First Alpha Energy Fund LP - spe-london.org · Oil Price (WTI, $/bbl) Oil rigs. Monthly prodn/rig...

27

SPE London Introduction to E&P 21 st November 2017 13 th Annual Seminar Global Context Miles Cudmore First Alpha Energy Capital LLP

Transcript of First Alpha Energy Fund LP - spe-london.org · Oil Price (WTI, $/bbl) Oil rigs. Monthly prodn/rig...

SPE London Introduction to E&P 21st November 201713th Annual Seminar

Global Context

Miles Cudmore

First Alpha Energy Capital LLP

Global Context

Industry structure• what is E&P, who is involved

Global energy trends• demand and supply by energy source• oil and gas resources and production• what is happening today

Key challenges• renewing exploration in the UK North Sea• making unconventionals work in the UK• resetting project delivery• improving UK operational performance

November 2017 2

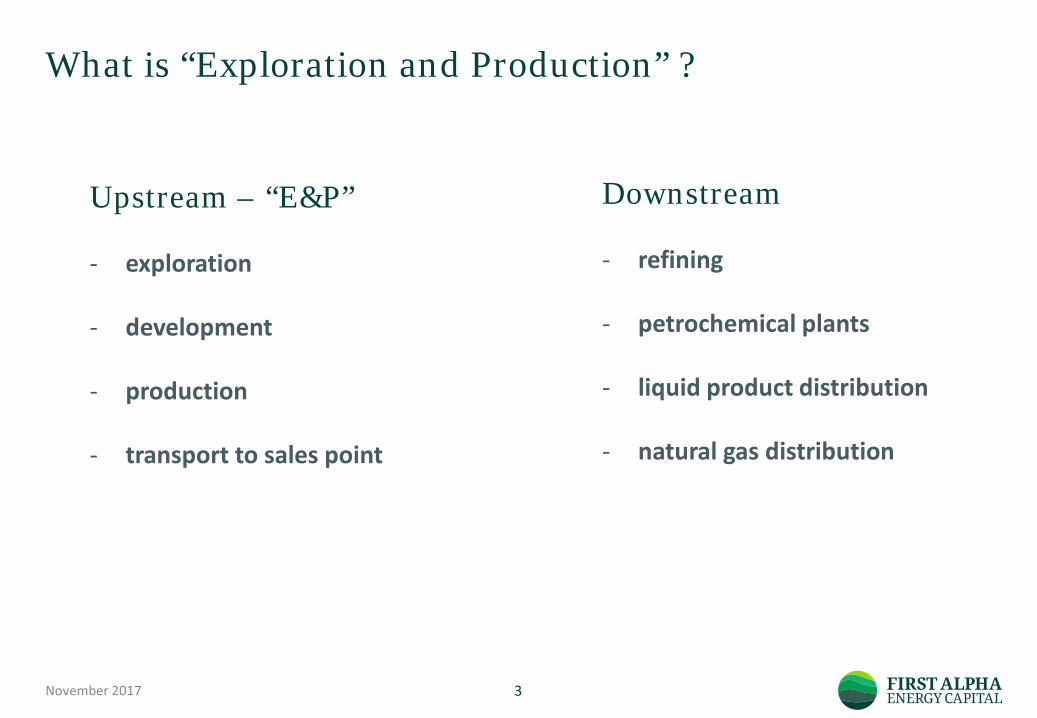

What is “Exploration and Production” ?

November 2017 3

Upstream – “E&P”

- exploration

- development

- production

- transport to sales point

Downstream

- refining

- petrochemical plants

- liquid product distribution

- natural gas distribution

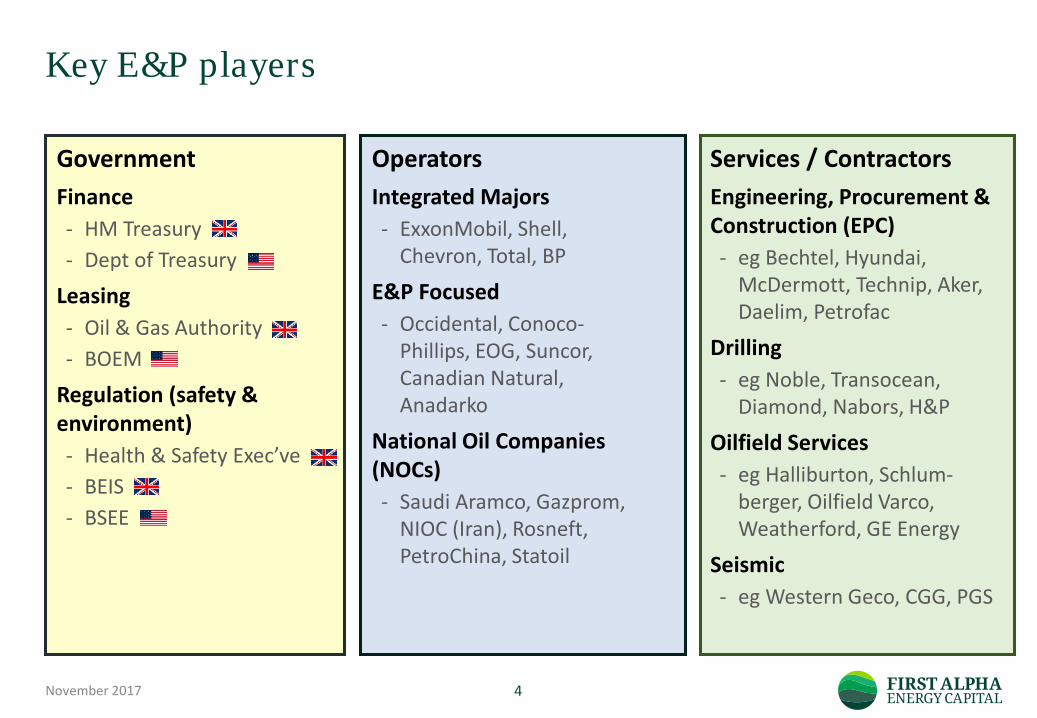

Key E&P players

November 2017 4

GovernmentFinance - HM Treasury- Dept of Treasury

Leasing - Oil & Gas Authority- BOEM

Regulation (safety & environment)- Health & Safety Exec’ve- BEIS- BSEE

OperatorsIntegrated Majors- ExxonMobil, Shell,

Chevron, Total, BP

E&P Focused- Occidental, Conoco-

Phillips, EOG, Suncor, Canadian Natural, Anadarko

National Oil Companies (NOCs)- Saudi Aramco, Gazprom,

NIOC (Iran), Rosneft, PetroChina, Statoil

Services / ContractorsEngineering, Procurement & Construction (EPC)- eg Bechtel, Hyundai,

McDermott, Technip, Aker, Daelim, Petrofac

Drilling- eg Noble, Transocean,

Diamond, Nabors, H&P

Oilfield Services- eg Halliburton, Schlum-

berger, Oilfield Varco, Weatherford, GE Energy

Seismic- eg Western Geco, CGG, PGS

2014 production, largest 21 companies

November 2017 5

0

2

4

6

8

10

12

14

Mill

ion

Barr

els O

il Eq

uiva

lent

per

day

Oil & liquids Gas

International Oil Companies

Data from Forbes magazine / WoodMackenzie

National Oil Companies

Energy Growth below GDP Growth

November 2017 6

Primary Energy Consumption

November 2017 7

-

1

2

3

4

5

6

7

8

1990 1995 2000 2005 2010 2015

Non OECD Driving Energy Growth• China consumes 23% of global primary

energy use• India at 5% and growing at > 5% pa• Pace of China energy growth has

slowed with reduced GDP growth and falling energy intensity

OECD Energy Demand Flat• Slow GDP growth matched by pace of

falling energy intensity• N America consumption 21% of global

primary energy use, EU 12%

Billion TonnesOil Equivalent

OECD

Non OECD

ChinaN America

EU

Data from BP Statistical Review of World Energy

Energy Sources

November 2017 8

2016 Points• Oil and grew by 1.8% boosted by GDP

growth and price falls• Coal fell 1.4%• Non fossil fuels hit high of 15% share

Macro picture• Renewables are fastest growing source

(16% pa average growth since 2006), but are only 3.8% of total

• Strongest growth in solar, 50% pa growth since 2006 (has slowed, 30% pa 2015 – 16); wind next highest (22% pa since 2006)

• Overall demand for oil and gas set to grow

• Reducing emissions requires coal to gas switch in addition to non fossil growth0%

10%

20%

30%

40%

50%

1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

Oil

Coal

Gas

Hydro

NuclearRen*

Shares of global primary energy

Data from BP Statistical Review of World Energy 2017

* Renewables plus biofuels

Oil and Gas Production

November 2017 9

0%

20%

40%

60%

80%

100%

0

10

20

30

40

50

60

70

80

90

100

1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

N America S & C AmericaEurope & Eurasia Mid EastAfrica Asia Pacific% Opec % OECD

0%

20%

40%

60%

80%

100%

0

1000

2000

3000

4000

5000

1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

N America S & C AmericaEurope & Eurasia Mid EastAfrica Asia Pacific% OECD

Million bpd Oil Production Billion Cubic Meters pa Gas Production(scaled to oil graph by equivalent energy)

Data from BP Statistical Review of World Energy

Oil and Gas Proved Reserves

November 2017 10

Thousand Million bbl Trillion Cubic Meters (scaled to oil graph by equivalent energy)

0%

20%

40%

60%

80%

100%

0

200

400

600

800

1000

1200

1400

1600

1800

1980 1985 1990 1995 2000 2005 2010 2015

N America S & C AmericaEurope & Eurasia Mid EastAfrica Asia Pacific% OPEC % OECD

0%

20%

40%

60%

80%

100%

0

30

60

90

120

150

180

210

240

270

1980 1985 1990 1995 2000 2005 2010 2015

N America S & C AmericaEurope & Eurasia Mid EastAfrica Asia Pacific% OECD

Data from BP Statistical Review of World Energy

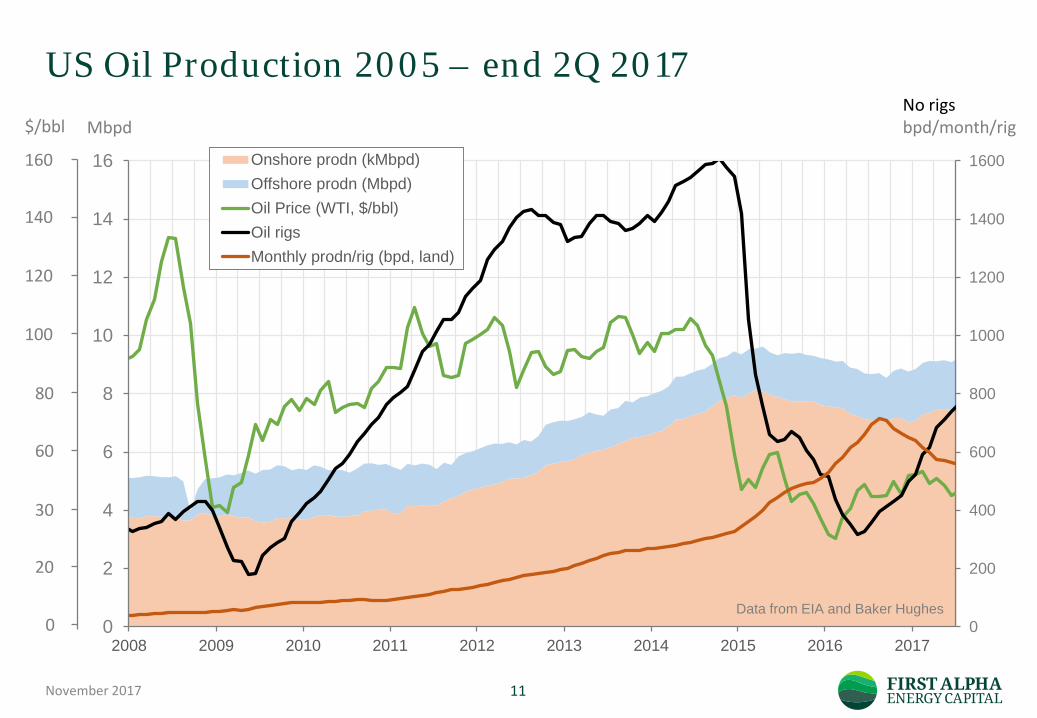

US Oil Production 2005 – end 2Q 2017

November 2017 11

$/bbl

160

140

120

100

80

20

30

60

0 0

200

400

600

800

1000

1200

1400

1600

0

2

4

6

8

10

12

14

16

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Onshore prodn (kMbpd)Offshore prodn (Mbpd)Oil Price (WTI, $/bbl)Oil rigsMonthly prodn/rig (bpd, land)

MbpdNo rigsbpd/month/rig

Data from EIA and Baker Hughes

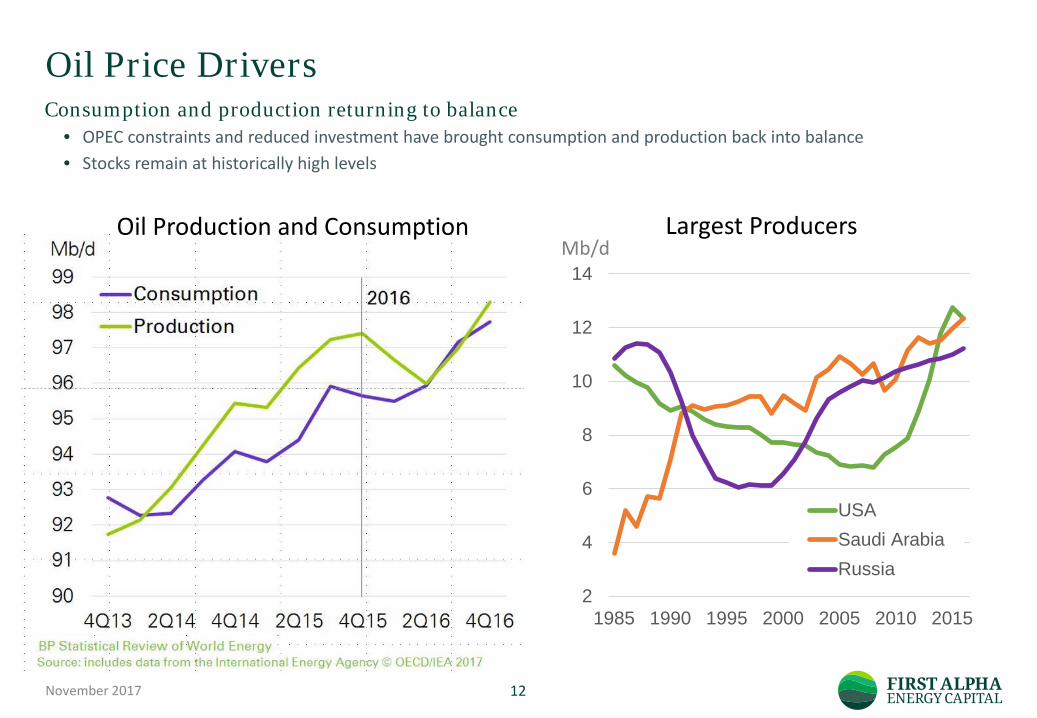

Oil Price Drivers

November 2017 12

2

4

6

8

10

12

14

1985 1990 1995 2000 2005 2010 2015

USASaudi ArabiaRussia

Mb/dLargest ProducersOil Production and Consumption

Consumption and production returning to balance• OPEC constraints and reduced investment have brought consumption and production back into balance• Stocks remain at historically high levels

Gas Market – recent trends

November 2017 13

0

2

4

6

8

10

12

14

16

18

2000 2002 2004 2006 2008 2010 2012 2014 2016

US Henry HubUK NBPAverage German import cifJapan cif

0

50

100

150

200

250

300

350

400

450

2000 2002 2004 2006 2008 2010 2012 2014 2016

AntrimBakkenWoodfordBarnettFayettevilleEagle FordHaynesvilleMarcellusUticaRest of US

US Shale Production – 50% world gas growth

Data from EIA

Gas Prices ($/million btu)bcm pa

Data from BP Statistical Review of World Energy

Global gas outlook

November 2017 14

0

20

40

60

80

100

120

1990 2000 2010 2020 2030 2040

OE

non-OECD

EIA World natural gas consumption Forecastquadrillion Btu bcf/d

Global LNG capacity additions, 2015 - 2019

Gas consumption expected to grow strongly. Over next 5 years, spot price weakness likely as new LNG capacity comes on line and US starts exports

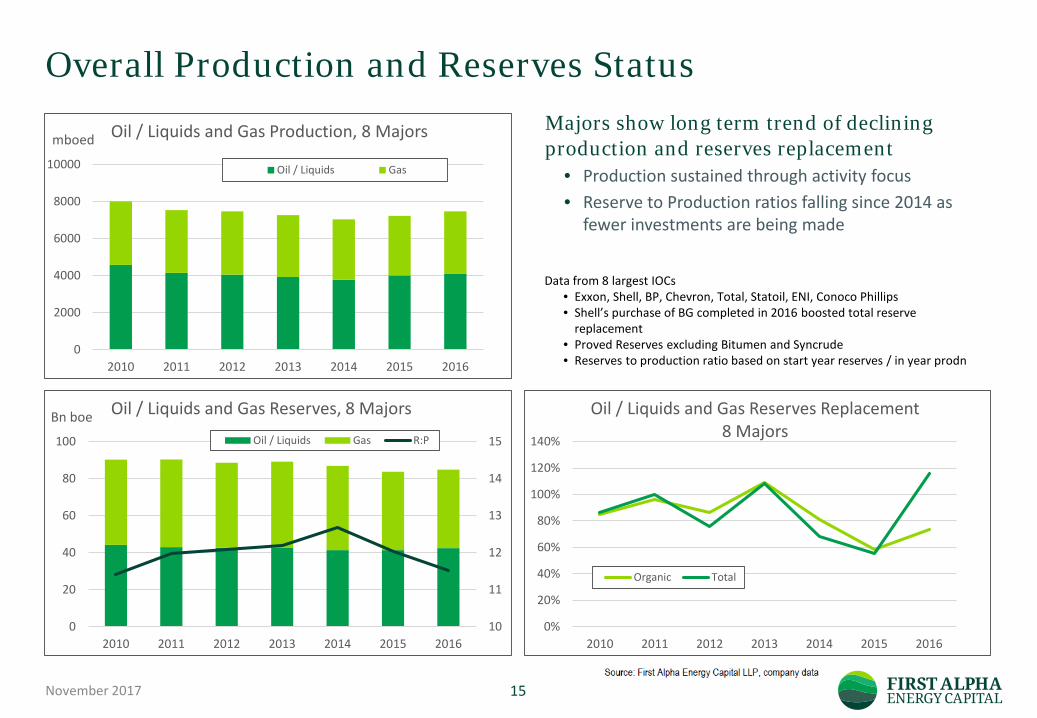

Overall Production and Reserves Status

November 2017 15

0

2000

4000

6000

8000

10000

2010 2011 2012 2013 2014 2015 2016

Oil / Liquids and Gas Production, 8 Majors

Oil / Liquids Gas

mboed

Data from 8 largest IOCs• Exxon, Shell, BP, Chevron, Total, Statoil, ENI, Conoco Phillips• Shell’s purchase of BG completed in 2016 boosted total reserve

replacement• Proved Reserves excluding Bitumen and Syncrude• Reserves to production ratio based on start year reserves / in year prodn

10

11

12

13

14

15

0

20

40

60

80

100

2010 2011 2012 2013 2014 2015 2016

Oil / Liquids and Gas Reserves, 8 Majors

Oil / Liquids Gas R:P

Bn boe

0%

20%

40%

60%

80%

100%

120%

140%

2010 2011 2012 2013 2014 2015 2016

Oil / Liquids and Gas Reserves Replacement8 Majors

Organic Total

Majors show long term trend of declining production and reserves replacement

• Production sustained through activity focus• Reserve to Production ratios falling since 2014 as

fewer investments are being made

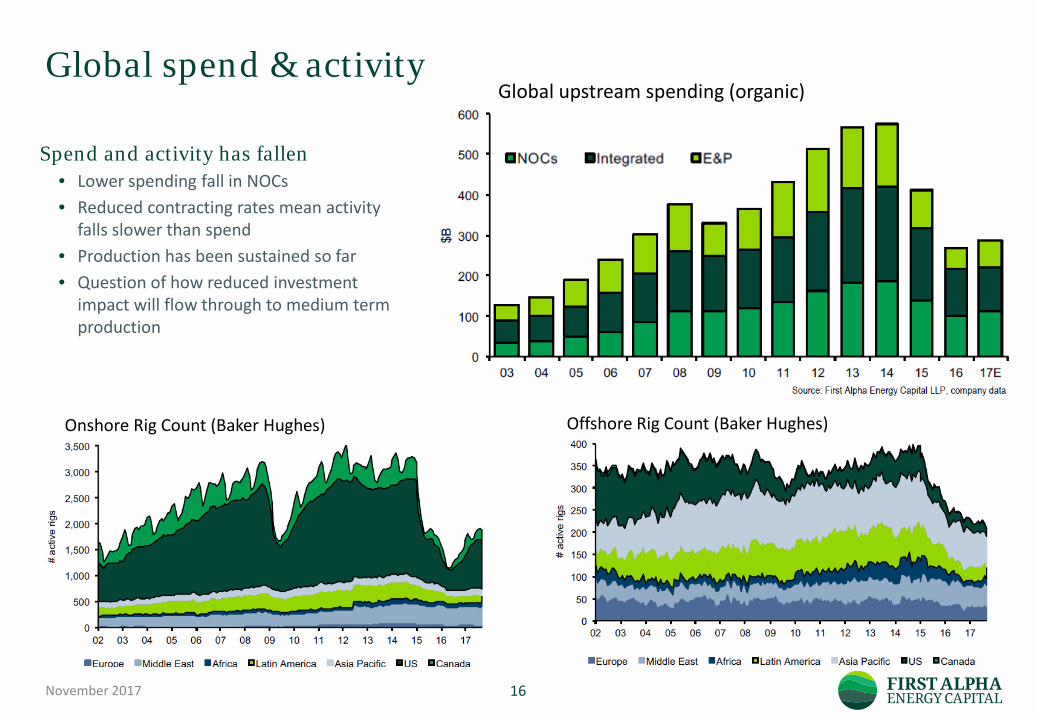

Global spend & activity

November 2017 16

Global upstream spending (organic)

Onshore Rig Count (Baker Hughes) Offshore Rig Count (Baker Hughes)

Spend and activity has fallen• Lower spending fall in NOCs• Reduced contracting rates mean activity

falls slower than spend• Production has been sustained so far• Question of how reduced investment

impact will flow through to medium term production

E&P Major Project Delivery (global)

November 2017 17

“Average”E&P

“Average” non E&P

70% of E&P developments delivered less value than planned; average loss of 35%

• average of 78% planned production delivered in first 4 years

• average cost overrun of 20% in real terms

In order of importance due to:-• scoping decisions based on incomplete reservoir

data • capital cost growth (supply chain / integration)• prioritising schedule over value

E&P Mega Project outcomes vs plan are also poorer than other sectors and E&P capital productivity has fallen

• Front End Loading (FEL) in E&P projects at “middle fair” level on average vs “upper good” for non E&P projects

• circa 60% of E&P projects are schedule driven than non E&P vs circa 30% of non E&P Projects

Majors need to materially improve project performance to remain competitive and replace reserves

Analysis: IPA

Cost Growth vs Front End Loading

Global Picture – key points

Oil and gas demand will continue to grow but at slower pace than GDP• falling energy intensity per unit GDP• continued growth in renewables, particularly for power

Remaining oil and gas reserves continue to grow, more is being found than produced• no shortage of resources globally, shale technology adding new volumes• value driven by portfolio and development efficiency• question is using resources in efficient and sustainable way

US shale production driving changes in both oil and gas• 2015 was first time a country has added 1 million bpd capacity for 3 years in a row• circa half of new global gas supply from US shale, becoming exporter• Shale creates new dynamic; elasticity of supply constraining prices

Industry facing big challenges and changes• material new technology driven supplies at time of slowing energy demand growth• lower prices and volatility possibly a “return to normal” • high cost / high tax areas are severely challenged• no room for poor project or operating performance

November 2017 18

Stages of Field Life

November 2017 19

Explore Appraise ProduceDevelop Abandon

“Access acreage, find new

resources”

“De-risk to enable project

launch”

“Develop fields, create new

hubs”

“Safely produce,add reserves,

maximise efficiency”

“Removefacilities, restore

environment”

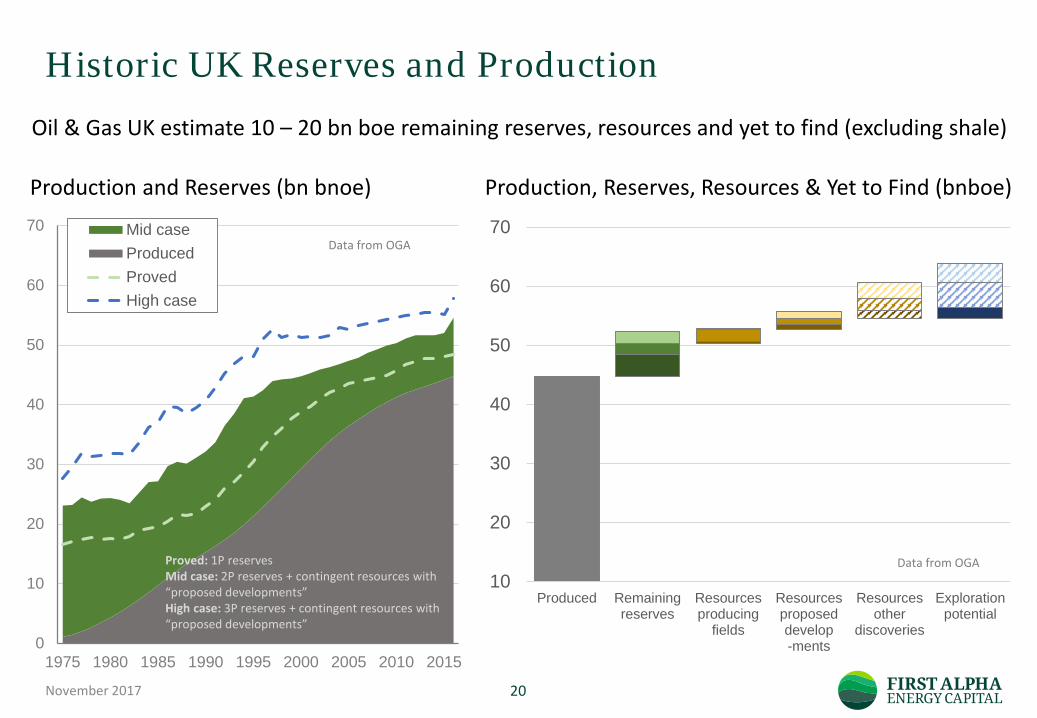

Historic UK Reserves and Production

November 2017 20

0

10

20

30

40

50

60

70

1975 1980 1985 1990 1995 2000 2005 2010 2015

Mid caseProducedProvedHigh case

10

20

30

40

50

60

70

Produced Remainingreserves

Resourcesproducing

fields

Resourcesproposeddevelop-ments

Resourcesother

discoveries

Explorationpotential

Production and Reserves (bn bnoe) Production, Reserves, Resources & Yet to Find (bnboe)

Oil & Gas UK estimate 10 – 20 bn boe remaining reserves, resources and yet to find (excluding shale)

Proved: 1P reservesMid case: 2P reserves + contingent resources with “proposed developments”High case: 3P reserves + contingent resources with “proposed developments”

Data from OGA

Data from OGA

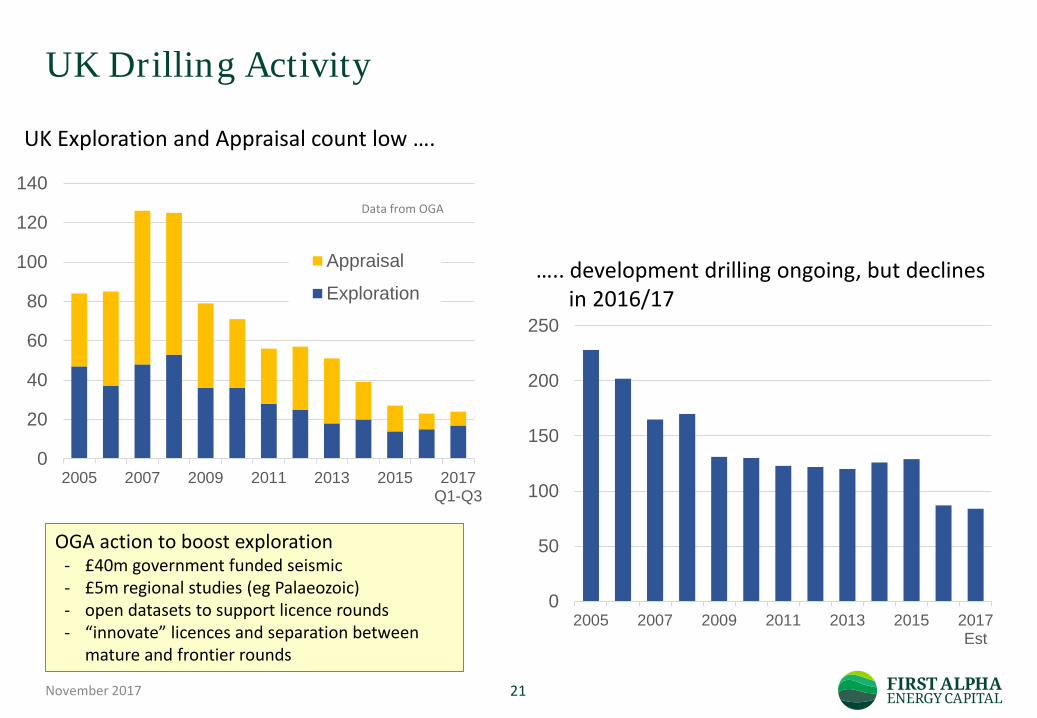

UK Drilling Activity

November 2017 21

0

20

40

60

80

100

120

140

2005 2007 2009 2011 2013 2015 2017Q1-Q3

Appraisal

Exploration

Data from OGA

….. development drilling ongoing, but declinesin 2016/17

UK Exploration and Appraisal count low ….

OGA action to boost exploration- £40m government funded seismic- £5m regional studies (eg Palaeozoic)- open datasets to support licence rounds- “innovate” licences and separation between

mature and frontier rounds

0

50

100

150

200

250

2005 2007 2009 2011 2013 2015 2017Est

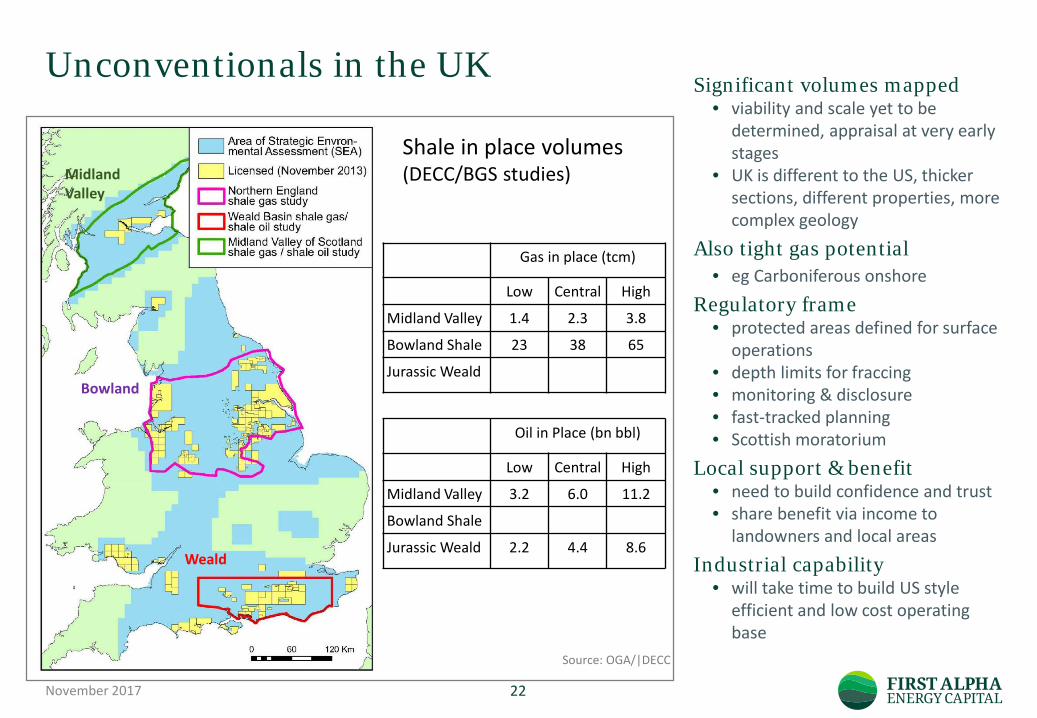

Unconventionals in the UK

November 2017 22

Gas in place (tcm)

Low Central High

Midland Valley 1.4 2.3 3.8

Bowland Shale 23 38 65

Jurassic Weald

Weald

Bowland

MidlandValley

Oil in Place (bn bbl)

Low Central High

Midland Valley 3.2 6.0 11.2

Bowland Shale

Jurassic Weald 2.2 4.4 8.6

Shale in place volumes(DECC/BGS studies)

Source: OGA/|DECC

Significant volumes mapped• viability and scale yet to be

determined, appraisal at very early stages

• UK is different to the US, thicker sections, different properties, more complex geology

Also tight gas potential • eg Carboniferous onshore

Regulatory frame• protected areas defined for surface

operations• depth limits for fraccing• monitoring & disclosure• fast-tracked planning• Scottish moratorium

Local support & benefit • need to build confidence and trust• share benefit via income to

landowners and local areas

Industrial capability• will take time to build US style

efficient and low cost operating base

UKCS Capital Investment

November 2017 23

Declining capital investment as operators seek to manage cash flow; falling unit development costs expected to stimulate activity (eg increased Private Equity fund activity)

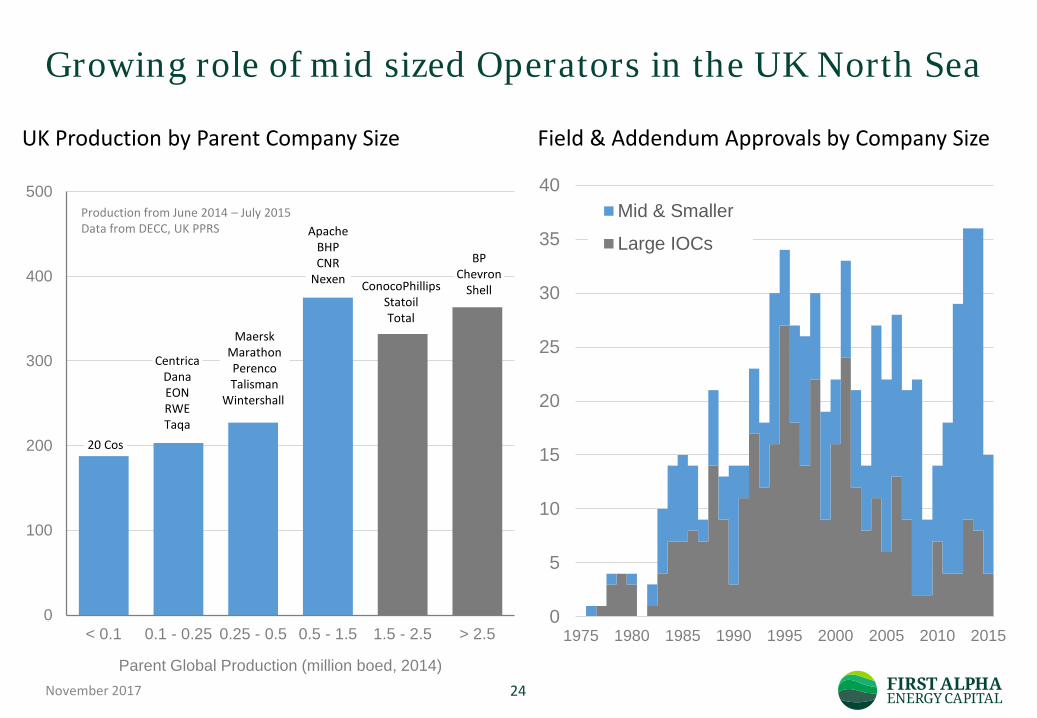

Growing role of mid sized Operators in the UK North Sea

November 2017 24

0

100

200

300

400

500

< 0.1 0.1 - 0.25 0.25 - 0.5 0.5 - 1.5 1.5 - 2.5 > 2.5

Parent Global Production (million boed, 2014)

0

5

10

15

20

25

30

35

40

1975 1980 1985 1990 1995 2000 2005 2010 2015

Mid & Smaller

Large IOCs

Production from June 2014 – July 2015Data from DECC, UK PPRS

ConocoPhillipsStatoilTotal

ApacheBHPCNR

Nexen

MaerskMarathonPerencoTalisman

Wintershall

CentricaDanaEONRWETaqa

20 Cos

BPChevron

Shell

UK Production by Parent Company Size Field & Addendum Approvals by Company Size

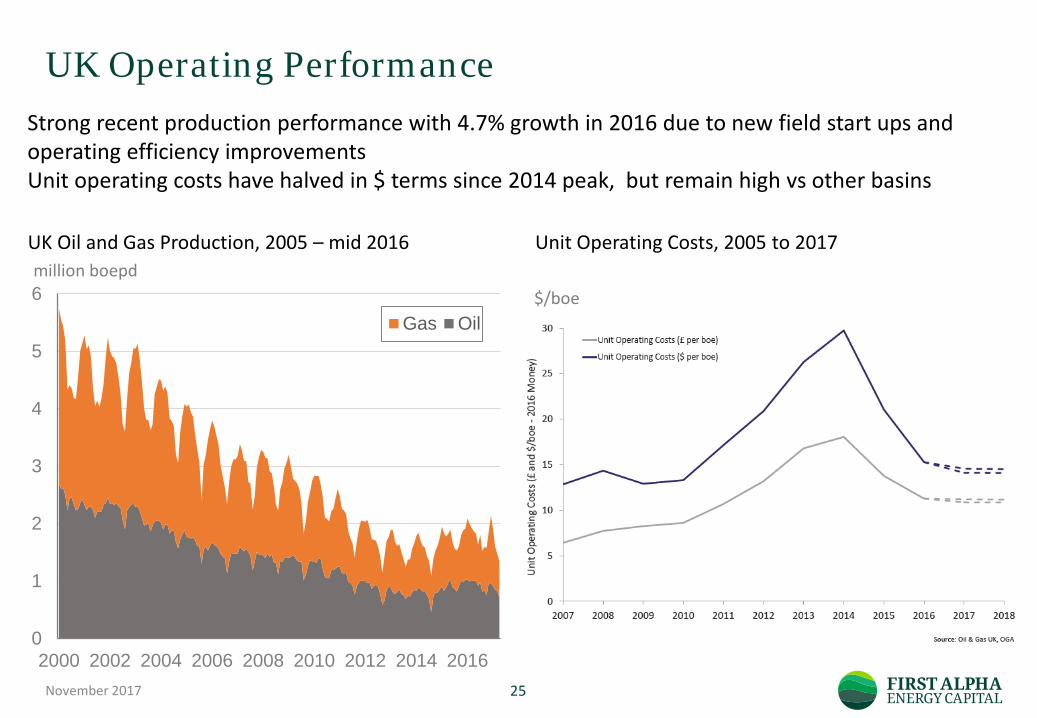

UK Operating Performance

November 2017 25

0

1

2

3

4

5

6

2000 2002 2004 2006 2008 2010 2012 2014 2016

Gas Oil$/boe

Unit Operating Costs, 2005 to 2017UK Oil and Gas Production, 2005 – mid 2016million boepd

Strong recent production performance with 4.7% growth in 2016 due to new field start ups and operating efficiency improvementsUnit operating costs have halved in $ terms since 2014 peak, but remain high vs other basins

UK Decommissioning

November 2017 26

Decommissioning activity growing, 14 fields ceased production in 2016, similar number expected in 2017 with ca 30 to 40 fields expected in 2018 and 2019

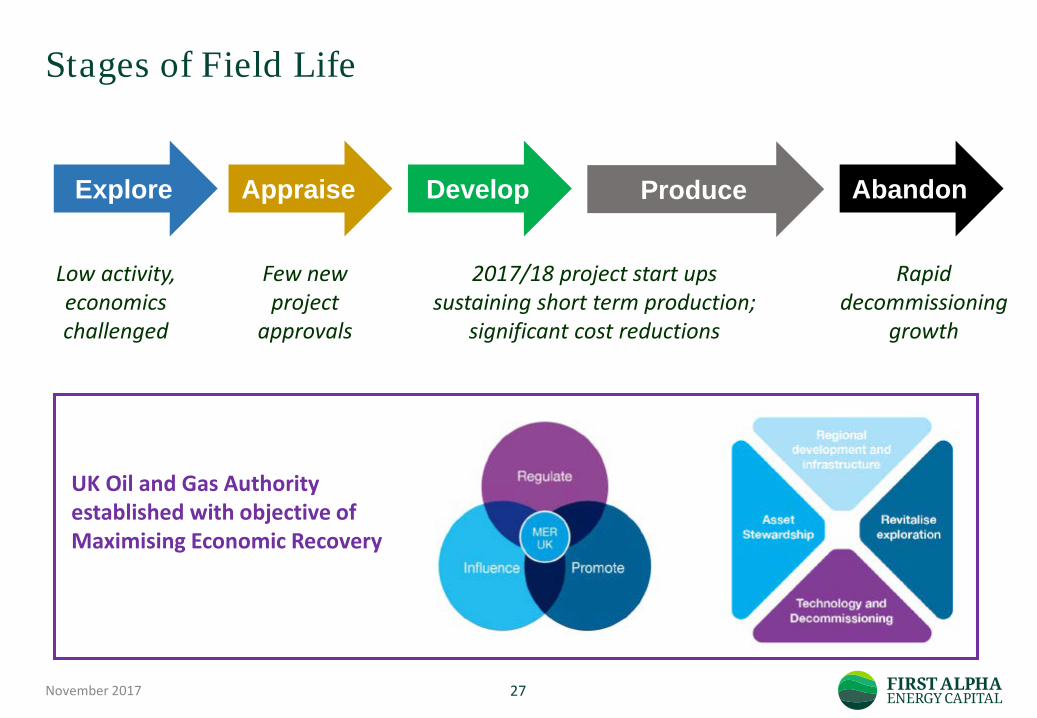

Stages of Field Life

November 2017 27

Explore Appraise ProduceDevelop Abandon

UK Oil and Gas Authority established with objective of Maximising Economic Recovery

Low activity, economics challenged

Few new project

approvals

2017/18 project start ups sustaining short term production;

significant cost reductions

Rapid decommissioning

growth