Florida International University - care-mendoza.nd.edu · shares issued by trading companies and...

65

1 Consequences of changing the auditor’s report: Evidence from the U.K. Elizabeth Gutierrez Universidad de Chile Miguel Minutti-Meza* University of Miami Kay W. Tatum University of Miami Maria Vulcheva Florida International University May 17, 2016 Abstract: The audit regulator in the United Kingdom made significant changes to the auditor’s report for large public companies with fiscal years beginning on or after October 1, 2012. The new report has to describe significant risks of material misstatement, the application of materiality, and the audit’s scope. We study changes in audit fees, audit quality, and investors’ reaction to the report’s public release in the two years before and after the new rules. We find mixed evidence of a change in audit fees, ranging from an increase of nearly four percent to no change, depending on model specification. We do not find evidence of changes in audit quality or investors’ reaction to the report’s public release. Further examining the content of the new reports, we document that the total length of the report, the length of the risks’ discussion, and the number of risks are positively associated with audit fees. Moreover, materiality is inversely related to audit quality. Thus, although the new report format had a small impact on audit fees and did not significantly change audit quality or investors’ reaction to the report, the mandated risk and materiality disclosures are associated with cross-sectional variation in audit fees and quality. The authors thank Keith Czerney, Pietro Bianchi, Like Jiang (discussant), Jake Krupa, Stephania Mason (discussant), Robert Pawlewicz, Matthew Phillips, Grace Pownall, Sundaresh Ramnath, Joe Schroeder, Michael Willenborg, and seminar participants at AAA Auditing Section Midyear Meeting 2016, AAA International Accounting Section Midyear Meeting 2016, Florida International University, the International Symposium on Audit Research (ISAR) 2015, Ohio State University, Public Company Accounting Oversight Board (PCAOB), and Singapore Management University for helpful comments and suggestions. All errors are our own. *Corresponding author: [email protected].

Transcript of Florida International University - care-mendoza.nd.edu · shares issued by trading companies and...

1

Consequences of changing the auditor’s report: Evidence from the U.K.

Elizabeth Gutierrez

Universidad de Chile

Miguel Minutti-Meza*

University of Miami

Kay W. Tatum

University of Miami

Maria Vulcheva

Florida International University

May 17, 2016

Abstract: The audit regulator in the United Kingdom made significant changes to the auditor’s report

for large public companies with fiscal years beginning on or after October 1, 2012. The new report has to

describe significant risks of material misstatement, the application of materiality, and the audit’s scope.

We study changes in audit fees, audit quality, and investors’ reaction to the report’s public release in the

two years before and after the new rules. We find mixed evidence of a change in audit fees, ranging from

an increase of nearly four percent to no change, depending on model specification. We do not find

evidence of changes in audit quality or investors’ reaction to the report’s public release. Further

examining the content of the new reports, we document that the total length of the report, the length of the

risks’ discussion, and the number of risks are positively associated with audit fees. Moreover, materiality

is inversely related to audit quality. Thus, although the new report format had a small impact on audit fees

and did not significantly change audit quality or investors’ reaction to the report, the mandated risk and

materiality disclosures are associated with cross-sectional variation in audit fees and quality.

The authors thank Keith Czerney, Pietro Bianchi, Like Jiang (discussant), Jake Krupa, Stephania Mason (discussant), Robert Pawlewicz, Matthew Phillips, Grace Pownall, Sundaresh Ramnath, Joe Schroeder, Michael Willenborg, and seminar participants at AAA Auditing Section Midyear Meeting 2016, AAA International Accounting Section Midyear Meeting 2016, Florida International University, the International Symposium on Audit Research (ISAR) 2015, Ohio State University, Public Company Accounting Oversight Board (PCAOB), and Singapore Management University for helpful comments and suggestions. All errors are our own. *Corresponding author: [email protected].

2

Consequences of changing the auditor’s report: Evidence from the U.K.

1. INTRODUCTION

Audit regulators worldwide are taking steps to enhance the content of the auditor’s report,

including the Financial Reporting Council (FRC) in the United Kingdom (U.K.) and Ireland, the

International Auditing and Assurance Standards Board (IAASB) across countries, and the Public

Company Accounting Oversight Board (PCAOB) in the U.S. In most countries, including the

United States (U.S.), the auditor’s report uses standardized language for the vast majority of

companies. Most importantly, the auditor’s opinion has a “pass or fail” nature regarding

compliance with accounting principles. Arguably, the auditor’s report provides financial

statement users with little company-specific information about the auditor’s work.

The FRC has promulgated changes issuing International Standard on Auditing (ISA) 700

(U.K. and Ireland, revised June 2013), “The Independent Auditor’s Report on Financial

Statements” (FRC 2013). This standard mandates significant modifications to the auditor’s

report for companies with a premium listing of equity shares on the London Stock Exchange

(LSE) Main Market with fiscal years beginning on or after October 1, 2012 (i.e., fiscal year-end

on or after September 2013).1 The new report is significantly longer than the previous

standardized report. The auditor must describe the most significant risks of material

misstatement, the application of materiality, and the audit’s scope.2 These disclosures were not

required by prior auditor’s report standards.

Concurrently with the FRC’s new standard, the IAASB and PCAOB issued proposals for 1 The Main Market is the LSE’s principal market for listed companies from the U.K. and overseas. There are three listing categories in the Main Market: premium, standard, and high growth. Premium listing is only open to equity shares issued by trading companies and closed- and open-end investment entities. Premium listed companies must comply with the U.K.’s highest standards of regulation and corporate governance. http://www.londonstockexchange.com/companies-and-advisors/main-market/main/market.htm. In our analyses we focus on premium listed non-financial companies incorporated in Great Britain. 2 In Appendix A we provide an example of a U.K. auditor’s report prepared in 2013 in accordance with the new rules.

3

revised auditor reporting standards (IAASB 2013; PCAOB 2013). An important new

requirement in both the IAASB and PCAOB standards is to communicate information specific to

key audit matters (KAMs – the IAASB proposal) or critical audit matters (CAMs – the PCAOB

proposal). Similar to the U.K. requirements regarding the assessment and disclosure of

significant risks of material misstatement, both KAMs and CAMs aim to provide additional

context about the auditor’s work.3 The IAASB issued revised auditor reporting standards in

January 2015, including ISA 701 “Communicating Key Audit Matters in the Independent

Auditor’s Report” (IAASB 2015c). The PCAOB continues to work on a revised standard and

intends to issue a reproposal in the second or third quarter of 2016.4

In this study we examine the consequences of the new auditor’s report in the U.K., in

terms of audit costs, audit quality, and investors’ reaction to the report’s filing. We take

advantage of the cut-off date for the adoption of the new report’s requirements, applicable to

companies with fiscal years starting on or after October 1, 2012. In our first set of analyses, we

examine data from two years before and after the cut-off date, and test for changes in audit fees,

as a proxy for audit costs; in absolute discretionary accruals, as a proxy for audit quality; and, in

three-day cumulative absolute abnormal returns and trading volume around the public

dissemination of the annual report, which includes the auditor’s report, as proxies for investors’

reaction to the report’s content.5

The regulatory cut-off date effectively results in having a treatment group of new report

adopters and a control group of non-adopters immediately before and after the September 2013

3 The PCAOB proposal also contains other changes, including enhancing the report’s writing and adding statements about auditor independence, auditor tenure, and the auditor’s responsibility for, and evaluation of, other information. 4 http://pcaobus.org/Standards/Documents/2016Q1-standard-setting-agenda.pdf 5 In additional analyses we examine the incidence of small earnings and total accruals as alternative proxies for audit quality; and, three-day abnormal signed returns and three-day trading spread around the report’s filing date as alternative proxies for investors’ reaction. We do not find evidence that the new report resulted in changes in the incidence of small earnings, total accruals, abnormal signed returns, or trading spread.

4

implementation date. In our second set of analyses, we examine the one-year pre-post adoption

changes for companies with fiscal year-end between September 2013 and February 2014 (i.e.,

adopters of the new report format starting in 2013), using as a benchmark the group of

companies with fiscal year-end between March and August 2013 (i.e., non-adopters of the new

report format in 2013). The control group, consisting of companies subject to the same listing

requirements, but fiscal year-end immediately before the September 2013 cut-off date, helps to

isolate the effects of the new report from time trends and other potential confounding factors

(i.e., short-term difference-in-differences analysis).6

We document mixed evidence regarding a change in audit fees. Examining two years

before and after the new rules, the new report is associated with an increment in audit fees of

approximately four percent. This estimate is reduced to approximately three percent after

including company fixed effects in our pre-post audit fee model. However, comparing

companies reporting six months before and after the regulatory cut-off, to the same companies a

year prior, we do not find evidence of a difference-in-differences effect of the new report on

audit fees. Furthermore, we do not find evidence that the new report had an overall impact on

audit quality or investors’ reaction. This lack of findings is consistent with several FRC’s

statements, including ISA 700 (U.K. and Ireland, revised June 2013), which explicitly mention

that the intent of the new requirements is to make public information previously discussed with

the audit committee and that meeting these requirements is not likely to be very costly (FRC

2013a, 2013b, 2013c).

6In our analyses we use all non-financial companies in the LSE Main Market Premium that meet the cut-off criteria, with available financial statement data in Thomson Reuters Worldscope and hand-collected data from annual reports. Our sample selection criteria are discussed in more detail in Section 4. We acknowledge that the industry composition of companies with fiscal year-ends before and after October is not identical. However, we only use the control group to isolate the one-year time difference between the year of adoption and the year prior (i.e., meet the parallel trends assumption of difference-in-differences). As additional analyses we also include firm fixed effects, aiming to isolate industry and any other time-invariant firm-specific characteristics.

5

We also conduct cross-sectional analyses pertaining to the two-year period following the

adoption of the new rules. We examine the association between audit fees, audit quality, and

investors’ reaction and several quantifiable elements of the new reports, including the total

length of the report, the length of the risks’ discussion, the number of risks, and the materiality

threshold.7 Under the new rules, the length of the report has tripled, increasing from one to

approximately three pages. The section on risks of material misstatement discloses on average

four risks. The average (median) materiality is 0.6 (0.5) percent of total assets.8 We document

that the length of the report, the length of the risks’ discussion, and the number of risks are all

positively related to audit fees, suggesting an association between auditor effort or risk premium

and the auditor’s assessment and disclosure of important audit issues. We also find that

materiality is positively related to absolute discretionary accruals, suggesting that materiality is

inversely related to audit quality. Moreover, we find some evidence that the length of the report

and the length of the risks’ discussion are negatively associated with three-day absolute

abnormal returns, indicating larger price reaction to more concise audit reports. However, we do

not find consistent evidence using abnormal trading volume.9

Our combined findings suggest that the risk and materiality disclosures in the report are

predictably related to cross-sectional variation in audit fees and quality. Arguably, if the risks

and materiality disclosures were strictly boilerplate, they would not be associated with these

outcomes. Nevertheless, comparing the two years before and after the adoption of the new rules,

7 We do not explicitly assess the effect of scope disclosures, beyond examining the effects of the total length of the auditor’s report, because the scope disclosures are difficult to quantify. In many cases the scope disclosures discuss the group structure of the audit without providing additional details. See for example, the scope section of the report included in Appendix A. 8 We scale the materiality amount in British Pounds by total assets in order to use the same denominator for all companies. However, our results do not depend on scaling by total assets. We also use the natural logarithm of the materiality amount in our main analyses. 9 In additional analyses we also report the results using signed three-day abnormal returns. We do not find an association between the report’s characteristics and signed three-day abnormal returns.

6

the new report had a relatively small impact on audit fees and did not significantly change audit

quality or investors’ reaction around the filing date.

Our study adds to the mixed evidence provided by other contemporaneous papers

examining the effect of the new U.K. audit regulation (Lennox et al. 2015; Reid et al. 2015a,

2015b). While closely related to these studies, our study differs in three aspects. First, we

examine a longer sample period that spans four years around the adoption of the new rules. Our

sample allows us to investigate changes beyond the first year after the adoption of the new rules.

Second, we use the September 2013 regulatory cut-off date to implement difference-in-

differences analyses, where the control group is comprised of companies listed in the same

market, with annual reports in the months just preceding the regulatory cut-off.10 Third, we

perform a series of cross-sectional tests examining the association between the report’s content

and audit fees, audit quality, and investor’s reaction. Lennox et al. (2015) document that the risk

disclosures are not incrementally informative to investors, focusing on changes in firm value and

the incremental impact of the risk disclosures on firm value.11 Furthermore, they do not find

evidence of either a change in market reaction in the short window surrounding the report’s

filing, or a significant change in audit fees after the adoption of the new rules. On the other hand,

Reid et al. (2015, 2015b) find a marginal increase in audit fees, a decrease of 0.019 in absolute

abnormal accruals, a decrease of 24 percent in the odds of meeting or beating analysts’ forecasts,

and an increase of approximately 12.7 percent in abnormal trading volume around the filing of

annual reports after the adoption of the new rules. 10 Both Lennox et al. (2015) and Reid et al. (2015a; 2015b) use companies listed in the LSE’s AIM market as a control group. AIM is an alternative international market for comparatively smaller growing companies. There are major differences between premium and AIM listed companies. A premium listing entails comparatively more rigorous standards and compliance with the U.K. Corporate Governance Code. Reid et al. (2015a; 2015b) also use companies listed in the U.S. New York Stock Exchange (NYSE) as an alternative control group. There are considerable differences between the NYSE and LSE premium listing requirements, as well as different litigation environments in the U.S. and U.K. 11 Lennox et al. (2015) examine the effect of risk disclosures as input of long-window equity valuation models.

7

Our findings can be of interest to regulators and other parties considering changes to the

auditor’s report. The U.K. is a large and developed market and our findings may be useful in

assessing similar changes to the auditor’s report in other similar jurisdictions. With regard to the

U.K., the findings of our study may help regulators and other interested parties, aiming to

enhance the usefulness of the currently mandated new report’s disclosure in the U.K. (FRC

2015).12 This study contributes to the literature on auditor’s reports and their association with the

cost of audits, audit quality, and investors’ reaction (Bedard et al. 2015; Butler et al. 2004;

Carcello and Li 2013; Czerney et al. 2014a, 2014b; Hay et al. 2006; Menon and Williams 2010).

We also contribute to the literature on risk disclosures in financial reports (Campbell et al. 2014;

Kravet and Muslu 2013). Finally, this study extends the descriptive evidence provided by

financial analysts and auditors on the consequences of the auditor’s report change in the U.K.

(Citi 2014, 2015; KPMG 2014; PwC 2015).

2. BACKGROUND AND HYPOTHESIS DEVELOPMENT

Effective changes to the auditor’s report in the U.K. in 2013

Currently, in most countries, including the U.S., the auditor’s report uses standardized

language for a vast majority of companies. However, investors and regulators have expressed

growing concern about the usefulness of the auditors’ reports. Arguably, the standardized

wording of the auditor’s report and the pass-fail nature of the auditor’s opinion may not give

financial statement users enough relevant information. For example, “until now, auditors’ letters

have been among the least interesting part of annual reports. If the opinions said the accounting

was proper – and virtually all did – and did not voice concern whether the company could stay in

business, the letters were basically the same. There was no reason for an investor to read them” 12 Reviews of the first two years of reports conducted by the FRC and involving discussions with investors and auditors suggest that there is room for improvement, for example by increasing the granularity of risk reporting and providing more explanations about the materiality, scope, and risk disclosures (FRC 2015, 2016).

8

(Norris 2014).

Audit regulators have taken steps to change the auditor’s report. The U.K. FRC has

moved forward by issuing ISA 700 (U.K. and Ireland, revised June 2013), “The Independent

Auditor’s Report on Financial Statements” (FRC 2013a). This new auditing standard mandates

significant changes to the auditor’s report for most large companies listed on the LSE with fiscal

years beginning on or after October 1, 2012.13 The new standard (paragraph 19A of ISA 700)

requires auditors to: (1) describe the most significant risks of material misstatement; (2) disclose

how the auditor applies the concept of materiality, including a materiality threshold for the

statements as a whole and performance materiality; and, (3) explain the scope of the audit.

The new FRC standard complements changes made to the U.K. Corporate Governance

Code in October 2012 (FRC 2012a, 2012b). The Code requires additional specific disclosures for

audit committees, including (1) a description of the significant issues that the audit committee

considered in relation to the financial statements, and how these issues were addressed; (2) an

explanation of how the audit committee has assessed the effectiveness of the external audit

process and the approach taken to the appointment or reappointment of the external auditor; (3)

information about the length of tenure of the current audit firm and when a tender was last

conducted; and, (4) if the external auditor provides non-audit services, an explanation of how the

audit committee ensures that auditor objectivity and independence are safeguarded (paragraph

C.3.8 of the U.K. Corporate Governance Code FRC 2014).

IAASB and PCAOB initiatives to enhance the auditor’s report

An important new requirement in both the IAASB and PCAOB standards is to

communicate information specific to key audit matters (KAMs – the IAASB proposal) or critical 13 In the U.K., the new rules apply to companies with a Premium listing of equity shares regardless of whether they are incorporated in the U.K. or elsewhere. In Ireland, these include Irish incorporated companies with a primary or secondary listing of equity shares on the Irish Stock Exchange.

9

audit matters (CAMs – the PCAOB proposal). Similar to the U.K. requirements regarding the

assessment and disclosure of significant risks of material misstatement, both KAMs and CAMs

aim to provide additional context about the auditor’s work.14 The IAASB issued revised auditor

reporting standards in January 2015, including ISA 700 “Forming an Opinion on Financial

Statements” and ISA 701 “Communicating Key Audit Matters in the Independent Auditor’s

Report” (IAASB 2015c).15

The PCAOB issued an initial proposed auditing standard on the auditor’s report in

August 2013 (PCAOB 2013). The proposed standard retains the basic elements from the existing

standard, including the requirement to express an opinion about whether or not the financial

statements are fairly presented in accordance with GAAP (i.e., “pass or fail” opinion). However,

the proposed standard makes significant changes to the existing report. It requires the auditor to

communicate CAMs, enhances certain language in the current report, and adds new elements.

The new elements are a statement about auditor independence, a statement about the auditor’s

responsibility for other information, and a disclosure on auditor tenure. The proposal to revise

the auditor report model is on the PCAOB’s standard-setting agenda for the second and third

quarter of 2016.

We note that the FRC, IAASB, and PCAOB requirements regarding significant risks of

material misstatement, KAMs, and CAMS do not have identical definitions (EY 2014). The

significant risks of material misstatement are risks that had the greatest effect on audit strategy,

14 The PCAOB proposal also contains other changes, including enhancing the report’s writing and adding statements about auditor independence, auditor tenure, and the auditor’s responsibility for, and evaluation of, other information. 15 The standards will be effective for audits of financial statements for periods ending on or after December 15, 2016. Early adoption is permitted. The key changes are: (1) inclusion and discussion of KAMs; (2) declaration of auditor independence and compliance with ethical standards; (3) signature of the engagement partner with a “harm’s way exemption”; (4) prescribed order of the presentation of the auditor’s report; (5) emphasis on the audit opinion and other firm-specific information; (6) auditor assessment of the appropriateness of the management’s going concern assumption and review of circumstances that might endanger this assumption; and (7) improved disclosure of auditor responsibilities.

10

allocation of resources, and directing of the efforts of the audit team (FRC 2013). KAMs are

areas of most significance in the audit, determined from matters discussed with those charged

with governance, that required auditor attention (IAASB 2015b). CAMs are areas of most

significant audit difficulty, including those that require significant auditor judgment (PCAOB

2013).

Effect of changes to the auditor’s report on audit fees, audit quality, and investors’ reaction

First, we are interested in determining whether the regulatory changes had an overall

impact on the cost of audits. Prior research has found positive association between audit fees and

client size, risk, complexity, and auditor litigation risk (Carcello and Li 2013; Hay et al. 2006;

Seetharaman et al. 2002). Therefore, a potential change in auditor effort and risk premium,

resulting from increased disclosures in the auditor’s report under the new regime, can impact the

cost of audits. Thus, we formulate the following alternative hypothesis:

H1: All else equal, the adoption of the new auditor’s report is associated with an

increase in audit fees.

We are also interested in determining whether the regulatory changes had an overall

impact on audit quality. The literature on audit quality has generally demonstrated that

reputation, litigation, and regulatory concerns shape the incentives that drive auditors to supply

audit quality (DeFond and Zhang 2014). Additional disclosures in the auditor’s report might put

companies and their auditors under more careful scrutiny by users, especially when it comes to

risk disclosures, and thus increase audit quality. Therefore, to test the effect of the new regulation

on audit quality, we formulate the following alternative hypothesis:

H2: All else equal, the adoption of the new auditor’s report is associated with an

increase in audit quality.

11

Finally, we examine whether the regulatory changes are associated with investors’

reaction to the filing of the auditor’s report. The new auditor’s report disclosures on the

significant risks of material misstatement, the application of materiality, and the scope of the

audit were not available to investors before the regulatory changes. These disclosures might

provide new information to the market and motivate a revision in the aggregate investors’ beliefs

about the value of the firm (i.e., price reaction), and a revision of differential pre-announcement

beliefs and announcement interpretations for individual investors (i.e., trading volume reaction)

(Bamber et al. 2011).

Previous studies of the auditor’s report in the U.S. demonstrate that non-standard

modifications, such as going concern opinions, have information content when they are not

expected (Menon and Williams 2010). More generally, Czerney et al. (2014a) document

investors’ reaction to various forms of explanatory language in the auditor’s report (e.g.,

adoption of new accounting standards, division of auditor responsibility, previous restatements,

and emphasis of matter paragraphs) and suggest that the report’s language may have an attention

directing effect. To investigate whether the new format of the auditor’s report has incremental

information content, we propose the following alternative hypothesis:

H3: All else equal, the adoption of the new auditor’s report is associated with investors’

reaction to the filing of annual reports.

However, there are three broad reasons why the changes to the report may not have an

observable effect on audit fees, audit quality, and investors’ reaction in the years immediately

following the adoption of the new rules.

First, regulators did not expect a large revision to the auditors’ methodologies, but instead

aimed to make public several matters already discussed privately between auditors and audit

12

committees. Several FRC statements explicitly mention that the new report’s requirements intend

to make public information previously discussed with the audit committee and that meeting these

requirements is not likely to be very costly. The report’s standard ISA (U.K. and Ireland) 700

(FRC 2013) mentions in paragraph A13A “assessed risks of material misstatement are likely to

have been identified by the auditor in meeting the requirements of ISA (U.K. and Ireland) 315.”

A Consultation Paper (FRC 2013c, paragraph 23) highlights that “investors did not think that

cost would be a significant issue as the costs would largely be related to the additional

consideration of public reporting of matters likely to have been already fully addressed in the

audit and reported to the audit committee.” A Feedback Statement (FRC 2013b, paragraph 6.1),

dealing with implementation issues, notes that “as the auditor is already required to disclose the

information to be included in the audit report to the audit committee the work effort in preparing

it and familiarizing the audit committee with it should be minimal.” Thus, increased disclosures

on auditors’ judgments not change auditors’ litigation risk or enable auditors to increase fees

significantly (i.e., increase number of billable hours or rate per hour). Furthermore, audit quality

may already have accounted for significant risks, even if the auditor or the client did not publicly

disclose such risks (i.e., on average, risks were adequately addressed and mitigated before the

new rules).

Second, the additional information may not be strictly new to investors or significant enough

to change the average perceptions about a company’s financial reporting quality. Disclosing

uncertainty regarding revenue recognition, tax accounting, valuation, etc. may already be

expected by investors given other information sources (e.g., management discussions, financial

analyst reports, audit committee reports) and investors may already infer the risk profile of a

company from other observable characteristics (size, presence of intangible assets including

13

goodwill, etc.).16

Third, the new rules could have a long-term impact not captured by our sample and proxies

for the cost of audits, audit quality, and investors’ reaction. According to FRC (2016, p. 4),

although investors have welcomed extended auditor reporting, and greatly value the enhanced

information it provides, they feel that more could still be done to enhance the reports. Investors

noted that they want more granular descriptions of risks, more transparency about assumptions

made by management and benchmarks used by auditors, and greater precision. For example,

“words like ‘significant’ are not necessarily sufficiently informative” (FRC 2016, p.21).

3. RESEARCH DESIGN AND MODEL SPECIFICATION

Pre-post adoption and difference-in-differences research design

We take advantage of the cut-off date for the adoption of the new auditor’s report

requirements, applicable to LSE Main Market premium listed companies with fiscal years

starting on or after October 1, 2012 (i.e., year-ends on or after September 2013). In our first set

of analyses, using data from two years before and two years after the cut-off date (see Figure 1-

A), we examine pre-post adoption changes in audit fees as a proxy for the cost of audits; in

absolute discretionary accruals as a proxy for audit quality; and, in three-day cumulative

abnormal trading volume and absolute abnormal returns around the public dissemination of the

annual report, which includes the auditor’s report, as proxies for investors’ reaction to the

auditor’s report.

The regulatory cut-off date effectively results in having a treatment group of new report

adopters and a control group of non-adopters immediately before and after the September 2013

implementation date. In a second set of analyses, we examine the one-year pre-post adoption 16 In private discussions with personnel from a Big-4 firm with experience with the report changes we confirmed that in the short term there were no fundamental changes to their methodology and that the ability to increase fees as a result of the new changes was limited.

14

changes for companies with fiscal year-end between September 2013 and February 2014 (i.e.,

adopters of the new report format), including as a benchmark the one-year pre-post changes for

companies with fiscal year-end between March and August 2013 (i.e., non-adopters of the new

report format, see Figure 1-B). Although the sample in the difference-in-difference analysis is

relatively small, we aim to capture short-term changes in outcomes around the adoption of the

new rules, while controlling for other confounding factors.

Next, we conduct additional cross-sectional analyses in the two years following the new

report rules (see Figure 1-C). We examine the association between the auditor’s report content

and audit fees, audit quality, and investors’ reaction. We start by examining the extent of the new

disclosures by focusing on the total length of the auditor’s report. Later on, we focus on

quantifiable elements of the new report, the risks’ discussion and the materiality threshold.

Audit fee analyses

Our measure of audit fees is the logarithm of total fees paid to the auditor for audit

services in each year. We manually obtain audit fees from the notes to the financial statements in

the annual report. To examine the effect of the new report on audit fees, we estimate the

following pre-post model, using all firm-year observations with available data two years before

and after the regulatory cut-off date in September 2013:

AFEESi,t = β0 + β1POSTi,t + β2SIZEi,t + β3ROAi,t + β4LEVi,t + β5CURRi,t

+ β6NSEGi,t + β7FORSALESi,t + β8BIG4i,t + β9CHAUDi,t + β10GCi,t

+ β11DECYEi,t + β12USLISTi,t + IndustryFE + εi,t (1a)

where for company i in year t, POSTi,t is a time indicator variable, equal to one for the two years

following the new report requirements (starting in September 2013), and zero otherwise,

capturing the overall pre-post adoption effect of the new report; SIZEi,t is the natural logarithm of

15

total assets; ROAi,t is net income before extraordinary items (NIBE) divided by total assets;

LEVi,t is long-term debt divided by total assets; FORSALESi,t is non-U.K. sales divided by total

sales; CURRi,t is current assets divided by total assets; NSEGi,t is the natural logarithm of the

number of business segments; USLISTi,t is equal to one if the company is cross-listed on the

NYSE, AMEX, or NASDAQ stock exchanges, and zero otherwise;17 CHAUDi,t is equal to one if

the company has an audit firm change in the current fiscal year, and zero otherwise; GCi,t is

equal to one if the auditor’s report includes a going concern qualification, and zero otherwise;

BIG4i,t is equal to one if the company is audited by a Big-4 auditor, and zero otherwise; and,

IndustryFE are 1-digit SIC Codes industry fixed effects.18 The control variables aim to isolate

the effects of client risk, size, and complexity, and have been commonly used in previous audit

fee research (Hay et al. 2006).

For our difference-in-differences analyses we estimate the following model, using firm-

year observations with fiscal year-end six months before (March to August 2013) and after

(September 2013 to February 2014) the regulatory cut-off date in September 2013, as well as the

same companies in the prior year:

AFEESi,t = β0 + β1ADOPTERi,t + β2YR2013i,t + β3ADOPTER*YR2013i,t

+ β4SIZEi,t + β5ROAi,t + β6LEVi,t + β7CURRi,t + β8NSEGi,t

+ β9FORSALESi,t + β10BIG4i,t + β11CHAUDi,t + β12GCi,t

+ β13DECYEi,t + β14USLISTi,t + IndustryFE + εi,t (1b)

where for company i in year t, ADOPTERi,t is an indicator variable for the September cut-off date

of the new report requirements, equal to one for companies with fiscal year-ends in the six

17 Including over-the-counter (OTC) listings in the USLISTi,t definition does not change our results. 18 All continuous variables in the regression models, except for the investors’ reaction dependent variables (absolute abnormal return and abnormal volume), are winsorized at the one and 99 percent levels to mitigate the presence of outliers. Our results are similar if we winsorize or truncate the investors’ reaction dependent variables (absolute abnormal return and abnormal volume) at the one and 99 percent levels. Standard errors are clustered by company.

16

months from September to February, and zero in the six months from March to August;

YR2013i,t is a time indicator variable, equal to one for companies with fiscal year-ends in the six

months around the adoption date in September 2013 (March 2013 to February 2014), and zero

for the same companies in the year before (March 2012 to February 2013); ADOPTER*YR2013i,t

is the interaction between ADOPTERi,t and YR2013i,t capturing the incremental one-year

difference for adopters of the new report format, compared to the one-year difference for non-

adopters of the new report format (i.e., short-term difference-in-differences estimator); and, all

other variables are as described above. We also include company fixed effects in models 1a and

1b and report the results in Section 6.

Finally, for our cross-sectional analyses of the association between audit fees and report

characteristics we estimate the following model, using firm-year observations for the two years

after the regulatory cut-off date in September 2013:

AFEESi,t = β0 + β1REPORT_DISCLi,t + β2SIZEi,t + β3ROAi,t + β4LEVi,t

+ β5CURRi,t + β6NSEGi,t + β7FORSALESi,t + β8BIG4i,t + β9CHAUDi,t

+ β10GCi,t + β11DECYEi,t + β12USLISTi,t + IndustryFE + εi,t

(1c)

where for company i in year t, REPORT_DISCLi,t is one of the following independent variables:

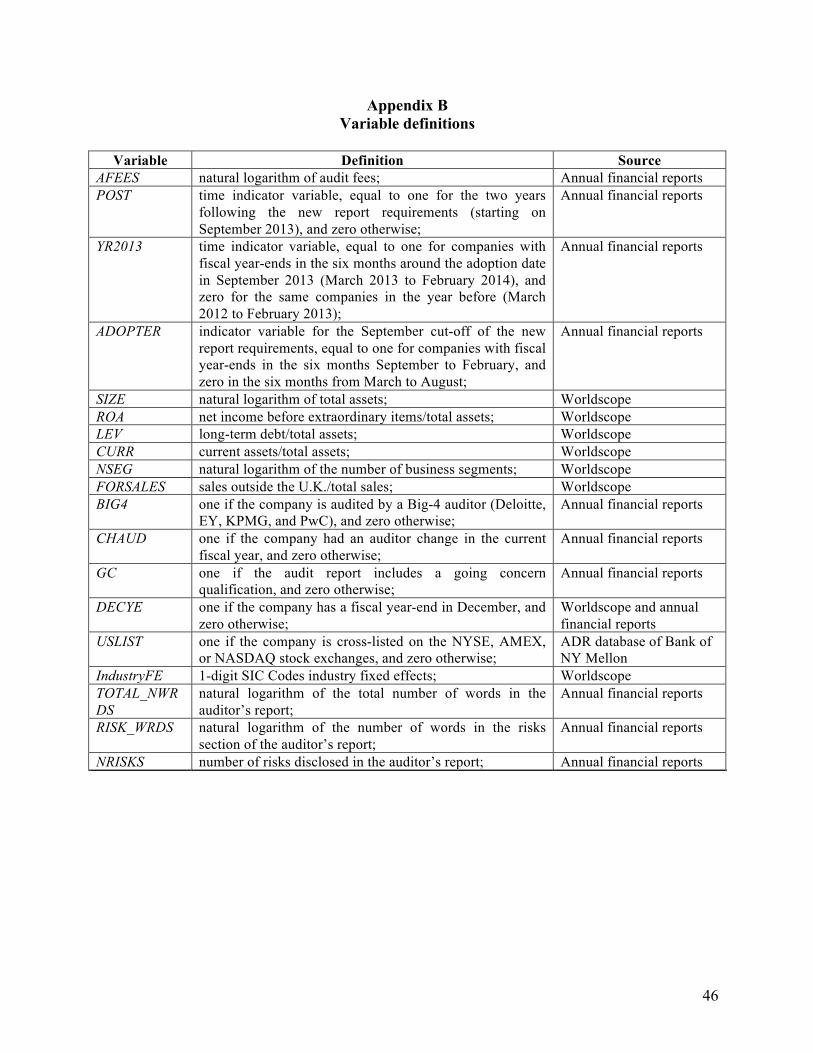

TOTAL_NWRDSi,t, the natural logarithm of the total number of words in the auditor’s report;

RISK_NWRDSi,t, the natural logarithm of the total number of words in the risks section of the

auditor’s report; NRISKSi,t, the number of risks disclosed in the auditor’s report; PERCMATi,t, the

materiality amount in British Pounds divided by total assets; or, LOGMATi,t, the natural

logarithm of the materiality amount.19 All other variables are as defined above.

19 For example, in the report in Appendix A there are two risks disclosed by the auditor (1) Fraud in revenue recognition, and (2) Risk of management override of internal controls. The number of words in the risks section is

17

Audit quality analyses

Our proxy for audit quality in our main analyses is the absolute value of discretionary

accruals. This measure arguably captures audit quality with respect to financial reporting quality,

where higher audit quality is defined as greater assurance that the financial statements faithfully

reflect the firm’s underlying economics conditioned on the financial reporting system and its

innate characteristics (DeFond and Zhang 2014). Moreover, this measure has been extensively

used in prior research on audit quality (e.g., Carcello and Li 2013; Lawrence et al. 2011; Reichelt

and Wang 2010). To examine the effect of the new report on audit quality, we estimate the

following pre-post model:

DACCRi,t = β0 + β1POSTi,t + β2SIZEi,t + β3ROAi,t + β4LEVi,t + β5BIG4i,t

+ β6USLISTi,t + IndustryFE + εi,t (2a)

where for company i in year t, DACCRi,t is absolute discretionary accruals, estimated using the

Jones model including ROA, scaling all variables by average assets.20 The control variables aim

to isolate the effects of client characteristics and have been used in previous research on audit

quality (e.g., Lawrence et al. 2011). All other variables are as defined above.

For our difference-in-differences analyses, using a similar research design as in our audit

fee analyses, we estimate the following model:

the word count of the paragraphs under each risk heading, 92 for the first risk and 90 for the second risk, total 182. The disclosed total materiality is £1.3 million. 20 Discretionary accruals are estimated using an annual cross-sectional model for each SIC-2 digit industry (Kothari et al. 2005) for all the companies on the London Stock Exchange. In order to obtain these companies, we use the WSCOPEUK list from Worldscope for securities on LSE, that are major and primary (EXDSCD = ‘LN’ MAJOR = ‘Y’ and ISINID = ‘P’) and that are not Investment Trusts or Closed-End Funds (TYPE = ‘EQ’). Discretionary accruals are the residual of the following model:

!"##$!,! = ! + !!!"#!,! + !!∆!"#$%!,! + !!!!"!,! + !!,! where for firm ! and year !, !"##$!,! is (income before extraordinary items - cash flow from operations)/average total assets; !"#!,! is (net income before extraordinary items)/average total assets; ∆!"#$%!,! is (!"#$%! −!"#$%!!!)/average total assets; and !!"!,! is gross property, plant, and equipment/average total assets.

18

DACCRi,t = β0 + β1ADOPTERi,t + β2YR2013i,t + β3ADOPTER*YR2013i,t

+ β4SIZEi,t + β5ROAi,t + β6LEVi,t + β7BIG4i,t +β8USLISTi,t

+ IndustryFE + εi,t (2b)

where all variables are as defined above. We also include company fixed effects in models 2a

and 2b and report the results in Section 6. Next, for our cross-sectional analyses we estimate the

following model, using firm-year observations for the two years after the regulatory cut-off:

DACCRi,t = β0 + β1REPORT_DISCLi,t + β2SIZEi,t + β3ROAi,t + β4LEVi,t

+ β5BIG4i,t + β6USLISTi,t + IndustryFE + εi,t

(2c)

where all variables are as defined above.

Analyses of investors’ reaction

Our two proxies for investors’ reaction are (1) the cumulative absolute abnormal returns

surrounding the date of the public distribution of the annual report, which includes the auditor’s

report (i.e., report filing date), and (2) the sum of three-day abnormal trading volume around the

report filing date. Absolute abnormal returns reflect the average change in investors’ belief due

to an announcement event. Abnormal trading volume, in turn, reflects the change in individual

investors’ beliefs (Garfinkel and Sokobin 2006). The later proxy arguably captures not only

information content, but also information asymmetry and investor disagreement regarding new

information. Prior literature suggests that while somewhat positively correlated, the two

measures can be considered largely independent of each other (Bamber and Cheon 1995). Any

given information event can result in high abnormal volume and almost no change in returns and

vice versa (Kandel and Pearson 1995). Thus, using the two measures together increases our

chances of finding an investor reaction to the new auditor’s report. Furthermore, utilizing both

measures is important given the comparatively small size of our sample (Cready and Hurtt

19

2002).

The auditor’s report is included in the release of each company’s full annual report. The

U.K. Companies Act mandates that annual reports must be publicly available. Specifically, DTR

6.3 requires a public announcement when the report is submitted to the National Storage

Mechanism and available for viewing on each company’s website. We search the company

announcements of annual filings using the Regulatory News Service (RNS) of the LSE, as well

as the National Storage Mechanism (NSM).21 The release of the full annual report follows an

earlier earnings announcement disclosure. For the companies in our sample the earnings

announcement is a very complete form of disclosure, containing full financial statements and

mentioning whether the auditor’s opinion was unqualified. Moreover, the current listing rules

require preliminary announcements to be agreed with the auditor prior to publication (FRC

2015). See Appendix C for an illustration about how we identify and calculate daily returns

around the annual report’s public release dates. To examine the effect of the new report on

investors’ reaction, we estimate the following pre-post model:

REACTIONi,t = β0 + β1POSTi,t + β2SIZEi,t + β3ROAi,t + β4LEVi,t + β5USLISTi,t

+ β6IOWNi,t + β7CHNIi,t + β8STDRETi,t + β9MTBi,t + β10BETAi,t

+ IndustryFE + εi,t (3a)

21 For example, see the announcement by ITE Group plc on December 24, 2013 in RNS that the annual report is available at: http://www.londonstockexchange.com/exchange/news/market-news/market-news-detail/11816292. html. The FRC requirements are described in detail at: http://fshandbook.info/FS/html/handbook/DTR/6/3. We could not identify reliable report filing dates in Worldscope, Bloomberg, or other online open sources. We find that the annual report filing dates in Worldscope and Bloomberg often correspond to the earnings release date as per the RNS announcements. The LSE RNS website can be accessed searching each company at: http:// www.londonstockexchange.com/prices-and-markets/markets/prices.htm. The NSM can be accessed searching each company at: http://www.morningstar.co.uk/uk/NSM. An alternative source is the website http://www.investegate.co.uk. For a small number of observations we cannot identify the specific announcement of the release of the annual report. In these cases we use the date of the announcement of the Annual General Meeting (if available), or the date of the Annual General Meeting, as release dates.

20

where for company i in year t, REACTIONi,t is one of two proxies for investors’ reaction,

ABS_ABRETi,t, the value of the sum of the three-day absolute abnormal returns by company,

calculated each day as the company returns = (Price Closet – Price Closet-1)/Price Closet-1 minus

same-day returns for the LSE value-weighted portfolio;22 or, ABVOLi,t, the natural logarithm of

the ratio of the company’s mean event-period volume divided by the company’s mean

estimation-period volume. Event-period volume is daily volume over the two-day event window

beginning on the report filing date, scaled by shares outstanding. Estimation-period volume is

measured over the trading period beginning 61 days before the earnings announcement date and

ending 40 days later (i.e., 21 days before the earnings announcement date);23 IOWNi,t is the

natural logarithm of the number of the company's shares held by institutional investors/total

number of shares outstanding as of the current fiscal year end;24 CHNIi,t is NIBE in year t minus

NIBE in year t-1 scaled by total assets in year t-1; STDRETi,t is the standard deviation of daily

stock returns in year t; MTBi,t is equity market value divided by book value; and, all other

variables are as defined above; and, BETAi,t is the slope coefficient from regressing the daily

return on the company's stock on daily returns of the value-weighed portfolio, over 220 day

period (-250, -21) relative to the filing date of the current year financial statements.

For our difference-in-differences analyses, using a similar research design as in our audit

fee and audit quality analyses, we estimate the following model:

REACTIONi,t = β0 + β1ADOPTERi,t + β2YR2013i,t + β3ADOPTER*YR2013i,t

+ β4SIZEi,t + β5ROAi,t + β6LEVi,t + β7USLISTi,t + β8IOWNi,t

+ β9CHNIi,t + β10STDRETi,t + β11BETAi,t + β12MTBi,t (3b)

22 We calculate market variables by aggregating companies’ individual data. We obtain the constituents of the LSE from WSCOPEUK list from Worldscope for securities on LSE, that are major and primary (EXDSCD = ‘LN’ MAJOR = ‘Y’ and ISINID = ‘P’) and that are not Investment Trusts or Closed-End Funds (TYPE = ‘EQ’). 23 Our measure of abnormal volume is consistent with DeFond et al. (2007) and Miller (2010) 24 We aggregate the percentage as reported by Thomson Reuters where we only exclude ‘Individuals’ from the ownership reported.

21

+ IndustryFE + εi,t

where all variables are as defined above. We also include company fixed effects in models 3a

and 3b and report the results in Section 6. For our cross-sectional analyses we estimate the

following model, using firm-year observations for the two years after the regulatory cut-off:

REACTIONi,t = β0 + β1REPORT_DISCLi,t + β2SIZEi,t + β3ROAi,t + β4LEVi,t

+ β5USLISTi,t + β6IOWNi,t + β7CHNIi,t + β8STDRETi,t + β9BETAi,t

+ β10MTBi,t + IndustryFE + εi,t

(3c)

where all variables are as defined above.

4. SAMPLE SELECTION AND DESCRIPTIVE STATISTICS

Sample selection

Table 1 shows the samples used in our analyses. We start our sample with all 691

companies incorporated in Great Britain, with ordinary stocks listed in the LSE Premium as of

December 31, 2013 and traded in the LSE Main Market.25 We merge this list of companies with

the Thomson Reuters Worldscope database and find 340 non-financial companies with SEDOL

identifiers (i.e., eliminate SIC codes 6000 to 6999). There is a large number of banking,

insurance, trust, and investment companies traded in the LSE Main Market (KPMG 2014). Our

study focuses on non-financial companies similar to prior literature (e.g., Carcello and Li 2013;

Czerney et al. 2014a, 2014b; Seetharaman et al. 2002).26

We read and manually code information from annual reports (e.g., auditor’s report 25 The companies listed in the LSE are available at: http://www.londonstockexchange.com/statistics/companies-and-issuers/companies-and-issuers.htm. We used the list available on April 30, 2015. 26 We identified only three “early” adopters in our sample. Vodaphone Group included an auditor’s report based on the FRC’s exposure draft for fiscal year-end March 31, 2013. Sky plc included an auditor’s report based on the revised FRC standard issued in June 2013 for fiscal year-end June 30, 2013. Ashmore Group included an auditor’s report based on the revised FRC standard issued in June 2013 for fiscal year-end June 30, 2013. Vodaphone Group and Sky plc are included in our sample. For these companies and consistent with the September 2013 cut-off, we considered March 31, 2014 and June 30, 2014 the first regular year of adoption.

22

length; name of audit firm and audit partner; number and description of significant risks of

material misstatement in the auditor’s report; materiality amount; audit fees; and, number and

description of significant accounting issues in the audit committee report). Finally, we

complement our data with financial and returns variables from the Thomson Reuters databases

(Worldscope, Fundamentals and Datastream).

Our main pre-post analyses of audit fees use 1,320 firm-year observations with available

data from two years before (660 observations) and two years after (660 observations) the

regulatory cut-off. In sensitivity analyses we use 1,248 firm-year observations from companies

with data for the full four-year panel. Our differences-in-differences analyses use 664 firm-year

observations that meet the criteria of our research design. There are 126 and 206 companies

reporting six months before and after the regulatory cut-off, also with data in the year prior. Our

cross-sectional analyses of the report length and risk disclosures use 651 firm-year observations

where we could extract the auditor report’s text and count the number of words. Our cross-

sectional analyses of materiality disclosures use 657 firm-year observations.27

Our main pre-post analyses of audit quality use 1,108 firm-year observations with

available data from two years before (568 observations) and two years after (540 observations)

the regulatory cut-off. In sensitivity analyses we use 912 firm-year observations from companies

with data for the full four-year panel. Our differences-in-differences analyses use 572 firm-year

observations that meet the criteria of our research design. There are 110 and 176 companies

reporting six months before and after the regulatory cut-off, also with data in the year prior. Our

cross-sectional analyses of the report length and risk disclosures use 533 firm-year observations

where we could extract the auditor report’s text and count the number of words. Our cross-

27 There are a few cases when the companies do not disclose a specific materiality amount. We code these cases as missing.

23

sectional analyses of materiality disclosures use 537 firm-year observations.

Our main pre-post analyses of investors’ reaction use 1,236 firm-year observations with

available data from two years before (615 observations) and two years after (621 observations)

the regulatory cut-off. In sensitivity analyses we use 1,112 firm-year observations from

companies with data for the full four-year panel. Our differences-in-differences analyses use 610

firm-year observations that meet the criteria of our research design. There are 111 and 194

companies reporting six months before and after the regulatory cut-off, also with data in the year

prior. Our cross-sectional analyses of the report length and risk disclosures use 605 firm-year

observations where we could extract the auditor report’s text and count the number of words.

Our cross-sectional analyses of materiality disclosures use 611 firm-year observations. The main

additional data restrictions compared to our fee analyses are the availability of market data and

identifying the date on which each company’s annual report is available to investors (i.e., filing

date) in the LSE RNS and NSM databases.

5. RESULTS

Audit fee analyses

Table 2, Panel A, reports the descriptive statistics for the variables used in our audit fee

analyses. The mean of AFEESi,t is 13.095 when POSTi,t =1 (untabulated, approximately 486,500

British Pounds in the post adoption period), compared to a mean of 13.014 when POSTi,t =0

(untabulated, approximately 448,600 British Pounds in the pre adoption period). However, the

difference in means between the pre and post adoption periods is not statistically significant (at

the ten-percent level).

The companies in our sample are relatively large, the mean SIZEi,t is 13.554 when POSTi,t

=1 (untabulated, approximately 767 million pounds in assets in the post adoption period). Most

24

of the companies have a Big 4 auditor (mean BIG4i,t = 0.936 when POSTi,t =1). The only

statistically significant differences in means between the pre and post adoption periods are a one-

percent decrease in ROAi,t (significant at the five-percent level), a three-percent increase in

auditor rotation CHAUDi,t (significant at the one-percent level), and a two-percent increase in the

incidence of going concern opinions GCi,t (significant at the five-percent level).

The length of the auditor’s report has increased by approximately two pages under the

new rules (untabulated, approximately 2,400 words in the new reports, compared to 757 words in

the old reports). The new section on risks of material misstatement has on average four risks

(untabulated, approximately 660 words, about 30 percent of the words in the new report). The

average materiality PERCMATi,t is 0.65 percent of total assets (the median is 0.5 percent, or half

of one percent).

Table 2, Panel B, Columns 1 shows coefficients and t-statistics for our pre-post adoption

analyses of audit fees, using data from two years before and two years after the regulatory cut-off

(Model 1a). The coefficient on POSTi,t = 0.038 in Column 1 (statistically significant at the one-

percent level) indicates that fees increased by approximately four percent after the adoption of

the new rules. However, the pre-post analysis doesn’t allow us to rule out a generalized increase

in fees due to other time-varying economic factors besides the adoption of the new report. As

documented in prior studies (Hay et al. 2006), we find that audit fees are positively associated

with client size (SIZEi,t), leverage (LEVi,t), current assets (CURRi,t), number of segments

(NSEGi,t), foreign sales (FORSALESi,t), receiving a going concern opinion (GCi,t), December

fiscal year-ends (DECYEi,t), and U.S. cross-listing status (USLISTi,t).

Table 2, Panel B, Column 2 shows coefficients and t-statistics for our differences-in-

differences analyses, using firm-year observations with fiscal year-end six months before (March

25

to August 2013) and after (September 2013 to February 2014) the regulatory cut-off in

September 2013, as well as the same companies in the prior year (Model 1b, see Section 3 for

additional details). The coefficient on ADOPTER*YR2013i,t = 0.021 in Column 2 (statistically

insignificant at the ten-percent level) does not show a short-term difference-in-differences effect

on audit fees. Hence, the 4 percent increase in the pre-post analysis cannot be entirely attributed

to the change in regulation. Also, one could argue that the “true” cost of complying with the new

audit report model is beyond audit fees. For example, if auditors and clients negotiate and split

compliance work to be done as well as audit fees, the “true” costs of the new rules may not be

directly reflected in audit fees.

Table 2, Panel C documents that audit fees are positively associated with the total length

of the report (Column 1, the coefficient on TOTAL_NWRDSit = 0.420 is statistically significant at

the one-percent level); the length of the risks’ discussion (Column 2, the coefficient on

RISK_NWRDSit = 0.082 is statistically significant at the one-percent level); and, the number of

risks (Column 3, the coefficient on NRISKSit = 0.074 is statistically significant at the one-percent

level). These findings suggest an association between auditor’s effort, or auditor’s risk premium,

and the auditor’s assessment and disclosure of difficult audit issues. In other words, the number

and length of the auditor’s risk disclosures are reflected in audit fees. Although unlikely, the

significantly positive relationship between audit fees and risk disclosure could also be

attributable to the risk premium paid by riskier clients. In contrast, in Table 2, Panel D we do not

find evidence of an association between audit fees and materiality. In Column 1, the coefficient

on PERCMATit = 0.128 and in Column 2 the coefficient on LOGMATit = 0.117 are not

statistically significant at the ten-percent level.28

28 Prior research has documented that client’s risks and materiality are associated with audit fees (Bell et al. 2000; Houston et al. 1999; Pratt and Stice 1994). A comparatively lower level of materiality and greater risk of

26

Audit quality analyses

Table 3, Panel A, reports the descriptive statistics of the data used in our audit quality

analyses. The absolute discretionary accruals for the companies in our sample have a mean of

0.048 in the pre and post adoption period (mean DACCRi,t = 0.048 when POSTi,t =0 and POSTi,t

=1). The only statistically significant difference in means between the pre and post adoption

periods in is a one-percent decrease in ROAi,t (significant at the ten-percent level).

Table 3, Panel B, Column 1 shows coefficients and t-statistics for our pre-post adoption

analyses of audit quality, using data from two years before and two years after the regulatory cut-

off date (Model 2a). The coefficient on POSTi,t = -0.001 in Column 1 (statistically insignificant

at the ten-percent level) indicates that audit quality did not change after the new rules were

adopted. As documented in prior studies (e.g., Kothari et al. 2005), we find that absolute

discretionary accruals are negatively associated with client size (SIZEi,t) and profitability

(ROAi,t). We document similar results for our differences-in-differences analyses (Model 2b) in

Table 3, Panel B, Column 2. The coefficient on ADOPTER*YR2013i,t = -0.007 in Column 2

(statistically insignificant at the ten-percent level) does not show a short-term difference-in-

differences effect on audit quality.

In Table 3, Panel C we do not find evidence of an association between audit quality and

the total length of the report (Column 1, the coefficient on TOTAL_NWRDSit = -0.008 is

statistically insignificant at the ten-percent level); the length of the risks’ discussion (Column 2,

the coefficient on RISK_NWRDSit = -0.003 is statistically insignificant at the ten-percent level);

and, the number of risks (Column 3, the coefficient on NRISKSit = -0.001 is statistically

misstatement can lead to an increase in the resources required to obtain audit evidence, and therefore to an increase in audit fees. Bell et al. (2000) find that the increase in the perceived business risk of the audit engagement results in higher audit fees, through the increase in the billable hours reported by the auditor. Nevertheless, as pointed out by Bell et al. (2000), specific risks cannot be incorporated in the audit fee determination if they cannot be quantified, if they are quantifiable only at the industry level, or if market conditions do not allow for the fees to reflect audit risk.

27

insignificant at the ten-percent level). In Column 1, the coefficient on PERCMATit = 0.034 and in

Column 2 the coefficient on LOGMATit = 0.021 are statistically significant at the one-percent

level. These findings suggest that audit quality decreases (i.e., absolute accruals increase) as

materiality increases.

Investors that are supportive of the new auditor’s report argue that audit judgment (e.g.,

the auditor’s assessment of risks and materiality) can increase the understanding of how audit

firms apply auditing standards and also enable investors to better evaluate the quality of the audit

(FRC 2013). As investors and regulators gain more insight into the audit process, auditors’

incentives to supply audit quality may increase due to a change in their litigation and regulatory

risk. Over time, the disclosures on materiality and risks may change the auditor’s judgments

regarding the amount and type of audit evidence, and therefore, lead to an increase in audit

quality. Contrary to this view, opponents to the new auditor’s report indicate that the new

disclosures may not enhance the understanding of investors because these issues are too complex

to be summarized in the auditor’s report (FRC 2013).

Analyses of investors’ reaction

Table 4, Panel A, reports the descriptive statistics of the data used in our investors’

reaction analyses. The means of ABS_ABRETi,t and ABVOLi,t on the report filing dates are 0.020

and -0.029 when POSTi,t =1, repsectively. The difference in means for the two variables from

the pre to the post period, insignificant at the ten-percent level, suggests that the auditor report is

not more informative to investors following the regulatory changes. The only statistically

significant difference in means between the pre and post adoption periods is a small decrease in

the standard deviation of stock returns (STDRETi,t) and an increase in market-to-book (MTBi,t),

both significant at the one-percent level. Appendix C provides an illustration of daily returns on

28

the dates of the earnings release versus the subsequent public release of the annual report.

Table 4, Panel B, Columns 1 and 3 show coefficients and t-statistics for our pre-post

adoption analyses of investors’ reaction, using absolute abnormal returns and abnormal volume

respectively (Model 3a). The coefficients on POSTi,t = 0.002 in Column 1, and POSTi,t = -0.022

in Column 3, are statistically insignificant at the ten-percent level. Table 4, Panel B, Columns 2

and 4 show coefficients and t-statistics for our differences-in-differences analyses. We do not

find a difference-in-difference effect on investors’ reaction. These combined findings indicate

that investors’ reaction to the auditor’s report content did not change, on average, after the new

rules were adopted.

In Table 4, Panel C we find a weak, negative association between absolute abnormal

returns and the total length of the report and the length of the risk discussion. In Column 1, the

coefficient on TOTAL_NWRDSi,t is -0.007, statistically significant at the ten-percent level; in

Column 2, the coefficient on RISK_NWRDSi,t is -0.003, statistically significant at the five-

percent level. This suggest that abnormal returns around report dissemination are lager for firms

with more concise audit reports. Nevertheless, we do not find evidence of an association between

abnormal volume and the total length of the report, the length of the risks’ discussion, or the

number of risks. Finally, in Table 4, Panel D we do not find an association between investors’

reaction and materiality.29

6. ADDITIONAL AND SENSITIVITY ANALYSES

29 Some research suggests that the disclosure of materiality in the auditor’s report might help reduce the audit expectation gap (De Martinis and Burrowes 1996). However, Houghton et al. (2011) also show in a series of interviews and focus groups that the concept of materiality is not easy to grasp for financial statement users. Users frequently associate materiality with the size of the items being audited instead of the conservatism and costs of the audit. Users also seem to focus more on the quantitative rather than the qualitative aspects of materiality. If investors have trouble in understanding materiality or the materiality threshold is relatively standardized, its disclosure might not produce a market reaction. Finally, materiality should be the maximum level of misstatement that will not affect a reasonable financial statement user. The market may not react to disclosed materiality levels if auditors are setting materiality to an acceptable level (i.e., the market agrees with the auditor’s determination of materiality).

29

Fixed effects, companies with data for the full panel, and bootstrapped standard errors

In order to mitigate the effect of time-invariant client characteristics, we also include

company fixed effects in our pre-post and difference-in-differences models. In our audit fee pre-

post model (1a) we find that the coefficient on POSTi,t is 0.027 (untabulated, statistically

significant at the five-percent level), indicating that audit fees increased by approximately three

percent in the two years after the adoption of the new rules. After including company fixed

effects in our pre-post and difference-in-differences models, we do not find evidence that the

new report had an overall impact on audit quality or investors’ reaction, confirming our main

analyses. Furthermore, in order to isolate auditor “style” and idiosyncratic differences among

audit firms in their reports, we also estimate our pre-post models including auditor fixed effects,

instead of a Big-4 indicator variable, and find similar inferences to those documented in the main

analyses.

We also estimate our pre-post models including only those companies that have data for

the full four-year pre-post period. These analyses are comparatively stricter about using each

company in the pre period as its own control for the post period. In our fee model (1a) we find

that the coefficient on POSTi,t is 0.026 (untabulated, statistically significant at the ten-percent

level), indicating that fees increased by approximately three percent in the two years after the

adoption of the new rules. Also, using observations with four years of data in model (2a), we do

not find evidence that the new report had an overall impact on audit quality. In our investors’

reaction pre-post model (3a), we find that the coefficient on POSTi,t is 0.002 (untabulated,

statistically significant at the ten-percent level) when the dependent variable is absolute abnormal

return, but we find no significant association between POSTi,t and abnormal trading volume.

Thus, our findings on investors’ reaction are in general consistent with our main analyses.

30

Finally, in order to mitigate concerns that our findings are the result of low power, we compute

standard errors for our pre-post and difference-in-differences models using bootstrap with 2,000

replications. We find similar inferences to those documented in the main analyses.

One-year differences pre-post adoption and between the first two years of adoption

In order to isolate one-year changes in the pre-post adoption years, we limit our samples

to the two years around the adoption of the new rules (t and t-1). In our fee model (1a) we find

that the coefficient on POSTi,t is 0.028 (untabulated, statistically significant at the one-percent

level), indicating that fees increased by approximately three percent in the first year after the

adoption of the new rules. We do not find evidence that the new report had an overall one-year

impact on audit quality or investors’ reaction, confirming our main analyses.

In order to compare the two years post adoption (t and t+1), we also estimate a modified

version of our pre-post models. We limit our samples to the post adoption years and include an

indicator variable for the second year of adoption (t+1). We do not find evidence of differences

between the two years post adoption in audit fees, audit quality, or abnormal trading volume, but

we find a significant coefficient for the indicator variable equals to -0.003 (untabulated,

statistically significant at ten-percent level). Finally, we examine the composition and number of

risks in the two years post adoption. We classify individual risks in 16 categories, based on our

interpretation of the main issue by reading the risk headings and disclosures. Table 5 shows the

percentage of companies reporting each risk type in years t and t+1. Revenue recognition is the

predominant risk type, disclosed in 71 and 61 percent of the reports in year t and t+1,

respectively. Risks associated with impairment of goodwill and long-term assets, tax accounting,

and business combinations are also commonly disclosed in the reports. Examining the pair-wise

correlation between risks, we find that some associations are positive and some negative.

31

However, we do not find a clear pattern. The only two risk types that appear often together are

revenue recognition and internal control issues (untabulated, pair-wise correlation is 0.30,

statistically significant at the five-percent level). However, among other risks, correlation

patterns are unclear. The most important change between year t and t+1 is a decrease in the

incidence of including internal control issues. This shift seems to follow concerns about the

boilerplate nature of some risk disclosures (Citi 2014).

The mean number of risks in year t and t+1 is 3.97 and 3.88, respectively (untabulated,

the median is 4 in both years). In order to compare the effect of changes in the number of risks in

the two years post adoption t and t+1, we also estimate a modified version of our cross-sectional

models of the association between NRISKSi,t and audit fees, audit quality, and investors’ reaction

(Models 1c, 2c, and 3c). We limit our samples to the post adoption years and include an indicator

variable for the second year of adoption (t+1), as well as an interaction between the second year

indicator and NRISKSi,t. The interaction coefficient between the second year indicator and

NRISKSi,t in the fee model is 0.049 (untabulated, statistically significant at the one-percent level),

in the audit quality model is 0.004 (untabulated, statistically significant at the ten-percent level),

and in the absolute abnormal returns and abnormal volume models is not statistically significant

(at the ten-percent level). These results indicate that changes in the number of risks year-over-

year can be meaningful in terms of audit fees and audit quality.

Accounting issues disclosed by the audit committee

There were other changes to corporate reporting in the U.K. around the same time, in

particular the changes to the U.K. Corporate Governance Code in October 2012 (FRC 2012b).

These changes require additional disclosures by the audit committee of the board of directors in

the corporate governance section of the annual report. To assess the potential importance of the

32

accounting risks in the audit committee report versus the risks in the auditor’s report, we include

NRISKSi,t the number of risks of material misstatement disclosed in the auditor’s report and also

ACNRISKSi,t the number of risks of material misstatement disclosed in the audit committee’s

report in Models (1c), (2c), and (3c). There is a large degree of overlap between these two

sources of significant risks. In untabulated analyses, the pairwise correlation between NRISKSi,t

and ACNRISKSi,t is 0.54 (statistically significant at the one-percent level). The FRC report

examining the first two years of auditor’s reports (FRC 2016, Table 13) documents that there is

74 and 85 percent overlap in the first and second year of adoption, respectively, on the types of

risk reported by auditors and audit committees. Including both NRISKSi,t and ACNRISKSi,t in our

cross-sectional fee analyses (Model 1c) we find that ACNRISKSi,t is positively associated with

fees (untabulated coefficient 0.036, statistically significant at the five-percent level) and

NRISKSi,t is not associated with audit fees. In our cross-sectional analyses of audit quality and

investor’s reaction (Models 2c and 3c) we do not find statistically significant coefficients (at the

ten-percent level) for NRISKSi,t and ACNRISKSi,t. Overall, it is difficult to conclude whether the

risks in the auditor’s report are more informative than the risks in the report of the Audit

Committee.

Reportable differences to the audit committee in the materiality section

In addition to reporting a materiality amount, companies also disclose a smaller threshold

for reportable issues to the audit committee. For example, in the report in Appendix A

materiality is 1.3 million pounds, but the auditor discloses that any differences over 62,000

pounds will be discussed with the audit committee, as well as misstatements below that amount

that, in the auditor’s view, warrant reporting for qualitative reasons. The correlation between

materiality and reportable differences scaled by total assets is 0.66 (both statistically significant

33

at the one-percent level). In Models (1c), (2c), and (3c), we included both PERCMATi,t the

materiality amount divided by total assets, and PERCREPDIFFi,t the reportable differences

amount divided by total assets. In untabulated analyses, we find a positive association between

PERCMATi,t and discretionary accruals (statistically significant at the five-percent level), but no

association between PERCREPDIFFi,t and audit fees, discretionary accruals, or investors’

reaction.

Additional proxies for audit quality

As an alternative proxy for audit quality, we use the incidence of small earnings as an

inverse proxy for audit quality (Carcello and Li 2013), defined as an indicator variable equal to

one if the change in net income before extraordinary items from year t-1 to year t, scaled by

market value of equity at year t-1, is in the interval [0,0.02], and zero otherwise. We estimate

logistic regression models using the incidence of small earnings as a dependent variable and the

same independent variables as in models (2a), (2b), and (2c), excluding industry fixed effects,

given the low incidence of the small earnings variable (the untabulated mean of this variable in

our pre-post sample is 0.014). In untabulated analyses, using this proxy we do not find evidence

that the new report resulted in changes in audit quality (i.e., pre-post or difference-in-differences

analyses). We do not find an association between this proxy and the length of the report or risk

section. We find a negative association between this proxy and the number of risks and the

length of the risk section (at the five-percent level). We find a positive association between this

proxy and LOGMATi,t, the natural logarithm of the materiality amount (statistically significant at

the ten-percent level).

We also use performance-adjusted (i.e., ROA-matched) discretionary accruals, following

Kothari et al. (2005). In untabulated analyses, using this proxy we do not find evidence that the

34

new report resulted in changes in audit quality (i.e., pre-post or difference-in-differences