Fiscal Reform in Indonesia - mof.go.jp · Indonesia’s neighbors •Total infrastructure...

35

Fiscal Reform in Indonesia Mohamad Ikhsan University of Indonesia

Transcript of Fiscal Reform in Indonesia - mof.go.jp · Indonesia’s neighbors •Total infrastructure...

Fiscal Reform in IndonesiaMohamad Ikhsan

University of Indonesia

Presentation Structure

What is an Inclusive Fiscal Policy

Why inclusive fiscal reform needed

Is Indonesia’s fiscal policy inclusive?

Why Indonesia fiscal policy not inclusive?

How to make Indonesia fiscal policy to be more inclusive

Inclusive fiscal policy

Most of studies emphasize on distributive aspect of fiscal policy.

I would prefer to use a broader definition or scope of fiscal policy.

My inclusive fiscal policy should satisfy all three fiscal policy function ala Musgrave and Musgrave:

Allocation function to support growth

There are a strong correlation between growth and poverty. A reduction of poverty need an economic expansion. Hence, a better and efficient budget allocation [both from tax structure and spending] will lead to economic growth and a stronger impact on poverty reduction.

Distributive function

Stabilization function

A countercyclical budget would help the whole economic agents to smooth their consumption and to have a better business environment their planning. The poor would get more benefit because they lack of tools of protection against shocks and fluctuation [low saving and or no access to the insurance market]

For resource rich country like Indonesia: stabilization function is essential for meeting national aspiration

Aspiration of the country Greater national prosperity

Improved access to essential services and human development

Population safe and secure from poverty and “insecurities”

Realizing these aspirations is not possible if: GDP growth is volatile

Macroeconomic instability is frequent

Public spending in priority development areas is volatile

Resource‐rich countries face particular challenges Price of main exports volatile in global markets (booms and busts)

Foreign reserves and/or the exchange rate tend to follow boom and bust cycles

Government revenues directly affected by these cycles

Government revenues indirectly affected as private spending is squeezed

Solution: establishing a sound fiscal framework.

4

Stabilization matters for resource rich country

‐15%

‐10%

‐5%

0%

5%

10%

15%

1970

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

Why inclusive fiscal reform needed?

Need a 6+ % p.agrowth rate to :1.create 1,8 m new

entrants 1% growth = 250

k - 300 k jobs2.To reduce poverty

to below 10% and near poor and vulnerable to below 30% of population

1997‐1999:Asian Financial

Crisis

1974 1st Oil Boom

1979 2nd Oil Boom

Global Oil

Shock

First Structural Reform

1988 ‐ 1996: High Growth

periodGlobal

Saving Glut

2008 – 2009:Global Financial Crisis

2012 ‐ sekarangWeakening commodity price;

Rebalancing of china economy;US normalization;

Global Political Uncertainy

before AFC 1998‘70 – ’97 : 7,2% p.a

Sumber: BPS, BKF diolah

’02 – ’16 : 5,5% p.a

To support growth

Indonesia’s Growth Episodes

5

Despite improvement, poverty reduction decelerates while inequality increases 6

‐1.5

‐1

‐0.5

0

0.5

1

1.5

2

2.5

02468101214161820

Poverty Rate (LHS)

Change in Poverty, yoy (RHS)

‐1.5‐1‐0.500.511.522.533.5

20

25

30

35

40

45yoy change Gini

Poverty reduction in 2016, though greater than in recent years, remains slower than before 2011.

The Gini coefficient in 2016 dropped below 40 for the first time since 2011.

• In order to continue the acceleration of poverty reduction and sustain the trend of falling inequality, improvements in fiscal policy are needed.

• In particular, Indonesia must spend more on the programs that are most cost‐effective at reducing inequality, such as direct transfers to poor and vulnerable households

Note: 2011‐2016 uses March Susenas data

How inclusive Indonesia’s fiscal policy recently?

• During the good times, spending mostly allocated to energy subsidy leaving capital and social spending low.

Excluding transfers, personnel is now the largest CG spending category, followed by goods and services and then capital

9

Economic composition of public spending by level of government

20 24

52

29

14

29

18

1614

21

23

170

24

3

3

0

1 4

2

7

534

22

10 6

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Central Province District National

2012(before fuel subsidy reform)

24 20

48

30

20 30

20

20

18

25

23

190

242

3

1

1 6

38

516

1613

5

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%Interestpayments

Subsidies

SocialAssistance

Others

Grants

Capital

Goods andservices

Personnel

2015(after fuel subsidy reform)

Percent

Source: World Bank COFIS database using MoF data Note: Central level excludes transfers to regions. Subnational 2015 uses budget data

Even after fuel subsidy reform,Capital spending and socialAssistance received lower portion than personnel

Hybrid Indicator of Coverage and Quality of Infrastructure Networks

Average Efficiency Score

Emerging Market Economies {n=50} 0.74

Emerging and Developing Asia {n=13} 0.69

All Countries {n=107} 0.73

Indonesia 0.65

Sumber: IMF, Making Public Investment More Efficient, 2016

There are rooms for improvement on the efficiency of spending

10

To accelerate growth requires significant increase in public (and private) infrastructure investment…

2.1

0.6

2.73.3

1.8

7.8

0.7 0.81.5

0.6 0.5

4.1

0

2

4

6

8

10

Central G

ov.

Subn

ationa

l Gov

.

Total G

ov.

SOE

Private

Total

Average (1995‐97)Average (2010‐14)

Public, SOE and private infrastructure investment fell sharply post Asian financial crisis and is behind many of Indonesia’s neighbors

• Total infrastructure investment in Indonesia has remained at 4 percent of GDP over the past decade.

• This is far below the pre‐1997 Asian financial crisis period of above 7 percent of GDP. It is also below Indonesia’s peers (China, India, Vietnam, Thailand).

Source: World Bank staff estimates

Nominal infrastructure investment levels as a share of GDP, percent

Source: BPS; World Bank staff estimatesNote: infrastructure excludes housing

Low spending and bad allocation has made public infrastructure behind

There is an urgent need to reverse the decline in core infrastructure capital stock (relative to the size of the

economy)…

10

20

30

40

50

60

70

1995 1997 1999 2001 2003 2005 2007 2009 2011

Share of total capital stock

Share of GDP

12

Infrastructure capital stock share of total capital stock and GDP, percent

Source: BPS; World Bank staff estimatesNote: infrastructure excludes housing

The infrastructure deficit is significant in every infrastructure sub‐sector• Roads: Road length grew only by 35 percent in

last decade, while vehicle growth was 300 percent;

• Ports: Jakarta’s Tanjung Priok port (75 percent of total trade) handles 6 million TEUs/year, compared with 30 million TEUs/year in Singapore;

• Electricity: 74 percent of Indonesians have access to electricity, compared with close to 100 percent for most of its neighbors. Indonesia’s power demand is expected to double in 7 years;

• Water supply and Sanitation: 36 percent of Indonesians have access to improved piped water, compared with 99 percent of Malaysians. Only 1% of urban water is properly collected and treated;

• Housing: Indonesia currently has substantial unmet housing needs. Estimates of the backlog range from around 11.9 million units (BPS, 2010) to 13.5 million by 2014 (home ownership information).

Source: World Bank analysis

… and improve Indonesia’s competitiveness

Source: Global Competitiveness Report 2015‐2016

Inadequate supply of infrastructure is among the top three problematic factors for doing business in Indonesia

Higher infrastructure investment could have delivered seven percent growth compared to 5.4 percent over 2001‐2012

5.4 6.07.3

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

Actual(3.1 percent)

Scenario I(5 percent)

Scenario II(10 percent)

Average real GDP growth over 2001‐2012 under different infrastructure capital stock

growth scenarios, percent

Simulation analysis based on assumed elasticities of 0.15 of GDP growth (cross country estimate) with respect to infrastructure capital stock

Source: World Bank staff estimates

Elasticities of infrastructure stock to output (GDP) from selected empirical researches

Country / Region Authors

Elasticity on output with respect to

infrastructure

Infrastructure measure

USA Aschauer (1989) 0.39 Public capital

Developing

countries

Easterly and Rebelo (1993)

0.16 Transport and communication

Cross‐country

Calderon and Serven (2003)

0.16 Transport and communication

Cross‐country

Esfahani and Ramires (2003)

0.12 Physical capital stock

South Asia Sahoo and Dash (2008)

0.18 ‐ 0.22 Physical capital stock

Cross‐country(meta‐analysis)

Ligthart and Bom (2009)

0.15 Public capital

China Sahoo et al. (2010)

0.20 ‐ 0.41 Physical capital stock

Recent fiscal policy in Indonesia has done relatively little to reduce poverty and inequality

The total impact of Indonesian taxes and government spending from 2012‐14 has been to reduce poverty by 1.1‐1.4 percentage points and the Gini coefficient by 2.6‐3.3 points

These reductions are relatively small by international standards.

This is due partly to the low impact of potentially progressive policies:

personal income tax collection is low with poor compliance;

social assistance spending is low;

health spending is low and much of it is not on the primary care which most benefits poorer households;

education spending is high and has some impact on inequality, but not to the degree seen in other countries.

It is also partly due to high spending on energy subsidies which predominantly benefit richer households.

15

Baseline Fiscal Policy Impact on Poverty and Inequality 2012‐14*

Note: *The 2012 result is from a fiscal incidence paper (World Bank and Ministry of Finance 2015), and the 2013 and 2014 results are from a coming update to that paper. The analysis is based on the Commitment to Equity framework (commitmentoequity.org), and applies standard fiscal incidence analysis to the majority of GoI taxes and spending

‐3.5

‐3

‐2.5

‐2

‐1.5

‐1

‐0.5

0

Poverty (percentagepoints)

Inequality (points ofGini)

2012 2013 2014 Average

2012 Effectiveness at Reducing Inequality Relative to Spending Levels

Source: Susenas 2012, World Bank calculations.Note: Effectiveness Index is Change in Market Income Gini to Final Income Gini / Budget as % of GDP

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

0

20

40

60

80

100

120

DirectTransfers

Education Health Subsidies

Percent of GDP

Effectiven

ess Ind

ex

Effectiveness Index (LHS) Budget (RHS)

(all HH (energy only)

Direct social assistance transfers are the most effective at reducing poverty and inequality but total spending is below the average of peer countries and it receives a small budget

allocation, relative to education and energy subsidies

15

The most effective programs at reducing inequality receive the smallest budget

Source: World Bank Aspire 2016. MoF 2016 Revised Budget.

2.40%

1.50%1.20% 1.10%

0.70% 0.62% 0.60%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

Brazil 20

11

Lower M

iddle Income 20

08‐

2014

East Asia

Pacific 20

08‐201

4 (all

income levels)

Bang

lade

sh 201

4

India 20

14

Indo

nesia

201

6

Phillipines 201

3

National HH based SA spending as a share of nominal GDP

Why Indonesia national budget not inclusive

Total national public spending has been below 20 percent of GDP even during the commodity boom…

The resource envelope for public expenditure has been limited by weak state revenue collection and maintenance of low fiscal deficits (adherence to fiscal rule of 3% of GDP)

18

National public expenditure by level of government (% GDP)% of GDP

10.5 10.2 11.3 11.7 11.9 11.4 10.3

1.4 1.31.3 1.6 1.7 1.5

1.3

5.1 4.84.9

5.1 5.7 6.8

5.8

16.9 16.217.5

18.4 19.3 19.717.4

0

2

4

6

8

10

12

14

16

18

20

2009 2010 2011 2012 2013 2014 2015

District

Province (excl.transfers todistricts)

Central (excl.transfers to SNGs)

National

Source: World Bank COFIS database using MoF data Notes: 2015 data for province and district are Budget. Remainder is realized expenditure

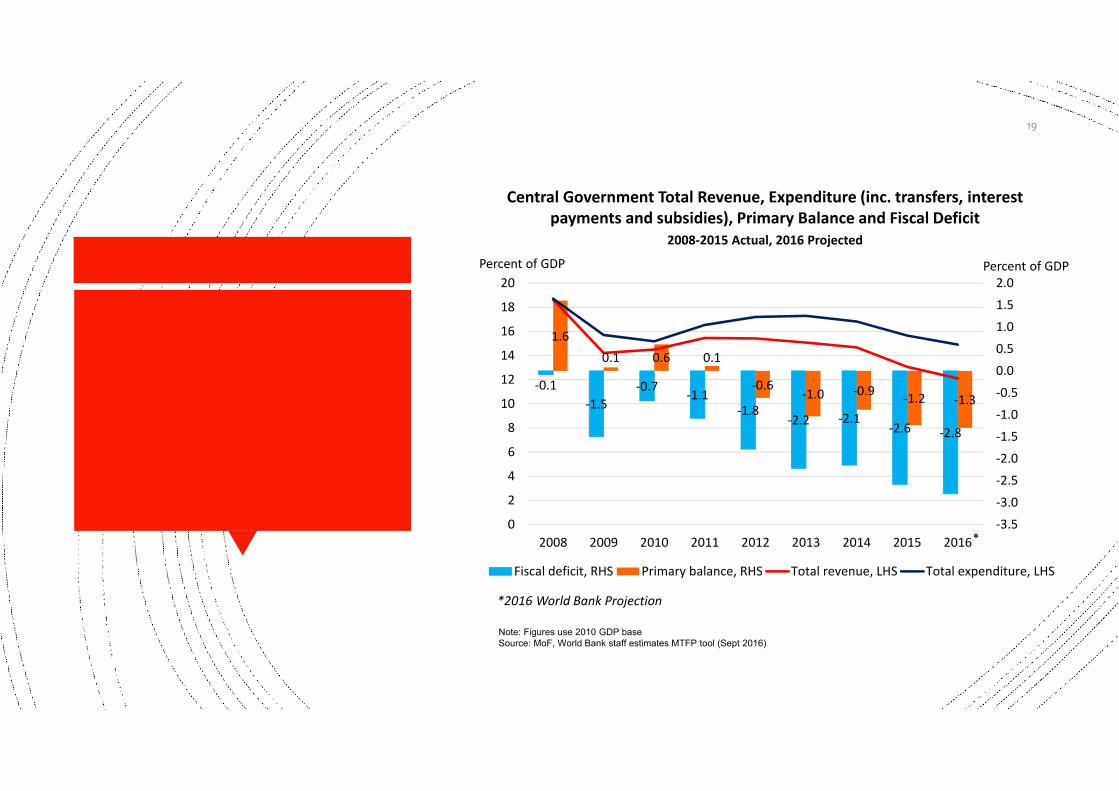

IDN: Post commodity boom: declining revenue & expenditure to GDP ratios and increasing primary & fiscal deficits (but within fiscal rule)

19

Central Government Total Revenue, Expenditure (inc. transfers, interest payments and subsidies), Primary Balance and Fiscal Deficit

2008‐2015 Actual, 2016 Projected

*2016 World Bank Projection

‐0.1‐1.5

‐0.7 ‐1.1‐1.8

‐2.2 ‐2.1‐2.6 ‐2.8

1.60.1 0.6 0.1

‐0.6‐1.0 ‐0.9 ‐1.2 ‐1.3

‐3.5

‐3.0

‐2.5

‐2.0

‐1.5

‐1.0

‐0.5

0.0

0.5

1.0

1.5

2.0

0

2

4

6

8

10

12

14

16

18

20

2008 2009 2010 2011 2012 2013 2014 2015 2016

Percent of GDPPercent of GDP

Fiscal deficit, RHS Primary balance, RHS Total revenue, LHS Total expenditure, LHS

*

Note: Figures use 2010 GDP baseSource: MoF, World Bank staff estimates MTFP tool (Sept 2016)

20122015

Brazil

ChinaEgypt

India

Indonesia,

MalaysiaMexicoPhilippines

Thailand

0

10

20

30

40

50

60

3.0 3.5 4.0 4.5 5.0

Expe

nditu

re as a

share of GDP

(%)

Log GDP per capita, 2012

Brazil

ChinaEgypt

India

Indonesia, Malaysia

Mexico

Philippines Thailand

0

10

20

30

40

50

60

70

3.0 3.5 4.0 4.5 5.0

Expe

nditu

re as a

share of GDP

(%)

Log GDP per capita, 2015

General Government Expenditure (% of GDP)

Indonesia’s level of expenditure (17.4% of GDP in 2015) is relatively low—nearly half of the average of emerging markets and middle‐income economies (32.3% of GDP)

…making Indonesia a small spender, in comparison with emerging markets and middle-income countries

Notes:(1) General government consists of central, state (province) and local (district) government(2) The sample of chosen countries are emerging markets and middle‐income economies, based on groupings by IMF Fiscal Monitor (April 2016)(3) There are 40 and 37 countries in the 2012 and 2015 sample(4) Horizontal axis: GDP per capita in respective years are in constant 2010 USD, then converted into logarithmic (log) form

Source: IMF Fiscal Monitor (April 2016) for fiscal data, WB COFIS Database for IDN expenditure data, and World Development Indicators for GDP per capita data

Caused by underperformanced revenues collections

y = 0.0005x + 21.803R² = 0.4799

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

0 10,000 20,000 30,000 40,000 50,000 60,000 70,000

Reve

nue Co

llection pe

r GDP

Per Capita GDP USD PPP

Tax collection per GDP and Per Capita GDP USD PPP, 2011

Indonesia

21

General Government Revenue (% of GDP)

BrazilChile

China

India

Indonesia, 14.8%

Libya

Malaysia

MexicoPhilippines

Thailand

0

10

20

30

40

50

60

3.0 3.5 4.0 4.5 5.0

Revenu

e as a sh

are of GDP

(%)

log GDP per capita (in 2010 US$)

Brazil

China

Egypt

Indonesia, 17.2%

Malaysia

Mexico

India

PhilippinesThailand

0

10

20

30

40

50

60

3.0 3.5 4.0 4.5 5.0

Revenu

e as a sh

are of GDP

(%)

log GDP per capita (in 2010 US$)

2012 2015

Among its emerging market and MIC peers, Indonesia has one of the lowest revenue-to-GDP ratios, pre and post commodity boom…

Notes:(1) General government consists of central, state (province) and local (district) government(2) The sample of chosen countries are emerging markets and middle‐income economies, based on groupings by IMF Fiscal Monitor (April 2016)(3) There are 40 and 37 countries in the 2012 and 2015 sample(4) Horizontal axis: GDP per capita in respective years are in constant 2010 USD, then converted into logarithmic (log) form

Source: IMF Fiscal Monitor (April 2016) for fiscal data, WB COFIS Database for IDN expenditure data, and World Development Indicators for GDP per capita data

20122015

Brazil

China

Egypt

India

Indonesia, ‐1.2%

MalaysiaMexicoPhilippines Thailand

‐25

‐20

‐15

‐10

‐5

0

5

10

15

3.0 3.5 4.0 4.5 5.0

Prim

ary ba

lance as a sh

are of GDP

(%)

log GDP per capita (in 2010 US$)

BrazilChina

Egypt

India

Indonesia, ‐0.4%

Malaysia

MexicoPhilippines

Thailand

‐10

‐5

0

5

10

15

20

25

30

3.0 3.5 4.0 4.5 5.0Prim

ary ba

lance as a sh

are of GDP

(%)

log GDP per capita (in 2010 US$)

*Primary balance is the overall fiscal balance excluding net interest paymentNotes:(1) General government consists of central, state (province) and local (district) government(2) The sample of chosen countries are emerging markets and middle‐income economies, based on groupings by IMF Fiscal Monitor (April 2016)(3) There are 40 and 37 countries in the 2012 and 2015 sample(4) Horizontal axis: GDP per capita in respective years are in constant 2010 USD, then converted into logarithmic (log) form

Source: IMF Fiscal Monitor (April 2016) for fiscal data, WB COFIS Database for IDN expenditure data, and World Development Indicators for GDP per capita data

General Government Primary Balance (% of GDP)

In 2015 IDN’s primary deficit (-1.2% of GDP) remains moderate relative to the average of emerging & MIC economies (-2.9% of GDP)…

2012 2015

BrazilChina

Egypt

India

Indonesia, ‐1.6%

Malaysia

MexicoPhilippines

Thailand

‐15

‐10

‐5

0

5

10

15

20

25

30

35

40

3.0 3.5 4.0 4.5 5.0

Fiscal balan

ce as a

share of GDP

(%)

log GDP per capita (in 2010 US$)

Brazil

China

Egypt

IndiaIndonesia, ‐2.5%

Malaysia

Mexico

PhilippinesThailand

‐25

‐20

‐15

‐10

‐5

0

5

3.0 3.5 4.0 4.5 5.0

Fiscal balan

ce as a

share of GDP

(%)

log GDP per capita (in 2010 US$)

Notes:(1) General government consists of central, state (province) and local (district) government(2) The sample of chosen countries are emerging markets and middle‐income economies, based on groupings by IMF Fiscal Monitor (April 2016)(3) There are 40 and 37 countries in the 2012 and 2015 sample(4) Horizontal axis: GDP per capita in respective years are in constant 2010 USD, then converted into logarithmic (log) form

Source: IMF Fiscal Monitor (April 2016) for fiscal data, WB COFIS Database for IDN expenditure data, and World Development Indicators for GDP per capita data

General Government Fiscal Balance (% of GDP)

…also IDN’s fiscal deficit (-2.5% of GDP) remains moderate relative to the average of emerging & MIC economies (-4.5% of GDP)

2012 2015

Brazil

China

Egypt

India

Indonesia, 27.2%

MalaysiaMexico

Philippines Thailand

0102030405060708090

100

3.0 3.5 4.0 4.5 5.0Gov

ernm

ent d

ebt a

s a sh

are of GDP

(%)

log GDP per capita (in 2010 US$)

Brazil

China

EgyptIndia

Indonesia, 23.0%

MalaysiaMexico

Philippines

Thailand

0

10

20

30

40

50

60

70

80

90

3.0 3.5 4.0 4.5 5.0Gov

ernm

ent d

ebt a

s a sh

are of GDP

(%)

log GDP per capita (in 2010 US$)

Similarly IDN’s public debt position (27.2% of GDP) remains solid relative to the average of emerging & MIC economies (45.4% of GDP)

General Government Debt (% of GDP)

Notes:(1) General government consists of central, state (province) and local (district) government(2) The sample of chosen countries are emerging markets and middle‐income economies, based on groupings by IMF Fiscal Monitor (April 2016)(3) There are 40 and 37 countries in the 2012 and 2015 sample(4) Horizontal axis: GDP per capita in respective years are in constant 2010 USD, then converted into logarithmic (log) form

Source: IMF Fiscal Monitor (April 2016) for fiscal data, WB COFIS Database for IDN expenditure data, and World Development Indicators for GDP per capita data

Finally ..Structural fiscal Reform is needed to

make Indonesia’s budget is inclusive

Addressing the Policy Gap is

Urgent

The fiscal deficit is structural not cyclical

The structural deficit is now near the 3% ceiling so little fiscal space left

In the face of an economic shock, fiscal policy will be pro‐cyclical

Structural measures needed not ad hoc/short‐term measures

Reforms can have lagged benefits and/or net cost up front (e.g., IT systems)

Fiscal credibility (lessons from Brazil)

Structural fiscal Reform is needed…

Triple Tracks strategy First Track : increase revenue collection through A comprehensive tax reform – particularly a tax administration reform

An integrated non tax reform strategy

Second track : Improve current spending practices both at central level and local level.

Third track : continue to improve sectoral allocation.

Indonesia has substantial tax revenue potential IMF (2013)1/ estimated

Indonesia’s tax effort between 0.42‐0.47 in 2011

IMF (2013)2/ also estimated Indonesia’s total revenue gaps of 5.0% of GDP

IMF (2011, 2014)3/ and Sugana‐Hidayat (2013)4/estimated VAT gaps between 47‐60% of the current revenue

Tax reform should focus on tax administration rather than policy

1 Fenochietto, R and Pessino, C, “Understanding Countries’ Tax Effort, Working Paper 13/244, IMF, November 2013

2 ___,”Taxing Times”, Fiscal Monitor, World Economic and Financial Surveys, IMF, October 20133 FAD, “Revenue Mobilization in Developing Countries”, IMF, March 2011; IMF Mission, “Tax Policy and Administration: Setting the Strategy for the Coming Years”, Fiscal Affairs Department, IMF, December 2014

4 Sugana, R and Hidayat A, “Analysis of VAT Revenue Potential and Gaps in Indonesia 2013”, Journal of Indonesian Economy and Development, University of Indonesia, July 2014.

Source: IMF2

Stochastic Frontier Analysis

Tax potential gap is substantial

Improving tax administration must be the first priority

Addresing tax policy should be conducted after tax admreform in place

First track: raising tax revenues

Despite current efforts on improving budget allocation, there is significant room to improve the allocative

efficiency of APBN spending

30

• Infrastructure: increase CG spend and DAK physical transfers

• Social Assistance Programs: increase CG spend

• Health: increase CG spend and DAK health transfers

• Subsidies: reduce energy (LPG, diesel, electricity) and non‐energy (fertilizers) subsidies

• Government administration: reduce personnel spending

• Education ‐ maintain• Agriculture ‐ maintain• DAU – base on realistic revenue

projections so not increase as share of revenues

• Dana Desa – more gradual expansion (relative to roadmap)

Improve relative allocation of CG/APBN spending by

Source: World Bank COFIS database using MoF data

375.5416.1

67.5104.0

350.3

77.3

177.9

387.3

0.0

50.0

100.0

150.0

200.0

250.0

300.0

350.0

400.0

450.0

2011 2012 2013 2014 2015 2016 2017

infrastructure

health

Energy subsidy

Before budget reformCommitment to reform

Budget Allocation (Rp tr)

education

Source: MOF

Second track: improvingBudget allocation

Improving allocative efficiency of CG/APBN spendingHigher infrastructure: increase CG spend & DAK physical

Increase CG and LG spending on infrastructures both for capital spending and O&M Improve the composition of infrastructures ‐ spend more on electricity, water and and sanitation, housing, transport and irrigation

Encourage PPP

31

Accelerating economic growth requires significant increase in public infrastructure investment to address the infrastructure deficit – from 2.3 percent to 5 percent of GDP GDP

0

20

40

60

80

100

Central SNG SOEs Private

Transport Energy TelecomIrrigation WSS

Composition of infrastructure investment by entity and sector (%), 2012

Improving allocative efficiency of CG/APBN spendingHigher health: increase CG spend and DAK health transfers

Health spending is low by international comparisons lowest in the world

To close half of the gap to the international average by 2020, Indonesia should double public health spending from 1.1 percent to 2.3 percent of GDP

Should be shared by central government and local government

Spend on supply side readiness

In addition to spending to Increase spending on JKN‐PBI to expand JKN coverage amongst the poor –covered in social assistance

32

Public expenditure on health as share of GDP vs income, 2014

Note: Both y‐ and x‐axes are loggedSource: World Development Indicators and COFIS

2.7%3.7%4.4%5.1%

6.0%7.2%8.8%

11.2%

15.7%

35.2%

0%

5%

10%

15%

20%

25%

30%

35%

40%

Poorest D

ecile 2 3 4 5 6 7 8 9

Richest D

ecile

Share of Ben

efits

Source: Susenas 2012, World Bank calculations.

2012 Fuel and Electricity SubsidiesShare of total benefits received by

decile

Most subsidies are not well targeted, regressive, and not cost effective

Improving allocative efficiency of CG/APBN spendingLower subsidies and Adopt a targeted and direct subsidy program

13.612.3

11.7 11.19.7

8.77.2

5.8

3.9

1.5

0

2

4

6

8

10

12

14

16

18

20

1 2 3 4 5 6 7 8 9 10

Incide

nce (%

)

Expenditure Decile

2015 Rastra (Raskin)Share of total benefits received by

decile

Source: Susenas 2015, World Bank calculations.

Target 25% poorest families

From technocracy to implementation:

institutional and political issues

ISSUES CHALLENGES

34

• Government policy ispolitical action

o How to get and involve mostof important stakeholders

• From policy perspective –except on revenue which isstill centralized, decisionand implementation onspending will be moredecentralized andfragmented.

• Many policies are designedand implemented notaccording to evidencebased and often reactiveto current circumtances

• Fragmented decision making processo There will no a dominant political party over next 10year

o There exist vested interest at all levels ‐ executive,legislative and judicative.

• Execution capacityo varies but generally weak.o Quality of project preparation generally declining

• Two big questionso How to ensure politician to conduct reforms under somany constraints

o How to upgrade implementation capacity at all levels.o Finally, budget is one of elements ofinclusive growth outcomes. Improvement ineconomic policies implementation andgovernance could be more important thanbudget to ensure a better inclusive growthoutcome.

Thank you