FISCAL ACCOUNTABILIT Y PLAN FOMILENIO II

122

1 FISCAL ACCOUNTABILITY PLAN FOMILENIO II Effective June 15, 2020

Transcript of FISCAL ACCOUNTABILIT Y PLAN FOMILENIO II

1

FISCAL ACCOUNTABILITY PLAN

FOMILENIO II

Effective June 15, 2020

Fiscal Accountability Plan –FOMILENIO II

2

Index 1 General Provisions ........................................................................................................... 5

1.1 The MCC’s Fiscal Accountability Framework ................................................................................. 6 1.2 MCC Cost Principles ....................................................................................................................... 8 1.3 Fiscal Agent .................................................................................................................................. 10 1.4 Authorized Parties ....................................................................................................................... 11 1.5 Authorized personnel for Procurement, Financial and Administrative Management Affairs ..... 12 1.6 Updates to the FAP ...................................................................................................................... 12

2 Budgets ......................................................................................................................... 14 2.1 Initial Budget................................................................................................................................ 14 2.2 Start and Approval of Budget Changes ........................................................................................ 14

3 Financial Plans, Disbursement Requests and Report Packages ........................................ 15 3.1 Multi-Year Financial Plan and Adjustments to the Multi-Year Financial Plan ............................. 16 3.2 Disbursement Requests and Reporting Packages ....................................................................... 20 3.3 SAP Procedures ............................................................................................................................ 27 3.4 Indefinite Delivery / Indefinite Quantity Contracts (IDIQ Contracts) .......................................... 28

4 Permitted Bank Accounts and the Common Payment System ......................................... 29 4.1 FOMILENIO II Local Banking Accounts ......................................................................................... 30 4.2 MCC’s Common Payment System (CPS) ...................................................................................... 31 4.3 Fiscal Agent’s responsibilities – Permitted Accounts and Common Payment System ................ 31 4.4 Exclusive Nature of the Accounts ................................................................................................ 32 4.5 Interest on Permitted Accounts .................................................................................................. 32

5 Budget Implementation & Financial Control ................................................................... 32 5.1 Control System ............................................................................................................................ 33

6 Procurement .................................................................................................................. 33 6.1 Public Procurement Plan ............................................................................................................. 34 6.2 Procurement Implementation Plan (PIP) ..................................................................................... 34 6.3 Procurement Performance Report (PPR) .................................................................................... 34 6.4 Launching the Procurement Process ........................................................................................... 35 6.5 Requisition of Purchase/Requisition Form .................................................................................. 35 6.6 Requisition of Purchase Evaluation and Approval ......................................................... 35 6.7 Small value purchases not included in the MCC Public Procurement Guidelines (NPC purchases)36 6.8 Charges for Tender Related Documentation ............................................................................... 38 6.9 Crosschecking a Supplier/Provider’s Eligibility ............................................................................ 39 6.10 Record of Financial Contractual Commitments ........................................................................... 39

Fiscal Accountability Plan –FOMILENIO II

3

6.11 Distribution of Contract documents and Record Management .................................................. 40 6.12 Awarding Bids / Offers over the Estimated Budget ..................................................................... 40 6.13 Advance Payments ...................................................................................................................... 41 6.14 Reconciling the Commitment’s Information ............................................................................... 42 6.15 Delivery Certificates of Goods or Services ................................................................................... 42 6.16 SAP procedures ............................................................................................................................ 43

7 Payment Processing ....................................................................................................... 45 7.1 Common Payment System (CPS) ................................................................................................. 48 7.2 Payments ..................................................................................................................................... 50 7.3 Deadline to Pay Providers ............................................................................................................ 53 7.4 Payment Authorization Limits ..................................................................................................... 54 7.5 Expiration of Payment Authority at the End of a Period ............................................................. 55 7.6 Reinstating the Payment Limit Authority .................................................................................... 55

8 Taxes ............................................................................................................................. 56 9 Cash Management ......................................................................................................... 57

9.1 Estimating Cash Requirements .................................................................................................... 58 9.2 Disbursements ............................................................................................................................. 59 9.3 Banking Reconciliation................................................................................................................. 60 9.4 Petty Cash .................................................................................................................................... 61 9.5 Fuel Vouchers .............................................................................................................................. 64

10 Accounting and Submitting Reports ............................................................................... 65 10.1 Accounting System ...................................................................................................................... 65 10.2 Account Catalogue ....................................................................................................................... 66 10.3 Accounting Regulations ............................................................................................................... 66 10.4 Monthly Reports .......................................................................................................................... 66 10.5 Quarterly Reports ........................................................................................................................ 67 10.6 Special Reports ............................................................................................................................ 67 10.7 Programming, Purpose and Publishing Reports .......................................................................... 67 10.8 Ret Withholding of Records ......................................................................................................... 68 10.9 Publishing Financial Reports ........................................................................................................ 68 10.10 SAP Procedures ............................................................................................................................ 68

11 Travels and vehicle use .................................................................................................. 69 11.1 Official International travels ........................................................................................................ 69 11.2 Official Local travels ..................................................................................................................... 72

12 Payroll and Personnel Administration ............................................................................ 76 12.1 Staffing plan ................................................................................................................................. 76 12.2 Definition of Management Team (Key Personnel) ...................................................................... 76 12.3 Appointment................................................................................................................................ 77 12.4 Terms of Employment ................................................................................................................. 77 12.5 Payroll .......................................................................................................................................... 78

Fiscal Accountability Plan –FOMILENIO II

4

12.6 SAP Procedures ............................................................................................................................ 80 13 Asset Management ........................................................................................................ 80

13.1 Legal Requirements for Assets Management .............................................................................. 81 13.2 Labeling assets ............................................................................................................................. 81 13.3 Record and maintenance of the Fixed Asset Register ................................................................. 81 13.4 Inventory ..................................................................................................................................... 82 13.5 Insurance ..................................................................................................................................... 83 13.6 Use of Assets................................................................................................................................ 83 13.7 Removing Fixed Assets due to damages, obsolescence, or robbery ........................................... 83 13.8 Asset Control during Compact Closure ........................................................................................ 84 13.9 Reassignment of Fixed Assets from one employee to another ................................................... 84 13.10 Transferring Assets and Terms of Use for Implementing Entities ............................................... 85 13.11 Handover process ........................................................................................................................ 85

14 Audit/Reviews ............................................................................................................... 86 14.1 Internal Audits ............................................................................................................................. 86 14.2 Other Audit Reviews of FOMILENIO II ......................................................................................... 86 14.3 External Audits ............................................................................................................................. 87 14.4 Submitting reports on the Improper Use of FOMILENIO II Funds or Assets. ............................... 87

15 Additional guidance on specific expenditures ................................................................. 88 15.1 Public Outreach and Events ......................................................................................................... 88 15.2 Resettlement Action Plan and Rights of way Payments .............................................................. 90 15.3 Payments to members of the Dispute Adjudication Boards (Conflict Resolution Tables - MRC) of FIDIC contracts. ......................................................................................................................................... 91

16 Annex List ...................................................................................................................... 91 16.1 ANNEX 1 – Approval and Support Matrix .................................................................................... 91 16.2 ANNEX 2– MCC Procedures to Submit Reports on Fraud and Corruption Allegations ............... 94 16.3 ANNEX 3 – Accounting and finance Codes .................................................................................. 96 16.4 ANNEX 4 – Petty Cash Counts ...................................................................................................... 99 16.5 ANNEX 5 – Delegation of Responsibilities Memo ...................................................................... 100 16.6 ANNEX 6 – Request for fuel voucher – Implementing Entities .................................................. 101 16.7 ANNEX 7 – Resettlement Action Plan (RAP) Payment Process .................................................. 102 16.8 ANNEX 8 – Special Reports (Data Call)....................................................................................... 105

Fiscal Accountability Plan –FOMILENIO II

5

1 General Provisions The Fiscal Accountability Plan (henceforth FAP) is a document focused on implementation, drafted as defined in section 3(a)(i) of Annex I of the Compact and Section 2.2 of the Program Implementation Agreement (PIA), meant to be used by FOMILENIO II, which is an Autonomous Institution created through Legislative Decree number 839, dated October 31st of 2014, to establish the principles, mechanisms and procedures meant to ensure an appropriate auditing process throughout the use of all funds provided by the Millennium Challenge Corporation (MCC). The FAP shall comply in every aspect with the MCC’s Cost Principles, and must include, amongst other things, the principles, mechanisms and procedures for the following core issues: (a) budgeting, (b) accounting, (c) cash management, (d) financial transactions (billing and payment), (e) opening and managing permitted accounts, (f) personnel management and payroll, (g) travel, allowances and the use of vehicles, (h) assets and inventory control, (i) audits and (j) reports. Essentially, the FAP is a financial operations manual, and is applicable to every activity financed by the MCC and/or the Salvadoran Government while at the same time serving as FOMILENIO II’s Internal Control Manual. All operating units (meaning, Management, the projects themselves, Fiscal Agent, the Procurement Agent, implementing partners, consultants, vendors and contractors) must follow and implement the policies and procedures described in this document. Therefore, this document will become the basis to evaluate both performance and development during FOMILENIO II audits conducted by internal and external auditors as well as the Fiscal Supervision Agent. At no time will any provision be able to go against the contents of the Compact or any other supplementary agreement. The FAP will be formally updated every six months to include any amendments to existing policies or to add new policies which may have been approved, as well as to compile work experiences throughout the implementation process taking place between each of the revisions. If necessary, it may also include provisional amendments (between each six month revision period) which will then be formalized and shared with FOMILENIO II personnel through “Administrative Memos” signed by the Executive Director. The Fiscal Agent will ensure these amendments are later brought up for approval, in the manner later determined by this document.

Fiscal Accountability Plan –FOMILENIO II

6

1.1 The MCC’s Fiscal Accountability Framework

The term “Fiscal Accountability” refers to the proper use and tracking which must take place of all financial Program Resources. It is based in a solid internal control system which is able to properly register, classify and report on every expense made. FOMILENIO II honors the trust and needs of all stakeholders given its responsibility over the Program’s vital resources.

Source: GAO MCC Data Analysis Note: MCC audits and reviews may occur anywhere within the framework. MCC may disburse the Convention funds directly to FOMILENIO II through the US Treasury Department System, or to the contractual parties, such as contractors, suppliers or project managers, with the approval of FOMILENIO II. Alternatively, MCC may disburse funds to the permitted accounts of FOMILENIO II, of which FOMILENIO II may reimburse the funds to its contracted parties.

http://www.gao.gov/new.items/d1052.pdf

Fiscal Accountability Plan –FOMILENIO II

7

The different stages of financial management, including budgeting, treasury, payments, accounting and all reporting will be conducted in accordance with the Accounting Standards Generally Accepted by Government Institutions. Deviations from Generally Accepted Accounting Principles FOMILENIO II has adopted certain accounting conventions that are deviations from generally accepted accounting principles for the following expenditures:

• All asset purchases are recorded as final expenditures and not recorded on the balance sheet. No depreciation is recorded.

Method of Accounting FOMILENIO II will follow the modified cash based accounting method for the recording and reporting of financial transactions

FOMILENIO II implemented SAP, a procurement and accounting managing system standardize by MCC which serves as the basis for audit and financial reports. FOMILENIO II shall produce auditable reports for audits of FOMILENIO II and for all other interested parties through this system. SAP shall be utilized by the FISCAL AGENCY UNIT to carry out the accounting and financial records of FOMILENIO II and to comply with MCC information requirements for the issuance of Financial Statements, Quarterly Financial Reports and other regulatory reports, as well as the information requirements specific to FOMILENIO II and the Government of El Salvador. MCC authorized the use of the informatics application SAFI while implementing SAP, since the SAFI Act is not applicable according to the Agreement. Manual registration, according to FAP principles are allowed for the implementation of 609g funds. Accounting mechanisms shall have:

• Record commitments to obligate budgeted funds; • Record disbursements, and assets and liabilities; • Generate reports as requested including current summary statement of accounts and

ad-hoc reports and in the formats specified by FOMILENIO II; • Produce financial reports for FOMILENIO II on the administration and management of

the Program; • Produce financial reports to MCC as specified;

Fiscal Accountability Plan –FOMILENIO II

8

• Ensure data security, and, where possible, provide on-line user-friendly access to FOMILENIO II and MCC.

1.2 MCC Cost Principles The MCC has a guiding principle which determines the cost principles applicable to an Accountable Entity, and Implementing Entity, a Fiscal Agent or a Procurement Agent, funded in whole or in part, by donations provided by MCC, unless otherwise specified in writing by the MCC directly. FOMILENIO II will base its operations in the Cost Principles established on the MCC Cost Principles for Government Affiliates, currently available in the following link: https://www.mcc.gov/resources/doc/guidance-cost-principles-for-government-affiliates The Cost Principles provide a framework in which cost elements may be identified or determined as “allowed” by the Donations being provided by the MCC, while also fulfilling the following criteria: 1. Be necessary and reasonable for the performance, monitoring and evaluation, or oversight

of a Program funded by a MCC Grant and be allocable thereto under these principles.

A “Reasonable Cost” are all those costs, that by its nature and amount, it does not exceed that which would be incurred by a prudent person, considering their responsibilities to the MCC Grant Agreement and the public-at-large, under the circumstances prevailing at the time the decision was made to incur the cost. In determining the reasonableness of a given cost, consideration must be given to: a) whether the cost is of a type or amount generally recognized as ordinary and necessary for the operation of the Government Affiliate and the proper and efficient performance of the MCC Grant, b) the restraints or requirements imposed by such factors as sound business practices, arm's length bargaining, applicable United States and Recipient Country laws and regulations, and the terms and conditions of the MCC Grant Agreement, c) market prices for comparable goods or services that are commercially reasonable for the geographic area; and, d) whether the Government Affiliate significantly deviates from established practices and policies of the Recipient Country Government regarding the incurrence of costs, which may unjustifiably increase cost. A “Necessary Cost” are all costs incurred in to fulfill the project’s purposes. All necessary costs must conform to: (a) the terms in the program’s funding agreement, as well as any other arrangements made, including advanced negotiations concerning any cost item; (b) all program regulations concerning costs; (c) all policies and procedures applicable to FOMILENIO II; and (d) all generally accepted accounting principles (GAAP). An example of a necessary cost would be the payment of airline tickets for FOMILENIO II personnel attending a workshop to discuss program objectives. An example of a non-necessary cost would be paying for airfare for the Manager’s family so they can visit the tourist sites of the location where the workshop will be held.

Fiscal Accountability Plan –FOMILENIO II

9

2. Conform to any limitations or exclusions set forth in this Policy, the Program Procurement

Guidelines, or any other provision or guidance required as part of the MCC Grant Agreement as to types or amount of cost items.

3. Be accorded consistent treatment in not being charged more than once to an MCC Grant. A cost may not be assigned to an MCC Grant as a direct cost if any other cost incurred for the same purpose in like circumstances has been allocated to the MCC Grant as an indirect cost.

4. Be allocable. A cost is allocable to a particular MCC Grant if the goods, works, and services involved are chargeable or assignable to that MCC Grant in accordance with relative benefits received. To be allocable, a cost must meet one of the following criteria: a) Is incurred specifically for the development, implementation, or closeout of the MCC

Grant Agreement; b) Benefits both the Program funded by the MCC Grant Agreement and other activities of

the Government Affiliate, and can be distributed in proportions that may be approximated using reasonable methods; or

c) Is necessary for the overall operation of the Government Affiliate and is assignable in part to the MCC Grant Agreement in accordance with this Policy.

A cost is “allocable” to a program if it is incurred specifically for the project/program, or if it is a shared cost which can be distributed to the program in reasonable proportion to the benefit received by the program. The Administrative and Financial Management/ Fiscal Agency must be careful when allocating cost to project or activities. The cost must be necessary in carrying out the program objectives and have a direct connection to the program activities. It is prohibited to charge cost based on estimates.

5. Be accounted for based on internationally accepted accounting practices or policies and

procedures of the recipient country;

6. Be incurred within the MCC Grant period, or as may be otherwise provided in the MCC Grant Agreement.

7. Be properly documented; and

Fiscal Accountability Plan –FOMILENIO II

10

The only acceptable proof that a charge to a project is allocable, reasonable, and necessary is adequate documentation. The documentation trail begins with the program agreement, and includes others supporting documentation, including vendor bids, receipts, etc. that document a clear link between the authorization and the expenditure. This could be either paper or paperless trail. FOMILENIO II offices must also document their unusual and customary business practices related to payroll, purchasing, vendor bids, internal controls, and other key financial management policies. Expense vouchers must describe the purpose of the expenditure, be properly approved, show sector source codes, project codes, account codes, activity codes, and have appropriate supporting documentation to substantiate the charge to the program.

8. Not be excluded as an unallowable cost under Section 5.3 of the Cost Principles for

Government Affiliates, or represent payment to an ineligible source per requirements of the Program Procurement Guidelines.

Depending on the facts and circumstances, certain cost elements of the Program may not be completely allowable. Therefore, it’s important that the Cost Principles for Government Affiliates are read and clearly understood, and that all updates to said Principles are also included in the FAP, as well as any amendments which may take place from time to time.

1.3 Fiscal Agent For the majority of Accountable Entities the Fiscal Agent is an outsourced unit, which given its independence is able to provide a degree of financial control. FOMILENIO II has therefore included a Fiscal Agent unit (from hereinafter referred to as a “Fiscal Agent”) within its Financial Management Unit, alongside the Manager of Finances, also acting as a Fiscal Agent. A certain degree of independence is maintained structuring the services for the Financial Department or the Financial Management as a whole. The contract’s terms of reference for the MF/FA, establish the role of the Fiscal Agent as a service provider as follows:

• Act as a Fiscal Agent for the Financial Management Unit and certify key documents identified in the Fiscal Accountability Plan (FAP) and public procurement guidelines for MCC’s program.

• Act as an authorized firm to manage all MCC funding. • Manage budget reallocations (re-distribute the budget between activities) as well as the

corresponding presentation and justification before FOMILENIO II’s senior management for a final approval.

• Carry out all activities pertaining to financial management in areas such as Treasury and Accounting.

Fiscal Accountability Plan –FOMILENIO II

11

• Carry out the role of financial management based on the Compact. • Comply with all internal control guidelines as well as with all of the Financial

Management Unit’s rules and regulations.

1.4 Authorized Parties Individuals authorized to partake in affairs concerning the financial administration on FOMILENIO II’s behalf are all those mentioned in ANNEX 1 – Approval and Support Matrix, who may only be replaced with MCC’s prior approval. All financial administration activities require signed approval from the authorized individuals. Document approval during procurement processes, as well as managing the resulting contracts within the Procurement Plan’s Framework is all regulated within Annex 1. Approval Requirements established by the MCC Program Procurement Guidelines. Other non-explicit approval activities within the Guidelines and for Procurement activities not included in PPG will be carried out by the delegated authorities based on ANNEX 1- Approval and Support Matrix. Approval authority cannot be delegated to a subordinate official except to provide back-up as a result of absence, leaves, medical incapacity, vacations, travel abroad, etc. In said cases, approval authority can only be delegated to a subordinate official at an immediate lower level and must be registered in writing, providing detailed information as to the fact that this is only a back-up due to temporary absence. In absence of an authorized subordinate official to approve a given transaction, an approval may always be delegated to the immediate superior level, to a supervisor without requiring written approval ANNEX 5 – Task Delegation Memo. For any and all delegation of authority, whenever the authority to sign is entrusted to someone else, the official entrusted with said task must sign their own name and the name of the person they’re signing on behalf of ie. “[Name of person 1]” on behalf of [Name of Person 2].” The person signing must never directly use the name of the official delegating approval authority. Role assignment and authorized transactions by role are documented in the positions and roles matrix (FOM II - SOD - SAP Positions and Functions). The final approved version can be found in Annex 1 of the IT Administrative Procedures and Policies.

Fiscal Accountability Plan –FOMILENIO II

12

1.5 Authorized personnel for Procurement, Financial and Administrative Management Affairs

Individuals authorized to participate in financial, procurement and financial administration affairs on behalf of FOMILENIO II are the following:

a) The AF will serve as the main official within FOMILENIO II responsible for the agency’s financial administration and fulfillment of the FAP and any Agreements here mentioned. In his or her absence, the Deputy Manager of Financial Administration is the principal official responsible for financial management and the administrative activities related to the compliance with the FAP.

b) The Public Procurement Manager / Procurement Agent will act as the main official

within FOMILENIO II responsible for any activities concerning procurement and fulfillment of the Public Procurement Guidelines for MCC’s program (PPG) and Procurement guidelines for low value procurement not included in PPG. The Public Procurement Manager/Public Procurement Agent will be responsible of managing the flow of procurement activities under the FOMILENIO II Program. The main role of the Public Procurement Manager/ Public Procurement Agent shall be to coordinate procurement activities conducted by FOMILENIO II, MCC and other entities, keep records of all procurement activities and report on the progress of said activities. In his or her absence, the Procurement Specialist – Consultants is the principal official responsible for procurement activities and the fulfillment of the Public Procurement Guidelines for MCC´s program (PPG).

c) The Administration and Finances Deputy Manager (SGA) is responsible for managing

FOMILENIO II’s Human Resources and Assets, managing the revolving fund, or petty cash the per diem policies and the coordination, among other activities.

1.6 Updates to the FAP Biannual updates to the FAP Given that FAP is a guideline for all financial and administrative activities, it is highly likely that during its implementation, some aspects require to be modified. Any issue faced during direct

Fiscal Accountability Plan –FOMILENIO II

13

application, for example, situations concerning procedures, will be described in writing by the person responsible of that particular area in FOMILENIO II for later review. Any amendments to FOMILENIO II’s basic documents (for example the main Compact or in the Supplementary ones) may also give way to changes in the rules and regulations included within the FAP. The FAP will be formally updated every six months, based on experience and the ever changing institutional environment. Every official biannual FAP update must be duly approved by FOMILENIO II’s Board of Directors, and there must be no objections issued by the MCC. Suggested modifications must be made in writing and go through a series of internal checks to guarantee their compliance with the terms of the main Compact as well as with the supplementary ones. Anyone requesting changes within the FAP must:

a) List the discrepancies between reality in the field and ongoing procedures; b) Provide the above mentioned list to an immediate supervisor; c) Suggest alternatives, referencing the governing documents (Main Compact,

supplementary agreements, legislation, etc.), procedures used in similar projects operating in the same area, legal practice in the field, etc; and

d) Forward said list and the above mentioned alternatives to the Fiscal Agent.

The Executive Director, Fiscal Agent, Procurement Agent and Legal Advisor with the support of MCC Fiscal Director:

1. Shall review suggested modifications and analyze them in light of the governing documents (Compact, Supplementary agreements, Legislation);

2. Shall carry out consultations and collect additional information from applicants to verify that the suggested modifications adequately address their request;

3. Shall submit proposed changes to the MCC’s Fiscal Director for an informal review; 4. Shall include MCC’s comments and modifications in the proposed revision; 5. Shall submit a revised draft of the FAP for approval of FOMILENIO II’s Board of Directors 6. Shall submit a revised draft of the FAP to the MCC for a formal non-objection;

After this procedure, the updated FAP shall enter into effect and replace all previous versions, being the only valid document in force.

The MCC’s Fiscal Director and the Fiscal Agent will guarantee that the FAP is periodically updated, in order to reflect the program’s operational changes. Provisional Updates to the FAP through Administrative Memorandums

Fiscal Accountability Plan –FOMILENIO II

14

Between each semi-annual FAP review and update, it may be required to issue amendments for existing policies or to issue completely new policies in answer or anticipation of changing circumstances. These amendments must be issued through a formal notice (Administrative Memorandums) issued by the Executive Director and with the MCC’s non-objection. During the FAP’s bi-annual update, these provisional Administrative Memorandums will be included in the FAP, forming a full instructions manual, filled with provisional instructions. Once the stipulations of the provisional Administrative Memorandums are included in the following FAP review, said Memorandums will expire, and be rendered ineffective.

2 Budgets

2.1 Initial Budget Original budgets are shown in the “Financial Grant Plan 609(g)” included in Annex II of the 609 (g) Donation Agreement and the “Multi-year Financial Plan” (MYFP) included in Annex II of the Compact, where the budget to finance the execution of the project is detailed (CIF) and the budget of the Compact.

2.2 Start and Approval of Budget Changes Changes on the budget for 609g section funds, as well as CIF/Agreement Budget funds must comply with the MCC’s approval requirements, as later described. There is no possibility of increasing the general amount of funds for the MCC, 609g and the CIF/Agreement, therefore, any increases experienced by any given activity must be compensated by and equivalent reduction in other activities. In a normal procedure, the sequence for the start and approval of budget activities will begin by updating the Detailed Financial Plans (DFP). Said sequence will be as follows: a) The requesting unit will determine any variation of the total estimated costs for a specific

sub-activity from the original (or revised) budgets. The requesting unit will then provide FOMILENIO II, after discussing it with the Procurement Manager/ Public Procurement agent and all stakeholders, shall provide to the General Manager, a revised estimate for all expenses during a given period based on the 609g Agreement or the CIF/Agreement, alongside an explanation of the reasons for the changes experienced and the steps taken or that may be implemented to avoid any further increase in costs. This will thus become a request for variations in the budget.

Fiscal Accountability Plan –FOMILENIO II

15

b) Any changes which may have an effect on staff remuneration (salary or benefits) will be quantified by the Administration Deputy Manager (SA).

c) The Project Manager will issue his recommendations to FOMILENIO II’s Fiscal Agent (AF). d) The Fiscal Agent will review all proposed changes and recommendations by the Project

Manager and determine if said modifications are reasonable and necessary. If this is the case and it implies an increase of the total expenses for an activity/sub-activity, the Fiscal Agent will also explore other aspects of the MCC Program or the CIF/Agreement budget and develop a drawdown proposal (or an array of reductions) within other activities/sub-activities, enough to compensate the proposed increase and draft the Budget Adjustment proposal. Fiscal Agent will have 3 working days to perform these activities.

e) The Budget Adjustment proposal will be sent to Project Managers, which will have 3 days to send any corrections to the budget adjustment proposal, including a technical justification. If Fiscal Agent doesn’t have any comments or request of possible modification/correction within the 3 days, the Fiscal Agent will be presented to the Executive Director for final approval.

f) In case any of the proposed Budget Adjustments are at an Activity level or even higher, they will need to be presented before the Board of Directors for their approval.

g) If approval is granted by the Board of Directors, the proposed changes will be presented to the MCC for their non-objection as part of the Disbursement Request, and then shown in Schedule A of the Quarterly Financial Report, alongside an explanation justifying said change.

h) If proposed changes impact the GOES budget, all procedures involved for said change will be the direct responsibility of the Fiscal Agent.

i) If the suggested changes are approved by the MCC, said proposals will be sent to the Ministry of Finances, who will in turn implement all necessary modifications within the GOES Budget in order to reflect budget variations.

3 Financial Plans, Disbursement Requests and Report Packages Financial plans are the means to plan future costs and achievements and to offer a basis meant to control said costs and identify problems which may arise, such as variations from the financial plan during the course of implementation. Financial plans exist at two levels:

a) The 609(g) Financial Plan, and the Compact’s Multi-Year Financial Plan show estimated costs for the whole term of the 609(g) agreement and the CIF/Agreement budget.

Fiscal Accountability Plan –FOMILENIO II

16

b) The Detailed Financial Plans (DFP) show both the commitments as well as the real expenses to date, plus future commitments and expenses for the remainder of the 609g and the CIF/Agreement quarters in greater detail.

3.1 Multi-Year Financial Plan and Adjustments to the Multi-Year Financial Plan

The initial financial plans were the “Program under section 609(g) Financial Plan” included in Annex II of agreement 609g and the CIF/Agreement’s “Multi-Year Financial Plan” (MYFP) included in Annex II of the Compact.

3.1.1. The Multi-Year Financial Plan (MYFP) The Multi-Year Financial Plan (MYFP) presented in Annex II of the Compact, establishes the estimated costs during the five years of the Convention breakdown by project, and the activities within each Project. It establishes the maximum expenditure limits on an annual basis. While annual project ceilings may be modified from time to time through the Quarterly Disbursement Request (QDR) on the basis of the review and planning of the Programs and Projects, the overall total amounts for the 5 Years, by activity, should not be higher than those established in the Compact. The most recent and approved Multi-Year Financial Plan is included in Annex A of the last approval of the Quarterly Deduction Request.

3.1.2. The Detailed Financial Plan (DFP) The Detailed Financial Plan (DFP) reflects the funding that the FOMILENIO II expects to commit and the cash it expects to need to meet obligations to vendors with respect to the Work Plans. The DFP breaks down FOMILENIO II commitments and cash requirements to the Sub-Activity level (or beyond, as dictated by the Work Plans) on a rolling quarterly basis for the upcoming four quarters, and on an annual basis for the remaining years of the Compact. The DFP consists of two spreadsheets, one for Commitment projections and another for Cash Requirement projections. The Fiscal Agent, with the support of and MCC Fiscal Accountability staff, is responsible for assisting the FOMILENIO II in developing a standard DFP format, including the level of detail and

Fiscal Accountability Plan –FOMILENIO II

17

the categories of expenses that will be consistent across projects and activities through the life of the Compact. This general categorization of expenses disaggregates the MYFP by Projects, Activities, and Sub-Activity. FOMILENIO II also subscribes agreements with Implementing Entities and gives them budgetary support via providing direct or physical item support. These agreements are shown in the DFP under the activities to which they relate and costs are broken down into the following two categories: (1) In-Kind Support; and (2) Direct Support. The direct funding only refers to salaries and other recurring operational expenses. While the other kinds of support are classified as “In Kind”.

3.1.3. The Quarter Each Quarter shall begin on the first day of January, April, July, and October for the purposes of the Detailed Financial Plans and Payment Requests. The first quarter starts with the date of Entry-into-Force (EIF), and ends either at the end of that same current quarter or at the end of the next quarter, whichever is most appropriate. The first Disbursement Request for Compact funds shall cover the same period as the first quarter (although disbursements may occur earlier under a 609g or CIF agreement).

3.1.4. The Quarterly Financial Report (QFR) The Quarterly Financial Report is intended to provide an overview of the financial developments since the last disbursement period and to explain and justify any proposed cash or funds requested (Payment Authority) for the next period. The QFR proposes adjustments to the MYFP to reallocate funding from one Project or Activity to another, reports actual expenditures, provides a cash reconciliation, and presents a summary of interest accrued at the MCA. The QFR must be submitted for the CIF and 609(g) grants until all funds are exhausted, or, in the case of CIF funds, until un-used budget and un-liquidated commitments are “rolled over” into the Compact QFR. Any final QFRs must be clearly marked as “FINAL”, after which there is no further need to submit QFRs for that particular funding source.

3.1.5. Modifying the Multi-Year Financial Plan

Fiscal Accountability Plan –FOMILENIO II

18

The Compact acknowledges the possibility of modifying the Multi-Year Financial Plan during its period of validity, as provided by section 6.2 of the Compact, Amendments and Modifications, which determines:

a) The Parties may only amend this Compact if done in writing. Said written agreement will also include the way in which these amendments will enter into effect. Additional Representatives will not represent the Parties for said purposes.

b) Regardless of the provisions of section 6.2(a), the Parties may amend any Annex, through a written agreement signed by the Parties, that will enter into effect immediately after being signed to (i) suspend, terminate or modify any Project or Activity; (ii) modify fund allocations as determined by Annex II, starting on this date, (iii) modify the implementation framework provided in Annex I, (iv) add, modify or remove any indicator, point of reference or projection, or any other information provided in Annex II starting on this date, subject to the MCC’s control and evaluation policy, and based on said policy, or (v) add, remove or exempt any condition previously described in Annex IV; as long as in each case, said modification (A) is consistent in every material aspect with the Program’s Objectives and the Project Objectives, (B) does not increase the amount of Program Financing above the total amount determined in section 2.1 (which may be modified through section 2.2(e), (C) does not represent an increase in the Funding required to Implement the Compact above the total amount established in section 2.2(a), (D) does not reduce the responsibilities or provision of Resources by the Government required within the framework of section 2.6(a), and does not extend the Compact’s term.

3.1.6. Requesting Reallocation of Funds

Requesting Reallocation of Funds during the normal Quarterly Reporting Cycle All reallocations of funds among or between the line items that are identified in the Multi-Year Financial Plan must be approved by the Board of FOMILENIO II and have a non- objection statement from MCC. Such reallocations shall be initiated by the SAF/AF, approved by the Executive Director, approved by the Board of FOMILENIO II and be granted the non-objection of the MCC, through the Quarterly (or periodic) Disbursement Request package. The reallocation of funds between the line items levels identified in the Multi-Year Financial Plan summarized in Annex II of the Compact, should be initiated by the person responsible for each corresponding Project, with the approval of the /AF and FOMILENIO II’s General Manager. Every reassignment of funds below the level of the items located within the Multi-Year Financial Plan summarized within Annex II of the Compact, may also be requested by FOMILENIO II’s Board of Directors. However, if such approval is not requested by the Board of FOMILENIO II, such changes shall in still be communicated to the Board of FOMILENIO II on a periodic basis. Reallocations concerning the Multi-Year Financial Plan and the Detailed Financial Plan must be document based on the table below and signed by FOMILENIO II’s Executive Director, and FOMILENIO II’s Board of Directors will be periodically kept up to date in writing. The original

Fiscal Accountability Plan –FOMILENIO II

19

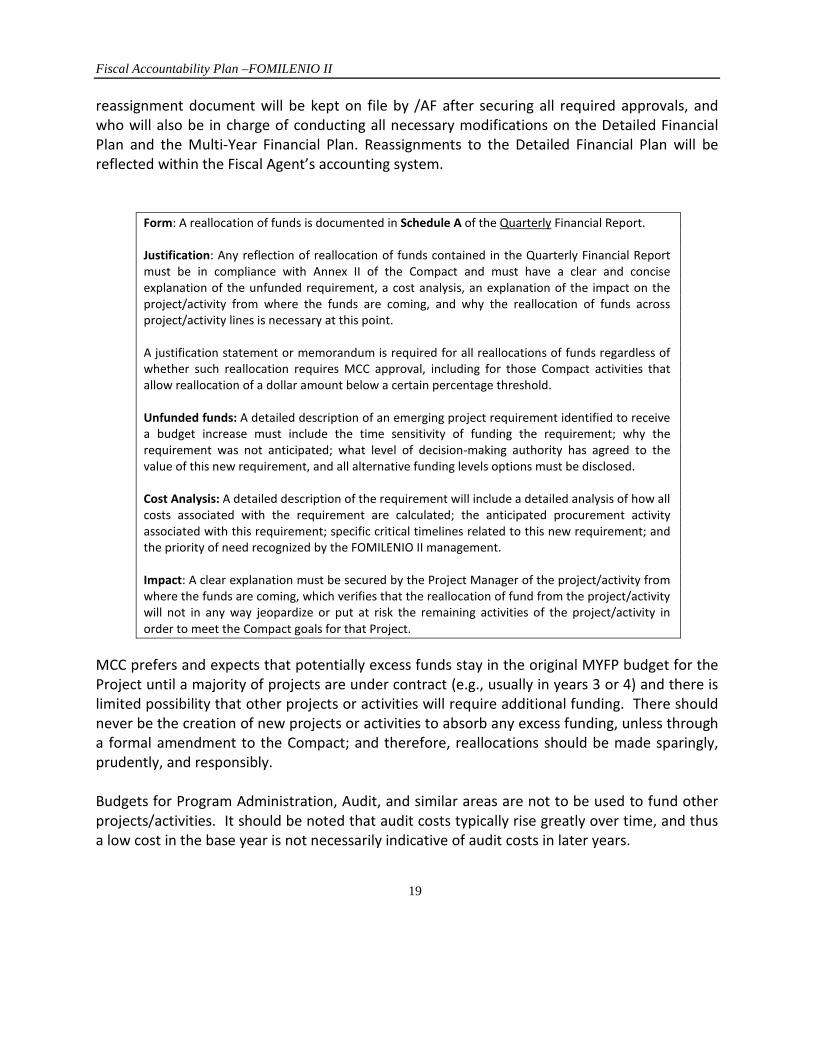

reassignment document will be kept on file by /AF after securing all required approvals, and who will also be in charge of conducting all necessary modifications on the Detailed Financial Plan and the Multi-Year Financial Plan. Reassignments to the Detailed Financial Plan will be reflected within the Fiscal Agent’s accounting system.

Form: A reallocation of funds is documented in Schedule A of the Quarterly Financial Report. Justification: Any reflection of reallocation of funds contained in the Quarterly Financial Report must be in compliance with Annex II of the Compact and must have a clear and concise explanation of the unfunded requirement, a cost analysis, an explanation of the impact on the project/activity from where the funds are coming, and why the reallocation of funds across project/activity lines is necessary at this point. A justification statement or memorandum is required for all reallocations of funds regardless of whether such reallocation requires MCC approval, including for those Compact activities that allow reallocation of a dollar amount below a certain percentage threshold. Unfunded funds: A detailed description of an emerging project requirement identified to receive a budget increase must include the time sensitivity of funding the requirement; why the requirement was not anticipated; what level of decision-making authority has agreed to the value of this new requirement, and all alternative funding levels options must be disclosed. Cost Analysis: A detailed description of the requirement will include a detailed analysis of how all costs associated with the requirement are calculated; the anticipated procurement activity associated with this requirement; specific critical timelines related to this new requirement; and the priority of need recognized by the FOMILENIO II management. Impact: A clear explanation must be secured by the Project Manager of the project/activity from where the funds are coming, which verifies that the reallocation of fund from the project/activity will not in any way jeopardize or put at risk the remaining activities of the project/activity in order to meet the Compact goals for that Project.

MCC prefers and expects that potentially excess funds stay in the original MYFP budget for the Project until a majority of projects are under contract (e.g., usually in years 3 or 4) and there is limited possibility that other projects or activities will require additional funding. There should never be the creation of new projects or activities to absorb any excess funding, unless through a formal amendment to the Compact; and therefore, reallocations should be made sparingly, prudently, and responsibly. Budgets for Program Administration, Audit, and similar areas are not to be used to fund other projects/activities. It should be noted that audit costs typically rise greatly over time, and thus a low cost in the base year is not necessarily indicative of audit costs in later years.

Fiscal Accountability Plan –FOMILENIO II

20

Requesting Reallocation of Funds outside of the normal Quarterly Reporting Cycle The request for reallocation of funds requiring MCC approval is submitted with the Quarterly Reporting package. However, requests for reallocation of funds may be submitted within the course of a quarterly disbursement period to supplement or amend an existing approved disbursement request via an “Out-of-Cycle Disbursement Request”. For more information, MCC Guidance on Out-of-Cycle Disbursement Requests, currently available at the following URL: https://assets.mcc.gov/guidance/mcc-guidelines-outofcycledisbursementrequests.pdf

3.2 Disbursement Requests and Reporting Packages No Disbursement Request shall be executed unless it is in accordance with the Compact. Disbursement Requests shall outline the cash needs over the next quarter. FOMILENIO II shall submit to MCC on a quarterly basis a Disbursement Request and Reporting Package for all sources of funds to include 609(g), CIF, and Compact financing. The Disbursement Request (DR) identifies resources needed for program implementation in the upcoming quarter specific for each funding source as mentioned above. The accompanying package of materials submitted in the Disbursement Request and Reporting Package (DRRP) is designed to offer MCC the information necessary to approve the Disbursement Request. The package provides information on execution of program activities, financial management, procurement actions, progress towards compact goals as defined in M&E indicators, and status of conditions precedent to disbursement. MCC granting Spending Authority through a Disbursement Request will be contingent on the Disbursement Request and Reporting Package being satisfactory, in form and substance. The Disbursement Request and Reporting Package (including all reports listed below) shall be submitted prior to the start of the quarter for which funds are requested, even for quarters in which the MCA is making a request of zero dollars. The DRRP is to be submitted to MCC twenty (20) calendar days prior to the end of each quarter (or by March 10, June 10, September 10, and December 20). Within the DRRP, the MYFP shall will be reviewed and adjusted quarterly no later than the 10th calendar day of the month preceding the quarter for which it covers and shall be submitted by FOMILENIO II to MCC for approval using Schedule A of the Quarterly Financial Report (QFR). Schedule A must be submitted even if no changes to the MYFP are proposed.

Fiscal Accountability Plan –FOMILENIO II

21

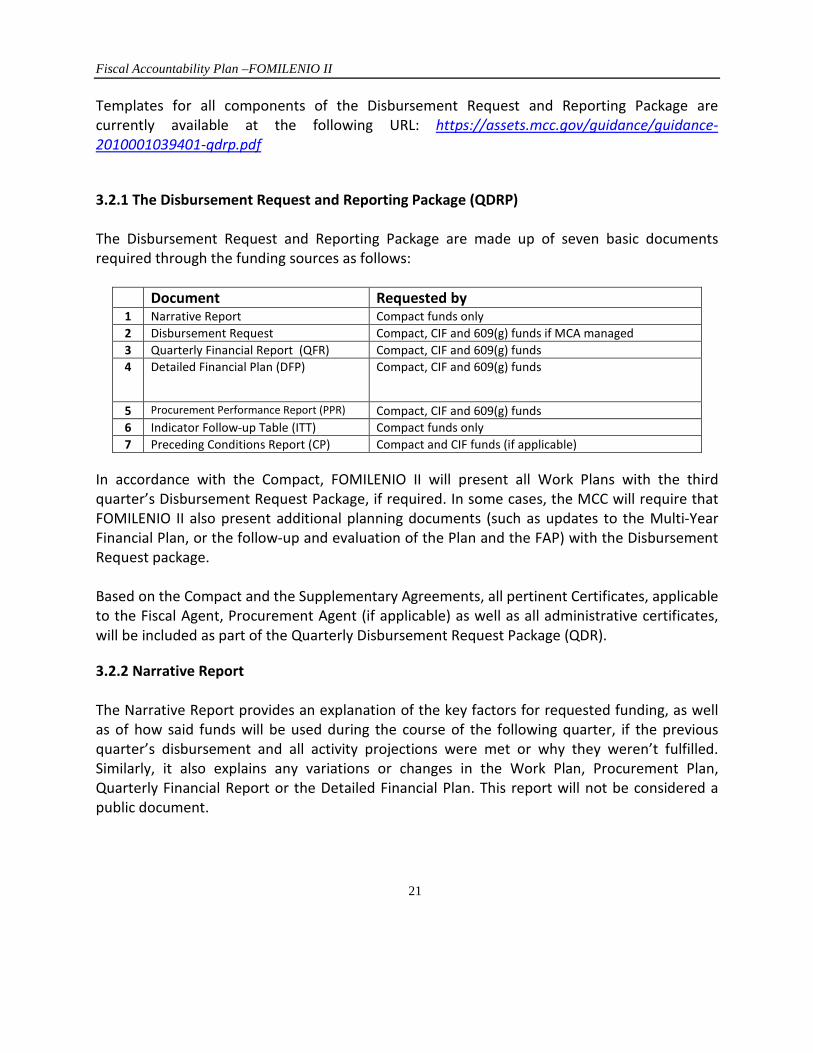

Templates for all components of the Disbursement Request and Reporting Package are currently available at the following URL: https://assets.mcc.gov/guidance/guidance-2010001039401-qdrp.pdf 3.2.1 The Disbursement Request and Reporting Package (QDRP) The Disbursement Request and Reporting Package are made up of seven basic documents required through the funding sources as follows:

Document Requested by 1 Narrative Report Compact funds only 2 Disbursement Request Compact, CIF and 609(g) funds if MCA managed 3 Quarterly Financial Report (QFR) Compact, CIF and 609(g) funds 4 Detailed Financial Plan (DFP) Compact, CIF and 609(g) funds

5 Procurement Performance Report (PPR) Compact, CIF and 609(g) funds 6 Indicator Follow-up Table (ITT) Compact funds only 7 Preceding Conditions Report (CP) Compact and CIF funds (if applicable)

In accordance with the Compact, FOMILENIO II will present all Work Plans with the third quarter’s Disbursement Request Package, if required. In some cases, the MCC will require that FOMILENIO II also present additional planning documents (such as updates to the Multi-Year Financial Plan, or the follow-up and evaluation of the Plan and the FAP) with the Disbursement Request package. Based on the Compact and the Supplementary Agreements, all pertinent Certificates, applicable to the Fiscal Agent, Procurement Agent (if applicable) as well as all administrative certificates, will be included as part of the Quarterly Disbursement Request Package (QDR). 3.2.2 Narrative Report The Narrative Report provides an explanation of the key factors for requested funding, as well as of how said funds will be used during the course of the following quarter, if the previous quarter’s disbursement and all activity projections were met or why they weren’t fulfilled. Similarly, it also explains any variations or changes in the Work Plan, Procurement Plan, Quarterly Financial Report or the Detailed Financial Plan. This report will not be considered a public document.

Fiscal Accountability Plan –FOMILENIO II

22

3.2.3 Disbursement Request (DR) The Disbursement Request is a document meant to represent a request from a FOMILENIO II Accountable Entity so that the MCC will create an account against which payments may be made to contractors or employees, or so that the MCC makes cash payments to a Permitted Account. The Disbursement Request is provided before every quarter for which funds are being requested, even for those quarters in which FOMILENIO II is requesting zero dollars. The Disbursement Request is the means which FOMILENIO shall utilize to request the Authorized Payments for the following fiscal quarter or any other term agreed upon by the MCC. The Disbursement Request is performed through the signatures of FOMILENIO II’s Executive Director as additional representative of the Government, FOMILENIO II’s Board of Director’s President and the Fiscal Agent. Within the Common Payments System (CPS), the Disbursement Request distinguishes between disbursement requests directly from the MCC to suppliers and cash disbursement requests from the MCC to the FOMILENIO II’s Permitted Account(s). 3.2.4 Quarterly Financial Report, (QFR) This financial report provides a summary of all FOMILENIO II’s financial activities in relation to the previous quarter, while also documenting and justifying any cash request for the following quarter. Furthermore, it is also a tool to present periodic financial information, request spending limits and justify disbursement requests. The Quarterly Financial Report is also used to notify the MCC of proposed adjustments to the Multi-Year Financial Plan (MYFP). The Quarterly Financial Plan includes the following programs:

• Schedule A – Request Application to Adjust the Multi-Year Financial Plan; • Schedule B - Summary of Adjustments to the Multi-Year Financial Plan, to date; • Schedule DPF-Commitments – Commitment Forecast Report (next period); • Schedule DFP-Cash – – Forecasted Program Cash Requirements (next period).

Schedules A and B account for proposed and executed reprogramming (reallocation) of funds across projects and/or activities within projects. 3.2.5 Detailed Financial Plan (DFP)

Fiscal Accountability Plan –FOMILENIO II

23

Schedules DFP-Commitments and DFP-Cash correspond to the Detailed Financial Plan, which reflects the funding that FOMILENIO II expects to commit and the cash (in the form of payments authority) it expects to need on hand to carry out the tasks included in the Work Plans. For planning purposes, the DFP-Commitment and DFP-Cash schedules break down the budget/financial categories to the activity level (or beyond to the Sub-Activity, where appropriate, given the level of detail included in Compact’s MYFP) on a rolling quarterly basis for the upcoming four quarters, and on an annual basis for the remaining years of the Compact. The level of detail of the DFP shall be determined by program planning needs. Different sectors within MCC will review the DFP to varying levels of specificity. The DFP must follow a format that allows for the Sub-Activity detail to be “rolled-up” to the Project/Activity level. The Fiscal Agent, with the collaboration of the Fiscal Agent and the MCC Fiscal Accountability staff, is responsible for assisting FOMILENIO II in developing a standard Detailed Financial Plan format, including the level of detail and the categories of expenses that will be consistent across Projects and Activities through the life of the Compact. Separate financial reports (i.e., separate QFRs) are required for all MCC funding sources:

• Compact; • Compact Implementation Funding (CIF); and • Compact development 609(g) grants.

For 609(g) and CIF funds, the DFP template is the same as for compact funds, but MCAs should distinguish between funding sources by developing independent DFP sheets. In countries for which 609(g) grant agreements require a detailed budget, this budget can serve as the quarterly DFP. 3.2.6 Procurement Performance Report (PPR) The Procurement Performance Report (PPR) is an integrated planning and reporting tool for procurement actions initiated by the MCA. The report is cumulative, so as to provide an overview of all completed and ongoing procurements. The PPR should include all approved, initiated, ongoing, and/or completed procurement actions valued at or above USD $25,000. This includes actions in the currently active and approved Procurement Plan, even if these actions have not yet begun. The PPR includes unique IDs for each procurement action for easy sorting.

Fiscal Accountability Plan –FOMILENIO II

24

The purpose of the PPR is for each MCA to provide MCC with a summary of the current status of procurements across its Program and thereby assist MCC in monitoring MCA compliance with the Program Implementation Agreement (PIA), Procurement Agreement, and the Procurement Plans. The PPR has six sections:

• Procurement Information; • Expression of Interest/Pre-Qualification; • Bidding/Solicitation Documents; • Evaluation of Bids/Proposals/Quotes; • Contract Award; and • Implementation.

3.2.7 Indicator Tracking Table (ITT) The Indicator Tracking Table (ITT) is an integrated planning and reporting tool that displays performance targets (projections) and tracks progress against them (actual performance). The ITT is designed to help MCC and MCAs track interim progress toward Compact goals. All performance indicators that are included in the latest approved M&E Plan for the Compact should be included in the ITT. This includes indicators at all levels of the results hierarchy including lower level output and process milestone indicators. Most indicators have annual performance targets associated with them in the M&E Plan. The ITT breaks these down into their quarterly components in order to facilitate more regular performance tracking. The process of breaking down the annual targets into quarterly targets takes place at the beginning of each compact year. Quarterly targets are only set for those indicators that are required to be reported on a quarterly basis, as per the M&E Plan. However, quarterly targets are no longer required as part of the reporting template to MCC. Instead, reporting actual performance on a quarterly basis (to be assessed against an annual target) is required where specified in the M&E Plan. A complete ITT provides detailed information that shows (1) quarterly, (2) annual and (3) five year end-of-compact basis targets for each performance indicator. The actual progress towards these targets is to be recorded quarterly. In addition, a column for current quarter actuals has been added to the ITT template so that MCC and MCA management receive more up-to-date information on indicator performance. The ITT should only report against indicators and targets approved in the M&E Plan. Modifications to indicators and targets may not be made in the ITT.

Fiscal Accountability Plan –FOMILENIO II

25

3.2.8 Conditions Precedent Report (CP report) The Conditions Precedent (CP) report is designed to summarize progress toward meeting CPs to disbursement. The CP report is a table designed to capture information about the timing, associated project activities, status and relevant documentation for each CP. The CP report lists all Compact CPs relevant for disbursement and tracks all CP deferrals or waivers requested by the MCA. It is important for MCAs to be specific about the documentation providing evidence of CP satisfaction, and to include a justification for any CP deferral requests. 3.2.9 Payment Authority for Approved Disbursement Requests

Approval Process for establishing a Payment Authority for each Disbursement Period FOMILENIO II submits a Disbursement Request and Reporting Package (Disbursement Request, Quarterly Financial Report, Conditions Precedent Report, Detailed Financial Plans and such other documents and reports as MCC may require in accordance with the applicable supplemental agreements and MCC policy) no later than 20 days prior to the commencement of each disbursement period. The package is circulated through the relevant MCC staff, including the Regional Point of Contact and the Department of Administration and Finance, for final approval, which then authorizes FOMILENIO II to begin making payments through the Common Payment System (CPS). MCC sends a disbursement response letter to FOMILENIO II detailing the amount of funds approved for the relevant disbursement period and any waiver or deferral of conditions precedent. MCC retains the authority to adjust the amount of funds to be disbursed for the applicable disbursement period based on progress achieved on the implementation of the projects and activities to be funded by the Compact, CIF agreement, and/or 609(g) grant agreement. Expiration of the Payment Authority at the End of the Period FOMILENIO II’s authority to submit payment requests to IBC relating to payments for expenditures included in an approved Disbursement Request shall expire on the last day of the applicable quarter covered by such Disbursement Request, except as otherwise provided in the section “Restoring Authorized Expenditures Limited Payment Authority” of this FAP. The Internal Business Center (IBC) or MCC shall notify FOMILENIO II in writing of the expiration of the authority to submit requests for payment to said Center (IBC), not less than ten business days before the final end of said quarter according to the approved disbursement request.

Fiscal Accountability Plan –FOMILENIO II

26

If a new Disbursement Request is not approved by the first day of the next quarter, FOMILENIO II will not have the authority to submit requests for payment to IBC for any expenditures relating to the approved Disbursement Request for the previous period, except as provided in the section “Restoring Authorized Expenditures Limited Payment Authority” of this FAP (both of which provide for an additional 30 days). At the end of that 30-day period, IBC must halt payments until such time as MCC approves a new Disbursement Request Package and/or IBC and receives notification from MCC’s Department of Administration and Finance that they can continue making payments. Reinstatement of Limited Payment Authority After the expiration of the payment authority at the end of the period previously described in the “Expiration of payment Authority at the End of the Period” section, MCC may authorize in exceptional circumstances only a temporary reinstatement of payment authority to cover specific payments. The total amount of the reinstated payment authority may only be as high as the unused spending authority from the prior period, and is only available during the first 30 days after the close of that period or until the date of approval of the next Disbursement Request submitted to MCC, whichever is earlier. The reinstated payment authority may be used only for expenditures that were approved by MCC in the most recent Detailed Financial Plan, but for which inadequate funds were budgeted or whose timing for payment is later than originally anticipated. The reinstated payment authority may not be used for expenditures for which Conditions Precedent to disbursement were not met, and the expense to be paid with the reinstated spending authority may not be included in the Detailed Financial Plan of the next period. Requests to use such funds are to be submitted to IBC using the following procedure: The Fiscal Agent submits a Special Payment Request Form authorized by the usual signatories and the MCC Resident Country Director (or its proxy). The Fiscal Agent should state the reason for the request in column 13, “Additional Information” of said special form. A Special Payment Request Form must be approved by the MCC RCD, and must be utilized if: • Upon occasions where goods or services, which were approved in the QFR, and are

delayed in delivery and/or the presentation of invoice falls into the next quarterly time frame, a one-time “Special Payment Request Form” must be utilized if the payment of this invoice falls above USD $500,000; or

Fiscal Accountability Plan –FOMILENIO II

27

• An invoice comes in during the current quarter for an activity which had been foreseen in the last quarter, the current quarter's QFR is not yet approved by MCC and the funds requested do not exceed USD $500,000.

3.3 SAP Procedures

a) Changes in the MYFP should be registered through FMBB, the capacity and authority to make these changes belongs to the Finance Management/ Fiscal Agency, these changes also require updating of the Quarterly Financial Reports (QFR-A/ QFRB) Through ZQFRA and ZQFRB. Any change in MYFP under an activity does not require MCC approval, but changes between each activity must be supported by prior MCC approval. b) Preparation of QDRP 1. Creation of Funds Reservation (FR) The program team provides quarterly estimates at Sub Activity level (in SAP it is called WBS), with this information the Finance Management/ Fiscal Agency creates a FR with the date of the first day of the relevant quarter for each Sub Activity through FMX1. 2. Creating the Purchase Requisition (PR)

With the FR number, the program team creates a PR, which will serve as a basis for the Public Procurement Management / Procurement Agency to subsequently create the Purchase Order or Contract (PO) through ME21N

3. Creation of the Financial Plan Detailed (DFP)

When creating the PR the program, the team should carefully set the dates on which they expect to receive the deliverables, taking into account that the date of the nearest deliverable (first line) is the date (Month/quarter) that SAP will use to schedule the COMMITMENT For the total amount of the PR), which will be reflected in the Commitment Financial Plan (DFP) and the dates of the deliverables of the subsequent lines will determine in which date (Month/ quarter) is being scheduled DISBURSEMENTS (payments) in the Financial - Detailed Plan (DFP - Cash). Once the program team finishes creating the PR, the Finance Management/ Fiscal Agency generates the DFP-Commitment through ZDFPCOMMIT and the DFP-Cash through ZDFPCASH reviewing and validating the information to be sent to probation Of MCC.

c) Establishment of Approved Quarterly and Payment Authority Commitments (After MCC approval)

Fiscal Accountability Plan –FOMILENIO II

28

The Commitments and Payment Authority approved by MCC are called in SAP “Payment Budget” and must be updated by the Finance / Fiscal Agency through ZF2_BUDCASH and ZF2_BUDCOMMIT d) Affecting the Commitment (Current Commitment)

The date of creation of the PO is the date (day, month, quarter) in which the Commitment is recorded in SAP, for purposes of the DFP-Commitment. At this time, the dates of the deliverables detailed in the PO lines are the dates on which the disbursements will be scheduled in the DFP-Cash and will replace the dates mentioned in the PR. The PO is created through ME21N. The dates of the deliverables that are included in the SAP System are for the purposes of financial planning.

e) Creation of the Fund Commitment

With the FR number, the Finance Management/ Fiscal Agency must also create the Fund Commitment through FMZ1, which will be used to record invoices that do not correspond to Purchasing Processes (NoN PO Invoices)

f) Quarter Closing Activities

The Finance Management / Fiscal Agency, at the end of each quarter should review the balances of the FR, the open PR and the POs in order to coordinate with the program team and the Public Procurement Management / Public Procurement Agency to make the necessary adjustments to the PR / PO deliverables dates in order to update the Schedule of commitments and disbursements. At the same time, it must review and adjust the funds of the funds commitments, so that the unused Payment Budget (Commitments and Disbursements) is returned to MYFP

g) Year-end activities

At the end of the year, in addition to the closing activities of each quarter, the Finance Management / Fiscal Agency must transfer the available balances of each MYFP sub-activity to the following year through FMEDDW.

3.4 Indefinite Delivery / Indefinite Quantity Contracts (IDIQ Contracts)

IDIQ contracts are those entered into with one or several providers, when what is needed has been established, but the delivery and quantity cannot be defined in advance nor the service time expected.

Fiscal Accountability Plan –FOMILENIO II

29

An IDIQ contract is the result of a brief procurement process which has taken place by using open, fair, and competitive procedures used transparently, as per any of the different procurement methods based on the Guidelines for public procurement within the framework of MCC’s Program. IDIQ Contracts are awarded based on the fulfillment of the evaluation criteria established by each tender document, such as works experience, or providing goods or services similar or equal to those required by FOMILENIO II, according to the Terms of Reference Provided and the Illustrative Work Order examples (meaning, only with indicative scopes and amounts). This type of contracts are originally entered into for specific terms and an exemplary global amount (common availability to be shared amongst the different Contractors based on later individual awards of Work Orders) without specifying neither the amount of works to be done, nor the date and/or terms required, meaning, they only include a previous agreement and the future availability of said Contractors to deliver what is being required from them. Later on, once the scopes, amounts and terms of the required works or services are determined, Contractors may be assigned by FOMILENIO II through work orders (PO) issued individually for each Contractor, as determined by the simplified award and requirement evaluation procedures established for the group of Contractors qualified to compete for each work order. Entering into an IDIQ Contract must not affect the budgetary commitments, until such a time as when the work orders (PO) are issued; being required to keep control of the availabilities assigned to IDIQ contracts, through one or several Purchase Requisition (PR) linked to a Fund Reservation (FR) created specifically for each IDIQ contract. One or several PR may be linked to the lines or deliverables for one or several POs, this division will be done accordingly with the assignment of multiple funding sources or multiple Projects/Activities associated to an IDIQ, which will allow showing the planning of commitments and disbursements in the DFP-Cash/Commitment in the different report periods.

4 Permitted Bank Accounts and the Common Payment System MCC uses two payment processes for banking and cash management. One payment process uses local banks to receive monthly grant disbursements from MCC and then makes re-disbursement payments from the local bank accounts. The other payment process requires the

Fiscal Accountability Plan –FOMILENIO II

30

Fiscal Agent to use the MCC Common Payments System (CPS) to transfer funds directly from the U.S. Treasury to the vendors of goods, works, and services received by FOMILENIO II. CPS may be used to process payments in U.S. Dollars or local currency directly to vendors, or to transfer funds to a Permitted Account used as a transit account enroute to a vendor.

4.1 FOMILENIO II Local Banking Accounts Two (or more, as described below) Permitted Accounts shall be opened at a local bank to manage selected MCA-El Salvador program funds: COMPACT FUNDS

• First – Permitted Account to Manage Funds for MCC funding • Second – Permitted Account to Manage Funds belonging to Government Counterpart

funds.

TAXES • Third – Permitted account to Manage Funds advanced by Government for tax

reimbursement.

No other bank accounts under FOMILENIO II’s name will be allowed, except with the express approval of MCC. The existing balance on Permitted Accounts should only serve to fulfill FOMILENIO II’s immediate cash needs and shall never exceed ONE MILLION DOLLARS (USD$1,000,000.00), except in the case of transit funds and funds in Fiscal Reimbursement Program accounts. Transit funds should NOT remain in the Permitted Account for over 72 hours. Any disbursement request made to the Permitted Account is coded as “NA/NA” at the PRF instead of assigning projects and activities. JUDICIAL GARNISHMENT

• Fourth – Permitted account to deposit funds provided by the garnishment of employee’s wage. The amounts discounted are not part of FOMILENIO II’s availability, however, they must be deposited and kept in a bank account separate from the other FOMILENIO II accounts and be available at all times to be pay or be transferred to the creditor or plaintiff as per the Judicial Order.

Fiscal Accountability Plan –FOMILENIO II

31

Control over these funds will be conducted separately from ordinary accounting procedures and will not be part of FOMILENIO II’s financial statements.

NON COMPACT FUNDS

• Fifth – Permitted Account for the management of other funds different than the financing of the Compact, arising from compliance with legal provisions in procurement processes and as a result of disputes or claims that FOMILENIO II must receive.

4.2 MCC’s Common Payment System (CPS) References the system used by MCC to process payments in United States of America dollars, or to process payments in foreign currency directly to asset, works and service suppliers and received by FOMILENIO II, or received by the Implementing Entities on behalf of FOMILENIO II. There are two types of systems, the International Treasury Services, ITS and the Secure Payment System, SPS, described in Section 7 below.

4.3 Fiscal Agent’s responsibilities – Permitted Accounts and Common Payment System

Individuals allowed to sign and who hold a primary level of responsibility within Permitted Accounts and the payment process through the Common Payment System are the following:

• Executive Director; • Finance Manager/Fiscal Agent • General Manager; • Administration and Finance Deputy Manager;

The Finance Manager, as a representative of the Fiscal Agency, will be an authorized account holder on all accounts, while the other three officials will only have the ability to co-sign or countersign. The individual with the authorized signature and alternative responsibility on Permitted Accounts and payment processes through CPS for the Fiscal Agent will be:

• Deputy Manager of Financial Administration

Fiscal Accountability Plan –FOMILENIO II

32

The Finance Manager, as a Fiscal Agent representative or the person designated to this end, will watch over to make sure there are two of those signatures available at all times to fulfill the needs of FOMILENIO II’s local checking account.

4.4 Exclusive Nature of the Accounts Permitted accounts will remain fully independent. MCC financing funds will not mix with the Government’s counterpart funds, Tax reimbursement funds or with any other funds belonging to any other source, previously authorized by the MCC.

4.5 Interest on Permitted Accounts Permitted bank accounts will earn interests based on the provisions of the Banking Agreement. All interests on the MCC financing’s permitted bank account will be reimbursed on a quarterly basis. The amount of said interests will not be included within accounting records.

5 Budget Implementation & Financial Control Budget Implementation includes several activities both related and sequential, including:

a) Determining necessary resources (assets, Works and services) to implement each project.

b) Enter into assets, works and service contracts after ensuring the contractor is not in the Excluded Parties List, as determined by the MCC Program’s Guidelines for Public Procurement.

c) Include all commitments on the budget system to guarantee the funds will be available to fulfill all contractual payments.

d) Verify the delivery of assets and services. e) Authorize and issue payments to assets and services providers.