Fiscal Decentralisation in Philippines

56

FISCAL DECENTRALIZATION IN THE PHILIPPINES

-

Upload

united-nations-human-settlements-programme-un-habitat -

Category

Documents

-

view

228 -

download

1

Transcript of Fiscal Decentralisation in Philippines

8/12/2019 Fiscal Decentralisation in Philippines

http://slidepdf.com/reader/full/fiscal-decentralisation-in-philippines 1/56

FISCALDECENTRALIZATIONIN THE PHILIPPINES

8/12/2019 Fiscal Decentralisation in Philippines

http://slidepdf.com/reader/full/fiscal-decentralisation-in-philippines 2/56

8/12/2019 Fiscal Decentralisation in Philippines

http://slidepdf.com/reader/full/fiscal-decentralisation-in-philippines 3/56

Sec1:iii

United Nations Human Settlements ProgrammeNairobi 2011

FISCAL DECENTRALIZATIONIN THE PHILIPPINES

8/12/2019 Fiscal Decentralisation in Philippines

http://slidepdf.com/reader/full/fiscal-decentralisation-in-philippines 4/56

iv

Te Global Urban Economic Dialogue Series

Fiscal Decentralisation in Philippines

First published in Nairobi in 2011 by UN-HABIA.Copyright © United Nations Human Settlements Programme 2011

All rights reservedUnited Nations Human Settlements Programme (UN-HABIA)P. O. Box 30030, 00100 Nairobi GPO KENYAel: 254-020-7623120 (Central Office)

www.unhabitat.org

HS/129/11EISBN Number(Series): 978-92-1-132027-5ISBN Number(Volume): 978-92-1-132414-3

Disclaimer

Te designations employed and the presentation of the material in this publication donot imply the expression of any opinion whatsoever on the part of the Secretariat of

the United Nations concerning the legal status of any country, territory, city or areaor of its authorities, or concerning the delimitation of its frontiers of boundaries.

Views expressed in this publication do not necessarily reflect those of the UnitedNations Human Settlements Programme, the United Nations, or its Member States.

Excerpts may be reproduced without authorization, on condition that the source is indicated.

Acknowledgements:

Director: Oyebanji Oyeyinka

Principal Editor and Manager: Xing Quan Zhang

Principal Author: Gilberto M. Llanto

English Editor: Roman Rollnick

Design and Layout: Peter Cheseret

8/12/2019 Fiscal Decentralisation in Philippines

http://slidepdf.com/reader/full/fiscal-decentralisation-in-philippines 5/56

v

U r b a n i z a t i o n

is one of themost powerful,irreversible forcesin the world. Itis estimated that93 percent ofthe future urbanpopulation growth

will occur in thecities of Asia and

Africa, and to a lesser extent, Latin Americaand the Caribbean.

We live in a new urban era with most ofhumanity now living in towns and cities.

Global poverty is moving into cities, mostlyin developing countries, in a process we callthe urbanisation of poverty .

Te world’s slums are growing and growingas are the global urban populations. Indeed,this is one of the greatest challenges we face inthe new millennium.

Te persistent problems of poverty andslums are in large part due to weak urbaneconomies. Urban economic development isfundamental to UN-HABIA’s mandate.Cities act as engines of national economicdevelopment. Strong urban economies

are essential for poverty reduction and the

provision of adequate housing, infrastructure,

education, health, safety, and basic services.

Te Global Urban Economic Dialogue seriespresented here is a platform for all sectorsof the society to address urban economicdevelopment and particularly its contributionto addressing housing issues. Tis work carriesmany new ideas, solutions and innovativebest practices from some of the world’sleading urban thinkers and practitioners

from international organisations, nationalgovernments, local authorities, the privatesector, and civil society.

Tis series also gives us an interestinginsight and deeper understanding of the widerange of urban economic development andhuman settlements development issues. It willserve UN member States well in their questfor better policies and strategies to address

increasing global challenges in these areas

Joan ClosUnder-Secretary-Generalof the United Nations,

Executive Director, UN-HABIA

FOREWORD

8/12/2019 Fiscal Decentralisation in Philippines

http://slidepdf.com/reader/full/fiscal-decentralisation-in-philippines 6/56

vi

8/12/2019 Fiscal Decentralisation in Philippines

http://slidepdf.com/reader/full/fiscal-decentralisation-in-philippines 7/56

CONTENTS

FOREWORD III

CONTENTS IV

CHAPTER 1 INTRODUCTION 1

Objective of the Report 2

CHAPTER 2 THE CONCEPT AND ELEMENTS OF FISCALDECENTRALIZATION 5

Oates decentralization theorem 5

An adequate enabling policy environment 7

CHAPTER 3 TAX-EXPENDITURE ASSIGNMENT 11

Local government tax revenues: trend and composition,

1989-2009 11

Local government expenditures: trend and composition,

1989-2003 19

CHAPTER 4 INTERGOVERNMENTAL FISCAL TRANSFERS 31

Instruments of intergovernmental fiscal transfers 31

Designing fiscal transfers 31

Philippine internal revenue allotment 33

Distributable resource pool 36

Distributive and allocative formula 38

CHAPTER 5 LOCAL GOVERNMENT FINANCING48 40

CHAPTER 6 CONCLUSIONS AND RECOMMENDATIONS 43

BIBLIOGRAPHY 44

8/12/2019 Fiscal Decentralisation in Philippines

http://slidepdf.com/reader/full/fiscal-decentralisation-in-philippines 8/56

viii

FISCAL DECENTRALIZATION IN THE PHILIPPINES

LISTS OF FIGURES, TABLES AND BOXES

LIST OF FIGURES

Figure 1 Three Branches of the Philippine Government 1

Figure 2 Philippine Local Government Units 2

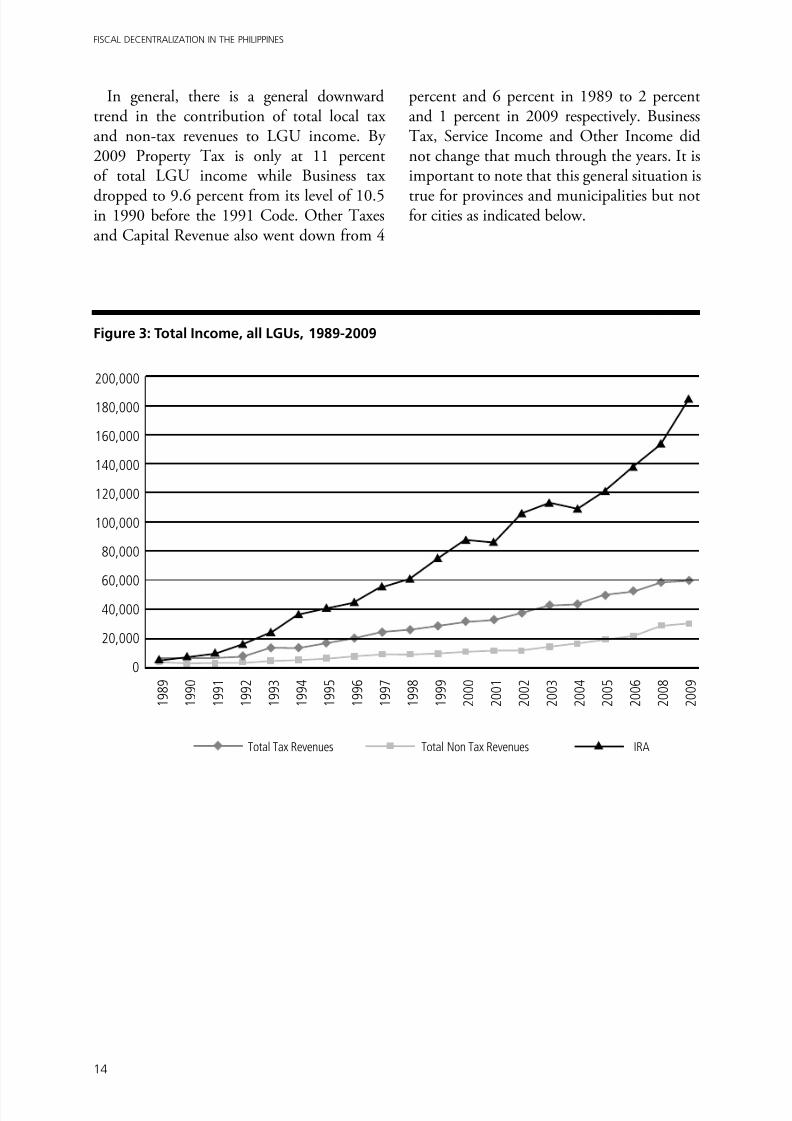

Figure 3 Total Income, all LGUs, 1989-2009 14

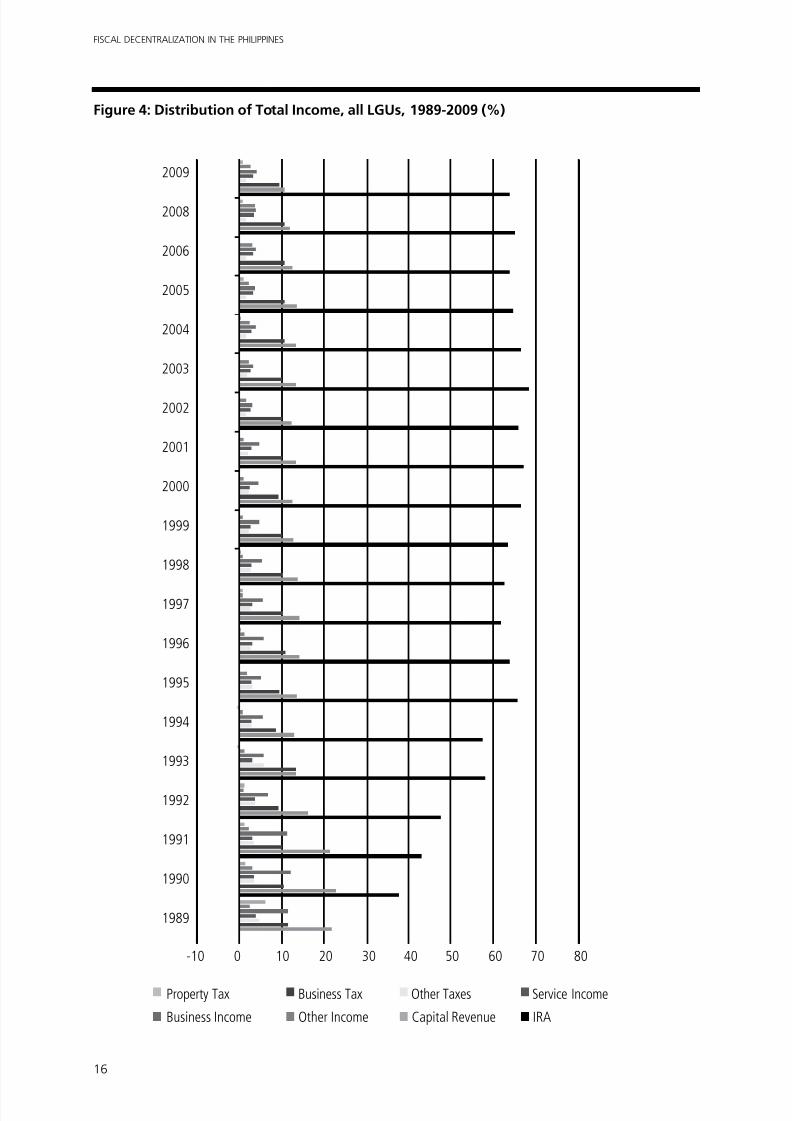

Figure 4 Distribution of Total Income, all LGUs, 1989-2009 (%) 16

Figure 5 Distribution of Income by type of LGU, 1990 17

Figure 6 Distribution of Income by type of LGU, 2009 17

Figure 7 Distribution of LGU Expenditures, All LGUs 1988-2003 20

Figure 8 Distribution of Total Expenditures - All Provinces, 1988-2003 22

Figure 9 Distribution of Total Expenditures - All Municipalities, 1988-2003 23

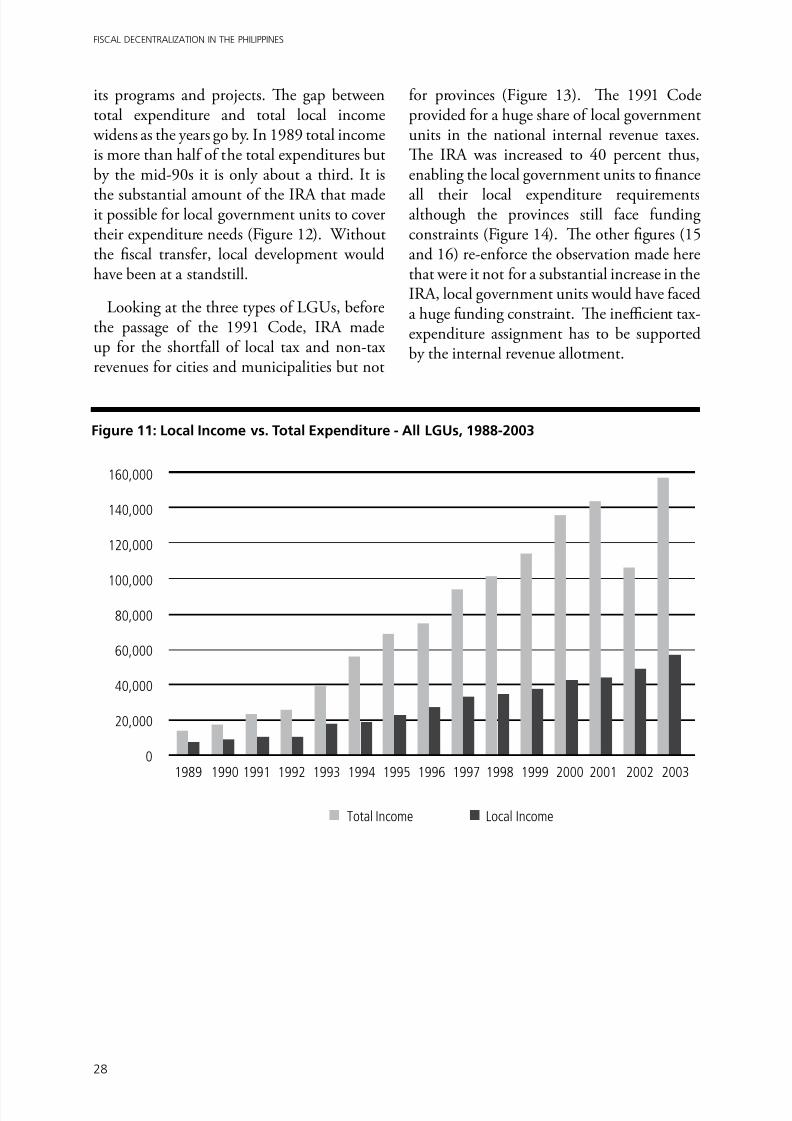

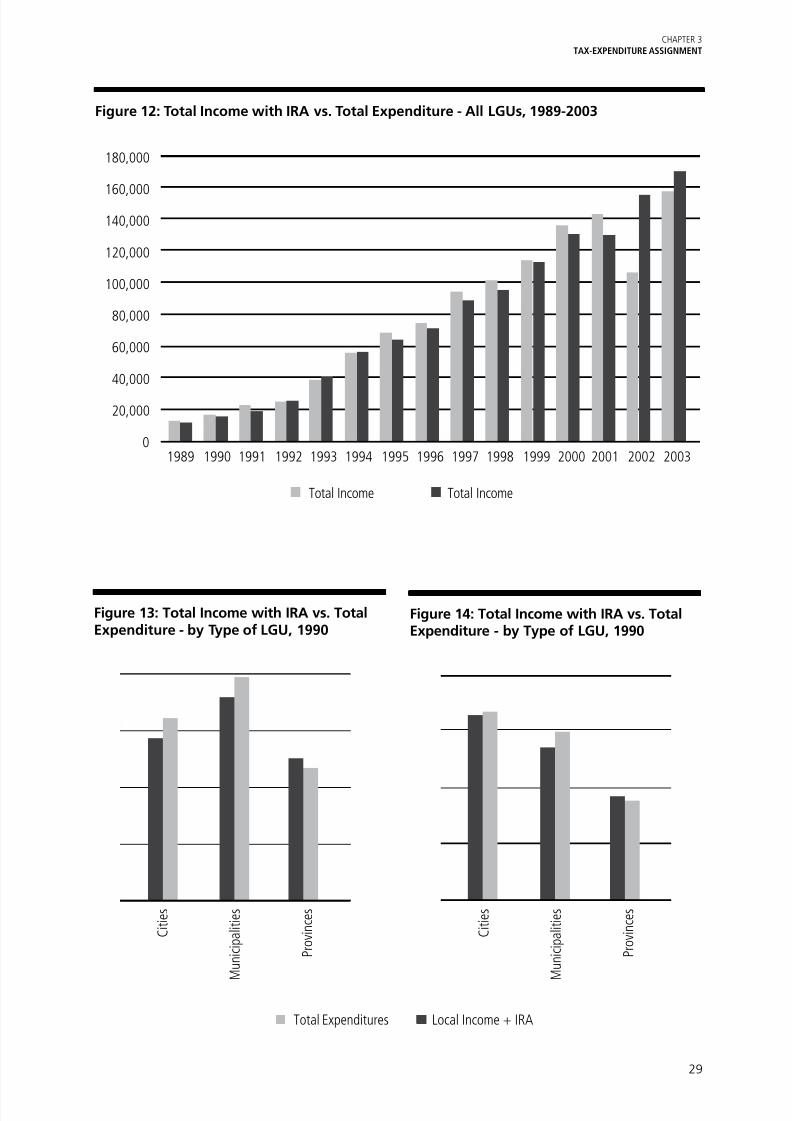

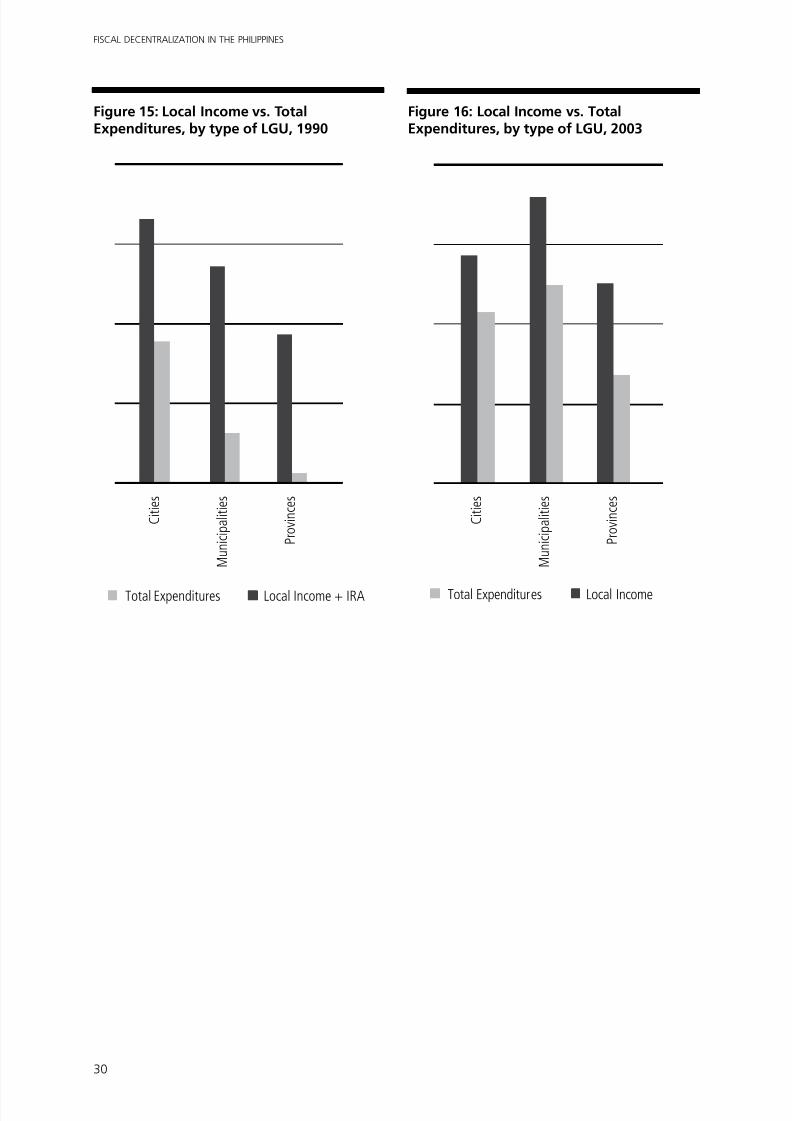

Figure 10 Distribution of Total Expenditures - All Cities, 1988-2003 24Figure 11 Local Income vs. Total Expenditure - All LGUs, 1988-2003 28

Figure 12 Total Income with IRA vs. Total Expenditure - All LGUs, 1989-2003 29

Figure 13 Total Income with IRA vs. Total Expenditure - by Type of LGU, 1990 29

Figure 14 Total Income with IRA vs. Total Expenditure - by Type of LGU, 1990 29

Figure 15 Local Income vs. Total Expenditures, by type of LGU, 1990 30

Figure 16 Local Income vs. Total Expenditures, by type of LGU, 2003 30

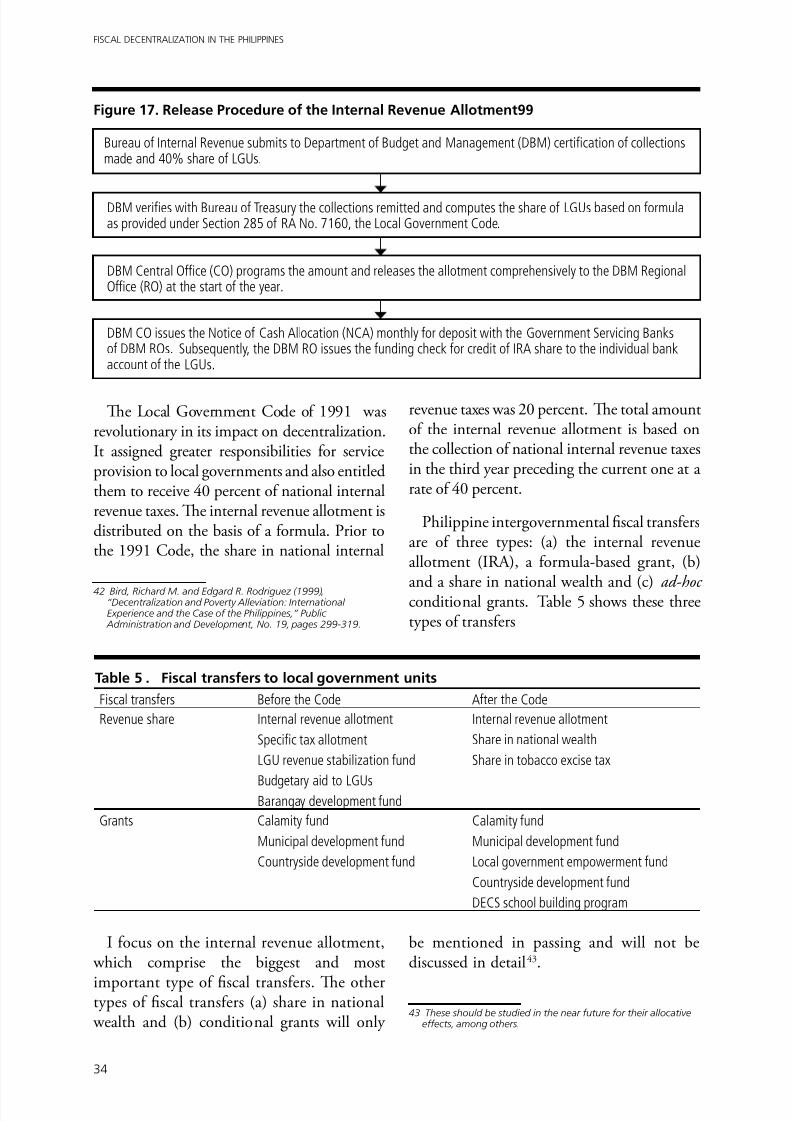

Figure 17 Release Procedure of the Internal Revenue Allotment99 34

LIST OF TABLES

Table 1 Tax assignment in cities, provinces and municipalities 12

Table 2 Distribution of Local Income, All LGUs, 1989-2009 (in million pesos) 15

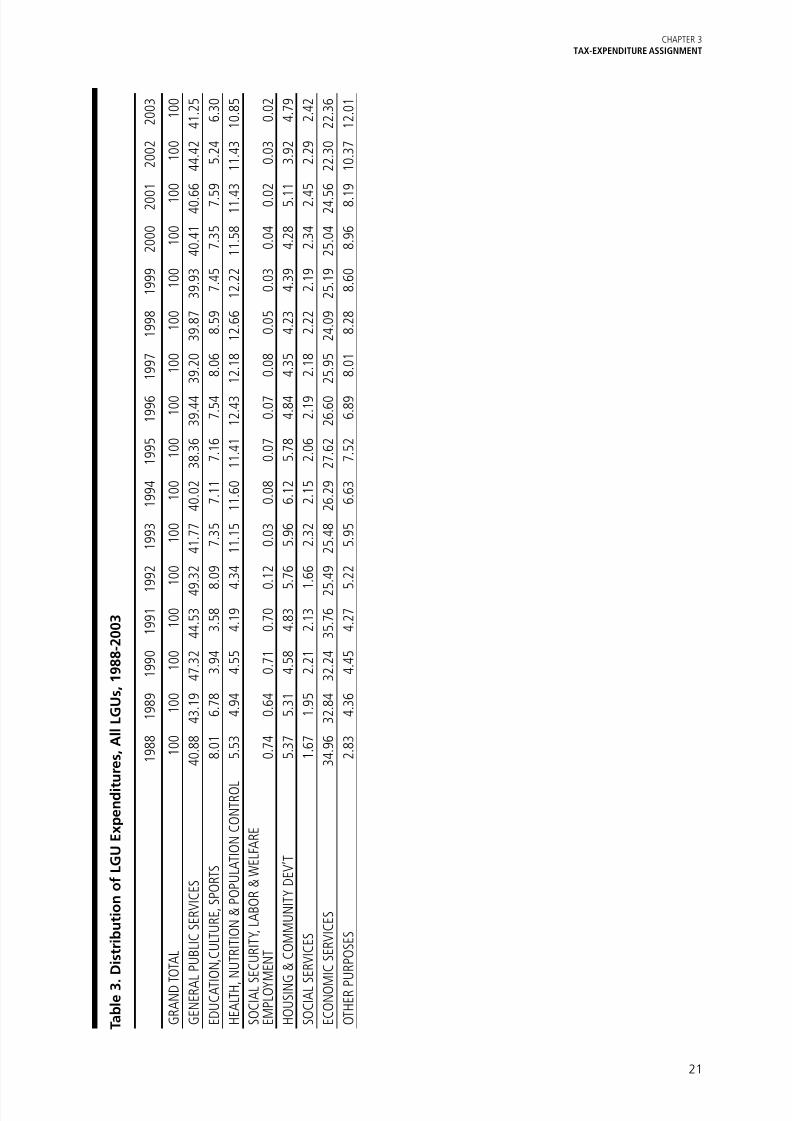

Table 3 Distribution of LGU Expenditures, All LGUs, 1988-2003 21

Table 4 Number of Awardees per Award Category (1994 – 2009) 26

Table 5 Fiscal transfers to local government units 34

Table 6 Percentage Shares of LGUs in the Internal Revenue Allotment 35

Table 7 Distribution Formula for the Internal Revenue Allotment 35

LIST OF BOXES

Box 1 Assessment level by type of land 13

Box 2 An assessment of tax assignment to local government units 18

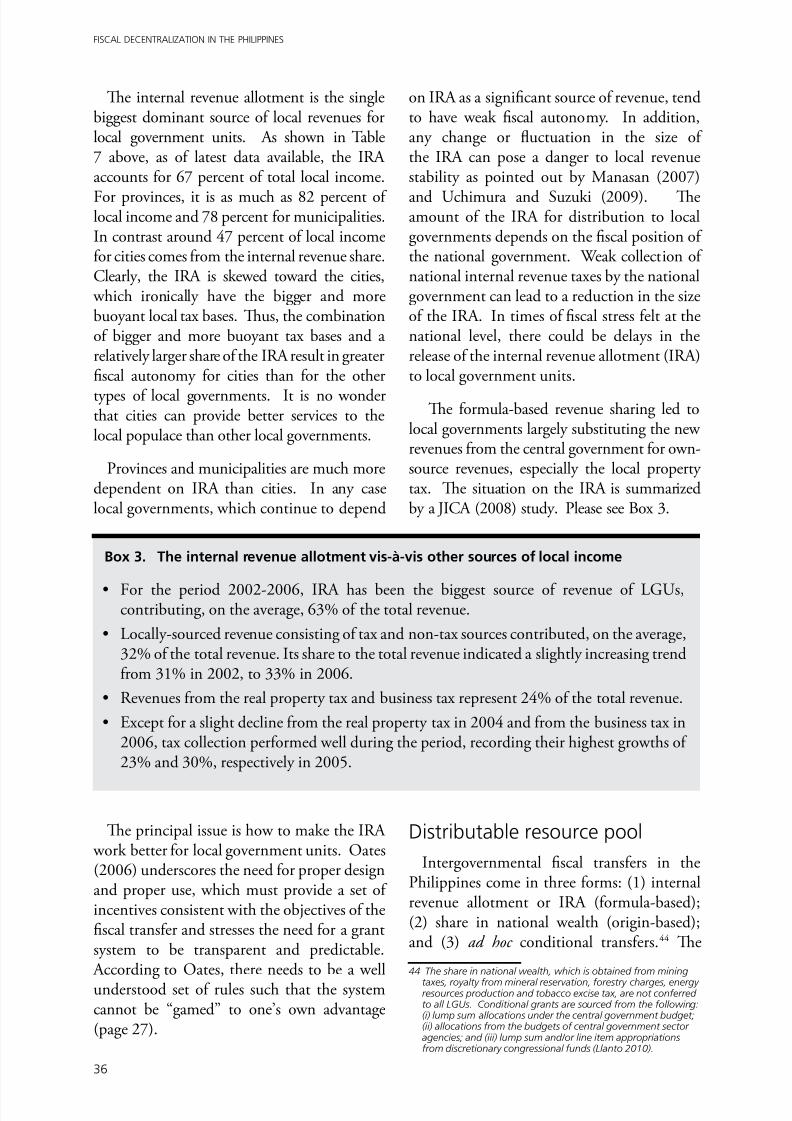

Box 3 The internal revenue allotment vis-à-vis other sources of local income 36

8/12/2019 Fiscal Decentralisation in Philippines

http://slidepdf.com/reader/full/fiscal-decentralisation-in-philippines 9/56

1

CHAPTER 1INTRODUCTION

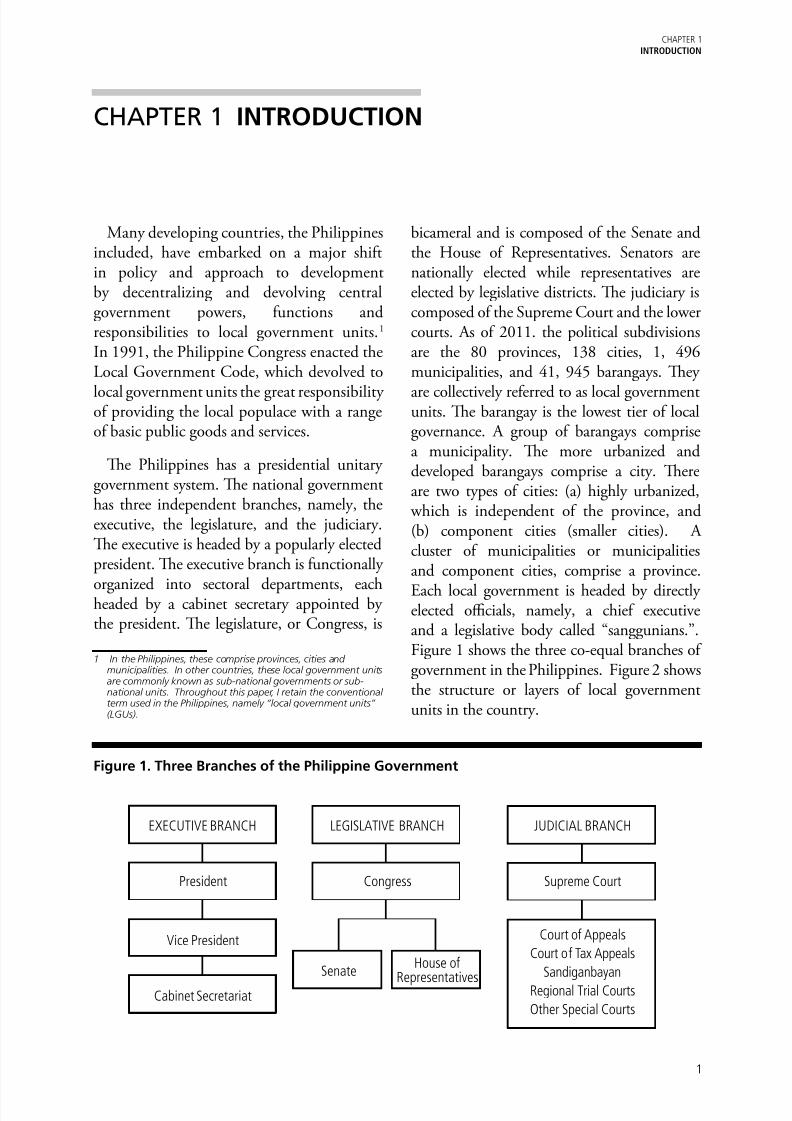

CHAPTER 1 INTRODUCTION

Many developing countries, the Philippinesincluded, have embarked on a major shiftin policy and approach to developmentby decentralizing and devolving centralgovernment powers, functions andresponsibilities to local government units.1 In 1991, the Philippine Congress enacted theLocal Government Code, which devolved to

local government units the great responsibilityof providing the local populace with a rangeof basic public goods and services.

Te Philippines has a presidential unitarygovernment system. Te national governmenthas three independent branches, namely, theexecutive, the legislature, and the judiciary.Te executive is headed by a popularly electedpresident. Te executive branch is functionally

organized into sectoral departments, eachheaded by a cabinet secretary appointed bythe president. Te legislature, or Congress, is

1 In the Philippines, these comprise provinces, cities andmunicipalities. In other countries, these local government unitsare commonly known as sub-national governments or sub-national units. Throughout this paper, I retain the conventionalterm used in the Philippines, namely “local government units”(LGUs).

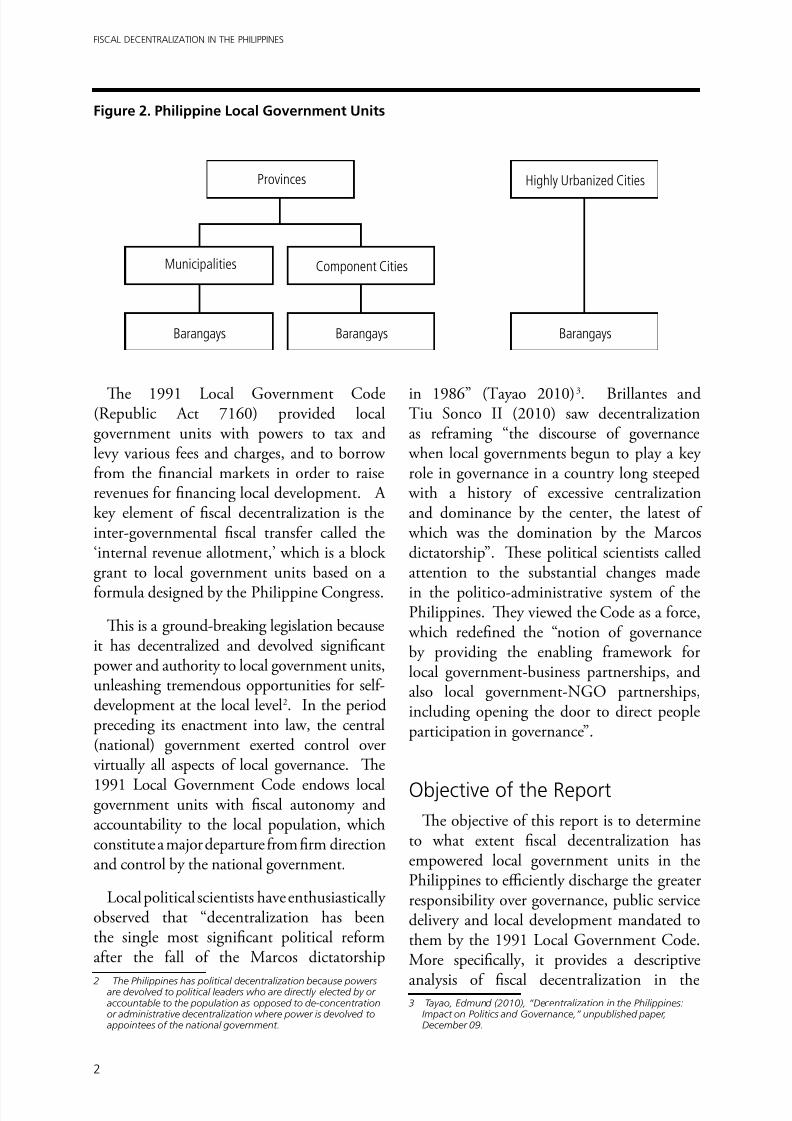

bicameral and is composed of the Senate andthe House of Representatives. Senators arenationally elected while representatives areelected by legislative districts. Te judiciary iscomposed of the Supreme Court and the lowercourts. As of 2011. the political subdivisionsare the 80 provinces, 138 cities, 1, 496municipalities, and 41, 945 barangays. Tey

are collectively referred to as local governmentunits. Te barangay is the lowest tier of localgovernance. A group of barangays comprisea municipality. Te more urbanized anddeveloped barangays comprise a city. Tereare two types of cities: (a) highly urbanized,

which is independent of the province, and(b) component cities (smaller cities). Acluster of municipalities or municipalitiesand component cities, comprise a province.

Each local government is headed by directlyelected officials, namely, a chief executiveand a legislative body called “sanggunians.”.Figure 1 shows the three co-equal branches ofgovernment in the Philippines. Figure 2 showsthe structure or layers of local governmentunits in the country.

Figure 1. Three Branches of the Philippine Government

EXECUTIVE BRANCH

President

Vice President

Cabinet Secretariat

LEGISLATIVE BRANCH

Congress

SenateHouse of

Representatives

JUDICIAL BRANCH

Supreme Court

Court of Appeals

Court of Tax Appeals

Sandiganbayan

Regional Trial Courts

Other Special Courts

8/12/2019 Fiscal Decentralisation in Philippines

http://slidepdf.com/reader/full/fiscal-decentralisation-in-philippines 10/56

2

FISCAL DECENTRALIZATION IN THE PHILIPPINES

Provinces

Municipalities

BarangaysBarangays

Highly Urbanized Cities

Component Cities

Figure 2. Philippine Local Government Units

Te 1991 Local Government Code(Republic Act 7160) provided localgovernment units with powers to tax andlevy various fees and charges, and to borrowfrom the financial markets in order to raiserevenues for financing local development. Akey element of fiscal decentralization is theinter-governmental fiscal transfer called the‘internal revenue allotment,’ which is a blockgrant to local government units based on a

formula designed by the Philippine Congress.

Tis is a ground-breaking legislation becauseit has decentralized and devolved significantpower and authority to local government units,unleashing tremendous opportunities for self-development at the local level2. In the periodpreceding its enactment into law, the central(national) government exerted control overvirtually all aspects of local governance. Te

1991 Local Government Code endows localgovernment units with fiscal autonomy andaccountability to the local population, whichconstitute a major departure from firm directionand control by the national government.

Local political scientists have enthusiasticallyobserved that “decentralization has beenthe single most significant political reformafter the fall of the Marcos dictatorship

2 The Philippines has political decentralization because powersare devolved to political leaders who are directly elected by oraccountable to the population as opposed to de-concentrationor administrative decentralization where power is devolved toappointees of the national government.

in 1986” (ayao 2010)3. Brillantes andiu Sonco II (2010) saw decentralizationas reframing “the discourse of governance

when local governments begun to play a keyrole in governance in a country long steeped

with a history of excessive centralizationand dominance by the center, the latest of

which was the domination by the Marcosdictatorship”. Tese political scientists calledattention to the substantial changes made

in the politico-administrative system of thePhilippines. Tey viewed the Code as a force,

which redefined the “notion of governanceby providing the enabling framework forlocal government-business partnerships, andalso local government-NGO partnerships,including opening the door to direct peopleparticipation in governance”.

Objective of the ReportTe objective of this report is to determine

to what extent fiscal decentralization hasempowered local government units in thePhilippines to efficiently discharge the greaterresponsibility over governance, public servicedelivery and local development mandated tothem by the 1991 Local Government Code.More specifically, it provides a descriptive

analysis of fiscal decentralization in the 3 Tayao, Edmund (2010), “Decentralization in the Philippines:

Impact on Politics and Governance,” unpublished paper,December 09.

Barangays

8/12/2019 Fiscal Decentralisation in Philippines

http://slidepdf.com/reader/full/fiscal-decentralisation-in-philippines 11/56

3

CHAPTER 1INTRODUCTION

Philippines. It focuses on local governmentfiscal policies and inter-governmental fiscaltransfer and identifies local finance policyreform issues, which policy makers shouldaddress to enable local government units to

improve their local revenue-raising effort.4 Te inability to raise adequate local revenues isat the core of the problem of local governmentunits in delivering local public services. Areason behind this is the inadequate taxingpowers assigned to local government units,resulting in a vertical fiscal imbalance, whichoccurs when the central government retainscontrol over major sources of tax revenues.

Te intergovernmental fiscal transfercalled the internal revenue allotment (IRA)significantly supplements or covers theinadequacy in local revenue collection. Teallocation or distribution formula for theinternal revenue allotment stands a close reviewand improvement even as it has become themost important source of revenue for manylocal government units, especially the poorermunicipalities. Te irony is that the internal

revenue allotment may have had a disincentiveeffect on local effort to raise revenues, makingmany local government units dependent on itfor funding local development and services.Te distribution formula for the IRA shouldbe improved but Philippine local governmentunits must exert effort to raise local revenuesbecause failure to do so results in inefficientlocal service delivery and diminishedaccountability. Te IRA received by local

government units has not been adequateenough to finance comprehensive servicedelivery and local development programs.

A case can also be made about the need forlocal government units to improve local publicexpenditure management. Under-spendingon vital local public goods and servicesaffects the level of welfare of households and

4 In the Philippines, sub-national governments are called “local

government units” (LGUs), which are comprised of provinces,municipalities, cities and “barangays.” Barangays are the

smallest political unit headed by a local elective officer called“barangay captain.” Municipalities and cities are comprised of

several barangays , respectively.

negates the advantages given to decentralizedregimes of better local service delivery arisingfrom closer matching of public services withlocal preferences and greater efficiency in theprovision of public goods. A recent paper by

Llanto and Quimba (2010) provides someempirical evidence that there has not beena significant improvement in the deliveryof health and education services despitedevolution5. Teir empirical analysis seems toindicate that decentralization has not resultedin an improvement in the delivery of localservices, contrary to the popular notion, whichtends to be based on anecdotal evidence.

Te report is organized as follows. oprovide context to the discussion, Section 2provides a brief review of the concept of fiscaldecentralization and its elements based onrecent literature. Section 3 discusses the tax-expenditure assignment at the local level. Itfirst discusses the structure and compositionof local tax revenues, fees and charges andthen describes the pattern of local governmentspending with focus on health and education,

major expenditure items for which data aremore readily available. A key finding is thepresence of an inefficient tax-expenditureassignment, which has constrained theenvisaged development of local areas by localpeople utilizing local resources. Tis confirmsearlier findings of Manasan (2007) who founda mismatch between revenue resources andexpenditure needs of the various levels of localgovernment.

An issue overlooked by many localresearchers is the need for local governmentunits to exert more effort to improve localexpenditure management. Te findings ofLlanto and Quimba (2010) show that manyLGUs have been under-spending, which pointouts out the need for more efficient localexpenditure management. Te key messageof this section is the importance of providing

5 Llanto, Gilberto M. and Francis Quimba (2010),“Decentralization and Local Service Delivery,” paper preparedfor the Local Government Foundation, unpublished.

8/12/2019 Fiscal Decentralisation in Philippines

http://slidepdf.com/reader/full/fiscal-decentralisation-in-philippines 12/56

4

FISCAL DECENTRALIZATION IN THE PHILIPPINES

local government units with ample powerand authority to raise the necessary revenuesto finance local development but at the sametime, local government units must exert utmosteffort in improving local public expenditure

management. It is commonplace to hear invarious forums in the country complaintsabout the inadequacy of local resources toaddress various development challenges.Llanto and Quimba (2010) indicate that thereis room for improving service delivery evenunder a regime of constrained resources.

Section 4 analyzes intergovernmental fiscaltransfers, basically the major block fiscal

grant called the “Internal Revenue Allotment(IRA).” Te IRA is the single biggest revenueitem for many LGUs and the section points outoutstanding issues affecting the efficacy of thisfiscal tool for helping with local development.Popular discourse on this topic inevitablygravitates around suggestions to increase theIRA from its current share of 40% of nationalinternal revenue taxes to 50 percent and even60 percent with apparent disregard about the

implications of the suggestion to the financingof the country’s overall national developmentagenda. Tere is a need for an in-depthresearch and analysis of the Philippineexperience with intergovernmental fiscal

transfers, which cover both conditional andunconditional fiscal grants. Te biggest part ofthe fiscal transfers is composed of the internalrevenue allotment. Te current discourse andproposals to increase the amount of the IRA,

and at the same time change the formula for itsdistribution has to be enlightened by findingsof systematic research and study that has yet tobe undertaken. Policy makers cannot simplyrely on the narrow metric of politics to decideon this significant issue. Tere is a cryingneed to produce an evidence-based policyrecommendation on how to improve the useof this important fiscal tool.

Section 5 summarizes the status of localgovernment units’ access to developmentcapital and identifies areas for policy reform.It looks at the outstanding constraints toaccess to the capital markets and officialdevelopment assistance and sketches pathwaysto reform6. Te final section pulls together thefindings in preceding sections, and draws someconclusions and policy recommendations.

6 The major issues on access to capital markets were first presented and analyzed in Llanto, Gilberto M., and others(1998), Local Government Units’ Access to the Private CapitalMarkets, Makati City: Philippine Institute for DevelopmentStudies. Some of those issues have been resolved, many othershave remained outstanding.

8/12/2019 Fiscal Decentralisation in Philippines

http://slidepdf.com/reader/full/fiscal-decentralisation-in-philippines 13/56

5

CHAPTER 2THE CONCEPT AND ELEMENTS OF FISCAL DECENTRALIZATION

CHAPTER 2 THE CONCEPT AND ELEMENTS OFFISCAL DECENTRALIZATION7

Oates decentralization theorem

A working definition of decentralizationis that by Faguet (2005) who defines it as“the devolution by central, (that is, national)government of specific functions, with all ofthe administrative, political and economic

attributes that these entail, to democraticlocal (i.e. municipal) governments which areindependent of the center within a legallydelimited geographic and functional domain”.

A common denominator behind policymakers’ decision to decentralize and devolve isthe belief that this paradigm shift can improvethe allocation problem in the economy,improve productive efficiency and bring aboutbetter cost recovery. In the last two decades,

decentralization has been at “the center stageof policy experiments in a large number ofdeveloping and transition economies in Latin

America, Africa and Asia” (Bardhan 2003,page 1) for a number of reasons. For example,a motivation for decentralization in Latin

America was the disenchantment with militaryrule and dictatorships, which has created apolitical culture that places a premium ondecentralized decision making to prevent a

return to the past. In China, decentralization was seen as a means for social cohesion,faster economic growth and preservation ofcommunist party rule (Shah, 1997).

In the Philippines, the enactment into lawof the Local Government Code in October10, 1991, which decentralized and and

7 The brief review of literature partly draws from GilbertoM. Llanto, “Decentralization, Local Finance Reforms and

New Challenges: The Philippines,” a paper presented at theThird Symposium on Decentralization and Local Finance atthe Institute for Comparative Studies in Local Governance(COSLOG), National Graduate Institute for Policy Studies, Tokyo,

Japan on March 10, 2009.

devolved vast powers to local governmentunits, introduced a significant shift in thepolicy and institutional framework fordevelopment. In their review of Philippinedecentralization, local scholars (Brillantesand iu, 2010; ayao, 2010) noted thatthe Philippine political and administrative

system has been dominated by the centralgovernment since the time of the Spanishcolonization. A long history of centralizationmeant that policies, programs, funding,allocation of resources, etc were controlledand implemented by the central governmentsituated in Manila (somewhat derisivelycalled “imperial Manila”). Tus, 1991 LocalGovernment Code (Republic Act No. 7160)

was a critical break point in the country’s

political and administrative framework. In hisreading of recent Philippine political history,ayao (2010) called decentralization as “singlemost significant political reform after the fallof the Marcos dictatorship in 1986.”

Te thinking behind this is that greaterinvolvement of LGUs or sub-national unitsin service provision, including the provisionof basic infrastructure such as local roads,

farm-to-market roads, communal irrigationfacilities, among others, will result in betterservice delivery and accountability, provideopportunities for people participationin development, and create an enablingenvironment for local private sectorinvestments.

Proponents of decentralization claim that ithas provided a framework for responsive and

accountable local governance. According toBird (1993) it has given local constituents whatthey want and are willing to pay for, and the

8/12/2019 Fiscal Decentralisation in Philippines

http://slidepdf.com/reader/full/fiscal-decentralisation-in-philippines 14/56

6

FISCAL DECENTRALIZATION IN THE PHILIPPINES

opportunity for greater local responsivenessand political participation. It has demonstrateda potential to lead to more appropriate andbetter-utilized facilities, lower costs per unitof service and improved operations and

maintenance (Klugman 1994)8. Devolutionis based on the subsidiarity principle andrests on the view that it results in improvedefficiency in the delivery of public services, andhence a more efficient allocation of resourcesin the economy (Dabla-Norris 2006)9. Tisperspective draws from the classic distinctiongiven by Musgrave about the different tasksof government in an economy: allocation(which is better done by local governments),

stabilization and redistribution (which arebetter done by central government).

Tese views echo the decentralization theorem(Oates,1972, page 55), which maintains that“each public service should be provided by the

jurisdiction having control over the minimumgeographical area that would internalizebenefits and costs of such provision.” Oates(1993) later observes that decentralization is a

mechanism to make policy more responsive tolocal needs and to involve the local populacein processes of democratic governance10. Teeconomic case for decentralization is theenhancement of efficiency that it introducesbecause locally provided public goods,

which are more responsive to local taste andpreferences are superior to centrally determinedgoods. Decentralization provides for “tailoringlevels of consumption to the preferences of

smaller, more homogeneous groups” (Wallisand Oates 1988, page 5). Decentralizationhas laid down the foundation of a new, major“institutional framework” for the provisionof a range of benefits to local constituents

8 However, according to Klugman (1994) greater efficiency neednot necessarily accompany decentralization, given the risk ofloss of economies of scale, duplication and overlap.

9 Shah (2004) points out that the principle of subsidiaritywas introduced by the Maastricht Treaty for assignment ofresponsibilities among members of the European Union.

According to this principle, taxing, spending and regulatoryfunctions should be exercised by the lowest levels of

government unless a convincing case can be made for assigningthe same to higher levels of government.

10 While a discussion of the opposing views may be interesting,this paper will not dwell on it because it is outside the scopeand objectives of the paper.

and the harnessing of local energy for localdevelopment, which could make governmentsto be “more responsive and efficient;” at thesame time decentralization offers a practicalavenue for “diffusing social and political

tensions and ensuring local cultural andpolitical autonomy” (Bardhan 2003, page 1).

Joumard and Kongsrud (2003) add that itcan strengthen the democratic process, allowgovernments to tailor the supply of publicgoods to local preferences and introduce somecompetition across jurisdictions, thus raisingpublic sector efficiency. At the same time, itmust be recognized that it can entail efficiency

losses, and make it difficult to implementredistributive policies and complicatemacroeconomic management (ibid). Acontrarian view is that “decentralization mayincrease the participation of people at thelocal level but sometimes it is only a smallprivileged elite group who get to participate”(Conyers 1990, page 18) quoted by Oates(1993). Faguet (2005) pointing out that thereis little agreement concerning the effects of

decentralization in the empirical literature,says that pessimists argue local governmentsare too susceptible to elite capture, and toolacking in technical, human and financialresources, to produce a heterogeneous rangeof public services that are both reasonablyefficient and responsive to local demand.

For political decentralization to beeffective, it should be accompanied by

fiscal decentralization. Many years ago in apaper prepared for the World Bank AnnualConference on Development Economics,anzi (1996) observed that decentralization offiscal activities can improve the allocation ofpublic spending by making it more consistent

with local preferences. Oates (1996) cites thepotential contribution of decentralization inenhancing allocative efficiency by providinga menu of local outputs that reflects the

8/12/2019 Fiscal Decentralisation in Philippines

http://slidepdf.com/reader/full/fiscal-decentralisation-in-philippines 15/56

7

CHAPTER 2THE CONCEPT AND ELEMENTS OF FISCAL DECENTRALIZATION

varying wishes and conditions in local areas11.Furthermore, it can provide “political glue forcountries with regional ethnic diversity” (anzi1996, page 295)12. Fiscal decentralizationis not always seen as conferring unmitigated

benefits to the local populace. Fiscaldecentralization is not without its share ofcontroversy. Oates (2006) mentions someanalysis that “reveals its dark side, especiallyin practice” and that “raises some seriousquestions about its capacity to provide anunambiguously positive contribution to animproved performance of the public sector”(pages 2-3). Smoke (2001) alludes to potentialmacroeconomic dangers and growth retarding

effects of fiscal decentralization, indicatinghowever that most of the evidence is anecdotaland relevant only under particular uncommoncircumstances or focused on correctable ratherthan inherent problems.

Tis is not the place to expound on thisinteresting facet of fiscal decentralization aspointed out by Oates and others but certainlyit poses a challenge to fiscal decentralization

analysts. Suffice it to say at this point thatthere is a need for more research and theproduction of comparative information onthe extent to which and the conditions under

which the alleged benefits and disadvantagesof fiscal decentralization have been realized(Smoke 2001).13

Te decentralization theorem argues thatsub-national governments can more efficiently

provide public services to identifiablerecipients up to the point at which the value

11 Oates, Wallace (1996), “Comment on ‘Conflicts and Dilemmasof Decentralization’ by Rudolf Hommes,” in Bruno, Michaeland Boris Pleskovic, editors, Annual World Bank Conference onDevelopment Economics, Washington, D.C.: The World Bank,

pages 351-353.12 Tanzi, Vito (1996), “Fiscal Federalism and Decentralization: A

Review of Some Efficiency and Macroeconomic Aspects,” inBruno, Michael and Boris Pleskovic, editors, Annual World BankConference on Development Economics, Washington, D.C.: TheWorld Bank, pages 295-316.

13 Smoke, Paul (2001) “Fiscal Decentralization in DevelopingCountries: A Review of Current Concepts and Practice,”Democracy, Governance and Human Rights ProgrammePaper Number 2, United Nations Research Institute for Social

Development, February. Professor Smoke declares thatanecdotal evidence and case studies provide some insights butthere is a need for more policy experimentation and systematicresearch to understand the prospects for fiscal decentralizationin developing countries.

placed on the marginal amount of services for which recipients are willing to pay is just equalto the benefit they receive (Ebel and Yilmaz,2002; Oates 1972, 2006 )14 o implementthis, sub-national (local) governments must be

given the authority to exercise “own source”taxation at the margin and be in a financialposition to do so. Tis is the essence of fiscaldecentralization (Ebel and Yilmaz 2002).

Following Smoke (2001), the key elementsthat should be included in a good fiscaldecentralization program are as follows:(a) an adequate enabling environment; (b)assignment of an appropriate set of functions

to local governments; (c) assignment of anappropriate set of local own-source revenuesto local governments; (d) the establishmentof an adequate intergovernmental fiscaltransfer system; and (d) the establishmentof adequate access of local governments todevelopment capital.

An adequate enabling policy

environmento begin with an enabling policy

environment for fiscal decentralization, whichis clearly stated in constitutional mandateor law, defining some minimum level ofautonomy, rights and responsibilities forlocal governments is important. Te return ofdemocratic governance in the Philippines afterthe 1986 People Power Revolution following

a long period of martial rule in the 70s and80s has provided an enabling environment fordecentralization. Te series of freely electeddemocratic governments since then havecontinued to recognize that it is good for afunctioning democracy to allow local leadersand people to have the power and responsibilityof deciding what goods and services to

14 Robert D. Ebel, Robert and Serdar Yilmaz (2002), “On theMeasurement and Impact of Fiscal Decentralization,” Policy

Research Working Paper 2809, The World Bank, March;Oates, Wallace (2006), “On the Theory and Practice of FiscalDecentralization,” IFIR Working Paper No. 2006-05, May;Oates, Wallace E. 1972. Fiscal Federalism. New York: HarcourtBrace Jovanovich

8/12/2019 Fiscal Decentralisation in Philippines

http://slidepdf.com/reader/full/fiscal-decentralisation-in-philippines 16/56

8

FISCAL DECENTRALIZATION IN THE PHILIPPINES

produce and finance. Te enactment into lawof the 1991 Local Government Code signals amajor departure from the traditionally centristapproach to governance and development indeveloping countries, which view the problem

of development as one requiring the presenceof a strong central government that will laydown policy directions and allocate resourcesaccordingly. It may be recalled that before theabove-mentioned period of martial rule, there

were a series of policy reforms leading towardlocal autonomy.

Atienza (2006) related the quest fordecentralization and autonomy in a recent

study 15

. Te 1991 Local Government Codemay be a radical piece of legislation but itis not the first decentralization law in thecountry and it passed after five years of debatein Congress (Uchimura and Suzuki 2009)16.Guevara (2004) recounted that in 1959 theLocal Autonomy Act (Republic Act 2264)

was passed to grant fiscal and regulatorypowers to local governments. In 1967, theDecentralization Act (Republic Act 5185)

increased the financial resources and powersof local governments. Te 1973 Constitutionof the Philippines mandated that the state“shall guarantee and promote the autonomyof local governments to ensure their fullestdevelopment as self-reliant communities.”Martial rule stymied those reform efforts.Te 1991 Local Government Code, then,“institutionalized a systematic allocation ofpowers and responsibility between the national

and local governments” (Guevara 2004, page1)17. Te 1991 Local Government Code wasa landmark legislation that gave rise to a majorshift in local governance (Manasan 2007).Te Code consolidated and amended theLocal Government Code of 1983, the Local

15 Atienza, Maria Ela (2006), “Local Governments and Devolutionin the Philippines,” in Noel Morada and Teresa Encarnacion,editors, Philippine Politics and Governance: An Introduction,Department of Political Science, University of the Philippines.

16 Uchimura, Hiroko and Yurika Suzuki (2009), “Measuring FiscalDecentralization in the Philippines,” IDE Discussion Paper No.209, Institute of Developing Economies, July.

17 Guevara, Milwida (2004), “The Fiscal Decentralization Processin the Philippines: Lessons from Experience,” http://www.econ.hit-u.ac.jp/~kokyo/APPPsympo04/PDF-papers-nov/guevara-i2004-revised2.pdf , date accessed August 29, 2011.

ax Code (Presidential Decree 231), and theReal Property ax Code (Presidential Decree464).

In the Philippines, the 1991 Local

Government Code devolved to localgovernment units the responsibility ofdelivering local and basic public servicesand raising local or own-source revenuesfor financing their expenditure assignment.Under the Local Government Code, localgovernment units have autonomy in decidingon the composition of local spending, taxingand borrowing that they would need to meetlocal development objectives. Tus, local

government units are now responsible for thefollowing areas: land use planning, agriculturalextension and research, community-based forestry, solid waste disposal system,environmental management, pollutioncontrol, primary health care, hospital care,social welfare services, local buildings andstructures, public parks, municipal servicesand enterprises such as public markets andabattoirs, local roads and bridges, health

facilities, housing, communal irrigation, watersupply, drainage, sewerage, flood control andinter-municipal telecommunications.

Te Local Government Code also transferredto local government units certain regulatoryfunctions. Te fiscal transfers to localgovernments were likewise increased, with40% of internally generated taxes allocatedto local governments through the Internal

Revenue Allotment (IRA). In addition, theCode encouraged the local government unitsto explore alternative sources of revenue byexercising their corporate powers in partnership

with the private sector. An innovationintroduced by the Code is the provision ofa framework for active participation of non-governmental organizations and civil societyin local governance18. Indeed, the new

18 For a detailed discussion, see Brillantes, Alex, GilbertoM. Llanto, James Alm and Gaudioso Sosmena (2009),“Decentralization and Devolution in the Philippines: Status,Triumphs, Tests and Directions,” Report submitted to theDepartment of the Interior and Local Government, unpublished

paper, April 29

8/12/2019 Fiscal Decentralisation in Philippines

http://slidepdf.com/reader/full/fiscal-decentralisation-in-philippines 17/56

9

CHAPTER 2THE CONCEPT AND ELEMENTS OF FISCAL DECENTRALIZATION

institutional framework for local developmenthas generated an enthusiastic response on thepart of local government units (LGUs) todeliver better public services to local citizens.It has promoted local autonomy by devolving

expenditure responsibilities and vested greatertaxing powers on local government units19.

19 The paper does not discuss the Organic Act of MuslimMindanao, which transfers to the regional government of theAutonomous Region of Muslim Mindanao all powers, functions,and responsibilities heretofore being exercised by the centralgovernment except (a) foreign affairs, (b) national defense, (c)postal service, (d) fiscal and monetary policy, (e) administrationof justice, (f) quarantine, (g) citizenship, naturalization andimmigration, (h) general auditing, civil service and elections,(i) foreign trade, (j) maritime, land and air transportation andcommunications that affect areas outside the ARMM, and(k) patents, trademarks, trade names and copyrights. For a

discussion see Manasan (2005).

Te succeeding sections of this paperfirst outline the current status of (a)the tax-expenditure assignment, (b) theintergovernmental fiscal transfer (IRA), and(c) the access of local government units to

development capital through borrowing, andthen highlight outstanding issues or problems

which should be addressed by policy makers.

8/12/2019 Fiscal Decentralisation in Philippines

http://slidepdf.com/reader/full/fiscal-decentralisation-in-philippines 18/56

10

FISCAL DECENTRALIZATION IN THE PHILIPPINES

8/12/2019 Fiscal Decentralisation in Philippines

http://slidepdf.com/reader/full/fiscal-decentralisation-in-philippines 19/56

11

CHAPTER 3TAX-EXPENDITURE ASSIGNMENT

A principal challenge faced by LGUsis finding the means to raise adequatefinancing for local development. Te LGUsare a heterogeneous group with varyingadministrative, financial and technicalcapacities. Tere is also great variation in thelevel of local development with the few highly

urbanized cities enjoying bigger and morebuoyant tax bases. Te rest of the LGUs arecomposed of smaller cities and municipalities

with weaker local economies. Provinces arealso a heterogeneous lot with great variationin economic, administrative, financial, andtechnical capacities. Te rising expectationsof the local populace for more and betterquality public services has to be matched bythe ability of local government units to find

substantial funding and to have better andmore efficient implementation of programsand project for local development. Te 1991Local Government Code assigned taxing andspending powers to local government units. Itis an acknowledged principle that matchingexpenditure and tax assignments is desirablebecause this will enable the local governmentsto shape the supply of public goods accordingto local preferences and willingness to pay

(Jourmard and Kongsrud 2003)20.

o assess the fiscal performance of the LGUs,time series data covering pre-decentralizationperiod (1989-1991) up to the present weretabulated21 Income data were obtained fromthe Statement of Income and Expenses (SIE)

while expenditure data were from the SAAOB(previously called Schedule of Appropriations

20 Joumard, Isabelle and Per Mathis Kongsrud. 2003. “Fiscal

relations across government levels.” Economics DepartmentWorking Papers No. 375, Organization for EconomicCooperation and Development, December 10.

21 Sources: Commission on Audit’s Annual Financial Reports forLocal Government Units

and Expenditures) from the Commission on Audit’s Annual Financial Reports for LocalGovernment Units for the years 1989 to 2009.

Local government tax revenues:trend and composition, 1989-2009

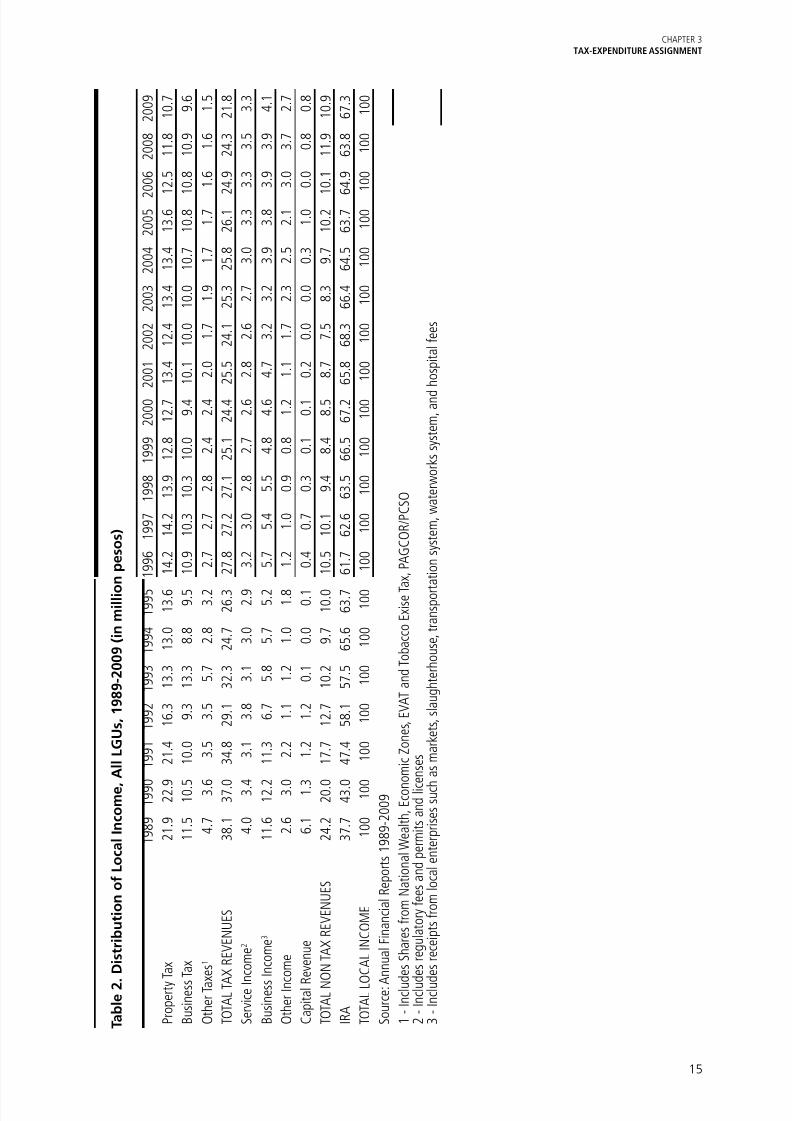

able 1 summarizes the various taxes thatare assigned to local government units bythe Local Government Code. Te Codehas empowered local government units toset local tax rates and collect own-sourcerevenues. Only cities and provinces can levythe real property tax. Te former shares theproceeds with their barangays while provincesshare the proceeds with the municipalities and

barangays. Both provinces and cities are also authorized to impose a tax on the transfer ofreal property, sand, gravel, and other quarryresources; amusement places; franchises;professionals; delivery vans and trucks; andidle lands. On the other hand, municipalitiesand cities, but not provinces, are allowed tolevy the community tax and the local businesstax (i.e.,turnover tax levied on the grossreceipts of businesses/traders)22.

Te main sources of local incomes arethe IRA, property tax, the business tax, andservice and business income from various localeconomic enterprises. However, Section 133 ofthe Code also provides a detailed list of taxes,

22 The first tier of government is the central government whichoperates through departments (ministries). The second tierof government is composed of local government units (LGUs)and one autonomous region, the ARMM. In general, the local

government structure is composed of three layers. Provincescomprise the first layer. In turn, the province is divided intomunicipalities and component cities, each of which is further

subdivided into barangays, the smallest political unit. At the same time, independent cities (or highly urbanized cities) existat the same level as the provinces, i.e., they share the samefunctions and authorities. Independent cities are divided directlyinto barangays (Manasan 2005).

CHAPTER 3 TAX-EXPENDITURE ASSIGNMENT

8/12/2019 Fiscal Decentralisation in Philippines

http://slidepdf.com/reader/full/fiscal-decentralisation-in-philippines 20/56

12

FISCAL DECENTRALIZATION IN THE PHILIPPINES

which are revenue-productive but which onlythe central government can impose. Teseinclude the individual and corporate income

taxes, customs duties, value-added tax, and theexcise taxes on alcoholic beverages, tobaccoproducts and petroleum products.

Table 1. Tax assignment in cities, provinces and municipalities

Tax base Cities Provinces Municipalities Barangays

Transfer of real property X X

Business of printing and publication X X

Franchise X X

Sand, gravel and other quarry resources X X * *

Amusement places X X *

Professionals X X

Real property X X * *

Delivery vans and trucks X XIdle lands X X

Business X X X

Community tax X X *

*shares in the proceeds of levy of province

Local generated revenues are basically thetax revenues and non-tax revenues obtainedfrom regulatory fees, service charge, incomefrom local enterprises and other receipts. Teshare of local own source revenues and non-tax revenues to total LGU income was at 62percent in 1989, decreasing over time. In2009, it stood at 33 percent. As IRA’s sharein the total LGU income increased throughthe years, tax revenues and non-tax revenues’share decreased. Please see able 2 and Figure3. From 38 percent in 1989 ax Revenuesshares dropped to 29 percent in 1992, andto 22 percent by 2009. As for the Non-axRevenues, from 24 percent in 1989 it wasdown to 13 percent in 1992. By 2002 Non-ax Revenue was at its lowest at 7.5 percent,then slowly picked up and was 11 percent by2009.

Tax Revenues includes Property Tax, BusinessTax and Licenses and Other Taxes . Propertyax is composed of real property tax, propertytransfer tax, real property tax on idle lands,special assessment tax and special educationtax. Under Property Tax , the major one is thereal property tax. Provinces can levy a realproperty tax not exceeding 1% of the assessedvalue of the real property. For cities, the realproperty tax rate should not exceed 2% of theassessed value of the real property. Te LocalGovernment Code defines the maximumassessment level for each type of real property(Box 1). Te assessment level varies from localgovernment to local government based onlocal ordinances passed by the legislative body(“sanggunian”).

8/12/2019 Fiscal Decentralisation in Philippines

http://slidepdf.com/reader/full/fiscal-decentralisation-in-philippines 21/56

13

CHAPTER 3TAX-EXPENDITURE ASSIGNMENT

Box 1. Assessment level by type of land

Assessment level on lands % (maximum under Local Government Code)

Residential 20%

Commercial 50%

Industrial 50%

Mineral 50%

Timberland 20%

Te Local Government Code defines“assessed value” (AV) as the fair marketvalue of the real property multiplied by theassessment level. It is synonymous to taxablevalue. Te assessment level is the percentage

applied to the fair market value to determinethe taxable value of the property. On the otherhand, “fair market value” is defined by theLocal Government Code as fair market value”as the price at which a property may be soldby a seller who is not compelled to sell andbought by a buyer who is not compelled tobuy. Te real property tax (RP) is computedas follows:

RP = AV x rate.

Buyers of real property pay a one-timeproperty transfer tax when title to a realproperty passes on to them. Te specialeducation tax is an additional 1% tax on theassessed value of real property in additionto the basic real property tax. A specialassessment tax on real property may be leviedto address a local development goal23. On theother hand, the real property tax on idle lands

has generally not been implemented by localgovernment units due to political constraints.

Business tax and licenses, or taxes on goodsand services in other years, includes businesstax, franchise tax, occupation tax, printingand publication taxes, tax on fishing vesselsand tax on delivery trucks and vans amongothers. Under the category of Other Taxes are

23 Recently Quezon City, one of the largest highly urbanized cities

imposed a special levy of 0.5 percent on residential lots withan assessed value of Pesos 100,000.00 (approximately US$2, 325.00 at the current exchange rate of Pesos 1 to US$ 1) tofinance the construction of housing for informal settlers in thecity..

community tax, amusement tax, tax on sandand gravel and other quarry products, etc.Non-Tax Revenues on the other hand consistsof Service Income, Business Income , Other Income and Capital Revenues . Service Income

is classified as Government Services andOperating and Service Income in earlier years,and Service Income + Permits and Licenses inlater years. Business Income includes incomefrom local economic enterprises or LEESsuch as markets, slaughterhouses, waterworksand transportation systems, and hospital feesamong others. Other Income consists of LGUShares from National Wealth, EconomicZones, EVA and obacco Exise ax, and

other miscellaneous income. Capital Revenues are mainly income from the sale of assets butin later years it also included receipts fromthe sale of confiscated goods and properties,disposed assets, securities and gains fromforeign exchange.

Te Property ax has been the largestcontributor when it comes to own-sourcerevenues with a share of 22 percent in 1989,followed by Business axes and Licenses andBusiness Income both at 10 percent but lateryears especially after devolution, show thatIRA has become a dominant source. Pleasesee Figure 4. Te local government unitsdepended more on the IRA and this haseroded the effort of local government units tocollect own-source revenues. For many localgovernment units, it is much easier to just relyon the IRA transfer than it is to collect real

property taxes and business taxes

24

.

24 The disincentive effect of IRA is discussed in succeeding paragraph below.

8/12/2019 Fiscal Decentralisation in Philippines

http://slidepdf.com/reader/full/fiscal-decentralisation-in-philippines 22/56

8/12/2019 Fiscal Decentralisation in Philippines

http://slidepdf.com/reader/full/fiscal-decentralisation-in-philippines 23/56

15

CHAPTER 3TAX-EXPENDITURE ASSIGNMENT

T a b l e 2 . D i s t r i b u t i o n o f L o c a l I n c o m e ,

A l l L G U s , 1 9 8 9 - 2 0 0 9 ( i n m i l l i o

n p e s o s )

1 9 8 9

1 9 9 0

1 9 9 1

1 9 9 2

1 9 9 3

1 9 9 4

1 9 9 5

1 9 9 6

1 9 9 7

1 9 9 8

1 9 9 9

2 0 0 0

2 0 0 1

2 0 0 2

2 0 0 3

2 0 0 4

2 0 0 5 2

0 0 6

2 0 0 8

2 0 0 9

P r o p e r t y

T a x

2 1 . 9

2 2 . 9

2 1 . 4

1 6 . 3

1 3 . 3

1 3 . 0

1 3 . 6

1 4 . 2

1 4 . 2

1 3 . 9

1 2 . 8

1 2 . 7

1 3 . 4

1 2 . 4

1 3 . 4

1 3 . 4

1 3 . 6

1 2 . 5

1 1 . 8

1 0 . 7

B u s i n e s s

T a x

1 1 . 5

1 0 . 5

1 0 . 0

9 . 3

1 3 . 3

8 . 8

9 . 5

1 0 . 9

1 0 . 3

1 0 . 3

1 0 . 0

9 . 4

1 0 . 1

1 0 . 0

1 0 . 0

1 0 . 7

1 0 . 8

1 0 . 8

1 0 . 9

9 . 6

O t h e r T a x e s 1

4 . 7

3 . 6

3 . 5

3 . 5

5 . 7

2 . 8

3 . 2

2 . 7

2 . 7

2 . 8

2 . 4

2 . 4

2 . 0

1 . 7

1 . 9

1 . 7

1 . 7

1 . 6

1 . 6

1 . 5

T O T A L T A

X R E V E N U E S

3 8 . 1

3 7 . 0

3 4 . 8

2 9 . 1

3 2 . 3

2 4 . 7

2 6 . 3

2 7 . 8

2 7 . 2

2 7 . 1

2 5 . 1

2 4 . 4

2 5 . 5

2 4 . 1

2 5 . 3

2 5 . 8

2 6 . 1

2 4 . 9

2 4 . 3

2 1 . 8

S e r v i c e I n c o m e 2

4 . 0

3 . 4

3 . 1

3 . 8

3 . 1

3 . 0

2 . 9

3 . 2

3 . 0

2 . 8

2 . 7

2 . 6

2 . 8

2 . 6

2 . 7

3 . 0

3 . 3

3 . 3

3 . 5

3 . 3

B u s i n e s s

I n c o m e 3

1 1 . 6

1 2 . 2

1 1 . 3

6 . 7

5 . 8

5 . 7

5 . 2

5 . 7

5 . 4

5 . 5

4 . 8

4 . 6

4 . 7

3 . 2

3 . 2

3 . 9

3 . 8

3 . 9

3 . 9

4 . 1

O t h e r I n c o m e

2 . 6

3 . 0

2 . 2

1 . 1

1 . 2

1 . 0

1 . 8

1 . 2

1 . 0

0 . 9

0 . 8

1 . 2

1 . 1

1 . 7

2 . 3

2 . 5

2 . 1

3 . 0

3 . 7

2 . 7

C a p i t a l R

e v e n u e

6 . 1

1 . 3

1 . 2

1 . 2

0 . 1

0 . 0

0 . 1

0 . 4

0 . 7

0 . 3

0 . 1

0 . 1

0 . 2

0 . 0

0 . 0

0 . 3

1 . 0

0 . 0

0 . 8

0 . 8

T O T A L N O N T A X R E V E N U E S

2 4 . 2

2 0 . 0

1 7 . 7

1 2 . 7

1 0 . 2

9 . 7

1 0 . 0

1 0 . 5

1 0 . 1

9 . 4

8 . 4

8 . 5

8 . 7

7 . 5

8 . 3

9 . 7

1 0 . 2

1 0 . 1

1 1 . 9

1 0 . 9

I R A

3 7 . 7

4 3 . 0

4 7 . 4

5 8 . 1

5 7 . 5

6 5 . 6

6 3 . 7

6 1 . 7

6 2 . 6

6 3 . 5

6 6 . 5

6 7 . 2

6 5 . 8

6 8 . 3

6 6 . 4

6 4 . 5

6 3 . 7

6 4 . 9

6 3 . 8

6 7 . 3

T O T A L L O

C A L I N C O M E

1 0 0

1 0 0

1 0 0

1 0 0

1 0 0

1 0 0

1 0 0

1 0 0

1 0 0

1 0 0

1 0 0

1 0 0

1 0 0

1 0 0

1 0 0

1 0 0

1 0 0

1 0 0

1 0 0

1 0 0

S o u r c e : A

n n u a l F i n a n c i a l R e p o r t s 1 9 8 9 - 2 0 0 9

1 - I n c l u d e s S h a r e s f r o m N a t i o n a l W e a l t h ,

E c o n

o m i c Z o n e s , E V A T a n d T o b a c c o E x i s e T a x ,

P A G C O R / P C S O

2 - I n c l u d e s r e g u l a t o r y f e e s a n d p e r m i t s a n d l i c e n s e s

3 - I n c l u d e s r e c e i p t s f r o m l o c a l e n t e r p r i s e s s u c h

a s m a r k e t s , s l a u g h t e r h o u s e ,

t r a n s p o r t a t i o n s y s t e m ,

w a t e r w o r k s s y s t e m ,

a n d

h o s p i t a l f e e s

8/12/2019 Fiscal Decentralisation in Philippines

http://slidepdf.com/reader/full/fiscal-decentralisation-in-philippines 24/56

16

FISCAL DECENTRALIZATION IN THE PHILIPPINES

Figure 4: Distribution of Total Income, all LGUs, 1989-2009 (%)

Property Tax Business Tax Other Taxes Service Income

Business Income Other Income Capital Revenue IRA

-10 0 10 20 30 40 50 60 70 80

2009

2008

2006

2005

2004

2003

2002

2001

2000

1999

1998

1997

1996

1995

1994

1993

1992

1991

1990

1989

8/12/2019 Fiscal Decentralisation in Philippines

http://slidepdf.com/reader/full/fiscal-decentralisation-in-philippines 25/56

17

CHAPTER 3TAX-EXPENDITURE ASSIGNMENT

Figures 5 and 6 compare the source ofincome of LGUs before (1990) the passage ofthe 1991 Code and after several years (2009).Te broad taxing powers benefited more thecities than provinces and municipalities. Tey

have been dominant in all types of local taxesand the internal revenue allotment. Te citieshave also the advantage of getting higher

amounts of IRA individually because there arefewer of them to divide the pie, so to speak.Tis has motivated municipalities to of gettinghigher amounts of IRA individually becausethere are fewer of them to divide the pie, so

to speak. Tis has motivated municipalitiesto convince legislators to pass special lawsconverting them into cities.

Figure 5: Distribution of Income by type of LGU, 1990

Provinces Cities Municipalities

80

70

60

50

40

30

20

10

0Property

taxBusiness

taxOthertaxes

ServiceIncome

BusinessIncome

OtherIncome

IRA TotalIncome

Figure 6: Distribution of Income by type of LGU, 2009

Provinces Cities Municipalities

80

70

60

50

40

30

20

10

0

Propertytax Businesstax Othertaxes ServiceIncome BusinessIncome OtherIncome IRA TotalIncome

8/12/2019 Fiscal Decentralisation in Philippines

http://slidepdf.com/reader/full/fiscal-decentralisation-in-philippines 26/56

18

FISCAL DECENTRALIZATION IN THE PHILIPPINES

An examination of revenue figures over theperiod 1989-2009 indicates a significant declinein the share of provinces and municipalities intotal LGU own-source revenue. Tis contrasts

with the continuous increase in the share

of cities in total LGU own-source revenue. An outstanding problem faced by provincesand municipalities is how to raise substantialrevenues when they do not have very productivetax bases to begin with. Te 1991 Code haveput certain limits on their taxing powers.Cities are more fortunate because they havebroader taxing powers than municipalities andprovinces. Please see able 1 above.

Because of an inefficient tax assignment,it is only the cities, which have the capacityto raise the needed revenues. As Manasan(2007) has observed the distribution ofown-source revenues is in favor of cities,and partly in favor of municipalities awayfrom provinces25. Te cities have larger taxbases and consequently, buoyant revenuesources but the majority of local governmentunits, that is, the municipalities have weaker

tax bases and thus, do not raise sufficientown-source revenues. Tey have remaineddependent on fiscal transfers, principally theinternal revenue allotment (IRA) for fundinglocal development activities.

Te dominance of IRA as revenue sourceis very obvious. Provinces and municipalities

25 Manasan, Rosario (2007), “Decentralization and Financingof Regional Development,” in Balisacan, Arsenio and Hal Hill,editors, The Dynamics of Regional Development: The Philippinesin East Asia, Quezon City: Ateneo de Manila University Press.

are most dependent on IRA. In an extremecase, the IRA allocations sometimes accountfor 95 percent of local revenues and, in at leastone case, 114 percent of total expenditures(ADB 2005)26. Te dependence on IRA

results in weaker local fiscal autonomy, whichcreates opportunities for greater control by thecentral government, contrary to the envisagedsituation of local governments able to respondto local needs and to match local outputs

with local preferences. o wean themselvesaway from central government control localgovernment units should strive for greater fiscalautonomy by working to significantly improveown-source revenues. Improving the collection

of real property and local business taxes is animportant step to boost local fiscal autonomy.

Limits on sub-national governmentdiscretion to determine tax rates and tax basessignificantly reduce local fiscal autonomy(Joumard and Kongsrud 2003).

Various researchers such as Manasan, Cuenca,Uchimura and Suzuki, Capuno, and Llanto,

among others have noted the inefficiency intax assignment to local government units inthe Philippines. Manasan (2005) provides agood summary 27 as shown in Box 2.

26 Asian Development Bank (2005), Decentralization in thePhilippines: Strengthening Local Government Financing &Resource Management in the Short Term, Mandaluyong City:

Asian Development Bank 27 Manasan, Rosario G. 2005. “Local Public Finance in the

Philippines: lessons in autonomy and accountability.” Philippine Journal of Development. Second Semester 2005, Vol. XXXIINo. 2: 32-102.

Box 2. An assessment of tax assignment to local government units

• Te Philippine tax assignment appears to be largely consistent with the traditional viewof tax assignment.

• It scores low on the autonomy criterion because (a) the Code fixes the tax rate of some ofthe taxes that are assigned to LGUs; (b) the Code sets limits (floors and ceilings) on thetax rates that LGUs may impose and maximum allowable rates are rather low; (c) in termsof real property assessment levels, the Code sets maximum assessment rates for different

classes of property; (d) the Code mandates that tax rates can only be adjusted once in fiveyears and by no more than 10 percent.

8/12/2019 Fiscal Decentralisation in Philippines

http://slidepdf.com/reader/full/fiscal-decentralisation-in-philippines 27/56

19

CHAPTER 3TAX-EXPENDITURE ASSIGNMENT

Tere are current legislative bills to modifythe taxing powers of LGUs, e.g., Senate Bill1458, which recommends transferring themandate to tax sand, gravel, and other quarryresources to cities and municipalities. HouseBill 1607 seeks to give additional sources ofrevenue to provinces by requiring componentcities to share their collection from realproperty taxes with the provinces. Tese

proposals should be carefully examined inview of the inequities in tax assignments andthe IRA allocation formula.

LOCAL GOVERNMENTEXPENDITURES: TREND ANDCOMPOSITION, 1989-200328

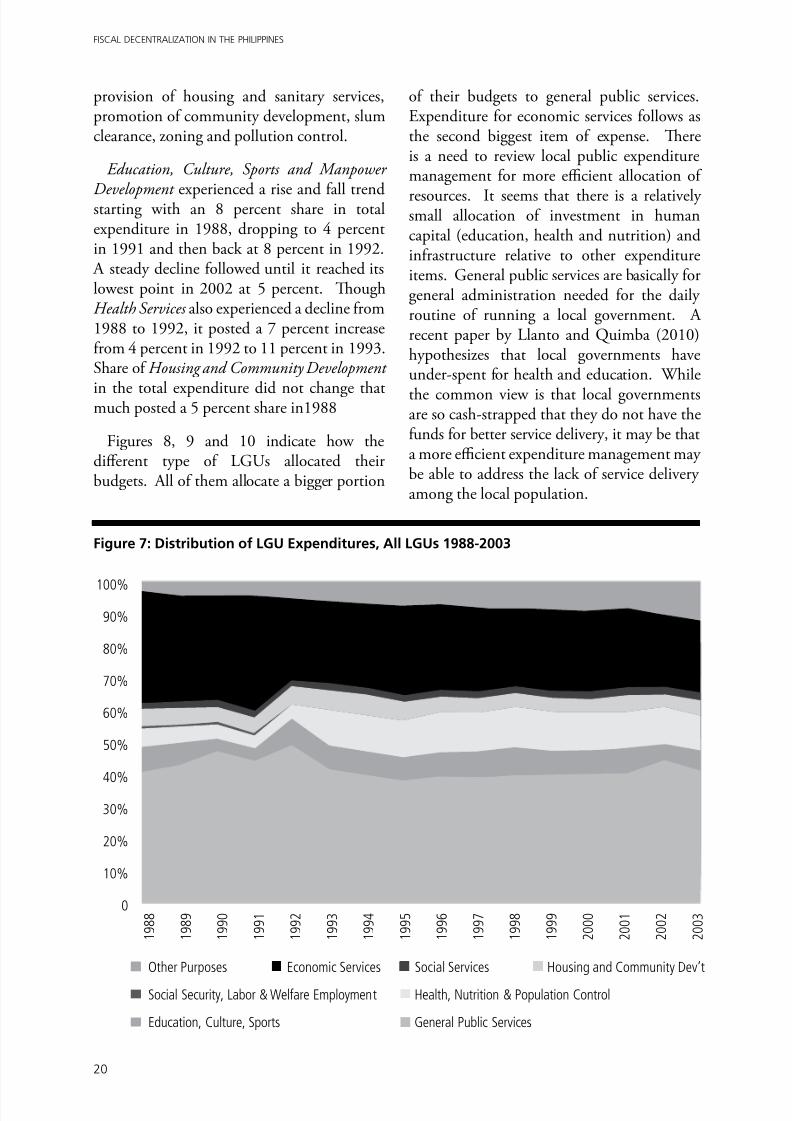

able 3 and Figure 7 show that local

governments spent most of their resources onGeneral Public Services. General Public Services (GPS) include the essential requirements torun the government such as the executiveand legislative services, treasury, assessment,budgeting and auditing services, propertyand supply administration, and informationservices. GPS is highest in the late 80s thruearly 90s, reaching its peak at 49 percent in

28 The period covered does not include the following years:

2004-2009 because of noise in the latter years. There is a needto review the Schedule of Appropriation, Allotment, Obligationand Balances (SAAOB) for local government units especially inview of the recent shift to the New Government AccountingSystem (NGAS).

1992. In 1993 it dropped to 40 percent andmaintained this level in the following years.

Te second largest local governmentexpense is on Economic Services with a shareof 35 percent in 1989 which steadily declinedthrough the years, with only 22 percent shareto total LGU expenditures by 2003.Economic Services refers to activities directed

towards the promotion and enhancementand the attainment of desired economicgrowth. Included in this category areagricultural, veterinary and natural resourceservices, architectural and engineeringservices, operation of local enterprises suchas markets, slaughter house, transportationand waterworks among others, cooperativeprograms, livelihood projects and othereconomic development programs.

Rounding up the major components of LGUexpenditure are education and health servicesand housing and community development.Education, Culture, Sports and ManpowerDevelopment covers expenditures for thesupport of schools and education facilities,planning and manpower development, sports,cultural preservation and enrichment. HealthServices pertains to expenditures for national

health programs including medical, dental andnutrition services. Housing and CommunityDevelopment includes expenditures for the

• Future Code amendments should consider giving LGUs greater discretion in setting taxrates by raising the maximum allowable tax rates.

• Tere is a need to move away from tax rates that are not indexed to inflation.

• Tere is a need to simplify the structure of local business tax because different categoriesof firms are subject to different rate schedules.

• Tere is a need to improve the tax administration machinery of local governments, e.g.,employ certified public accountants to improve tax audit capability; use automation toimprove revenue performance, etc.

• Tere is a need to revise the schedule of market values for real property purposes because manyprovinces and cities have done a general revision of such schedules only once since 1991.

• Tere is a need for many LGUs to revise their tax codes since only a few have made

revision since 1992 even if some tax rates are not indexed to inflation.

8/12/2019 Fiscal Decentralisation in Philippines

http://slidepdf.com/reader/full/fiscal-decentralisation-in-philippines 28/56

20

FISCAL DECENTRALIZATION IN THE PHILIPPINES

provision of housing and sanitary services,promotion of community development, slumclearance, zoning and pollution control.

Education, Culture, Sports and Manpower

Development experienced a rise and fall trendstarting with an 8 percent share in totalexpenditure in 1988, dropping to 4 percentin 1991 and then back at 8 percent in 1992.

A steady decline followed until it reached itslowest point in 2002 at 5 percent. ToughHealth Services also experienced a decline from1988 to 1992, it posted a 7 percent increasefrom 4 percent in 1992 to 11 percent in 1993.Share of Housing and Community Development

in the total expenditure did not change thatmuch posted a 5 percent share in1988

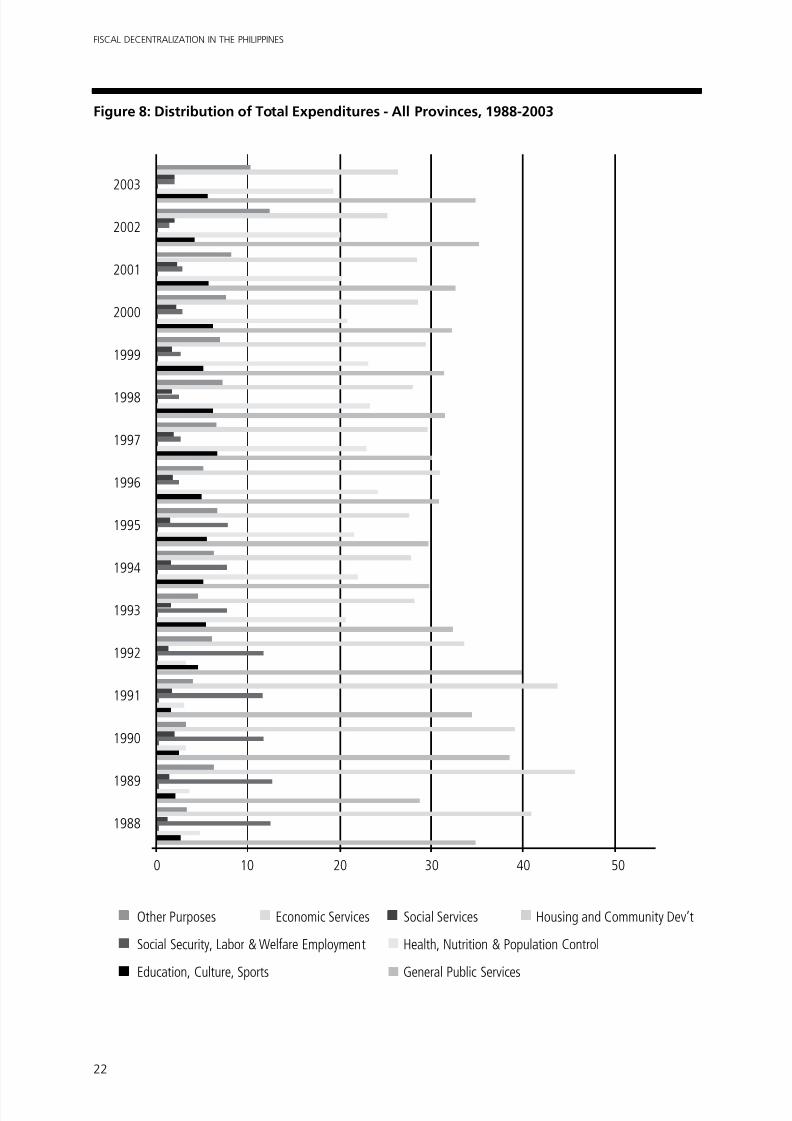

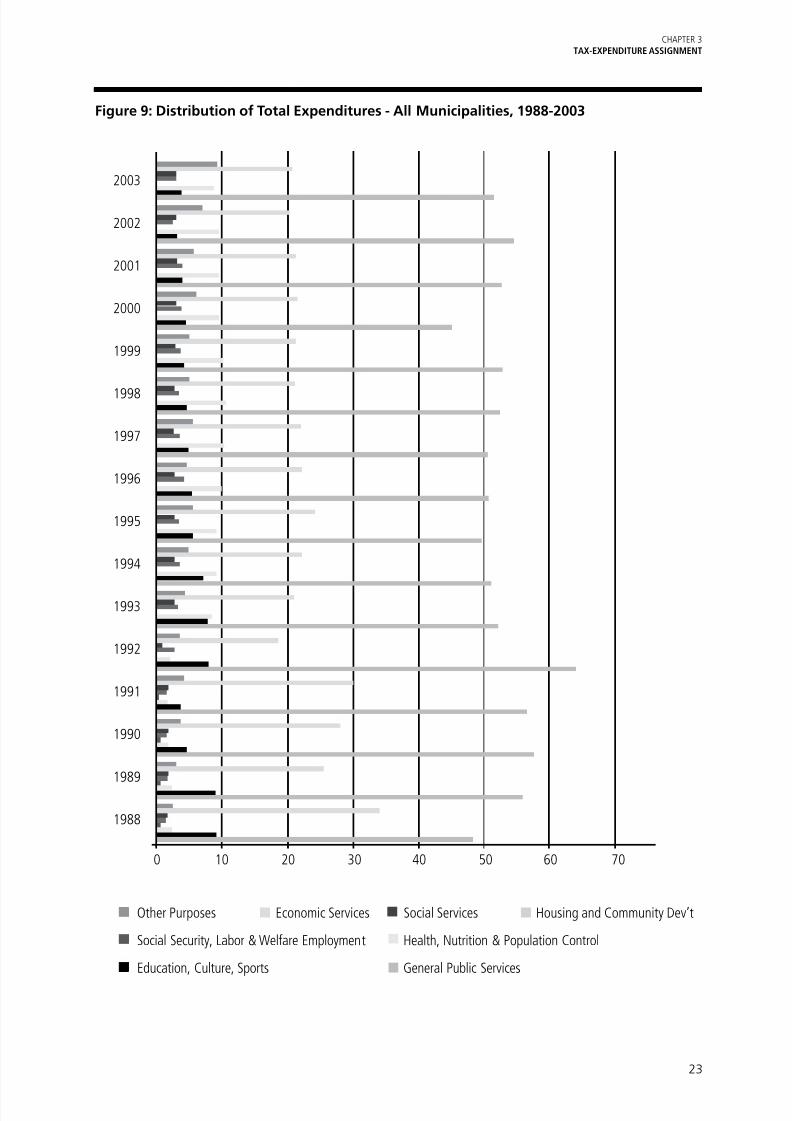

Figures 8, 9 and 10 indicate how thedifferent type of LGUs allocated theirbudgets. All of them allocate a bigger portion

of their budgets to general public services.Expenditure for economic services follows asthe second biggest item of expense. Tereis a need to review local public expendituremanagement for more efficient allocation of

resources. It seems that there is a relativelysmall allocation of investment in humancapital (education, health and nutrition) andinfrastructure relative to other expenditureitems. General public services are basically forgeneral administration needed for the dailyroutine of running a local government. Arecent paper by Llanto and Quimba (2010)hypothesizes that local governments haveunder-spent for health and education. While

the common view is that local governmentsare so cash-strapped that they do not have thefunds for better service delivery, it may be thata more efficient expenditure management maybe able to address the lack of service deliveryamong the local population.

100%

90%

80%

70%

60%

50%

40%

30%

20%

10%

0

1 9 8 8

1 9 8 9

1 9 9 0

1 9 9 1

1 9 9 2

1 9 9 3

1 9 9 4

1 9 9 5

1 9 9 6

1 9 9 7

1 9 9 8

1 9 9 9

2 0 0 0

2 0 0 1

2 0 0 2

2 0 0 3

Figure 7: Distribution of LGU Expenditures, All LGUs 1988-2003

Other Purposes Economic Services Social Services Housing and Community Dev’t

Social Security, Labor & Welfare Employment Health, Nutrition & Population Control

Education, Culture, Sports General Public Services

8/12/2019 Fiscal Decentralisation in Philippines

http://slidepdf.com/reader/full/fiscal-decentralisation-in-philippines 29/56

21

CHAPTER 3TAX-EXPENDITURE ASSIGNMENT

T a b l e 3 .

D i s t r i b u t i o n o f L G U E x p e n d i t

u r e s , A l l L G U s , 1 9 8 8 - 2 0 0 3

1 9 8 8

1 9 8 9

1 9 9 0

1 9 9 1

1

9 9 2

1 9 9 3

1 9 9 4

1 9 9 5

1 9 9 6

1 9 9 7

1 9 9 8

1 9 9 9

2 0 0 0

2 0 0

1

2 0 0 2

2 0 0 3

G R A N D T

O T A L

1 0 0

1 0 0

1 0 0

1 0 0

1 0 0

1 0 0

1 0 0

1 0 0

1 0 0

1 0 0

1 0 0

1 0 0

1 0 0

1 0

0

1 0 0

1 0 0

G E N E R A L P U B L I C S E R V I C E S

4 0 . 8

8

4 3 . 1

9

4 7 . 3

2

4 4 . 5

3

4 9 . 3

2

4 1 . 7

7

4 0 . 0

2

3 8 . 3

6

3 9 . 4 4

3 9 . 2

0

3 9 . 8

7

3 9 . 9

3

4 0 . 4

1

4 0 . 6

6

4 4 . 4

2

4 1 . 2

5

E D U C A T I O N , C

U L T U R E ,

S P O R T S

8 . 0

1

6 . 7

8

3 . 9

4

3 . 5

8

8 . 0

9

7 . 3

5

7 . 1

1

7 . 1

6

7 . 5 4

8 . 0

6

8 . 5

9

7 . 4

5

7 . 3

5

7 . 5

9

5 . 2

4

6 . 3

0

H E A L T H ,

N U T R I T I O N & P O P U L A T I O N C O N T R O L

5 . 5

3

4 . 9

4

4 . 5

5

4 . 1

9

4 . 3

4

1 1 . 1

5

1 1 . 6

0

1 1 . 4

1

1 2 . 4 3

1 2 . 1

8

1 2 . 6

6

1 2 . 2

2

1 1 . 5

8

1 1 . 4

3

1 1 . 4

3

1 0 . 8

5

S O C I A L S

E C U R I T Y , L A B O R & W E L F A R E

E M P L O Y M E N T

0 . 7

4

0 . 6

4

0 . 7

1

0 . 7

0

0 . 1

2

0 . 0

3

0 . 0

8

0 . 0

7

0 . 0 7

0 . 0

8

0 . 0

5

0 . 0

3

0 . 0

4

0 . 0

2

0 . 0

3

0 . 0

2

H O U S I N G

& C O M M U N I T Y D E V ’ T

5 . 3

7

5 . 3

1

4 . 5

8

4 . 8

3

5 . 7

6

5 . 9

6

6 . 1

2

5 . 7

8

4 . 8 4

4 . 3

5

4 . 2

3

4 . 3

9

4 . 2

8

5 . 1

1

3 . 9

2

4 . 7

9

S O C I A L S

E R V I C E S

1 . 6

7

1 . 9

5

2 . 2

1

2 . 1

3

1 . 6

6

2 . 3

2

2 . 1

5

2 . 0

6

2 . 1

9

2 . 1

8

2 . 2

2

2 . 1

9

2 . 3

4

2 . 4

5

2 . 2

9

2 . 4

2

E C O N O M

I C S E R V I C E S

3 4 . 9

6

3 2 . 8

4

3 2 . 2

4

3 5 . 7

6

2 5 . 4

9

2 5 . 4

8

2 6 . 2

9

2 7 . 6

2

2 6 . 6

0

2 5 . 9

5

2 4 . 0

9

2 5 . 1

9

2 5 . 0

4

2 4 . 5

6

2 2 . 3

0

2 2 . 3

6

O T H E R P U R P O S E S

2 . 8

3

4 . 3

6

4 . 4

5

4 . 2

7

5 . 2

2

5 . 9

5

6 . 6

3

7 . 5

2

6 . 8

9

8 . 0

1

8 . 2

8

8 . 6

0

8 . 9

6

8 . 1

9

1 0 . 3

7

1 2 . 0

1

8/12/2019 Fiscal Decentralisation in Philippines

http://slidepdf.com/reader/full/fiscal-decentralisation-in-philippines 30/56

22

FISCAL DECENTRALIZATION IN THE PHILIPPINES

Other Purposes Economic Services Social Services Housing and Community Dev’t

Social Security, Labor & Welfare Employment Health, Nutrition & Population Control

Education, Culture, Sports General Public Services

Figure 8: Distribution of Total Expenditures - All Provinces, 1988-2003

2003

2002

2001

2000

1999

1998

1997

1996

1995

1994

1993

1992

1991

1990

1989

1988

0 10 20 30 40 50

8/12/2019 Fiscal Decentralisation in Philippines

http://slidepdf.com/reader/full/fiscal-decentralisation-in-philippines 31/56

23

CHAPTER 3TAX-EXPENDITURE ASSIGNMENT

Figure 9: Distribution of Total Expenditures - All Municipalities, 1988-2003

Other Purposes Economic Services Social Services Housing and Community Dev’t

Social Security, Labor & Welfare Employment Health, Nutrition & Population Control

Education, Culture, Sports General Public Services

2003

2002

2001

2000

1999

1998

1997

1996

1995

1994

1993

1992

1991

1990

1989

1988

0 10 20 30 40 50 60 70

8/12/2019 Fiscal Decentralisation in Philippines

http://slidepdf.com/reader/full/fiscal-decentralisation-in-philippines 32/56

24

FISCAL DECENTRALIZATION IN THE PHILIPPINES

Figure 10: Distribution of Total Expenditures - All Cities, 1988-2003

Other Purposes Economic Services Social Services Housing and Community Dev’t

Social Security, Labor & Welfare Employment Health, Nutrition & Population Control

Education, Culture, Sports General Public Services

2003

2002

2001

2000

1999

1998

1997

1996

1995

1994

1993

1992

1991

1990

1989

1988

0 10 20 30 40 50

8/12/2019 Fiscal Decentralisation in Philippines

http://slidepdf.com/reader/full/fiscal-decentralisation-in-philippines 33/56

25

CHAPTER 3TAX-EXPENDITURE ASSIGNMENT

A joint study by the Asian DevelopmentBank and the World Bank in 2005 pronouncedthat overall the devolution of expenditureresponsibilities to LGUs is consistent with theprinciple of subsidiarity (ADB 2005)29. Te

report also noted that few devolved activitieshave spillover benefits outside LGU territorial

jurisdictions and that the Code allowed LGUsto regroup into larger cooperative units whenthey deem appropriate. As proof, it citedseveral cases of inter-LGU cooperation incoastal resource management, solid wastemanagement, water supply developmentand distribution, and construction of inter-municipal roads. Metropolitan arrangements

have also appeared in several places. Loehrand Manasan (1999) find that the devolutionof expenditure responsibilities to LGUs isgenerally consistent with the decentralizationtheorem. Te devolved activities are those “thatcan be provided at lower levels of government. . . and few of them have benefits that spillover outside the territorial jurisdiction ofthe LGUs with exception of those related toenvironmental management” (Manasan 2005,

page 37)30.

During the period after the enactment ofthe Local Government Code, there seems tobe a marked increase in LGU spending asmore resources had been made available toLGUs. A JICA study (2008) notes that the topthree service areas where improvement withdevolution was noted in sample provinces,cities and municipalities are: 1) social welfare;

2) health and nutrition; and 3) agricultureand fisheries. Undoubtedly the changesbrought about the passage of the 1991 LocalGovernment Code have resulted in an increasein LGU spending.

On the other hand, whether there has been anoverall improvement of public service delivery,governance and local development now thatthese functions are with local government

29 Asian Development Bank (2005), Decentralization in thePhilippines: Strengthening Local Government Financing &Resource Management in the Short Term, Mandaluyong City:

Asian Development Bank 30 An exception is education (Manasan, 2005).

units is an empirical question. Tere has beenan improvement in public service delivery butperhaps not in a significant way for all localgovernment units. Llanto and Quimba (2010)report recent findings of a survey conducted

by the Philippine Institute for DevelopmentStudies, namely that:

• For health, despite more than 10 yearsafter devolving this function to localgovernment units, there is still an overlap inthe provision of services by LGUs and thenational government. LGUs still have notfully built capacity to provide better healthcare services. Finally, LGUs and the central

government’s Department (Ministry) ofHealth have not clearly identified cost-sharing and assignment of functionsregarding delivery of health service.

• For education, the School BasedManagement approach which centers ongiving the authority to school principals andinvolving parents and other stakeholders inschool decisions is a good start for properphasing and right-sizing of functions yet

to be devolved. However, there is need forclear and proper delineation of functions,capacities and funds between local andnational offices.

• For LGUs to better manage their own water resources there is a need for a cleardelineation of powers, functions, andresponsibilities, institutional development,and source of financing.

Pending better data and the conduct ofmore systematic and in-depth studies, thereseems to be at best only anecdotal evidencesupporting claims of improvement in servicedelivery in several local government units.

For example, Klugman (1994) reportsa Philippine study by Jimenez and others(1988) that for given levels of enrolmentand quality, schools which rely more heavily

on local funding are more efficient. Tereis a lower cost of delivery of educationservices. Tey also find that students at

8/12/2019 Fiscal Decentralisation in Philippines

http://slidepdf.com/reader/full/fiscal-decentralisation-in-philippines 34/56

26

FISCAL DECENTRALIZATION IN THE PHILIPPINES

schools which relied more heavily upon localfunding had better ‘achievement scores’. Aspecial education fund, a surcharge on taxeson real property is administered by thelocal school board composed of the school

principal, local government representativeand parents. Te ADB (2005) noted agrowing number of examples of excellencein service delivery, which seem to indicatethat well-performing local governments maybe distinguished by their ability to accessresources more effectively, and managethem more transparently and accountably.

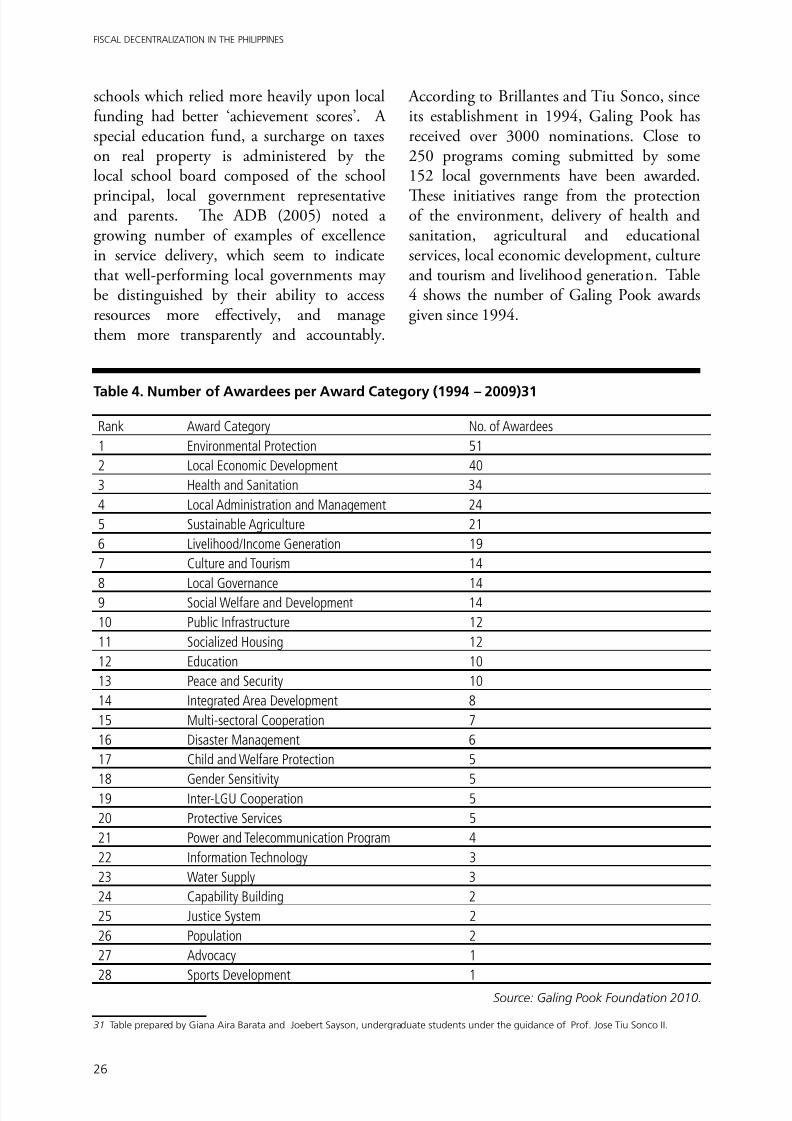

According to Brillantes and iu Sonco, sinceits establishment in 1994, Galing Pook hasreceived over 3000 nominations. Close to250 programs coming submitted by some152 local governments have been awarded.

Tese initiatives range from the protectionof the environment, delivery of health andsanitation, agricultural and educationalservices, local economic development, cultureand tourism and livelihood generation. able4 shows the number of Galing Pook awardsgiven since 1994.

Table 4. Number of Awardees per Award Category (1994 – 2009)31

Rank Award Category No. of Awardees

1 Environmental Protection 51

2 Local Economic Development 40

3 Health and Sanitation 34

4 Local Administration and Management 24

5 Sustainable Agriculture 21

6 Livelihood/Income Generation 19