FIXED INCOME What’s Next for Private Credit?

6

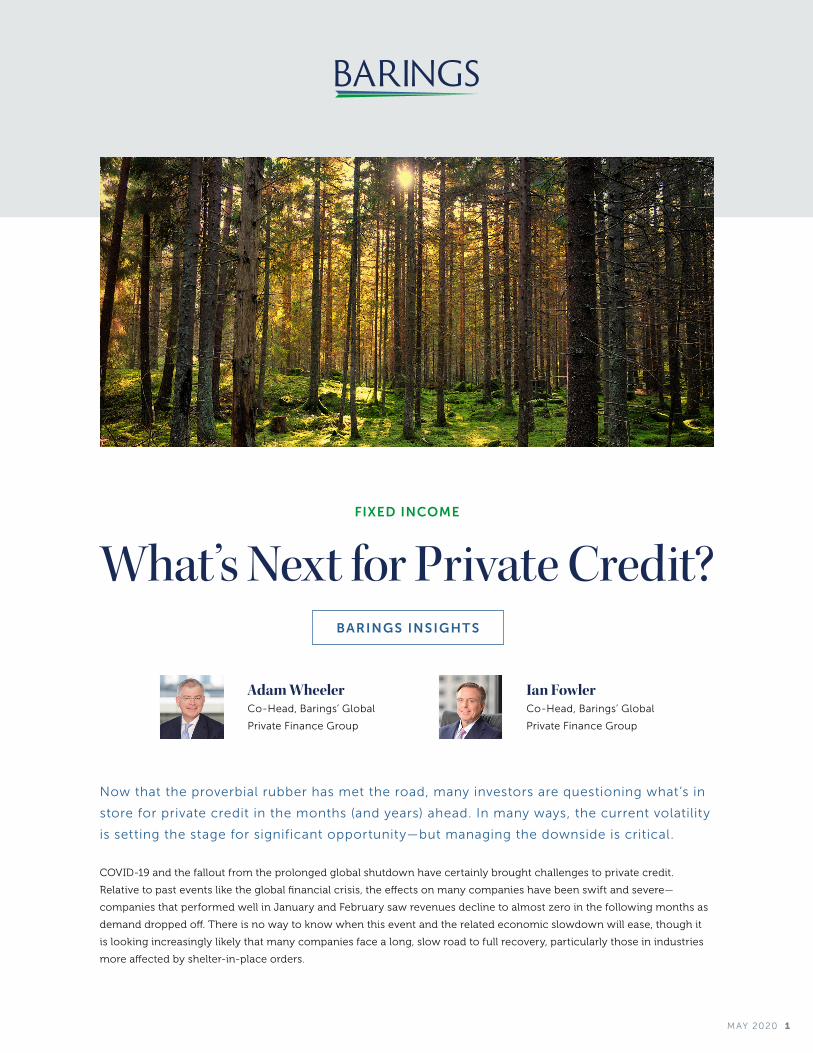

MAY 2020 1 What’s Next for Private Credit? Now that the proverbial rubber has met the road, many investors are questioning what’s in store for private credit in the months (and years) ahead. In many ways, the current volatility is setting the stage for significant opportunity—but managing the downside is critical. COVID-19 and the fallout from the prolonged global shutdown have certainly brought challenges to private credit. Relative to past events like the global financial crisis, the effects on many companies have been swift and severe— companies that performed well in January and February saw revenues decline to almost zero in the following months as demand dropped off. There is no way to know when this event and the related economic slowdown will ease, though it is looking increasingly likely that many companies face a long, slow road to full recovery, particularly those in industries more affected by shelter-in-place orders. BARINGS INSIGHTS FIXED INCOME Adam Wheeler Co-Head, Barings’ Global Private Finance Group Ian Fowler Co-Head, Barings’ Global Private Finance Group

Transcript of FIXED INCOME What’s Next for Private Credit?

MAY 2020 1

What’s Next for Private Credit?

Now that the proverbial rubber has met the road, many investors are questioning what’s in

store for private credit in the months (and years) ahead. In many ways, the current volatility

is setting the stage for significant opportunity—but managing the downside is critical.

COVID-19 and the fallout from the prolonged global shutdown have certainly brought challenges to private credit.

Relative to past events like the global financial crisis, the effects on many companies have been swift and severe—

companies that performed well in January and February saw revenues decline to almost zero in the following months as

demand dropped off. There is no way to know when this event and the related economic slowdown will ease, though it

is looking increasingly likely that many companies face a long, slow road to full recovery, particularly those in industries

more affected by shelter-in-place orders.

BARINGS INSIGHTS

FIXED INCOME

Adam WheelerCo-Head, Barings’ Global

Private Finance Group

Ian FowlerCo-Head, Barings’ Global

Private Finance Group

BARINGS INSIG HT S MAY 2020 2

There are bright spots, to be sure. As an asset class, private credit can offer an opportunity to

invest in high-quality companies through private investments that offer a potential yield premium

relative to the broadly syndicated loan markets—with greater downside protection in the form

of covenants. But some strategies and segments of the market are better positioned to deliver

attractive risk-adjusted returns than others, and the key going forward will be to differentiate those

capable of effectively managing the downside.

For the last several years, we have continued to see the most attractive value in what we consider

the traditional or true middle market—companies with EBITDA between $15 and $50 million. Within

this space, as we mentioned here and here, we see particular value in the more conservative parts

of the capital structure, namely first lien senior debt, with a specific focus on industries that are

truly suitable for illiquid investments, avoiding spaces such as retail, restaurants and oil & gas.

Realizing the Consequences of Late-cycle Style Drift

Today, traditional middle market companies have a potential advantage over their smaller and

larger counterparts. On the one hand, they have greater enterprise value than the lower part of the

middle market1, where loss potential in the event of default tends to be higher as smaller companies

typically have fewer “levers to pull” in the event of financial difficulties. On the other hand, relative

to the upper end of the market2, mid-middle market companies are likely to require less financing

to bridge themselves through shorter-term shocks and periods of deteriorating economic growth.

This sweet spot has also been more insulated in recent years from some of the riskier behavior

exhibited in other parts of the middle market. Over the last several years in particular, we started to

see a degree of late-cycle style drift across private credit more broadly. As more managers raised

larger and larger funds, there was more capital chasing deals in the space (FIGURE 1). Because

capital needs to be deployed over a set time period, typically two to three years, it can be more

efficient to ramp large funds with larger investments in upper middle market companies than to try

and find smaller, more traditional middle market opportunities.

1. Companies with $15 million or less of EBITDA. 2. Companies with EBITDA over $40 million and up to $75–$100 million.

FIGURE 1: Global Private Debt Fundraising Nearly Quadrupled in the Last Decade

SOURCE: Preqin. As of December 31, 2019.

Year of Final Close

Aggregate Capital Raised ($ billion)Number of Funds Closed

Nu

mb

er

of

Fun

ds

Clo

sed

Ag

gre

gate

Cap

ital Raise

d

250

200

150

100

50

0

$140

$120

$100

$40

$20

$0

$80

$60

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

BARINGS INSIG HT S MAY 2020 3

FIGURE 2: Leverage Levels Over Time

SOURCE: Reuters LPC. As of December 31, 2019.

Large Corp. Inst. MM

7.3x

6.8x

5.8x

6.3x

5.3x

4.3x

3.8x2003 2004 2005 2006 2007 2008 2009 2010 20122011 2013 2014 2015 2016 2017 2018 2019

4.8x

HIGHER LEVER AGEIn some cases, the lines with the broadly syndicated market started to blur. Specifically,

leverage levels in some transactions were beginning to resemble those for larger,

broadly syndicated corporates. In fact, total leverage during the last cycle peaked at 5.5x

for U.S. middle market deals, compared to more than 7x for their broadly syndicated

counterparts. Heading into this crisis, middle market leverage, on average, was close to

6.2x, versus roughly 6.8x for large corporates (FIGURE 2). For comparison, leverage on

more traditional first lien senior debt has remained closer to 4.5x. Even at the lower end

of the middle market, while leverage remained low at an absolute level, it was much

higher relative to history.

Additionally, as the popularity of unitranche debt—essentially a hybrid between

senior and mezzanine debt—increased, and competition intensified, leverage

continued to rise as a means of maintaining anticipated returns. This resulted in

deep first-lien debt that had a much higher risk profile than is typical of traditional

senior debt. In some cases, these highly leveraged first lien deals, often marketed

as more conservative senior debt, were actually quite aggressively structured—

and investors weren’t necessarily being compensated for the increased risk they

were taking. In essence, many of these deals looked more akin to “mequity” risk—

or mezzanine/equity risk—given the high leverage and often significant level of

execution risk in converting adjustments to cash.

Ultimately, this can result in very real liquidity issues—and, in fact, already has.

We noted here that the next downturn could very likely be driven by liquidity

challenges, and COVID has not only turned that into reality but also exacerbated

it, with companies across the market experiencing significant cash flow problems.

While measures like the Paycheck Protection Program (PPP) in the U.S. have

provided near-term support that many companies in this space have been able to

take advantage of, the longer-term outlook is far less certain and depends largely on

the longevity and severity of the pandemic.

BARINGS INSIG HT S MAY 2020 4

WE AKER DOCUMENTATIONCompounding this, covenants and structural protections have been diluted in recent

years, meaning that if or when companies encounter liquidity issues, they may not

be well-telegraphed. While covenant-lite transactions aren’t necessarily troubling in

the more liquid broadly syndicated market—as investors have the ability to sell out of

assets more readily—they are a critical part of managing losses in the illiquid private

lending markets. At the most basic level, maintenance covenants give managers the

ability to track the performance of a company to help ensure it is in compliance with

certain performance metrics. They also give lenders a seat at the negotiating table if a

company runs into trouble.

In this capacity, the lack of robust covenant packages can have a material impact

on the severity of defaults and the ultimate recovery values. While weakening

documentation has been widespread across the middle market, it has been most

pronounced in the upper part of the market, where almost 50% of transactions

in recent years were cov-lite, versus 20% in the traditional middle market.3 This,

combined with increased leveraged levels, essentially resulted in liquid assets in an

illiquid wrapper—transactions that were priced and structured in a way that were not

adequately compensating investors for the illiquidity of the private credit market.

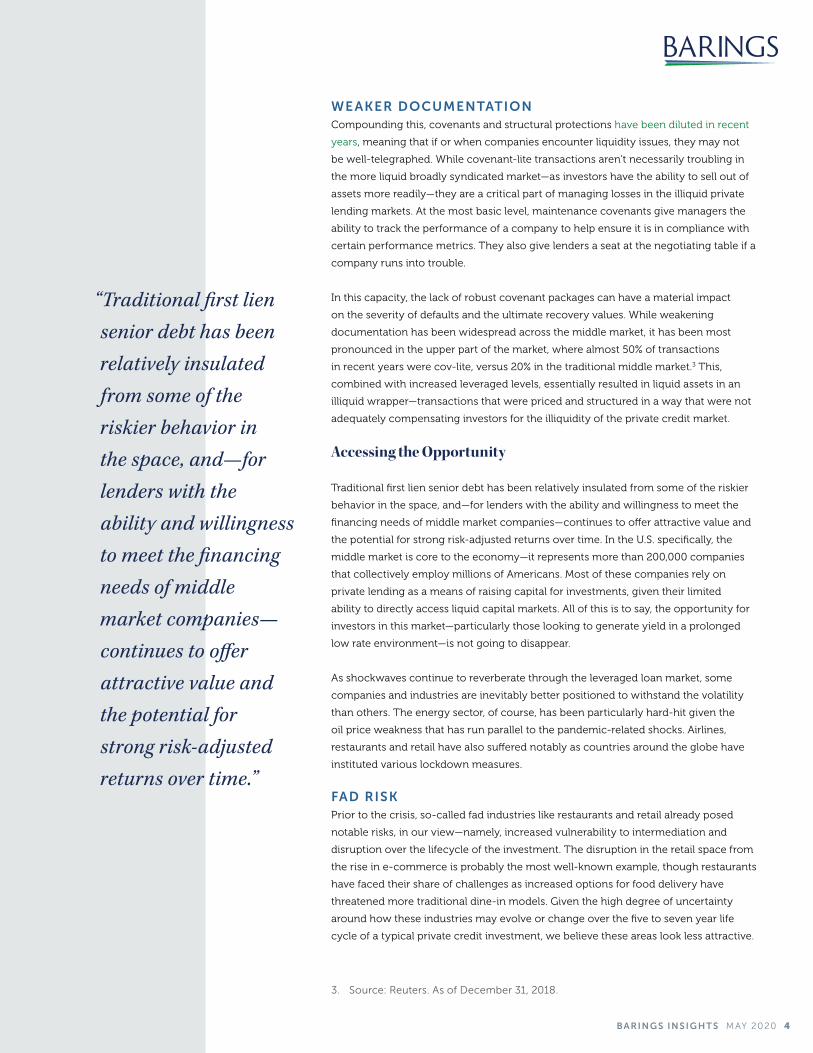

Accessing the Opportunity Traditional first lien senior debt has been relatively insulated from some of the riskier

behavior in the space, and—for lenders with the ability and willingness to meet the

financing needs of middle market companies—continues to offer attractive value and

the potential for strong risk-adjusted returns over time. In the U.S. specifically, the

middle market is core to the economy—it represents more than 200,000 companies

that collectively employ millions of Americans. Most of these companies rely on

private lending as a means of raising capital for investments, given their limited

ability to directly access liquid capital markets. All of this is to say, the opportunity for

investors in this market—particularly those looking to generate yield in a prolonged

low rate environment—is not going to disappear.

As shockwaves continue to reverberate through the leveraged loan market, some

companies and industries are inevitably better positioned to withstand the volatility

than others. The energy sector, of course, has been particularly hard-hit given the

oil price weakness that has run parallel to the pandemic-related shocks. Airlines,

restaurants and retail have also suffered notably as countries around the globe have

instituted various lockdown measures.

FAD RISKPrior to the crisis, so-called fad industries like restaurants and retail already posed

notable risks, in our view—namely, increased vulnerability to intermediation and

disruption over the lifecycle of the investment. The disruption in the retail space from

the rise in e-commerce is probably the most well-known example, though restaurants

have faced their share of challenges as increased options for food delivery have

threatened more traditional dine-in models. Given the high degree of uncertainty

around how these industries may evolve or change over the five to seven year life

cycle of a typical private credit investment, we believe these areas look less attractive.

3. Source: Reuters. As of December 31, 2018.

“Traditional first lien senior debt has been relatively insulated from some of the riskier behavior in the space, and—for lenders with the ability and willingness to meet the financing needs of middle market companies—continues to offer attractive value and the potential for strong risk-adjusted returns over time.”

BARINGS INSIG HT S MAY 2020 5

In our view, dependable and defensive sectors tend to be better positioned to withstand challenges.

Diversification is also critical, as it helps protect the overall performance of a portfolio from weakness in a

few sectors or industries. In addition to fad risks, we also don’t invest in cyclical businesses like oil and gas,

or mining. In fact, 80% of defaults in the leveraged loan market over the last five years were in sectors where

we don’t invest.4 When we think about middle market deals, and the illiquidity in the market, we assume

that we are holding an investment until maturity.

Additionally, the substantial growth of the private credit market over the last decade will naturally

result in more middle market issuers running into stressed situations. And the aforementioned weaker

documentation, higher leverage levels and proliferation of new entrants will likely be key factors

contributing to the growing distressed opportunity in this space.

What’s Next?

The long-term effects of the coronavirus and related economic slowdown are impossible to quantify,

and things may get worse before getting better. However, when it comes to private credit, there are also

potential upsides to volatility, particularly longer-term. For an asset class that has been characterized

in recent years by increasing competition, lack of transparency and a degree of style drift—which as

mentioned above has caused market dynamics to become somewhat distorted—this event will almost

certainly “lift the curtain” to some degree and differentiate those strategies that are built to last.

Indeed, risk management and experience have come to the forefront as managers and investors alike seek

to navigate the challenges facing businesses today—and grapple with the tragic toll the virus has taken

around the world. When it comes to investing in this asset class, deploying capital in the good times is one

thing; managing investments through the tough times is another. And in this environment of heightened

uncertainty, it is critical for investors to partner with managers that have experience managing through the

ups and downs of economic cycles.

The big question today is how long this crisis will last, and whether companies have sufficient liquidity

to endure it. At Barings, we are re-underwriting and stress testing every company we’re invested in to try

and gauge whether it can endure a prolonged low-demand environment. As part of that analysis, we are

differentiating companies that have an immediate need for liquidity from those that may need cash down

the road and/or that ultimately look well-positioned to withstand the crisis.

Despite the current challenges, we believe private credit markets remain attractive, and the asset class has

generated solid risk-adjusted returns over time. When deal flow returns and supply/demand dynamics begin

to normalize, we believe there is a strong likelihood that the post-crisis environment will be more attractive

than that immediately preceding this crisis. Specifically, we think there is a good chance of seeing better

pricing, lower overall leverage and more robust structural protections—creating what may be very favorable

conditions for deploying capital and generating strong risk-adjusted returns for investors. In our view,

managers who have remained focused on the true middle market—and maintained a disciplined approach

rather than chasing yield through higher leverage or looser covenant structures—are best positioned to

endure this near-term shock and capitalize on the longer-term opportunity.

4. Source: S&P. As of December 31, 2018.

IMPORTANT INFORMATION

Any forecasts in this document are based upon Barings opinion of the market at the date of preparation and are

subject to change without notice, dependent upon many factors. Any prediction, projection or forecast is not

necessarily indicative of the future or likely performance. Investment involves risk. The value of any investments

and any income generated may go down as well as up and is not guaranteed by Barings or any other person.

PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS. Any investment results, portfolio

compositions and or examples set forth in this document are provided for illustrative purposes only and are not

indicative of any future investment results, future portfolio composition or investments. The composition, size of,

and risks associated with an investment may differ substantially from any examples set forth in this document. No

representation is made that an investment will be profitable or will not incur losses. Where appropriate, changes

in the currency exchange rates may affect the value of investments. Prospective investors should read the offering

documents, if applicable, for the details and specific risk factors of any Fund/Strategy discussed in this document.

Barings is the brand name for the worldwide asset management and associated businesses of Barings LLC and its

global affiliates. Barings Securities LLC, Barings (U.K.) Limited, Barings Global Advisers Limited, Barings Australia Pty

Ltd, Barings Japan Limited, Baring Asset Management Limited, Baring International Investment Limited, Baring Fund

Managers Limited, Baring International Fund Managers (Ireland) Limited, Baring Asset Management (Asia) Limited,

Baring SICE (Taiwan) Limited, Baring Asset Management Switzerland Sarl, and Baring Asset Management Korea

Limited each are affiliated financial service companies owned by Barings LLC (each, individually, an “Affiliate”).

NO OFFER: The document is for informational purposes only and is not an offer or solicitation for the purchase

or sale of any financial instrument or service in any jurisdiction. The material herein was prepared without any

consideration of the investment objectives, financial situation or particular needs of anyone who may receive it.

This document is not, and must not be treated as, investment advice, an investment recommendation, investment

research, or a recommendation about the suitability or appropriateness of any security, commodity, investment, or

particular investment strategy, and must not be construed as a projection or prediction.

Unless otherwise mentioned, the views contained in this document are those of Barings. These views are made

in good faith in relation to the facts known at the time of preparation and are subject to change without notice.

Individual portfolio management teams may hold different views than the views expressed herein and may make

different investment decisions for different clients. Parts of this document may be based on information received

from sources we believe to be reliable. Although every effort is taken to ensure that the information contained in

this document is accurate, Barings makes no representation or warranty, express or implied, regarding the accuracy,

completeness or adequacy of the information.

Any service, security, investment or product outlined in this document may not be suitable for a prospective

investor or available in their jurisdiction.

Copyright and Trademark

Copyright © 2020 Barings. Information in this document may be used for your own personal use, but may not be

altered, reproduced or distributed without Barings’ consent.

The BARINGS name and logo design are trademarks of Barings and are registered in U.S. Patent and Trademark

Office and in other countries around the world. All rights are reserved.

*As of March 31, 2020

20-1192386

LEARN MORE AT BARINGS.COM

Barings is a $327+ billion* global financial services firm dedicated to meeting the evolving investment and

capital needs of our clients and customers. Through active asset management and direct origination, we provide

innovative solutions and access to differentiated opportunities across public and private capital markets.

A subsidiary of MassMutual, Barings maintains a strong global presence with business and investment

professionals located across North America, Europe and Asia Pacific.