Fintech Lending Business Model - Microsoft · 2019-11-26 · Fintech Lending in Indonesia will...

22

This presentation document is strictly confidential and solely for the use of PT investree Radhika Jaya and investree (Thailand) Limited. The content have been summarized to suit presentation needs; for actual definitions, descriptions and exclusion, please refer to the corresponding directorate. 2019 | PT investree Radhika Jaya Investree Indonesia’s Leading SME Marketplace Lending November 2019

Transcript of Fintech Lending Business Model - Microsoft · 2019-11-26 · Fintech Lending in Indonesia will...

This presentation document is strictly confidential and solely for the use of

PT investree Radhika Jaya and investree (Thailand) Limited. The content

have been summarized to suit presentation needs; for actual definitions,

descriptions and exclusion, please refer to the corresponding directorate.

2019 | PT investree Radhika Jaya

InvestreeIndonesia’s Leading SME Marketplace

Lending

November 2019

Copyright 2019 | PT Investree Radhika Jaya CONFIDENTIAL

“The needs of having a large

working capital at the beginning is

a big challenge for SMEs engaged

in the content creation industry.

This usually forces smaller

companies to forego big business

opportunities. Luckily, I met

Investree which was able to help

me conquer this challenge”

The USD 0.4 mio funding amount

from Investree helped Iman double

sales to USD 1.5 mio in 2018 and

further fuelled the company’s

growth.Iman SyafeiFounder, ReKreasi Creative

Playground

(Marketing and Advertising Agency

founded in 2014)

Impact Story

2

Copyright 2019 | PT Investree Radhika Jaya CONFIDENTIAL

TOTAL

POPULATIONINTERNET

USERS

268.2Million

150.2Million

URBANISATION

56%PENETRATION

56%

E-COMMERCE

CONSUMERS

107Million

YoY CHANGE

5.9%

MOBILE

CONNECTIONS

355.5Million

% OF POPULATION

133%

BANK AC

PENETRATIONCREDIT CARD

PENETRATION

49%PENETRATION

2.4%PENETRATION

MOBILE MONEY

ACCOUNT

MSMEs ACCESS

TO CREDIT

3.1%PERCENTAGE

Indonesia is likely to be less impacted by the possible US-China trade

war due to its lower global value chain participation and linkages with

China. Also, Indonesia’s credit cycle is in a recovery phase while most

economies have a slowing phase of the credit cycle. – AMRO Asia

OPPORTUNITIES FINANCIAL INCLUSION

Global Perspective

26%RATIO

Indonesia - Largest economy in South East AsiaBlooming into a Digital Economy Era

Source:: Digital 2019 Indonesia, World Bank, AMRO

3

Copyright 2019 | PT Investree Radhika Jaya CONFIDENTIAL

2,563

22,665

54,714

259,635

4,359,448

12,832,271

Fintech Lending GrowthIn Indonesia

Fintech Lending

Start-up

Registered and Supervised

by OJK

127 Fintech Lending Players supervised

by Indonesia Financial Authority (OJK)

Dec-

17

Dec-

18Aug-19

Dec-

17Dec-

18Aug-19 Dec-17 Dec-18 Aug-19

Source: OJK – Aug 2019

100,940

207,506

530,385

Lender

Accounts

Borrower

AccountsLoans Distributed

(IDR Million)

Registere

d

114

Licensed

13

Conventional

119

Shariah

8

Total

127

Copyright 2019 | PT Investree Radhika Jaya CONFIDENTIAL

Lender & BorrowerCharacteristics

Source: OJK – Aug 2019

Copyright 2019 | PT Investree Radhika Jaya CONFIDENTIAL

What problems are we solving? Serving the Underserved $165.8 bio Credit Gap

Source: SME Finance Forum (Managed by IFC), The Edge Singapore – “Addressing Indonesia’s Financial

Inclusion Gap”, Bank Indonesia

Financial

Knowledge

High Bank Costs

Less Focus

Despite

Regulatory

Enforcement

High Growth

of Corporate

Sector

Lack of

Robust

Credit

Scoring

High customer

acquisition and

servicing costs in rural

areas as traditional

banks do not leverage

technology $165.8

Billion

MSME Credit

Gap in

Indonesia

Many MSMEs lack the financial

knowledge to comply with the procedures

and requirements set by conventional banks

Unbankable

60 million MSMEs in

Indonesia are

considered high risk

and “unbankable”, with

no collateral and no

credit history

Lack of robust credit scoring system,

with the credit assessment process

being labor intensive

Bank of Indonesia

Regulation No.

17/12/PBI/2015 enforces

a minimum credit portion

served to MSMEs by

banks, however only 60%

of banks reached the

minimum of 15% (2017)

Many large banks focus

more on corporate

sector, evident in the

higher growth of

corporate vs MSME

6

Copyright 2019 | PT Investree Radhika Jaya CONFIDENTIAL

Business

Segment

Consumer

Segment

Corporate

(> USD 14.2

mio sales per

year)

Commercial (USD

3.5 - 14.2

mio sales per year)

Upper income

(> USD 4.3k per

year)

Medium

(USD 0.2 - 3.5 mio

sales per year)

Mass affluent

income

(USD 2.6 –

4.3k per year)

Mass income

(USD 1.3 – 2.6k

per year)

Lower income

(<USD 1.3k

per year)

Micro SME

< USD 0.02

mio sales

per year

Small

(USD 0.02 – 0.2

mio sales per

year)

• On the business borrower segment

side, SMEs are firms whose

financial requirements are too

large for microfinance, but are too

small to be effectively served by

corporate banking models

• On the consumer borrower

segment, the missing middle

segment falls below the banks

primary target and are seldom not

served by them

• Registered total number of MSME is

60 mio companies mostly

considered Micro.

• SMEs contribute 59% of the

country’s GDP and employ’s 97% of

the country’s total workforce

• SMEs contribution growth on

investment on average/year is 8.5-

10.5%

SMEs – The Missing Middle in IndonesiaThat can empower Small and Medium Entrepreneurs

Source: PwC, OJK, World Bank, Global Findex 2018

Exchange rate: 1 USD = 14,117 RP

P2B

Len

din

g S

pace

Ban

k’s

Pri

mary

Targ

et

Ban

k’s

Prim

ary

Targ

et

7

Copyright 2019 | PT Investree Radhika Jaya CONFIDENTIAL

21 1841,629

5,313

15,797

2016 2017 2018 2019 2020

CAGR

793%

CAG

R

214%

Fintech Lending Market

Fintech Lending in Indonesia will reach USD 15.8 bio of accumulative loan

disbursements in 2020 , representing an increment of USD 14.2 bio from 2018 to

2020

Actual Forecasted

Source: PwC, OJK, World Bank, Global Findex 2018

Exchange rate: 1 USD = 14,117 RP

Accumulative Loan Disbursements (USD mio)

Key Drivers of Fintech Lending Growth

Mobile phone subscription growth is

steady going forward, which supports the

awareness and adoption rate of Fintech

Lending

The increase use cases of Fintech

Lending, as a result of collaborations with

other digital platforms (ie. E-commerce,

ride-haling, logistics) and acceptance from

various customer segments

The development of supportive IT

infrastructure and digital IDs, resulting in

wider coverage and faster KYC processes,

which will produce a steady retention and

adoption ratio

Market OpportunityFintech Lending to reach USD 15.8 bio by 2020

8

Copyright 2019 | PT Investree Radhika Jaya CONFIDENTIAL

Our mission is to use technology and data to make loans more affordable and accessible to SMEs

9

Copyright 2019 | PT Investree Radhika Jaya CONFIDENTIAL

Investree Milestones

10

Copyright 2019 | PT Investree Radhika Jaya CONFIDENTIAL

Loan Application

Platform Fees

Loan evaluation

and selection

Platform Fees

Loan Agreement

Loan Investment

Loan Repayment

Interest Payment

SME Borrower

Private Lenders

Institutional Lenders

Investree Lending

Platform

Revenue Model:

• Market Place Fees: 3-5% of

loan amount paid by

borrower

• Lender Fees: 0.5–2% of

funding amount paid by

institutional lender

Investree is a pure marketplace.

It matches borrowers and

lenders through its platform

and does not fund any loans

itself

Administer Loan Process

Legal Agreements,

repayment and monitoring

Due Dilligence Using

Robust Credit Risk

Analysis

Matching

Borrower

and Lender

2 3

Safety & Security by

Specialized Credit Insurance facility

4

The Business ModelA B2B Marketplace Lending Platform for SMEs

1

11

Copyright 2019 | PT Investree Radhika Jaya CONFIDENTIAL

Suppliers &

Vendors

Borrower Demographics

Institutional Business & Retail Borrowers

Small

ManufacturersResellers Online Merchants

21%

15%

13%12%

12%

9%

5%

4%4%

3%2%

Creative & Media

Food & Food Processing

Trade

Technology

Services

Heavy Industry

Utilities

Logistics & Transportation

Manufacturing

Consultation

Construction

21% Borrowers are from Creative & Media

Industries

The BorrowerFast and Flexible Loans

Source:: Borrower Demographics as on YTD 2019

12

Copyright 2019 | PT Investree Radhika Jaya CONFIDENTIAL

Annual Disbursed Institutional Lending has

increased to approximately 20% since inception

Business Loans, Government Retail Bonds, Money Market

Funds

Institutional Onshore

Lenders

Institutional Offshore

Lenders

Domestic Retail

Lenders

Lender Presence Heat Map Lender Demographics

Age Group 21-30 constitute 57% of retail lenders

Retail Lenders are present across

Indonesia with 84% of them in Java

99% 96%

80% 81%

1% 4%

20% 19%

Dec-16 Dec-17 Dec-18 July-19

Retail Lender Institutional Lender

Excludes

$14.2m (Rp

200 bio)

agreed

financing

capacity by

Bank BRI

The LenderSecured and Transparent Transactions

Source:: Lender Presence and Age Group Data as on July-19

13

Copyright 2019 | PT Investree Radhika Jaya CONFIDENTIAL

Disbursem

ent

Loan

Grading

Risk Based

Pricing

Borrowers Credit Bureau AML-AT

Traditional Data

Rule Based

Engine

Scoring

Models

Machine

Learning

Monitoring &

Control

Proprietary risk scoring engine

Decisi

on

Engine

Risk GradingBullet Payment Loan

(Effective per Annum)

A + 12%

A 13% – 14%

B 15% – 16%

C 17% – 19%

C - 19% – 20%

Account-

ing

Software

E-commercePayment

GatewayProcurement

Non - Traditional Data

Invoice Financing Loan rates Internal

Data

We Generate our own Risk Scoring Model Using Traditional and Non-traditional Data

14

Invoice Financing Buyer Financing Working Capital

Term Loans

Online Seller

Financing

Government Retail

Bond

What is it?

Short term invoice

financing of reputable

payers. Also includes pre-

invoice and account

payable financing

Limit

• 80% of invoice value

• Up to IDR 2 Bio (USD

138,00)

Tenor

• 14-180 days

• Bullet repayment

options

Average Loan Size*

USD 36,761

What is it?

Loans available for buyers

/ distributors / resellers of

the supply chain

Limit

• 100% LTV from

Purchase Order

• Up to IDR 2 Bio (USD

138,000)

Tenor

6-12 months

Average Loan Size*

USD 87,483

What is it?

(1) Regular Term Loan

(2) Contract Based

Financing

(3) Merchant Cash

Advance

Limit

• 80% of LTV of online

sales or 80% of

contract value

• Up to IDR 2 Bio

(US138,000)

Tenor

MCA – Upto 24 months,

Regular – Upto 12 months

Average Loan Size*

USD 44,899

What is it?

Historical data based

working capital loans to

sellers on e-commerce

marketplaces

Limit

• Based on IDIR

Calculation

• Up to IDR 2 Bio (USD

138,000)

Tenor

Up to 24 months

Average Loan Size *

USD 2,551

What is it?

• Mandated by Ministry of

Finance for online

distribution of

government bonds

• Risk free investment

grade

Limit

Investment starts from IDR

1 Mio (USD 68)

Shariah approved product / in-progress

Share

74%

* Based on loans disbursed and no. of borrower transactions

in July 2019Copyright 2019 | PT Investree Radhika Jaya

Our Product OfferingInvoice Financing constitutes 74% of the product portfolio

Share

6%

Share

13%

Share

1%Share

6%

Copyright 2019 | PT Investree Radhika Jaya CONFIDENTIAL

E-ProcurementRegional

Expansion

SME

Credit

Scoring

E-Invoice &

Cloud ERPE-Commerce

Payment

Gateway

E-Procurement solution to

stack along with existing

SME financing solution

Collaboration with third-

parties to tap into

government, SOE, and

private supply chains

In-house credit scoring

capability designed

specifically for SMEs

Leverage AI and technology

to improve internal loan

quality

Provide credit scoring as a

service to other parties

Collaboration with third-party

E-invoice solution to stack

along with existing SME

financing solution

Leverage existing anchors to

tap into both customer and

supplier side for e-invoicing

Collaboration with third-party

Future plan to integrate with

ERP or cloud accounting

Regional expansion into

Thailand and Philippines

Maintain market leader

position in Indonesian SME

B2B lending marketplace

Tap into international

institutional lender base

Tap into both on-line and

off-line payment gateways

Leverage partners’

payment capabilities for

access to data, payment

security and channelling

To supplement e-

procurement, e-invoicing,

and ERP capabilities

Strategic partnerships

with top e-commerce

platforms to tap into

online sellers

Leverage partners’

ecosystem for access

to data and channelling

Investree Eco-System

Exclusive JV

Initiatives

Non-JV Initiatives

Evolving from traditional P2P to B2B SME Lending Marketplace

Credit

Scoring

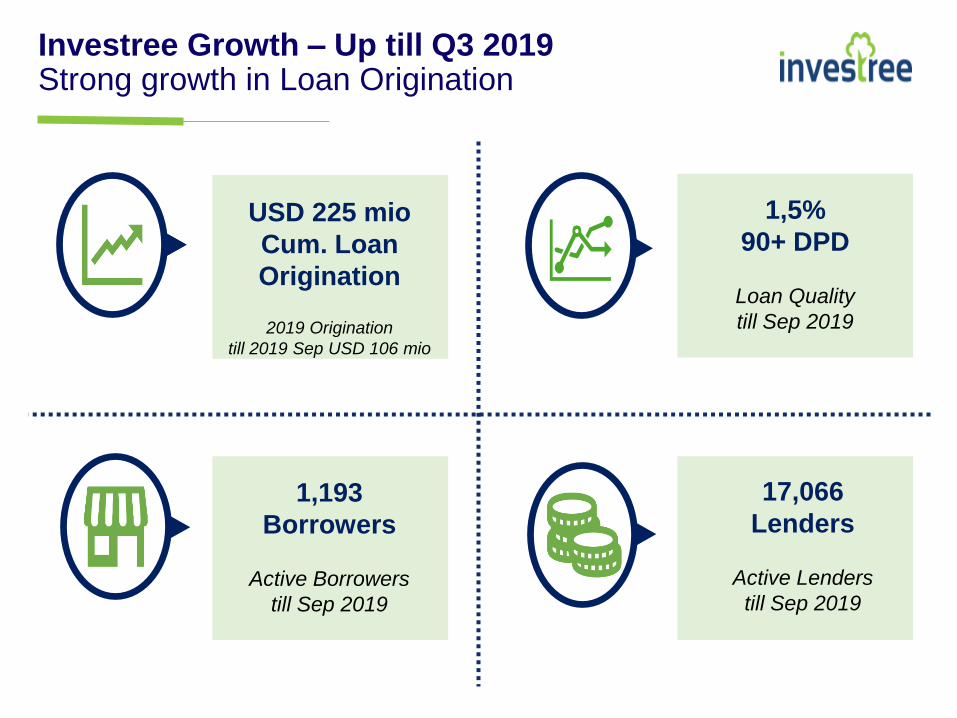

USD 225 mio

Cum. Loan

Origination

2019 Origination

till 2019 Sep USD 106 mio

17,066

Lenders

Active Lenders

till Sep 2019

1,193

Borrowers

Active Borrowers

till Sep 2019

1,5%

90+ DPD

Loan Quality

till Sep 2019

Investree Growth – Up till Q3 2019Strong growth in Loan Origination

Copyright 2019 | PT Investree Radhika Jaya CONFIDENTIAL

Adrian Gunadi

Co-Founder & CEO

Dr. Amiruddin

Co-Founder

KC Lim

Co-Founder

Eri Reksoprodjo

Chairman

• Over 18 years foreign and local

banking experience in the retail

and wholesale sectors

• Last 6 years’ experience as

Managing Director Retail

Banking of Bank Muamalat

Indonesia

• Endeavor Entrepreneur

• Current Chairman of AFPI

• Extensive experience in the

banking and financial industry

since 1994

• Previously worked in companies

such as British Gas, Bakrie

Finance, AAA Securities,

Deutsche Bank, Nomura

• Last role was Head of Indonesia –

Wealth Management di Sumitomo

Mitsui Banking Corporation

• A senior finance professional

with 27 years experience.

Currently, Managing Partner of

Kejora Ventures

• Previously, Country

Manager/Executive Director at

Natixis, Partner at Saratoga

Investama Sedaya and Senior

Advisor for SGD 300 million SE

Asia fund

• Over 21 years banking career

experience

• Last role was FICC sales for

Goldman Sachs in SE Asia

• CFA Charterholder

• Splits his time between

Singapore, Indonesia and

Thailand

TeamExperienced bankers with skin in the game

Copyright 2019 | PT Investree Radhika Jaya CONFIDENTIAL

Muliaman D. Hadad

Senior Advisor

Azharuddin Lathif

Shariah Supervisory Board

M. Suaidy Masud

Shariah Supervisory Board

• Currently officiates as Ambassador

of the Embassy of The Republic of

Indonesia to Switzerland and

Liechtenstein

• Former Deputy Governor of Bank

Indonesia and former Chairman of

the Board of Commissioners of the

Financial Services Authority

• Currently serves as Director of the

Sharia Supervisory Board – The

Indonesian Council of Ulama (DSN-MUI)

Institute

• Consultant in Legal Constituition and

Legal Aid Institute, of Shariah Faculty

Law of Syarif Hidayatullah UIN

Jakartaand Arbitrators in National Sharia

Arbitration Board (Basyaras) MUI

• Currently Secretary to the Economic

Empowerment Commission at the

Indonesian Islamic Leadership Assembly

(MUI)

• Currently Vice-Director for the Shariah

Business Incubation Center (Pinbas), also

at MUI

• Currently Vice-Chairman Indonesian

Islamic Merchant Association (ISMI)

• Currently Expert Staff to Legislative

Council

AdvisorsWith Regulatory and Shariah expertise

Fajar

Technology Advisor

• Cofounder and CTO of Happyfresh,

online grocery startup based

• Ex-Engineering director at Yahoo

• Cofounded Koprol, a mobile social

network, sold to Yahoo

• Ex-Lead Software Engineer at Gap

Inc.

• Computer science engineering

graduate from Ohio State University

Copyright 2019 | PT Investree Radhika Jaya CONFIDENTIAL

Salman Baharuddin

Chief of SalesAmalia Safitri

Chief of Risk

Ade Fauzan

Chief Operation Officer

Dickie WIdjaja

Chief Information OfficerAstranivari

Chief Marketing Officer

Ex- Citibank, Credit

Suisse, UBSEx- Citibank, HSBC,

Maybank, Danamon

Ex- Permatabank, Bank

Muamalat, Maybank,

BTPN

Ex- Indosat, Citibank,

Phillips Indonesia

Ex- Lycos Asia, AstraWorld,

Telkomsel, Current Vice-

Chair of AFTECH

Senior Management That lead a team of 170+ professionals

Ex- BFI Finance, VIVA,

Telkomsel, Citilink, Bank

BTPN, Mandiri

Ariyo Putro

Chief of Human Capital

Andi Andries

Chief Product Officer

Ex-Indosurya, Danamon,

GE CapItal, ANZ, Lippo

Daniel Armanto

Chief Technology Officer

Ex- Tiket.com, Yahoo,

Happy5, Adskom

Copyright 2019 | PT Investree Radhika Jaya CONFIDENTIAL

“Empowering many

more Imans out

there”

Iman SyafeiFounder, ReKreasi Creative Playground

(Marketing and Advertising Agency

founded in 2014)

Copyright 2019 | PT Investree Radhika Jaya CONFIDENT

IAL

22