First Ten Years P1 bk - MIGA

38

OVERVIEW The 10 years since the establishment of the Multilateral Investment Guarantee Agency (MIGA), 1988–98, have borne witness to a burgeoning of foreign direct investment (FDI) in developing countries and transition economies. In recognition of the value of FDI as a source of external capital for their development, the host governments of these countries also have exhibited growing enthusiasm for attracting foreign investments through economic reform and liberalization programs. In this decade, MIGA played a vital role in facilitating FDI by providing confidence to both investors and host governments that their concerns would be respected. In looking over this period of transformation, it is clear that MIGA has been “the right institution, in the right place, at the right time.” This report examines the 10-year history of MIGA, the initial challenges during start-up, its innovative and dynamic evolution, its role in facilitating FDI flows to developing countries, and some of the continuing challenges. OVERVIEW 1

Transcript of First Ten Years P1 bk - MIGA

OVERVIEW

The 10 years since the establishment of the Multilateral Investment Guarantee Agency(MIGA), 1988–98, have borne witness to a burgeoning of foreign direct investment (FDI) indeveloping countries and transition economies. In recognition of the value of FDI as a sourceof external capital for their development, the host governments of these countries also haveexhibited growing enthusiasm for attracting foreign investments through economic reformand liberalization programs.

In this decade, MIGA played a vital role in facilitating FDI by providing confidenceto both investors and host governments that their concerns would be respected. In lookingover this period of transformation, it is clear that MIGA has been “the right institution, inthe right place, at the right time.”

This report examines the 10-year history of MIGA, the initial challenges duringstart-up, its innovative and dynamic evolution, its role in facilitating FDI flows to developingcountries, and some of the continuing challenges.

OVERVIEW 1

MIGA: THE FIRST TEN YEARS2

TABLE 1. NET LONG-TERM RESOURCE FLOWS TO DEVELOPING COUNTRIES, 1990–97(in billions of U.S. dollars)Category 1990 1991 1992 1993 1994 1995 1996 1997*

All Developing Countries 98.3 116.3 143.9 208.1 206.2 243.1 281.6 300.3Official Development

Finance 56.4 62.7 53.8 53.6 45.5 54.0 34.7 44.2Total Private Flows 41.9 53.6 90.1 154.6 160.6 189.1 246.9 256.0

Debt Flows 15.0 13.5 33.8 44.0 41.1 55.1 82.2 103.2Commercial Bank Loans 3.8 3.4 13.1 2.8 8.9 29.3 34.2 41.1Bonds 0.1 7.4 8.3 31.8 27.5 23.8 45.7 53.8Other 11.1 2.7 12.4 9.4 4.7 2.0 2.3 8.3

Foreign Direct Investment 23.7 32.9 45.3 65.6 86.9 101.5 119.0 120.4Portfolio Equity Flows 3.2 7.2 11.0 45.0 32.6 32.5 45.8 32.5

* PreliminarySource: The World Bank, Global Development Finance, 1998.

I. ORIGINS

Over the past decade, FDI has become a major source of external capital for theeconomic growth of the less developed countries and transition economies. Between 1990and 1997, official flows of development finance have declined (Table 1). In addition, therehas been a significant shift in official concessional flows to finance refugee relief and peace-keeping efforts. The Organisation for Economic Co-operation and Development (OECD)estimated that roughly 12 percent of all official development assistance (including technicalcooperation grants) now goes to emergency aid, up from less than 2 percent in 1990.

Meanwhile, private net capital flows to developing countries have soared over the sameperiod, reaching an estimated $256 billion in 1997, a sixfold increase since 1990. Private flowsnow account for more than 85 percent of total aggregate net long-term resource flows (Table 1).

However, FDI accounts for the largest source of capital, constituting more than 40 per-cent of the total in recent years. FDI flows to developing countries and transition economiesaveraged just under $20 billion per year in the 1980s when the creation of MIGA cameunder consideration. The level was still no more than $24 billion by 1990. However, between1990 and 1992, the annual increase in FDI almost doubled (to $45 billion) and between1992 and 1994 it almost doubled again (to about $87 billion). The trend has continued sincethen, increasing fivefold over the entire period since 1990, to $120 billion in 1997.

The Initial Setting

In the first half of the 1980s, net flows of FDI averaged $19 million a year and thenumber of nationalizations and expropriations were on a downturn from their heights in the1970s. Yet the five years prior to 1983, when the idea of a multilateral investment insurance

3

agency was first considered by the Executive Directors of the World Bank, witnessed 42 ex-propriations in 29 countries in Africa, Latin America, and Asia. Interactions between multi-national corporations and host countries in the developing world continued to be marred bymutual suspicion, recurrent rancor, and conflict.

The debt crisis of the mid-1980s in Latin America showed that developing countriesincreasingly would have to rely on FDI rather than commercial bank lending or officialgovernment assistance. The challenge for the international community was, then, to finda mechanism to help provide stability for foreign investors, against noncommercialrisks to operations, and at the same time reassure host countries that their developmentconcerns would be adequately addressed through the participation of foreign firms in theireconomies.

The new affiliate of the World Bank Group, MIGA, was conceived to enhance theconfidence of both sides. On October 11, 1985, the World Bank’s Board of Governors endorsedMIGA’s Convention (charter) with the objective:

“to enhance the flow to developing countries of capital and technology for pro-ductive purposes under conditions consistent with their developmental needs,policies and objectives, on the basis of fair and stable standards for the treatmentof foreign investment.”

MIGA’s activities were to take two forms: investment insurance and technical assis-tance for investment promotion. Its guarantee program would provide insurance to investorsagainst political risks in the developing countries and, eventually, in transition economies. Itstechnical assistance and legal advisory services would assist host government authorities indesigning appropriate policies to better attract international firms. MIGA’s presence wouldhelp provide a framework within which foreign investors could operate in a country withlegal assurances of fair treatment of the investors and amicable arrangements to settle disputes.In order to qualify for MIGA insurance, prospective projects would have to be economically,financially, and environmentally sound, and likely to contribute to the economic develop-ment of the host country.

Within the World Bank Group, MIGA was to be an agency with its own countrymembership and capital base. World Bank membership would be a prerequisite for MIGAmembers. Other membership requirements would include signature and ratification of theMIGA Convention, along with payment of a capital subscription. Members could partici-pate as Category I countries (industrial nations) or Category II countries (self-declared de-veloping countries). Those countries in transition from socialist to market economies wereexpected to choose Category II status to qualify for MIGA-insured investment and MIGA-sponsored technical services.

ORIGINS

MIGA: THE FIRST TEN YEARS4

Start-Up

The history of MIGA has been a story of extraordinary growth, innovation, andexpansion to capacity. However, it must be recalled that its origins were less than auspicious.

The World Bank’s Board of Governors approved MIGA’s Convention in the fall of1985, but MIGA lacked the minimum number of members required to bring it into beinguntil April 12, 1988, when MIGA was formally launched. In the ensuing year, only one-fourth of the countries that had been assigned MIGA shares had completed the applicationprocess to become new members. Many developing countries that were major recipients ofFDI were absent altogether.

Several factors hindered membership growth. Under the Convention, membershipin MIGA is open to all members of the World Bank, but membership is not automatic. Eachstate seeking to join MIGA must follow the procedures set out in MIGA’s governing docu-ments. While satisfying the requirements for membership is normally a straightforward matter,it is not without its legal and practical complications. The Legal Department assumedresponsibility for reviewing the membership application shortly after MIGA’s establishmentand for a number of years spent a considerable amount of time addressing membershipissues. These issues tended to be of three kinds. The most frequent were legal questionsregarding the requirements to be fulfilled. Because it is a treaty, MIGA’s Convention must besigned by a duly authorized representative of the state seeking membership. The Conventionmust then be ratified in accordance with the country’s constitutional requirements, and aninstrument of ratification must be filed with the World Bank. Finally, shares in MIGA mustbe paid for in local and freely convertible currencies. These requirements are not unusualwithin the context of the establishment of a new multilateral development institution, butthey bring with them a considerable number of practical questions.

Philosophical issues also needed to be addressed. Many developing countries havelong been skeptical of resolving investment disputes through international arbitration asopposed to local courts, and some have been opposed to replacing the original investor withits investment insurer when a dispute is under negotiation. Both compulsory internationalarbitration and subrogation, as the replacement is called, are central to the claims manage-ment process envisioned by MIGA’s founders and set out in the Convention. It fell to MIGA’slegal staff, therefore, to explain these concepts to potential member countries and persuadethem of the benefits of this approach to dispute resolution. In addition, given the number ofcountries that joined MIGA and the disparate political and legal cultures they represented,there were a considerable number of questions that were particular to specific countriesseeking membership—issues of language, payment, interpretation of the Convention—whichneeded to be addressed in order to facilitate a country’s adherence to the Convention.

5

As a result, a vicious cycle seemed to plague MIGA’s growth. The slow expansion inmembership constrained MIGA’s investment income, which limited staff growth. A modeststaff (initially less than a dozen members) restricted the marketing of guarantees to potentialinvestors and slowed the issuance of guarantee contracts. This, in turn, put a restraint on staffexpansion, and efforts to increase country membership. As MIGA completes its first decadeof existence, these issues of membership are largely matters of archival interest only. TheLegal Department continues to work with countries that are not yet members, but thedemands of this activity are now far reduced from MIGA’s early years.

ORIGINS

MIGA: THE FIRST TEN YEARS6

II. THE GUARANTEE PROGRAM

At the time of MIGA’s establishment, a number of national agencies and privateinsurers were already providing political risk coverage to international investors. The varyingeligibility criteria of existing national agencies, however, excluded certain investors, coun-tries, or projects from consideration. Private insurers were constrained in the terms and extentof coverage that they offered.

Early Rationale

The MIGA Convention designed a guarantee program to complement rather thancompete with national and regional investment insurance programs and private insurers ofpolitical risk. MIGA was to fill the niches, or gaps, in the market caused by the differingeligibility requirements of the other existing programs. In particular, MIGA could insureinvestments in countries that were ineligible for coverage by other programs; or in projectsfor which ownership, residence, or sources of procurement made the investor ineligible.

There was also a broader rationale for the creation of MIGA. Its shareholder com-prised both industrial and developing countries, and would be uniquely placed to serve as anhonest broker, guiding all concerned parties toward a common definition of fairness andequitable treatment. This neutrality would help avert disputes from arising altogether, orprovide a channel for impartial mediation and amicable settlement when they did arise.

This position of honest broker was enhanced by the requirement of the MIGAConvention, which required that MIGA obtain the consent of a host government prior toissuing of an investment guarantee. Thus, beyond providing financial compensation to inves-tors for actual losses, MIGA’s involvement in a proposed project was meant to mitigate thelikelihood that such losses would occur.

Finally, supported by its own membership of developed and developing countries,and by virtue of its own status as a member of the World Bank Group, MIGA was designedto be particularly effective in pursuing salvage. Altogether, MIGA was meant to have a deter-rent effect, which would be particularly valuable to investors in projects acutely vulnerableto changes in host government policies and commitments.

This aspect of the “comfort” that MIGA participation can provide to investors hasgrown in importance over the 10 years of MIGA’s existence. It will occupy a central place inthe later discussion of the extent to which a booming market in private political risk insur-ance is still not able to obviate the need for MIGA.

7

Structure of Coverage

From the beginning, MIGA’s Guarantee Program has provided extended protection(up to 20 years) against losses arising from four types of political risks:

♦ Transfer restrictions, which prevent investors or lenders from converting local cur-rency into foreign exchange or transferring the proceeds abroad. (Unexpected changesin the value of a local currency are considered a commercial risk and must be coveredby commercial hedging techniques.)

♦ Expropriation in the forms of direct or indirect acts by a host government that reduceor eliminate ownership of, control over, or rights to the insured investment.

♦ War and civil disturbance (including politically motivated acts of sabotage or terrorism)resulting in destruction, damage, or disappearance of, tangible assets or interferencewith the ability of a foreign enterprise to operate.

♦ Breach of contract by a host government, provided the investor obtains an arbitrationaward or judicial sentence for damages and is unable to enforce it after a specifiedperiod, or in certain cases when the investor is unable to obtain the award or sentence.

Eligible projects include new investments and the expansion, modernization, privati-zation, or financial restructuring of existing investments in a developing member country.Eligible forms of investments include equity, shareholder loans, loan guarantees issued byequity investors, and loans to unrelated borrowers (under certain circumstances). Technicalassistance, management, and franchising and licensing agreements also are eligible, providingthey have terms of at least three years and the investor’s remuneration is tied to the project’soperating results.

Eligible investors should be nationals of a member country other than the country inwhich the investment is to be made. A corporation is eligible if it is either incorporatedin and has its principal place of business in a member country, or if it is majority owned bynationals of member countries. State-owned corporations are eligible if they operate on acommercial basis.

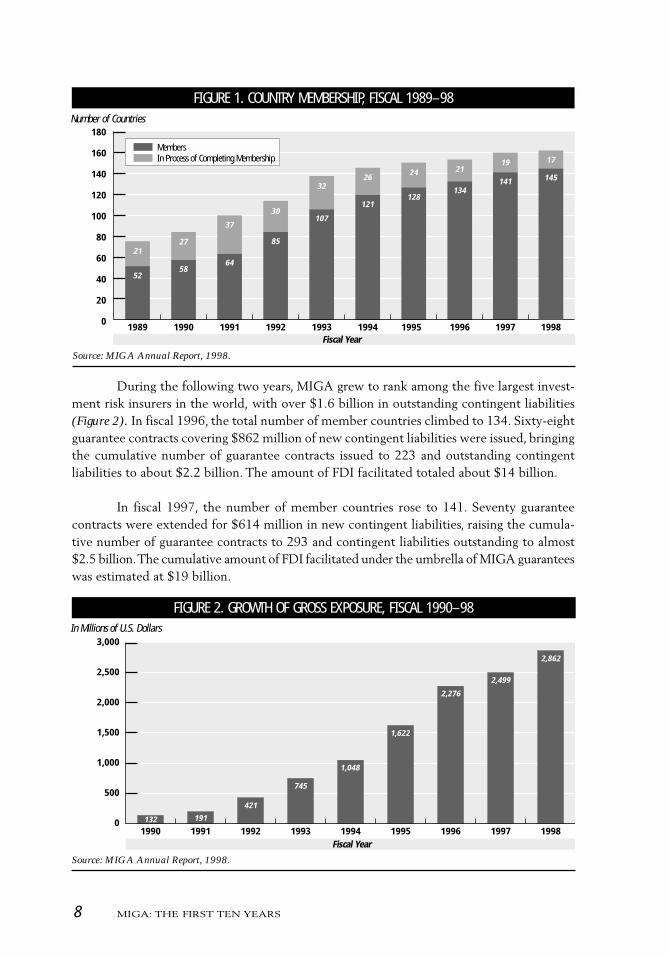

MIGA’s Takeoff

The early years laid the foundations for MIGA’s takeoff in the midst of a major surgein global FDI flows. In its first five years, country membership reached 107 (Figure 1). Twenty-one guarantee contracts were written in eight host countries in 1992, with $313 million ofcoverage supporting $600 million in investment. In the following year, 27 guarantee contractswere written in 14 host countries, with $374 million of coverage supporting $1.8 billion ininvestment.

THE GUARANTEE PROGRAM

MIGA: THE FIRST TEN YEARS8

During the following two years, MIGA grew to rank among the five largest invest-ment risk insurers in the world, with over $1.6 billion in outstanding contingent liabilities(Figure 2). In fiscal 1996, the total number of member countries climbed to 134. Sixty-eightguarantee contracts covering $862 million of new contingent liabilities were issued, bringingthe cumulative number of guarantee contracts issued to 223 and outstanding contingentliabilities to about $2.2 billion. The amount of FDI facilitated totaled about $14 billion.

In fiscal 1997, the number of member countries rose to 141. Seventy guaranteecontracts were extended for $614 million in new contingent liabilities, raising the cumula-tive number of guarantee contracts to 293 and contingent liabilities outstanding to almost$2.5 billion. The cumulative amount of FDI facilitated under the umbrella of MIGA guaranteeswas estimated at $19 billion.

FIGURE 1. COUNTRY MEMBERSHIP, FISCAL 1989–98

180

160

140

120

100

80

60

40

20

0

Number of Countries

1989 1990 1991 1992 1993 1994 1995 1996 1997

141

19

21

52

27

58

37

64

30

85

3226 24 21

134128

121

107

1998

145

17

Fiscal Year

In Process of Completing MembershipMembers

FIGURE 2. GROWTH OF GROSS EXPOSURE, FISCAL 1990–98

Source: MIGA Annual Report, 1998.

Source: MIGA Annual Report, 1998.

In Millions of U.S. Dollars

0

500

1,000

1,500

2,000

2,500

3,000

Fiscal Year1990 1991 1992 1993 1994 1995 1996 1997 1998

2,862

191132

421

745

1,048

1,622

2,276

2,499

9

In fiscal 1998, the number of member countries reached 145, and 17 countries werein the process of fulfilling membership requirements (see Annex 1: MIGA Member andSignatory Countries). MIGA issued 55 new guarantee contracts for $830 million in coverageand had about $2.8 billion in outstanding contingent liabilities. Between fiscal 1990 and1998, MIGA issued a total 348 guarantee contracts for $4.2 billion in total coverage, facilitatingan estimated $25 billion in FDI (Table 2).

TABLE 2. MIGA‘S GUARANTEE PORTFOLIO AND FDI FACILITATED, FISCAL 1990–98Category 1990 1991 1992 1993 1994 1995 1996 1997 1998 Total

Number of Guarantees Issued 4 11 21 27 38 54 68 70 55 348Amount of Guarantees Issued

(millions of U.S. dollars) 132 59 313 374 372 672 862 614 830 4,228Estimated FDI Facilitated

(billions of U.S. dollars) 1.0 0.9 0.6 1.8 1.3 2.3 6.5 4.7 6.1 25.2

Source: Gerald T. West and Ethel I. Tarazona, MIGA and Foreign Direct Investment: Evaluating Developmental Impacts,The World Bank, 1998.Note: For consistency purposes, MIGA has applied the same measurement standards currently used for projectsguaranteed by MIGA in previous fiscal years. This has resulted in slightly different statistics for FDI facilitated infiscal years 1991, 1992, and 1993 from what was published earlier by MIGA.

MIGA’s Role in Enhancing the Flow of ForeignDirect Investment

Among all sources of external support, the contribution of FDI to the developmentprocess is particularly valuable. The most widely used models of economic developmentcharacterize developing countries as suffering from the consequences of a vicious cycle inwhich low levels of productivity lead to low wages, which lead to low savings, which leadto low levels of investment, which then perpetuate low levels of productivity. FDI is able tobreak this vicious cycle by infusing new capital to complement local savings. The viciouscycle can be transformed into a virtuous cycle of reinvestment and expansion.

FDI is especially desirable because it is more stable than other sources of externalfunding. Most movements in international financial markets consist of transfers of short-term debt instruments and near-money equivalents, which cross borders via computers withinfractions of a second. As witnessed during the Mexican peso crisis of 1994–95 and the Asiafinancial crisis of 1997–98, commercial bank lending can become only slightly less volatile,turning negative in very short periods of time (with net lending by banks limited to projectfinance; and to short-term, trade-related loans to only the most creditworthy borrowers).Movements of portfolio capital can likewise become highly unstable, as witnessed by thewide swings in stock markets in recent years in both Asia and Latin America.

In comparison, FDI is an activity in which the parent corporation establishes its ownaffiliate in a host country to engage in a somewhat longer-term activity of production, pro-cessing, or distribution. Unsound economic policies and political crises in a host country canand do force foreign investors to delay projects or, in extreme cases, to withdraw altogether.

THE GUARANTEE PROGRAM

MIGA: THE FIRST TEN YEARS10

Ownership of fixed assets, however, makes FDI comparatively “patient” capital. Indeed, periodsof financial crisis that normally spur short-term capital flight actually strengthen the interna-tional competitive position of foreign investors. As has been demonstrated in Latin Americaand Asia, following a currency devaluation and economic restructuring, domestic costs arelowered in foreign currency terms. The fundamental prospects for foreign direct investorsthus improve.

Focusing on FDI as a source of capital is only the narrowest—not the most important—of the contributions that foreign firms can provide to the development process. In additionto complementing local savings, foreign firms can supply more effective management, mar-keting, and technology to improve productivity. This raises efficiency and leads to higherrates of economic growth.

From a more dynamic perspective, FDI stimulates competition, encourages techno-logical innovation, and engenders worker training and adoption of managerial best practicesand quality standards among rivals and suppliers. This continuous process only partially com-pensates foreign firms for the spillover effects that affect other participants in the economy.These spillovers, or externalities, suggest that the social value of foreign investment activitiesare greater than the rewards reaped by private investors.

To assess MIGA’s role in stimulating FDI activity around the world, MIGA con-ducted a confidential and anonymous survey of all current guarantee holders in 1994, and1996. Seventy-three percent of all MIGA clients responded. A majority of the respondentsin both surveys considered MIGA coverage to have been “absolutely critical” in their deci-sion to proceed with their planned investment. Almost all reported a desire to use MIGAinsurance again.

Some of the indicators of the direct developmental impact of MIGA-guaranteedprojects include the flow of capital, amount of output produced, number of jobs created,and the exports and taxes generated. Between fiscal 1990 and 1998, MIGA-supported projectsdirectly created an estimated 46,800 new jobs. In 1998, a detailed evaluation of 25 MIGA-guaranteed projects issued during fiscal 1991–95 showed that the initial development impactsanticipated by investors were surpassed by the actual impacts of the projects (Table 3).

TABLE 3. SELECTED DEVELOPMENTAL IMPACTS (25 EVALUATED PROJECTS)Percent

Impacts Anticipated Actual Difference

Number of New Jobs Directly Created 5,026 5,796 +15

(in millions of U.S. dollars)Annual Taxes and Duties Paid to the Government 53.5 87.4 +63Annual Exports Generated * 353.1 399.8 +13Total Project Investment Facilitated 1358.3 1,546.4 +14

* Includes only the 8 export-generating projects.Source: Gerald T. West and Ethel I. Tarazona, MIGA and Foreign Direct Investment: Evaluating Developmental Impacts,The World Bank, 1998.

11

Diversifying the Destination ofForeign Direct Investment

A source of persistent concern has been that FDI tends to flow to only a relativelysmall number of developing countries. In 1997, for example, 10 developing countriesaccounted for some 72 percent of all FDI flows (Table 4). China alone received about $37 bil-lion or 30 percent of the total (although a substantial component of these investments rep-resented so-called round tripping by indigenous capital holders).

TABLE 4. FDI FLOWS TO THE TOP TEN RECIPIENT DEVELOPING COUNTRIES(in billions of U.S. dollars)Country 1991 Country 1994 Country 1997*

Mexico 4.7 China 33.8 China 37.0China 4.3 Mexico 11.0 Brazil 15.8Malaysia 4.0 Malaysia 4.3 Mexico 8.1Argentina 2.4 Peru 3.1 Indonesia 5.8Thailand 2.0 Brazil 3.1 Poland 4.5Venezuela 1.9 Argentina 3.1 Malaysia 4.1Indonesia 1.5 Indonesia 2.1 Argentina 3.8Hungary 1.5 Nigeria 1.9 Chile 3.5Brazil 1.1 Poland 1.9 India 3.1Turkey 0.8 Chile 1.8 Venezuela 2.9

Top 10 share in FDI to alldeveloping countries (%) 74.2 76.1 72.3

* PreliminarySource: The World Bank, Global Development Finance, 1998.

However, since its inception, MIGA has deliberately allocated its scarce guaranteeresources in a manner that was contrary to the conventional follow-the-herd phenomenonamong international investors. In fiscal 1998, MIGA guarantees outstanding in the 10 largestrecipients still amounted to only 27 percent of all guarantees (Table 5).

TABLE 5. MIGA‘S GROSS EXPOSURE IN THE TOP TEN COUNTRIES RECEIVING FDIMIGA Guarantees Outstanding

(as of June 30, 1998)

Ranking in 1997 Country Millions of U.S. dollars Percentage of portfolio

1 China 131.1 4.62 Brazil 195.0 6.83 Mexico 0.0 0.04 Indonesia 80.4 2.85 Poland 24.3 0.96 Malaysia 0.0 0.07 Argentina 236.1 8.38 Chile 31.3 1.19 India 9.6 0.3

10 Venezuela 68.5 2.4Total 776.3 27.2

Source: Rankings, The World Bank, Global Development Finance, 1998; MIGA guarantees outstanding, MIGA AnnualReport 1998.

THE GUARANTEE PROGRAM

MIGA: THE FIRST TEN YEARS12

Overall, MIGA’s portfolio is well diversified by country (see Annex 2: Risk Profile).As of the end of fiscal year 1998, MIGA had guarantees outstanding for projects in 52 devel-oping member countries. In all, MIGA has facilitated FDI into 62 developing membercountries. Of particular note, 28 percent of MIGA’s portfolio consists of projects in thepoorest countries, countries that are eligible for concessional lending by the InternationalDevelopment Association (IDA) (Table 6). Since it began operating, MIGA has issued about$1 billion in coverage for investments in 26 IDA-eligible member countries.

TABLE 6. MIGA GUARANTEES OUTSTANDING IN 22 IDA-ELIGIBLE COUNTRIESMIGA guarantees outstanding*

(as of June 30, 1998)

Country Millions of U.S. dollars Percentage of portfolio

Pakistan 169.8 5.9China 131.1 4.6Kyrgyz Republic 64.7 2.3Bolivia 62.5 2.2Bangladesh 59.2 2.1Uganda 54.0 1.9Mali 50.0 1.8Mozambique 40.0 1.4Nepal 32.8 1.2Guyana 30.6 1.1Honduras 25.9 0.9Equatorial Guinea 24.0 0.8Azerbaijan 19.2 0.7India 9.6 0.3Sri Lanka 7.1 0.3Guinea 6.0 0.2Kenya 4.7 0.2Cape Verde 2.4 0.1Angola 2.3 0.1Georgia 2.1 0.1Madagascar 1.7 0.1Tanzania 0.3 0.01

Total $800.0 28.31

*In addition, MIGA guarantees covered investments of about $200 million in Cameroon, Egypt, Ghana, and Vietnam.Source: MIGA Annual Report, 1998.

13

MIGA as a Catalyst for New Investment:The Case of KAFCO in Bangladesh

A detailed examination of individual MIGA-supported projects demonstrates howMIGA has acted as a catalyst for investors, lenders, and other investment insurers to ventureinto countries.

The Karnaphuli Fertilizer Company Limited (KAFCO), near Chittagong City inBangladesh, is one such example. In fiscal 1991 and 1993, MIGA issued four guaranteecontracts covering portions of the investments (about $500 million) by the Marubeni andChiyoda Corporations in a major ammonia and granular urea processing plant. MIGA assessedthe developmental impacts of the project in September 1996.

After employing 2,000 workers during the construction phase, KAFCO hired 602full-time regular workers on a permanent basis, of whom only 5 were expatriates. Bangladeshinationals held more than 95 percent of the management positions. Contractors employedanother 320 workers. KAFCO wages and salaries averaged two to four times higher thancomparable host country rates.

The company also stimulated related businesses by procuring some $33 million inlocal goods and services, approximately $2 million in contractual services, and about $1 mil-lion in administrative services. KAFCO used state-of-the-art technology, which increasedefficiency, lowered production costs, and conserved energy use at the plant. These develop-ments provided the incentive for other fertilizer companies in Bangladesh to improve theirtechnologies and increase industry standard in the country.

To ensure the availability of skilled workers to manage the plant, KAFCO created anon-going training program with more than a 1,000 participants. Forty-four managers weresent for training in Denmark, the Netherlands, Indonesia, Japan, Pakistan, and Singapore.Workers in other fertilizer firms also benefited from technology workshops conducted byKAFCO. The company also provided social infrastructure, including a residential complex ofmodern family apartments in new five-story buildings. The company built a 5 bed healthclinic with a full-time doctor and several nurses, and a school with 15 teachers providingclasses up to the high school level to 115 students.

KAFCO was the first company in Bangladesh to develop ammonia for export, allowingthe country to diversify away from traditional commodities such as tea and jute. KAFCOgenerated almost $91 million in hard currency earnings in 1995, or 3 percent of the totalmerchandise exports from Bangladesh, an amount comparable to the total export earningsfrom jute and tea combined. In addition, KAFCO paid about $3.5 million to the govern-ment in taxes and duties in 1995, an amount that was due to expand considerably with theexpiration of an initial tax holiday.

THE GUARANTEE PROGRAM

MIGA: THE FIRST TEN YEARS14

The KAFCO project was, at the time, the largest joint-venture foreign investment inBangladesh and has provided Bangladesh with direct benefits and other economic externali-ties. KAFCO has also served as a good example for domestic firms in its use of advancedtechnology, product quality, human resources management, and investment in social ser-vices. The project is now widely considered to be a showcase for foreign investment inBangladesh. It involved collaboration of four semigovernmental agencies and four privatecompanies. Financing for the project included loans from four national export credit agen-cies, commercial banks, and shareholders. (Several of those investors and agencies reportedthat it was the first time they had seriously considered a project in Bangladesh). Further-more, KAFCO made ground-breaking use of investment insurance provided by five organi-zations, including MIGA.

MIGA as a Catalyst for Policy Reform:The Case of Banco de Boston in Argentina

The MIGA guarantee facility has played a strategic role in reinforcing broader policyreforms as well. The timing of the insurance of a MIGA guarantee and project selection haveenabled MIGA (in conjunction with other members of the World Bank Group) to have acatalytic effect on general policy reform, and participate in a type of political externality. Agood example is a project in Argentina, guaranteed by MIGA in fiscal 1993, in which theFirst National Bank of Boston (now BankBoston) created a long-term mortgage program inthe country.

After a number of years of poor macroeconomic management, the Government ofArgentina undertook a comprehensive restructuring program whose centerpiece—aConvertibility Plan to place the peso at par with the U.S. dollar—was passed in April 1991.Willing to take the risk that internal economic discipline would curb the legacy of rampantinflation, the Bank of Boston positioned itself as the first major private financial institutionwith a program to meet what bank planners estimated to be a pent-up demand for lowerinterest mortgages. MIGA was asked to provide coverage against currency transfer risk andexpropriation of funds.

When the MIGA guarantee was issued to Bank of Boston, prevalent mortgage rateswere about 23 percent per annum, with a maximum tenor of five years, and were availableto only the highest income earners. The Bank of Boston used the guaranteed funds to beginto offer 10-year maturities, with doubled amortization periods and lower mortgage pay-ments. The number of qualifying applications from lower income earners expanded. Otherbanks followed Bank of Boston’s lead, which stimulated vigorous competition within thefinancial sector. Reinforced by the crucial ingredient of Argentine economic discipline, between1992 and 1997, 5-year/23 percent mortgages gave way to loans of up to 20 years with interestrates of 12 to 15 percent.

15

Fiscal 1993 Fiscal 1998

Manufacturing28%

Mining22%

Infrastructure3%

Services2%

Financial36%

Tourism 1%Agribusiness

8%

Manufacturing20%

Mining 15%

Infrastructure19%

Oil and Gas 2%

Financial38%

Tourism3%Agribusiness 2%

Services1%

In a virtuous cycle that helped the Argentine reform program stay on track, thechanges in the mortgage market had twin positive effects on the domestic economy. First, itstimulated a construction boom that affected brick, cement, wood, steel, and home furnish-ing and home appliance businesses; and second, it created increased employment in thebanking sector itself. This, in turn, helped to offset the job loss (and political discontent) thataccompanied the onset of macroeconomic reform. Between 1991 and 1993 alone, FDI flowsinto Argentina almost doubled.

Evolution of MIGA Coverage by Regionand Sector

In fiscal 1998, the Latin America and the Caribbean Region continued to form thelargest portion of MIGA’s guarantee portfolio with a 44 percent share, followed by the Europe& Central Asia and Asia & Pacific Regions. Africa’s share of the outstanding portfolio hasincreased from 1 percent to about 7 percent between fiscal 1992 and 1998. (In fiscal 1998,the Middle East Region comprised almost 2 percent of MIGA’s outstanding portfolio, whereasthere were no outstanding liabilities in the region until fiscal year 1996).

There have been changes in the relative proportions of the sectors covered in MIGA’sportfolio since its early years (Figure 3). Between fiscal 1993 and 1998, the share of MIGA’sportfolio devoted to infrastructure has expanded sixfold. (Furthermore, about 35 percent ofthe 1,300 active applications at the end of fiscal 1998 are in the infrastructure sector, whichsuggests a strong basis for continued growth in coverage).

FIGURE 3. OUTSTANDING PORTFOLIO BY SECTOR, FISCAL 1993 AND 1998

THE GUARANTEE PROGRAM

Source: MIGA Annual Report, 1998.

MIGA: THE FIRST TEN YEARS16

Fiscal 1993 Fiscal 1998

Distribution of Investor Countries

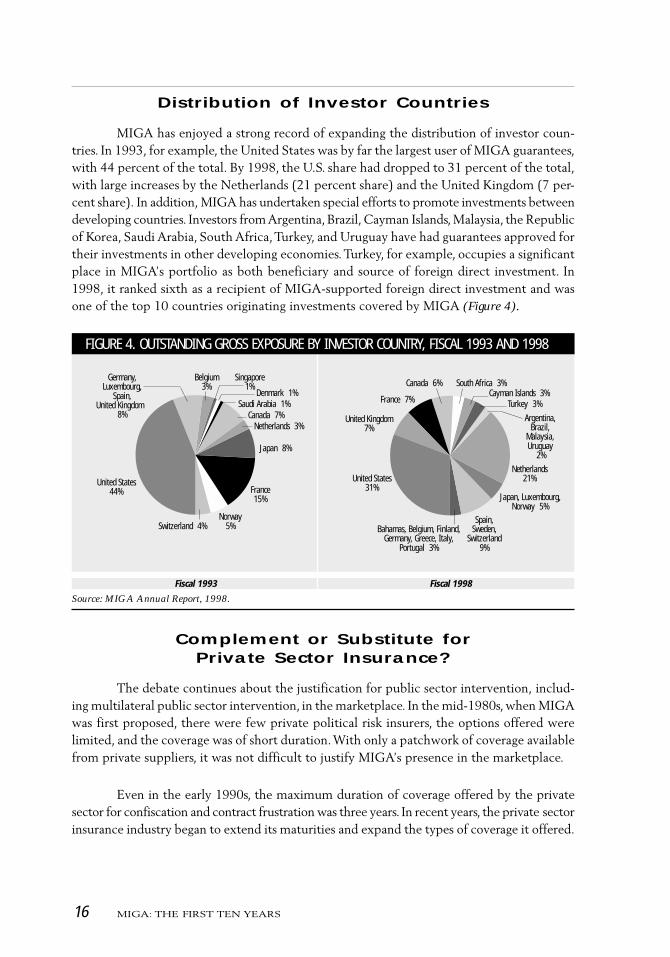

MIGA has enjoyed a strong record of expanding the distribution of investor coun-tries. In 1993, for example, the United States was by far the largest user of MIGA guarantees,with 44 percent of the total. By 1998, the U.S. share had dropped to 31 percent of the total,with large increases by the Netherlands (21 percent share) and the United Kingdom (7 per-cent share). In addition, MIGA has undertaken special efforts to promote investments betweendeveloping countries. Investors from Argentina, Brazil, Cayman Islands, Malaysia, the Republicof Korea, Saudi Arabia, South Africa, Turkey, and Uruguay have had guarantees approved fortheir investments in other developing economies. Turkey, for example, occupies a significantplace in MIGA’s portfolio as both beneficiary and source of foreign direct investment. In1998, it ranked sixth as a recipient of MIGA-supported foreign direct investment and wasone of the top 10 countries originating investments covered by MIGA (Figure 4).

FIGURE 4. OUTSTANDING GROSS EXPOSURE BY INVESTOR COUNTRY, FISCAL 1993 AND 1998

Complement or Substitute forPrivate Sector Insurance?

The debate continues about the justification for public sector intervention, includ-ing multilateral public sector intervention, in the marketplace. In the mid-1980s, when MIGAwas first proposed, there were few private political risk insurers, the options offered werelimited, and the coverage was of short duration. With only a patchwork of coverage availablefrom private suppliers, it was not difficult to justify MIGA’s presence in the marketplace.

Even in the early 1990s, the maximum duration of coverage offered by the privatesector for confiscation and contract frustration was three years. In recent years, the private sectorinsurance industry began to extend its maturities and expand the types of coverage it offered.

United States44%

Canada 7%Netherlands 3%

Norway5%Switzerland 4%

France15%

Singapore1%

Germany,Luxembourg,

Spain,United Kingdom

8%

Belgium3%

Denmark 1%Saudi Arabia 1%

Japan 8%

United Kingdom7%

Turkey 3%

Netherlands21%United States

31%

Spain,Sweden,

Switzerland9%

Canada 6%

Argentina,Brazil,

Malaysia,Uruguay

2%

Japan, Luxembourg,Norway 5%

France 7%

South Africa 3%Cayman Islands 3%

Bahamas, Belgium, Finland,Germany, Greece, Italy,

Portugal 3%

Source: MIGA Annual Report, 1998.

17

New participants have entered the marketplace. In addition, insurance capacity has continuedto rise. Given the current robust growth of private political risk insurers, might it be possiblesimply to let private markets meet the demand for political risk insurance by internationalinvestors? How will this development affect MIGA’s presence in the marketplace?

From its very beginnings, MIGA was expected to provide guarantee services toinvestors in projects of acute vulnerability to changes in host government policies or com-mitments. Such acute vulnerability is especially pronounced for investors in natural resourceand infrastructure projects, who must make large fixed investments with long payback periods.The profitability of such projects is highly sensitive to the stability of the regulatory environ-ment in the host country. These investors seldom have control over the rapidly changingtechnological processes, advertising, and marketing that many manufacturing firms useto defend themselves against host authorities who want to change the terms of their initialinvestment agreements. They face unavoidable exposure to what the business literature refersto as the obsolescing bargain.

The obsolescing bargain is the propensity of host authorities—often successors tothose who signed the original investment agreements—to tighten the terms and conditionsof investment contracts drawn to reward high early risk and uncertainty, after it has dissipatedand the project has proved successful.

Private markets alone find it difficult to deal effectively with the phenomenon ofthe obsolescing bargain. To be sure, investors and financial backers in such projects can insiston yet higher initial risk premiums to reflect the vulnerability of their status. However, theproblem posed by the obsolescing bargain is not the lack of generous treatment at the frontend of a long-term investment, but rather the stability of treatment over the life of the long-term investment. Investors and financial backers can raise the hurdle rate that such projectsmust meet before they agree to make the investment, but this merely leaves many commer-cially promising projects without sponsors.

There exists, therefore, what public policy analysis identifies as a market failure—inthis case, a failure in contract “markets”—which requires public sector intervention to cor-rect. The challenge is to find some mechanism that helps ensure the credibility of commit-ments. The ability to make credible commitments strengthens the negotiating position of allparties, and serves the interests of host countries as well as international investors and lenders.MIGA is ideally positioned to reinforce the credibility of host country commitments, andthus help correct for this form of market failure.

MIGA has an open channel for policy dialogue with each host country in which itissues guarantees, a dialogue that is exercised through the ongoing technical assistance MIGAprovides on investment matters, and which is backed by a host country’s undertakings as amember of MIGA (including mutual agreements on the legal protection of MIGA-insuredinvestments).

THE GUARANTEE PROGRAM

MIGA: THE FIRST TEN YEARS18

More broadly, MIGA influence over the maintenance of appropriate host countrypolicies toward foreign investment is buttressed by MIGA’s close relationship with otheragencies in the World Bank Group (in particular, the IBRD and IDA), a relationship thatprovides leverage over current guarantee and lending activities; leverage over future guaran-tee and lending activities; and leverage over other sources of investment, finance, and assis-tance. This leverage strengthens MIGA’s hand in mediating between foreign investors andhost authorities, and in pursuing recovery should mediation fail.

The umbrella of protection against breach of contract that comes from MIGA’spresence derives, therefore, not simply from the compensation its guarantees provide butalso from its role in deterring any abrogation of promises solemnly entered into by a hostcountry. This deterrence role survives the transition from one host country government toanother.

In the 10 years of MIGA’s existence, MIGA has not suffered a claim loss. Indeedthere have been no claims lodged. MIGA has been able to resolve disputes between clientsand host countries before they become claims. In several pre-claim situations, MIGA wasable to find satisfactory solutions for all parties involved, safeguarding the client’s invest-ment and allowing the host country to continue benefiting from it.

Financial Constraints on MIGA’sGuarantee Activities

In the first half of the 1980s, when the creation of MIGA was under early discussion,flows of FDI to the developing world averaged $19 billion annually (in 1985 FDI had droppedto $9 billion). The establishment of an investment insurer with a capital base of $1 billion,with a capability to write coverage up to five times its capital and reserves, or more than$5 billion, appeared to be sufficiently large to cover the demand. There seemed little needthen to anticipate that FDI flows would grow to an annual level of about $120 billion, asthey did in 1997.

With FDI flows more than quintupling since the mid-1980s, the demand for politi-cal risk insurance services from all sources likewise has expanded sharply. The 25 membersof the Berne Union that provide investment insurance (including MIGA) have reported amore than sixfold increase in annual coverage (from $2 billion in 1989 to $15 billion in1997), with their total portfolios more than doubling (from $17 billion in 1990 to $40 bil-lion in 1997). At the margin, in the recent period, there has been an 80 percent increase innew coverage and a 25 percent increase in total portfolio. MIGA had received some 40 newpreliminary applications each month, with a pipeline of about 100 definitive applicationsand approximately 1,300 preliminary applications at the end of fiscal 1998.

Beginning in 1996, MIGA management reported to its Board that the extrapolationof existing positive trends could, if unfettered by financial limitations, double the size of itsportfolio by the year 2000. Within its existing financial constraints, in contrast, MIGA faceda future of stagnation or, quite possibly, retrenchment in the event of large claims.

19

MIGA’s financial constraints took two forms: insurance capacity (the so-called head-room problem, and liquidity, or capacity to pay claims. The constraints on insurance capacitysprang directly from multiplying the amount of its assets (subscribed capital and reserves,totaling about $ 1,092 million in 1996) by the prescribed risk-to-assets ratio of 3.5:1, yieldingan underwriting capacity of about $3.8 billion. MIGA management forecasted a need toimpose restrictions on new underwriting as early as mid-1997 unless assets could be augmentedor the allowable risk-to-asset ratio increased. (MIGA had already increased the allowablerisk-to-assets ratio from 1.5:1 to 2.5:1 in 1994, and to 3.5:1 in 1996.)

The constraints on liquidity, or on capacity to pay claims arose from a total exposurein MIGA’s guarantee portfolio in 1996 of approximately $2.3 billion backed by claims reservesand retained earnings of some $37 million, promissory notes of members of $100 million,paid-in cash portions of capital subscriptions of $211 million, and callable capital of $847 mil-lion. Any potential claims outlays larger than the $37 million in reserves and retained earn-ings would require MIGA to cash portions of the promissory notes, or liquidate part of thepaid-in capital, or call in portions of the callable capital subscriptions. While MIGA then hadand continues to have a claims-free record, management did not think it prudent to assumethat this would continue indefinitely.

Some of the pressure from these constraints could be relieved by slowing the issuanceof new coverage, by imposing tighter limits per project and per country, and by greaterselectivity in choosing where to offer guarantees. But in view of MIGA’s record of facilitatinginvestment in new and untried regions and activities, and in view of increasing demand frommegaprojects in infrastructure and natural resources, there seemed little reason to penalizeMIGA for those activities where it was demonstrating increasing success.

Consequently, in 1997, the Development Committee approved a $1 billion recapi-talization package for MIGA; MIGA’s Council of Governors approved the package inApril 1998, when voting of member countries commenced. This recapitalization packageconsisted of an $850 million capital increase, of which $150 million was payable in cash and$700 million was callable, accompanied by a grant transfer of $150 million from the IBRD toMIGA. The capital increase was part of a 10-year strategy that would allow MIGA’s netcontingent liabilities to grow to approximately $10 billion by the end of the period.

Cooperative Efforts to Expand Capacity

The 10-year strategy considered by the Board of Directors to expand the underwritingcapacity of MIGA envisioned the issuance of up to $24 billion in new guarantees. Theexpansion of funding described in the previous section would allow to achieve that objec-tive. Article 21 of the MIGA Convention calls for cooperation with other insurers to encour-age such insurers to provide coverage of noncommercial risks in developing members coun-tries on conditions similar to those applied by the Agency. As its guarantee portfolio matured,MIGA intensified its efforts to work with other insurers to enlarge its own guarantee capacity.

THE GUARANTEE PROGRAM

MIGA: THE FIRST TEN YEARS20

Two options have been reinsurance and coinsurance. Over the years, MIGA has co-insured or reinsured national insurers from Australia, Canada, Italy, Japan, Norway, Spain,the United Kingdom, and the United States. MIGA also has worked closely with privateinsurers such as the American Insurance Group (AIG), Inc.; Lloyd’s of London; ACE Insur-ance Company, Ltd. (ACE); Sovereign Risk; UNISTRAT; and Zurich-American Political Risk.

In 1997, MIGA launched two new innovative mechanisms for coinsurance and rein-surance. The Cooperative Underwriting Program (CUP) was designed to encourage privateinsurers to cover projects in developing countries whose risks they might otherwise havebeen reluctant to assume. In the CUP arrangement, MIGA is the insurer-of-record but retainsonly a portion of the risk for its own account. One or more private insurers underwrite theremainder of the coverage. For MIGA, this arrangement offers a multiplier effect in the useof its assets in providing coverage. For the private insurers, this arrangement offers the com-fort of having MIGA serve as mediator if disputes arise and of having MIGA seek remediesif mediation fails (this arrangement also offers the option of protected self-insurance if aproject sponsor decides to use a captive insurance entity for the CUP agreement).

In fiscal 1997, MIGA signed its first contract under the CUP, with Enron Corpora-tion of the United States, for a power project in Indonesia. In fiscal 1998, MIGA signed acoinsurance contract with Zurich-American Political Risk for an integrated oil and gasexploration project in Argentina, sponsored by El Paso Energy International Company. Inaddition, MIGA concluded a cooperation agreement with Brockbank Syndicate Manage-ment Ltd. of Lloyd’s of London in fiscal 1998. Under the agreement, Brockbank will makeavailable up to $100 million in additional capacity per transaction, on a case-by-case basis.

In the field of reinsurance, MIGA adopted an unprecedented approach by signing aquota share treaty, or whole portfolio reinsurance agreement, with ACE, a subsidiary of ACELimited. The MIGA-ACE agreement was the first of its kind between a private insurer anda multilateral agency to provide long-term (up to 20 years) political risk insurance. Underterms of this agreement, ACE reinsures MIGA contracts of guarantee written for amountsexceeding $5 million. This enables MIGA to offer additional guarantee capacity across itsentire portfolio, and also to expand its gross guarantee capacity at the project and countrylevel. With underwriting limits (net of reinsurance) at $225 million per country and $50 mil-lion per project, the ACE arrangement facilitates significantly larger guarantee capacity(a feature of particular importance in supporting the infrastructure, energy, and miningsectors). The agreement expanded MIGA’s per-project-coverage limit by $25 million andper-country limit up to $100 million.

21

In addition, MIGA operates two investment guarantee trust funds established tofacilitate foreign investment in Bosnia and Herzegovina and in the West Bank and Gaza.MIGA issues guarantees on behalf of, and pays compensation from, the trust funds. The trustfunds provide long-term insurance for eligible small and medium-size investments. Eligibleinvestments include new contributions associated with the expansion, modernization, orfinancial restructuring of existing projects, and for acquisitions that involve the privatizationof state enterprises. The European Union has sponsored the Investment Guarantee TrustFund for Bosnia and Herzegovina with a special credit line for this purpose. The PalestinianAuthority, through an IDA loan, has contributed to the Investment Guarantee Trust Fundfor the West Bank and Gaza. In 1998, the Government of Japan and the European Invest-ment Bank provided additional contributions to the West Bank and Gaza trust fund.

THE GUARANTEE PROGRAM

MIGA: THE FIRST TEN YEARS22

III. TECHNICAL ASSISTANCE ACTIVITIES

MIGA’s Investment Marketing Services Department (IMS) is the institutional conduitthrough which MIGA provides technical assistance services to its member countries. Theoperations of IMS over time are best understood in the context of the origins and growth ofMIGA’s technical assistance function.

Origins of MIGA’sTechnical Assistance Function

When MIGA was conceived, its creators saw the need for a technical assistance andadvisory function that would serve to complement its guarantee activity. The precise natureof the recommended function is recorded in the MIGA Convention. The two relevant articlesof the MIGA Convention are Articles 2(b) and 23. Article 2(b) indicates that “to serve itsobjective of encouraging the flow of investments for productive purposes among developingmember countries, thus supplementing the activities of the IBRD, IFC and other interna-tional development finance institutions, the Agency shall carry out appropriate complemen-tary activities to promote the flow of investments to and among developing member countries.”

Article 23 of the MIGA Convention elaborates more precisely the nature of thecomplementary activities envisaged by those who created MIGA. The focus of these activi-ties was to be investment promotion, broadly defined. Indeed, the importance of the rolethat sections (a) and (c) of this particular Article have played in future deliberations on therole and functions of MIGA and its technical assistance arm justify a specific citation of thesesections:

(a) The Agency shall carry out research, undertake activities to promote invest-ment flows and disseminate information on investment opportunities in developingcountries with a view to improving the environment for foreign investment flows tosuch countries. The Agency may, upon the request of a member, provide technicaladvice and assistance to improve the investment conditions in the territories of thatmember. In performing these activities, the Agency shall:

(i) be guided by relevant investment agreements among member countries;(ii) seek to remove impediments, in both developed and developing membercountries, to the flow of investment to developing member countries; and(iii) coordinate with other agencies concerned with the promotion of foreigninvestment, and in particular the International Finance Corporation.

……

(c) The Agency shall give particular attention in its promotional efforts to the im-portance of increasing the flow of investments among developing member countries.

23

At the first meeting of the Board of Directors on June 22, 1988, the president andchairman of the board presented operational regulations for the implementation of the Con-vention. Chapter seven of the Operational Regulations directed MIGA to “carry out advi-sory and technical programs for the purpose of helping developing member countries toobtain increased flows of foreign investment for productive purposes,” and indicated thatthese programs are “principally intended to complement the programs of the World Bank,the IFC and other development agencies in improving conditions and institutions in devel-oping countries for the encouragement of foreign investment, including the reduction ofimpediments to investment.”

Institutionalization of theTechnical Assistance Function

The ratification of the Convention and the development of the ancillary operationalregulations set the stage for MIGA to develop an institutional capability to execute thefunctions assigned to it under Articles 2(b) and 23. To carry out the technical assistancefunction assigned by its Convention, in 1989 MIGA management established the Policy andAdvisory Services (PAS) unit.

By this time, MIGA’s institutional capability for conducting technical assistance alsoinvolved another unit within the World Bank Group. Between the 1985 submission of theMIGA Convention to member governments of the IBRD and the 1988 ratification of thatConvention by a plurality of members, another unit had been created and had quickly be-come involved in providing advice and assistance to governments in the area of investmentpromotion.

In 1986, the Foreign Investment Advisory Service (FIAS) was formed, largely out ofthe foreign investment related activities of the Development Department of the IFC. FIASwas mandated to provide advice to member governments of the IFC interested in improvingthe attractiveness of their countries as sites for foreign investment. In light of this newdevelopment, and given the importance the MIGA Convention placed on cooperationbetween MIGA and other units of the World Bank Group in its investment promotion role,it was decided that one component of the advisory role of the newly established MIGAshould be delivered through the mechanism of MIGA’s joining with IFC to oversee thenascent FIAS.

To this end, a joint venture agreement was formulated between IFC and MIGA,which was approved by the Boards of both institutions on September 14 and October 26,1988, respectively. The joint venture agreement assigned to FIAS the responsibility forexecuting several components of MIGA’s mandate. The operational regulations to the MIGAConvention were then changed on January 25, 1989 to recognize this new development.

TECHNICAL ASSISTANCE ACTIVITIES

MIGA: THE FIRST TEN YEARS24

In particular, the revised operations regulations indicated that “projects primarilyintended to provide technical or advisory services to members and research essential to suchservices should be designed and carried out by the Foreign Investment Advisory Service, afacility to be jointly administered and supported by the Agency and the IFC. Other technical,advisory and consultative activities primarily designed to serve the membership of the Agencyas a whole or to support the guarantee program may be carried out solely by the Agency orin association with other international or national agencies, as it judges in each case to bemost effective and appropriate.”

The division of responsibility between FIAS and PAS was that FIAS would beresponsible for advising a member government on its laws, policies, institutions and pro-grams designed to attract and retain foreign investment. PAS was assigned the responsibilityof providing operational assistance to member countries in the execution of their invest-ment promotion programs. The choice of this particular role for PAS came out of the find-ings of senior managers at MIGA that this was the area in which there was the least assis-tance available to developing countries from the international development community.

Executing the Technical Assistance Function:1989 to 1993

With the division of service responsibility between FIAS and PAS clearly defined,MIGA moved to the implementation of its technical assistance function, which can be readilydivided into two five-year periods: the early (1989 to 1993) period, and the later (1994 to1998) period. In the early period, MIGA executed its technical assistance function withrespect to policy through its joint venture with IFC in the form of FIAS. Beyond policyadvice in this form, the early period was characterized by the attempts of PAS to identifyits niche in the market for foreign investment-related advisory services by internationalinstitutions.

MIGA received many requests from countries for assistance in the operational sideof investment promotion. Given this interest, and the fact that its policy advisory functionhad been delegated to FIAS, PAS concentrated on assisting member countries in organizingand conducting of traditional investment promotion activities such as conferences and mis-sions. PAS was determined to execute these functions effectively since, at the time, the inter-national development community had some concerns about the effectiveness with whichconferences and missions achieved the goal of influencing flows of FDI.

PAS submitted its first work program to the Board of MIGA prior to the start offiscal 1990 (July 1989 to June 1990). This work program indicated that PAS would be involvedin two types of investment promotion technical assistance. The first was the preparation ofcountry investor guides in three or four developing countries. The second was the organiza-tion of conferences and seminars in a few selected countries.

25

The organization of conferences was to become the most important activity for PASduring its early years. At this time, other international development institutions also wereinvolved in organizing conferences. PAS sought to make the conferences it sponsored morefocused and effective by concentrating on identifying recent important changes in a hostcountry’s investment environment, discussing the need for additional changes as seen byprospective investors and expert observers, and by adding a sectoral focus to these confer-ences. PAS sponsored four such conferences between 1989 and 1993: in Ghana (February1990), Hungary (September 1990), Jamaica (February 1991), and Pakistan (November 1991).

The other principal vehicle for providing technical assistance during this early periodwas the Executive Development Program. These programs were in the form of short (two- tofour-day) training programs designed to help entrepreneurs and relevant policy makers indeveloping member countries, particularly those without significant experience in operatingin a market economy, develop skills in negotiating with foreign investors. Four such execu-tive development programs were held between 1989 and 1993: in Portugal, for five Portuguese-speaking African countries (September 1991); Hungary (September 1991); Czechoslovakia(October 1991); and Angola (April 1992).

While the investment promotion conferences and the executive development pro-grams were the principal mechanisms used in the transfer of MIGA’s technical assistance,PAS also coordinated one outward investment mission, one investment roundtable, and oneresearch study during the 1989 to 1993 period.

In sum, these 11 discrete promotional activities benefited 20 of MIGA’s developingmember countries. However, PAS had difficulty in providing technical assistance to moremember countries because of budgetary constraints. MIGA’s Convention provided nodedicated source of funding for its technical assistance activities.

This early period of MIGA’s technical assistance activities concluded with changesin MIGA’s focus. The first change was a reorientation in PAS’s technical assistance activity.This change initially was presented to the MIGA Board in January 1993. At this time, theMIGA Board was divided on MIGA’s technical assistance role. Board members from severalindustrial countries were of the opinion that MIGA should discontinue its technical assis-tance activities; board members from several developing countries were of the view that theentire technical assistance function should be handled through the FIAS joint venture.

It was in this context that a major reorientation of MIGA’s technical assistanceactivities was proposed. Henceforth, MIGA’s technical assistance arm would focus sharplyon three areas mandated in its Convention: Assistance in the actual execution of investmentpromotion, participation in the dissemination of information on investment opportunities,and assistance in capacity-building of investment promotion agencies to ensure their long-term viability.

TECHNICAL ASSISTANCE ACTIVITIES

MIGA: THE FIRST TEN YEARS26

This change in focus was endorsed in an independent evaluation of MIGA’s technicalassistance function, which was commissioned by MIGA’s executive vice president in February1993; and the report, which was presented to the MIGA Board in May 1993. This evaluationconcluded that PAS had operated with severe budgetary constraints and that it had not yetbeen successful in making its investment promotion conferences significantly more effectivethan the typical investment promotion conference sponsored by international organizations.The review also pointed out that MIGA’s focus was not adequately placed on the develop-ment of the capabilities of investment promotion agencies, and that PAS’s relationship withFIAS was not as complementary as was befitting the relationship between two related unitsof the World Bank Group.

Against this backdrop, the evaluation endorsed the new orientation developed byPAS management, which included more sharply focused technical assistance services thatwould be clearly distinguished from the policy services offered by FIAS. While the evalua-tion supported this distinction, it also recommended closer working relations between FIASand PAS, including the possibility of a merger. The review also proposed that PAS be pro-vided with additional resources, and be encouraged to extend its services to more membercountries.

It was with respect to the linkages between PAS and FIAS that MIGA managementproposed a second important change, which occurred in November 1993, when the man-agement of MIGA proposed that MIGA should discontinue its support for FIAS. (Until thatpoint, MIGA had been making an annual contribution of $400,000 to FIAS’s operatingbudget.)

Management’s proposal was accepted by the Board and MIGA officially withdrewits financial support and oversight of FIAS in June 1994. (By then, FIAS had secured finan-cial support from the IBRD, so it still retained its joint venture status.) This decision wastaken by the Board only after much debate as to whether the more appropriate responsemight not be (as advocated by the evaluators in 1993) the merger of PAS and FIAS. Indeed,a proposal for a merger of FIAS and PAS was considered by the MIGA Board. The eventualacceptance of the proposal for withdrawal and the maintenance of a separate technical assis-tance function by PAS was based, in large part, on the view that the MIGA Conventionmandated that it carry out a specialized and distinct technical assistance function.

Executing the Technical Assistance Function:1994 to 1998

MIGA’s technical assistance function in this period focused initially on implement-ing the change in orientation recommended by MIGA management and endorsed in the1993 review. This change sought to identify both the areas in which PAS would not beinvolved, and those in which it would seek to develop a distinctive service competence. Withrespect to the first, MIGA’s decision to discontinue its ownership relationship with FIASmade it even more important for there to be a clear separation in activity between MIGA

27

and FIAS. This separation was not meant to jeopardize, but rather to support, increasedcooperation with other units of the World Bank Group, which was not only desirable, butwas also a clear directive of the MIGA Convention.

Immediately after the change in this relationship, in June 1994, the name of MIGA’stechnical assistance unit was changed from Policy Advisory Services, to Investment Market-ing Services (IMS). The new name, proposed by the executive vice president, was meant tomake it clear that technical assistance to countries in the area of foreign investment attrac-tion was not policy advice. (This, after all, was what was suggested by the existing nameof Policy Advisory Services.) Rather, the new name was meant to indicate that the technicalassistance to be provided by MIGA was to be in the actual marketing and promotion ofcountries as sites for foreign investment.

The focus of the newly formed IMS was implementing the new technical assistanceorientation by both developing innovative services and expanding the scope of service cover-age to as many developing countries as possible. This expansion in the scope of services wasin recognition of MIGA’s role as a full-fledged multilateral institution with a responsibilityto provide benefits to as many members as possible.

The limited service coverage of those early years had aroused concern among severalMIGA Board members, particularly those from several developing countries that were notsignificant recipients of FDI inflows. These countries argued that circumstances did not allowthem to benefit from MIGA’s guarantee activities because of the paucity of foreign invest-ments. Consequently, in the short term, the only mechanism through which these countrieswould be able to benefit from their MIGA membership was through technical assistanceservices. Every effort, therefore, was to be made to ensure the widest possible coverage oftechnical assistance services. In addition, the 1993 review also had recommended an expan-sion in service coverage.

These dual goals affected the manner in which IMS’s technical services were devel-oped. Recall that the reorientation proposed three types of technical assistance:

♦ Direct investment promotion support♦ Dissemination of information on investment opportunities and business operating

conditions♦ Capacity-building activities for institutions involved in investment promotion.

Direct Investment Promotion Support

Direct investment promotion support was accomplished primarily through themechanism of investment promotion conferences. Such conferences had been the principalform in which promotional assistance was provided during the early period of MIGA’s tech-nical assistance function. During the 1994 to 1998 period, however, IMS reoriented theseconferences in keeping with its dual objectives: That is, it tried simultaneously to make the

TECHNICAL ASSISTANCE ACTIVITIES

MIGA: THE FIRST TEN YEARS28

conferences effective vehicles for promoting investment, and of value to as many of its mem-ber countries as possible. In so doing, it developed the model of single-sector, multi-countryconferences. This new approach stood in contrast to the single-country, multi-sector confer-ences that predominated in the earlier period of MIGA’s history.

It was believed that single-sector conferences were more appropriate vehicles forattracting investment because a sector-specific conference was more likely to attract invest-ment decision-makers than would a conference with a general focus. Multi-country confer-ences also allowed more MIGA members, prospectively, to benefit from a single event. Therewas also the view that in certain sectors, multi-country conferences attract serious investorsbecause they provide a forum in which multiple investment opportunities can be simulta-neously evaluated.

The two sectors in which most of these conferences occurred were mining andtourism. These sectors were chosen, in part, because of the availability of the requisite exper-tise, but they were also chosen because they were believed to best lend themselves to thesingle-sector, multi-country approach to conference organization. IMS organized four con-ferences on mining investments in Africa and four tourism conferences between late 1993and 1997.

In 1998, IMS expanded its mining conferences beyond Africa. It organized the first“Global Mining Investment Opportunities Symposium” in conjunction with the 100th anni-versary of the Canadian Institute of Mining in May 1998; and a symposium, “Mining Invest-ment and Business Opportunities in Central Asian, the Balkan and Caucasus Countries” in June1998, in collaboration with the OECD.

In another effort to improve the effectiveness of its conferences, IMS sought tomake conferences one element of a larger promotional process that also included a prepara-tory stage and follow-up activity. This shift was driven by the belief that in the absence ofdetailed preconference preparation, including careful prospecting for appropriate attendeesand studious preparation of information to be released, and without thorough postconferencefollow-up activities, promotional conferences had little chance of influencing investmentflows.

It was in this context that IMS initiated preconference workshops and postconferencemissions. The workshops were designed to train government officials in project presentation,negotiation of investments, and identification of the appropriate enabling environment forinvestment. The postconference missions, particularly sectorally focused missions, allowedcountry representatives to meet with international investors. It was in the spirit of providinga full package of services that IMS organized 15 promotional conferences (inclusive of the10 in mining and tourism), 9 outward investment missions, and 14 workshops and trainingprograms in tourism and mining between fiscal 1994 and fiscal 1998.

29

Dissemination of Information

Another type of IMS was assistance with the dissemination of information aboutpromotional opportunities, potential investors, and investment projects. The principal mecha-nism used by IMS to achieve its information dissemination mandate has been the develop-ment of an internet-based Investment Promotion Network (IPAnet). The idea of launchingan electronic network of information on investment promotion activities and investmentpromotion opportunities was conceived by MIGA in 1993.

IPAnet was introduced in September 1993 and officially launched in October 1995.IPAnet fit neatly into the reoriented technical assistance program because it was innovativeand could benefit almost all MIGA members. In addition, it was highly congruent withMIGA’s mandate to disseminate information on investment opportunities.

Designed as a clearinghouse for investment-related information, IPAnet containeddatabases, directories, and targeted communications. By the end of fiscal 1998, it boastedmore than 8,000 users from 170 countries, and its databases could classify and provide accessto more than 8,000 documents from more than 300 sources, covering information in excessof 160 countries. In April 1998, IPAnet was selected by the London Financial Times as Websiteof the Week.

In addition to information dissemination through IPAnet, IMS also has engaged inother efforts to distribute information on investment opportunities and the activities of in-vestment promotion agencies. For example, IMS sponsored the development of a CD-ROMon opportunities in the mining sectors of African countries.

IMS also assisted in the establishment of the World Association of Investment Pro-motion Agencies (WAIPA) and the Association of African Investment Promotion Agencies(AFRIPA) to facilitate information sharing and collaboration among investment promotionagencies. Also in Africa, IMS sponsored the publication and distribution of a regional invest-ment promotion newsletter, Locate Africa, and assisted in organizing roundtables amongAfrican investment promotion agencies (IPAs). In fiscal 1998, IMS extended the geographi-cal reach of its roundtable series, organizing the “First Annual Meeting of Chief Executivesfrom Eurasian IPAs.”

In May 1998, a new information dissemination service was launched, Privatization-Link, which could be accessed through a specialized window in IPAnet. PrivatizationLinkwas set up to carry profiles of state-owned enterprises being privatized, background infor-mation on privatization agencies, and laws related to privatization activities. By the end offiscal 1998, PrivatizationLink contained about 100 company profiles from 25 countries.

TECHNICAL ASSISTANCE ACTIVITIES

MIGA: THE FIRST TEN YEARS30

Capacity Building Activities

The third aspect of IMS activities has been in the area of building the capacity ofIPAs so that they themselves can engage in effective promotion. These institutional capacity-building activities fall into three main categories: training programs in investment promotion;installation of specialized management information systems and training in their use; and aprogram of field-based, ongoing assistance.

The training program includes a skill training module, promotion strategy, investorservice and capacity building workshops, and seminars focused on training embassy officialsin investment promotion. In the context of its training efforts, between fiscal 1994 and fiscal1998, IMS conducted 8 promotion strategy workshops; 34 capacity building, promotionstrategy; and skill-training workshops; and 4 embassy seminars.

One of the most important elements of IMS’s capacity-building activities has beenin development of specialized management information systems and the installation of thesesystems, with appropriate training, in IPAs. The IMS Department’s signature MiS system wasdeveloped jointly by MIGA and FIAS.

The MiS system originally included two modules: The first was the Investor TrackingSystem (ITS), which is a tool for tracking, managing, and reporting on relations with inves-tors from point of first contact to measurement of the impact of the investment project.It includes contact management, work management, investment analysis, and reportingfeatures. The second module, as originally conceived, was the Business Operating Conditions(BOC) module, a hypertext database tool that allows for easy development of an electronicrepository of information on business operating conditions in select countries. The BOC’sutility has been eclipsed by the development of the Internet’s World Wide Web and othermultimedia applications. Accordingly, IMS began offering the ITS as a stand-alone MiSapplication.

By 1997, IMS had installed its MiS package in six countries: Ghana, Malawi,Venezuela, South Africa, Uganda, and Zimbabwe. These installations were accompanied by11 needs assessments and training programs. The system is usually installed in an agency overa 12- to 18-month period. A full package of technical assistance associated with an installa-tion would include a feasibility assessment, an investment promotion skills training module,system installation/configuration, system administrator training, end-user training, a usageaudit, system customization, manager training, and a final usage audit.

The final element of capacity building has been the provision of ongoing field-basedassistance. In one such arrangement, an IMS staff member was seconded to the Governmentof Namibia to engage in investment promotion efforts on behalf of Namibia and other southernAfrican states. This arrangement was specially funded by the Swedish Government.

In 1998, a more comprehensive program of field-based assistance for African coun-tries was initiated, with funding provided by the Government of Japan, based largely on

31

arrangements negotiated by MIGA’s then-executive vice president. This program of supportfor African promotion agencies (AFRI-IPA Support Program) was managed by the seniorIMS staff member who had been seconded to the Government of Namibia. It was initiatedas a three-year pilot program of field-based assistance in southern Africa, West/CentralAfrica, and East Africa. By the end of fiscal 1998, the AFRI-IPA Support Program had orga-nized an investment mission and three regional workshops on foreign investment promotionin Africa.

In concert with efforts to reorient its technical assistance program, in its second fiveyears of existence MIGA’s technical assistance arm sought to satisfy other elements of MIGA’stechnical assistance mandate, especially the organizational coordination element of this man-date. Recall, for example, that Article 23(a) subsection (iii) of its Convention stipulates thatMIGA’s technical assistance function should be coordinated “with other agencies concernedwith the promotion of foreign investment, and in particular the International FinanceCorporation.”

Inter and Intra-Organizational Relationshipsin Technical Assistance