Fixed Income and FX Weekly - Swedbanki/@sbg/@ib/documents/... · Fixed Income and FX Weekly 20...

27

Fixed Income and FX Weekly 20 June, 2011 Norges Bank to signal two more hikes in 2011, but Greece and soft patch dominates markets Bjørn Roger Wilhelmsen Chief Strategist, FX & Fixed Income +47 23 11 62 63 [email protected]

Transcript of Fixed Income and FX Weekly - Swedbanki/@sbg/@ib/documents/... · Fixed Income and FX Weekly 20...

Fixed Income and FX Weekly

20 June, 2011

Norges Bank to signal two more hikes in 2011, but Greece and soft patch dominates markets

Bjørn Roger WilhelmsenChief Strategist, FX & Fixed Income+47 23 11 62 [email protected]

Good morning,

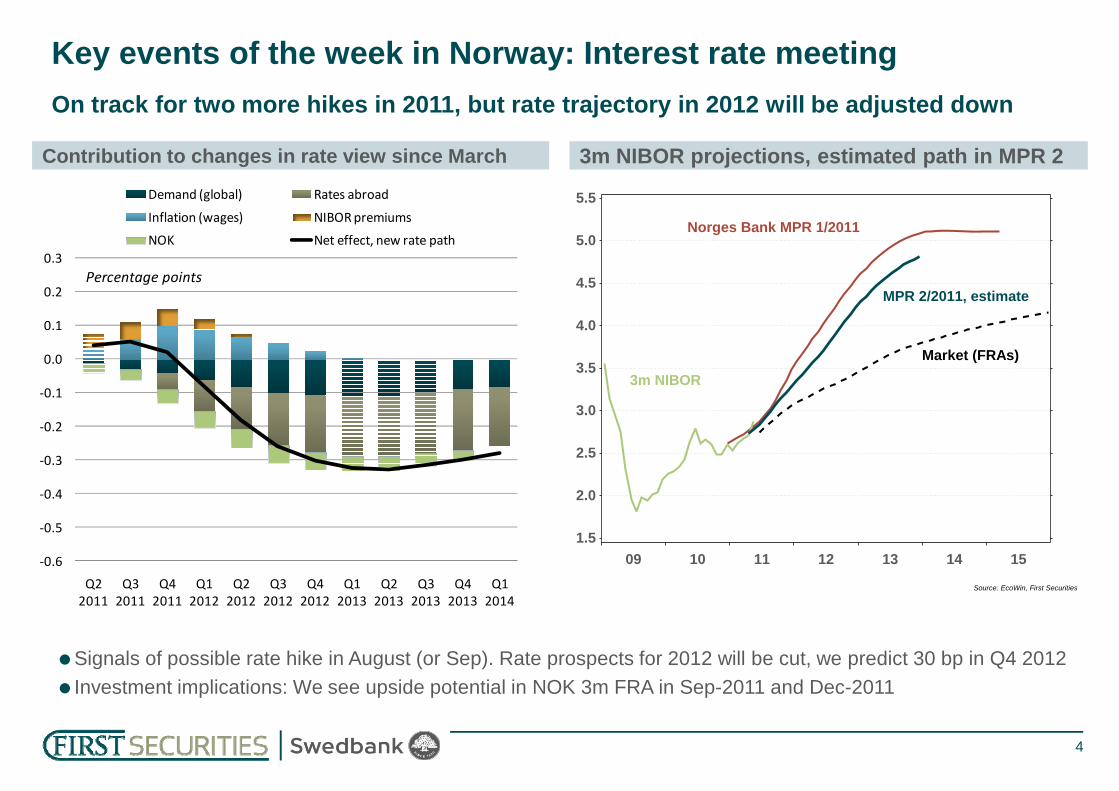

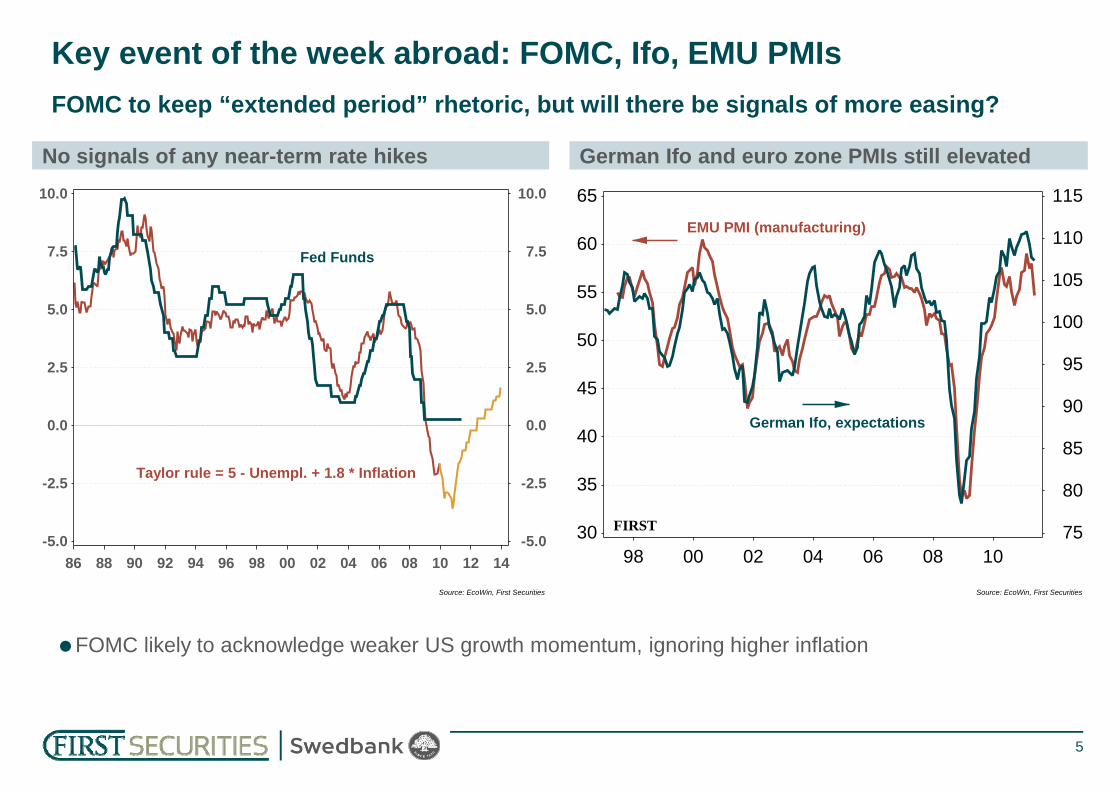

The Norges Bank will almost certainly leave rates on hold on Wednesday this week, but should signal that 25 bpmove in Q3 with a 50-50 split on August and September (instead of September and October in the previous report). A third hike of the year should be penciled in for December, taking the key policy rate to 2.75%. As this is somewhat more hawkish than expectations currently prevailing in the market, front FRAs may increase a little on Wednesday. However, market ‘s developments this week will be dominated by the developments in the Greek debt crisis. Eurozone finance ministers agree to “Vienna plan” – adding funding also from private sources on a voluntary basis. Moreover, indicators of business confidence in the euro zone should provide more information about the extent to which euro area growth is slowing or not. On the other side of the Atlantic, the Federal Reserve will repeat the “extended period” phrase and should acknowledge a weaker US growth momentum, while ignoring higher inflation. Evidence of weaker US growth momentum has lead us to revise our “fair value” estimate on 10 yr US treasury yield to 3.6%, down 40 bp since April. In currency space, we made a substantial change to our forecast for CHFNOK. The CHF strength has been explained as a “safe haven” trade amid the escalation of the euro area sovereign debt crisis. In absent of the old “Deutsche Mark”, investors have preferred to buy CHF as a play on the growth differentials between north and south Europe. The strong correlation between the business cycles in Germany and Switzerland has reinforced the “Deutsche Mark”, investors have preferred to buy CHF as a play on the growth differentials between north and south Europe. The strong correlation between the business cycles in Germany and Switzerland has reinforced the appetite for the Swiss franc. The strong Swiss franc was never expected to be maintained for ever, as business confidence and the exports industry would suffer. However, business confidence and the exports sector have been resilient. This suggests that the CHF overvaluation can be maintained for longer. Another question is to what degree the CHF is overvalued? Looking at the real exchange rate, the CHF has appreciated far less than suggested by developments in the nominal exchange rate. When comparing with Norway, Swiss wage and price inflation has been much lower for decades. This suggests that the “fair value” of CHFNOK should be time varying and at the moment much higher than it was, say, 10 years ago. A rough estimate of the long-term fair value of CHFNOK, based on inflation differentials, is between 5.50 and 6.00. Consequently, a return to 5.00 or below seems unlikely.On balance, we continue to believe that the Swiss franc is somewhat overvalued against the NOK, although not to the same degree as previously though. Looking ahead, the developments in CHFNOK will in particular depend on 1) Developments in the euro area debt crisis; 2) Developments in Swiss business confidence and exports industry. Neither suggests that the CHF is set to depreciate sharply in the near-term.

2

• Key economic events of the week: Norges Bank Board meeting

3

• Fixed Income Strategy: Sep-11 and Dec-11 FRAs may increase after Norges Bank

• FX Strategy: CHFNOK may stay elevated for longer

3m NIBOR projections, estimated path in MPR 2Contribution to changes in rate view since March

On track for two more hikes in 2011, but rate trajectory in 2012 will be adjusted down

Key events of the week in Norway: Interest rate meeting

-0 1

0.0

0.1

0.2

0.3

Demand (global) Rates abroad

Inflation (wages) NIBOR premiums

NOK Net effect, new rate path

Percentage points

3.5

4.0

4.5

5.0

5.5

3.5

4.0

4.5

5.0

5.5

MPR 2/2011, estimate

3m NIBOR

Market (FRAs)

Norges Bank MPR 1/2011

4

-0.6

-0.5

-0.4

-0.3

-0.2

0.1

Q2 2011

Q3 2011

Q4 2011

Q1 2012

Q2 2012

Q3 2012

Q4 2012

Q1 2013

Q2 2013

Q3 2013

Q4 2013

Q1 2014

Source: EcoWin, First Securities

09 10 11 12 13 14 151.5

2.0

2.5

3.0

1.5

2.0

2.5

3.0

Signals of possible rate hike in August (or Sep). Rate prospects for 2012 will be cut, we predict 30 bp in Q4 2012Investment implications: We see upside potential in NOK 3m FRA in Sep-2011 and Dec-2011

German Ifo and euro zone PMIs still elevatedNo signals of any near-term rate hikes

FOMC to keep “extended period” rhetoric, but will there be signals of more easing?

Key event of the week abroad: FOMC, Ifo, EMU PMIs

2.5

5.0

7.5

10.0

2.5

5.0

7.5

10.0

Fed Funds

95

100

105

110

115

45

50

55

60

65

EMU PMI (manufacturing)

5

Source: EcoWin, First Securities

86 88 90 92 94 96 98 00 02 04 06 08 10 12 14-5.0

-2.5

0.0

-5.0

-2.5

0.0

Taylor rule = 5 - Unempl. + 1.8 * Inflation

Source: EcoWin, First Securities

98 00 02 04 06 08 1075

80

85

90

30

35

40

FIRST

German Ifo, expectations

FOMC likely to acknowledge weaker US growth momentum, ignoring higher inflation

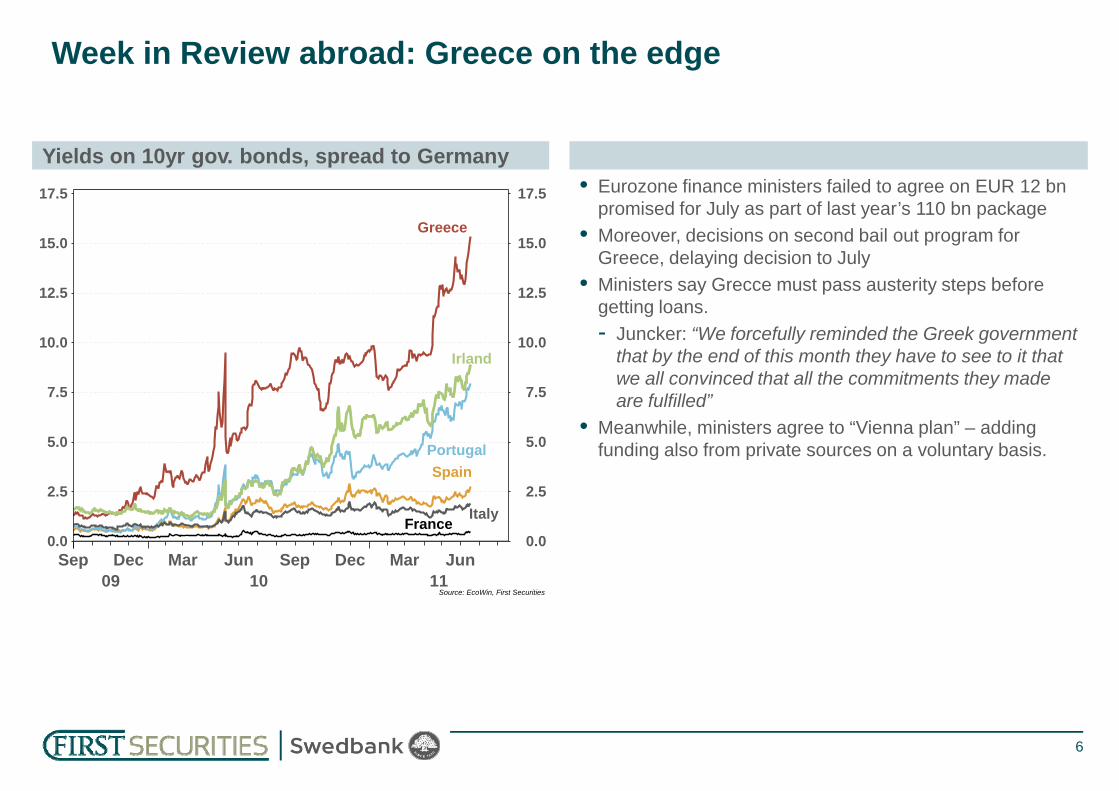

Yields on 10yr gov. bonds, spread to Germany

Week in Review abroad: Greece on the edge

• Eurozone finance ministers failed to agree on EUR 12 bnpromised for July as part of last year’s 110 bn package

• Moreover, decisions on second bail out program for Greece, delaying decision to July

• Ministers say Grecce must pass austerity steps before getting loans.- Juncker: “We forcefully reminded the Greek government

that by the end of this month they have to see to it that we all convinced that all the commitments they made are fulfilled”7.5

10.0

12.5

15.0

17.5

7.5

10.0

12.5

15.0

17.5

Greece

Irland

6

are fulfilled”• Meanwhile, ministers agree to “Vienna plan” – adding

funding also from private sources on a voluntary basis.

Source: EcoWin, First Securities

Sep09

Dec10

Mar Jun Sep Dec11

Mar Jun0.0

2.5

5.0

7.5

0.0

2.5

5.0

7.5

PortugalSpain

ItalyFrance

Will the ISM manufacturing survey drop below 50 in June? Possibly

Week in Review abroad: US economic slowdown continues

US business surveys

-100

10203040

-100

10203040 NY Empire State

ISM model

50

55

60

65

50

55

60

65

Estimate

US business confidence (ISM)

7

Source: EcoWin, First Securities

00 01 02 03 04 05 06 07 08 09 10 11-60-50-40-30-20

-60-50-40-30-20

FIRSTPhil. Fed

Source: EcoWin, First Securities

01 02 03 04 05 06 07 08 09 10 11 12 1330

35

40

45

30

35

40

45 Model

Weaker US growth momentum is a key factor behind the sharp decline in interest rates since April

• Key economic events of the week: Norges Bank Board meeting

8

• Fixed Income Strategy: Sep-11 and Dec-11 FRAs may increase after Norges Bank

• FX Strategy: CHFNOK may stay elevated for longer

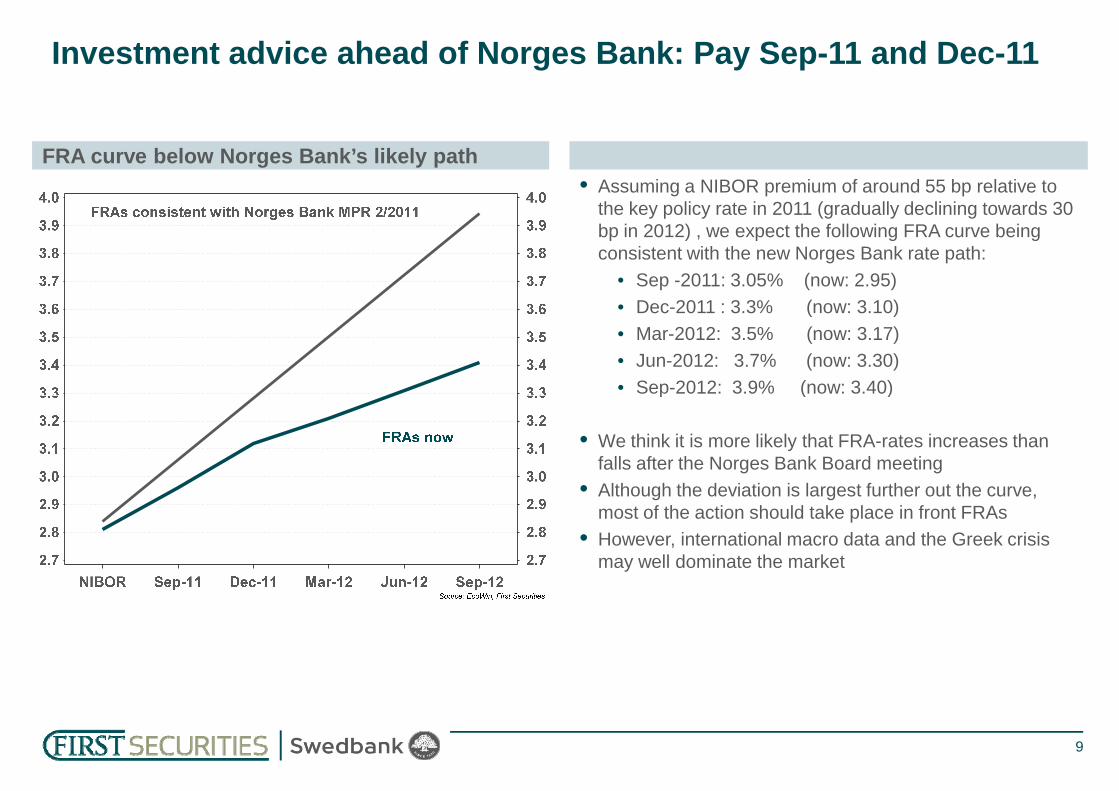

FRA curve below Norges Bank’s likely path

Investment advice ahead of Norges Bank: Pay Sep-11 and Dec-11

• Assuming a NIBOR premium of around 55 bp relative to the key policy rate in 2011 (gradually declining towards 30 bp in 2012) , we expect the following FRA curve being consistent with the new Norges Bank rate path:

• Sep -2011: 3.05% (now: 2.95)• Dec-2011 : 3.3% (now: 3.10)• Mar-2012: 3.5% (now: 3.17)• Jun-2012: 3.7% (now: 3.30)• Sep-2012: 3.9% (now: 3.40)

9

• Sep-2012: 3.9% (now: 3.40)

• We think it is more likely that FRA-rates increases than falls after the Norges Bank Board meeting

• Although the deviation is largest further out the curve, most of the action should take place in front FRAs

• However, international macro data and the Greek crisis may well dominate the market

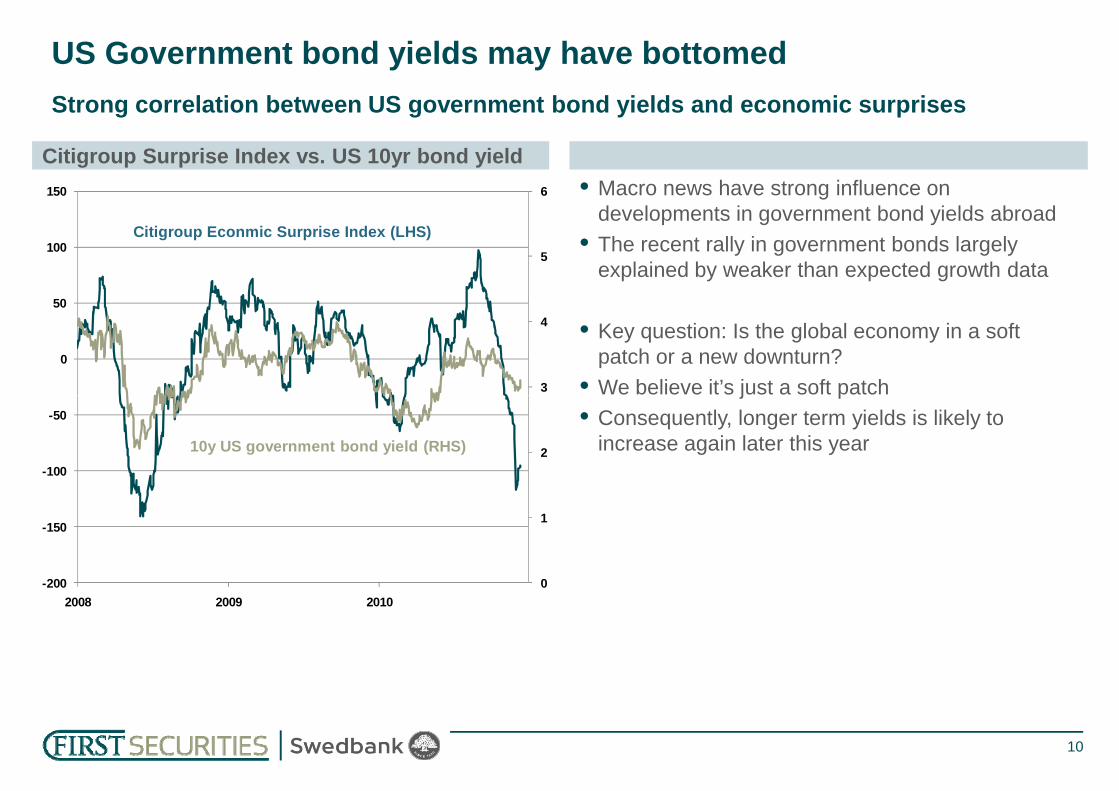

Citigroup Surprise Index vs. US 10yr bond yield

Strong correlation between US government bond yields and economic surprises

US Government bond yields may have bottomed

• Macro news have strong influence on developments in government bond yields abroad

• The recent rally in government bonds largely explained by weaker than expected growth data

• Key question: Is the global economy in a soft patch or a new downturn?

• We believe it’s just a soft patch3

4

5

6

0

50

100

150

Citigroup Econmic Surprise Index (LHS)

10

• We believe it’s just a soft patch• Consequently, longer term yields is likely to

increase again later this year

0

1

2

-200

-150

-100

-50

2008 2009 2010

10y US government bond yield (RHS)

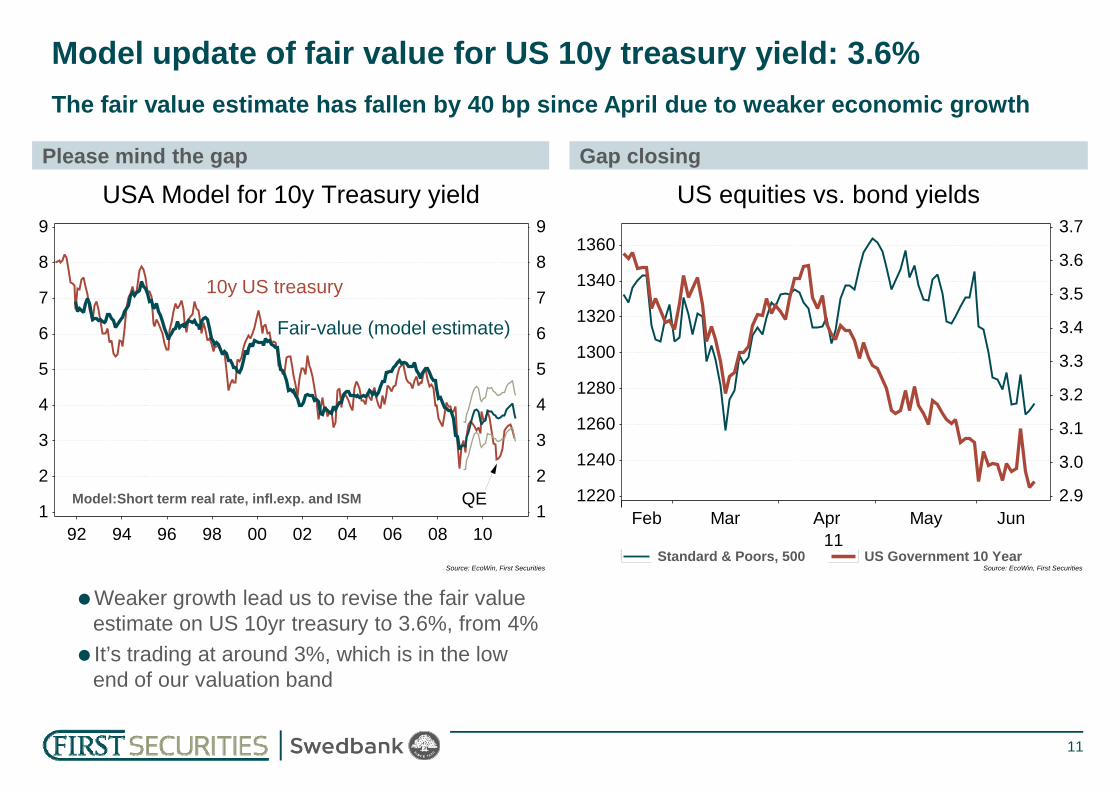

Gap closingPlease mind the gap

The fair value estimate has fallen by 40 bp since April due to weaker economic growth

Model update of fair value for US 10y treasury yield: 3.6%

USA Model for 10y Treasury yield

5

6

7

8

9

5

6

7

8

9

10y US treasury

Fair-value (model estimate)

US equities vs. bond yields

3 2

3.3

3.4

3.5

3.6

3.7

1280

1300

1320

1340

1360

11

Source: EcoWin, First Securities

92 94 96 98 00 02 04 06 08 101

2

3

4

1

2

3

4

QEModel:Short term real rate, infl.exp. and ISM

Standard & Poors, 500 US Government 10 YearSource: EcoWin, First Securities

Feb11

Mar Apr May Jun2.9

3.0

3.1

3.2

1220

1240

1260

Weaker growth lead us to revise the fair value estimate on US 10yr treasury to 3.6%, from 4%It’s trading at around 3%, which is in the low end of our valuation band

Interest rate yield curves, swapsNOKSEK box 2-10 yr, interest rate swaps

p/l + 15 bp since inception

Trade update: NOKSEK box in 2-10 performing well

2.5

3.0

3.5

4.0

4.5

2.5

3.0

3.5

4.0

4.5 NOK

SEK

EURUK-50

-25

0

25

50

75

-50

-25

0

25

50

75

12

Trade details: Pay NOK 2y and SEK 10y, receive SEK 2y and NOK 10yCase: The slope of the yield curve in Norway is too steep vs. the Swedish curveTrade opened at +40 on 29.March for a target of -10. Now trading at +25

Source: EcoWin, First Securities1y 2y 3y 4y 5y 6y 7y 8y 9y 10y

0.5

1.0

1.5

2.0

0.5

1.0

1.5

2.0

Source: EcoWin, First Securities

00 01 02 03 04 05 06 07 08 09 10 11-175

-150

-125

-100

-75

-175

-150

-125

-100

-75

10 yr Norway asset swap spread and crisis

p/l + 5 bp since inception

Trade update (II): Swap spread contraction performing well too

75

100

125

150

75

100

125

150Mexico crisis

Russian crisis

Global Fianancial Crisis

EZ debt crisis

10 yr Norway asset swap spread

85

90

95

100

105

85

90

95

100

105Basis points

13

Source: EcoWin, First Securities

94 96 98 00 02 04 06 08 10 12 140

25

50

0

25

50

Source: EcoWin, First Securities

Jan11

Feb Mar Apr May Jun65

70

75

80

65

70

75

80

Trade opened at +98 for a target of +65 bpNow trading at +93

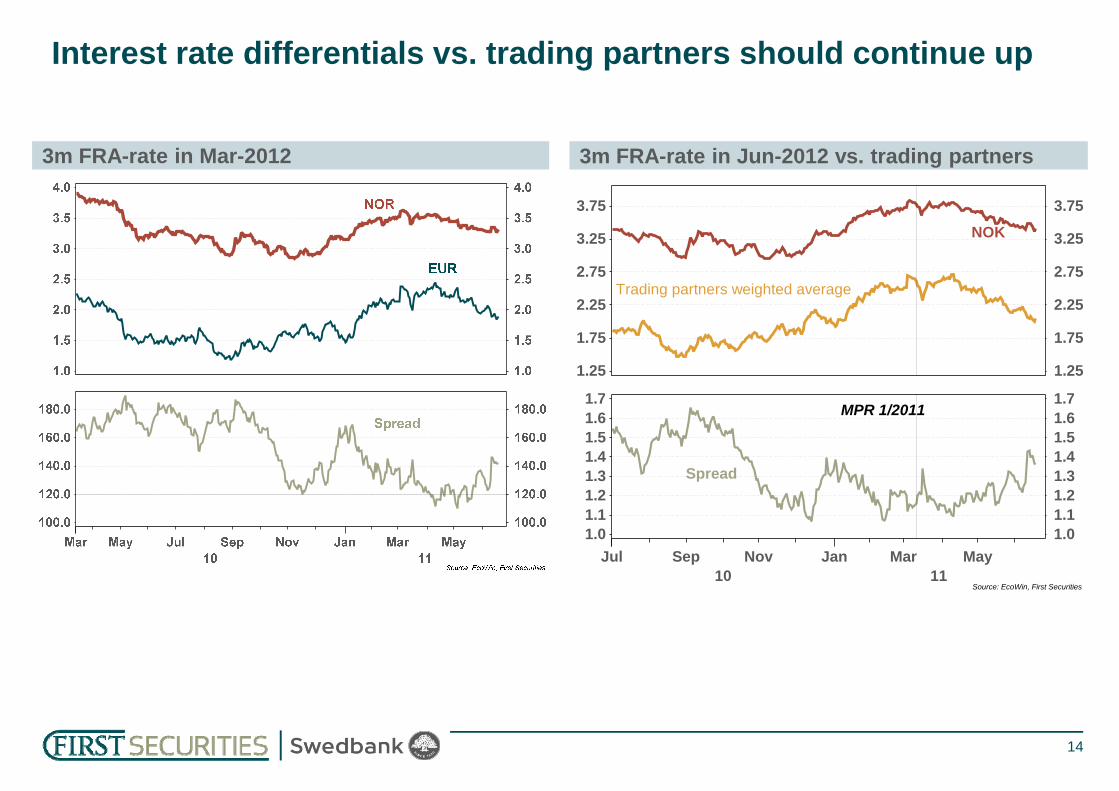

3m FRA-rate in Jun-2012 vs. trading partners3m FRA-rate in Mar-2012

Interest rate differentials vs. trading partners should continue up

1 71 7

1.25

1.75

2.25

2.75

3.25

3.75

1.25

1.75

2.25

2.75

3.25

3.75

NOK

Trading partners weighted average

14

Source: EcoWin, First Securities

Jul10

Sep Nov Jan11

Mar May1.01.11.21.31.41.51.61.7

1.01.11.21.31.41.51.61.7

Spread

MPR 1/2011

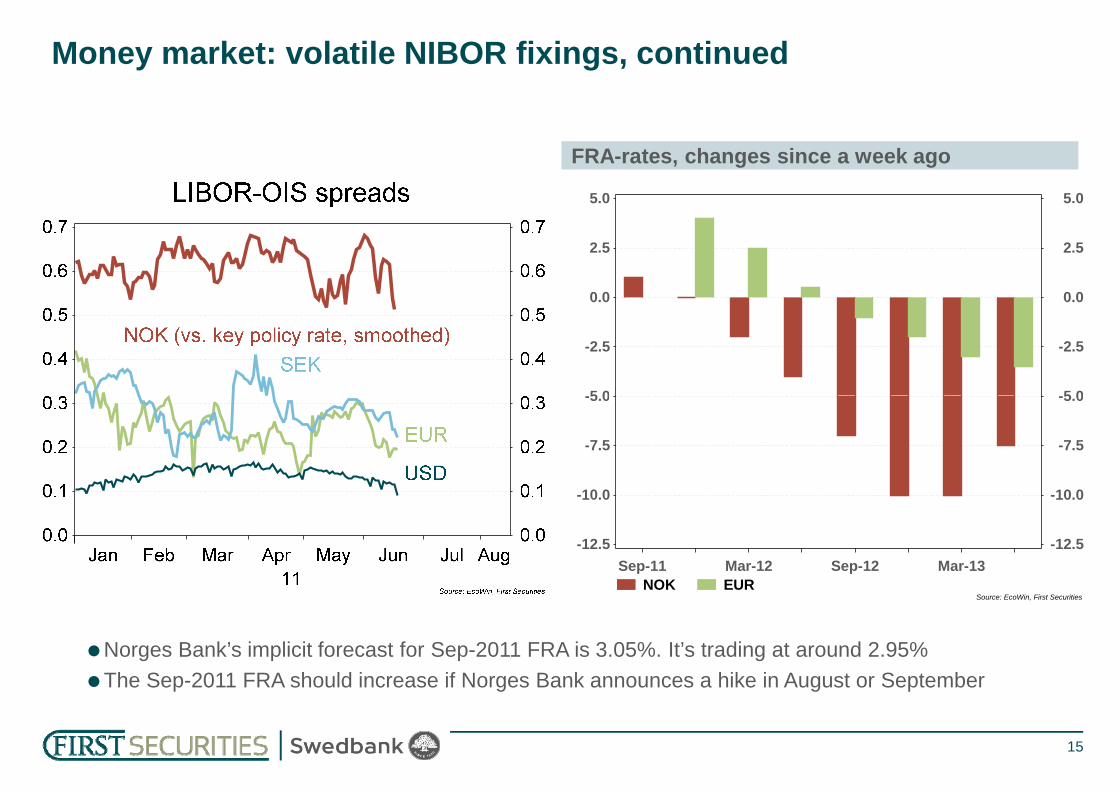

Money market: volatile NIBOR fixings, continued

FRA-rates, changes since a week ago

5 0

-2.5

0.0

2.5

5.0

5 0

-2.5

0.0

2.5

5.0

15

Norges Bank’s implicit forecast for Sep-2011 FRA is 3.05%. It’s trading at around 2.95%The Sep-2011 FRA should increase if Norges Bank announces a hike in August or September

NOK EURSource: EcoWin, First Securities

Sep-11 Mar-12 Sep-12 Mar-13-12.5

-10.0

-7.5

-5.0

-12.5

-10.0

-7.5

-5.0

NOK interest rate swap, yield curve2-5-10 fly vs. 1y interest rate swap

5 yr segment has outperformed 2yr and 10 yr

Trade on watch list: Pay 5 yr segment vs. wings

16

The 2-5-10 fly should trade at 25-30 bp when short-term rates are low and when Norges Bank has embarked on an hiking cycle. The 2-5-10 fly is currently detached from the 1y IRSTrade idea to watch: Pay 5 yr vs 2y and 10yEntry target: -5 bp

• Key economic events of the week: Norges Bank Board meeting

17

• Fixed Income Strategy: Sep-11 and Dec-11 FRAs may increase after Norges Bank

• FX Strategy: CHFNOK may stay elevated for longer

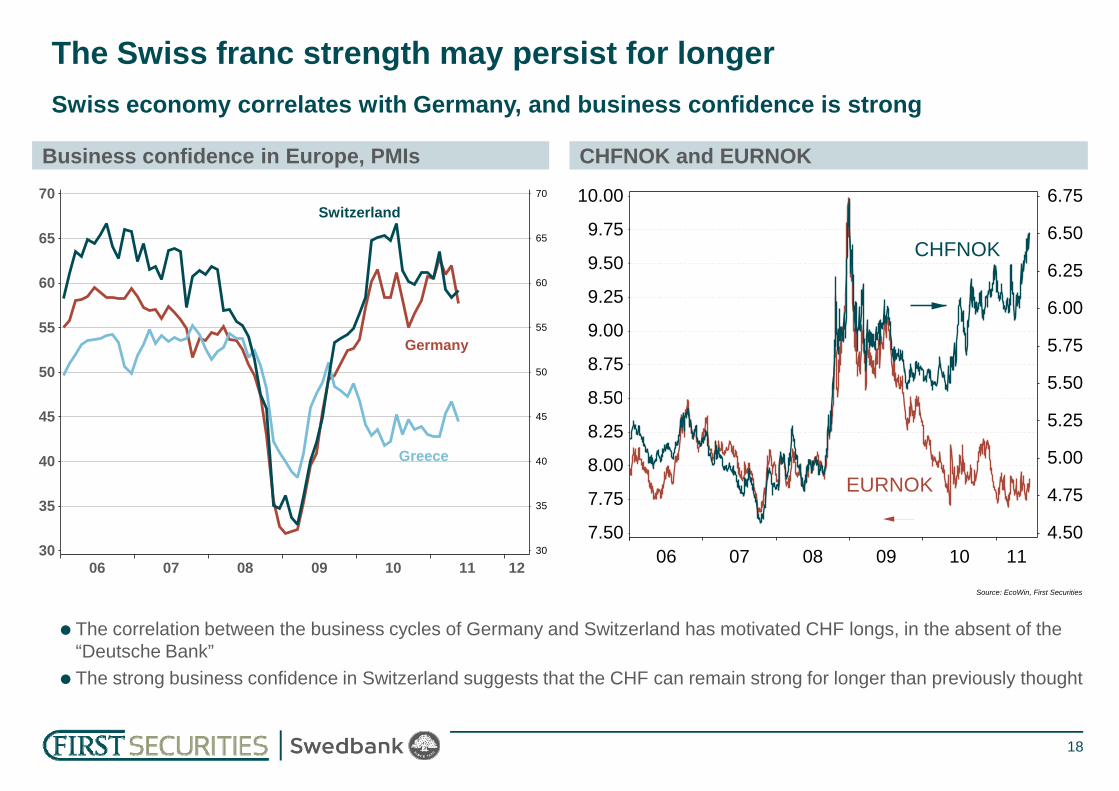

CHFNOK and EURNOKBusiness confidence in Europe, PMIs

Swiss economy correlates with Germany, and business confidence is strong

The Swiss franc strength may persist for longer

50

55

60

65

70

50

55

60

65

70Switzerland

Germany

5.50

5.75

6.00

6.25

6.50

6.75

8 50

8.75

9.00

9.25

9.50

9.75

10.00

CHFNOK

18

06 07 08 09 10 11 1230

35

40

45

30

35

40

45

Greece

Source: EcoWin, First Securities

06 07 08 09 10 114.50

4.75

5.00

5.25

7.50

7.75

8.00

8.25

8.50

EURNOK

The correlation between the business cycles of Germany and Switzerland has motivated CHF longs, in the absent of the “Deutsche Bank”The strong business confidence in Switzerland suggests that the CHF can remain strong for longer than previously thought

Current account balance, % of GDPExports of goods, constant prices (2002 = 100)

Is the strong CHF a problem for the exports industry? Apparently not

120

130

140

150

160

120

130

140

150

160Germany

Switzerland

Norway

Per

cent

19

Source: EcoWin, First Securities

02 03 04 05 06 07 08 09 10 11 1290

100

110

120

90

100

110

120Greece

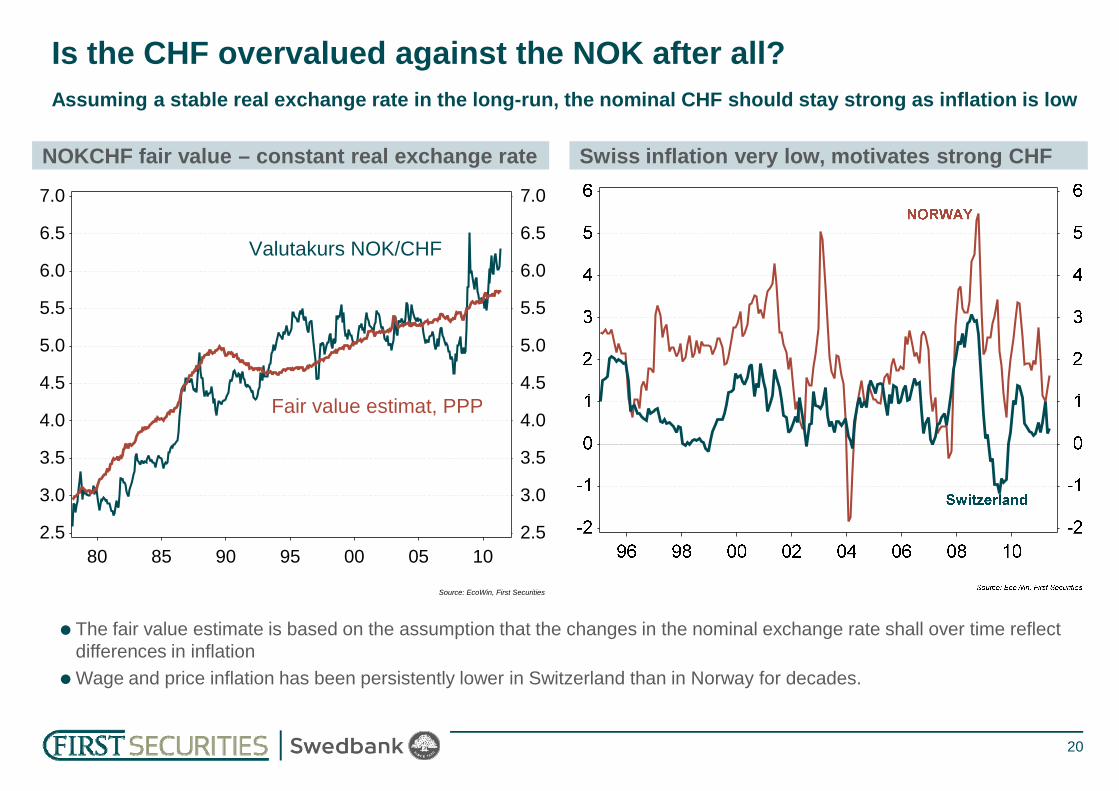

Swiss inflation very low, motivates strong CHFNOKCHF fair value – constant real exchange rate

Assuming a stable real exchange rate in the long-run, the nominal CHF should stay strong as inflation is low

Is the CHF overvalued against the NOK after all?

4.5

5.0

5.5

6.0

6.5

7.0

4.5

5.0

5.5

6.0

6.5

7.0

Valutakurs NOK/CHF

20

Source: EcoWin, First Securities

80 85 90 95 00 05 102.5

3.0

3.5

4.0

2.5

3.0

3.5

4.0Fair value estimat, PPP

The fair value estimate is based on the assumption that the changes in the nominal exchange rate shall over time reflect differences in inflationWage and price inflation has been persistently lower in Switzerland than in Norway for decades.

EURNOK now trading at 200 day moving average

EURNOK should continue to range trade 7.70/75 – 7.95

EURNOK, important levels7.67.77.87.98.08.18 2

7.67.77.87.98.08.18 2

7.70

7.95

21

Source: EcoWin, First Securities

Jan10

Apr Jul Oct Jan11Apr

8.28.38.48.58.68.7

8.28.38.48.58.68.7

200 day moving average (now 7.91)

8.20

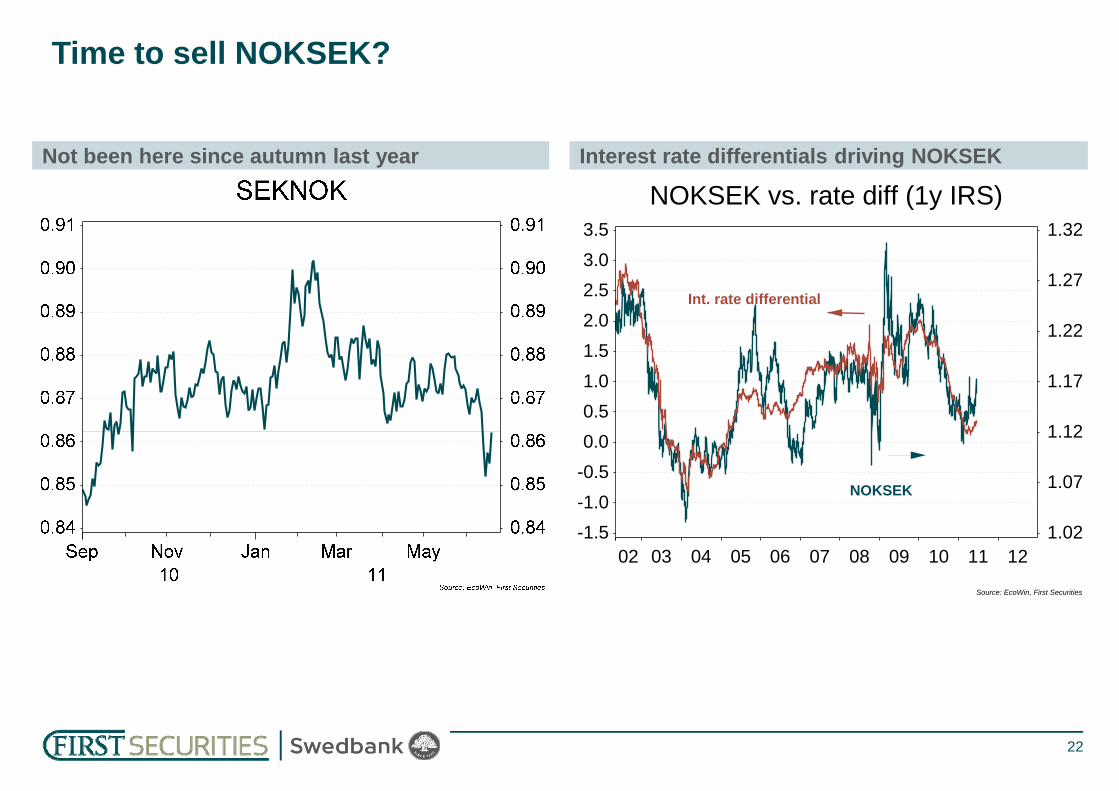

Interest rate differentials driving NOKSEKNot been here since autumn last year

Time to sell NOKSEK?

NOKSEK vs. rate diff (1y IRS)

1.17

1.22

1.27

1.32

1.01.52.02.53.03.5

Int. rate differential

22

Source: EcoWin, First Securities

02 03 04 05 06 07 08 09 10 11 121.02

1.07

1.12

-1.5-1.0-0.50.00.5

NOKSEK

Oil price and NOK TWINOK TWI and interest rate differentials

Interest rate differentials signals weaker NOK, but commodity prices signals stronger

Short-term NOK drivers: Mixed signals

90.0

92.5

95.0

97.5

100.0

102.51.25

1.50

1.75

2.00

2.25NOK TWI i-44 (inverted)

23

Source: EcoWin, First Securities

08 09 10 11

105.0

107.5

110.0

112.50.25

0.50

0.75

1.00

2 y rate spread to trading partners

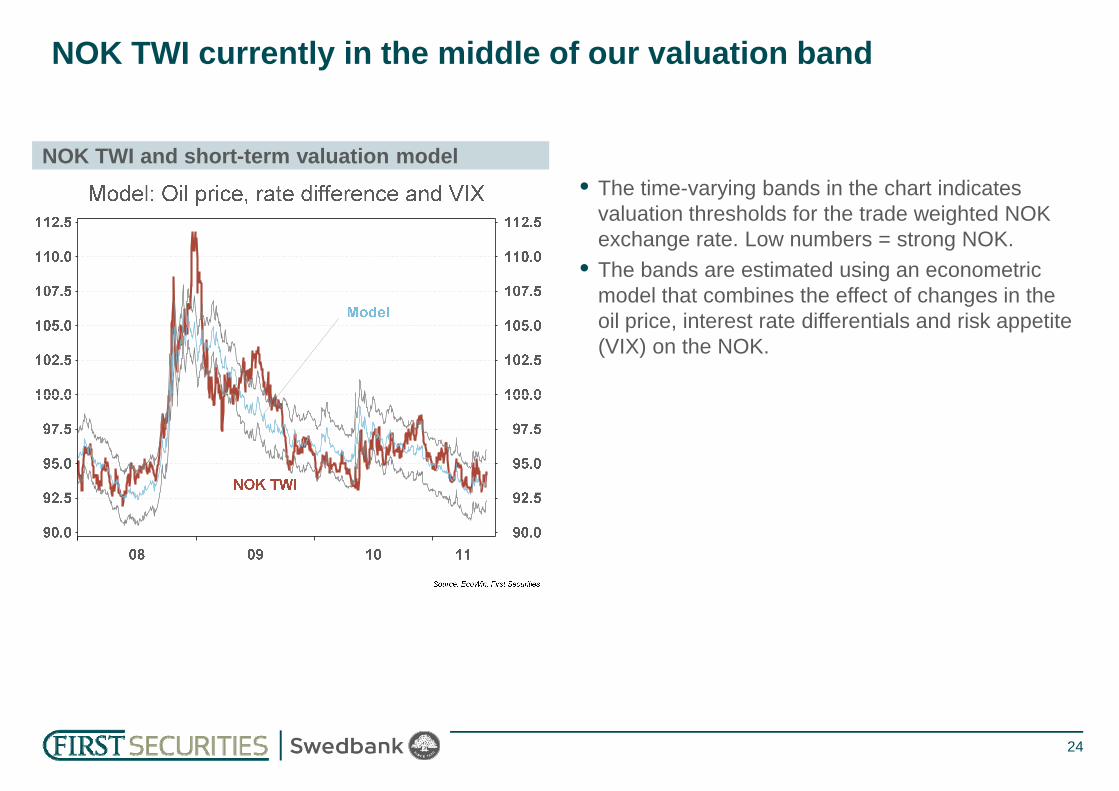

NOK TWI and short-term valuation model

NOK TWI currently in the middle of our valuation band

• The time-varying bands in the chart indicates valuation thresholds for the trade weighted NOK exchange rate. Low numbers = strong NOK.

• The bands are estimated using an econometric model that combines the effect of changes in the oil price, interest rate differentials and risk appetite (VIX) on the NOK.

24

FX forecast table

3m forecast 12m forecast14/6/11 Change Change Change Spot Change Spot Change Trade

last week last month in 2011 forecast in % forecast in % WeightsEURNOK 7.816 -0.3% -0.9% 0.3% 7.75 -0.8% 7.70 -1.5% 0.39SEKNOK 0.859 -1.1% -2.0% -0.9% 0.88 2.5% 0.85 -1.5% 0.21GBPNOK 8.880 1.0% -1.6% -5.6% 8.7 -1.5% 9.5 6.8% 0.09

25

GBPNOK 8.880 1.0% -1.6% -5.6% 8.7 -1.5% 9.5 6.8% 0.09DKKNOK 1.048 -0.3% -1.0% -5.9% 1.04 -0.7% 1.03 -1.4% 0.08USDNOK 5.403 0.5% -3.1% -7.2% 5.24 -3.1% 5.58 3.3% 0.06JPYNOK 6.720 0.1% -2.4% -5.3% 6.31 -6.1% 6.20 -7.7% 0.03CHFNOK 6.465 0.3% 3.7% 3.6% 6.20 -4.1% 5.70 -11.8% 0.01

TWI 94.0 -0.3% -1.4% -1.7% 93.8 -0.2% 93.7 -0.3%

Forecast table, Norway

Norway - forecast tableChange y/y, average 2010 2011 2012 2013GDP Mainland (ex. oil & ship) 2.1 2.8 3.7 3.0Private consumption 3.7 3.3 4.1 4.0Mainland investments -3.1 5.5 7.9 7.4

26Source:

Oil sector investments -12.4 10.0 8.0 4.0Exports, goods, mainland 4.9 5.6 4.9 4.0Imports 9.0 5.6 6.1 5.3

This document was prepared exclusively for the benefit and internal use of selected parties in order to evaluate the feasibility of a possible transaction or transactions and does not carry any right of publication or disclosure to any other party. This document is incomplete without reference to, and should be viewed solely in conjunction with, the oral briefing provided by First Securities AS. This presentation may not be used for any other purposes without the prior written consent of First Securities AS. This presentation is not prepared in accordance with the requirements applying to investment researches.This document does not constitute or form part of an offer or invitation or recommendation to subscribe for or purchase any securities. The distribution of this document may be restricted by law in certain jurisdictions and person into whose possession this document comes should inform themselves about, and observe, any such restriction. Any failure to comply with these restrictions may constitute a violation of the laws of any such jurisdiction. First Securities AS shall not have any responsibility for any such violations. Any decision to purchase or subscribe for securities in

27

any responsibility for any such violations. Any decision to purchase or subscribe for securities in any offering must be made solely on the basis of the information contained in the prospectus or other offering circular issued in connection with such offering. In preparing this document we have relied upon and assumed, without independent verification, the accuracy and completeness of all information available from public sources or which was provided to us or otherwise reviewed by us. The information contained in this document has been taken from sources deemed to be reliable. We do not represent that such information is accurate or complete and it should not be relied on as such. Any opinions expressed herein reflect our judgement at this date, all of which are accordingly subject to change. First Securities AS accept no liability whatsoever for any direct, indirect or consequential loss rising from the use of this document or its contentsFirst Securities AS and/or their employees may hold shares, options or other securities of any issuer referred to in this document and may, as principal or agent, buy or sell such securities. First Securities AS may have other financial interests in transactions involving these securities.

![Online Change of Address Form - College Savings Bank · FX]M: Messages FX]M: View Cust... Snapshot Online Banking - Fixed Rate CD A Pane Window First time Welcome Cherie Smith Last](https://static.fdocuments.in/doc/165x107/6003639720ab206ac9632407/online-change-of-address-form-college-savings-bank-fxm-messages-fxm-view-cust.jpg)