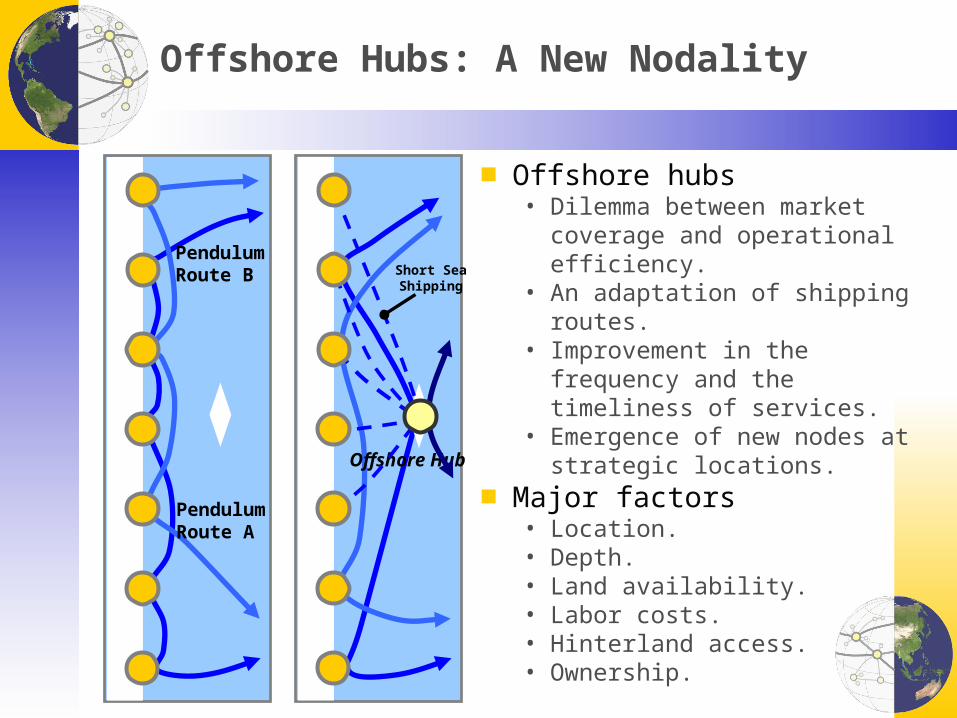

Offshore Hubs: A New Nodality

■ Offshore hubs• Dilemma between market coverage

and operational efficiency.• An adaptation of shipping routes.• Improvement in the frequency and

the timeliness of services.• Emergence of new nodes at strategic

locations.■ Major factors

• Location.• Depth.• Land availability.• Labor costs.• Hinterland access.• Ownership.

Short SeaShipping

Pendulum Route A

Pendulum Route B

Offshore Hub

Ports with the Highest Transshipment Function, 2004

98%

96%

95%

95%

91%

90%

90%

90%

87%

86%

86%

85%

81%

72%

70%

57%

57%

55%

50%

50%

1.1

3.3

3.1

2.1

19.4

0.7

0.5

1.4

1

1

0.7

2.5

1.9

1.6

1.4

0.9

0.6

5.3

3.2

2.6

30% 40% 50% 60% 70% 80% 90% 100%

Freeport

Tanjung Pelepas

Gioia Tauro

Salalah

Singapore

Port Said

Cagliari

Malta

Damietta

Kingston

Taranto

Algeciras

Panama (2)

Colombo

Sharjah

Piraeus

Las Palmas

Kaohsiung

Dubai

Port Klang

0 5 10 15 20 25

Transshipment share

Volume (M TEU)

Las Palmas: At the Crossroad of Transatlantic Shipping

■ Emergence of an offshore hub• Above 600,000 TEU (2005).• An intermediacy node along major

maritime routes and major markets; relay transshipment.

• Deviation effect:• Minimal for: circum-Africa /

Western Europe, Mediterranean / Central America, Europe-Med. / South America.

• Algeciras:• Biggest competitor.• Net advantage (low deviation) for

the Mediterranean / North America route).

Las Palmas

Global Port Operators: Using Nodes to Control Global Flows

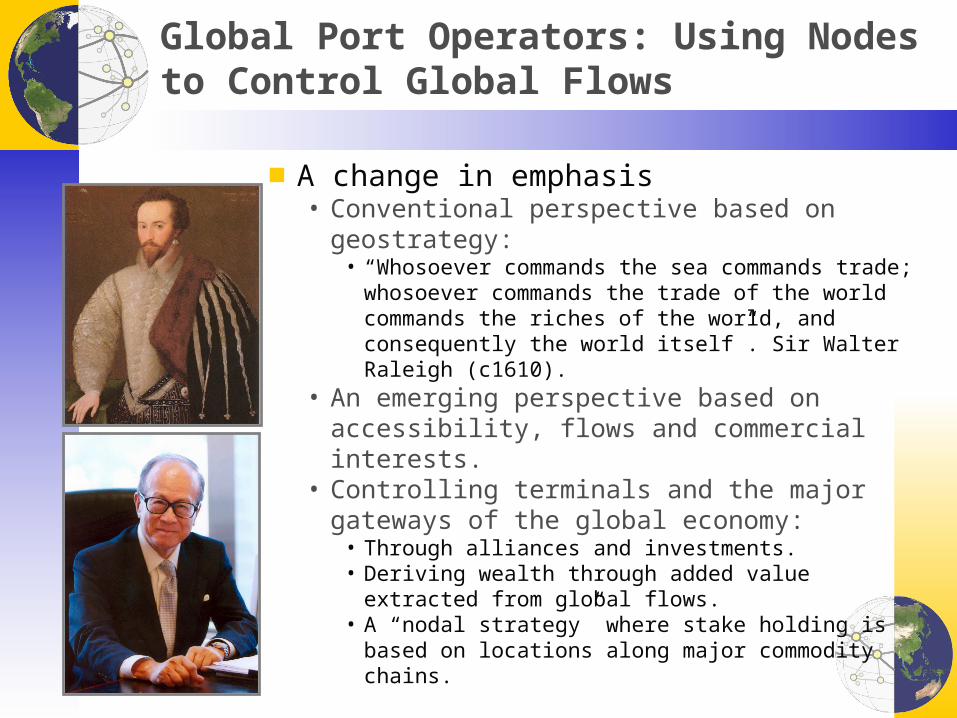

■ A change in emphasis• Conventional perspective based on geostrategy:

• “Whosoever commands the sea commands trade; whosoever commands the trade of the world commands the riches of the world, and consequently the world itself”. Sir Walter Raleigh (c1610).

• An emerging perspective based on accessibility, flows and commercial interests.

• Controlling terminals and the major gateways of the global economy:

• Through alliances and investments.• Deriving wealth through added value extracted from

global flows.• A “nodal strategy” where stake holding is based on

locations along major commodity chains.

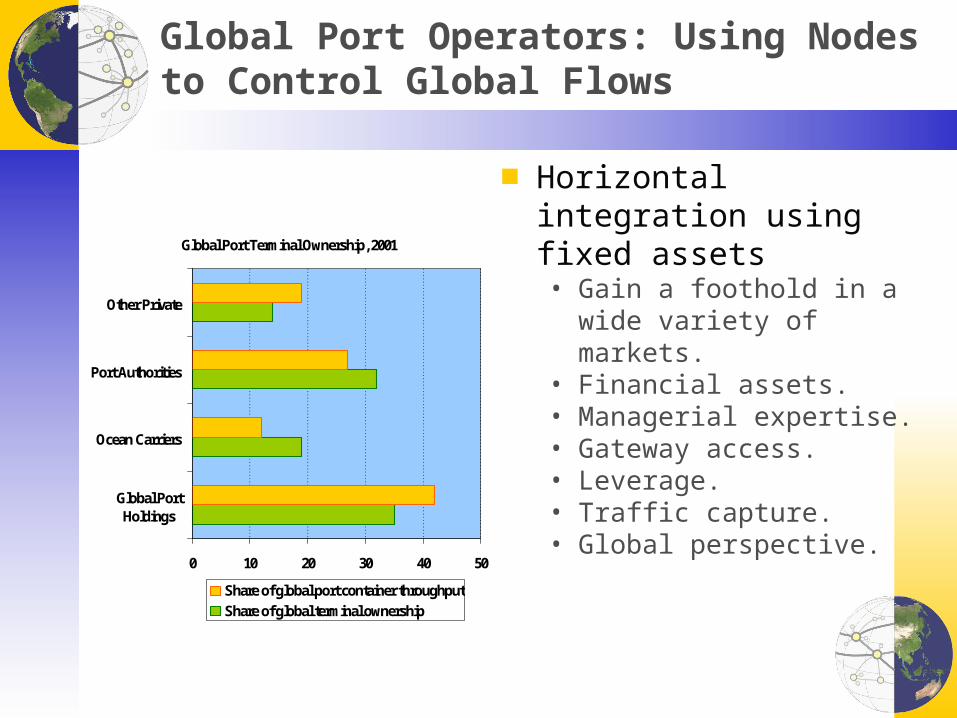

Global Port Operators: Using Nodes to Control Global Flows

Global Port Terminal Ownership, 2001

0 10 20 30 40 50

Global PortHoldings

Ocean Carriers

Port Authorities

Other Private

Share of global port container throughputShare of global terminal ownership

■ Horizontal integration using fixed assets• Gain a foothold in a wide variety of

markets.• Financial assets.• Managerial expertise.• Gateway access.• Leverage.• Traffic capture.• Global perspective.

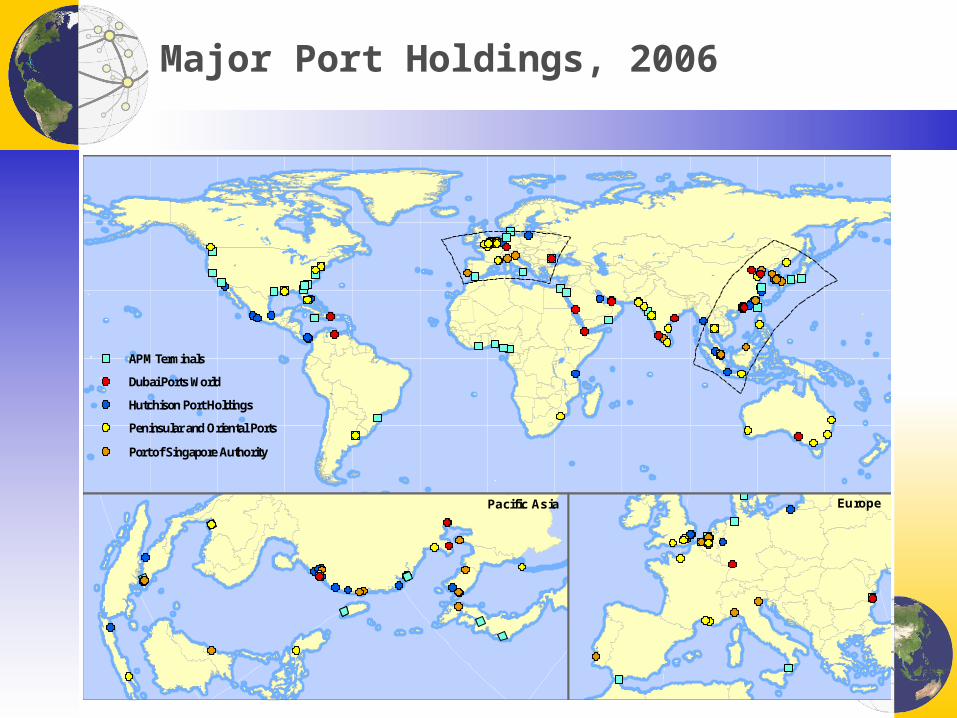

Major Port Holdings, 2006

Pacific Asia Europe

APM Terminals

Dubai Ports World

Hutchison Port Holdings

Peninsular and Oriental Ports

Port of Singapore Authority

Conclusion: Emergence of a Global Nodal Space

■ The logistical node• Central and intermediate locations; gateways or hubs.• Geographical and functional integration brought by the

emergence of global production networks:• Extension and complexity.• Control and synchronization of flows.

• Effectively captures and adds value within global supply chains.• Competition (between and within nodes).

■ Challenges and opportunities• Congestion (offshore hubs and port regionalization).• Integration (intermodal and transmodal).• Energy prices (logistical friction).• Macro-economic changes (trade imbalances).